beatrice scheubel* what do we know about the global ... · yes economic and political links with...

TRANSCRIPT

What do we know about the global financial safety net?

A new database.

ECB-PUBLIC

Beatrice Scheubel*Livio Stracca*European Central Bank

NBER Summer InstituteIFM data session

Boston, 10 July 2017

* The views expressed do not necessarily reflect those of the ECB or the European System of Central Banks

Rubric

www.ecb.europa.eu ©

Agenda

What do we know about the global financial safety net? 2

1

2 What is covered in the data set?

Why we do we need data on the Global Financial Safety Net?

3 How can the data be used?

ECB-PUBLIC

4 Concluding remarks

Appendix5

Rubric

www.ecb.europa.eu ©

Agenda

What do we know about the global financial safety net? 3

1

2 What is covered in the data set?

Why do we need data on the Global Financial Safety Net?

3 How can the data be used?

ECB-PUBLIC

4 Concluding remarks

Appendix5

Rubric

www.ecb.europa.eu ©

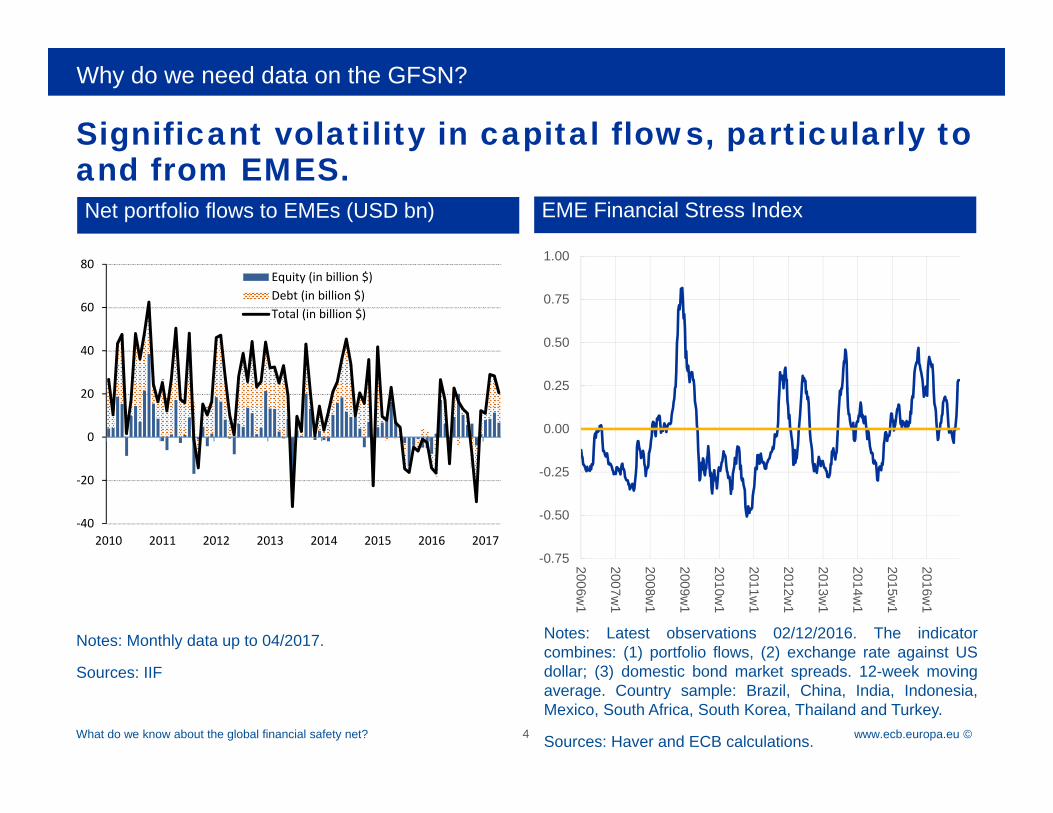

Significant volatility in capital flows, particularly to and from EMES.•Net portfolio flows to EMEs (USD bn) •EME Financial Stress Index

Why do we need data on the GFSN?

What do we know about the global financial safety net? 4

Notes: Monthly data up to 04/2017.

Sources: IIF

‐40

‐20

0

20

40

60

80

2010 2011 2012 2013 2014 2015 2016 2017

Equity (in billion $)Debt (in billion $)Total (in billion $)

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

2006w1

2007w1

2008w1

2009w1

2010w1

2011w1

2012w1

2013w1

2014w1

2015w1

2016w1

Notes: Latest observations 02/12/2016. The indicatorcombines: (1) portfolio flows, (2) exchange rate against USdollar; (3) domestic bond market spreads. 12-week movingaverage. Country sample: Brazil, China, India, Indonesia,Mexico, South Africa, South Korea, Thailand and Turkey.

Sources: Haver and ECB calculations.

Rubric

www.ecb.europa.eu ©

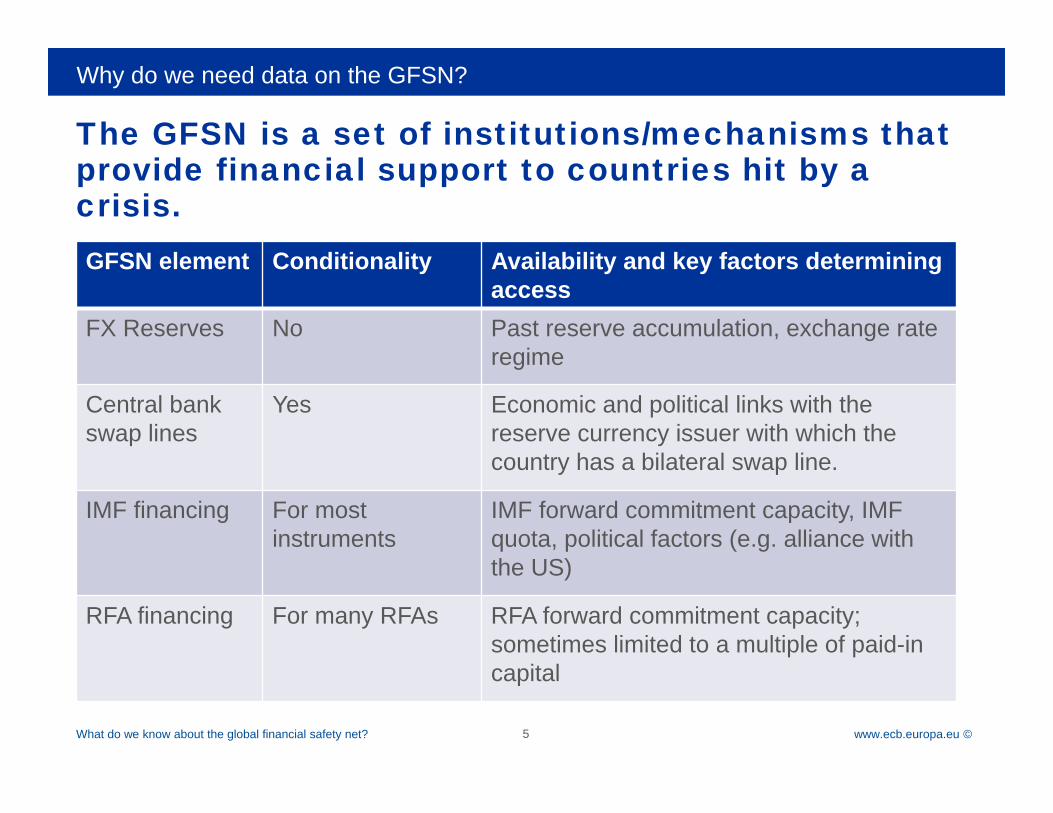

The GFSN is a set of institutions/mechanisms that provide financial support to countries hit by a crisis.GFSN element Conditionality Availability and key factors determining

accessFX Reserves No Past reserve accumulation, exchange rate

regime

Central bank swap lines

Yes Economic and political links with the reserve currency issuer with which the country has a bilateral swap line.

