bioethanol in europe - feagri - faculdade de engenharia ... · bioethanol in europe ......

TRANSCRIPT

AGRENER 2006Campinas, BRJunho 6-8, 2006

Bioethanol in EuropeAdequate Conditions to Face International Competition?

Bioetanol na EuropaCondições adequadas para enfrentar a competição international?

Oliver Henniges

Department of Agricultural Economics(Prof. Zeddies)

UNIVERSITY OF HOHENHEIMStuttgart, Germany

1. General Framework in D and EU (Condições gerais na Alemanha e União Européia)

2. Production Costs (Custos de produção)

Germany (BR, USA, CN, AUS, TH)

3. Competitiveness (Competitividade)

4. Risks from European Perspective(Riscos de uma perspectiva Européia)

Structure

Bioethanol in EuropeAdequate Conditions to Face International Competition?

• Kyoto Protocol ⇒ CO2 reduction

• Energy (in)dependence

• Jobs in rural areas

• Market relief for agricultural commodities

• Alternative incomes for farmers

• Maintenance of sugar beet cultivation?!

Why Bioethanol?

General Framework D and EU

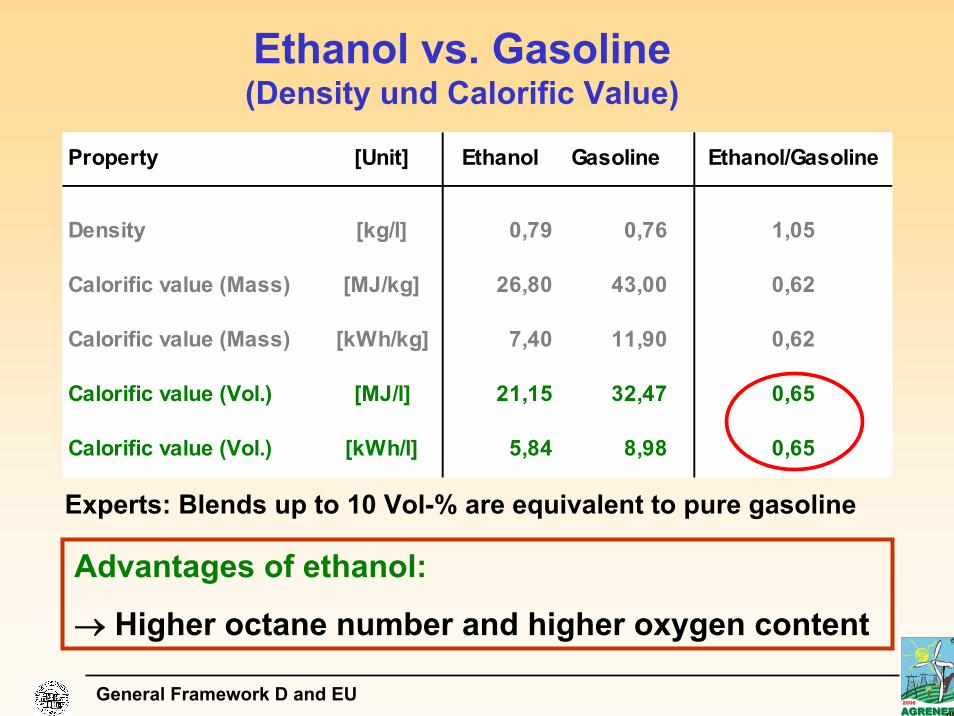

Ethanol vs. Gasoline(Density und Calorific Value)

Property [Unit] Ethanol Gasoline Ethanol/Gasoline

Density [kg/l] 0,79 0,76 1,05

Calorific value (Mass) [MJ/kg] 26,80 43,00 0,62

Calorific value (Mass) [kWh/kg] 7,40 11,90 0,62

Calorific value (Vol.) [MJ/l] 21,15 32,47 0,65

Calorific value (Vol.) [kWh/l] 5,84 8,98 0,65

Experts: Blends up to 10 Vol-% are equivalent to pure gasoline

Advantages of ethanol:

→ Higher octane number and higher oxygen content

General Framework D and EU

Share of renewable energy in fuels by end of

2005 2,00 % (+ 0,75 %points per year)2010 5,75 % (→ 8,8 Vol.-% )

For Germany that means:

