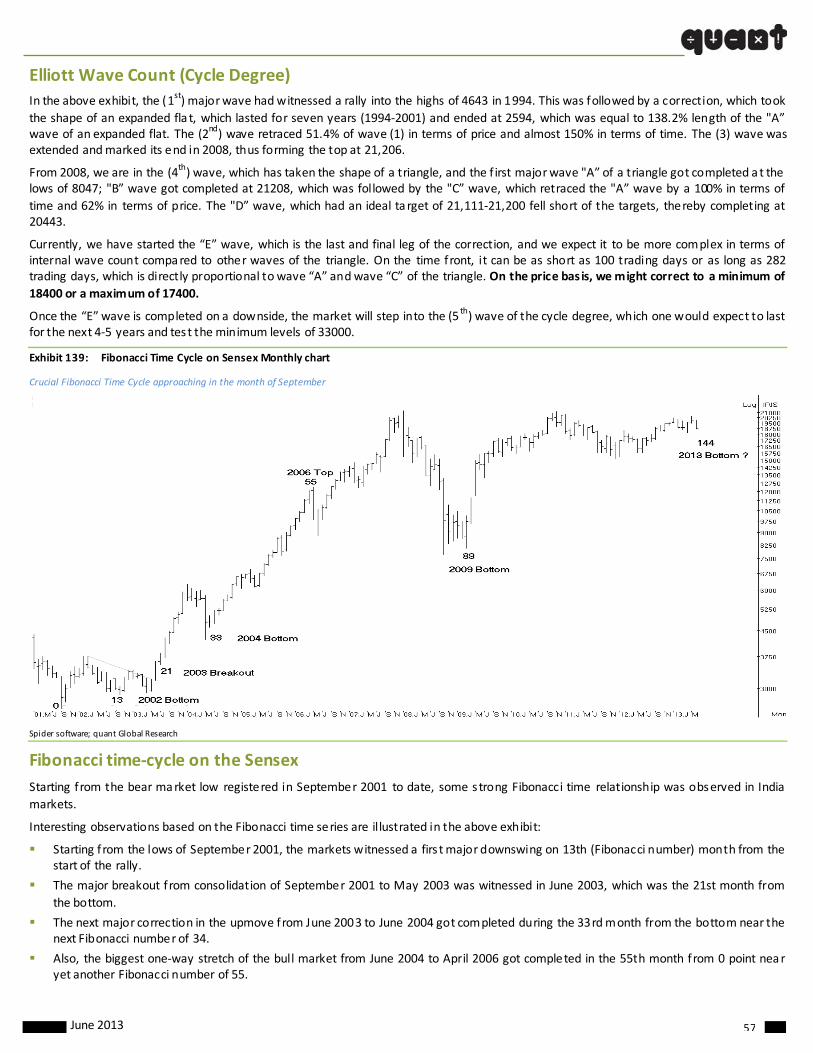

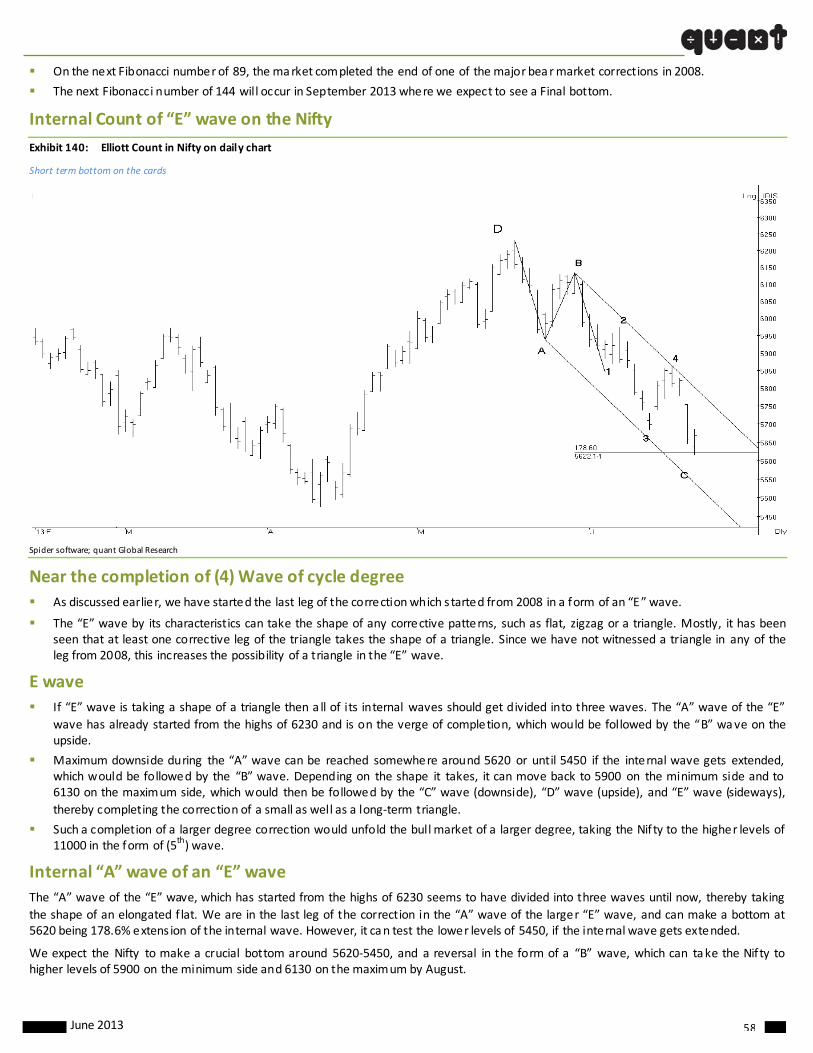

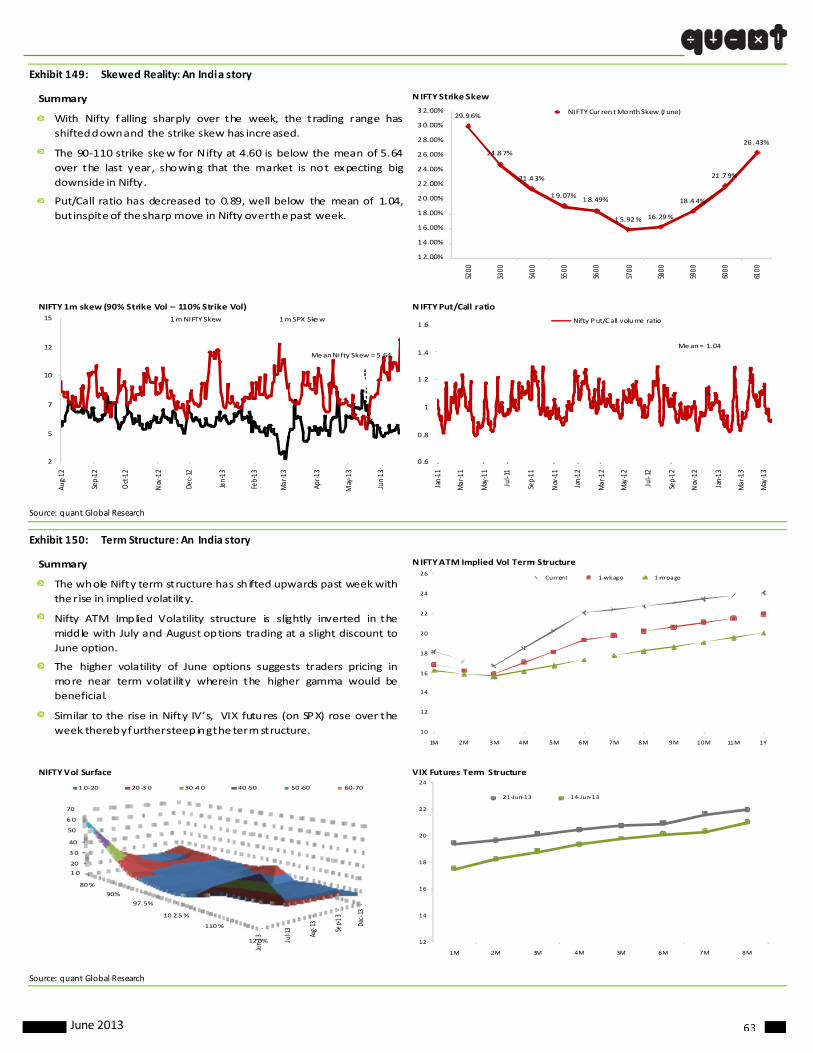

based on our analysis we have the following trading … on our analysis we have the following...

TRANSCRIPT

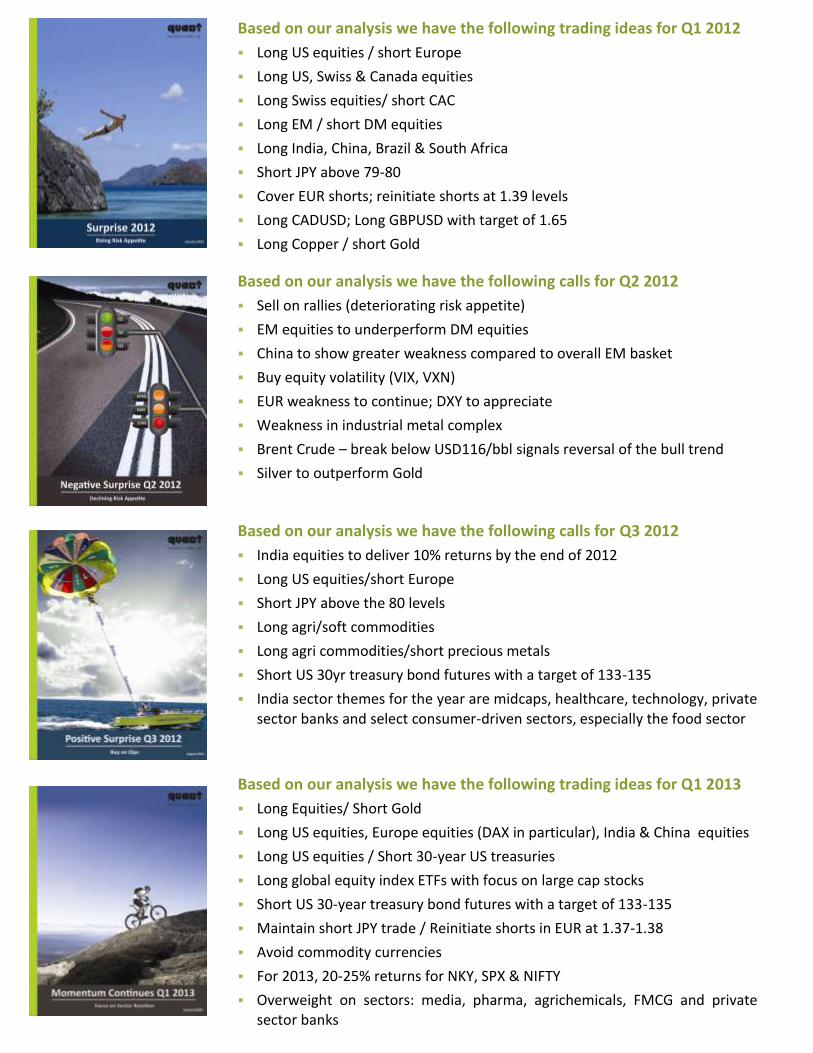

Based on our analysis we have the following trading ideas for Q1 2012

Long US equities / short Europe

Long US, Swiss & Canada equities

Long Swiss equities/ short CAC

Long EM / short DM equities

Long India, China, Brazil & South Africa

Short JPY above 79-80

Cover EUR shorts; reinitiate shorts at 1.39 levels

Long CADUSD; Long GBPUSD with target of 1.65

Long Copper / short Gold

Based on our analysis we have the following calls for Q2 2012

Sell on rallies (deteriorating risk appetite)

EM equities to underperform DM equities

China to show greater weakness compared to overall EM basket

Buy equity volatility (VIX, VXN)

EUR weakness to continue; DXY to appreciate

Weakness in industrial metal complex

Brent Crude – break below USD116/bbl signals reversal of the bull trend

Silver to outperform Gold

Based on our analysis we have the following calls for Q3 2012

India equities to deliver 10% returns by the end of 2012

Long US equities/short Europe

Short JPY above the 80 levels

Long agri/soft commodities

Long agri commodities/short precious metals

Short US 30yr treasury bond futures with a target of 133-135

India sector themes for the year are midcaps, healthcare, technology, private sector banks and select consumer-driven sectors, especially the food sector

Based on our analysis we have the following trading ideas for Q1 2013

Long Equities/ Short Gold

Long US equities, Europe equities (DAX in particular), India & China equities

Long US equities / Short 30-year US treasuries

Long global equity index ETFs with focus on large cap stocks

Short US 30-year treasury bond futures with a target of 133-135

Maintain short JPY trade / Reinitiate shorts in EUR at 1.37-1.38

Avoid commodity currencies

For 2013, 20-25% returns for NKY, SPX & NIFTY

Overweight on sectors: media, pharma, agrichemicals, FMCG and private sector banks

C

2013 Q3‐Q4 Outlook As liquidity drives equity markets higher in Q1/Q2 of 2013, we expect this momentum to

rebuild in second half of Q3 after recent sharp corrections due to volatility in currency markets. However, global equity markets may remain susceptible to bouts of volatility due

to higher impact costs and lower retail participation. We maintain our stand that any sharp fall in 2013, should be seen as a buying opportunity. The upswing in US equities which started in Q4 2011 should resume from mid August taking US equity markets higher in 2013.

European equity markets are also expected to rally with a lag with DAX leading th e way. Commodities currencies will remain under pressure; Brazil, Russia and Chinese equities will continue their underperformance. In India, while we favoured large cap Nifty stocks for H1 2013, H2 2013 should see increased stock specific action in the midcaps space.

Asset Allocator Recommendations – Reducing DM bond exposure and increasing allocations to global equities remains our key strategy for 2013. For equities, we recommend buying on dips rather than selling the rallies as global economic growth recovers. Naked shorts in

equities should be avoided in 2013 as the bias continues to be positive. Exposure to commodity markets should be avoided as commodities will continue to underperform global equities. We continue to recommend reducing Gold exposure but remain positive on Agri

commodities specially Cotton, Coffee and Sugar.

Big calls for CY 2013

Equities to outperform bonds globally

Equities to outperform commodities and energy in particular

Agri Commodities to outperform Gold; Cotton, Coffee & Sugar are the best play

US Dollar to outperform JPY, Euro, AUD, CHF; DXY will rally to 85‐87 in Q3/Q4

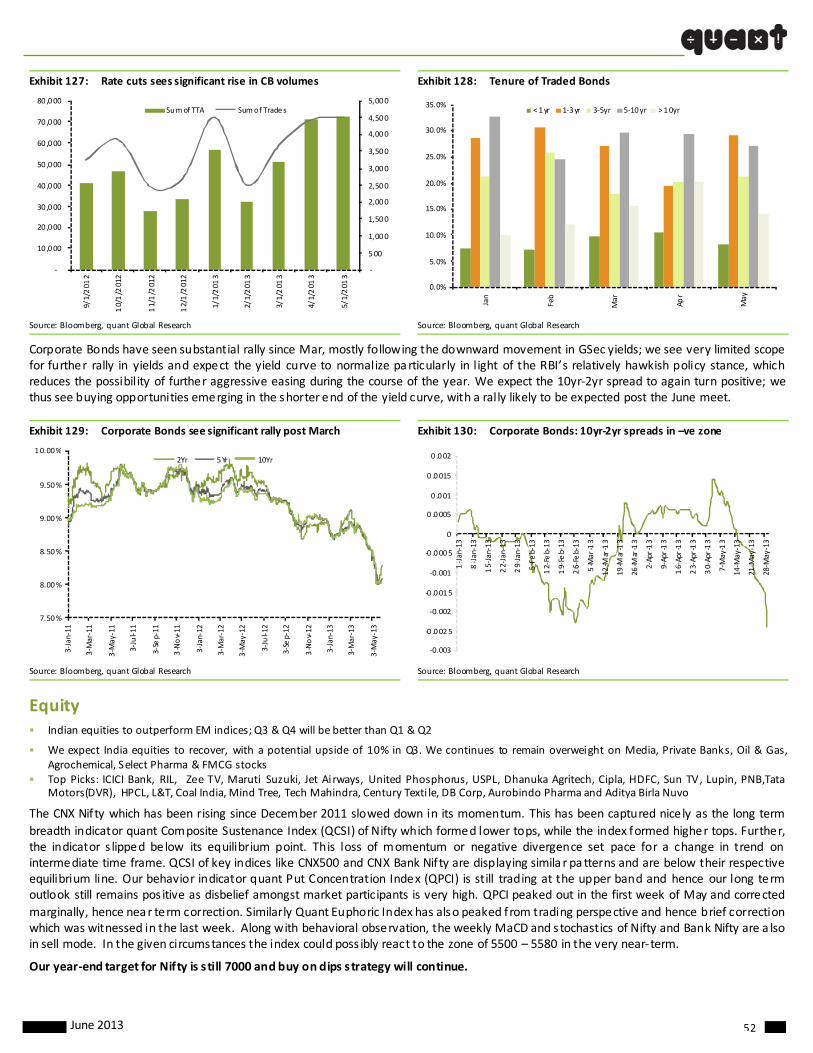

Indian equities to outperform EM indices; Q3 & Q4 will be better than Q1 & Q2

Hang Seng outperformance continues to Shanghai Composite Indices & CSI 300

Chinese equities to underperform global equities; but still deliver positive returns in 2013

