barriers to entry and firm performance: a proposed model and curvilinear relationships

TRANSCRIPT

This article was downloaded by: [University of Connecticut]On: 05 October 2014, At: 20:53Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Journal of Strategic MarketingPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/rjsm20

Barriers to entry and firm performance:a proposed model and curvilinearrelationshipsFahri Karakaya b & Satyanarayana Parayitam ba Department of Marketing , Charlton College of Business,University of Massachusetts , Dartmouth, North Dartmouth , MA ,02747 , USAb Department of Management , Charlton College of Business,University of Massachusetts , DartmouthPublished online: 19 Dec 2012.

To cite this article: Fahri Karakaya & Satyanarayana Parayitam (2013) Barriers to entry and firmperformance: a proposed model and curvilinear relationships, Journal of Strategic Marketing, 21:1,25-47, DOI: 10.1080/0965254X.2012.734689

To link to this article: http://dx.doi.org/10.1080/0965254X.2012.734689

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Barriers to entry and firm performance: a proposed model andcurvilinear relationships

Fahri Karakayaa* and Satyanarayana Parayitamb

aDepartment of Marketing, Charlton College of Business, University of Massachusetts, Dartmouth,North Dartmouth, MA 02747, USA; bDepartment of Management, Charlton College of Business,

University of Massachusetts, Dartmouth

(Received 15 May 2012; final version received 20 September 2012)

This research examines the relationships among the barriers to market entry: capitalrequirements; competitive advantage of incumbent firms; business environment; andfirm competence, and their relationship to firm performance. Through a mail survey,data were collected on a sample of 190 companies. A hierarchical regression analysisenabled the assessment of the relationships among barriers to entry and firmperformance. In addition, the paper examines the quadratic function of second degreeamong the variables to see the curvilinear relationships between independent anddependent variables. The results indicate the presence of curvilinear relationshipsbetween some barriers for market entrants and performance of market entrants. Whilethe examination of linear relationships between barriers and firm performance isimportant, the analyses of curvilinear relationships shed more light into ourunderstanding of barriers and performance. Therefore this study contributes to theliterature by highlighting the importance of U-shaped and inverted curvilinearrelationships between barriers to entry and firm performance.

Keywords: barriers to entry; market entry barriers; market entry; competition;competitive advantage; capital requirements; firm competence; firm performance;curvilinear relationship

Introduction

Barriers to market entry are factors that influence firm profitability by preventing new

competitors from entering markets (Bain, 1956; Karakaya & Stahl, 1989; Porter, 1985;

Simon, 1996, 2005). Bain (1956, p. 3), who pioneered the concept of barriers to entry,

defined barriers as:

the advantage of established sellers in an industry over potential entrant sellers, theiradvantages being reflected in the extent to which established sellers can persistently raise theirprices above a competitive level without attracting new firms to enter the industry.

Incumbent firms raise barriers to entry to limit the number of competitors in a market.

As a result, the incumbent firms enjoy supernormal long-term industry profits (Han, Kim, &

Kim, 2001). The extant literature highlights six major barriers to entry: cost advantages of

incumbent firms; capital requirements; product differentiation advantages of incumbent

firms; access to distribution channels; customer switching costs; and government

regulations (Karakaya & Stahl, 1989; Porter, 1985). More recently, Karakaya and Kerin

(2007) examined additional barriers to entry that included incumbent structural advantage,

q 2013 Taylor & Francis

*Email: [email protected]

Journal of Strategic Marketing, 2013

Vol. 21, No. 1, 25–47, http://dx.doi.org/10.1080/0965254X.2012.734689

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

incumbent market strength, and financial investment of both incumbent firms and market

entrants.

Barriers to entry affect the competitive behavior of both potential market entrants and

incumbent firms. The ability to create or heighten barriers influences each incumbent

firm’s strategy and choice of action which in turn affect profitability. Consequently,

barriers to entry influence the market entrants’ decision to enter markets and their

formulation of competitive strategies (Pehrsson, 2009). Incumbent firms intentionally

build barriers to deter market entry (Gruca & Sudharshan, 1995) to dominate the market

and maximize profits. Indeed, when barriers to entry exist, incumbent firms engage in less

deterrence or defensive actions (Burch & Smiley, 1992; Karakaya & Yannopoulos, 2010).

Strong barriers do not just protect the incumbents before market entry. They safeguard

them even after initial market entry by slowing down the speed of entry, enabling them to

catch up with the new market entrants (Han et al., 2001). However, barriers to entry

provide little protection for incumbents if market entrants have innovative products (Han

et al., 2001; Markides, 1997). This is also true with innovative channels such as

eCommerce. For example, travel services such as Expedia, Travelocity, and Priceline

successfully entered the US market in the mid-1990s and were able to successfully expand

their markets to other countries. With the Internet as a new distribution channel, Apple’s

ITunes business practically rejuvenated Apple Inc., leading to other innovative and

successful products such as the IPhone, Apple TV, and Ipad.

Rationale for the present study

Previous research on the relationship between barriers to entry and firm performance

supports that higher barriers lead to lower firm performance (Cicic, Patterson, & Shoham,

2002; Patterson & Cicic, 1995; Shoham & Albaum, 1995). However, this is only true for

new market entrants. The presence of high barriers in a market forces new market entrants

to allocate more resources to overcome barriers, adversely affecting firm performance.

Literature review indicates that previous studies have not considered the interrelationships

among barriers to entry and their individual impact on firm performance (Karakaya &

Kerin, 2007). For example one of the most recent studies related to this topic was

conducted by Johnson and Tellis (2008) where the authors mostly ignored the impact of

barriers to entry when examining the drivers of success for market entry into China and

India. The rationale for the present study stems from the following reasons: (1) there is no

prior empirical research that studies the complex interrelationships among the barriers to

entry and firm performance; (2) the available existing research studies are mostly

descriptive and are scattered, focusing on the linear relationship between barriers to entry

and firm performance; (3) the relationships among the barriers to entry are more complex

than were hypothesized in earlier studies, for example, one barrier may lead to another

(capital requirements may lead to competitive advantage); (4) the conflicting results that

were found in earlier studies necessitate in-depth study of relationships among variables;

and (5) specification of a new model depicting the relationships. With the above rationale,

the present research addresses the shortcomings of previous research and builds a more

robust and sophisticated model of entry barriers. More specifically, this research attempts

to fill the void on interrelationships among barriers by developing a model that focuses on

capital requirements, unfavorable business environment, firm competence of market

entrants, and competitive advantage of incumbent firms as barriers for market entrants. We

select market entry into eCommerce markets to conduct this study because there have been

innumerable entries into and exit from the market since the emergence of the eCommerce

F. Karakaya and S. Parayitam26

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

industry in the early 1990s (see Cochran, Darrat, & Elkhal, 2006). Furthermore,

eCommerce will become important even for companies that are brick and mortar today

and will determine their success (Fruhling & Digman, 2000).

Theoretical background and hypotheses

Resource-based view and barriers to entry

The barriers such as capital requirements, competitive advantage, firm competence and

even the business environment to a certain extent are related to the resources a company

has. Thus, we use the resource-based view (RBV) as a theoretical platform for explaining

the relationship between barriers to entry and firm performance. According to RBV, which

is well documented in the literature (see, for example, Mahoney, 1995), firm resources are

primary predictors of superior performance (Wernerfelt, 1984). Firm resources help

organizations build competitive advantage. Indeed, RBV defines important factors that

relate to developing sustainable competitive advantage (Barney, 1986; Dierickx & Cool,

1989; Kor & Mahoney, 2004; Peteraf & Barney, 2003; Wernerfelt, 1984). These factors

are resources that are rare, unique, valuable, not perfectly imitable by competitors, and

competitively superior (Priem & Butler, 2001). Proponents of RBV argue that resources

possessing these characteristics ultimately lead to higher firm performance through

sustained competitive advantage (Barney, 1991). According to Grant (1991), major

sources of barriers to entry include economies of scale, having patent(s), experience, brand

reputation, or some other resource that incumbent firms enjoy but take time to acquire. The

resources relating to barriers to entry are categorized as financial capital, physical capital,

human capital, and organizational capital (Barney, 1991).

Lack of resources impacts the perception of business environment. When market

entrants perceive lack of resources (e.g. unavailability of financial capital), they also

perceive an unfavorable business environment because they do not have the means to deal

with such uncontrollable or uncertain environment. Similarly, when market entrants

perceive lack of resources (e.g. capital), they also perceive that their firm does not have

competence. Therefore, lack of firm competence is rooted in the RBV theory, and it is a

major barrier to entry. For example, previous research has linked information technology

capability to firm performance (Bharadwaj, 2000; Wade & Holland, 2004). Other

researchers have indicated that eCommerce adoption is related to technology competence

(Stockdale & Standing, 2004, 2006; Zhu, Kraemer, & Xu, 2003), technical resource

competence (To & Ngai, 2006), technical know-how (Darch & Lucas, 2002), and

organizational readiness (Hadaya & Pellerin, 2008). Potential market entrants lacking

technical or non-technical competencies face barriers to entry. On the other hand,

incumbent firms with strong competencies deter market entry of new firms into their

markets because potential market entrants perceive incumbent competencies as a major

barrier to overcome. Hence, resources are the key to building competence and securing

sustained competitive advantage to deter market entry of new competition.

