berkeley healthcare coalition research summary september 2015

DESCRIPTION

How Berkeley SHIP Threw Our Dependents OverboardThis fall, many students will arrive to campus perhaps unaware of substantial changes this year to our health insuranceplan, Berkeley SHIP. Most significantly, University Health Services (UHS), our health plan’s administrators, madea rather shocking decision last spring to discontinue health insurance for dependents and voluntary plan enrollees.What’s more, UHS made this call without the knowledge of most of the people affected by this loss of insuranceand only superficial consultation with student groups on our campus. The Berkeley Healthcare Coalition has beeninvestigating how this decision was reached, how it affects students, and whether the rather drastic measure was in factjustified.TRANSCRIPT

How Berkeley SHIP Threw Our Dependents Overboard

A Summary Prepared by the Berkeley Healthcare Coalition

September 4, 2015

Figure 1: Members of the Berkeley Healthcare Coalition of UAW 2865 rally to restore dependent healthcare in frontof UC Berkeley’s California Hall on June 19, 2015. Image by photographer Rusi Mchedlishvili.

IntroductionThis fall, many students will arrive to campus perhaps unaware of substantial changes this year to our health insuranceplan, Berkeley SHIP. Most significantly, University Health Services (UHS), our health plan’s administrators, madea rather shocking decision last spring to discontinue health insurance for dependents and voluntary plan enrollees.1

What’s more, UHS made this call without the knowledge of most of the people affected by this loss of insuranceand only superficial consultation with student groups on our campus. The Berkeley Healthcare Coalition has beeninvestigating how this decision was reached, how it affects students, and whether the rather drastic measure was in factjustified. We summarize our key findings in the 10 points below.

UHS is the administrative body that makes healthcare decisions for the UC Berkeley campus community. BerkeleySHIP, our campus’ insurance plan, is negotiated by UHS and is currently provided by Aetna. In July 2014, Aetnaprepared a document outlining the high costs of certain Berkeley SHIP users, particularly dependents and voluntaryplan students. In that document, the company painted a misleading picture of a 2013-14 deficit, threatening thatbenefits would either need to be cut or our premiums increased substantially in 2015-16. Despite serious concerns withthe story Aetna told, UHS and their main advisory committee SHIAC (Student Health Insurance Advisory Committee)did not challenge Aetna, demand more information, or even double check their numbers. Instead, they sided withAetna. UHS and SHIAC also manipulated student groups to gain support for the proposition to drop insurance fordependents and voluntary plan members in order to avoid ostensibly imminent yet unsubstantiated premium hikes.UHS did this despite receiving a much better offer, which included dependent healthcare, with another insurer throughUC SHIP, the health plan offered at most other UC schools. The information Aetna and UHS presented to Berkeleystudents to compel them to stay with Aetna and eliminate insurance for some of the most vulnerable members of ourcommunity was misleading in several ways.

1 The calculations were flawed.The numbers Aetna presented to UHS, which were then shared with several campus administrators and student groups,include an adding error that results in a $250,000 over-estimation of the medical costs for graduate students’ depen-dents. Though this is a relatively small sum in the context of our health plan, the error impacts many other numbersin Aetna’s document, including the reported “Medical Loss Ratio” (sometimes also referred to as a “Medical Bene-fits Ratio” or “Medical Cost Ratio”). This figure, which we refer to as the MLR, is a percentage that indicates whatproportion of our premium dollars was spent on medical costs; the difference is what Aetna retains to cover its laborcosts, advertising expenses, and profits. MLRs are highly regulated under the Affordable Care Act (ACA), and mis-representing them is illegal. Despite these errors, which are relatively easy to spot, this flawed document was used tomake high-level decisions about our health plan (see Appendix A, Figure 2).

