benchmarking liability claims management · • best practice liability claims mgmt • assessment...

TRANSCRIPT

Benchmarking Liability Claims Management

Rod McInnes & Steve Curley

Agenda

• Objective• Best Practice Claims Mgmt• Survey Methodology• Industry Results• Insurer Performance• Conclusions

Objective

• Best Practice Liability Claims Mgmt• Assessment of

– Current Industry Practice– Individual Insurer Performance

• Opportunities for Improvement• Conclusions

Why Best Practice?

• Claims costs the major expense• Claim handling expense a fraction of

costs• Good claims management can deliver

20%+ claims cost savings (for long tail business)

• Potential for competitive advantage

Best Practice Claims Management

• Developed elements of Best Practice• Experienced based

– Strategic & Operational Reviews– Australia and Overseas

• Achievable• Evolving – Not Fixed• Key Elements – not necessarily

comprehensive

Best Practice Elements• Claims Management Model• Early Claims Reporting • Triage and Segmentation• Timely Effective Communication• Appropriate Reserving• Proactive Management• Identify & Address Outliers• Optimal Resourcing • Effective Provider Management• Efficient Claims System• Measuring Performance

Best Practice Element Definitions

• Definitions would vary by class• Focus on Liability • 46 Components of Best Practice• Describe for each Component

– Best Practice– Satisfactory Practice– Poor Practice

Claims Management ModelComponent Description of Best PracticeDocumentation

Outcome Focus

Fully documented claims management model, providing guidance, direction and an overarching framework for claims staff

Claims management focused on outcomes and bottom line

Expected claims outcomes documented and linked to performance standards for claims staff

Staff performance assessment primarily based on assessment against these outcome focused standards.

Clarity of Expected Outcomes

Staff Performance

Consistency

Training

Claims management consistent across the class - no significant variation between branch, team or individual

Claims management model forms the basis for claims staff training (induction & other)

Claims Management Model - Documentation

Poor Satisfactory BestLimited documentation – reliant on individual expertise

Claims documentation focused on process (ie claims manual) - philosophy & approach not covered

Fully documented claims management model providing guidance, direction and an overarching framework for claims staff

Survey Methodology (1)• Rate Industry

Performance• Against poor,

satisfactory & best descriptors

• By Component (grouped in 11 elements)

Category ScorePoor 1

Mid-point 2

Satisfactory 3

Mid-point 4

Best 5

Survey Methodology (2)

• Questionnaire for liability claims practitioners

• Current & former• Targeted most senior liability claims mgr • 20 responses received (from 30 issued)• Includes most major liability insurers

Verify Best Practice Model

• Comment on missing / superfluous components

• Missing eg– Recoveries– Culture

• Nothing Superfluous• Validates Our Best Practice Model

Interpretation of Results• Examined proportion rated

– Best Practice – Above Satisfactory (better than satisfactory but not

best)

• Benchmark of 60% = “Good”• Shortfall below “good” represents opportunity• Summary results for the 11 best practice

elements

Claims Management Model - Results

0%

25%

50%

75%

100%

Documentation Outcome Focus Clarity ofExpectedOutcomes

StaffPerformance

Consistency Training

Best Practice Above Satisfactory Element Ave "Good"

Early Claim Reporting

0%

25%

50%

75%

100%

Promote Early Contact Monitor Delays Systems to Facilitate Reporting

Best Practice Above Satisfactory Element Ave "Good"

