before the maharashtra electricity regulatory commission 58 42/order-110 of 2016-19072017.pdf ·...

TRANSCRIPT

MERC Order_ Case No 110 of 2016 Page 1

Before the

MAHARASHTRA ELECTRICITY REGULATORY COMMISSION

13th

Floor, Centre No.1, World Trade Centre, Cuffe Parade, Mumbai - 400 005

Tel: 022-22163964/65/69 Fax: 022-22163976

E-mail: [email protected]

Website: www.merc.gov.in / www.mercindia.org.in

CASE No. 110 of 2016

In the matter of

Petition of Tata Power Co. Ltd. (Transmission) for review of Multi-Year Tariff Order

dated 30.6.2016 in Case No. 22 of 2016

Coram

Shri. Azeez M. Khan, Member

Shri. Deepak Lad, Member

The Tata Power Company Limited (Transmission) ……Petitioner

Appearance:

For Petitioner 1) Shri Amit Kapur (Adv.)

2) Smt. Swati Mehendale

ORDER

Dated: 19 July, 2017

1. M/s Tata Power Co. Ltd. (Transmission) (TPC-T), Bombay House, 24, Homi Mody

Street, Fort, Mumbai, filed a Petition on 8 August, 2016 under Section 85 of the MERC

(Conduct of Business) Regulations, 2004 for review of the Commission’s Multi-Year

Tariff (MYT) Order dated 30 June, 2016 in Case No. 22 of 2016. Thereafter, TPC-T filed

an amended Petition on 26 August, 2016 adding certain issues for review.

2. In its original Petition, TPC-T had only sought as follows:

“…b. Approve the Number of Bays for FY 2014-15 as presented in the instant

review petition and allow the impact of Rs 1.53croreon O&M entitlement and also

to consider the corresponding impact on interest on working capital arising out of

the same…”

In its Revised Petition, TPC-T’s prayers are as follows:

MERC Order_ Case No 110 of 2016 Page 2

“…b. Allow Interest During Construction of Rs. 21.74 crore for a period FY 2008-

09 to FY 2011-12 for Bandra Kurla Complex land;

c. Allow Capitalisation of Rs. 26.54 crore as against the Scheme of 110/33kV sub-

station at Ixora, Panvel;

d. Allow Capitalisation of Rs. 1.83 crore towards 8 Bays of 33kV at Parel for FY

2014-15;

e. Consider number of Bays commissioned at Ixora and Parel Receiving Stations

while computing O&M expenses applicable for FY 2014-15;

f. Allow O&M entitlement on Bays which are commissioned and capitalised but

unutilised for FY 2014-15;

g. Correct the opening and addition of number of Bays for FY 2014-15 on account

of error in the consideration of Ixora Bays and allow the impact of Rs 1.53 crore

on O&M entitlement and also to consider the corresponding impact on interest on

working capital arising out of the same;

h. Allow additional fixed charges on account of prayer (b) to (f) above;…”

3. In its original Petition, TPC-T had stated that-

3.1. The Commission has erred in not considering the number of Bays

commissioned at Ixora Receiving Station in Panvel while computing the normative

O&M expenses for FY 2014-15. A total of 35 Bays (8 Bays between 66 kV and 400 kV

and 27 Bays below 66 kV) were deducted from the opening balance of the number of

Bays of FY 2014-15 as approved in the provisional Truing Up of FY 2014-15 in the

Mid-Term Review (MTR) Order dated 26 June, 2015 in Case No. 5 of 2015 to arrive at

the opening balance of FY 2014-15.

3.2. The Ixora Receiving Station was commissioned in FY 2013-14, and its

capitalisation was claimed by TPC-T in the Truing up of FY 2013-14. However, the

corresponding number of Bays had been included in the addition of FY 2014-15 in the

current Petition and not in the opening balance of FY 2014-15. The capitalisation and

addition of Bays were disallowed in FY 2013-14 in the MTR Order.

3.3. Consequently, the Ixora Bays were required to be removed from the Bay

additions of FY 2014-15. The correct representation of Bays for FY 2014-15 is as

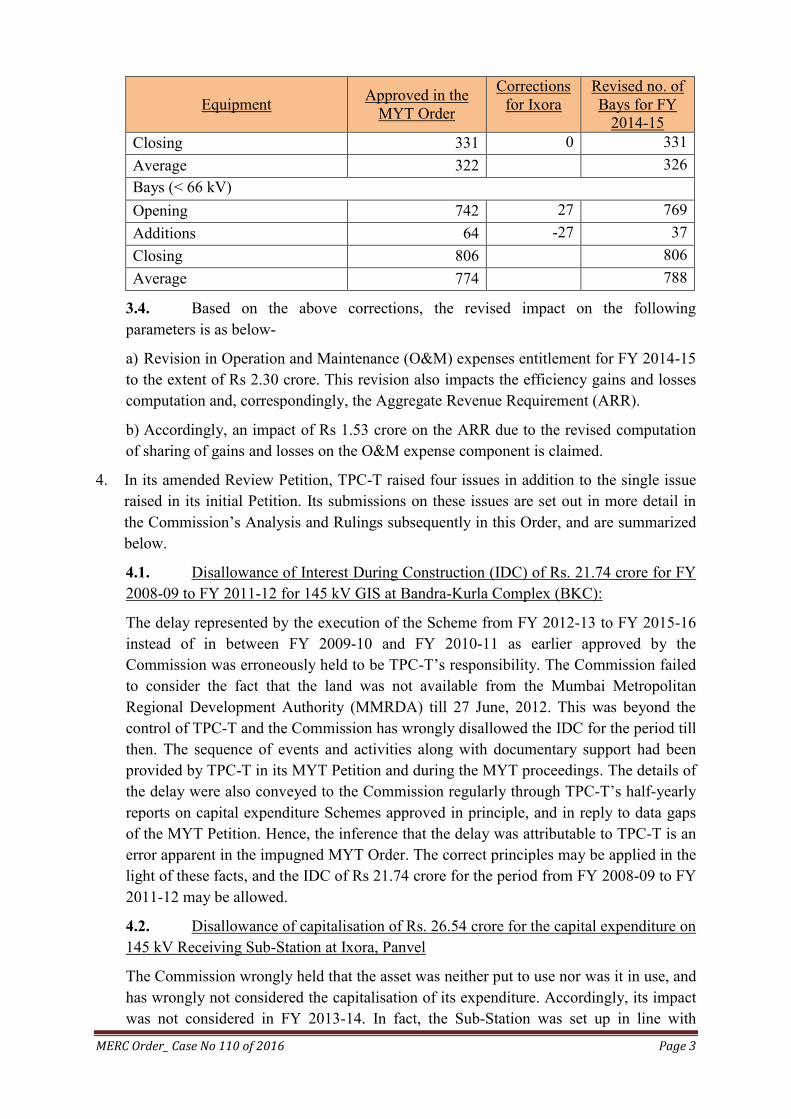

follows:-

Table 1: Break-up of approved capital cost of 145 kV GIS Sub-Station Scheme at BKC

Equipment Approved in the

MYT Order

Corrections

for Ixora

Revised no. of

Bays for FY

2014-15

Bays (between 66 kV and 400 kV)

Opening 312 8 320

Additions 19 -8 11

MERC Order_ Case No 110 of 2016 Page 3

Equipment Approved in the

MYT Order

Corrections

for Ixora

Revised no. of

Bays for FY

2014-15

Closing 331 0 331

Average 322 326

Bays (< 66 kV)

Opening 742 27 769

Additions 64 -27 37

Closing 806 806

Average 774 788

3.4. Based on the above corrections, the revised impact on the following

parameters is as below-

a) Revision in Operation and Maintenance (O&M) expenses entitlement for FY 2014-15

to the extent of Rs 2.30 crore. This revision also impacts the efficiency gains and losses

computation and, correspondingly, the Aggregate Revenue Requirement (ARR).

b) Accordingly, an impact of Rs 1.53 crore on the ARR due to the revised computation

of sharing of gains and losses on the O&M expense component is claimed.

