beer project

DESCRIPTION

beer projectTRANSCRIPT

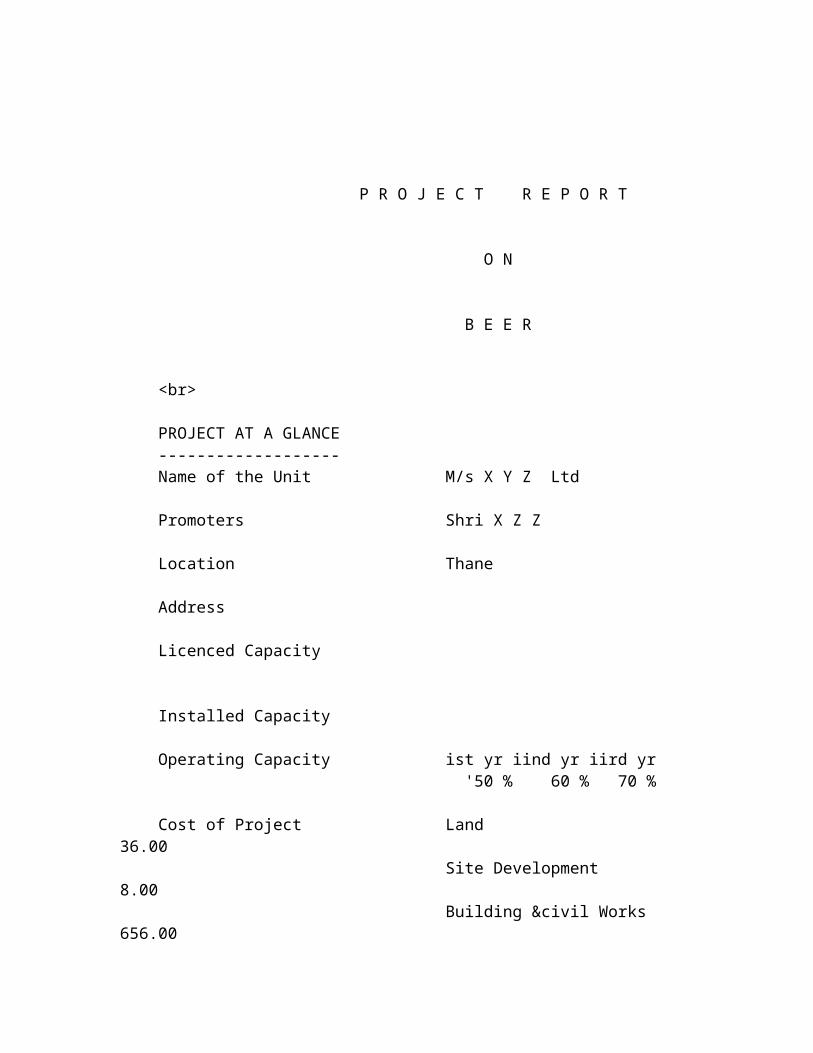

P R O J E C T R E P O R T

O N

B E E R

<br>

PROJECT AT A GLANCE ------------------- Name of the Unit M/s X Y Z Ltd

Promoters Shri X Z Z

Location Thane

Address

Licenced Capacity

Installed Capacity

Operating Capacity ist yr iind yr iird yr '50 % 60 % 70 %

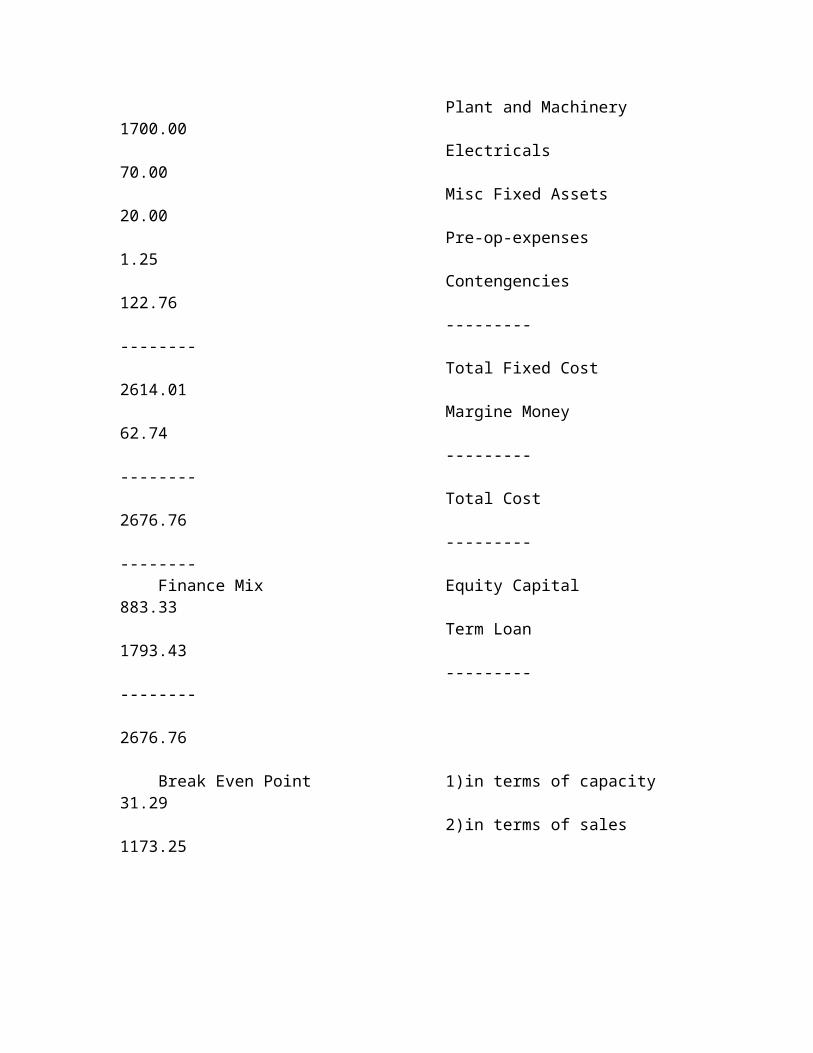

Cost of Project Land 36.00 Site Development 8.00 Building &civil Works 656.00 Plant and Machinery 1700.00 Electricals 70.00 Misc Fixed Assets 20.00 Pre-op-expenses 1.25 Contengencies 122.76 --------- -------- Total Fixed Cost 2614.01 Margine Money 62.74 --------- -------- Total Cost 2676.76

--------- -------- Finance Mix Equity Capital 883.33 Term Loan 1793.43 --------- -------- 2676.76

Break Even Point 1)in terms of capacity 31.29 2)in terms of sales 1173.25

<br>

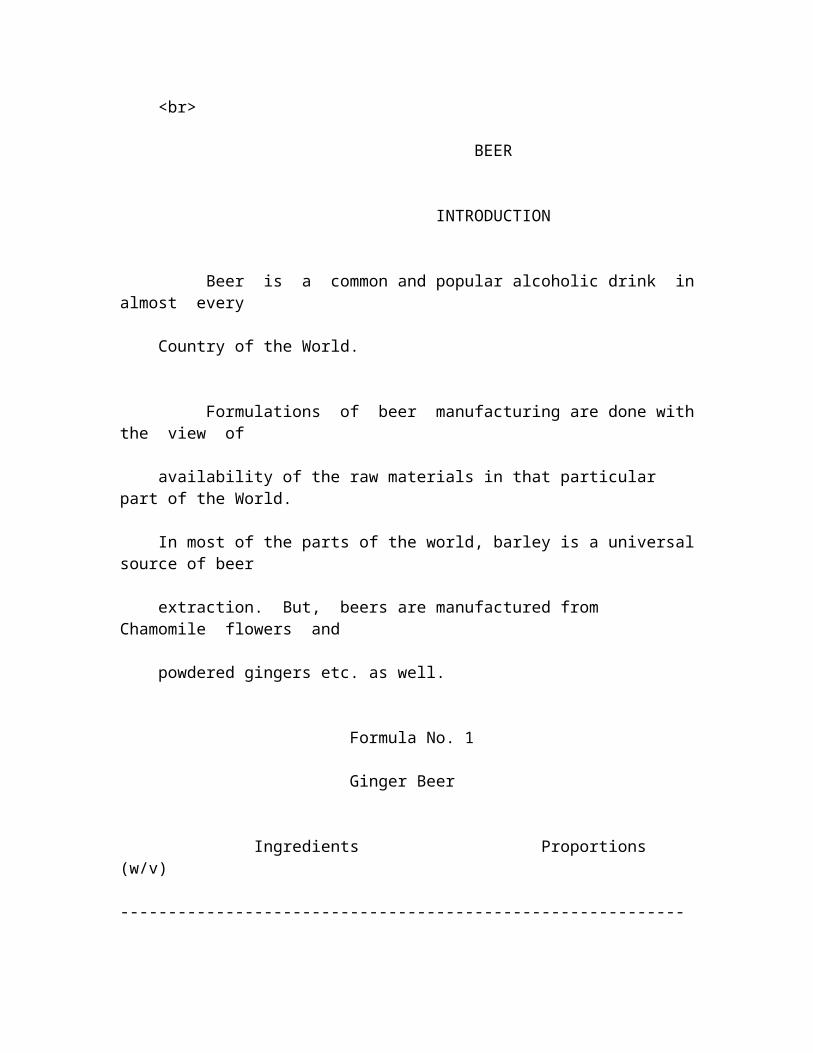

BEER

INTRODUCTION

Beer is a common and popular alcoholic drink in almost every

Country of the World.