Effects of capital requirements and business environment on competitive advantage

The barrier of capital requirements is one of the most important obstacles to market entry

for competition. High capital requirements limit the number of firms in a market and allow

the incumbent firms to maximize their market share and profits. Moreover, the presence of

high capital requirements increases the competitive advantage of incumbent firms. Based

on RBV, availability of resources generates competitive advantage (Barney, 1986;

Journal of Strategic Marketing 27

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Dierickx & Cool, 1989; Wernerfelt, 1984). For example, when firms have sufficient

financial resources, the capital requirement barrier is low and insignificant. Indeed,

previous research indicates that firms with adequate resources are likely to develop

competitive advantage such as product differentiation which results from product

characteristics including physical, service, and image (Sashi & Stern, 1995). Another

important competitive advantage is cost. When incumbent firms have cost advantages and

charge low prices, they deter entry of new competition into their markets (Coeurderoy &

Dur &, 2004; Karakaya & Stahl, 1989, 1992; Porter, 1985). Cost advantages are related to

a firm’s internal or external environment, rooted in resources. Firms with adequate

resources are likely to develop technology and processes in their operations that achieve

cost advantages.

Unfavorable business environments such as distribution channels, inability to meet

demand and security issues (Razi, Tarn, & Siddiqui, 2004) do not just act as barriers to

entry for the potential market entrants; they provide competitive advantage for the

incumbent firms, simply by limiting the number of firms that can enter the market.

For example, many small manufacturers see access to distribution channels as a barrier

to reaching consumers because distributors are selective in choosing their vendors.

In addition, retail stores such as supermarkets charge high fees for shelf space (Rennhoff,

2008), which puts the smaller companies at a disadvantageous position. Based on the

above we offer the following hypotheses:

H1: Capital Requirements barrier for market entrants is positively related to

Competitive Advantage of incumbent firms.

H2: Unfavorable Business Environment barrier for market entrants is positively related

to Competitive Advantage of incumbent firms.

Effects of capital requirements and unfavorable business environment barriers for

market entrants on perceived firm competence of market entrants

As indicated earlier, firm competence or the lack thereof is an important barrier to market

entry. Previous research indicates that there is a relationship between IT capability

and adoption of new innovation, which in turn affects firm competence (Iacovou,

Benbasatand, & Dexter, 1995). For example, the technical complexity of new innovation

is a major determinant of product adoption (Agarwal & Prasad, 1998; Cooper & Zmud,

1990; Forman, 2005). Technical complexity of new products and technology is related to

the skills and knowledge of employees. A study conducted by Darch and Lucas (2002)

showed that lack of knowledge and technological skills were barriers to engaging in

eCommerce for Small and Medium Enterprises (SMEs). Lack of knowledge and skills are

more apparent in SMEs relative to large firms (Duan, Mullins, Hamblin, & Stanek, 2002).

Lack of skills and knowledge create the perception of inability to successfully utilize new

products or technology. Related to the preceding factors, technical know-how and

insufficient infrastructure are also related to firm competence and have been shown to

serve as barriers to eCommerce adoption (Dubelaar, Sohal, & Savic, 2005). In addition,

employee skills and knowledge are closely linked to firm competence (Ruiz-Ortega &

Garcıa-Villaverde, 2008) whereas a skilled and knowledgeable work force is crucial in the

successful implementation of technology (Allison, 1999). However, the shortage of skilled

employees has been recognized as one of the major problems that firms face (Bingi, Mir, &

Khamalah, 2000) and is a barrier for eCommerce adoption and its successful

implementation (Duan et al., 2002).

F. Karakaya and S. Parayitam28

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Availability of financial and non-financial resources eliminates or reduces many of the

weaknesses just mentioned, thus lowering the capital requirements barrier and

strengthening firm competence. Based on the resource-based theory, business

environment (positive or negative) can have an impact on firm competence. For example,

the business environment impacts the availability of skilled employees and access to

distribution channels. Previous research linked business environment (external

environment) to firm competence (Collis & Montgomery, 2008). If business environment

is sound (e.g. availability of skilled employees, technical know-how, etc.) new firms may

enter the market and compete with the existing firms. Therefore, a dynamic business

environment hinders performance of both market entrants and the incumbent firms and

adversely affects firm competence. Based on the above arguments, we propose the

following hypotheses:

H3: Capital Requirements barrier for market entrants is negatively related to Market

Entrant Competence.

H4: Unfavorable Business Environment for market entrants is negatively related to

Market Entrant Competence.

Effects of competitive advantage and firm competence on firm performance

Competitive advantage and firm competence play an important role in determining

company effectiveness (Fuentelsaz, Gomez, & Polo, 2002). Indeed, Porter (1985) suggests

that competitive advantage is the main objective of a firm in competitive markets.

Competitive advantage consists of many variables such as cost advantage, product

differentiation, proprietary product technology or trade secrets, and so on, and they serve

as barriers for market entrants. However, the variables that determine competitive

advantage do change and the firms that follow the changes are more successful than the

ones that do not (Olusoga, Mokwa, & Noble, 1995). Tippins and Sohi (2003) indicate that

IT competence consists of technical knowledge; extent of IT usage; and computer-based

hardware, software, and support personnel, all of which can translate into competitive

advantage. While the competitive advantage of the focal firm is positively related to firm

performance, the competitive advantage enjoyed by a rival firm will result in lowering the

focal firm’s performance. For example, a study by Coltman, Devinney, and Midgley

(2007) showed that firms could expect significant e-business performance when their IT

capability is at an advanced stage. In addition, the study by Tippins and Sohi (2003)

indicated that organizational learning plays an important role in mediating the influence of

IT competency on firm performance. Similarly, Santhanam and Hartono (2003) specified

that superior IT capability leads to superior and sustained firm performance.

This discussion leads us to suggest the following hypotheses:

H5: Competitive Advantage of incumbent firms is negatively related to market entrant

performance.

H6: Firm Competence of market entrants is positively related to market entrant

performance.

Curvilinear effect of capital requirements and business environment on performance

The capital needed continues long after a company enters a market. Two studies, Coltman

et al. (2007) and Thornton and Marche (2003), dealing with the relationship between

financial barriers and firm performance, provide conflicting evidence. The study by

Journal of Strategic Marketing 29

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Thornton and Marche (2003) showed that many new market entrants indeed failed because

they were unable to secure sufficient funds from either venture capitalists or generate the

funds themselves. On the other hand, the research by Coltman et al. (2007) showed no

relationship between performance and financial barriers for aggregate analysis of the total

sample. However, the study indicated significant relationships when the authors used a

segmentation-based approach of latent variables modeling for the segment of firms driven

by organizational and financial constraints.

Many start-up firms entering markets require additional funding because they may not

earn any profit for some years. For example, Amazon.com did not report any profit until

2003 although it was launched in 1995. While capital requirements adversely affect firm

performance at the beginning, as the financial requirements increase, the height of entry

barriers increases, thereby preventing the new firms to enter the market. As a consequence,

the firm performance will increase eventually. Therefore, we expect a U-shaped

relationship between capital requirements and firm performance. This curvilinear

relationship may also explain the reasons why the earlier studies (Coltman et al., 2007;

Thornton & Marche, 2003) found conflicting results.

On the contrary, during initial market entry situations when the business environment

barrier is usually high, the incumbent firm performance increases because of the small

number of competitors in the market. This is also partially due to first mover advantages

held by incumbent firms (Usero & Fernandez, 2009). As the business environment barrier

becomes lower, new firms are able to enter the market. Some followers or later market

entrants are more successful than others. For example, the followers that take non-market

actions are more successful than the followers that take more market actions (Usero &

Fernandez, 2009). As a result, the firm performance of incumbent firms will gradually

decrease. Therefore, we expect an inverted U-shaped relationship between unfavorable

business environment barrier and market entrant performance. This is also consistent with

the order of market entry literature that provides abundant examples of early and late

market entry advantages such as better products, higher market shares and profits (see De

Castro & Chrisman, 1995; Kerin, Varadarajan, & Peterson, 1992; Robinson & Fornell,

1985; Usero & Fernandez, 2009). Based on the above opinions, we offer the following

hypotheses:

H7: The relationship between Capital Requirements barrier for market entrants and

Market Entrant Performance is U-shaped.

H8: The relationship between Unfavorable Business Environment barrier for market

entrants and Market Entrant Performance is inverted U-shaped.

