behaviour in a canadian multi-payer, multi-provider … in a canadian multi-payer, multi-provider...

TRANSCRIPT

Behaviour in a Canadian

multi-payer, multi-provider health care market:

the case of the physiotherapy market in Ontario

by

Paul D. Holyoke

A thesis submitted in conformity with the requirements

for the degree of Doctor of Philosophy

Department of Health Policy, Management and Evaluation

University of Toronto

© Paul Holyoke 2009

ii

Behaviour in a Canadian multi-payer, multi-provider health care market: the case of the physiotherapy market in Ontario

Ph.D., 2009

Paul D. Holyoke

Department of Health Policy, Management and Evaluation, Faculty of Medicine, University of Toronto

Abstract

This is a study of several contentious issues in Canadian health policy involving the

interaction of public and private payers and for-profit (FP) and not-for-profit (NFP) providers;

the influence of health professionals on market structure; and the role of foreign investment. A

case study was used, the Ontario physiotherapy market in 2003-2005, with its complex mix of

payers and providers and foreign investment opportunities.

Key market features were: fragmented but substantial payer influence, effective though

uncoordinated cost control across payers, constrained labour supply, and fragmented patient

referral sources. These features increased the complexity of providers’ interactions with patients

and payers, reducing standardization and therefore favouring local, professional-owned small

business FP providers (FP/s) for ambulatory care. NFP Hospitals’ market share declined.

The findings generally confirmed expected behavioural differences between FP and NFP

providers but expected differences between investor-owned FP providers (FP/c) and FP/s

providers were not generally found. FP/s dominated the market, and FP/c providers appeared to

mimic FP/s market behaviours, competing in local sub-markets.

With no single or dominant payer, cost control difficulties were expected, but all 11 payer

categories (public and private) used various cost control mechanisms, resulting in significant

iii

collective but uncoordinated influence. Generally, no payer alone supported a provider’s

operations.

The dominant labour suppliers, regulated physiotherapists, were scarce and exerted

significant pressure, affecting market structure by asserting individual preferences and

professional interests. FP/s dominance resulted, supported by the traditional patient referral

source, physicians in small practices.

Very little foreign investment was found despite little protection for domestic providers

under NAFTA.

In sum, this study showed FP and NFP provider stereotypes are subject to payer pressure:

FP/c organizations can adapt by mimicking FP/s, and payers can modify NFPs’ assumed

community orientation. Labour shortages and historical referral patterns can make individual

professionals and their preferences more influential than their collective profession without

diminishing the importance of professional interests. The degree and structure of payer control

can make a market unattractive to foreign investors. Finally, this market – neither a planned or

standard market – had a service provision pattern more broadly influenced by professionalism

and practitioner interests than policies or prices.

iv

Acknowledgements

I want to acknowledge the tremendous level of professional support I received during the

preparation of this dissertation from the members of my thesis committee. Dr. Raisa Deber, my

supervisor, was supportive and challenging the entire time, providing me with valuable

mentorship, and helpful guidance and suggestions. Raisa also helped me keep the doctoral work

in perspective with lively discussions about popular music and Canadian and American politics.

Professor Molly Verrier, a member of my thesis committee, contributed substantially with very

helpful challenges to the analysis of the physiotherapy market as it emerged, ensuring a good

balance among the various disciplinary perspectives I was trying to reflect in this work. Dr. Tony

Culyer, also a member of my thesis committee, was very supportive through the entire process.

He provided excellent critiques and suggestions for improvements, and provided very useful

advice on a number of fronts.

I also want to thank Dr. Karen Spalding, Dr. Sharon Switzer-McIntrye and Dr. Rhonda

Cockerill for agreeing to be reviewers for the defence of my dissertation. They asked some

provocative and probing questions, and the dissertation was improved as a result.

Many other people provided support throughout the entire process. I would like to

acknowledge Dr. Michel Landry, who gave helpful suggestions during the formulation of the

research questions and the data collection phase, and was a good sounding board for some of the

interesting and challenging issues that arose. Cindy Gauvreau, also doing doctoral work in the

Department of Health Policy, Management and Evaluation, provided support and help with some

of the methodological issues. Exceptional assistance during the data collection phase was also

provided by Dr. Nibal Lubbad, Jonah Perucha, Philip Galacgac, and Känecy Oñate.

Of course, I will always be grateful to my family – Daisy, Grace and Alice – who were

always encouraging and supportive and interested in my work, and who helped me balance my

academic work with a rich home life.

Finally, I wish to acknowledge the financial support of the Canadian Institutes for Health

Research in the form of a Doctoral Research Award.

v

Table of Contents

Abstract .......................................................................................................................... ii Acknowledgements ...................................................................................................... iv List of acronyms and terms ....................................................................................... viii List of tables ................................................................................................................ xiv List of figures ............................................................................................................. xvii List of appendices .................................................................................................... xviii

Chapter 1 – Introduction and overview ................................................... 1

1.1 Statement of the issues ........................................................................................... 1

1.1.1 Public & private financing and FP & NFP delivery of health care ................ 3 1.1.2 The role of health professionals ..................................................................... 4 1.1.3 Investment in a health care market ................................................................. 5

1.2 Organization of the report ....................................................................................... 7

Chapter 2 – The structure of health care markets .................................. 9

2.1 Ideal markets and health care markets .................................................................. 9

2.1.1 Uncertainty of demand .................................................................................. 10 2.1.2 Asymmetry of information ............................................................................. 11 2.1.3 Insurance as a response to the uncertainty of demand ............................. 12 2.1.4 Regulation to address provider moral hazard ............................................. 13 2.1.5 Government involvement .............................................................................. 15

2.2 Porter’s model applied to health care markets ................................................... 16

2.2.1 Outline of Porter’s model .............................................................................. 16 2.2.2 Rivalry among existing providers in a market ............................................. 18 2.2.3 Buyer power .................................................................................................... 33 2.2.4 Supplier power ............................................................................................... 40 2.2.5 Threat of new entrants ................................................................................... 42 2.2.6 Threat of substitutes ...................................................................................... 51

2.3 Research questions ............................................................................................... 52

Chapter 3 – Study design and methods ................................................ 56

3.1 Case study – the physiotherapy market in Ontario ............................................ 56 3.2 Data collection and analysis ................................................................................. 59

3.2.1 Documents ...................................................................................................... 59 3.2.2 Secondary analysis of existing data files .................................................... 62 3.2.3 Market Participants Database ....................................................................... 67 3.2.4 Survey of physiotherapy provider organizations in 12 counties ............... 70

vi

3.2.5 Key informant interviews ............................................................................... 77 3.2.6 Ethics and confidentiality .............................................................................. 82

3.3 Outline of subsequent chapters ........................................................................... 83

Chapter 4 – Overview of the physiotherapy market ............................. 85

4.1 Need for physiotherapy services .......................................................................... 85 4.2 Buyers and sellers ................................................................................................. 88 4.3 Services being bought and sold ........................................................................... 91 4.4 Eligible labour supply ............................................................................................ 95

