basel accords daren warner chief financial officer

TRANSCRIPT

Basel Accords

Daren Warner Chief Financial Officer

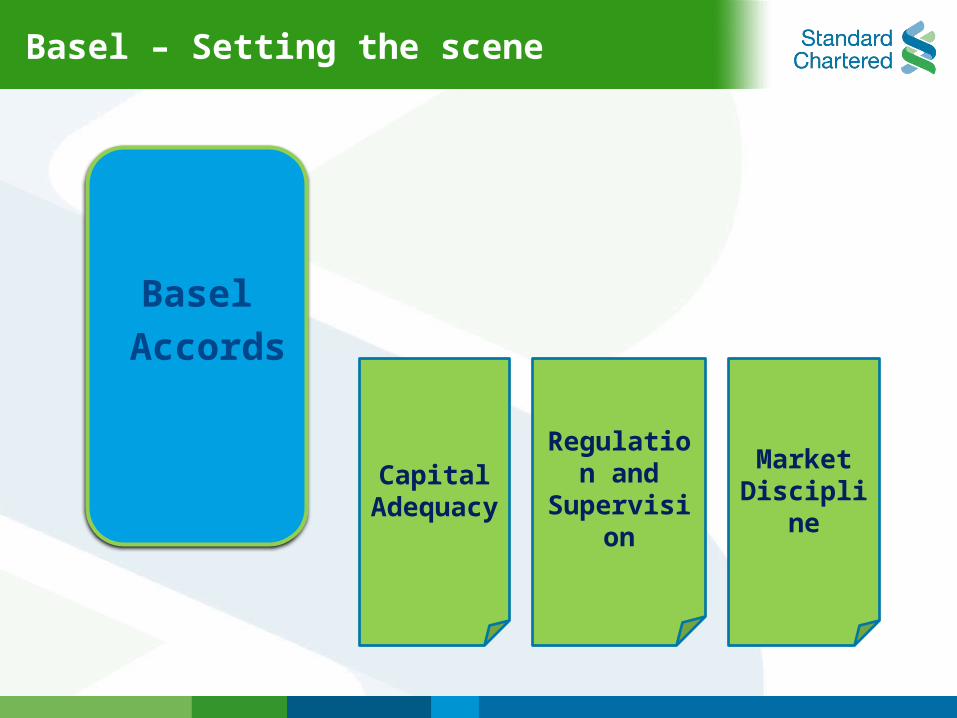

Basel

Accords

Capital Adequacy

Market Discipline

Regulation and

Supervision

Basel – Setting the scene

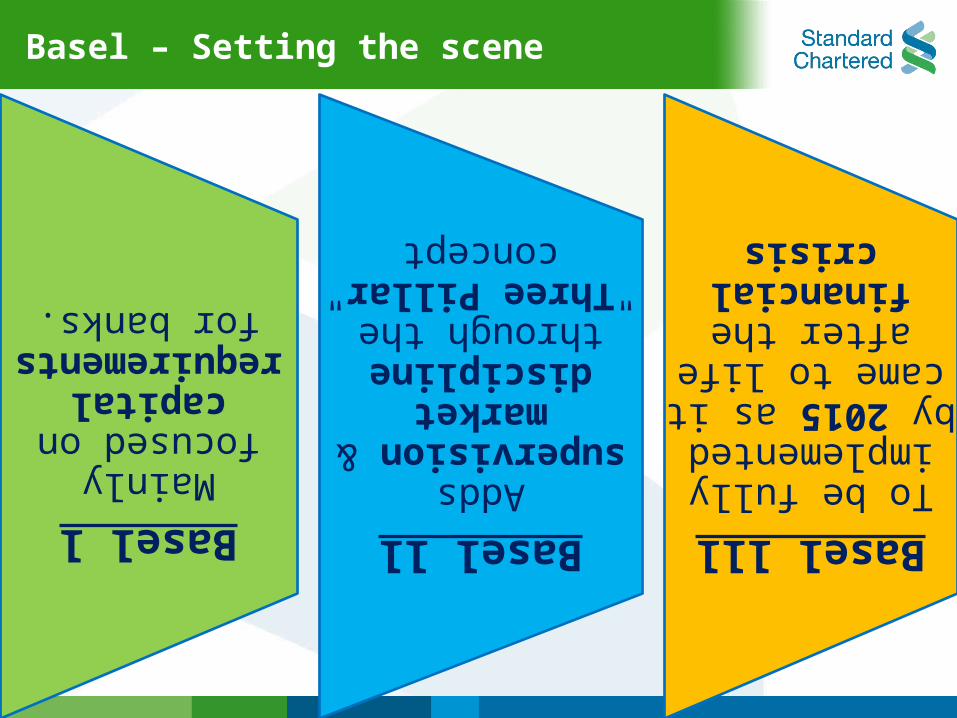

Basel lMainly focused on capital requirements for banks.

Basel llAdds supervision & market

discipline through the "Three Pillar" concept

Basel lllTo be fully implemented by 2015

as it came to life after the financial crisis

Basel – Setting the scene

Basel History

Basel History

The story behind Basel- The liquidation of Herstatt Bank

The release of Deutsche Marks to Herstatt in Frankfurt in exchange for US Dollars to be delivered to New York

Because of the time-zone differences, counterparty bank did not receive their payment as the Herstatt Bank ceased its operation

Basel l

Basel l

Establishment of Basel l

1988 Basel Accord- the Basel Committee published a set of minimal capital requirements for banks

Mainly focused on capital requirements for banks

Focused primarily on Credit Risk, market risk was an afterthought

By 1992, Basel l was enforced by law in the G-10 [Belgium, Canada, France, Germany, Italy, Japan, Luxembourg, Netherlands, Spain, Sweden, Switzerland, UK, and the USA]

Basel l

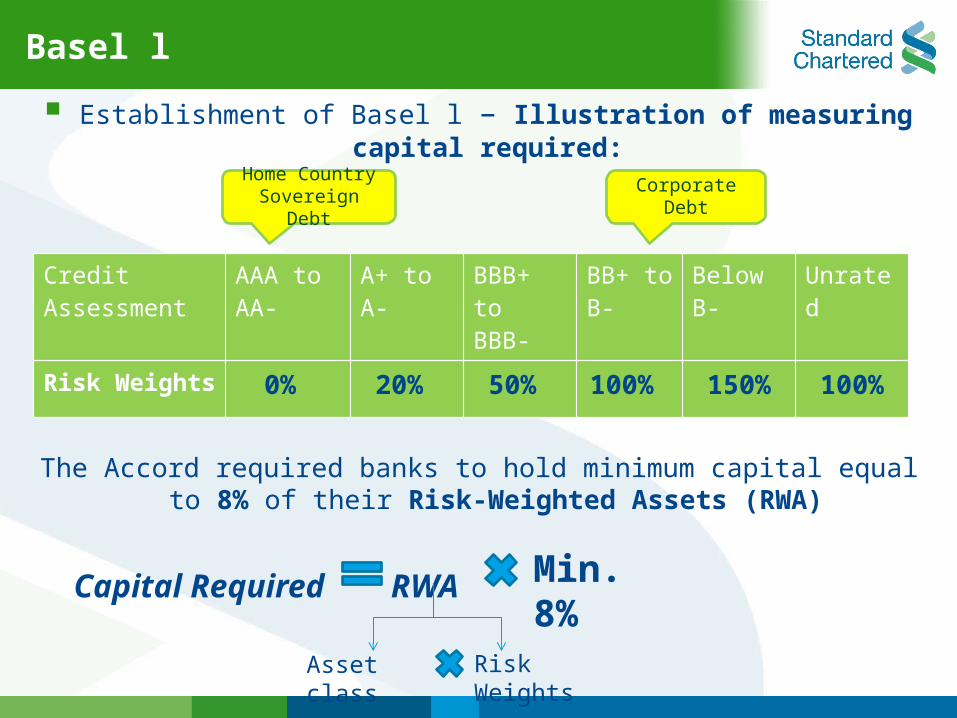

Establishment of Basel l – Illustration of measuring capital required:

The Accord required banks to hold minimum capital equal to 8% of their Risk-Weighted Assets (RWA)

Capital Required RWA

Credit Assessment

AAA to AA-

A+ to A- BBB+ to BBB-

BB+ to B-

Below B-

Unrated

Risk Weights 0% 20% 50% 100% 150% 100%

Min. 8%

Asset class Risk Weights

Home Country Sovereign Debt

Corporate Debt

Basel l

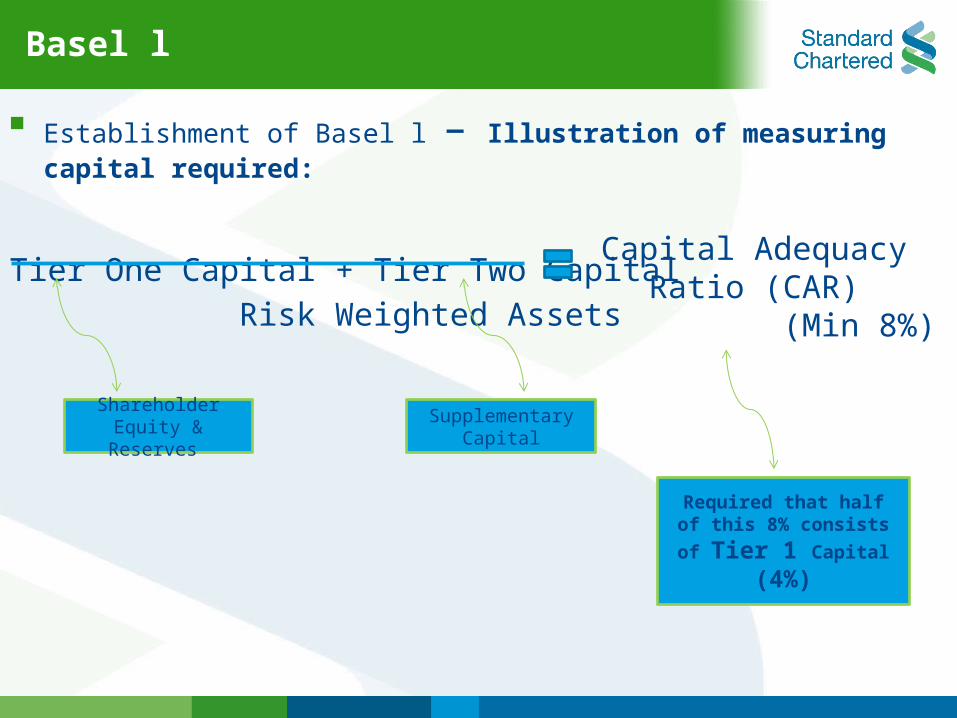

Establishment of Basel l – Illustration of measuring capital required:

Tier One Capital + Tier Two Capital

Risk Weighted Assets Capital Adequacy Ratio

(CAR) (Min 8%)

Shareholder Equity & Reserves

Supplementary Capital

Required that half of this

8% consists of Tier 1 Capital (4%)

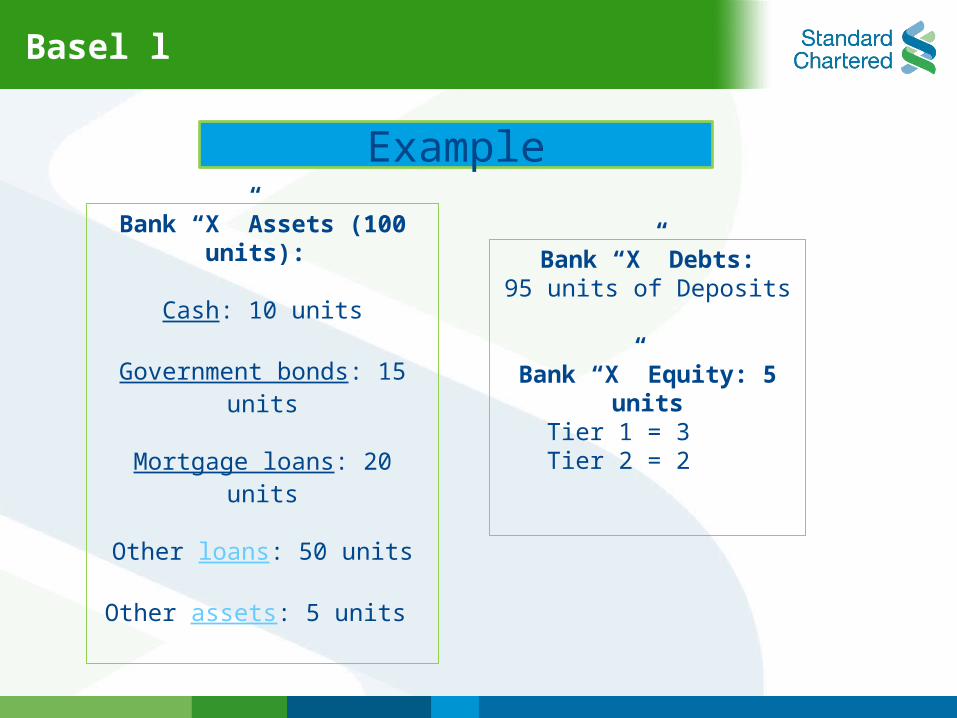

Example

Bank “X ”Assets (100 units):