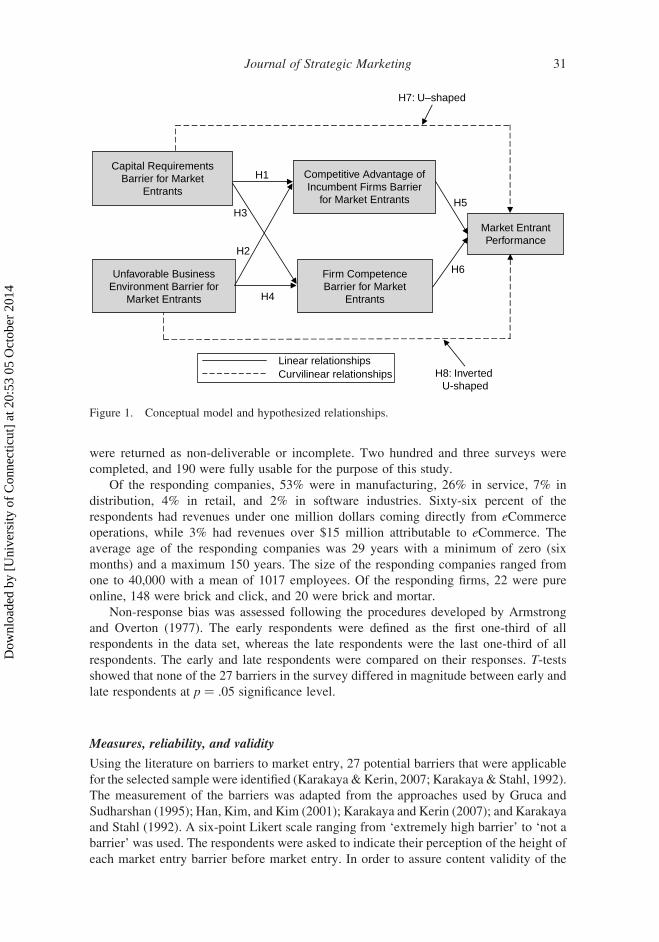

A conceptual model showing the relationships among the barriers, and performance

and the hypotheses is presented in Figure 1.

Methodology

Data collection

One thousand businesses located in the USA were randomly selected from a mailing list of

e-corporations directory. The business executives listed as the contact persons were

described as ‘top level professionals who are responsible for strategic business decisions

relating to the Internet’. A cover letter and the questionnaire were mailed to the selected

executives in the mailing list during spring 2009. A promise to provide the summary

results of the study was offered as an incentive to complete the survey. Thirty-two surveys

F. Karakaya and S. Parayitam30

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

were returned as non-deliverable or incomplete. Two hundred and three surveys were

completed, and 190 were fully usable for the purpose of this study.

Of the responding companies, 53% were in manufacturing, 26% in service, 7% in

distribution, 4% in retail, and 2% in software industries. Sixty-six percent of the

respondents had revenues under one million dollars coming directly from eCommerce

operations, while 3% had revenues over $15 million attributable to eCommerce. The

average age of the responding companies was 29 years with a minimum of zero (six

months) and a maximum 150 years. The size of the responding companies ranged from

one to 40,000 with a mean of 1017 employees. Of the responding firms, 22 were pure

online, 148 were brick and click, and 20 were brick and mortar.

Non-response bias was assessed following the procedures developed by Armstrong

and Overton (1977). The early respondents were defined as the first one-third of all

respondents in the data set, whereas the late respondents were the last one-third of all

respondents. The early and late respondents were compared on their responses. T-tests

showed that none of the 27 barriers in the survey differed in magnitude between early and

late respondents at p ¼ .05 significance level.

Measures, reliability, and validity

Using the literature on barriers to market entry, 27 potential barriers that were applicable

for the selected sample were identified (Karakaya &Kerin, 2007; Karakaya & Stahl, 1992).

The measurement of the barriers was adapted from the approaches used by Gruca and

Sudharshan (1995); Han, Kim, and Kim (2001); Karakaya and Kerin (2007); and Karakaya

and Stahl (1992). A six-point Likert scale ranging from ‘extremely high barrier’ to ‘not a

barrier’ was used. The respondents were asked to indicate their perception of the height of

each market entry barrier before market entry. In order to assure content validity of the

H7: U–shaped

H4

H1

H5H3

H2

H6

Capital RequirementsBarrier for Market

Entrants

Unfavorable BusinessEnvironment Barrier for

Market Entrants

Firm CompetenceBarrier for Market

Entrants

Market EntrantPerformance

Competitive Advantage ofIncumbent Firms Barrier

for Market Entrants

Linear relationshipsCurvilinear relationships H8: Inverted

U-shaped

Figure 1. Conceptual model and hypothesized relationships.

Journal of Strategic Marketing 31

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

questionnaire, the surveywas pre-testedwith 10 local eCommerce executives. Thewording

of a few questions was slightly modified based on their feedback.

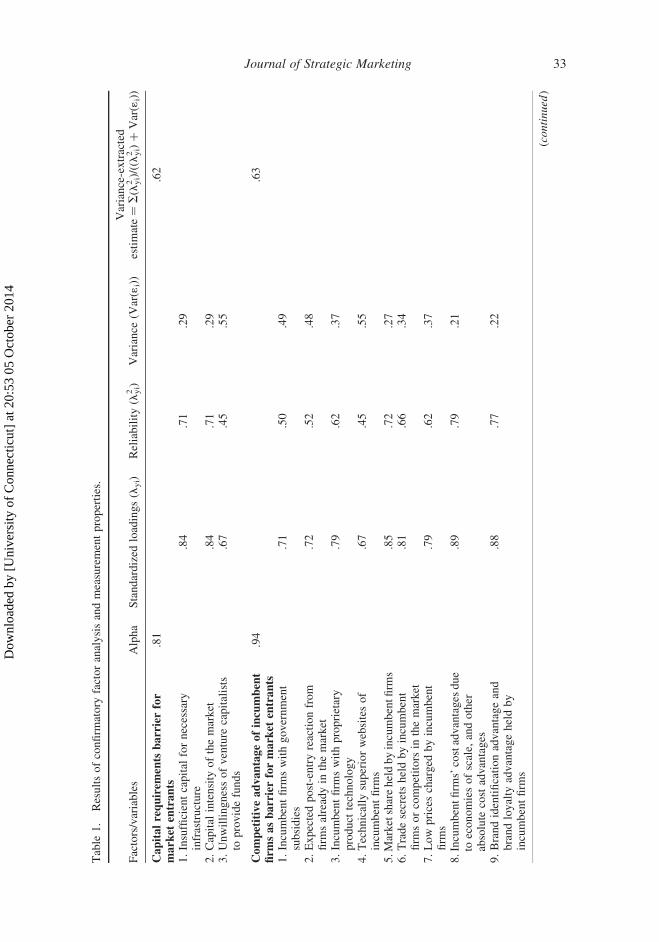

We followed the procedures outlined by Anderson and Gerbing (1988) by assessing

the reliability and unidimensionality of each construct. We conducted a confirmatory

factor analysis (CFA) using Lisrel. All of the items loaded on their respective constructs

were statistically significant. The results of the CFA for all variables and the measurement

properties are reported in Table 1. We also checked the measurement properties of the

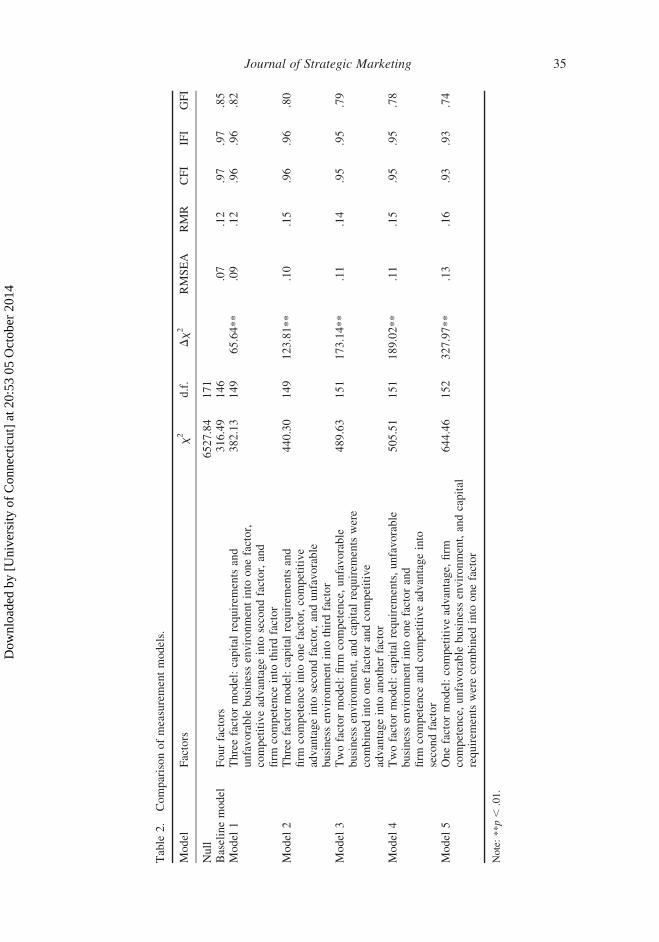

variables by comparing the baseline model with five alternate models. The comparison of

these models with the baseline model presented in Table 2 reveals the following goodness

of fit statistics: x2 ¼ 316.49 with d.f. ¼ 146; x2/d.f. ¼ 2.167; GFI ¼ 0.85; CFI ¼ 0.97;

RMSEA ¼ 0.07. Overall, these results suggest that the four-factor model renders evidence

of construct distinctiveness for firm competence, business environment, competitive

advantage, and capital requirements.