Formulations of beer manufacturing are done with the view of

availability of the raw materials in that particular part of the World.

In most of the parts of the world, barley is a universal source of beer

extraction. But, beers are manufactured from Chamomile flowers and

powdered gingers etc. as well.

Formula No. 1

Ginger Beer

Ingredients Proportions (w/v) -----------------------------------------------------------

Powdered Ginger 28 gms.

Cream of tarter 14 gms.

Citric Acid 7 gms.

Sugar 453 gms.

Yeast (q.s.)

Water 4.5 lits.

<br>

Formula No. 2

Chamomile Beer

Ingredients Proportions (w/v) ---------------------------------------------------------------

Chamomile flowers 57 gms.

Ground ginger 14 gms.

Malt extract 228 gms.

Sugar 907 gms.

Yeast 7 gms.

Water 9 lits.

The manufacturing processes and quality control measure, can make

the beer nutritious, energy packed and refreshing.

There are four board categories of beer :-

1. Pale Beer.

2. Dark Beer

3. Strong Beer.

4. Special Beer.

<br>

POLLUTION

This unit require a NOC form the Pollution Control Board.

USES & APPLICATION

A special use of beer is for the control of sodium intake in the

treatment of disease e.g. congestive heart failure, high blood pressure

and certain Kidney and liver ailments. Beer cannot (because of its low

say 4.2), harbor any pathigenic germs. The content of nourishing

components are all in dissolved form. Beer is free from fat. The

alcohol in the beer is effective according to the amount &

concentration.

<br>

MANUFACTURING PROCESS

Washing, wort boiling, fermenting, lagering, filtering and

bottling constitute the beer making. Finely crushed malt & water under

enzymetic activity, convert starch into sugar & proteins into peptides

& amino-acids during mashing. The dissolved product after mashing is

termed 'wort' and the insoluble residues are called spent grain (sold

as cattle fedder). The wort is boiled with hops destroying the enzymes

while bitter substances are extracted from hops. Wort boiling results

in conversions of protein into coagulate & flocculate in the form of

flakes which after separation from the wort is called sludge. The wort

is cooled to, the yeast is added which converts sugar into alcohol and

Co2, during fermentation. At the completion of fermentation yeast is

separated from beer, and there after green beer matures in lagering

tanks slowly. Sediments settle at the tanks and then to bottling

machine. The beer is pasteurised to keep its clear color for longer

period of time.

<br>

MARKET SURVEY

The beer & breweries market is expanding bt leaps & bounds. Great

many brands of beer are available in the country in a range of prices

but demnd is still out smarting the supply heavily.

The best selling brands are :- haywards, London Pilsner,

Kingfisher, King fisher Diet, Flying Horse Royal, Golden Eagle, Solan,

Kalyani Super Strong, London Diet, Khajuraho and Hayards 2000. The

trend is towards stornger beer. The alcohol content makes a beer

strong.

The Indian beer market is worth Rs. 1350 crore. The market is

growing @ 12% p.a. The leaders in the market are UB group (32%), Mohan

Meakin (28%), shaw Wallce (10%), Associated Brewries (7%) and othere

(23%) of the total beer output.

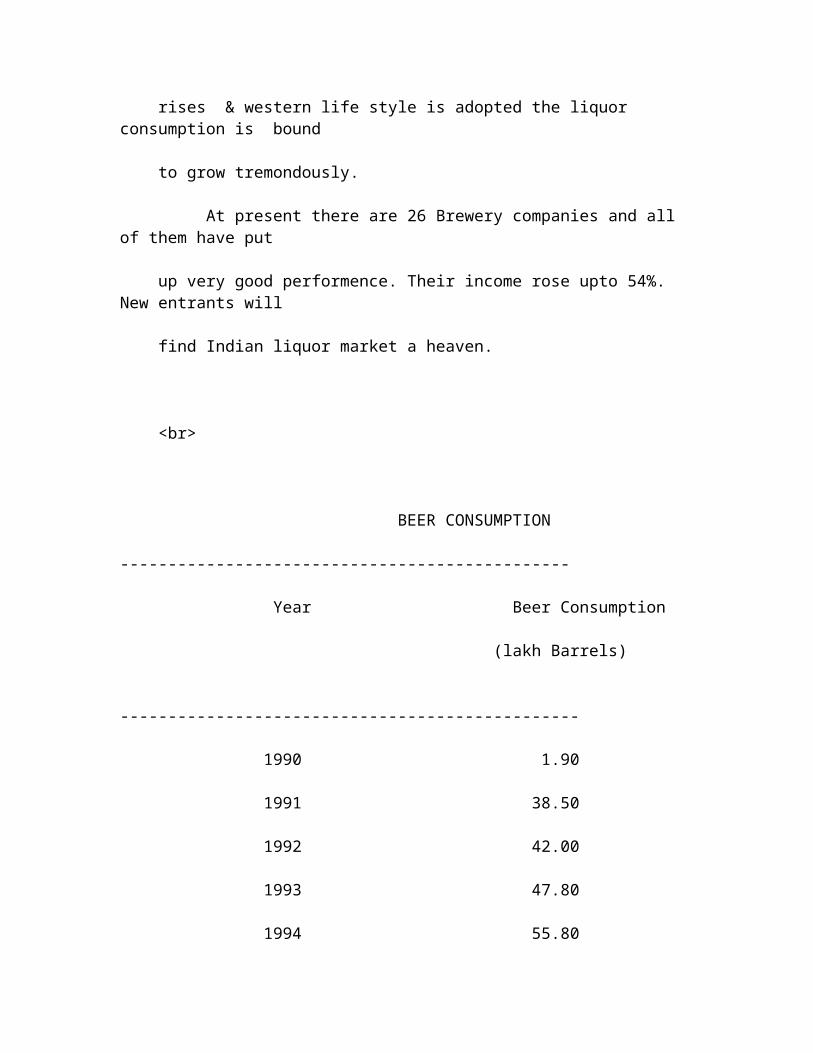

Beer has a tremendous future potential as drinking is no longer

considered a stigma rather it is a status symbol today. As the income

rises & western life style is adopted the liquor consumption is bound

to grow tremondously.

At present there are 26 Brewery companies and all of them have put

up very good performence. Their income rose upto 54%. New entrants will

find Indian liquor market a heaven.

<br>

BEER CONSUMPTION -----------------------------------------------

Year Beer Consumption

(lakh Barrels)

------------------------------------------------

1990 1.90

1991 38.50

1992 42.00

1993 47.80

1994 55.80

1995 61.30

--------------------------------------------------

<br>

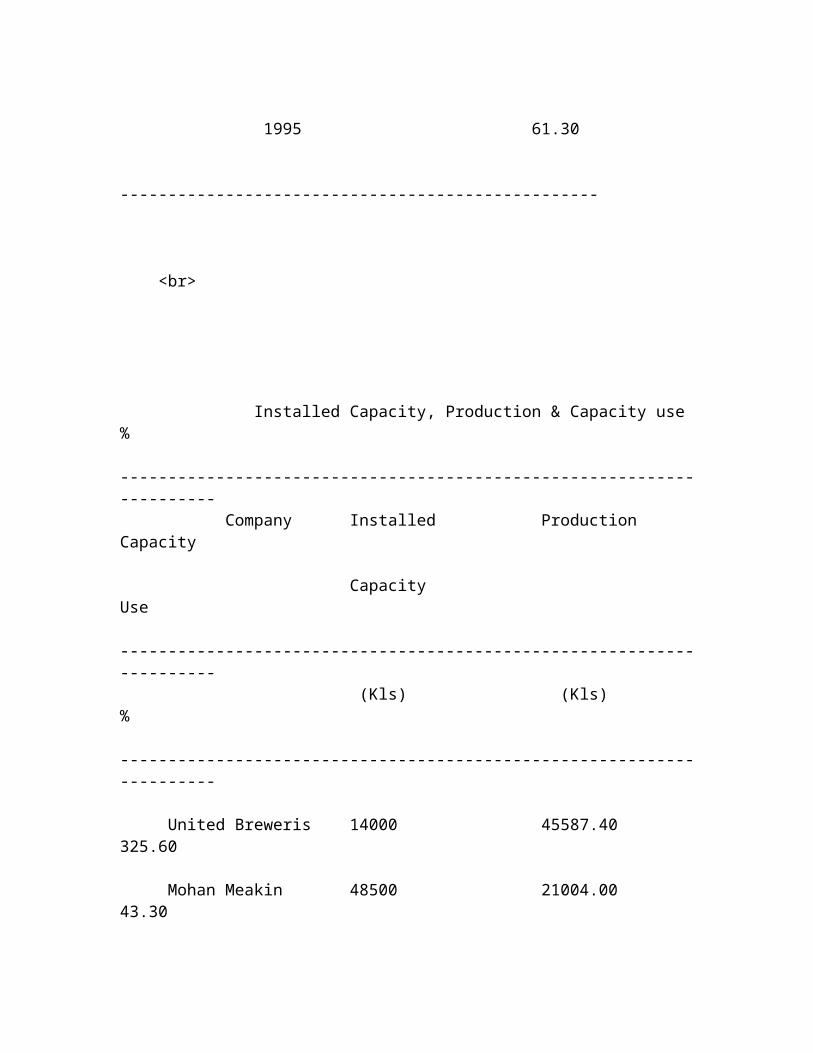

Installed Capacity, Production & Capacity use % ---------------------------------------------------------------------- Company Installed Production Capacity