Cash: 10 units

Government bonds: 15 units

Mortgage loans: 20 units

Other loans: 50 units

Other assets: 5 units

Bank “X” Debts:95 units of Deposits

Bank “X” Equity: 5 unitsTier 1 = 3Tier 2 = 2

Basel l

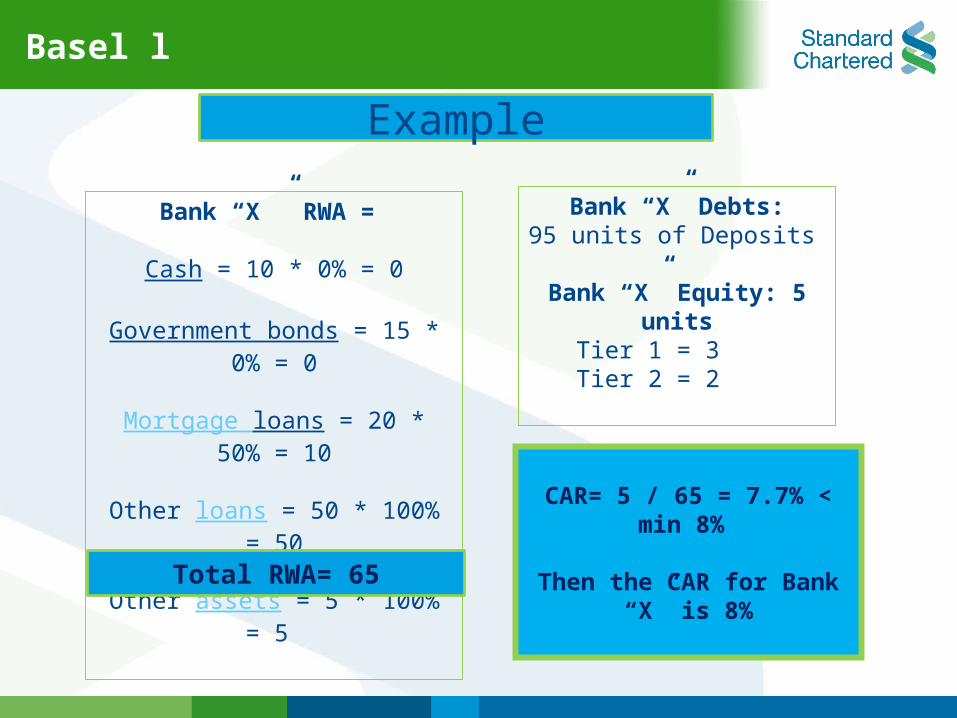

Example

Bank “X ” RWA =

Cash = 10 * 0% = 0

Government bonds = 15 * 0% = 0

Mortgage loans = 20 * 50% = 10

Other loans = 50 * 100% = 50

Other assets = 5 * 100% = 5

Bank “X” Debts:95 units of Deposits

Bank “X” Equity: 5 unitsTier 1 = 3Tier 2 = 2

Total RWA= 65

CAR= 5 / 65 = 7.7% < min 8%

Then the CAR for Bank “X” is 8%

Basel l

Basel l

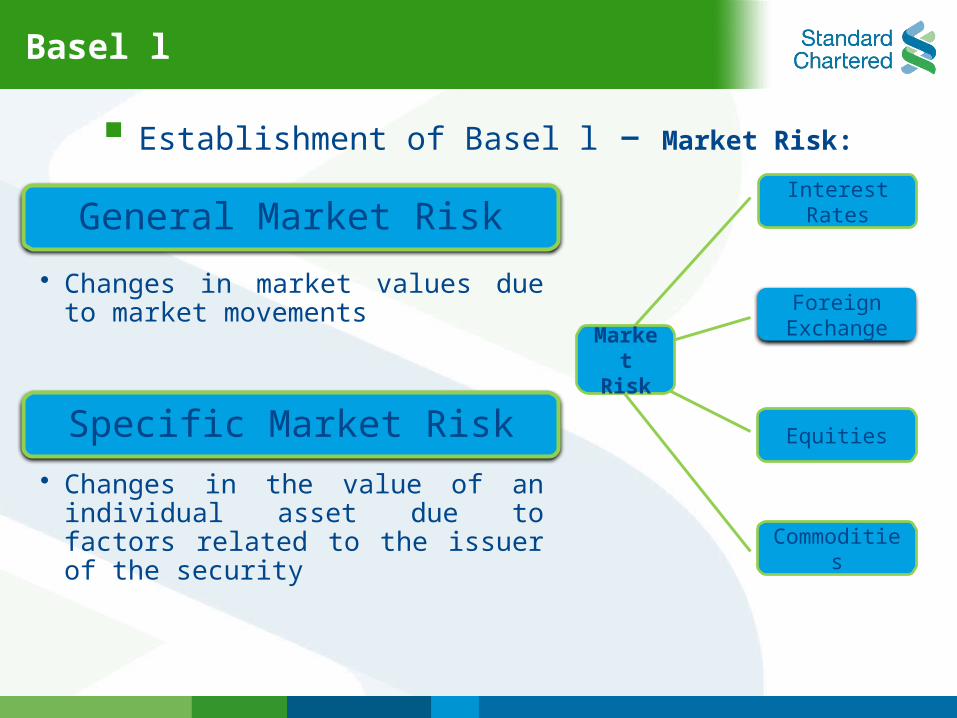

Establishment of Basel l – Market Risk:

General Market Risk

• Changes in market values due to market movements

Specific Market Risk

• Changes in the value of an individual asset due to factors related to the issuer of the security

Foreign Exchange

Interest Rates

Commodities

Equities

Market Risk

Basel l

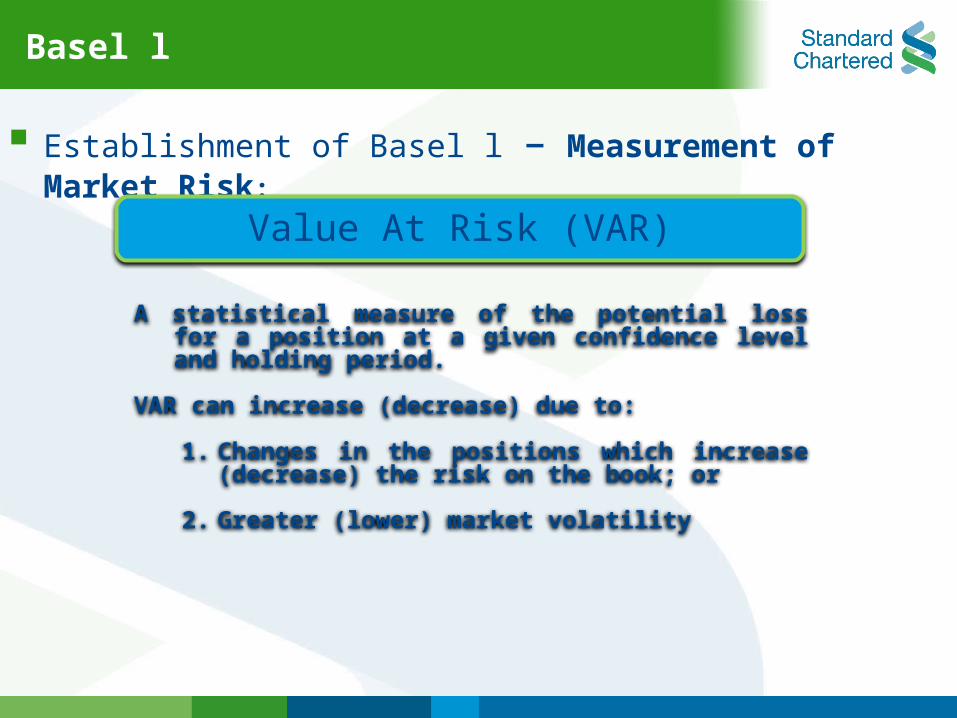

Establishment of Basel l – Measurement of Market Risk:

Value At Risk (VAR)

A statistical measure of the potential loss for a position at a given confidence level and holding period.

VAR can increase (decrease) due to:

1. Changes in the positions which increase (decrease) the risk on the book; or

2. Greater (lower) market volatility

Basel l

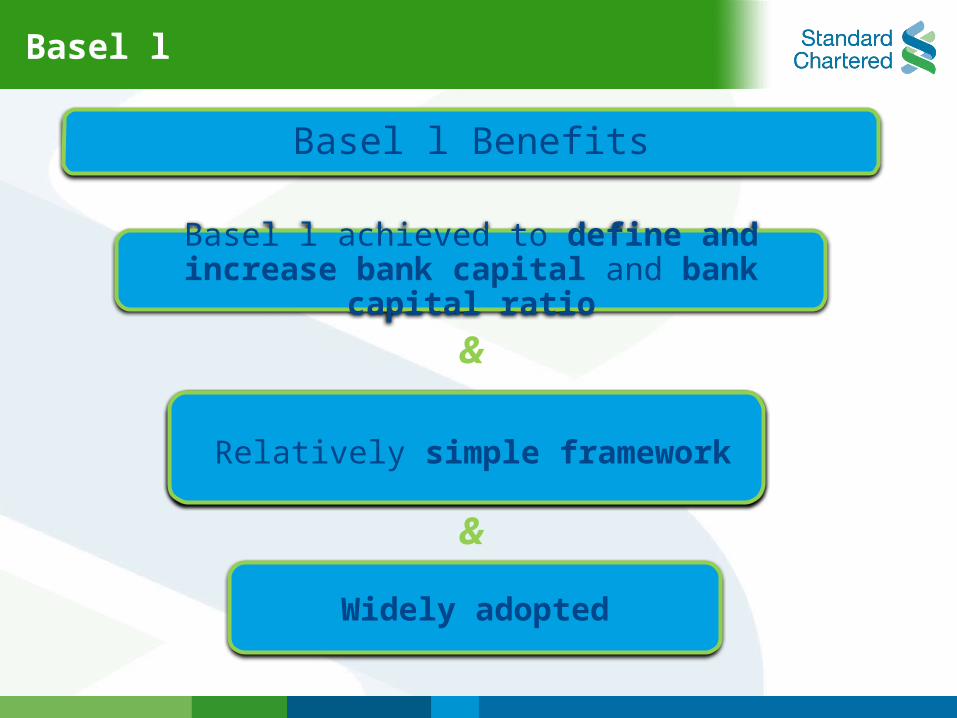

Basel l Benefits

Basel l achieved to define and increase bank capital and bank capital ratio

Relatively simple framework

Widely adopted

&

&

Relatively simple framework

Basel l

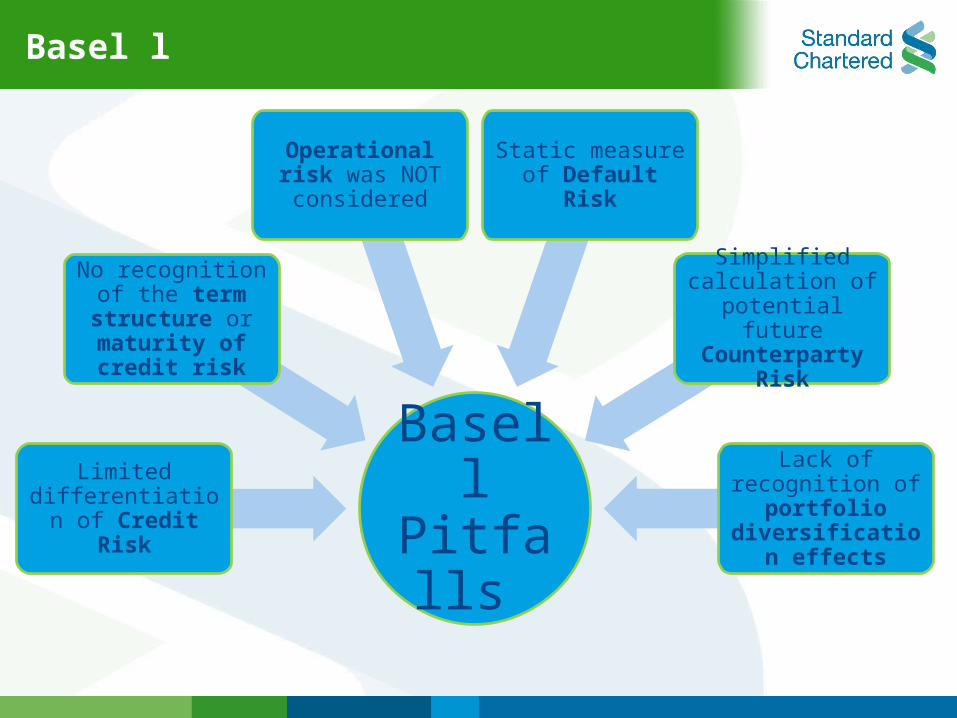

Basel l Pitfalls

Limited differentiation of

Credit Risk

No recognition of the term structure

or maturity of credit risk

Operational risk was NOT

considered

Static measure of Default Risk

Simplified calculation of

potential future Counterparty Risk

Lack of recognition of portfolio

diversification effects

Basel l

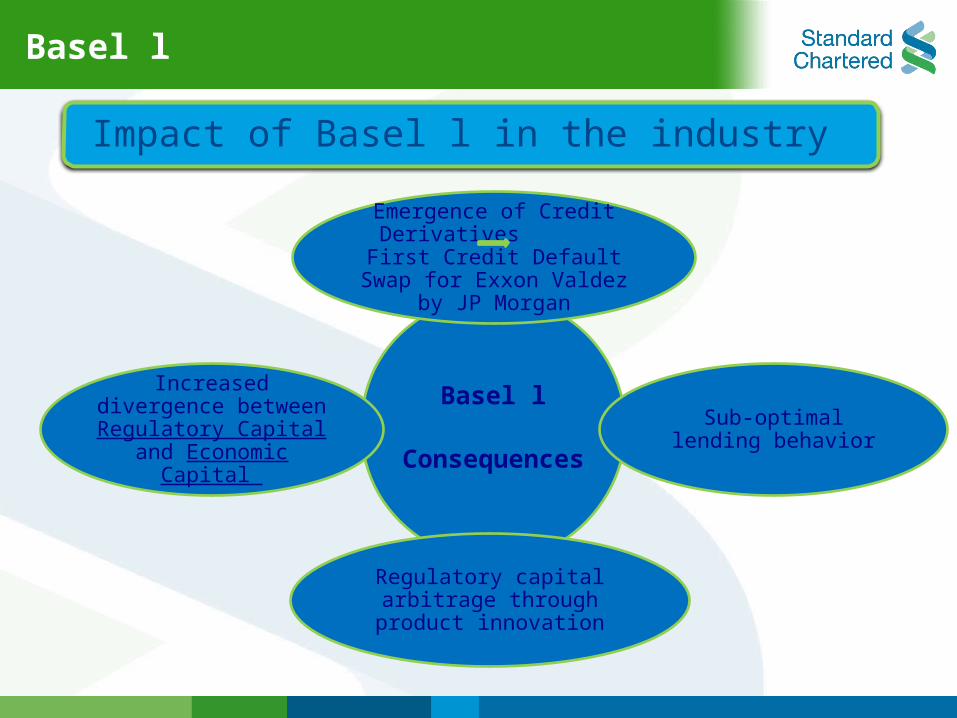

Impact of Basel l in the industry

Basel l

Consequences

Emergence of Credit Derivatives First Credit Default Swap for Exxon Valdez by

JP Morgan

Increased divergence between Regulatory Capital and Economic

Capital Sub-optimal lending behavior

Regulatory capital arbitrage through product innovation

Basel ll

Basel ll

Establishment of Basel ll

2004,The committee published their Basel ll

Purpose: Creating international standards about how much capital banks need to guard against the financial and operational risks

November 2007, Implementation of Basel ll Accord

Risks bank exposed to Amount of Capital required

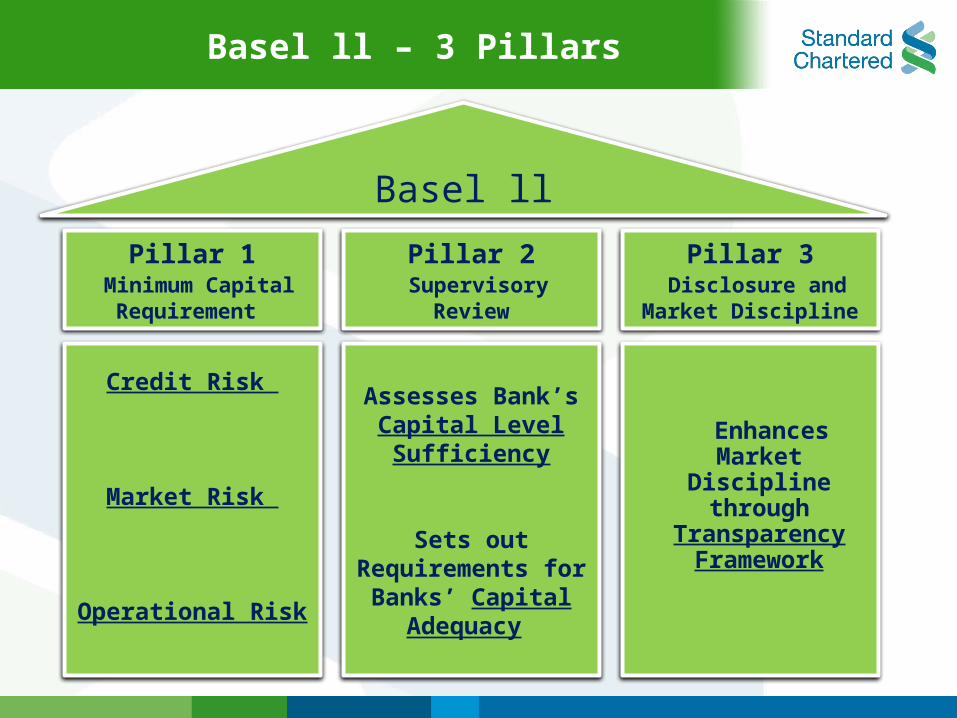

Basel ll – 3 Pillars

Basel ll

Pillar 1 Minimum Capital

Requirement

Pillar 2 Supervisory Review

Pillar 3 Disclosure and Market

Discipline

Assesses Bank’s Capital Level Sufficiency

Sets out Requirements for

Banks’ Capital Adequacy

Enhances Market Discipline through

Transparency Framework

Credit Risk

Market Risk

Operational Risk

Basel ll

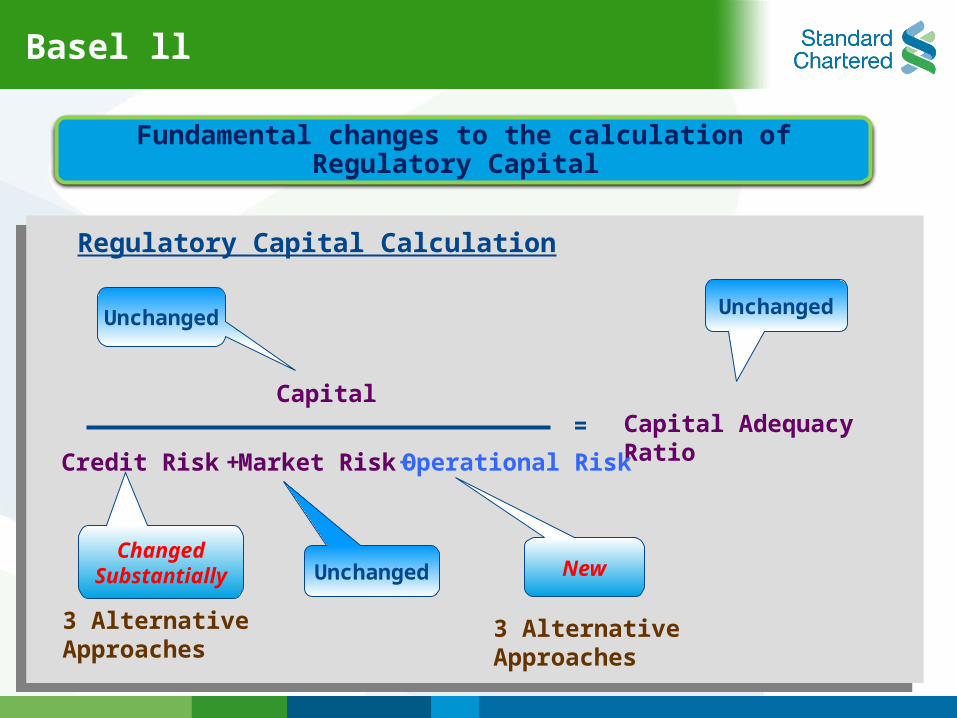

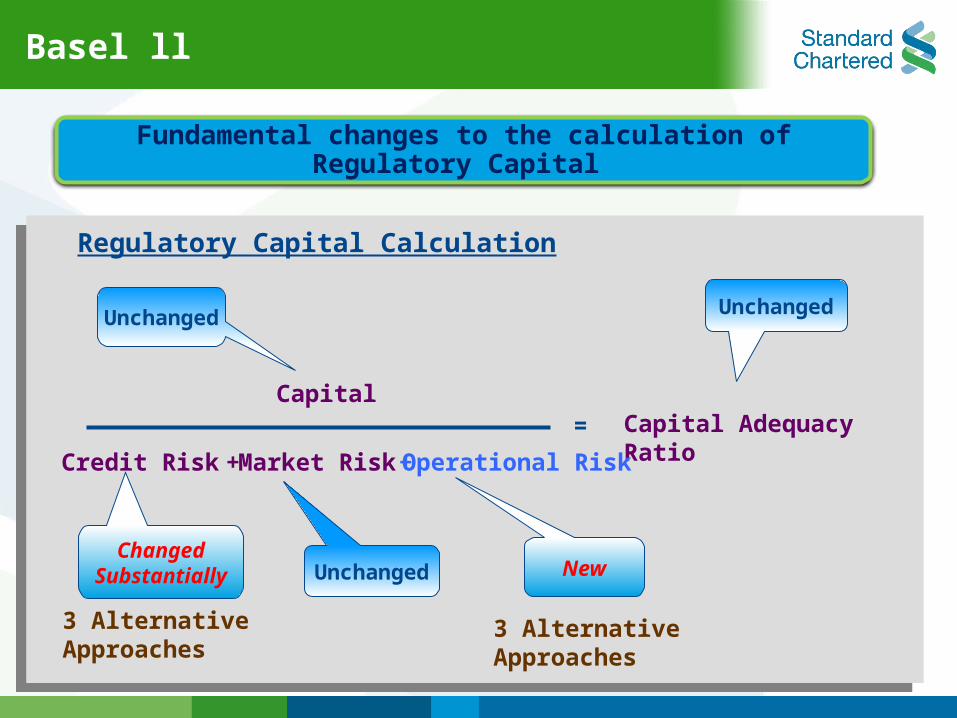

Fundamental changes to the calculation of Regulatory Capital

Regulatory Capital Calculation

Unchanged

Unchanged

Unchanged

=

Credit Risk

Capital Capital Adequacy Ratio

ChangedSubstantially

3 Alternative Approaches

New

3 AlternativeApproaches

Market Risk Operational Risk + +

Basel ll

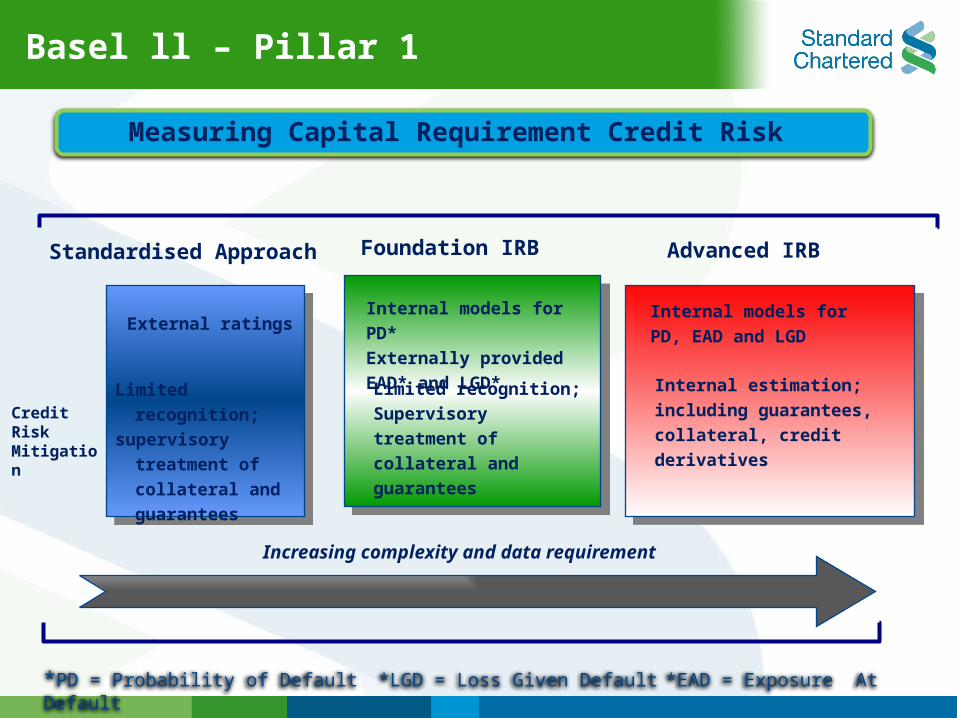

Pillar 1

Basel ll – Pillar 1

Increasing complexity and data requirement

Standardised Approach

Limited recognition;

supervisory treatment

of collateral and

guarantees

Credit Risk Mitigation

External ratings

Foundation IRB

Internal models for PD*

Externally provided EAD*

and LGD*

Limited recognition;

