basic data - · pdf fileciti transaction services latin america & mexico guatemala 313...

TRANSCRIPT

G U AT E M A L A

G U AT E M A L ACiti Transaction Services Latin America & Mexico

313

COUNTRY OVERVIEW

BASIC DATACapital City:

Land Area:

Population:

Main Towns:

Climate:

Language:

Measures:

Currency:

Time:

Government:

Guatemala City

108,889 sq km; two-thirds mountainous (volcanic), heavily forested in the north, fertile coastal plains

14.4m (2010; IMF)

Population in ’000 (2007)Guatemala City (capital) & metropolitan area 2,937 Subtropical; temperate in highlands

Spanish; at least 21 Mayan indigenous languages, plus two non-Mayanindigenous languages

Metric system; also old Spanish units

1 quetzal (Q)=100 centavos; average exchange rate in 2011: Q7.79:US$1.

6 hours behind GMT

President Otto Pérez MolinaVice-president Roxana BaldettiAgriculture, livestock & food Efraín Medina Communications, transport & public works Alejandro Sinibaldi Culture & sport Carlos BatzínDefense Ulises Noé AnzuetoEconomy & trade Sergio de la TorreEducation Cinthia del AguilaEnergy & mine Erick ArchilaEnvironment & natural resources Roxana SobenesFinance Pavel CentenoForeign relations Harold CaballerosHealth & social welfare Francisco ArredondoInterior Mauricio López BonillaLabor & social security Carlos ContrerasCentral Bank President Edgar Barquín Durán

Source: The Economist Intelligence Unit as of February 2012

G U AT E M A L A

314

B. POLITICAL STRUCTURE

Official NameRepublic of Guatemala

Form of State Unitary republic

Head of State President, elected by universal suffrage for a single term of four years; cabinet, headed and appointed by the president

National Legislature Unicameral Congress, with 158 members, elected every four years; re-election possible for members and leader of Congress

Legal System US-style Supreme Court system.

National Elections A former army general, Otto Pérez Molina, won the second-round presidential election run-off held on November 6th 2011 with 53.8% of the vote. The next presidential, legislative and municipal elections are set to take place in September 2014

Main Political Organizations Main opposition parties: Unidad Nacional de la Esperanza (UNE); Gran Alianza Nacional(GANA); Unión del Cambio Nacional (UCN); Libertad Democrática Renovada (LIDER);Compromiso, Renovación y Orden (CREO); Encuentro por Guatemala (EG); Visión conValores (VIVA); Partido de Avanzada Nacional (PAN); Frente Republicano Guatemalteco(FRG); Frente Amplio; Partido Unionista (PU).

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

315

C. POLITICAL OUTLOOK 2012 – 2016

During his four-year term, the president, Otto Pérez Molina, of the right-wing Partido Patriota (PP), will seek to pass a long-standing fiscal reform that will be key to delivering improvements in security and higher spending on social programmes, which he pledged during the campaign. In his first year in power, Mr. Pérez Molina will enjoy broad support in Congress (the unicameral 158-seat legislature) by way of a newly-established alliance that will almost double the 57 seats held by the PP. Although the alliance is not expected to prove longlasting, it should allow the ruling party to pass fundamental legislation early on including a fiscal reform, the creation of a ministry for social development to institutionalise existing social programmes and laws to strengthen the security forces. Such co-operation in Guatemala’s highly polarised and fragmented legislature will be made possible by a debilitated opposition. The main opposition party, the centre-left Unidad Nacional de la Esperanza (UNE), which has recently suffered a series of defections that have halved the 40-seat bench obtained in the September 2011 election,will continue to be weakened by ongoing criminal investigations involving the party’s founders and leaders. The populist libertarian Libertad Democrática Renovada (LIDER), which was defeated in the November run-off, will focus on recruiting defectors to increase its 14-seat bench to be able to present a more significant challenge to the PP. Nonetheless, given the fluid nature of party allegiances in Guatemala, the ruling party’s window of opportunity will be small. The Economist Intelligence Unit does not expect the PP’s broad alliance to still be in existence in 2013, when legislative paralysis, a common feature of the political scene, is likely to set in once again, complicating policymaking and reducing political effectiveness. Organized crime and drug-trafficking will continue to threaten political stability and foreign investment in 2012-16, although we expect the new government to make some progress in reducing the murder rate from the current 39 per 100,000, especially since the 2012 budget now contemplates higher spending on security. The high-profile cases under investigation by the UN-sponsored Comisión Internacional Contra la Impunidad en Guatemala (CICIG, an international commission in charge of investigating and prosecuting criminal organisations), whose mandate runs out in late 2014, will continue to suffer setbacks, owing to a corrupt legal system. However, continuity in the attorneygeneral’s office which, at least in the short term, appears to be assured by Mr. Pérez Molina, and government support for the CICIG will help to strengthen Guatemala’s judiciary gradually, which will, in turn, improve the business environment. Opposition (in the form of roadblocks and strikes) to mining activities and the construction of hydroelectric plants in protected or indigenous areas will remain a source of tension throughout 2012-16, as the new government pushes through new projects to boost economic growth.

