basic accounting concepts.docx

TRANSCRIPT

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 1/12

Basic Accounting Concepts

Business Entity Concept/Accounting Entity Concept

According to this concept, the business is considered as a separate business entity from its owner(s). Thus the

financial information of the business will be recorded and reported separately from its owner’s personal financial

information.

Going Concern

For accounting purposes, it is assumed that the business will operate for an indefinite period of time and thus

considered as ‘going concern’. For this reason, the realizable value of the property owned by business will not be

relevant.

Money Measurement

Only those transactions will be recorded in the financial books which can be measured in terms of money. Anything

which cannot be measured in monetary terms will not be considered as a part of the accounting data.

Historical Cost

All assets will be recorded at their cost price. This means that machinery purchased years ago will be recorded at its

original cost of purchase even though its value is lower now.

The reason for doing so is because the business is considered as a going concern and we need not be worried about

the saleable value of the asset.

Accounting Period

The life a business is considered to be indefinite. But for accounting purposes, the life of the business is divided into

specified periods of time. The period may be a month, a half year, a full year or any length of time.

Accrual Concept

Accrual concept states that revenue is recognized when it is earned and expenses when they are incurred.

Any income or revenue generated must be recorded in the books of accounts whether the payment for it is received

or not. Similarly, any expense done by the business should be recorded irrespective of the fact that the business has

paid for it or not.

Objectivity

Any transaction which is recorded in the accounting books should be verifiable. In other words, the transaction

should backed by some proof in the form of a receipt, invoice, cheque, voucher etc.

Consistency

According to this concept, the same accounting method should be applied in each accounting period when preparing

financial reports. This makes it easy to compare results of one period with another period and the stakeholders can

get a more realistic idea about the performance of the business.

Prudence

It involves being cautious while reporting accounting information. The assets should not be overstated and the

liabilities should not be understated.

This is why closing stock is always valued at the lower of cost or market value so that the profits are not overstated.

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 2/12

Matching Principle

This principle is based on accrual concept of accounting. It states that revenue earned during a specific period has to

be matched with the expenses incurred with earning that revenue. The following point should be considered:

If an item of revenue is shown in the Profit and Loss account, all expenses incurred on it, whether paid or not, should

be shown as expenses in the Profit and Loss account.

An expense will be recorded in the books of accounts if the revenue associated with it has not been realized.

Incomes received in advance should not be shown in Profit and Loss account.

All the cost and expenses incurred on good remaining unsold at end of the year must be carried forward to next year

as these goods will be sold in the next accounting period.

What are Non Profit Organizations?

Sole trader, Partnership and Limited companies have Profit as their main objective. However, Clubs, societies and

associations does not only exist to make profit. They may be formed to promote cultural and recreational interest.

Thus their final accounts are different from those organizations which solely exist to earn profit.

The final accounts of a non-profit organization includes of

Trading Accounts (only if there is a restaurant or canteen)

Receipts and Payments Accounts

Income and Expenditure Account

Balance Sheet

Receipts and Payments AccountFormat for Receipts and Payments Account

Receipt and Payments Account

for the year ended 31 December 2010

Dr. Cr.

Receipts Amount Payments Amount

Balance b/d (Opening

balance)

All Cash receipts

XXXX

XXXX

All cash payments xxxxx

XXXX

Balance c/f (closing

balance)