Capacity Use ---------------------------------------------------------------------- (Kls) (Kls) % ----------------------------------------------------------------------

United Breweris 14000 45587.40 325.60

Mohan Meakin 48500 21004.00 43.30

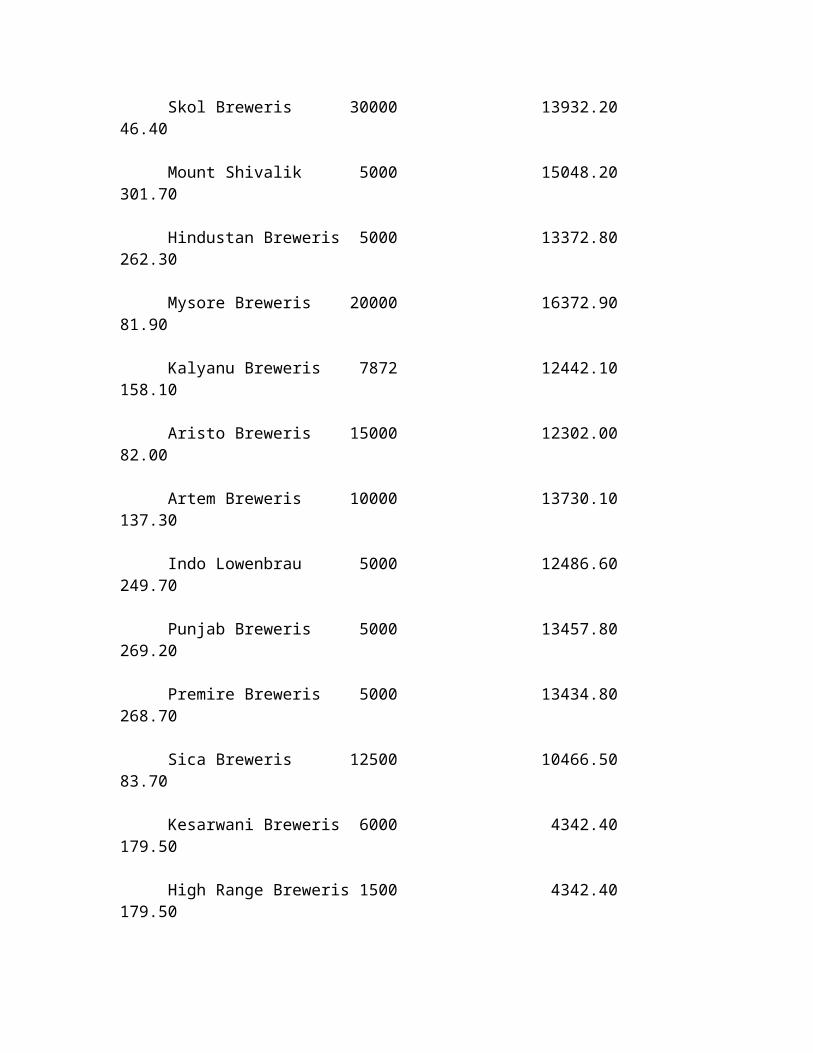

Skol Breweris 30000 13932.20 46.40

Mount Shivalik 5000 15048.20 301.70

Hindustan Breweris 5000 13372.80 262.30

Mysore Breweris 20000 16372.90 81.90

Kalyanu Breweris 7872 12442.10 158.10

Aristo Breweris 15000 12302.00 82.00

Artem Breweris 10000 13730.10 137.30

Indo Lowenbrau 5000 12486.60 249.70

Punjab Breweris 5000 13457.80 269.20

Premire Breweris 5000 13434.80 268.70

Sica Breweris 12500 10466.50 83.70

Kesarwani Breweris 6000 4342.40 179.50

High Range Breweris 1500 4342.40 179.50

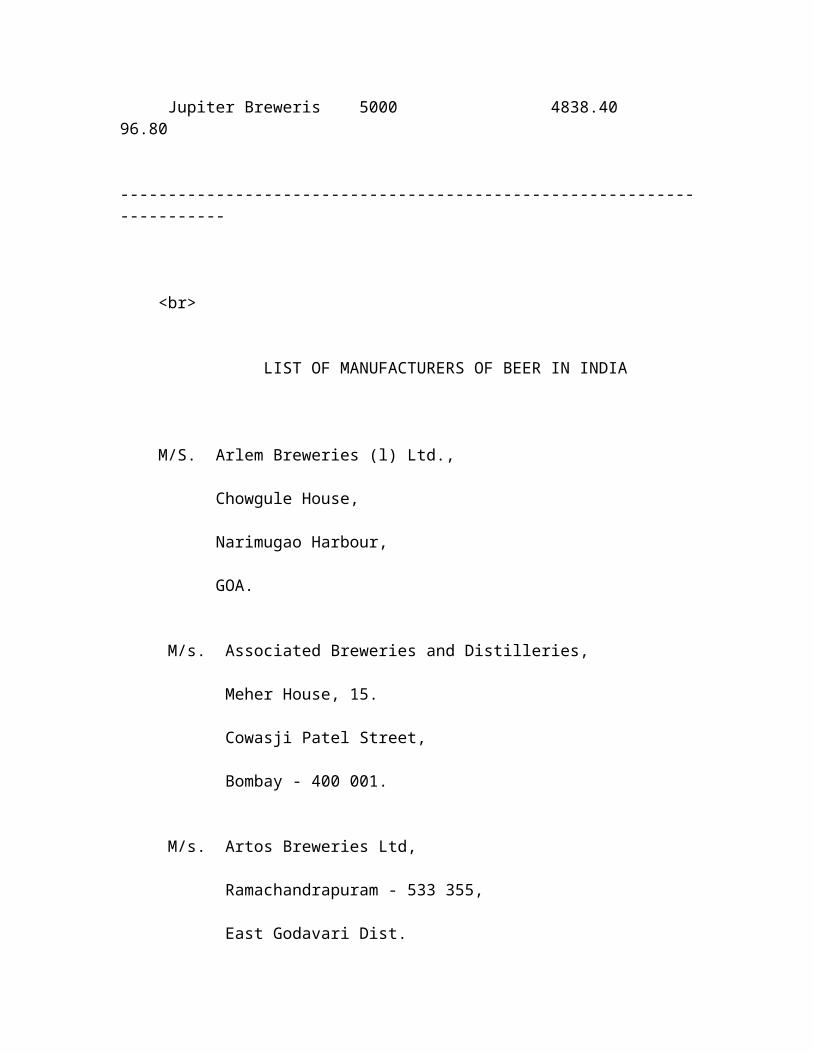

Jupiter Breweris 5000 4838.40 96.80

-----------------------------------------------------------------------

<br>

LIST OF MANUFACTURERS OF BEER IN INDIA

M/S. Arlem Breweries (l) Ltd.,

Chowgule House,

Narimugao Harbour,

GOA.

M/s. Associated Breweries and Distilleries,

Meher House, 15.

Cowasji Patel Street,

Bombay - 400 001.

M/s. Artos Breweries Ltd,

Ramachandrapuram - 533 355,

East Godavari Dist.

M/s. Devans Modern Breweries Ltd.,

Bohri

P.O. Talab Tilla,

Jammu Kashmir - 2.

<br>

M/s. Harayana Breweries Ltd.,

41, K.M. Stone,

G.T. Road,

Murthal.

Sonepat,

Haryana.

M/s. Indo Lowen Bran Breweries Ltd.,

Mahajan House,

E - 1 & 2 South Extension,

New Delhi.

M/s. Khoday Brewery & Distilling co,

9, Seshadri Road,

Bangalore - 560 009.

<br>

M/s. Liasons Breweries Ltd,

Industrial Area,

Govindpura,

Bhopal,

Madhya Pradesh.

M/s. Mohanwachi Rocky Spring

Water Breweries Ltd,

P.O. Khopali,

Dt. Kolaba,

Maharashtra.

M/s. Narang Breweries,

3, Cavalry Lines,

Delhi - 110 007.

M/s. Premier Breweries Ltd.,

Kode Street,

Palghat - 678 623

Kerala.

M/s. Vinadala Distilleries Pvt. Ltd,

Chateau De Kauser,

Premavathipet Vaze,

P.O. Gaganpahad,

Hyderabad.

Andhra Pradesh.

M/s. Jupitor Breweries Ltd,

West Bengal.

<br>

SUPPLIERS OF PLANT & MACHINERY

A. Boilers

M/s. Compact Boilers and Fabricators,

44 - Yusuf Building,

4th Floor,

Veer Nariman Road,

Bombay - 400 001.

