basic cash flow analysisttsmedia.ttstrain.com/cashflowclb012116.pdf1/21/2016 1 basic cash flow...

TRANSCRIPT

1/21/2016

1

BASIC CASH FLOW ANALYSIS

January 21, 2016

1

CASH FLOW

NET PROFITS DON’T REPAY LOANS

What will your customer do with the loan proceeds?

How much will your customer need to borrow?

When will your customer be able to generate enough cash to repay the loan?

2

1/21/2016

2

CASH FLOW

Net profit line on income statement will not answer these questions

Net profits are not cash; they are the result of accounting techniques and policies

Cash and only Cash can repay loans

3

OPEN DISCUSSION

HOW DO YOU DEFINE CASH FLOW?

WHEN DO YOU USE CASH FLOW ANALYSIS?

4

1/21/2016

3

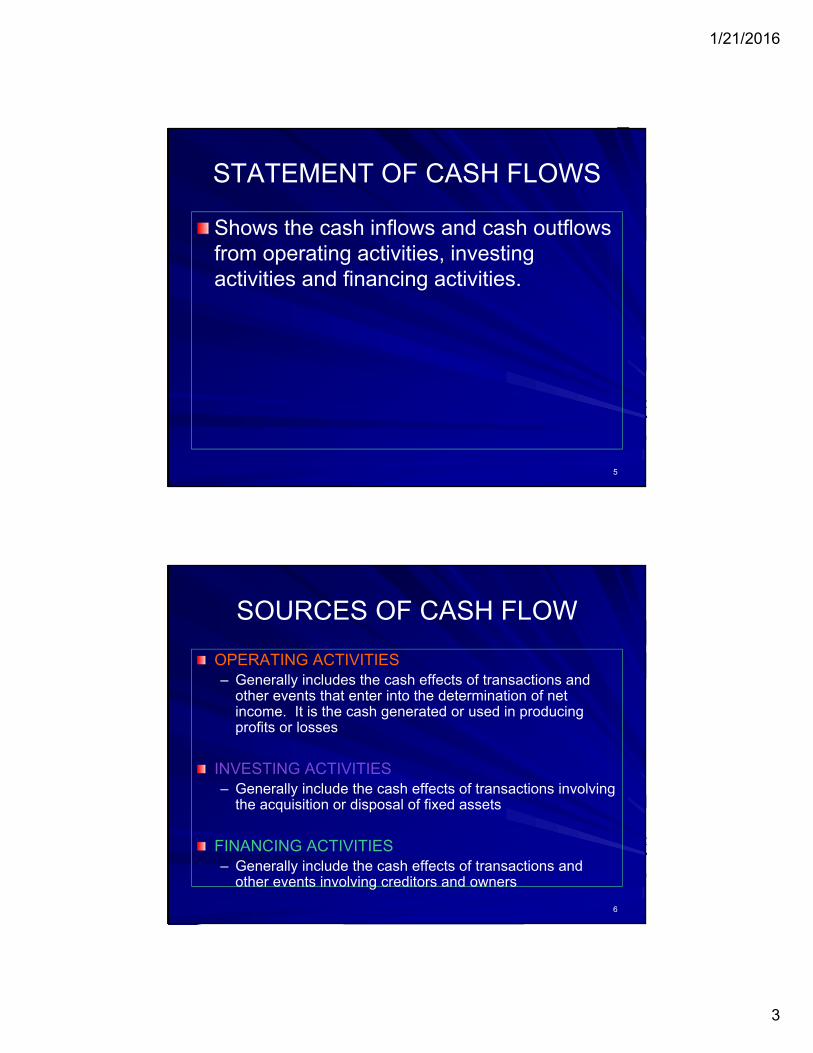

STATEMENT OF CASH FLOWS

Shows the cash inflows and cash outflows from operating activities, investing activities and financing activities.

5

SOURCES OF CASH FLOW

OPERATING ACTIVITIES– Generally includes the cash effects of transactions and

other events that enter into the determination of net income. It is the cash generated or used in producing profits or losses

INVESTING ACTIVITIES– Generally include the cash effects of transactions involving

the acquisition or disposal of fixed assets

FINANCING ACTIVITIES– Generally include the cash effects of transactions and

other events involving creditors and owners

6

1/21/2016

4

CASH FLOW

Cash can come from:– Profits– Sales of assets– Infusion of capital– Loan proceeds– Extensions of additional credit from suppliers

Our challenge is to identify cash inflows/outflows, analyze what has caused them and which ones are most significant, and how future cash flow may differ from the past.

7

SOURCES OF CASH FLOW

INCOME STATEMENT– Sources

Sales/RevenueOther IncomeGain of Sale of Assets

– UsesCost of Goods SoldOperating ExpensesInterest ExpenseIncome taxesLoss on Sale of Assets and Other Expenses

8

1/21/2016

5

SOURCES OF CASH FLOW

Sources and Uses of Cash can be determined from the Balance Sheet also.