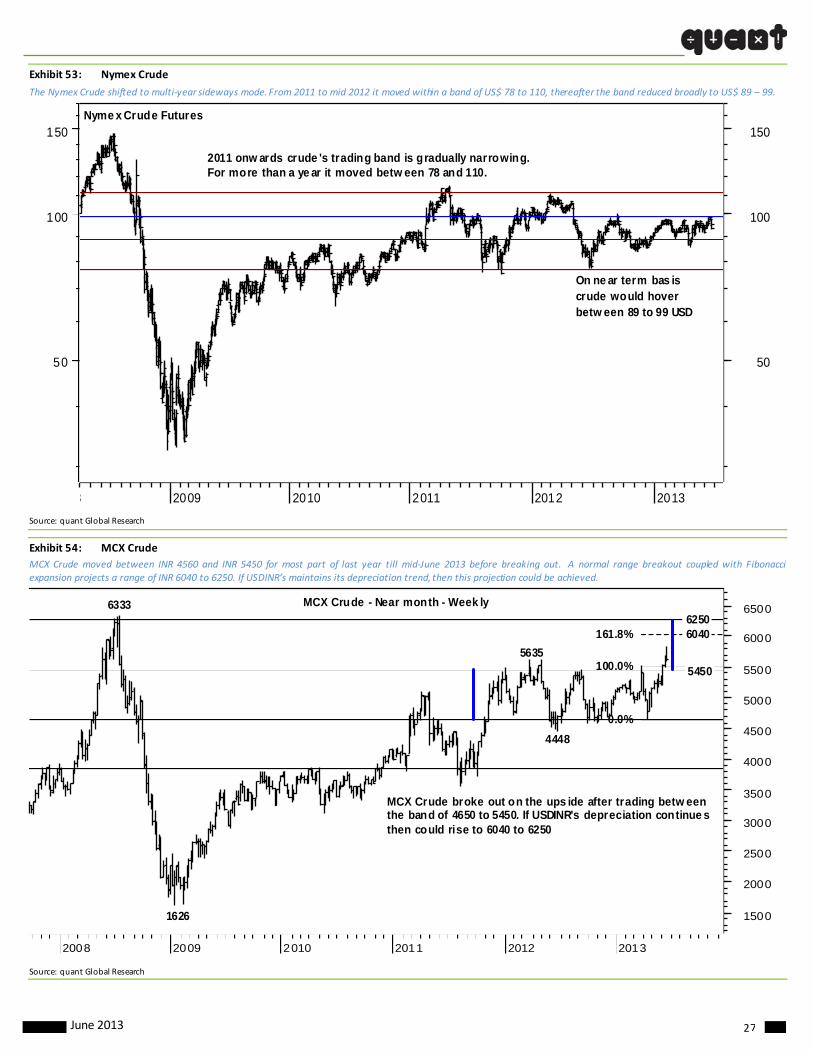

Nymex crude to underperform equities but to remain volatile; Bullish in the near term with a

target of US$ 103/barrel but year‐end target is US$ 83‐85

Maintain our US, Japan and India equity market calls for 2013 giving absolute returns of 20‐25%. FIIs clients should hedge JPY exposure to protect their absolute gains

INR to appreciate in second half of Q3 and it will recover. 55‐62 range for H2 2013

Maintain Nifty target for year‐end is 7000 with a positive bias for second half of Q3

Maintain USD‐JPY year‐end target of 95‐97 and Euro target of 1.22

Based on our analysis we have the following trading ideas for Q3 2013:

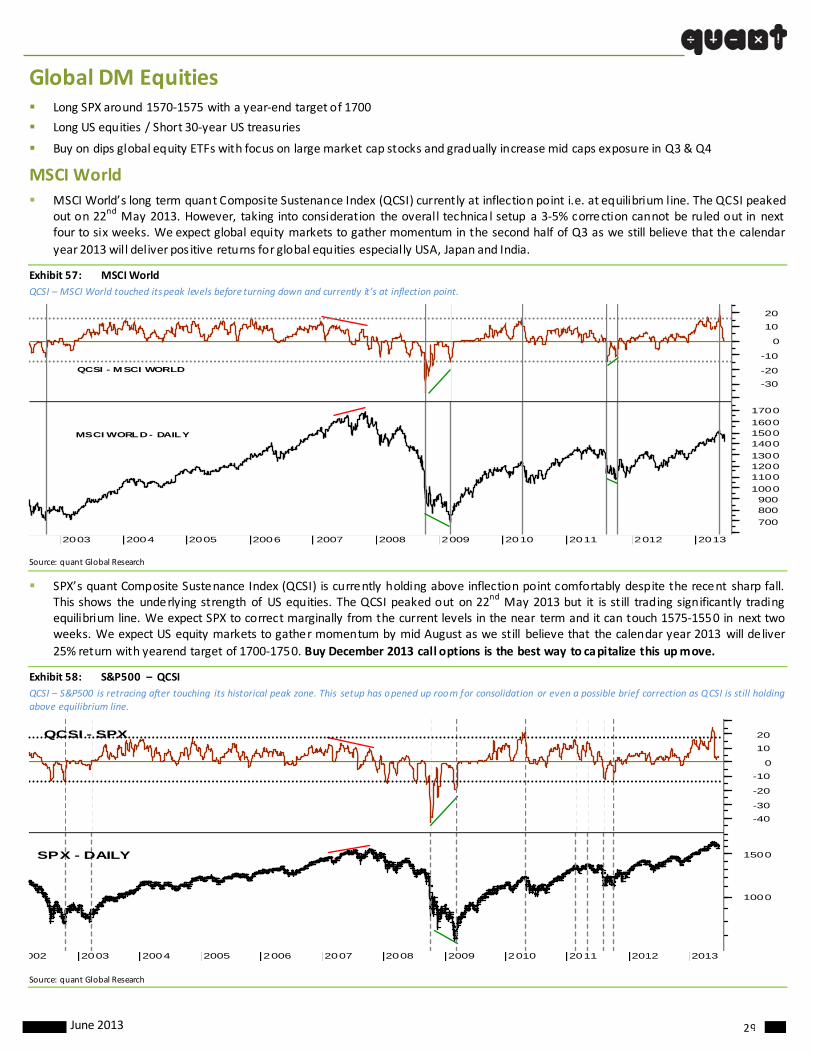

Long SPX around 1570‐75 with a yearend target of 1700

Long US equities / Short 30‐year US treasuries

Maintain short JPY trade and re‐initiate shorts in Euro at 1.32‐1.33 with first target 1.27 and

yearend target of 1.21‐1.22

Buy on dips global equity ETFs with focus on large market cap stocks and gradually increase mid caps exposure in Q3/Q4

Avoid exposure to commodities in general; Long Cotton, Coffee and Sugar

Short US 30yr treasury bond futures with a target of 130 by year end

We expect India equities to recover, with a potential upside of 10% in Q3. We continues to remain overweight on Media, Private Banks, Oil & Gas, Agrochemical , Select Pharma &

FMCG stocks

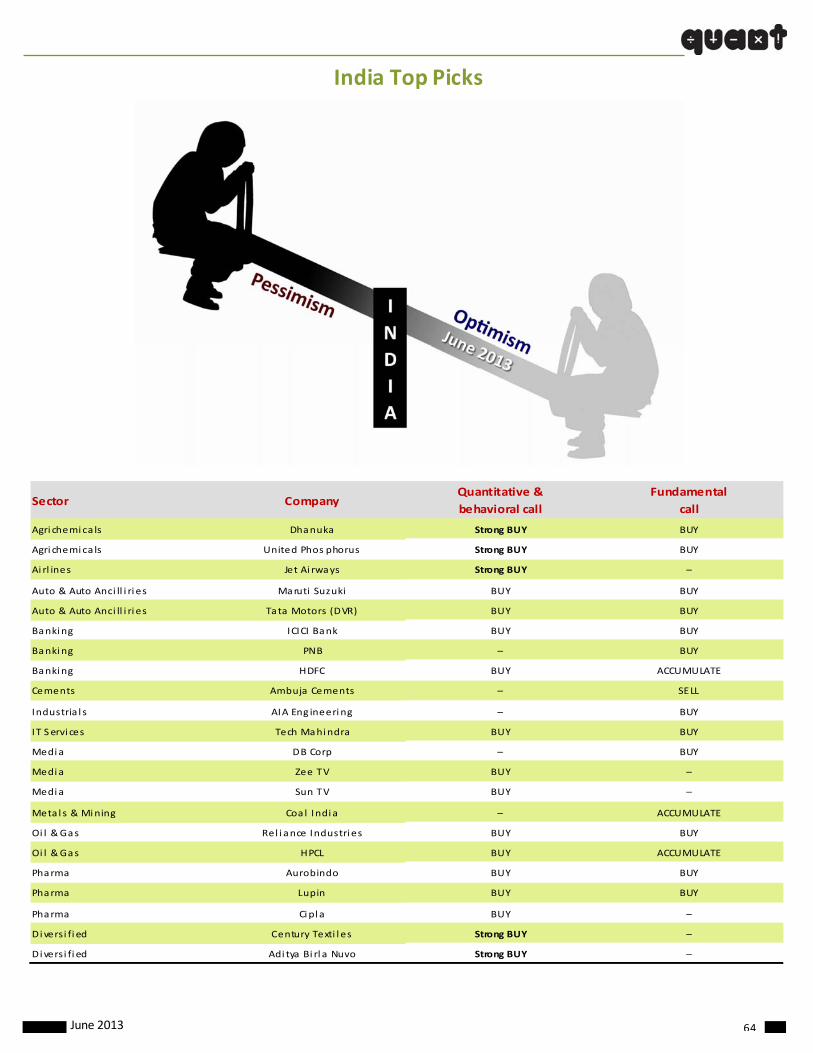

Top Picks

ICICI Bank, RIL, Zee TV, Maruti Suzuki, Jet Airways, United Phosphorus, USPL, Dhanuka

Agritech, Cipla, HDFC, Sun TV, Lupin, PNB,Tata Motors(DVR), HPCL, L&T, Coal India, Mind Tree, Tech Mahindra, Century Textile, DB Corp, Aurobindo Pharma and Aditya Birla Nuvo.

Sandeep Tandon

sandeep.tandon@quant capital.co.in

+91 22 4088 0251

Arunkumar S

+91 22 4088 0152

Pushpa Rai

+91 22 4287 1455

Bhupesh Bameta, CFA

+91 22 4088 0367

Anshum Bhambri

+91 22 4088 0136

Piyush Singh

+91 22 4088 0291

Rishav Dev

+91 22 4088 0147

Hardik Ruparel

+91 22 4088 0187

Alok Bisht

+91 22 4287 1585

Aniruddha Iyer

+91 22 4287 1511

Gaurav Balre

+91 22 4287 1516

Kumar Chitalia

+91 22 4088 0135

Rebuilding Momentum in Q3 2013 Volatility to Continue in Global Currencies

Global Macro Stra tegy | Gathering Momentum 2013 Series – III Global Outlook June 2013

June 2013 2

INDEX

Macro Risk …………………………………………………………………………………………………………………………….. 3

Global Fund Flows …………………………………………………………………………………………………………………………….. 10

Global Currencies …………………………………………………………………………………………………………………………….. 15

Global Commodities …………………………………………………………………………………………………………………………….. 20

Global DM Equities …………………………………………………………………………………………………………………………….. 29

Global EM Equities …………………………………………………………………………………………………………………………….. 33

Global Fixed Income …………………………………………………………………………………………………………………………….. 35

India Outlook …………………………………………………………………………………………………………………………….. 44

Macro …………………………………………………………………………………………………………………………….. 44

Fixed Income …………………………………………………………………………………………………………………………….. 51

Equity …………………………………………………………………………………………………………………………….. 52

Key Stock Picks …………………………………………………………………………………………………………………………….. 64

June 2013 3

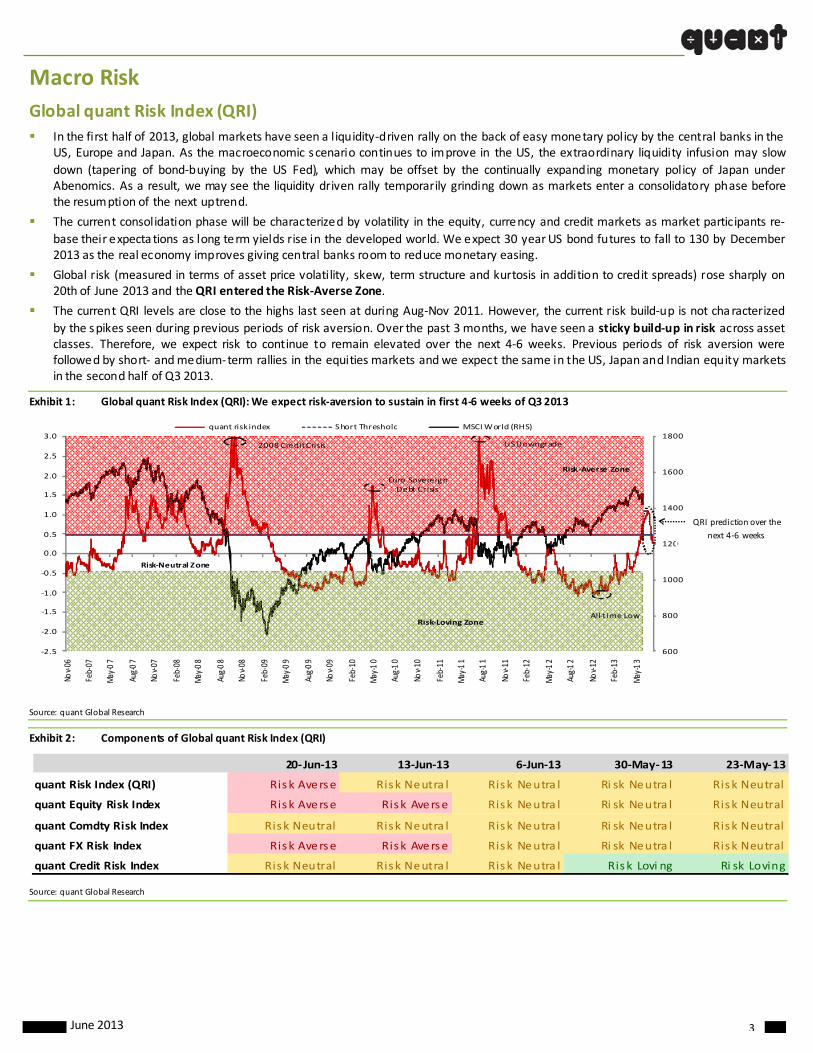

Macro Risk

Global quant Risk Index (QRI)

In the first half of 2013, global markets have seen a l iquidity‐driven rally on the back of easy monetary policy by the central banks in the US, Europe and Japan. As the macroeconomic scenario continues to improve in the US, the extraordinary liquidity infusion may slow

down (tapering of bond‐buying by the US Fed), which may be offset by the continually expanding monetary policy of Japan under Abenomics. As a result, we may see the liquidity driven rally temporarily grinding down as markets enter a consolidatory phase before the resumption of the next uptrend.

The current consolidation phase will be characterized by volatility in the equity, currency and credit markets as market participants re‐

base their expecta tions as long term yields rise in the developed world. We expect 30 year US bond futures to fall to 130 by December 2013 as the real economy improves giving central banks room to reduce monetary easing.

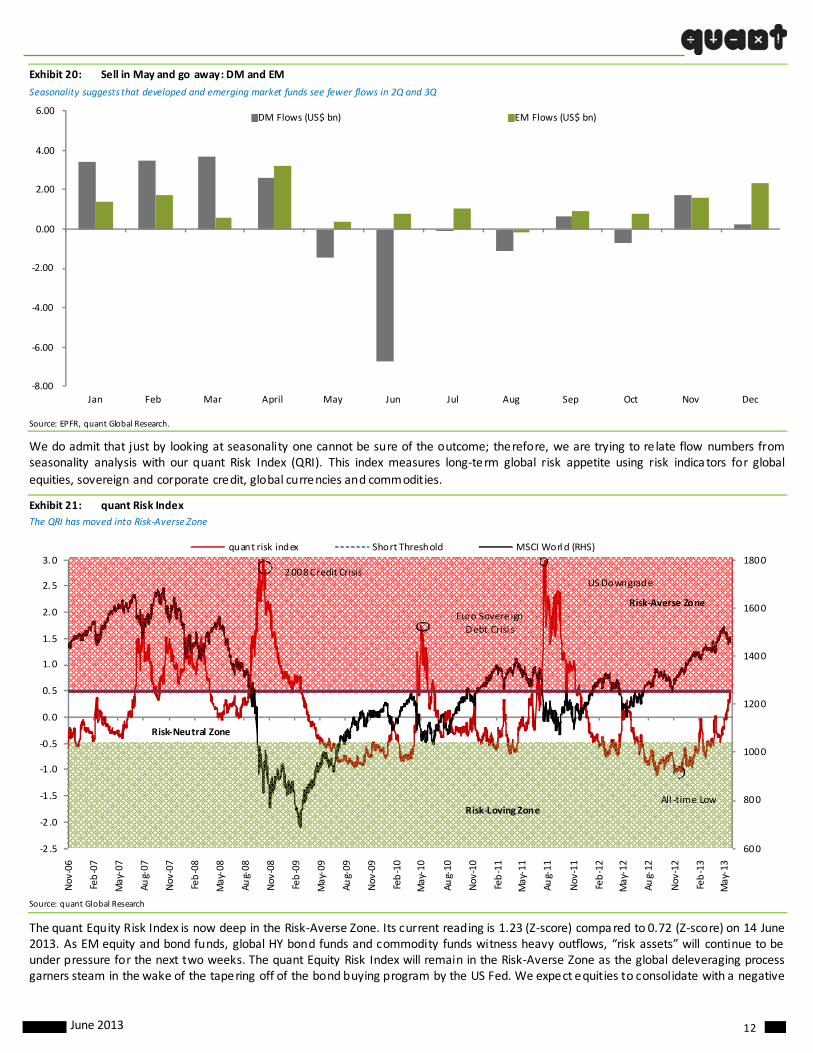

Global risk (measured in terms of asset price volatility, skew, term structure and kurtosis in addition to credit spreads) rose sharply on 20th of June 2013 and the QRI entered the Risk‐Averse Zone.

The current QRI levels are close to the highs last seen at during Aug‐Nov 2011. However, the current risk build‐up is not characterized

by the spikes seen during previous periods of risk aversion. Over the past 3 months, we have seen a sticky build‐up in risk across asset classes. Therefore, we expect risk to continue to remain elevated over the next 4‐6 weeks. Previous periods of risk aversion were followed by short‐ and medium‐term rallies in the equities markets and we expect the same in the US, Japan and Indian equity markets in the second half of Q3 2013.

