berkeley board fellows & social sector solutions professional development workshop

TRANSCRIPT

The Intersection of Finance and Strategy:

Using Financial Data to Inform Strategic Decisions

By

Brent Copen

Why do so many

nonprofits endure

ongoing financial

challenges, even in

good economic

times?

Chapter 1:

An

Introduction

To The

Nonprofit

Business

Model

Components of the Business Model

Who we are

& what we do

How we do it

How we finance it

Business Model

4

Source: The Nonprofit Strategy Revolution

The Business Model

How we

do it

How we finance it

Who we are & What

we do

5

Source: The Nonprofit Strategy Revolution

Where we

work

Our competitive

advantage

A Question for the group

Are nonprofits allowed to

generate profits?

6

Surpluses Reinvested in The Business

7

New opportunities

Facility

Rainy day

Investment

A Question For The Group

Who is the nonprofit’s

“customer”?

8

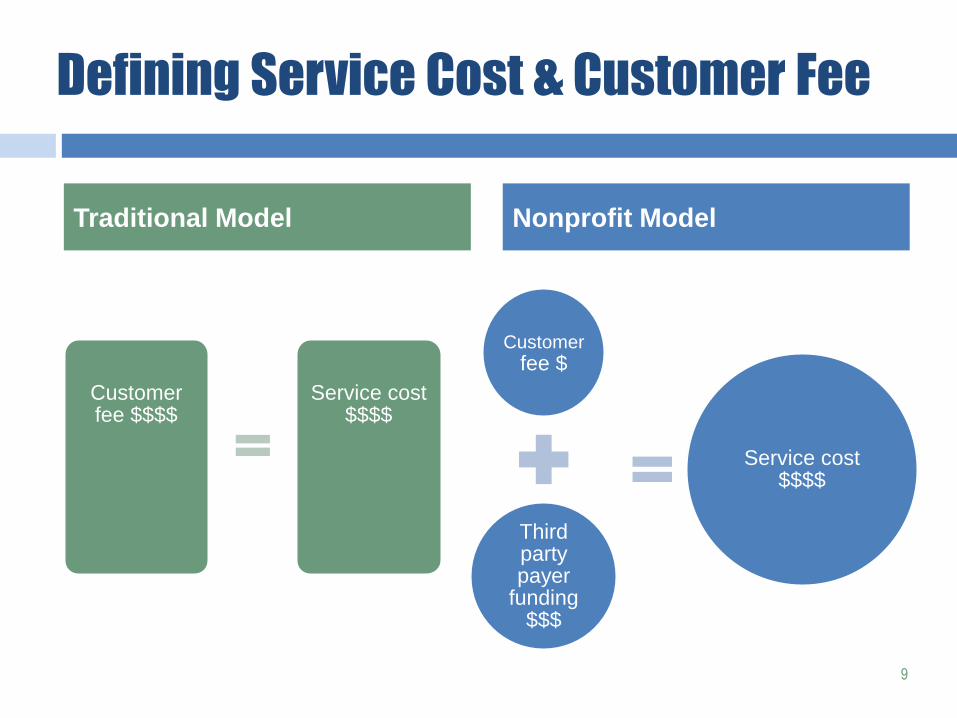

Customer fee $

Third party payer

