basics of finance

TRANSCRIPT

Finance basicsMicrofinance June 2015

Finance training

Contents

1. Cost calculation

2. Pricing methods

3. How to make a sales forecast

4. How to make a budget

5. Finance tracking

Cost calculationTypes of cost

Principles

Type of costing

Financials of a small business

• When running a cost calculation, we offer have to break the costs into three groups:

1. Fixed costs

2. Variable costs

3. Direct costs

4. Indirect costs

Common mistake are often made on Indirect costs. Pay special attention to this part.

Types of costs

• Direct costs: Direct costs can be directly traced to the product. Material and labor costs are good examples.

• Indirect costs: These can’t be directly traced to the product; instead, these costs are allocated, based on some level of activity. For example, overhead costs are considered indirect costs.

• Fixed costs: Fixed costs don’t vary with the level of production. A good example is a lease on a building.

• Variable costs: Unlike fixed costs, variable costs change with the level of production. For example, material used in production is a variable cost.

Principles

• Matching principle: This principle states that your company’s revenue should be matched with the expenses that relate to that revenue. If you sell lamps in May, you create revenue for that month. The May revenue should be matched with the expenses you incurred for the lamps sold in May. So, the cost of the lamp is matched with the sales proceeds for the lamp’s sale.

• Principle of conservatism: Accountants often need to make judgments. Conservatism means that the decision should generate the least attractive financial result. If there’s a decision about revenue, the conservative choice is to delay recognizing revenue in the financial statements. Expenses should be posted to the financial statements sooner rather than later. These choices generate financial statements that are less optimistic, which is why the approach is called conservative.

Types of costing

• Job costing: This method of costing assumes that every customer job is different. Plumbers and carpenters are good examples of businesses that use cost accounting. Because every job is different, each customer job is assigned material, labor, and overhead costs.

• Process costing: Companies use process costing when partially completed units are moved from one production area to another. Process costing assumes that the products you produce are similar or even identical.

• Activity-based costing (ABC): ABC costing can be used for both job costing and process costing analysis. You use ABC costing to assign costs to your product more specifically. ABC costing analyzes the activities that cause you to incur costs; you then connect the cost to the activity.

Common pitfalls

• Total fixed costs vs. fixed costs per unit: Some cost accounting questions provide you with a fixed cost per unit. If you determine that you need fixed costs to answer the question, pause for a minute. Try to find total fixed costs in the question and use that number. Fixed costs per unit should be avoided. That’s because, at some point, you sell enough to cover your costs. As a result, the additional units you produce don’t have any fixed costs attached to them. Fixed cost per unit is misleading.

Pricing methodsTypes of cost

Principles

Type of costing

Pricing methods

• Cost-plus pricing - Set the price at your production cost, including both cost of goods and fixed costs at your current volume, plus a certain profit margin.

• Target return pricing - Set your price to achieve a target return-on-investment (ROI)

• Value-based pricing - Price your product based on the value it creates for the customer. This is usually the most profitable form of pricing, if you can achieve it.