Gasoline consumption 2005: 25 Mio t

2,00 Energy % 10 mln hl (1.0 bln liters)5,75 Energy % 29 mln hl (2.9 bln liters)

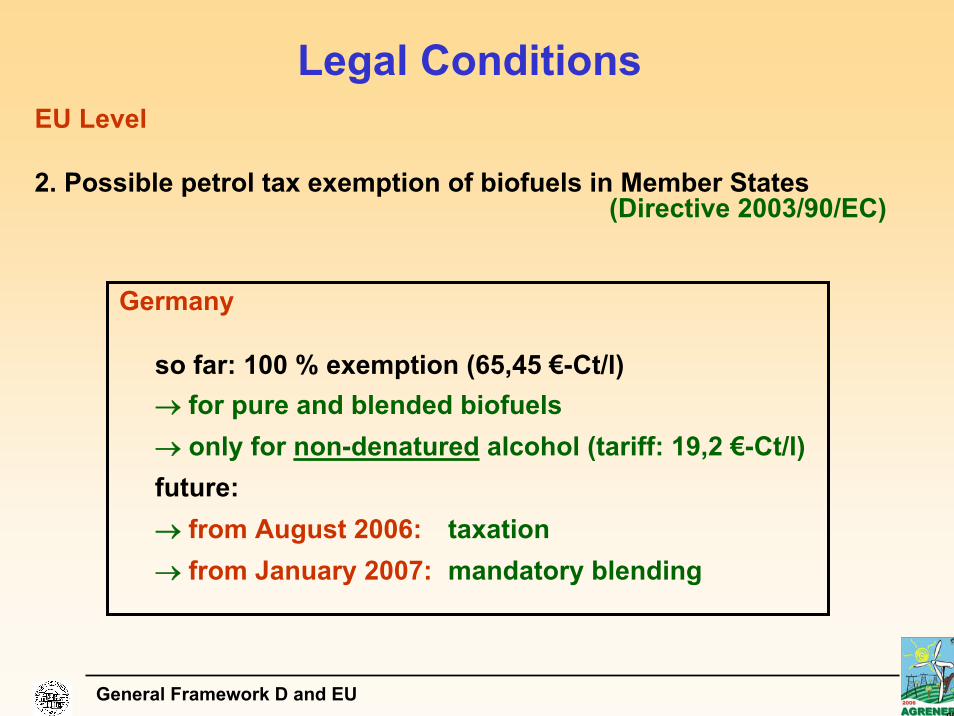

Legal ConditionsEU Level

1. Support of Biofuels (Directive 2003/30/EC)

General Framework D and EU

Legal Conditions

Germany

so far: 100 % exemption (65,45 €-Ct/l)→ for pure and blended biofuels→ only for non-denatured alcohol (tariff: 19,2 €-Ct/l)future:→ from August 2006: taxation→ from January 2007: mandatory blending

