basel committee revises basel iii on the capital … · 1 attorney advertisement news bulletin june...

TRANSCRIPT

1 Attorney Advertisement

News Bulletin June 22, 2011

Basel Committee Revises Basel III on the Capital Treatment for Bilateral Counterparty Credit Risk

On 1 June 2011, the Basel Committee on Banking Supervision (the “BCBS”) published a press release1 announcing that it had finished its review of and finalised the Basel III capital treatment for counterparty credit risk (“CCR”) in bilateral trades. Following the review, it has made a minor change to the credit valuation adjustment (“CVA”), being the measure of the risk of loss caused by changes in the credit spread of a counterparty due to changes in its credit quality. The existing Basel II regime addresses counterparty default and credit migration risk but not the risk of mark-to-market losses caused by credit valuation adjustments.

In December 2010, the BCBS published the Basel III rules2 setting out, amongst other things, capital requirements for CCR exposures, which included capital rules for CVA risk that involved both the standardised and advanced methods. At the time it published the main text of Basel III, the BCBS stated that the level and reasonableness of the standardised CVA risk capital charge was subject to a final impact assessment, which has now been completed. Its review found that the standardised method as set out in the December 2010 rules text could be unduly punitive for low-rated counterparties with long maturity transactions. In order to narrow the gap between the capital required for CCC-rated counterparties under the standardised and the advanced methods, the BCBS has decided to reduce the weight applied to CCC-rated counterparties from 18% to 10%.

The BCBS has issued a revised version of the Basel III capital rules, including the relevant change (in paragraph 104).3 The BCBS has indicated that all other aspects of the regulatory capital treatment for CCR and CVA risk remain unchanged from the December 2010 text. The press release also states that the BCBS is presently completing its review of the capitalisation of bank exposures to central counterparties and expects to finalise its December 2010 proposals before the end of 2011.

1 http://www.bis.org/press/p110601.pdf. 2 http://www.bis.org/publ/bcbs189_dec2010.pdf; see also Morrison & Foerster client alert: Basel III: The (Nearly) Full Picture (December 23, 2010), http://www.mofo.com/files/Uploads/Images/101223-Basel-III-The-Nearly-Full-Picture.pdf. 3 http://www.bis.org/publ/bcbs189.pdf.

2 Attorney Advertisement

Contacts

Peter Green +44 20 7920 4013 [email protected]

Nimesh Christie +44 20 7920 4175 [email protected]

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2011 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

1 Attorney Advertisement

News Bulletin April 2011

Possible Structures to Address Bail-In Proposals

Background

One important aspect of the international response to the financial crisis is the ongoing work in relation to proposals that banks and other financial institutions be required to issue debt with “bail-in” features, i.e. debt that is subject to write-down or conversion into equity in certain circumstances. The Financial Stability Board and Basel Committee for Banking Suspension are continuing to consider proposals in this regard, particularly in relation to institutions regarded as systemically important. A recent working document published by the DG Internal Market and Services of the EU Commission (the “EU Paper”) set out various technical details of a possible EU framework for bank recovery and resolution. Amongst the more controversial aspects of the EU Paper is a proposal that a mechanism be introduced allowing relevant regulatory authorities of member states to require a bank to write down or convert to equity some or all of the debt owed to its unsecured creditors (subject to certain exemptions) upon the occurrence of specified trigger events.

Feedback to the EU Paper so far, including from the European Central Bank, has highlighted that such approach is likely to have a significant impact on the way banks obtain funding and should not be introduced without a full impact assessment being carried out. The EU Paper is therefore subject to development and change and the EU Commission may make significant changes to its approach following completion of the consultation process. We understand that concerns in relation to the EU proposals and the other international initiatives referred to above are already leading some investors away from unsecured senior bank debt and towards covered bonds.

As referred to above, the EU Paper envisages that certain debt might be excluded from the write-down and conversion powers including (i) swaps, repos and other derivative transactions, (ii) trade creditors, (iii) short term debt, (iv) retail and wholesale deposits (v) secured debt (including covered bonds) and (vi) claims covered by master netting arrangements. These exemptions will be critically important in structuring any debt instruments designed to fall outside any statutory bail-in power and are likely to be subject to considerable scrutiny and debate. If the EU Commission proceeds with the proposals, it may therefore seek to tighten-up or reduce the exemptions it currently envisages. The extent of some of these exemptions is also unclear including whether secured debt that is under collateralised will be fully or only partially exempt from the requirements.

Although covered bonds and asset backed securities (including rmbs and cmbs) are an available source of funding for banks, and would be likely to fall within any exemption there are limitations and cost implications of such structures. We understand that some banks are considering “quasi” securitisation or covered bond structures that offer greater flexibility to issuers whilst offering investors senior debt of the bank that is not likely to be subject to write-down or conversion into equity once the bail-in legislation is finalised. We set out below our thoughts as to possible structures that could meet these objectives.

2 Attorney Advertisement

Possible Structures

In light of the above, we have set out some preliminary thoughts below as to how senior debt could be structured so as to not be subject to any statutory bail-in power of a regulatory authority to require the debt to be subject to write-down or conversion into equity upon the occurrence of specified trigger events. We have sought to avoid structures likely to be regarded too complex by investors or which have multiple tranches of debt. We have also sought to develop structures which could be structured as fixed income products. Such structures would need considerable further analysis, particularly in respect of relevant insolvency laws, tax legislation and laws impacting upon the validity of the security granted by the issuer.

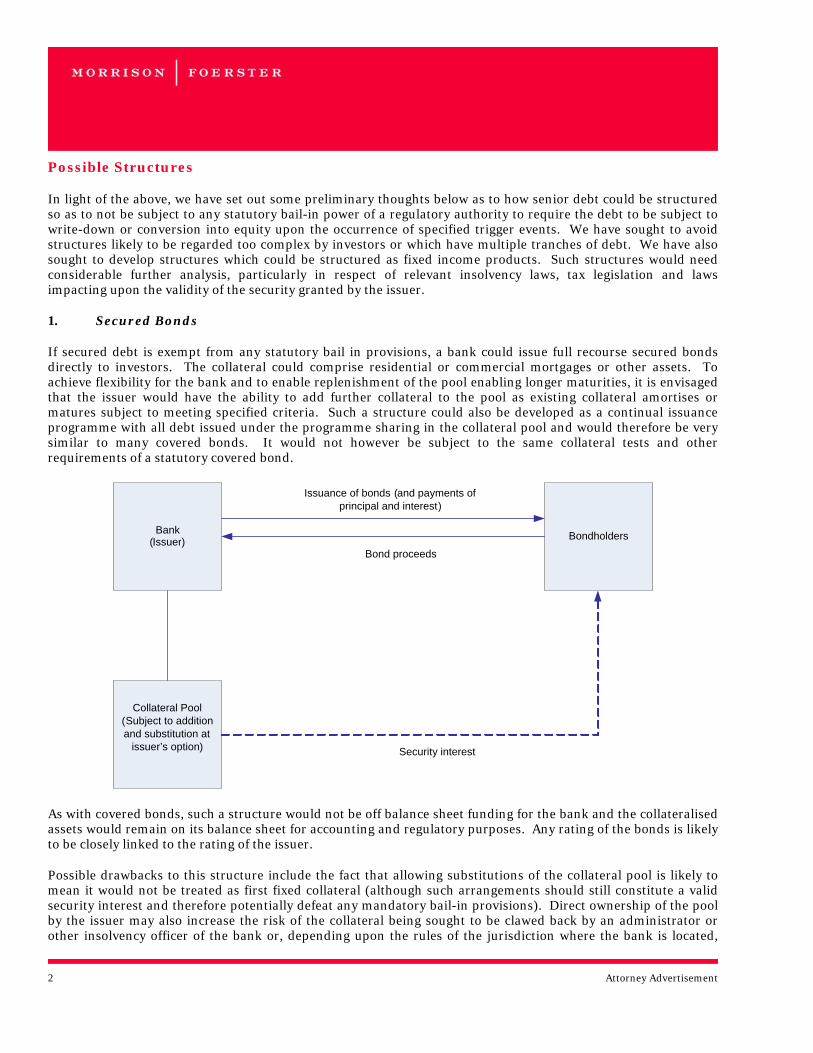

1. Secured Bonds

If secured debt is exempt from any statutory bail in provisions, a bank could issue full recourse secured bonds directly to investors. The collateral could comprise residential or commercial mortgages or other assets. To achieve flexibility for the bank and to enable replenishment of the pool enabling longer maturities, it is envisaged that the issuer would have the ability to add further collateral to the pool as existing collateral amortises or matures subject to meeting specified criteria. Such a structure could also be developed as a continual issuance programme with all debt issued under the programme sharing in the collateral pool and would therefore be very similar to many covered bonds. It would not however be subject to the same collateral tests and other requirements of a statutory covered bond.

As with covered bonds, such a structure would not be off balance sheet funding for the bank and the collateralised assets would remain on its balance sheet for accounting and regulatory purposes. Any rating of the bonds is likely to be closely linked to the rating of the issuer.

Possible drawbacks to this structure include the fact that allowing substitutions of the collateral pool is likely to mean it would not be treated as first fixed collateral (although such arrangements should still constitute a valid security interest and therefore potentially defeat any mandatory bail-in provisions). Direct ownership of the pool by the issuer may also increase the risk of the collateral being sought to be clawed back by an administrator or other insolvency officer of the bank or, depending upon the rules of the jurisdiction where the bank is located,

Bank ( Issuer ) Bondholders

Collateral Pool ( Subject to addition and substitution at

issuer’s option )

Issuance of bonds (and payments of principal and interest)

Bond proceeds

Security interest

3 Attorney Advertisement

being subject to a moratorium against enforcement or liable to transfer to a third party under relevant statutory resolution or recovery powers. Such concerns may be alleviated by using a structure along the lines set out under heading 2 below. It is also likely that under any such structure, upon an insolvency of the issuer, the bonds would need to be accelerated and the collateral realised reasonably shortly after the insolvency of the issuer. This would therefore mean that, unlike many covered bond structures, the noteholders would not be able to continue to receive scheduled principal and interest following a default of the issuer.