Exhibit 1: Global quant Risk Index (QRI): We expect risk‐aversion to sustain in first 4‐6 weeks of Q3 2013

Source: quant Global Research

Exhibit 2: Components of Global quant Risk Index (QRI)

Source: quant Global Research

600

800

1000

1200

1400

1600

1800

Nov‐06

Feb‐07

May

‐07

Aug‐07

Nov‐07

Feb‐08

May

‐08

Aug‐08

Nov‐08

Feb‐09

May

‐09

Aug‐09

Nov‐09

Feb‐10

May

‐10

Aug‐10

Nov‐10

Feb‐11

May

‐11

Aug‐11

Nov‐11

Feb‐12

May

‐12

Aug‐12

Nov‐12

Feb‐13

May

‐13

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0quant risk index Short Threshold MSCI World (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

All‐t ime Low

2008 CreditCrisis US Downgrade

Euro Sovereign Debt Crisis

Risk‐Neutral Zone

20‐ Jun‐13 13‐Jun‐13 6‐Jun‐13 30‐May‐13 23‐May‐13

quant Risk Index (QRI) Risk Averse Risk Neutra l Risk Neutra l Ri sk Neutra l Risk Neutral

quant Equity Risk Index Risk Averse Risk Averse Risk Neutra l Ri sk Neutra l Risk Neutral

quant Comdty Risk Index Risk Neutral Risk Neutra l Risk Neutra l Ri sk Neutra l Risk Neutral

quant FX Risk Index Risk Averse Risk Averse Risk Neutra l Ri sk Neutra l Risk Neutral

quant Credit Risk Index Risk Neutral Risk Neutra l Risk Neutra l Risk Lovi ng Ri sk Loving

QRI prediction over the

next 4‐6 weeks

June 2013 4

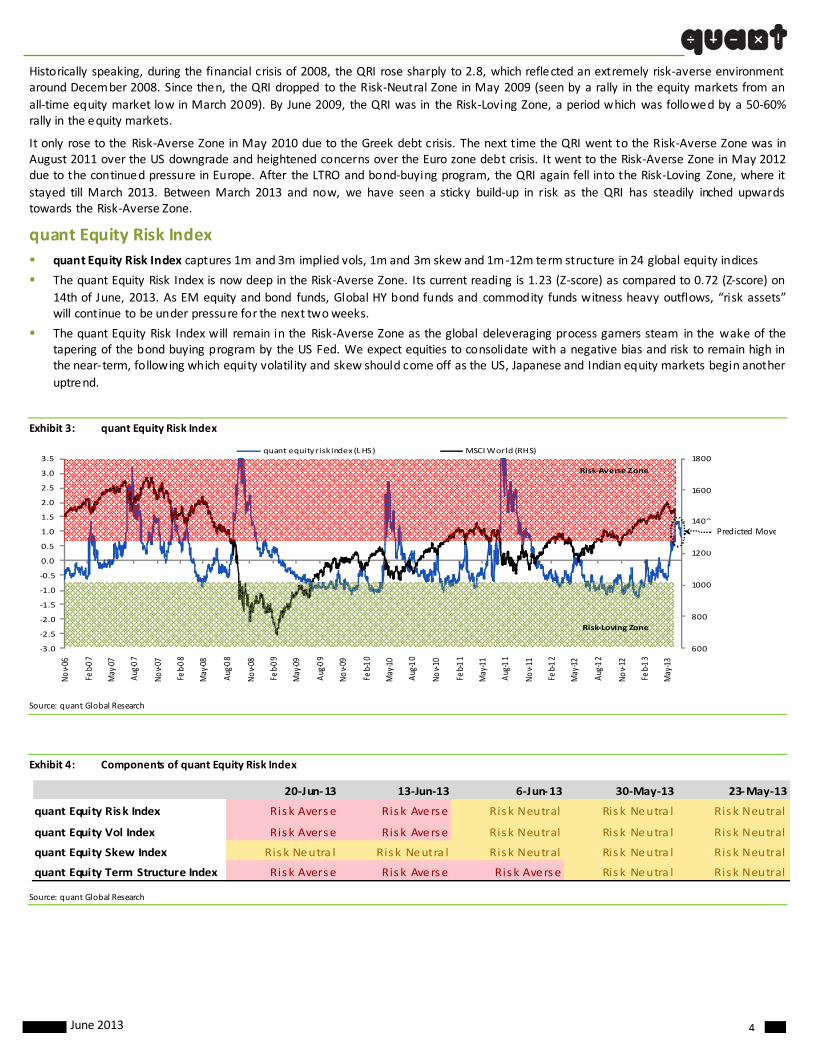

Historically speaking, during the financial crisis of 2008, the QRI rose sharply to 2.8, which reflected an extremely risk‐averse environment around December 2008. Since then, the QRI dropped to the Risk‐Neutral Zone in May 2009 (seen by a rally in the equity markets from an

all‐time equity market low in March 2009). By June 2009, the QRI was in the Risk‐Loving Zone, a period which was followed by a 50‐60% rally in the equity markets.

It only rose to the Risk‐Averse Zone in May 2010 due to the Greek debt crisis. The next time the QRI went to the Risk‐Averse Zone was in August 2011 over the US downgrade and heightened concerns over the Euro zone debt crisis. It went to the Risk‐Averse Zone in May 2012 due to the continued pressure in Europe. After the LTRO and bond‐buying program, the QRI again fell into the Risk‐Loving Zone, where it

stayed till March 2013. Between March 2013 and now, we have seen a sticky build‐up in risk as the QRI has steadily inched upwards towards the Risk‐Averse Zone.

quant Equity Risk Index

quant Equity Risk Index captures 1m and 3m implied vols, 1m and 3m skew and 1m ‐12m term structure in 24 global equity indices

The quant Equity Risk Index is now deep in the Risk‐Averse Zone. Its current reading is 1.23 (Z‐score) as compared to 0.72 (Z‐score) on

14th of June, 2013. As EM equity and bond funds, Global HY bond funds and commodity funds witness heavy outflows, “risk assets” will continue to be under pressure for the next two weeks.

The quant Equity Risk Index will remain in the Risk‐Averse Zone as the global deleveraging process garners steam in the wake of the tapering of the bond buying program by the US Fed. We expect equities to consolidate with a negative bias and risk to remain high in the near‐term, following which equity volatility and skew should come off as the US, Japanese and Indian equity markets begin another

uptrend.

Exhibit 3: quant Equity Risk Index

Source: quant Global Research

Exhibit 4: Components of quant Equity Risk Index

Source: quant Global Research

600

800

1000

1200

1400

1600

1800

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Nov‐06

Feb‐07

May

‐07

Aug

‐07

Nov‐07

Feb‐08

May

‐08

Aug

‐08

Nov‐08

Feb‐09

May

‐09

Aug

‐09

Nov‐09

Feb‐10

May

‐10

Aug

‐10

Nov‐10

Feb‐11

May

‐11

Aug

‐11

Nov‐11

Feb‐12

May

‐12

Aug

‐12

Nov‐12

Feb‐13

May

‐13

quant equity risk index (LHS) MSCI World (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

20‐Jun‐13 13‐Jun‐13 6‐Jun‐13 30‐May‐13 23‐May‐13

quant Equity Risk Index Risk Averse Risk Averse Risk Neutral Risk Neutra l Risk Neutral

quant Equity Vol Index Risk Averse Risk Averse Risk Neutral Risk Neutra l Risk Neutral

quant Equity Skew Index Risk Neutra l Risk Neutra l Risk Neutral Risk Neutra l Risk Neutral

quant Equity Term Structure Index Risk Averse Risk Averse Risk Averse Risk Neutra l Risk Neutral

Predicted Move

June 2013 5

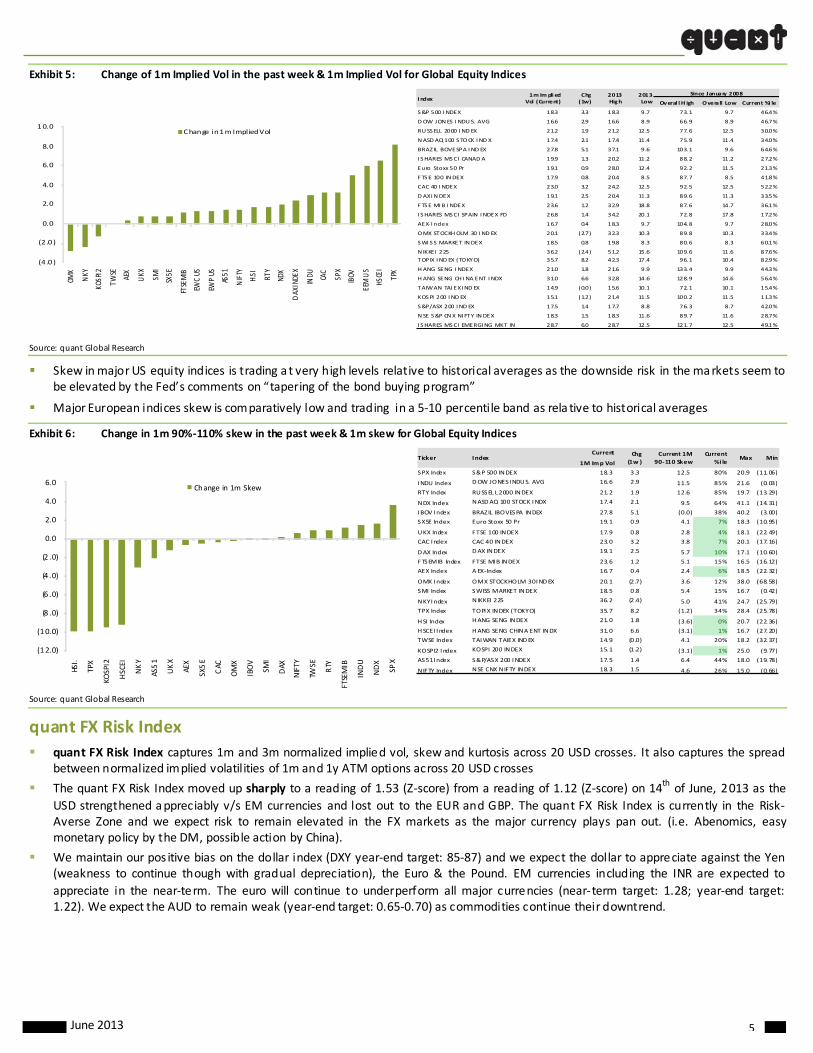

Exhibit 5: Change of 1m Implied Vol in the past week & 1m Implied Vol for Global Equity Indices

Source: quant Global Research

Skew in major US equity indices is trading at very high levels relative to historical averages as the downside risk in the markets seem to be elevated by the Fed’s comments on “tapering of the bond buying program”

Major European indices skew is comparatively low and trading in a 5‐10 percentile band as rela tive to historical averages

Exhibit 6: Change in 1m 90%‐110% skew in the past week & 1m skew for Global Equity Indices

Source: quant Global Research

quant FX Risk Index

quant FX Risk Index captures 1m and 3m normalized implied vol, skew and kurtosis across 20 USD crosses. It also captures the spread between normalized implied volatilities of 1m and 1y ATM options across 20 USD crosses

The quant FX Risk Index moved up sharply to a reading of 1.53 (Z‐score) from a reading of 1.12 (Z‐score) on 14th of June, 2013 as the

USD strengthened appreciably v/s EM currencies and lost out to the EUR and GBP. The quant FX Risk Index is currently in the Risk‐Averse Zone and we expect risk to remain elevated in the FX markets as the major currency plays pan out. (i.e. Abenomics, easy monetary policy by the DM, possible action by China).

We maintain our pos itive bias on the dollar index (DXY year‐end target: 85‐87) and we expect the dollar to appreciate against the Yen (weakness to continue though with gradual depreciation), the Euro & the Pound. EM currencies including the INR are expected to

appreciate in the near‐term. The euro will continue to underperform all major currencies (near‐term target: 1.28; year‐end target: 1.22). We expect the AUD to remain weak (year‐end target: 0.65‐0.70) as commodities continue their downtrend.

Overal l H igh Overall Low Current %i le

S&P 500 I NDEX 18.3 3.3 18.3 9.7 73. 1 9.7 46.4%

DOW JONES I NDUS. AVG 16.6 2.9 16.6 8.9 66. 9 8.9 46.7%

RUSSELL 2000 I ND EX 21.2 1.9 21.2 12.5 77. 6 12.5 30.0%

NASDAQ 100 STOCK I ND X 17.4 2.1 17.4 11.4 75. 9 11.4 34.0%

BRAZ IL BOVESPA I ND EX 27.8 5.1 37.1 9.6 103. 1 9.6 64.6%

I SHARES MSCI CANADA 19.9 1.3 20.2 11.2 88. 2 11.2 27.2%

Euro Stoxx 50 Pr 19.1 0.9 28.0 12.4 92. 2 11.5 21.3%

FTSE 100 INDEX 17.9 0.8 20.4 8.5 87. 7 8.5 41.8%

CAC 40 I NDEX 23.0 3.2 24.2 12.5 92. 5 12.5 52.2%

DAX I NDEX 19.1 2.5 20.4 11.3 89. 6 11.3 33.5%

FTSE MIB I NDEX 23.6 1.2 32.9 18.8 87. 6 14.7 36.1%

I SHARES MSCI SPAIN I NDEX FD 26.8 1.4 34.2 20.1 72. 8 17.8 17.2%

AEX‐ I ndex 16.7 0.4 18.3 9.7 104. 8 9.7 28.0%

OMX STOCKHOLM 30 I ND EX 20.1 (2.7) 32.3 10.3 89. 8 10.3 33.4%

SWI SS MARKET INDEX 18.5 0.8 19.8 8.3 80. 6 8.3 60.1%

N IKKEI 225 36.2 (2.4) 51.2 15.6 109. 6 11.6 87.6%

TOPIX I ND EX (TOKYO) 35.7 8.2 42.3 17.4 96. 1 10.4 82.9%

HANG SENG I NDEX 21.0 1.8 21.6 9.9 133. 4 9.9 44.3%

HANG SENG CH INA ENT I NDX 31.0 6.6 32.8 14.6 128. 9 14.6 56.4%

TAIWAN TAI EX I ND EX 14.9 (0.0) 15.6 10.1 72. 1 10.1 15.4%

KOSPI 200 I ND EX 15.1 (1.2) 21.4 11.5 100. 2 11.5 11.3%

S&P/ASX 200 I ND EX 17.5 1.4 17.7 8.8 76. 3 8.7 42.0%

NSE S&P CNX NI FTY INDEX 18.3 1.5 18.3 11.6 89. 7 11.6 28.7%

I SHARES MSCI EMERGING MKT IN 28.7 6.0 28.7 12.5 121. 7 12.5 49.1%

Since January 2008Index

1m Im pli ed Vol (Current)

Chg (1w)

2013 High

2013 Low

Current

1M Imp Vol

SPX Index S&P 500 INDEX 18.3 3.3 12.5 80% 20.9 (11.06)

INDU Index DOW JONES INDUS. AVG 16.6 2.9 11.5 85% 21.6 (0.03)

RTY Index RUSSEL L 2000 INDEX 21.2 1.9 12.6 85% 19.7 (13.29)

NDX Index NASDAQ 100 STOCK INDX 17.4 2.1 9.5 64% 41.1 (14.31)

IBOV I ndex BRAZIL IBOVESPA INDEX 27.8 5.1 (0.0) 38% 40.2 (3.00)

SX5E Index Euro Stoxx 50 Pr 19.1 0.9 4.1 7% 18.3 (10.95)

UKX Index FTSE 100 INDEX 17.9 0.8 2.8 4% 18.1 (22.49)

CAC I ndex CAC 40 INDEX 23.0 3.2 3.8 7% 20.1 (17.16)

DAX Index DAX INDEX 19.1 2.5 5.7 10% 17.1 (10.60)

FTSEMIB Index FTSE MIB INDEX 23.6 1.2 5.1 15% 16.5 (16.12)

AEX Index A EX‐Index 16.7 0.4 2.4 6% 18.5 (22.32)

OMX I ndex OMX STOCKHOLM 30 INDEX 20.1 (2.7) 3.6 12% 38.0 (68.58)

SMI Index SWISS MARKET INDEX 18.5 0.8 5.4 15% 16.7 (0.42)

NKY I ndex NIKKEI 225 36.2 (2.4) 5.0 41% 24.7 (25.79)

TPX Index TOPIX INDEX (TOKYO) 35.7 8.2 (1.2) 34% 28.4 (25.78)

HSI Index HANG SENG INDEX 21.0 1.8 (3.6) 0% 20.7 (22.36)

HSCEI I ndex HANG SENG CHINA ENT INDX 31.0 6.6 (3.1) 1% 16.7 (27.20)

TWSE Index TAIWAN TAIEX INDEX 14.9 (0.0) 4.1 20% 18.2 (32.37)

KOSPI2 I ndex KOSPI 200 INDEX 15.1 (1.2) (3.1) 1% 25.0 (9.77)

AS51 I ndex S&P/ASX 200 INDEX 17.5 1.4 6.4 44% 18.0 (19.78)

NIFTY Index NSE CNX NIFTY INDEX 18.3 1.5 4.6 26% 15.0 (0.66)

MinTicker IndexChg

(1w )

Current

%i leMax

Current 1M

90‐110 Skew

(4 .0 )

(2 .0 )

0.0

2.0

4.0

6.0

8.0

10.0

OMX

NKY

KOSPI2

TWSE

AEX

UKX SMI

SX5E

FTSEMIB

EWC US

EWP US

AS51

NIFTY

H.SI

RTY

NDX

DAX IN

DEX

INDU CAC

SPX

IBOV

EEM US

HSCEI

TPX

Change in 1m Implied Vol

(12.0)

(10.0)

(8 .0)

(6 .0)

(4 .0)

(2 .0)

0.0

2.0

4.0

6.0

HSI.