funding $$$

Service cost $$$$

Defining Service Cost & Customer Fee

Customer fee $$$$

Service cost $$$$

Traditional Model Nonprofit Model

9

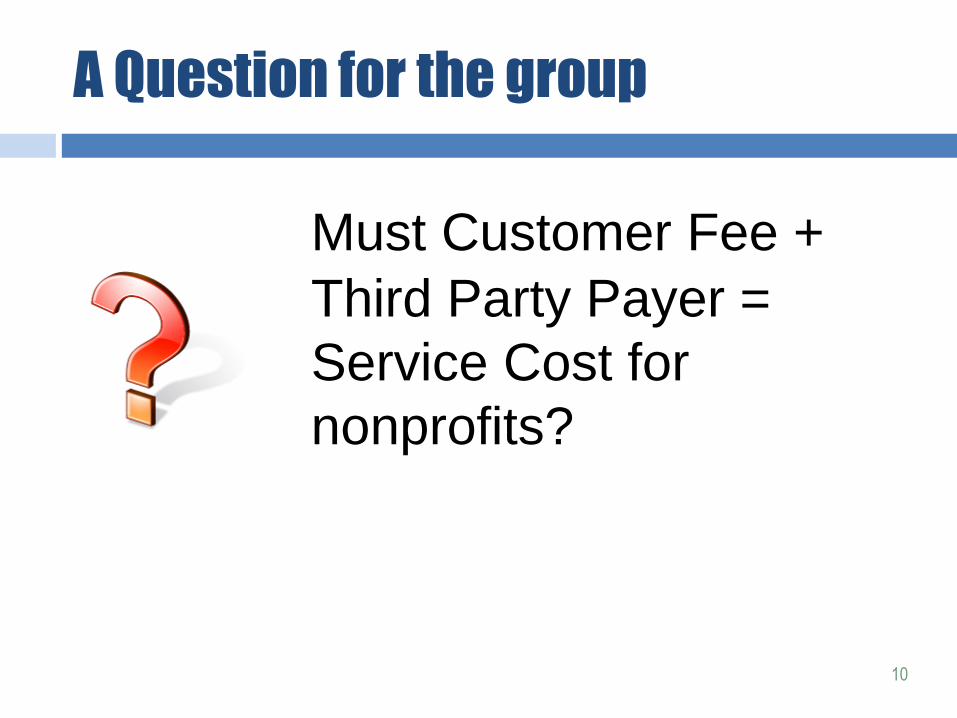

A Question for the group

Must Customer Fee +

Third Party Payer =

Service Cost for

nonprofits?

10

For Profit:

Service Cost = Customer Fee

11

Item Cost Fee

Ingredients

Coffee $0.12

Dairy $0.05

Cup + lid + sleeve $0.25

Overhead

Labor $0.90

Rent $0.25

Marketing $0.12

G & A $0.50

Operating profit $0.30

Service cost $2.49

Customer fee $2.49

Non Profit:

Service Cost ≠ Customer Fee

12

Item Cost Fee

Ingredients

Coffee $0.12

Dairy $0.05

Cup + lid + sleeve $0.25

Overhead

Labor $0.90

Rent $0.25

Marketing $0.12

G & A $0.50

Operating profit $0.30

Service cost $2.49

Customer fee $2.00

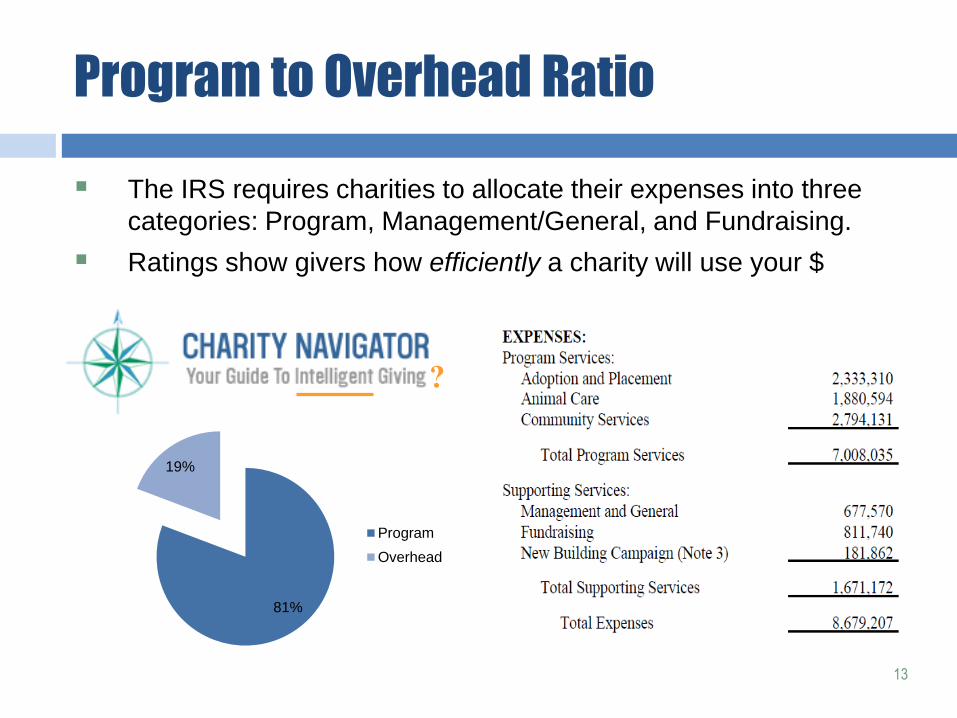

Program to Overhead Ratio

The IRS requires charities to allocate their expenses into three

categories: Program, Management/General, and Fundraising.