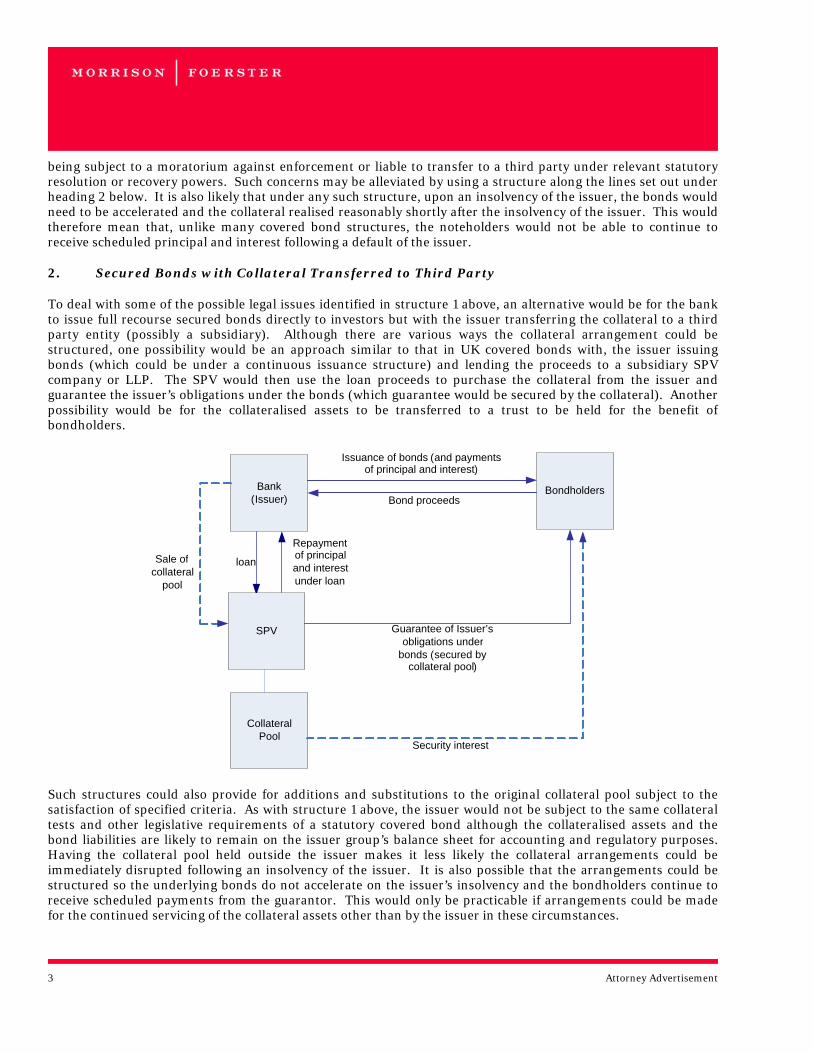

2. Secured Bonds with Collateral Transferred to Third Party

To deal with some of the possible legal issues identified in structure 1 above, an alternative would be for the bank to issue full recourse secured bonds directly to investors but with the issuer transferring the collateral to a third party entity (possibly a subsidiary). Although there are various ways the collateral arrangement could be structured, one possibility would be an approach similar to that in UK covered bonds with, the issuer issuing bonds (which could be under a continuous issuance structure) and lending the proceeds to a subsidiary SPV company or LLP. The SPV would then use the loan proceeds to purchase the collateral from the issuer and guarantee the issuer’s obligations under the bonds (which guarantee would be secured by the collateral). Another possibility would be for the collateralised assets to be transferred to a trust to be held for the benefit of bondholders.

Such structures could also provide for additions and substitutions to the original collateral pool subject to the satisfaction of specified criteria. As with structure 1 above, the issuer would not be subject to the same collateral tests and other legislative requirements of a statutory covered bond although the collateralised assets and the bond liabilities are likely to remain on the issuer group’s balance sheet for accounting and regulatory purposes. Having the collateral pool held outside the issuer makes it less likely the collateral arrangements could be immediately disrupted following an insolvency of the issuer. It is also possible that the arrangements could be structured so the underlying bonds do not accelerate on the issuer’s insolvency and the bondholders continue to receive scheduled payments from the guarantor. This would only be practicable if arrangements could be made for the continued servicing of the collateral assets other than by the issuer in these circumstances.

Bank ( Issuer )

Bondholders

Collateral Pool

Issuance of bonds (and payments of principal and interest)

Bond proceeds

Security interest

SPV

Repayment of principal and interest under loan

loan Sale of collateral

pool

Guarantee of Issuer’s obligations under

bonds (secured by collateral pool)

4 Attorney Advertisement

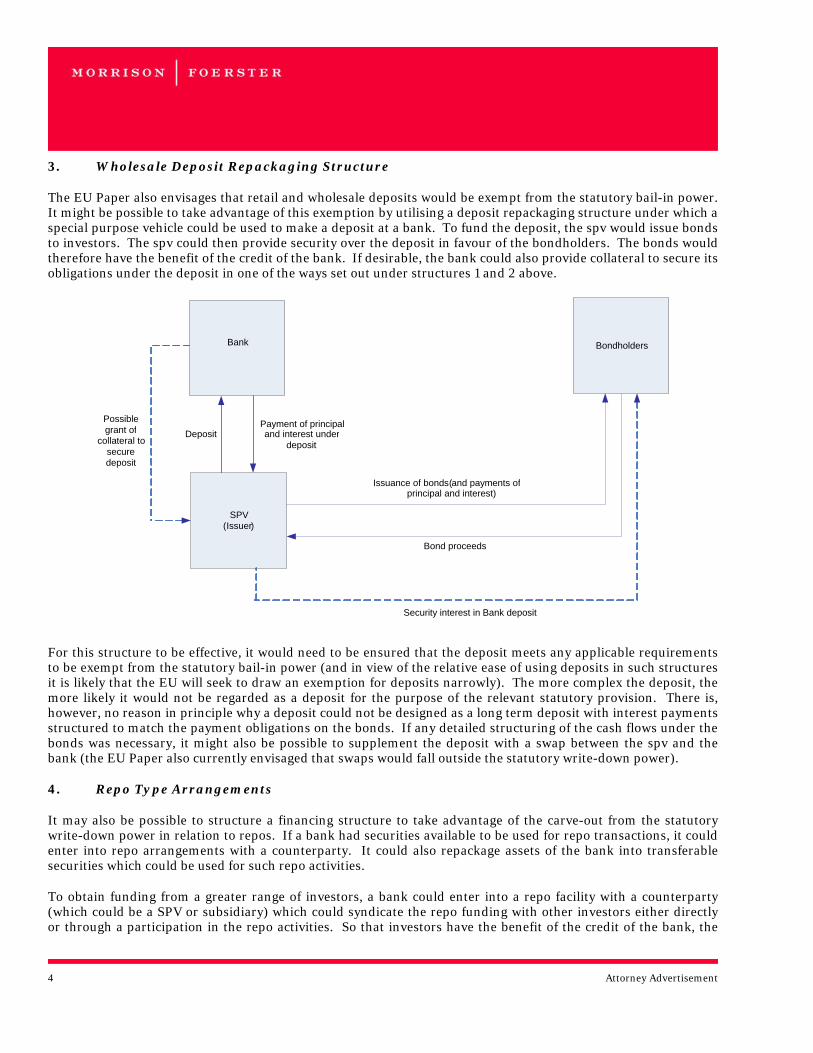

3. Wholesale Deposit Repackaging Structure

The EU Paper also envisages that retail and wholesale deposits would be exempt from the statutory bail-in power. It might be possible to take advantage of this exemption by utilising a deposit repackaging structure under which a special purpose vehicle could be used to make a deposit at a bank. To fund the deposit, the spv would issue bonds to investors. The spv could then provide security over the deposit in favour of the bondholders. The bonds would therefore have the benefit of the credit of the bank. If desirable, the bank could also provide collateral to secure its obligations under the deposit in one of the ways set out under structures 1 and 2 above.

For this structure to be effective, it would need to be ensured that the deposit meets any applicable requirements to be exempt from the statutory bail-in power (and in view of the relative ease of using deposits in such structures it is likely that the EU will seek to draw an exemption for deposits narrowly). The more complex the deposit, the more likely it would not be regarded as a deposit for the purpose of the relevant statutory provision. There is, however, no reason in principle why a deposit could not be designed as a long term deposit with interest payments structured to match the payment obligations on the bonds. If any detailed structuring of the cash flows under the bonds was necessary, it might also be possible to supplement the deposit with a swap between the spv and the bank (the EU Paper also currently envisaged that swaps would fall outside the statutory write-down power).