4. In its amended Review Petition, TPC-T raised four issues in addition to the single issue

raised in its initial Petition. Its submissions on these issues are set out in more detail in

the Commission’s Analysis and Rulings subsequently in this Order, and are summarized

below.

4.1. Disallowance of Interest During Construction (IDC) of Rs. 21.74 crore for FY

2008-09 to FY 2011-12 for 145 kV GIS at Bandra-Kurla Complex (BKC):

The delay represented by the execution of the Scheme from FY 2012-13 to FY 2015-16

instead of in between FY 2009-10 and FY 2010-11 as earlier approved by the

Commission was erroneously held to be TPC-T’s responsibility. The Commission failed

to consider the fact that the land was not available from the Mumbai Metropolitan

Regional Development Authority (MMRDA) till 27 June, 2012. This was beyond the

control of TPC-T and the Commission has wrongly disallowed the IDC for the period till

then. The sequence of events and activities along with documentary support had been

provided by TPC-T in its MYT Petition and during the MYT proceedings. The details of

the delay were also conveyed to the Commission regularly through TPC-T’s half-yearly

reports on capital expenditure Schemes approved in principle, and in reply to data gaps

of the MYT Petition. Hence, the inference that the delay was attributable to TPC-T is an

error apparent in the impugned MYT Order. The correct principles may be applied in the

light of these facts, and the IDC of Rs 21.74 crore for the period from FY 2008-09 to FY

2011-12 may be allowed.

4.2. Disallowance of capitalisation of Rs. 26.54 crore for the capital expenditure on

145 kV Receiving Sub-Station at Ixora, Panvel

The Commission wrongly held that the asset was neither put to use nor was it in use, and

has wrongly not considered the capitalisation of its expenditure. Accordingly, its impact

was not considered in FY 2013-14. In fact, the Sub-Station was set up in line with

MERC Order_ Case No 110 of 2016 Page 4

Clause 5.3.2 of the National Electricity Policy, 2005 and Regulation 8 of the State Grid

Code, and pursuant to the approval given by the Commission and the State Transmission

Utility (STU). The Project is entirely based on the requirement of the Deemed

Distribution Licensee, and TPC-T cannot be held responsible till the time the load is not

required by that Licensee. The sequence of events and the correspondence with Ixora

Construction Pvt. Ltd. (‘Ixora Construction’) regarding the requirement of the Sub-

Station as also the corresponding approvals were set out in the MYT Petition.

4.3. Disallowance of capitalisation towards 8 Air-Insulated Sub-Station (AIS) Bays

of 33 kV at Parel for FY 2014-15

The Commission erred in not allowing capitalisation towards 8 Bays of 33 kV at Parel

for FY 2014-15, and wrongly held that these Bays have been idle since commissioning

in FY 2014-15. In fact, these Bays have been “put in use” since commissioning since

they are fully charged, and the Transmission Licensee cannot be penalised for the

inefficiency of the Distribution Licensees for failing to get the cable connected to the

source. The details of events with reference to the correspondence with the STU for

approval to the Scheme, allotment of Bays to the Distribution Licensees, etc. had been

set out. The Project is entirely based on the requirement of the Distribution Licensees

and was completed after taking due approvals. Disallowing capitalisation of these Bays

will deprive TPC-T of its legitimate expenses and is unjust. Capitalisation of Rs 1.83

crore with regard to these Bays may be allowed along with its impact on Fixed Charges.

4.4. Disallowance of O&M Entitlement on unutilised Bays for FY 2014-15 of Rs.

10.66 crore

The Commission has wrongly held that the O&M expenditure on the Bays which are

not in use cannot be allowed. O&M expense entitlement for 91 Bays (at <66 kV and >66

kV voltage levels) has been disallowed, with disallowance on 57 Bays on the principle

of asset not put to use (which includes 31 Bays of Ixora) and 34 Bays on the principle

that these Bays are capitalised but unutilised by the Beneficiaries. Regulation 65.1 of the

MYT Regulations, 2011 relating to O&M expenses does not provide for disallowance if

the asset is not in use after capitalisation. The concept of disallowing capitalisation on

the ground of ‘not put to use’ or ‘not in use’ is provided in Regulation 27.1 of MYT

Regulations, 2011 which has nothing to do with O&M expenses. Once the Bays are

capitalised, these Bays are in a charged condition though not connected, and are required

to be maintained to prevent any failure. The major maintenance activities includes

monitoring of SF6 levels, checking of operating mechanisms, topping up SF6 in case of

low gas level, and periodic testing of the breakers to ensure desired performance. Details

of these Bays were provided, and their status was reported to the Commission on a

regular basis and in reply to data gaps raised on the MYT Petition.

5. At the hearing held on 27 December, 2016, TPC-T made a presentation on the issues

raised in the Review Petition. The proceedings are summarized below.

5.1 Issue No.1: Disallowance of IDC for 145 kV GIS at BKC of Rs. 21.74 crore for the

period from FY 2008-09 to FY 2011-12

MERC Order_ Case No 110 of 2016 Page 5

TPC-T contended that the Commission has wrongly held that it is responsible for the

delay by commencing the 145 kV GIS BKC Scheme only in FY 2012-13 and

commissioning it in FY 2015-16 as against the approved schedule of FY 2009-10 to

FY 2010-11. The Commission did not consider the fact that the land possession was

not available from MMRDA till 27 June, 2012. The status of the Scheme was

regularly communicated through half-yearly reports to the Commission. This issue of

delay in acquiring land was not fully clarified in the impugned MYT Order. TPC-T

has submitted the chronology of events to show that the delay of around four years in

obtaining land from MMRDA was beyond its control and that, therefore,

disallowance of IDC for that period is not correct. The Appellate Tribunal for

Electricity (ATE), in its Judgment in Power Co. of Karnataka Vs CERC dated 15

May, 2015, has held that delays by Government agencies in handing over possession

of land constitutes force majeure. TPC-T has set out the various stages with the time

that MMRDA has taken in the process of final allotment and possession of land.

Issue No. 2: Disallowance of capitalisation of Rs. 26.54 crore of 145 kV Sub-Station

at Ixora, Panvel

The capitalisation was disallowed in the impugned Order stating that the asset was not

put to use. The Scheme was executed subsequent to approval from STU and the

Commission. The Receiving Sub-Station and Bays are completed and energised since

18 February, 2015. The SEZ Co-Developer, Ixora Construction, a Deemed

Distribution Licensee, is not using the system because of its own delay. The

Transmission Licensee cannot be penalised for non-utilisation of the asset by the

Distribution Licensee.

The Commission asked TPC-T whether it had executed a Connection Agreement and

/or Bulk Power Transmission Agreement (BPTA) with Ixora Construction. TPC-T

replied that it had not executed a Connection Agreement due to Ixora Construction’s

disputes with other parties. However, TPC-T sought for examining the issues of

Connection Agreement and BPTA with Ixora Construction and filing an additional

submission.

Issue No.3: Disallowance of capitalisation of Rs. 1.83 crore for 8 33 kV Bays at Parel

Receiving Station

The Commission has disallowed this capitalisation, holding that these Bays have been

idle since commissioning in FY 2014-15. TPC-T has commissioned and charged these

Bays and they are ready to use. However, the Beneficiaries (TPC (Distribution) (TPC-

D) and Brihanmumbai Electric Supply and Transport Undertaking (BEST)) have

failed to utilize the Bays, which is beyond the control of TPC-T. The Scheme has

been executed subsequent to approval of STU and the Commission.

To the Commission’s query as to whether it had executed a Connection Agreement

and /or BPTA with BEST and TPC-D as envisaged under the State Grid Code, TPC-T

replied that it had not done so. The Commission also asked whether TPC-T had

approached the Grid Co-ordination Committee (GCC) set up under the State Grid

Code for utilization of its commissioned transmission infrastructure by its

Beneficiaries. TPC-T replied that there is a mechanism under Section 39(2) of the EA,

MERC Order_ Case No 110 of 2016 Page 6

2003 and State Grid Code for co-ordination relating to the Intra-State Transmission

System (InSTS), but it is wanting in implementation. However, it would file its

additional submission after examining the Connection Agreement and BPTA issues.