2 Last year’s premium increases were ignored.In the same document, Aetna painted a dire story that our plan was projected to run roughly $5.5 million below thecompany’s anticipated earnings in 2013-14 (Figures 2 and 3).2 Again, this projected number is slightly off due to thecalculation error described above. Errors aside, Aetna never mentioned that students were actually already on target torepay the bulk of this projected deficit through a 2014-15 premium increase. After this substantial premium increase,our plan generated about $46.8 million in 2014-15 (Figure 4), or an additional $3.4 million from the previous year. We

1The Berkeley SHIP voluntary plan was an optional insurance extension for students who had recently graduated (sometimes referred to as“continuation plan members”) or had withdrawn from the university. In addition, voluntary students’ partners, spouses, and children could alsoenroll in Berkeley SHIP health insurance. While all of these types of voluntary plans were eliminated in the 2015-16 plan, graduate students onfiling fee and concurrently enrolled undergraduate students can still enroll in voluntary insurance in 2015-16.

2The company anticipated an 84% MLR (Figure 4) based upon $43.4 million in premiums (Figure 2). Aetna expected to retain 16% of thepremium revenue, or about $6.9 million. However, in July 2014, Aetna projected a 96.8% MLR (Figure 2), which is erroneously inflated by 0.6%as noted in Point 1. Errors aside, this projected MLR would leave Aetna only 3.2% of the premium volume, or about $1.4 million, a difference ofabout $5.5 million. Significantly, while we refer to below-anticipated MLRs as “deficits,” Aetna never references a particular dollar amount theyanticipate earning; their projections are always rendered as percentages of premiums.

2

calculate that our medical costs will total about $41.3 million at the end of 2014-15,3 which would earn Aetna about$5.5 million, still about $2 million shy of Aetna’s probable 2014-15 expectations, assuming they again aimed for an84% MLR. Nevertheless, why wasn’t the additional premium revenue source from 2014-15 taken into considerationin the projections prepared by Aetna and circulated by UHS? Even in later documents prepared to justify the changesto our insurance, the 2014-15 premium increases are never accounted for—as if they never happened.