EU Level

2. Possible petrol tax exemption of biofuels in Member States (Directive 2003/90/EC)

General Framework D and EU

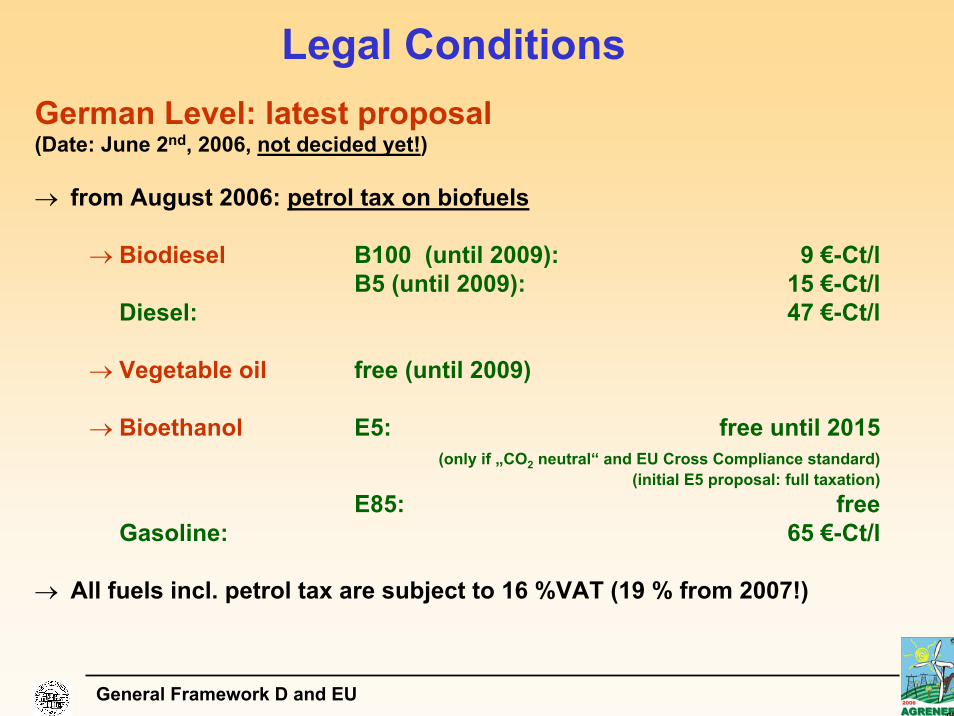

Legal ConditionsGerman Level: latest proposal (Date: June 2nd, 2006, not decided yet!)

→ from August 2006: petrol tax on biofuels

→ Biodiesel B100 (until 2009): 9 €-Ct/lB5 (until 2009): 15 €-Ct/l

Diesel: 47 €-Ct/l

→ Vegetable oil free (until 2009)

→ Bioethanol E5: free until 2015 (only if „CO2 neutral“ and EU Cross Compliance standard)

(initial E5 proposal: full taxation)E85: free

Gasoline: 65 €-Ct/l

→ All fuels incl. petrol tax are subject to 16 %VAT (19 % from 2007!)

General Framework D and EU

Legal ConditionsGerman Level: latest proposal (Date: June 2nd, 2006, not decided yet!)

from January 2007: mandatory biofuel share based on energy content→ 2.0 % ethanol in gasoline market (from 2010: 3.0 %)

→ 0,73 mln tons

→ 4.4 % biodiesel in diesel market→ 1.4 mln tons

→ From 2010: “global quota” of 5.7 % biofuels in fuel market(from 2011: 6 %)

→ Implementation of tradeable biofuel credits (Source: FO Licht)

General Framework D and EU

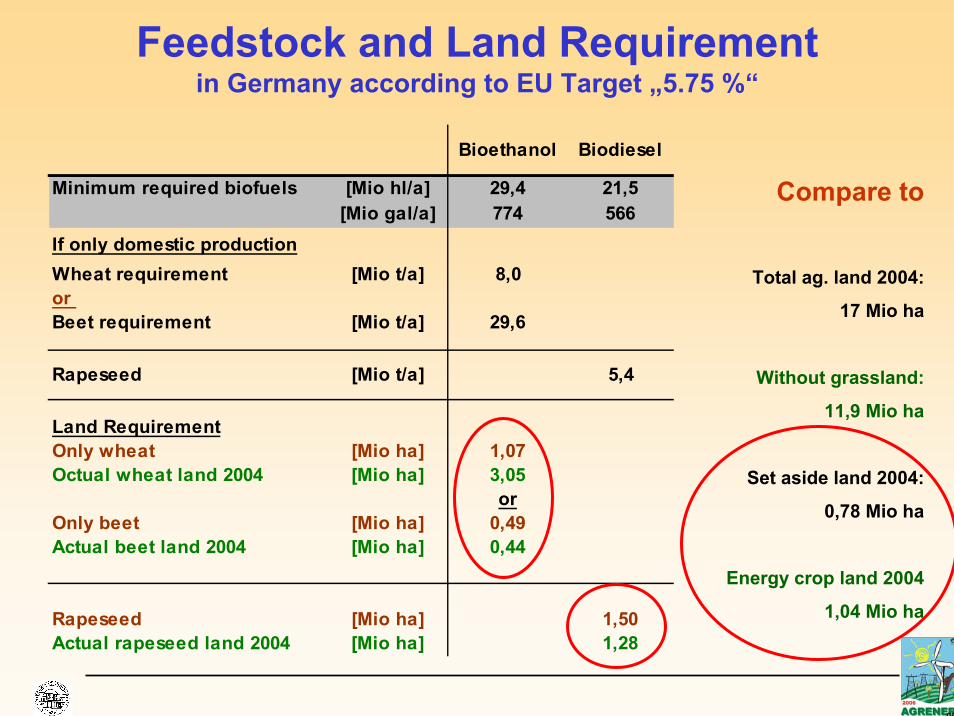

Feedstock and Land Requirementin Germany according to EU Target „5.75 %“

Bioethanol Biodiesel

Minimum required biofuels [Mio hl/a] 29,4 21,5[Mio gal/a] 774 566

If only domestic productionWheat requirement [Mio t/a] 8,0or Beet requirement [Mio t/a] 29,6