IMF financing For most instruments

IMF forward commitment capacity, IMF quota, political factors (e.g. alliance with the US)

RFA financing For many RFAs RFA forward commitment capacity; sometimes limited to a multiple of paid-in capital

Why do we need data on the GFSN?

What do we know about the global financial safety net? 5

Rubric

www.ecb.europa.eu ©

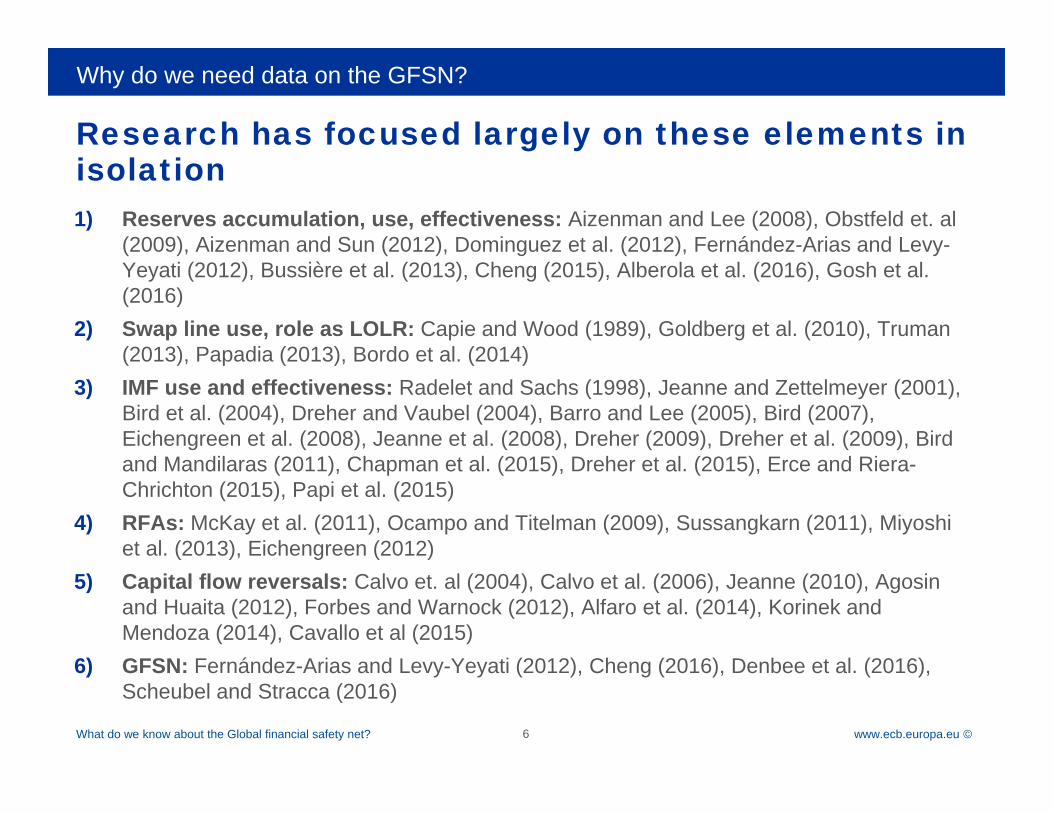

Research has focused largely on these elements in isolation1) Reserves accumulation, use, effectiveness: Aizenman and Lee (2008), Obstfeld et. al

(2009), Aizenman and Sun (2012), Dominguez et al. (2012), Fernández-Arias and Levy-Yeyati (2012), Bussière et al. (2013), Cheng (2015), Alberola et al. (2016), Gosh et al. (2016)

2) Swap line use, role as LOLR: Capie and Wood (1989), Goldberg et al. (2010), Truman (2013), Papadia (2013), Bordo et al. (2014)

3) IMF use and effectiveness: Radelet and Sachs (1998), Jeanne and Zettelmeyer (2001), Bird et al. (2004), Dreher and Vaubel (2004), Barro and Lee (2005), Bird (2007), Eichengreen et al. (2008), Jeanne et al. (2008), Dreher (2009), Dreher et al. (2009), Bird and Mandilaras (2011), Chapman et al. (2015), Dreher et al. (2015), Erce and Riera-Chrichton (2015), Papi et al. (2015)

4) RFAs: McKay et al. (2011), Ocampo and Titelman (2009), Sussangkarn (2011), Miyoshi et al. (2013), Eichengreen (2012)

5) Capital flow reversals: Calvo et. al (2004), Calvo et al. (2006), Jeanne (2010), Agosinand Huaita (2012), Forbes and Warnock (2012), Alfaro et al. (2014), Korinek and Mendoza (2014), Cavallo et al (2015)

6) GFSN: Fernández-Arias and Levy-Yeyati (2012), Cheng (2016), Denbee et al. (2016), Scheubel and Stracca (2016)

Why do we need data on the GFSN?

What do we know about the Global financial safety net? 6

Rubric

www.ecb.europa.eu ©

Agenda

What do we know about the global financial safety net? 7

1

2 What is covered in the data set?

Why we do we need data on the Global Financial Safety Net?

3 How can the data be used?

ECB-PUBLIC

4 Concluding remarks

Appendix5

Rubric

www.ecb.europa.eu ©

Existing GFSN data – harmonisedExisting data Added value

FX reserves WB World Development Indicators (WDI)

IMF International Financial Statistics (IFS)

Harmonized Database

Country levelLarge sample (198 countries)Annual frequency (1960-2014)

Stata & Excel

Publicly accessible at https://www.ecb.europa.eu/pub/rese

arch/occasional-papers/html/index.en.html

Swap lines Central bank websites

RFA lending RFA websites

IMF lending IMF Monitoring of Fund Arrangements (MONA)

IMF International Financial Statistics

WB World Development Indicators

MDB loans () MDB websites

Hedging instruments /

What is covered in the data set?