TPX

KOSPI2

HSCEI

NKY

AS51

UKX

AEX

SX5E

CAC

OMX

IBOV

SMI

DAX

NIFTY

TWSE

RTY

FTSEMIB

INDU

NDX

SPX

Change in 1m Skew

June 2013 6

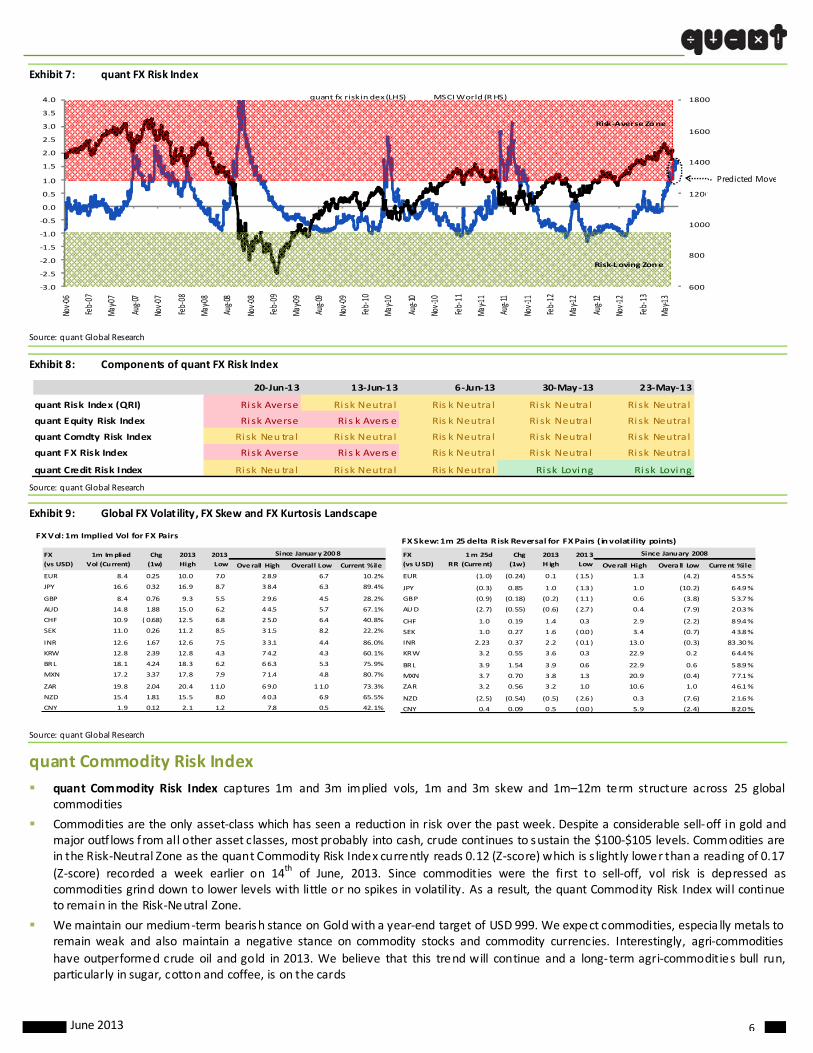

Exhibit 7: quant FX Risk Index

Source: quant Global Research

Exhibit 8: Components of quant FX Risk Index

Source: quant Global Research

Exhibit 9: Global FX Volat ility, FX Skew and FX Kurtosis Landscape

Source: quant Global Research

quant Commodity Risk Index

quant Commodity Risk Index captures 1m and 3m implied vols, 1m and 3m skew and 1m–12m term structure across 25 global commodities

Commodities are the only asset‐class which has seen a reduction in risk over the past week. Despite a considerable sell‐off in gold and major outf lows from all other asset classes, most probably into cash, crude continues to sustain the $100‐$105 levels. Commodities are in the Risk‐Neutral Zone as the quant Commodity Risk Index currently reads 0.12 (Z‐score) which is s lightly lower than a reading of 0.17

(Z‐score) recorded a week earlier on 14th of June, 2013. Since commodities were the first to sell‐off, vol risk is depressed as commodities grind down to lower levels with little or no spikes in volatility. As a result, the quant Commodity Risk Index will continue to remain in the Risk‐Neutral Zone.

We maintain our medium ‐term bearish stance on Gold with a year‐end target of USD 999. We expect commodities, especia lly metals to remain weak and also maintain a negative stance on commodity stocks and commodity currencies. Interestingly, agri‐commodities

have outperformed crude oil and gold in 2013. We believe that this trend will continue and a long‐term agri‐commodities bull run, particularly in sugar, cotton and coffee, is on the cards

600

800

1000

1200

1400

1600

1800

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Nov‐06

Feb‐07

May‐07

Aug‐07

Nov‐07

Feb‐08

May‐08

Aug‐08

Nov‐08

Feb‐09

May‐09

Aug‐09

Nov‐09

Feb‐10

May‐10

Aug‐10

Nov‐10

Feb‐11

May‐11

Aug‐11

Nov‐11

Feb‐12

May‐12

Aug‐12

Nov‐12

Feb‐13

May‐13

quant fx risk in dex (LHS) MSCI World (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

20‐Jun‐13 13‐Jun‐13 6‐Jun‐13 30‐May ‐13 23‐May‐13

quant Risk Index (QRI) Ri sk Averse Ri sk Neutra l Ris k Neutra l Ri sk Neutra l Ri sk Neutra l

quant Equity Risk Index Ri sk Averse Ri s k Avers e Ris k Neutra l Ri sk Neutra l Ri sk Neutra l

quant Comdty Risk Index Ri sk Neu tra l Ri sk Neutra l Ris k Neutra l Ri sk Neutra l Ri sk Neutra l

quant FX Risk Index Ri sk Averse Ri s k Avers e Ris k Neutra l Ri sk Neutra l Ri sk Neutra l

quant Credit Risk Index Ri sk Neu tra l Ri sk Neutra l Ris k Neutra l Ri sk Loving Ri sk Loving

FX Vol: 1m Implied Vol for FX Pairs

Ove rall High Overall Low Current %ile

EUR 8.4 0.25 10.0 7.0 28.9 6.7 10.2%

JPY 16.6 0.32 16.9 8.7 38.4 6.3 89.4%

GBP 8.4 0.76 9.3 5.5 29.6 4.5 28.2%

AUD 14.8 1.88 15.0 6.2 44.5 5.7 67.1%

CHF 10.9 ( 0.68) 12.5 6.8 25.0 6.4 40.8%

SEK 11.0 0.26 11.2 8.5 31.5 8.2 22.2%

INR 12.6 1.67 12.6 7.5 33.1 4.4 86.0%

KRW 12.8 2.39 12.8 4.3 74.2 4.3 60.1%

BRL 18.1 4.24 18.3 6.2 66.3 5.3 75.9%

MXN 17.2 3.37 17.8 7.9 71.4 4.8 80.7%

ZAR 19.8 2.04 20.4 11.0 69.0 11.0 73.3%

NZD 15.4 1.81 15.5 8.0 40.3 6.9 65.5%

CNY 1.9 0.12 2.1 1.2 7.8 0.5 42.1%

Since January 2008FX

(vs USD)

1m Implied

Vol (Current)

Chg

(1w)

2013

High

2013

Low

FX Skew: 1m 25 delta Risk Reversal for FX Pairs ( in volatility points)

Overall High Overa ll Low Current %ile

EUR (1.0) (0.24) 0 .1 ( 1.5 ) 1.3 (4.2) 45.5%

JPY (0.3) 0.85 1 .0 ( 1.3 ) 1.0 (10.2) 64.9%

GBP (0.9) (0.18) (0 .2) ( 1.1 ) 0.6 (3.8) 53.7%

AUD (2.7) (0.55) (0 .6) ( 2.7 ) 0.4 (7.9) 20.3%

CHF 1.0 0.19 1 .4 0.3 2.9 (2.2) 89.4%

SEK 1.0 0.27 1 .6 ( 0.0 ) 3.4 (0.7) 43.8%

INR 2.23 0.37 2 .2 ( 0.1 ) 13.0 (0.3) 83 .30%

KRW 3.2 0.55 3 .6 0.3 22.9 0.2 64.4%

BRL 3.9 1.54 3 .9 0.6 22.9 0.6 58.9%

MXN 3.7 0.70 3 .8 1.3 20.9 (0.4) 77.1%

ZAR 3.2 0.56 3 .2 1.0 10.6 1.0 46.1%

NZD (2.5) (0.54) (0 .5) ( 2.6 ) 0.3 (7.6) 21.6%

CNY 0.4 0.09 0 .5 ( 0.0 ) 5.9 (2.4) 82.0%

Since January 2008FX

(vs USD)

1m 25d

RR (Current)

Chg

(1w)

2013

H igh

2013

Low

Predicted Move

June 2013 7

Exhibit 10: quant Commodity Risk Index

Source: quant Global Research

Exhibit 11: Components of quant Commodity Risk Index

Source: quant Global Research

Exhibit 12: Global Commodity Volatility Landscape

Source: quant Global Research

600

800

1000

1200

1400

1600

1800

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

Nov‐06

Feb‐07

May‐07

Aug‐07

Nov‐07

Feb‐08

May‐08

Aug‐08

Nov‐08

Feb‐09

May‐09

Aug‐09

Nov‐09

Feb‐10

May‐10

Aug‐10

Nov‐10

Feb‐11

May‐11

Aug‐11

Nov‐11

Feb‐12

May‐12

Aug‐12

Nov‐12

Feb‐13

May‐13

quan t comdty risk index (LHS) MSCI World (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

20‐Jun‐13 13‐Jun‐13 6‐Jun‐13 30‐May‐13 23‐May‐13

quant Comdty Risk Index Ri sk Neutral Ri sk Neutral Ri sk Neutra l Ri sk Neutra l Ri sk Neutra l

quant Comdty Vol Index Ri sk Neutral Ri sk Neutral Ri sk Neutra l Ri sk Neutra l Ri sk Neutra l

quant Comdty Skew Index Ri sk Neutral Ri sk Averse Ris k Averse Ris k Averse Ris k Averse

quant Comdty Term Structure Index Ri sk Neutral Ri sk Neutral Ris k Averse Ris k Averse Ris k Averse

Oil and Metals 1m Implied Vol

Soft Commodities 1m Implied VolSoft Commodities 1m Implied Vol Change in one week

Oil and Metals 1m Implied Vol Change in one week

Overall

High

Overall

Low

Current

%ile

WTI CRUDE FUTURE Aug13 21.5 3.0 29.4 16.4 100.4 16.4 5.5%

BRENT CRUDE FU TR Aug13 21.9 2.9 27.2 13.6 105.3 13.6 8.1%

GASOLINE RBOB FUT Ju l13 21.9 0.8 28.2 17.3 109.2 17.3 3.7%

NY Ha rb ULSD Fu t Jul13 18.8 1.2 25.5 15.8 79.4 15.8 4.4%

GAS OIL FUT (ICE ) Aug13 17.2 (0 .9) 25.6 14.2 104.4 14.2 2.4%

NATURAL GAS FU TR Ju l13 27.3 (1 .7) 36.7 27.0 160.7 27.0 0.0%

ICE NAT GAS FUT R Ju l13 15.8 (0 .2) 23.5 14.3 46.9 14.3 6.3%

GOLD 100 OZ FUTR Aug13 26.4 8.1 40.3 10.3 63.3 10.3 83.4%

SILVER FUTURE Ju l13 41.4 1 1.4 55.6 18.5 93.1 18.5 76.0%

PLATINUM FUTU RE Jul13 22.0 0.3 26.1 13.9 66.0 13.9 45.6%

PALLADIUM FUTU RE Se p13 31.4 2.0 31.4 17.4 109.5 16.2 54.0%

COPPER FUTURE Se p13 27.4 4.7 27.4 15.6 97.9 15.6 36.4%

Since Ja nuary 20082 013

LowIndex

1m Implied

Vol (Current)

Chg

(1w)

2013

High

(4.0 )

(2.0 )

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Natural Gas

Gas O

il

Natural Gas (ICE

)

Platinum

Gasolin

e

Heating Oil

Palladium

Bren

t Crude

WTI Crude

Copp

er

Gold

Silver

1m Imp lied Vol Change

(4.0 )

(2.0 )

0.0

2.0

4.0

6.0

8.0

10.0

Cotton

Rough Rice

Coffe

e

Cattle Fe

eder

Lean

Hog

s

Live

Cattle

Cocoa

Soybea

n Oil

Sugar

Soybea

n Mea

l

Soyb

ean

Palm

Oil

Whe

at

Corn

1m Impl ied Vol ChangeOveral l Overal l Current

CORN FUTURE Dec13 36.8 8.9 36.8 17.3 62.1 17.1 55.2%

WHEAT FUTURE(CBT) Sep13 29.1 5.8 30.6 22.1 79.2 19.3 15.4%

SOYBEAN FUTURE Nov13 24.4 2.4 24.7 15.8 61.7 15.8 43.2%

SOYBEAN MEAL FUTR Dec13 30.1 2.0 30.1 21.0 54.6 16.4 60.8%

ROUGH RICE (CBOT) Sep13 17.0 (1.4) 20.7 9.0 63.8 9.0 15.2%

CRUDE PALM OIL FU Sep13 14.3 2.9 70.9 11.3 93.9 11.3 1.7%

SOYBEAN OIL FUTR Dec13 18.0 1.3 21.1 15.8 64.4 15.8 9.3%

COFFEE 'C' FUTURE Sep13 25.0 (1.1) 34.0 20.6 52.3 20.6 6.0%

SUGAR #11 (WORLD ) Oct13 19.1 1.6 24.4 16.0 67.2 16.0 2.6%

COTTON NO.2 FUTR Dec13 21.8 (2.8) 39.3 19.2 82.8 16.7 4.8%

COCOA FUTURE Sep13 22.3 0.4 27.9 19.9 55.4 19.9 3.9%

L IVE CATTLE FUTR Aug13 10.7 (0.1) 13.2 9.3 29.8 9.2 5.6%

CATTLE FEEDER FUT Aug13 10.3 (0.3) 14.1 7.4 27.7 6.4 14.7%

LEAN HOGS FUTURE Aug13 16.8 (0.2) 19.5 8.2 46.3 6.1 21.1%

Sinc e January 2008Index

1m Impli ed

Vol (Current)

Chg

(1w)

2013

High

2013

Low

Predicted Move

June 2013 8

quant Credit Risk Index

quant Credit Risk Index measures the credit risk as priced by sovereign and corporate CDS (and bond spreads)

The perception of credit worthiness is very important for the smooth functioning of the financial markets. As demonstrated by the global financial crisis, any shock to these perceptions can lead to severe stress in the financial systems. We compute the quant credit risk index using normalized 5 yr CDS spreads for Investment Grade (IG) and High Yield (HY) corporates in the US, Europe, EM and Asia and normalized 5 yr CDS spreads of global sovereigns

Credit spreads have finally deteriorated after the 8‐9 month tightening in spreads of global sovereigns, US and European Investment

Grade (IG) and High Y ield (HY) corporates. The quant Credit Risk Index is currently in the Risk‐Neutral Zone for the firs t time since August 2012 with a reading of 0.11 (Z‐score) as compared to ‐0.41 on the 14th of June, 2013 and we expect it to continue in the Risk‐Neutral Zone albeit with a small march to the upper band as yie lds continue to rise in the High Yie ld, MBS and Treasury markets.

Exhibit 13: quant Credit Risk Index

Source: quant Global Research

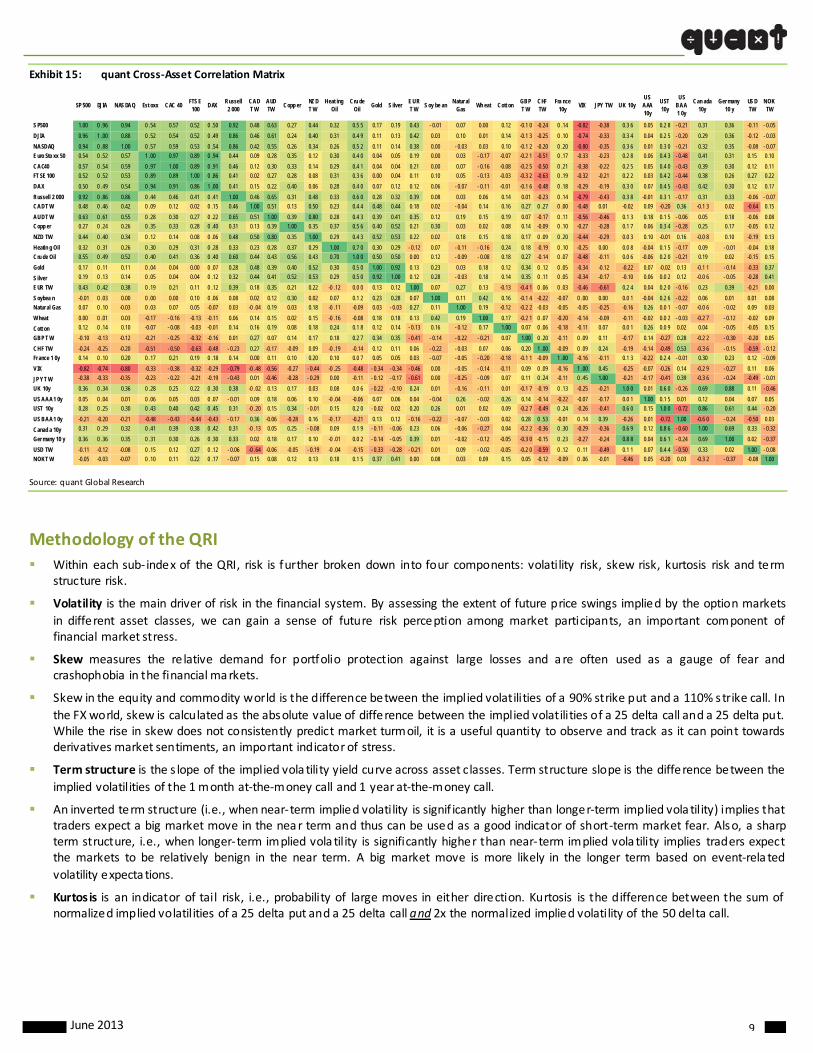

quant Cross‐Asset Correlation Index

As EM equity and bond funds, Global HY bond funds and commodity funds witness heavy outflows, risk assets continue to be under pressure.

