before the securities appellate tribunal …takeovercode.com/uploads/case_laws/7591luxottica.pdf ·...

TRANSCRIPT

BEFORE THE SECURITIES APPELLATE TRIBUNAL

MUMBAI

In the matter of:

Appeal No.61/2002

1. Luxottica Group SpA 2. Ray Ban Holdings Inc. 3. Bausch & Lomb Indian Holding Inc. Appellants

Vs.

Securities & Exchange Board of India Respondent

Appearance:

Shri Aspi Chinoy,

Sr.Advocate

Shri Shashivansh Bahadur

Advocate

Shri V. N. Kaura

Advocate For Appellants

Shri Rafique Da

da

Sr.Advocate

Shri Kumar Desai

Advocate

Ms. Daya Gupta

Advocate

Shri J. Ranganayakulu,

Jt. Legal Adviser, SEBI

Shr

i Vinay Chauhan

Legal Officer, SEBI for Respondent

ORDER

The order passed by the Respondent (SEBI) on 5.8.2002 in the matter of acquisition of shares/voting rights and control of Ray Ban Sun Optics India Ltd. (formerly known as Bausch & Lomb India Ltd.) by Luxottica S. p. A is under challenge in the present appeal.

The Appellant No.1 (the Luxottica Group S.p.A) is a company registered under the laws of Italy. It is engaged inter alia in the design, manufacture and marketing of prescription/spectacle frames and sunglasses (‘Eyewear’ business/ ‘the Business’). It has operations in several countries directly or through its subsidiaries.

The Appellant No.2 is a corporate entity incorporated under the laws of USA. It is a wholly owned indirect subsidiary of the Appellant No.1. The Appellant No.3 is also a corporate entity incorporated under the laws of USA. It is a wholly owned subsidiary of the Appellant No.2 and an indirect subsidiary of the Appellant No.1.

Certain other entities, namely Bausch & Lomb Inc. Ray Ban Sun Optics India Ltd.(formerly known as Bausch & Lomb India Ltd.), Bausch & Lomb South Asia Inc, Bausch & Lomb South Asia Holdings Inc., are also involved in the matter. Bausch & Lomb Inc., a corporate entity incorporated in New York, belongs to the Bausch & Lomb Group of USA. Bausch & Lomb Group is engaged in the production, marketing and distribution of sunglasses and spectacle frames and certain related accessories (Eyewear and Eyecare business) in various localities around the world.

Ray Ban Sun Optics India Ltd., (the Target Company) is a public limited company incorporated in India. Its shares are listed on the stock exchanges at Jaipur, Mumbai, Delhi, Calcutta and Ahmedabad. 44.152% of its share capital is held by Appellant No.3. It is engaged in the business of manufacturing and dealing in all kinds of opthalmicotic and pharmaceutical devices and opthalmic care products including contact lenses, sunglasses, spectacles, frames, solutions, cleaners and accessories for the same. Its product range is broadly divided into two categories namely the ‘Eyewear products’ which consisted of sunglasses and prescription frames and the "Eyecare/Visioncare products" which consisted of contact lenses, cleaning solutions and distribution of surgical products. The said categorization of business has a bearing in the matter under consideration.

Bausch & Lomb South Asia Inc.,a New York Company, is a 100% subsidiary of Bausch & Lomb Inc. Initially it was holding 44.152% share capital of the Target company. The said shareholding was subsequently transferred to Appellant No.3.

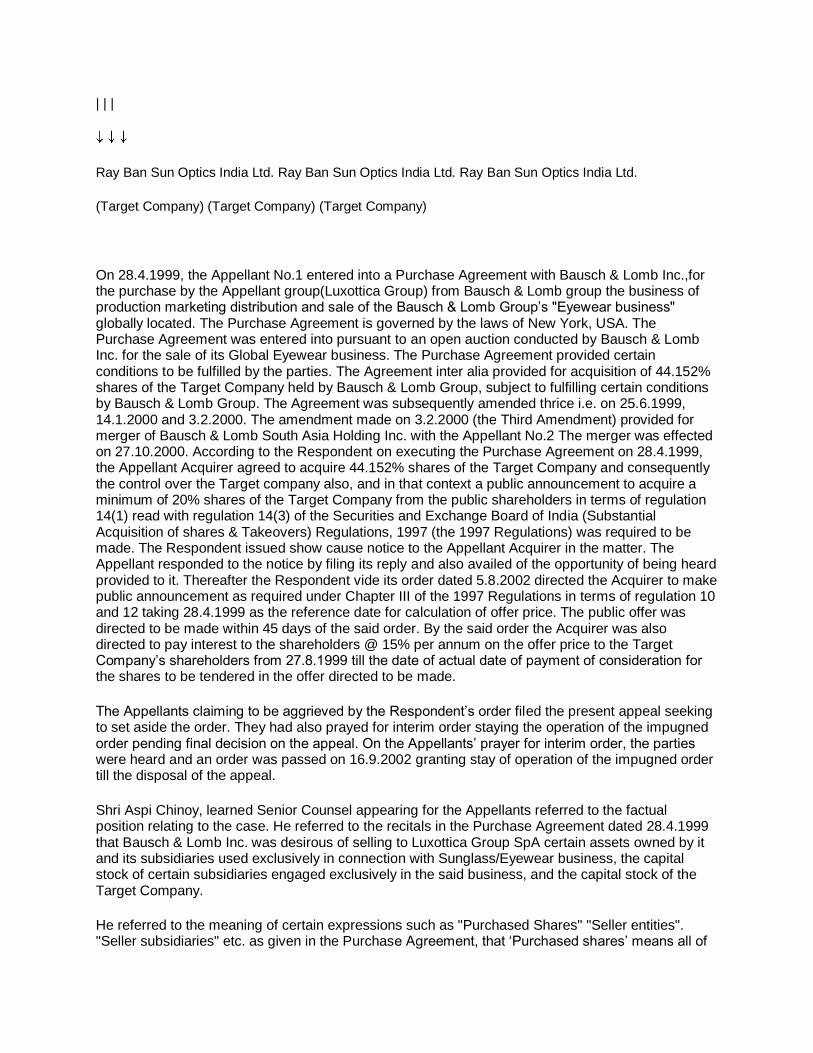

Bausch & Lomb South Asia Holdings `Inc., also a corporate entity incorporated in USA was a wholly owned subsidiary of Bausch & Lomb Inc. This company merged with the Appellant No.2 some time in October 2000. The following chart provided by the Appellants indicates the position of each of the above referred to entities involved in the acquisition under consideration in the present appeal:

On 28.4.1999 On 24.3.2000 On 27.10.2000

Bausch & Lomb Inc. Bausch & Lomb Inc. Luxottica Group SpA

| | |

| | |

| | |

|

| Bausch & Lomb Merged into Ray Ban Holdings Inc.

| South Asia on 27.10.2000

| Holding Inc. |

| |

| | |

| | |

| | |

| | |

Bausch & Lomb Inter-se transfer of Bausch & Lomb Indian Bausch & Lomb Indian

South Asia Inc. 44.152% in Target Holdings Inc. Holdings Inc.

Company on

24.3.2000 | |

| | |

| | | |44.152% |44.152% |44.152%

| | |

| | |

| | |

| | |

Ray Ban Sun Optics India Ltd. Ray Ban Sun Optics India Ltd. Ray Ban Sun Optics India Ltd.

(Target Company) (Target Company) (Target Company)

On 28.4.1999, the Appellant No.1 entered into a Purchase Agreement with Bausch & Lomb Inc.,for the purchase by the Appellant group(Luxottica Group) from Bausch & Lomb group the business of production marketing distribution and sale of the Bausch & Lomb Group’s "Eyewear business" globally located. The Purchase Agreement is governed by the laws of New York, USA. The Purchase Agreement was entered into pursuant to an open auction conducted by Bausch & Lomb Inc. for the sale of its Global Eyewear business. The Purchase Agreement provided certain conditions to be fulfilled by the parties. The Agreement inter alia provided for acquisition of 44.152% shares of the Target Company held by Bausch & Lomb Group, subject to fulfilling certain conditions by Bausch & Lomb Group. The Agreement was subsequently amended thrice i.e. on 25.6.1999, 14.1.2000 and 3.2.2000. The amendment made on 3.2.2000 (the Third Amendment) provided for merger of Bausch & Lomb South Asia Holding Inc. with the Appellant No.2 The merger was effected on 27.10.2000. According to the Respondent on executing the Purchase Agreement on 28.4.1999, the Appellant Acquirer agreed to acquire 44.152% shares of the Target Company and consequently the control over the Target company also, and in that context a public announcement to acquire a minimum of 20% shares of the Target Company from the public shareholders in terms of regulation 14(1) read with regulation 14(3) of the Securities and Exchange Board of India (Substantial Acquisition of shares & Takeovers) Regulations, 1997 (the 1997 Regulations) was required to be made. The Respondent issued show cause notice to the Appellant Acquirer in the matter. The Appellant responded to the notice by filing its reply and also availed of the opportunity of being heard provided to it. Thereafter the Respondent vide its order dated 5.8.2002 directed the Acquirer to make public announcement as required under Chapter III of the 1997 Regulations in terms of regulation 10 and 12 taking 28.4.1999 as the reference date for calculation of offer price. The public offer was directed to be made within 45 days of the said order. By the said order the Acquirer was also directed to pay interest to the shareholders @ 15% per annum on the offer price to the Target Company’s shareholders from 27.8.1999 till the date of actual date of payment of consideration for the shares to be tendered in the offer directed to be made.