What do we know about the global financial safety net? 8

ECB-PUBLIC

Plus: crises data, private capital flow episodes, macro data

Rubric

www.ecb.europa.eu ©

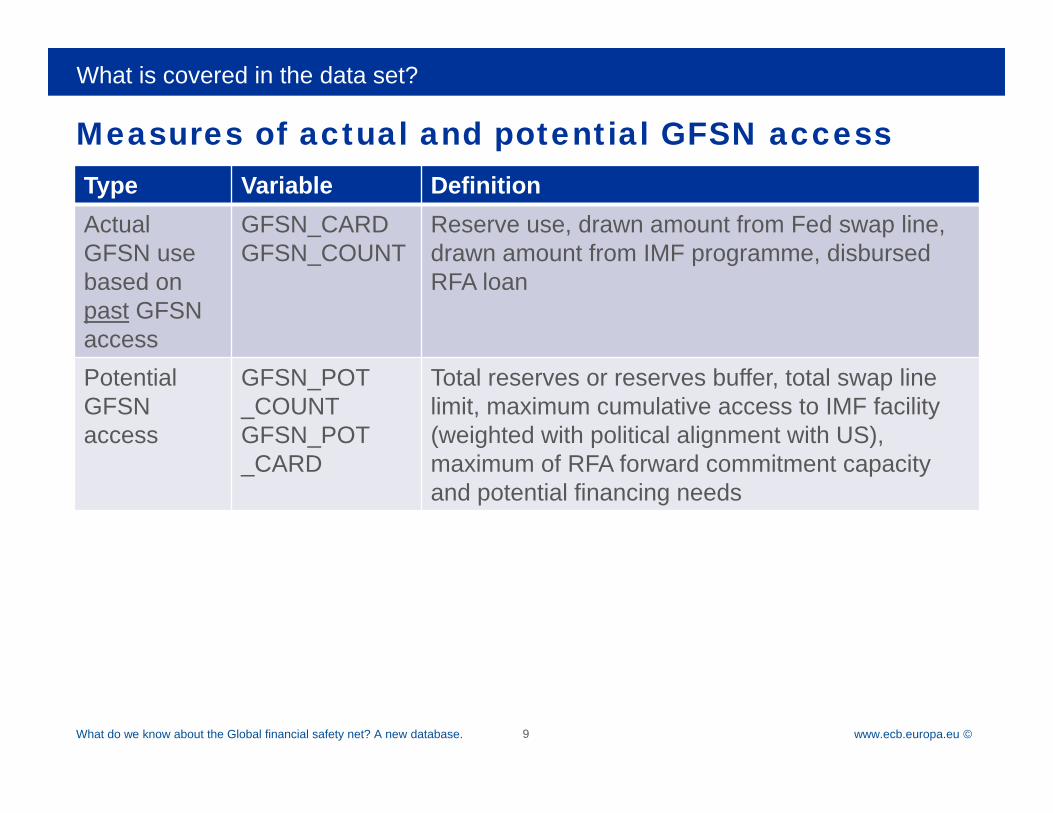

Measures of actual and potential GFSN accessType Variable DefinitionActual GFSN use based onpast GFSN access

GFSN_CARDGFSN_COUNT

Reserve use, drawn amount from Fed swap line, drawn amount from IMF programme, disbursed RFA loan

Potential GFSN access

GFSN_POT_COUNTGFSN_POT_CARD

Total reserves or reserves buffer, total swap line limit, maximum cumulative access to IMF facility (weighted with political alignment with US), maximum of RFA forward commitment capacity and potential financing needs

What is covered in the data set?

What do we know about the Global financial safety net? A new database. 9

Rubric

www.ecb.europa.eu ©

Agenda

What do we know about the global financial safety net? 10

1

2 What is covered in the data set?

Why we do we need data on the Global Financial Safety Net?

3 How can the data be used?

ECB-PUBLIC

4 Concluding remarks

Appendix5

Rubric

www.ecb.europa.eu ©

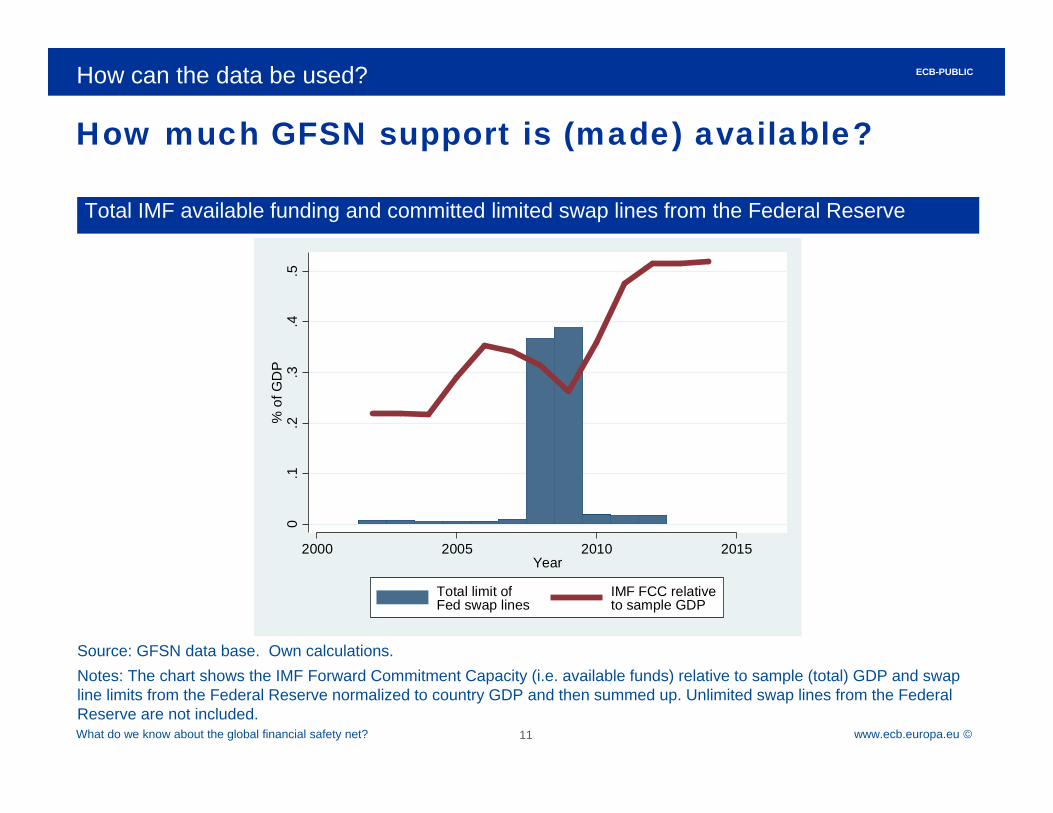

How much GFSN support is (made) available?

Source: GFSN data base. Own calculations. Notes: The chart shows the IMF Forward Commitment Capacity (i.e. available funds) relative to sample (total) GDP and swap line limits from the Federal Reserve normalized to country GDP and then summed up. Unlimited swap lines from the Federal Reserve are not included.

