b.com-2 - weeblycityofcommercepk.weebly.com/uploads/5/6/7/6/56761669/cost... · expenses...

TRANSCRIPT

COST ACCOUNTING B.com-2 Regular Annual Examination 2015

Compiled & Solved By: JAHANGEER KHAN

B.com-2

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 1

Q.1: MANUFACTURING CONCERN: Record of Muqeem and Baber shows the following information for 2015:

Sales 500 T.V Sets

Material Purchased

Direct Labour

FOH (2/3 of D/Labour)

Selling Expense

General Expenses

Rs.1,000,000 300,000 ? 200,000 5% of sales 10% of sales

Inventory Jan 01, 2015 Inventory Dec 31, 2015 Material Rs.50,000 No unfinished work on hand ----- Finished Goods (50 T.V Sets) 70,000 Finished Goods (70 T.V Sets) ? Material Rs.70,000 REQUIRED:

(a) The number of units manufactured. (b) Income Statement for the year ended Dec 31, 2015. (c) Unit cost T.V manufactured. (d) Finished goods ending inventory using FIFO. (e) Gross Profit per unit sold.

SOLUTION 1 (a): Units in Ending Finished goods 70 Add: Units Sold 500 Units Available for Sale 570 Less: Units in Beginning Finished goods (50) Number of Units Manufactured 520

SOLUTION 1 (b):

COMPUTATION FOR COST OF GOODS MANUFACTURED Raw Material Used: Raw Material (01-01-2015) 50,000 Add: Raw Material Purchased 300,000 Raw Material Available for use 350,000 Less: Raw Material (31-12-2015) (70,000)

Direct Material Used 280,000 Add: Direct Labour used (200,000 x3/2) 300,000

Prime Cost 580,000 Add: Factory Overhead 200,000

Cost of Goods Manufactured 780,000

MUQEEM AND BABER INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2015 Sales 1,000,000 Less: Cost of Goods Sold: Finished goods (01-01-2015) 70,000 Add: Cost of goods Manufactured 780,000 Finished Goods Available for use 850,000 Less: Finished Goods (31-12-2015) (105,000)