Ratings show givers how efficiently a charity will use your $

13

?

81%

19%

Program

Overhead

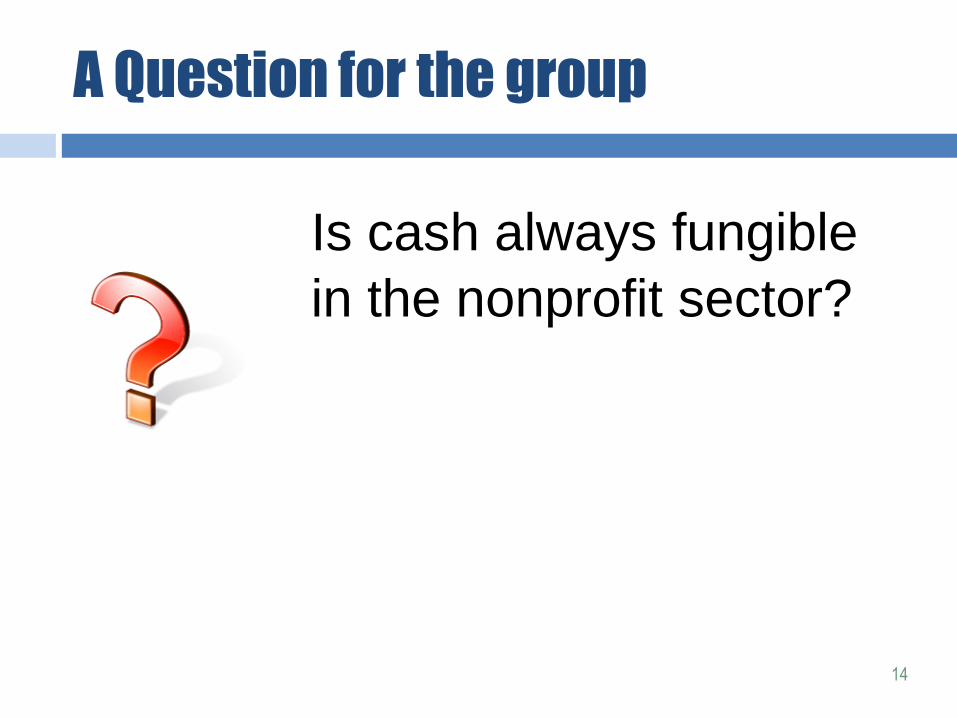

A Question for the group

Is cash always fungible

in the nonprofit sector?