•Total IMF available funding and committed limited swap lines from the Federal Reserve

How can the data be used?

What do we know about the global financial safety net? 11

ECB-PUBLIC

0.1

.2.3

.4.5

% o

f GD

P

2000 2005 2010 2015Year

Total limit ofFed swap lines

IMF FCC relativeto sample GDP

Rubric

www.ecb.europa.eu ©

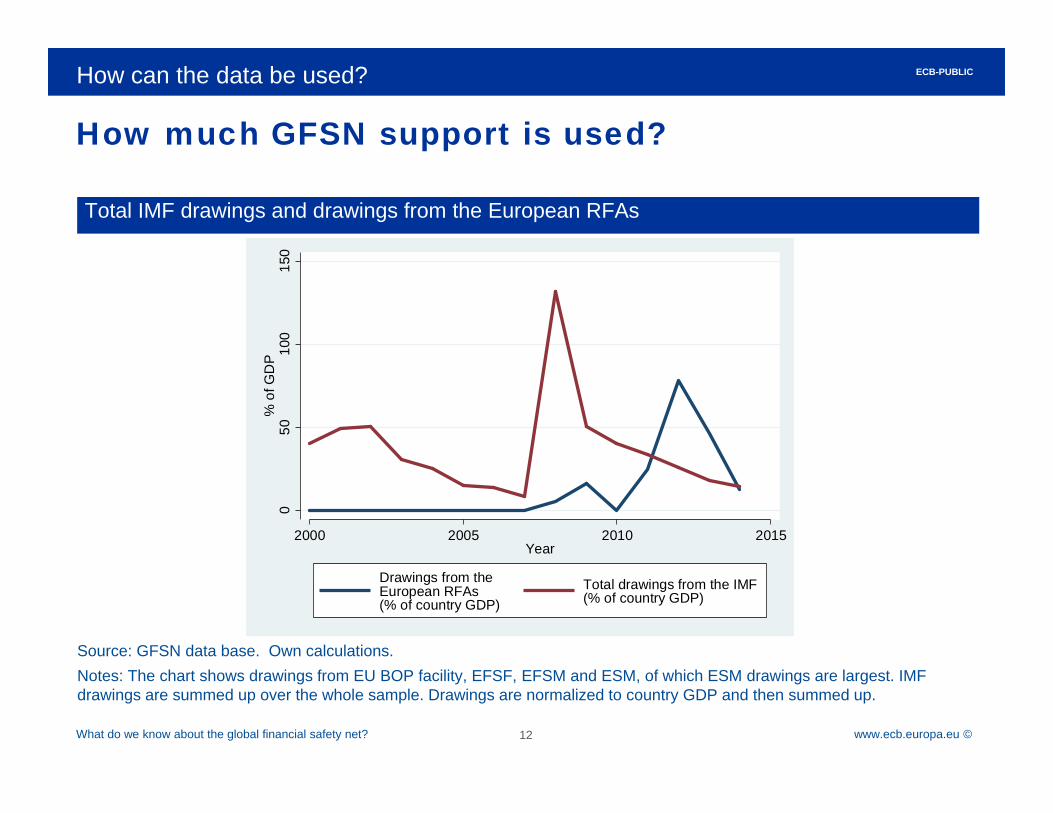

How much GFSN support is used?

Source: GFSN data base. Own calculations. Notes: The chart shows drawings from EU BOP facility, EFSF, EFSM and ESM, of which ESM drawings are largest. IMF drawings are summed up over the whole sample. Drawings are normalized to country GDP and then summed up.

•Total IMF drawings and drawings from the European RFAs

How can the data be used?

What do we know about the global financial safety net? 12

ECB-PUBLIC

050

100

150

% o

f GD

P

2000 2005 2010 2015Year

Drawings from theEuropean RFAs(% of country GDP)

Total drawings from the IMF(% of country GDP)

Rubric

www.ecb.europa.eu ©

0.5

11.

52

% o

f GD

P

2000 2005 2010 2015Year

Drawn IMF amount Drawn reserve amountDrawn RFA amount

Ecuador

01

23

45

% o

f GD

P

2000 2005 2010 2015Year

Drawn IMF amount Drawn reserve amount

ArgentinaBankingcrisis

Which layer of the GFSN will be used and when?

Source: GFSN data base. Own calculations. Notes: Reserve use defined as negative reserve flow whose absolute value is larger than the country-specific standard deviation; otherwise zero. Crises based on Laeven and Valencia (2012).

How can the data be used?

What do we know about the global financial safety net? 13

ECB-PUBLIC

•Argentina •Ecuador

Currencycrisis

Banking crisis start 1998, currency crisis start 1999

Rubric

www.ecb.europa.eu ©

Does GFSN use trigger or attenuate capital outflows?

Source: GFSN data base. Own calculations. Notes: GFSN_CARD adds disbursed IMF loans, disbursed RFA loans, drawn Fed swap lines and use of reserves defined as negative flow of reserves larger than country-specific standard deviation, measured as % of GDP.

•Argentina

How can the data be used?

What do we know about the global financial safety net? 14

ECB-PUBLIC

•Thailand

05

10

1960 1980 2000 2020

213

Drawn amount from the GFSN Private capital outflows

year

Graphs by 3-digit IMF country code

-50

510

1980 1990 2000 2010

578

Drawn amount from the GFSN Private capital outflows

year

Graphs by countrycode

Rubric

www.ecb.europa.eu ©

How do GFSN access and crisis outcomes compare between countries?

Source: GFSN data base. Own calculations.

•Greece

How can the data be used?

What do we know about the global financial safety net? 15

ECB-PUBLIC

•Latvia

-20

-10

010

20%

of G

DP

11.

52

2.5

% o

f GD

P

2000 2005 2010 2015Year

Drawings from theIMF

Drawings from theEU BOP facility(2nd axis)

Total private capitaloutflows (2nd axis)

Latvia

-10

010

20%

of G

DP

020

4060

% o

f GD

P

2008 2010 2012 2014 2016Year

Drawings from theEFSF/ESM

Drawings from theIMF

Total private capital outflows(2nd axis)

Greece

Rubric

www.ecb.europa.eu ©

Does GFSN use affect the duration of a sudden stop?

Source: GFSN data base. Own calculations. Notes: Change of reserves defined as negative reserves flow larger than country-specific standard deviation, measured as % of GDP. Sudden stop defined as in Forbes and Warnock (2012), applied to measure of private capital flows provided in the data base. Capital account restrictions as measured by Fernández et al. (2015). Below average restrictions defined as overall restrictions index below sample median.

•Below-average cap. account restrictions

How can the data be used?

What do we know about the global financial safety net? 16

ECB-PUBLIC

•Above-average cap. account restrictions

USAUSAUSAUSA

GBR

DNKDNK

NORNORSWESWECHECHECAN

JPNJPNJPN

ISL

NZLNZLNZL

PER ISRISREGYHKG

KOR

SGPSGP NGA

BGR

HUN

ROM

11.