Since March 2013, we are seeing firs t signs of RISK ON behavior as a ll assets (including money market funds) are experiencing outflows (most probably into cash). As a result, cross‐asset correla tions are mirroring asset returns as seen by the graph below.

Exhibit 14: quant Cross‐Asset Correlation Index

Source: quant Global Research

600

800

1000

1200

1400

1600

1800

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Nov‐06

Feb‐07

May‐07

Aug‐07

Nov‐07

Feb‐08

May‐08

Aug‐08

Nov‐08

Feb‐09

May‐09

Aug‐09

Nov‐09

Feb‐10

May‐10

Aug‐10

Nov‐10

Feb‐11

May‐11

Aug‐11

Nov‐11

Feb‐12

May‐12

Aug‐12

Nov‐12

Feb‐13

May‐13

quant credit risk index (LHS) MSCI World (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

600

800

1000

1200

1400

1600

1800

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Mar‐06

Jun‐06

Sep‐06

Dec‐06

Mar‐07

Jun‐07

Sep‐07

Dec‐07

Mar‐08

Jun‐08

Sep‐08

Dec‐08

Mar‐09

Jun‐09

Sep‐09

Dec‐09

Mar‐10

Jun‐10

Sep‐10

Dec‐10

Mar‐11

Jun‐11

Sep‐11

Dec‐11

Mar‐12

Jun‐12

Sep‐12

Dec‐12

Mar‐13

Jun‐13

quant Cross‐Asset Correlation Index MSCI World (RHS)

Predicted Move

Signs of RISK ON behavior

June 2013 9

Exhibit 15: quant Cross‐Asset Correlation Matrix

Source: quant Global Research

Methodology of the QRI

Within each sub‐ index of the QRI, risk is further broken down into four components: volatility risk, skew risk, kurtosis risk and term structure risk.

Volatility is the main driver of risk in the financial system. By assessing the extent of future price swings implied by the option markets

in different asset classes, we can gain a sense of future risk perception among market participants, an important component of financial market stress.

Skew measures the re lative demand for portfolio protection against large losses and are often used as a gauge of fear and crashophobia in the financial markets.

Skew in the equity and commodity world is the difference between the implied volatilities of a 90% strike put and a 110% s trike call. In

the FX world, skew is calculated as the absolute value of difference between the implied volatilities of a 25 delta call and a 25 delta put. While the rise in skew does not consistently predict market turmoil, it is a useful quantity to observe and track as it can point towards derivatives market sentiments, an important indicator of stress.

Term structure is the s lope of the implied vola tility yield curve across asset classes. Term structure slope is the difference between the

implied volatilities of the 1 month at‐the‐money call and 1 year at‐the‐money call.

An inverted term structure (i.e., when near‐term implied volatility is signif icantly higher than longer‐term implied vola tility) implies that traders expect a big market move in the near term and thus can be used as a good indicator of short‐term market fear. Also, a sharp term structure, i.e., when longer‐term implied vola tility is significantly higher than near‐term implied vola tility implies traders expect the markets to be relatively benign in the near term. A big market move is more likely in the longer term based on event‐rela ted

volatility expecta tions.

Kurtosis is an indicator of tail risk, i.e., probability of large moves in either direction. Kurtosis is the difference between the sum of normalized implied volatilities of a 25 delta put and a 25 delta call and 2x the normalized implied volatility of the 50 delta call.

SP 500 DJIA NAS DAQ Est oxx CAC 40FTS E 100

DAXRussell 2 000

CAD T W

AUD TW

Copp erNZ D T W

Heat ing Oil

Cru de Oil

Gold S ilverE UR T W

S oy be anNatur al

GasWh eat Cott on

GBP T W

CHF TW

Fra nce 10y

VIX JPY TW UK 10yUS AAA 10y

UST 10y

US BAA 1 0y

Can ada 10y

Ger many 10 y

US D TW

NOK TW

S P500 1.00 0 .96 0.94 0 .54 0.57 0.52 0 .50 0.92 0.48 0.63 0.27 0.44 0.32 0.5 5 0.17 0.19 0.43 - 0.01 0.07 0.00 0.12 -0.1 0 -0.24 0 .14 -0.82 -0.38 0.3 6 0.05 0.2 8 - 0.21 0.31 0.36 -0.11 - 0.05

DJIA 0.96 1 .00 0.88 0 .52 0.54 0.52 0 .49 0.86 0.46 0.61 0.24 0.40 0.31 0.4 9 0.11 0.13 0.42 0.03 0.10 0.01 0.14 -0.1 3 -0.25 0 .10 -0.74 -0.33 0.3 4 0.04 0.2 5 - 0.20 0.29 0.36 -0.12 - 0.03

NASDAQ 0.94 0 .88 1.00 0 .57 0.59 0.53 0 .54 0.86 0.42 0.55 0.26 0.34 0.26 0.5 2 0.11 0.14 0.38 0.00 - 0.03 0.03 0.10 -0.1 2 -0.20 0 .20 -0.80 -0.35 0.3 6 0.01 0.3 0 - 0.21 0.32 0.35 -0.08 - 0.07

E uro Sto xx 50 0.54 0 .52 0.57 1 .00 0.97 0.89 0 .94 0.44 0.09 0.28 0.35 0.12 0.30 0.4 0 0.04 0.05 0.19 0.00 0.03 - 0.17 -0.07 -0.2 1 -0.51 0 .17 -0.33 -0.23 0.2 8 0.06 0.4 3 - 0.48 0.41 0.31 0.15 0.10

CAC40 0.57 0 .54 0.59 0 .97 1.00 0.89 0 .91 0.46 0.12 0.30 0.33 0.14 0.29 0.4 1 0.04 0.04 0.21 0.00 0.07 - 0.16 -0.08 -0.2 5 -0.50 0 .21 -0.38 -0.22 0.2 5 0.05 0.4 0 - 0.43 0.39 0.30 0.12 0.11

FT SE 100 0.52 0 .52 0.53 0 .89 0.89 1.00 0 .86 0.41 0.02 0.27 0.28 0.08 0.31 0.3 6 0.00 0.04 0.11 0.10 0.05 - 0.13 -0.03 -0.3 2 -0.63 0 .19 -0.32 -0.21 0.2 2 0.03 0.4 2 - 0.44 0.38 0.26 0.27 0.22

DAX 0.50 0 .49 0.54 0 .94 0.91 0.86 1 .00 0.41 0.15 0.22 0.40 0.06 0.28 0.4 0 0.07 0.12 0.12 0.06 - 0.07 - 0.11 -0.01 -0.1 6 -0.48 0 .18 -0.29 -0.19 0.3 0 0.07 0.4 5 - 0.43 0.42 0.30 0.12 0.17

Russell 2 000 0.92 0 .86 0.86 0 .44 0.46 0.41 0 .41 1.00 0.46 0.65 0.31 0.48 0.33 0.6 0 0.28 0.32 0.39 0.08 0.03 0.06 0.14 0.01 -0.23 0 .14 -0.79 -0.43 0.3 8 -0.01 0.3 1 - 0.17 0.31 0.33 -0.06 - 0.07

CAD T W 0.48 0 .46 0.42 0 .09 0.12 0.02 0 .15 0.46 1.00 0.51 0.13 0.50 0.23 0.4 4 0.48 0.44 0.18 0.02 - 0.04 0.14 0.16 0.27 0 .27 0 .00 -0.48 0.01 -0.02 0.09 -0.20 0.36 -0.1 3 0.02 -0.64 0.15

AUD T W 0.63 0 .61 0.55 0 .28 0.30 0.27 0 .22 0.65 0.51 1.00 0.39 0.80 0.28 0.4 3 0.39 0.41 0.35 0.12 0.19 0.15 0.19 0.07 -0.17 0 .11 -0.56 -0.46 0.1 3 0.18 0.1 5 - 0.06 0.05 0.18 -0.06 0.08

Copp er 0.27 0 .24 0.26 0 .35 0.33 0.28 0 .40 0.31 0.13 0.39 1.00 0.35 0.37 0.5 6 0.40 0.52 0.21 0.30 0.03 0.02 0.08 0.14 -0.09 0 .10 -0.27 -0.28 0.1 7 0.06 0.3 4 - 0.28 0.25 0.17 -0.05 0.12

NZD TW 0.44 0 .40 0.34 0 .12 0.14 0.08 0 .06 0.48 0.50 0.80 0.35 1.00 0.29 0.4 3 0.52 0.53 0.22 0.02 0.18 0.15 0.18 0.17 0 .09 0 .20 -0.44 -0.29 0.0 3 0.10 -0.01 0.16 -0.0 8 0.10 -0.19 0.13

Heatin g Oil 0.32 0 .31 0.26 0 .30 0.29 0.31 0 .28 0.33 0.23 0.28 0.37 0.29 1.00 0.7 0 0.30 0.29 - 0.12 0.07 - 0.11 - 0.16 0.24 0.18 -0.19 0 .10 -0.25 0.00 0.0 8 -0.04 0.1 5 - 0.17 0.09 - 0.01 -0.04 0.18

Cru de Oil 0.55 0 .49 0.52 0 .40 0.41 0.36 0 .40 0.60 0.44 0.43 0.56 0.43 0.70 1.0 0 0.50 0.50 0.00 0.12 - 0.09 - 0.08 0.18 0.27 -0.14 0 .07 -0.48 -0.11 0.0 6 -0.06 0.2 0 - 0.21 0.19 0.02 -0.15 0.15

Gold 0.17 0 .11 0.11 0 .04 0.04 0.00 0 .07 0.28 0.48 0.39 0.40 0.52 0.30 0.5 0 1.00 0.92 0.13 0.23 0.03 0.18 0.12 0.34 0 .12 0 .05 -0.34 -0.12 -0.22 0.07 -0.02 0.13 -0.1 1 - 0.14 -0.33 0.37

S ilver 0.19 0 .13 0.14 0 .05 0.04 0.04 0 .12 0.32 0.44 0.41 0.52 0.53 0.29 0.5 0 0.92 1.00 0.12 0.28 - 0.03 0.18 0.14 0.35 0 .11 0 .05 -0.34 -0.17 -0.10 0.06 0.0 2 0.12 -0.0 6 - 0.05 -0.28 0.41

E UR TW 0.43 0 .42 0.38 0 .19 0.21 0.11 0 .12 0.39 0.18 0.35 0.21 0.22 -0 .12 0.0 0 0.13 0.12 1.00 0.07 0.27 0.13 -0.13 -0.4 1 0 .06 0 .03 -0.46 -0.61 0.2 4 0.04 0.2 0 - 0.16 0.23 0.39 -0.21 0.00

S oybea n -0.01 0 .03 0.00 0 .00 0.00 0.10 0 .06 0.08 0.02 0.12 0.30 0.02 0.07 0.1 2 0.23 0.28 0.07 1.00 0.11 0.42 0.16 -0.1 4 -0.22 -0.07 0 .00 0.00 0.0 1 -0.04 0.2 6 - 0.22 0.06 0.01 0.01 0.08

Natur al Gas 0.07 0 .10 -0.03 0 .03 0.07 0.05 -0.07 0.03 -0 .04 0.19 0.03 0.18 -0 .11 -0.09 0.03 - 0.03 0.27 0.11 1.00 0.19 -0.12 -0.2 2 -0.03 -0.05 -0.05 -0.25 -0.16 0.26 0.0 1 - 0.07 -0.0 6 - 0.02 0.09 0.03

Wheat 0.00 0 .01 0.03 -0.17 - 0.16 -0.13 -0.11 0.06 0.14 0.15 0.02 0.15 -0 .16 -0.08 0.18 0.18 0.13 0.42 0.19 1.00 0.17 -0.2 1 0 .07 -0.20 -0.14 -0.09 -0.11 -0.02 0.0 2 - 0.03 -0.2 7 - 0.12 -0.02 0.09

Cott on 0.12 0 .14 0.10 -0.07 - 0.08 -0.03 -0.01 0.14 0.16 0.19 0.08 0.18 0.24 0.1 8 0.12 0.14 - 0.13 0.16 - 0.12 0.17 1.00 0.07 0 .06 -0.18 -0.11 0.07 0.0 1 0.26 0.0 9 0.02 0.04 - 0.05 -0.05 0.15

GBP T W -0.10 -0.13 -0.12 -0.21 - 0.25 -0.32 -0.16 0.01 0.27 0.07 0.14 0.17 0.18 0.2 7 0.34 0.35 - 0.41 - 0.14 - 0.22 - 0.21 0.07 1.00 0 .20 -0.11 0 .09 0.11 -0.17 0.14 -0.27 0.28 -0.2 2 - 0.30 -0.20 0.05

CHF TW -0.24 -0.25 -0.20 -0.51 - 0.50 -0.63 -0.48 - 0.23 0.27 -0.17 -0.09 0.09 -0 .19 -0.14 0.12 0.11 0.06 - 0.22 - 0.03 0.07 0.06 0.20 1 .00 -0.09 0 .09 0.24 -0.19 -0.14 -0.49 0.53 -0.3 6 - 0.15 -0.59 - 0.12

Fr ance 1 0y 0.14 0 .10 0.20 0 .17 0.21 0.19 0 .18 0.14 0.00 0.11 0.10 0.20 0.10 0.0 7 0.05 0.05 0.03 - 0.07 - 0.05 - 0.20 -0.18 -0.1 1 -0.09 1 .00 -0.16 -0.11 0.1 3 -0.22 0.2 4 - 0.01 0.30 0.23 0.12 - 0.09

V IX -0.82 -0.74 -0.80 -0.33 - 0.38 -0.32 -0.29 - 0.79 -0 .48 -0.56 -0.27 - 0.44 -0 .25 -0.48 - 0.34 - 0.34 - 0.46 0.00 - 0.05 - 0.14 -0.11 0.09 0 .09 -0.16 1 .00 0.45 -0.25 -0.07 -0.26 0.14 -0.2 9 - 0.27 0.11 0.06

JP Y T W -0.38 -0.33 -0.35 -0.23 - 0.22 -0.21 -0.19 - 0.43 0.01 -0.46 -0.28 - 0.29 0.00 -0.11 - 0.12 - 0.17 - 0.61 0.00 - 0.25 - 0.09 0.07 0.11 0 .24 -0.11 0 .45 1.00 -0.21 -0.17 -0.41 0.39 -0.3 6 - 0.24 -0.49 - 0.01

UK 10y 0.36 0 .34 0.36 0 .28 0.25 0.22 0 .30 0.38 -0 .02 0.13 0.17 0.03 0.08 0.0 6 - 0.22 - 0.10 0.24 0.01 - 0.16 - 0.11 0.01 -0.1 7 -0.19 0 .13 -0.25 -0.21 1.0 0 0.01 0.6 0 - 0.26 0.69 0.88 0.11 - 0.46

US AAA 1 0y 0.05 0 .04 0.01 0 .06 0.05 0.03 0 .07 - 0.01 0.09 0.18 0.06 0.10 -0 .04 -0.06 0.07 0.06 0.04 - 0.04 0.26 - 0.02 0.26 0.14 -0.14 -0.22 -0.07 -0.17 0.0 1 1.00 0.1 5 0.01 0.12 0.04 0.07 0.05

UST 10y 0.28 0 .25 0.30 0 .43 0.40 0.42 0 .45 0.31 -0 .20 0.15 0.34 - 0.01 0.15 0.2 0 - 0.02 0.02 0.20 0.26 0.01 0.02 0.09 -0.2 7 -0.49 0 .24 -0.26 -0.41 0.6 0 0.15 1.0 0 - 0.72 0.86 0.61 0.44 - 0.20

US BAA 1 0y -0.21 -0.20 -0.21 -0.48 - 0.43 -0.44 -0.43 - 0.17 0.36 -0.06 -0.28 0.16 -0 .17 -0.21 0.13 0.12 - 0.16 - 0.22 - 0.07 - 0.03 0.02 0.28 0 .53 -0.01 0 .14 0.39 -0.26 0.01 -0.72 1.00 -0.6 0 - 0.24 -0.50 0.03

Canad a 10y 0.31 0 .29 0.32 0 .41 0.39 0.38 0 .42 0.31 -0 .13 0.05 0.25 - 0.08 0.09 0.1 9 - 0.11 - 0.06 0.23 0.06 - 0.06 - 0.27 0.04 -0.2 2 -0.36 0 .30 -0.29 -0.36 0.6 9 0.12 0.8 6 - 0.60 1.00 0.69 0.33 - 0.32

Ger many 10 y 0.36 0 .36 0.35 0 .31 0.30 0.26 0 .30 0.33 0.02 0.18 0.17 0.10 -0 .01 0.0 2 - 0.14 - 0.05 0.39 0.01 - 0.02 - 0.12 -0.05 -0.3 0 -0.15 0 .23 -0.27 -0.24 0.8 8 0.04 0.6 1 - 0.24 0.69 1.00 0.02 - 0.37

USD TW -0.11 -0.12 -0.08 0 .15 0.12 0.27 0 .12 - 0.06 -0 .64 -0.06 -0.05 - 0.19 -0 .04 -0.15 - 0.33 - 0.28 - 0.21 0.01 0.09 - 0.02 -0.05 -0.2 0 -0.59 0 .12 0 .11 -0.49 0.1 1 0.07 0.4 4 - 0.50 0.33 0.02 1.00 - 0.08

NOK T W -0.05 -0.03 -0.07 0 .10 0.11 0.22 0 .17 - 0.07 0.15 0.08 0.12 0.13 0.18 0.1 5 0.37 0.41 0.00 0.08 0.03 0.09 0.15 0.05 -0.12 -0.09 0 .06 -0.01 -0.46 0.05 -0.20 0.03 -0.3 2 - 0.37 -0.08 1.00