Issue No. 4: Disallowance of O&M expenses of Rs.10.66 crore towards unutilised

Bays

The Commission has disallowed the O&M expenditure of Rs 10.66 crore for 91 Bays

(at <66 kV and >66 kV voltage levels) which are not in use. Out of 91 Bays, 57 Bays

are disallowed because they are not put to use, and 34 Bays on the ground that they

are capitalised but remain unutilised by the Beneficiaries. The disallowed Bays are

already capitalised, but were not utilised by the Distribution Licensees to cater to their

load. These Bays are kept in charged condition and are required to be maintained to

prevent any failure. Regulation 61.5 of the MYT Regulations, 2011 allows normative

O &M expenses for all Bays in the Transmission Sub-Station of a Transmission

Licensee, excluding only the Bays maintained by Generators. Hence, TPC-T’s O & M

expenses entitlement for FY 2014-15 corresponding to 77 Bays may be approved.

Issue No.5: Error while considering the Bays commissioned at 145 kV Ixora

Receiving Sub-Station while computing the normative O&M expenses for FY 2014-

15

TPC-T had included 35 Bays at Ixora Sub-Station in the addition of Bays during FY

2014-15 in its MYT Petition to derive the normative O & M expenses. The

Commission had disallowed the capitalisation in FY 2013-14 towards the Ixora Sub-

Station, and consequently not considered these Bays while calculating O & M

expenses. While calculating normative O & M expenditure, these 35 Bays were

deducted from the opening balance of FY 2014-15 instead of deducting them from the

addition of Bays for FY 2014-15. This is an arithmetic error which needs to be

rectified.

5.2 The Commission gave TPC-T a week to file its additional submissions, and the

matter was reserved for orders.

6. TPC-T’s additional written submission dated 17 January, 2017 is summarized as below:

6.1. The Connection Agreement was not signed since Ixora Construction is not

ready with the necessary information required to be entered in the Agreement. The

responsibility of signing the Connection Agreement is that of both TPC-T and Ixora

Construction, as will be seen from Regulation 14 of the State Grid Code. The sequence

of events is set out along with documentary support. Inspite of the STU’s direction to

Ixora Construction to execute the Connection Agreement, it remained un-executed as the

work was not completed by Ixora Construction. Further, a BPTA is signed at the time of

allotment of long-term Transmission Capacity Rights (TCR) to the Transmission System

User (TSU), and is granted by the STU on a Long-term Open Access (LTOA)

application by the TSU. The Transmission Licensee is only a party to the BPTA and not

the initiator. During the establishment of the Receiving Sub-Station, there was no

indication from either the STU or from Ixora Construction with regard to any delay in

the requirement or for a change in the schedule. In the absence of a specific application

MERC Order_ Case No 110 of 2016 Page 7

for surrender of capacity under Regulation 9 of the MERC (Transmission Open Access)

Regulations, 2016 (‘TOA Regulations’), TPC-T was committed to establishing the

Receiving Sub-Station. Although no written record is available about having raised the

issue at the GCC, TPC-T had informed the STU about the readiness of the Receiving

Sub-Station in advance and also followed up with the STU for allocation of the outlets in

writing, and has now enclosed copies of the correspondence. However, there was no

response from the STU.

6.2. As regards the disallowance of 8 AIS Bays at Parel, the Connection

Agreement has not been signed as the Distribution Licensees are not ready with the

necessary information to be filled in the Agreement as per Regulations 13 and 14 of the

State Grid Code. The sequence of events has been submitted, including the details of

Connection Application made by the Distribution Licensees, i.e., BEST and TPC-D. A

BPTA is signed at the time of allotment of long-term TCR to the TSUs based on the

LTOA applications and is granted by the STU. The role of the Transmission Licensee is

to be a party to the BPTA as the TSU is connected to its Transmission System. BPTA

initiation is the responsibility of the TSU.

Commission’s Analysis and Rulings

7. Issue 1: Disallowance of IDC of Rs. 21.74 crore for 145 kV GIS Sub-Station at

Bandra-Kurla Complex for FY 2008-09 to FY 2011-12

TPC-T’s Submission

7.1. The Commission erroneously held that the long delay in this Scheme was

attributable to TPC-T inasmuch as it was actually undertaken from FY 2012-13 to

FY 2015-16 as against the approved execution period of FY 2009-10 to FY 2010-11.

The Commission did not consider the fact that was not available from MMRDA

till 27 June, 2012. As such, this delay was beyond the control of TPC-T, as will be

seen from the details set out below, and the Commission wrongly disallowed IDC

for the corresponding period.

7.2. The Commission erred in not considering the following events that led to

the delay, which were not attributable to TPC-T:

(a) A DPR for the Scheme with an estimated cost of Rs. 129.67 crore

was submitted on 14 March, 2007, and was approved in principle by the

Commission vide letter dated 24 April, 2007.

(b) Expecting BKC to be a high load growth area and the demand

likely to go up by 100 MVA, on 21 January, 2008 TPC-T submitted a

revised DPR to establish a 110/33kV Sub-Station at BKC instead of 22 kV

and 11 kV, with an estimated cost of Rs. 230.50 crore. The Commission

gave in-principle approval for establishing a 145 kV GIS Sub-Station on 9

May, 2008.

(c) On 8 October, 2008, MMRDA offered a plot to TPC-T for a

Receiving Sub-Station on a temporary basis as initially the 110 kV GIS

MERC Order_ Case No 110 of 2016 Page 8

based Station was planned to be commissioned on leased land. At TPC-

T’s request, MMRDA agreed in December, 2008 to convert the temporary

lease to a permanent lease of 80 years.

(d) TPC-T paid Rs. 86. 11 crore as the lease premium on 29 January,

2009 and signed a Lease Deed with MMRDA on 12 March, 2009.

However, MMRDA could not hand over the entire plot to it for the

following reasons:

(i) Part of the plot was encroached upon by the adjoining plot

and holder;

(ii) Re-profiling of the plot was under process due to the

proposed widening of the road by MMRDA; and

(iii) MMRDA also decided to develop a Food Court in the

adjacent Recreation Ground (RG) plot.

(e) After constant follow-up with MMRDA, an alternative adjacent

plot was identified for the new Sub-Station. TPC-T requested MMRDA

for swapping of plots, which was approved after more than a year, on 19

December, 2011. The modified Lease Deed was executed on 1 June, 2012

and Commencement Certificate upto plinth level for the proposed Sub-

Station was issued by MMRDA.

(f) The GIS Building work started on 28 December, 2012, after

getting a Commencement Certificate from the Municipal Corporation of

Greater Mumbai (MCGM), and the Receiving Station was commissioned

in March, 2015. The Mumbai Region Electrical Circle (MREC) gave

provisional permission for charging the 145 kV BKC Receiving Station on

23 April, 2015.

7.3. In the above circumstances, the Commission’s observation that no work

was done till FY 2011-12 is incorrect, and the delay is not attributable to TPC-T.

Moreover, the status of the Scheme was reported to the Commission from time to

time as follows:

(a) Progress reports dated 29 June and 15 December, 2010, 2 August,

2011, 28 December, 2012, 10 December, 2013, 16 June 2014, 23 January

and 24 November, 2015.

(b) Response to data gap queries on the MYT Petition, the details of

which have been re-iterated in the present Review Petition.

7.4. TPC-T has acted in pursuance of the in-principle approval granted by the

Commission for this Scheme and created the asset accordingly in order to meet

MERC Order_ Case No 110 of 2016 Page 9

load growth, strengthen the existing system, increase efficiency, meet statutory

requirements, etc. All efforts were made to procure land, but the delay by

MMRDA was beyond TPC-T’s control. TPC-T has also referred to the ATE

Judgment dated 15 May 2015 in Appeal No. 108 of 2015 in support of its

contention.

Commission’s Analysis and Ruling

7.5. The comparison of the capital expenditure on the components of the

revised DPR approved in principle and that claimed by TPC-T is as below:

Table 2: Break-up of Approved and Claimed Capital Cost of 145 kV GIS Sub-Station

Scheme at BKC

Sr.