We further tested for discriminant validity by following the procedures outlined by

Fornell and Larcker (1981). We compared the square roots of the average variance

extracted (AVE) estimates of the measures with the correlation between constructs

(Table 3). The square roots of the AVEs (.79, .79, .68, and .71) are greater than all of the

corresponding correlations, thus indicating adequate discriminant validity.

As is the case in survey research, common method variance is a widely discussed and

complex problem (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003). From a

methodological standpoint, since we collected data from a single source, it is possible

that self-report and mono-method bias may threaten the validity of research (Podsakoff &

Organ, 1986). At the conceptual level, we addressed the problem by using the manifest

variables that are theoretically representative measures of latent constructs and

measurements that are unambiguous. In order to minimize the common-method bias,

we followed the procedures outlined by Podsakoff and Organ (1986) and conducted

Harman’s one factor test. More than a single factor emerged demonstrating that common

method variance does not exist. The social desirability effect was also addressed by having

the survey completed anonymously.

The capital requirements barrier for market entrants included items that assess the

market entrant’s perceptions of capital intensity of the market, willingness of venture

capitalists to provide funds, and the necessary capital for infrastructure. The reliability for

the capital requirements scale was strong, with an alpha of .81.

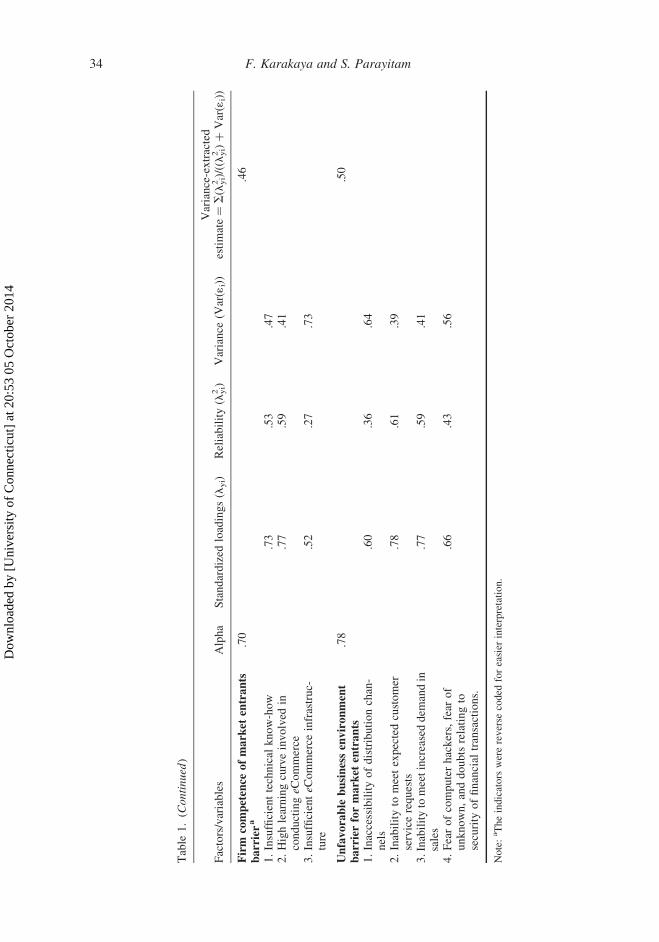

We measured the unfavorable business environment barrier for market entrants with

four items, on a six-point scale, drawing from the literature (Dubelaar et al., 2005; Razi

et al., 2004; Wen & Tarn, 2001). Unfavorable business environment is usually caused by

factors external to market entrants, but some external factors are likely to cause internal

problems. For example, inability to meet increased demand may be due to lack of supply

which then causes market entrants to view the business environment as negative. The

following items assessed the market entrant’s perception of the business environment:

inaccessibility of distribution channels; eCommerce security issues; inability to meet

increased demand; and inability to meet expected customer service requirements. The

alpha for the aggregated measure was .78.

We measured the competitive advantage of incumbent firms barrier for market entrants

using nine items, on a six-point scale, adapted from Karakaya and Kerin (2007) and

Karakaya and Stahl (1992). This measure captured the perception of the market entrants

about the competitive advantage enjoyed by the incumbent firms. The sample items of this

measure read as ‘Cost advantage of incumbent firms’, ‘Brand loyalty advantage of

incumbent firms’, ‘Trade secrets held by incumbent firms or competitors in the market’,

F. Karakaya and S. Parayitam32

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Table

1.

Resultsofconfirm

atory

factoranalysisandmeasurementproperties.

Factors/variables

Alpha

Standardized

loadings(l

yi)

Reliability(l

2 yi)

Variance

(Var(1

i))

Variance-extracted

estimate¼

S(l

2 yi)/((l

2 yi)þ

Var(1

i))

Capitalrequirem

ents

barrierfor

market

entrants

.81

.62

1.Insufficientcapital

fornecessary

infrastructure

.84

.71

.29

2.Capital

intensity

ofthemarket

.84

.71

.29

3.Unwillingnessofventure

capitalists

toprovidefunds

.67

.45

.55

Competitiveadvantageofincumbent

firm

sasbarrierformarket

entrants

.94

.63

1.Incumbentfirm

swithgovernment

subsidies

.71

.50

.49

2.Expectedpost-entryreactionfrom

firm

salreadyin

themarket

.72

.52

.48

3.Incumbentfirm

swithproprietary

product

technology

.79

.62

.37

4.Technically

superiorwebsitesof

incumbentfirm

s.67

.45

.55

5.M

arketshareheldbyincumbentfirm

s.85

.72

.27

6.Tradesecretsheldbyincumbent

firm

sorcompetitors

inthemarket

.81

.66

.34

7.Low

pricescharged

byincumbent

firm

s.79

.62

.37

8.Incumbentfirm

s’costadvantages

due

toeconomiesofscale,

andother

absolute

costadvantages

.89

.79

.21

9.Brandidentificationadvantageand

brandloyalty

advantageheldby

incumbentfirm

s

.88

.77

.22

(continued

)

Journal of Strategic Marketing 33

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Table

1.(C

ontinued

)

Factors/variables

Alpha

Standardized

loadings(l

yi)

Reliability(l

2 yi)

Variance

(Var(1

i))

Variance-extracted

estimate¼

S(l

2 yi)/((l

2 yi)þ

Var(1

i))

Firm

competence

ofmarket

entrants

barriera

.70

.46

1.Insufficienttechnical

know-how

.73

.53

.47

2.Highlearningcurveinvolved

inconductingeC

ommerce

.77

.59

.41

3.InsufficienteC

ommerce

infrastruc-

ture

.52

.27

.73

Unfavorable

businessenvironment

barrierformarket

entrants

.78

.50

1.Inaccessibilityofdistributionchan-

nels

.60

.36

.64

2.Inabilityto

meetexpectedcustomer

servicerequests

.78

.61

.39

3.Inabilityto

meetincreaseddem

andin

sales

.77

.59

.41

4.Fearofcomputerhackers,fear

of

unknown,anddoubtsrelatingto

security

offinancial

transactions.

.66

.43

.56

Note:aTheindicators

werereverse

coded

foreasier

interpretation.

F. Karakaya and S. Parayitam34

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Table

2.

Comparisonofmeasurementmodels.

Model

Factors

x2

d.f.

Dx2

RMSEA

RMR

CFI

IFI

GFI

Null

6527.84

171

Baselinemodel

Fourfactors

316.49

146

.07

.12

.97

.97

.85

Model

1Threefactormodel:capital

requirem

entsand

unfavorable

businessenvironmentinto

onefactor,

competitiveadvantageinto

secondfactor,and

firm

competence

into

thirdfactor

382.13

149

65.64**

.09

.12

.96

.96

.82

Model

2Threefactormodel:capital

requirem

entsand

firm

competence

into

onefactor,competitive

advantageinto

secondfactor,andunfavorable

businessenvironmentinto

thirdfactor

440.30

149

123.81**

.10

.15

.96

.96

.80

Model

3Twofactormodel:firm

competence,unfavorable

businessenvironment,andcapital

requirem

entswere

combined

into

onefactorandcompetitive

advantageinto

another

factor

489.63

151

173.14**

.11

.14

.95

.95

.79

Model

4Twofactormodel:capital

requirem

ents,unfavorable

businessenvironmentinto

onefactorand

firm

competence

andcompetitiveadvantageinto

secondfactor

505.51

151

189.02**

.11

.15

.95

.95

.78

Model

5Onefactormodel:competitiveadvantage,firm

competence,unfavorable

businessenvironment,andcapital

requirem

entswerecombined

into

onefactor

644.46

152

327.97**

.13

.16

.93

.93

.74

Note:**p,

.01.