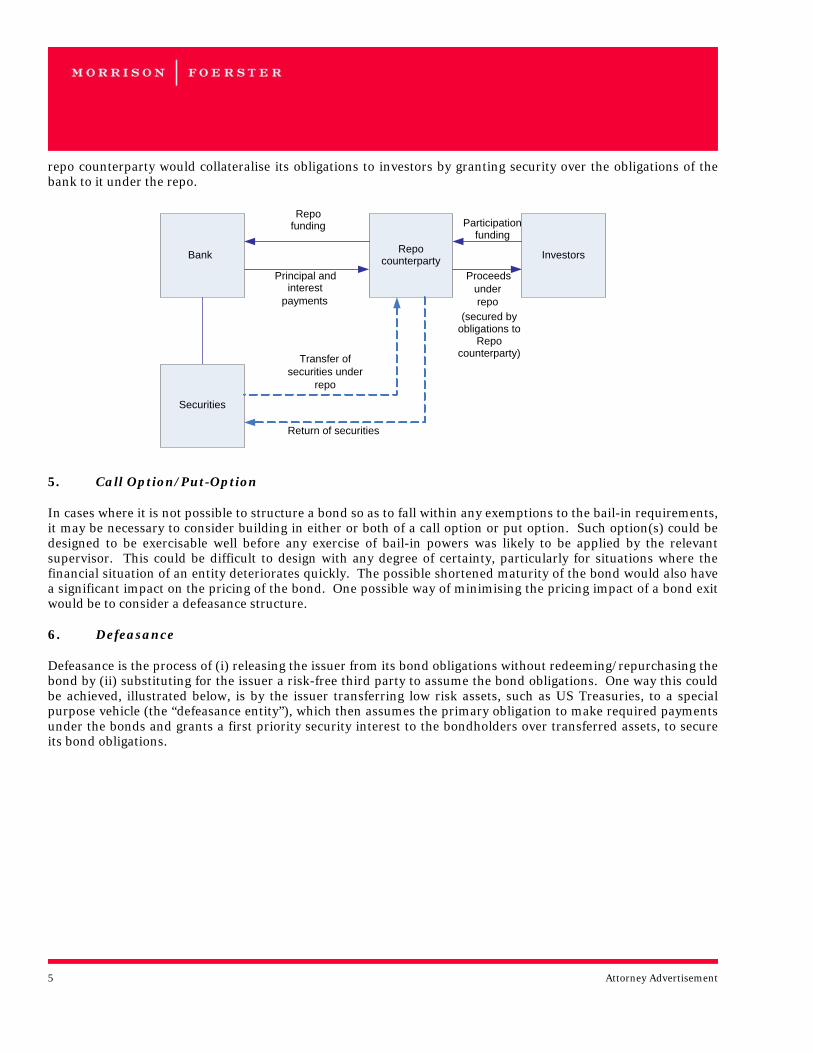

4. Repo Type Arrangements

It may also be possible to structure a financing structure to take advantage of the carve-out from the statutory write-down power in relation to repos. If a bank had securities available to be used for repo transactions, it could enter into repo arrangements with a counterparty. It could also repackage assets of the bank into transferable securities which could be used for such repo activities.

To obtain funding from a greater range of investors, a bank could enter into a repo facility with a counterparty (which could be a SPV or subsidiary) which could syndicate the repo funding with other investors either directly or through a participation in the repo activities. So that investors have the benefit of the credit of the bank, the

Bank Bondholders

SPV ( Issuer)

Payment of principal and interest under

depositDeposit

Bond proceeds

Possible grant of

collateral to secure deposit

Issuance of bonds (and payments of principal and interest)

Security interest in Bank deposit

5 Attorney Advertisement

repo counterparty would collateralise its obligations to investors by granting security over the obligations of the bank to it under the repo.

5. Call Option/Put-Option

In cases where it is not possible to structure a bond so as to fall within any exemptions to the bail-in requirements, it may be necessary to consider building in either or both of a call option or put option. Such option(s) could be designed to be exercisable well before any exercise of bail-in powers was likely to be applied by the relevant supervisor. This could be difficult to design with any degree of certainty, particularly for situations where the financial situation of an entity deteriorates quickly. The possible shortened maturity of the bond would also have a significant impact on the pricing of the bond. One possible way of minimising the pricing impact of a bond exit would be to consider a defeasance structure.

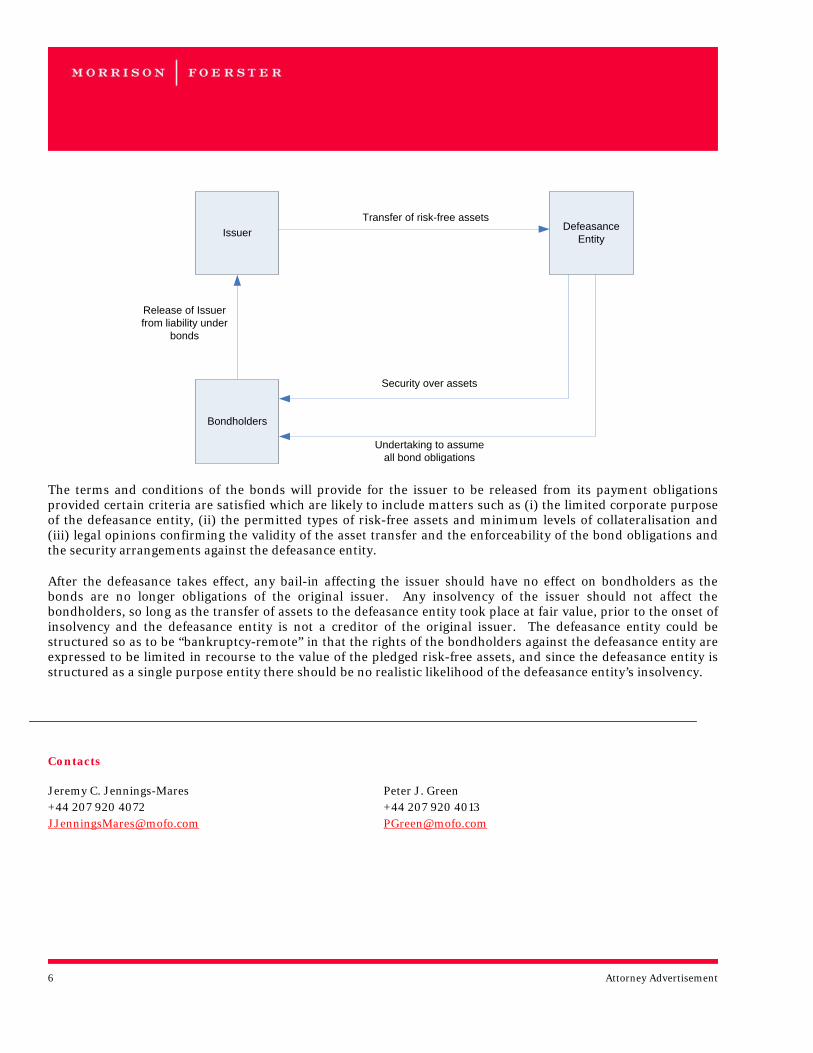

6. Defeasance

Defeasance is the process of (i) releasing the issuer from its bond obligations without redeeming/repurchasing the bond by (ii) substituting for the issuer a risk-free third party to assume the bond obligations. One way this could be achieved, illustrated below, is by the issuer transferring low risk assets, such as US Treasuries, to a special purpose vehicle (the “defeasance entity”), which then assumes the primary obligation to make required payments under the bonds and grants a first priority security interest to the bondholders over transferred assets, to secure its bond obligations.

Bank Repo counterparty

Securities

Investors

Repo funding

Principal and interest

payments

Transfer of securities under

repo

Return of securities

Participation funding

Proceeds under repo

(secured by obligations to

Repo counterparty)

6 Attorney Advertisement

Issuer Defeasance Entity

Bondholders

Transfer of risk-free assets

Release of Issuer from liability under

bonds

Security over assets

Undertaking to assume all bond obligations

The terms and conditions of the bonds will provide for the issuer to be released from its payment obligations provided certain criteria are satisfied which are likely to include matters such as (i) the limited corporate purpose of the defeasance entity, (ii) the permitted types of risk-free assets and minimum levels of collateralisation and (iii) legal opinions confirming the validity of the asset transfer and the enforceability of the bond obligations and the security arrangements against the defeasance entity.

After the defeasance takes effect, any bail-in affecting the issuer should have no effect on bondholders as the bonds are no longer obligations of the original issuer. Any insolvency of the issuer should not affect the bondholders, so long as the transfer of assets to the defeasance entity took place at fair value, prior to the onset of insolvency and the defeasance entity is not a creditor of the original issuer. The defeasance entity could be structured so as to be “bankruptcy-remote” in that the rights of the bondholders against the defeasance entity are expressed to be limited in recourse to the value of the pledged risk-free assets, and since the defeasance entity is structured as a single purpose entity there should be no realistic likelihood of the defeasance entity’s insolvency.

n & Foerster

Contacts

Jeremy C. Jennings-Mares +44 207 920 4072 [email protected]

Peter J. Green +44 207 920 4013 [email protected]

7 Attorney Advertisement

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2011 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

1 Attorney Advertisement

News Bulletin January 21, 2010

The Minimum “Bail-in” Criteria for Regulatory Capital

Further to the 16 December 20101 publication of the final Basel III rules, as reported in our client alert “Basel III: The (Nearly) Full Picture,”2 on 13 January 2011 the Basel Committee on Banking Supervision (“BCBS”) announced the minimum requirements to ensure that all regulatory capital instruments are capable of fully absorbing losses at the point a bank becomes non-viable.3 In its December 2010 papers, BCBS stated that it would be developing more detailed eligibility criteria for contingent capital to address issues of loss absorbency at the point of a bank’s non-viability. Therefore, the minimum requirements set out in the 13 January 2011 paper are additional to the criteria for Tier 1 and Tier 2 capital instruments set out in its December 2010 papers.

BCBS incorporates into the new requirements all of the specific proposals (the “gone-concern” proposals) set out in its consultative document on the matter, which we discussed in our client alert dated 25 August 2010.4

We summarise the key requirements below.

Post-trigger Instrument

Any compensation to the instrument holders as a result of the write-off must be (i) paid immediately and (ii) in the form of common stock (or its equivalent in the case of non-joint stock companies). The issuing bank must maintain all prior authorisations necessary under applicable national company laws and its articles of association (e.g., authorised share capital) in readiness for this contingency.

BCBS has not proposed a single method of calculating the number of shares to be issued upon such write-off or conversion. Based on its consultative document, it appears that BCBS intends that each country should be free to impose a suitable method in that country’s own national context.

1 Basel III: A global regulatory framework for more resilient banks and banking systems (16 December 2010), http://www.bis.org/publ/bcbs189.pdf, and Basel III: International framework for liquidity risk measurement, standards and reporting (16 December 2010), http://www.bis.org/publ/bcbs188.pdf. 2 See Morrison & Foerster client alert: Basel III: The (nearly) full picture (23 December 2010), http://www.mofo.com/files/Uploads/Images/101223-Basel-III-The-Nearly-Full-Picture.pdf. 3 BCBS press release: “Basel Committee issues final elements of the reforms to raise quality of regulatory capital” and annex: “Minimum requirements to ensure loss absorbency at the point of non-viability” (13 January 2011), http://www.bis.org/press/p110113.pdf. 4 See Morrison & Foerster client alert: Super-Absorbent Bank Regulatory Capital (25 August 2010), http://www.mofo.com/files/Uploads/Images/100825SuperAbsorbent.pdf.