14

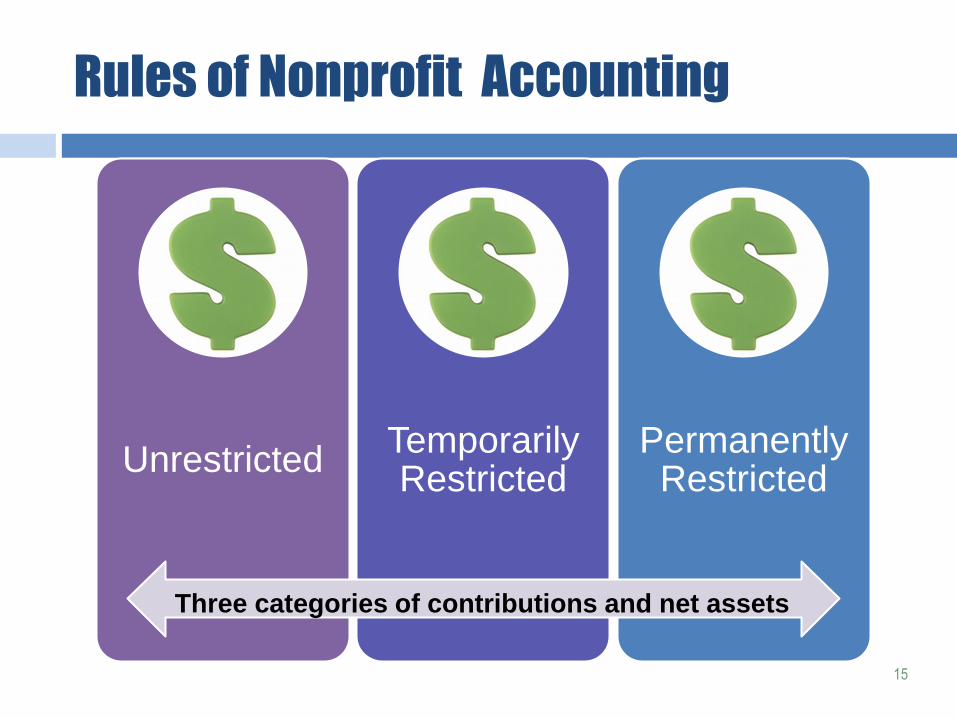

Rules of Nonprofit Accounting

15

Unrestricted Temporarily Restricted

Permanently Restricted

Three categories of contributions and net assets

The Bottom Line for Nonprofits

16

Income Statement or Statement of Activities

Total Change in Net Assets (surplus/Deficit): $450,000

Temporarily restricted Change $400,000 Receipts in excess of releases

Unrestricted Change in Net Assets $50,000

Non-operating Revenues $100,000 e.g. campaign revenues for capital

Unrestricted Operating Change in Net Assets ($50,000)

Balance Sheet or Statement of Financial Position

Total Net Assets (Equity): $15M

Permanently Restricted $10M e.g. endowment

Temporarily Restricted $4M e.g. multi-year funding

Unrestricted Net Assets $1M

Unrestricted Plant and Equipment Net Assets $1.5M

Unrestricted Liquid Net Assets ($500k)

Cash and Cash Equivalents $2M

Temporarily Restricted $1.8M Prepaid for future uses

Unrestricted $200k

Chapter 2:

A Look at

The

Numbers

Statement of Activities

<#>

Analyzing the Statement of Activities

Go to the unrestricted column first

Segregate operating revenues/expenses from non-

operating

Analyze results

Look for amazement numbers

19

Budgeting

A budget is a plan for how an organization will get and use money

over a period of time to achieve specific goals

A declaration of priorities and how limited resources are allocated

A budget, as a planning tool, is only as good as your assumptions

Be explicit about your assumptions

Monitoring the budget is critical to reaching your goals

20

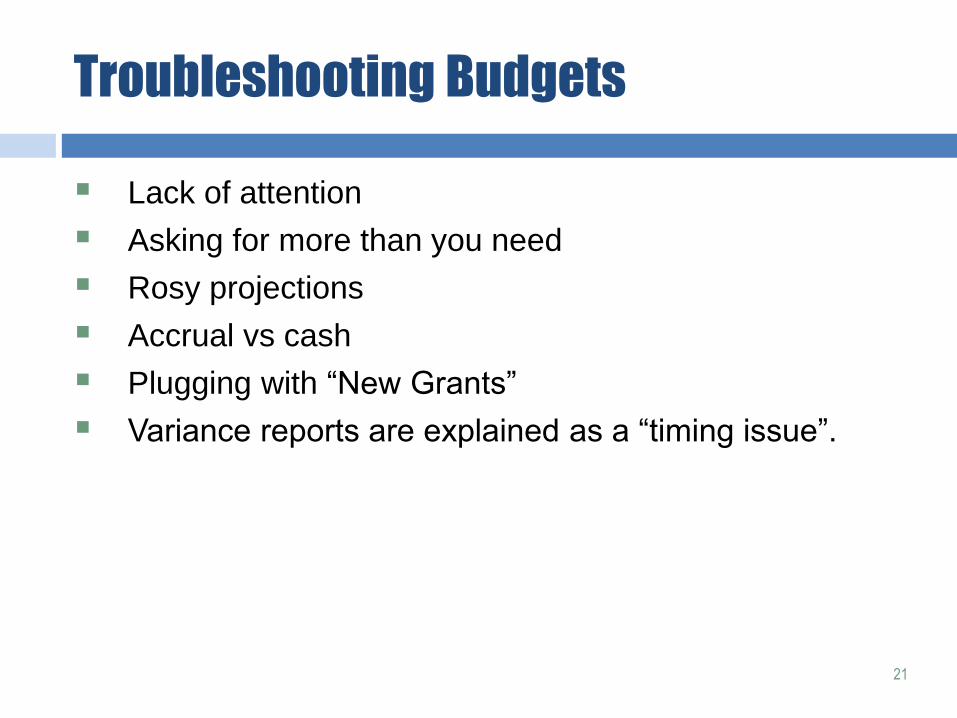

Troubleshooting Budgets

21

Lack of attention

Asking for more than you need

Rosy projections

Accrual vs cash

Plugging with “New Grants”

Variance reports are explained as a “timing issue”.

Program Profitability

22

Program Direct Indirect

$ in Thousands School Afterschool Fitness Residential Camp

Subtotal

Program General Total Budget

Revenue Earned

Tuition/fees 972 207 826 217 2,222 2,222

Rental income 1,145 1,145 1,145

Other 42 42 42

Revenue Contributed

Individual 25 1 26 67 93

Grants 5 14 19 19

Net assets released 97 97 97

0

Total revenue 1,044 222 826 1,242 217 3,551 67 3,618

Expenses

Total expenses 1,258 208 731 988 180 3,365 421 3,786

Surplus/Deficit -214 14 95 254 37 186 -354 -168

Allocation 157 26 91 124 23

Total surplus/deficit -371 -12 4 130 14

From Jeanne Bell Peters and Elizabeth Schaffer, Financial Leadership for Nonprofit Executives: Guiding Your Organization to

Long-term Success, Fieldstone Alliance, 2002. Adapted from Boston Consulting Group’s Growth-Share Matrix.

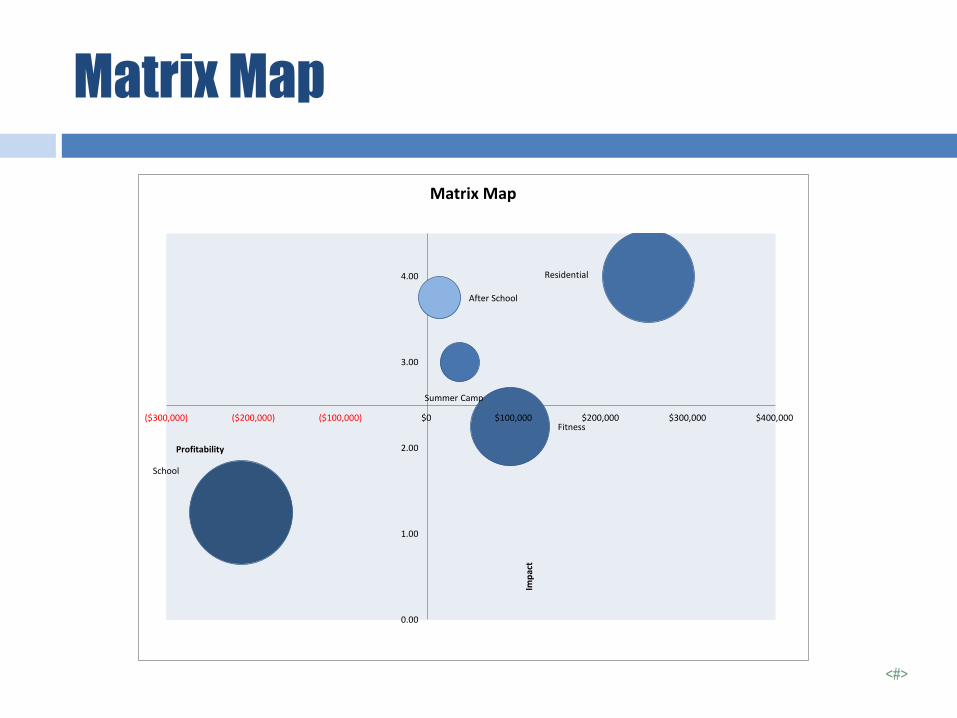

Dual-Bottom Line Matrix

23

High Mission Impact Low Sustainability

High Mission Impact High Sustainability

Low Mission Impact Low Sustainability

Low Mission Impact High Sustainability

Financial Sustainability

Mis

sio

n Im

pac

t

Dual Bottom Line – Sample Questions

Program aligns with Theory of Change (i.e. to realize the

impact we want to have in our community.

