behavioral finance – fss 2013 - weber.bwl.uni … filebehavioral finance – fss 2013 basic ......

TRANSCRIPT

Behavioral Finance – FSS 2013Basic Concepts of Decision Theory

1Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Course Information

• Exercise Course Behavioral Finance:• Exercise Course Behavioral Finance:- Wednesday, 12:00 - 13:30 (B3), SN 169- Overall 8 sessions- Session 1 - 3: Christian Ehm- Session 4 - 7: Ulrich Seubert- Session 8: Your questions

Christian EhmOffi h b i t t i L5 2 (R 006)Office hours: by appointment in L5, 2 (Room 006)

+49 621 181 1539

2Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Course Information

D t E i C B h i l Fi• Dates Exercise Course Behavioral Finance:

- Exercise course 1: 27.02.2013 Introduction to Behavioral

- Exercise course 2: 06.03.2013

Finance: Basic Concepts of Decision Theory

- Exercise course 3: 13.03.2013

or 20 03 2013

Individual investorbehavior

or 20.03.2013

Easter Break Linking individual behavior

- Exercise courses 4-7: tbdand market outcomes,Markets, event studies, and return anomalies

- Exercise course 8: tbd Q&A session (if desired)

3Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

(exam date: 08.06.2013)

Course Information

Slides will be available in advance http://bank bwl uni-mannheim dehttp://bank.bwl.uni-mannheim.de (direct link: http://weber.bwl.uni-

mannheim.de/de/lehre/diplom und master msc/fin 620 bemannheim.de/de/lehre/diplom_und_master_msc/fin_620_behavioral_finance/exercise_course_fss_2013/)

Check the homepage also for changes in schedule / updatesCheck the homepage also for changes in schedule / updates

Downloads require authorizationo oads equ e aut o at o Login: bankFSS13 Password: campbell2006p

4Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive versus Descriptive Decision Theory

Basics of Prescriptive Decision Theory (Chapter 7, 9 - 11) and

Descriptive Decision Theory (Chapter 13)

5Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive versus Descriptive Decision Theory

Neoclassicism:Neoclassicism:• Homo economicus acts to obtain the highest possible well-being for himself.

He is seen as "rational" in the sense that well-being as defined by the utility function is optimized given perceived opportunities.

• Assumption that people behave like economistsOptimization problem under constraints• Optimization problem under constraints

Behavioral Finance:Behavioral Finance:• People often make decisions based on approximate rules of thumb, not

strictly rational analyses, they do not act like the ideal homo economicus y y , y• Behavioral finance applies scientific research on human and social

cognitive and emotional biases to better understand economic decisions

6Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive versus Descriptive Decision Theory

Prescriptive TheoryPrescriptive Theory

EUTEfficient capital markets

Portfolio Theory

CAPM

D i ti Th

CAPMBayesian Updating

Descriptive Theory

Naive Diversification Myopic Loss AversionBehavioralFinance

Prospect TheoryFinance

Judgement Biases

7Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Concept:

Prescriptive Decision Theory: Expected Utility Theory (EUT)

Concept:Through a so-called “utility function” every consequence is assigned a utility value and the

• Daniel BernoulliJohn von Neumannconsequence is assigned a utility value and the

expected utility (EU) of different alternatives is calculated. The higher the expected utility of an lt ti i th t thi lt ti i f d

• John von Neumann• Oskar Morgenstern

alternative is the stronger this alternative is preferred.

)()EU(n

).a(up)aEU( i1i

i

Th EUT i b d iThe EUT is based on axioms:

• complete orderp• continuity• independence

EUT

8Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Axioms of EUT:

Prescriptive Decision Theory: Axioms of Expected Utility Theory (EUT)

Complete OrderingComplete Ordering• Completeness: f.a. a, b it holds: a b or b a• Transitivity: from a b and b c follows a c

Continuityif a b c then there exists some probability pif a b c, then there exists some probability psuch that: b ~ p · a + (1 – p) · c

Independenceif a b, it must hold for each lottery c and probability p:

p a + (1 p) c p b + (1 p) cp · a + (1 – p) · c p · b + (1 – p) · c.

9Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Utility u(x) of Example :

Expected Utility Theory (EUT)

y ( )Outcome xOutcome xExample :

1.020% very exciting

M i A Th H bbit

0.380% moderate

EU( ) 20%*1 0 80%*0 3 0 44Movie A: The Hobbit

1 050% very exciting

EU(a)= 20%*1.0+80%*0.3=0.44

1.0

0 0

50%

50%

very exciting

horrible

Movie B: Django Unchained

0.0horrible

EU(b)= 50%*1.0+50%*0.0=0.50

10Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive Decision Theory: Portfolio Theory and CAPMPrescriptive Decision Theory: Portfolio Theory and CAPM

E(Ri) CAPM

E(Rm)Portfolio Theory

Harry M. Markowitz

Rf Market portfolio

y

William F. Sharpe

E(i)E(m) John Lintner, Jan Mossin,Jack Treynor

• Portfolio Theory: Diversify your portfolio! Choose your preferred

Jack Treynor

y y y p y pcombination of risk and return from the set of efficient portfolios!

• CAPM: Keep a combination of the risk free asset and the market tf li !

11Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

portfolio!

Problems of the Markowitz Optimization

M d l W ld R litModel World(true parameters)

Reality(estimated parameters)

Asset A B A B

E(return) 0.08 0.08 0.08 0.09

E( i ) 0 2 0 2 0 2 0 2E(variance) 0.2 0.2 0.2 0.2

E(correlation) 0.99 0.99

Markowitz- 0 5 0 5 -5 35 6 35

(based on DeMiguel et al. (2009))

weights 0.5 0.5 -5.35 6.35

12Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive Decision Theory: Bayesian Updating

Bayes‘ theoremy

Given: • a priori probabilities p(yi)• likelihoods p(sj|yi)

Wanted: • a posteriori probabilities p(yi|sj)

Th B• Thomas BayesObservation of a signals1: test is positive

p(s1|y1) = 90%p(s1|y2) = 10%

Original evaluationUpdated evaluationWhat is the probabilityof an infection giveny1: infected of an infection given the test is positive?

p(y1) = 0.01%p(y2) = 99.99%

y1: infected

p(y1|s1) = ?

13Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Prescriptive Decision Theory: Bayesian Updating

Bayes‘ theorem, example

)pos.tests,inf.y(p

)pos.tests|inf.y(p

11

11

)pos.tests,inf.y(p

)pos.tests(p)p,y(p

11

1

11

)infnotypostests(p)infnoty(p)infypostests(p)infy(p)inf.y|pos.tests(p)inf.y(p

)pos.tests,inf.noty(p)pos.tests,inf.y(p

111

1211

%0899.0%99.99%10%01.0%90

%01.0%90

)inf.notypos.tests(p)inf.noty(p)inf.ypos.tests(p)inf.y(p 212111

Bayes‘ theorem, in general

kkjk

iji

kjk

ji

j

jiji )y|s(p)y(p

)y|s(p)y(p)s,y(p

)s,y(p)s(p

)s,y(p)s|y(p

14Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

kk

Bayes‘ Theorem

Example:

Dr. Feelgood went for a walk at full noon in Syldenna. g ySuddenly he heard a bang, looked around, and ...

... saw a blue taxi speeding away from a damaged parked car.

Taxis in Syldenna: 5 x blue25 x green25 x green

Hit rate of Dr. Feelgood: 80% for both colors

15Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Bayes‘ Theorem

Actual Color Taxis in Syldenna

Taxis Dr. Feelgoodregards as green

Taxis Dr. Feelgoodregards as bluey

5 blue Taxis 20% of 5 is 1 taxi 80% of 5 are 4 taxisblue

green

80% of 25 is 20 20% of 25 are 525 green taxis

green

5 of 30 taxis areblue: 1/6

1/21 = 5 % 5/9 = 56 %error probability

probability correct 20/21 = 95% 4/9 = 44%

16Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Bayes‘ Theorem

E ampleExample:

p(b) = 1/6( ) 5/6

p(Fb|b) = 0.8(F | ) 0 8p(g) = 5/6 p(Fg|g) = 0.8

%44451

618.0

)Fb|b(p

%449

652.0

618.0

)Fb|b(p

%9520658.0

)Fg|g(p

%9521

612.0

658.0

)Fg|g(p

17Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Bayes‘ Theorem

Correct probability that Dr. Feelgood is right:

- If he says the taxi was green he is right with a probability of 95 %.