M/s. ACC Vickers Babcock Ltd.,

Express Towers,

Nariman Point,

Bombay - 400 026.

B. Tanks

M/s. Acmec India Corporation,

16, Manu Mansion,

Old Custems House Rd.,

Bombay.

M/s. Breweries Engg. Corp.

A -10, Lane No. 4,

Anand Parbhat Industrial Estate,

New Rohtak Road,

New Delhi - 110 025.

<br>

C. Fermentor

M/s. Acmec India Corporation,

16, Manu Mansion,

Old Custems House Rd.,

Bombay.

M/s. Breweries Engg. Corp.

A-10, Lane No. 4,

Anand Parbhat Industrial Estate,

New Rohtak Road,

New Delhi - 110 025.

<br>

SUPPLIERS OF HOPS

M/s. Rup Pharma,

A - 1, Udyognagar,

Navsri,

Distt.-Bulsar,

Gujarat.

M/s. Chemiloids,

Brindavan Colony,

Vijayawada.

M/s. Amjar Pvt. Ltd.,

2, Hormuz Mantions,

72, Bhulabhai Desai Road,

Bombay - 400 026.

<br>

COMPLETE BREWERY PLANT SUPPLIERS

M/s. Alfa - Lavel (India) Ltd.,

Bombay -Pune Road,

Dapodi,

Pune - 411 012.

Maharashtra.

M/s. Breweries Enginering Pvt. Ltd.,

A - 10, Lans No. 4,

Anand Parbat Industrial Area,

New Rohtak Road,

New Delhi - 55.

<br>

RAW MATERIALS SUPPLIERS ADDRESSES

A. Malt

M/s. Barmalt India Pvt. Ltd.,

3, Osian Bldg.,

12, Nehru Place,

New Delhi - 11 00 19.

Ph. - 644 0089.

M/s. Imperial Malts Pvt. Ltd.,

4/13, Safdarjung Enclave,

New Delhi -11 00 29.

Ph. - 603139, 608832.

M/s. Malt Company (India) Pvt. Ltd.,

P.O. B - 1,

Khandsa Road,

Gurgaon - 122 001.

Ph : (01272) 21446/21448

<br>

PACKAGING MATERIAL'S SUPPLIERS

M/s. H.G.F. Laminates,

8/1/B, Diamond Harbour Road,

Calcutta - 700 027.

M/s. Flowmore Polymers Ltd.,

7, Community Centre,

New Friends Colony

New Delhi - 110065.

M/s. Mazda Packaging Ltd.,

22, Chittaranjan Avenue,

Calcutta - 700 002.

<br>

A. Glass Bottles

M/s. Divecha Glass Industries,

155, Maker Chambers VI,

220, Nariman Point,

Bombay - 4000 21.

Ph. 241157/241167

M/s. Jagatjit Industries,

Ashoka Estate,

9th Floor, 24, Barakhamba Road,

New Delhi - 110 001.

Tel. : 331 7027

M/s. Haldyn Glass Ltd.,

Western Express Highway,

Goregaon (E),

Bombay - 4000 63.

<br>

M/s. Mahalaxmi Glass Works Ltd.,

Dr. E. Moses Road,

Post Box No. 6251,

Bombay - 400011.

B. Crown Corks

M/s. Ashok Products,

Swami Premdas Road,

Fatehpura,

Baroda - 39 0006.

M/s. AIFSO Enterprises,

A - 1, Veena Beena Apartments,

Sewri (W), Bombay - 400 015.

Ph. 4130926/ 4137339.

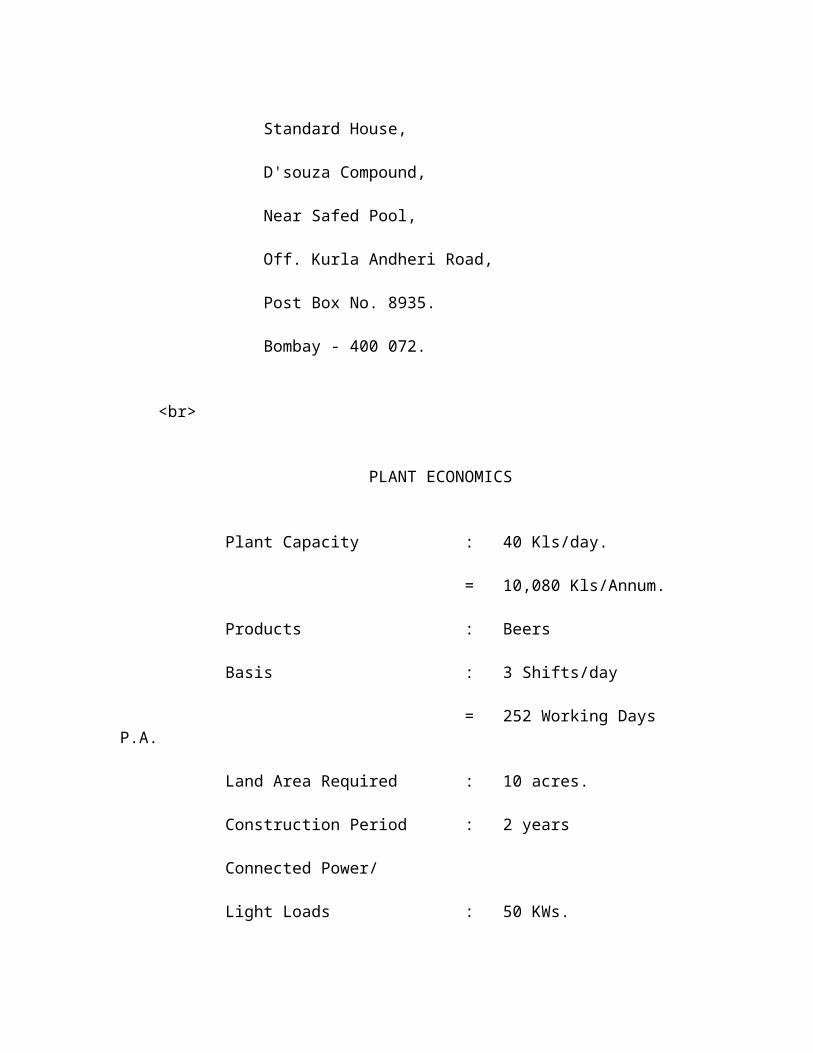

M/s. Standard Tin Works,

Standard House,

D'souza Compound,

Near Safed Pool,

Off. Kurla Andheri Road,

Post Box No. 8935.

Bombay - 400 072.

<br>

PLANT ECONOMICS

Plant Capacity : 40 Kls/day.

= 10,080 Kls/Annum.

Products : Beers

Basis : 3 Shifts/day

= 252 Working Days P.A.

Land Area Required : 10 acres.

Construction Period : 2 years

Connected Power/

Light Loads : 50 KWs.

Other Energies : Boiler Fuel

Employment Potential : 250 Persons

<br>

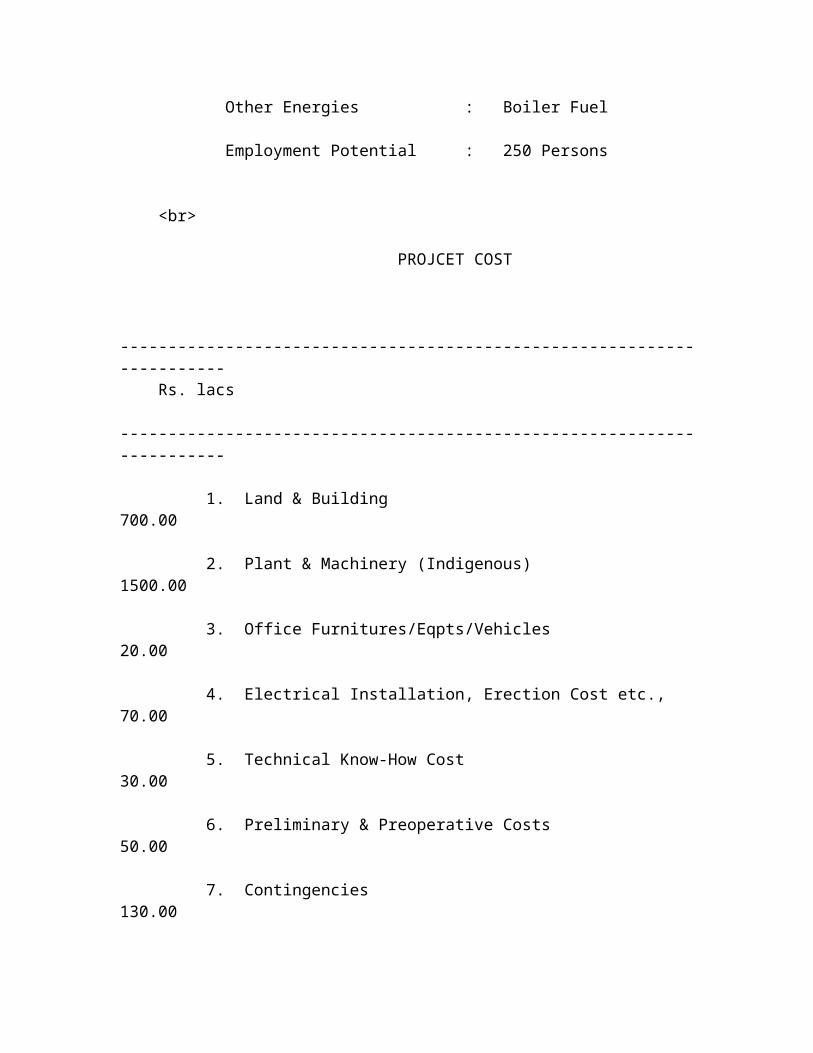

PROJCET COST

----------------------------------------------------------------------- Rs. lacs -----------------------------------------------------------------------