Supervisory treatment of

collateral and guarantees

Advanced IRB

Internal models for PD,

EAD and LGD

Internal estimation; including

guarantees, collateral, credit

derivatives

Measuring Capital Requirement Credit Risk

*PD = Probability of Default *LGD = Loss Given Default *EAD = Exposure At Default

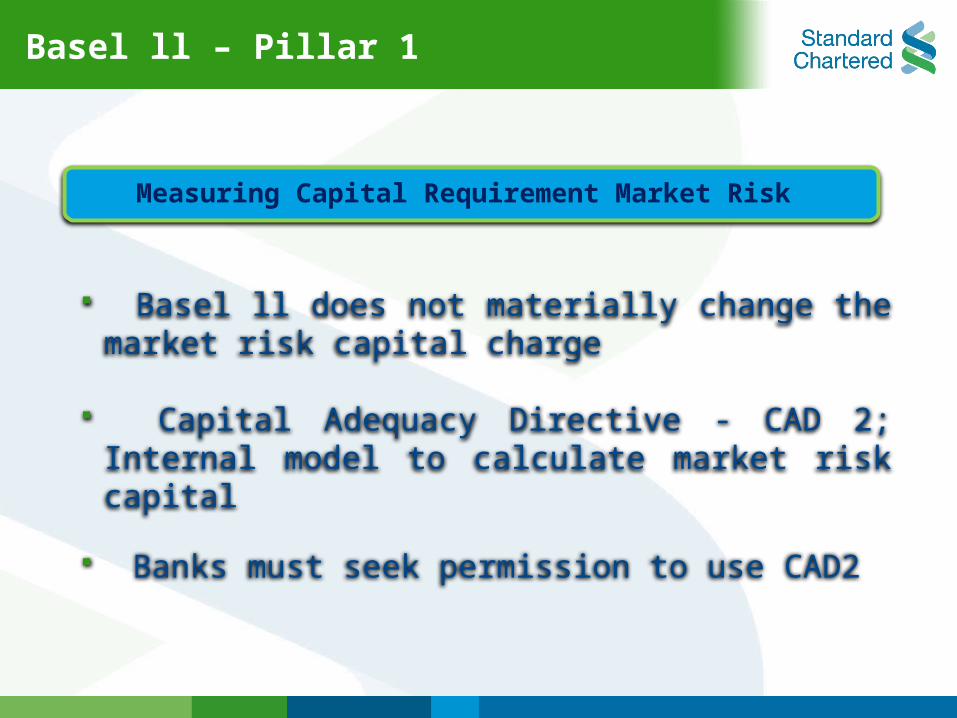

Measuring Capital Requirement Market Risk

Basel ll – Pillar 1

Basel ll does not materially change the market risk capital charge

Capital Adequacy Directive - CAD 2; Internal model to calculate market risk capital

Banks must seek permission to use CAD2

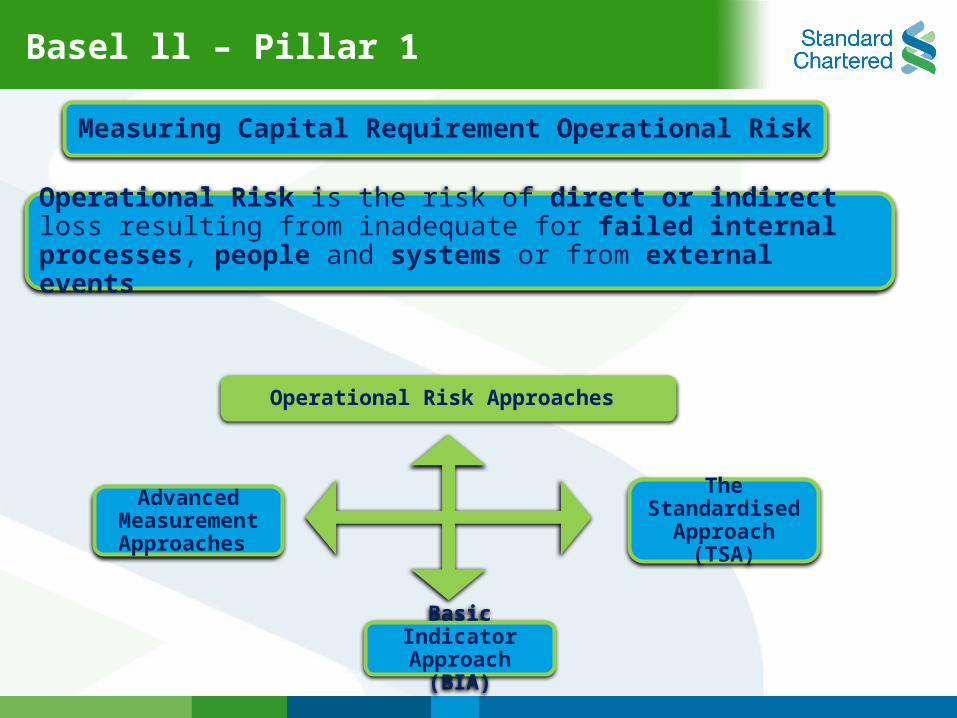

Measuring Capital Requirement Operational Risk

Basel ll – Pillar 1

Operational Risk is the risk of direct or indirect loss resulting from inadequate for failed internal processes, people and systems or from external events

Basic Indicator Approach (BIA)

Advanced Measurement Approaches

The Standardised

Approach (TSA)

Operational Risk Approaches

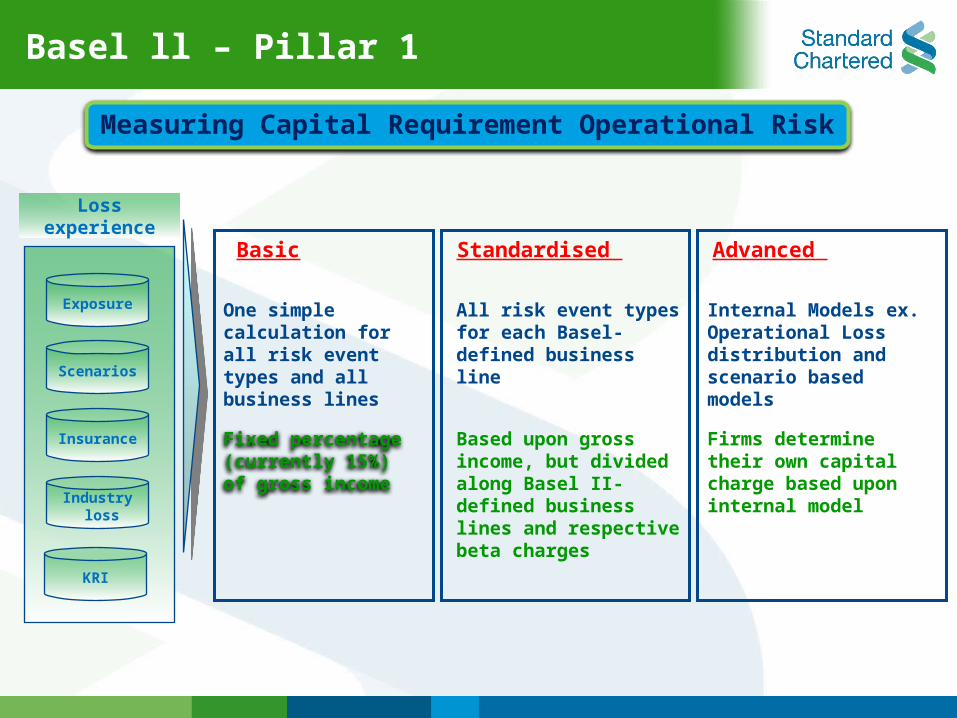

Fixed percentage (currently 15%) of gross income

Exposure

Scenarios

Insurance

KRI

Industry loss

Loss experience

Basic Advanced

Based upon gross income, but divided along Basel II-defined business lines and respective beta charges