COUNTRY OVERVIEW

G U AT E M A L A

316

In his first months in office, Mr. Pérez Molina, a retired army general, will need to demonstrate his respect for democracy and human rights, to compensate for the negative international image of the Guatemalan army, which is tainted by the institution’s responsibility for the majority of atrocities committed during the country’s bloody civil war (1960-96). This reputation could become a handicap with European donor nations as well as the US, with which Mr. Pérez Molina is seeking closer military co-operation to combat rising crime and drug trafficking. Nonetheless, this will not impact relations with Mexico and Central American countries, with which trade ties and security co-operation is set to deepen. Support for free-trade agreements (FTAs) will deepen under the PP government, which views export promotion as a key policy. The first steps towards building trade ties with China are likely to take place in the outlook period, as Guatemala tries to diversify away from its dependency on the US. During the outlook period Guatemala will occupy a non-permanent seat on the UN Security Council. This will widen the country’s foreign policy concerns to issues beyond the country’s traditional agenda, although it will have limited domestic impact. A resolution of the long-standing territorial dispute with Belize is unlikely in the medium term, although efforts to solve the dispute at the International Court of Justice (ICJ) in The Hague are likely.

D. ECONOMIC PERFORMANCE

GDP data for the third quarter of 2011 compiled by the Banco de Guatemala (Banguat, the central bank) show that year-on-year GDP growth accelerated to 4.3%, from the 3.9% and 3.1% recorded in the second and first quarters, respectively. As in previous quarters, growth was driven by firm domestic demand, which was boosted by private and government consumption. Although annual growth in remittances was comparatively slower in the third quarter (6.2% compared with 9.5% in the first half of the year), it has continued to underpin private consumption, as has employment growth. Owing to legislative paralysis prior to the September 2011 election, the government of Mr. Colom experienced funding constraints that resulted in lower year-on-year growth of government consumption during the third quarter. A pick-up in construction led investment to post the highest annual growth rate since the third quarter of 2007, but it remains well below pre-crisis levels. Exports of goods and services outpaced growth in imports for the first time since the last quarter of 2009, leading the external sector to boost GDP growth in the third quarter.

Based on third quarter results and official upwards revisions to second quarter results, the Economist Intelligence Unit has revised its GDP estimate for 2011 to 3.8% (from 3.6% previously). Stronger momentum from 2011 and an improved outlook for the US, vwe now forecast growth of 1.8% instead of 1.3%, will allow Guatemala to sustain growth in 2012, despite slower global GDP and trade growth.

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

317

Although Guatemala has continued to grow steadily, the rate of growth has been insufficient to reduce poverty and create jobs. The latest poverty survey, executed every five years by the Instituto Nacional de Estadística (INE, the national statistics office), show that the share of people living in poverty (under US$2 per day) has increased to 53.7% in 2011, from the 51% registered in 2006, a period characterized by a very rapid expansion in remittances from the US. However, this was still below the rate registered in 2000 (56%). Remittances grew more than six-fold from 2000 to 2006.from US$563,439 to US$3.6m.but only grew by 21% between 2006 and 2011.to US4.4m.owing to harsher economic conditions in the US and tougher immigration controls. In 2000-08 almost 100,000 Guatemalans migrated per year (mostly illegally) to the US, while estimates for 2008-11 put the net migration rate closer to 10,000 a year, suggesting that remittances will not rise much further than current levels. The increase in poverty also reflects the effect of higher food price inflation in 2006-11. Food prices, which make up more than 40% of the consumer price index, hit poor people disproportionately. However, the poverty survey also showed a decrease in extreme poverty rates (those living under US$1.25 a day), from 15.2% in 2006 to 13.3% in 2011. This is arguably the result of the former government’s conditional cash transfers programme, Mi Familia Progresa, which was widely criticized for having no controls and being a source of political patronage. Although these programmes are set to continue under the new administration, which will create a new ministry to oversee and implement them, they will only make a small contribution to lowering poverty levels.