Pricing methods

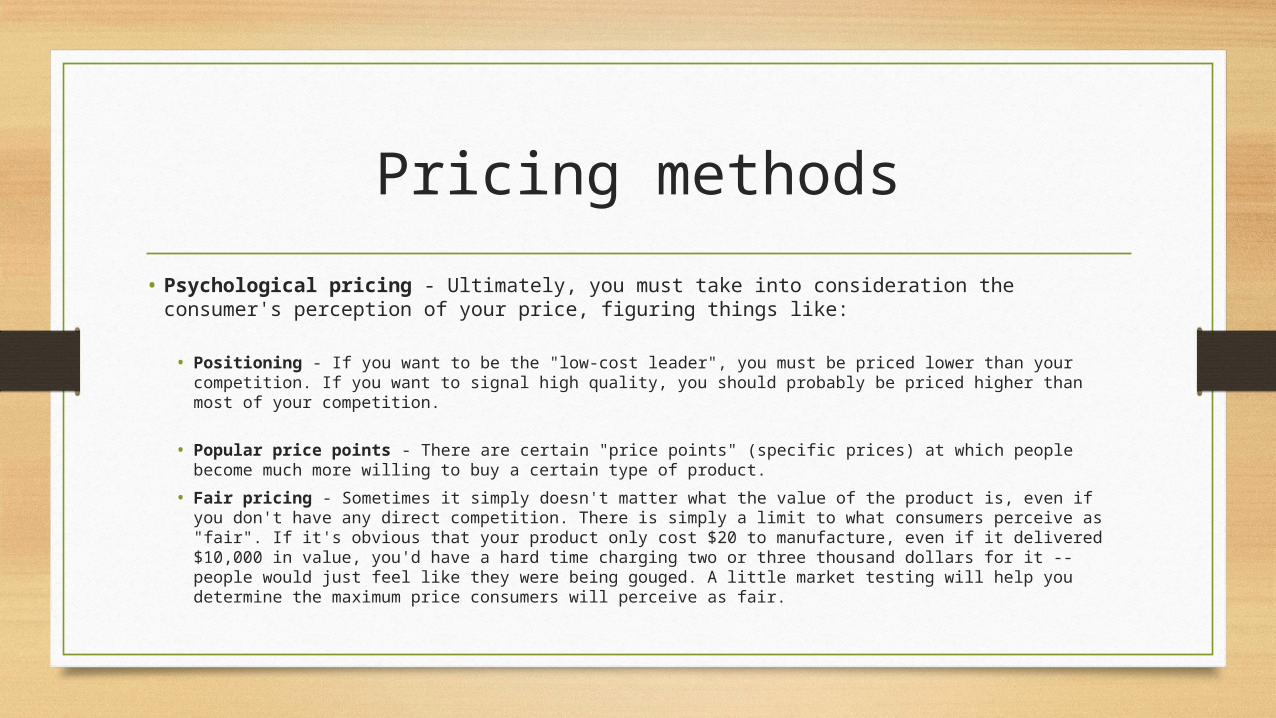

• Psychological pricing - Ultimately, you must take into consideration the consumer's perception of your price, figuring things like: • Positioning - If you want to be the "low-cost leader", you must be priced lower than your competition.

If you want to signal high quality, you should probably be priced higher than most of your competition.

• Popular price points - There are certain "price points" (specific prices) at which people become much more willing to buy a certain type of product.

• Fair pricing - Sometimes it simply doesn't matter what the value of the product is, even if you don't have any direct competition. There is simply a limit to what consumers perceive as "fair". If it's obvious that your product only cost $20 to manufacture, even if it delivered $10,000 in value, you'd have a hard time charging two or three thousand dollars for it -- people would just feel like they were being gouged. A little market testing will help you determine the maximum price consumers will perceive as fair.