Standardised

Firms determine their own capital charge based upon internal model

One simple calculation for all risk event types and all business lines

All risk event types for each Basel-defined business line

Internal Models ex. Operational Loss distribution and scenario based models

Measuring Capital Requirement Operational Risk

Basel ll – Pillar 1

Basel ll

Fundamental changes to the calculation of Regulatory Capital

Regulatory Capital Calculation

Unchanged

Unchanged

Unchanged

=

Credit Risk

Capital Capital Adequacy Ratio

ChangedSubstantially

3 Alternative Approaches

New

3 AlternativeApproaches

Market Risk Operational Risk + +

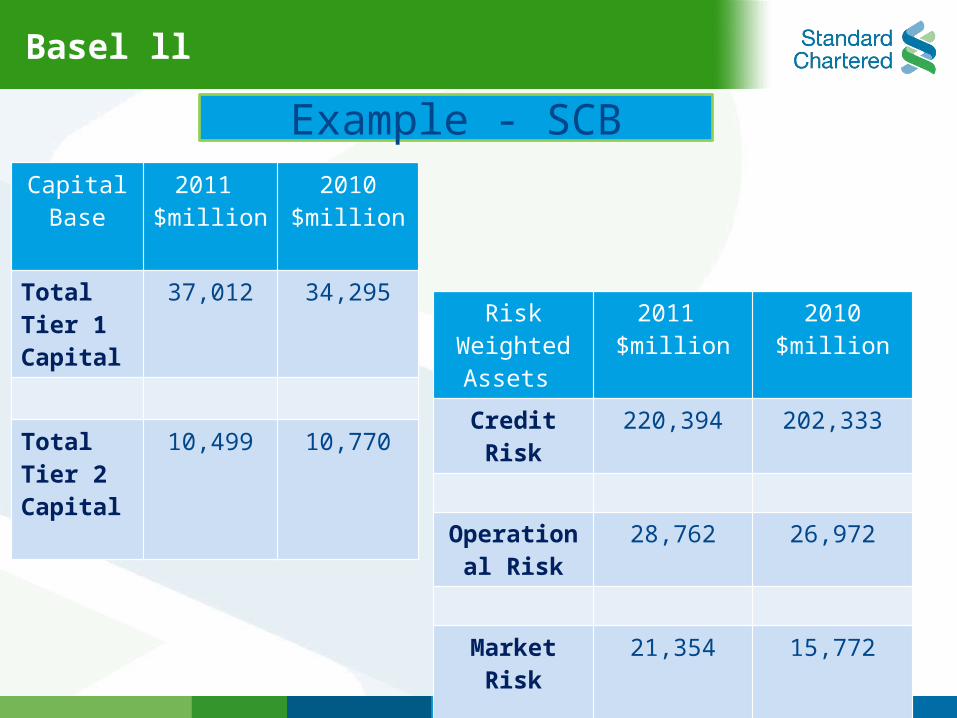

Example - SCBCapital Base

2011 $million

2010$million

Total Tier 1 Capital

37,012 34,295

Total Tier 2 Capital

10,499 10,770

Risk Weighted Assets

2011 $million

2010$million

Credit Risk 220,394 202,333

Operational Risk

28,762 26,972

Market Risk 21,354 15,772

Total RWA 270,510 245,077

Basel ll

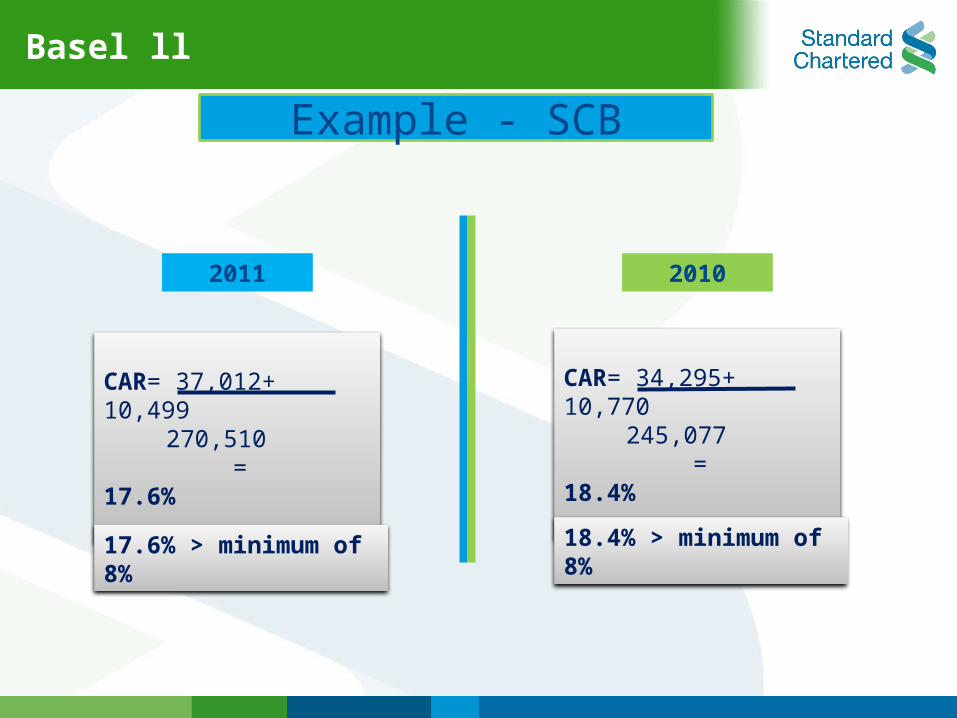

Example - SCB

CAR= 37,012+ 10,499 270,510

= 17.6%

CAR= 34,295+ 10,770 245,077

= 18.4%

2011 2010

17.6% > minimum of 8% 18.4% > minimum of 8%

Basel ll

Basel ll

Pillar 2

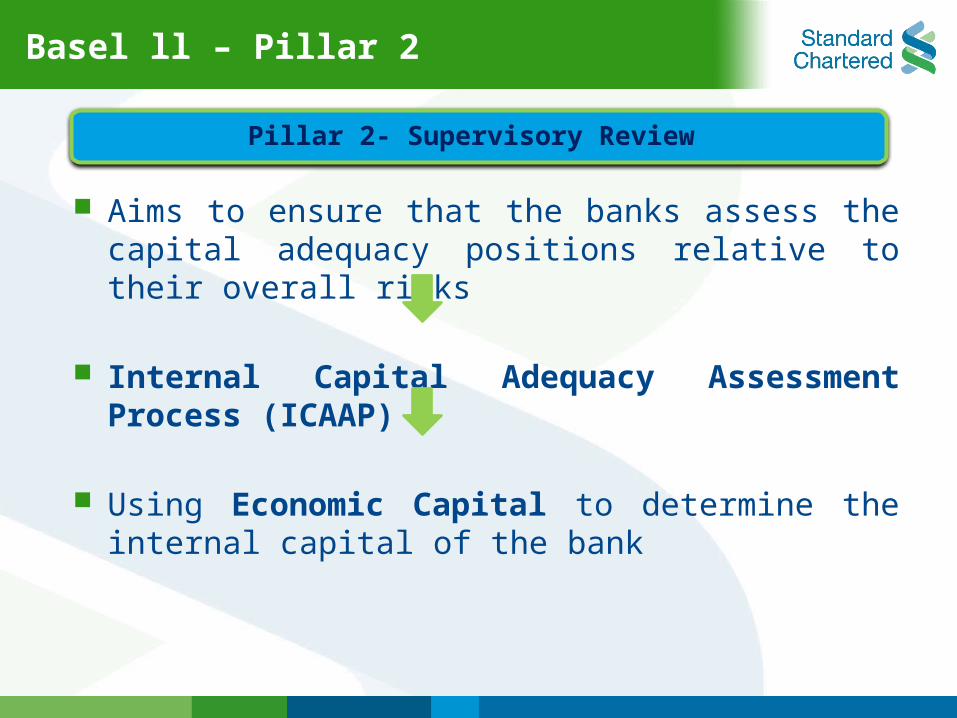

Basel ll – Pillar 2

Aims to ensure that the banks assess the capital adequacy positions relative to their overall risks

Internal Capital Adequacy Assessment Process (ICAAP)

Using Economic Capital to determine the internal capital of the bank

Pillar 2- Supervisory Review

Basel ll – Pillar 2

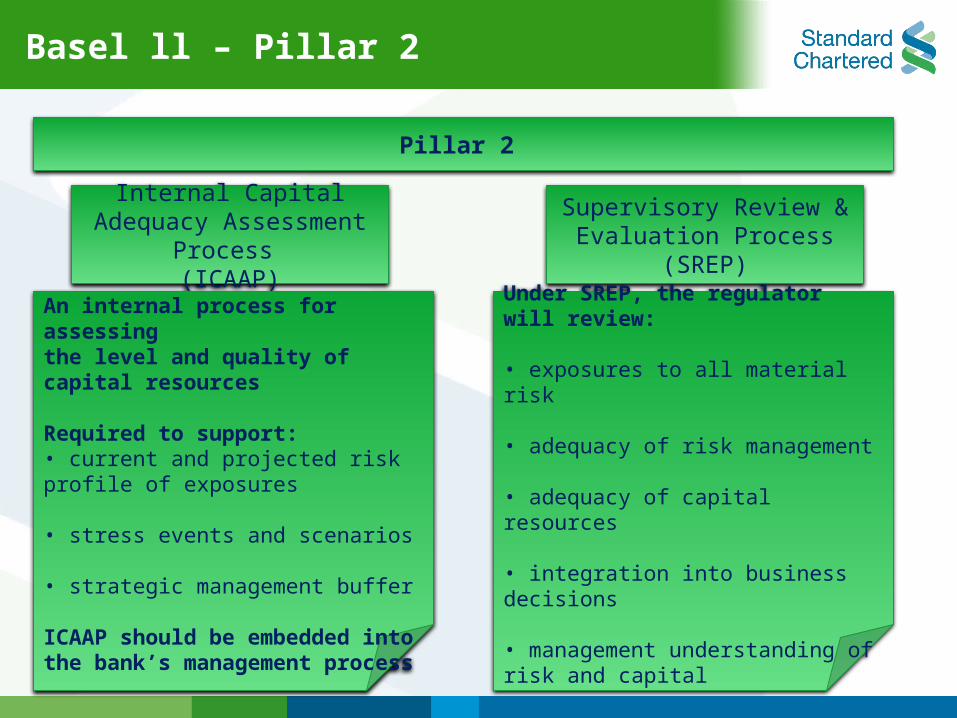

Pillar 2

Internal Capital Adequacy Assessment Process

(ICAAP)

Supervisory Review & Evaluation Process

(SREP)

An internal process for assessingthe level and quality of capital resources

Required to support:• current and projected risk profile of exposures

• stress events and scenarios

• strategic management buffer

ICAAP should be embedded into the bank’s management process

Under SREP, the regulator will review:

• exposures to all material risk

• adequacy of risk management

• adequacy of capital resources

• integration into business decisions

• management understanding of risk and capital

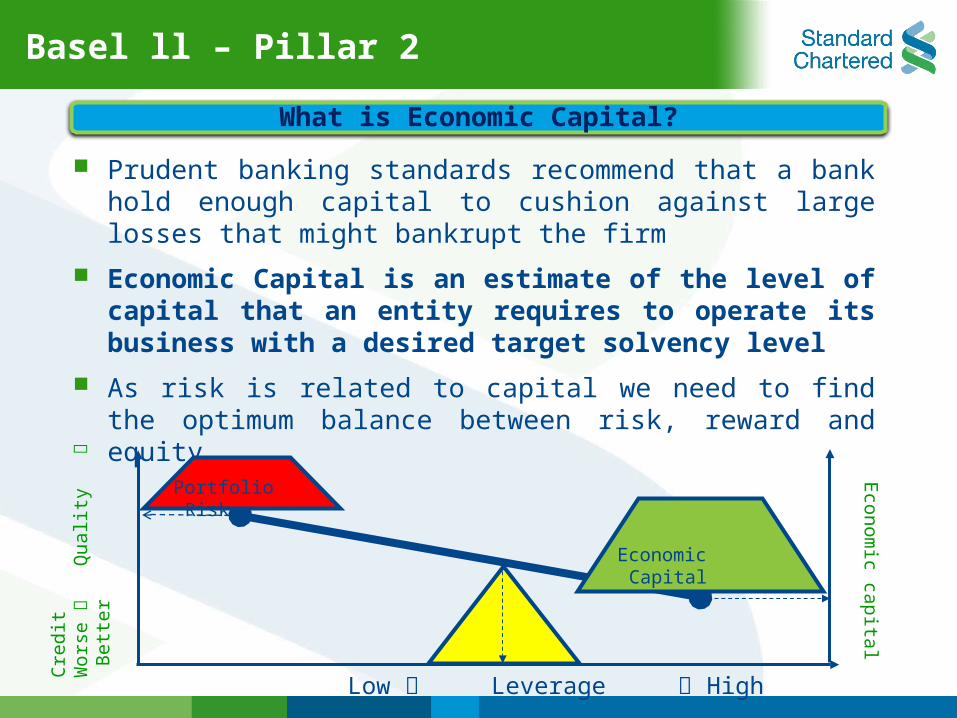

Prudent banking standards recommend that a bank hold enough capital to cushion against large losses that might bankrupt the firm

Economic Capital is an estimate of the level of capital that an entity requires to operate its business with a desired target solvency level

As risk is related to capital we need to find the optimum balance between risk, reward and equity

Cre

dit

Wor

se

Q

ual

ity

B

ette

r

Low Leverage High

Portfolio Risk

Economic Capital

Econom

ic capital

What is Economic Capital?

Basel ll – Pillar 2

Basel ll

Pillar 3

Enhanced Market discipline through transparency framework

Market disclosure:– capital structure – risk management policies and practices – risk profile – capital adequacy

Discusses the role of materiality of information, frequency of disclosures and the issue of proprietary or confidential information

Basel ll – Pillar 3

Pillar 3- Disclosure and Market Discipline

Pillar 3 disclosures will be published on the Group website and its location will be referenced in the Annual Report and Accounts

Firms are exempt from disclosing information which is:

– Immaterial

– Proprietary; public sharing would undermine Group’s competitive position

– Confidential information; information where we have binding agreements to the effect with customers/counterparties