No. Particulars

DPR

approved

(Rs.

Crore)

TPC-T

claimed (Rs.

Crore)

Remarks

A Hard Cost

i Land 140.00 95.00

ii Other Sub-Station electrical

equipment excluding GIS 23.60

25.90

iii 145kV GIS with accessories 18.00 19.06

iv 33kV GIS with accessories 12.16 12.80

v

110 kV Power cable with

accessories 5.75

22.14 Change in cable route

due to MMRDA

requirements

vi Cable related civil jobs &

services

4.77

vii Civil and related works 4.60 28.83

viii Consultancy services 1.00 1.55

ix Contingency 5.75

x Staff cost

5.43

xi Others

3.00

Sub-Total 210.86 218.49

B Soft Cost

i

IDC

IDC against

Land

19.64

42.92 Additional IDC

against land cost

ii IDC against

equipment

12.01

Sub-Total 19.64 54.93

Grand Total 230.50 273.42

7.6. From the comparison above, it will be seen that the hard cost has

remained almost the same as approved in principle against the Scheme DPR.

However, the soft cost in terms of IDC has increased by more than 2.5 times of the

MERC Order_ Case No 110 of 2016 Page 10

approved IDC due to the delay in completion of the Project and in the actual

construction work. The record shows that the site commencement was 28

December, 2012 as against the Commission’s DPR approval on 9 May, 2008.

7.7. The Commission had observed in the impugned Order that the land was

bought long back, in FY 2008-09, as part of the 145 kV GIS Sub-Station capital

expenditure Scheme at BKC, in accordance with the approved DPR. The schedule

approved was from FY 2009-10 to FY 2010-11. However, the Scheme could start

only in FY 2012-13 and was completed/ commissioned in FY 2015-16, five years

later than the approved schedule (although the Commission noted in its Order that

some capitalisation on this Scheme was also proposed in FY 2016-17).

7.8. In various submissions during the proceedings of the impugned Order,

TPC-T had stated that the delay was due to delay in plot allotment by MMRDA,

delay in building approval by MMRDA and delay in the Commencement

Certificate above plinth level. This has been re-iterated by TPC-T in its Review

Petition, but with more detailed explanations and further supporting material,

including the relevant correspondence, copies of Lease Deeds, approved/allotted

site plans, etc. Based on these revised submissions and details, summarized above,

the Commission has now revisited the matter considering the sequence of events

with regard to obtaining land from MMRDA and the commencement of work on

this land which have now been presented by TPC-T. The chronology of events is

set out below:

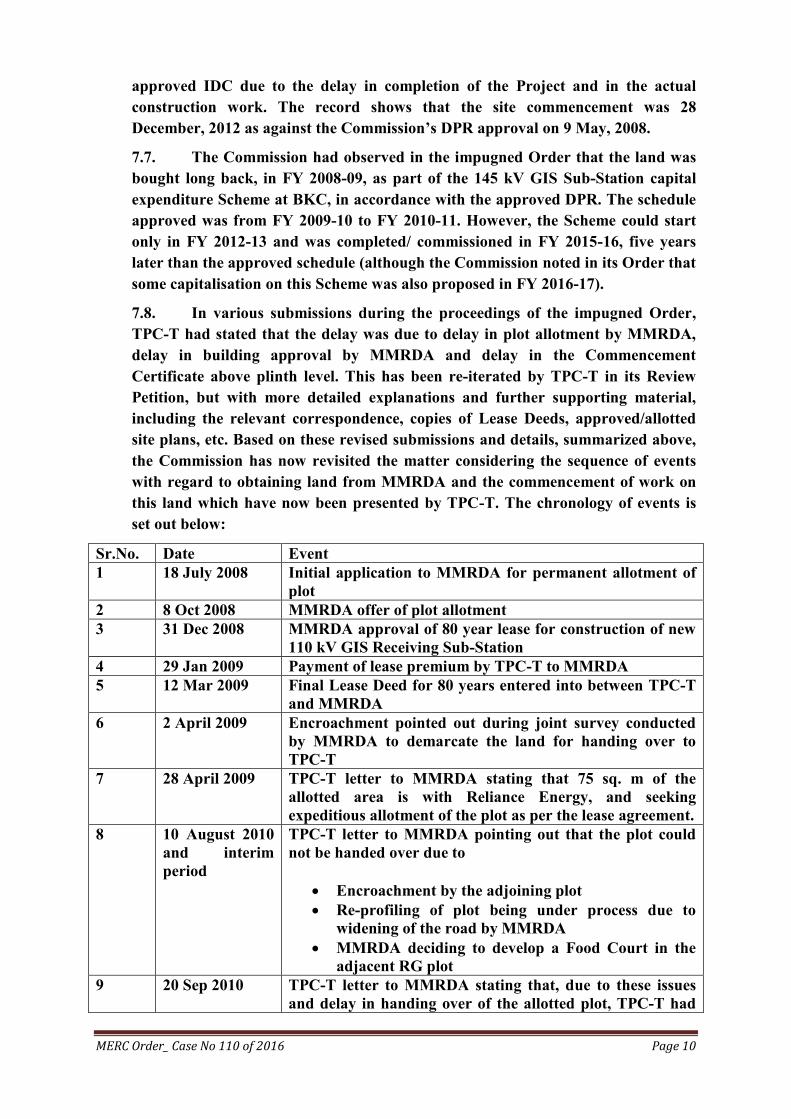

Sr.No. Date Event

1 18 July 2008 Initial application to MMRDA for permanent allotment of

plot

2 8 Oct 2008 MMRDA offer of plot allotment

3 31 Dec 2008 MMRDA approval of 80 year lease for construction of new

110 kV GIS Receiving Sub-Station

4 29 Jan 2009 Payment of lease premium by TPC-T to MMRDA

5 12 Mar 2009 Final Lease Deed for 80 years entered into between TPC-T

and MMRDA

6 2 April 2009 Encroachment pointed out during joint survey conducted

by MMRDA to demarcate the land for handing over to

TPC-T

7 28 April 2009 TPC-T letter to MMRDA stating that 75 sq. m of the

allotted area is with Reliance Energy, and seeking

expeditious allotment of the plot as per the lease agreement.

8 10 August 2010

and interim

period

TPC-T letter to MMRDA pointing out that the plot could

not be handed over due to

Encroachment by the adjoining plot

Re-profiling of plot being under process due to

widening of the road by MMRDA

MMRDA deciding to develop a Food Court in the

adjacent RG plot

9 20 Sep 2010 TPC-T letter to MMRDA stating that, due to these issues

and delay in handing over of the allotted plot, TPC-T had

MERC Order_ Case No 110 of 2016 Page 11

identified an adjoining plot and requested MMRDA to allot

it. TPC-T also mentioned that modifications of design and

drawings for the Receiving Sub-Station had to be revised

thrice considering the changes in the allocated plot.