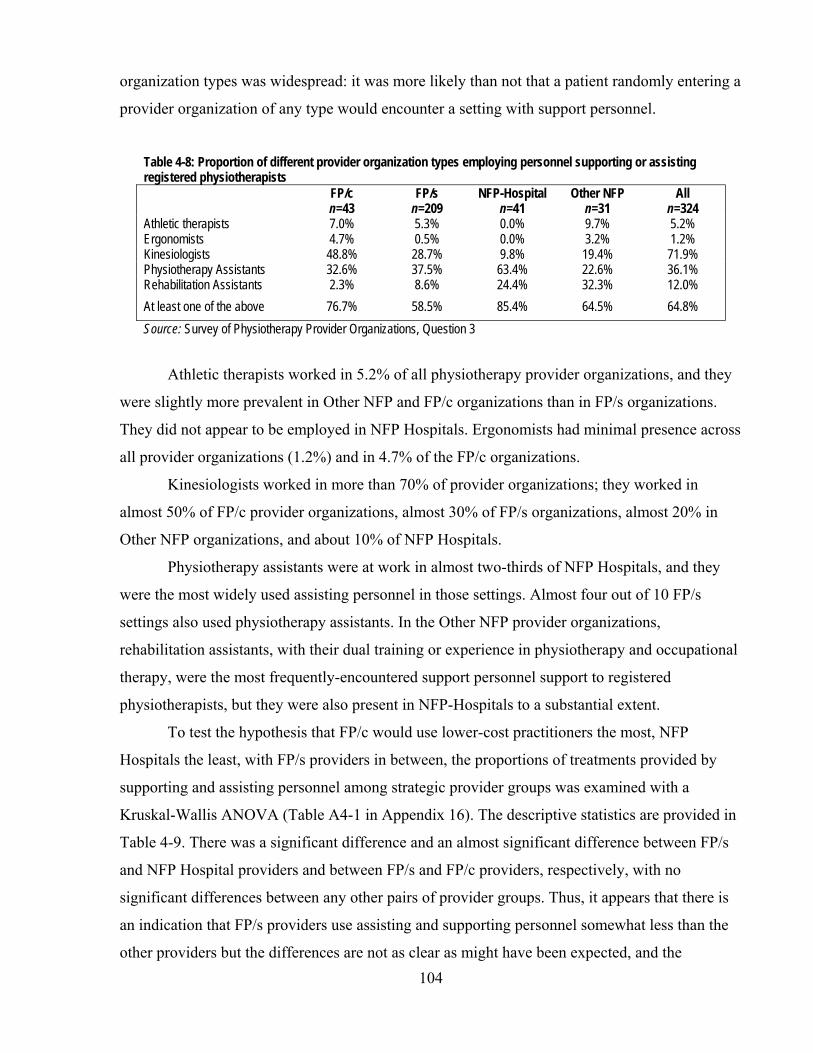

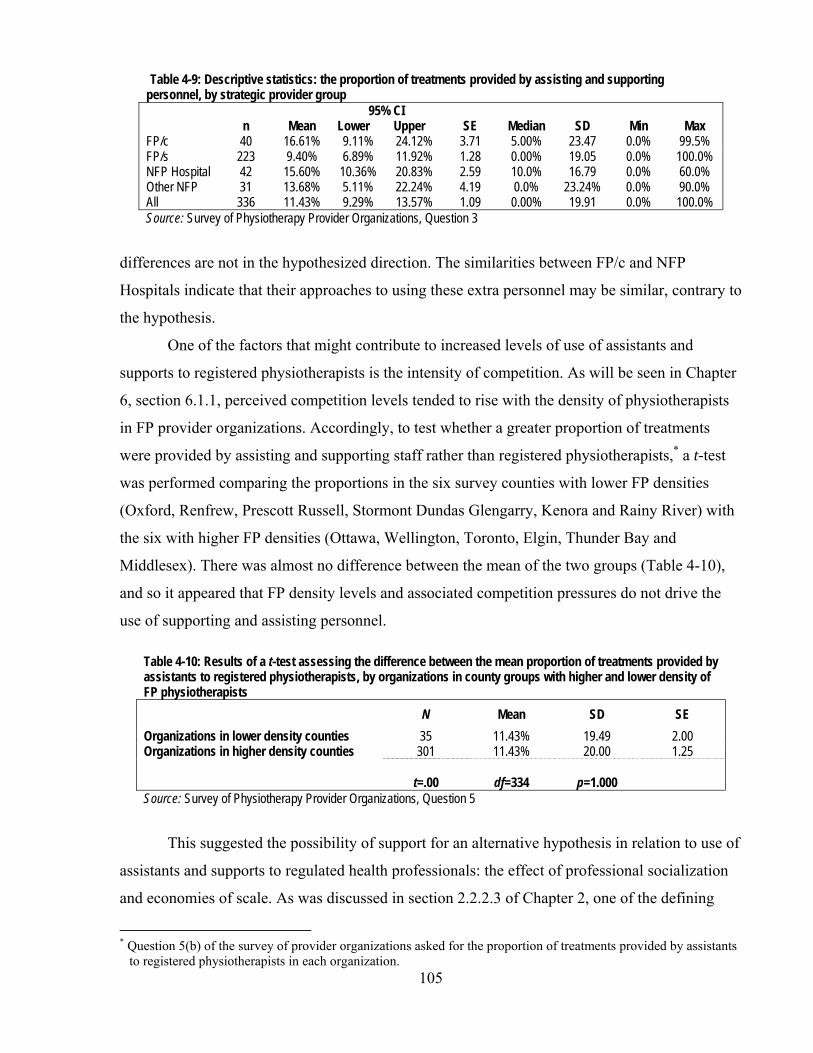

4.4.1 Practitioners ................................................................................................... 95 4.4.2 Services provided by registered physiotherapists ................................... 100 4.4.3 Supporting and assisting personnel .......................................................... 103

4.5 Registered physiotherapists ............................................................................... 106

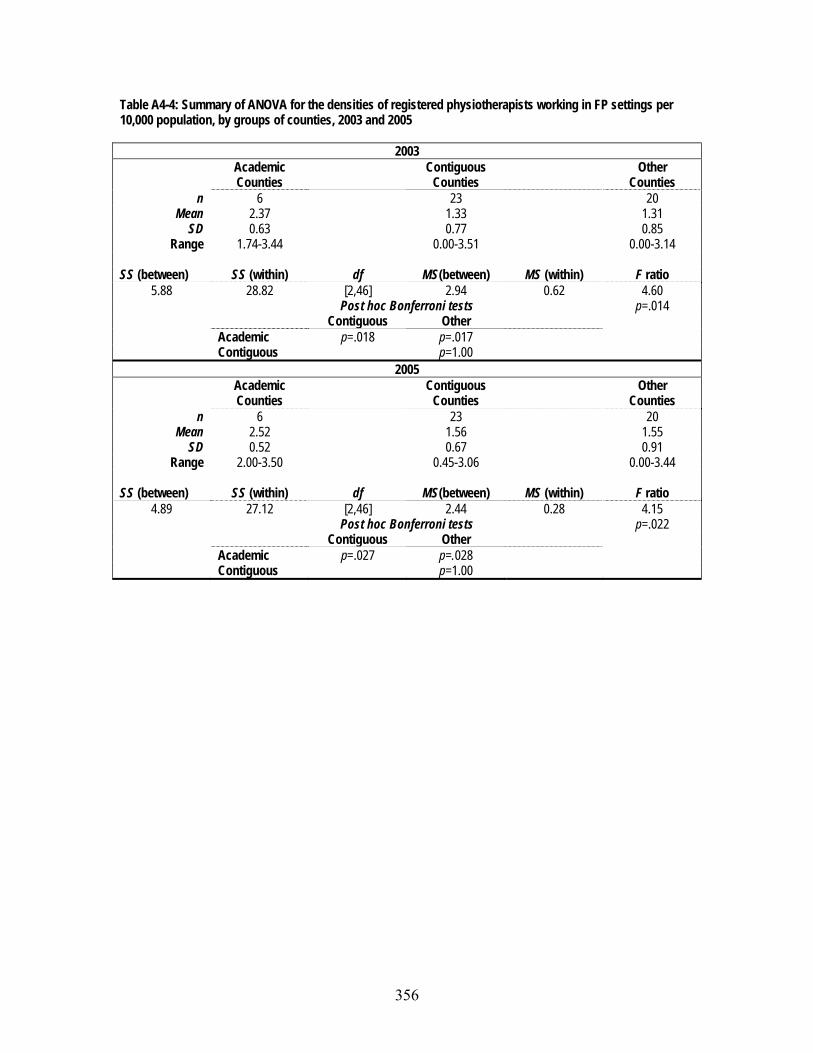

4.5.1 High demand for labour ............................................................................... 106 4.5.2 Number of registered physiotherapists ..................................................... 109 4.5.3 Geographic distribution of registered physiotherapists .......................... 110 4.5.4 Two cohorts of physiotherapists ................................................................ 117

4.6 Review of findings in this chapter ...................................................................... 119

Chapter 5 – Revenue sources, buyer power ....................................... 122

