basic principle of financial statement analysis

TRANSCRIPT

BASIC PRINCIPLE OF FINANCIAL STATEMENT ANALYSIS

KHOMSATUN (7101413011)NUR MAIZAH RAHMAWATI (7101413052)

Analysis’s purpose

to select, evaluate, interpreting and compare financial data, along with other pertinent information, in order to formulate an assessment of a company’s present and future financial condition and performance.

Method of financial statement analysis

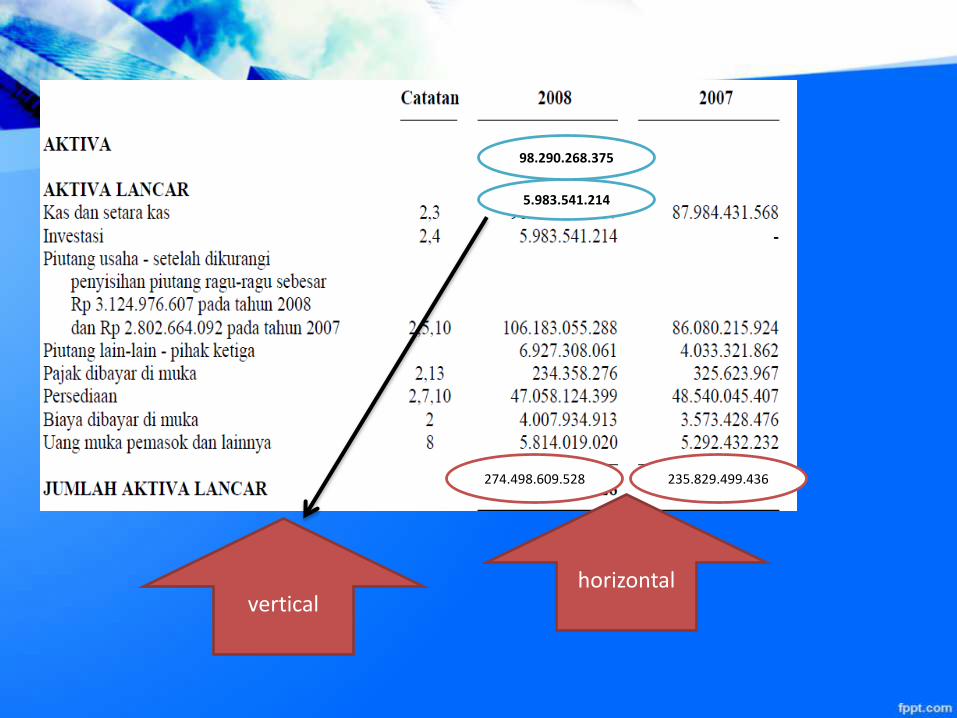

1. Horizontal common-size analysis uses the amounts in accounts in a specified year as the base, and subsequent years’ amounts are stated as a percentage of the base value.

• Useful when comparing growth of different accounts over time.

2. Vertical common-size analysis uses the aggregate value in a financial statement for a given year as the base, and each account’s amount is restated as a percentage of the aggregate.

• Balance sheet: Aggregate amount is total assets.

• Income statement: Aggregate amount is revenues or sales.

235.829.499.436274.498.609.528

horizontal

5.983.541.214

98.290.268.375

vertical

1. LIQUIDITY• Liquidity is the ability to satisfy the company’s short-term obligations using

assets that can be most readily converted into cash.

SOLVENCY

Solvency is a measure of the long-term financial viability of a business which means its ability to pay off its long-term obligations such as bank loans, bonds payable, etc

Total Liability• Total Debt to Equity Ratio = ------------------ x 100 %.

equity

Total liability• Total Debt to capital Assets = ------------------- x 100 %.

Total Asset

long term liability• Long Term Debt to = -------------------------------- x 100 %

Equity Ratio equity

Profitability

Profitability is the ability of a business to earn profit for its owners. While liquidity ratios and solvency ratios are relationships that explain the financial position of a business profitability ratios are relationships that explain the financial performance of a business. Key profitability ratios include net profit margin, gross profit margin, operating profit margin, return on assets, return on capital, return on equity, etc.