Basel ll – Pillar 3

Pillar 3- Disclosure and Market Discipline

Basel ll

SCB Position

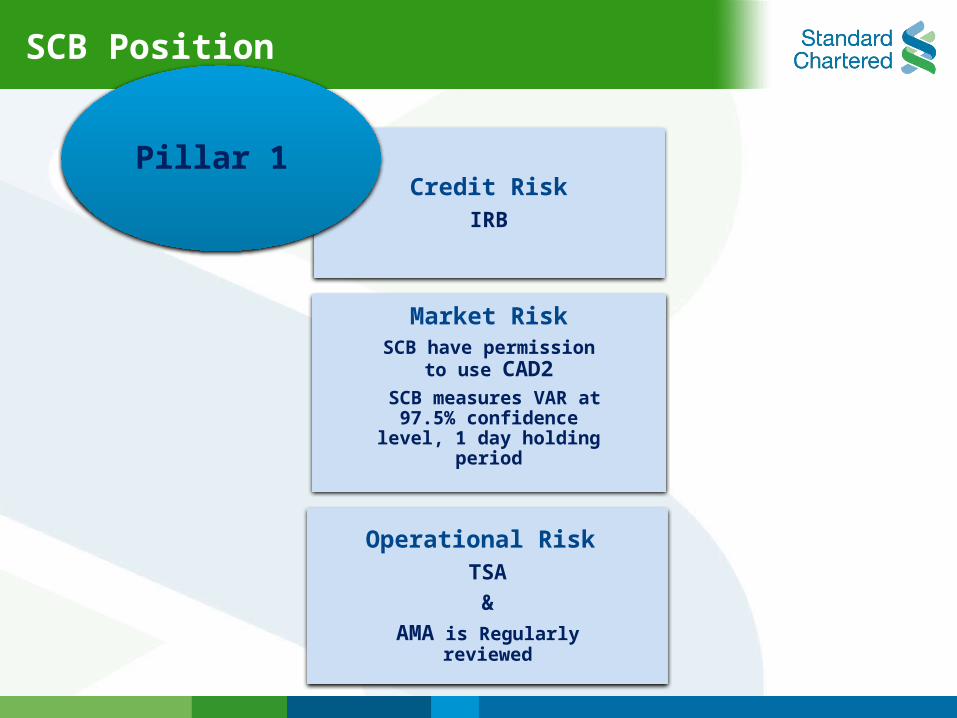

For SCB Group the Basel II regime started on 1 January 2008

Credit RiskIRB

Market RiskSCB have permission to

use CAD2 SCB measures VAR at

97.5% confidence level, 1 day holding period

Operational Risk TSA

&

AMA is Regularly reviewed

Pillar 1

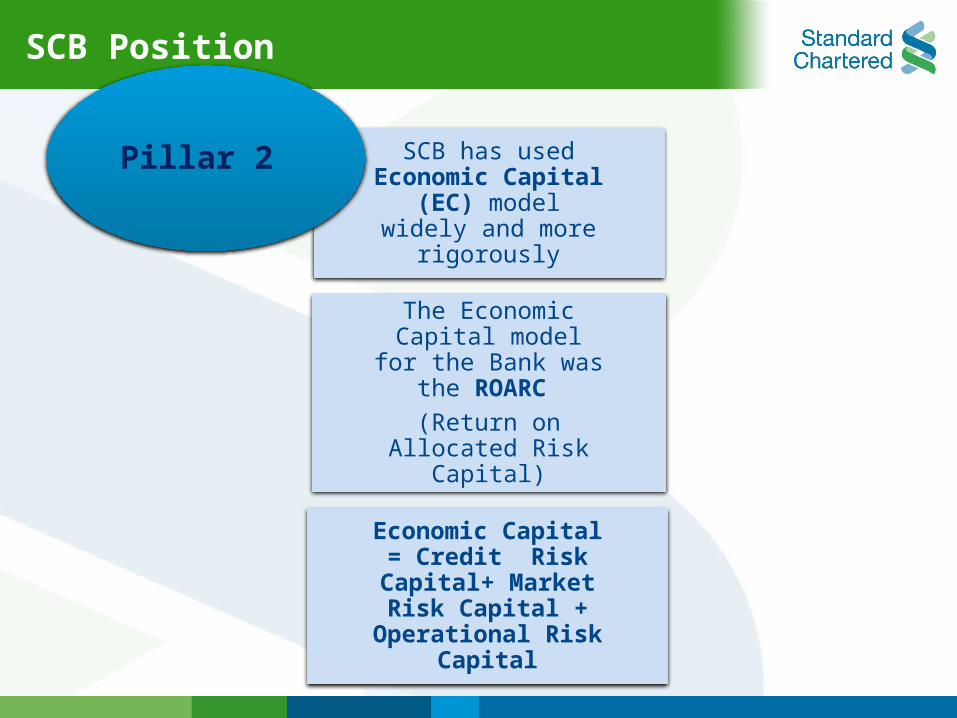

SCB Position

SCB has used Economic Capital (EC) model widely

and more rigorously

The Economic Capital model for the Bank was the ROARC

(Return on Allocated Risk Capital)

Economic Capital = Credit Risk Capital+ Market Risk Capital +

Operational Risk Capital

Pillar 2

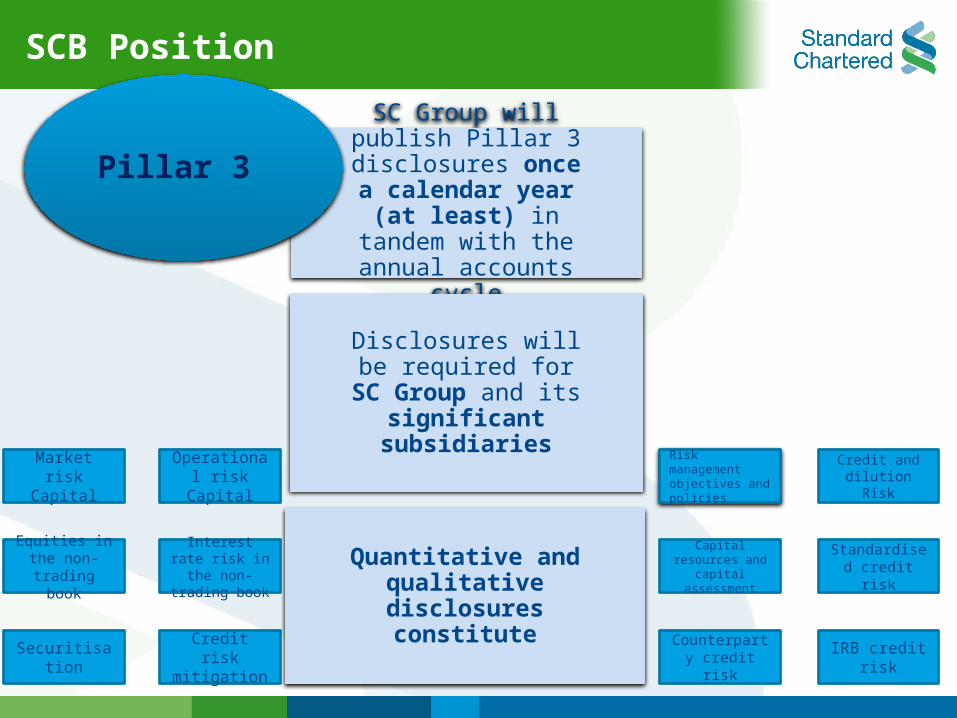

SCB Position

SC Group will publish Pillar 3 disclosures

once a calendar year (at least) in tandem

with the annual accounts cycle

Disclosures will be required for SC Group and its

significant subsidiaries

Quantitative and qualitative

disclosures constitute

Pillar 3

Risk management objectives and policies

Credit and dilution Risk

Capital resources and capital assessment

Standardised credit risk

Counterparty credit risk

IRB credit risk

Market risk Capital

Operational risk Capital

Equities in the non-trading

book

Interest rate risk in the non-

trading book

SecuritisationCredit risk mitigation

SCB Position

The recent global financial crisis has revealed weaknesses in the whole approach to risk management that has been developed through the Basel II process

Basel II did not adequately anticipate some risks such as a collapse in market liquidity as investor confidence disappeared and deep losses in the market value of securities held by banks

Basel ll

The impact of the financial crisis on Basel ll

Is much more complex than Basel I

Relies on high quality, accurate data

Makes regulatory capital closer to economic capital

Emphasizes risk quality

Will make RWA and capital much more volatile

Needs a definite change in the risk culture

Basel ll

Basel ll Synopsis

Basel lll

Basel lll

Basel III is a comprehensive set of reform measures, developed by the Basel Committee on Banking Supervision, to strengthen the regulation, supervision and risk management of the banking sector

Aims to improve and strengthen banking sector’s :

Ability to absorb shocks arising from financial and economic stress

Risk management and governance

Transparency and disclosures

Basel lll – attempts to encourage banks to hold larger percentages of Government Bonds to provide a riskless safety net should they run into liquidity problems

Basel lll

Does Holding large percentage of Government Bonds REALLY save the bank

from Bankruptcy ?

Example: Holding of Italian debt (20% risk-

weighting) bankrupted MF Global in the space of a week!

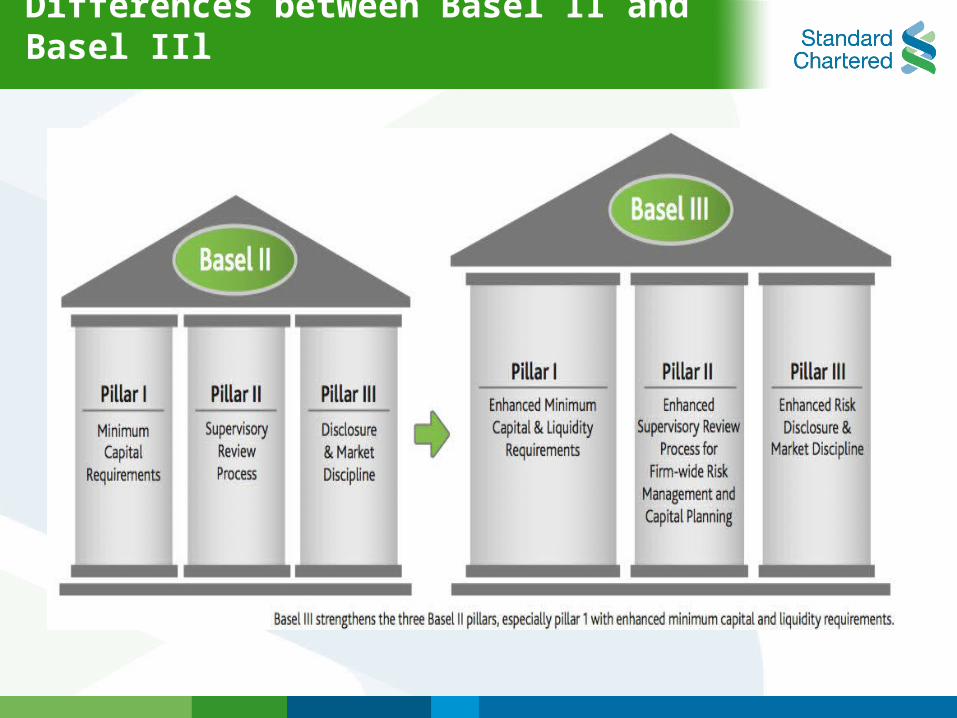

Differences between Basel II and Basel IIl

Differences between Basel II and Basel IIl

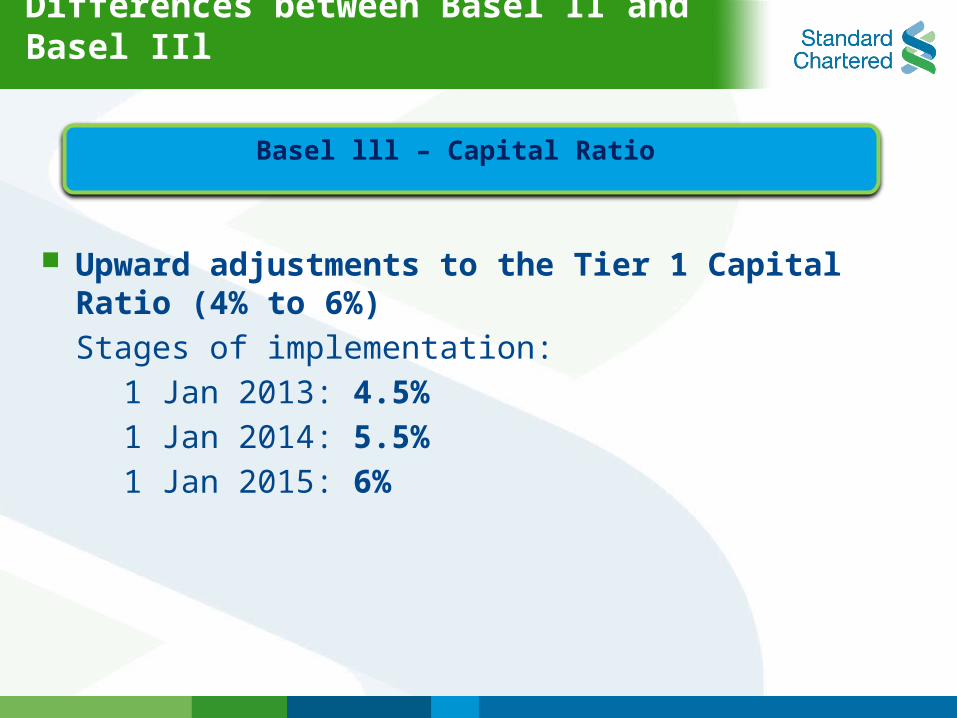

Upward adjustments to the Tier 1 Capital Ratio (4% to 6%)

Stages of implementation:

1 Jan 2013: 4.5%

1 Jan 2014: 5.5%

1 Jan 2015: 6%

Basel lll – Capital Ratio

Differences between Basel II and Basel IIl

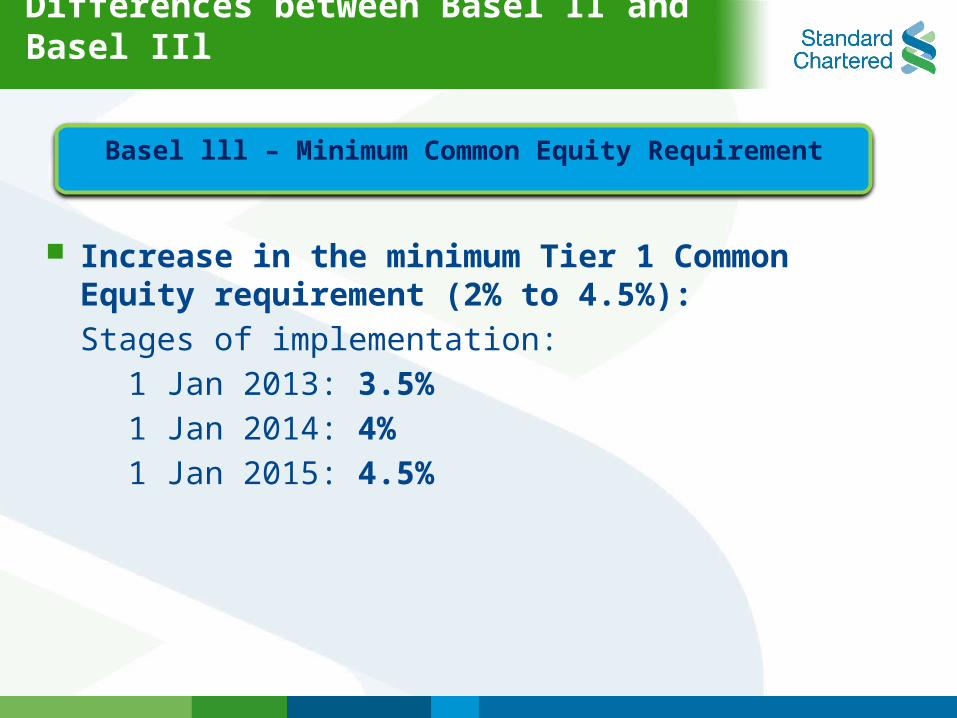

Basel lll – Minimum Common Equity Requirement

Increase in the minimum Tier 1 Common Equity requirement (2% to 4.5%):