COUNTRY OVERVIEW

G U AT E M A L A

318

E. ECONOMIC FORECAST

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

319

COUNTRY OVERVIEW

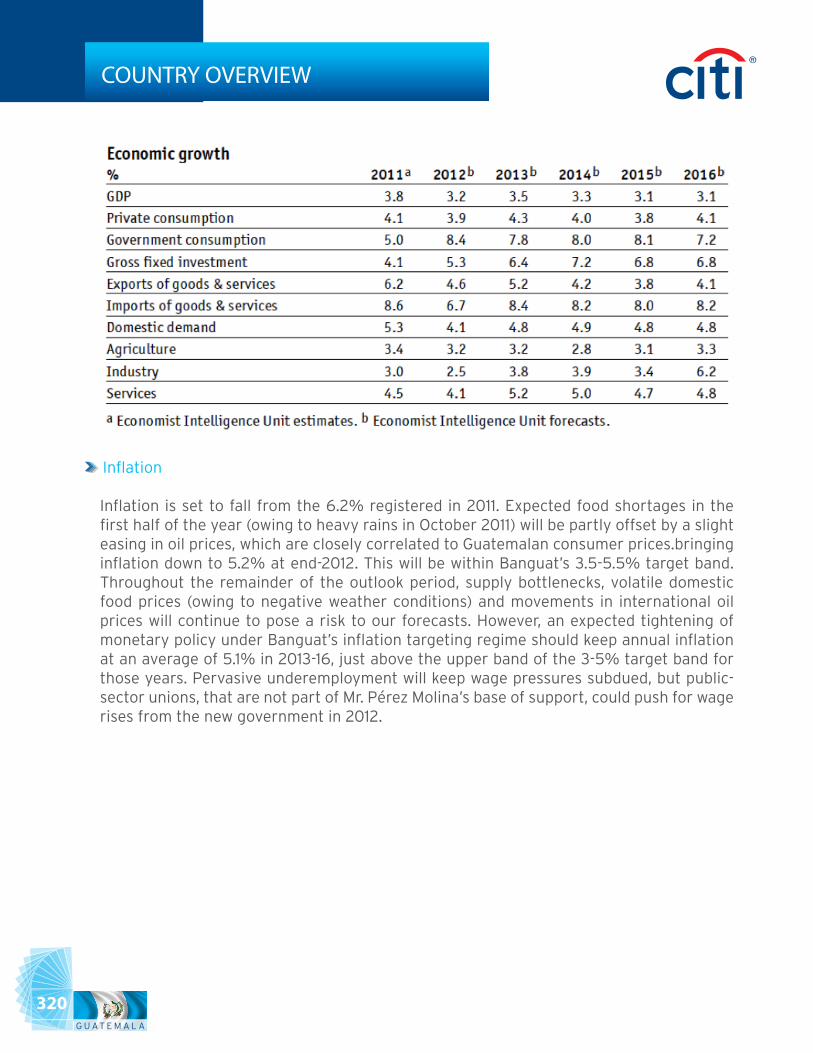

Economic Growth

After expanding by an estimated 3.8% in 2011 (an upwards revision from our previous 3.6% estimate, as a result of a stronger than expected performance in the third quarter of the year and official upwards revisions to second quarter results), GDP growth will slow to 3.2% in 2012, but remain relatively firm owing to stronger than previously forecast growth in the US. On the assumption that global conditions improve, GDP growth will accelerate to 3.5% in 2013 and remain at an average of 3.2% in 2014-16, constrained by low productivity and insufficient (but growing) investment. There remain, however, significant downside risks to our forecasts, owing to a potential global financial crisis triggered by a disorderly sovereign default in the euro zone. The outlook in the US will continue to dominate Guatemalan growth trends in 2012-16, as it is Guatemala’s main export market and source of remittances, which affects private consumption. Growth in private consumption, which accounts for 85% of GDP, will still underpin GDP growth in the outlook period, and will average 4% in 2012-16. Assuming that some revenue-raising measures are implemented, government consumption growth will remain firm, at an average of 7.9% in 2012-16 (from an estimated 5% in 2011), driven by spending on security and social programmes. Gross fixed investment growth, which began to recover in 2011, will gather pace throughout the outlook period, driven by public-private partnerships (PPPs) for long-overdue infrastructure upgrading.

Growth in real exports will slow in 2012, but the fall will be contained by an FTA with the US, securing demand abroad. Nonetheless, import growth.driven by increasing demand for fuels, as well as consumer and industrial goods, will continue to outpace that of exports throughout the outlook period, resulting in a negative contribution of net trade to GDP growth.On the supply side, we expect agriculture to expand by an average of 3.1% in 2012-16, as it continues to recover from damage caused by weather-related natural disasters in 2010 and 2011. Industrial output (which is driven by the export-oriented manufacturing sector) will slow in 2012 but will recover thereafter, as external demand gathers strength. The depressed construction sector will begin to recover slowly in 2012, driven by private infrastructure developments, investment projects in the energy sector and public works. Some progress in improving Guatemala’s security situation is likely to boost the tourism sector in the medium term. Overall, the services sector will continue to outperform others, owing to growth in financial and professional services.

G U AT E M A L A

320

Inflation

Inflation is set to fall from the 6.2% registered in 2011. Expected food shortages in the first half of the year (owing to heavy rains in October 2011) will be partly offset by a slight easing in oil prices, which are closely correlated to Guatemalan consumer prices.bringing inflation down to 5.2% at end-2012. This will be within Banguat’s 3.5-5.5% target band. Throughout the remainder of the outlook period, supply bottlenecks, volatile domestic food prices (owing to negative weather conditions) and movements in international oil prices will continue to pose a risk to our forecasts. However, an expected tightening of monetary policy under Banguat’s inflation targeting regime should keep annual inflation at an average of 5.1% in 2013-16, just above the upper band of the 3-5% target band for those years. Pervasive underemployment will keep wage pressures subdued, but public-sector unions, that are not part of Mr. Pérez Molina’s base of support, could push for wage rises from the new government in 2012.

