bio world congress - 2014 gomes... · uranium elemental carbon ... • trends in demand • degree,...

TRANSCRIPT

BIO World Congress - 2014

General Information

BNDES Highlights

Founded on June 20th, 1952.

100% state-owned company under private law.

Key instrument for implementation of Federal Government’s

industrial and infrastructure policies.

Main provider of long-term financing in Brazil.

Emphasis on financing investment projects.

Support to micro, small and medium-sized companies.

Support to Export and Internationalization of Brazilian companies.

InfrastructureInfrastructure

Heavy Industry – Consumer GoodsHeavy Industry – Consumer Goods

Technological DevelopmentTechnological Development

Time Line

Imports SubstitutionImports Substitution

EnergyEnergy

AgribusinessAgribusiness

ExportsExports

Privatization ProgramPrivatization Program

Urban and Social DevelopmentUrban and Social Development

Social InclusionSocial Inclusion

InnovationInnovation

SustainabilitySustainability

Small BusinessSmall Business

50’s 60’s 70’s 80’s 90’s 00’s Today

BNDES Uruguay Montevideo(2009)

BNDES Limited London (UK) (2009)

Rio de Janeiro

Brasília

Recife

São Paulo

2.872 employees February, 2014

BNDES - Headquarters & Offices

Subsidiary

BNDES Africa Johannesburg (2013)

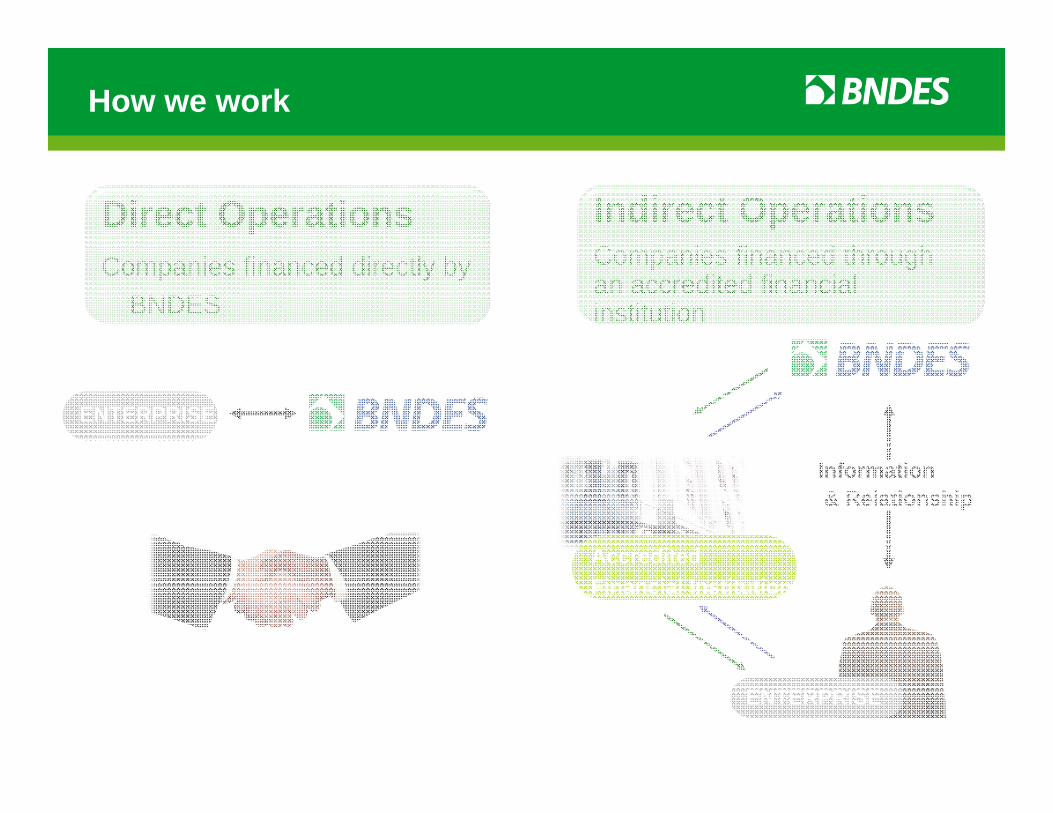

How we work

How we work

ENTERPRISE

AccreditedFinancial Institution

ENTERPRISE

Information& Relationship

Direct OperationsCompanies financed directly by

BNDES

Indirect OperationsCompanies financed through an accredited financial institution

Direct Operations

Power Plants Oil Rigs

ArenasIndustries

Examples:

What does BNDES support?

Innovation Industrial Projects Infra-structure Projects

Agriculture Equipments Exports Capital Market Operations

Equipment, and Services

Capital Market

Capital Market

The BNDESPAR plays a key role owing to:

Its commitment to long-term projects.