Stages of implementation:

1 Jan 2013: 3.5%

1 Jan 2014: 4%

1 Jan 2015: 4.5%

Differences between Basel II and Basel lll

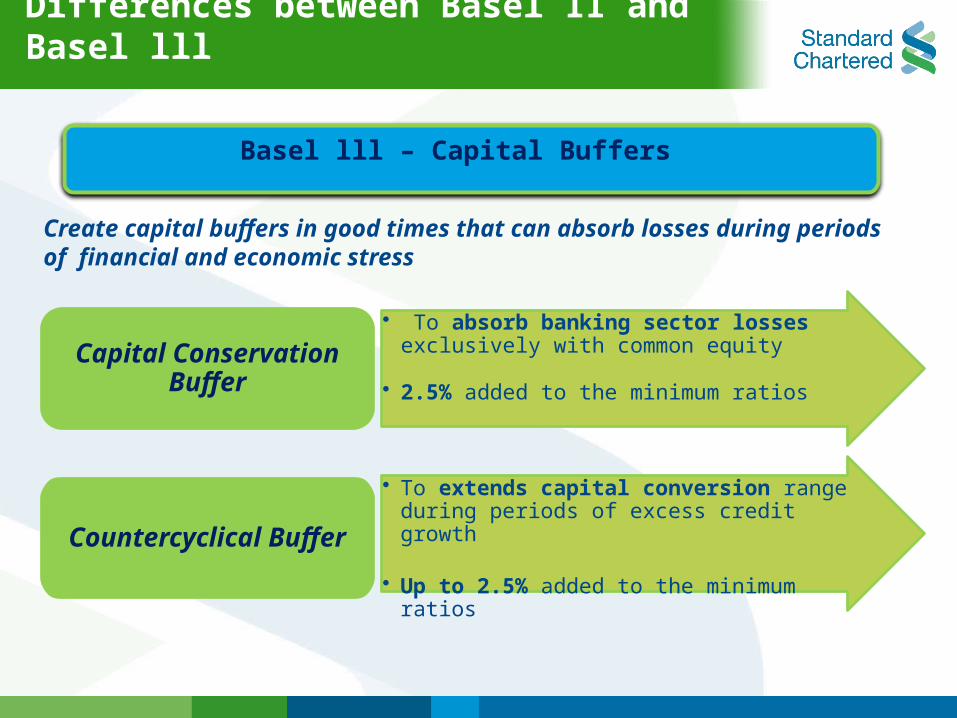

Basel lll – Capital Buffers

Create capital buffers in good times that can absorb losses during periods of financial and economic stress

• To absorb banking sector losses exclusively with common equity

• 2.5% added to the minimum ratiosCapital Conservation

Buffer

• To extends capital conversion range during periods of excess credit growth

• Up to 2.5% added to the minimum ratiosCountercyclical Buffer

Differences between Basel II and Basel IIl

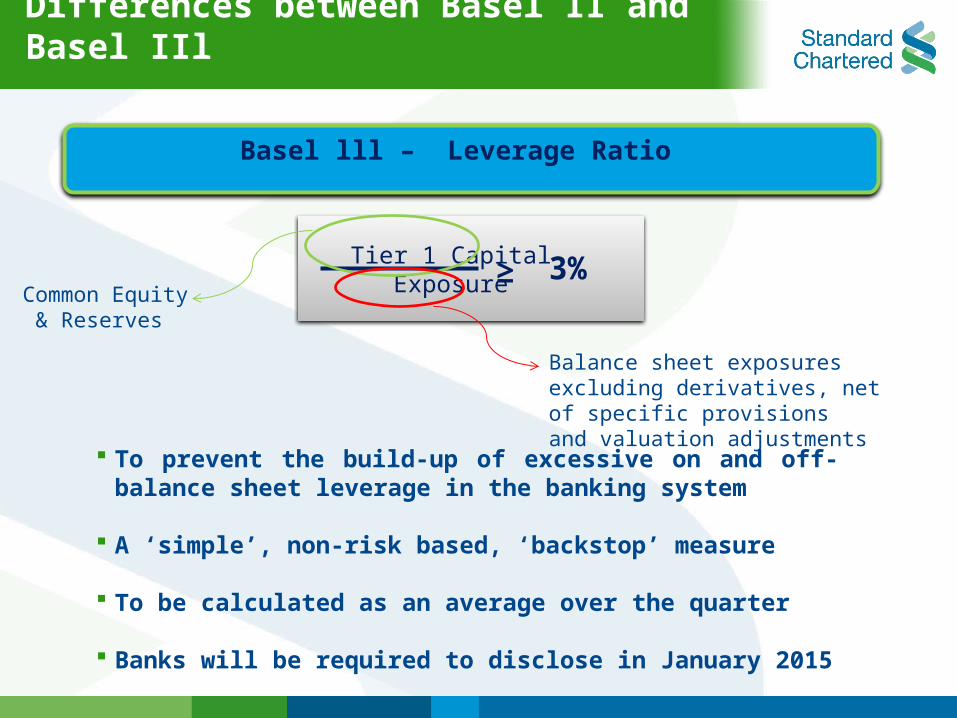

Basel lll – Leverage Ratio

Tier 1 Capital Exposure ≥ 3%

To prevent the build-up of excessive on and off-balance sheet leverage in the banking system

A ‘simple’, non-risk based, ‘backstop’ measure

To be calculated as an average over the quarter

Banks will be required to disclose in January 2015

Common Equity & Reserves

Balance sheet exposures excluding derivatives, net of specific provisionsand valuation adjustments

Differences between Basel II and Basel IIl

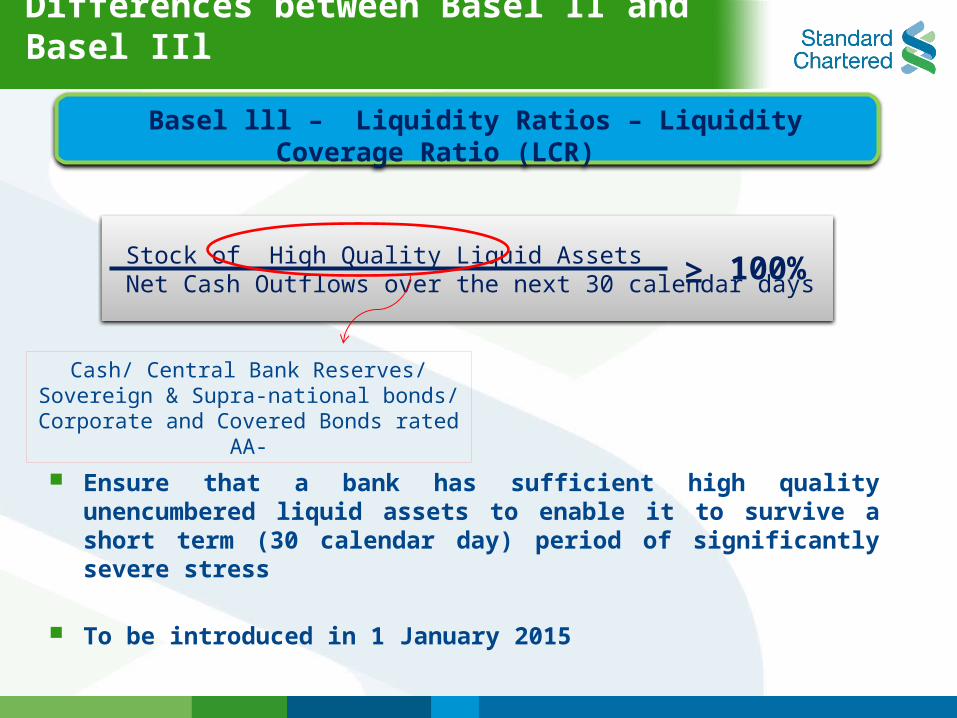

Ensure that a bank has sufficient high quality unencumbered liquid assets to enable it to survive a short term (30 calendar day) period of significantly severe stress

To be introduced in 1 January 2015

Basel lll – Liquidity Ratios – Liquidity Coverage Ratio (LCR)

Stock of High Quality Liquid Assets Net Cash Outflows over the next 30 calendar days ≥ 100%

Cash/ Central Bank Reserves/ Sovereign & Supra-national bonds/ Corporate and

Covered Bonds rated AA-

Differences between Basel II and Basel IIl

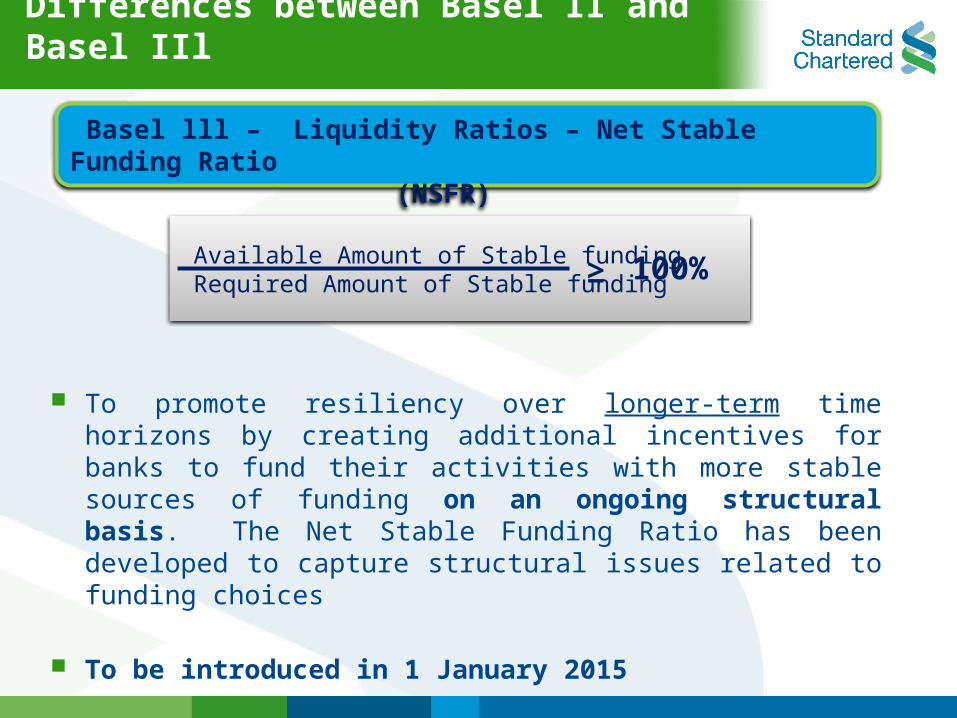

To promote resiliency over longer-term time horizons by creating additional incentives for banks to fund their activities with more stable sources of funding on an ongoing structural basis. The Net Stable Funding Ratio has been developed to capture structural issues related to funding choices

To be introduced in 1 January 2015

Basel lll – Liquidity Ratios – Net Stable Funding Ratio (NSFR)

