biocon investors presentation july 2013

Post on 18-Oct-2014

1.130 views

DESCRIPTION

Biocon Investors Presentation July 2013TRANSCRIPT

Innovative Science Affordable Medicine

www.biocon.com

Investor Presentation July 2013

Certain statements in this release concerning our future growth prospects are forward-looking

statements, which are subject to a number of risks, uncertainties and assumptions that could cause

actual results to differ materially from those contemplated in such forward-looking statements.

Important factors that could cause actual results to differ materially from our expectations include,

amongst others general economic and business conditions in India, our ability to successfully

implement our strategy, our research and development efforts, our growth and expansion plans and

technological changes, changes in the value of the Rupee and other currencies, changes in the Indian

and international interest rates, change in laws and regulations that apply to the Indian and global

biotechnology and pharmaceuticals industries, increasing competition in and the conditions of the

Indian biotechnology and pharmaceuticals industries, changes in political conditions in India and

changes in the foreign exchange control regulations in India. Neither the company, nor its directors and

any of the affiliates have any obligation to update or otherwise revise any statements reflecting

circumstances arising after this date or to reflect the occurrence of underlying events, even if the

underlying assumptions do not come to fruition.

Safe Harbor

2

Biocon: Who are we?

• Small Molecules

• Biosimilars

• Branded Formulations

• Research Services

• Novel Molecules

Growth Segments

Financials

Outlook

Agenda

3

Biocon: Who are We?

Biocon: Global Ambitions with Indian Roots

Mission: “To be an integrated biotechnology enterprise of global distinction”

Value Creation along 3 axes:

Leveraging the India advantage to deliver high value, licensable R&D assets

Strategic Research and marketing partnerships that provide global access

Reducing therapy costs of chronic diseases. (diabetes, cancer & auto-immune diseases)

5

Evolving with the Times

1978 -1999

1999 - 2004

2004 - 2009

2009 – 2014

2014 & Beyond

An Enzymes Company Revenue: ` 32 Crores

Building the India Business and expertise in biologics Revenue: ` 1,194 Crores

People: 3,500+

Investment intensive phase with focus on R&D, capacity &

partnership execution Revenue (FY 13): ` 2,538 Crores

People: 6,700+

Transforming into a Biopharma company

Revenues: ` 549 Crores

People: 700+

Unwavering focus through the years on Innovation & Difficult to make, niche products to create tangible differentiators for sustainable growth

6

Poised for a global platform with launch of finished formulations & biosimilars in regulated

markets

Group Revenue at ` 723 Crores (22% YoY growth)

YoY Growth* across verticals:

EBITDA at ` 175 Crores (EBITDA Margin: 24% )

R&D Expense: ` 43 Crores (10 % of Biopharma Revenue)

PAT at ` 94 Crores (PAT Margin: 13% )

Financial Performance

Q1 FY14 Highlights

8 *YoY comparison of Q1 FY14 Sales vs. Q1 FY13 Sales; #CER: Constant Exchange Rates

Business Vertical Absolute Growth Growth at CER#

Biopharma 21% 19%

Branded Formulations 17% N.A.

Total Biopharma 20% 19%

Research Services 26% 22%

Total Sales 22% 20%

Novel Molecules

Unlock Value

through Licensing

Growth Verticals

ANDAs & 505(b)(2) filings

Small Molecules

Research Services

Integrated offerings

Insulins, MAbs & Other

Biologics Biosimilars (Biologics &

Insulins)

Rapidly growing- India-centric

business

Branded Formulations

EMERGING MARKETS FOCUS EMERGING MARKETS FOCUS

Growth Verticals: Aligned with Shifting Paradigms

9

Aligning For Growth: Reorganizing for greater synergy

Function Based Organization -----> Business Units

Sustaining the Entrepreneurial Spirit: Agility in decision making Responsibility with Accountability Greater Synergy amongst functions: Aligning people to the greater goal

Marketing

Finance

Manufacturing

Small Molecules

Generic Insulins

Biosimilar MAbs

… …

Earlier Organization Structure New Organization Structure

10

R&D Branded Formulations

Growth Segments: Snapshot

Small Molecules

APIs (Generic & Novel)

Formulations 505(b)(2) & ANDAs

Current Portfolio Constituents

Statins Simvastatin, Atorvastatin, Lovastatin, Rosuvastatin, Fluvastatin & Pravastatin

Immuno suppressants Tacrolimus, MMF & MPA

Other Biopharma Orlistat, Fidaxomicin, 50+ other molecules

Product Portfolio which leverage our core fermentation capabilities and have a high degree of complexity Early mover in niche products coupled with economies of scale. Portfolio based Approach

12

Biosimilars: Demystifying

“a biological product that is highly similar to the reference product notwithstanding minor differences in clinically inactive components, and.. no clinically meaningful differences against the reference product in terms of the safety, purity and potency.”