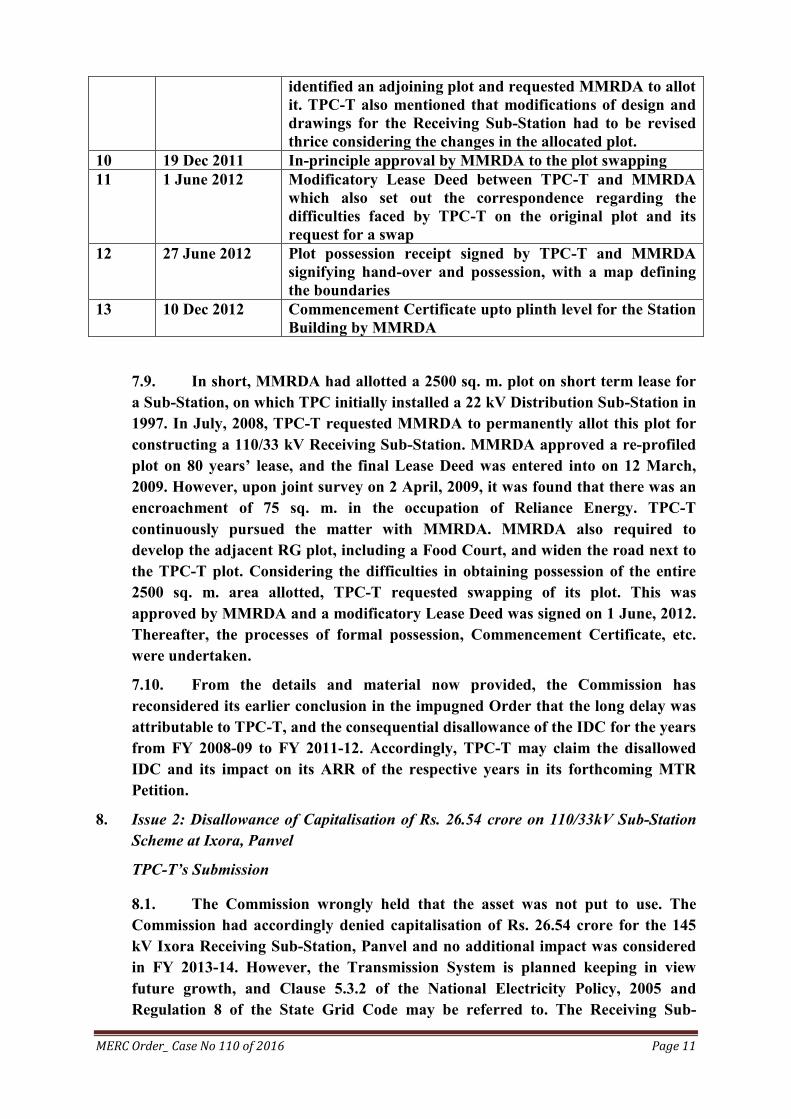

10 19 Dec 2011 In-principle approval by MMRDA to the plot swapping

11 1 June 2012 Modificatory Lease Deed between TPC-T and MMRDA

which also set out the correspondence regarding the

difficulties faced by TPC-T on the original plot and its

request for a swap

12 27 June 2012 Plot possession receipt signed by TPC-T and MMRDA

signifying hand-over and possession, with a map defining

the boundaries

13 10 Dec 2012 Commencement Certificate upto plinth level for the Station

Building by MMRDA

7.9. In short, MMRDA had allotted a 2500 sq. m. plot on short term lease for

a Sub-Station, on which TPC initially installed a 22 kV Distribution Sub-Station in

1997. In July, 2008, TPC-T requested MMRDA to permanently allot this plot for

constructing a 110/33 kV Receiving Sub-Station. MMRDA approved a re-profiled

plot on 80 years’ lease, and the final Lease Deed was entered into on 12 March,

2009. However, upon joint survey on 2 April, 2009, it was found that there was an

encroachment of 75 sq. m. in the occupation of Reliance Energy. TPC-T

continuously pursued the matter with MMRDA. MMRDA also required to

develop the adjacent RG plot, including a Food Court, and widen the road next to

the TPC-T plot. Considering the difficulties in obtaining possession of the entire

2500 sq. m. area allotted, TPC-T requested swapping of its plot. This was

approved by MMRDA and a modificatory Lease Deed was signed on 1 June, 2012.

Thereafter, the processes of formal possession, Commencement Certificate, etc.

were undertaken.

7.10. From the details and material now provided, the Commission has

reconsidered its earlier conclusion in the impugned Order that the long delay was

attributable to TPC-T, and the consequential disallowance of the IDC for the years

from FY 2008-09 to FY 2011-12. Accordingly, TPC-T may claim the disallowed

IDC and its impact on its ARR of the respective years in its forthcoming MTR

Petition.

8. Issue 2: Disallowance of Capitalisation of Rs. 26.54 crore on 110/33kV Sub-Station

Scheme at Ixora, Panvel

TPC-T’s Submission

8.1. The Commission wrongly held that the asset was not put to use. The

Commission had accordingly denied capitalisation of Rs. 26.54 crore for the 145

kV Ixora Receiving Sub-Station, Panvel and no additional impact was considered

in FY 2013-14. However, the Transmission System is planned keeping in view

future growth, and Clause 5.3.2 of the National Electricity Policy, 2005 and

Regulation 8 of the State Grid Code may be referred to. The Receiving Sub-

MERC Order_ Case No 110 of 2016 Page 12

Station was set up pursuant to the approval of the Commission and the STU. Once

it was created and energised, it was put to use and is in use as far as the

Transmission Licensee is concerned. The Transmission Licensee cannot be

penalised for non-utilisation by the Distribution Licensee (in this case, Ixora

Construction, a Deemed Distribution Licensee).

8.2. The background is as follows:

a) The Govt. of India (Ministry of Commerce), on 19 February 2009,

notified as a SEZ an area in certain villages in Khalapur and Panvel

Talukas of Raigad District. On 20 August 2009, it approved Ixora

Construction Pvt. Ltd. as a Co-Developer for providing infrastructure

facilities in the SEZ.

b) On 7 March 2011, Ixora Construction appointed TPC-T as

Consultant to provide EHV connectivity from TPC–T’s Lines for the SEZ

Project and signed the work order.

c) On 14 December 2011, the STU granted approval for validation

and verification of the DPR for construction of the Receiving Sub-Station.

On 20 December 2011, TPC-T submitted the DPR to the Commission. On

16 March 2012, the Commission gave in-principle approval for the

construction of the 110/33kV Sub-Station at Ixora, Panvel.

d) On 5 November 2012, a Lease Agreement was signed between

Sunny Vista Realtors Pvt. Ltd. [the SEZ Developer] and TPC-T for

providing transmission connectivity to the distribution network being

developed by Ixora Construction through a LILO arrangement on the

existing Transmission Lines. TPC-T entered into a Lease Agreement to

develop the 110/33kV Receiving Sub-Station to provide transmission

connectivity for giving feeder outlets to the other Distribution Licensees

or consumers, whenever required.

e) On 5 March, 2013, the Superintending Engineer, Mumbai Region

Electrical Circle, PWD approved the drawings of the proposed Sub-

Station.

f) The development of the SEZ stopped in May, 2013 due to various

reasons, because of which Ixora Construction did not develop its

distribution network to take HT outlets from TPC-T’s network through

the Ixora Receiving Sub-Station. The Commission has held TPC-T liable

by not allowing capitalisation of the asset.

g) On 16 December, 2013, TPC-T requested the STU to advise

Maharashtra State Electricity Distribution Co. Ltd. (MSEDCL) to

furnish the Scheme for taking 33 kV outlets from TPC-T’s proposed Sub-

MERC Order_ Case No 110 of 2016 Page 13

Station and stated that, as per the STU, the 33 kV outlets from TPC-T’s

Receiving Sub-Station are to be given to Ixora Construction and

MSEDCL. TPC-T also informed that the Sub-Station is expected to be

completed by 31 March, 2014. However, there was no response from the

STU and MSEDCL.

h) On 25 March, 2014, TPC-T informed the Superintending

Engineer, Mumbai Region Electrical Circle, PWD that all the works of

the Sub-Station were completed as per the standard method of

construction and were ready for inspection. On 31 March, 2014, the

installation was tested and site inspection was done on 26 September,

2014 by the Electrical Inspector.

i) On 6 February, 2015, TPC-T sought final charging permission, for

which approval was given by the Electrical Inspector on 18 February,

2015.

8.3. As regards the absence of a Connection Agreement and/ or BPTA raised

by the Commission at the hearing, the position is as follows:

a) No Connection Agreement was signed since Ixora Construction

was not ready with the required details. Regulation 13 of the State Grid

Code regarding the procedure and application for establishing connection

arrangements for connection to and use of the InSTS was referred to.

b) The responsibility of signing a Connection Agreement was of both

TPC-T and Ixora Construction, as borne out by Regulation 14 of the

State Grid Code.

c) TPC-T has referred to the clearance of the DPR by the STU and

the Commission’s in-principle approval, and has provided a snapshot of

the STU Plan for FY 2012-13 to FY 2016-17 reflecting this Scheme.

d) The STU approved grid connectivity to Ixora Construction subject

to furnishing the following:

i) Connection Agreement.

ii) Strategy/PPA for grid support in case of failure of supply

from contracted source.

iii) Completion report of works in the scope of Ixora

Construction.

iv) Application to STU for Long Term Open Access.