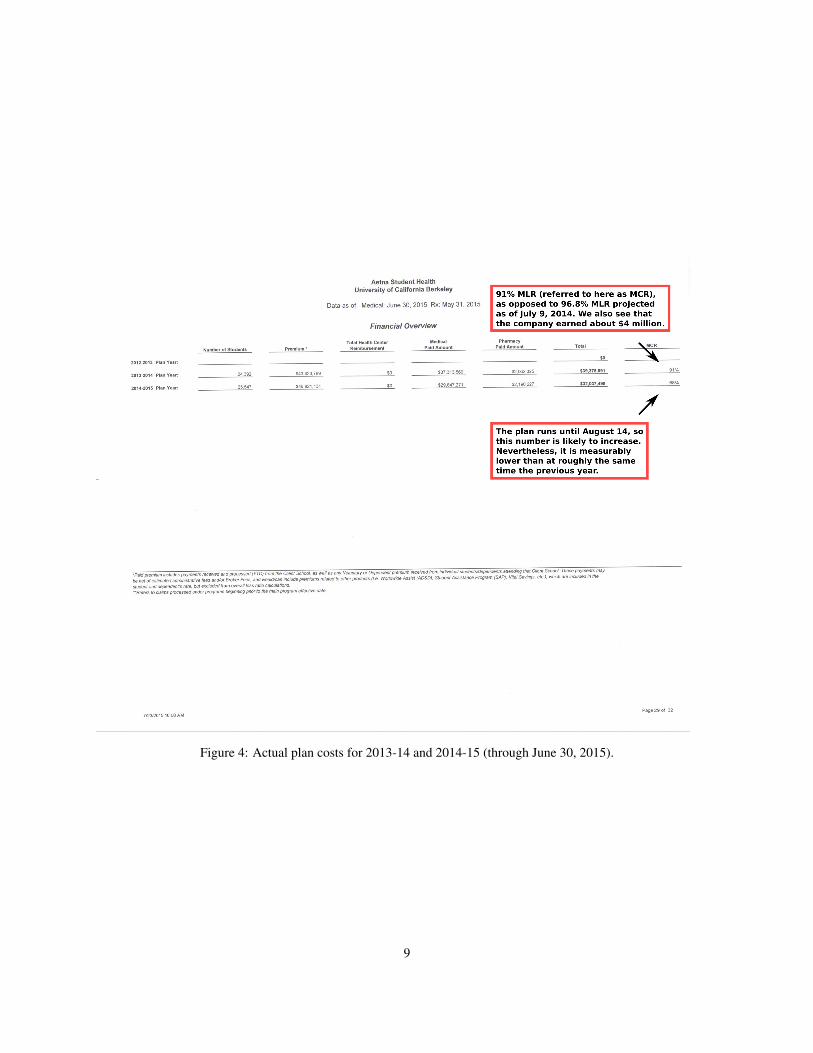

3 Aetna’s projected 2013-14 deficit was exaggerated.Aetna’s projected 2013-14 deficit turned out to have been overblown, as the company significantly overestimated ourmedical costs in their July 2014 report. When all was said and done, Aetna actually earned around $4 million that year,still a $2.9 million shortfall from their projections, but only half the deficit Aetna and UHS presented to students in thefall of 2014 (see Figure 4).4 Yet, it was based on these exaggerated deficit projections that students and administratorswere asked to make the decision to cut people off of the Berkeley SHIP insurance plan.

4 The ostensibly imminent premium hikes don’t add up.In November, Aetna and UHS told students that if they didn’t vote to cut dependents and recently graduated studentsoff of our plan, Aetna would raise everyone’s premiums by 31% in 2015-16, on top of the previous year’s premiumhikes we describe above. This would amount to new premium increases of roughly $550 for undergraduates, $850for graduate students, and an average of $1,300 for voluntary (also called “continuation”) enrollees and dependentsin 2015-16.5 We have no idea what would justify these exorbitant numbers, as we calculate that to cover the excessmedical claims of our dependents and voluntary enrollees and let Aetna earn its expected share would only cost about$80 extra per person,6 nowhere near the huge fee hikes Aetna threatened with. Where do these numbers come from?Who is checking them for accuracy? These hikes follow a pattern of unexplained and rapidly rising healthcare costssince we signed the deal with Aetna in 2013.7

5 The promised savings were inflated.Even though Aetna and UHS were able to pressure students to kick dependents and voluntary plan members off ofSHIP, they still increased 2015-16 premiums by $390 for undergraduate students and by $600 for grad students, and

3We used two methods to calculate this figure, both of which yield similar results.I Citing data indicating that 2013-14 and 2014-15 medical costs largely remained flat [3], we will look at the average cost Per Member Per Year(PMPY) in 2013-14 and apply that same rate to the number of people covered in 2014-15 to determine aggregate costs. In 2013-14, medical costswere $39,375,891 and 24,392 people were covered (Figure 4), averaging $1,614 PMPY. In 2014-15, there were 25,547 people covered (Figure 4),meaning that medical costs would be approximately $41.2 million. Since the plan’s premium revenues are $46,821,131 (Figure 4), the 2014-15MLR will be about 88.1% using this method.II Again, we look at last year’s plan to calculate this year’s medical costs, and we assume we will incur the same fraction of costs at the same point inthe calendar year. As of July 9, 2014, Aetna reported 2013-14 medical costs of $31,565,447 (Figure 2); their final costs that year were $39,375,891(Figure 4). This means that 20% of the costs came after July 9. As of June 30, 2015, Aetna reported 2014-15 medical costs of $32,037,498.The 2014-15 report was prepared nine days earlier than the comparable 2013-14 report. To compensate for this 9 day difference, we calculate anadditional 2.5% cost (9/365) incurred over this period in addition to the 20% costs that will presumably be filed after July 9, based on last year’sclaims. Here, $32,037,498 represents about 77.5% of the year’s total costs, meaning that medical costs will be approximately $41.3 million for2014-15. Since the plan’s premium revenues are $46,821,131 (Figure 4), the 2014-15 MLR will be about 88.3% using this method.We use the method (method II) that calculates slightly higher medical costs and slightly lower revenues for Aetna in our analysis above.