Rapeseed [Mio t/a] 5,4

Land RequirementOnly wheat [Mio ha] 1,07Octual wheat land 2004 [Mio ha] 3,05

orOnly beet [Mio ha] 0,49Actual beet land 2004 [Mio ha] 0,44

Rapeseed [Mio ha] 1,50Actual rapeseed land 2004 [Mio ha] 1,28

Compare to

Total ag. land 2004:

17 Mio ha

Without grassland:

11,9 Mio ha

Set aside land 2004:

0,78 Mio ha

Energy crop land 2004

1,04 Mio ha

1. General Framework in D and EU

2. Production Costs D, BR, USA, CN (AUS, TH)

3. Competitiveness

4. Risks from European Perspective

Structure

Bioethanol in EuropeAdequate Conditions to Face International Competition?

Bioethanol in Germany

long ethanol tradition ...

Production Costs

Bioethanol in Germany

today...Production Costs

Production Costs in Germany

Assumptions:

• Multiple feedstock planta) 0,5 mln hl/yearb) 2,0 mln hl/year

• Raw materialBeet campaign (90 days): beet juiceRest of year: wheat→ 64 % ethanol from wheat, 36 % from beet

• Wheat Price: 100 €/t → Beet Price: ?

Production Costs

Production Costs in Germany(Multiple feedstock plant)

Production Costs

For the content of this slide please contact the author under:

Beet Price?

Production Costs

For the content of this slide please contact the author under:

Production Costs in Germany(Multiple feedstock plant)

Production Costs

For the content of this slide please contact the author under:

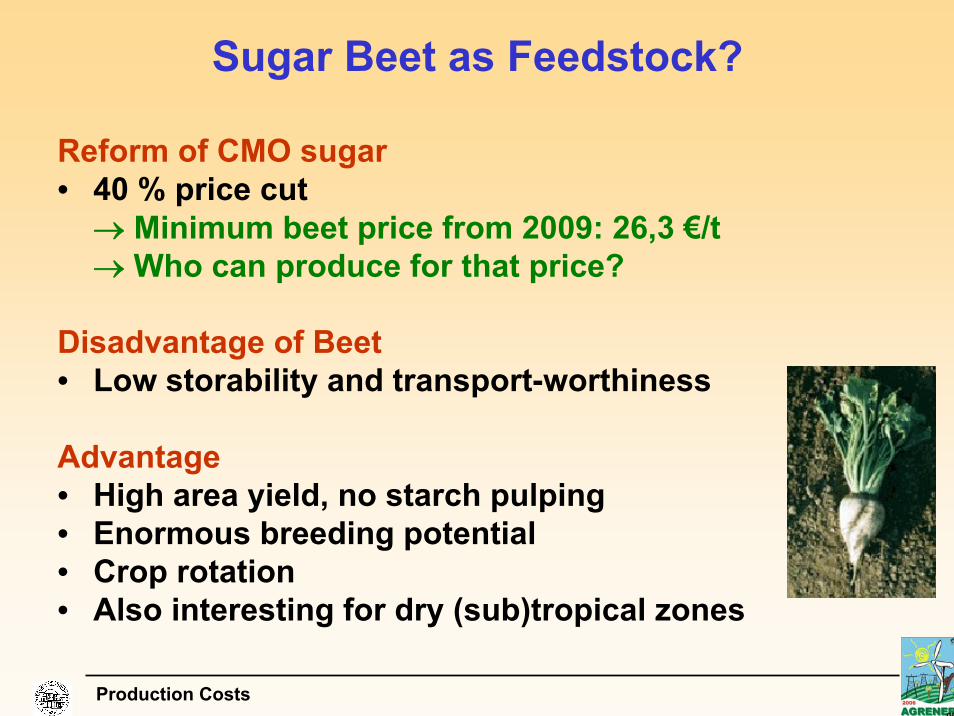

Sugar Beet as Feedstock?