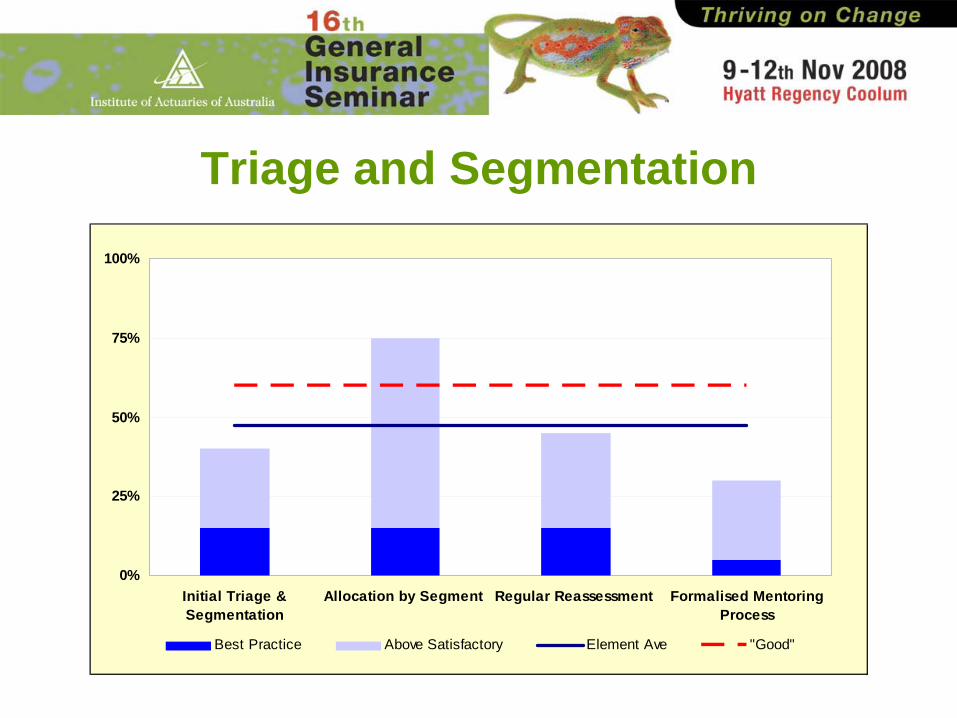

Triage and Segmentation

0%

25%

50%

75%

100%

Initial Triage &Segmentation

Allocation by Segment Regular Reassessment Formalised MentoringProcess

Best Practice Above Satisfactory Element Ave "Good"

Timely Effective Communication

0%

25%

50%

75%

100%

Early Contact Regular Systematic Comms Simple Clear Language

Best Practice Above Satisfactory Element Ave "Good"

Reserving

0%

25%

50%

75%

100%

Reserving Policy Initial Estimates &Regular Reviews

Legal Advisers Consistent Application

Best Practice Above Satisfactory Element Ave "Good"

Proactive Management

0%

25%

50%

75%

100%

Individual ClaimsMgmt Strategy

StrategiesOutcome Focused

Active Approach Regular Review Claims OfficerPrimarily

Responsible

Best Practice Above Satisfactory Element Ave "Good"

Identify & Address Outliers

0%

25%

50%

75%

100%

Identify & Address Outliers Continuous Sweeps for Outliers

Best Practice Above Satisfactory Element Ave "Good"

Provider Management

0%

25%

50%

75%

100%

Provider Selection Provider contract Provider Fees Allocation of Work PerformanceManagement

Best Practice Above Satisfactory Element Ave "Good"

Resourcing

0%

25%

50%

75%

100%

Target File Loads Actively MonitorFile Loads

StaffCompetencies

StaffPerformanceAssessment

RegularPerformance

Reviews

Sample FileReviews

Best Practice Above Satisfactory Element Ave "Good"

Claims Systems

0%

25%

50%

75%

100%

Modern Efficient System Efficient Support Process Measurement System Flexibility

Best Practice Above Satisfactory Element Ave "Good"

Measuring Performance

0%

25%

50%

75%

100%

Broad Based Monitoring Qualitative Monitoring Quantitative Monitoring

Best Practice Above Satisfactory Element Ave "Good"

Summary of Industry Results

0% 10% 20% 30% 40% 50% 60% 70%

Claims Management Model

Early Claims Reporting

Triage and Segmentation

Timely Effective Communication

Reserving

Proactive Management

Identify and Address Outliers

Provider Management

Resourcing

Claims System

Measuring Performance

Individual Insurer Performance

• Self against their peers• Across same Best Practice Elements• Asked to rate whether

– Below industry– On par with industry– Better than industry– At best practice

Results – Self Assessment vs Peers

0%

10%

20%

30%

40%

50%

Below IndustryAve

Industry Ave Mix of Ave /Better than Ave

ConsistentlyBetter than Ave

Best Practice

Rescaled Self Assessment

0%

10%

20%

30%

40%

50%

PerformanceGap

ConsistentlyBetter than Ave

Best Practice

Performance Gap Analysis44%

50%

56%

61%

35%

33%

61%

56%

61%

83%

83%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Claims Management Model

Early Claims Reporting

Triage and Segmentation

Timely Effective Communication

Reserving

Proactive Management

Identify and Address Outliers

Provider Management

Resourcing

Claims Systems

Measuring Performance

Performance Gap Consistently Better than Average Achieving Best Practice

Most Important Elements

• Proactive Management• Resourcing • Reserving

• Some correlation with performance• How to prioritise improvement efforts

Conclusions

• Poor understanding of current performance

• Claims managers not well placed to assess

• Significant scope for improvement• Better understanding insurer position

required• Further benchmarking required

Thank You

Questions?