21.

41.

61.

82

Av. d

urat

ion

of s

udde

n st

op (y

ears

)

0 .5 1 1.5Change in reserves ( % of GDP )

Change in reserves Fitted values

USAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSA

GBRGBRGBRGBRGBRGBRGBRGBRGBRGBRGBRGBRGBR

DNKDNKDNKDNKDNKDNKDNKDNKDNKDNKDNKDNKDNK

NORNORNORNORNORNORNORNORNORNORNORNORNORNORSWESWESWESWESWESWESWESWESWESWESWESWESWECHECHECHECHECHECHECHECHECHECHECHECHECHECANCANCANCANCANCANCANCANCANCANCANCANCANCAN

JPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPNJPN

ISLISLISLISLISLISLISLISLISLISLISLISL

TURTURTURTURTURTURTURTURTURTURTURTURTURTURTURTUR

AUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUS

NZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZL

ZAFZAFZAFZAFZAFZAFZAFZAFZAFZAFZAFZAFZAFZAF ARGARGARGARGARGARGARGARGARGARGARGARGARGARG

BRABRABRABRABRABRABRABRABRABRABRABRABRA

CHLCHLCHLCHLCHLCHLCHLCHLCHLCHLCHLCHLCHLCHLCHL

COLCOLCOLCOLCOLCOLCOLCOLCOLCOLCOLCOLCOL

MEXMEXMEXMEXMEXMEXMEXMEXMEXMEXMEXMEXMEXMEX PERPERPERPERPERPERPERPERPERPERPERPER

VENVENVENVENVENVENVENVENVENVENVENVENVENVENVEN

IRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRNIRN ISRISRISRISRISRISRISRISRISRISRISRISRISR

KWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWTKWT

SAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAUSAU

EGYEGYEGYEGYEGYEGYEGYEGYEGYEGYEGYEGYHKGHKGHKGHKGHKGHKGHKGHKGHKGHKGHKGINDINDINDINDINDINDINDINDINDINDINDINDINDINDIND

IDNIDNIDNIDNIDNIDNIDNIDNIDNIDNIDNIDNIDNIDNKORKORKORKORKORKORKORKORKORKORKORKORKOR

MYSMYSMYSMYSMYSMYSMYSMYSMYSMYSMYSMYSMYSMYSMYS

PAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAKPAK

PHLPHLPHLPHLPHLPHLPHLPHLPHLPHLPHLPHLPHLPHLPHL

SGPSGPSGPSGPSGPSGPSGPSGPSGPSGPSGPSGP

THATHATHATHATHATHATHATHATHATHATHATHATHATHATHATHA

NGANGANGANGANGANGANGANGANGANGANGANGAALBALBALBALBALBALBALBALBALBALBALBALBALB

BGRBGRBGRBGRBGRBGRBGRBGRBGRBGRBGRBGRBGR

RUSRUSRUSRUSRUSRUSRUSRUSRUSRUSRUSRUS

CHNCHNCHNCHNCHNCHNCHNCHNCHNCHNCHNCHNCHNCHN

UKRUKRUKRUKRUKRUKRUKRUKRUKRUKRUKRUKRCZECZECZECZECZECZECZECZECZECZECZECZE

HUNHUNHUNHUNHUNHUNHUNHUNHUNHUNHUN

LTULTULTULTULTULTULTULTULTULTULTULTULTU

HRVHRVHRVHRVHRVHRVHRVHRVHRVHRVHRVHRV MKDMKDMKDMKDMKDMKDMKDMKDMKDMKDMKDMKD

BIHBIHBIHBIHBIHBIHBIHBIHBIHBIHBIHBIHBIH

POLPOLPOLPOLPOLPOLPOLPOLPOLPOLPOLPOLPOLPOLPOL ROMROMROMROMROMROMROMROMROMROMROMROMROM

11.

21.

41.

61.

82

Av.

dur

atio

n of

sud

den

stop

(yea

rs)

0 .5 1 1.5Change in reserves ( % of GDP )

Change in reserves Fitted values

Rubric

www.ecb.europa.eu ©

Is potential GFSN access correlated with a country’s risk rating?

Source: PRS Group and GFSN data base. Own calculations. Notes: The chart shows a measure of potential access which adds the stock of reserves, maximum cumulative access under a standard IMF facility and the maximum of a country’s financing needs and an RFA’s forward commitment capacity.

•Correlation between the country composite risk rating and potential GFSN access

How can the data be used?