The Appellants claiming to be aggrieved by the Respondent’s order filed the present appeal seeking to set aside the order. They had also prayed for interim order staying the operation of the impugned order pending final decision on the appeal. On the Appellants’ prayer for interim order, the parties were heard and an order was passed on 16.9.2002 granting stay of operation of the impugned order till the disposal of the appeal.

Shri Aspi Chinoy, learned Senior Counsel appearing for the Appellants referred to the factual position relating to the case. He referred to the recitals in the Purchase Agreement dated 28.4.1999 that Bausch & Lomb Inc. was desirous of selling to Luxottica Group SpA certain assets owned by it and its subsidiaries used exclusively in connection with Sunglass/Eyewear business, the capital stock of certain subsidiaries engaged exclusively in the said business, and the capital stock of the Target Company.

He referred to the meaning of certain expressions such as "Purchased Shares" "Seller entities". "Seller subsidiaries" etc. as given in the Purchase Agreement, that ‘Purchased shares’ means all of

the issued and outstanding shares of the capital stock of the Transferred subsidiaries held by the Seller Entities, ‘Seller Entities’ means Seller subsidiaries. ‘Seller’ means Bausch & Lomb Inc. He also referred to the names of the "Seller Subsidiaries" and ‘Transferred subsidiaries’ given in schedule 1.1(a) and 1.1(b) to the Agreement. As per the Purchase Agreement the shares of eight subsidiaries of Bausch & Lomb Inc described as Transferred subsidiaries in the Agreement (including the Target Company) were to be acquired, that 34 companies described as Seller subsidiaries were not to be transferred to the Appellants and they were to continue as subsidiaries of Bausch & Lomb Inc. These 34 Seller subsidiaries, some of them holding shares in the Transferred subsidiaries, were only to sell to the Appellants the assets held by them relating to the Eyewear business and the shares of the eight Transferred subsidiaries held by them. Shri Chinoy submitted that reference to "stock" shown against 4 seller subsidiaries in the schedule 1.1(a), which include Bausch & Lomb South Asia Inc., is not the stock of the 4 Seller subsidiaries listed, but is a reference to the stock of the 8 ‘Transferred Subsidiaries’ which was held by these Seller subsidiaries and was required to be sold by them to the Appellants. Learned Senior Counsel submitted that in terms of clause 2.1 of the Purchase Agreement, on the Closing date, Bausch & Lomb Inc. was to cause the Seller subsidiaries to sell and transfer the Purchased shares and the other Purchased assets. He submitted that the expressions "Closing" and the "Closing Date" have been defined in article 3.1, that the Closing Date stated therein is 25.6.1999. In respect of transfer of the foreign assets/shares which required foreign approval (i.e. Deferred Shares or Deferred Assets), the Closing was to be deferred till the receipt of such foreign approval, that between the Closing Date and the Deferred Closing Date, the Deferred Assets and such of the 8 Transferred subsidiaries as were represented by any Deferred Shares, were to be administered as stipulated by Schedule 3.3.(c) that (i)the Seller subsidiaries were to continue to hold the Deferred Assets and the Deferred Shares till the Deferred Closing,(ii) the portion of the Purchase price relating to the Deferred Shares and Assets was to be held by the Seller in Escrow till the Deferred Closing occurred.(iii) pending the Deferred Closing, the applicable Seller Entities and the Deferred Subsidiaries were to operate the business for the account of the Buyer. Accordingly in the case of a Deferred Country having Deferred Shares, the Seller entity owning the Deferred Shares was to pay to the Buyer any net after tax distribution (dividend) received from the Deferred Subsidiary during the Deferral Period, (iv) pending the Deferred Closing the Buyer subsidiaries were to grant the Deferred Subsidiary a royalty free license to use the Intellectual Property and the non complete clause was not to apply to the continuance of business by such Deferred Subsidiaries.

In the event a Deferred Closing had not occurred within 18 months the Deferred Net Assets and Deferred Shares and the allocable portion of the purchase price were to be administered as per Schedule 3.3.(d) that (i) the proposed purchase (of such Deferred Assets or Deferred Shares) was to be abandoned and the Seller Entity was to refund to the Buyer, the portion of the purchase price allocated to such Deferred Assets and Shares, without interest. (ii) the Buyer was to enter into an agreement with such Seller Entity / Deferred Subsidiary, to provide sunglasses and sunglass products, to enable such Seller subsidiary to continue its existing business, (iii)the Buyer was also entitled at its discretion to elect to discontinue such business and require the Seller to liquidate the Deferred net Assets and the Shares of such Deferred Subsidiaries and to pay the net proceeds of such liquidation to the Buyer.

Out of the 8 subsidiaries to be transferred, the Target Company was the only subsidiary which was not exclusively engaged in the sunglass / Eyewear business. It was also carrying on the Eyecare / contact lens business. More over the applicable Seller Entity (Bausch & Lomb South Asia Inc) did not hold 100% shares of the Target Company. It held only 44% of the total shares of Target Company Accordingly the Target Company was required to be and was separately referred to / dealt with. Clause 6.4 of the Purchase Agreement specifically provides for the treatment of the Target Company. The said Clause 6.4(a) stipulated that the seller would use commercially reasonable efforts to purchase from the Target Company, all assets which did not relate to the sunglasses / eyewear business. (ii) the Target Company was to remain as a Deferred Subsidiary until such

transactions / divestment of the non sunglass/Eyewear business had occurred, and (iii)if such transaction (i.e. divestment / sale of the non Eyewear business) had not occurred within 24 months, the proposed transfer of the Target Company.’s shares was to be abandoned.

It has been provided in Clause 6.4(d) that Clause 6.4 was to prevail over any other Clause/Section of the Agreement. It was submitted that the Agreement/intent to acquire the 44% shares of the Target Company from Bausch & Lomb South Asia Inc, was accordingly conditional/contingent upon the divestment / sale of the non Eyewear business (i.e. sale of the Eyecare / contact lens business) by the Target Company, that such conditional / contingent agreement could not be enforced, performed, or implemented till the condition / contingency had occurred – i.e. till the non Eyewear business had been divested by the Target Company. At the time of execution of the Agreement on 28.4.1999 therefore, what "Product" the Appellant wanted to purchase in India, did not actually exist, and its price was indeterminate. Further under section 293(1)(a) of the Companies Act, 1956 such divestment required the approval of the shareholders of the Target Company in General Meeting and as 56% of the total shares of the Target Company were held by third parties / the public passage of the resolution required their support that Bausch & Lomb South Asia Inc which held only 44% of the share capital of the Target Company could not guarantee/ensure the passage of the Resolution. If the required divestment did not take place within 24 months, the proposed purchase / transfer was to be abandoned.

Learned Senior Counsel submitted that on receipt of Regulatory approval, Closing vis a vis the USA transaction occurred in June 1999, that on 3

rd February 2000, i.e. before the divestment of the non

Eyewear business had taken place & whilst the contingent agreement regarding the acquisition of the 44% shares of the Target Company had not become enforceable, the parties amended the Agreement of 28

th April 1999 by deleting & substituting Clause 6.4, that the substituted clause 6.4

provided that the 44% shares of the Target Company then held by Bausch & Lomb South Asia Inc. would be transferred to the newly created Seller Subsidiary which would then be merged with a newly created Buyer Subsidiary, under the laws of the State of Delaware USA. On 3

rd Feb 2000 the

Appellant No.1 entered into a Technical Assistance Agreement with the Target Company to provide Technical Assistance till the merger / Closing date, that this was necessary as under the U.S. Closing which had already occurred in June 1999, the Intellectual Property / Technological know-how had already been acquired by & transferred to the Buyer/ Luxottica. However, clause 16.2 of the Technical Assistance Agreement specifically recorded that neither Luxottica nor any of its subsidiaries/affiliates "shall have or has ever had, any role in either the day to day or the long term management of B & L India" On 21

st July 2000 the shareholders of the Target Company . passed the

requisite Resolution under section 293(1) (a) of the Companies Act for the divestment / sale of the Company’s non Eyewear business – i.e. the Eyecare business / assets. Pursuant thereto the sale of the Eyecare business / assets to a subsidiary of Bausch & Lomb Inc for Rs.258 million was effected on 23

rd October, 2000. Bausch & Lomb South Asia Inc. had on 24.3.2000 transferred the 44%

shares of the Target Company to another specially created Seller subsidiary in Delaware viz. Bausch & Lomb Indian Holdings Inc.(i.e. Appellant No.3). Pursuant to the divestment and satisfaction of the condition and pursuant to a merger Agreement dated 27

th October 2000, Bausch

& Lomb South Asia Holdings Inc merged with Ray Ban Holding Inc (Appellant No.2) a specially created Buyer subsidiary in the State of Delaware USA and the said merger has been duly recognised and certified to by the Secretary of State, Delaware USA. On 29

th/30

th October 2000 the

Board of Directors of the Target Company was reconstituted & nominees of Luxottica Group were appointed as its directors.