Thus, the STU had directed Ixora Construction to execute a Connection

Agreement. However, it remained unexecuted as the expected work has

still not been completed by Ixora Construction.

MERC Order_ Case No 110 of 2016 Page 14

e) Thus, TPC-T had followed the due procedure required as a

Transmission Licensee for establishment of the Receiving Sub-Station. A

Connection Application was made by Ixora Construction indicating its

intention to connect to the Transmission System, and the responsibility of

executing the Agreement and LTOA was with it.

f) A Connection Agreement can be signed only when the equipment

and site are ready at both the connecting ends, i.e., the TPC-T and Ixora

ends. While TPC-T was ready with the Sub-Station, the equipment at the

Ixora Construction end was not. A BPTA is signed at the time of

allotment of long-term TCR to the TSU, which is given by the STU upon

the TSU’s LTOA application. The Transmission Licensee is only a party

to the BPTA and not an initiator.

g) During the establishment of the Receiving Sub-Station, there was

no indication from either the STU or Ixora Construction of a delay in the

requirement or a change in schedule. In the absence of any application for

surrender of capacity under Regulation 9 of the Transmission Open

Access Regulations, 2016, TPC-T had a commitment to establishing the

Sub-Station.

h) Sections 39 and 40 of EA, 2003 set out the functions of the STU

and the Transmission Licensee. Although there is no written record of

TPC-T having raised the issue in the GCC meetings, it had informed the

STU about the readiness of the Receiving Sub-Station in advance and also

followed up in writing with the STU for allocation of the outlets, but there

was no response.

8.4. Considering these facts, the capitalisation of Rs. 26.54 crore against the

Scheme of 110/33 kV Receiving Sub-Station at Ixora, Panvel and the consequent

impact on Fixed Charges may be approved.

Commission’s Analysis and Ruling

8.5. Admittedly, the 110/33 kV Receiving Sub-Station at Ixora, Panvel has not

been put to use. While disallowing the capitalisation claimed by TPC-T on this

ground in the impugned MYT Order, the Commission had cited the proviso to

Regulation 27.1 of the MYT Regulations, 2011, which reads as follows:

“27.1 Capital cost for a project shall include:

(a) the expenditure incurred or projected to be incurred, including interest

during construction and financing charges, any gain or loss on account of

foreign exchange risk variation on the loan during construction up to the

date of commercial operation of the project, as admitted by the Commission,

after prudence check;

MERC Order_ Case No 110 of 2016 Page 15

(b) capitalised initial spares subject to the ceiling rates specified in this

Regulation; and

(c) additional capital expenditure determined under Regulation 28:

Provided that the assets forming part of the project but not put to use or not

in use, shall be taken out of the capital cost.”

A similar treatment is given to assets which are not put to use in the 2nd

proviso to

Regulation 23(1) of the current MYT Regulations, 2015 also.

8.6. In the impugned Order, the Commission had noted that, in its earlier

MTR Order dated 26 June 2015 in Case No. 5 of 2015 also (para. 5.3.10), it had

disallowed capitalisation of Rs. 26.54 crore against the Scheme since the assets had

not been put to use. TPC-T’s argument in the subsequent MYT proceedings were

along the lines of its present contentions, as recorded in the impugned Order:

“4.3.3 The Commission may also consider the capitalisation of Rs. 26.54

Crore towards the 145 kV Ixora Receiving Sub-station, which was earlier

disallowed in the MTR Order. That Receiving Sub-station was developed

after receiving due approvals from all the concerned authorities, including

the Commission. It has been established, commissioned and is ready for

taking outlets. However, it is only because the other concerned entities have

not taken their outlets that the Receiving Sub-station has not been put to

use, which is beyond TPC-T’s control as the Transmission Licensee.

4.3.4 Section 61 of the EA, 2003, the Central Electricity Regulatory

Commission (CERC) Tariff Regulations, 2009 and 2014, the MYT

Regulations, on this issue. The Commission may consider its submission

under the provision in the MYT Regulations for removal of difficulties, and

allow the capitalisation for Bays relating to the 145 kV Ixora Receiving Sub-

station. The additional impact is Rs 3.37 Crore in FY 2014-15 on account of

Return on Equity (RoE), Interest on Long Term Loan and Depreciation,

corresponding to the capitalisation of Rs 26.54 Crore in FY 2013-14.”

8.7. On these contentions, and considering the proviso to Regulation 27.1 of

the MYT Regulations, 2011 quoted above, the impugned Order held as follows:

“145 kV Receiving Sub-station at Panvel (Ixora)

4.3.19 As regards the capitalisation on this Scheme, TPC-T has referred to

the CERC Regulations and an ATE Judgment. However, the Commission

notes that the assets have still not been put to use, and TPC-T has admitted

that it cannot say when they would be. The proviso to Regulation 27.1

(quoted at para. 4.3.13 above) specifies that the project assets not put to use

or not in use shall be removed from the capital cost.

4.3.20 Hence, the Commission has not considered the capitalisation of Rs.

26.54 Crore for the 145 kV Receiving Sub-station at Panvel (Ixora, and no

additional impact has been considered in FY 2013-14.”

8.8. Thus, this issue has been decided by the Commission on two earlier

occasions: in its MTR Order in Case No. 5 of 2015, and reiterated in the

subsequent impugned MYT Order in Case No. 22 of 2016 when TPC-T had raised

similar contentions as it has done now. In these circumstances and considering the

MERC Order_ Case No 110 of 2016 Page 16

regulatory provisions, the Commission is of the view that no modification of its

earlier ruling is warranted, quite apart from the fact that TPC-T’s claim does not

fall within the limited ambit of review set out in Regulation 85(a) of the Conduct of

Business Regulations.

9. Issue 3: Disallowance of Capitalisation towards 8 Bays of 33 kV at Parel for FY

2014-15

TPC-T’s Submission

9.1. The Commission erred in not considering the following facts:

a) The Bays have been ‘put in use’ since their commissioning as they

are fully charged, and the Transmission Licensee cannot be penalised for

the inefficiency of the Distribution Licensees in failing to get the cable

connected to the source, which is beyond its control.

b) The Transmission System is planned keeping in view future

growth. Clause 5.3.2 of the National Electricity Policy, 2005 requires that

network expansion should be planned and implemented considering the

anticipated transmission needs in the Open Access regime.

c) Regulation 8 of the State Grid Code provides that the

Transmission System Plan shall cover 5 years. Accordingly, TPC-T had

set up the Parel Sub-Station as approved by both the STU and the

Commission. Regulation 27.1 (a) of the MYT Regulations, 2011 provides

that the capital cost of a Project shall include the expenditure incurred or

projected to be incurred.

9.2. Two 33 kV outlets were sought from TPC-T by BEST and six by TPC-D.

TPC-T has submitted the sequence of activities along with supporting material,

including the Distribution Licensee’s request for load shifting to 33 kV, STU

Scheme approval and Commission’s in-principle capital expenditure approval,

commissioning of the 8 33 kV Bays and their allocation by STU. The STU Plan for

FY 2012-13 to FY 2016-17 included the establishment of a 75 MVA transformer

and 33 kV GIS at Parel Receiving Station during FY 2013-2014. These AIS Bays at

Parel were kept charged since 30 March, 2015.

9.3. With regard to the issue of Connection Agreement and/ or BPTA with

BEST and TPC-D and whether it had approached the GCC for utilization of the

transmission infrastructure, TPC-T referred to Regulations 13 and 14 of the State

Grid Code. The two Distribution Licensees had made Connection Applications for

the 33 kV outlets, which were granted by the STU on 27 October, 2009 and 15

April, 2015 to TPC-D and BEST, respectively. A Connection Agreement requires

details of the equipment used for establishing connection at the TSU and

Transmission Licensee end; safety and technical compliance prior to charging; site

details and site responsibility schedules relating to operations and safety;

MERC Order_ Case No 110 of 2016 Page 17

communication facilities and site access details. The equipment and site are to be

ready at both the connecting ends. TPC-T was ready with the Sub-Station whereas

TPC-D and BEST were not, and they could not execute a Connection Agreement.