It records the place cash was either generated or spent

In order to determine this you must know the Rules of Cash Flow

9

RULES OF CASH FLOWBALANCE SHEET

INCREASE DECREASE SOURCE USE

Asset X

Asset X

Liability X

Liability X

Net Worth X

Net Worth X

10

1/21/2016

6

CASH VS. ACCRUAL

Accrual Bal Sheet Adj. Cash Flow

Sales 1,000,000 (400,000) A/R 600,000

COGS (700,000) 300,000 A/P (400,000)

Gross Prof 300,000 200,000

Oper. Exp. (200,000) 100,000 A/E (100,000)

Pre-Tax Inc 100,000 100,000

Income Tax (34,000) 14,000 ITP (20,000)

Net Income 66,000 80,000

11

A.S. FINDUS COMPANY

12

1/21/2016

7

Traditional Cash Flow

2005 2006

Net Profit 51 115+Depreciation 111 154+Interest 41 54

Available Cash Flow 203 323/CPLTD + Interest 67 77

Debt Coverage Ratio 3.03x 4.19x

13

3 Fallacies with this approach

1. It is Income Statement Focused Only

2. It covers operations for one year only

3. We bankers think “we are all that” because we believe our customers will pay us first from Available Cash Flow before their Payroll and Suppliers

14

1/21/2016

8

UCA CASH FLOW ANALYSIS

Explanation of UCA Form

15

TARGET POINTS 1 & 2Sales 11,025

*Accounts Receivable (311)

Cash Collected-Sales 10,714

Cost of Sales (-Dep.) (8,240)

*Inventory (443)

*Accounts Payable 234

Cash Paid for Product (8,449)

Cash Fr. Trading Act. 2,26516

1/21/2016

9

TARGET POINT 3

SG& A Exp. (- Dep/Int) (2,399)

*Prepaid Expenses (7)

*Accrued Expenses 95

Cash Paid For Operations (2,311)

Cash After Operations (45)

17

TARGET POINT 4Other Income (Exp.) 14

*Other Assets & Liabs. (14)

Income Tax Expense (77)

*Deferred Taxes 0

*Income Taxes Payable (2)

Other Inc/Exp/Taxes (79)

Net Cash After Operations (124)

18

1/21/2016

10

TARGET POINTS 5 & 6Interest Expense (54)

*Interest Payable 1

Dividends Declared (30)

*Dividends Payable 30

Cash Paid for Div/ Int. (53)

Cash After Financing (177)

Less: CPLTD (23)

Cash After Debt Amor (200)19

Reconciliation of Retained Earnings

Beginning Retaining (end of 2005) 915

+Profits for 2006 115

Expected Ending Ret. Earn. 1,030

Actual Ending Ret. Earn. 1,000

Rule:

If the Actual < Expected, you have one question

“Who took the money”

20

1/21/2016

11

TARGET POINT 7*Fixed Assets (232)

*Investment 0

*Intangibles 0

Cash Paid Plant & Invest. (232)

Financing Surplus/

(Requirement) (432)

21

Reconciliation of Net Fixed Assets

Beginning NFA 533- Current Year’s Depreciation (154)

Expected Ending NFA 379

Actual Ending NFA 611

Difference (232)

Rule:

If the Actual > Expected = Bought Assets

If the Actual < Expected = Sold Assets22

1/21/2016

12

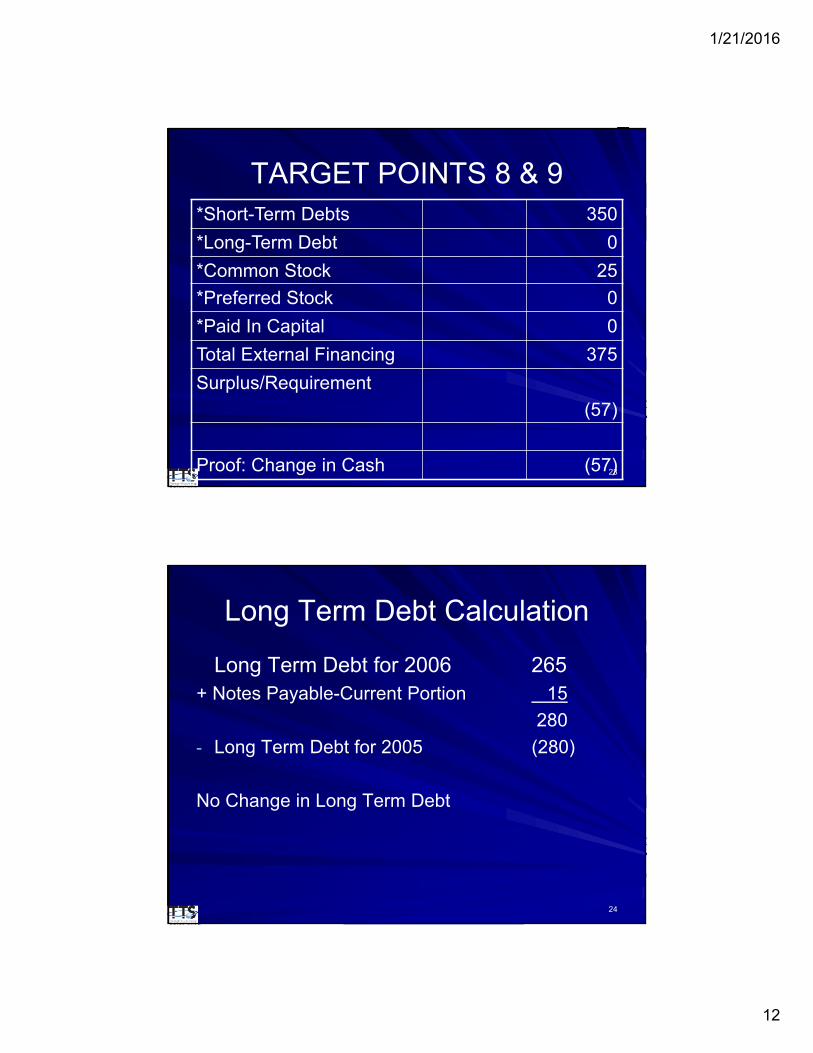

TARGET POINTS 8 & 9*Short-Term Debts 350

*Long-Term Debt 0

*Common Stock 25

*Preferred Stock 0

*Paid In Capital 0

Total External Financing 375

Surplus/Requirement

(57)

Proof: Change in Cash (57)23

Long Term Debt Calculation

Long Term Debt for 2006 265+ Notes Payable-Current Portion 15

280

- Long Term Debt for 2005 (280)

No Change in Long Term Debt

24

1/21/2016

13

What Happened to Cash Flow?

• Increase in A/R of 311,000

• Increase in Inventory of 443,000

• Marginally Profitable Operations

25

How Did the Company Survive?

• They borrowed money from the bank to pay the bank!!!

• They used the Line of Credit for this purpose and to fund the addition to Fixed Assets

• Both are violations of bank financing rules

26

1/21/2016

14

CASH FLOW IMPACT

2004 2005 2006

Sales Growth N/A 42.0% 30.0%

Gross Profit 24.7% 24.5% 25.3%

Operating Exps. 23.3% 23.7% 23.6%

Net Profit Margin 0.6% 0.6% 1.0%

27

CASH FLOW IMPACTTurnover In Days

2004 2005 2006

A/R 29.2 .2 29.4 3.5 32.9

INVENTORY 19.6 2.5 17.1 15.8 32.9

ACCTS. PAY. 11.1 2.1 13.2 7.4 20.6

28

1/21/2016

15

CASH FLOW IMPACT

1 DAYS SALES = $11,025,000365 DAYS

= $30,205

1 DAYS COGS = $8,240,000 365 DAYS

= $22,575

29

CASH FLOW IMPACT

A/R: $30,205 X 3.5 Days = $105,718

INV: $22,575 x 15.8 Days = $356,685

A/P: $22,575 x _7.4 Days = $167,055

Net Cash Flow Impact = $295,348

30

1/21/2016

16

INDIRECT CASH

FLOW METHOD

31

DIFFERENCES

• Other Current Accounts are accounted for in the Investing Activities Section

• CPLTD and LTD are calculated by considering the change from last year rather than the method demonstrated above

• Bottom Line: We still reach the same conclusion

32

1/21/2016

17

Global Cash Flow Analysis

Business Cash Flow

+Net Personal Cash Flow

= Global Cash Flow

33

Thanks for joining us!Bankers Insight Group

3695 F Cascade Road #1201

Atlanta, Georgia 30331

Wesley Kavelaris

TTS

www.BankWebinars.com

800-831-0678

34

Upcoming Webinars

January 26th – Advertising Compliance

January 26th – Improving Employee Performance in Everyday Work Situations & Reviews

January 27th – Home Equity Lines of Credit

January 27th – Best-Ever Compliance Checklists for Consumer Loans

January 28th – 20 Legal Account Ownerships, Titles, Sample Signature Cards and Legal Documentation

January 28th – Deliver Training That Sticks

February 2nd – Writing High-Impact Executive Summaries

February 3rd – Excel Explained: Internal Control

February 3rd – Call Report for Banks - Recent Changes, Highlights, and Pitfalls

February 5th – BSA Series: Customer Due Diligence Preparing for the Change