Program demonstrates excellent execution (e.g. as

demonstrated by excellent client feedback, measurable

impact in our community, focused and enthusiastic staff,

etc.)

Program fills an important gap (based on cultural

competence, geographic access, and other factors, we

are the best agency to offer this program.)

Program has leverage potential (e.g. as a feeder to

other programs).

24

Matrix Map

<#>

School

After School

Fitness

Residential

Summer Camp

0.00

1.00

2.00

3.00

4.00

($300,000) ($200,000) ($100,000) $0 $100,000 $200,000 $300,000 $400,000

Imp

act

Profitability

Matrix Map

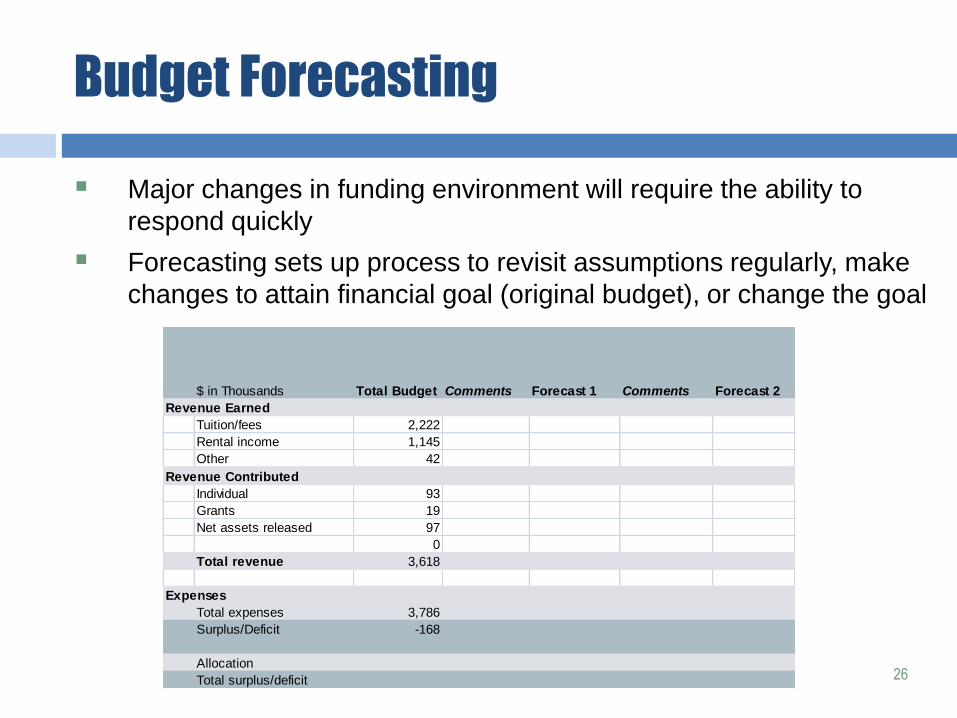

Budget Forecasting

26

Major changes in funding environment will require the ability to

respond quickly

Forecasting sets up process to revisit assumptions regularly, make

changes to attain financial goal (original budget), or change the goal

$ in Thousands Total Budget Comments Forecast 1 Comments Forecast 2

Revenue Earned

Tuition/fees 2,222

Rental income 1,145

Other 42

Revenue Contributed

Individual 93

Grants 19

Net assets released 97

0

Total revenue 3,618

Expenses

Total expenses 3,786

Surplus/Deficit -168

Allocation

Total surplus/deficit

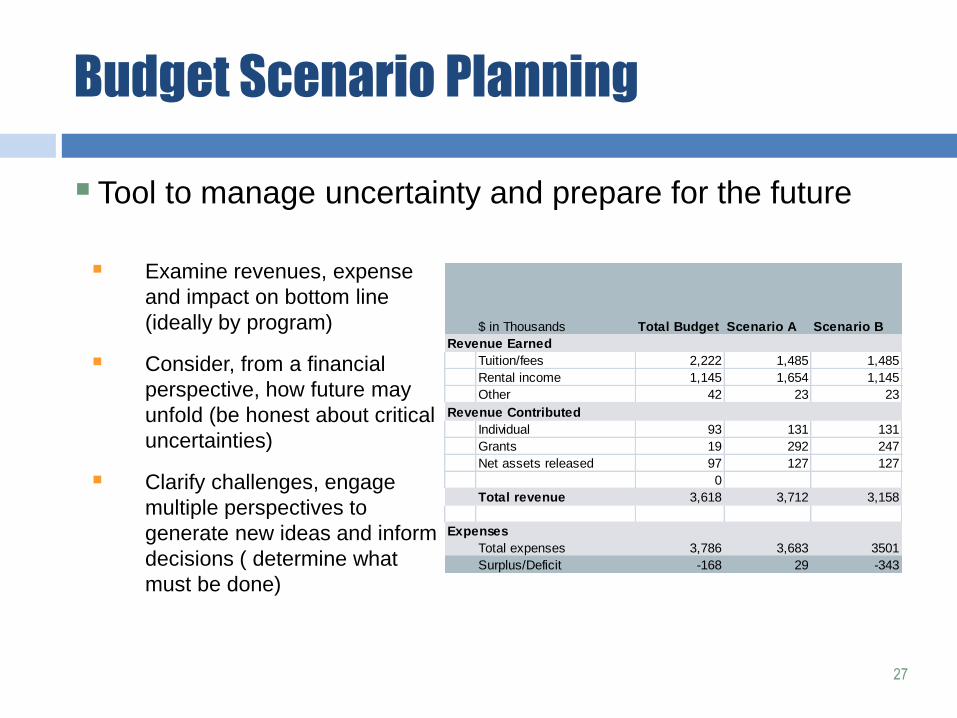

Budget Scenario Planning

27

Examine revenues, expense

and impact on bottom line

(ideally by program)

Consider, from a financial

perspective, how future may

unfold (be honest about critical

uncertainties)

Clarify challenges, engage

multiple perspectives to

generate new ideas and inform

decisions ( determine what

must be done)

Tool to manage uncertainty and prepare for the future

$ in Thousands Total Budget Scenario A Scenario B

Revenue Earned

Tuition/fees 2,222 1,485 1,485

Rental income 1,145 1,654 1,145

Other 42 23 23

Revenue Contributed