4In total, after two years of our contract with Aetna, the company could be running about $4.9 million below expectations.5This information was presented in a November 2014 slideshow presented to the GA, slide 6 [4].6If we total the 2013-14 estimated medical costs in Figure 2 for undergraduate dependents, graduate dependents, and voluntary (continuation)

plan members ($2,737,112) and subtract their total premiums ($960,557), we end up with a difference of $1,776,555. With more than 25,500 peopleon the Berkeley SHIP plan in the 2014-15 year, this would mean an average premium increase of about $69.67 per person. Even if we accountedfor Aetna’s expected 84% MLR (i.e., if we include a 16% surcharge to cover Aetna’s operating costs), the average increase per person would beabout $80.82. Significantly, these calculations are based off of projections that we know ended up being overestimates, meaning the final averagecost to cover these individuals is likely a bit lower. See Point 3.

7For more detailed information on these rising costs, see our Berkeley Healthcare Report, forthcoming.

3

our deductibles went up from $200 to $300 this year. Why these substantial hikes, especially after cutting people fromour plan? Aetna and UHS obviously intended to raise premiums regardless of how students voted on the question ofkeeping dependents and voluntary members on the plan; it was simply a matter of how steep the hikes would be. Inyet another set of documents obtained by the UAW 2865 from the UC Office of the President, it was calculated thatvoting dependents off the plan would reduce Aetna’s already planned premium increases by $193 per undergraduateand $384 per graduate student (Figure 5). But we didn’t end up saving quite that much. In other words, the premiumsavings students were promised turned out to be inflated, perhaps to increase the pressure to drop dependents andvoluntary members.8 After voting people off the plan, graduate students in particular “saved” less than they were toldthey would.

6 UHS had a better insurance offer.Most concerning is that last year, Berkeley students had a better insurance offer. UHS had an opportunity to end itscontract with Aetna, walking away from this flawed plan and rejoining UC SHIP, a decision students at UC Davisopted for last year when they ended their contract with Aetna. UC SHIP not only would have allowed us to maintaininsurance for dependents and voluntary members, but it would have cost us slightly less and offered roughly equalcoverage. However, SHIAC, a committee closely associated with UHS, pressured student groups into approving theirsuggestion to stay with Aetna in spite of this compelling offer (Figure 6). SHIAC asserted that this decision was in ourbest interests ostensibly to save $250,000 in IT costs. This is hard to believe. While $250,000 is a significant sum ofmoney for students, it is a relatively minor cost in the larger scheme of our health plan. It is also the sum of the errorwe caught in Point 1, indicating that UHS isn’t carefully monitoring accounting issues of this magnitude. SHIAC alsocited vague concerns about UC SHIP’s “operational and financial stability.” However, UC SHIP actually appears to bein very sound financial health this year (Figure 7). Why didn’t we follow UC Davis’ decision and abandon Aetna torejoin UC SHIP? Why didn’t UHS at least use this counter offer to negotiate a better deal with Aetna? The accuracyof Aetna’s projections aside, why does UHS assume responsibility for the profitability of Aetna’s activities? To date,UHS has not been willing to share the specifics of their contract with Aetna, but their actions suggest either a conflictof interest or the existence of a contract that annulled UHS’s bargaining position.

7 Aetna was reporting better returns last year.In 2014-15, the year Aetna and UHS were asking students to make this decision, they were reporting better returnsthan at the same time the year before. Our calculations are that the plan’s final MLR will likely end up at about 88.3%in 2014-15, still earning Aetna about 4.3% below probable expectations, but showing signs of steady improvementfrom Aetna’s perspective following significant annual premium increases and relatively stable medical costs.9 So whythe urgency to drop people from our insurance plan?