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

321

COUNTRY OVERVIEW

Exchange Rates

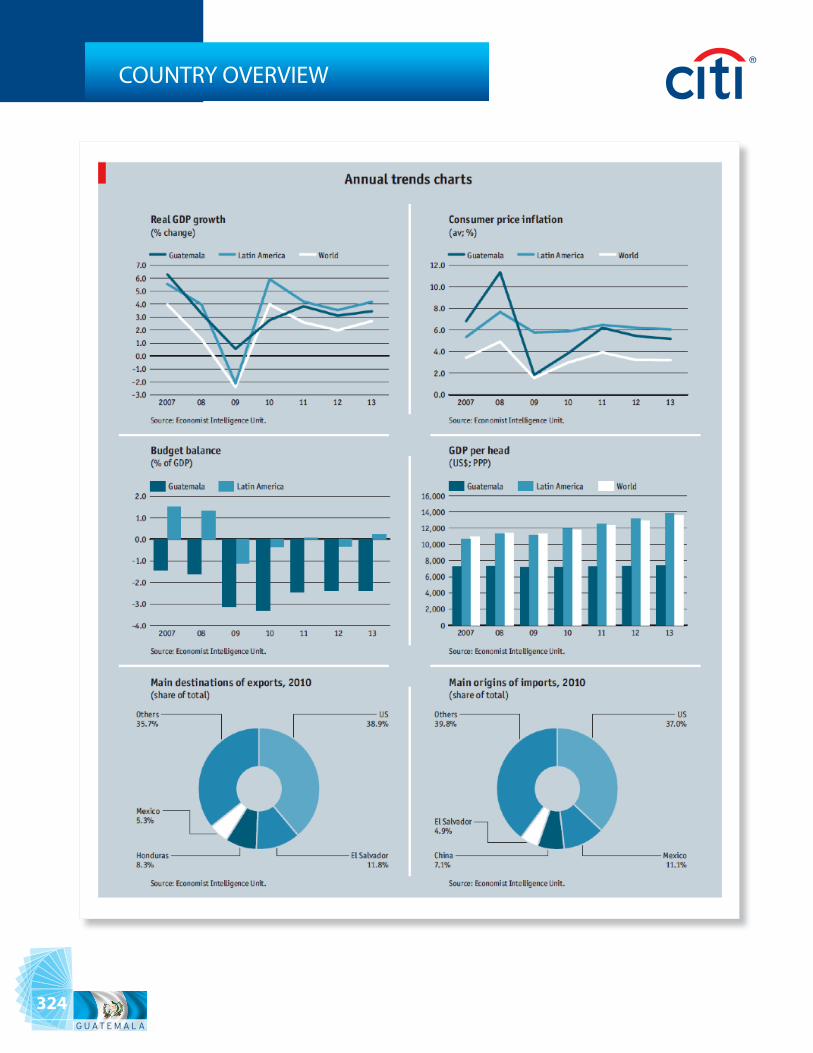

In 2011 the quetzal appreciated by 2.2% in nominal terms. Further appreciation (driven by strong US dollar inflows resulting from high export-earnings and remittances) was offset by volatility in global currency markets, a trend that is set to continue in 2012. Barring a global recession caused by the unfolding European debt crisis, we expect the currency to continue on a gentle appreciating trend in 2012, to Q7.76:US$1 by year-end, supported by remittance inflows and exports earnings. The quetzal will thereafter appreciate to Q7.7:US$1 by 2016, but stronger appreciation will be contained by a growing current-account deficit. Banguat will continue to make discretionary interventions to smooth sharp exchange-rate fluctuations, aided by a comfortable and stable reserves cushion (which stood at US$6.2bn in 2011, equivalent to around four months of imports).

G U AT E M A L A

322

COUNTRY OVERVIEW

External Sector

Developments in the trade account will continue to drive the current-account deficit. In 2012 the current-account deficit will narrow slightly, to 5.1% of GDP (from an estimated 5.4% in 2011), owing to an easing of the merchandise trade and income deficits. The current-account deficit will widen thereafter, to reach 6% of GDP by 2016, driven by a narrower transfers surplus, as growth in remittances remains well below the double-digit rates registered in the boom years of 2002-07. In contrast, the structurally large trade deficit is set to remain relatively stable, at an average of 12.6% of GDP in 2012-16. The small services deficit in 2011 (estimated at 0.6% of GDP) will narrow slightly to an average of 0.4% of GDP in 2012-16, as tourism earnings grow (on the assumption that there is some progress in combating insecurity under the new government). Export earnings, remittances and foreign direct investment (FDI) will boost the accumulation of reserves, to reach US$8.6bn by 2016.

G U AT E M A L ACiti Transaction Services Latin America & Mexico

323

COUNTRY OVERVIEW

G U AT E M A L A

324

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

325

COUNTRY OVERVIEW

G U AT E M A L A

326

COUNTRY OVERVIEW

G U AT E M A L ACiti Transaction Services Latin America & Mexico

327

BANKING SYSTEM

A. BANKS IN GUATEMALA

As of September 2011 there were 18 banks operating in Guatemala, 19 domestic and one foreign. According to the Central Bank of Guatemala (Banco de Guatemala.Banguat), Total assets in the banking system reached US$18.9bn in September 2010, up 7.71% from a year earlier, and the total amount of outstanding credit to the private sector (52.29% of total assets) reached Q76bn in September 2010, (1.09% annual growth). Following a regional trend, the banking sector in Guatemala is becoming increasingly concentrated. The top three banks controlled almost 65% of total market assets as of September 2010, according to figures from the Superintendency of Banks (Superintendencia de Bancos.SB).