It was stated that the Respondent SEBI issued a show cause notice dated 19th February 20002 to

the Appellants alleging that :

" the Appellants were "acquirers" under regulation 2(1)(b) as by the Agreement dated 28

th April 1999, they had agreed to acquire 44% of the shares & control of the Target

Company., that the acquisition was not eligible for exemption under Regulation 3 (1)(j)(ii), by virtue of Regulation 3 (1)(k) which stipulated that exemption thereunder would not be applicable if by virtue of acquisition or change in control of any unlisted company whether in India or abroad, the acquirer acquires shares, or voting rights, or control of a listed company, and the Appellants were required to make a public announcement within 4 working days from 28

th April 1999."

Appellants’ reply to the show cause notice vide letter dated 5.3.2002 was referred to by the learned Senior Counsel. The reply inter alia pointed out that (i) the agreement to purchase the 44% shares of the Target Company was ultimately conditional / contingent upon the sale / divestment of the non eyewear business / assets of the Target Company. (ii) the obligation to purchase the said 44% shares would arise only if and when all the Eyewear assets had been purchased by Bausch & Lomb Inc and the price consideration was to be determined "solely on the basis of the assets, liabilities and operations of B & L India Ltd., which are primarily related to the Eyewear business, adjusted to take into account the applicable partial ownership," that (iii) it was not within the power of the Seller (B & L South Asia Inc) to dispose off the non Eyewear business/assets of the Target Company as under section 293(1)(a) of the Companies Act such transfer / disposal required a Resolution of the shareholders in general meeting and B & L Inc had only 44% of the shares and could not have got such resolution passed without the concurrence / support of the other 56% shareholders, that that under New York Law & under section 31 & 32 of the Indian Contract Act, a conditional / contingent agreement could not be enforced or performed unless the condition had been fulfilled / the contingency had occurred. The Contingent Agreement to acquire the 44% shares of the Target Company would mature into a legally enforceable contractual obligation only if and when, the requisite resolution under section 293(1)(a) of the Companies Act was passed in General Meeting and the non Eyewear business of the Target Company, were purchased by B & L Inc and the sale proceeds used to discharge the liabilities of the non Eyewear Business, that if this had not happened within 24 months the transaction would have been abandoned. The shareholders passed the requisite resolution under section 293(1)(a) on 21

st July, 2000 and the transfer/divestment was

effected on 23rd

October 2000. Before such contingency had occurred, the parties had on 3rd

February 2000 substituted clause 6.4 and had decided to pursue a merger of the shareholding companies. The merger which took place on 27

th October 2000 under the laws of Delaware USA

was exempted under Regulation 3 (1)(j)(ii), that this exemption was not affected by the explanation to Regulation 3 (1)(k).

Learned Senior Counsel submitted that the Respondent brushed aside the submissions and passed the impugned order dated 5

th August 2002 directing the Appellants to make a Public Offer taking 28

th

April 1999 as the reference date for fixing the price and to pay interest at 15% per annum from 27th

August 1999 by which date the offer process should have been completed. He submitted that according to the Respondent (i) the Appellants’ contention that it was not an acquirer in terms of Regulation 2 (1)(b) as the Agreement dated 28

th April 1999 relating to the Target Company was

conditional/contingent on the occurrence of events which were uncertain both factually and legally, was untenable. SEBI has merely held that to fall within the definition of an acquirer in Regulation 2 (1)(b) it was not necessary that one should actually acquire shares; that it was sufficient if a person agreed to acquire shares. SEBI has not dealt with the issue of whether a person whose agreement to acquire shares was contingent/conditional could be held to be an acquirer under Regulation 2 (1)(b). (ii) making a Public Announcement/Offer was a pre acquisition requirement and that the acquirers could have made a conditional public announcement stating the conditions subject to which the acquisition was to be carried out. SEBI has noted that under the Regulations public announcement could be made subject to the receipt of statutory approvals or receipt of minimum level of acceptance from the shareholders and has held therefrom that all conditional announcements/offers could be made. SEBI has held that "Thus when the acquirer, in the instant case announced his intention to acquire the 44.152% capital of the Target Company by way of entering into purchase Agreement with the Seller on 28

th April 99, it constituted an intention to

acquire indirectly, the control over the target company and the obligation to make public announcement arose on that day, which was to be made within 4 working days of 28.4.99 i.e. the date of entering into the said agreement", (iii) the exemption under Regulation 3 (1)(j)(ii) was not available as the Regulations had already been triggered on 28

th April 99 "any actions subsequent to

the triggering of the said Regulations will not have bearing on the making of an open offer by the acquirer as the said regulations have already been triggered." That the merger route had been devised by the acquirer as a device / artifice subsequently with the intention of circumventing the Regulations and avoiding making a public offer & was contrary to the spirit and policy of the Regulations.

It was submitted by the learned Senior Counsel that the Appellants had not agreed to acquire or pay for the shares of the Target Company with its non Eyewear business, that they had only agreed to acquire & pay for the shares of the Target Company, subject to / conditional upon the Target Company divesting itself of its non Eyewear business. According to the Appellants the Agreement dated 28

th April 1999 in so far as it pertains to the 44% shares of the Target Company was

contingent/conditional on Bausch & Lomb Inc arranging to buy the business & assets of the Target Company which did not relate to the Eyewear / sunglasses Business and the Target Company utilizing the sale proceeds to discharge the liabilities relating to the Eyecare business, that even the consideration payable was to be fixed post divestment only with reference to the assets relating to the Eyewear Business, adapted to the Bausch & Lomb Inc.’s limited / 44% interest therein. The divestment of the non Eyewear Business of the Target Company was effected only on 23

rd October

2000 – when the non Eyewear Assets were sold. Accordingly requiring the Appellants to make a public offer in April 1999, and at the price prevalent in April 99, would amount to compelling the Appellants to (a) acquire the shares of a Company whose business and assets (Eyewear Business and Eyecare / Contact lens Business), were totally different from the business and assets of the Company which the Appellants had agreed to acquire under the contingent agreement dated 28

th

April 1999 (b) acquire and pay for the business and assets of the Eyecare Business, which the parties had expressly agreed would be excluded / disposed off prior to the acquisition. (c) pay to the shareholders of the Target Company a price for their shares which included the value of the Eyecare Business, that in April 1999 the share price ranged from Rs 100/- - 139/- , that however, at the time of divestment in October 2000 the share price ranged from Rs.30 to 39 /share.

It was submitted the agreement dated 28th April 1999 did not make the Appellants "acquirers" or

trigger the public announcement/public offer requirements of the regulations. The contingent/conditional agreement / decision to acquire the 44% shares if and when the Target Company divested its non Eyewear business did not make the Appellant an "acquirer" in terms of Regulation 2 (1)(b) and did not trigger the Regulations/Public Offer requirements, unless and until the contingency had occurred / the condition had been fulfilled. The Regulations do not envisage or permit such a conditional announcement / offer being made. The only conditional offers permitted under the Regulations, are an offer being made conditional to the receipt of the statutory approvals, or an offer being made conditional to the receipt of a minimum level of acceptances by the shareholders. The Scheme & provisions of the Regulations preclude any other conditional offer being made. Accordingly the Appellant could not be required to make an offer conditional on the divestment of the non Eyewear business by the Target Company. Although the public announcement / offer is a pre acquisition requirement, it is only triggered when there is an unconditional / final decision, or agreement to acquire shares on the part of the acquirer. A conditional decision, or a contingent agreement to acquire shares, is not covered by regulation 2 (1)(b) read with regulation 14. The triggering requirements of regulation 2 (1)(b) read with regulation 14 are "entering into an agreement for acquisition of shares" or "deciding to acquire shares". These words necessarily connote a final decision / binding agreement on the part of the acquirer. Regulations 2 (1)(b) & 14 do not refer to "entering to a contingent agreement for acquisition of shares" or "conditionally deciding to acquire shares" Under both New York Law & the Indian Contract Act, such a contingent agreement or a conditional decision cannot be enforced, and

creates no obligations until and unless the contingency occurs or the condition has been fulfilled. Moreover Regulation 22 (1) expressly stipulates that a public announcement of offer to acquire shares of a target company shall be made only when the acquirer is able to implement the offer. A contingent agreement/ conditional decision can be implemented only if and when the contingency occurs / the condition is satisfied. Accordingly by the express terms of Regulation 22 a contingent Agreement cannnot trigger the regulations until and unless the contingency has occurred and the agreement has become enforceable / capable of implementation, that SEBI has totally failed to consider this aspect whilst deciding that regulation 2 (1)(b) was attracted.