Reform of CMO sugar• 40 % price cut

→ Minimum beet price from 2009: 26,3 €/t→ Who can produce for that price?

Disadvantage of Beet• Low storability and transport-worthiness

Advantage• High area yield, no starch pulping• Enormous breeding potential• Crop rotation• Also interesting for dry (sub)tropical zones

Production Costs

in

Brazil (Cane)

Production CostCalculations forother Countries

USA (Corn)

Production Costs

Production CostCalculations forother Countries

AustraliaAustralia (Cane, (Cane, MolassesMolasses))

Production Costs

Production CostCalculations forother Countries

Thailand (Cane)

Production Costs

Feedstock Feedstock forfor futurefuture: : Cassava?Cassava?

Production CostCalculations forother Countries

China (Corn)Production CostCalculations forother Countries

For the content of this slide please contact the author under:

Production CostCalculations forother Countries China (Corn)

Manual Manual HarvestHarvestProduction CostCalculations forother Countries

China (Corn)

For the content of this slide please contact the author under:

Manual Manual HarvestHarvestProduction CostCalculations forother Countries

China (Corn)

For the content of this slide please contact the author under:

1. General Framework in D and EU

2. Production Costs D (BR, USA, CN, AUS, TH)

3. Competitiveness

4. Risks from European Perspective

Structure

Bioethanol in EuropeAdequate Conditions to Face International Competition?

International Comparison of Production Costs

Assumptions:

- Plant Capacity: 2 Mill hl/a (200 Mill. Liters per year)

- No subsidies considered

- 5 % Risk premium included

- Bagasse for internal energy need

Competitiveness

(Gross Prod. Costs – Co-Product Sale = Net Prod. Costs)

For the full content of this slide please contact the author under:

< Costs EU

* USD1.2/EUR

** without profit margin and VAT

Competitiveness of Brazilian Ethanol in D (cost-based)

(D = Deutschland = Alemanha)Competitiveness

For the content of this slide please contact the author under:

≥ Costs EU

* USD1.3/EUR

** without profit margin and VAT

Competitiveness of Brazilian Ethanol in D (January 2006)

Competitiveness (D = Deutschland = Alemanha)

For the content of this slide please contact the author under:

* USD1.2/EUR

** without profit margin and VAT

Low Price Scenario(January 2004)

< Costs EU

Competitiveness (D = Deutschland = Alemanha)

For the content of this slide please contact the author under:

* USD1.2/EUR

** without profit margin and VAT

Low Price and Low Tariff

EU Ethanol (†)

Competitiveness (D = Deutschland = Alemanha)

For the content of this slide please contact the author under:

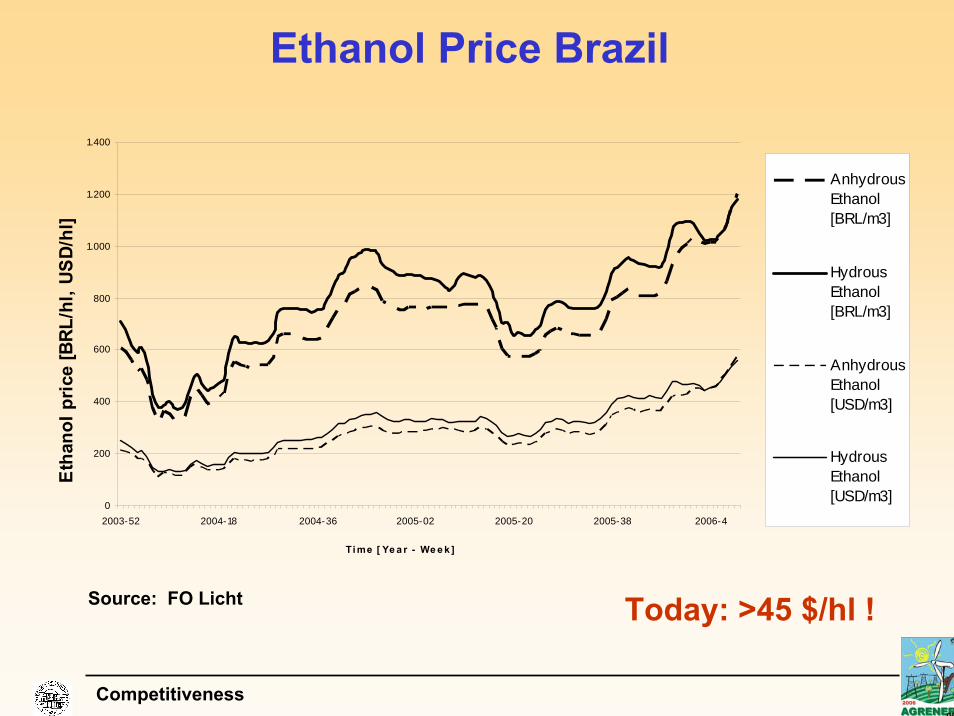

Ethanol Price Brazil

Source: FO Licht Today: >45 $/hl !

Competitiveness

0

200

400

600

800

1.000

1.200

1.400

2003-52 2004-18 2004-36 2005-02 2005-20 2005-38 2006-4

Ti me [ Ye a r - We e k ]

Etha

nol p

rice

[BRL

/hl,

USD/

hl]

AnhydrousEthanol[BRL/m3]

HydrousEthanol[BRL/m3]

AnhydrousEthanol[USD/m3]

HydrousEthanol[USD/m3]

Who benefits?

Competitiveness against Gasoline in Germany

Competitiveness

For the full content of this slide please contact the author under:

1. General Framework in D and EU

2. Production Costs D (BR, USA, CN, AUS, TH)

3. Competitiveness

4. Risks from European Perspective

Structure

Bioethanol in EuropeAdequate Conditions to Face International Competition?

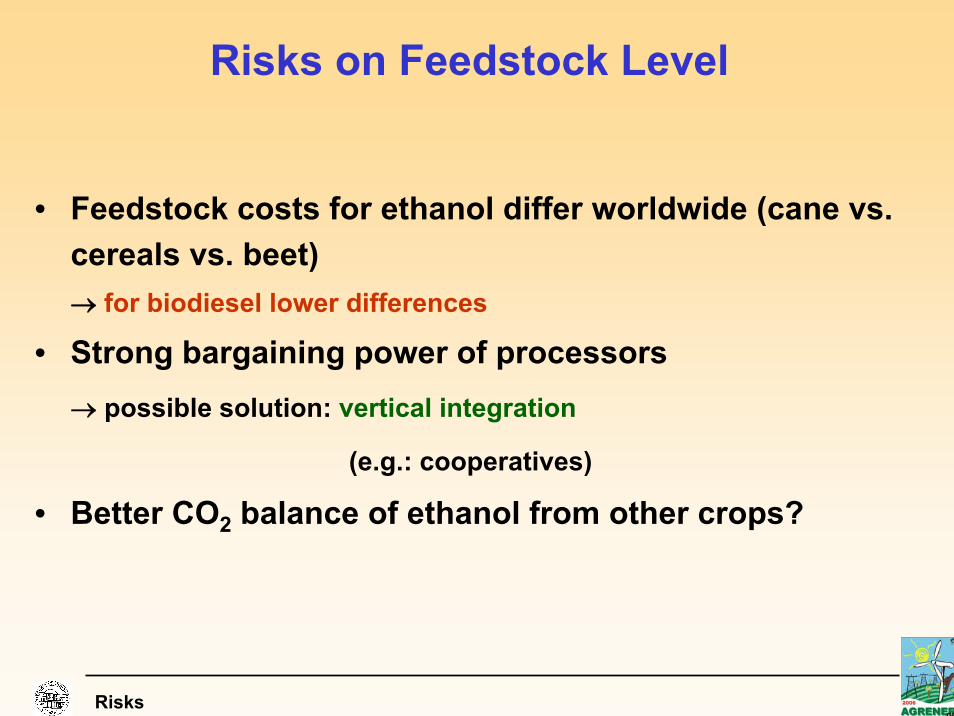

Risks on Feedstock Level

• Feedstock costs for ethanol differ worldwide (cane vs. cereals vs. beet)→ for biodiesel lower differences

• Strong bargaining power of processors→ possible solution: vertical integration

(e.g.: cooperatives)

• Better CO2 balance of ethanol from other crops?