- If he says the taxi was blue he is right with a probability of only 44 %.

In experiments (Kahneman/Tversky, Psychological Review, 1973) p ( y, y g , )participants estimate a probability of about 80 % for both colors (hit rate)

18Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

F f M k t Effi i

Prescriptive Decision Theory: Efficient Market Hypothesis

Forms of Market Efficiency“A market in which prices always fully reflect all available information is called efficient.“ Fama (1970)

W k F S i St F St FWeak Form Semi-Strong Form Strong Form

Prices reflect information Prices reflect all publicly • Prices reflect all• Prices reflect information about past prices

• Information set = all

• Prices reflect all publicly available information

• Information set = all publicly

• Prices reflect all information, including inside information• Information set = allInformation set all

historical security pricesInformation set all publicly

available information, like e.g., past stock prices, economic reports, brokerage firm

Information set all information both public and private

Technical analysis is of no

recommendations, investment advisory letters, etc.

Fundamental analysis is of no Insider information is of no

19Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

yvalue

yvalue value

Descriptive Decision Theory

Descriptive Decision Theory:

Att ti t d ib h t l ill t ll d• Attempting to describe what people will actually do

• How people actually make decisions

Experimental research

• Laboratory experimentsy p

• In-class experiments

• Field studiesField studies

• Survey studies

•

20Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

• ...

Descriptive Decision Theory

Nobel Prize in Economic Sciences 2002Nobel Prize in Economic Sciences 2002

Daniel Kahneman

“for having integrated insights from psychological research intopsychological research into

economic science, especially concerning human judgment and

decision making under uncertainty”

One of the “books of the year” in New York Times, Wall Street Journal, The Economist…

21Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

decision-making under uncertainty

Judgment biases

Descriptive Decision Theory: Heuristics and Biases

Evaluation biasesJudgment biases

• Overconfidence• Hindsight Bias

Evaluation biases

• Reference Point Dependency• Hindsight-Bias • Anchoring and Adjustment• Availability Heuristics• Base Rate Neglect

• Loss Aversion• Mental Accounting• Ambiguity• Base Rate Neglect

• Representative Heuristics• Conjunction Fallacy• Law of Small Numbers

• Ellsberg Paradoxon• Prospect Theory

Law of Small Numbers• Gambler's Fallacy• Framing

E l tiInput

InformationInformation

EvaluationInput

22Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Overconfidence

D B d d Th l (1995)

„Perhaps the most robust

De Bondt und Thaler (1995):

„ pfinding in the psychology of judgment is that people are overconfident “overconfident.

Decision makers are too sure concerning• their abilities (car driving, time management, stock picking)( g g p g)• their knowledge• future market prices•• ...

23Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Overconfidence

Better than Average EffectBetter than Average Effect

Consider your driving skills.

Who of you thinks that you are above average compared to the other people in this room?p p

Study revealed that most of participants considered th l t b killf l th th d i i ththemselves to be more skillful than the average driver in the group.SVENSON, Ola, 1981. „Are we all less risky and more skillful than our fellow drivers?“, Acta Psychologica

24Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

y y g47 (1981) 143-148.

Descriptive Decision Theory: Overconfidence

Miscalibration

In the following we ask you for various estimates. Please clarify g y yyour estimates by giving two numbers: one upper and one lower limit. Make sure that you set your limits in a way that in your

i i th t lopinion the true value• doesn’t fall below your lower limit with a high probability

(i e with 95 % certainty)(i.e. with 95 % certainty)• doesn’t exceed your upper limit with a high probability

(i e with 95 % certainty)(i.e. with 95 % certainty)

25Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Overconfidence

Have a try: Questions for your fellow students orf ilfamily

How many mobile phones are registered in India in September 2008?

How long is the Mississippi (km)?

How many Starbucks stores are located in Germany in September 2009

How many babies are born each day (worldwide)?

How many babies have ever been born (worldwide)?How many babies have ever been born (worldwide)?

What is the market capitalization of Exxon Mobile, the largest company worldwide, at the end of 2008 (dollar) ?

What was the highest share price of „Deutsche Bank“ in 2009 (euros) ?

How many accredited credit institutions exist in Germany?