Large Molecules (proteins): greater complexity

Very difficult to make and demonstrate bio-similarity; Extensive development process

Process development and Capacity constraints

Insulin & Insulin Analogs (4)

Monoclonal Antibodies (3)

Other Biologics (2)

A biosimilar

is…

Unlike a small

molecule…

Current Portfolio

Biosimilar Definition: Biologics Price Competition and Innovation Act of 2009 13

Herceptin

~6 Bn, 18%

Avastin

~6 Bn, 18%

Enbrel

~8 Bn, 24%

Humira

~10 Bn,28%

Neulasta

~4 Bn, 12%

rh-Insulin

~ 3 Bn, 18%

Glargine

~7 Bn, 35%

Lispro

~2 Bn, 13%

Aspart

~4 Bn, 23%

Detemir

~2 Bn, 9% Glulisine

~0.3 Bn, 2%

Biosimilars: Opportunity

Total Insulins Market:

~ USD 19 Bn*

The Insulin Pie Biosimilar MAbs & Other Biologic

Opportunity : ~ USD 34 Bn*

*Market Size of innovator products MAT March 2013, All figures rounded off to nearest USD Billion, %ages on absolute numbers 14

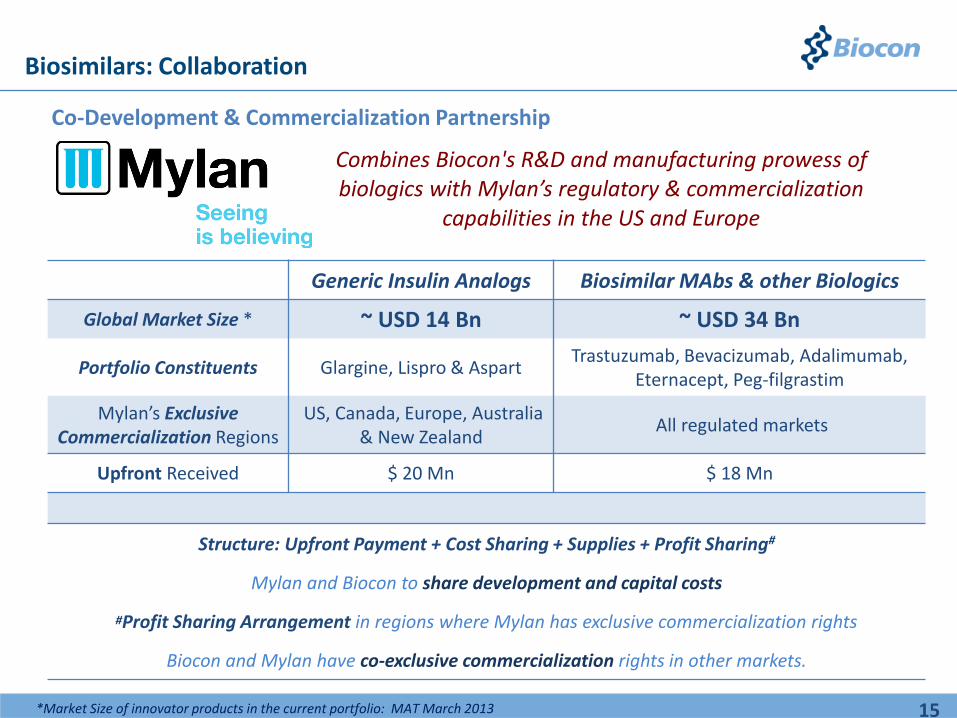

Combines Biocon's R&D and manufacturing prowess of biologics with Mylan’s regulatory & commercialization

capabilities in the US and Europe

*Market Size of innovator products in the current portfolio: MAT March 2013

Generic Insulin Analogs Biosimilar MAbs & other Biologics

Global Market Size * ~ USD 14 Bn ~ USD 34 Bn

Portfolio Constituents Glargine, Lispro & Aspart Trastuzumab, Bevacizumab, Adalimumab,

Eternacept, Peg-filgrastim

Mylan’s Exclusive Commercialization Regions

US, Canada, Europe, Australia & New Zealand

All regulated markets

Upfront Received $ 20 Mn $ 18 Mn

Structure: Upfront Payment + Cost Sharing + Supplies + Profit Sharing#

Mylan and Biocon to share development and capital costs

#Profit Sharing Arrangement in regions where Mylan has exclusive commercialization rights

Biocon and Mylan have co-exclusive commercialization rights in other markets.