Cost Of goods Sold (745,000) Gross Profit 255,000

Less: Operating Expenses: Selling Expenses (1,000,000 x 5%) 50,000

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 2

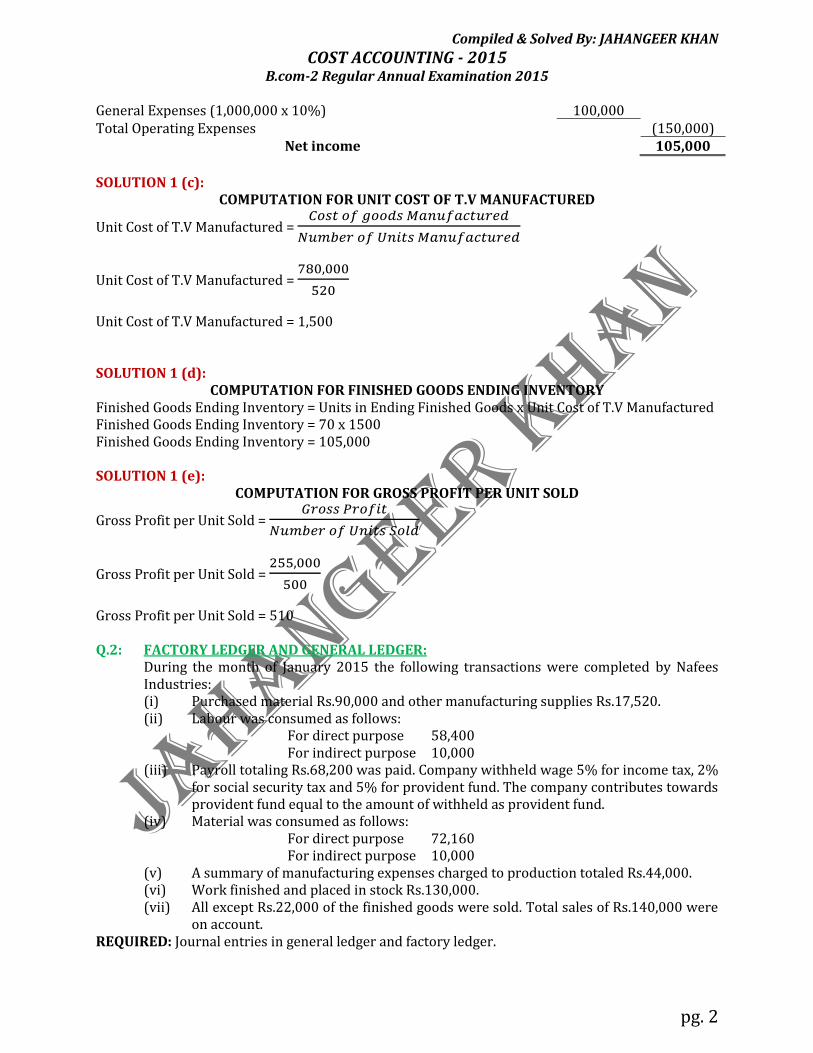

General Expenses (1,000,000 x 10%) 100,000 Total Operating Expenses (150,000)

Net income 105,000

SOLUTION 1 (c):

COMPUTATION FOR UNIT COST OF T.V MANUFACTURED

Unit Cost of T.V Manufactured =

Unit Cost of T.V Manufactured =

Unit Cost of T.V Manufactured = 1,500 SOLUTION 1 (d):

COMPUTATION FOR FINISHED GOODS ENDING INVENTORY Finished Goods Ending Inventory = Units in Ending Finished Goods x Unit Cost of T.V Manufactured Finished Goods Ending Inventory = 70 x 1500 Finished Goods Ending Inventory = 105,000 SOLUTION 1 (e):

COMPUTATION FOR GROSS PROFIT PER UNIT SOLD

Gross Profit per Unit Sold =

Gross Profit per Unit Sold =

Gross Profit per Unit Sold = 510 Q.2: FACTORY LEDGER AND GENERAL LEDGER:

During the month of January 2015 the following transactions were completed by Nafees Industries: (i) Purchased material Rs.90,000 and other manufacturing supplies Rs.17,520. (ii) Labour was consumed as follows:

For direct purpose 58,400 For indirect purpose 10,000

(iii) Payroll totaling Rs.68,200 was paid. Company withheld wage 5% for income tax, 2% for social security tax and 5% for provident fund. The company contributes towards provident fund equal to the amount of withheld as provident fund.

(iv) Material was consumed as follows: For direct purpose 72,160 For indirect purpose 10,000

(v) A summary of manufacturing expenses charged to production totaled Rs.44,000. (vi) Work finished and placed in stock Rs.130,000. (vii) All except Rs.22,000 of the finished goods were sold. Total sales of Rs.140,000 were

on account. REQUIRED: Journal entries in general ledger and factory ledger.

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 3

SOLUTION 2:

NAFEES INDUSTRIES GENERAL LEDGER

GENERAL JOURNAL S.no Particulars P/R Debit Credit

1. Factory Ledger 107,520 Voucher Payable 107,520 (To record raw material purchased)

2. Payroll 68,200 Income Tax (68,400 x 5%) 3,410 Provident Fund (68,400 x 2% ) 1,364 Social Securities (68,400 x 5%) 3,410 Accrued Payroll 60,016 (To record payroll of the month)

3 (a). Accrued Payroll 60,016 Voucher Payable 60,016 (To record voucher issued for accrued payroll)

3 (b). Voucher payable 60,016 Bank 60,016 (To record payment of accrued payroll)

3 (c). Factory ledger 68,200 Payroll 68,200 (To close factory payroll account)

4. Factory Ledger 3,410 Provident Fund 3,410 (To record contribution of provident fund)

5. Accounts Receivable 140,000 Sales 140,000 (To record sold goods on account)

6. Cost of Goods Sold 108,000 Factory Ledger 108,000 (To record cost of goods sold)

NAFEES INDUSTRIES

FACTORY LEDGER GENERAL JOURNAL

S.no Particulars P/R Debit Credit 1. Raw Material 107,520 General Ledger 107,520 (To record raw material purchased)