1. Land & Building 700.00

2. Plant & Machinery (Indigenous) 1500.00

3. Office Furnitures/Eqpts/Vehicles 20.00

4. Electrical Installation, Erection Cost etc., 70.00

5. Technical Know-How Cost 30.00

6. Preliminary & Preoperative Costs 50.00

7. Contingencies 130.00

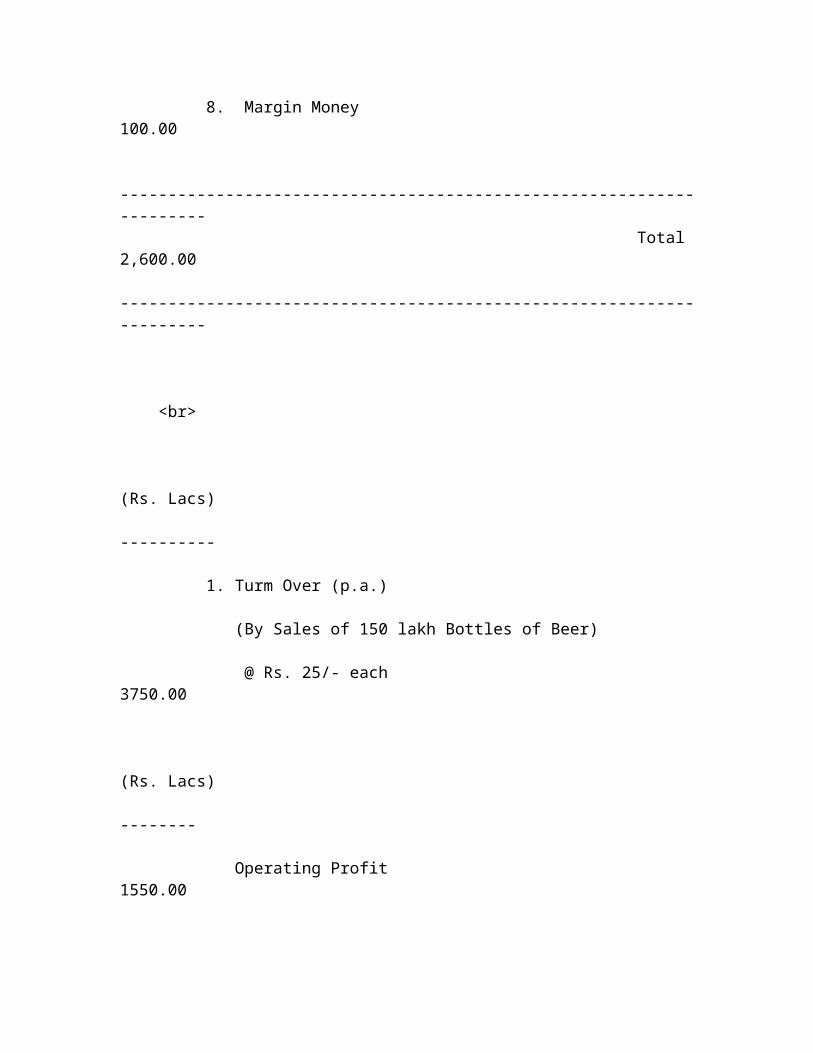

8. Margin Money 100.00

--------------------------------------------------------------------- Total 2,600.00 ---------------------------------------------------------------------

<br>

(Rs. Lacs) ----------

1. Turm Over (p.a.)

(By Sales of 150 lakh Bottles of Beer)

@ Rs. 25/- each 3750.00

(Rs. Lacs) --------

Operating Profit 1550.00

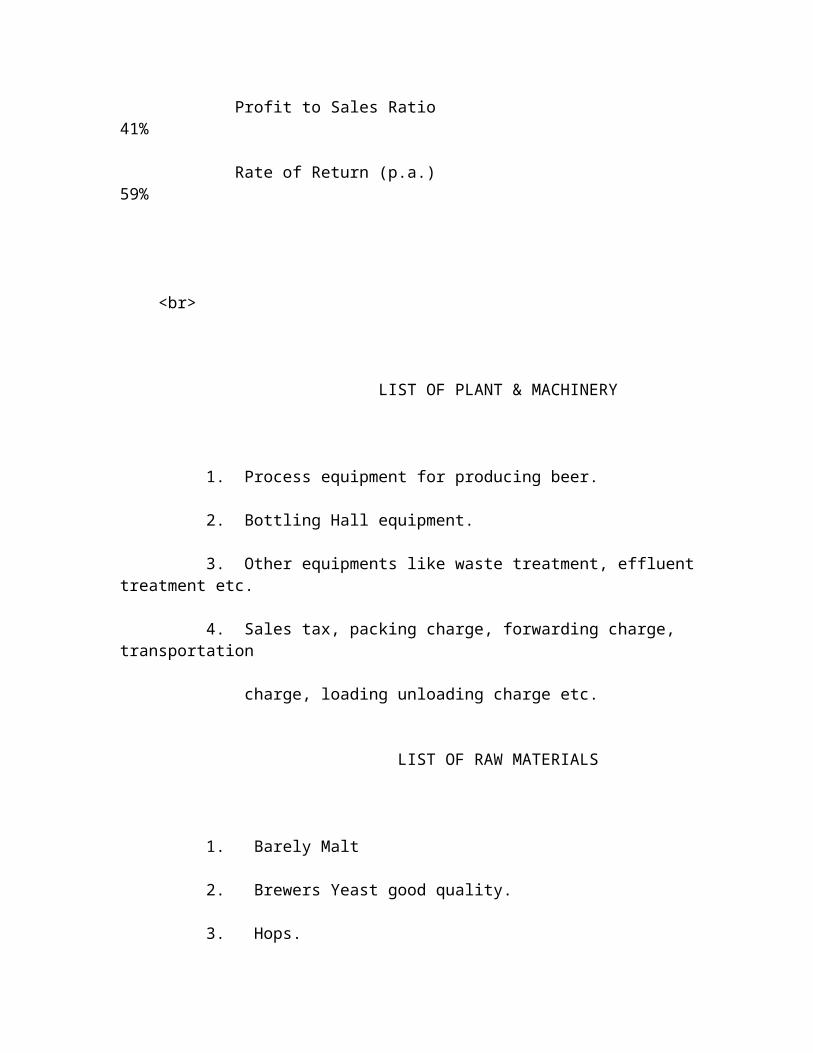

Profit to Sales Ratio 41%

Rate of Return (p.a.) 59%

<br>

LIST OF PLANT & MACHINERY

1. Process equipment for producing beer.

2. Bottling Hall equipment.

3. Other equipments like waste treatment, effluent treatment etc.

4. Sales tax, packing charge, forwarding charge, transportation

charge, loading unloading charge etc.

LIST OF RAW MATERIALS

1. Barely Malt

2. Brewers Yeast good quality.

3. Hops.

4. Glass Bottles.

5. Other Miscellaneous

(a) Urea.

(b) Ammonium Nitrate.

(c) Enzyme.

<br>

PROJECT MANAGEMENT & CONSTRUCTION SCHEDULE ------------------------------------------

INTRODUCTION : -------------- Project management and project planning has a direct impact on

construction schedule. The length of the gestation period destermines

not only the quantum of financial charges such as interest but also

project costs. It also effects the provision for contigencies which is

linked with price movements. Since price movements has althrough

adopted an upward trend, the gestation period could have a very

significant bearing on the total capital cost. Any extension in time

schedule may also alter the market structure with the emergence of new

completitors.

PROJECT HANDLING: ---------------- The total project activities can be broadly divided into two groups. In

the first group, there will be activities involving approval firm

various governmet department such as registration of the company with

local office of the Registrar of Companies in the in the department of

company Affairs, registration or letters of intent with DGTD or other

statutory body, allotment of land, sanction of power connection, no

objection certificate from pollution control board, sanction of long

term loans from Financial Institutions, cash credit facility with bank

etc. Approval of foreign collabration from competent authouity,

clearance from SEBI for pulic issueetc. are necessary.

<br>

(YOU CAN BRIEFLY WRITE THE ACTUAL STATUS AND FUTURE PLANNING OF THE PROPOSED PROJECT AS EXPLAINED IN THE FOLLOWING EXAMPLE).

In proposed case promoters already purchased the required land and

formalties of diversion is already completed. Clearance from pollution

control brad is not required. Further the state electricity borad has

already given their written consent for necessary power connection and

lastly the financial instiution has agreed to provide working capital

finace. The major part of formalities are in progress and as soon as

the term loan is approved by bank and actual implementation os the

project can be started without delay.

Further firm has already selected consultants for necessary technical

assistance in selected of plant and machinery etc. Civil drawing

details layout is already prepared to avoid delay.