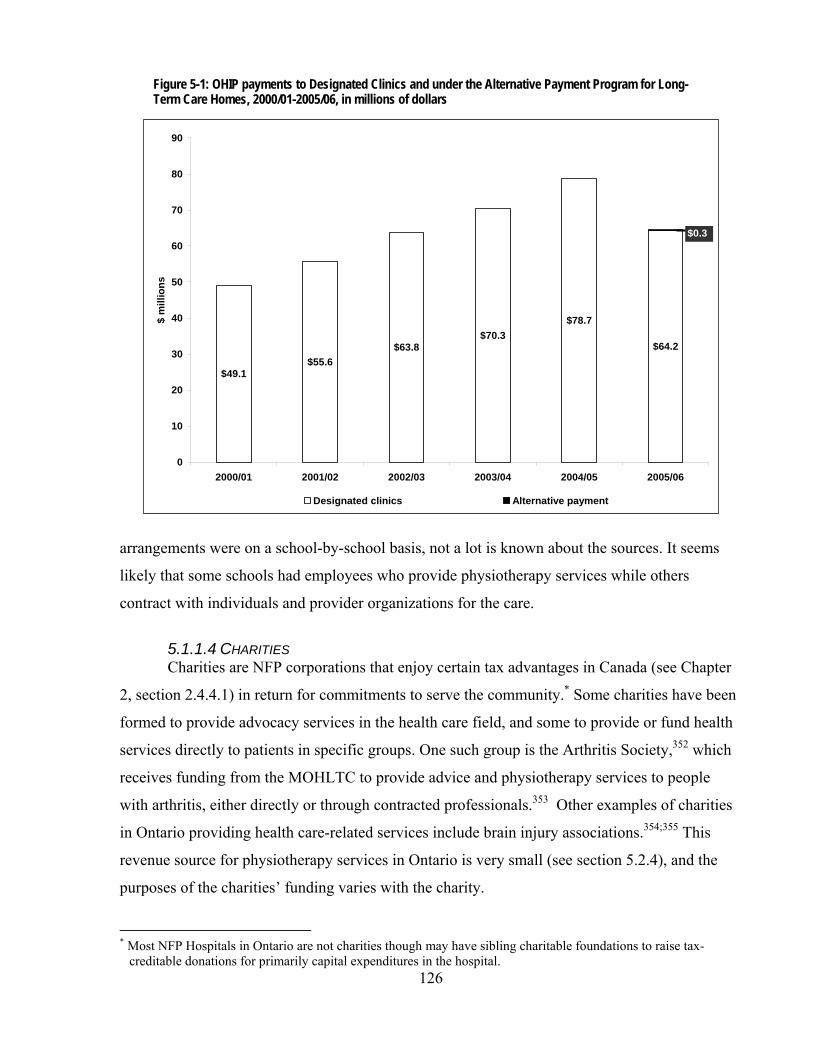

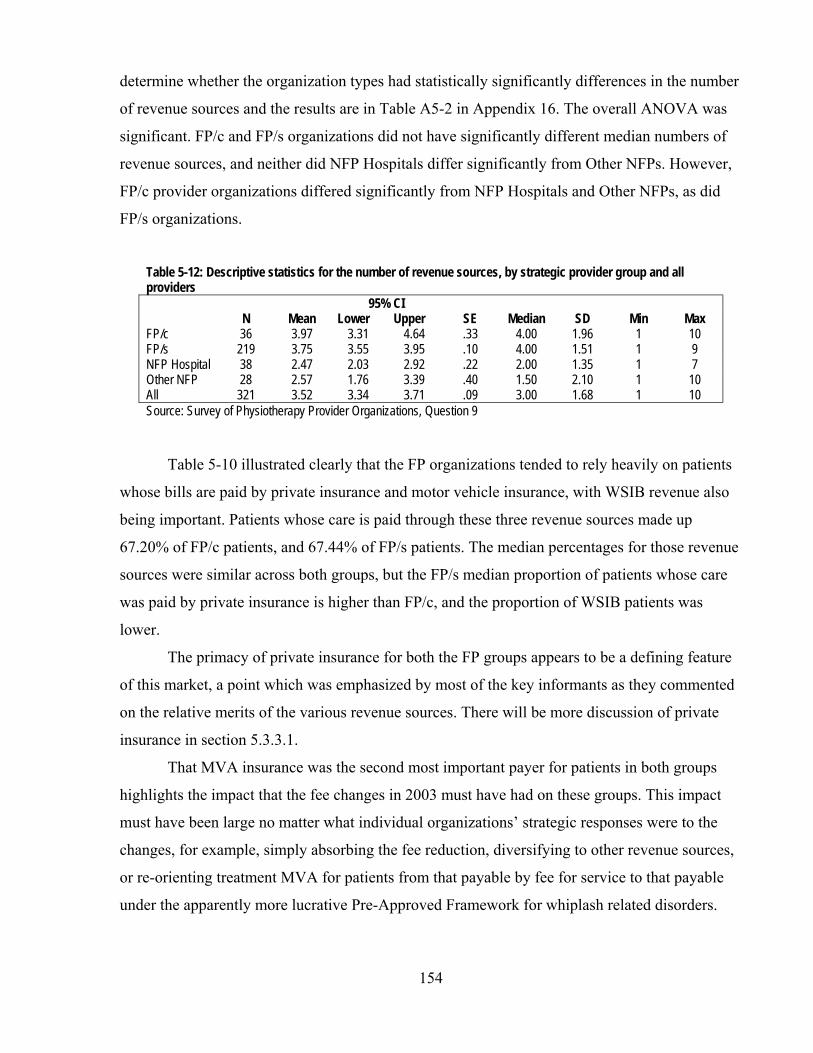

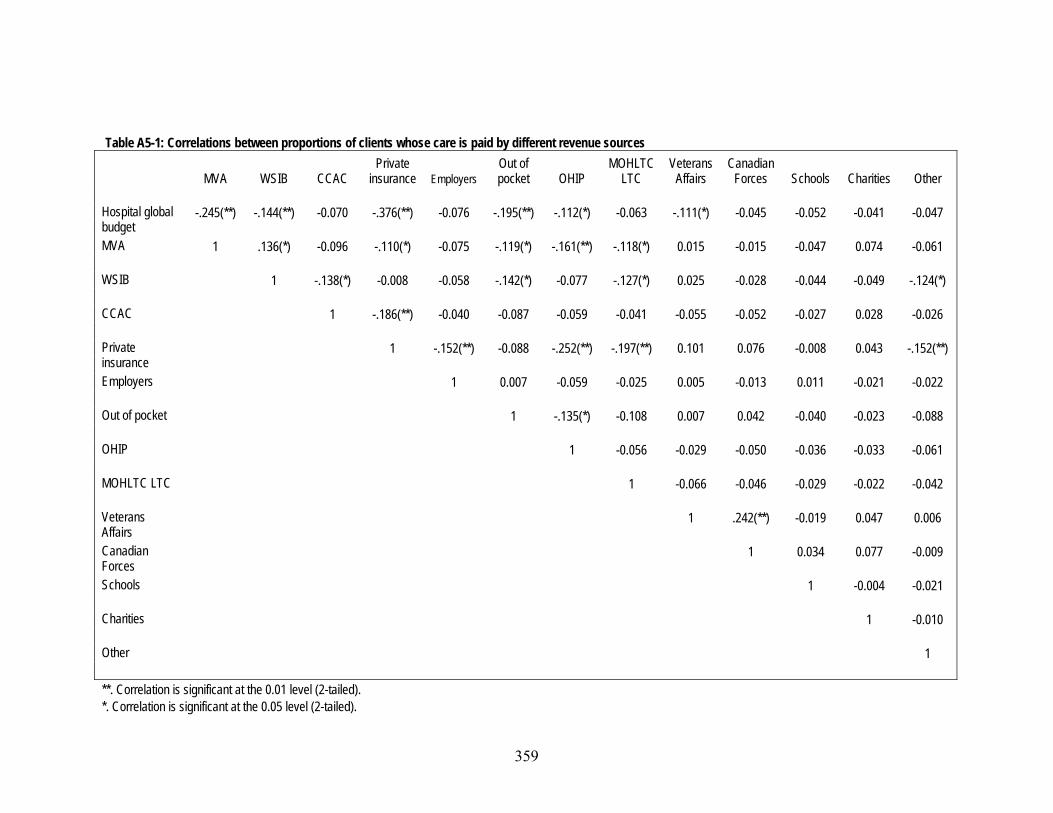

5.1 Revenue sources in the physiotherapy market ................................................. 122

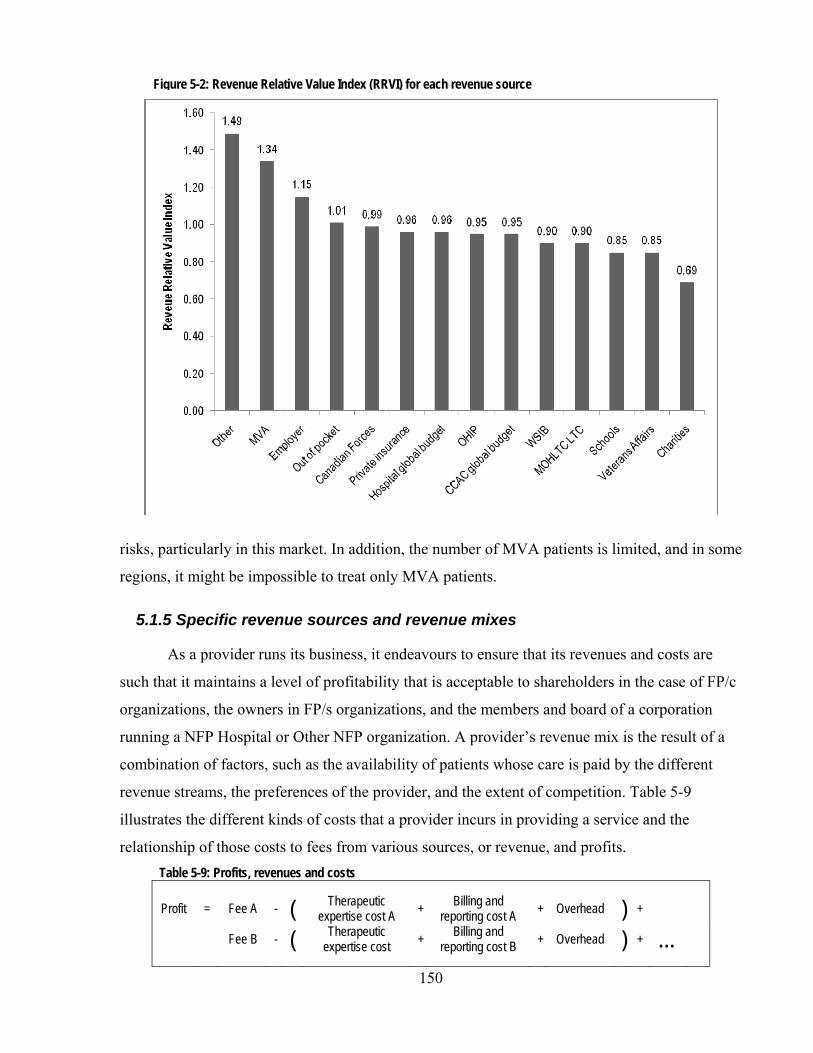

5.1.1 Revenue sources’ terms and conditions ................................................... 122 5.1.2 Complexity of the revenue sources ............................................................ 140 5.1.3 Negotiation of fees ....................................................................................... 145 5.1.4 Relative value of revenue sources .............................................................. 148 5.1.5 Specific revenue sources and revenue mixes ........................................... 150

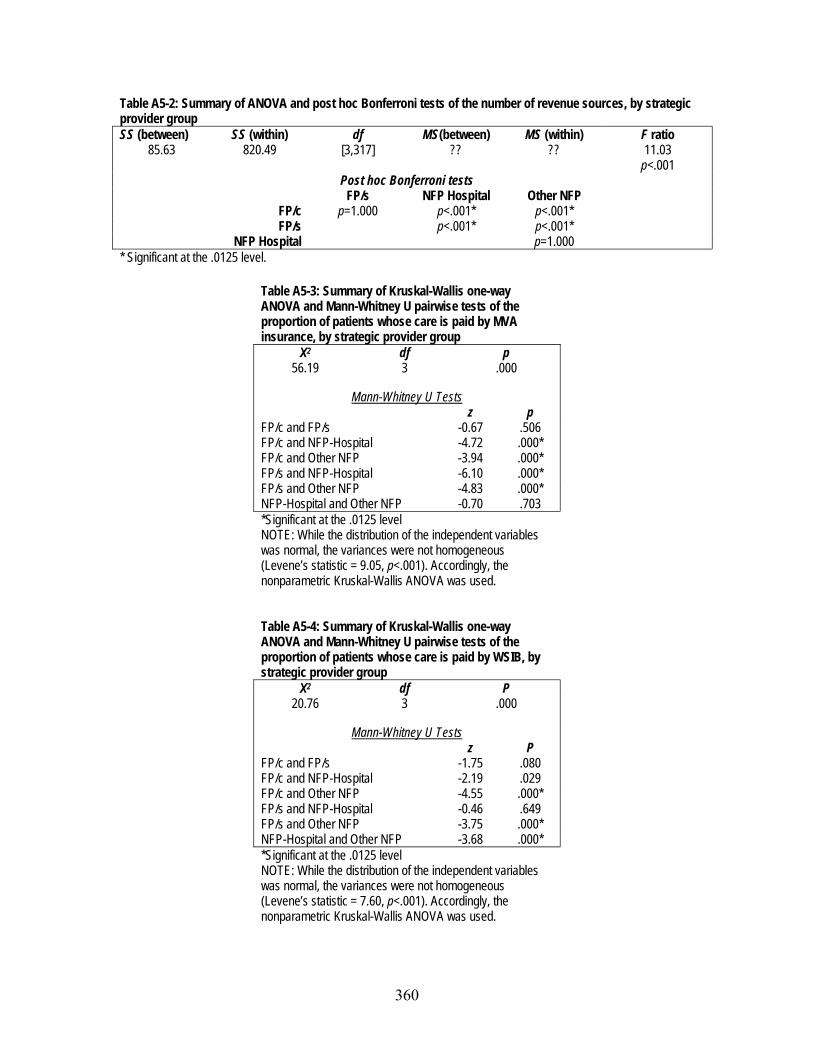

5.2 Strategic provider groups and four revenue sources ...................................... 156

5.2.1 Highest revenue fee – MVA insurance ....................................................... 156 5.2.2 Lowest revenue fee – WSIB ......................................................................... 157 5.2.3 Niches with low administrative burden ...................................................... 164

5.3 Overview of findings in this chapter .................................................................. 167

Chapter 6 – Rivalry among strategic groups of providers ................ 171

6.1 Perceptions of competition ................................................................................. 172

6.1.1 The amount of competition ......................................................................... 172 6.1.2 Competing with whom? ............................................................................... 174 6.1.3 Competition and service mix....................................................................... 178

vii

6.1.4 Competition for the supply of patients ....................................................... 179

6.2 Variety of services and patients in the market .................................................. 181

6.2.1 Variety of services ........................................................................................ 181 6.2.2 Mix of patients .............................................................................................. 185