B. CITIBANK IN GUATEMALA

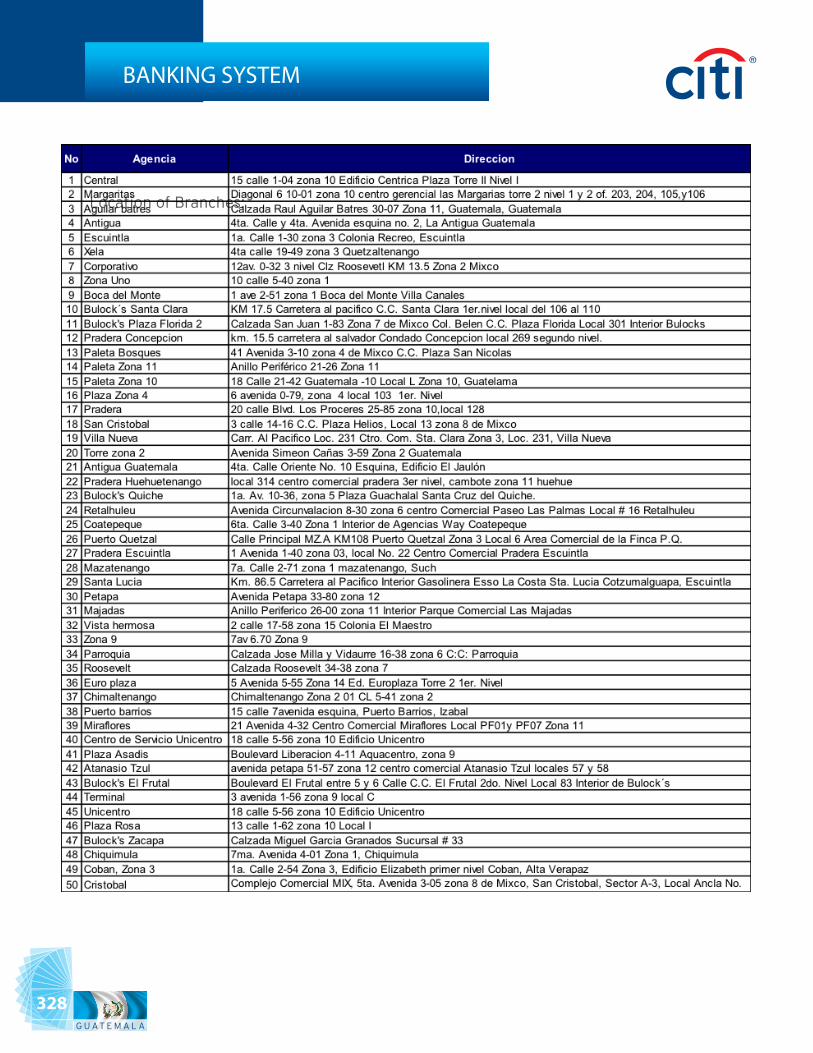

Citibank N.A. Guatemala has been operating in Guatemala since December 3, 1990. Focusing on Global Finance, the bank currently has and now has 96 branches throughout the country strategically located which it serves client companies with world-class commercial banking services. Citivalores, a subsidiary of Citibank’s corporate parent Citicorp, is an active brokerage house and a registered member of Bolsa de Valores Nacional, the country’s most important securities exchange. Citibank, Guatemala - Banking Services

• Liquidity Management / Domestic & International Account Structures• Information Management• Payables Management• Receivables Management• Regional Implementation• Customer Service• FX Management• Local Cash Management Services• Corporate Cards• Custody & Clearing (Global Marketing)• Asset Servicing** (Provides coverage through off-shore products• Depository Receipts• Trade Product and Services

G U AT E M A L A

328

Location of Branches:

BANKING SYSTEM

G U AT E M A L ACiti Transaction Services Latin America & Mexico

329

BANKING SYSTEM

G U AT E M A L A

330

CLEARING SYSTEM

C. CLEARINGHOUSE

The payment-clearing system, the Clearing House (Cámara de Compensación), was created by Decree 16/2002 and established in early 2002. The Clearing House is responsible for the daily clearing of all checks in the banking system via banks. reserve accounts at the Central Bank of Guatemala (Banco Central de Guatemala. Banguat). The Monetary Council’s Resolution JM-51.2003, implemented in August 2005, authorized Banguat to hand over the administration of the Clearing House to the private Guatemalan Bankers. Association (Asociación Bancaria de Guatemala.ABG). The ABG and all the banks in the banking system have hired the private company Imágenes Computarizadas Guatemala to operate the clearing system.

Monetary Council Resolution JM-140.2004, which went into effect in December 2005, implemented, among other things, a system of gross real-time liquidation that further speeded up the payment-clearing system. The system was launched in January 2006. In November 2007 under the Monetary Council Resolution JM-140.2007, the ACH (Cámara de Compensación automatizada) was launched in Guatemala giving an international method of payment for local transfers.

D. LOCAL CLEARING SYSTEM

The clearing process in Guatemala is made through a public Clearinghouse managed by the Central Bank and located in Guatemala City, the capital. All local banks are required by law to be a member of the network. The Clearinghouse clears only local currency checks drawn under local banks and their agencies throughout the country, authorized by the Monetary Board and regulated by the Superintendent of Banks. There are two daily clearing sessions for the collection of checks and a third one when banks return any unpaid checks because of insufficient or uncollected funds, etc. All banks maintain a local currency account with the Central Bank in which the difference between the total amounts for the checks received in and sent for collection is debited or credited every day. Because each bank has a delegate for the three daily sessions, the time required to clear drafts is one day for drafts drawn against banks located in Guatemala City. The time required to clear checks drawn on branches in the interior of the country usually is also one day and rarely exceeds two days.

G U AT E M A L ACiti Transaction Services Latin America & Mexico

331

FOREIGN EXCHANGE CONTROLS

E. FOREIGN CLEARING SYSTEM

International check clearing can take up to 60 days, especially when checks are not dollar-denominated or are drawn on banks that do not have correspondent relations with US banks. Banking commissions for such transactions are often prohibitive as well.Guatemala’s private-sector banks, finance companies and exchange houses are allowed to buy and sell foreign currencies. With the easing of exchange controls, there is unrestricted access to foreign currency without delays. No legal constraints apply to foreign-exchange transactions for remittances or any other capital flows. With the 2001 law governing foreign currency, financial institutions no longer deposit their foreign currency with the Banco Central de Guatemala, the central bank, on a daily basis.

In Guatemala, there is an active spot market used by importers, exporters, business and individuals. All foreign currency transactions must be made through authorized financial institutions. A form must be filled out for all transactions involving foreign investments, remittance of dividends and repatriation of capital. The Central Bank registers all daily transactions and publishes a weighted average rate which is used as a reference for next day’s transactions. There is also an informal, unregulated foreign exchange market where the rate varies slightly from that of the formal market. This market operates only on a cash basis and usually involves small transactions. Exchange rates are freely determined in each transaction in both the formal and the informal market.

A. TAXES

Corporate Income Tax

Income tax reforms in 2004 contained a corporate-tax component. Firms can choose between staying in the regular income tax system (31% tax on profits) or a simplified one (5% on gross revenues). Firms choosing the 5% rate are not subject to the Peace Accord Support Tax (Ley del Impuesto Extraordinario y Temporal de Apoyo a los Acuerdos de Paz. IETAAP) applied to assets or revenue, depending on which is higher. (The IETAAP expires at end-2008, however. A new 1% Solidarity Tax is expected to take its place but remains pending approval as of December 2008.) Firms choosing the 5% rate must present audited accounts to the tax authorities.