How many countries were involved in World War II?

Wh t i th l ti f S h ll I l d i 2009?

26Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

What is the population of Seychelles Islands in 2009?

Descriptive Decision Theory: Overconfidence: Comparison with other studies

No of correct answers outside the statedStudy No. of correct answers outside the stated interval (average)

Glaser et al. (WP, 2005) 6.6 ( )

Klayman et al. (OBHDP, 1999) 6.7

Russo and SchoemakerRusso and Schoemaker(1992) 6.2

Biais et al. (RES, 2005) 7.4

In-class-experiment

27Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Hindsight-Bias

When some event occurred, people believe in retrospect that they have evaluated the event to be more likely (ex ante) than they really did.

Example:Poll at 1.1.2010 Poll at 1.1.2011

( f )(before world soccer championship)

How likely is it that Germany ill h t l t th ifi l

(after championship)

At 1.1.2010, how likely did you think it was that Germany wouldwill reach at least the semifinals

in the World Cup 2010?

think it was that Germany would reach at least the semifinals in the

World Cup 2010?

Ø-answer:(fictitious)20 % 50 %

28Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

( )

Descriptive Decision Theory: Hindsight-Bias

Questionnaire study with 90 bankers in London and Frankfurt (Biais/Weber, MS, 2009)

Group B Group A

What do you think would be the assessment by your average colleague

What do you think was the b f b k l d b assessment by your average colleague

of the number of bankers employed by Lazard in New York in August 2001?

(Correct answer: 200)

number of bankers employed by Lazard in New York in August

2001?(Correct answer: 200)

Frankfurt: 3477L d 1876

Frankfurt: 692L d 642

29Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

London: 1876 London: 642

Descriptive Decision Theory: Hindsight-Bias

The Hindsight Bias...• ... is particularly strong if small probabilities are involved • ... is particularly problematic if ex ante good and substantial

decisions (but which happen to turn out bad) are ex post evaluated by othersby others

- within (firm) hierarchies- in trialsin trials- in political institutions

“You could have known that before.“ou cou d a e o t at be o e

“I knew it all along”

30Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Anchoring and Adjustment

• Anchoring: A “near at hand” first guess serves as an

Making evaluations often turns out to be a two-step procedure:

g ganchor point

• Adjustment: Further thinking causes adjustment of j g joriginal guess

Adjustment is often insufficient

Anchor point influencesfinal evaluation

What determines the anchor point? endogenous/exogenousparameters

31Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Anchoring and Adjustment

E lExample:

Group 1 Group 2Group 1

Will the HangSeng indexbe above or below 15 000

Group 2

Will the HangSeng indexbe above or below 19 000be above or below 15,000

points at the end of the year?be above or below 19,000

points at the end of the year?

What point level will the HangSeng index reach at

What point level will the HangSeng index reach at g g

the end of the year?g g

the end of the year?

Ø-answer:(fictitious)

16,200 17,700

32Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Availability bias

The easier we remember an example of a special event, the more likely we believe it is.

In most cases heuristics are suitable however in some situations the following is true:

F A il bilitFrequency Availability

• Conspicuity:• Conspicuity: Many people believe that in NY it‘s more likely to fall victim to a violent crime than

to die of natural death.

• Constructability: Are there more words with the letter R at initial or at third position?

• Recent events: How likely is it that in a Bundesliga match somebody is red-carded?

33Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Base Rate Neglect

A th l f b bilit dj t t i th di lAnother example for probability adjustment in the medical area:

Rare sickness: a priori probability: 0.01%

Test with diagnosis quality of 90%i.e. 90% of sick people are tested positivep p p

90% of healthy people are tested negative

Thi th t if th t t i iti th b bilit th t iThis means that if the test is positive the probability that a person is sick is lower than 0.1 % (see Bayesian updating)

• Insufficient consideration of the base rate (= a priori probability)• Confusion about conditional probabilities

• Inverse effect in signaling-updating-tasks Conservatism

34Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Conservatism

Descriptive Decision Theory: Representativeness heuristic

The probability that some object belongs to some category is evaluatedThe probability that some object belongs to some category is evaluated to be higher if the object looks representative for the category.