A BPTA is entered into when a long term TCR is assigned to the TSU based on the

LTOA application. While the Transmission Licensee has to be a party to the

BPTA as the TSU is connected to its Transmission System, BPTA initiation is the

responsibility of the TSU.

Commission’s Analysis and Ruling

9.4. While disallowing the capitalisation of the 8 33 kV Bays which have

remained idle since commissioning in FY 2014-15, in the background of the

proviso to Regulation 27.1 of the MYT regulations, 2011 (quoted at para. 8.5

above), the impugned Order cited the following observation in its Tariff Order in

Case No. 169 of 2011 relating to MSETCL:

“5.1.2. The Commission feels that the above reasons do not justify the non-

utilization of assets commissioned by the utilities, as these have associated

costs which are borne by the consumers through Tariff. It is also true that

the utilities undertaking the electricity business need to do forward

planning. Investments in assets need to be planned keeping in mind the long

term requirement, for example a horizon of 5-10 years, instead of short term

requirements. This need is greater for transmission utilities which has to

plan for huge network expansion arising out of the generation evacuation

and supply to the load centres. However, it is necessary to create a balance

between long term planned investments and burdening the consumers with

the associated cost of that planning. The consumer doesn’t get benefit out of

these unutilised Bays/ assets, though they are required to pay for it….”

9.5. However, in the impugned MYT Order, the Commission acknowledged

that the installation of GIS Sub-Stations is more technically feasible and

economically viable due to Right of Way and space constraints in Mumbai and the

future requirement of Bays, but that some remained unutilised because of delay in

commissioning of the Transmission Lines for which they were proposed. The

Commission also recognised that additional Bays may also be erected at the

beginning of execution of the GIS Sub-Station, considering difficulties that may

arise later in the availability of matching configurations of GIS bus and inter-

connection, compatibility of GIS switchgear, structural stability of additional

Bays, additional spares of the same make, etc. Hence, it did not disallow the

capitalisation against these GIS Bays (while not approving the O&M expenses).

However, the Commission noted that no such constraints applied to AIS Bays,

including 33 kV Bays. Hence, the Commission disallowed the capitalisation of

these unutilised Bays.

9.6. In these circumstances, as in the similar case of the Ixora Receiving Sub-

Station (Issue 2) discussed earlier and considering the proviso to Regulation 27.1

of the MYT Regulations, 2011 (quoted at para. 8.5 above), the Commission holds

that review of the disallowance of capitalisation towards the 8 33kV Bays at Parel

for FY 2014-15 is not warranted.

MERC Order_ Case No 110 of 2016 Page 18

10. Issue 4: Disallowance of O&M expenses of Rs. 10.66 crore on unutilised Bays in FY

2014-15

TPC-T’s Submission

10.1. The Commission wrongly disallowed the O&M expenditure on 91 Bays

(at <66 kV and >66 kV voltage levels). O&M expenses on 57 Bays were disallowed

since the assets were not put to use (including 31 Ixora Bays), and on 34 Bays

because they were capitalised but remained unutilised by the Beneficiaries.

10.2. Regulation 65.1 of the MYT Regulations, 2011 does not provide that the

O&M expenses will not be allowed if the asset is not in use after capitalisation. The

proviso of Regulation 27.1 disallowing capitalisation on the ground of the asset

‘not put to use’ or ‘not in use’ also has nothing to do with O&M expenses. Once

the Bays are capitalised, they are not connected to cater to the load but still have to

be kept charged and maintained to prevent any failure.

10.3. Long-term planning is necessary for development of the Transmission

System, and its augmentation is based on future projections of load growth

provided by the Distribution Licensees. It also has to be developed much before

the Distribution System so that, when the actual growth takes place and the

Distribution Licensee requires outlets, it is ready. Moreover, all these Bays have

been developed after approval from the STU and the Commission. Despite having

approved the normative O&M expenditure of Rs. 177.67 crore based on the

approved number of Bays and Line ckt. kms., in terms of Regulation 61.5.1 of the

MYT Regulations, 2011, the Commission disallowed the O&M entitlement of the

unutilised Bays for FY 2014-15.

10.4. Once an asset is capitalised, it is ready to be used and requires regular

maintenance till it is de-capitalised. Such maintenance includes the component of

employee cost, and the manpower at the serving Station is not proportional to the

number of Bays.

Commission’s Analysis and Ruling

10.5. While the MYT Regulations, 2011 do not expressly address it, the

disallowance of O&M expenses on the unutilised Bays has to be seen in the light of

the basic principles underlying the passing through of costs to consumers, and the

nature of those costs. In its impugned Order, the Commission had, in fact,

considered the issue of the O&M expenses incurred on the unutilised Bays on that

basis, and concluded as follows:

“5.1.2. However, the Commission is of the view that the claim for O&M

expenses against the unutilised AIS and GIS Bays is not justified. Even

though the capitalisation for the unutilised GIS Bays has been allowed,

these Bays are not in use or remain idle in the network. Hence, allowing

O&M expenses on these Bays would amount to approving expenditure

without any benefit to consumers. Therefore, the Commission has

considered the impact of unutilised GIS as well as AIS Bays while

calculating the normative O&M expenses for FY 2014-15.”

MERC Order_ Case No 110 of 2016 Page 19

10.6 It is well understood that O&M expenditure may have to be incurred on

Bays even if they are not utilised, and TPC-T has only reiterated this in these

proceedings. The Commission finds no justification to review its considered and

reasoned decision, quoted above, to disallow such expenses.

11. Issue 5: Non-consideration of number of Bays commissioned at Ixora Receiving Sub-

Station in computation of normative O&M expenses for FY 2014-15

TPC-T’s Submission

11.1. The Commission had approved normative O&M expenditure of Rs.

177.67 crore based on the approved number of Bays & Line ckt. km. as per the

MYT Regulations, 2011. However, it erred in not considering the number of Bays

commissioned at the Ixora Receiving Sub-Station while computing the normative

O&M expenses for FY 2014-15. A total of 35 Bays (8 Bays between 66 kV and 400

kV and 27 Bays of <66 kV) were deducted from the opening balance of the number

of Bays of FY 2014-15 as approved in the provisional Truing Up of FY 2014-15 in

the earlier MTR Order in Case No. 5 of 2015. The Ixora Bays were not included in

the opening balance of FY 2014-15, which has affected the calculation of

normative opening balance for that year.

11.2. The Ixora Receiving Sub-Station was commissioned in FY 2013-14, and

its capitalisation was claimed in the Truing up of FY 2013-14. However, the

Commission had disallowed this capitalisation and not considered the number of

Bays for this purpose in FY 2013-14. Hence, the closing balance of FY 2013-14,

which was the opening balance for FY 2014-15, did not include the Ixora Bays.

Therefore, deducting them from the opening balance of FY 2014-15 has reduced

the normative O&M expenses for FY 2014-15. A correction in the number of Bays

is claimed as in the Table below:

Table 3: Number of Bays to be considered for FY 2014-15

Equipment Approved in

impugned MYT

Order

Corrections sought

for Ixora

Revised no. of

Bays for FY 2014-

15

Bays (Between 66 kV and 400 kV)

Opening 312 8 320

Additions 19 -8 11

Closing 331 0 331

Average 322 326

Bays (Less than 66 kV)

Opening 742 27 769

Additions 64 -27 37

Closing 806 0 806

Average 774 788

MERC Order_ Case No 110 of 2016 Page 20

11.3. The Commission may consider the number of Ixora Bays that were

removed from the opening balance of FY 2014-15 and re-calculate the normative

O&M expenses for FY 2014-15 as follows:

Table 4: Revised O&M Entitlement for FY 2014-15 Norm -Bays Norm

(Rs Lakhs/Bay)

No. of Bays as

approved in

the T.O.