What do we know about the global financial safety net? 17

ECB-PUBLIC

ALB

ALBALBALBALBALBALBALB

ALB

ALB

ALB

ALB ALBALBALBALB

ALB

ALB ALBALBALB

ALBALBALBALBALB

ALBALB

ALBARGARG

ARGARGARG

ARGARGARG ARGARGARG

ARG

ARGARG ARGARGARG

ARGARGARG ARGARGARG

ARGARGARG ARGARG

ARG ARGARG AUS AUSAUSAUSAUSAUSAUSAUSAUS

AUSAUSAUSAUS AUSAUSAUSAUSAUSAUS AUSAUSAUSAUSAUSAUSAUSAUSAUSAUS AUSAUS

AUTAUTAUTAUTAUT

AUTAUTAUT AUTAUTAUTAUTAUTAUTAUT

AUTAUT

AUTAUTAUTAUT

AUTAUTAUT

AUTAUT

AUTAUT

AUTAUTAUTBELBELBEL

BELBELBELBELBELBELBELBEL BELBELBEL

BELBEL

BEL BELBEL

BELBEL

BELBEL BELBELBELBEL

BEL

BELBELBEL

BRABRA BRA BRA BRABRA BRA

BRABRA

BRABRA

BRABRABRABRA

BRABRABRABRABRABRA BRABRA BRABRABRABRABRA

BRA BRABRA

BGRBGR

BGR

BGR

BGRBGRBGRBGR

BGRBGR

BGRBGRBGR

BGR

BGR

BGRBGRBGRBGRBGR

BGR

BGRBGR

BGR

BGRBGRBGR

BGR

BGRBGR

CANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCANCHL CHL

CHLCHL CHL

CHL

CHL

CHL CHLCHL

CHL CHLCHL

CHL CHLCHL CHLCHL

CHL CHLCHL

CHLCHL

CHLCHLCHL CHLCHL

CHLCHL

CHLCHNCHN

CHNCHNCHN

CHN

CHN

CHNCHN

CHN CHN

CHNCHNCHNCHN

CHNCHN

CHN CHNCHN

CHN

CHNCHN

CHNCHN

CHNCHNCHN CHNCHNCOL

COLCOLCOL COLCOLCOLCOLCOL

COL COLCOL COLCOLCOLCOLCOLCOLCOL COL

COLCOLCOLCOL COL COLCOL COLCOL COLCOL

HRVHRV

HRVHRVHRVHRV HRVHRVHRVHRVHRV HRVHRVHRV

HRVHRV

CYP

CYPCYPCYPCYP

CYP

CYP

CYPCYP

CYPCYP CYP CYP

CYPCYP CYP

CYPCYP

CYPCYPCYP

CYPCYP

CYPCYPCYPCYPCYP

CYPCYP

CZECZECZE CZECZE CZECZECZE

CZECZE

CZECZECZECZE

CZECZE

CZECZE

CZE CZECZECZEDNK

DNKDNKDNK

DNKDNKDNKDNK

DNKDNKDNK DNKDNK

DNKDNKDNKDNKDNKDNKDNKDNK

DNK

DNKDNKDNKDNKDNK

DNK

DNKDNKDNKEGYEGY

EGY

EGYEGY

EGY

EGY

EGY

EGY

EGYEGYEGY

EGYEGY

EGYEGY

EGY

EGY

EGYEGYEGY

EGY

EGYEGY

EGYEGY

EGY

EGYEGYEGY

EGYEST

EST

ESTESTESTESTEST

ESTESTEST EST

ESTESTEST

EST

EST FINFINFINFIN FIN

FINFINFINFIN FINFINFINFINFINFINFINFIN

FINFINFINFIN

FINFINFIN

FINFINFINFINFINFINFINFRAFRA FRAFRAFRAFRAFRA

FRAFRAFRAFRA FRAFRAFRA FRAFRAFRAFRA FRAFRAFRAFRAFRAFRAFRAFRAFRA FRA

FRA FRA FRADEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUDEUGRCGRC

GRCGRC

GRC GRCGRC

GRC GRCGRCGRCGRCGRCGRCGRC GRCGRC

GRCGRC

GRCGRCGRC GRCGRCGRC

GRCGRC GRCGRC GRC

GRC

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKGHKG

HKG

HKG HKGHKG

HKGHKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKG

HKGHKG

HKG

HKG

HUNHUNHUN

HUNHUNHUN

HUNHUN

HUN HUNHUN

HUN

HUN

HUN

HUNHUNHUN

HUNHUN

HUNHUN

HUNHUN

HUN

HUN

HUN

HUN HUNHUNHUN

ISLISLISL ISLISLISL ISLISLISLISLISL

ISL

ISLISL

ISL

ISL

ISLISL

ISL

ISLISLISLISL

ISL

ISL

ISL

ISL

ISL

ISLISLISLIND

INDINDINDIND INDINDINDINDIND

INDINDIND

INDIND INDINDINDIND INDINDINDIND

INDIND

INDIND INDINDINDINDIDNIDN

IDNIDN

IDNIDN

IDNIDN

IDNIDNIDNIDN IDNIDNIDN

IDNIDN

IDNIDNIDN IDNIDNIDN IDNIDN IDNIDN

IDN

IDNIDNIDNIRN

IRNIRN

IRNIRN IRNIRNIRNIRN

IRNIRNIRN IRNIRNIRN IRNIRN IRNIRN IRNIRNIRN IRNIRN IRNIRNIRN IRNIRN

IRN IRNIRLIRL IRLIRL

IRL IRLIRLIRL

IRLIRL IRLIRL

IRL IRLIRL IRLIRLIRL

IRLIRL IRL

IRLIRLIRL IRLIRLIRL

IRLIRLIRL

IRL

ISRISR

ISR ISR

ISR

ISR

ISRISRISRISR

ISRISRISRISRISR ISRISR

ISR

ISRISRISRISRISRISRISR

ISR

ISRISR

ISR

ISR

ISR

ITAITA

ITAITAITA ITAITAITA

ITAITAITA

ITAITA

ITA ITAITAITAITAITA

ITA ITA ITAITAITA

ITAITA

ITAITA ITAITAITA JPNJPN

JPNJPN

JPN

JPN

JPN

JPN

JPNJPN

JPN

JPN

JPNJPN

JPN

JPN JPNJPN JPN

JPN

JPNJPNJPN

JPN

JPNJPN

JPN

JPNJPN

JPNJPN

KOR

KOR

KOR

KOR

KORKORKORKORKORKORKORKOR

KOR

KOR

KOR

KOR

KORKOR

KORKOR

KOR

KORKOR

KORKOR

KOR

KOR

KORKOR

KWTKWT

KWT

KWT

KWT

KWT

KWT

KWT

KWTKWT

KWTKWTKWT

KWT

KWT

KWT

KWTKWT

KWT KWT

KWTKWT

KWT

KWT

KWTKWT

KWT

KWT

KWT

KWTKWT

LVALVALVALVALVALVA

LVALVALVA LVALVA

LVALVA

LVA

LVA

LVALTULTULTULTULTULTULTULTULTULTULTULTU LTULTULTULTU

LUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUXLUX

MYS

MYSMYSMYS

MYS MYS

MYS

MYS

MYS

MYS

MYS

MYSMYS

MYSMYSMYS

MYS

MYS

MYS

MYS

MYS

MYSMYSMYS

MYSMYS

MYS

MYSMYSMYS

MYSMLT

MLT

MLT

MLT

MLT MLT

MLT

MLT

MLT

MLT

MLTMLT

MLT

MLT

MLT

MLT

MLT

MLTMLTMLT

MLT

MLTMLT

MLT

MLT

MLTMLTMLT

MEX

MEX

MEXMEXMEX

MEX

MEXMEX

MEXMEX

MEXMEXMEX

MEX

MEXMEX

MEX

MEXMEX

MEX

MEXMEX

MEX

MEX

MEXMEXMEX

MEX

MEXMEX

MEX NLDNLD

NLDNLD

NLDNLDNLDNLDNLD

NLDNLDNLDNLDNLD

NLDNLDNLDNLD NLDNLD

NLDNLD NLDNLD NLD

NLD

NLDNLD

NLDNLDNLDNZL NZLNZLNZLNZLNZLNZLNZL NZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZLNZL NZLNZLNZLNZLNZLNZLNZL

NGA NGANGA

NGANGANGA

NGANGANGA

NGA

NGANGANGA

NGANGA

NGA

NGANGA

NGA

NGANGA

NGANGA

NGA

NGA NGA

NGA

NGANGA

NGA

NGA

NORNORNORNOR

NOR NORNORNORNOR NORNORNOR

NORNORNOR NORNORNOR

NORNORNORNORNOR NOR

NORNOR NORNORNOR

NORNORPAKPAKPAKPAKPAKPAKPAK PAKPAK PAKPAKPAK

PAKPAK PAKPAKPAKPAK PAK

PAKPAKPAK

PAKPAKPAKPAKPAK PAKPAKPAK PAK

PERPERPERPERPERPERPERPERPERPERPER

PERPER PER PER

PERPERPER

PERPERPERPER PERPERPER

PERPER

PER

PERPER

PERPHL

PHLPHLPHL

PHLPHL

PHLPHLPHLPHL

PHLPHL

PHL

PHL

PHL

PHL

PHLPHL

PHL

PHLPHL

PHL

PHL

PHL PHLPHLPHLPHL

PHLPHL

PHL POL