Co-Development & Commercialization Partnership

15

Biosimilars: Collaboration

Portfolio Biosimilar Molecule

Global Trials

Generic Insulins

rh- Insulin

Glargine

Lispro & Aspart

Biosimilar MAbs and other biologics

Trastuzumab

Bevacizumab, Adalimumab

Etanercept, Peg-filgrastim

Process Development / Scale-up / Preclinical

Phase 1/II b

Market Phase

III

Emerging Markets First strategy coupled with a regional partnership commercialization approach Biosimilar Trastuzumab: patient recruitment completed for India Phase III trial. Generic rh Insulin registered in 45+ countries; generic insulin glargine registered in 10+ nations

16

Biosimilars: Pipeline

16

Biocon’s First Manufacturing expansion overseas : Iskandar, Johor

Asia’s largest integrated Insulins manufacturing facility

Investment to the tune of ~$ 160 Mn in the first phase

Development on-going at full steam

1st Phase expected to be completed by 2014

Key Highlights

Biosimilars: Malaysia Insulin Facility

17

Branded Formulations: Snapshot

• An India Centric Business with Global Ambitions

• Front Ending of our vertically integrated API & Biologics pipeline

• Portfolio highlights: • Insugen & Basalog:

India’s largest selling generic insulin & analog

• BioMAb EGFR: India’s 1st indigenous novel MAb for head & neck cancer

INDIA PRODUCT RANKINGS#

Cardiology

Clotide 1

Myokinase 2

Oncotherapeutics

Evertor 1

BioMAb EGFR 2

Abraxane 3

Immunotherapy

Calpsor C, Picon, Tbis 2

Nephrology

Tacrograf 3

Bio-products

Ivnex 2

Comprehensive Care

Genpirome & Cegava TZ 2

#: ORG IMS Latest MAT 2013, IPSOS

Branded Formulations: Sustained Growth

18

65

86

259

347

101

FY 12 FY13 FY14

Revenues in ` crore

Q1

* Includes biosimilars # Market Share as per latest MAT reports, IPSOS, LASSCHN

Branded Formulations

19

Biologics*

Remaining Portfolio

India’s Fastest growing Insulin company

Biocon: 34% | Sanofi: 15% | Novo: 5%

#4 in overall insulin market

#3 in the 40 IU Insulin market

#1 in the Glargine vial market

Biocon’s Volume Market share#

100 IU Insulin: 21%

Glargine vials: 84%

79

130

179

107

130

169

186

259

347

FY11 FY12 FY13

Revenues in ` crore

Market Share # of other flagship brands:

BioMAb EGFR: 50%

Evertor: 46%

Picon: 33%

Calpsor C: 34%

Novel Molecules: Pipeline

Therapeutic Area Molecule

Oncology Nimotuzumab

Autoimmune Itolizumab

Diabetes IN-105

Oncology Anti CD – 20

Oncology Fusion Proteins

Pre-Clinical

Phase II

Phase 1

Market Phase

III Discovery

#

India Trials

Itolizumab: India Commercial Launch in Q2 FY14

Anti CD 20 (BVx 20) has entered the clinic in India

Multiple Global Trials planned for Oral Insulin in collaboration with BMS

20

Currently on hold

Biocon will continue global development of the molecule through Phase II via redesigned trials.

Partnership encompasses Financial, Strategic and Clinical Support throughout the development phase

BMS will have an exclusive option post phase II to further develop & commercialise the asset worldwide (excl. India)

Biocon will receive licensing fee in addition to potential regulatory & commercialization milestones, when BMS exercises its option

Combines Biocon's novel asset and development experience with BMS’ novel drug development,

regulatory & commercialization capabilities.

Novel Molecules: Collaboration

IN-105 Option Agreement: BMS (First-in-Class Oral Prandial Insulin)

21

Novel Molecules: Itolizumab Profile

First-in-Class Therapy :Novel MOA with an excellent safety profile

Very low Infection rates vis-à-vis other approved therapies

Modulates TH17 Pathway: Frontrunner in the hot bed of research in auto immune space

Marketing Approval received in India post a successful Phase III trial in Psoriasis (200+ patients); Commercial launch in Q2 FY14

Excellent clinical remission & safety data in phase III for Psoriasis

Promising preclinical and clinical efficacy data in other auto immune diseases (Rheumatoid Arthritis, Psoriatic Arthritis etc)