PROJECT SCHEDULING : ------------------- The management will be scheduling these activities so as to complete

the job in an acceptable time span and finally control the conduct of

the scheduled work. In matters of planning. themamagement will consider

the requirement, availability and employment of the necessary man power

and facilities for carrying out the programme in such a manner that

cost and time required are properly balanced and excessive demands on

key resources is avoided.

<br>

PROJECT CONSTRUCTION SCHEDULE : ------------------------------- A detailed programme in the form of CPM network will be prepared

convering all the key contracts. The detailed will highlight the dates

for i)Invitation of tendrs, ii) receipt of quotations iii) Scrutiny of

bids, iv) receipt of materials and eqipment and machinery taking into

consideration the time required for preparation of bids and delivery

periods of various purchased items. A schedule of work in will be

prepared to set in detail all the units comprising the project. A

complete procurement specification will be prepared for each item of

plant and machinery and for civil and structural work.

TIME SCHEDULE: -------------- A construction programme has been developed to accomplish the desired

objectives within a time span which is as short aas possible without

being excessively curtailed. A time span of Eight months for project

completion defined by erection and commissioning of the plant is

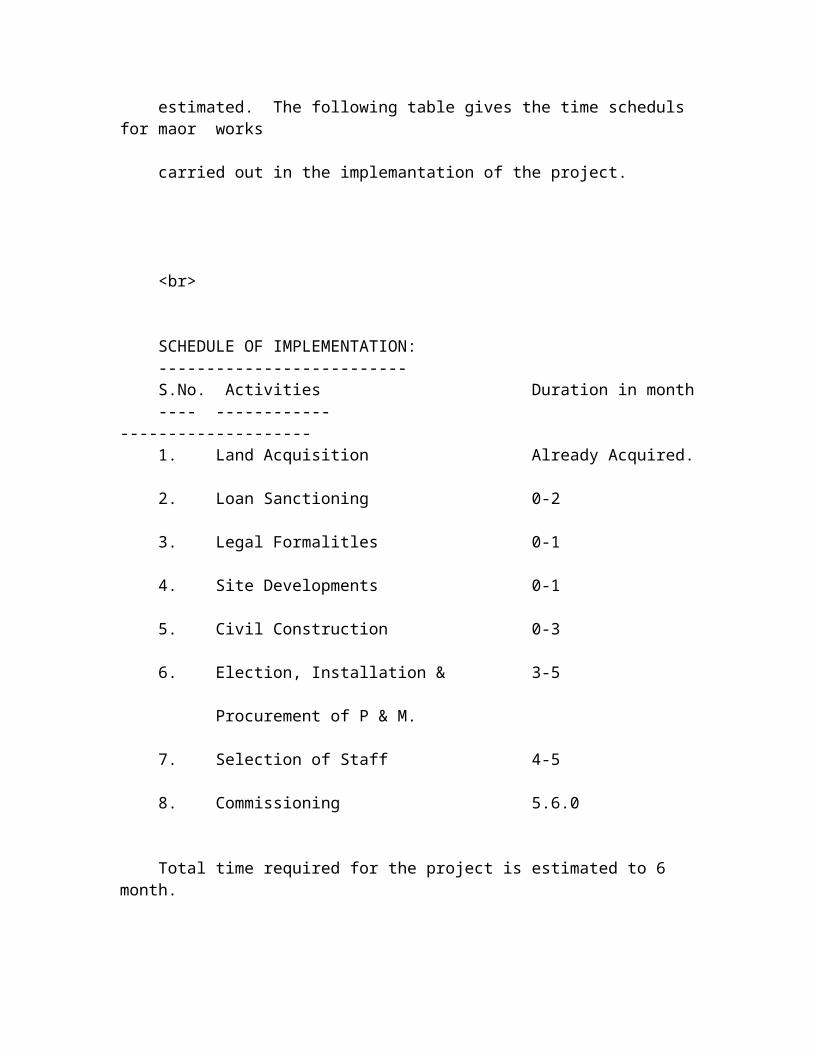

estimated. The following table gives the time scheduls for maor works

carried out in the implemantation of the project.

<br>

SCHEDULE OF IMPLEMENTATION: -------------------------- S.No. Activities Duration in month ---- ------------ -------------------- 1. Land Acquisition Already Acquired.

2. Loan Sanctioning 0-2

3. Legal Formalitles 0-1

4. Site Developments 0-1

5. Civil Construction 0-3

6. Election, Installation & 3-5

Procurement of P & M.

7. Selection of Staff 4-5

8. Commissioning 5.6.0

Total time required for the project is estimated to 6 month.

<br>

PRINCIPLES OF PLANT LAYOUT --------------------------

Some of the guiding principles for detailed plant layout will be

discussed for the benefit of those making layout decisions for the

first time.

Storage Layout : Storage facilities for raw materials and intermediate

and finished products may be located in isolated areas or in adjoining

areas. Hazardous materials become a decided menace to life and

property when stored in large quantities and should consequently be

isolated. Storage in adjoining areas to reduce materials handling may

introduce an obstacle toward future expansion of the plant. Arranging

storage of materials so as to facilitate or simplify handling is also a

point to be considered to design. Where it is possible to pump a

single material to an elevation so that subsequent handling can be

accomplished by gravity into intermediate reaction and storage units,

costs may be reduced. Liquids can be stored in small containers,

barrels,s horizontal or vertical tanks and vats, either indoors or out

of doors.

Equipment Layout : In making a layout, ample space should be assigned

to each piece of equipment ; accessibility is an important factors for

maintenance.

<br>

It is extremely poor economy to fit the equipment layout too

closely into a building. A slightly larger building than appears

necessary will cost little more than one that is crowded. The extra

cost will indeed be small in comparison with the penalties that will be

extracted if, in order to iron out the kinks, the building must be

expanded.

The operations that constitute a process are essentially a series

of unit operations that may be carried on simultaneously. These

include filtration, evaporation, crystallization, separation, and

drying. Since these operations, are repeated several times in the flow

of materials, kit should be possible to arrange the necessary equipment

into groups of the same kinds possible to arrange the necessary

equipment into groups of the same kinds. This sort of layour will make

possible a division of operation labour so that one or two operators

can be detailed to tend all equipment of a like nature.

<br>

The relative levels of the several pieces of equipment and their

accessories determine their placement. Although gravity flow is

usually preferable, it is not altogether necessary because liquids can

be transported by lowing or by pumping, and solids can be moved by

mechanical means. Gravity flow may be siad to acost nothing to

operate, whereas the various mechanical means of transportation involve

the first cost of the necessary equipment and the cost of operation and

maintenance. But material must be elevated to a level where gravity

flow must start. However, gravity flow usually means a multistory

layout, whereas the factors favoring a single-story plant may largely,

if not entirely, compensate for the cost of mechanical transportation.

Access for intial construction and maintenance is a necessary part

of planning. for example, overhead equipment must have space for

lowering into place, and heat-exchange equipment should be located near

access areas where trucks or hoist can be dplaced for pulling and

replacing tube bundles. Thus, space should be provided for repair and

replacement equipment, such as cranes and forked trucks, as well as

access way around doors and underground hatches.

<br>

Safety : A great deals of planning is governed by local and national

safety and fire code requirements. Fire protection consisting of

reservoirs, mains, hydrant, hose houses, fire pumps, reservoirs,

sprinklers in building, explosion barriers and directional routing of

explosion forces to clear areas, and dikes for combvustible-product

storage tanks must be incorporated to protect costly plant investment

and reduce insurance rates.

Plant Expansion : Expansion must always be kept in mind. The

question of multiplying the number of units or increasing the size of

the prevailing unit merits more study than it can be given here.

Suffice it to say that one must exercise engineering judgement ; that

as a penalty for bad judgement, scrapping of present serviceable

equipment constitutes but one phase, for shutdown due to remodeling may

involve a greater loss of money than that due to rejected equipment.

Nevertheless, the cost of change must sometimes be borne, for the

economies of larger units may, in the end, make replacement imperative.

<br>

Floor Space : Floor space may or may not be a major factor in the

design or a particular plant. The value of land may be a considerable

item. the engineers however, follow the rule of practicing economy of

floor space, consistent with good housekeeping in the plant land with

proper consideration give to line flow of materials, access to

equipment, space to permit working on parts of equipment that need

frequent servicing, and safety and comfort of the operators.

Utilities Servicing : The distribution of gas, air, water, steam,

power, and electricity is not always a major item, inasmuch as the

flexibility of distribution of these serivces permits designing to meet

almost any condition. But a little regard for the proper placement of

each of these services, practicing good design, aids in ease of

operation, orderliness, and reduction in costs of maintenance. No

pipes should be laid on the floor or between the floor and the 7-ft

level, where the operator must pass or work. Chaotic arrangement of

piping invites chaotic operation of the plant. The flexibility of

standard pipe fittings and power-transmission mechanisms renders this

problem one of of minor diffculty.

<br>

Building : After a complete study of quantitative factors, the seletion

of the building or buildings must be considered. Standard factory

buildings are to be desired, but, if none can be found satisfactory to

handle the space and process requirements of the chemical engineer,

then a competent architect should be consulted to design a building

around the process - not a beautiful structure into which a process

must fit. It is fundamental in chemical engineering industries that

the buildings should be built arount the process, instead of the

process being made to fit building of conventional design.