The size and quality of its portfolio.

Its performance in moments of higher volatility in the market.

Its capacity to attract other investors.

Its focus on corporate governance.

Its capacity to invest in all market sectors.

Capital Market

CriatecFundCriatecFund

Venture Capital FundsVenture Capital Funds

Private Equity FundsPrivate Equity Funds

Initial Public Offerings (IPO)Initial Public Offerings (IPO)

Public OfferingsPublic Offerings

Capital Markets

General Indicators

3,9 4,0 3,9

5,96,4

4,2

6,6

8,3

11,3

6,7

5,5

7,1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Disbursements to Finance Exports

US$ billion Converted to US dollar on the disbursement dates

R$ bilhões

156,1

43,547,1

168,4

137,4 139,7

52,364,9 92,2

190,4

17,328,5

16,2

41,165,5

9,919,6

146,4

2005 2006 2007 2008 2009 2010 2011 2012 2013

Desembolsos BNDES Emissões na Bovespa

16 Firms48%*

20 Firms(includes Petrobras R$120 bi share offering)26%*

(*) Foreign investors participation

In R$ Billion

BNDES vs. Capital Market

75 Firms75%*

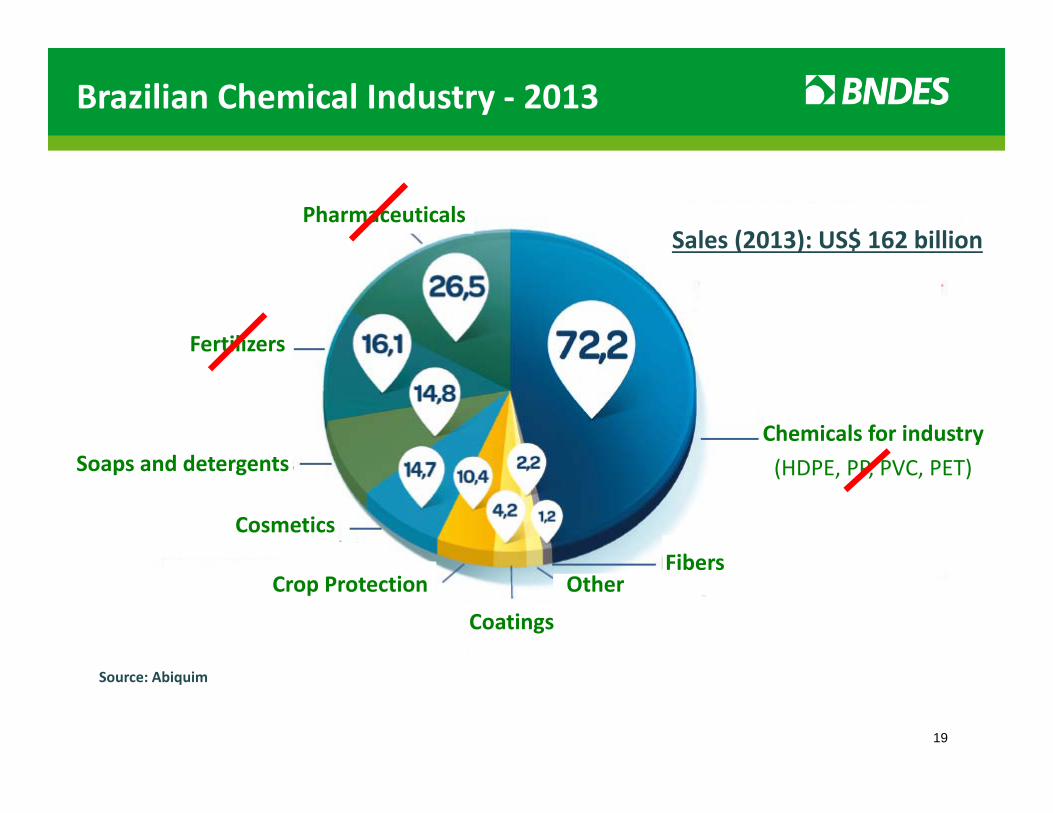

Chemical Industry

Diversification Study

17

Brazilian Chemical Industry ‐ 2013

Imports ExportsUS$ billions FOB

Trade balance ‐ Chemicals

Source: MDIC/Secex

• Technical Sector Agenda – Products from renewable sources

• Structured initiatives - Capacity building in human capital

• Infrastructure improvements

• Regulations for chemicals used for crop protection

• Chemical industry diversification study on Diversification of the Chemical Industry

• Incentivize the use of locally available raw materials

• Incentives for investment

• Incentives for innovation

• Policies to encourage the use of natural gas as a feedstock

STRATEGIC AGENDA(SHORT TERM)