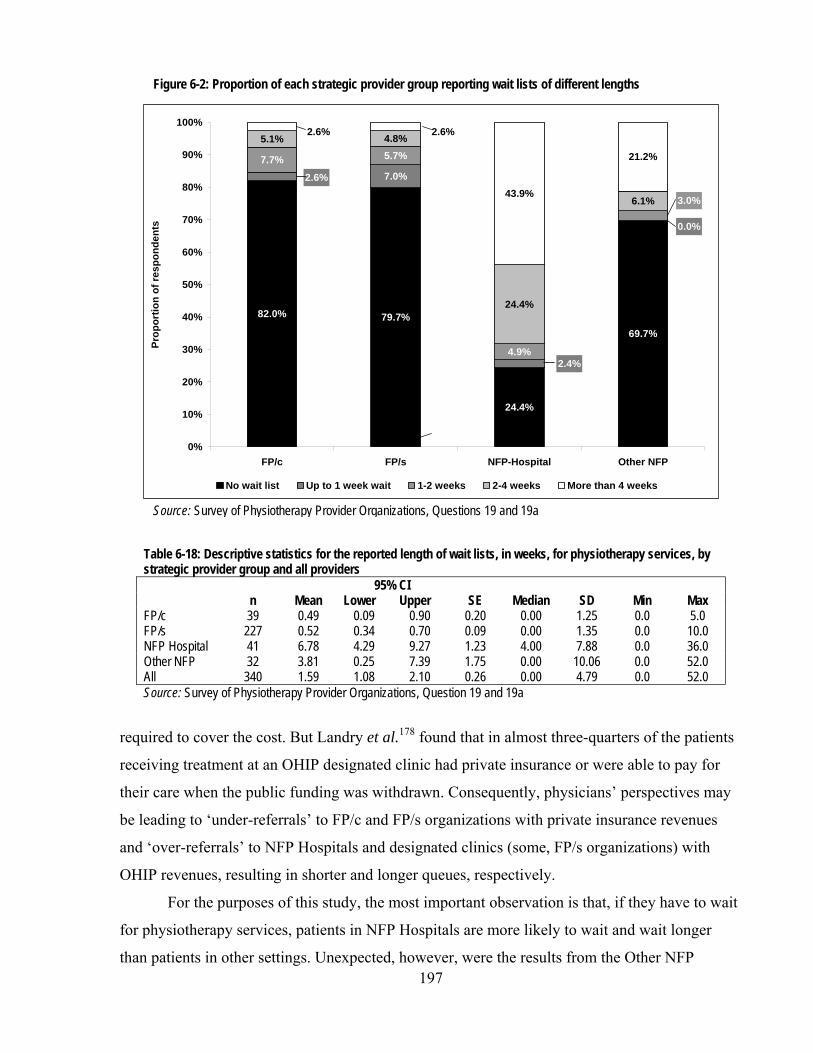

6.3 Wait lists ............................................................................................................... 196 6.4 Overview of findings in this chapter .................................................................. 199

Chapter 7 – The threat of new entrants ............................................... 202

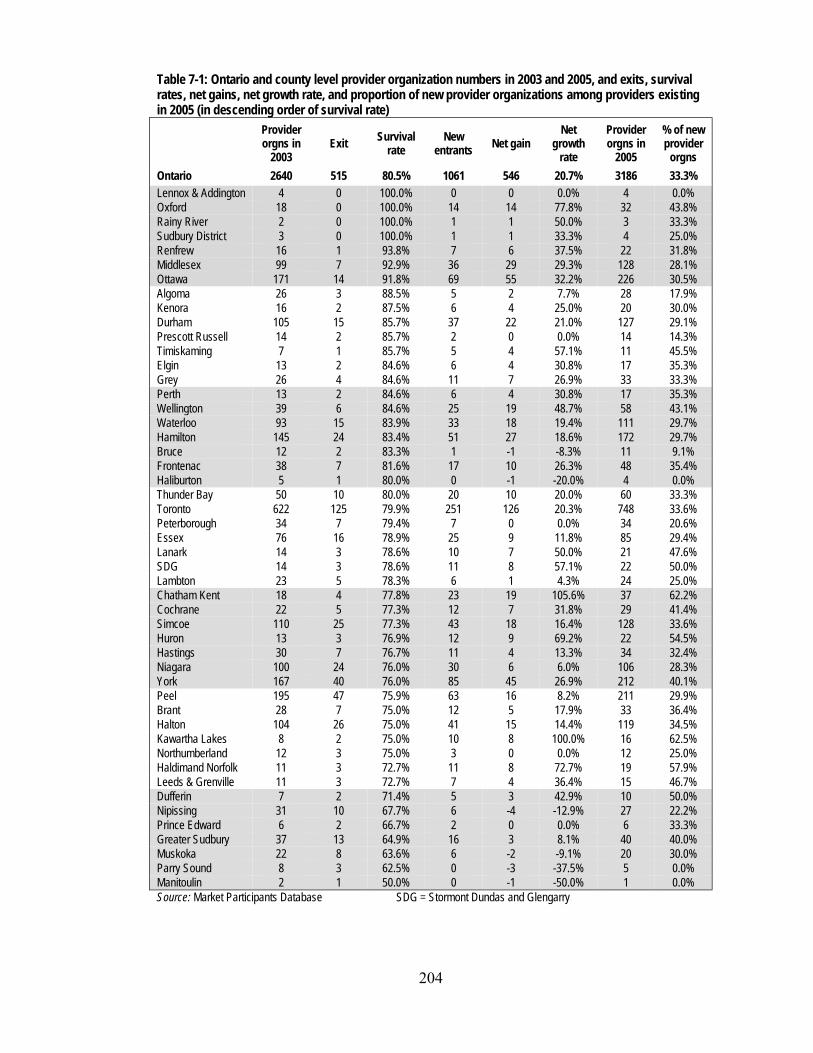

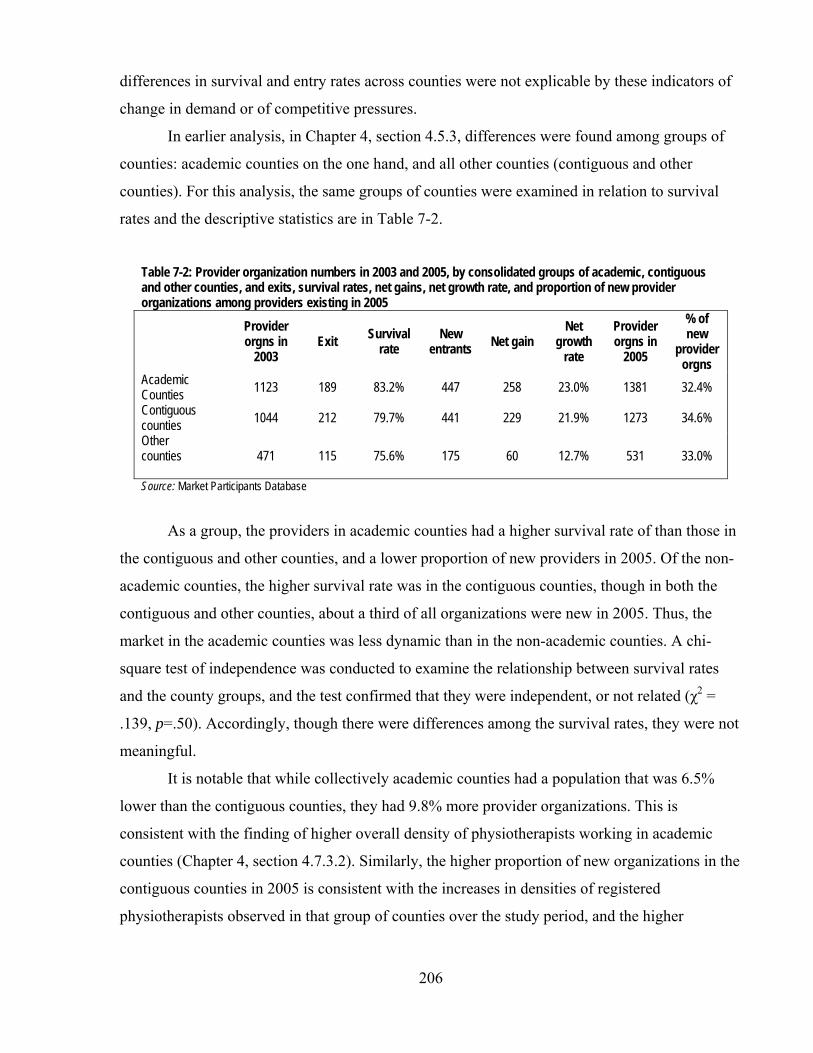

7.1 Survival in the physiotherapy market ................................................................ 202

7.1.1 Entry and survival rates ............................................................................... 203 7.1.2 Survival ......................................................................................................... 209

7.2 Foreign investment in the market ....................................................................... 214

7.2.1 Insurers ......................................................................................................... 214 7.2.2 Provider organizations ................................................................................ 217

7.3 Overview of findings in this chapter .................................................................. 225

Chapter 8 – Discussion and conclusions ........................................... 228

8.1 Review of findings ............................................................................................... 228

8.1.1 Research Question 1: Behaviour of FP and NFP provider organizations 228 8.1.2 Research Question 2: Fragmented payers and cost control .................... 231 8.1.3 Research Question 3: Labour supply and supply of patients .................. 233 8.1.4 Research Question 4: Entry, exit and survival in this market .................. 235 8.1.5 Research Question 5: Foreign investment................................................. 236 8.1.6 Key organization-level features of the market ........................................... 236 8.1.7 Market-level observations – neither planned nor ideal ............................. 241

8.2 Implications for the future of the physiotherapy market .................................. 244 8.3 Implications for Canadian health policy ............................................................ 247 8.4 Study challenges and limitations – opportunities for research ....................... 251

8.4.1 Methodological challenges.......................................................................... 251 8.4.2 Limitations and opportunities for future research .................................... 253

viii

List of acronyms and terms

Acronyms CCAC Community Care Access Centre

CPO College of Physiotherapists of Ontario. See Chapter 2, section 2.1.4.

FP For-profit. The presumed dominant motivation of a FP business is the pursuit of an excess of revenues over costs (profit) that can be distributed to owners of or investors in the business. See Chapter 2, section 2.2.2.3.

FP/c A FP/c organization is a FP business corporation that is predominantly or exclusively owned by investors other than the principal managers or employees of the business. See Chapter 2, section 2.2.2.3.