June 2013 10

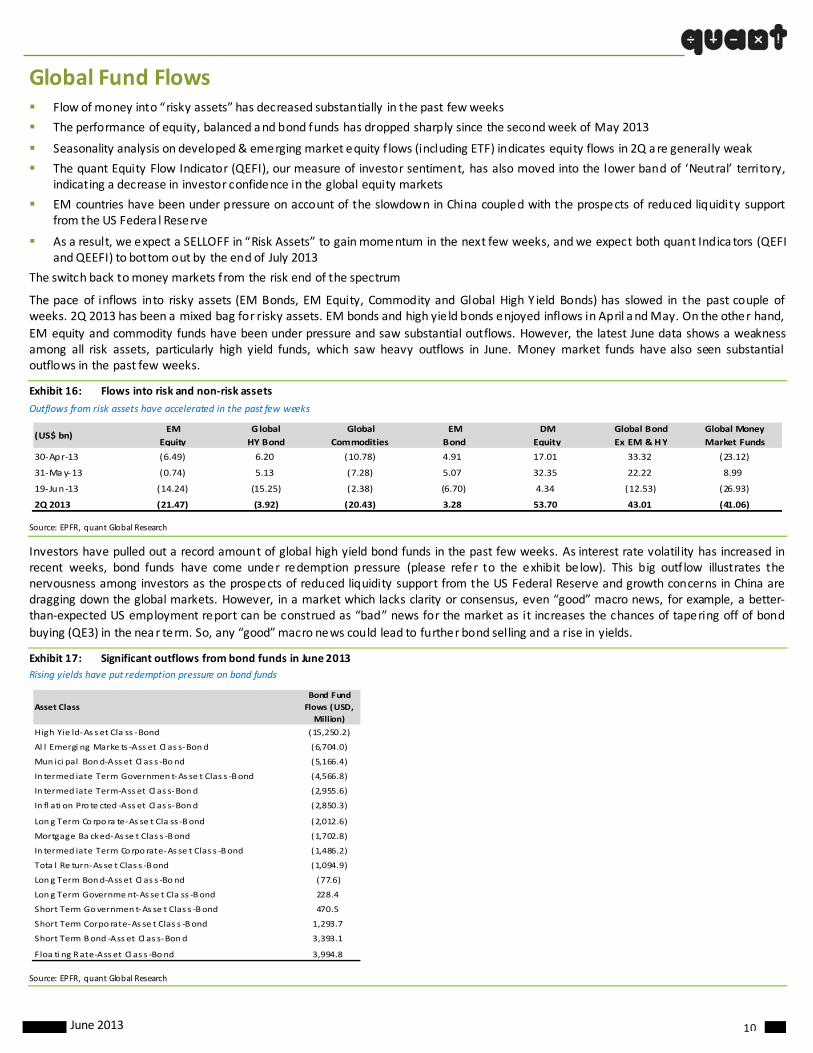

Global Fund Flows Flow of money into “risky assets” has decreased substantially in the past few weeks

The performance of equity, balanced and bond funds has dropped sharply since the second week of May 2013

Seasonality analysis on developed & emerging market equity f lows (including ETF) indicates equity flows in 2Q are generally weak

The quant Equity Flow Indicator (QEFI), our measure of investor sentiment, has also moved into the lower band of ‘Neutral’ territory, indicating a decrease in investor confidence in the global equity markets

EM countries have been under pressure on account of the slowdown in China coupled with the prospects of reduced liquidity support from the US Federa l Reserve

As a result, we expect a SELLOFF in “Risk Assets” to gain momentum in the next few weeks, and we expect both quant Indica tors (QEFI and QEEFI) to bottom out by the end of July 2013

The switch back to money markets from the risk end of the spectrum

The pace of inflows into risky assets (EM Bonds, EM Equity, Commodity and Global High Y ield Bonds) has slowed in the past couple of weeks. 2Q 2013 has been a mixed bag for risky assets. EM bonds and high yie ld bonds enjoyed inflows in April and May. On the other hand,

EM equity and commodity funds have been under pressure and saw substantial outflows. However, the latest June data shows a weakness among all risk assets, particularly high yield funds, which saw heavy outflows in June. Money market funds have also seen substantial outflows in the past few weeks.

Exhibit 16: Flows into risk and non‐risk assets

Outflows from risk assets have accelerated in the past few weeks

Source: EPFR, quant Global Research

Investors have pulled out a record amount of global high yield bond funds in the past few weeks. As interest rate volatility has increased in recent weeks, bond funds have come under redemption pressure (please refer to the exhibit below). This big outf low illustrates the nervousness among investors as the prospects of reduced liquidity support from the US Federal Reserve and growth concerns in China are dragging down the global markets. However, in a market which lacks clarity or consensus, even “good” macro news, for example, a better‐than‐expected US employment report can be construed as “bad” news for the market as it increases the chances of tapering off of bond

buying (QE3) in the near term. So, any “good” macro news could lead to further bond selling and a rise in yields.

Exhibit 17: Significant outflows from bond funds in June 2013

Rising yields have put redemption pressure on bond funds

Source: EPFR, quant Global Research

(US$ bn)EM

Equity

Global

HY Bond

Global

Commodities

EM

Bond

DM

Equity

Global Bond

Ex EM & HY

Global Money

Market Funds

30‐Apr‐13 (6.49) 6.20 (10.78) 4.91 17.01 33.32 (23.12)

31‐May‐13 (0.74) 5.13 (7.28) 5.07 32.35 22.22 8.99

19‐Jun ‐13 (14.24) (15.25) (2.38) (6.70) 4.34 (12.53) (26.93)

2Q 2013 (21.47) (3.92) (20.43) 3.28 53.70 43.01 (41.06)

Asset Class

Bond Fund

Flows (USD,

Million)

High Yie ld‐As s et Cla ss ‐Bond (15,250.2)

Al l Emergi ng Marke ts ‐Ass et Cl as s‐Bond (6,704.0)

Mun ici pal Bond‐Ass et Cl as s ‐Bond (5,166.4)

In termed iate Term Governmen t‐As se t Clas s ‐Bond (4,566.8)

In termed iate Term‐Ass et Cl as s‐Bond (2,955.6)

In fl ati on Pro te cted ‐Ass et Cl as s‐Bond (2,850.3)

Lon g Term Co rpo ra te‐As se t Cla ss ‐Bond (2,012.6)

Mortgage Ba cked‐As se t Clas s ‐Bond (1,702.8)

In termed iate Term Co rpo rate‐As se t Clas s ‐Bond (1,486.2)

Tota l Re turn‐As se t Clas s ‐Bond (1,094.9)

Lon g Term Bond‐Ass et Cl as s ‐Bond (77.6)

Lon g Term Governme nt‐As se t Cla ss ‐Bond 228.4

Short Term Governmen t‐As se t Clas s ‐Bond 470.5

Short Term Corpo rate‐As se t Clas s ‐Bond 1,293.7

Short Term Bond ‐Ass et Cl as s‐Bond 3,393.1

Floa ti ng Rate‐Ass et Cl as s ‐Bond 3,994.8

June 2013 11

The performance of equity, balanced and bond funds has dropped sharply s ince the second week of May 2013. Equity funds NAV has corrected by 2.8% since 8 May whereas bond and balanced funds have corrected by 3% each during the same period. Talks on “tapering

off” of US Fed’s QE program has driven up bond yields and caused s ignificant losses to bond investors.

Exhibit 18: EPFR survey of performance of fund managers in different asset classes

Performance of equity and bond funds has dropped sharply

Source: EPFR, quant Global Research

We think it is important to highlight this turning point as there is some degree of nervousness among bond and equity investors. We are

already seeing a weakness in select emerging markets like Brazil, India, China and Russia, even as investors grapple with concerns of continued l iquidity flows. Emerging market funds, both equities and bonds, are particularly under sharp redemption pressure. In the past four weeks, dedicated EM equity funds have seen outf lows of USD 17.1 billion, with GEM and Asia Ex Japan funds seeing outflows of USD 9.9 billion and USD 5.1 billion, respectively. EM bond funds have also seen outflows of USD 6.9 billion in the past four weeks, a majority of which has come from EM hard currency funds, which saw outflows of USD 4.3 billion. Local currency EM funds also saw outflows of USD 1.9

billion in the past four weeks (please refer to exhibit below).

Exhibit 19: Sizeable outflows from EM equity and EM bond funds

Concerns on a decelerating China economy and the US Federal Reserve’s move to end QE3 has increased redemption pressure on EM equity and bond funds

Source: EPFR, quant Global Research

Our seasonality analysis on developed & emerging market equity f lows (including ETF) indicates that in 2Q, equity flows, in general are weak (please refer to exhibit below). This analysis is based on the past 12 years’ monthly data and shows that equity investors are heavy

buyers of developed & emerging market equities from January to April. The inflows into funds dry up between May and October and again pick up in the last two months of the year.

80

85

90

95

100

105

110

115

120

125

Jan‐11

Jan‐11

Feb‐11

Mar‐11

Mar‐11

Apr‐11

May‐11

Jun‐11

Jun‐11

Jul‐11

Aug‐11

Aug‐11

Sep‐11

Oct‐11

Oct‐11

Nov‐11

Dec‐11

Dec‐11

Jan‐12

Feb‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

May‐12

Jun‐12

Jul‐12

Jul‐12

Aug‐12

Sep‐12

Sep‐12

Oct‐12

Nov‐12

Nov‐12

Dec‐12

Jan‐13

Jan‐13

Feb‐13

Mar‐13

Apr‐13

Apr‐13

May‐13

Jun‐13

All Equity Funds NAV

All Bond Funds NAV

All Balanced Funds NAV

All Alternative Currency Funds NAV

‐0.8

‐0.6

‐0.4

‐0.2

0

0.2

0.4

0.6

0.8

1

Jan‐12

Feb‐12

Mar‐12

Apr‐12

May‐12

Jun‐12

Jul‐12

Aug‐12

Sep‐12

Oct‐12

Nov‐12

Dec‐12

Jan‐13

Feb‐13

Mar‐13

Apr‐13

May‐13

EM Bond Flows %AUM (4WMA) EM Equi ty Flows %AUM (4WMA)

June 2013 12

Exhibit 20: Sell in May and go away: DM and EM

Seasonality suggests that developed and emerging market funds see fewer flows in 2Q and 3Q

Source: EPFR, quant Global Research.

We do admit that just by looking at seasonality one cannot be sure of the outcome; therefore, we are trying to re late flow numbers from seasonality analysis with our quant Risk Index (QRI). This index measures long‐term global risk appetite using risk indica tors for global

equities, sovereign and corporate credit, global currencies and commodities.

Exhibit 21: quant Risk Index

The QRI has moved into Risk‐Averse Zone

Source: quant Global Research

The quant Equity Risk Index is now deep in the Risk‐Averse Zone. Its current reading is 1.23 (Z‐score) compared to 0.72 (Z‐score) on 14 June 2013. As EM equity and bond funds, global HY bond funds and commodity funds witness heavy outflows, “risk assets” will continue to be under pressure for the next two weeks. The quant Equity Risk Index will remain in the Risk‐Averse Zone as the global deleveraging process garners steam in the wake of the tapering off of the bond buying program by the US Fed. We expect equities to consolidate with a negative

‐8.00

‐6.00

‐4.00

‐2.00

0.00

2.00

4.00

6.00

Jan Feb Mar April May Jun Jul Aug Sep Oct Nov Dec

DM Flows (US$ bn) EM Flows (US$ bn)

600

800

1000

1200

1400

1600

1800

Nov

‐06

Feb‐07

May‐07

Aug‐07

Nov

‐07

Feb‐08

May‐08

Aug‐08

Nov

‐08

Feb‐09

May‐09

Aug‐09

Nov

‐09

Feb‐10

May‐10

Aug‐10

Nov

‐10

Feb‐11

May‐11

Aug‐11

Nov

‐11

Feb‐12

May‐12

Aug‐12

Nov

‐12

Feb‐13

May‐13

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

quant risk index Short Threshold MSCI Worl d (RHS)

Risk‐Loving Zone

Risk‐Averse Zone

All ‐time Low

2008 Credit CrisisUS Downgrade

Euro Sovere ign

Debt Crisi s

Risk‐Neutral Zone

June 2013 13

bias and risk to remain high in the near term, following which equity vols & skew should come off as the US and Japan equity markets begin another uptrend.

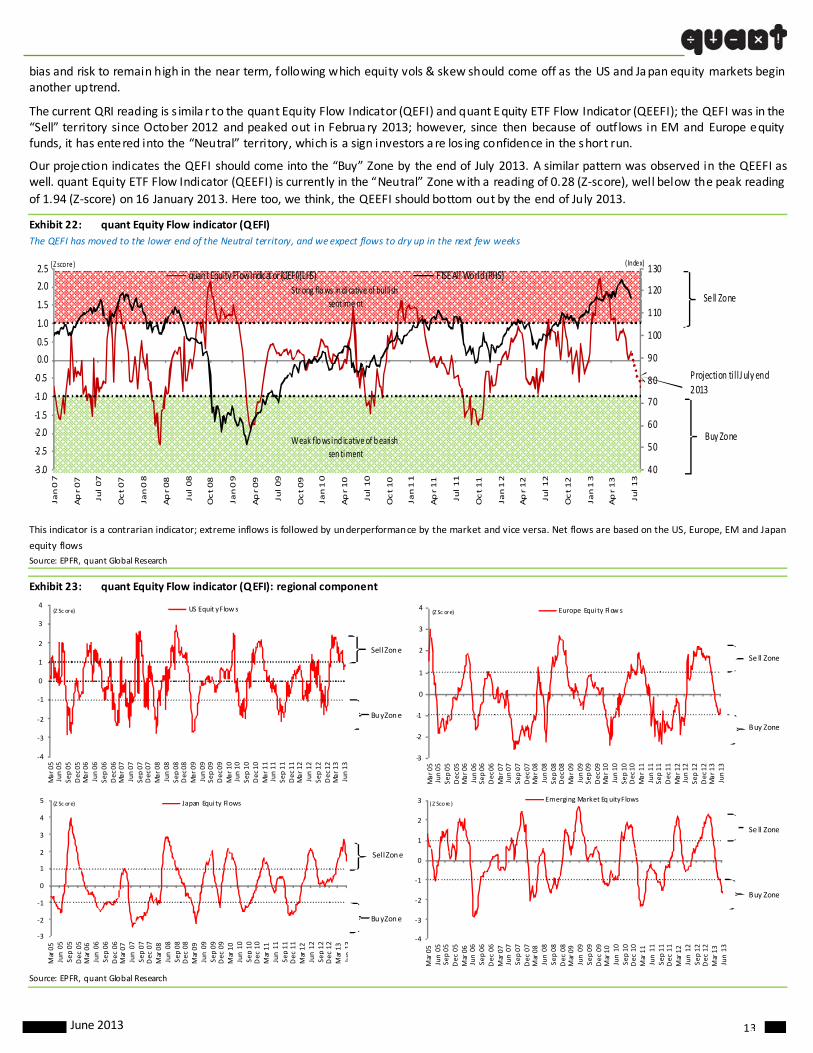

The current QRI reading is s imila r to the quant Equity Flow Indicator (QEFI) and quant Equity ETF Flow Indicator (QEEFI); the QEFI was in the “Sell” territory since October 2012 and peaked out in February 2013; however, since then because of outf lows in EM and Europe equity funds, it has entered into the “Neutral” territory, which is a sign investors are los ing confidence in the short run.

Our projection indicates the QEFI should come into the “Buy” Zone by the end of July 2013. A similar pattern was observed in the QEEFI as well. quant Equity ETF Flow Indicator (QEEFI) is currently in the “Neutral” Zone with a reading of 0.28 (Z‐score), well below the peak reading

of 1.94 (Z‐score) on 16 January 2013. Here too, we think, the QEEFI should bottom out by the end of July 2013.

Exhibit 22: quant Equity Flow indicator (QEFI)

The QEFI has moved to the lower end of the Neutral territory, and we expect flows to dry up in the next few weeks

This indicator is a contrarian indicator; extreme inflows is followed by underperformance by the market and vice versa. Net flows are based on the US, Europe, EM and Japan

equity flows

Source: EPFR, quant Global Research

Exhibit 23: quant Equity Flow indicator (QEFI): regional component

Source: EPFR, quant Global Research

Str ong flows indicative of bul lish sent iment

Weak flows ind icative of bearish sen timent

Sell Zone

Buy Zone

(Z score) ( Index)

40

50

60

70

80

90

100

110

120

130

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

Jan 07

Apr 07

Jul 07

Oct 07

Jan 08

Apr 08

Jul 08

Oct 08

Jan 09

Apr 09

Jul 09

Oct 09

Jan 10

Apr 10

Jul 10

Oct 10

Jan 11

Apr 11

Jul 11

Oct 11

Jan 12

Apr 12

Jul 12

Oct 12

Jan 13

Apr 13

Jul 13

quant Equity Flow Indicator (QEFI)(LHS) FTSE All World (RHS)

Projection till J uly end

2013

‐4

‐3

‐2

‐1

0

1

2

3

4

Mar 05

Jun 05

Sep 05

Dec 05

Mar 06

Jun 06

Sep 06

Dec 06

Mar 07

Jun 07

Sep 07

Dec 07

Mar 08

Jun 08

Sep 08

Dec 08

Mar 09

Jun 09

Sep 09

Dec 09

Mar 10

Jun 10

Sep 10

Dec 10

Mar 11

Jun 11

Sep 11

Dec 11

Mar 12

Jun 12

Sep 12

Dec 12

Mar 13

Jun 13

US Equit y Flow s

Sel l Zone

Buy Zone

‐3

‐2

‐1

0

1

2

3

4

Mar 05

Jun 05

Sep 05

Dec 05

Mar 06

Jun 06

Sep 06

Dec 06

Mar 07

Jun 07

Sep 07

Dec 07

Mar 08

Jun 08

Sep 08

Dec 08

Mar 09

Jun 09

Sep 09

Dec 09

Mar 10

Jun 10

Sep 10

Dec 10

Mar 11

Jun 11

Sep 11

Dec 11

Mar 12

Jun 12

Sep 12

Dec 12

Mar 13

Jun 13

Europe Equi ty Flow s

‐3

‐2

‐1

0

1

2

3

4

5

Mar 05

Jun 05

Sep 05

Dec 05

Mar 06

Jun 06

Sep 06

Dec 06

Mar 07

Jun 07

Sep 07

Dec 07

Mar 08

Jun 08

Sep 08

Dec 08

Mar 09

Jun 09

Sep 09

Dec 09

Mar 10

Jun 10

Sep 10

Dec 10

Mar 11

Jun 11

Sep 11

Dec 11

Mar 12

Jun 12

Sep 12

Dec 12

Mar 13

Jun13

Japan Equi ty Flows

‐4

‐3

‐2

‐1

0

1

2

3

Mar 05

Jun 05

Sep 05

Dec 05

Mar 06

Jun 06

Sep 06

Dec 06

Mar 07

Jun 07

Sep 07

Dec 07

Mar 08

Jun 08

Sep 08

Dec 08

Mar 09

Jun 09

Sep 09

Dec 09

Mar 10

Jun 10

Sep 10

Dec 10

Mar 11

Jun 11

Sep 11

Dec 11

Mar 12

Jun 12

Sep 12

Dec 12

Mar 13

Jun 13

Emerging Market Eq uity Flows

Se ll Zone

Buy Zone

Sel l Zone

Buy Zone

Se ll Zone

Buy Zone

(Z Sc ore) ( Z Score )

(Z Sc ore) (Z Sc ore)

June 2013 14

Exhibit 24: quant Equity ETF Flow indicator (QEEFI)

The QEEFI has moved to the lower end of the Neutral territory, and we expect flows to dry up in the next few weeks

This indicator is a contrarian indicator, extreme inflows is followed by underperformance by the market and vice versa. Net flows are based on US ,Europe, EM and Japanese

equity flows.