Key Differentiators

28 Weeks 12 Weeks Baseline

22

Research Services: Snapshot

2000

Today

India’s largest CRO with 1,500 + scientists, working with 16 of the Top 20 pharma

companies in the world. Capital Investment of ~$120 Mn

An investment of ~$20 Mn supported by 100+ scientists focused on building

a world class CRO

23

Customized models

Evolving Services

Niche Offerings

Integrated Platforms

o Bioanalytical testing of small and large molecules

o Antibody Drug Conjugate (ADC) development

o Unique In-Vivo Models- Human tumour tissue Xenograft

o Early and rapid toxicology evaluation (Cardiomyocytes )

o Commercial scale production of NCEs

o High potency (cytotoxic) API manufacturing

o Formulation development

o Dedicated/customized infrastructure

o End-to-end services

o Risk sharing: Milestone based

o Incubation: IP sharing

o Integrated Drug Discovery and Development

o Biologics Discovery and Development

o Syngene- Clinigene axis

Research Services: Capabilities & Collaboration Models

24

Research Services: Key Customers

o Dedicated Infrastructure: Abbott Nutrition and R&D Centre

o India focused product

development addressing local needs with customized offerings tailored to local taste & texture preferences

o Long term contract for 50+ FTEs focused on: • Maternal & Child Nutrition • Diabetes Care

o Dedicated Infrastructure: BMS Biocon Research Centre

o BMS’ largest research facility outside the US

o 7 years contract, currently in its 4th year of operations

o 450+ FTEs committed to integrated (end-to-end) research in a variety of therapeutic areas

25

72 88 124

155

318

410

557

FY 11 FY 12 FY 13 FY 14

Research Services: Performance

o PE Investment of ` 125 Crores for a 7.69% stake, assigning Syngene a post money valuation of `1,625 Crores

o Investment earmarked for enhancing Syngene’s service offerings, capacities & fund future growth

o GE brings in corporate best practices along with avenues for capability enhancement and new offerings

26

Revenues in ` crore

Q1

Financials

Revenue 1,194 260 1,493 318 1,858 407 2,148 445 2,538 467

R&D Spend 60 13 79 17 118 26 137 28 164 137

EBITDA 372 81 455 97 573 125 579 120 596 110

Net profit 238 52 273 58 340 74 338 70 509 94

EPS (FV: ` 5) 11.9 13.6 17.0 16.9 25.4

FY09 FY10 FY11 FY12

FY08-12: Avg.exch.rate in that fiscal : 1Q FY13: USD 1 = ` 55.86; 1Q FY14: USD 1= ` 54.64

# Biopharma Sales excluding branded Formulations

Financial Performance

Q1 FY14 Q1 FY13

Revenue 723 | 129 593 | 108

R&D Spends 43 | 8 36 | 6

% of Biopharma Sales # 10% 10%

EBITDA 175| 31 139 | 25

EBITDA Margin 24% 23%

Net Profit 94| 17 79 | 14

PAT Margin 13% 13%

EPS 4.7 3.9

All Figures in ` Crore / USD Mn except EPS

FY13

28

349

432

86

101 122

155 593

723

Q1 FY13 Q1 FY14

Regulated Markets*

56% India 28%

RoW 16%

Revenue: Detailed

29

All Figures in ` crore unless otherwise specified

Core Biopharma

Licensing

Branded Formulations

Research Services

Other Income

Geography Wise Sales Breakup:

` 723

*: Including Deemed Exports

Core Business Margins: Detailed

FY 09 FY 10 FY 11 FY 12 FY 13 Q1 FY14

Revenue 1,194 1,493 1,858 2,148 2,538 723

Less: Other Income 54 32 52 99 110 28

Less: Licensing Income 12 51 153 127 25 8

Core Revenues 1,127 1,410 1,654 1,922 2,403 687

EBITDA 372 455 573 579 596 175

Add: R&D Expense 60 79 118 137 164 43

Less: Other Income 54 32 52 99 110 28

Less: Licensing Income 12 51 153 127 25 8

Net EBITDA 365 450 487 490 625 182

EBITDA Margin 32% 32% 29% 25% 26% 26%

Outlook

49%

5%

20% 10%

10% 40%

10%

25%

20%

5%

30%

20%

25%

20%

5%

FY 12 A

2015 E

2018 E

Small Molecules

Biosimilars (Insulins + MAbs)