FP/s A FP/s organization is a FP business that is owned predominantly or exclusively by the principal managers or employees of the business. See Chapter 2, section 2.2.2.3.

FSCO Financial Services Commission of Ontario

IBC Insurance Bureau of Canada

MOHLTC Ontario’s Ministry of Health and Long-Term Care

MVA Motor vehicle accident

NFP Not for profit. The presumed dominant motivation of a NFP organization is something other than the pursuit of profits. See Chapter 2, section 2.2.2.3.

OHIP Ontario Health Insurance Plan

PAF Pre-Approved Framework. A protocol or guideline for treating whiplash injuries established by the Financial Services Commission of Ontario. See Chapter 5, section 5.1.1.8.

WSIB Workplace Safety and Insurance Board

Terms Access (to health care) If patients have good access to health care, they are able to receive

necessary health care.1 Access can be influenced by financial, physical, institutional and social factors.2

Acute care “Acute care includes health services provided to persons suffering from serious and sudden health conditions that require ongoing professional nursing care and observation. Examples of acute care include post-operative observation in an intensive care unit, and care and observation while waiting for emergency surgery.”3

ix

Ancillary services In this study, “ancillary services” are those services listed in the Survey of Physiotherapy Provider Organizations (see Chapter 3, section 3.2.4) that were offered by less than a third of all respondents to the survey (see Chapter 4, section 4.3).

Canada Health Act The Canada Health Act is a federal law specifying the terms and conditions that provincial public health insurance plans must meet to be eligible to receive federal funding for health. The principal terms and conditions are these: accessibility, portability, public administration, universality and comprehensiveness of the provincial plans.4

Common services In this study, “common services” are those services listed in the

Survey of Physiotherapy Provider Organizations (see Chapter 3, section 3.2.4) that were offered by more than a third of all respondents to the survey (see Chapter 4, section 4.3).

Community Care Access Community Care Access Centres (CCACs) are NFP corporations Centres established under the Community Care Access Centres Act, 2001,5

and are designated as the eligible recipients of public funding from the MOHLTC under the Long-Term Care Act, 1994.6 They provide home care services (including physiotherapy services) to people who need them. See Chapter 5, section 5.1.1.5.

Delivery “Delivery” of health care services refers to the organization, management and provision of health care services.7

Demand “Demand” is the expression of an individual’s desire to purchase something; in the health care context, this can be different from need. See Chapter 2, section 2.1.1.

Designated clinic A “designated clinic” is a health care provider organization named by the Ontario Ministry of Health and Long-Term Care as eligible to receive public funding for the provision of physiotherapy to certain patients under OHIP. See Chapter 5, section 5.1.1.2.

Economies of scale There are economies of scale for a producer of goods or services when the “amount of resource used per unit of output falls at higher output rates”.2

Entry In the analysis of provider organizations’ entry into the physiotherapy market in this study, “entry” means that an organization was not in business in 2003 but was in business in 2005. See Chapter 3, section 3.2.3.2.

Exit In the analysis of provider organizations’ exit from the physiotherapy market in this study, “exit” means that an organization was in business in 2003 but was not in business in 2005. See Chapter 3, section 3.2.3.2.

x

Fee for service A fee for service is “a method of remunerating professionals … according to an agreed fee-schedule specifying what is payable for each item of service supplied.”2

Financing “Financing” refers to “how services are paid for.”7

Foreign investment “Foreign investment” is investment in businesses in Canada by corporations or individuals that do not reside in Canada.8

Global budget A global budget is an amount of money granted to a health care provider organization to provide services to a segment of the population. Subject to any constraints imposed by the grantor, the provider organization decides how to allocate the budget among possible programs and services.

Health profession, health In this study, a “health professional” is a member of a college of a professional “health profession” as defined in, regulated under and given

occupational protection by the Ontario Regulated Health Professionals Act.9 Under that Act, the regulated health professions include physiotherapy, medicine, and nursing.

Market A market is a mechanism through which consumers (buyers) express their demand for goods and services and producers (sellers) make goods and services available. The market enables the exchange of those goods and services. See Chapter 2, section 2.1.

Medicare “Canada's national health insurance program, often referred to as "Medicare", is designed to ensure that all residents have reasonable access to medically necessary hospital and physician services, on a prepaid basis. Instead of having a single national plan, [there is] a national program that is composed of 13 interlocking provincial and territorial health insurance plans, all of which share certain common features and basic standards of coverage.”10 With public insurance, access to health care services is on the basis of an individual’s need rather than on the ability to pay.

Motor vehicle accident The risk of motor vehicle accidents is insurable in Ontario with (MVA) insurance MVA insurance, also known as automobile or auto insurance.

MVA insurance is a revenue source for physiotherapy providers in Ontario. See Chapter 5, section 5.1.1.8.

Need A person’s “need” for health care services refers to the potential

for those services to make a positive impact on that person’s health status. Generally, decisions about “need” are guided or entirely made by health professionals and practitioners. See Chapter 2, section 2.1.1.

Niche market A niche market is “a specialized but profitable corner of the market”.11

OHIP designated clinic See “designated clinic”.

xi

Ontario Health Insurance The Ontario Health Insurance Plan or OHIP is constituted under Plan Ontario’s Health Insurance Act12 to administer publicly-funded

health insurance, Medicare, in Ontario. Payer In this study, “payer” refers to one of the revenue sources (Chapter

5, section 5.1) for physiotherapy provider organizations.

Physiotherapist/ Following the Physiotherapy Act, 199113, this study uses the term Physical Therapist “physiotherapist” to describe only physiotherapists registered with

the College of Physiotherapists of Ontario, the organization given the responsibility to regulate the physiotherapy health profession. “Physical therapist” is another term reserved exclusively for the professionals regulated under the Physiotherapy Act and it is therefore interchangeable for “physiotherapist”. For consistency, however, “physiotherapist” rather than rather “physical therapist” is used in this study.

Other therapists who provide physiotherapy services but who are

not registered are labelled more generically in this study, for example, as “therapists” or “other practitioners”; where they are members of other regulatory Colleges such as chiropractors or physicians, those regulated terms are used.

Physiotherapy/ Physiotherapy is a health profession in Ontario. The practice of Physical Therapy physiotherapy is described by the Ontario Physiotherapy Act13 as

follows: The practice of physiotherapy is the assessment of physical

function and the treatment, rehabilitation and prevention of physical dysfunction, injury or pain, to develop, maintain, rehabilitate or augment function or to relieve pain.

“Physical therapy” is a term also used to describe the profession regulated under the Physiotherapy Act and it is interchangeable for “physiotherapy”. For consistency, however, “physiotherapist” rather than rather “physical therapist” is used in this study.

Practitioner A “practitioner” is “a person practicing a profession…; a person who regularly does a particular activity, esp. one requiring skill”.14 In this study, this term includes health professionals.

Private “Private” refers to activities, assets, resources or organizations that are not of a government, not public. Private organizations may be operated on a FP or NFP basis.

Private health insurance “Private health insurance” refers to insurance policies to insure specified health care services not insured publicly under Medicare. See Chapter 5, section 5.1.1.11.

xii

Program of Care One of a number of protocols for treating injuries, including soft tissue injury, established by the Workplace Safety and Insurance Board. See Chapter 5, section 5.1.1.9.

Provider “Provider” means an individual, partnership or corporation that produces health care services for patients.

Provider organization A “provider organization” is a provider’s outlet or setting for providing health care services to patients. A provider organization may be constituent part or subsidiary of a larger corporation (including a hospital corporation) that owns other provider organizations or undertakes other activities; if not a constituent part or subsidiary, it is a legal entity separate from all others.

Public “Public” refers to activities, assets, resources or organizations that are of a government, not private.

Quality (of health care) Quality of health care refers to “the extent to which care meets accepted standards.”1

Scope of practice A “scope of practice” is specified in each of the laws constituting regulatory organizations (Colleges) for health professions in Ontario, and states what services members of the profession can provide. In the case of physiotherapy, section 3 of the Physiotherapy Act, 1991,13 states as follows:

The practice of physiotherapy is the assessment of physical function and the treatment, rehabilitation and prevention of physical dysfunction, injury or pain, to develop, maintain, rehabilitate or augment function or to relieve pain.

Strategic groups “Strategic groups” refers to groups of firms or organizations in a market that use similar approaches to the market and to competition.15 See Chapter 2, section 2.2.2.1.

Strategic provider groups See “strategic groups”.

Survival In the analysis of provider organizations’ survival in the physiotherapy market in this study, “survival” means that an organization was in business in 2003 and was also in business in 2005. “Survivor” has a corresponding meaning. See Chapter 3, section 3.2.3.2.

Therapist See “physiotherapist”.

Trade treaty A trade treaty is a formal agreement binding at least two states regarding matters of trade in goods, services or both.

xiii

Workplace Safety and The Workplace Safety and Insurance Board (WSIB) is a NFP Insurance Board statutory corporation established in 1917 to provide no-fault

insurance coverage for almost 70% of Ontario workers if they are injured or contract diseases as a result of their work.16 It is the workers’ compensation authority in Ontario. See Chapter 5, section 5.1.1.9.