STRUCTURAL AGENDA (MEDIUM TERM)

The Study is part of the “Plano Brasil Maior”, that has additional short and long term initiatives

• Identify and analyze opportunities for diversifying the Brazilian chemical industry, including specialties, value added products and new technologies- Commodity thermoplastic resins (PP, PE, PVC and PET), pharmaceuticals (drugs, vaccines, hormones and active ingredients) and fertilizers (N, P and K) are not part of the primary focus of the study

• Suggest instruments and actions as part of an industrial policy for the Brazilian chemical sector.- With an integrated view of the short, medium and long term

19

Brazilian Chemical Industry ‐ 2013

Pharmaceuticals

Fertilizers

Soaps and detergents

Cosmetics

Crop Protection

Coatings

Chemicals for industry(HDPE, PP, PVC, PET)

FibersOtheOther

Sales (2013): US$ 162 billion

Source: Abiquim

Project Schedule

Report 722/aug/14

Business model design

Financial and economic analysis

Initial prioritiza‐tionof segments

Mapping and Segmenta‐tion

Research on selected segments

Priortization and validation

Mapping of existing dev. policies and

identification of int’l best practice

S2

S1

S4

IP

1/jul/13

9/sep/13

Design of development policies

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug

IP

Detailed evaluation of opportunitiesScenario planning and development policies

Initial prioritization and segmentation of chemicals

S Seminars IPIndustry Panels

Final prioritization of opportuni-ties

S3

Report 53/jun/14

Report 428/apr/14

Report 3fev/14

Report 66/aug/14

Individual interveiws

22/may/14Report 3fev/14

64 segments and a business perspective

Tarderiv.

Organics

Acrylicacid anddeivati

Metacrylicacid andderiv.

Fattyacids and

deriv.Aromatics

Butadiene, isopreneandderiv.

Celluloseand

deriv.

Waxes and

paraffins

Copolymers

Cumeneand

deriv.

Elastomers

Ethylenederiv.

Methanederiv.

Ethyleneoxide and

deriv..

Propenederiv.

Vinylderiv.Lubricants

Fine chemicals intermediaries

Polymers intermediaries

Special Polymers

Aramids Carbonfibers

Polycar-bonates Polycetals

Specialpolyamides

High tenacitypolyester

Polyetherpolyols andpolyurethane

Politetra-metileno éter glicol

Resinas epóxidas

Polibutileneterephthalate

Catalysts and additives

Food additives Constructionchemicals

Leatherchemicals

Mining chemicals

O&G Chemicals

Polymersadditives Catalysts Flavor and

fragrances

Dyes, pigments andcoatings

Synteticdyes

Printinginks Coating

Soaps, cleaning andcosmetics

Cleaningproducts Cosmetics

Other

Explo-sives

Refrigerants Reagents

Glues andsealantsGlues,

adhesivesand

sealants

Pesticides

Pesticides

Photographics

Photographics

Chain

Inorganics

Inorganicacids

Aluminum deriv.

Boronderiv.

Chlorineand

Alkalis

Cobaltderiv.

Phosphorus andderiv.

Industrial gases

Iodineand

deriv.

Radioactivemat.

Nickelderiv.

Titaniumdioxideand

deriv.

Niobiumderiv.

Sulfphates Rare earthderiv. Uranium

Elemental carbonderiv.

Siliconderiv.

Note: Pharmaceuticals, fertilizers and commodity plastics resines (HDPE, PP, PVC and PET are out of the scope of the study.

Industrial intermediaries

Market

Market and production factors guided the selection of segments to deep dive

A multi‐criteria analysis tool was used to ensure the robustness of the results

• Imports +Exports (US$)- Average 08-12

• Production (US$)- Average 07-11

• CAGR imports + exports (%)

• Unit Price (US$/kg)-Average 08-12

• Trends in Demand

• Degree, current and future, of availability and cost competitiveness of raw materials

• Degree of technological dominion and the potential to develop or purchase it

• Availability of qualified labor

• Quality of available infrastructure

• Regulatory restrictions

• Necessity for investment

Dem

and

Con

ditio

nsFa

ctor

s of

Pro

duct

ion

Infra-structure

CRITERIA

• Size

Capital

Legal Environ.Labor

• Growth

• Value‐added

• Technology

• Raw Materials

INDICATORS SOURCEQua

ntita

tive

Qua

litative

• Trends

• Aliceweb

• Consortium

• Validation from the school of chemistry

• Global Insight

• Macro tendencies

• Aliceweb

• Associations

• PIA

23

Step 3 ‐ Segments Prioritized

Crop ProtectionLubricants Oleochemicals Construction chemicals Chemicals for E & P Chemicals for mining