Research Services

Branded Formulation

Licensing & Other Income

~ $450 Mn

$1 Billion +

~ $700 Mn

31

Targeting $1 Bn Revenues in 5 Years

Exchange Rate: 1 USD =` 50

• Commercialization of generic rh-Insulin in regulated markets

• Launch of generic insulin glargine in large semi-regulated markets

• Commercialization of biosimilar trastuzumab in India & other emerging markets

• Clinical development of generic rh-Insulin for US

Biosimilars: Global Development & Commercialization

• Generic insulin plant in Malaysia comes on stream: augmenting capacity and cost advantage

• Research Services add further facilities & capabilities to catalyze the next growth wave

Capacity Enhancement

• Development/Commercialization partnership in developed markets: generic rh-insulin, Itolizumab

• Emerging Market partnerships for small molecules & biosimilars

Partnerships

Key Milestones: 2015 E

32

o Small Molecules - Improved product Mix o Research Services - Sustained Growth Momentum

o Branded Formulations - Differentiated Value offerings

o Biosimilars - Geographical Expansion in regulated markets

o Novel Molecules - Out-licensing and Global Development

Growth drivers supplemented by addition of new offerings (products, services & partnerships)

Reaching $1 Bn by 2018

33

Looking Ahead

30%

20%

25%

20%

5%

Exchange Rate: 1 USD =` 50

• Continuous evolution of the biosimilar & therapeutic regulatory landscape in major regulated markets

• Regulatory approvals, Patient enrollment, R&D development, process refinement etc. determine the pace and quantum of the R&D activities

Biosimilars & Novel Molecules: Regulatory Clarity

• Relationship management: New Contracts, Contract Renewal & Scope Expansion

R&D Outsourcing: Research Services

Partnership Management

34

Risks…

www.biocon.com

Innovative Science Affordable Medicine

Investor Contact: Saurabh Paliwal Sweta Pachlangiya [email protected] [email protected]

APPENDIX

~955

~70

~180 ~1,205

2011 A DevelopedMarkets

Emerging Markets 2016 E

USD Bn

~ 5% CAGR

Global Pharma Market

Source: IMS Institute of Healthcare informatics,The Global Use of Medicines: Outlook Through 2016

Emerging Markets to contribute ~ 75% of the Total Pharma Growth by 2016

Global Pharma Spending expected to cross $1.2 Trillion by 2016 Emerging Markets projected growth CAGR: ~10%

Developed Markets expected growth CAGR: ~2%

Emerging Markets growth driven by:

Increased Government Healthcare Spending Growing Affluence

Global Pharma Growth Catalyst: Emerging Markets

37

*includes: OTC, diagnostics and non-therapeutics sales worth $118 Bn in 2011 and $145 Bn in 2016 E

Global Pharma Growth Catalyst: Generics & Biosimilars

Source: IMS Institute for Healthcare Informatics, IMS Market Prognosis, May 2012

Small Molecules,

~ 425

Biosimilars~5

Small Molecules,

~ 241

Biosimilars ~ 1

Generic Spending to Increase by ~75% in the next 5 years vs. Branded drugs’ growth of 9%

Biosimilars will grow 5 fold to $5 Bn

956

~1,205

USD Bn

Branded* 714

Branded* 745

Generic 242

Generic 430

2011 2016 E

Back 38

Small Molecules & Biosimilars: Comparison (1)

Small Molecules Molecular Weight: Less than 700 Daltons

Synthetic, Organic compounds

[Chemistry based products]

Well defined structure & relatively stable

Monoclonal Antibody Molecular Weight: ~150,000 Daltons (~250x in size)

Biologics- prepared in living organisms

[Proteins]

Complex physiochemical characteristics & heat sensitive

39

Small Molecules & Biosimilars: Comparison (2)

Regulatory Requirements

PK/PD (establishing BA/BE)

CMC Studies

Clinical Trial

PK/PD studies

Preclinical studies

Biological Characterization

Physio-chemical Characterization

Generics: Small Molecules Biosimilars

40

Biosimilars: Regulatory Landscape

41

~61% | Promoters ~ 8 % | Employees & ESOP trust ~31 % | Public

Biocon

Business Structure & Holdings

Syngene International, India | ~88% Custom research, drug discovery

Clinigene International, India | 100% Clinical development

Biocon Research , India | 100% R&D- Novel Molecules Biocon Biopharmaceuticals | 100% MAbs and Biosimilars Biocon Sdn. Bhd, Malaysia | 100% Overseas subsidiary Biocon SA, Switzerland | 100% Overseas subsidiary

NeoBiocon, UAE | 50% Overseas subsidiary

BIOPHARMA SUBSIDIARIES

RESEARCH SERVICES

Spanning the entire Value Chain with capabilities ranging from discovery to manufacturing

42