*Under review as per recent tax changes

G U AT E M A L A

332

FOREIGN EXCHANGE CONTROLS

The reform also eliminated the compensation to new firms for losses during their first five years of operations and tax deductions for the reinvestment of profits. A corporate tax exemption (applicable only on the 31% rate) may be allowed if dividends remitted abroad are paid by an entity that has already paid its income tax liability for the fiscal period in which the dividends were generated. Branch profits are still taxed at 10%. Capital gains are taxed at a rate of 10%.

Withholding Tax

Withholding Taxes: 10% percent on dividends, profits, income and other benefits paid or credited by companies domiciled in Guatemala. There is also a withholding of 10% on payment or credit of interest, fees, commissions, bonuses, salaries, and other benefits.

Other Taxes

30 % on payments or credits for royalties and other remuneration’s for the use of patents and trademarks and for scientific, economic, financial and technical advises.Interest bearing accounts are taxed according to the location of the company:

Companies residing in Guatemala:

• Income tax: Flat rate of 30% on income after allowable deductions such as operating expenses and other taxes paid. • Annual Company Tax (ACT): Companies domiciled in Guatemala must pay quarterly a 1.5 percent tax on one quarter of the amount resulting after subtracting fiscal credits owed, total liabilities and retained utilities from total assets. Each quarter, the correspondent payment of the annual company tax may be credited to the correspondent quarterly payment of the income tax• Value Added Tax (VAT): The Value Added Tax is levied at a uniform rate of 12 percent. The Value Added Tax paid by individuals may be credited to their personal income tax. • Stamp Tax: Receipts for professional services are subject to a 3 percent stamp tax, when the recipient is not subject to the Value Added Tax.

Non-resident Companies:

• Income Tax: Flat rate of 30% on income after allowable deductions such as operating expenses and other taxes paid. • Value Added Tax (VAT): The Value Added Tax is levied at a uniform rate of 12 percent. The Value Added Tax paid by individuals may be credited to their personal income tax. • Stamp Tax: Receipts for professional services are subject to a 3% stamp tax, when the recipient is not subject to the Value Added Tax.

G U AT E M A L ACiti Transaction Services Latin America & Mexico

333

TRADE REGULATIONS

The Stockmarket Law (Ley de Mercado de Valores) establishes the framework for the securities markets. A reform to the law, approved by Congress in August 2008, strengthens mechanisms to make information more readily available to the public regarding the issuing institutions. It penalizes activities such as illegal deposit-taking and illegal intermediation of equity instruments. It also places stiffer sanctions on those illegal activities that are already specified in prior legislation. Lastly, the reform requires a risk evaluation for all issuing institutions.

In May 2005, the Central Bank’s (Banco de Guatemala.Banguat) Monetary Council (Junta Monetaria) allowed banks to trade in bonds issued by private companies. This produced a moderate increase in the number of issuers operating in the market. In October 2007, the Monetary Council approved a resolution to allow banks to issue long-term bonds (minimum of 20 years), which can also count as part of capital requirements. The bonds can be issued in national or international markets for an amount up to 30% of a firm’s primary capital. The market is currently relatively closed, and most participation is limited to private banks trading repurchasing agreements (repos).

A. IMPORT AND EXPORT REGULATIONS

In May 2006 El Salvador, Guatemala, Honduras and Nicaragua agreed to unify import and export tariffs and custom regulations. By February 2009, 95.7% of tariffs had been harmonized, according to the latest statistics available from the Secretariat for Central American Economic Integration (Secretaría de Integración Económico Centroamericano - SIECA). The remaining 4.3% to be unified include tariffs on medicines, metals, petroleum products and agricultural goods.

El Salvador has made strides in consolidating a free-trade area with Guatemala and Honduras. An agreement signed in early 2004 between the three nations stipulates that persons, merchandise and vehicles may freely move between the three countries, with some exceptions. Tariffs still apply to coffee, sugar cane, ethyl alcohol and distilled alcoholic beverages, and petroleum products.

G U AT E M A L A

334

TRADE REGULATIONS

B. REGIONAL TRADING ASSOCIATIONS

DR-CAFTAGuatemala’s legislature ratified the Dominican Republic - Central American Free-Trade Agreement (DR-CAFTA) with the United States in March 2005. Guatemala passed implementing legislation in May 2006 and became a full participating member in DR-CAFTA on July 1st 2006. The agreement provided for the immediate elimination of tariffs and quotas on more than 99.5% of industrial exports to the US, whereas Guatemala granted immediate access to 81.9% of US products; the rest of the products have a 20-year tariff-elimination schedule.

SICA

System of Central American Integration (Sistema de la Integración Centroamericana – SICA) have member countries, Costa Rica, El Salvador, Guatemala, Honduras, and Nicaragua.

G U AT E M A L ACiti Transaction Services Latin America & Mexico

335

INVESTMENT OPPORTUNITIES

A. TREASURY BILLS

The Guatemalan government issues Treasury bonds (certificados de bonos del Tésoro) and other debt instruments to regulate liquidity. In the year-to-end- September 2008, the government issued Q3.55bn worth of bonds. At end-2007 there was Q31.5bn in Treasury bonds in circulation.

C. REPURCHASE AGREEMENTS

During 2007, 75% of the paper negotiated in the Bolsa de Valores Nacional (BVN) market was in the form of repos; on the Corporación Bursátil, some 90% of trading consisted of repos. Maturity ranges from 1 day to 36 months--in 2007 almost 71% of all repos issued on the BVN were for seven days or less.