The Regulations did not envisage or permit a Public announcement / Public offer being made to the shareholders of the Target Company, contingent or conditional on the divestment of the non Eyewear business by the Target Company the only conditional offers envisaged / permitted under the Regulations, are an offer being made conditional to the receipt of statutory approvals, or an offer being made conditional to the receipt of a minimum level of acceptances by the shareholders. The Scheme & provision of the Regulations precludes any other Conditional Offer being made. Regulation 16(xvi) read with the proviso to regulation 22 (12) & Regulation 27(1)(b) which envisage and permit an offer being made conditional on receipt of statutory approvals for acquiring the shares, posit that an offer conditional/contingent on any other event/circumstance is neither envisaged nor permitted that (i)under Regulation 16(xvi) an offer can be made subject to receipt of statutory approvals if any required to be obtained for the purpose of acquiring the shares. (ii) the Proviso to Regulation 22(12) accordingly stipulates that time for completion of the public offer/payment can be extended by SEBI "due to non receipt of statutory approvals" (iii) regulation 27(1) stipulates that an offer once made shall not be withdrawn except where the statutory approvals required have been refused; or the sole acquirer has died. Accordingly if an offer is required to be made conditional to any other circumstance/event (for example the divestment of the Target Company’s Eyecare division) – under Regulation 27 it can not be withdrawn even if such contingent event does not occur, or if the condition is not satisfied. This would lead to the absurd situation that the acquirer would have to buy and retain the shares received through the public offer – even though the contingent triggering acquisition fails / does not go through. 27(1) (d) does stipulate that SEBI can permit withdrawal if "such circumstances as in the opinion of the Board merits withdrawal"; - that it is only an enabling discretionary power conferred on SEBI and confers no right on the person making the offer.

The rigid time frame stipulated under Regulation 22 for the completion of the offer and payment to the shareholders, necessarily excludes conditional or contingent offers being made – except for offers conditional on receipt of the requisite statutory approvals. Regulation 22 mandatorily requires a Public offer to be completed and payment to be made within 120 days of the public announcement (i.e. 60 days + 30 days + 30 days under Regulations 22(5), 22(6) & 22 (12). ) The Proviso to Regulation 22 (12) enables/empowers SEBI to grant extension of time only on the ground of "non receipt of requisite statutory approvals" Under the Regulations SEBI has no power to extend time, till occurrence of the contingent event or satisfaction of the precondition. This clearly rules out a public offer being made contingent/conditional on any event other than receipt of statutory approvals. Otherwise under Regulation 22(12) the acquirer would be required to complete the Public Offer & make payment to the shareholders, even if the contingency has not occurred, or the condition has not been satisfied. For example in the present case the contingency (divestment of the non Eyewear Business) had not occurred till Oct 2000 – yet if a contingent offer was mandated / envisaged under the Regulations, the Appellants would have been required to pay for and acquire the public shares within 120 days of April 1999 i.e. by August 1999 – even when they had no obligation to acquire the 44% shares of the Target Company from Bausch & Lomb Inc & its subsidiaries. Following observation from the Bhagwati Committee Report 2002 was referred to:

"The Committee was informed that currently the Regulations provide for making an offer conditional upon level of acceptance only .. .. .. The Committee felt that

pursuant to an acquisition under a MOU, the acquirer is required to make an offer to the public and hence such a public offer can not be conditional, unless of course the MOU itself is rescinded and not acted upon if the public offer does not elicit the requires acceptances"

Moreover requiring an offer to be made conditional upon the occurrence of an uncertain event even assuming whilst denying that such contingent offers are permitted by the Regulations, would result in considerable prejudice to the shareholders and practical difficulties. On the offer being made, shareholders desirous of accepting the offer would have to deposit their shares. However such shares would then remain blocked for an indeterminate period: i.e. till the uncertain contingent event occurred, or till its occurrence became impossible. In the meanwhile the shareholders would be deprived of their right to deal with/ sell their shares in the market. If the contingency event did not occur within the stipulated period (24 months in the present case) or became impossible of performance, the shareholders would then be required to take back their shares. As stated above such situation is not contemplated by the Regulations.

SEBI has not considered any of these aspects and has merely relied on the judgements of the Tribunal & the Hon’ble Bombay High Court in the case of BP Plc V SEBI (2001) 31 SCL 203 (SAT); (2001) 34 SCL (BOM)), to hold that all conditional offers are envisaged and permissible. The judgement of the Tribunal & the Hon’ble Bombay High Court in the case of BP Plc were restricted to a public offer being made conditionally on the receipt of statutory permissions and minimum acceptances from the shareholders. No other conditions were considered or dealt with in the BP Plc case. This is apparent from para 25 read with para 13 of the High Court judgement. Neither of these judgements deal with or support the proposition that an offer can be made contingent or conditionally on any other event (such as divestment of the non eyewear business in the present case.). Accordingly SEBI’s order that a public announcement / offer could have been made contingent/ conditional upon the divestment of the non eyewear business, receives no support from the decision of the Tribunal or the High Court.

It was submitted referring to the arguments in Reply, SEBI had orally sought to support the order on three grounds which are not to be found in the order: (i)that the Agreement dated 28

th April 1999

provided for unconditional /immediate acquisition of the stock of B & L South Asia Inc which held the 44% shares of the Target Company and accordingly triggered the Regulations (ii) the Agreement was not really conditional as the occurrence of the conditions even was within the control of the parties who were also entitled to waive performance thereof, and (iii) that having regard to Schedules 3.3(c) & 3.3(d) the Agreement dated 28

th April 1999 in effect provided for an immediate

acquisition with a provision of defeasance if the condition was not fulfilled. It is well settled that a quasi judicial order made by SEBI can only be sustained with reference to the reasons mentioned therein. Such a statutory order cannot be supplemented or sustained by reasons mentioned in the course of arguments. Moreover if an order of SEBI could be sustained on grounds not mentioned in the order it would render the Appellate Provisions negatory – as an appeal would necessarily be directed against the reasons stated in the order. Hon’ble Supreme Court’s decision in Mohinder Singh Gill V Chief Election Commissioner (AIR 1978 SC 851) was cited in support.

It was further submitted that even otherwise it is factually incorrect to allege that the Agreement dated 28

th April 1999 provided for unconditional/immediate acquisition of the stock of Bausch &

Lomb South Asia Inc which held the 44% shares of the Target Company. The Agreement provided for acquisition of only the 8 Transferred subsidiaries listed in Schedule 1.1.(b). The Agreement did not provide for the acquisition of the 34 Seller subsidiaries listed in Schedule 1.1.(a) and their stock. These 34 companies were to remain subsidiaries of Bausch & Lomb Inc and they/their shares were not to be transferred to the Appellants. Bausch & Lomb South Asia Inc which held the 44% shares of the Target Company is listed at SR No 4 of Schedule 1.1.(a). and was not agreed to be transferred to the Appellants. The reference to stock against Bausch & Lomb South Asia Inc is to be 44%

shares/stock of the Target Company which was held by Bausch & Lomb South Asia Inc & which was to be transferred to the Appellants on the divestment of the Eyecare Business. The submission that the Agreement was not really contingent or conditional (as the conditions could be waived by the Appellants) is contrary to the SEBI order, which in fact proceeds on the basis that the Appellants could have made a conditional offer. The pre-condition of divestment of the Eyecare / Contact lens business was imposed, as the Appellants had not agreed to acquire or pay for the Eyecare / contact lens business & assets and had agreed to acquire and pay only for the Eyewear / sunglasses business & assets. Accordingly there was no question of the Appellants being able to waive the pre-condition. The fact that Cause 6.4 of the Agreement provided that the seller could choose to waive the pre condition, is of no relevance in deciding the rights / obligations of the Buyer/Appellants. Moreover at no time did the seller grant such waiver – which would have resulted in the seller transferring the non Eyewear business & assets (i.e. the Eyecare business & assets) without having received any consideration for the same from the buyer / Appellants. The performance of the pre-condition was not within the control of Bausch & Lomb Inc even though its nominees controlled the Board of the Target Company. Disposal of the business of Eyecare required a resolution of the shareholders of the Target Company in general meeting and could not be done by a Board Resolution. Moreover B & L Inc through its subsidiaries, held only 44% of the shares of the Target Company and accordingly required the concurrence of the remaining 56% shareholders. Reference to Clause (g) of Schedule 3.3.(d) does not alter this position. Clause (g) of Schedule 3.3(d) only provides that if the Appellant decides to discontinue business in the deferred country, it can direct the Seller/Seller subsidiary concerned to dispose off the deferred shares and pay to it the net sale proceeds. However, in such a circumstance the Buyer/Appellant would not be acquiring the Deferred Shares i.e. the shares of the Target Company as they would be sold / disposed of to third parties by the Seller subsidiary & the Buyer / Appellants would only receive from the Seller subsidiaries, the net sale proceeds.