POL

POLPOLPOLPOLPOLPOL

POLPOL

POLPOL

POL

POL

POLPOLPOL

POLPOLPOLPOLPOLPOL

POL

POL POLPOL

POLPOLPOL

PRT

PRT

PRTPRTPRT

PRT

PRTPRT PRTPRT

PRT

PRT

PRT

PRTPRTPRT PRT

PRTPRT

PRTPRTPRT PRTPRT

PRT

PRT PRT

PRT

PRT

PRT

PRT

ROMROMROMROM ROMROM

ROMROMROMROMROMROM ROM

ROMROM

ROM

ROMROM

ROM

ROMROM

ROM

ROMROM

ROM

ROMROM

ROMROM

ROMRUS

RUSRUS RUSRUS

RUSRUS

RUSRUS

RUSRUS

RUSRUSRUS

RUS

RUSRUSRUS

RUS

RUS

RUS

RUSSAU SAUSAUSAU

SAU

SAU

SAU

SAU

SAU

SAUSAUSAU

SAUSAU

SAU

SAU

SAU

SAU SAU

SAUSAU

SAU

SAU

SAU

SAU

SAU

SAUSAU SAU

SAUSAU SRBSRBSRBSRB SRBSRBSRB

SRB

SGP

SGP

SGP

SGP

SGPSGP

SGP

SGPSGP

SGP

SGP

SGP

SGPSGP

SGPSGPSGP

SGP

SGP

SGP

SGPSGP

SGP

SGPSGP

SGP

SGP

SGP

SGPSGPSGP

SVK

SVK SVKSVK

SVK

SVK

SVK

SVKSVK

SVKSVK

SVKSVKSVKSVKSVKSVK

SVKSVK

SVKSVK

SVKSVN

SVN

SVN

SVN

SVNSVN

SVN

SVN

SVNSVN

SVN

SVN

SVNSVN

SVNSVN

ZAFZAFZAF

ZAFZAF

ZAFZAFZAF

ZAFZAF

ZAFZAF ZAFZAFZAF ZAFZAF

ZAF ZAF ZAFZAFZAF ZAFZAFZAFZAFZAF

ZAFZAFZAF

ZAF ESPESPESPESP

ESPESPESP ESP

ESPESPESP

ESPESPESPESP ESP

ESPESP

ESPESP ESP

ESPESP ESPESP ESPESPESP ESPESPESP

SWESWESWESWESWESWESWESWESWESWESWESWESWESWESWESWESWE

SWESWESWESWESWESWESWESWESWESWESWESWESWE SWE

CHE

CHE

CHECHECHE

CHE

CHECHECHECHECHECHECHE

CHE

CHECHECHE

CHE

CHECHECHE

CHE

CHE

CHECHECHE CHECHECHE

CHE

CHE

THA

THATHA

THATHATHA

THA

THATHA

THA

THA

THA

THA

THA

THA THA

THA

THA

THATHATHATHA

THA THA

THA

THA

THA

THATHATHA

THATURTUR TURTUR

TURTURTURTURTURTUR

TURTUR TURTURTURTUR TURTURTURTUR

TURTUR TURTUR

TUR TURTURTURTURTUR TUR

UKR UKR UKRUKRUKRUKR

UKR

UKR UKR UKRUKRUKR

UKRUKRUKR

UKRAREARE ARE

ARE

ARE AREAREARE AREAREARE ARE AREARE ARE AREAREARE ARE

ARE AREAREAREAREAREAREAREARE

ARE AREAREGBR GBRGBRGBRGBRGBRGBRGBRGBRGBRGBRGBRGBR GBRGBR GBRGBRGBRGBR GBR

GBRGBR GBRGBRGBRGBR GBRGBRGBR GBRGBR USAUSAUSAUSAUSA USAUSA USAUSA USAUSA USAUSAUSAUSAUSAUSAUSA USAUSAUSA USA USAUSAUSAUSAUSAUSA USAUSAUSA

VEN

VEN

VEN VEN

VENVENVENVEN

VEN

VEN

VEN

VEN

VENVENVEN VENVENVEN VEN

VEN

VEN

VEN

VENVEN

VENVENVEN

VEN

VENVEN

VEN

050

100

150

200

Pot

entia

l GFS

N a

cces

s, %

of G

DP

20 40 60 80 100Composite risk rating (PRS)

Potential GFSN access Fitted values

Rubric

www.ecb.europa.eu ©

Agenda

What do we know about the global financial safety net? 18

1

2 What is covered in the data set?

Why we do we need data on the Global Financial Safety Net?

3 How can the data set be used?

ECB-PUBLIC

4 Concluding remarks

Appendix5

Rubric

www.ecb.europa.eu ©

• Global insurance against (financial) crises becomes more important.

• There is no clear single international lender of last resort.• To answer the question which institution would be in the best

position to provide lending for a particular crisis, we need to understand the interaction between the different layers of the GFSN.

• Our data base provides comprehensive data on both GFSN coverage and key macro variables.

• Correlation analysis suggests a relation between sudden stops and use of the GFSN (also confirmed by a local projections exercise)

• Follow-up work: Taming the global financial cycle. What role for global safety nets?

Concluding remarks

What do we know about the global financial safety net? 19

Rubric

www.ecb.europa.eu ©

Contact

Beatrice Scheubel:beatrice.scheubel(at)ecb.europa.euLivio Stracca:livio.stracca(at)ecb.europa.eu

Concluding remarks

What do we know about the global financial safety net? 20

Rubric

www.ecb.europa.eu ©

References

Manuel R. Agosin and Franklin Huaita. Overreaction in capital flows to emerging markets: Booms and sudden stops. Journal of

International Money and Finance, 31:1140 – 1155, 2012.

Enrique Alberola, Aitor Erce, and Jose Maria Serena. International reserves and gross capital flows dynamics. Journal of

International Money and Finance, 60:151 – 171, 2016.

Joshua Aizenman and Jaewoo Lee. Financial versus monetary mercantilism: Long-run view of large international reserves

hoarding. The World Economy, 31(5): 539 – 611, 2008.

Joshua Aizenman and Yi Sun. The financial crisis and sizable international reserves depletion: From ‘fear of floating' to the `fear

of losing international reserves'? International Review of Economics and Finance, 24:250 – 269, 2012.

Laura Alfaro, Sebnem Kalemli-Ozcan, and Vadym Volosovych. Sovereigns, upstream capital flows, and global imbalances.

Journal of the European Economic Association, 12:1240 – 1284, 2014.

Robert J. Barro and Jong-Wha Lee. IMF programs: Who is chosen and what are the effects? Journal of Monetary Economics,

52:1245 – 1269, 2005.

Graham Bird. The IMF: A bird's eye view of its role and operations. Journal of Economic Surveys, 21:683 – 745, 2007.

Concluding remarks

What do we know about the global financial safety net? 21

Rubric

www.ecb.europa.eu ©

References

Graham Bird and Alex Mandilaras. Once bitten: The effect of IMF programs on subsequent reserve behaviour. Review of

Development Economics, 15:264 – 278, 2011.