Journal of Strategic Marketing 35

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Table

3.

Descriptivestatistics.

Variables

Mean

Standarddeviation

12

34

56

78

1.Age(years)

28.01

27.15

12.Size(number

of

employees)

1.69

.899

0.53***

1

3.eC

ommerce

experience

4.00

2.67

0.01

20.06

14.Competitiveadvantageof

incumbentfirm

sbarrier

2.72

1.16

0.13

0.10

20.17*

1

5.Firm

competence

barrier

3.34

1.11

0.23**

0.26**

20.18*

0.40*

16.Unfavorable

businessenvironment

barrier

2.58

0.99

0.16*

0.25**

20.15

0.65**

0.42***

1

7.Capital

requirem

entsbarrier

2.86

1.23

20.33

0.07

20.07

0.64***

0.29***

0.61***

18.Firm

perform

ance

2.23

0.57

0.29***

20.26**

0.13

20.26**

20.27**

20.19*

20.13

1

Note:***p,

.001;**p,

.01;*p,

.05.

F. Karakaya and S. Parayitam36

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

‘Technically superior websites of incumbent firms’, and ‘High market share held by

incumbent firms’. The alpha for the aggregated measure was .94.

Firm competence of market entrants was measured with three items, on a six-point

scale, developed by Allison (1999); Bingi, Mir, and Khamalah (2000); Darch and Lucas

(2002); Duan et al. (2002), and Dubelaar et al. (2005). These items measured the extent to

which market entrants perceive their own competence in terms of eCommerce

infrastructure, technical knowhow, and learning curve involved in conducting

eCommerce. The three items measuring this construct were reverse coded for easier

interpretation. The alpha for this construct was .70.

We measured firm performance of market entrants by combining three perceptual

variables. The market entrants were asked to assess: (a) their satisfaction with the

performance of eCommerce initiative; (b) the percent of sales attributable to eCommerce;

and (c) whether they achieved the return on investment as expected. The alpha for this

construct was .55.

The study also included three control variables of company age, size, and experience.

Company age was measured in terms of number of years in business. Company size was

measured by taking natural logarithm of the number of employees. eCommerce experience

was measured in terms of number of years the firm has engaged in eCommerce.

The hypotheses were tested using hierarchical regression analysis. All of the models

included the control variables prior to introducing the main effect variables. As suggested

by Aiken and West (1991), we used centered variables in regression analyses because this

procedure yields coefficients that are relatively free of multicollinearity.

To test the curvilinear relationships, the nature of quadratic function of ‘Dependent

Variable’ with respect to the ‘Independent Variable’ is examined. The quadratic function

is expressed as below:

Y ¼ b0 þ b1 Xþ b2X2

(a) The first-order condition for finding the maximum or minimum point is dY/dX ¼ 0;

(b) the second order condition for determining maximum point is d2Y/dX2 , 0 (which

implies that the slope of the curve after the maximum point is negative); and the second ordercondition for minimum point is d2Y/dX

2 . 0 (which implies that the slope of the curve afterthe minimum point is positive).

When b2 is negative, and d2Y/dX2 , 0; then the curve will be inverted U-shaped.

When b2 is positive, and d2Y/dX2 . 0; then the curve will be U-shaped.

We hypothesized that b2 is positive for capital requirements barrier for market

entrants, implying a U-shaped relationship between market entrant performance and

capital requirements barrier for market entrants. We also hypothesized that b2 is negative

for unfavorable business environment barrier for market entrants implying an inverted

U-shaped relationship between market entrant performance and unfavorable business

environment for market entrants.

Results

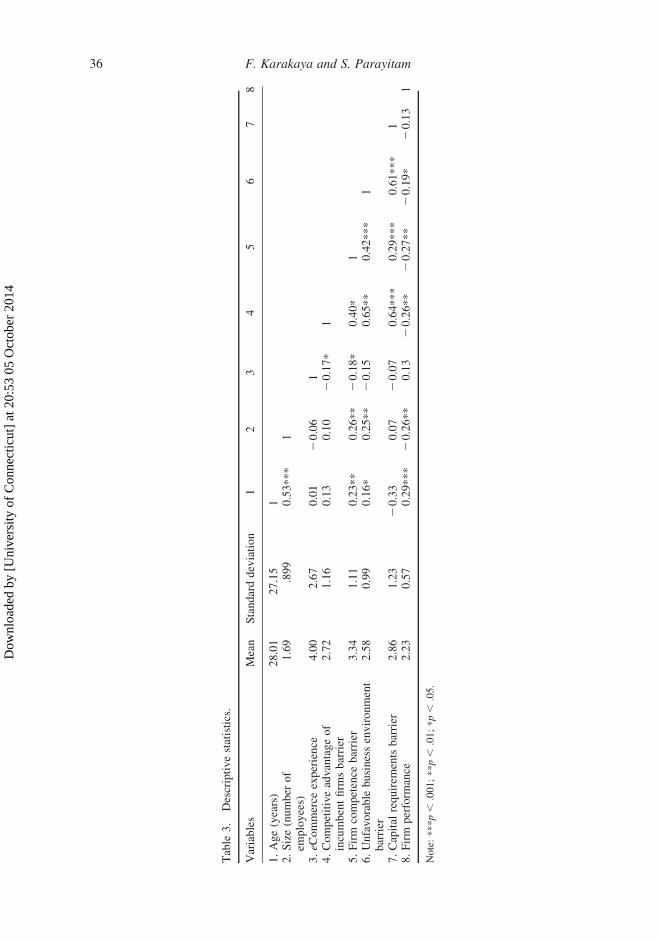

The means, standard deviations, and correlations among the variables studied are reported

in Table 3. The preliminary analysis of the correlations revealed significant positive

correlations between predictor variables. The largest correlation among the predictor

Journal of Strategic Marketing 37

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

variables was .65, which suggests multicollinearity was not a serious problem in this study

(Tsui, Ashford, St Clair, & Xin, 1995). Furthermore, the CFA provided discriminant

validity of the measures and suggested the jangle fallacy (high correlations between the

variables) was not a problem. As another check of multicollinearity, we examined the

variance inflation factor (VIF) of each independent variable, which showed no indication

of multicollinearity.

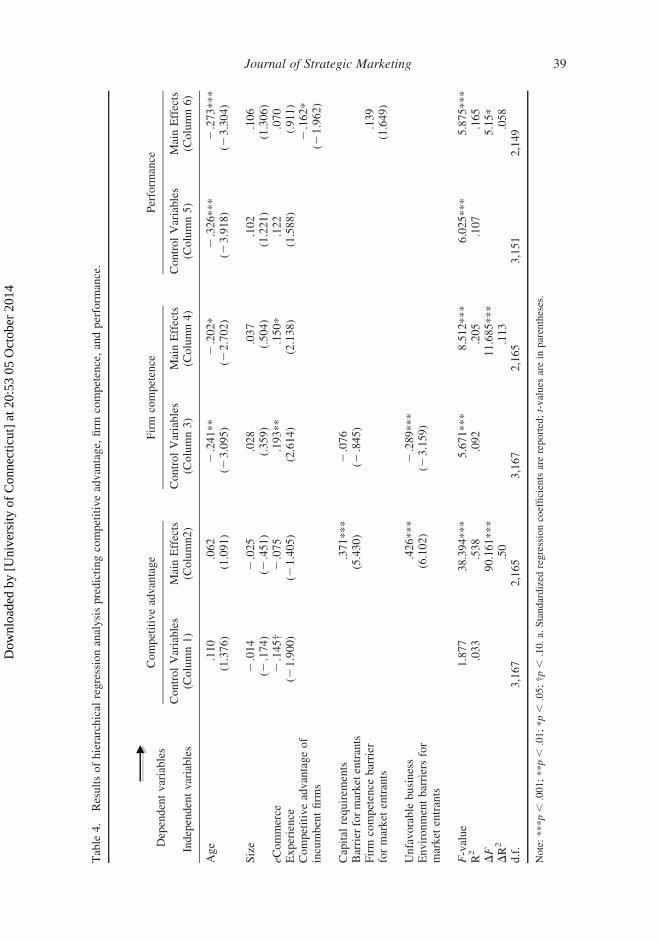

Table 4 presents the results of the hierarchical regression analyses predicting

competitive advantage of incumbent firms (H1 & H2), firm competence of market entrants

(H3 & H4), and performance (H5 & H6). Columns 1 and 2 in Table 4 show competitive

advantage of incumbent firms as dependent variables. In step 1, we entered the control

variables age, size, and eCommerce experience of firms. Of these control variables, only

eCommerce experience was somewhat significant (b ¼ .145, p , .10). The main effects

were entered in step 2 (Column 2). The results indicated that capital requirements

(b ¼ .371, p , .001) and business environment (b ¼ .426, p , .001) were significant.