2 Attorney Advertisement

Trigger Event

The trigger event (“Trigger Event”) is the decision either (i) that a write-off (or conversion) is necessary or (ii) to make a public sector injection of capital (or equivalent support), whichever is earlier. Each of these is subject to a determination by the relevant authority that the bank would otherwise become non-viable.

Any issuance of new shares upon the Trigger Event must be timed to precede any public sector injection of capital, to prevent a dilution of the public sector capital.

Treatment of Banking Groups

The relevant jurisdiction for determining the Trigger Event is that in which the capital is given recognition for regulatory purposes. Where an issuing bank is part of a wider banking group, and wants to include the instrument in both its solo capital and the group’s consolidated capital, both the jurisdictions of the issuing bank and the banking group must be capable of triggering write-down or conversion. Therefore, the instrument’s contractual terms must specify an additional Trigger Event by reference to the supervisory authority of the consolidated group (i.e., in addition to the relevant authority of the bank’s home jurisdiction).

In such case, any common shares issued as compensation to the instrument holders can be those of either the issuing bank or the group parent company (including any successor in resolution).

Transitional Arrangements

Instruments which are issued on or after 1 January 2013 must meet these minimum requirements as a pre-condition to receiving regulatory capital treatment. To minimise the impact on existing creditors, instruments which are issued prior to 1 January 2013 which do not meet the minimum requirements will be gradually phased out from that date. The Basel III rules published in December 2010 fix the base at the nominal amount of such instruments outstanding on 1 January 2013. Their recognition will be capped at 90% from 1 January 2013, with the cap reducing by 10% in each subsequent year.

Potential Implications

Banks may seek to refinance part or all of their outstanding Additional Tier 1 or Tier 2 capital, in anticipation of the new minimum “bail-in” criteria as well as the more stringent capital requirements under Basel III. Some have already started this process by issuing hybrid capital instruments, but with trigger events which are set by reference to defined capital ratios, rather than left to be decided at the discretion the regulator.

On 6 January 2011, the European Commission suggested in a consultation paper in relation to bank recovery and resolution that regulators could be given the power to write-down senior debt as part of the resolution tools.5 Given the overall uncertainty as to the factors which the regulators may take into account in determining the Trigger Event, it is unclear what kind of investor appetite there might be for new instruments which develop based on the new requirements.

It will also be interesting to see the effect that the requirements have upon the issuance of hybrid debt instruments, particularly Tier 2 instruments which have previously only been required to absorb losses on a gone-concern basis, when a firm is wound-up or becomes insolvent. The new requirements are therefore likely to blur some of the distinctions between Tier 1 and Tier 2 instruments. It is possible that previous investors in Tier 2 instruments may be unwilling to take the additional risk of the instruments being written-off or converted into common shares upon the occurrence of a trigger event.

5 European Commission consultation paper: EU framework for bank recovery and resolution (6 January 2011), http://ec.europa.eu/internal_market/consultations/docs/2011/crisis_management/consultation_paper_en.pdf.

3 Attorney Advertisement

Next Steps

BCBS has stated that systemically important banks should have additional “going-concern” loss absorbency (i.e., at a point prior to the Trigger Event referred to above) that could be provided by contingent capital instruments beyond the minimum criteria, and that it is working with the Financial Stability Board to develop an integrated approach which may involve a combination of capital surcharges, contingent capital and bail-in debt.6 BCBS is expected to develop this work in the next few months.7

bout Morrison & Foerster

Contacts

Peter Green +44 20 7920 4013 [email protected] Helen Kim +44 20 7920 4147 [email protected]

Jeremy Jennings-Mares +44 20 7920 4072 [email protected]

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2011 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

6 See Morrison & Foerster client alert: The New Global Minimum Capital Standards Under Basel III (15 September 2010), http://www.mofo.com/files/Uploads/Images/100915-Basel-III.pdf. 7 See Remarks of Nout Wellink, BCBS chairman: “Basel III and beyond” (17 January 2011), http://www.bis.org/speeches/sp110118.pdf.

1 Attorney Advertisement

News Bulletin December 23, 2010

Basel III: The (Nearly) Full Picture

Following endorsement of its proposed reforms of the Basel II framework at the G20 Seoul Summit in November 2010, the Basel Committee on Banking Supervision (“BCBS”) published the final Basel III rules on 16 December 2010. The rules are contained in two separate documents: (1) Basel III: A global regulatory framework for more resilient banks and banking systems and (2) Basel III: International framework for liquidity risk measurement, standards and reporting,1 together with the results of the BCBS’s comprehensive quantitative impact study (“QIS”).2

We summarise below certain of the key features of the new Basel III rules.

Quality and Quantity of Capital

As foreshadowed in their December 2009 proposals3 and the revised July 2010 proposals,4 BCBS has resolved that the predominant form of bank capital should be common shares (or the equivalent for non-joint stock companies), retained earnings and other reserves (“Common Equity Tier 1 Capital”); deductions from capital and prudential filters must be harmonised internationally and generally applied at the level of common equity; Tier 1 capital instruments other than Common Equity Tier 1 Capital (“Additional Tier 1 Capital”) must have very strong equity-like characteristics, such as deep subordination and fully discretionary, non-cumulative dividend/coupon payments, and must be perpetual and contain no incentive to redeem; capital instruments other than Tier 1 Capital (“Tier 2 Capital,” since Tier 3 will be eliminated) will need to contain certain minimum, harmonised characteristics; and all elements of capital will be required to be disclosed and reconciled to the bank’s reported accounts.

1. Definition of Capital

The definition of capital is substantially the same as initially proposed in December 2009, except as to certain regulatory adjustments applicable to Common Equity Tier 1 Capital which were modified and relaxed in July 2010.

1 Basel III: A global regulatory framework for more resilient banks and banking systems (16 December 2010), http://www.bis.org/publ/bcbs189.pdf, and Basel III: International framework for liquidity risk measurement, standards and reporting (16 December 2010), http://www.bis.org/publ/bcbs188.pdf. 2 BCBS Results of the comprehensive quantitative impact study (16 December 2010), http://www.bis.org/publ/bcbs186.pdf. 3 See Morrison & Foerster client alert: More, More, More: A Summary of the Basel Proposals (2 February 2010), http://www.mofo.com/files/Publication/2f280bc1-1b9a-4d98-929f-0a4554236d0f/Presentation/PublicationAttachment/7cf62184-8f7b-48c4-a4f8-1de08055cfe4/SummaryoftheBaselProposals02022010.pdf. 4 See Morrison & Foerster client alert: A little bit less and a bit longer: Update on Basel Capital & Liquidity Reforms (6 August 2010), http://www.mofo.com//files//Uploads/Images/100806BaselCapital.pdf.

2 Attorney Advertisement

Total Capital consists of (i) Tier 1 Capital (going-concern capital), comprising Common Equity Tier 1 and Additional Tier 1 Capital, and (ii) Tier 2 Capital (gone-concern capital).

Common Equity Tier 1 Capital consists of (i) common shares issued by the bank; (ii) any resulting stock surplus (share premium); (iii) retained earnings; (iv) accumulated other comprehensive income and other disclosed reserves; and (v) common shares issued by its consolidated subsidiaries qualifying as Common Equity Tier 1 Capital and held by third parties (i.e., minority interests), subject to regulatory adjustments.

Common shares must satisfy certain specified criteria, including the following: (i) in a liquidation, be the most subordinated claim; (ii) be perpetual (i.e., no redemption/maturity date), without creating any expectation for redemption; (iii) have non-obligatory distributions (i.e., non-payment is not an event of default); (iv) absorb losses on a going-concern basis; and (v) be neither secured nor guaranteed.

An instrument that does not constitute a common share (or equivalent for non-joint stock companies) may still constitute Additional Tier 1 Capital if it meets certain criteria, including:

• as to permanence:

− be perpetual, without any incentive for the issuer to redeem (e.g., interest rate step-ups);

− be callable by the issuer only after a minimum of five years, and only with prior supervisory approval; and

− have its principal repayable (whether on redemption or buy-back) only with prior supervisory approval.

• as to flexibility of payments:

− dividends/coupons must be fully discretionary (i.e., cancellable on a non-cumulative basis); and

− must not have any credit-sensitive dividend feature.

• as to loss absorbency:

− in a liquidation be subordinated to all depositors and creditors, including holders of subordinated debt (i.e., it must be senior only to common equity);

− not contribute to liabilities exceeding assets under any balance sheet solvency test; and

− debt instruments must have principal loss absorption capacity through mandatory conversion to common shares or write-down at a pre-specified trigger point, and otherwise not have any feature which hinders recapitalisation.

An instrument that does not qualify as Tier 1 Capital may still constitute Tier 2 Capital if it meets certain criteria, including:

• as to permanence:

− have a minimum original maturity of at least five years, with no incentive to redeem; and

− be callable only by the issuer and only after a minimum of five years, with prior supervisory approval.

• as to flexibility of payments:

− not have a credit-sensitive dividend feature.

• as to loss absorbency:

− in a liquidation be subordinated to depositors and unsubordinated creditors.

3 Attorney Advertisement

In the case of both Additional Tier 1 and Tier 2 instruments, if issued through a non-operating entity or SPV, the issue proceeds must be immediately available to an operating entity or holding company in the consolidated group.

Regulatory adjustments: In calculating the Common Equity Tier 1 Capital, certain items must be fully deducted or de-recognised, including:

• goodwill and other intangibles (except mortgage servicing rights);

• deferred tax assets (“DTAs”) whose realisation depends on the bank’s future profitability;

• cashflow hedge reserves relating to hedging of items which are not fair valued on the balance sheet;

• any increase in equity capital resulting from securitisation transactions; and

• unrealised gains and losses resulting from changes in bank’s own credit risk on fair valued liabilities.