xxxxx

XXXXX XXXXX

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 3/12

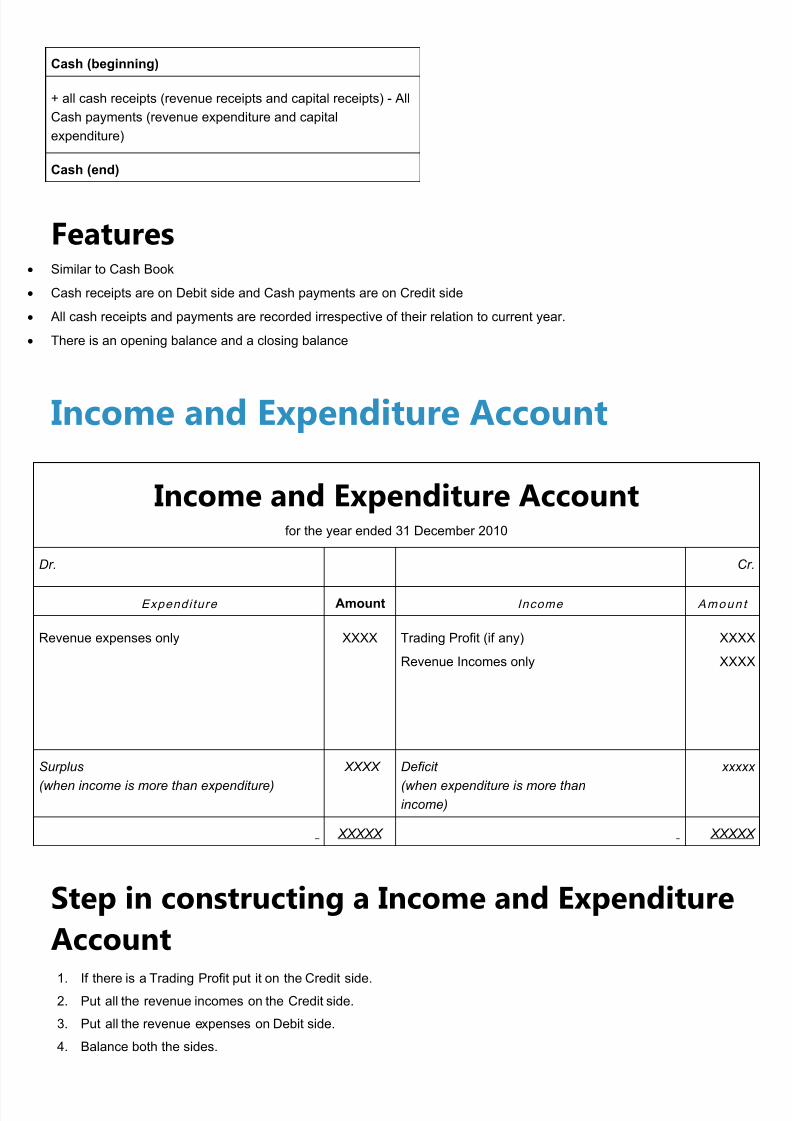

Cash (beginning)

+ all cash receipts (revenue receipts and capital receipts) - All

Cash payments (revenue expenditure and capital

expenditure)

Cash (end)

Features Similar to Cash Book

Cash receipts are on Debit side and Cash payments are on Credit side

All cash receipts and payments are recorded irrespective of their relation to current year.

There is an opening balance and a closing balance

Income and Expenditure Account

Income and Expenditure Accountfor the year ended 31 December 2010

Dr. Cr.

Expendi ture Amount Income Amoun t

Revenue expenses only XXXX Trading Profit (if any)

Revenue Incomes only

XXXX

XXXX

Surplus

(when income is more than expenditure)

XXXX Deficit

(when expenditure is more thanincome)