The model was significant (F ¼ 38.39, p , .001; R2 ¼ .538), and explained 53.8 percent

of the variance in competitive advantage. The main effects model (DF ¼ 90.16, p , .001;

DR2 ¼ .50) explained an additional 50% variance when compared to the control variables

model. Thus, the results support H1 and H2.

The effects of the control variables on firm competence of market entrants are captured

in Column 3 of Table 4. Both company age and eCommerce experience were significant

predictors of firm competence. The regression coefficients of age (b ¼ 2 .241, p , .05)

and eCommerce experience (b ¼ .193, p , .05) are significant, and the model explained

9.2% of the variance in firm competence due to these control variables (F ¼ 5.67,

p , .001). The main effect variables were entered in step 2. Column 4 of Table 4 shows

the regression results. The regression coefficient of capital requirements barrier for market

entrants was not significant (b ¼ 2 .076, p . .10) whereas the regression coefficient of

business environment was significant (b ¼ 2 .289, p , .05). The main effects model

explained 20.5% of the variance in firm competence of market entrants and the model is

significant (F ¼ 8.51, p , .001; R2 ¼ .205; DF ¼ 11.68, p , .001; DR2 ¼ 0.113). These

results support H4 but do not support H3.

Table 4 also provides the regression results of competitive advantage of incumbent

firms and firm competence predicting firm performance. As seen in Column 5, the

regression coefficient of company age was significant (b ¼ 2 .326, p , .001), but the

other control variables were not significant. The regression model was significant,

explaining 10.7% of the variance in performance attributable to the control variables

(F ¼ 6.025, p , .001). The regression analysis in Column 5 of Table 4 revealed that in

addition to the company age (b ¼ 2 .273, p , .001), the competitive advantage was

significant (b ¼ 2 .162, p , .05), thus supporting H5. The regression coefficient of firm

competence was not significant (b ¼ .139, p . .10), not supporting H6. The regression

model was significant, explaining 16.5% variance in firm performance (F ¼ 5.87,

p , .001; R2 ¼ .165; DF ¼ 5.15, p , .05; DR2 ¼ .058).

Hypotheses 7 and 8 are related to curvilinear relationships between capital requirements

barrier, unfavorable business environment barrier, and market entrant performance.

We followed the procedures of Aiken andWest (1991) to test the curvilinear relationships.

The regression results are presented in Table 5. Column 1 of Table 5 shows the effects

of the control variables on firm performance (these are the same as Column 5 in Table 4).

Only company age was significant. In the main effects model (Column 2), again, only

company agewas significant (b ¼ 2 .271, p , .001). The squared terms of themain effects

variables were entered in step three of the regression analyses. Column 3 of Table 5 shows

F. Karakaya and S. Parayitam38

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Table

4.

Resultsofhierarchical

regressionanalysispredictingcompetitiveadvantage,firm

competence,andperform

ance.

Dependentvariables

Competitiveadvantage

Firm

competence

Perform

ance

Independentvariables

ControlVariables

(Column1)

MainEffects

(Column2)

ControlVariables

(Column3)

MainEffects

(Column4)

ControlVariables

(Column5)

MainEffects

(Column6)

Age

.110

.062

2.241**

2.202*

2.326***

2.273***

(1.376)

(1.091)

(23.095)

(22.702)

(23.918)

(23.304)

Size

2.014

2.025

.028

.037

.102

.106

(2.174)

(2.451)

(.359)

(.504)

(1.221)

(1.306)

eCommerce

2.145†

2.075

.193**

.150*

.122

.070

Experience

(21.900)

(21.405)

(2.614)

(2.138)

(1.588)

(.911)

Competitiveadvantageof

incumbentfirm

s2.162*

(21.962)

Capital

requirem

ents

.371***

2.076

Barrier

formarketentrants

(5.430)

(2.845)

Firm

competence

barrier

formarket

entrants

.139

(1.649)

Unfavorable

business

Environmentbarriersfor

market

entrants

.426***

(6.102)

2.289***

(23.159)

F-value

1.877

38.394***

5.671***

8.512***

6.025***

5.875***

R2

.033

.538

.092

.205

.107

.165

DF

90.161***

11.685***

5.15*

DR2

.50

.113

.058

d.f.

3,167

2,165

3,167

2,165

3,151

2,149

Note:***p,

.001;**p,

.01;*p,

.05;†p,

.10.a.Standardized

regressioncoefficientsarereported;t-values

arein

parentheses.

Journal of Strategic Marketing 39

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

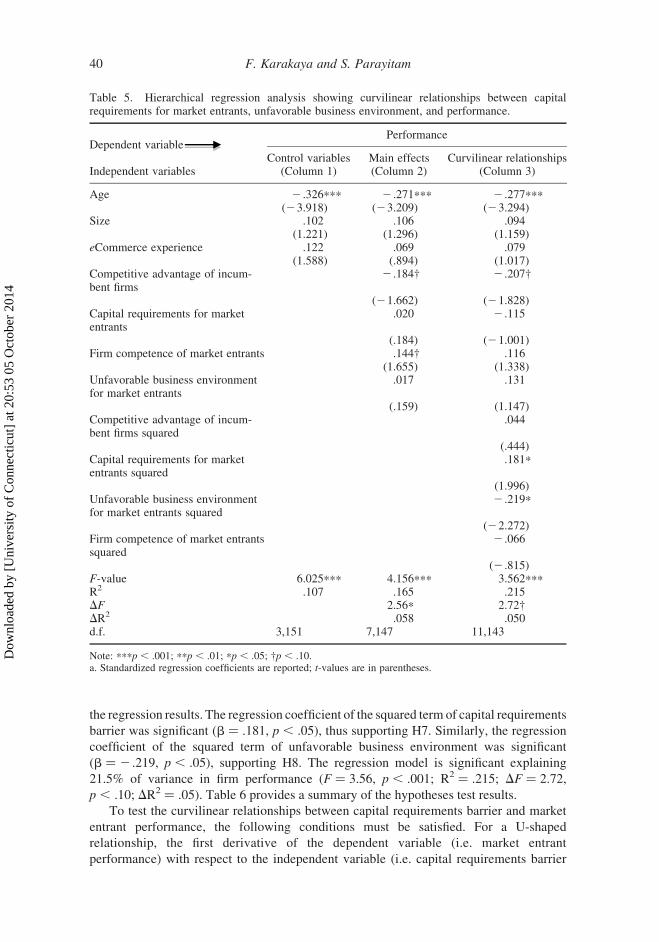

the regression results. The regression coefficient of the squared term of capital requirements

barrier was significant (b ¼ .181, p , .05), thus supporting H7. Similarly, the regression

coefficient of the squared term of unfavorable business environment was significant

(b ¼ 2 .219, p , .05), supporting H8. The regression model is significant explaining

21.5% of variance in firm performance (F ¼ 3.56, p , .001; R2 ¼ .215; DF ¼ 2.72,

p , .10; DR2 ¼ .05). Table 6 provides a summary of the hypotheses test results.

To test the curvilinear relationships between capital requirements barrier and market

entrant performance, the following conditions must be satisfied. For a U-shaped

relationship, the first derivative of the dependent variable (i.e. market entrant

performance) with respect to the independent variable (i.e. capital requirements barrier

Table 5. Hierarchical regression analysis showing curvilinear relationships between capitalrequirements for market entrants, unfavorable business environment, and performance.

Dependent variablePerformance

Independent variablesControl variables

(Column 1)Main effects(Column 2)

Curvilinear relationships(Column 3)

Age 2 .326*** 2 .271*** 2 .277***(23.918) (23.209) (23.294)

Size .102 .106 .094(1.221) (1.296) (1.159)

eCommerce experience .122 .069 .079(1.588) (.894) (1.017)

Competitive advantage of incum-bent firms

2 .184† 2 .207†

(21.662) (21.828)Capital requirements for marketentrants

.020 2 .115

(.184) (21.001)Firm competence of market entrants .144† .116

(1.655) (1.338)Unfavorable business environmentfor market entrants

.017 .131

(.159) (1.147)Competitive advantage of incum-bent firms squared

.044

(.444)Capital requirements for marketentrants squared

.181*

(1.996)Unfavorable business environmentfor market entrants squared

2 .219*

(22.272)Firm competence of market entrantssquared

2 .066

(2 .815)F-value 6.025*** 4.156*** 3.562***R2 .107 .165 .215DF 2.56* 2.72†DR2 .058 .050d.f. 3,151 7,147 11,143

Note: ***p , .001; **p , .01; *p , .05; †p , .10.a. Standardized regression coefficients are reported; t-values are in parentheses.