The Agreement dated 28th April 1999 read with Schedules 3.3 ( c) & 3.3.(d) thereto does not support

the allegation that there was an immediate sale / transfer of the shares/ assets with a right of defeasance if the conditions were not fulfilled. The Agreement and in particular clause 6.4 provided that the transaction for acquisition of the shares of the Target Company, would be closed only if and when the Target Company had divested its Eyecare business and further that if this divestment / closing did not occur within 24 months, the proposed transaction would be abandoned. In such event the Seller would have remained the owner of the said 44% shares of the Target Company. Clause 6.4 did make Schedules 3.3( c ) & (d) applicable to India. However, Schedule 3.3( c ) in fact expressly stipulated that during the deferral period the Seller would continue to hold the deferred shares and that the deposited price would be held in escrow until a closing occurred. Schedule 3.3(d) further provided that if the divestment / deferred closing did not take place within 18 months (modified to 24 months for India) the price which had been held in escrow would be refunded to the Buyer / Appellants albeit without interest. The fact that Clause (e) read with clause (e) (viii) of Schedule 3.3( c )did provide that during the deferral period the applicable Seller entity and the Deferred subsidiary would operate the business for the account of the Buyer – i.e. that the Seller entity owning the Deferred Shares would pay to the Buyer the net after tax distribution (dividend) received from the Deferred Subsidiary during the deferral period; - can not lead to the inference that there was an immediate transfer / sale with a right of defeasance. In fact such clauses are clearly inconsistent with an immediate transfer / sale. If there was in fact an immediate transfer / sale, the shares/ Deferred Subsidiary would have belonged to the Buyer who would ipso facto have been entitled to the business / profits/dividends. Clauses (e) (ii) and (e) (iv) of Schedule 3.3( c )which required the Buyer to enter into an agreement with the deferred subsidiary to continue to make available Intellectual Property and sunglasses / sunglass products available to the deferred subsidiary, during the deferral period / pending closing, also establish that there was no immediate sale/transfer. In fact the Technical Assistance Agreement dated 3

rd February 2000 entered into

between the Buyer/Luxottica SpA and the Target Company expressly provides that during the deferred period neither the Buyer/Luxottica SpA nor its subsidiaries "shall have or ever has had. any

role in either the day to day or the long term management of B & L India".

It was submitted that the acquisition of the said 44% shares of the Target Company on 27th October

2000 was pursuant to a scheme of merger of the two subsidiaries in Delaware USA, under the laws of Delaware USA and is accordingly exempted from regulations 10, 11 and 12 by virtue of the statutory exemption granted by regulation 3(1)(j)(ii): The Contingent Agreement dated 28

th April 1999

created no enforceable / binding obligation to acquire the said 44% shares of the Target Company until and unless the contingent event (i.e. the divestment of the non Eyewear Business and utilization of the sale proceeds to discharge the liabilities of the said non Eyewear Business) had occurred. Prior to the contingent event / pre-condition having occurred, the Parties by the Third amendment dated 3

rd February 2000 deleted and substituted Clause 6.4 of the Agreement and

provided that the said 44% shares of the Target Company which were held by Bausch & Lomb South Asia Inc would be transferred to a subsidiary which would be merged with a Buyer subsidiary in Delaware and under the laws of Delaware USA. The divestment of the non Eyewear Business was affected on 23

rd October 2000 and pursuant to Merger Agreement dated 27

th October 2000, the

said seller subsidiary holding the said 44% shares of the Target Company merged with the said buyer subsidiary in Delaware on 27

th October 2000 under the applicable laws of Delaware. In the

show cause notice, SEBI had only contended that the acquisition was not eligible for exemption under Regulation 3(1)(j)(ii), by virtue of Regulation 3 (1)(k) which stipulated that exemption thereunder would not be applicable if by virtue of a acquisition or change in control of any unlisted company whether in India or abroad, the acquirer acquires shares, or voting rights, or control of a listed company. In the order SEBI has neither referred to nor held the Appellant Buyer on this ground. The order however proceeds on the totally different ground and of which no notice or opportunity to show cause had been given; that exemption under Regulation 3 (1)(j)(ii) was not available as the Regulations had already been triggered on 28

th April 1999 and "any actions

subsequent to the triggering of the said Regulations will not have bearing on the making of an open offer by the acquirer as the said regulations have already been triggered" that the merger route had been devised by the acquirer as a device/artifice subsequently with the intention of circumventing the Regulations and avoiding making a public offer and was contrary to the spirit and policy of the Regulations. It was submitted that it was not open to SEBI to hold against the Appellants on a ground of which no reference was made/ notice was given in the show cause notice and in respect of which the Appellants had no opportunity of explaining, rebutting or showing case against. The order is accordingly vitiated by a failure to follow the fundamental principles of natural justice & fairplay.

It was further submitted that SEBI is not correct/ in holding that exemption under Regulation 3 (1)(j)(ii) was not available to the merger acquisition on 27

th October 2000 as the Regulations had

already been triggered on 28th

April 1999, as the Regulations were not triggered by the Contingent/Conditional Agreement dated 28

th April 1999 as a contingent agreement creates no

enforceable obligation and is not capable of implementation until and unless the contingent event had occurred / the pre-condition had been satisfied. Moreover on 3

rd February 2000 (i.e. when the

contingent event had not occurred and no obligation had attached) the parties had deleted / substituted clause 6.4 and provided for a merger of the Seller Subsidiary which held the 44% shares of the Target Company with the Buyer subsidiary. Pursuant thereto the merger took place on 27

th

October 2000. With reference to SEBI’s "denying" the exemption of 3(1)(j)(ii) on the ground that the merger route had been devised by the acquirer as a device / artifice subsequently with the intention of circumventing the Regulations and avoiding making a Public Offer and such a merger was contrary to the spirit and policy of the Regulations and placing reliance in this regard in the course of arguments on the judgement of the Hon’ble Supreme Court of India in the case of Mc Dowell Vs Sales Tax Officer (AIR 1986 SC 649). it was submitted that it is not open for SEBI to seek to deny a statutory exemption by referring to spirit and policy of the regulations. The plain language of Regulation 3 (1)(j)(ii) exempts from the operation of regulations 10,11, and 12 to acquisitions "pursuant to a scheme of .. .. merger .. .. under any law or regulation, Indian or foreign". Regulation 3

(1)(j)(ii) is a statutory exemption and if the express terms of the Regulation are satisfied SEBI can not seek to deny such statutory exemption by an administrative order. In this context this Tribunal’s decision in the case of Eaton Corporation Vs. SEBI (2001)33 SCL 326 (SAT) was referred to. In the present case the certificates issued by officials of the State of Delaware USA establish that the merger has taken place under the laws of Delaware USA. Accordingly SEBI cannot seek to deny exemption or contend that Regulations 10 & 12 are applicable. The plain language of Regulation 3(1)(j)(ii) confers the exemption if the condition stipulated therein is satisfied. The Regulation confers a statutory exemption and gives no jurisdiction / discretion on SEBI to refuse the exemption. Accordingly SEBI can not purport to deny the exemption once the conditions thereof are satisfied by reference to the alleged spirit or policy of the Regulations. The reference to the judgement in the case of Mc Dowell (supra) is misplaced. The judgement dealt with and is restricted to schemes for tax evasion. Moreover in that case the Tax Officer had jurisdiction to consider the question inasmuch as he was considering in assessment proceedings whether excise duty which was paid by the buyer under an arrangement with the seller could be included within the definition of turnover of the seller. In the present case there is no question of SEBI having jurisdiction to consider whether a merger duly carried out under the laws of Delaware USA was entitled to the exemption of 3(1)(j)(ii)or not. There is also no scope of restricting/limiting the scope of Regulation 3(1)(j)(ii) by a process of interpretation/ construction, inasmuch as the language of Regulation 3(1)(j)(ii) is plain and clear. Even if exemption of Regulation 3(1)(j)(ii) is denied, a public announcement and offer could only be directed to be made with reference to 23

rd October 2000 for the purpose of price and interest from

23rd

January 2001.