Available Amount of Stable funding Required Amount of Stable funding ≥ 100%

Basel lll

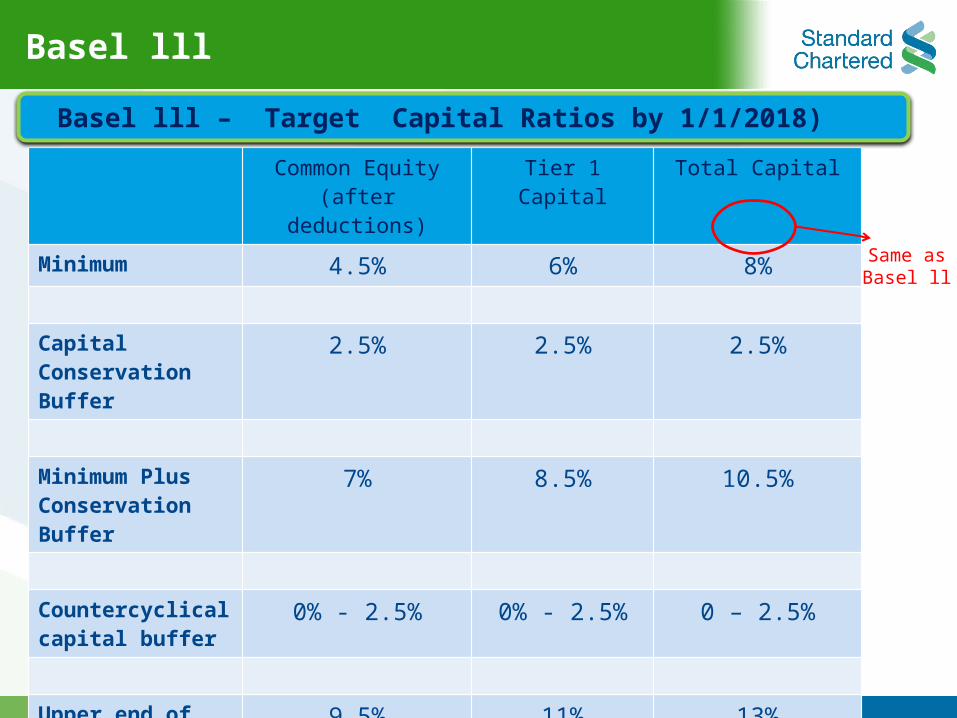

Common Equity (after deductions)

Tier 1 Capital Total Capital

Minimum 4.5% 6% 8%

Capital Conservation Buffer

2.5% 2.5% 2.5%

Minimum Plus Conservation Buffer

7% 8.5% 10.5%

Countercyclical capital buffer

0% - 2.5% 0% - 2.5% 0 – 2.5%

Upper end of minimum capital

9.5% 11% 13%

Basel lll – Target Capital Ratios by 1/1/2018)

Same as Basel ll

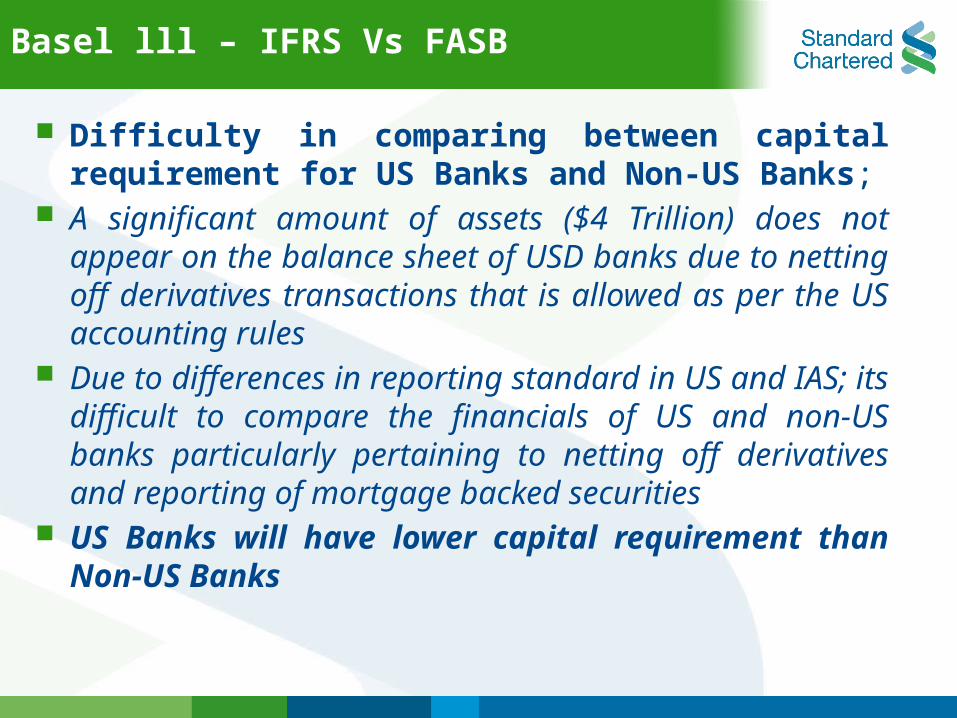

Basel lll – IFRS Vs FASB

Difficulty in comparing between capital requirement for US Banks and Non-US Banks;

A significant amount of assets ($4 Trillion) does not appear on the balance sheet of USD banks due to netting off derivatives transactions that is allowed as per the US accounting rules

Due to differences in reporting standard in US and IAS; its difficult to compare the financials of US and non-US banks particularly pertaining to netting off derivatives and reporting of mortgage backed securities

US Banks will have lower capital requirement than Non-US Banks

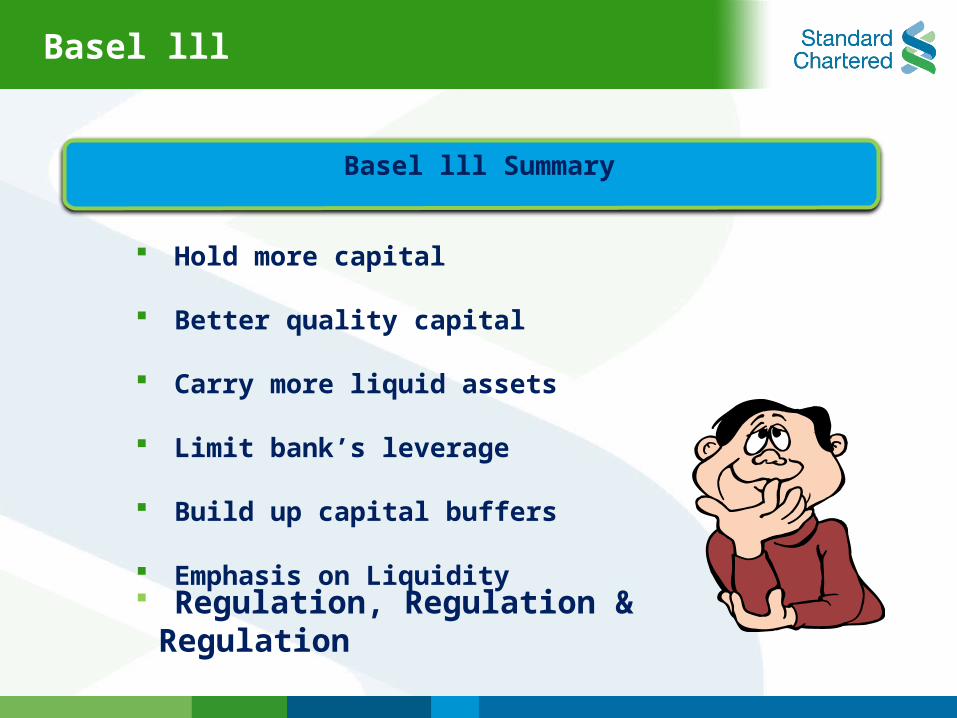

Hold more capital

Better quality capital

Carry more liquid assets

Limit bank’s leverage

Build up capital buffers

Emphasis on Liquidity

Basel lll

Basel lll Summary

Regulation, Regulation & Regulation

Regulation Examples

Basel l, ll, lll

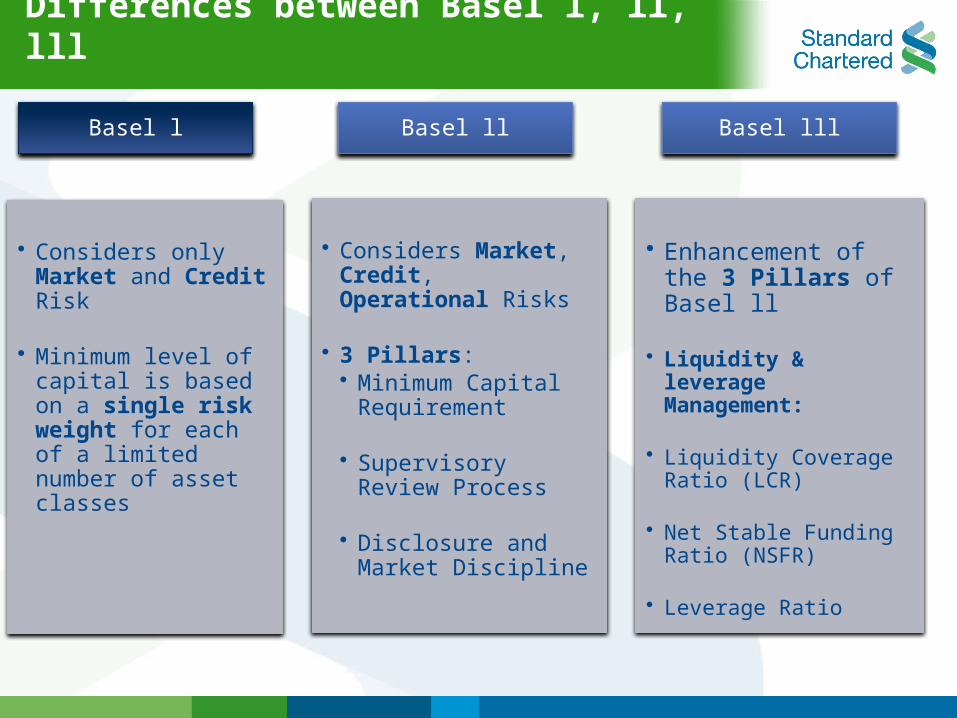

Differences between Basel l, ll, lll

Basel l

• Considers only Market and Credit Risk

• Minimum level of capital is based on a single risk weight for each of a limited number of asset classes

Basel ll

• Considers Market, Credit, Operational Risks

• 3 Pillars:• Minimum Capital

Requirement

• Supervisory Review Process

• Disclosure and Market Discipline

Basel lll

• Enhancement of the 3 Pillars of Basel ll

• Liquidity & leverage Management:

• Liquidity Coverage Ratio (LCR)

• Net Stable Funding Ratio (NSFR)

• Leverage Ratio

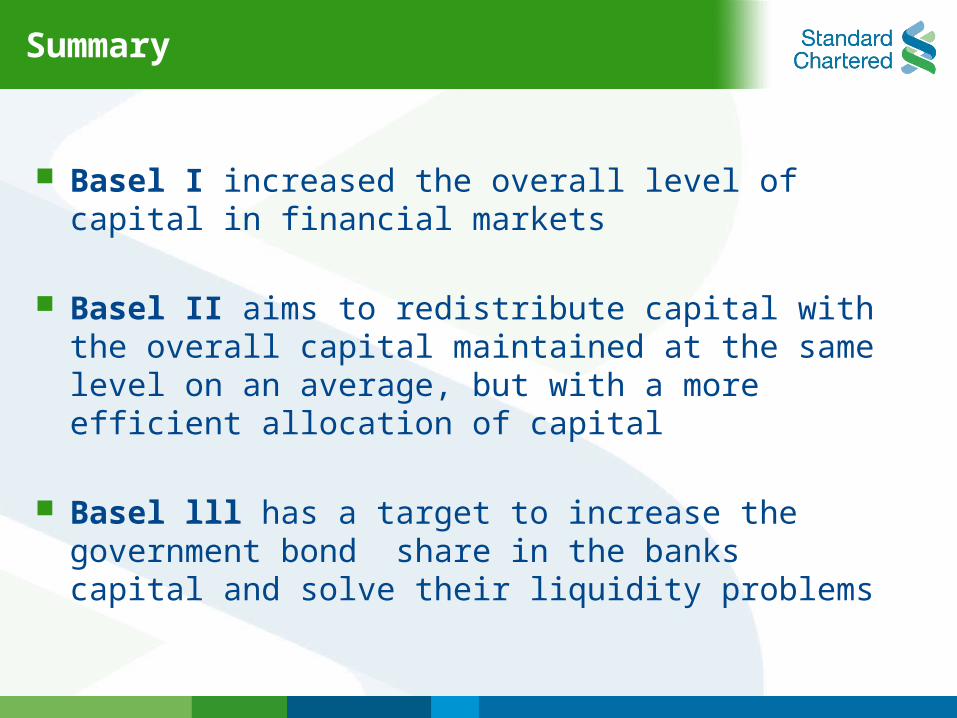

Summary

Basel I increased the overall level of capital in financial markets

Basel II aims to redistribute capital with the overall capital maintained at the same level on an average, but with a more efficient allocation of capital

Basel lll has a target to increase the government bond share in the banks capital and solve their liquidity problems

Q & A