In addition, certain assets, such as significant investments in the common shares of unconsolidated financial institutions; mortgage servicing rights; and DTAs arising from timing difference, will be given only limited recognition as Common Equity Tier 1 Capital.

Disclosure requirements: To improve transparency of regulatory capital, banks will be required to disclose in their audited financial statements information regarding the instruments included in their regulatory capital and a full reconciliation of all those elements back to their balance sheets. BCBS has stated that it will issue more detailed Pillar 3 disclosure requirements in 2011.

2. Minimum Capital Standards

As foreshadowed in the BCBS 12 September 2010 press release,5 the new minimum capital requirements will be phased in between 1 January 2013 and 1 January 2015, as follows:

From 1 January 2013

From 1 January 2014

From 1 January 2015

Common Equity Tier 1/ Risk-weighted assets (“RWAs”)

3.5% 4.0% 4.5%

Tier 1 Capital/ RWAs 4.5% 5.5% 6.0%

Total Capital/ RWAs 8.0% 8.0% 8.0%

Regulatory adjustments will be phased in at 20% of the required adjustments to Common Equity Tier 1 per annum, starting at 20% on 1 January 2014, building to 100% from 1 January 2018. The same approach will apply to deductions from Additional Tier 1 and Tier 2 Capital.

Existing instruments that no longer qualify as non-Common Equity Tier 1 or Tier 2 Capital will be gradually phased out. Fixing the base at the nominal amount of such instruments outstanding on 1 January 2013, their recognition will be capped at 90% from 1 January 2013, with the cap reducing by 10% in each subsequent year. Existing public sector capital injections will be grandfathered until 1 January 2018.

5 See Morrison & Foerster client alert: The New Global Minimum Capital Standards Under Basel III (15 September 2010), http://www.mofo.com/files/Uploads/Images/100915-Basel-III.pdf.

4 Attorney Advertisement

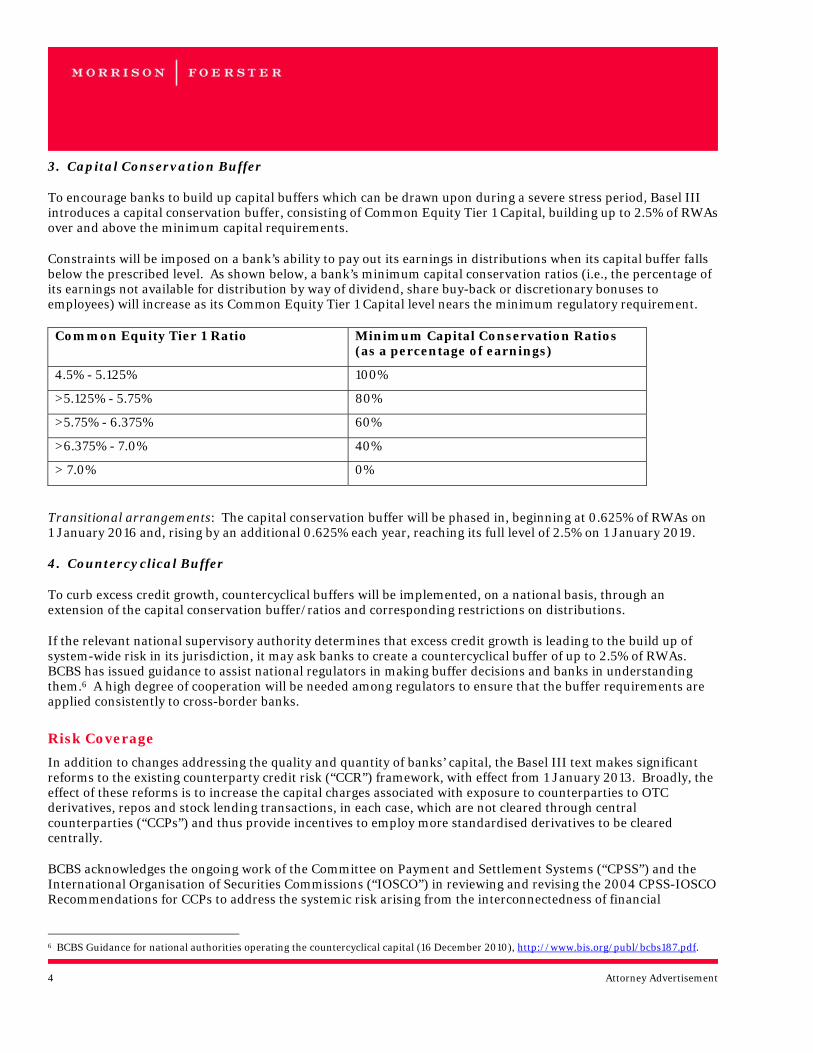

3. Capital Conservation Buffer

To encourage banks to build up capital buffers which can be drawn upon during a severe stress period, Basel III introduces a capital conservation buffer, consisting of Common Equity Tier 1 Capital, building up to 2.5% of RWAs over and above the minimum capital requirements.

Constraints will be imposed on a bank’s ability to pay out its earnings in distributions when its capital buffer falls below the prescribed level. As shown below, a bank’s minimum capital conservation ratios (i.e., the percentage of its earnings not available for distribution by way of dividend, share buy-back or discretionary bonuses to employees) will increase as its Common Equity Tier 1 Capital level nears the minimum regulatory requirement.

Common Equity Tier 1 Ratio Minimum Capital Conservation Ratios (as a percentage of earnings)

4.5% - 5.125% 100%

>5.125% - 5.75% 80%

>5.75% - 6.375% 60%

>6.375% - 7.0% 40%

> 7.0% 0%

Transitional arrangements: The capital conservation buffer will be phased in, beginning at 0.625% of RWAs on 1 January 2016 and, rising by an additional 0.625% each year, reaching its full level of 2.5% on 1 January 2019.

4. Countercyclical Buffer

To curb excess credit growth, countercyclical buffers will be implemented, on a national basis, through an extension of the capital conservation buffer/ratios and corresponding restrictions on distributions.

If the relevant national supervisory authority determines that excess credit growth is leading to the build up of system-wide risk in its jurisdiction, it may ask banks to create a countercyclical buffer of up to 2.5% of RWAs. BCBS has issued guidance to assist national regulators in making buffer decisions and banks in understanding them.6 A high degree of cooperation will be needed among regulators to ensure that the buffer requirements are applied consistently to cross-border banks.

Risk Coverage

In addition to changes addressing the quality and quantity of banks’ capital, the Basel III text makes significant reforms to the existing counterparty credit risk (“CCR”) framework, with effect from 1 January 2013. Broadly, the effect of these reforms is to increase the capital charges associated with exposure to counterparties to OTC derivatives, repos and stock lending transactions, in each case, which are not cleared through central counterparties (“CCPs”) and thus provide incentives to employ more standardised derivatives to be cleared centrally.

BCBS acknowledges the ongoing work of the Committee on Payment and Settlement Systems (“CPSS”) and the International Organisation of Securities Commissions (“IOSCO”) in reviewing and revising the 2004 CPSS-IOSCO Recommendations for CCPs to address the systemic risk arising from the interconnectedness of financial

6 BCBS Guidance for national authorities operating the countercyclical capital (16 December 2010), http://www.bis.org/publ/bcbs187.pdf.

5 Attorney Advertisement

institutions through the derivatives markets. Among other things, the revised Recommendations are intended to cover the risk management of CCPs.

In this regard, BCBS has also issued a separate consultative document setting out its proposals relating to the capitalisation of bank exposures to CCPs and inviting comments until 4 February 2011.7 Whereas the Basel II framework permits exposures to CCPs to be given a risk weighting of zero, BCBS now proposes that trades cleared through “qualifying CCPs” that meet the revised CPSS-IOSCO standards be subject to a risk weight of 2%, to reflect the fact that even regulated CCPs are not completely free of risk. Exposures to non-qualifying CCPs are proposed to be treated in the same way as any other non-centrally cleared, bilateral, OTC derivatives exposure, attracting significantly higher capital charges. BCBS expects to finalise its proposals by September 2011.

Enhanced CCR management: The Basel III rules bolster the existing requirements as to a bank’s CCR management in a number of ways, e.g., (i) expanding the CCR stress testing requirements for banks using the internal model method (“IMM”), and (ii) initial validation and ongoing review and regular back-testing of its IMM approach.

External credit ratings: To try and address the BCBS’s view that the existing capital framework has encouraged investors to place too much reliance on external credit ratings, the following requirements will be introduced by Basel III:

• An issue-specific rating assessment may only be applied by a bank to an unrated issue by the same issuer if the unrated issue ranks pari passu with or senior to the rated issue; if the borrower has an issuer rating, only senior claims on that issuer will benefit from the issuer rating;

• Banks should develop methodologies to assess for themselves the credit risk of securitisation exposures, whether externally rated or unrated;

• In determining the eligibility of an external credit assessment institution (“ECAI”), national supervisors should refer to the IOSCO Code of Conduct Fundamentals for Credit Rating Agencies;

• Certain changes to the eligibility criteria, for credit risk mitigation purposes, of entities providing credit protection, in order to eliminate certain “cliff-effects”; and

• Banks must use the chosen ECAIs and their ratings consistently for both risk weighting and risk management purposes. In general, banks should use solicited ratings from eligible ECAIs, but national supervisors may allow them to use unsolicited ratings.

BCBS is also conducting a more fundamental review of the securitisation framework, including its reliance on external ratings.

Leverage Ratio

To constrain the build-up of excessive leverage in the banking system, a new leverage ratio will be introduced, based on banks’ Capital compared to their Exposure as follows:

Capital will be based on the new definition of Tier 1 Capital and items that are deducted from Capital should also be deducted from the Exposure.

Exposure should follow accounting standards, as follows:

7 BCBS Consultative Document: Capitalisation of bank exposures to central counterparties (20 December 2010), http://www.bis.org/publ/bcbs190.pdf.