2. Work in Process 58,400 Factory Overhead 10,000 Accrued Payroll 68,400 (To record direct and indirect labour used)

3. Accrued Payroll 68,200 General Ledger 68,200 (To record payroll sent to general office)

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 4

S.no Particulars P/R Debit Credit

4. Work in Process 72,160 Factory overhead 10,000 Raw Material 82,150 (To record direct and indirect use of material)

5. Work in Process 44,000 Applied Factory Overhead 44,000 (To record manufacturing expenses charged to

production)

6. Finished Goods 130,000 Work in Process 130,000 (To record goods completed and placed in stock)

7. General Ledger 108,000 Finished goods 108,000 (To record cost of goods sold )

Q.3: JOB ORDER COSTING:

The following data relates to Raza Manufacturing Company for its operation for the year ended Dec 31, 2015. Raw material purchased on account Rs.200,000 Material issued to factory: Direct Rs.140,000 Indirect 20,000 Labour used: Direct labour for production 240,000 For general use 24,000 Other FOH cost incurred on account 180,000 FOH @90% of direct labour have been applied. Cost goods valued Rs.516,000 were transferred from factory to Godown as completed. Finished good costing Rs.66,000 were in the ending inventory and the rest were sold at 20% above cost.

REQUIRED: (a) General journal entries to record the above transactions and to close the FOH account. (b) Work in process, Finished Goods and Factory Overhead accounts.

SOLUTION 3 (a):

RAZA MANUFACTURING COMPANY GENERAL JOURNAL

S.no Particulars P/R Debit Credit 1. Raw Material 200,000 Accounts Payable 200,000 (To record purchase of raw material on account)

2. Work in Process 140,000 Factory Overhead 20,000 Raw Material 160,000 (To record material issued to factory)

3. Work in Process 240,000 Factory overhead 24,000 Accrued Payroll 264,000 (To record direct and indirect use of labour)

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 5

S.no Particulars P/R Debit Credit

4. Factory Overhead 180,000 Accounts Payable 180,000 (To record factory cost incurred on account)

5. Work in Process ((240,000x90%)) 216,000 Applied Factory Overhead 216,000 (To record factory overhead applied to

production)

6. Finished Goods 516,000 Work in Process 516,000 (To record goods completed and transferred out)

7. Cost of Goods Sold (516,000 – 66,000) 450,000 Finished Goods 450,000 (To record cost of goods sold)

8. Accounts Receivable (450,000 x 120/100) 540,000 Sales 540,000 (To record sold goods on account)

9. Cost of Goods Sold 8,000 Under Applied Factory Overhead 8,000 (To close under applied factory overhead)

SOLUTION 3 (b):

RAZA MANUFACTURING COMPANY GENERAL LEDGERS

Work in Process

2. Raw Material 140,000 6. Finished goods 516,000 3. Accrued Payroll 240,000 Balance c/d 80,000 5. Applied Factory Overhead 216,000 596,000 596,000

Balance b/d 80,000

Finished Goods 6. Work in Process 516,000 7. Cost of Goods sold 450,000 Balance c/d 66,000 516,000 516,000

Balance b/d 66,000

Factory Overhead 2. 20,000 5. Work in Process 216,000 3. 24,000 9. Cost of Goods Sold 8,000 4. 180,000 224,000 224,000