Risks

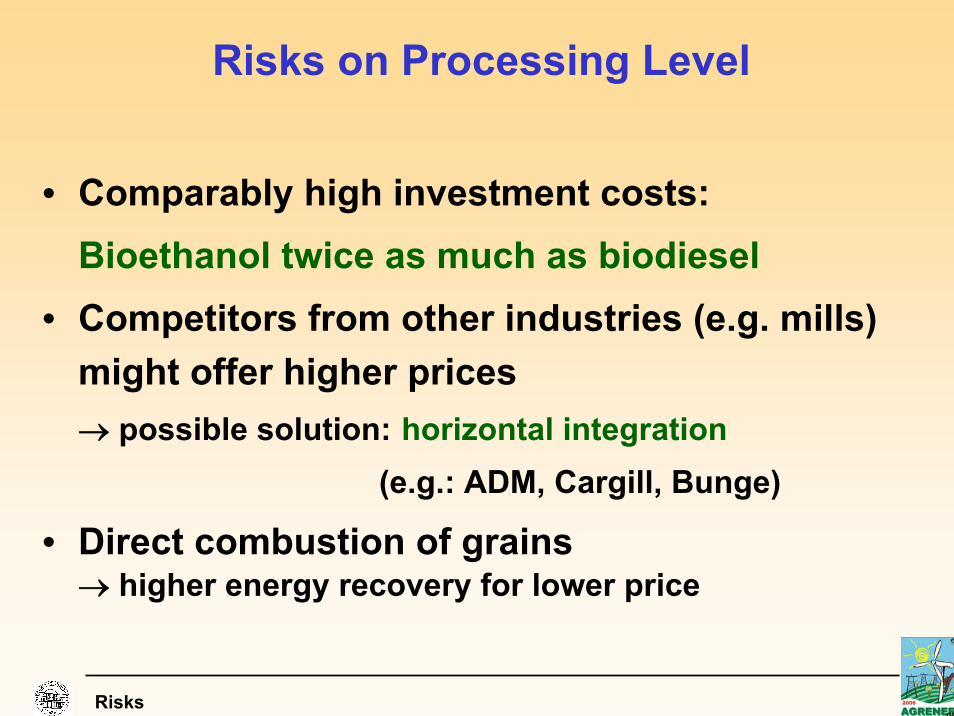

Risks on Processing Level

• Comparably high investment costs:Bioethanol twice as much as biodiesel

• Competitors from other industries (e.g. mills) might offer higher prices→ possible solution: horizontal integration

(e.g.: ADM, Cargill, Bunge)

• Direct combustion of grains → higher energy recovery for lower price

Risks

Risks on Marketing Level

• Other products – other markets – other risks:Fuels instead of food→ other sellers and quality requirements

• policy-dependent demand• Market power (vs. internat. petrol companies)• Technical problems (vapour pressure)• Gasoline demand stagnates (Diesel increases)• Future: Synfuels?