With reference to the direction to pay interest @ 15% per annum by way of compensation to the shareholders with effect from 27.8.1999 which, according to SEBI, is the alleged date on which the "offer process" would have been complete, it was submitted that assuming though without admitting, the worst position that the Appellant’s appeal is disallowed and the Appellant held to have been under obligation to have made a public announcement on 28.4.1999, the levy of interest @ 15% is without any basis for the reasons: that (i) the rate of 15% per annum is excessive, that the Hon’ble Supreme Court has held in Smt. Kushnuma Begum Vs. New India Insurance Co. Ltd., ((2001) 2 SCC 9) that where no rate of interest is specified, 9% per annum (which at that time was linked to the nationalised bank rate of interest for fixed deposit for one year) was considered reasonable compensation, that SEBI has itself on different occasions, where rate of interest is not specified by a particular Regulation, levied interest at different rates of 10%, 12% etc., that the rate of interest differs from time to time and currently it ranges from 5% to 7% on bank deposits for one year, which should have been the norm in this case also. Apart from the question of rate, interest should have been applied only in case of those shareholders who were shareholders on 28

th April 1999 (the date

on which according to SEBI, the public announcement should have been made) and continue to remain shareholders in an uninterrupted manner till today, and not to all shareholders who were shareholders at the time of the impugned order. This principle has now been settled by the Tribunal in Clariant International Ltd., V SEBI (2003)42 SCL 834 (SAT) Further, SEBI has also ignored the fact that even if an offer was to have been made by the Appellant pursuant to a public announcement in April, 1999, it would have had to be a conditional offer maturing with the sale of the Eyecare assets by the Target Company which ultimately took place on 23.10.2000 and therefore the shareholders could not have expected any money for their shares till that date and, as such the period from which interest could have been levied under such circumstances would only be effective from 23

rd October, 2000 and not earlier, that in the context the Counsel for SEBI had left the

question of the rate, the extent and the period of applicability of interest to the Tribunal, that it was submitted that the Tribunal may not direct to pay interest in the facts and circumstances, as the question of levy of interest does not arise as the Appellant had no obligation to make a Public Announcement under the Regulations.

Shri Rafique Dada, learned Senior Counsel appearing for the Respondent SEBI submitted that the main question for consideration in the present appeal is as to whether upon entering into the

Purchase Agreement on 24th April, 1999, the Acquirer (Luxotticca Group) had decided to acquire

44.152% of the shares of the Target Company. If the answer to the question is in the affirmative, then the 1997 Regulations are triggered and the subsequent merger of the entities on 27.10.2000 would not entitle the Acquirer to the automatic exemption under Regulation 3(1)(j)(ii). He submitted that in order to arrive at a conclusion as to whether Luxottica Group had decided to acquire the said 44.152% shares of the Target company, several factors need to be taken into consideration. Learned Senior Counsel submitted that the Purchase Agreement was entered into pursuant to the Luxottica Group being declared as the successful bidder at the auction held to sell the world wide Eyewear business of Bausch & Lomb Group. According to him the purchase Agreement merely provided the methodology by which what was purchased by the Luxottica Group at the said auction were to be transferred to it.

Luxottica Group had bid for and had purchased the worldwide Eyewear business of Bausch & Lomb Group. Bausch & Lomb Group could have taken only assets/liabilities relating to the Eyecare business carried on by the Target Company just as Luxottica group had agreed and had taken over assets and liabilities relating to Eyewear business of Bausch & Lomb in other countries. i.e. to say Eyewear business could have been spun off from other businesses carried on by the Target Company. Luxottica Group however agreed to take over 44.152% shares of the Target Company held by Bausch & Lomb South Asia Inc, a 100% subsidiary of Bausch & Lomb Inc.

It is not disputed that Bausch & Lomb Inc through its 100% subsidiary Bausch & Lomb South Asia Inc by reason of holding the said 44.152% shares of the Target Company had appointed all the six directors on the Board of the Target Company and was in control of the said company. Therefore Luxottica Group upon agreeing to acquire 44.152% shares would be entitled to exercise the same control over the Target Company. It was submitted that Luxottica Group by agreeing to acquire 44.152% of. the Target Company had triggered the Regulations. With reference to the Appellants’ claim that since purchase of the 44.152% shares in the Target Company by Luxottica Group was conditional upon the business as other than Eyewear business conducted by the Target Company being hive off/spun off and therefore by merely entering into the said agreement by itself would not trigger the said 1997 Regulations.

Learned Senior Counsel submitted that the so called condition precedent was not an impediment to Closure as both the parties to the Purchase Agreement were in a position to ensure that the said condition precedent was duly fulfilled as can be seen from the fact that the Target Company was a subsidiary of Bausch & Lomb South Asia Inc and it has been described as such in the Purchase Agreement, that all the six directors on the Board of the Target Company prior to and on the date of the said Purchase Agreement i.e. on 28-4-1999 were nominees of Bausch & Lomb Group, that Bausch & Lomb South Asia Inc by virtue of holding 44.152% of the capital stake of the Target Company exercises actual control of the Target Company. Since Bausch & Lomb South Asia Inc a 100% subsidiary of Bausch & Lomb Inc held 44.152% of the shares of the Target Company, Bausch & Lomb Group could get and in fact got the necessary Resolution passed for spinning off non Eyewear business of the Target Company. He submitted that the ground realities have to be taken into account.

Learned Senior Counsel referred to the recitals in the Purchase Agreement and submitted that from the recitals and the scheme of the Purchase Agreement it is clear that the Appellants had agreed to acquire the shares/control of the Target Company. He referred to the definition of the following expressions viz. Agreement, Baseline Date, Baseline Net Operating Assets, Business Assets, Closing Net Operating Assets, Purchase Price, Purchased Shares, Seller Entities and Transferred Subsidiaries, in the purchase Agreement.

Shri Rafique Dada, learned Senior Counsel, referred to the chronology of events and submitted that

prior to 28.4.1999, i.e. the date on which the Purchase Agreement was executed between the Parties, Bausch & Lomb Group held 44.152% shares in the paid up capital of the Target Company. An open auction was conducted by Bausch & Lomb Inc. for sale of business of production, marketing and distribution of sunglasses and spectacle frames and certain related accessories and the price was fixed with reference to the said business prior to entering into the Purchase Agreement. He submitted that U.S. Regulatory approval was obtained and "Killer Loop Transaction" referred to in Article 3.2(b) of the Agreement has been completed. According to the said Article the Appellant was required to purchase the Purchased Shares constituting all of the issued and outstanding shares (the Killer Loop Shares) of capital stock of Killer Loop SpA, an Italian corporation, also described as one of the Transferred subsidiaries, from Bausch & Lomb Group in consideration for the part payment of the purchase price and immediately thereafter the Killer Loop which by then would have become a subsidiary of the Appellant to purchase all the Purchased Assets and all of the remaining Purchased Shares etc. by paying the balance Purchase Price due. The Killer Loop transaction was completed on 6.6.1999. Therefore 6.6.1999 is the first Closing date. He submitted that the Purchase Agreement was subsequently amended thrice i.e. on 25.6.1999, 14.1.2000 and 3.2.2000. On 3.2.2000 a Technical Assistance Agreement between the Appellant No.1 and the Target Company was executed. On 5.6.2000 the Target company issued Notice of the general meeting to its shareholders for considering and approving the resolution for selling and transferring its Eyecare business to Bausch & Lomb Eyecare (India) P Ltd., a proposed Indian subsidiary of Bausch & Lomb South Asia Inc, in its general meeting on 21.7.2000 pursuant to section 293(1) of the Companies Act, 1956. On 21.7.2000 shareholders of the Target Company passed the resolution approving sale of the Eyecare business, that on 9.8.2000 the Target Company entered into an Agreement for the said sale with the said subsidiary of Bausch & Lomb Group, that on 23.10.2000 actual transfer of business of the Target Company other than that of the Eyewear took place. Thereafter on 27.10.2000, Merger Agreement between Bausch & Lomb Inc, Bausch & Lomb South Asia Holding Inc. and Luxottica Group SpA and Ray Ban Holdings Inc. was executed. On 30.10.2000, Board of Directors of the Target Company was reconstituted by appointing six directors of Luxottica Group on the Target Company’s Board. Learned Senior Counsel submitted that if there was no merger on 27.10.2000, the closing date would be 23.10.2000. According to Shri Dada on the executing of the Purchase Agreement dated 28.4.1999, the 1997 Regulations triggered and the Third amendment and the merger was only a device. In this context he pointed out that pursuant to the agreement reached at, 44.152% shares in the Target Company held by Bausch & Lomb South Asia Inc. was transferred to Bausch & Lomb Indian Holdings Inc which was subsidiary of Bausch & Lomb South Asia Holdings Inc. It was all part of the scheme emerging from the Purchase Agreement and the said Bausch & Lomb South Asia Holdings Inc merged with Ray Ban Holdings Inc. (Appellant No.2) and consequently Bausch & Lomb Indian Holdings Inc. became the subsidiary of the Appellant No.1 as well, and as a result 44.152% of the Target Company’s shares also got transferred to the Appellants group.