6 Attorney Advertisement

• On-balance sheet, non-derivative exposures must be net of specific provisions and valuation adjustments must be stated without deduction of physical or financial collateral, guarantees or credit risk mitigation purchased and no netting of loans and deposits is allowed;

• Exposure to repos, reverse repos and stock loans should be calculated by applying the accounting measure of exposure and the Basel netting rules; and

• Further detailed rules are applicable in respect of derivatives and off-balance sheet items.

The transition period for the leverage ratio will consist of (i) a supervisory monitoring period from 1 January 2011, and (ii) the parallel run period from 1 January 2013 until 1 January 2017, during which BCBS proposes to test a minimum leverage ratio of 3%. Bank level disclosure of the leverage ratio and its components will start on 1 January 2015.

Basel III Liquidity Rules

The document entitled “Basel III: International framework for liquidity risk measurement, standards and reporting” sets out the amended rules relating to liquidity, including the details of the two new liquidity ratios to be applied by banking supervisors.

1. Liquidity Standards

BCBS has developed two separate standards for supervising liquidity risk.

The Liquidity Coverage Ratio (“LCR”) is designed to ensure that banks have a sufficient stock of high-quality liquid assets to survive a significant liquidity stress scenario lasting 30 days. LCR builds on the traditional internal methodologies used by banks to assess exposure to contingent liquidity events and is defined as (stock of high-quality liquid assets) ÷ (total net cash outflows over the next 30 days). A bank’s LCR must be at least 100%. The scenario envisaged by BCBS involves combining many of the factors experienced by banks in the last few years, such as reductions in retail deposits, reductions in unsecured wholesale funding capacity, etc. into one huge multi-faceted stress scenario.

Certain high-quality liquid assets would be included on the asset side on an unlimited, undiscounted basis, whereas other lesser-quality/less liquid assets would be discounted and their eligibility limited to 40% of the overall stock.

The Net Stable Funding Ratio (“NSFR”) is designed to promote resilience over a longer period of one year by encouraging banks to fund themselves with a minimum amount of equity and debt financing which is expected to be a reliable source of funds over a one-year period under conditions of extended stress. NSFR builds on the traditional “net liquid asset” and “cash capital” methodologies used by internationally-active banks.

The ratio will provide that a bank’s Available Stable Funding (“ASF”) must be at least equal to its Required Stable Funding (“RSF”).

ASF is defined as the total sum of a bank’s (a) capital; (b) preferred stock with a maturity of one year or more; (c) liabilities with effective maturities of one year or more; and (d) that portion of non-maturity deposits, term deposits and/or wholesale funding with maturities of less than one year which is expected to stay with the bank for an extended period in a stress event. A factor will be applied to discount each funding item’s face value for the purpose of the NSFR, with less stable funding sources receiving a higher discount factor.

RSF is defined as the amount of stable funding required by supervisors and is to be measured using supervisory assumptions on the liquidity risk profiles of an institution’s assets, OBS exposures and other selected activities. The RSF amount is calculated by taking the value of each asset held by the bank and applying a factor of between

7 Attorney Advertisement

0% and 100% to that value, depending on the assessment of how readily that asset could be realised by the bank – with cash receiving a factor of 0%.

2. Application Issues

Reporting: LCR should be reported at least monthly, or more frequently in stressed situations, at the discretion of the supervisor. NSFR should be reported at least quarterly.

Scope: BCBS acknowledges that there may be national differences in the liquidity treatment of certain items that are subject to national discretion. A cross-border banking group should apply the liquidity parameters adopted in the home jurisdiction to all legal entities being consolidated, except as to the treatment of retail/small business deposits which should, in most circumstances, follow the parameters adopted in host jurisdictions where the entities operate. The consolidated LCR should reflect the liquidity transfer restrictions (e.g., non-convertibility of local currency, foreign exchange controls) in relevant jurisdictions which inhibit the transfer of liquid assets and fund flows within the group.

Observation periods and transitional arrangements: The revised LCR will be introduced on 1 January 2015, and the revised NSFR will move to a minimum standard by 1 January 2018.

Observations and Next Steps

The regulatory capital provisions under Basel III have been long-anticipated. Concerns had been raised during consultations that the stringent new rules would make banks less profitable and hinder their lending activities, which are needed to support economic recovery. The amendments to the proposals in July 2010 and the lengthy transition period for the new provisions were partly designed to address those concerns. However, one of the findings of the QIS, which was based on the 2009 financial data provided by participating banks, was that the Group 1 banks which participated in the QIS would have to make up a Common Equity Tier 1 shortfall of €165bn to meet their new minimum requirements (assuming Basel III had been in place at the end of 2009) or €577bn to meet their new target requirements (so as not to be subject to any restrictions on distributions). The QIS notes that the same banks had after-tax profits for 2009 of €209bn.

The same banks would have achieved an average leverage ratio of 2.8% (compared to the proposed 3%), an average LCR of 83% (compared to the required 100%) and an average NSFR of 93% (compared to the required 100%). However, these findings arguably have limited significance given that the full details of the liquidity framework have yet to be calibrated and finalised by BCBS during the observation period, which will last until 2016.

As discussed above, BCBS is also continuing further work in relation to certain other issues, including the capitalisation of exposures to CCPs. In addition, BCBS announced that it continues to collaborate with the Financial Stability Board in relation to the additional loss absorption capacity requirements expected to be imposed on systemically-important banks and in relation to developing more detailed eligibility criteria for contingent capital, to address issues of loss absorbency at the point of a bank’s non-viability.8

8 See BCBS press release: Basel III rules text and results of the quantitative impact study issued by the Basel Committee (16 December 2010), http://www.bis.org/press/p101216.htm.

8 Attorney Advertisement

bout Morrison & Foerster

Contacts

Peter Green +44 20 7920 4013 [email protected] Helen Kim +44 20 7920 4147 [email protected]

Jeremy Jennings-Mares +44 20 7920 4072 [email protected]

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2010 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

1 Attorney Advertisement

News Bulletin October 25, 2010

BCBS Principles for Enhancing Corporate Governance

Background

On 4 October 2010, the Basel Committee on Banking Supervision (“BCBS”) published a set of principles for enhancing corporate governance in banks (the “Principles”).1 The Principles are intended to provide targeted supervisory guidance. BCBS published initial guidance on corporate governance practices in 1999 and revised principles in 2006. BCBS launched a public consultation in March 2010,2 to address deficiencies which came to light since the financial crisis. The Principles should be considered in the context of the wider regulatory drive to strengthen corporate governance and restructure executive compensation practices for financial institutions.

Sound Corporate Governance Principles

BCBS’s guidance is designed both to reinforce basic governance principles and to identify good practices for implementing them.

Board Practices

Board’s overall responsibilities

Principle 1: The board has overall responsibility for the bank, including corporate governance and oversight of senior management. Responsibilities of the board include:

• Ultimate responsibility for the bank’s business, risk strategy, and financial soundness, as well as its corporate governance and compensation system. Board members should exercise their “duty of care” and “duty of loyalty” to the bank under applicable national laws and supervisory standards. The board should review related party transactions to assess risk and attach appropriate restrictions.

• Corporate values and code of conduct. The board should take the lead in setting professional standards and corporate values, including the avoidance of excessive risks, and communicate these throughout the bank.

• Oversight of senior management.

1 BCBS Principles for enhancing corporate governance (4 October 2010), http://www.bis.org/publ/bcbs176.pdf. 2 BCBS Consultative Document: Principles for enhancing corporate governance (16 March 2010), http://www.bis.org/publ/bcbs168.pdf?noframes=1 (comments deadline: 15 June 2010).

2 Attorney Advertisement

Board qualifications

Principle 2: Board members should be qualified for their positions, understand their role clearly, and exercise sound and objective judgment about the bank’s affairs. Members should be recruited from a sufficiently broad population and vetted for potential conflicts of interest to enable objective independent judgment. They should be provided with tailored ongoing education.

Board’s own practices and structure

Principle 3: The board should define appropriate governance practices for its own work and ensure that such practices are followed and continuously improved. The board should structure itself, in terms of size, meetings, and committees, to promote efficiency, in-depth reviews, and robust discussion of issues. The chairman of the board (“COB”) should provide effective leadership. Where the COB and chief executive officer (“CEO”) roles are vested in the same person, countervailing measures (e.g., appoint a lead board member or senior independent board member) should be implemented. An increasing number of banks require the COB to be a non-executive. Large or internationally active banks should have a risk committee to advise the board on overall risk strategy, including capital and liquidity. The risk committee should communicate with the risk management function and chief risk officer (“CRO”) (see Principle 6) and have access to external expert advice, particularly on strategic transactions. The board also should have a formal written conflicts of interest policy.

Group structures

Principle 4: In a group structure, the parent company’s board has overall responsibility for corporate governance across the group.

Senior Management

Principle 5: Senior management should ensure that the bank’s activities are consistent with the business strategy, risk profile, and policies approved by the board. Management should promote accountability and transparency and implement proper risk management systems and internal controls (e.g., internal audit, compliance) (see Principles 6-7).

Risk Management and Internal Controls

Principle 6: Banks should have effective internal controls and a risk management function (including a CRO) with authority, independence, and access to the board. Internal controls should place checks on employee discretion and confirm the bank’s compliance with policies and procedures as well as laws and regulations. Large or internationally active banks should have an independent senior executive responsible for the risk management function (e.g., CRO). The risk management function should be independent of the business units, and encompass all risks, on- and off-balance sheet and at firmwide, portfolio, and business-line levels. The CRO should be distinct from other executive functions and not have responsibility for business operations. He should have direct access to the board and its risk committee.

Personnel and resources

Risk management personnel should be properly qualified, in market and product knowledge and risk disciplines. They must be capable of challenging the business lines on all aspects of risks arising from the bank’s activities. Adequate resources (e.g., personnel, information technology (“IT”) system) should be allocated to risk management and internal controls.

Principle 7: Risks should be monitored on a firmwide and individual entity basis and the risk management and internal control systems should be kept current.