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 6

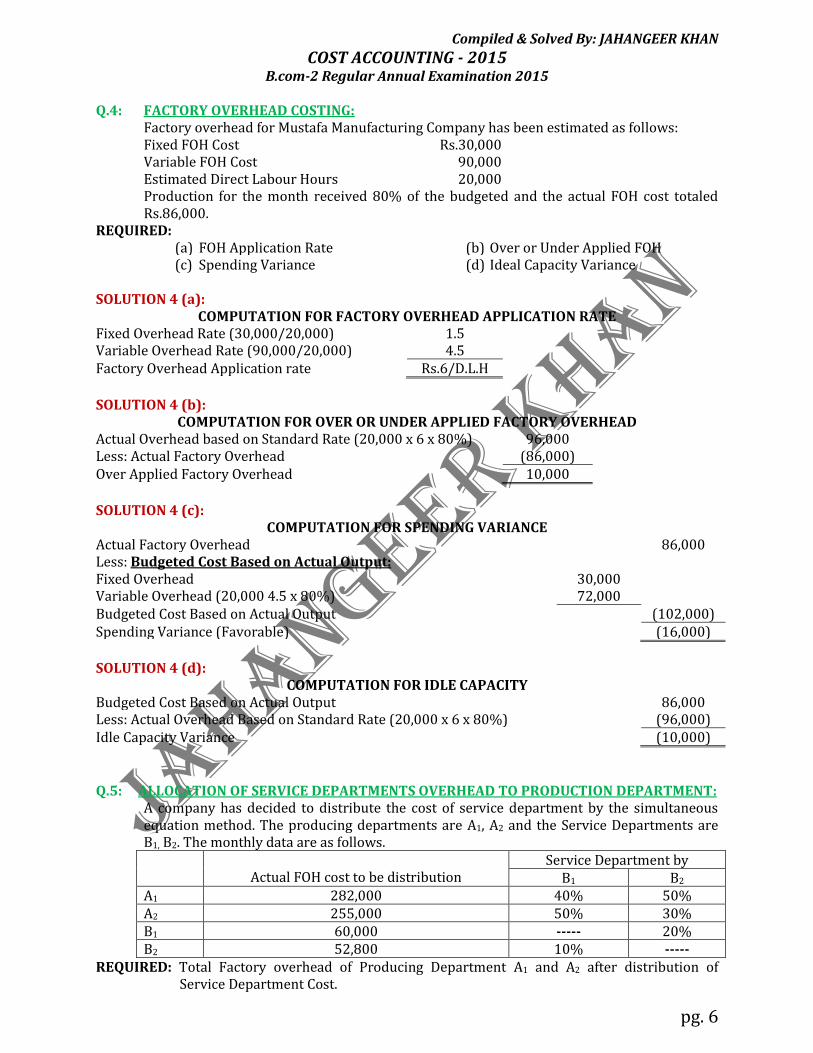

Q.4: FACTORY OVERHEAD COSTING:

Factory overhead for Mustafa Manufacturing Company has been estimated as follows: Fixed FOH Cost Rs.30,000 Variable FOH Cost 90,000 Estimated Direct Labour Hours 20,000 Production for the month received 80% of the budgeted and the actual FOH cost totaled Rs.86,000.

REQUIRED: (a) FOH Application Rate (b) Over or Under Applied FOH (c) Spending Variance (d) Ideal Capacity Variance

SOLUTION 4 (a):

COMPUTATION FOR FACTORY OVERHEAD APPLICATION RATE Fixed Overhead Rate (30,000/20,000) 1.5 Variable Overhead Rate (90,000/20,000) 4.5 Factory Overhead Application rate Rs.6/D.L.H

SOLUTION 4 (b):

COMPUTATION FOR OVER OR UNDER APPLIED FACTORY OVERHEAD Actual Overhead based on Standard Rate (20,000 x 6 x 80%) 96,000 Less: Actual Factory Overhead (86,000) Over Applied Factory Overhead 10,000

SOLUTION 4 (c):

COMPUTATION FOR SPENDING VARIANCE Actual Factory Overhead 86,000 Less: Budgeted Cost Based on Actual Output: Fixed Overhead 30,000 Variable Overhead (20,000 4.5 x 80%) 72,000 Budgeted Cost Based on Actual Output (102,000) Spending Variance (Favorable) (16,000)

SOLUTION 4 (d):

COMPUTATION FOR IDLE CAPACITY Budgeted Cost Based on Actual Output 86,000 Less: Actual Overhead Based on Standard Rate (20,000 x 6 x 80%) (96,000) Idle Capacity Variance (10,000)

Q.5: ALLOCATION OF SERVICE DEPARTMENTS OVERHEAD TO PRODUCTION DEPARTMENT:

A company has decided to distribute the cost of service department by the simultaneous equation method. The producing departments are A1, A2 and the Service Departments are B1, B2. The monthly data are as follows.