Normative

O&M

(Rs. Crores)

Revised No. of

Bays as per this

Review Pettion

Normative

O&M

(Rs. Crores)

Diff

a b c=a*b d e=a*d f=e-c

Between 66 kV

and 400 kV

33.67 321.50 108.25 325.50 109.60

Less than 66 KV 7.04 774.00 54.49 787.50 55.44

Norms

Transmission

Lines

Norm

(Rs Lakhs/Ckt

Km)

No. of Ckt Km Normative

O&M

(Rs. Crores)

No. of Ckt Km Normative

O&M

(Rs. Crores)

Between 66 kV

and 400 kV

1.29 1157.12 14.93 1157.12 14.93

Normative O&M

Expenditure

177.67 179.96 2.30

Table 5: Revised Net Entitlement due to change in Sharing of Gain / (Loss) of

O&M Expenses for FY 2014-15 Rs Crores

ParticularsApproved in

MYT Order

Revised

Submission

Diff

O&M expenditure as per norms of MYT

Regulations

(a) 177.67 179.96 -2.30

Actual approved O&M expenditure (b) 149.96 149.96 0

Increase in O&M expenditure on account of

uncontrollable expenditure

(c ) 0.00 0.00 0.00

Actual O&M Expenditure with uncontrollable

expenditure

(d=b+c) 149.96 149.96 0.00

Amount passed on to the Transmission System

Users

(e=(a-d)/3) 9.24 10.00 -0.77

Amount to be retained by the Transmission

Licensee

(f=(a-d)*2/3) 18.47 20.00 -1.53

Net entitlement (g=a-e) 168.43 169.96 -1.53

The additional impact of Rs. 1.53 crore for FY 2014-15 may be allowed to TPC-T.

Commission’s Analysis and Ruling

11.4. In its MYT Petition, TPC-T had included the capitalisation of the Ixora

Receiving Sub-Station in the opening balance of Gross Fixed Assets (GFA) for FY

2014-15, but the number of Ixora Bays was not included in the opening balance of

Bays. Generally, the capitalisation and addition of Bays for a capital expenditure

Scheme are claimed in the same year. However, this was not followed in this case,

resulting in an oversight while computing the opening balance of Bays of FY 2014-

15. This has a consequential impact on the normative O&M expenses approved in

the impugned MYT Order.

11.5. The Commission has now revised the opening balance of the number of

Bays for FY 2014-15 after including the Ixora Bays. The revised number of Bays

and normative O&M expenses for FY 2014-15 have been re-computed as shown in

the Tables below.

Table 6: Opening and Closing balance of Bays approved for FY 2014-15

MERC Order_ Case No 110 of 2016 Page 21

Particulars No. of Bays

Opening of 66 kV to 400 kV Bays as approved in MYT

Order 312

Addition of Ixora Bays between 66 kV to 400 kV 8

Opening balance of 66 kV to 400 kV Bays as approved in

this Order 320

Addition of Bays as approved in MYT Order 19

Addition of Bays considered in this Order after

excluding Ixora Bays (19 – 8) 11

Closing balance of 66 kV to 400 kV Bays as approved in

this Order 331

Average balance of 66 kV to 400 kV Bays as approved in

this Order 326

Opening Balance of <66 kV Bays as approved in MYT

Order 742

Addition of Ixora Bays <66 kV 27

Opening balance of <66 kV Bays as approved in this

Order 769

Addition of Bays as approved in MYT Order 64

Addition of Bays considered in this Order after

excluding Ixora Bays (64 - 37) 37

Closing balance of <66 kV Bays as approved in this

Order 806

Average balance of <66 kV Bays in FY 2014-15 as

approved in this Order 788

Table 7: Normative O&M Expenses approved for FY 2014-15 based on number of

Bays approved in this Order

Calculation of Normative O&M Expense for Bays (A) (Approved in this Order)

Particulars Number of Bays approved

in this Order

Norm (Rs.

Lakh/Bay)

Normative O&M

Expense (Rs. Crore)

Between 66 kV

and 400 kV

326 33.67 109.60

Less than 66 kV 788 7.04 55.44

Total 165.04

MERC Order_ Case No 110 of 2016 Page 22

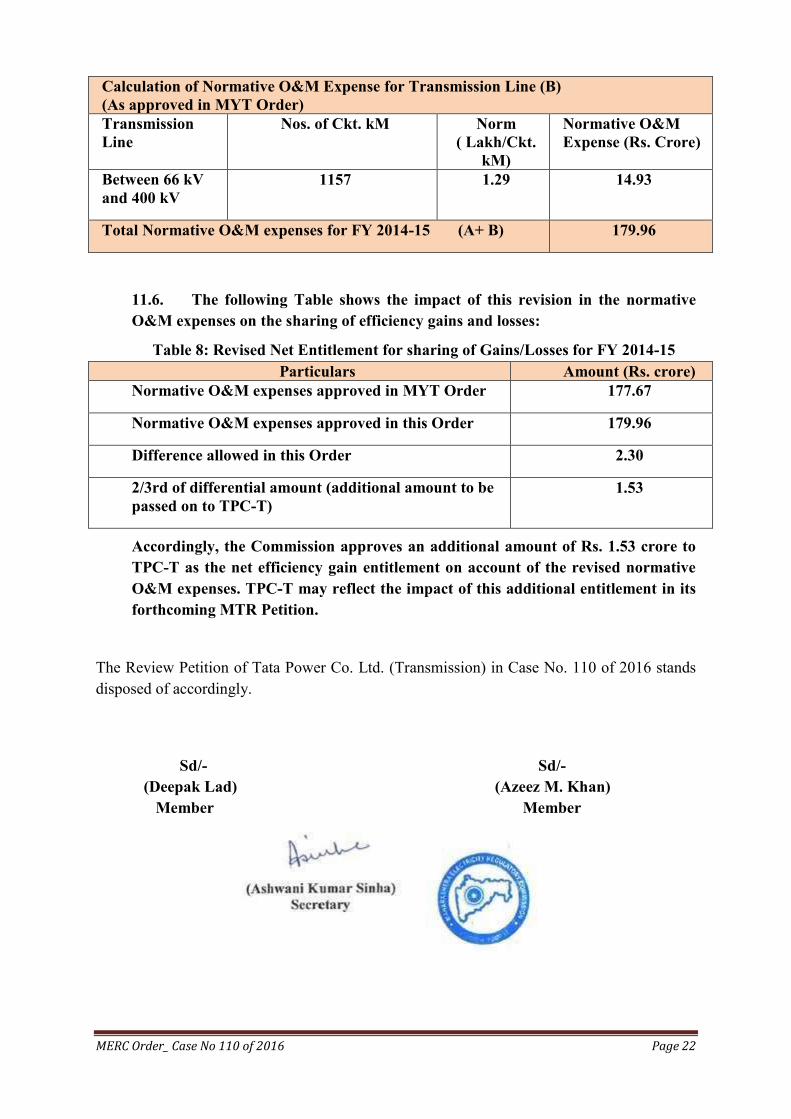

Calculation of Normative O&M Expense for Transmission Line (B)

(As approved in MYT Order)

Transmission

Line

Nos. of Ckt. kM Norm

( Lakh/Ckt.

kM)

Normative O&M

Expense (Rs. Crore)

Between 66 kV

and 400 kV

1157 1.29 14.93

Total Normative O&M expenses for FY 2014-15 (A+ B) 179.96

11.6. The following Table shows the impact of this revision in the normative

O&M expenses on the sharing of efficiency gains and losses:

Table 8: Revised Net Entitlement for sharing of Gains/Losses for FY 2014-15

Particulars Amount (Rs. crore)

Normative O&M expenses approved in MYT Order 177.67

Normative O&M expenses approved in this Order 179.96

Difference allowed in this Order 2.30

2/3rd of differential amount (additional amount to be

passed on to TPC-T)

1.53

Accordingly, the Commission approves an additional amount of Rs. 1.53 crore to

TPC-T as the net efficiency gain entitlement on account of the revised normative

O&M expenses. TPC-T may reflect the impact of this additional entitlement in its

forthcoming MTR Petition.

The Review Petition of Tata Power Co. Ltd. (Transmission) in Case No. 110 of 2016 stands

disposed of accordingly.

Sd/- Sd/-

(Deepak Lad) (Azeez M. Khan)

Member Member