xiv

List of tables

Table 2-1: Possible strategies of providers with different means of integrating services ........................................... 20 Table 2-2: List of terms and conditions commonly found in health insurance policies .............................................. 37 Table 2-3: Characteristics of inputs and production in health care markets: examples of high, medium and low

contestability .............................................................................................................................................. 43 Table 3-1: Data used to answer the research questions and test the hypotheses, by chapter ....................................... 60 Table 3-2: List of stakeholders identified for the document analysis portion of this study ........................................ 61 Table 3-3: Laws, regulations and international trade treaties analyzed for this study ................................................. 62 Table 3-4: Ontario counties, by type ........................................................................................................................... 67 Table 3-5: Counties from which the pool of participants in the Survey of Physiotherapy Providers were drawn ...... 71 Table 3-6: Concordance of Porter’s five forces model with questions in the key informant Interview Guide ........... 79 Table 4-1: Revenue sources and providers in the Ontario physiotherapy market ....................................................... 89 Table 4-2: Correspondence of the four strategic provider groups identified in this study with Landry’s 9 “delivery models” ...................................................................................................................................... 88 Table 4-3: Correspondence of the 10 revenue sources used in Chapter 5 of this study with Landry’s 9 revenue “streams” ...................................................................................................................................... 90 Table 4-4: Proportions of physiotherapy provider organizations offering various services, by all providers and by

strategic provider groups ........................................................................................................................... 92 Table 4-5: Certain registered health professions with a scope of practice that can be applied to physiotherapy services ...................................................................................................................................................... 97 Table 4-6: Percentage of different services always, sometimes and never provided by registered physiotherapists

across all provider organizations ............................................................................................................. 101 Table 4-7: Ratio of number of provider organizations in each strategic provider group whose physiotherapists always provided exercise therapy to the number whose physiotherapists sometimes provided exercise therapy ....................................................................................................................................... 102 Table 4-8: Proportion of different provider organization types employing personnel supporting or assisting registered physiotherapists ........................................................................................................ 104 Table 4-9: Descriptive statistics: the proportion of treatments provided by assisting and supporting personnel, by

strategic provider group ........................................................................................................................... 105 Table 4-10: Results of a t-test assessing the difference between the mean proportion of treatments provided by assistants to registered physiotherapists, by organizations in county groups with higher and lower density of FP physiotherapists ................................................................................................................. 105 Table 4-11: Results of a t-test assessing the difference between the mean proportion of treatments provided by assistants to registered physiotherapists, by organization ownership (owned by registered physiotherapist, not owned by registered physiotherapist) ...................................................................... 106 Table 4-12: Selected employment characteristics in 2002 of 2000 graduates of Canadian bachelor degree programs in various health related educational programs ....................................................................... 107 Table 4-13: Descriptive statistics: the number of registered physiotherapists in provider organizations with at least 1, by strategic provider groups ........................................................................................................ 110 Table 4-14: Results of a t-test assessing the difference between the mean number of registered physiotherapists, by organization ownership (owned by registered physiotherapist, not owned by registered physiotherapist) ....................................................................................................................................... 110 Table 4-15: Number of all physiotherapists in direct patient care per 10,000 population (density), and by strategic provider group, by county, in 2003 and 2005, sorted by decreasing all-provider density ......... 113 Table 4-16: Population and proportion of physiotherapists in each of the academic, contiguous and other counties groups; and, mean density of physiotherapists in all provider organizations and each strategic provider group ........................................................................................................................... 114 Table 4-17: Population in 2005 and population change from 2003 to 2005 for Ontario, academic counties and the four counties with the fastest-growing population from 2003 to 2005, in order of decreasing population .............................................................................................................................. 115 Table 4-18: Proportion of survey respondents (physiotherapy organizations) in higher- and lower-population counties, by all respondents and strategic provider groups; and proportion of population in each group of counties ............................................................................................................................. 116 Table 5-1: Fees for treatment of Whiplash Injuries under a MVA policy as of June 1, 2005 ................................... 131

xv

Table 5-2: Summary of information requirements of MVA insurance health provider reporting forms: Treatment Plan (OCF-18), Pre-approved Framework Treatment Confirmation Form (OCF-23/198), and Auto Insurance Standard Invoice (OCF-21) ............................................................. 133 Table 5-3: Fees payable for the WSIB’s Program of Care for Acute Lower Back Injuries in 2005 ......................... 136 Table 5-4: Summary of information requirements of WSIB health provider reporting forms: Program of Care for Acute Low Back Injuries Initial Assessment Report and Care & Outcomes Summary form ............ 137 Table 5-5: Summary of terms and conditions of the revenue sources ....................................................................... 142 Table 5-6: Most likely practice areas in which services would be paid by the various revenue sources .................. 143 Table 5-7: Median fees received from different revenue sources, all providers ....................................................... 145 Table 5-8: Respondents’ views of adequacy of selected fees and their stated propensity to charge patients extra, in descending order of percentage of respondents who said the fee was too low .......................... 147 Table 5-9: Profits, revenues and costs ....................................................................................................................... 150 Table 5-10: Descriptive statistics for revenue sources (percentage of patients), by all providers and strategic provider groups ........................................................................................................................................ 152 Table 5-11: Revenue sources of organizations with only one revenue source .......................................................... 153 Table 5-12: Descriptive statistics for the number of revenue sources, by strategic provider group and all Providers .................................................................................................................................................. 154 Table 5-13: Proportion of provider organizations that do not treat MVA patients .................................................... 157 Table 5-14: Descriptive statistics for the proportion of patients whose care is paid for by MVA insurance, by strategic provider group and all providers ............................................................................................... 157 Table 5-15: Proportion of provider organizations that do not treat WSIB patients ................................................... 158 Table 5-16: Descriptive statistics for the proportion of patients whose care is paid for by the WSIB, by strategic provider group and all providers .............................................................................................................. 158 Table 5-17: Concordance of categories of physiotherapy providers used in the WSIB data with the strategic provider groups in this study ................................................................................................................... 159 Table 5-18: Shares of WSIB payments and patients, by provider groups, 2003 and 2004 ........................................ 160 Table 5-19: Shares of WSIB payments for different treatment types, by provider groups, 2003 and 2004 .............. 161 Table 5-20: Shares of WSIB patients for different treatment types, by provider groups, 2003 and 2004 ................. 162 Table 5-21: Proportion of WSIB-paid regular physiotherapy treatments and number of treatments per patient, by provider group, 2003 and 2004 ........................................................................................................... 163 Table 5-22: Share of WSIB payments for Program of Care, by provider groups, 2003 and 2004 ............................ 163 Table 5-23: Proportion of provider organizations that treat private insurance patients ............................................. 165 Table 5-24: Descriptive statistics for the proportion of patients whose care is paid for by private insurance, by strategic provider group and all providers ............................................................................................... 165 Table 5-25: Proportion of provider organizations that treat patients who pay for their own care ............................. 166 Table 5-26: Descriptive statistics for the proportion of patients who pay for their own care, by strategic provider group and all providers .............................................................................................................. 166 Table 6-1: Descriptive statistics for the perception of competition, on a scale of 1 to 5, from “no competition” to “a lot of competition”, by strategic provider group and all providers ................................................. 172 Table 6-2: Perceived top competitor reported by provider organizations, by strategic provider group and all Providers .................................................................................................................................................. 175 Table 6-3: Second top competitors identified by survey respondents, by top competitor ......................................... 176 Table 6-4: Responses to the survey question, “Does your Organization have the profile or range of clients it wants now? (Yes/No)”, by strategic provider group and all respondents ................................................ 178 Table 6-5: Changes to the profile or range of patients provider organizations said they would like to be serving if they were dissatisfied with their current patient profile ........................................................... 178 Table 6-6: Logistic regression results: modeling the probability of a physiotherapy organization perceiving more competition being dissatisfied with its patient profile .................................................................... 179 Table 6-7: Proportions of physiotherapy provider organizations offering various services, by all providers and by strategic provider groups .................................................................................................................... 182 Table 6-8: Descriptive statistics for the number of services offered, by strategic provider group and all providers .................................................................................................................................................. 183 Table 6-9: Mean percentage makeup of practice areas, by all providers and by strategic providers groups ............ 185

xvi

Table 6-10: Descriptive statistics of the number of provider organizations’ practice areas, by all providers and by strategic provider group ...................................................................................................................... 186 Table 6-11: Descriptive statistics for the proportion of providers’ patients with orthopaedic and musculoskeletal conditions (other than sports medicine patients), by strategic provider group and all providers ............. 188 Table 6-12: Descriptive statistics for the proportion of providers’ patients in the practice area of sports medicine, by strategic provider group and all providers .......................................................................................... 190 Table 6-13: Descriptive statistics for the proportion of prevention and health promotion patients, by strategic provider group and all providers .............................................................................................................. 192 Table 6-14: Characteristics of providers with more and less than 10% of their clients receiving prevention and health promotion services (PHPS) ........................................................................................................... 193 Table 6-15: Results of 14 t-tests comparing the mean proportion of clients whose care was paid by different revenue sources, by two groups, those with more than 10% of clients receiving prevention and health promotion services (PHPS) and those with less than 10% ............................................................ 194 Table 6-16: Descriptive statistics for the proportion of neurology/neurotrauma patients, by strategic provider group and all providers ............................................................................................................................ 194 Table 6-17: Reported length of wait lists, all respondents ......................................................................................... 196 Table 6-18: Descriptive statistics for the reported length of wait lists, in weeks, for physiotherapy services, by strategic provider group and all providers ............................................................................................... 197 Table 6-19: Providers’ stated propensity to refer patients to another provider organization in the face of a wait list, by strategic provider group ............................................................................................................... 198 Table 7-1: Ontario and county level provider organization numbers in 2003 and 2005, and exits, survival rates, net gains, net growth rate, and proportion of new provider organizations among providers existing in 2005 (in descending order of survival rate) ......................................................................................... 204 Table 7-2: Provider organization numbers in 2003 and 2005, by consolidated groups of academic, contiguous and other counties, and exits, survival rates, net gains, net growth rate, and proportion of new provider organizations among providers existing in 2005 ....................................................................... 206 Table 7-3: Mean number of registered physiotherapists per CPO organization, 2003 and 2005, and change from 2003 to 2005 ................................................................................................................................... 207 Table 7-4: Mean number of registered physiotherapists per CPO provider organization ......................................... 208 Table 7-5: Survival rates and new providers across Ontario, by all provider organizations in the Market Participant Database, and in subsets of the Database .............................................................................. 210 Table 7-6: Survival rates of provider organizations in subgroups of the Market Participants Database, compared with the survival rates of provider organizations not in the subgroups, with chi-square statistics .................................................................................................................................. 210 Table 7-7: MVA insurance companies in Ontario with more than 1% market share in 2005 (with insurance companies with common corporate ownership grouped together), by market share and by

ownership/control .................................................................................................................................... 216 Table 7-8: Responses to question about where a provider organization was based, if a corporation or a partnership ............................................................................................................................................... 218

xvii

List of figures

Figure 2-1: Forces driving industry competition (Porter’s ‘five forces model’) .......................................................... 17 Figure 3-1: Locations of the three categories of Ontario counties ............................................................................... 68 Figure 3-2: Comparison of proportion of provider organizations in each county, in the CPO list and among survey respondents .................................................................................................................................... 76 Figure 5-1: OHIP payments to Designated Clinics and under the Alternative Payment Program for Long-Term Care Homes, 2000/01-2005/06, in millions of dollars ............................................................................. 126 Figure 5-2: Revenue Relative Value Index (RRVI) for each revenue source ............................................................ 150 Figure 6-1: Proportion of survey respondents’ perceptions of competition, by strategic provider group ................. 173 Figure 6-2: Proportion of each strategic provider group reporting wait lists of different lengths ............................. 197 Figure 8-1: Competitive forces in Ontario’s physiotherapy market .......................................................................... 237

xviii

List of appendices

Appendix 1: Survey Questionnaire ........................................................................................................................... 279 Appendix 2: Survey – First Information Letter ........................................................................................................ 292 Appendix 3: Survey – Reminder Card ...................................................................................................................... 294 Appendix 4: Survey – Second Information Letter .................................................................................................... 296 Appendix 5: Survey – Codebook .............................................................................................................................. 299 Appendix 6: Key Informants Interview Guide ......................................................................................................... 312 Appendix 7: Key Informants Interviews – Information Letter and Invitation to Participate .................................... 319 Appendix 8: Survey – Original Ethics Approval ...................................................................................................... 321 Appendix 9: Survey – Protocol Amendment Approval ............................................................................................ 324 Appendix 10: Survey – First Ethics Approval Renewal ............................................................................................ 326 Appendix 11: Survey – Second Ethics Approval Renewal ....................................................................................... 328 Appendix 12: Survey – Third Ethics Approval Renewal .......................................................................................... 330 Appendix 13: Key Informants Interviews – Ethics Approval ................................................................................... 332 Appendix 14: Key Informants Interviews – Consent Form ....................................................................................... 334 Appendix 15: Forms for Completion by Physiotherapy Provider Organizations and Others .................................... 336 Appendix 16: Details of the Results of Specific Statistical Texts ............................................................................. 353