Sales forecastDefinition

Factors

Types of forecasting

Helpful tips

Sales forecast

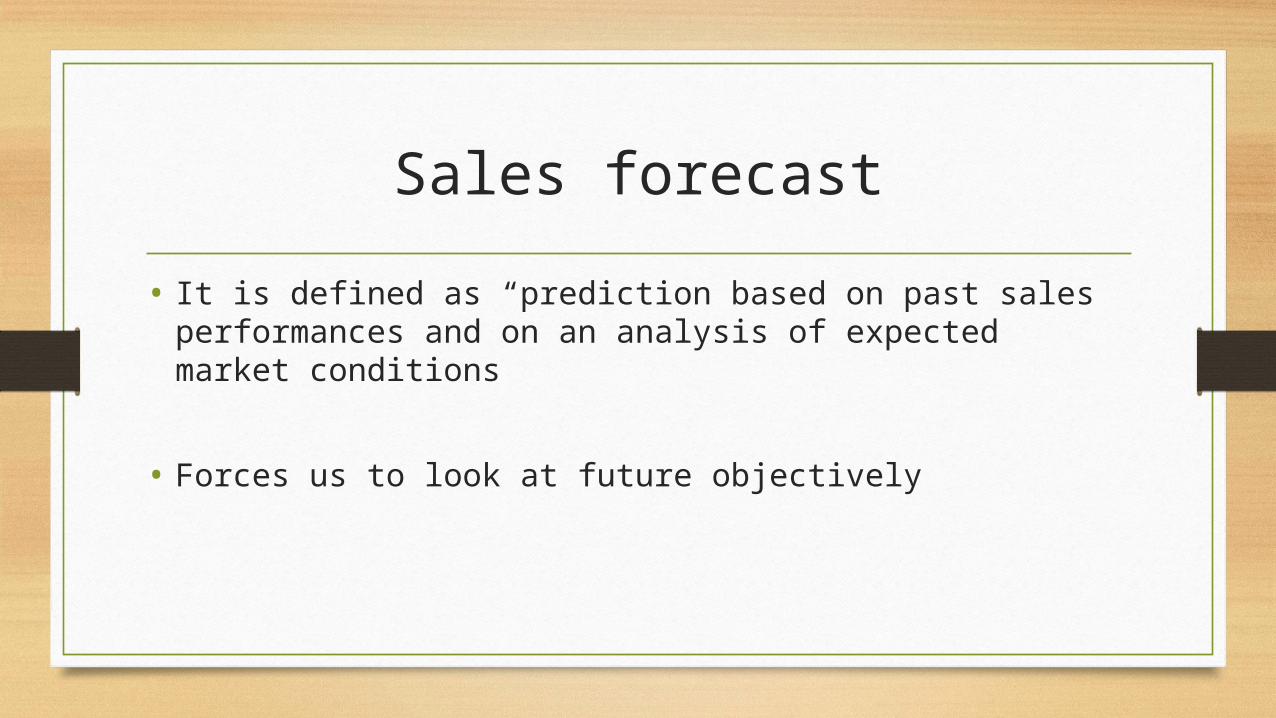

• It is defined as “prediction based on past sales performances and on an analysis of expected market conditions