8 Was this a sham to get rid of costly members?Aetna kept a list of the 15 costliest people on our plan in 2013-14, which included individuals with brain damage,ovarian endometriosis, significant mental health needs, and cancers. We don’t know if these were students or theirfamily members, but as shown in Figures 2 and 3, we do know that Aetna was zeroing in on our sick dependentsand volunteer plan members (also called “continuation plan members”) and wanted to remove them from our healthplan to lower Aetna’s costs and increase the company’s margins. At present, it is unclear if Aetna’s method forcalculating costs for dependents and volunteer plan members is an appropriate or legal way to identify and isolate“risky populations” under ACA guidelines. There are provisions in the ACA to prevent insurance companies from

8We note that these calculated savings are inconsistent with the difference between the premium hikes that were threatened with in November andour final premium increases after voting people off the plan. Here are the discrepancies: The actual difference between the November projections [4]and final premium increases are about $160 for undergraduates ($550-$390) and $250 for graduates ($850-$600). At some point, someone inflatedthese projected premiums savings to $193 for undergraduates and $384 for graduates (Figure 5), where the latter is particularly off the mark.

9See Note 3 for our calculations.

4

making financial decisions based on a few high-cost individuals, but it seems that these peoples’ health needs mayhave driven Aetna’s decisions nonetheless.10

9 Cutting health insurance will negatively impact people.

While the dropping of dependent and voluntary insurance was framed as a non-issue impacting a relatively smallgroup of people, the loss of health insurance has detrimental implications for a number of communities at Cal. Theseinclude undocumented people, who have very limited access to affordable alternative health insurance; internationalpeople, many of whom are not eligible for Medi-Cal and also now need to purchase several forms of supplementaryinsurance to meet visa requirements; and people with significant health needs, many of whom will struggle to findaccess to life-sustaining healthcare at an affordable price, even through the Exchange marketplaces.11 Moreover, theelimination of these forms of health insurance sends a signal that UC Berkeley does not support students with families,particularly if our family members have significant health needs and/or are not U.S. citizens. We are concerned thatUHS failed to advocate for our broader community, jeopardizing the health of many individuals who need access tocare most.

10 UHS manufactured student consent.

UHS sought support for their plans from both the Graduate Assembly (GA) and Associated Students of University ofCalifornia (ASUC), but never obtained it through a democratic process. At a November 2014 meeting of the ASUC, aUHS representative/SHIAC member12 briefly presented candidate budgeting measures introduced to curb the excessivepremium hikes that would result from renewing their contract with Aetna [4]. ASUC senators refused to take a voteon the proposed measures, requesting more information. After a similar presentation during a November 2014 GAmeeting, a straw poll (an informal, non-binding vote) was taken to gauge the GA delegates’ sentiment regarding UHS’sproposal, and the result favored dropping dependents and other voluntary plan members. This straw poll, however, didnot substantiate formal approval from the GA. UHS did not obtain formal approval from GA delegates before finalizingtheir decision to remove dependent and voluntary coverage from the plan. Instead, in February 2015, UHS/SHIACapproached the ASUC and the GA with a new presentation outlining two available options (remain with Aetna anddrop dependents or return to UC SHIP, keep dependents, and have lower premiums; see Figure 8). Shortly thereafter,UHS/SHIAC provided the GA and ASUC executive boards with a prewritten letter of support (Figure 9), endorsingthe UHS-prefered option of staying with Aetna. While the GA executive board declined to sign the letter, they alsofailed to bring the issue to the attention of their constituents. The ASUC executive board, in contrast, signed theletter, without ASUC senate approval. We find that UHS clearly attempted to pressure the GA and ASUC executiveboards to garner superficial support for their preferred health insurance arrangements. Neither of these student bodiestruly challenged UHS’s narrative or sought to expand the conversation among students who were impacted by thesedecisions.

10Aetna seems to have been eligible to receive subsidies through an ACA program called “reinsurance” for enrolling relatively high-cost peoplein its insurance plan. Reinsurance subsidies are intended to deter insurance companies from trying to dump costly people with significant healthcareneeds from insurance plans. At present, we are not certain whether Aetna received reinsurance benefits starting in 2014.

11To be clear, the BHC celebrates the ACA and its provision of affordable healthcare for millions of previously uninsured people. Nevertheless,there remain gaps in its coverage. More information on insurance access for non-U.S. citizens can be found at Think Progress [2] and in the BerkeleyHealthcare Coalition’s forthcoming report, which considers the impact of the loss of insurance for members of the UC Berkeley community.