The Central Bank’s (Banco de Guatemala - Banguat) Monetary Council (Junta Monetaria) inaugurated an interbank electronic board (mesa electrónica) in 1999. The board facilitates the flow of short-term funds among banks, eliminating the need to cover shortfalls through repos on the stockmarket. The aim was to avoid the rapid peaks in interest rates for repos that banks generate when they need to meet their daily deposit requirements. The board has mainly served

D. TIME DEPOSITS

Rates paid on time deposits in Guatemala vary widely from bank to bank. For the most part, time deposits pay additional percentage points more than yields offered on sight accounts of comparable maturities.

E. CERTIFICATES OF DEPOSIT

The Central Bank of Guatemala (Banco Central de Guatemala.Banguat) is the largest issuer of certificates of time deposit (certificados de depósito a plazo. CDPs) as a means of managing liquidity in the financial system.

G U AT E M A L A

336

In September 2004 the Monetary Council authorized the Banguat to issue CDs in US dollars. These CDs are issued under two conditions: they cannot have maturities longer than one year, and the interest rates must be within an adequate range to capture excess dollars in the market and stabilize the dollar’s value against the quetzal. The interest rates should not attract new capital flows into the country or discourage investments in productive economic endeavors. At end-November 2008 Banguat had Q66.8m in outstanding CDs. The central bank is required to pay interest on CDs.

F. STOCK MARKET

There are currently two stock exchanges operating in Guatemala, the National Stock Exchange (Bolsa de Valores Nacional.BVN) and the Stock Corporation (Corporación Bursátil), both regulated by the Securities Commission (Comisión de Valores). Corporación Bursátil is a strategic alliance between three companies; it started operations in 1992 and was originally created to trade commodities, coffee and grains. However, the exchange has evolved into a smaller version of the BVN, which was created in 1986 and authorized the following year.

INVESTMENT OPPORTUNITIES

G U AT E M A L ACiti Transaction Services Latin America & Mexico

337

CITI SOLUTIONS AND SERVICES

A. LOCAL CASH

Account Services: Under Guatemalan law, customers who wish to open Demand Deposit accounts can open both Quetzals and USD Dollar Accounts.

Payments: 90% of payment transactions in Guatemala are made via check or cash. Large Volume Cash Center: Cash centers exist in Guatemala City, Quetzaltenango, and Escuintla.

Citibank’s Accounts Services Solutions in GuatemalaLocal Currency Resident & Non-Resident USD Smart Accounts, (Zero Balance Account and Target Balance account) DDA• Interest Rate: None • Min. Balance Requirement: Q 300,000.00 • Overdraft Facility: Available with contract

N.O.W. Account• Interest Rate: varies • Min. Balance Requirement: Q 500,000.00 • Overdraft Facility: Available with contract

Documentation & Regulation

To open a Quetzal account with Citibank Guatemala, companies (resident & non-resident) must submit:

• Articles of incorporation, amendments and by-laws; if a foreign company, it must be duly authorized by the consulate of the domicile country. • Power of attorney issued to the legal representative. • Account contract signed by the legal representative. • Signature cards & letter from the legal representative authorizing signature. • NIT (Tributary Identification Number). • All documentation must be duly authorized by the Chamber of Commerce.

B. COLLECTION

In spite our local presence, there is a local network extension agreement between Citibank Guatemala and Banrural (the bank with the local largest presence, more than 700 branches in country), that give the 100% country coverage to facilitate the collection of deposits to our corporate clients.

G U AT E M A L A

338

CITI SOLUTIONS AND SERVICES

In order to give a specialized product that solves conciliation needs of deposits, SpeedCollect, is a simple deposit service of Identified deposit of checks and/or cash at any Citi branch or partner branch where a pre-printed deposit slip will be used by the depositor (customers of our customer) to include Invoice information of payment such as Invoice number, Payer ID, Dates and amounts so that our customers can later identify and reconcile their Account Receivables, with benefits as

• Increase efficiency and reduce days sales outstanding and overall costs• Citi provide Pre-Printed Deposit slips for distribution • The payers fill out payment data and make a SpeedCollect Deposit for a simple identification.• Monitoring of collections via Citidirect Electronic Banking• Reconcilement faster from the collections reports available with deposit Information• Allow Business Process Reengineering in your Receivables Management• Interfaces between ERPs and deposit information for an automatic reconciliation

C. CITIDIRECT ONLINE BANKING FOR LOCAL CASH MANAGEMENT

CitiDirect is an award-winning Web-based global electronic banking service that:

• Centralizes banking functions and streamlines processes • Provides direct, real-time access to accounts in an easy-to-use, Web-based environment• Is available in 22 languages, 24 hours a day, 6.5 days a week• Provides one-click access to frequently used services and features, plus single sign-on for cash and trade services• Offers a wide variety of customizable reports and immediate access to critical information• Saves valuable time by allowing unattended import and export sessions, plus the ability to generate regularly scheduled reports • Brings you the global solutions of an industry leader with the convenience of local banking• Electronic initiation and authorization of transactions.• Security: software encryption, user profiles, audit trail reports.• Upload & Download capabilities• Reporting and export capabilities

G U AT E M A L ACiti Transaction Services Latin America & Mexico

339

D. PAYABLE MANAGEMENT SERVICE

Checks are the most used payment method to transfer funds between accounts from different banks. There are two daily clearing sessions for the collection of checks and a third one when banks return any unpaid checks because of insufficient or uncollected funds, etc. Incoming funds transfers may be manually thru Citibank Guatemala’s Account in Citibank N.A. New York, or by instructions received thru Citidirect (Citi Electronic Platform) for LCY book to book transactions. The local electronic solution used for Corporate clients is Citidirect/Paylink with the following advantages:• Access to multiple payment instruments from one platform• Local language• User Security and Confidentiality of data• Detailed Reporting • High Level Security Features• Pre-Formatted Payments File• Online Payment Channel (CitiConnect) Advice to Beneficiaries • Remote Authorization• Consolidated Payment Information Access • Single Customer Service Contact and Process

Different payment instruments are allowed thru Citidirect/Paylink:• Customer Check: check issued against customer’s account. The account is debited when the supplier deposits the check and the clearing process is completed. • Manager Check: check issued against bank’s account. Customer’s account debited in value date.• Book Transfer: electronic transfer between Guatemala Citibank accounts• ACH / Interbank Transfer: electronic transfer between Citibank accounts and other banks accounts in country.