3 Attorney Advertisement

Risk methodologies and activities

Banks should conduct forward-looking stress tests under various adverse scenarios, as well as back-test actual performance against risk estimates. A subsidiary bank’s portfolios should be stress-tested also on the potential risks to the parent. Internal risk measurements should include a qualitative assessment of risks relative to return and the external risk landscape. External assessments (e.g., credit rating, purchased risk models) can also be useful. There should be an approval process for new products and the risk management function should be actively involved in the due diligence for mergers and acquisitions. The bank’s treasury and finance functions should promote firmwide risk management through robust internal pricing of risk as well as financial controls. Business units should be accountable for managing risks arising from their own activities.

Principle 8: Effective risk management requires robust communication both across the organisation and through reporting to the board and senior management.

Principle 9: The board and senior management should effectively utilise the work of internal audit functions, external auditors, and internal control functions. The board and senior management are responsible for the financial statements and reporting. They should encourage internal auditors to adhere to national and international professional standards (e.g., Institute of Internal Auditors standards) and promote their independence. Non-executive board members should meet regularly with external auditors and the heads of internal audit and compliance.

Compensation3

Banks should implement the Financial Stability Board (“FSB”) Principles for Sound Compensation Practices and its Implementation Standards (the “FSB Principles”)4 or applicable national provisions that are consistent with the FSB Principles.

Principle 10: The board should actively oversee the compensation system and ensure that it operates as intended. Board members who are involved in the design and operation of the compensation system (e.g., the compensation committee) should be independent, non-executive members knowledgeable about such arrangements and the incentives and risks involved. Compensation of control functions (e.g., CRO, risk management) should be based on the achievement of their objectives without compromising their independence.

Principle 11: An employee’s compensation should be aligned with prudent risk-taking. Banks should align compensation with prudent risk-taking and adjust variable compensation to reflect all the risks an employee takes over a multi-year horizon (e.g., through deferred compensation arrangements with “claw-back” provisions). The mix of cash, equity, and other forms of compensation should be consistent with risk alignment. “Golden parachutes” (i.e., large payouts to terminated executives not based on performance) should be avoided. See our alert discussing incentive compensation practices for financial institutions, Incentive Compensation for Financial Institutions: Balancing Business Drivers and New Regulatory Oversight, which discusses a number of structuring alternatives that are consistent with the principles set forth in the BCBS consultative document on compensation.

Complex or Opaque Corporate Structures

Principle 12: The board and senior management should know the bank’s operational structure and the risks that it poses (i.e., “know-your-structure”). The board should set policies for establishing new entities or structures based on established criteria (e.g., regulatory, tax, financial reporting, governance) and avoid setting up

3 On 14 October 2010, BCBS also published a consultative document on the Range of Methodologies for Risk and Performance Alignment of Remuneration, http://www.bis.org/publ/bcbs178.pdf. Comments may be submitted by 31 December 2010. 4 FSB Principles for sound compensation practices (April 2009), www.financialstabilityboard.org/publications/r_0904b.pdf, and Implementation standards (25 September 2009), http://www.financialstabilityboard.org/publications/r_090925c.pdf.

4 Attorney Advertisement

unnecessarily complicated structures. When they establish business or product lines that do not match the legal entity structure (“matrix structures”), banks should ensure that all risks are captured and assessed on an individual entity and group-wide basis.

Principle 13: Where a bank operates non-transparent structures or in jurisdictions not meeting international banking standards, its board and senior management should understand and mitigate their risks (i.e., “understand-your-structure”). Operating in jurisdictions that are not transparent or compliant with international banking standards (e.g., prudential supervision, tax, anti-money laundering) or through complex or opaque structures (e.g., special purpose vehicles or trusts) may pose risks or impede business oversight. Moreover, providing certain services or structures for customers (e.g., company formation agent or trustee services, complex structured finance) may expose banks to indirect risks. The board and senior management should seek to mitigate such risks.

Disclosure and Transparency

Principle 14: The governance of the bank should be adequately transparent to its shareholders, depositors, other relevant stakeholders, and market participants.

About Morrison & Foerster

Contacts

Peter Green +44 20 7920 4013 [email protected] Helen Kim +44 20 7920 4147 [email protected]

Jeremy Jennings-Mares +44 20 7920 4072 [email protected]

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2010 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

1 Attorney Advertisement

News Bulletin September 15, 2010

The New Global Minimum Capital Standards Under Basel III

On 12 September 2010, the Group of Central Bank Governors and Heads of Supervision, the oversight body of the Basel Committee on Banking Supervision (“BCBS”), issued a press release1 announcing a substantial strengthening of the capital requirements, and its full endorsement of the agreement it had reached on 26 July 20102 in relation to the proposed reforms to the Basel II framework.3 These elements are intended to form part of a package of reforms to be known as Basel III.

The press release contains a table summarising the new requirements on minimum regulatory capital and buffers, as well as a timetable for phasing in the new reforms.

The New Capital Requirements

Minimum common equity and Tier 1 capital requirements

The minimum requirement for common equity, the highest form of loss-absorbing capital, will be raised from the current 2% to 4.5% of total risk-weighted assets (“RWAs”). The overall Tier 1 capital requirement, comprising not only common equity but also other qualifying financial instruments, will increase from the current minimum of 4% to 6%.

There will be no change to the minimum total capital requirement, which will remain at the current 8% level.

Capital conservation buffer

In addition to the minimum capital requirements, banks will be required to hold a capital conservation buffer of 2.5%. This buffer may be used to absorb losses during periods of financial and economic stress, but if a bank’s buffer falls below 2.5%, the bank will find itself subject to constraints on the payment of dividends and discretionary bonuses, until the buffer is replenished. This buffer must be funded with common equity, after application of deductions. This effectively mandates a minimum core Tier 1 capital ratio of 7%.

1 BCBS press release: Group of Governors & Heads of Supervision announces higher global minimum capital standards (12 September 2010), http://www.bis.org/press/p100912.pdf. 2 BIS Press Release: Group of Governors & Heads of Supervision reach broad agreement on Basel Committee capital & liquidity reform package (26 July 2010), http://www.bis.org/press/p100726.htm and Annex (26 July 2010), http://www.bis.org/press/p100726/annex.pdf. 3 See Morrison & Foerster client alert: More, More, More: A Summary of the Basel Proposals (2 February 2010), http://www.mofo.com/files/Publication/2f280bc1-1b9a-4d98-929f-0a4554236d0f/Presentation/PublicationAttachment/7cf62184-8f7b-48c4-a4f8-1de08055cfe4/SummaryoftheBaselProposals02022010.pdf.

2 Attorney Advertisement

Countercyclical buffer

A requirement to maintain countercyclical buffer in the range of 0% to 2.5%, consisting of common equity or other fully loss-absorbing capital, will be phased in to protect the banking sector from periods of “excess aggregate credit growth,” by effectively extending the required amount of the capital conservation buffer to counter a system-wide buildup of risk resulting from such credit growth. This would be implemented based on national circumstances.4

Leverage ratio

As a backstop to these risk-based measures, a non-risk-based leverage ratio will also be introduced in 2018. It is currently proposed that a minimum Tier 1 leverage ratio of 3% be tested during a parallel run period and then subjected to an appropriate review and calibration process, before migrating to Pillar 1 treatment.

Systemically important banks

The BCBS intends that systemically important banks should have loss-absorbing capacity beyond these minimum standards, and work is being carried out on this issue by the Financial Stability Board (“FSB”) and the BCBS to develop an integrated approach which may include a combination of capital surcharges, contingent capital and bail-in debt. In addition, work is continuing to strengthen resolution regimes and to strengthen the loss-absorbency of non-common Tier 1 and Tier 2 capital instruments.5

Transitional Arrangements

The new rules will be phased in from 1 January 2013 to 1 January 2019. Member countries must transpose the new rules into their national laws prior to, and begin implementing them from, 1 January 2013. However, they may impose shorter transition periods, as appropriate.

Common equity and Tier 1 capital

The minimum common equity and Tier 1 capital requirements, in relation to RWAs, will be phased in between 1 January 2013 and 1 January 2015, as illustrated in Annex 1:

The BCBS had proposed in its December 2009 Consultative Document “Strengthening the resilience of the banking sector” and in its July 2010 paper that certain deductions and prudential filters should be applied in determining a bank’s common equity Tier 1 capital, including deductions relating to minority interests, goodwill, deferred tax assets, investments in certain financial entities and mortgage servicing rights.

These regulatory adjustments to common equity will be phased in from 1 January 2014, starting at 20% of the deduction that would otherwise be required and rising by another 20% on each anniversary, until being fully deducted from common equity as from 1 January 2018.6

4 See also Morrison & Foerster client alert: A Little Bit Less and a Bit Longer: Update on Basel Capital and Liquidity Reforms (6 August 2010), http://www.mofo.com//files//Uploads/Images/100806BaselCapital.pdf. 5 See BCBS Consultative Document: A proposal to ensure the loss absorbency of regulatory capital at the point of non-viability (19 August 2010), http://www.bis.org/publ/bcbs174.pdf?noframes=1 (comments deadline: 1 October 2010). See also Morrison & Foerster client alert: Super-Absorbent Bank Regulatory Capital (25 August 2010), http://www.mofo.com/files/Uploads/Images/100825SuperAbsorbent.pdf. 6 See Annex 2.

3 Attorney Advertisement

Capital conservation buffer

The capital conservation buffer will be phased in at an initial level of 0.625% of RWAs from 1 January 2016 and increasing each subsequent year by 0.625%, to reach its final level of 2.5% of RWAs from 1 January 2019.

The BCBS has stated that countries experiencing excessive credit growth should consider accelerating their build-up of the capital conservation buffer and the countercyclical buffer.

Qualification/Recognition of Capital Instruments

Existing public sector injections of capital will be grandfathered until 1 January 2018.

In the case of existing capital instruments that no longer qualify as non-common equity Tier 1 or Tier 2 capital, they will be gradually “de-recognised” by 10% per year (of their nominal amount outstanding as at 1 January 2013) over a 10-year period, starting from 1 January 2013. In addition, where those instruments contain incentives to redeem (such as interest rate step-ups), such instruments will be de-recognised at their effective maturity date.