12It appears that the GA had a lack of clarity as to the role of this particular individual: specifically, whether she represented the opinions of UHS,SHIAC or both [5]. Regardless, she had a potential conflict of interest: after making presentations promoting UHS’s preferred Aetna option to theGA, the ASUC, and their executive boards, she took a paid staff position with UHS as their student health insurance manager. That position hasincluded making presentations which defend the university’s decision to stay with Aetna.

5

ConclusionsAll of this happened in the lead up to Aetna’s merge with Humana earlier this summer, an acquisition worth about $37billion.13 We don’t know at present how this merger impacted Aetna’s business practices, but it appears that they werereporting ever-higher profits just before the buy-out was announced. We are working on confirming a statement from abroker at our union’s June 19 healthcare meeting that Aetna cut similar benefits for as many as 50 student health plansthis year.14 If so, it seems as if many schools should be asking similar questions as the ones we’ve outlined here.

We as a Berkeley student body need to continue seeking information about why and in whose interests decisionsabout our student health plan are made. Many members in our community will be struggling this year as a result of thisunfortunate and controversial decision—one we will all end up paying for with poorer coverage through an insurancecompany set on pushing profits.

The Berkeley Healthcare Coalition will continue to advocate on behalf of our entire community, students andtheir family members, in good health or with health needs. To get in touch, contact us at [email protected].

13For analysis on this merger and its potential impact for consumers, see [1].14To date, we’ve been able to confirm that Aetna cut most dependent health insurance options for Arizona State University, Cal Poly San Luis

Obispo, Emory University, University of Arizona, and University of California Santa Barbara.

6

A Supporting Evidence

Figure 2: July 2014 Aetna Report, cost projections.

7

Figure 3: July 2014 Aetna Report, anticipated MLR and cost drivers.

8

Figure 4: Actual plan costs for 2013-14 and 2014-15 (through June 30, 2015).

9

Figure 5: Promised premium savings for voting dependents off of Berkeley SHIP. At present, we are uncertain whoprepared these numbers, which were received from the UC Office of the President through a Request for Informationmade by the student workers union UAW 2865.

10

Figure 6: SHIAC document demonstrating better offer and internal pressure to stay with Aetna.

11

Figure 7: UC SHIP Financial Statement.

12

Status of Student Health Insurance Plan Renewal—February 12, 2015

Decision point and timeline By February 27, 2015, the campus needs to decide whether it will continue to manage its own Student Health Insurance Plan (SHIP) through Aetna Student Health or return to UC SHIP through Anthem. The key factors in this decision include premium costs, whether the campus feels returning to UC SHIP is worth certain risks, and whether the campus can successfully manage the operational changes required to return to UC SHIP for 2015-‐16. Analysis of options There are real and potential advantages and disadvantages to both options. Berkeley SHIP (Aetna) UC SHIP (Anthem) Pros • Berkeley retains control over benefits

• No subsidization of other UC campuses • TBD: A 3 year contract with Aetna Student Health would provide stability and predictability for benefit levels and premiums

• Berkeley has invested well over $250,000 in infrastructure and staffing costs to institute IT and procedural systems to integrate with Aetna

• No dependent or continuation plan (significant premium reduction when these groups are not included)

• Lower premium costs to students o Per semester premium increases from

FY14 to FY15: $160 for undergraduates and $241 for graduate students

• Lower deductible: $200 per year • System wide pooling (greater number of students enrolled) and UC’s renewal methodology (financial formula for subsequent years’ premium costs) could lead to better prices for Berkeley students

• TBD If no three-‐year contract with Aetna: Systemwide pooling methodology means greater predictability of premium costs over time

Cons • Slightly higher premium costs to students o Per semester premium increases

from FY14 to FY15: $194 for undergraduates and $300 for graduate students

o Compared to UC SHIP: $34 dollars more per semester for undergraduates and $59 for more per semester for graduate students

• Higher deductible: $300 per year • No dependent or continuation plan (contributes to increased premiums due to high utilization by these subscribers)

• Systemwide pooling and UC’s renewal methodology might lead to worse prices for Berkeley students

• Systemwide pooling and UC’s renewal methodology may result in Berkeley subsidizing premium increases for other UC campuses