F. Karakaya and S. Parayitam40

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

for market entrants) must be equal to zero, and the second derivative of the Y with respect

to X must be greater than zero.

The quadratic curve fit of firm performance as dependent variable and capital

requirements as independent variable form the following equation:

Y ðFirm PerformanceÞ ¼ 2:1812 0:085Xþ 0:044X2 whereX ¼ Capital Requirements

dY=dX ¼ 20:085þ 0:088X ¼ 0 ð1Þ

d2Y=dX2 ¼ 0:362 . 0 ð2Þ

This positive second derivative implies that the curve is U-shaped.

By solving for X from Equation (1) we obtain X ¼ 0.965.

Since the second derivative of the function is greater than zero, the function has a

minimum value of 2.13 at X ¼ 0.965.

½Y ¼ 2:1812 ð0:085Þð0:965Þ þ 0:044ð0:965Þ2 ¼ 2:13�

These results show that the relationship between capital requirements and firm

performance is U-shaped.

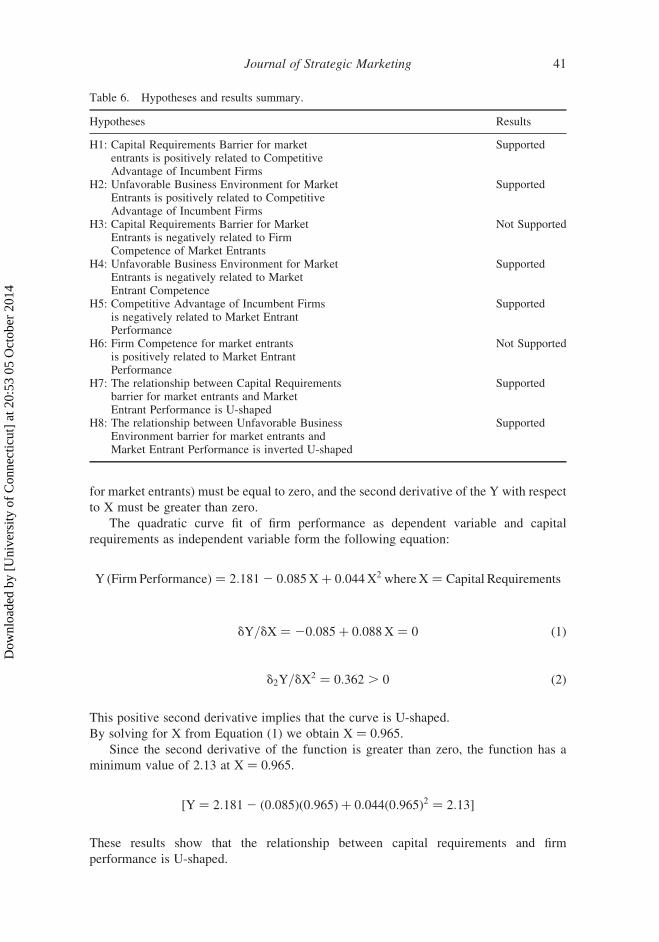

Table 6. Hypotheses and results summary.

Hypotheses Results

H1: Capital Requirements Barrier for marketentrants is positively related to CompetitiveAdvantage of Incumbent Firms

Supported

H2: Unfavorable Business Environment for MarketEntrants is positively related to CompetitiveAdvantage of Incumbent Firms

Supported

H3: Capital Requirements Barrier for MarketEntrants is negatively related to FirmCompetence of Market Entrants

Not Supported

H4: Unfavorable Business Environment for MarketEntrants is negatively related to MarketEntrant Competence

Supported

H5: Competitive Advantage of Incumbent Firmsis negatively related to Market EntrantPerformance

Supported

H6: Firm Competence for market entrantsis positively related to Market EntrantPerformance

Not Supported

H7: The relationship between Capital Requirementsbarrier for market entrants and MarketEntrant Performance is U-shaped

Supported

H8: The relationship between Unfavorable BusinessEnvironment barrier for market entrants andMarket Entrant Performance is inverted U-shaped

Supported

Journal of Strategic Marketing 41

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

The quadratic curve fit of firm performance as dependent variable and unfavorable

business environment as independent variable is captured hereunder:

Y ðFirm PerformanceÞ ¼ 2:2882 0:081Xþ 0:043X2 where X ¼ Business Environment

dY=dX ¼ 20:0812 0:086X ¼ 0 ð1Þ

d2Y=dX2 ¼ 20:086 , 0 ð2Þ

This negative value of the second derivative implies that the curve is inverted-U shaped.

By solving for X from Equation (1) we obtain X ¼ 20.941.

Since the second derivative of the function is greater than zero, the function has a

maximum value of 2.33 at X ¼ 20.941.

½Y ¼ 2:1812 ð0:081Þð20:941Þ2 0:043ð20:941Þ2 ¼ 2:33�

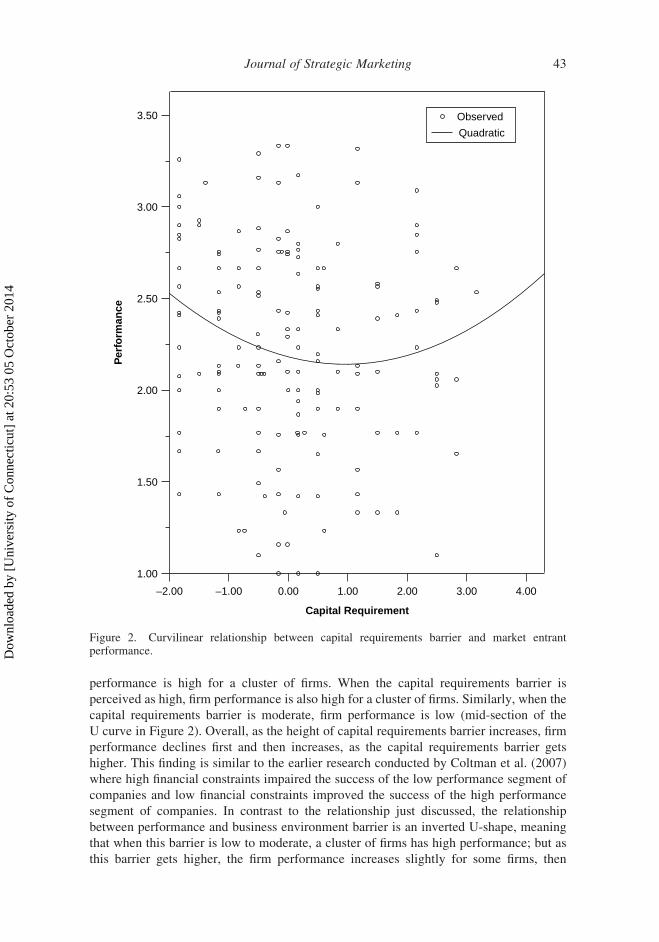

For plotting the curvilinear relationship between capital requirements formarket entrants and

firm performance, we used the intercept of 2.181, with the coefficient of capital requirements

(b1 ¼ 2 .85) and the coefficient of the squared term of capital requirements (b2 ¼ .44). This

plot also supports the hypothesized U-shaped curvilinear relationship between capital

requirements and firm performance (H7). Figure 2 captures this relationship.

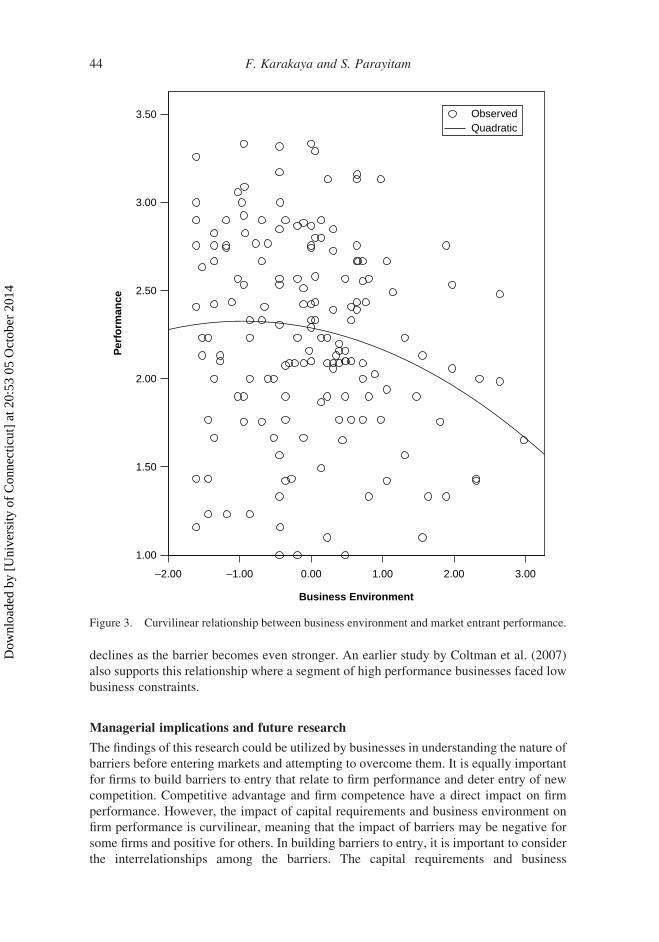

It was hypothesized that the relationship between business environment and firm

performance would be inverted U-shaped. For plotting the curvilinear relationship, we

used the intercept of 2.28 and the regression coefficients for the business environment and

the squared term business environment (b1 ¼ 2 .88; and b2 ¼ 0.43 respectively). The plot

presents an inverted U-shaped curvilinear relationship between business environment and

firm performance as seen in Figure 3. Thus, H8 is supported.