Actual FOH cost to be distribution Service Department by

B1 B2 A1 282,000 40% 50% A2 255,000 50% 30% B1 60,000 ----- 20% B2 52,800 10% -----

REQUIRED: Total Factory overhead of Producing Department A1 and A2 after distribution of Service Department Cost.

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 7

SOLUTION 5:

COMPUTATIONS

1. TOTAL COST OF DEPARTMENT B1: B1 = 60,000 + 20% B2 B1 = 60,000 + 0.2 (52,800 + 0.1B1 ) B1 = 60,000 + 10,560 + 0.02B1 B1 - 0.02B1= 70,560 0.98B1 = 70,560 B1 = 70,560/0.98

B1 = 72,000

2. TOTAL COST OF DEPARTMENT B2:

B2 = 52,800 + 10% B1 B2 = 52,800 + 0.1 (72,000) B2 = 52,800 + 7,200

B2 = 60,000

3. Cost Distribution of Department B1:

A1 = 72,000 x 40%

A1 = 28,800

A2 = 74,000 x 50%

A2 = 36,000

B2 = 72,000 x 10%

B2 = 7,200

4. Cost Distribution of Department B2:

A1 = 60,000 x 50%

A1 = 30,000

A2 = 60,000 x 30%

A2 = 18,000

B1 = 60,000 x 10%

B1 = 6,000

SCHEDULE OF FACTORY OVERHEAD DISTRIBUTION

Particulars

Producing Department Service Department Total A1 A2 B1 B2

Overhead Before Distribution 282,500 255,000 60,000 52,800 649,800 Overhead Distribution of Service Department:

B1 28,800 36,000 (72,000) 7,200 ----- B2 30,000 18,000 6,000 (60,000) -----

Total Factory Overhead 341,300 309,000 ----- ----- 649,800

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 8

Q.6: INVENTORY LEDGER AND VARIANCE:

SANA Company produces a product from one basic raw material. During one week of operation the material ledger card reflected the following: Opening Balance 1,400 Lbs @ Rs.1.60 peer Lb Received 1,000 Lbs @ Rs.1.80 peer Lb Issued 800 Lbs Issued 800 lbs Received 1,200 Lbs @ Rs.2.00 peer Lb Issued 800 Lbs Other Costs for the week were: Direct Labour Cost Rs.1,800 FOH Cost 1,490 1,770 units were completed and 1,500 units were sold. There was no beginning inventory of Finished goods and no work in process is left in process over the week end.

REQUIRED: (a) Inventory Ledger Card under FIFO and LIFO method. (b) Ledger account for Material, Work in Process, Finished Goods and Cost of Goods Sold under

FIFO method. SOLUTION 6 (a):

SANA COMPANY INVENTORY LEDGER CARD

PERPETUAL SYSTEM – FIFO METHOD

S.no Purchased Issued Balance Units Unit

Cost Total Units Unit

Cost Total Units Unit

Cost Total

1. 1,400 1.60 2,240

2. 1000 1.80 1,800 1,400 1,000

1.60 1.80

2,240 1,800

3. 800 1.60 1,280 600 1.000

1.60 1.80

960 1,800

4. 600 200

1.60 1.80

960 360

800 1.80 1,440

5. 1,200 2.00 2,400 800 1,200

1.80 2.00

1,440 2,400

6. 800 1.80 1,440 1,200 2.00 2,400

2,200 ----- 4,200 2,4400 ----- 40,40 1,200 ----- 2,400

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 9

SANA COMPANY

INVENTORY LEDGER CARD PERPETUAL SYSTEM – LIFO METHOD

S.no Purchased Issued Balance Units Unit

Cost Total Units Unit

Cost Total Units Unit

Cost Total

1. 1,400 1.60 2,240

2. 1000 1.80 1,800 1,400 1,000

1.60 1.80

2,240 1,800

3. 800 1.80 1,440 1400 200

1.60 1.80

2,2400 360

4. 200 600

1.80 1.60

360 960

800 1.60 1,280

5. 1,200 2.00 2,400 800 1,200

1.60 2.00

1,280 2,400

6. 800 2.00 1,600 800 400

1.60 2.00

1,280 800

2,200 ----- 4,200 2,400 ----- 4,360 1,200 ----- 2,080

SOLUTION 6 (b):