• Forces us to look at future objectively

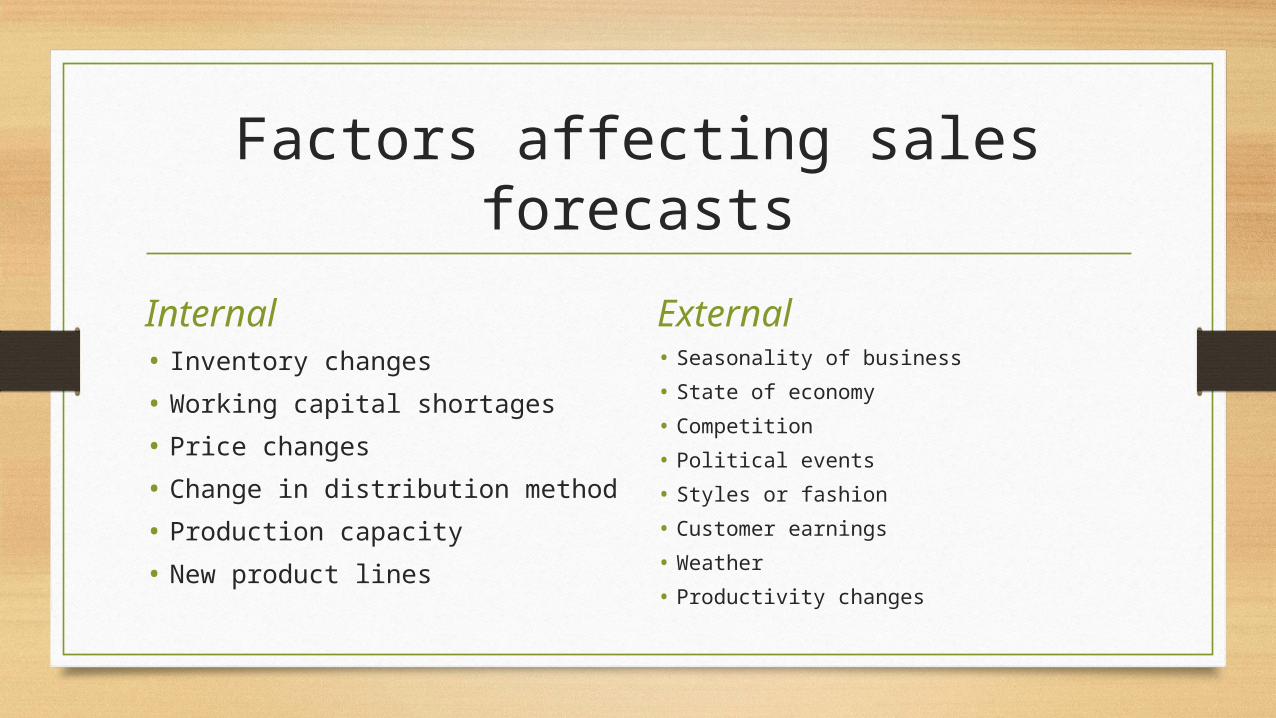

Factors affecting sales forecasts

Internal• Inventory changes

• Working capital shortages

• Price changes

• Change in distribution method

• Production capacity

• New product lines

External• Seasonality of business

• State of economy

• Competition

• Political events

• Styles or fashion

• Customer earnings

• Weather

• Productivity changes

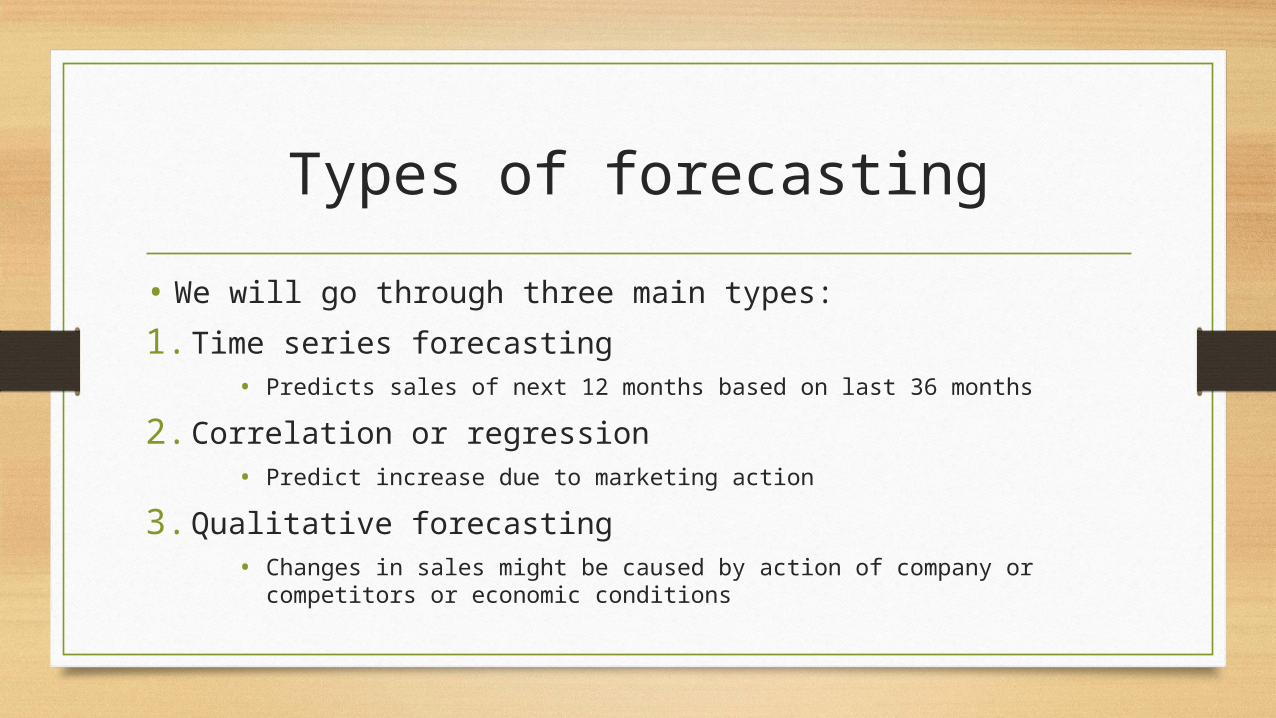

Types of forecasting

• We will go through three main types:

1. Time series forecasting• Predicts sales of next 12 months based on last 36 months

2. Correlation or regression• Predict increase due to marketing action

3. Qualitative forecasting• Changes in sales might be caused by action of company or

competitors or economic conditions

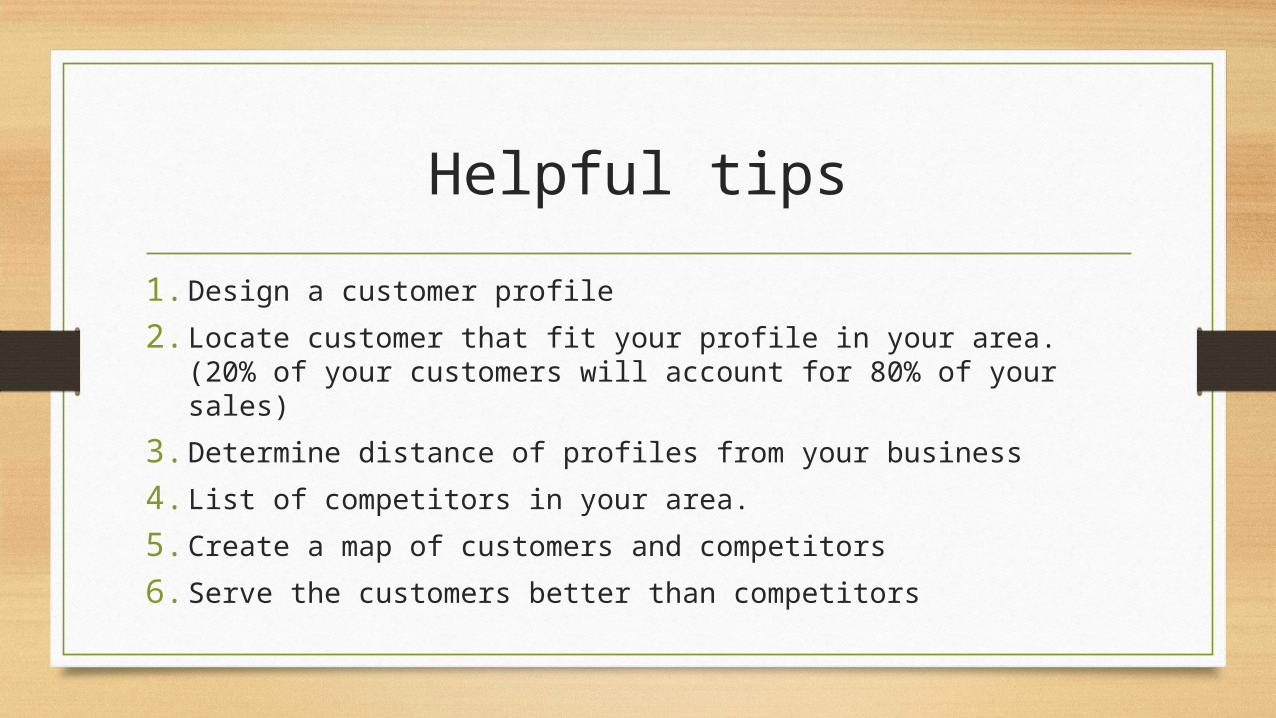

Helpful tips

1. Design a customer profile

2. Locate customer that fit your profile in your area. (20% of your customers will account for 80% of your sales)

3. Determine distance of profiles from your business

4. List of competitors in your area.

5. Create a map of customers and competitors

6. Serve the customers better than competitors

Budgeting

What is a budget?

• Detailed financial plan

• Given time period

• Revenues and Expenses

• Often – cash flow/Balance sheet

Two sides of a budget

1. Cost calculation

2. Sales forecast

Working with the two, you can create your budget. The budget can give a forecast of how cash flow will change in the future and prepare accordingly.

END