Learned Senior Counsel referred to the following material clauses in the Purchase Agreement and also the amendments thereto and submitted that Bausch & Lomb Inc, New York agreed to sell and the Luxottica Group agreed to buy for a total consideration of US$640,000,000- all world wide assets owned by Bausch & Lomb Inc. New York and its subsidiaries which are used exclusively in connection with the Eyewear business described in the Purchase Agreement, capital stock of certain subsidiaries of Bausch & Lomb Inc. based in different countries and engaged exclusively in the Eyewear business described in the Purchase Agreement and 44% capital stock owned by B&L South Asia Inc. a wholly owned subsidiary of Bausch & Lomb Inc. New York, in the Target Company. Total eight subsidiaries of Bausch & Lomb described as Transferred subsidiaries were identified for the purpose of transferring them to the Appellant No.1 that the Target Company was one of those eight Transferred subsidiaries shown in Schedule 1.1(b) of the Purchase Agreement. As per the Purchase Agreement, the entire exercise of transferring the identified subsidiaries was to be carried out in two stages i.e. in the first stage Killer Loop SpA, a subsidiary of Bausch & Lomb Group was to be transferred to Luxottica Group subject to fulfillment of certain conditions viz.

Regulatory approvals etc. and in the second stage, which was to happen only if first stage was complete, Killer Loop, which after becoming Luxottica Group’s subsidiary was to acquire other Transferred subsidiaries including 44% shares held by Bausch & Lomb South Asia Inc. in the Target Company.

He submitted that the conditions governing the Target Company were stipulated more specifically in Section 6.4 (Treatment of Bausch & Lomb India) stating that:

"(a) "Seller shall use commercially reasonable efforts to purchase from B & L India as soon as practicable all assets of B & L India which do not relate primarily to the Business (i.e. Eyewear business)and to cause B & L India to use the proceeds of such sale to satisfy any liabilities; which do not relate primarily to the Business. If such transactions have not been consummated prior to the Closing date, B & L India shall be treated as a deferred subsidiary pursuant to section 3.3. until such transactions have occurred and until there are no other circumstances that would cause B & L India to remain a deferred subsidiary; provided that (a) Seller may waive the condition that the sale transaction be consummated prior to a Deferred Closing (b) the period after which a transfer of the Purchased Shares of B & L India will be abandoned as contemplated by Schedule 3.3 (d) shall be twenty four (24) months and (c) any payments pursuant to schedules 3.3(c) and 3.3(d) shall be computed solely on the basis of the assets, liabilities and operations of B & L India which are primarily related to the Business, adjusted to take into account the applicable Sellers Entity’s partial ownership interest in Bausch & Lomb India."

He referred to clause (e)(vii) of Schedule 3.3( c ) on Treatment of Deferred Net Assets and Deferred subsidiaries during Deferred period. The clause is "in the case of Deferred Countries having Deferred Net Assets, as soon as practicable following the applicable Deferred Closing, each applicable Seller Entity shall pay to each applicable Buyer Entity, or each applicable Buyer Entity shall pay to each applicable Seller Entity, as the case may be, and shall deliver appropriate documentation with respect to, any after-tax income received from or after-tax losses incurred by the applicable Seller Entity with respect to the Business as operated in the Deferred Country so that, as between the Seller Entities and the Buyer Entities, the operations in the Deferred Country during the Deferred Period shall have been for the account of the applicable Buyer Entity on or after-tax basis."

He submitted that in terms of clause (g), the discretion is given to the Appellant buyer to elect to discontinue the Business in one or more of the Deferred Counties.

Learned Senior Counsel submitted that it is clear that it was decided that the Appellants would buy the Eye Wear business of the Target Company, that the conditions stipulated in the Agreement establishes this fact, that Bausch & Lomb was to run the business during the interim period, that it shows that the Appellants had acquired control. The agreement was to acquire shares and control, that the factum of control is clear from the clauses of the Agreement.

Learned Senior counsel submitted that Section 6.4 of the Agreement was amended as per Section 2.1 of the Third Amendment to the Purchase Agreement dated 3.2.2000 which read as follows:

"2.1 Sub section 6.4 (a) is hereby amended by deleting it in its entirely and inserting in lieu thereof the following:

(a)(i) Seller shall use commercially reasonable efforts to purchase as

soon as reasonably practicable from B & L India all assets of B&L India which do not relate primarily to the Business and to cause B&L India to use the proceeds of such sale to satisfy any liabilities which do not relate primarily to the Business (such transactions are hereinafter referred to, collectively as the "Spin off transactions"). By virtue of the fact that the Spin off transactions were not consummated prior to the Closing date, B&L India has been and shall be treated as a Deferred Subsidiary pursuant to Section 3.3 until the Spin off Transactions shall have occurred and until there are no other circumstances that would otherwise cause B&L India to remain a Deferred Subsidiary; provided that (a) the period after which a transfer of the Purchased Shares of B&L India will be abandoned as contemplated by Schedule 3.3 (d) shall be twenty four (24) months and (b) any payments pursuant to schedule 3.3 (c) and 3.3.(d) shall be computed solely on the basis of the assets, liabilities and operations of B&L India which are primarily related to Business, adjusted to take into account the Applicable Sellers entity’s partial ownership interests in B&L India. The Deferred Closing for B&L India shall be effectuated though a merger of certain subsidiaries of Buyer and Seller, as is set forth with greater particularity in Section 6.4(a) (ii) below.

(a)(ii) On or before March 1, 2000 or as soon as reasonably practicable thereafter, each of Seller and Buyer shall form a direct or indirect wholly owned subsidiary, each of which shall be organized under the laws of Delaware, USA. The subsidiary to be formed by Buyer is referred to herein as "Buyer Sub" and the subsidiary to be formed by Seller is referred to herein as "Seller Sub". On or before March 1, 2000, or as soon as reasonably practicable thereafter, Seller sub shall form a direct or indirect wholly owned subsidiary which shall be organized under the laws of Delaware, USA and is referred to herein as "Seller Sub 2". As soon as thereafter as practicable, Seller shall cause B&L South Asia, Inc. to transfer the Purchased Shares of Bausch & Lomb India to Seller Sub 2. Subject to section 6.4 (a) (iii) below, as promptly as practicable following the consummation of the Spin Off transactions, Seller and Buyer shall cause Seller Sub to be merged with and into Buyer Sub, which shall be the surviving corporation (the Indian Merger" and the date on which the Indian Merger is completed shall be the "Indian Closing Date"), pursuant to and in accordance with the scheme of merger under the applicable laws of the jurisdiction of incorporation of Buyer Sub and Seller Sub and the consummation of the Indian Merger shall constitute the Deferred Closing for Bausch & Lomb India for all purposes of this Agreement. As soon as reasonably practicable following the Indian Closing Date, Buyer shall use commercially reasonable efforts to cause the entity name of B&L India, Ltd to be changed so that the entity name does not retain or include any reference to Bausch & Lomb or any other trade name or trademark of Seller not transferred pursuant to the Agreement."

Learned Senior Counsel stated that it could be noticed that the manner of Closing of the Target Company by way of merger was first time stipulated as per the third amendment executed on 3

rd

February 2000.

The third amendment was admittedly made only pursuant to a legal opinion obtained on 28.1.2000.By the said amendment, the said alleged condition precedent i.e. spinning off non Eyewear business remained as a condition precedent and only the mode by which transfer of ownership of the said 44.152% shares of the Target Company held by Bausch & Lomb South Asia Inc were to be transferred to Luxottica Group was changed from normal ordinary transfer of shares from Bausch & Lomb South Asia Inc to a Luxottica Group Company to the merger route. The said merger was to be effected by Bausch & Lomb Group first by setting up two subsidiaries and Bausch & Lomb South Asia Inc transferring the said 44.152% shares to the 2nd of the new subsidiaries and by merger of the first of the 2 subsidiary with a subsidiary to be set up by Luxottica Group. This convoluted methodology for effecting simple transfer of shares from Bausch & Lomb Group to Luxottica Group was adopted only for the purpose of evading the compliance of 1997 Regulations and to make it difficult for SEBI to unravel and find out the breach of the said 1997 Regulations. He submitted that upon a plain reading of the relevant clauses of the Purchase Agreement as unamended by the 3

rd amendment, it is clear that upon entering into the said Agreement, Luxottica

group had acquired control of the Target Company and during the interregnum period, i.e. the period between the date of the agreement i.e. 24

th April 1999 and 22

nd October 2000 i.e. the date on which

condition precedent was fulfilled i.e. hiving off the non Eyewear business by the Target Company the business of the Target Company was to be carried on for and on behalf of Luxottica Group. Upon execution of the said Agreement control of the Target Company having passed from Bausch & Lomb Group to the Luxottica Group, there was change in control within the meaning of regulation 12 of 1997 Regulations.