COMPUTATIONS 1. COST OF GOODS MANUFACTURED:

Direct Material 4,040 Add: Direct Labour 1,800 Prime Cost 5,440 Add: Factory Overhead 1,490 Cost of Goods Manufactured 7,330

2. COST OF ENDING FINISHED GOODS:

Per Unit Cost =

Per Unit Cost =

Per Unit Cost = 4.1412 Number of Units Manufactured 1,770 Less: Units Sold 1,500

Units in Ending Finished Goods 2,70

Cost of Ending Finished Goods = Units in Ending Finished Goods x Per Unit Cost Cost of Ending Finished Goods = 2,70 x 4.14 Cost of Ending Finished Goods = 1,118

3. COST OF GOODS SOLD: Cost of Goods Sold = Units Sold x Per Unit Cost Cost of Goods Sold = 1,500 x 4.1412 Cost of Goods Sold = 6,212

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 10

SANA COMPANY

GENERAL LEDGERS

Raw Material 1. Balance 2,240 3. Work in Process 1,280 2. Purchases 1,800 4. Work in Process 1,320 5. Purchases 2,400 6. Work in Process 1,440 Balance c/d 2,400 6,440 6,440

Balance b/d 2,400

Work in Process

3. Raw Material 1,280 Finished Goods 7,330 4. Raw Material 1,320 6. Raw Material 1,440 Accrued Payroll 1,800 Factory Overhead 1,490 7,330 7,330

Finished Goods Cost of Goods Manufactured 7,330 Cost of Goods Sold 6,212 Balance c/d 1,118 7,330 7,330

Balance b/d 1,118

Cost of Goods Sold

Finished Goods 6,212 Balance c/d 6,212 6,212 6,212

Balance b/d 6,212

Q.7: LABOUR COSTING:

10 men crew works as team in processing department. Each is paid a bonus if his group exceeds the standard production of 200 kilogram per hour. For calculating the amount of bonus, the percentage by which the group production extends the standard is determined first. One half of this percentage is than applied to a wage rate of Rs.480 to determine the hourly bonus rate. Each man in the crew is paid a bonus for his groups excess production in addition to the wage at hourly rate. Production Record for the week is as follows:

Day Hours Worked Production in Kg. Monday 79 16,040 Tuesday 80 17,599

Wednesday 74 16,200 Thursday 78 17,429

Friday 80 18,036 REQUIRED: On the basis of production records:

(a) The Group Bonus for each day and for the week.

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 11

(b) The weeks earning for each employee assuming that each worker earns Rs.480 per hour and each worked the same number of hours in the week.

SOLUTION 7 (a):

SCHEDULE OF BONUS Day Hours Worked

(A) Production in

Kg. Bonus Rate

(B) Bonus (A) x (B)

Monday 79 16,040 21.79 1,721.41 Tuesday 80 17,599 21.79 1,743.2

Wednesday 74 16,200 21.79 1,612.46 Thursday 78 17,429 21.79 1,699.62

Friday 80 18,036 21.79 1,743.2 Total 391 85,304 21.79 8.519.89

COMPUTATIONS 1. STANDARD PRODUCTION:

Standard Production = Total Hours Worked x Per Hour Standard Units Standard Production = 391 x 200 Standard Production = 78,200 Kg.