In many cases only the control area requires housing, with the

process equipment eracted outdoors. This is known as outdoor

consturction and such layouts should be considered for many types of

plants. What consideration must be given to buildings depends upon

conditions. It the designer must adapt his design to fit and old

building or building space already erected, his problem is cut out for

him and be was limiting conditions. However, the selection of the

design of a new building to meet the requirements of the process is

more scientific. In this case, one finds before him practically all

types of standard building, built in units, interlocking or otherwise,

ready for shipment and erection.

<br>

Throughout chemical industry, much thought must be given to the

disposal of waste liquors, fumes, dusts, and gases. Ventilation, fume

elimination, and drainage may require the installation of extra

equipment. This may involve the design of the individual pieces of

operating equipment, or it may require the installation of isolated

equipment. If the latter be the case, the location of such equipment

where it will be interfere with the flow of materials in process should

be practiced. The selection of the proper piece of equipment for doing

this service is also an important point; the less attention the

ventilating, fume, or waste-elimination systems require, the better

service they may render. Sometimes air conditioning of the plant is

called for an may required an elaborate setup. But the installation of

such equipment, when needed, pays in better service from operators,

less discomfort, greater production, and a better morale than when such

conditions are left to nature.

<br>

It must be recognized that there is not only one solution to the

problem of layout of the equipment. There are many rational designs.

Which plant to adopt must be decided upon after exercise of engineering

judgement and after striking a balance job the advantages and

disadvantages of each possible choice.

Material-handling Equipment : Consideration of equipment for materials

handling is only a minor factor in most cases of handling devices. But

where this operation is paramount in a process, serious thought must be

given to it. Again it should be said that engineering judgement must

be exercised. Whenever possible, one should take advantage of the

topography of the site location, one should take advantage in the

process.

Railcoads and Roads : Existing or possible future railroads and

highways adjacent to the plant must be known in order to plan rail

siding and access roads within the plant. Railroad spurs and roadways

of the correct capacity and at the right location should be provided

for ina traffic study and over-all master track and road plan of the

plant area. Some of the factors in rail-track planning are :

<br>

1. Existing and future off-site main rail facilities.

2. Permissible radius of curvature for spurs - consult local rail

authorities.

3. Provision for traffic handling - arrangement of spurs and ladder

track and switching.

4. Adequate spur facilities

a. Loading and unloading facilities for initial plant

construction and subsequent operations. b. Rack stations for liquid handling

c. Storage space for full and empty cars.

d. Space for cleaning and car repairs.

Major provisions in road planning for multipurpose service are :

1. A means of interplant movement for road traffic, both pedestrian

and vehicular

2. Heavier and wider roads for large-scale traffic

3. Routing of heavy traffic outside the operational areas

4. Roadways for access to initial construction, maintenance, and

repair points

5. Roadways to isolated points, storage tanks, and safety equipment,

such as fire hydrants.

<br>

PLANT LOCATION FACTORS ----------------------

Factors which generally apply to the economic and operability

aspect of plant site location are classified into two major groups.

The primary factors listed apply to choice of a region, whereas the

specific factors looked at in choosing an exact site location whithin

the region. All factors are important in making a site location

selection.

Primary Factors ------- -------

1. Raw - material supply :

a. Availability form existing or future suppliers

b. Use of substitute materials

c. Distance

2. Markets :

a. Demand versus distance

b. Growth or decline

c. Inventory storage requirements

d. Competition - present and future.

3. Power and fuel supply :

a. Availability of electricity and various type of fuel

b. Future reservers

c. Costs

<br>

4. Water supply :

a. Quality - temperature, mineral content, bacteriological content.

b. Quantity

c. Dependability - may involve reservoir construction

d. Costs.

5. Climate :

a. Investment required for construction

b. Humidity and temperature conditions

c. Hurricane, a tornado, and earthquake history.

Specific Factors -------- -------

6. Transportation :

a. Availability of various services and projected rates 1. Rail - dependable for light and heavy shipping over all distances

2. Highways - regularly used for short distance and generally small quantities

3. Water - cheaper, but may be slow and irregular

4. Pipeline - for gases and liquids, particularly for petroleum products

5. Air - for business transportation of personnel

<br>

7. Waste disposal :

a. Regulations laws

b. Stream carry-off possibilities

c. Air-pollution possibilities

8. Labor : 1. Availability of skills

2. Labor relations - history and stability in area

3. Stability of labor rates

9. Regulatory laws :

a. Building codes

b. Zoning ordinances

c. Highway restrictions

d. Waste - disposal codes

10. Taxes :

a. State and local taxes

1. Income

2. Unemployment insurance

3. Franchise

4. use

5. Property

b. Low assessment or limited term exemptions to attract industry

11. Site characteristics :

a. Contour of site

b. Soil structure

c. Access to rail, highway, and water

d. Room for expansion

e. Cost of site

f. Site and facilities available by expansion on present company-owned property

<br>

12. Community factors :

a. Rural or Urban

b. Housing costs

c. Cultural aspects - churches, libra ries, theaters

d. School system

e. Recreation facilities

f. Medical facilities - hospitals, doctors

13. Vulnerability to wartime attack :

a. Distance form important facilitics

b. General industry concentration

14. Flood and fire control :

a. Fire hazards in surrounding area

b. Floor history and control

<br>

COST OF THE PROJECT ------------------- Rs in Lacs

--------------------------------------------------------- PARTICULARS AMOUNT ---------------------------------------------------------

Land 36.00

Site Development 8.00

Building & Civil Works 656.00

Plant and Machinery 1700.00

Electricals Installation 70.00

Misc Fixed Assets 20.00

Pre Operative Expenses 1.25

Provision For Contengencies 122.76

--------------------------------------------------------- Total Fixed Cost 2614.01

Margin Money for working Capital 62.74 ---------- Total Cost of Project 2676.76 ==========

<br>

ALLOCATION OF PRE-OP AND CONTENCIES Rs in Lacs ----------------------------------------------------------------- PARTICULARS Pre-Op Contengc Basic Total Cost Cost -----------------------------------------------------------------

Site Development 0.00 0.40 8.00 8.40

Building & Civil Works 0.33 32.82 656.00 689.15

Plant and Machinery 0.87 85.04 1700.00 1785.91

Electricals Installation 0.04 3.50 70.00 73.54

Misc Fixed Assets 0.01 1.00 20.00 21.01

----------------------------------------------------------------- 1.25 122.76 2454.00 2578.01 -----------------------------------------------------------------

<br>

WORKING CAPITAL REQUIREMENT-----------------------------------------------------------------------------------------------------------Item Ma Ist Year IInd Year rg -------------------------------------------------- in Marg. Bnk. Total Marg. Bnk. Total--------------------------------------------------------------------------------Raw Material 25 16.25 48.75 65.00 18.96 56.88 75.83

Work in Progress 25 0.75 2.24 2.98 0.85 2.54 3.38

Finished Goods 25 23.44 70.31 93.75 27.34 82.03 109.38

Debtors 10 18.75 56.25 75.00 21.88 65.63 87.50

Expenses 100 3.56 10.68 14.25 3.91 11.73 15.63

-------------------------------------------------- 62.74 188.23 250.98 72.93 218.79 291.73

Less : Creditors 0.00 32.50 32.50 0.00 37.92 37.92

--------------------------------------------------Net WC required 62.74 155.73 218.48 72.93 180.88 253.81--------------------------------------------------------------------------------

Raw material One Month Finished Goods 15 days work in progress one day Debtors 15 days

expenses one month

<br>

PROJECTED PROFIT AND LOSS ACCOUNT --------------------------------- Rs. in Lacs ----------------------------------------------------------------- OPERATING YEARS Particulars------------------------------------------------------ i ii iii iv v ----------------------------------------------------------------- Capacity Utilisation as a % of installed c 50 60 70 70 70

--------------------------------------------

Sales 2250.00 2625.00 3000.00 3000.00 3000.00

Variable Cost

Raw Material 780.00 910.00 1040.00 1040.00 1040.00

Salary & Wages 90.00 105.00 120.00 120.00 120.00

Power Charges 9.99 11.65 13.32 13.32 13.32

Fuel

Repair & Maintenance 2.00 2.00 2.00 2.00 2.00

Packing Material

Insurance 39.21 39.21 39.21 39.21 39.21

Depreciation (S L M) 166.93 166.93 166.93 166.93 166.93 --------------------------------------------

Total Variable Cost 1088.12 1234.79 1381.45 1381.45 1381.45

Gross Profit 1161.88 1390.21 1618.55 1618.55 1618.55

Fixed Expenses

& Selling exp. --------------

Salary 25.00 25.00 25.00 25.00 25.00

Administrative Expens 4.75 4.75 4.75 4.75 4.75

Selling Exp. 225.00 26.25 30.00 30.00 30.00 -------------------------------------------- Net Profit before tax & Intt & Depreciation 907.13 1334.21 1558.80 1558.80 1558.80