Instruments that no longer qualify as common equity Tier 1 capital will be excluded from common equity Tier 1 capital as from 1 January 2013,7 provided that instruments containing the following features will be gradually de-recognised in the manner set out in the previous paragraph:

• they are issued by a non-joint stock company;

• they are treated as equity under the prevailing accounting standards; and

• they receive unlimited recognition as part of Tier 1 capital under current applicable national banking law.

Leverage ratio

As announced on 26 July 2010, the supervisory monitoring process will commence on 1 January 2011, followed by the parallel run period from 1 January 2013 to 1 January 2017. Disclosure of the leverage ratio and its components will start from 1 January 2015. Based on the results of the parallel run period, final adjustments will be made in the first half of 2017, with a view to the ratio being given Pillar 1 treatment under the Basel framework from 1 January 2018.8

Liquidity ratios

As also announced on 26 July 2010, BCBS intends to introduce (i) the liquidity coverage ratio (“LCR”) from 1 January 2015 and (ii) the revised net stable funding ratio (“NSFR”), as a minimum standard by 1 January 2018, in each case following an observation phase.9

Next Steps

The new capital standards will be presented at the G20 summit meeting in Seoul on 11 – 12 November 2010 for endorsement before taking effect.

7 See Annex 2. 8 See Annex 2. 9 See Annex 2.

4 Attorney Advertisement

Annex 1

Basel III Minimum Capital Requirements

12

11

9

10

8

7

6

5

4

3

2

1

0

2010 2011 2012 2013 201620152014 2017 2018 2019 2020 2021 2022

10.5%

8.625%

9.25%

9.875%

Capital Conservation Buffer

Other Capital

Other Tier 1 Capital

Tier 1 Common Equity

3.5%

4%

4.5%4.5%

5.5%

6%

% of Risk- Weighted Assets

5 Attorney Advertisement

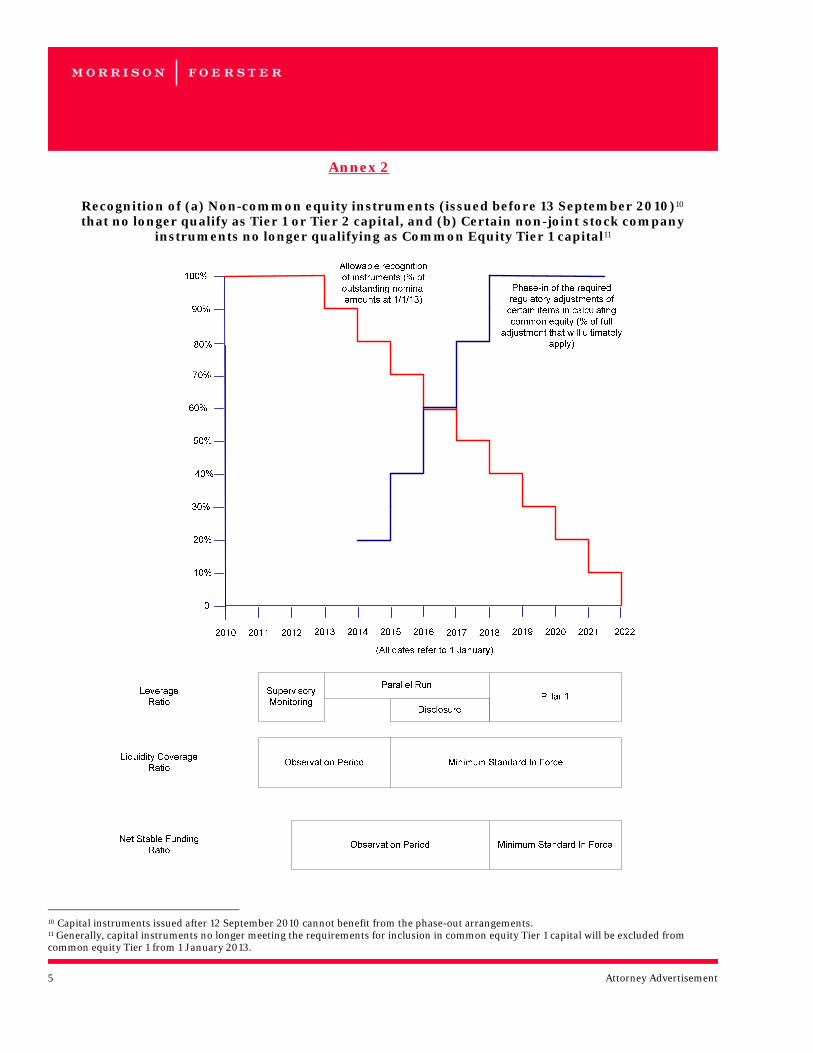

Annex 2

Recognition of (a) Non-common equity instruments (issued before 13 September 2010)10 that no longer qualify as Tier 1 or Tier 2 capital, and (b) Certain non-joint stock company

instruments no longer qualifying as Common Equity Tier 1 capital11

10 Capital instruments issued after 12 September 2010 cannot benefit from the phase-out arrangements. 11 Generally, capital instruments no longer meeting the requirements for inclusion in common equity Tier 1 capital will be excluded from common equity Tier 1 from 1 January 2013.

6 Attorney Advertisement

About Morrison & Foerster

UK Authors

Peter Green +44 20 7920 4013 [email protected] Helen Kim +44 20 7920 4147 [email protected]

U.S. Contacts

Jeremy Jennings-Mares +44 20 7920 4072 [email protected]

Oliver Ireland (202) 778-1614 [email protected]

Anna Pinedo (212) 468-8179 [email protected]

About Morrison & Foerster We are Morrison & Foerster—a global firm of exceptional credentials. Our clients include some of the largest financial institutions, investment banks, Fortune 100, technology and life science companies. We’ve been included on The American Lawyer’s A-List for seven straight years, and Fortune named us one of the “100 Best Companies to Work For.” Our lawyers are committed to achieving innovative and business-minded results for our clients, while preserving the differences that make us stronger. This is MoFo. Visit us at www.mofo.com. © 2010 Morrison & Foerster LLP. All rights reserved. Because of the generality of this update, the information provided herein may not be applicable in all situations and should not be acted upon without specific legal advice based on particular situations.

1 Attorney Advertisement

News Bulletin August 25, 2010

Super-Absorbent Bank Regulatory Capital

The Basel Committee on Banking Supervision (“BCBS”) has refined its views on the features capital instruments must possess in order to be acceptable as regulatory capital. On 19 August 2010, BCBS published a consultative document1 containing a proposal to require, as a pre-condition of regulatory capital treatment, that the contractual terms of capital instruments issued by banks provide for write-off or conversion to common equity, at the discretion of the relevant regulatory authority, in the event that the bank issuer is unable to support itself in the private market (the “Gone-Concern Proposal”).

Background

BCBS had previously published two consultative documents (referred to as the Basel III framework)2 relating, inter alia, to the definition of capital, the treatment of counterparty credit risk, the introduction of a leverage ratio and the imposition of global liquidity standards.

In the first of these consultative documents entitled “Strengthening the resilience of the banking sector,” BCBS highlighted its ongoing review of the role of contingent capital instruments involving mandatory write-off or conversion features, both:

• as a criterion for Tier 1 and/or Tier 2 capital to ensure loss absorbency (which has led to the Gone-Concern Proposal); and

• more generally in relation to minimum regulatory capital and buffers.3

At the time, BCBS stated that it would discuss specific proposals in its July 2010 meeting.

BCBS has now stated its view that all bank regulatory capital instruments must be capable of absorbing loss (at least) in “gone-concern situations.” By gone-concern situations, BCBS is referring not only to insolvency or liquidation situations (in which circumstances it notes that all bank regulatory capital instruments qualify as 1 BCBS Consultative Document: A proposal to ensure the loss absorbency of regulatory capital at the point of non-viability (19 August 2010), http://www.bis.org/publ/bcbs174.pdf?noframes=1 (comments deadline: 1 October 2010).

2 BCBS Consultative Documents (17 December 2009): (1) Strengthening the resilience of the banking sector (17 December 2009), http://www.bis.org/publ/bcbs164.pdf?noframes=1; and (2) International framework for liquidity risk measurement, standards and monitoring, http://www.bis.org/publ/bcbs165.pdf?noframes=1.

3 See Morrison & Foerster client alert: More, More, More: A Summary of the Basel Proposals (2 February 2010), http://www.mofo.com/files/Publication/2f280bc1-1b9a-4d98-929f-0a4554236d0f/Presentation/PublicationAttachment/7cf62184-8f7b-48c4-a4f8-1de08055cfe4/SummaryoftheBaselProposals02022010.pdf. See also Morrison & Foerster client alert: A Little Bit Less and a Bit Longer: Update on Basel Capital and Liquidity Reforms (6 August 2010), http://www.mofo.com//files//Uploads/Images/100806BaselCapital.pdf.

2 Attorney Advertisement

“loss-absorbent”) but also the situations where the relevant bank fails without public sector support. In this regard, BCBS believes that any government injection of capital to rescue a failing bank should not be applied to protect the holders of regulatory capital instruments.

BCBS outlines the proposed mechanism for enhancing the entry criteria of regulatory capital, primarily by requiring the inclusion, in all regulatory capital instruments, of write-off or conversion provisions which can be triggered by regulators at the “point of non-viability.” The point of non-viability refers to the contingency that a bank becomes “unable to support itself in the private market” such that it needs rescuing by the public sector, rather than in the narrow sense of insolvency or liquidation.

BCBS had considered three different options which could help ensure that, as a pre-condition of being treated as regulatory capital, an instrument (in particular a Tier 2 instrument) is capable of bearing loss at the point of non-viability.

Option 1: Developing national and international bank resolution frameworks that enable losses to be allocated to all capital instruments issued by internationally active banks that have reached the point of non-viability.

Option 2: Identifying systemically important banks and prohibiting them from including Tier 2 instruments in their regulatory capital.

Option 3: Mandating that all regulatory capital instruments include a mechanism in their terms and conditions that ensures they will take a loss at the point of non-viability.