CITI SOLUTIONS AND SERVICES

G U AT E M A L A

340

CITI SOLUTIONS AND SERVICES

E. INTERNATIONAL CASH

US domiciled Demand Deposit Account with Citigroup N.A., New York (NY DDA), which will allow the client to safely and efficiently move funds between Latin America and the US via Cross-Border Funds Transfers (where permitted by regulations in each country). NY DDAs will have the primary function of receiving USD payments from clients throughout Latin America. Additionally, the NY DDA will give the ability to manage idle funds flowing from Latin America to the US for overnight investment purposes, and can also be used to fund capital needs or cover the deficit positions of local subsidiary accounts.

Additional funds that have been up-streamed to the NY DDA can be invested overnight in Citigroup, N.A. Nassau Bahamas via the Automatic Sweep investment service. Overnight Sweep is the last transaction of our business day; so all funds posted to your account are available for inclusion in the sweep.

Interest is credited and compounded monthly and the interest rate paid is tied to the daily 10:00 AM rate. The minimum balance required for the sweep is $250,000. Trade Servicesf. Documentary Collection g. Letter of Credits h. StandBy Letter of Credit

Trade Financei. Channel Financej. Discount of International Receivablesk. Pre & Post Export Financing l. Import Financing

G U AT E M A L ACiti Transaction Services Latin America & Mexico

341

MARKET GUIDE FOR TREASURY

Allowed —No materialrestrictions

Operating Accounts1 Non-Residents ResidentsOnshore local currencyOnshore foreign currencyOffshore local currency Offshore foreign currency

Overdrafts Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Interest-Bearing Accounts Non-Residents Residents Onshore local currency operating accountsOnshore foreign currency operating accounts

Time Deposits Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Domestic Notional Pooling2 Non-Resident to Resident Residents OnlyOnshore local currencyOnshore foreign currency

Inter-company Lending Non-Resident to Resident Resident to NonresidentOnshore local currencyOnshore foreign currency

Non-Residents Only Residents OnlyOnshore local currencyOnshore foreign currency

FX Convertibility/Transferability• Local currency is freely convertible domestic and offshore.

Allowed —Straightforwardregulations,approval orlicense

Allowed —Challengingregulatoryapproval orlicense

Allowed —Subject to acomplex setof rules

StrictlyProhibited

G U AT E M A L A

342

MARKET GUIDE FOR TREASURY

Other Payment and Clearing Considerations for Treasury• No major restrictions on ACH.• No major restrictions on Non-Residents making payment on behalf of Residents.

For more information, please visit www.transactionservices.citi.com.

Notes:1 Offshore accounts are available only in USD.2 Notional pooling is not available at local market in CR.

G U AT E M A L ACiti Transaction Services Latin America & Mexico

343

CONTACT INFORMATION

Sales Heads

Industry Sector Heads

Carolina JuanTreasury and Trade Solutions Client Sales ManagementLatin America & Mexico HeadCiti Transaction ServicesEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026

Industrials SectorInes Vargas BarreraEmail: [email protected]: +52 (181) 8366 - 5190Of. Phone: +52 (81) 1226 - 8525

Branding, Consumer and Healthcare SectorOscar MazzaEmail: [email protected]: +1 (305) 588 - 9396Of. Phone: +1 (305) 347 - 1336

Technology, Media and Telecom SectorGabriel KirestianEmail: [email protected]: +54 (911) 3301 - 4826Of. Phone: +54 (11) 4329 - 1516

Energy, Power and Chemicals SectorPeter LangshawEmail: [email protected]: +55 (11) 6183 - 6958Of. Phone: +55 (11) 6183 - 6958

Public SectorJorg PaascheEmail: [email protected]: +52 (1) 55 5453 - 0103Of. Phone: +52 (55) 2226 - 6020Based: Mexico DF, Mexico

Non Bank FI Sector (NFBI)Ricardo DessyEmail: [email protected]: +54 (911) 6641 - 9752Of. Phone: +54 (11) 4329 - 1471Based: Buenos Aires, Argentina

BrazilAdoniro CestariEmail: [email protected]: +55 (11) 7130 - 9447Of. Phone: +55 (11) 4009 - 7838Based: Sao Paulo, Brazil

Central AmericaEvelin MadridEmail: [email protected]: + 506 8701 - 4529Of. Phone: +506 2588 - 7541Based: San Jose, Costa Rica

MexicoMiguel YtuarteEmail: [email protected]: +52 (1) 55 4088 - 2284Of. Phone: +5255 (1226) 8895Based: Mexico DF, Mexico

Andean RegionCarolina JuanEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026Based: Bogota, Colombia

ArgentinaAdrian ScosceiraEmail: [email protected]: +54 (911) 5674 - 6966Of. Phone: +54 (11) 4329 - 1194Based: Buenos Aires, Argentina

Citi Transaction Serviceswww.transactionservices.citi.com

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world. All other trademarks are the property of their respective owners.