2. EXCESS PRODUCTION: Actual Production 85,304 Less: Standard Production (78,200)

Excess Production 7,104

3. EXCESS PRODUCTION RATE:

Excess Production Rate =

x 100

Excess Production Rate =

x 100

Excess Production Rate = 9.08%

4. BONUS RATE: Bonus Rate = 1/2 Wage Rate x Excess Production Rate Bonus Rate = 1/2 (480) x 9.08% Bonus Rate = 240 x 9.08% Bonus Rate = Rs.21.79

SOLUTION 7 (b): COMPUTATION FOR WEEKLY EARNINGS OF EACH EMPLOYEE

Hours Worked by Each Employee =

Hours Worked by Each Employee =

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 12

Hours Worked by Each Employee = 39.1 hours

Regular Wage (39.1 x 480) 18,768 Add: Bonus (39.1 x 21.79) 851.99 Weekly Earnings of Each Employee Rs.19,619.99

Q.8: PROCESS COSTING:

The following information was taken from the books of Kashif Steel Work for the month of January 2015. Cost of units in process at beginning of Jan 2015 Rs.60,000 Cost of material placed in production 274,800 Direct Labour Cost incurred 168,000 FOH Cost incurred 201,600 The data extracted from the production records relating to the above process as follows: Units in process at beginning of Jan (40% completed as to material and 60% completed as to conversion cost)

2000 Units

Units placed in production 11,000 Units Units in process at end (75% completed as to material and 80% completed as to conversion cost)

3,000 Units

REQUIRED: (a) (i) Equivalent Production Unit. (ii) Total Cost of Units completed under (FIFO) Flow of Cost. (iii) Total Cost of Units in Process at the End.

(b) General Journal Entries to record the cost charged to production and production completed.

SOLUTION 8 (a) (i):

COMPUTATION FOR UNITS COMPLETED Beginning Units 2,000 Add: Units Placed in production 11,000 Total Units in Production Process 13,000 Less: Ending Units (3,000) Units Completed 10,000

COMPUTATION FOR EQUIVALENT PRODUCTION UNITS

Particulars

Direct Material

Direct Labour

Factory overhead

Units Completed 10,000 10,000 10,000 Less: Beginning Work in process Direct Material (2,000 x 40%) (8,00) Conversion (2,000 x 60%) (1,200) (1,200) 9,200 8,800 8,800 Add: Ending Work in Process Direct Material (3,000 x 75%) 2,250 Conversion (3,000 x 80%) 2,400 2,400 Equivalent Production Units 11,450 11,200 11,200

Compiled & Solved By: JAHANGEER KHAN

COST ACCOUNTING - 2015 B.com-2 Regular Annual Examination 2015

pg. 13

SOLUTION 8 (a) (ii):

COMPUTATIONS

1. PER UNIT COST Cost ÷ Equivalent Units = Unit Cost Direct Material 274,800 ÷ 11,450 = 24 Direct Labour 168,000 ÷ 11,200 = 15 Factory Overhead 201,600 ÷ 11,200 = 18

Per Unit Cost Rs.57

2. TOTAL COST OF UNITS COMPLETED: Cost of Beginning 2,000 Units in Process: Cost of Beginning Work in Process 60,000 Add: Cost Added During the Month Direct Material (2,000 x 60% x 24) 28,800 Direct Labour (2,000 x 40% x 15) 12,000 Factory Overhead (2,000 40% x 18) 14,400

Total Cost Added During the Month 55,200 Total Cost of Beginning 2,000 Units in Process 115,200

Add: Cost of Remaining 8,000 Units (8,000 x 57) 456,000 Total Cost of Units Completed 571,200

SOLUTION 8 (a) (iii):

COMPUTATION FOR TOTAL COST OF UNITS IN PROCESS AT THE END Direct Material (3,000 x 75% x 24) 54,000 Direct Labour (3,000 x 80% x 15) 36,000 Factory Overhead (3,000 x 75% x 18) 43,200 Total Cost of Units in Process at the End 133,200

SOLUTION 8 (b):

KASHIF STEEL WORK GENENRAL JOURNAL

S.no Particulars P/R Debit Credit 1. Work in Process 644,400 Raw Material 274,800 Accrued Payroll 168,000 Factory Overhead 201,600 (To record cost charged by the department during

the month)

2. Work in Process 571,200 Work in process 571,200 (To record goods completed and transferred out)