xxxxx

XXXXX XXXXX

Step in constructing a Income and Expenditure

Account

1. If there is a Trading Profit put it on the Credit side.2. Put all the revenue incomes on the Credit side.

3. Put all the revenue expenses on Debit side.

4. Balance both the sides.

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 4/12

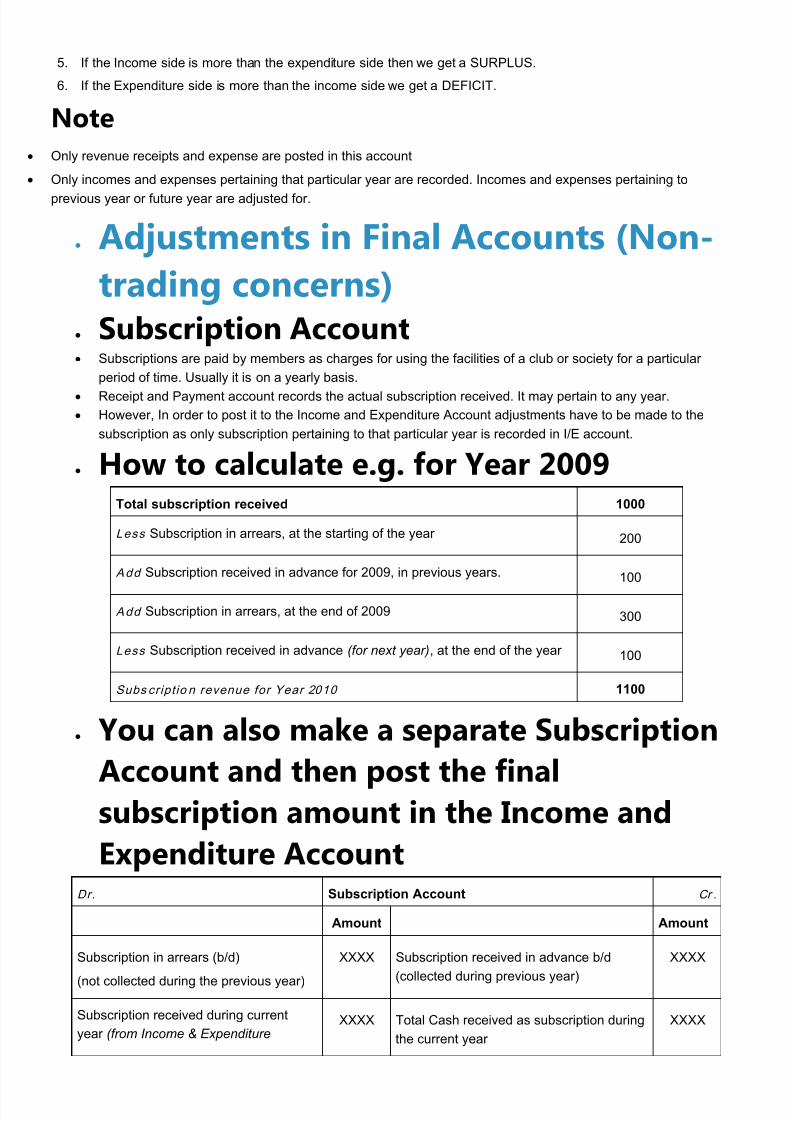

5. If the Income side is more than the expenditure side then we get a SURPLUS.

6. If the Expenditure side is more than the income side we get a DEFICIT.

Note Only revenue receipts and expense are posted in this account

Only incomes and expenses pertaining that particular year are recorded. Incomes and expenses pertaining to

previous year or future year are adjusted for.

Adjustments in Final Accounts (Non-

trading concerns) Subscription Account Subscriptions are paid by members as charges for using the facilities of a club or society for a particular

period of time. Usually it is on a yearly basis.

Receipt and Payment account records the actual subscription received. It may pertain to any year.

However, In order to post it to the Income and Expenditure Account adjustments have to be made to the

subscription as only subscription pertaining to that particular year is recorded in I/E account.

How to calculate e.g. for Year 2009Total subscription received 1000

Less Subscription in arrears, at the starting of the year 200

Add Subscription received in advance for 2009, in previous years. 100

Add Subscription in arrears, at the end of 2009 300

Less Subscription received in advance (for next year), at the end of the year 100

Subs cript io n revenue for Year 2010 1100

You can also make a separate Subscription

Account and then post the finalsubscription amount in the Income and

Expenditure AccountDr. Subscription Account Cr .

Amount Amount

Subscription in arrears (b/d)

(not collected during the previous year)

XXXX Subscription received in advance b/d

(collected during previous year)

XXXX

Subscription received during current

year (from Income & ExpenditureXXXX Total Cash received as subscription during

the current year

XXXX

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 5/12

Account)

Subscription in advance c/d

(collected for subsequent year)

XXXX Subscription in arrears c/d

(not yet collected for current year)

XXXX

XXXX XXXX

Subscription in arrears b/d XXXX Subscription in advance b/d XXXX

What are the reasons for difference in Bank Statement and Cash Book?

These can be summarized as follows:

Cheque issued by the trader but the customer has not yet presented it to the bank for encashment.

This will show a less bank balance in the trader’s Cash book as he has already issued the cheque, but the bank will

not reduce the amount till the cheque is presented to it.

Cheque received by the trader was deposited into the bank for collection but the bank did not realize the funds and

did not credit the Trader’s account.

Trader deposited a cheque into bank but it was dishonored by the bank. The reason may be the customer does not

have sufficient cash in his bank account.

Bank pays interest to the trader on his deposit but the trader will not come to know this till he receives the Bank

statement and thus his cash book will show less balance as compared to bank statement.

Bank might receive direct payment of interest or dividends on behalf of the trader for any investments made by the

trader. The trader will not come to know the details till he gets a bank statement and thus his Cash book will be

understated.

Bank might charge transaction fees or Bank charges or interest on any overdraft which the trader will only know

when he receives the bank statement.

A customer or debtor might directly pay into the trader’s bank account and the trader might not be aware of this.

A Bank may pay bills, insurance premiums or some payment based on the standing instruction of the trader. The

details of these transactions will only be available to the trader once he receives the bank statement.

A bank reconciliation statement can be prepared by taking the balance either as per cash book or as per pass book as

a starting point.

If the statement is started with the balance as per bank column of the cash book, the answer arrived at the end will

be balance as per pass book.

Alternatively, if the statement is started with the balance as per pass book, the answer arrived at in the end will be

the balance as per cash book.

A debit balance as per cash book shows the amount of the money in the bank, whereas, a credit balance means that

the business has taken an overdraft. In the same way, a credit balance as per pass book shows a positive bank

balance whereas debit balance as per pass book shows an Overdraft.

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 6/12

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 7/12

How to make Debtors Control Account Sales transaction takes place

It is recorded in the Sales Journal

From the Sales Journal entry is posted to the Sales Ledger.