Graham Bird, Mumtaz Hussein, and Joseph P. Joyce. Many happy returns? Recidivism and the IMF. Journal of International

Money and Finance, 23(2): 231 – 251, 2004.

Michael D. Bordo, Owen Humpage, and Anna J. Schwarz. The evolution of the federal reserve swap lines since 1962. Working

Paper 1414, Federal Reserve Bank of Cleveland, 2014.

Matthieu Bussière, Gong Cheng, Menwie D. Chinn, and Noëmie Lisack. For a few dollars more: Reserves and growth in times

of crises. Journal of International Money and Finance, 52:127 – 145, 2013.

Guillermo A. Calvo, Alejandro Izquierdo, and Luis-Fernando Mejía. On the empirics of sudden stops: The relevance of balance-

sheet effects. IDB Publications (Working Papers) 6516, Inter-American Development Bank, 2004.

Guillermo A. Calvo, Alejandro Izquierdo, and Ernesto Talvi. Sudden stops and phoenix miracles in emerging markets. American

Economic Review, 96:405 – 410, 2006.

Forrest Capie and Geoffrey E. Wood. Monetary Economics in the 1980s. Macmillan, London, 1989.

Concluding remarks

What do we know about the global financial safety net? 22

Rubric

www.ecb.europa.eu ©

References

Eduardo Cavallo, Andrew Powell, Mathieu Pedemonte, and Pilar Tavella. A new taxonomy of sudden stops: Which sudden

stops should countries be most concerned about? Journal of International Money and Finance, 51:47 – 70, 2015.

Terrence Chapman, Songying Fang, Xin Li, and Randall W. Stone. Mixed signals: IMF lending and capital markets. British

Journal of Political Science, 1 – 21, 2015.

Gong Cheng. A growth perspective on foreign reserve accumulation. Macroeconomic Dynamics, 19(06):1358 – 1379, 2015.

Gong Cheng. The global financial safety net through the prism of g20 summits. Working Paper 13, ESM, 2016.

Edd Denbee, Carsten Jung, and Francesco Paternò. Stitching together the global financial safety net. Bank of England

Financial Stability Papers 36, 2016.

Kathryn M. E. Dominguez, Yuko Hashimoto, and Takatoshi Ito. International reserves and the global financial crisis. Journal of

International Economics, 88:388 – 406, 2012.

Axel Dreher. IMF conditionality: theory and evidence. Public Choice, 141:233 – 267, 2009.

Axel Dreher and Roland Vaubel. The causes and consequences of IMF conditionality. Emerging Markets Finance and Trade,

40:26 – 54, 2004.

Concluding remarks

What do we know about the global financial safety net? 23

Rubric

www.ecb.europa.eu ©

References

Axel Dreher, Jan-Egbert Sturm, and James Vreeland. Global horse trading: IMF loans for votes in the united nations security

council. European Economic Review, 53(7):742 – 757, 2009.

Axel Dreher, Jan-Egbert Sturm, and James R. Vreeland. Politics and IMF conditionality. Journal of Conflict Resolution,

59(1):120 – 148, 2015.

Barry Eichengreen. Regional financial arrangements and the international monetary fund. Working Paper 394, ABDI, 2012.

Barry Eichengreen, Poonam Gupta, and Ashoka Mody. Sudden stops and IMF supported programs. In Financial Markets

Volatility and Performance in Emerging Markets, pages 219 – 266. National Bureau of Economic Research, Inc, 2008.

Altor Erce and Daniel Riera-Crichton. Catalytic IMF? A gross flows approach. ESM Working Paper, 2015.

Andrés Fernández-Arias and Eduardo Levy-Yeyati. Global financial safety nets: Where do we go from here? International

Finance, 15(1):37 – 68, 2012.

Kristin J. Forbes and Francis Warnock. Capital flow waves: Surges, stops, flight, and retrenchment. Journal of International

Economics, 88:235 – 251, 2012.

Atish R. Gosh, Jonathan D. Ostry, and Charalambos G. Tsangarides. Shifting motives: Explaining the buildup in official

reserves in emerging markets since the 1980s. IMF Economic Review, pages 1 – 57, 2016.

Concluding remarks

What do we know about the global financial safety net? 24

Rubric

www.ecb.europa.eu ©

References

Linda S. Goldberg, Craig Kennedy, and Jason Miu. Central bank dollar swap lines and overseas dollar funding costs. NBER

Working Papers 15763, National Bureau of Economic Research, Inc, 2010.

Olivier Jeanne. Dealing with volatile capital flows. Policy Briefs PB10-18, Peterson Institute for International Economics, 2010.

Olivier Jeanne and Jeromin Zettelmeyer. International bailouts, moral hazard and conditionality. Economic Policy, 16(33):407 –

432, 2001.

Olivier Jeanne, Jonathan D. Ostry, and Jeromin Zettelmeyer. A theory of international crisis lending and IMF conditionality,

2008.

Anton Korinek and Enrique G. Mendoza. From sudden stops to Fisherian deflation: Quantitative theory and policy implications.

Annual Review of Economics, 6:299 – 332, 2014.

Julie McKay, Ulrich Volz, and Regine Wölfinger. Regional financial arrangements and the stability of the international monetary

system. Journal of Globalization and Development, 2:1948 – 1837, 2011.

Toshiyuki Miyoshi, Stephanie Segal, Preya Sharma, and Anish Tailor. Stocktaking the Fund's engagement with regional

financing arrangements. IMF, 2013.

Concluding remarks

What do we know about the global financial safety net? 25

Rubric

www.ecb.europa.eu ©

References

Maurice Obstfeld, J. C. Shambaugh, and A. M. Taylor. Financial instability, reserves, and central bank swap lines in the panic of

2008. American Economic Review, 99:480 – 486, 2009

Jose Antonio Ocampo and Daniel Titelman. Subregional financial cooperation: the south American experience. Journal of Post

Keynesian Economics, 32: 249 – 268, 2009.

Francesco Papadia. Central bank cooperation during the great recession. Policy contribution, Bruegel, 2013.

Luca Papi, Andrea F. Presbitero, and Alberto Zazzaro. IMF lending and banking crises. IMF Economic Review, 63(3):644 –

691, 2015.

Steven Radelet and Jeffrey D. Sachs. The east Asian financial crisis: diagnosis, remedies, prospects. Brookings Papers on

Economic Activity, 29:1 – 90, 1998.

Beatrice D. Scheubel and Livio Stracca. What do we know about the global financial safety net? Rationale, data and possible

evolution, 2016.

Chalongphob Sussangkarn. Chiang Mai Initiative Multilateralization: Origin, development, and outlook. Asian Economic Policy

Review, 6:203 – 220, 2011.

Edwin Truman. Enhancing the global financial safety net through central bank cooperation. 2013.

Concluding remarks

What do we know about the global financial safety net? 26