1

Chapter 1 – Introduction and overview

1.1 Statement of the issues

This is a study of several contentious and important issues in Canadian health policy. The

issues, all involving the operation of health care markets, include (1) the impact of the interaction

of public and private payers and for-profit (FP) and not-for-profit (NFP) providers; (2) the

influence of health care professionals on the structure of a market and on the activities of

provider organizations in that market; (3) the factors influencing provider organizations’ entry

into, survival in and exit from health care markets; and, (4) the role of foreign investors in

Canadian health care.

There is little room or opportunity for direct investigation of these issues, particularly on

a comparative basis, when looking at the dominant health care sub-sectors – hospitals and

physicians – in Canadian health care. Medicare, now embodied in the Canada Health Act,17 was

an innovation of the 1950s, 1960s and 1970s in the method of financing of health care provided

by these sub-sectors, and in securing universal access for Canadians to these kinds of health care

services. Several of the issues mentioned above appear to have been settled within Medicare in

the early years of innovation, either explicitly or passively, though there is continuing interest in

the policy choices that have been made over the years. For example, the question of whether

public and private payers should co-exist was resolved in favour of a single public payer in each

province for hospital and physician services, but the question about the usefulness of adding

payers, including private payers, continues to be raised.

Citizens, policy makers, and researchers who search for evidence-based policy options

for modifications to the health care system commonly look to jurisdictions outside Canada and

their experience with issues like private financing, for-profit delivery of health care, alternative

approaches to health human resources supply, and the role of corporate investors in the provision

of health care services. Of course, Canada’s proximity to the United States means that the

American health care system is examined often but some look to European and Australian

models.18-22 Regarding foreign investment questions, researchers look to other sectors of the

economy, notably to manufacturing. Some of the debate that results from these investigations of

foreign or “international” health care systems or other sectors is about the generalizability of the

findings to the Canadian health care sphere: can the Dutch experience with private health

insurance, for example, be used to understand how private health insurance would work in and

affect the Canadian health care system23 or can findings about the effect of parallel private health

2

insurance schemes on wait times in a publicly-funded system in England and New Zealand24 be

applied in Canada?

This study takes a different approach to studying these issues. Instead of examining

foreign models and experiences, or the experience in manufacturing, this study examines in

considerable detail a Canadian health care market that has many of the attributes of interest in

Canadian health care policy and research: the Ontario physiotherapy market in the period 2003 to

2005.

This market has a broad mix of private and public payers, some regulated heavily, some

not. It has a mix of NFP provider organizations and FP provider organizations, both small

businesses and investor-owned corporations. At its core are self-regulated health professionals –

physiotherapists – with protection of occupational title but not of scope of practice.

Consequently, there are other health professionals and some unregulated practitioners in this

market. Also, in many respects the market is open to foreign investment in that there are no

market-wide protections in international trade treaties for domestic providers.

The physiotherapy market and the buyers and sellers in it have experienced a number of

interesting policy changes in the last ten years, and the effects of most of these changes had been

in place by the study period 2003-2005. For example, in the 1990s there were significant changes

in the pattern of buying services in two important sectors, motor vehicle accident (MVA)

insurance and workers’ compensation. In the study period, however, there were also abrupt

reductions of fees without the input of providers and the introduction of proposals for new

regulations for more overlapping and potentially substitute professional groups. Also, the market

was and continues to be working within a context of an aging population, which brings signs that

the demand for services from this market will increase.

Physiotherapy services and services related to physiotherapy are of course bought and

sold in this market. Ontario’s Physiotherapy Act13 defines “physiotherapy” as follows:

The practice of physiotherapy is the assessment of physical function and the treatment, rehabilitation and prevention of physical dysfunction, injury or pain, to develop, maintain, rehabilitate or augment function or to relieve pain.

The Ontario Physiotherapy Association,25 the association for physiotherapists in Ontario

describes the scope and value of physiotherapy services more expansively, though consistent

1with its members’ interests, it only refers to “physiotherapists” as providing these services and

not others:

3

Physiotherapy is a drug-free health care practice. Physiotherapists work in partnership with individuals of all ages to break down the barriers to physical function whether that means working with patients pre and post surgery, helping people come back from illness and chronic disease, injury, industrial and motor vehicle accidents and age related conditions. Physiotherapists also play an important role in health promotion and disease prevention.

Physiotherapy can play a role before a patient receives acute care services (such as surgery) as

well as after patients have passed through an acute phase of their disability, whether they have

received other health care services or not during an acute phase. Physiotherapy services can also

be used by individuals who want to avoid injury and disability by maintaining their health status

and physical functioning. Thus, the physiotherapy market is not an isolated niche market;

instead, it touches on a great many areas of the whole health care system.

This study takes this interesting market and examines it from several perspectives to look

at the issues mentioned – public and private financing; FP and NFP delivery of health services;

the influence of health professionals; entry, exit and survival patterns of health care provider

organizations; and, foreign investment. An introduction to each of these issues follows, with the

specific research questions that are addressed in this study.

1.1.1 Public & private financing and FP & NFP delivery of health care

A significant part of the national debate over health care in Canada continues to be

whether private FP delivery of health care is to be avoided or encouraged. Most hospital services

are delivered by NFP organizations (either public or private) and most physician services in

Canada are delivered through private FP organizations, practices owned by physicians. However,

faced with financial pressures exerted by public payers and with changes in technology and

preferences for community- rather than hospital-based delivery of some health services, NFP

hospitals have shed, or ‘passively privatized’, services 21;26-28and where possible, FP providers

are picking up the business. Many in Canada hoped that the Report of the Commission on the

Future of Health Care in Canada18 (the ‘Romanow Report’) in 2002 would settle the issues of

privatization and “profitization”29 in Canadian health care since it weighed heavily in support of

continued and increased NFP delivery of services traditionally covered by Medicare for reasons

of potential superior capacity for cost containment, quality and equitable access. However,

advocates for increased involvement of the private FP providers continue to raise the issues,

pressing for expansion of FP services, arguing that they can provide cost advantages and more

efficient and more innovative delivery.30-32 Advocates of private insurance argue that more

4

private financing options can increase consumer choice, access and efficiency of the health care

system.32-34

In Ontario’s physiotherapy market, there is a rich mix of FP and NFP providers, and this

study tests a number of theories about behaviours of FP and NFP providers – for example, how

they position themselves in the market and how they respond to financial incentives. The study

specifically answers the following research question:

Research Question 1: Do provider organizations supply health care services

differently depending on their FP and NFP status and their corporate form?

With respect to financing or payment for health care services, a commonly identified

strength of the Medicare program in Canada is the single public payer in each provincial

jurisdiction (mandated by the Canada Health Act4) with the power to influence substantially the

terms and conditions of the delivery of care and, particularly, costs.18;35 Advocates of increased

involvement of private insurers of course would like to move beyond the single public payer, and

they stress positive aspects of multiple payers, including patient choice and beneficial effects of

competition.30-32 As will be seen, 11 different types of payers in the Ontario physiotherapy

market are identified in this study, including both private and public insurers. This market

therefore allows a look at the role that the various payers have as they buy services, and how

they affect the kind and range of services that are made available to patients. The study answers

this research question:

Research Question 2: Are public and private payers in a health care market similar

or different in their approach to and relationship with providers, and what effect do

they have on the supply of services in a health care market?

1.1.2 The role of health professionals

Physicians have been the subject of much study in the literature, and many of the theories

of health professional behaviour are based on this traditionally powerful profession. The

physiotherapy market depends heavily on the regulated physiotherapy profession, but the

profession in Ontario has a short regulatory history, having had a regulatory regime like

physicians’ (which dates from 186936) only since 1991.13 In addition, the occupational protection

that physiotherapists have is of their title only: other practitioners cannot legally call themselves

“physiotherapists.” However, the range and scope of the services physiotherapists offer in the

5

health care market can be offered by a number of other regulated and unregulated practitioners.

The effect of this less restrictive scheme of professional regulation is examined in this study, in

circumstances of a relatively constrained supply of physiotherapists.

Though the regulatory scheme permits patients’ direct access to physiotherapists,

historical patterns of referrals from physicians to physiotherapists (reflecting patterns established

before regulation)36 and the common place of physiotherapy services within a continuum of care,

mean that providers rely heavily on relationships with other health professionals and health care

institutions for business. The effect of this practical integration of patient supply across

professional groups without, as will be seen, the financial supports for clinical integration is

interesting and will be shown to have important effects on the structure of the market.

Research Question 3: What role do the supply of labour and the pattern of supply of

patients to health care providers have in the structure of the provider organizations

in a health care market?