Source: EPFR, quant Global Research

Exhibit 25: quant Equity ETF Flow indicator (QEEFI) : regional component

Source: EPFR, quant Global Research

Once we put the current reading of all indicators into perspective along with the seasonality factor, we expect risk appetite to go down until the middle of 3Q 2013. As we have highlighted earlier, risk aversion has returned as investors ponder an end to QE3 and concerns re‐emerging on China g rowth. The only positive that we saw in this week’s data was heavy inflows of USD 7.0 billion into US equity funds; however, we note EPFR data is until Wednesday close (June 19, 2013) and outflows in the past couple of days would not get reflected until the next week. Therefore, we are of the view this is not necessarily the end of the SELLOFF in both equity and bond markets.

We expect the SELLOFF in “Risk Assets” to gain momentum in the next couple of weeks, and both quant Indicators (QEFI and QEEFI) are expected to bottom out by the end of July 2013.

Str ong flows indicative of bul lish

se ntiment

We ak flows indicative o f bearish sentimen t

Sell Zone

Buy Zone

(Z S core ) (I ndex)

40

50

60

70

80

90

100

110

120

130

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan 07

Apr 07

Jul 07

Oct 07

Jan 08

Apr 08

Jul 08

Oct 08

Jan 09

Apr 09

Jul 09

Oct 09

Jan 10

Apr 10

Jul 10

Oct 10

Jan 11

Apr 11

Jul 11

Oct 11

Jan 12

Apr 12

Jul 12

Oct 12

Jan 13

Apr 13

Jul 13

quant Equity ETF Flow In dicator (QEEFI)(LHS) FTSE All World (RHS)

Projection ti ll July end

2013

‐4.0

‐3.0

‐2.0

‐1.0

0.0

1.0

2.0

3.0

4.0

5.0

Feb 05

Jul 05

Dec 05

May 06

Oct 06

Mar 07

Aug 07

Jan 08

Jun 08

Nov 08

Apr 09

Sep 09

Feb 10

Jul 10

Dec 10

May 11

Oct 11

Mar 12

Aug 12

Jan 13

Jun 13

US ETF Flows

‐5.0

‐4.0

‐3.0

‐2.0

‐1.0

0.0

1.0

2.0

3.0

4.0Fe

b 05

Jul 05

Dec 05

May 06

Oct 06

Mar 07

Aug 07

Jan 08

Jun 08

Nov 08

Apr 09

Sep 09

Feb 10

Jul 10

Dec 10

May 11

Oct 11

Mar 12

Aug 12

Jan 13

Jun 13

Europe ETF Flows

‐3 .0

‐2 .0

‐1 .0

0.0

1.0

2.0

3.0

4.0

5.0

Feb 05

Jul 0

5

Dec 05

May 06

Oct 06

Mar 07

Aug 07

Jan 08

Jun 08

Nov 08

Apr 09

Sep 09

Feb 10

Jul 1

0

Dec 10

May 11

Oct 11

Mar 12

Aug 12

Jan 13

Jun 13

Japan ETF Flows

‐4.0

‐3.0

‐2.0

‐1.0

0.0

1.0

2.0

3.0

Feb 05

Jul 05

Dec 05

May 06

Oct 06

Mar 07

Aug 07

Jan 08

Jun 08

Nov 08

Apr 09

Sep 09

Feb 10

Jul 10

Dec 10

May 11

Oct 11

Mar 12

Aug 12

Jan 13

Jun 13

Emergin g Mar ket ETF Flow s

l b l h

Sel l Zone

Buy Zone

Se ll Zone

Buy Zone

Sel l Zone

Buy Zone

Sell Zone

Buy Zone

(Z Score ) ( Z Score )

( Z Score ) ( Z Score )

June 2013 15

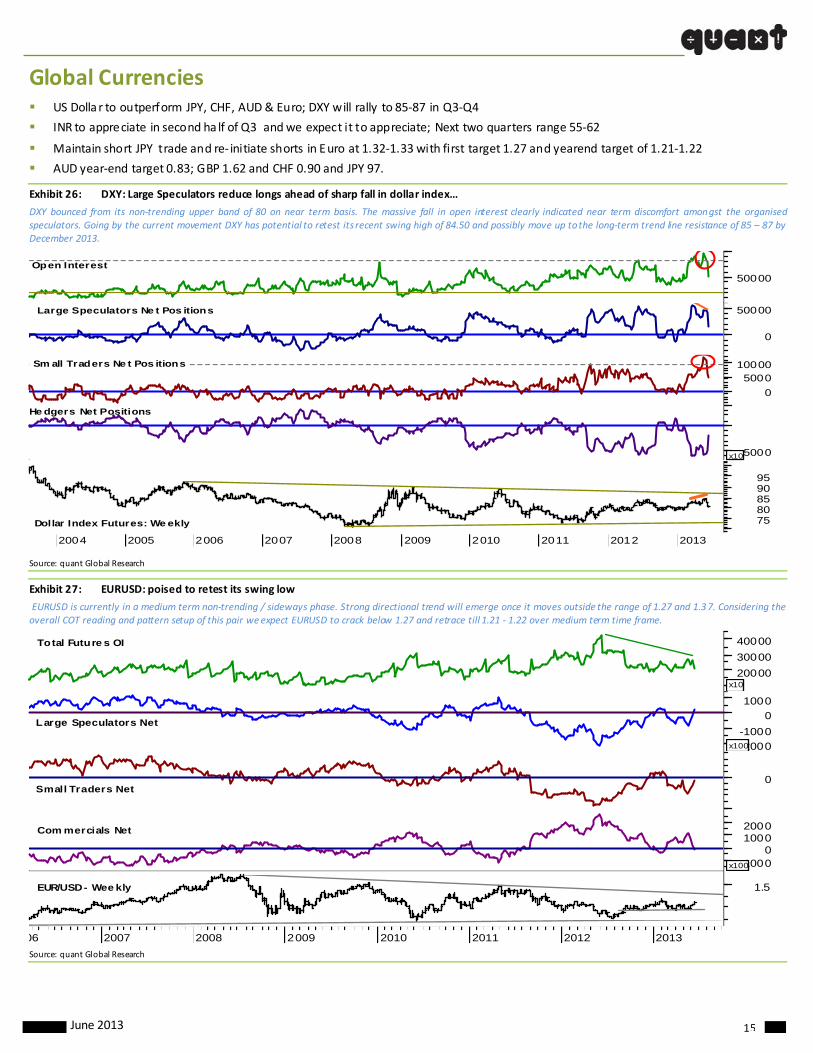

Global Currencies US Dolla r to outperform JPY, CHF, AUD & Euro; DXY will rally to 85‐87 in Q3‐Q4

INR to appreciate in second ha lf of Q3 and we expect it to appreciate; Next two quarters range 55‐62

Maintain short JPY trade and re‐ initiate shorts in Euro at 1.32‐1.33 with first target 1.27 and yearend target of 1.21‐1.22

AUD year‐end target 0.83; GBP 1.62 and CHF 0.90 and JPY 97.

Exhibit 26: DXY: Large Speculators reduce longs ahead of sharp fall in dollar index…

DXY bounced from its non‐trending upper band of 80 on near term basis. The massive fall in open interest clearly indicated near term discomfort amongst the organised speculators. Going by the current movement DXY has potential to retest its recent swing high of 84.50 and possibly move up to the long‐term trend line resistance of 85 – 87 by December 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

7580859095

Dollar Index Futures: We ekly

-5000x10

He dgers Net Positions

0

500010000Sm all Traders Ne t Pos itions

0

50000Large Speculators Ne t Pos itions

50000Open Interest

Source: quant Global Research

Exhibit 27: EURUSD: poised to retest its swing low

EURUSD is currently in a medium term non‐trending / sideways phase. Strong directional trend will emerge once it moves outside the range of 1.27 and 1.37. Considering the overall COT reading and pattern setup of this pair we expect EURUSD to crack below 1.27 and retrace till 1.21 ‐ 1.22 over medium term time frame.

06 2007 2008 2009 2010 2011 2012 2013

1.5EUR/USD - Wee kly

-10000

10002000

x100

Com mercials Net

0Small Traders Net

-2000

-1000

0

1000

x100

Large Speculators Net

20000

30000

40000

x10

Total Future s OI

Source: quant Global Research

June 2013 16

Exhibit 28: EURUSD Daily

The EURUSD is nearing its 200 DMA and the near term indicators are suggesting that it will be broken. Initially 1.27 could act as support before it gives way for 1.21 – 1.22.

2009 2010 2011 2012 2013

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

EURUSD - Daily

EURUSD on its w ay to test its 200 DMA.Ne ar term indicators are alre ady in sell mode.We expect th is pair to te st it medium term sw ing low of 1.20 - 1.21

Source: quant Global Research

Exhibit 29: USDJPY: bouncing from its support of 94

USDJPY is moving up after testing its historical support of 95. The price patterns and overall reading of commitments of traders indicates this pair can possi bly move to 110 – 120 in the long‐term and 97‐99 by year‐end.

2008 2009 2010 2011 2012 2013

90100110120130

Japanes e Ye n Futures: Weekly

10000

x10

Com mercials Hedgers Net

-5000x10Small Trade rs Net

-1000

0

x100

Large Speculators Net

10000

20000

30000

x10

JPY Future s OI

Source: quant Global Research

June 2013 17

Exhibit 30: AUDUSD Spot

AUDUSD was dumped sharply after prolonged non‐trending phase. It broke its historic support zone of 0.9388 and 0.9582 and likely to halt around 0.91 briefly (38% retracement of 0.60 to 1.11), and subsequently drop to its 50% retracement of 0.85.

8 2009 2010 2011 2012 2013

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

38.2%

50.0%

61.8%

AUDUSD Spot: Weekly

Source: quant Global Research

Exhibit 31: CFTC ‐ AUD

The Large Speculators and Small Traders short position is at its historic high level, indicating their negative bias on this pair. With this currency pair breaking its support zone, it is likely to react till 0.83‐0.85.

2008 2009 2010 2011 2012 2013

60708090

100Australian Dollar Future s: Week ly

-1000-500

0500

x100Com mercial hedgers ne t

0Small traders net

-5000

5000

x10

Large speculators net

5000100001500020000

x10

Total Futures Open Interes t

Source: quant Global Research

June 2013 18

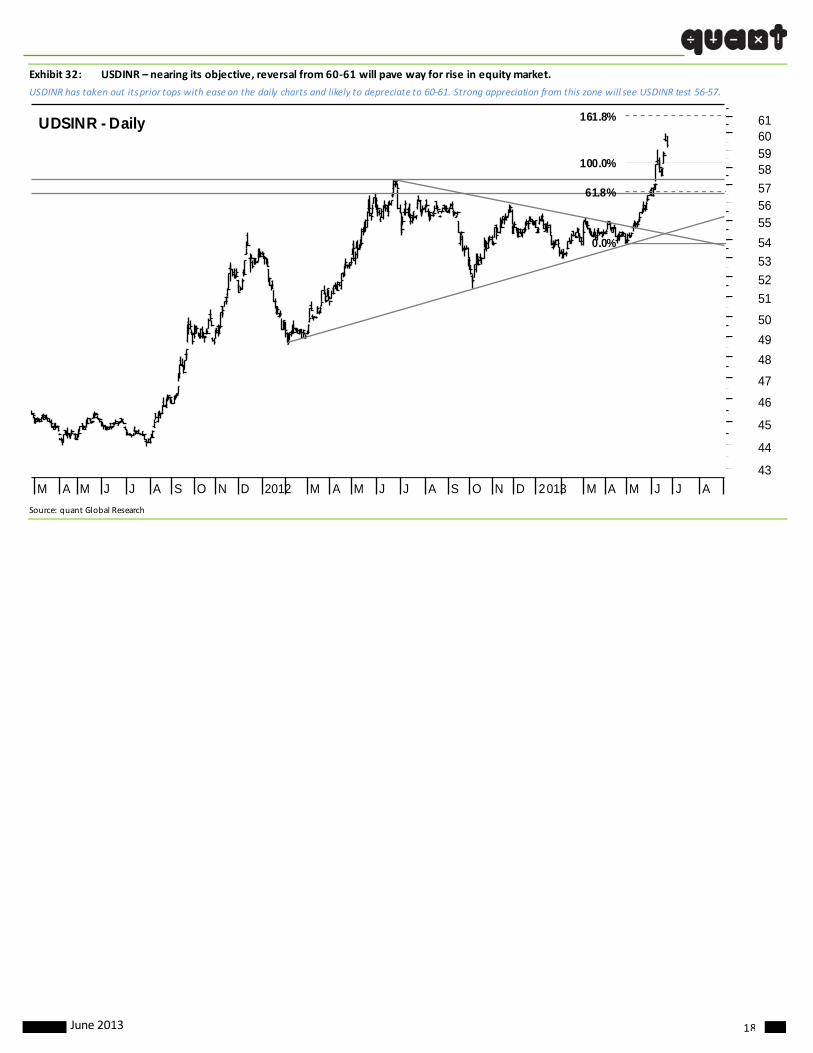

Exhibit 32: USDINR – nearing its objective, reversal from 60‐61 will pave way for rise in equity market.

USDINR has taken out its prior tops with ease on the daily charts and likely to depreciate to 60‐61. Strong appreciation from this zone will see USDINR test 56‐57.

Source: quant Global Research

M A M J J A S O N D 2012 M A M J J A S O N D 2013 M A M J J A

43

44

45

46

47

48

49

50

51

52

53

54

555657

58596061

0.0%

61.8%

100.0%

161.8%UDSINR - Daily

June 2013 19

2013 Currency consensus

Exhibit 33: Consensus G 10 currency outlook Exhibit 34: Consensus Asian currency outlook

Source: Bloomberg, quant Global Research Source: Bloomberg, quant Global Research

Exhibit 35: Consensus EMEA currency outlook Exhibit 36: Consensus Latin America currency outlook

Source: Bloomberg, quant Global Research Source: Bloomberg, quant Global Research

G10 Currencies 2013 Q3 2013 Q4 2014 Q1 2014 Q2

EURUSD 1.28 1.27 1.27 1.27

USDJPY 103 105 106 105

EURJPY 132 133 134 134

GBPUSD 1.51 1.49 1.49 1.52

EURGBP 0.85 0.85 0.84 0.85

USDCHF 0.97 1.00 1.01 1.01

EURCHF 1.24 1.26 1.27 1.27

USDCAD 1.02 1.03 1.03 1.02

AUDUSD 0.96 0.96 0.96 0.96

NZDUSD 0.80 0.80 0.80 0.80

EURDKK 7.45 7.46 7.46 7.46

USDDKK 5.83 5.92 5.92 5.97

EURNOK 7.5 7.45 7.39 7.25

USDNOK 5.84 5.91 5.95 5.95

EURSEK 8.50 8.46 8.40 8.30

USDSEK 6.63 6.69 6.73 6.73

DXY 83.8 85.7 85.9 84.0

Asian Currencies 2013 Q3 2013 Q4 2014 Q1 2014 Q2

USDCNY 6.13 6.1 6.08 6.05

USDHKD 7.76 7.76 7.77 7.76

USDINR 55.25 55 54 55.9

USDIDR 9842 9854 9795 9875

USDMYR 3.06 3.06 3.02 3.07

USDPHP 41.5 41.2 41.0 41.3

USDSGD 1.25 1.25 1.24 1.23

USDKRW 1128 1113 1095 1081

USDTWD 30 29.8 29.5 29.2

USDTHB 30.1 30 30 30.3

USDVND 21000 21000 21000 21000

EMEA Currencies 2013 Q3 2013 Q4 2014 Q1 2014 Q2

EURCZK 26 25.8 25.7 25.5

USDCZK 20.23 20.56 20.5 20.62

EURHUF 297 296 295 295

USDHUF 232 238 238 239

EURPLN 4.21 4.15 4.12 4.07

USDPLN 3.28 3.29 3.29 3.29

EURRUB 41.3 41.12 40.5 40.57

USDRUB 32.05 31.89 31.43 32.00

RUBBASK 35.78 35.48 35.33 35.5

USDTRY 1.85 1.85 1.85 1.85

USDILS 3.68 3.63 3.63 3.6

USDZAR 9.78 9.68 9.5 9.55

Latin America Currencies 2013 Q3 2013 Q4 2014 Q1 2014 Q2

USDARS 5.56 5.85 6.16 6.4

USDBRL 2.05 2.04 2.05 2.08

USDCLP 480 480 493 493

USDCOP 1855 1875 1839 1900

USDMXN 12.28 12.1 12 11.95

USDPEN 2.58 2.57 2.55 2.52

USDVEF 6.3 6.3 7.65 7.8

June 2013 20

Global Commodities Outlook We expect limited ups ide to Brent crude in the near term based on higher ref ineries run, North Sea maintenance and subdued

inventory buildup by Saudi Arabia. However, we do not expect Brent crude to move above US$110/bbl during the mid third quarter

and expect a gradual correction in the fourth quarter on easing of Iran’s nuclear issue, seasonal demand decline and North Sea maintenance completion.