Risks

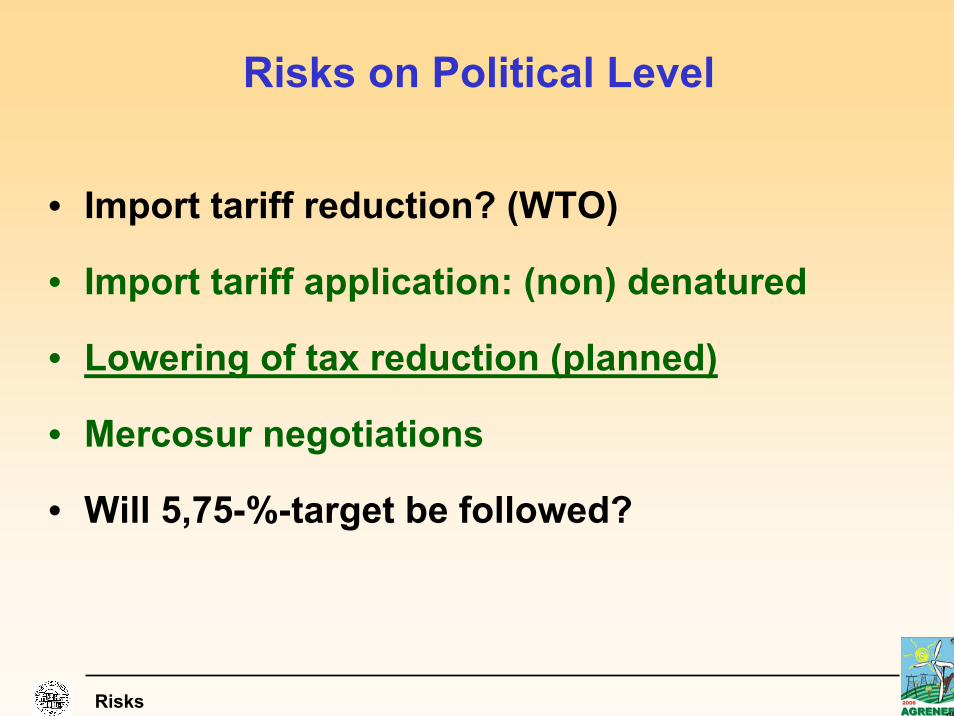

Risks on Political Level

• Import tariff reduction? (WTO)

• Import tariff application: (non) denatured

• Lowering of tax reduction (planned)

• Mercosur negotiations

• Will 5,75-%-target be followed?

Risks

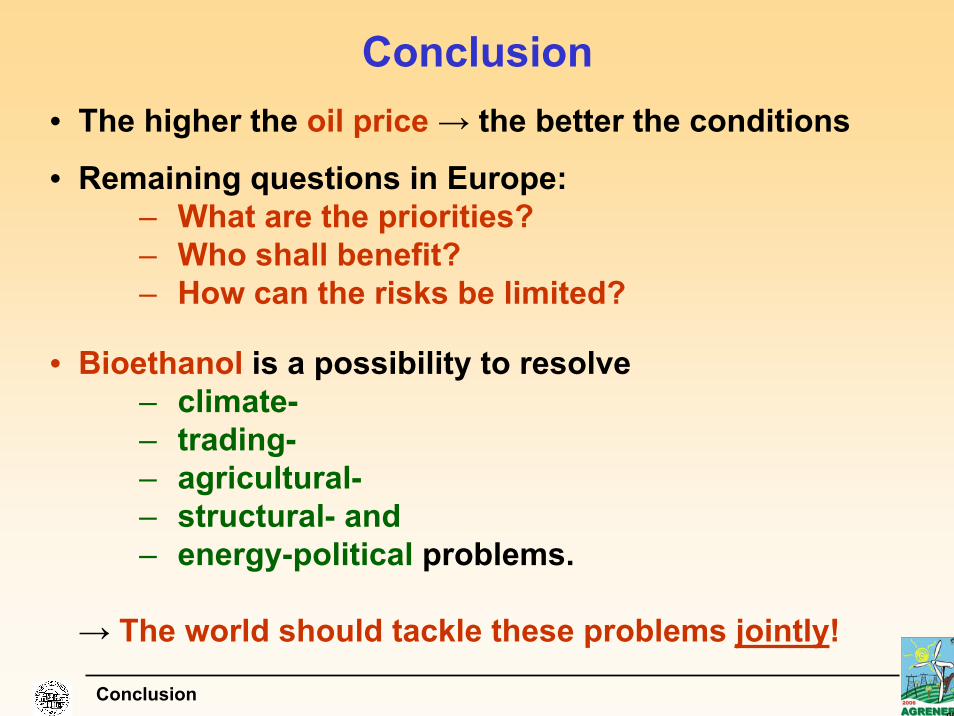

Conclusion• The higher the oil price → the better the conditions

• Remaining questions in Europe:– What are the priorities?– Who shall benefit?– How can the risks be limited?

• Bioethanol is a possibility to resolve– climate-– trading-– agricultural-– structural- and– energy-political problems.

→ The world should tackle these problems jointly!

Conclusion

Best Solution for Ethanol?

Outlook

Drink the Bestand

Burn the Rest!

Best Solution for World Cup?(Melhor Solução para o Campeonato Mundial de Futebol)

Outlook

Thank you for your attention!

Muito obrigado pela atenção!

O final:Alemanha - Brasil!

AGRENER 2006Campinas, BRJunho 6-8, 2006

Bioethanol in EuropeAdequate Conditions to Face International Competition?

Bioetanol na EuropaCondições adequadas para enfrentar a competição international?

Oliver Henniges

Department of Agricultural Economics(Prof. Zeddies)

UNIVERSITY OF HOHENHEIMStuttgart, Germany