• 1 year contract only with no rate guarantee for future years

• Additional financial investment will be needed to integrate with Anthem systems and procedures, at a time of a key management vacancy at University Health Services

• Technological integration may be impeded due to the UCB IT moratorium and result in our inability to change plans regardless

• While UCOP/Anthem will allow flexibility with plan design, there is no negotiating premiums set by their renewal methodology

Figure 8: Comparison between SHIP renewal options, supplied to the GA by UHS. It seems reasonable to assume thatthe same or a similar document was sent out to ASUC as well, but to date, we have not been able to confirm this.

13

February 24, 2015

Dear Chancellor Dirks,

On behalf of UC Berkeley’s over 37,000 students, the ASUC, Graduate Assembly, and Committee on Student Fees support staying with Aetna Student Health for the 2015-16 school year. As the student leaders of this campus, we believe the benefits of staying with our current provider for another year outweigh the benefits of re-joining UC SHIP. We have carefully reviewed the options presented by UC SHIP for the upcoming school year. Although the UC SHIP plan offer was competitive, students still do not have confidence in UC SHIP and have concerns about its operational and financial stability.

• The benefits of staying with our current provider for another year outweigh the benefits of re-joining UC SHIP.

• The price difference between UC SHIP and Aetna is relatively small and not worth the transition costs incurred.

• Student leadership does not have confidence in UC SHIP, especially concerns about its operational and financial stability.

• University Health Services invested $250,000 in IT and communications infrastructure to transition from Anthem to Aetna, and would need to spend approximately $250,000 to transition back to UC SHIP. The lost original investment and need for new $250,000 investment if we transition back to UC SHIP creates a financial risk we cannot support.

• SHIP remains a high-quality, competitive plan in the marketplace.

• Having a UC Berkeley specific insurance plan allows us better financial control of our program and also allows us benefit flexibility, thus, we can tailor our plan to our specific student population.

• The majority of Graduate Assembly supported dropping SHIP’s dependent/continuation plan as a cost-savings measure.

• We are in support of revisiting our options next year for the 2016-17 plan year.

We ask that you stand behind our students in remaining with our current SHIP provider Aetna Student Health for the 2015-16 school year. We thank you for your continued support of Berkeley students.

Sincerely

John Ready

Pavan Upadhyayula

Joy Chen GA President ASUC President CSF Co-‐Chair

CC: Rosemarie Rae, CFO Claudia Covello, UHS Executive Director VCSA Harry LeGrande VCAF John Wilton

Figure 9: Prewritten letter sent to the GA and ASUC by UHS/SHIAC. This letter ended up being signed by the ASUCpresident, not by the GA president. To date, we haven’t been able to verify whether the Committee on Student FeesAnd Budget Review (CSF) co-chair signed the letter or not.

14

References[1] D. Diamond. Aetna buys humana for $37 billion, but deal doesn’t add up. http://www.forbes.com/

sites/dandiamond/2015/07/03/aetna-buys-humana-for-34-billion-but-deal-doesnt-add-up/, July 3, 2015. [Online; accessed August 1, 2015].

[2] E. Y.-H. Lee. A simple guide to the affordable care act for immigrants. http://thinkprogress.org/immigration/2013/10/01/2708441/affordable-care-act-immigrant-types-coverage/, Oct 1, 2013. [Online; accessed August 1, 2015].

[3] The Commonwealth Fund. Health insurance marketplace premiums. http://www.commonwealthfund.org/interactives-and-data/maps-and-data/health-insurance-marketplace-premiums, 2015. [Online; accessed August 1, 2015].

[4] The Graduate Assembly. Berkeley SHIP Changes. http://ga.berkeley.edu/wp-content/uploads/2015/04/SHIP-Presentation.pdf, November 2014. [Online; accessed August 1, 2015].

[5] The Graduate Assembly. Minutes from the november delegate meeting. http://ga.berkeley.edu/wp-content/uploads/2015/04/November-Minutes.pdf, November 6 , 2014. [Online; accessed Septem-ber 1, 2015].

15