He submitted that Hon’ble Supreme Court in Mc Dowell & Co. Ltd. v. Commercial Tax Officer AIR 1986 SC 649 had made it clear that use of sophisticated legal devices to avoid compliance of the legal requirement is not acceptable. He referred to the following observation:

"In our view the proper way to construe a statute, while considering a device to avoid tax, is not to ask whether the provisions should be construed literally or liberally, nor whether the transaction is not unreal and not prohibited by the statute, but whether the transaction is a device to avoid tax, and whether the transaction is such that the judicial process may accord its approval to it. A hint of this approach is to be founded in the judgement of Desai, J.. in Wood Polymer Ltd. and Bengal Hotels Limited, (1977) 47 Com Cas 597 (Guj) where the learned Judge refused to accord sanction to the amalgamation of companies as it would lead to avoidance of tax. It is neither fair not desirable to expect the legislature to intervene and take care of every device and scheme to avoid taxation. It is up to the Court to take stock to determine the nature of the new and sophisticated legal devices to avoid tax and consider whether the situation created by the devices could be related to the existing legislation with the aid of ‘emerging’ techniques of interpretation was done in Ramsay (1982) AC 300) Burma Oil (1982 STC 30) and Dawson 1984-1 All ER 530), to expose the devices for what they really are and to refuse to give judicial benediction"

Shri Dada submitted that even though the said observation was made in the context of avoidance of tax, the principle laid down therein is in equal force applicable to the Appellants’ case also as it had a device brought in to avoid compliance of the provisions of the Takeover Regulations.

Learned Senior Counsel submitted that a Technical Assistance Agreement was also entered into on 3

rd February 2000. Section 16 of the said Technical Assistance Agreement provided that: "16.1This

Agreement provides a framework whereby Bausch & Lomb India may request such Technical Assistance and provide such Business Information as Bausch & Lomb India regards, in its sole and

absolute discretion, to best enhance its corporate objectives. Bausch & Lomb India shall have no obligation, whether as a consequence of this Agreement or otherwise, to request or to follow or utilize any Technical Assistance that Luxottica may provide. 16.2. The parties acknowledge and agree that whether as a consequence of this Agreement or otherwise, neither Luxottica nor any of its subsidiaries or affiliates, including, without limitation, any individual who may provide Technical Assistance hereunder, shall have, or even has had, any role in either the day to day or the long term management of Bausch & Lomb India."

Learned Senior Counsel submitted that from the said clauses it is clear that under the Purchase Agreement the Appellants had decided to acquire 44.152% shares of the Target Company and thereafter a scheme was devised with a view to keep the acquisition out of the purview of the Regulations. With this objective amendments were made to the Purchase Agreement, that the first amendment was made on 25

th June 1999, the second one on 14

th January 2000 and the third one

on 3rd

February 2000. He submitted that as per the Appellants’ version the third amendment was made pursuant to an opinion received on 28

th January 2000 by them from their Counsel advising to

enter into an arrangement of merger so as to avoid the risk of making a public offer before acquiring 44.152% shares of the said Target Company. Pursuant to such legal advice a strategy was planned by the Parties to the Agreement. The first step towards such strategy was the incorporation of a company known as Ray Ban Sun Optics Inc. USA, by the Appellants. This was followed by the hiving off all the business of the Target Company except the Eyewear business on 23

rd October

2000. Four days later, that is on 27th October 2000, a merger agreement was entered into between

the Bausch & Lomb South Asia Holdings Inc and Ray Ban Sun Optics Inc USA pursuant to which these two entities merged and in this way the 44.152% shares of the Target Company were acquired by the Appellants. In para 5.2 of the said Merger Agreement it has been provided that:

"Section 5.2 Substitution of Bausch & Lomb India Directors. The parties hereto confirm to each other that they will use their respective best efforts to cooperate with respect to a meeting of the Board of Directors of B&L India currently intended to be held on October 30, 2000, or as soon thereafter as is possible, at which the current directors of B&L India shall resign and shall be replaced by directors designated by Buyer, with such resignations and appointments to occur in a manner and pursuant to such resignations and other documents as shall be agreed upon by the parties respective Indian Counsel."

Learned Senior Counsel pointed out that on the Board of the Target Company prior to the merger (before 29

th October 2000) there were 6 Directors of Bausch & Lomb Group, that after the merger

(after 30th October 2000) 6 Directors of the Luxottica Group replaced them.

He submitted that it is clear from the Purchase Agreement that the Appellant No 1 had decided to acquire 44.152% shares of the Target Company. Immediately upon such merger getting fructified there was, as aforesaid, a change in the management of the Target Company by including six Directors of the Appellant on the Board of the Target Company. From the actions on the part of the Appellants commencing from 28

th April 1999 it is clear that a decision was arrived at to acquire the

44.152% shares of the Target company, that the modus operandi was changed from purchase to merger only with a view to circumvent the Regulations as per the subsequent legal advice received by them.

Learned Senior Counsel also cited Article 7 which stipulates the ‘Condition precedent ‘ and Article 9 which is on "Termination of the Agreement".

It was submitted that the first amendment is relevant as the same was effected after the first Closing Date and after receipt of U.S. Regulatory Approvals which were obtained on 6.6.1999 whereby what

was agreed between the Parties to happen upon the US Regulatory Approvals being obtained were incorporated.

It was submitted that upon reading of Regulation 2(1)(b) i.e. definition of "acquirer" Regulation 2(1) (c) i.e. definition of "control" and Regulation 10 relating to acquisition of 15% or more shares or voting rights, together with explanation of Regulation 11 and Regulation 12 relating to acquisition of control and the provisions of Regulation 14(1) and 14(3) relating to public announcement, it is clear that 1997 Regulation can be triggered even by person (i) agreeing to purchase shares of the Target Company above the limits prescribed and/or (ii) agreeing to acquire control of a target company (iii) and/or agreeing to acquire a holding company or companies which are listed or unlisted in India or abroad.

He cited the Tribunal’s decision in B.P.Amoco V SEBI (2001) 31 SCL 203 and also the Hon’ble Bombay High Court’s decision in the appeal against the said order (2001) 34 SCL 469, that the Hon’ble High Court upholding the Tribunal’s order in the matter had stated that:

"it is very clear that even someone who "agrees to acquire shares or voting rights" or agrees to acquire control over the target company" would come within the definition of ‘acquirer’. Therefore it is explicitly apparent and clear that the word ‘acquirer’ would not only means that those who have already acquired shares and also those ‘who agree to acquire shares’ or agree to acquire control over the target company’."

Learned Senior Counsel also cited the following portion from the Tribunal’s order in B.P. Amoco V SEBI (2001) 31 SCL 203.

"On a perusal of regulation 14 it is clear that a public announcement is required to be made not later than four working days after any change or changes decided to be made, as would result in any acquisition of control over the target company. On a plain reading of regulation 14 (3) it is difficult to agree with the view that the term ‘change or changes decided to be made’ must be read in the light of regulation 12 and be construed so as to mean decision taken for such changes, as would result in the acquisition of control of the target company. The word ‘would’ used in regulation 14 (3) conveys that what the said regulation is concerned with is the likely acquisition of control and not the actually effected acquisition of control. The word ‘would’ in the context need be understood in its literary sense as ‘expressing probability’. Thus when appellant No.1 announced its intention to acquire the shares of Burma Castrol on 14-3-2000, the announcement constituted an intention to acquire, albeit, indirectly the control over all its subsidiary companies including the Indian subsidiary viz. Castrol (India) Ltd. on the same day itself i.e. 14-3-2000."

This view was confirmed by the Hon’ble Bombay High court in appeal filed by B. P. Amoco (2001) 34 SCL 46.

Once the 1997 Regulations are triggered the acquirer has to make a public announcement as per regulation 14, that making of public announcement is a requirement that has to be fulfilled before taking over control/acquisition of shares or voting rights beyond the prescribed limit. The purpose of making a public announcement is to make public and the share holders of the Target company aware of the substantial acquisition of shares or impending change in the management or control on take over of the target company or acquisition of shares above the prescribed limit. Once the 1997 Regulations are triggered the acquirer has to make public announcement as per the regulations within 4 days and is thereafter required to follow that provisions of the Regulations and failure to do so would be visited with penal action under regulation 45 and section 15(H) of SEBI Act. In the facts

of the present case, 1997 Regulations were triggered upon execution of the Purchase Agreement on 28