E l Fli f i i i iExample: Flip a fair coin six times

Sequence 1: Sequence 2:

H T T H T H T T T T T H

Most individuals believe that sequence 1 is more likely to be obtained.

Is this just a misunderstanding? (sequence not relevant)Is this just a misunderstanding? (sequence not relevant)Sequence 1:

H T T H T H

Sequence 2:

T T T H H H

Most individuals still believe that sequence 1 is more likely than sequence 2.

H T T H T H T T T H H H

35Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Conjunction fallacy

A compounded (and thereby more specific) event is evaluated to be more likely because it looks more representative.

Example: In your opinion how likely are the following events?Example: In your opinion, how likely are the following events?

Event 1: Event 2:The DAX declines by more than 200

Tomorrow a major German company willannounce a strong decrease in profits and

points tomorrow.

Ø-answer:

the DAX will decline by more than 200 points.

(fictitious)2% 3%

36Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Conjunction fallacy

The famous example of Linda“ (Tversky und Kahneman Psychological Review 1983)The famous example of „Linda (Tversky und Kahneman, Psychological Review, 1983)

Linda is 31 years old, single, outspoken and very bright. She majored in philo-sophy As a student she was deeply concerned with issues of discriminationsophy. As a student, she was deeply concerned with issues of discrimination and social justice, and also participated in anti-nuclear demonstrations.

Rank the following statements about Linda by their probability:

Linda is a teacher in elementary school•Linda is a teacher in elementary school•Linda works in a bookstore and takes Yoga classes•Linda is active in the feminist movement• ...•Linda is a bank teller•Linda is an insurance salesperson

8%

• ...•Linda is a bank teller and is active in the feminist movement20%

37Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Misinterpretation of stochastic processes

“La of small n mbers““Law of small numbers“

• Individuals overestimate the information content of small samples.

“Three consecutive successful investmentThree consecutive successful investmentrecommendations; that can’t be a coincidence“

A l i

• Assumed recognition of systematic patterns

Autocorrelation

in actually not auto-correlated sequences.

· Hot-hand-phenomenon

· Belief in the success of technical analysis

38Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Misinterpretation of stochastic processes

Gambler's fallacGambler's fallacy

Belief that a red number is more likelyBelief that a red number is more likely after 5 consecutive black numbers.

Reason: Wrong understanding of “Law of big numbers“

It holds: Number of redNumber of black 1

B t t

It i f t th t th b bilit f “ d” d t d d

But not: Number of red – Number of black 0

It is a fact, that the probability for “red” does not depend on historical events.

39Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

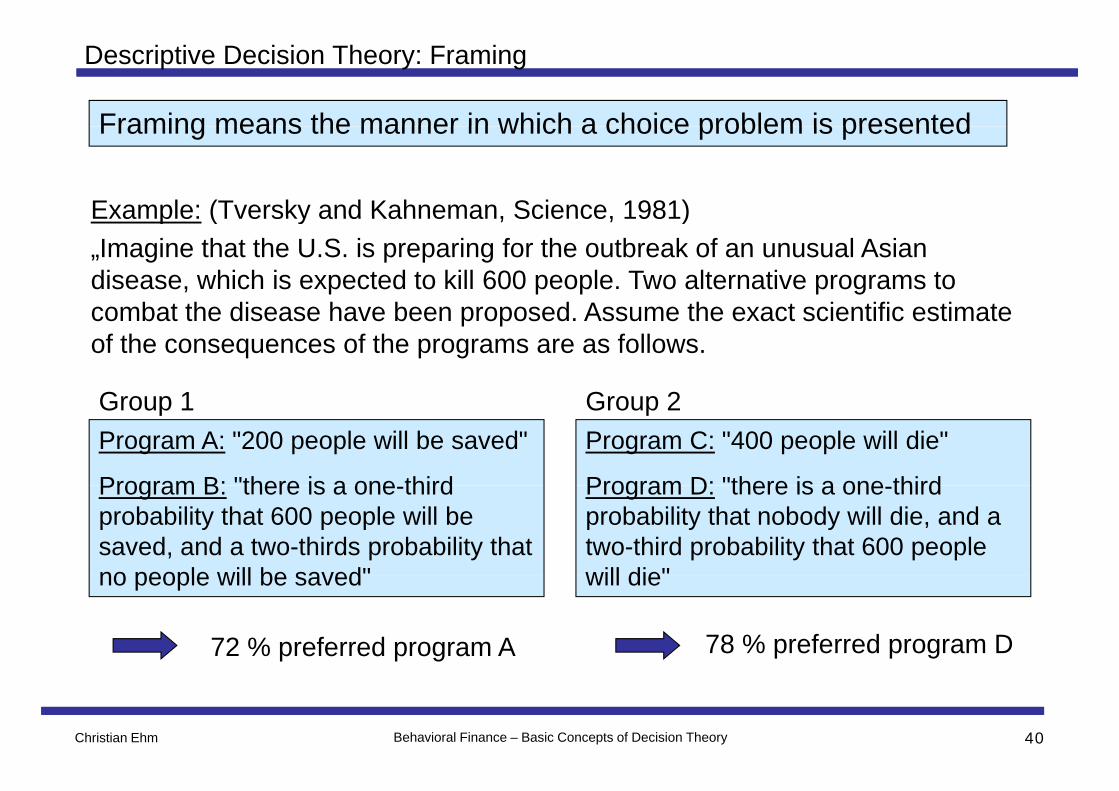

Descriptive Decision Theory: Framing

Framing means the manner in which a choice problem is presentedFraming means the manner in which a choice problem is presented

Example: (Tversky and Kahneman Science 1981)Example: (Tversky and Kahneman, Science, 1981)„Imagine that the U.S. is preparing for the outbreak of an unusual Asian disease, which is expected to kill 600 people. Two alternative programs to

b t th di h b d A th t i tifi ti tcombat the disease have been proposed. Assume the exact scientific estimate of the consequences of the programs are as follows.

G 1 G 2Program A: "200 people will be saved"

Program B: "there is a one third

Program C: "400 people will die"

Program D: "there is a one third

Group 1 Group 2

Program B: there is a one-third probability that 600 people will be saved, and a two-thirds probability that no people will be saved"

Program D: there is a one-third probability that nobody will die, and a two-third probability that 600 people will die"no people will be saved will die

72 % preferred program A 78 % preferred program D

40Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Heuristics and Biases

Judgment biases Evaluation biasesJudgment biases

• Overconfidence• Hindsight Bias

Evaluation biases

• Reference Point Dependency• Hindsight-Bias • Anchoring and Adjustment• Availability Heuristics• Base Rate Neglect

• Loss Aversion• Mental Accounting• Ambiguity• Base Rate Neglect

• Representative Heuristics• Conjunction Fallacy• Law of Small Numbers

• Ellsberg Paradoxon• Prospect Theory

Law of Small Numbers• Gambler`s Fallacy• Framing

E l tiInput

InformationInformation

EvaluationInput

41Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Reference Point Dependent Evaluation

Rational decision making requires the valuation of aggregated outcomes.

Basic result: Individual decisions are not based on the valuation of total l h b h l i f l h h l i f i

g q gg g

wealth, but on the valuation of wealth changes relative to a reference point (often the status quo).

100 €100%

b200 €50%Framing-

100 €a b0 €50%

S t f 200 € d

effects

Secure payment of 200 € and

0 €50% 100%a´ b´

0 €

-200 €50%-100 €

100%

42Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Loss Aversion

Assume you have to face the following pair of decisions:

Typical answers

Alternative a: +500 $100%1.or

Alternative b:+1000 $

0 $25%

75%

Alternative c: -500 $100%2.or

Alternative d:0 $

1000 $

25%

%Alternative d:-1000 $75%

43Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Loss Aversion

“Loss aversion refers to the fact that people tend to be more sensitive to decreases in their wealth than to increases.”

+$20050% +$200

-$100

50%

50%Famous (hypothetical) statement:

„... I won’t bet because I would feel the $100 loss more than the $200 gain.”

44Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Mental Accounting

• Mental accounting attempts to describe the process whereby people• Mental accounting attempts to describe the process whereby people code, categorize and evaluate economic outcomes

• People group their assets into a number of isolated mental accounts• People group their assets into a number of isolated mental accounts which are optimized separately

Examples: (Thaler (1985))

Mr. X is up $50 in a monthly poker game. He has a queen high flush and calls a $10 bet. Mr. Y owns 100 shares of IBM which went up ½ today and is even in the poker game. He has a king high flush but he folds. When X wins, Y thinks to himself, “If I had been up $50 I would have called too.“p

Mr. and Mrs. J have saved $15,000 toward their dream vacation home. They hope to buy the home in five years The money earns 10% in a money markethope to buy the home in five years. The money earns 10% in a money market account. They just bought a new car for $11,000 which they financed with a three-year car loan at 15%.

45Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Ambiguity

Ambiguity Aversion g yPreference for known risks over unknown risks

Concept: p(heads) p(tails)

p(DAX +) p(DAX 0/-)p(DAX +) p(DAX 0/ )

Problem: Certainty of probability measuring

Contradiction to EUT:Contradiction to EUT:EUT requires that only the probability of an event is relevant for the valuation, not the uncertainty of the probability.

46Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Ellsberg Paradoxon

urn 1: urn 2:

5 white, 5 blue balls 10 white and blue balls in an unknown proportion

First question: You win when you draw a blue ball

p p

First question: You win, when you draw a blue ball. Which urn do you prefer?

Second question: You win when you draw a white ballSecond question: You win, when you draw a white ball. Which urn do you prefer?

47Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Prospect Theory

In general:In general: also concept of value function

a better than b

• Kahneman and Tversky, 1979• Tversky and Kahneman, 1992 (CPT)

a better than bif and only if V(a) > V(b)

Furthermore: also additive form n

ii avpaV )()()(

• Shape of the value function

i 1

• Shape of the value function- Reference point dependent evaluation- Loss aversion (losses are weighted more heavily than gains)( g y g )- Different risk attitude for gains and losses

• Probability weighting

48Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Prospect Theory

Sh f th l f tiShape of the value function

value functionvalue functionv(x)

concave

v(x) =x, for x 0

-k(-x), for x < 0

concaverisk aversewith k 1,

1

Loss aversion gains xlosses x Loss aversion gains xlosses x

convexrisk prone

Reference point d d

49Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

dependency

Descriptive Decision Theory: Prospect Theory

Risk aversion and risk seeking:gconcaverisk averse

+$10050%

50

v(50)

100

v(100) +$100

$0

50%

50%+$50100%

vs.A B

50 100 $

Under prospect theory: v(A)<v(B) 0.5*v(100)+0.5*v(0)<1*v(50)

$10050%

convexrisk prone

-50-100

-$100

$0

50%

50%-$50100%

vs.A B

v(-50)

v( 100)

$0

Under prospect theory: v(A)>v(B) 0.5*v(-100)+0.5*v(0)>1*v(-50)

50Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

v(-100) ( ) ( ) ( )

Descriptive Decision Theory: Prospect Theory vs. EUT

Prospect TheoryEditing-Phase:

Expected Utilityg

Combination, Segregation,

Cancellation Coding

reference point

Cancellation, Coding

• reference point

• gain / loss

•

• terminal assets

• special value function: v

• Probability transformation: • utility function

•

51Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Prospect Theory

P b bilit i hti f tiProbability weighting function:

Weighting functions for gains

52Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

(w+) and losses (w-)

Descriptive Decision Theory: Prospect Theory „in the Wild“

Source: Camerer C (2000) Prospect Theory in the wild In D Kahneman & A Tversky (Eds )

53Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Source: Camerer, C. (2000). Prospect Theory in the wild. In D. Kahneman. & A. Tversky (Eds.)Choice, Values, and Frames. New York: Cambridge University Press, pp. 288-300

Descriptive Decision Theory: Expected utility theory and prospect theory

Peter participates in a quiz show. He is wondering whether to answer thelast question. There are two possible answers. The right answer earns him1 million, in case of a wrong answer he falls back to 16,000 €. The secondgoption is to quit the game and to go home with 500,000 €. Peter thinks thatanswer A is the right one with a subjective probability of 0.7, answer B isright with a probability of 0.3 respectively.right with a probability of 0.3 respectively.