Special polyamides High tenacity polyesterFragrances and flavors Food additives Cellulose derivatives Cosmetics

Methacrylic acid and derivatives Industrial additives Catalysts Chlorine and alkalies Glues, Adhesives and Sealants Synthetic organic dyes

Methane derivativesElastomers Propylene derivativesTitanium oxide and derivatives Cleaning products and intermediates Laboratory reagents Coatings and related products

Aromatics Leather chemicalsButadiene and derivatives Polyurethanes Silicon derivatives Carbon fibers Surfactants

Hig

h Pr

iorit

yM

edia

nPr

iorit

y

Selected segments represent ~70% of imports and exports

Média das importações e exportações por segmentos(US$B, 2008-2012, exceto produtos fora do escopo)

Fonte: AliceWeb, Receita Federal, Análise Bain e Gas Energy

Alta prioridade Média prioridade Baixa prioridade

Legenda

Growth is backed up by the strong demand for goodsPerspective is positive

Note: Only the top 10 markets are represented in 2017 (estimated). These countries should represent ~ 64% of the world market in 2017 Source: Euromonitor; Bain / Gas Energy Analysis

The cosmetics and personal care industries, by country(US$B)

Forecast

Cosmetics

Cleaning products: perspective is also positive

Note: For domestic useSource: Abipla Annual Report, 2013

Cleaning products

Pre-salt will generate demand for biodegradable drillingfluids; Renewables have advantages

Source: Bain / Gas Energy Analysis

Demanda de químicos para E&P no Brasil(US$B)

Fonte: Freedonia; Análise Bain / Gas Energy

Projeção

EstimulaçãoCimentaçãoCompletaçãoProduçãoPerfuração

18% 18%

• Drilling fluids represented 72% of Brazilian demand for chemicals for E&P in 2011

• The base, vehicle where the additives are submerged, represent 80% to 90% of the cost of these fluids

• IBAMA e a Petrobras signed an agreement setting minimum standards for the toxicity biodegradability and toxicity of drilling fluids: bases (currently made from tradi onal paraffin) should be replaced, as of 2015, by bases made from oleochemical n‐paraffins, olefins or fatty esters

E&P chemicals

28

Preliminary analysis

SegmentBrazil Market ($ million) % Brazil

Brazil CAGR (07‐12)

Imports ($million)

Exports ($million)

Balance ($ milion)

Crop Protection 9.700 20,5% 16,1% 5.400 500 (4.900)Lubricants 4.500 2,6% 2,6% 1.120 210 (910)Oleochemicals 7.700 4,6% 4,0% 515 1.800 1.285O&G Chemicals 600 3,3% 23,0% 84 9 (75)Food additives (animal) 690 10,8% 15,0%Flavours and fragrances 1.200 4,6% 303 452 149Cosmetics 41.800 9,7% 12,4% 830 580 (250)Carbon Fibers 47 5,2% 40,0% 97 0 (97)

29

Preliminary analysis

Segment Some opportunities Crop Protection All segments

Lubricants Re-refining and bio-lubricants

Oleochemicals Soy, palm, palm oil, sugar and tallow derivatives

O&G Chemicals Demulsifiers and corrosion inhibitors, Petrobras pre salt projects

Food additives (animal) Aminoacids: Lysine

Flavours and fragrances Value added natural essences

Cosmetics Bio based products, cluster strenghtening, aerosol deodorants

Carbon Fibers Wind blades

*Sum of the financial value of imports and exports (average (2008‐2012)**Average value of imports and exports in 2012 Source: AliceWeb, Bain / Gas Energy Analysis

PRELIMINARY

Some clusters to be strenghtened

New technologies (bio and nano)

will be analyzed horizontally

Oleochemicals

Consumer Goods

Surfactants

Construction

Crop Protection

Aromatics

C1,C2,C3

C4Distance between bubbles:“economic distance” of segments

Size of the bubble: Imports + Exports (US$300M)

Potential clusters

Final Remarks

•The government is investing in creating a stable environment for the chemical industry and in other related infrastructure

•Key segments of the chemical industry with strong fundamentals were selected for a deep dive: Oleochemicals, Surfactants, E&P Chemicals and Cosmetics are some examples that can be produced from Renewable sources, through Biotechnology

•Cosmetics and cleaning products in Brazil are growing above global rates and the opportunity for E&P chemicals is huge. Oleochemicals’ demand perspectives are strong: imports grew 12%p.a. from 2008 to 2012 MARKET OPPORTUNITY

•Clusters that are able to integrate the value chain, from renewable raw materials to valued added downstream industries, would benefit from scale gains and would increase the robustness of the projects

•Detailed information about the study can be obtained at BNDES website