Based on aforementioned reasons simila r to Brent, we expect limited near‐term upside on NYMEX WTI crude to US$100/bbl, assuming Brent‐WTI differential of US$7‐8/bbl would be maintained.

Commodities

Similar to 3Q CY12, crude prices are gearing up for a run‐up in 3Q CY13 but with limited upside

Despite subdued demand growth in China, we expect limited upside to crude prices in 3Q CY13. However, unlike 3Q CY12, when Brent and WTI crude prices jumped by US$17/bbl and US$11/bbl q‐q, respectively, we do not expect Brent crude prices to susta in above US$110/bbl and WTI above US$100/bbl due to expectations of easing of Iran’s nuclea r issue. Subsequently, we anticipate gradual correction in crude

prices by 4Q CY13.

Our expectations of a run‐up, although limited, of Brent and WTI crude during 3Q CY13 is based on the following three factors: 1) maintenance activities in the North Sea, which would impact 0.3 mmbpd of North Sea production, 2) a seasonal increase in global ref ineries run by 2.3 mmbpd q‐q, and 3) negligible crude inventory buildup by Saudi Arabia during January‐April vs 17 mmbbl buildup historically to cater to peak summer demand.

Improving simple refiners GRM and weakening of Brent crude backwardation would lead to an increase in crude appetite for global refineries. However, higher refinery runs can possibly depress GRM by the end of 3Q CY13 when seasona l demand growth would soften, and, subsequently, develop a downward pressure on crude prices by 4Q CY13. Overall, we observed s imple refiners GRM improved US$1.3/bbl q‐q to ‐US$1.4/bbl in North‐West Europe (Brent hydro‐skimming) and US$4.9/bbl q‐q to US$6.4/bbl in Asia (Minas hydro‐skimming). M1‐M3 (next month less third month Brent futures) backwardation declined to US$0.6/bbl in June from 1.2/bbl in March,

implying minimal risk of inventory losses for ref iners.

Based on aforementioned reasons, we estimate “Call on OPEC Crude” would rise to 31.7 mmbpd during 3Q CY13 vs the current 30.7 mmbpd of OPEC production, implying major 1.2 mmbpd of global crude inventory drawdown that would be supportive for crude prices.

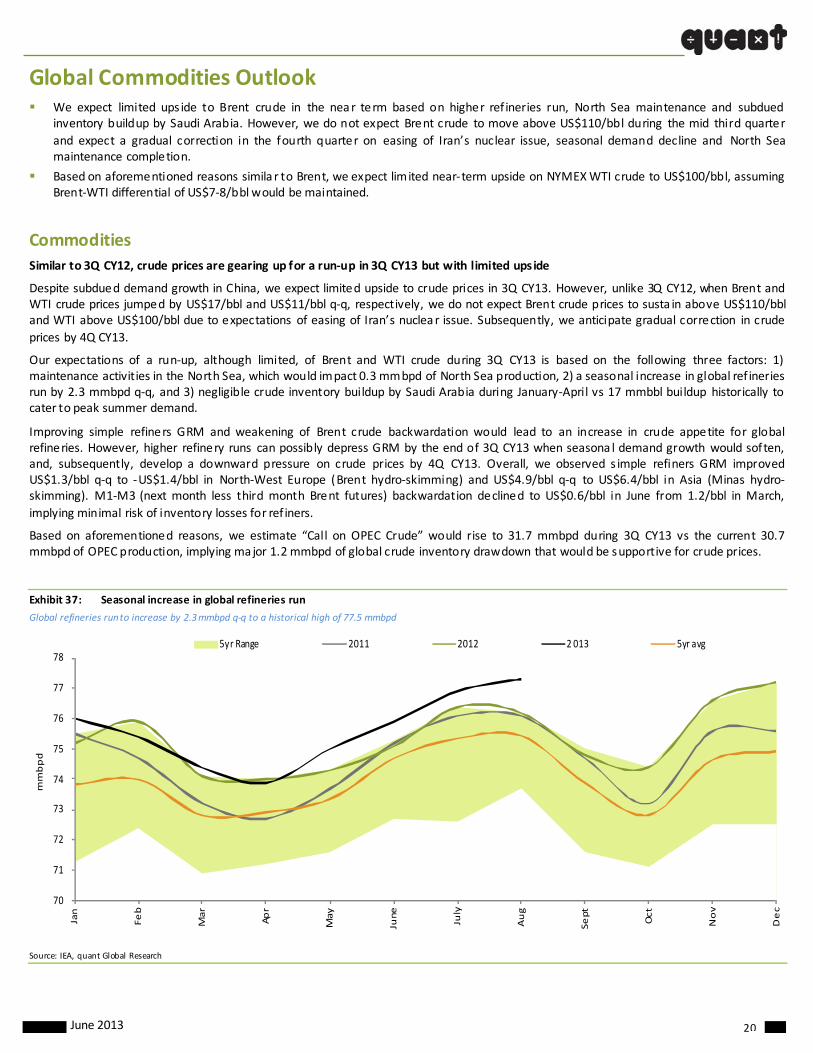

Exhibit 37: Seasonal increase in global refineries run

Global refineries run to increase by 2.3 mmbpd q‐q to a historical high of 77.5 mmbpd

70

71

72

73

74

75

76

77

78

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

mmbpd

5yr Range 2011 2012 2 013 5yr avg

Source: IEA, quant Global Research

June 2013 21

Exhibit 38: Crude inventory buildup by Saudi Arabia

Negligible crude inventory buildup by Saudi Arabia during January‐April vs 17 mmbbl build historically to cater to peak summer demand

170

190

210

230

250

270

290

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

mmbbl

5yr range 2011 2012 201 3 5yr average

Source: JODI, quant Global Research

Exhibit 39: Simple refineries GRM and Brent crude backwardation trend

Improving simple refiners GRM and weakening of Brent crude backwardation would lead to the increase in crude appetite for global refineries

0

2

4

6

8

10

12

14

16

18

(4)

(2)

0

2

4

6

8

Jan ‐13 Feb ‐13 Mar‐13 Apr‐13 May‐13 Jun‐13

US$/bbl

US$/bbl

Brent hydroskimming (NWE) Minas hydroskimming (Asia) LLS cracking (US Gulf) (RH S)

(0 .5 )

‐

0.5

1.0

1.5

2.0

2.5

3.0 Jun‐12

Jul‐1

2

Jul‐1

2

Aug‐12

Sep‐12

Sep‐12

Oct‐12

Nov‐12

Nov‐12

Dec‐12

Jan‐13

Jan‐13

Feb‐13

Mar‐13

Apr‐13

Apr‐13

May‐13

Jun‐13

US$

/bbl

Brent M1 ‐M3 price s

Source: Bloomberg, quant Global Research

Exhibit 40: Estimate for “Call on OPEC Crude”

We estimate “Call on OPEC Crude” would increase to 31.7 mmbpd during 3Q CY13 vs the current 30.7 mmbpd of OPEC production

2 9.4

0.6

1.9

(0. 3)

0.3 (0.2 )

31.7

28.0

28.5

29.0

29.5

30.0

30.5

31.0

31.5

32.0

32.5

2Q CY13 Call on OPEC crude

Increase from USA PADD3 refiners

In crease from other gl obal refiners (ex ‐US)

Non‐OPEC crude supply inc rease (ex‐US)

Saudi & Jap an direc t crude burn

OECD stock drawdown 3Q CY13 estimated Call on OPEC crude

mmbp

d

Source: quant Global Research estimates

June 2013 22

Steel

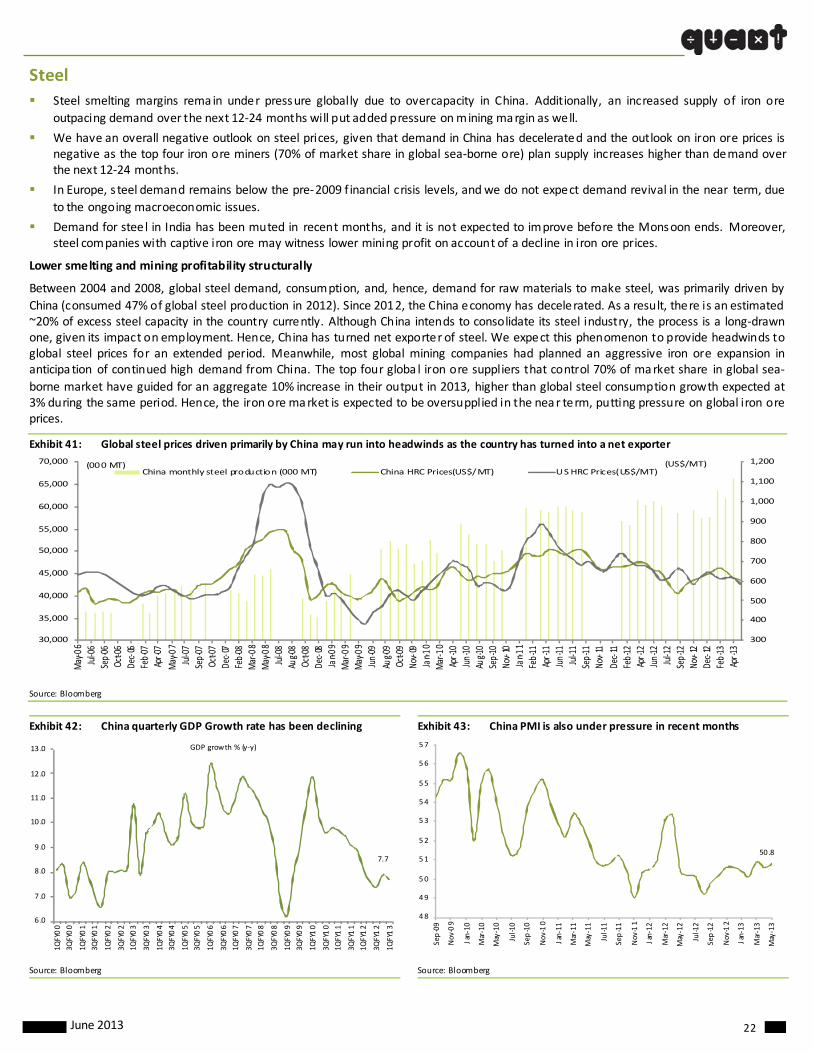

Steel smelting margins rema in under pressure globally due to overcapacity in China. Additionally, an increased supply of iron ore

outpacing demand over the next 12‐24 months will put added pressure on mining margin as well.

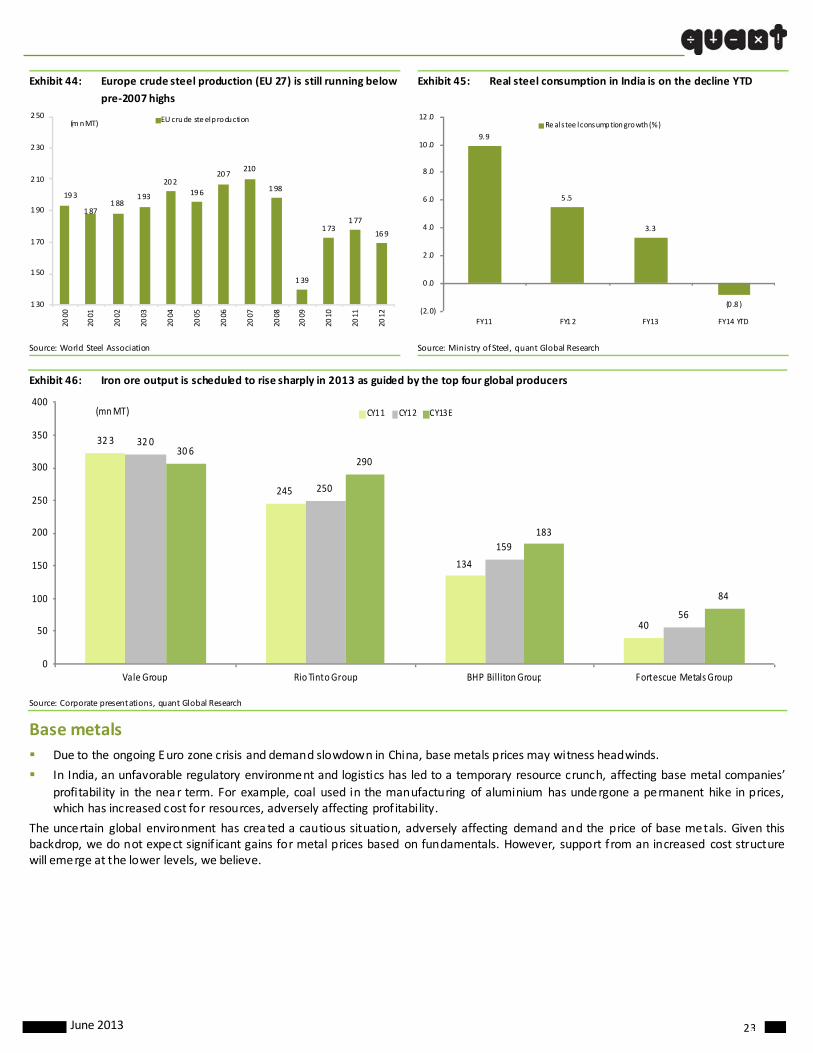

We have an overall negative outlook on steel prices, given that demand in China has decelerated and the outlook on iron ore prices is negative as the top four iron ore miners (70% of market share in global sea‐borne ore) plan supply increases higher than demand over the next 12‐24 months.

In Europe, steel demand remains below the pre‐2009 f inancial crisis levels, and we do not expect demand revival in the near term, due

to the ongoing macroeconomic issues.

Demand for steel in India has been muted in recent months, and it is not expected to improve before the Monsoon ends. Moreover, steel companies with captive iron ore may witness lower mining profit on account of a decline in iron ore prices.

Lower smelting and mining profitability structurally

Between 2004 and 2008, global steel demand, consumption, and, hence, demand for raw materials to make steel, was primarily driven by

China (consumed 47% of global steel production in 2012). Since 2012, the China economy has decelerated. As a result, there is an estimated ~20% of excess steel capacity in the country currently. Although China intends to consolidate its steel industry, the process is a long‐drawn one, given its impact on employment. Hence, China has turned net exporter of steel. We expect this phenomenon to provide headwinds to global steel prices for an extended period. Meanwhile, most global mining companies had planned an aggressive iron ore expansion in anticipa tion of continued high demand from China. The top four globa l iron ore suppliers that control 70% of market share in global sea‐

borne market have guided for an aggregate 10% increase in their output in 2013, higher than global steel consumption growth expected at 3% during the same period. Hence, the iron ore market is expected to be oversupplied in the near term, putting pressure on global iron ore prices.

Exhibit 41: Global steel prices driven primarily by China may run into headwinds as the country has turned into a net exporter

300

400

500

600

700

800

900

1,000

1,100

1,200

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

May‐06

Jul‐06

Sep‐06

Oct‐06

Dec‐06

Feb‐07

Apr‐0

7

May‐07

Jul‐07

Sep‐07

Oct‐07

Dec‐07

Feb‐08

Mar‐08

May‐08

Jul‐08

Aug‐0

8Oc

t‐08

Dec‐08

Jan‐0

9Mar‐09

May‐09

Jun‐09

Aug‐0

9Oc

t‐09

Nov‐09

Jan‐1

0Mar‐10

Apr‐1

0Jun‐10

Aug‐1

0Sep‐10

Nov‐10

Jan‐ 1

1Feb‐11

Apr‐1

1Jun‐11

Jul‐11

Sep‐11

Nov‐11

Dec‐11

Feb‐12

Apr‐1

2Jun‐12

Jul‐12

Sep‐12

Nov‐12

Dec‐12

Feb‐13

Apr‐1

3

(US$/MT)(000 MT)China monthly steel production (000 MT) China HRC Prices(US$/MT) US HRC Prices(US$/MT)

Source: Bloomberg

Exhibit 42: China quarterly GDP Growth rate has been declining Exhibit 43: China PMI is also under pressure in recent months

7.7

6 .0

7 .0

8 .0

9 .0

10 .0

11 .0

12 .0

13 .0

1QFY00

3QFY00

1QFY01

3QFY01

1QFY02

3QFY02

1QFY03

3QFY03

1QFY04

3QFY04

1QFY05

3QFY05

1QFY06

3QFY06

1QFY07

3QFY07

1QFY08

3QFY08

1QFY09

3QFY09

1QFY10

3QFY10

1QFY11

3QFY11

1QFY12

3QFY12

1QFY13

GDP growth % (y‐y)

50 .8

48

49

50

51

52

53

54

55

56

57

Sep‐09

Nov

‐09

Jan‐10

Mar‐10

May‐10

Jul‐10

Sep‐10

Nov

‐10

Jan‐11

Mar‐11

May‐11

Jul‐11

Sep‐11

Nov

‐11

Jan‐12

Mar‐12

May‐12

Jul‐12

Sep‐12

Nov

‐12

Jan‐13

Mar‐13

May‐13

Source: Bloomberg Source: Bloomberg

June 2013 23

Exhibit 44: Europe crude steel production (EU 27) is still running below

pre‐2007 highs

Exhibit 45: Real steel consumption in India is on the decline YTD

193

187188

193

202

196

207210

198

139

173177

169

130

150

170

190

210

230

250

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(m n MT) EU crude steel production

9.9

5 .5

3.3

(0 .8 )(2.0)

0 .0

2 .0

4 .0

6 .0

8 .0

10 .0

12 .0

FY11 FY12 FY13 FY14 YTD

Re al stee l consumption growth (%)

Source: World Steel Association Source: Ministry of Steel, quant Global Research

Exhibit 46: Iron ore output is scheduled to rise sharply in 2013 as guided by the top four global producers

32 3

245

134

40

32 0

250

159

56

30 6290

183

84

0

50

100

150

200

250

300

350

400

Vale Group Rio Tinto Group BHP Billiton Group Fortescue Metals Group

(mn MT) CY11 CY12 CY13E

Source: Corporate presentations, quant Global Research

Base metals

Due to the ongoing Euro zone crisis and demand slowdown in China, base metals prices may witness headwinds.