Individual 93 131 131

Grants 19 292 247

Net assets released 97 127 127

0

Total revenue 3,618 3,712 3,158

Expenses

Total expenses 3,786 3,683 3501

Surplus/Deficit -168 29 -343

Strategic vs. Business Planning?

Strategic planning is, at its best, the process of

considering and making strategic decisions.

- Periodic examination of organizational, programmatic

and/or operational strategies

Business planning is the process of determining the

parameters of an economically and operationally

successful undertaking

- Business planning is most powerful when the strategy calls

for some major change that must be tested.

- The value of the business plan is directly related to the

rigor of the planning process.

28

Source: La Piana Consulting

Business Planning: What Makes

Nonprofits Different?

Market failure. Nonprofits must make up the market

shortfall by attracting other sources of revenue –

including from third party payers.

Third party payers. A nonprofit organization’s

“customers” are not just the individuals and groups

availing themselves of a particular product or service.

Difficulty accessing growth capital. Venture capital,

long a fixture of the for-profit sector, has only recently

become a viable option for some nonprofits.

29

Source: La Piana Consulting

1-10-100 Rule

30

The Financials

“As every seasoned investor knows, financial projections for a new

company are an act of imagination. An entrepreneurial venture

faces far too many unknowns…Don’t misunderstand me: business

plans should include numbers. But those numbers should

appear mainly in the form of a business model that shows the

entrepreneurial team has thought through the key drivers of

the venture’s success or failure.”

- by William A Sahlman, How to Write a Great Business Plan

31