1.1.3 Investment in a health care market

The factors that have influenced entry and exit in the physician part of Medicare markets

are generally assumed to be relatively personal and professional. In addition to the numbers of

medical students graduating from Canadian medical schools, factors include physicians’

preferences for practice style, the place of their education, their gender and age, their ability to

move to other jurisdictions (including the United States where, for some physicians, overall

market conditions are perceived as better than in Canada), and the availability of bonus payments

for practice in areas perceived by physicians to be less desirable.37;38 For hospitals,

predominantly NFP in Canada, there is less influence of market factors than governmental and

policy factors. Investments in new hospitals are organized by provincial governments (even if

some of the capital comes from sources other than taxes) and entry and exit of hospitals has been

decided by government policy and legislation.39;40 Overall, and despite the pressures commonly

perceived in these markets, researchers have remarked on substantial stability in these markets

due to the underlying societal and institutional power physicians and hospitals have enjoyed in

Canada before and after Medicare was introduced.41

The factors motivating entry and exit of provider organizations from Canadian health

care markets in which there is a greater influence of market forces and competition are not

widely known but it could be assumed that, as participants in the market drive toward greater

6

market share and economies of scale, there would be a trend toward fewer, larger corporations

owning chains of health care provider organizations.42 Potentially, such chains could, as in the

United States, be purchased by or enter into arrangements with organizations like Wal-Mart

Stores Inc. to offer services in multiple locations in a retail rather than health care setting,43;44

dramatically changing the nature of the health care delivered.45 This study uncovers patterns of

entry, exit and survival in the physiotherapy market and some of the factors influencing these

phenomena, in response to the following research question:

Research Question 4: What characterizes the organizations that survive in a

contestable health care market and those that exit and enter?

Another significant debate that has arisen since negotiations over the North American

Free Trade Agreement (NAFTA)46 in the late 1980s and early 1990s is about special protections

from foreign competition for Canadian health care providers. Under NAFTA, there are no

specific exceptions for domestic health care providers, though there are general provisions

governing governmental programs and programs with a social purpose. The General Agreement

on Trade in Services (GATS),47 in effect from 1995, specifically allows foreign competition in

health insurance other than for services covered by Medicare – medically necessary physician

and hospital services. Some commentators argue persuasively that the Canadian hospital and

physician markets are not open to foreign investors under the NAFTA or the GATS because they

are parts of governmental financing programs and are not open to commercial activity.48;49

However, if these markets – or indeed, other health care markets – were open to commercial

activity, there is concern about the potential for the application of the trade rules to

fundamentally change the makeup of these markets. Some fear that global firms, given the

opportunity, would penetrate the Canadian market and overwhelm smaller Canadian firms,

using, where available, cross-border economies of scale and expertise in competitive health care

markets.

Discovering the degree to which the Ontario physiotherapy market is fundamentally

globalized – that is, whether foreign insurers and providers participate in the market – is one of

the goals of this study. The fifth research question poses the issue in the following manner:

Research Question 5: Is there a significant presence of foreign investors or foreign

corporate providers in health care markets? What mechanisms help produce this

pattern?

7

1.2 Organization of the report

Because of the wide range and large number of market issues raised by the research

questions, a framework for a systematic review of the physiotherapy market was necessary.

Michael Porter’s generic model of the five ‘forces” that structure a market15 has been adapted for

this purpose. The five forces are: the relationships among existing sellers (providers) in a market,

the power of buyers, the power of suppliers, the potential threat of new entrants to a market, and

the role of substitute products and services. The discussion of these five forces provides a

structure for the chapters and the discussion of the issues in this study.

Chapter 2 clarifies some basic features of markets in general and how health care markets

differ from other markets. The chapter then amplifies the theory, the literature and other sources

briefly mentioned in this introductory chapter to illuminate the five formal research questions

and to provide the basis for the hypotheses tested in this study. Chapter 3 discusses the study

design, as well as further explanation of the use of the physiotherapy market as a case study to

explore the research questions. Chapter 3 also outlines the methods and data used in the study.

The fourth chapter provides more general contextual information about the physiotherapy

market, including assessments of the need for physiotherapy services and a description of the

major groups of providers (organized by their FP or NFP status and corporate form) and payers

(or buyers). There is also a discussion of the variety of services that are bought and sold in the

market. Chapter 4 also reviews the labour supply that is able to participate in the market, the

services provided by registered (or regulated) physiotherapists and by others, as well as the

numbers and distributions of physiotherapists across Ontario.

Chapter 5 contains a discussion of the revenue sources or buyers in the market, covering

first the terms and conditions that govern the payments made by 11 different revenue sources.

The chapter then turns to a discussion of the relationships between specific revenue sources and

different groups of providers.

The sixth chapter discusses the perceptions of provider organizations in the market about

competition generally among themselves and with others, and about competition for the supply

of patients. There is also a comparative analysis of the kinds of services different provider groups

offer in the market, the mix of patients that each serves, and the issue of wait lists for service.

Chapter 7 discusses the issues of entry into and exit from the market by providers, and

characteristics of provider organizations that may influence their ability to survive in the

8

physiotherapy market. It also deals with the question of the extent of foreign investment and

ownership in both the buyer and provider sides of the market.

The final Chapter, 8, provides a summary of the findings in the study and the answers to

the research questions. It also provides reflections on the future of the physiotherapy market in

light of the findings and implications for other health care markets. Because of the novel

approach taken in this study – the examination of a complex Canadian health care market with

multiple payers and providers – there is also a reflection on some of the methodological issues

that arose during the study, the study’s limitations, and opportunities for future research.

9

Chapter 2 – The structure of health care markets

This chapter deals with the literature and theory that frame the research study and put it in

context. To provide a foundation for the examination of the research questions, section 2.1

reviews essential features of ideal markets and two dimensions on which health care markets are

generally said to diverge significantly from the ideal: uncertainty of demand for health care and

asymmetry of information between providers and patients.

In section 2.2, the general features of health care markets (including the two divergent

dimensions) are integrated into a generic model for analyzing a market, Porter’s15 ‘five forces

model.’ The Porter model provides a way to assess providers’ performance and sustainability in

a market. The five forces in the model are:

• Rivalry among existing sellers

• Buyer power

• Supplier power

• Threat of new entrants

• Threat of substitutes

Section 2.3 reviews the theory and literature pertaining to each of these forces in turn.

The fleshed-out model of a health care market provides the structure to generate

hypotheses in relation to the research questions. These hypotheses follow the review of the

literature that gives rise to each, and at the end of this chapter, in section 2.4, the hypotheses are

presented together.

2.1 Ideal markets and health care markets

A market is a mechanism through which consumers (buyers) express their demand for

goods and services and producers (sellers) make goods and services available. The market

enables the exchange of those goods and services, and one of the key pieces of information that

enables the exchange is price. From the sellers’ perspective, there is a range (or “vector” in the

terminology of economists) of minimum prices that they must receive to produce different

quantities of the good or services; there is also a vector of maximum prices that sellers are

willing to pay for different quantities of those goods or services. Where the two vectors intersect,

there is neither excess demand nor excess supply and the market is said to have cleared.50

10

Ideal markets are information-rich arenas in which buyers seek sellers with specific

products or services at a price acceptable to them. Buyers participate in the market with a level of

certainty about the nature of sellers and about the products and services those sellers can supply.

In an ideal market, there are enough buyers and sellers so that none, individually or collectively,

can influence the market as a whole. The sellers compete to supply goods and services at prices

that satisfy buyers’ demands. High-price sellers reduce their prices to meet their competitors’ or

differentiate their goods and services.

While all the ideal characteristics for markets to clear rarely co-exist in actual markets,

many markets are assumed to have them in some measure, moving toward a state of equilibrium

in which competition among sellers induces cost- and price-cutting or differentiation on quality,

and in which buyers’ demands are satisfied. Sources of innovation, including technological

innovation and new kinds of demands from buyers, can upset the path to equilibrium. Sellers and

buyers make adjustments in reaction to these disturbances and eventually the market moves

toward equilibrium again. Some markets, however, may remain out of equilibrium for long

periods of time.

There is a general consensus in the literature42;50-52 that health care markets have certain

features that mean they are not ideal markets. Two of these features are uncertainty of demand

for health care (which gives rise to a demand for insurance) and asymmetry of information

between health care providers and patients. Drawing on several sources,42;50-52 these features are

reviewed in the next section, along with common responses from the market and from

governments.

2.1.1 Uncertainty of demand

Generally, there is more uncertainty about purchasing health care than about purchasing

other goods and services. People do not usually plan to consume health care as they might plan

to purchase consumer goods because illness occurs relatively randomly: people do not generally

know when they may become ill and need health services, except perhaps for regular checkups

and preventative care. Furthermore, with health care, there is a difference between “need” and

“demand” though both are commonly cited as the appropriate information on which to make

societal resource allocations.42 “Need” refers to the potential for health care to make a positive

impact on a person’s health status and generally, consumers’ decisions about “need” are guided

or entirely made by health service providers. “Demand,” on the other hand, is the expression of

an individual’s desire to purchase something. Unlike ordinary consumer goods, it is thought that

11

people ought not to consume health services that they do not need, and prices for health services

ought not to be at such a level that individuals who need them cannot get them.53

The unknowns and uncertainties, and the differences between demand and need, mean

that health care markets are not ideal for patients to gather information and make rational choices

about what health services they could benefit from. In light of the uncertainties, people often turn

to insurance, the role of which is discussed in section 2.1.3.

2.1.2 Asymmetry of information

In an ideal market, consumers are able to obtain information about options so that they

can satisfy their own interests and preferences, and can decide whether to allocate their resources

to one good or service rather than another. Patients are generally not interested so much in

buying health care as they are in being healthy or becoming healthier, and they are unsure about

the way their health status may be enhanced by the consumption or use of health services.42;51

Even where information is available, providers and not patients are in control of many of the

consumption decisions since health practitioners usually have much more knowledge about the

technical aspects of care than patients. Providers interpret a patient’s symptoms into a diagnosis

and then, drawing from their training and experience, they prescribe and often implement what

they see as the measures that constitute the care that is “needed” by a patient or that is

“necessary”.

The imbalance of information between the patient and the health practitioner is called

‘asymmetry of information’, and in these circumstances, the health practitioner acts as the agent

of the patient (the principal). Agency theory says that as long as their respective interests and

their tolerance for risk and cost are the same, the agent will act as the principal would act if he or

she knew what the agent knows. However, the interests and risk tolerance may not align, and if

they do not, there will be conflict.54 “Conflict of interest” situations are an example: when

providers refer patients to themselves or to other organizations in which they have a pecuniary

interest,55 the providers’ interest may eclipse the patients’. There may also be instances when the

health care services that are defined by providers as “needed” are in fact detrimental to a

person’s health or have a negligible positive effect. Furthermore, health practitioners act as

“gatekeepers” for many services – patients cannot purchase most surgical procedures or

prescription drugs, for example, unless practitioners authorize them.

Some researchers argue that technological advances, including the Internet, will make