From where do you get information to draw

Debtors Control Accounts?Information Source

Total Opening Balance Trial Balance at close of previous period

Total Sales Sales Journal

Dishonoured Cheques Cash Book

Discount allowed withdrawn General Journal

Any charges to debtors General Journal

Total cash and cheques received from debtors Cash book

Discount allowed Cash Book

Returns inwards and allowances Returns Inwards journal

Bad Debts General Journal

How do we prepare Creditors Control Account? Also known as Purchases Ledger Control Account

It accounts for all Creditors appearing in the Purchases Ledger.

From where do you get information to draw

Creditors Control Accounts?Information Sources

Total cash and cheques paid to creditors Cash Book

Discount received Cash Book

Returns outwards and allowances Returns Outwards Journals

Total opening balances Trial Balance at close of previous period

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 8/12

Total purchases Purchases Journal

Any charges by creditors Journal

Minority balances in Control AcccountsNormally, debtors accounts have debit balances

Creditors accounts contain credit balances.

There may instances when debtors might return some goods after their accounts have been settled and this may lead

them to have a credit balance.

What to do? The Debtors control Account will have both the debit and credit balances brought down.

Same procedure will take place for Creditors Control Account.

Through this the true financial position is shown i.e. the exact amount owing by debtors as well as the amount owing

to them.

Trial BalanceTrial Balance is a statement prepared with the debit and credit balances of ledger accounts toverify the arithmetical accuracy of the book.

The Trial Balance checks the equality of debits and credits in the ledger by listing each account along with its ending

balance.

Accounts to be

placed on debit

side

Accounts to be

placed on credit

side

Assets

Expenses

Drawings

Liabilities

Capital

Revenue

Errors revealed by Trial Balance

Errors in calculation Any calculation mistake, especially totaling mistake or balancing mistake will be revealed by Trial Balance as both the

side will not match.

Errors of omission of one entryIf by mistake only one entry is made for a transaction, Trial Balance will not balance.

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 9/12

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 10/12

Assets Assets are items of value owned by the business. Examples include

Building

Machinery

Motor vehicle

Cash at bank

Cash in hand

Stock

Debtors (people who own money to the business)

LiabilitiesThese denote the amounts which the business owes to others. Examples include

Creditors (people to whom the business owes money)

Bills payable Bank overdraft

Bank loan

Owner’s equity The funds of a business provided for by its owners.

Owner’s equity = Assets – Liabilities

Owner’s equity increases by Owner’s equity decreases by

Profits Losses

Additional investment into the business Drawings

Double entry SystemLook at an example:

You own a business, for example, selling shoes.

When you buy shoes from manufacturer: Transaction is your stock increase because new stock comes in. You pay for that stock and thus your cash reduces.

What does it mean? Two entries

Stock increases

Cash decreases

This system is known as Double entry system of book-keeping because for every transaction there are two

entries.

In this system all transactions are entered in a set of accounts.

An account is a place where all the information referring to a particular asset or liability or to capital is

entered.

Thus there is an account for everything in the business e.g. machinery, furniture, creditors, debtors and even capital.

What is an AccountEach account is shown on a different page.

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 11/12

Page is divided vertically into two halves.

Left side is Debit side; right side is Credit side

Rules of Debit and Credit

There are two systems or practices of putting the accounts.

American SystemThis system classifies accounts into five categories:

Assets accountDebit the increase in assets; Credit the decrease in assets

Liabilities accountDebit the decrease in liabilities; Credit the increase in liabilities

Capital accountDebit the decrease in Capital; Credit the increase in Capital

Revenue accountDebit the decrease in income; Credit the increase in income

English systemClassification of Accounts

Personal AccountsPersonal accounts are those which are opened under the NAME of individuals, firms, company, institution etc.

For example John’s account, dinesh’s account, Coca-Cola ltd account, bank account etc.

Rule

Debit the Receiver

Credit the Giver

Real Accounts All the assets owned by the business can be classified in this account. These can be categorized as

Tangible real accounts

All those which can be seen, touched and measured such as

Building

Land

Cash account

Stock account

Furniture account

7/28/2019 Basic Accounting Concepts.docx

http://slidepdf.com/reader/full/basic-accounting-conceptsdocx 12/12

Intangible real accountsThose accounts which cannot be touched or seen. Examples include

Goodwill account

Patent accounts

Rule

Debit what comes inCredit what goes out

Nominal AccountsThese include all those accounts which are related with incomes/gains and expenses/losses of the business.

Incomes/gains Expenses/losses

Commission received account Rent paid account

Discount received account Salary paid account

Interest received account Commission paid account

Dividends received account Discount allowed account

Loss due to theft account

Loss due to fire account

Rule

Debit all expense and losses

Credit all incomes and gains