Peter maximizes his expected utility He has no further wealth apart fromPeter maximizes his expected utility. He has no further wealth apart fromthe realized gain. His preferences can be described with the utility function

xxu )(In this situation: would Peter answer or not?

xxu )(

54Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Expected utility theory and prospect theory

Candidate in a quiz show, answering or not?

do answer: right answer: 1 million

wrong answer: 16,000

do not answer: 500,000

x)x(u => Maximize expected utility: x)x(u => Maximize expected utility:

EU (answer) =

EU (not answer) =

95.737000,163.0000,000,17.0

11.707000,500

As EU (answer) > EU (not answer), Peter answers

55Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

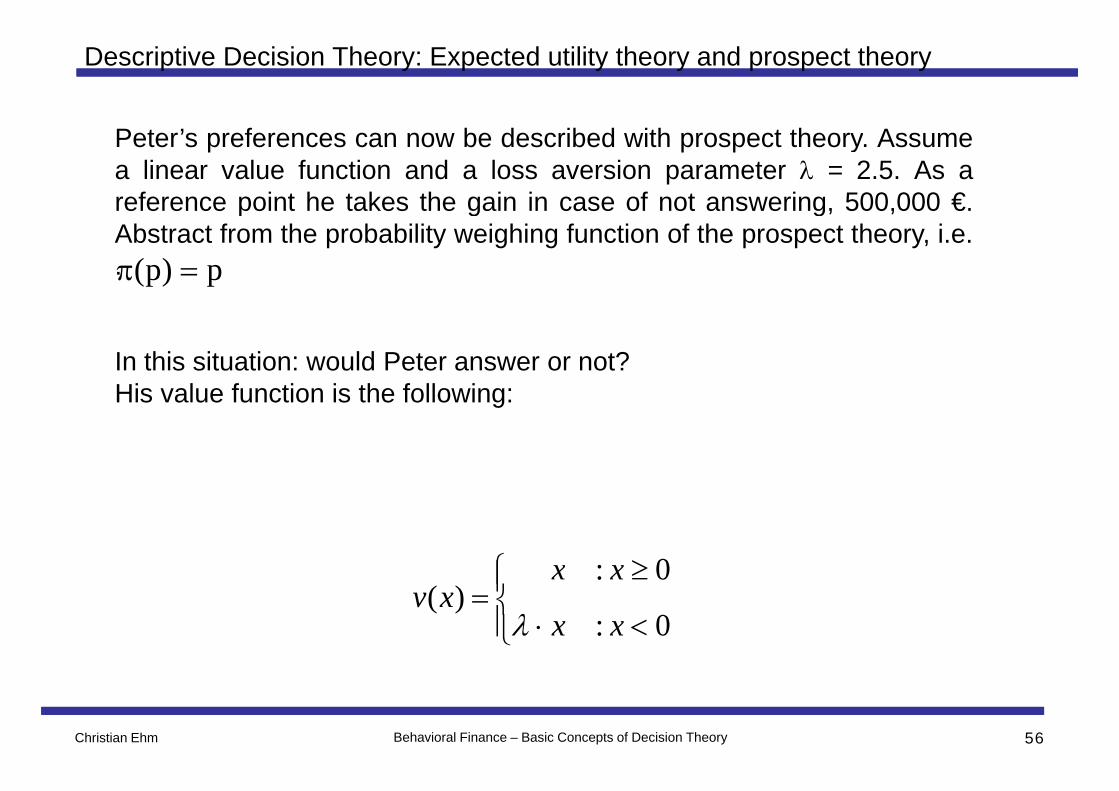

Descriptive Decision Theory: Expected utility theory and prospect theory

Peter’s preferences can now be described with prospect theory. Assumea linear value function and a loss aversion parameter = 2.5. As areference point he takes the gain in case of not answering, 500,000 €.p g gAbstract from the probability weighing function of the prospect theory, i.e.. p)p(

In this situation: would Peter answer or not?His value function is the following:His value function is the following:

0: xx

0:

0:)(

xx

xxxv

56Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm

Descriptive Decision Theory: Expected utility theory and prospect theory

Candidate in a quiz show, answering or not?

do answer: right answer: 1 million

wrong answer: 16,000

do not answer: 500,000

b) Maximize prospect value: 520x:x

)x(v

b) Maximize prospect value: 5.20x:x

)x(v

v (answer) =

v (not answer) = 0

000,13)000,484(5,23.0000,5007.0

As v (not answer) > v (answer), Peter does not answer

57Behavioral Finance – Basic Concepts of Decision TheoryChristian Ehm