Interest on term loan 248.84 195.04 141.23 87.43 33.63

Interest on Working 23.36 27.13 30.90 30.90 30.90 Capital -------------------------------------------- Net profit before tax 634.93 1112.04 1386.66 1440.46 1494.27

Income tax 59.34 209.78 291.13 317.91 341.00 -------------------------------------------- Net profit 575.59 902.27 1095.53 1122.56 1153.27 --------------------------------------------

<br>

PROJECTED CASH FLOW STATEMENT----------------------------- Rs. in Lacs-------------------------------------------------------------------------Particulars CONSTN i ii iii iv v PERIOD-------------------------------------------------------------------------SOURCES OF FUNDS----------------

Increase in Capital 883.33 0.00 0.00 0.00 0.00 0.00

Increase in Unsecured 0.00 0.00 0.00 0.00 0.00 0.00

Increase in Term Loan 1793.43 0.00 0.00 0.00 0.00 0.00

Increase in WC Loan 0.00 155.73 25.14 25.14 0.00 0.00

Net ProfitBefore Intt & Tax 0.00 883.77 1307.08 1527.89 1527.89 1527.89

Depreciation 0.00 166.93 166.93 166.93 166.93 166.93 ----------------------------------------------------

TOTAL SOURCES (A) 2676.76 1206.43 1499.15 1719.97 1694.82 1694.82

----------------------------------------------------

DISPOSITION OF FUNDS--------------------Increase in capital e 2614.01 0.00 0.00 0.00 0.00 0.00

Increase in Working C 0.00 218.48 35.33 35.33 0.00 0.00

Decrease in term Loan 0.00 358.69 358.69 358.69 358.69 358.69

Intt on Term Loan 0.00 248.84 195.04 141.23 87.43 33.63

Income Tax 0.00 59.34 209.78 291.13 317.91 341.00 ----------------------------------------------------TOTAL DISPOSITIONS(B) 2614.01 885.34 798.83 826.38 764.02 733.31 ----------------------------------------------------

Net Surplus (A - B) 62.74 321.09 700.32 893.58 930.80 961.51

Opening Balance 0.00 62.74 383.83 1084.15 1977.74 2908.54

Closing Balance 62.74 383.83 1084.15 1977.74 2908.54 3870.05

-------------------------------------------------------------------------

<br>

PROJECTED BALANCE SHEET------------------------------------------------------------------------------------------------Particulars CONSTN i ii iii iv v PERIOD-------------------------------------------------------------------------

LIABILITIES-----------

Capital 883.33 883.33 883.33 883.33 883.33 883.33

Unsecured Loan 0.00 0.00 0.00 0.00 0.00 0.00

Reserves & Surplus 0.00 575.59 1477.86 2573.39 3695.94 4849.21

Term Loan 1793.43 1434.74 1076.06 717.37 358.69 0.00

Working Capital Loan 0.00 155.73 180.88 206.02 206.02 206.02

---------------------------------------------------- TOTAL : 2676.76 3049.39 3618.12 4380.11 5143.98 5938.56 ----------------------------------------------------

ASSETS :--------Gross Block 2614.01 2614.01 2614.01 2614.01 2614.01 2614.01

Less : Depreciation 0.00 166.93 333.85 500.78 667.71 834.64

Net Block 2614.01 2447.09 2280.16 2113.23 1946.30 1779.38

Net Current Assets 0.00 218.48 253.81 289.14 289.14 289.14

Cash & Bank Balance 62.74 383.83 1084.15 1977.74 2908.54 3870.05 ---------------------------------------------------- TOTAL : 2676.76 3049.39 3618.12 4380.11 5143.98 5938.56-------------------------------------------------------------------------

<br>

Interest and Repayment schedule ---------------------------------------------------- Opn Bal Insmnt Clo Ba Yr.Pay. Qtr Int Yr Int ---------------------------------------------------- 1793.43 89.67 1703.76 67.254 1703.76 89.67 1614.08 63.891 1614.08 89.67 1524.41 60.528 1524.41 89.67 1434.74 358.69 57.165 248.84

1434.74 89.67 1345.07 53.803 1345.07 89.67 1255.40 50.440 1255.40 89.67 1165.73 47.077 1165.73 89.67 1076.06 358.69 43.715 195.04

1076.06 89.67 986.38 40.352 986.38 89.67 896.71 36.989 896.71 89.67 807.04 33.627 807.04 89.67 717.37 358.69 30.264 141.23

717.37 89.67 627.70 26.901 627.70 89.67 538.03 23.539 538.03 89.67 448.36 20.176 448.36 89.67 358.69 358.69 16.813 87.43

358.69 89.67 269.01 13.451 269.01 89.67 179.34 10.088 179.34 89.67 89.67 6.725 89.67 89.67 -0.00 358.69 3.363 33.63-------------------------------------------------------------------------

<br>

Depreciation Schedule (Straight Line Method) --------------------------------------------------------- Particulars Cost Rate Dep --------------------------------------------------------- Buildings 689.15 3.76 25.91 Plant and Machinery 1785.91 7.52 134.30 Electricals 73.54 7.52 5.53 Misc Fixed Assets 21.01 5.64 1.19 --------------------------------------------------------- 166.93 =========================================================

Depreciation Schedule (W.D.V. Method) Rs. in Lacs ----------------------------------------------------------------- Particulars Building Plant Misc Total MachenerFixed ElectricAssets -----------------------------------------------------------------

Total Cost 689.15 1859.45 21.01

Depreciation rate (%) 10.00 25.00 15.00

1 - Year Depreciation 68.92 464.86 3.15 536.93

W.D.V. -58.92 1394.59 17.86

2 - Year Depreciation -5.89 348.65 2.68 345.43

W.D.V. -53.02 1045.94 15.18

3 - Year Depreciation -5.30 261.48 2.28 258.46

W.D.V. -47.72 784.45 12.90

4 - Year Depreciation -4.77 196.11 1.94 193.28

W.D.V. -42.95 588.34 10.97

5 - Year Depreciation -4.29 147.09 1.65 144.44

W.D.V. -38.65 441.26 9.32

6 - Year Depreciation -3.87 110.31 1.40 107.85

W.D.V. -34.79 330.94 7.92

7 - Year Depreciation -3.48 82.74 1.19 80.45

W.D.V. -31.31 248.21 6.74

8 - Year Depreciation -3.13 62.05 1.01 59.93

W.D.V. -28.18 186.15 5.73

9 - Year Depreciation -2.82 46.54 0.86 44.58

W.D.V. -25.36 139.62 4.87

-----------------------------------------------------------------

<br>

INCOME TAX LIABILITY -------------------- Rs. in Lacs ----------------------------------------------------------------- OPERATING YEARS Particulars------------------------------------------------------ i ii iii iv v -----------------------------------------------------------------

Net profit before tax 634.93 1112.04 1386.66 1440.46 1494.27

Depreciation (S L M) 166.93 166.93 166.93 166.93 166.93

--------------------------------------------

Total 801.86 1278.97 1553.59 1607.39 1661.19

Less : Depreciation W.D.V. Method 536.93 345.43 258.46 193.28 144.44 --------------------------------------------

Net Profit 264.93 933.54 1295.13 1414.11 1516.76

Less : Decuction (80 I B) 25 % of Profit 66.23 233.38 323.78 353.53 379.19

-------------------------------------------- Taxable Profit 198.70 700.15 971.35 1060.59 1137.57

Income Tax 59.34 209.78 291.13 317.91 341.00

-----------------------------------------------------------------

<br>

DEBT SERVICE COVERAGE RATIO ---------------------------

----------------------------------------------------------------- OPERATING YEARS

Particulars------------------------------------------------------ i ii iii iv v -----------------------------------------------------------------

Net Profit 575.59 902.27 1095.53 1122.56 1153.27

Add: Depreciation 166.93 166.93 166.93 166.93 166.93

Interest 248.84 195.04 141.23 87.43 33.63

-------------------------------------------- Total Cash Available 991.35 1264.23 1403.69 1376.92 1353.82 Payment of Loan & Interest (A)

--------------------------------------------

Interest 248.84 195.04 141.23 87.43 33.63

Repayment of Principa 358.69 358.69 358.69 358.69 358.69

--------------------------------------------

Total Payment Obligat 607.52 553.72 499.92 446.11 392.31

Debt Service Coverage 1.63 2.28 2.81 3.09 3.45 Ratio --------------------------------------------

<br>

Break Even Point ---------------- Rs in Lacs -------- Sales Realisation 3750.00

Variable Cost ------------- Raw Material 1300.00 Salary and Wages 150.00 Power and Fuel 16.64

Factory Overheads 22.50 Repairs and maintenance 2.00 Selling Expenses 100.00 Interest on Working Capital 30.90 -------- Total Variable Cost 1622.05

Fixed Cost ---------- Administrative exp 250.00 Depreciation 166.93 interest on Term Loan 248.84 -------- Total Fixed Cost 665.77

Contribution = sales-Variable Cost 2127.95

Break Even Point = fist X 100/ contribu 31.29 Break Even Point in Terms Of Sales 1173.25

<br>

C O N C L U S I O N -------------------

In nutshall considering the excellent market

potentiality and good debt service coverage

ratio. Low BEP, the prospects for the

project are very bright so there seems no risk

to proprietor as well as to financial

institution.