Profitability Gross profit

• Gross Profit Margin = ---------------------- x 100 %.Net sales

COGS + adm. expenses• Operating Ratio = --------------------------------- x 100 %.

Net sales

Net profit after tax• Net Profit Margin = ---------------------------- x 100 %.

Net sales

Net profit after tax• Return On Investment = ----------------------------- x 100 %.

total assets

ACTIVITY RATIO

Activity ratios explain the level of efficiency of a business. Key activity ratios include inventory turnover, days sales in inventory, accounts receivable turnover, days sales in receivables, etc.

net sales

– Total Assets = ------------------------- x 1 kali.

Turn Over Total assets

sales on credit

– Receivable Turnover = -------------------------- x 1 kali.

receivable

receivable average x 360

– Average Collection = ----------------------------- x 1 hari.

Periode sales on credit

cost of good soldInventory Turnover = ----------------------------- x 1 kali.

Inventory

Inventory x 360Average day’s = ----------------------------- x 1 hari.

Inventory cost of goods sold

net salesWorking Capital = ------------------------------------- x 1 kali.Turnover current assets – current liability

Technic of financial statement analysis

Comparing of financial

statement

Trend

Common size statement

Cash flow statement

Working capital analysis

Ratio analysis

Gross profit analysis

Break even analysis

Financial statement comparing analysis

Is an analysis method to compare financial statement for 2 period or over the period that shown :

a. Absolut data

b. Fluctuating value in rupiah

c. Fluctuating value in precentage

d. Comparing value in ratio

e. Total of precentage

Example: Income Statement PT Telkom

Periode2011 (Rp)

Periode 2012 (Rp)

Berkurang-Bertambah(Rp)

Berkurang-Bertambah (%)

Income 71.253 77.143

Salary Exp 8.555 9.786

Depreciation Exp 14.863 14.456

Adv. Exp 3.278 3.094

Admin Exp 2.935 3.036

Other Exp 192 1.973

Gross profit 41.430 44.798

Income tax 5.387 5.866

Net profit 36.043 38.932

Balance sheet compare

2011(RP) 2012(RP) +/- (RP) +/- (%)

Cash 9.634 13.118 3484 36

acc. Receivable 406 701 295 72

Inventory 758 579 179* 23,6*

Fixed asset 74.897 77.047 2150 2,9

Total aktiva 85.695 91.445 9420 11

Current liability 22.187 24.107 1920 8,6

Long term liab. 19.884 20.284 400 2

Capital 43.624 47.054 7100 16,3

Total pasiva 85.695 91.445 9420 11

Analysis…????

TREND PERCENTAGE ANALYSIS

calculates the percentage change for one account over a period of time of two years or more.

• Percentage change To calculate the percentage change between two

periods:• Calculate the amount of the increase/(decrease) for

the period by subtracting the earlier year from the later year. If the difference is negative, the change is a decrease and if the difference is positive, it is an increase.

• Divide the change by the earlier year's balance. The result is the percentage change.

Common size statement

A company financial statement that displays all items as percentages of a common base figure. This type of financial statement allows for easy analysis between companies or between time periods of a company.

Working capital analysis

An analysis to determine changes in working capital is to compare its sources with its uses. Recall that transactions involving only current asset and current liability accounts have no net effect on working capital.

Cash flow statement analysis

to determine how a company uses its cash assets. The choice to use cash to acquire an asset, to meet a liability, or to retire a debt is a process of investment and disinvestment, and a manager always has choices to make, some smart and some maladroit. It’s important to keep track of how well a company’s management is making these choices.

Ratio analysis

It's comparing the number against previous years, other companies, the industry or even the economy in general. Ratios look at the relationships between individual values and relate them to how a company has performed in the past, and how it might perform in the future.

Gross profit analysis

is designed to pick apart the reasons why the gross profit margin changes from period to period, so that management can take steps to bring the gross margin in line with expectations. A decline in gross profits can be an indicator of serious problems, so the figure is closely watched.

Break even analysis

An analysis to determine the point at which revenue received equals the costs associated with receiving the revenue. Break-even analysis calculates what is known as a margin of safety, the amount that revenues exceed the break-even point. This is the amount that revenues can fall while still staying above the break-even point.