Discussion and conclusions

The goal of this research was to examine the interrelationships among barriers to market

entry and test the impact of barriers on firm performance while controlling for firm

characteristics. As the results show, capital requirements and business environment

barriers have a positive impact on competitive advantage. In other words, higher capital

requirements and higher business environment barriers give incumbent firms higher

competitive advantage, which is itself a major barrier to entry. The capital requirements

barrier does not impact firm competence but the unfavorable business environment barrier

negatively affects firm competence. Lower business environment barrier results in higher

firm competence. As expected, the competitive advantage of incumbent firms negatively

impacts performance of market entrants while the firm competence has marginal effect on

performance of market entrants. When the competitive advantage of incumbent firms is

high, the performance of new market entrants is low. The relationship between firm

performance and firm competence is weak but positive, meaning that a stronger firm

competence would lead to a stronger firm performance.

There is a curvilinear relationship between firm performance and capital requirements

and the business environment barriers. It appears that a cluster of firms perceiving capital

requirements as a high barrier also has high performance, but as the perception of capital

requirements barrier becomes low, firm performance declines, but then increases as the

capital requirements barrier continues to get higher. From the U-shaped relationship, one

can also see that when the capital requirement barrier is perceived as low, firm

F. Karakaya and S. Parayitam42

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

performance is high for a cluster of firms. When the capital requirements barrier is

perceived as high, firm performance is also high for a cluster of firms. Similarly, when the

capital requirements barrier is moderate, firm performance is low (mid-section of the

U curve in Figure 2). Overall, as the height of capital requirements barrier increases, firm

performance declines first and then increases, as the capital requirements barrier gets

higher. This finding is similar to the earlier research conducted by Coltman et al. (2007)

where high financial constraints impaired the success of the low performance segment of

companies and low financial constraints improved the success of the high performance

segment of companies. In contrast to the relationship just discussed, the relationship

between performance and business environment barrier is an inverted U-shape, meaning

that when this barrier is low to moderate, a cluster of firms has high performance; but as

this barrier gets higher, the firm performance increases slightly for some firms, then

3.50

3.00

2.50

2.00

Per

form

ance

1.50

1.00

–2.00 –1.00 0.00 1.00 2.00 3.00 4.00

Capital Requirement

Observed

Quadratic

Figure 2. Curvilinear relationship between capital requirements barrier and market entrantperformance.

Journal of Strategic Marketing 43

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

declines as the barrier becomes even stronger. An earlier study by Coltman et al. (2007)

also supports this relationship where a segment of high performance businesses faced low

business constraints.

Managerial implications and future research

The findings of this research could be utilized by businesses in understanding the nature of

barriers before entering markets and attempting to overcome them. It is equally important

for firms to build barriers to entry that relate to firm performance and deter entry of new

competition. Competitive advantage and firm competence have a direct impact on firm

performance. However, the impact of capital requirements and business environment on

firm performance is curvilinear, meaning that the impact of barriers may be negative for

some firms and positive for others. In building barriers to entry, it is important to consider

the interrelationships among the barriers. The capital requirements and business

3.50

3.00

2.50

2.00

1.50

1.00

Per

form

ance

–2.00 –1.00 0.00 1.00 2.00 3.00

Business Environment

ObservedQuadratic

Figure 3. Curvilinear relationship between business environment and market entrant performance.

F. Karakaya and S. Parayitam44

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

environment barriers impact the competitive advantage barrier. Similarly, the unfavorable

business environment barrier impacts firm competence. Therefore, firms should attempt to

build competitive advantage and strengthen their competence, which is more controllable

compared to other barriers to entry.

While this study showed high reliability and validity of the measures used, it also has

some limitations. First, the study has a generalizability dilemma. We only focused on

market entry into eCommerce markets. Thus, we can only say that the results apply to the

eCommerce markets despite the fact that the respondents come from a variety of other

industries. We suggest that the present model can be extended to include other markets in

general. Second, although we tested a large number of barriers to market entry, it is

possible to have other barriers in different markets. Future research could include other

industries and compare the differences in the magnitude of barriers.

The present research attempted to study the relationships between barriers to market

entry and firm performance. Interestingly, the study revealed some linear relationships and

some curvilinear relationships implying that future researchers need to focus on quadratic

moderated relationships between the barriers to market entry and firm performance. This

study did not consider firm strategy. It is highly likely that firm strategy and barriers to

entry are related and firm strategy affects firm performance. Therefore, examining specific

firm strategies and linking them to barriers to entry and performance is an area of research

that can prove beneficial and contribute to the literature. Furthermore, longitudinal studies

can help in identifying some reciprocal relationships between the variables. The present

study adds to the current theoretical work and provides some avenues for future research.

References

Agarwal, R., & Prasad, J. (1998). A conceptual and operational definition of personal innovativenessin the domain of information technology. Information Systems Research, 9, 204–215.

Aiken, L.S., &West, S. (1991).Multiple regression: Testing and interpreting interactions. NewburyPark, CA: Sage.

Allison, L.K. (1999). Information systems professional development: A work-based learning model.Journal of Contemporary Professional Development, 2(3), 86–92.

Anderson, J.C., & Gerbing, D.W. (1988). Structural equation modeling in practice: A review andrecommended two-step approach. Psychological Bulletin, 103, 411–423.

Armstrong, J., & Overton, T. (1977). Estimating nonresponse bias in mail surveys. Journal ofMarketing Research, 14, 396–402.

Bain, J. (1956). Barriers to new competition. Cambridge, MA: Harvard University Press.Barney, J.B. (1986). Strategic factor markets, expectations, luck, and business strategy.Management

Science, 32, 1231–1241.Barney, J.B. (1991). Firm resources and sustained competitive advantage. Journal of Management,

17, 1231–1241.Bharadwaj, A.S. (2000). A resource-based perspective on information technology capability and

firm performance: An empirical investigation. MIS Quarterly, 24, 169–196.Bingi, P., Mir, A., & Khamalah, J. (2000). The challenges facing global ecommerce. Information

Systems Management, 17(4), 26–34.Burch, D.S., & Smiley, R. (1992). Who deters entry? Evidence on the use of strategic entry

deterrence. Review of Economics and Statistics, 74, 509–521.Cicic, M., Patterson, P., & Shoham, A. (2002). Antecedents of international performance: A service

firms’ perspective. European Journal of Marketing, 36, 1103–1118.Cochran, J.J., Darrat, A.F., & Elkhal, K. (2006). On the bankruptcy of internet companies: An

empirical inquiry. Journal of Business Research, 59, 1193–1200.Coeurderoy, R., & Durand, R. (2004). Leveraging the advantage of early entry: Proprietary

technologies versus cost leadership. Journal of Business Research, 57(6), 583–590.Collis, D.J., & Montgomery, C.A. (2008). Competing on resources. Harvard Business Review,

86(7/8), 140–150.

Journal of Strategic Marketing 45

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Coltman, T.R., Devinney, T.M., & Midgley, D.F. (2007). E-business strategy and firm performance:A latent class assessment of the drivers and impediments to success. Journal InformationTechnology, 22(2), 87–102.

Cooper, R.B., & Zmud, W. (1990). Information technology implementation research: Atechnological diffusion approach. Management Science, 36, 123–139.

Darch, H., & Lucas, T. (2002). Training as an eCommerceEnabler. Journal of Workplace Learning,14(4), 148–155.

De Castro, J.O., & Chrisman, J.J. (1995). Order of market entry, competitive strategy, and financialperformance. Journal Business Research, 33, 165–177.

Dierickx, I., & Cool, K. (1989). Asset stock accumulation and sustainability of competitiveadvantage. Management Science, 35, 1504–1511.

Duan, Y., Mullins, R., Hamblin, D., & Stanek, S. (2002). Addressing ICTs skill challenges in SMEs:Insights from three country investigations. Journal of European Industrial Training, 26,430–441.

Dubelaar, C., Sohal, A., & Savic, V. (2005). Benefits, impediments and critical success factors inB2C e-business adoption. Technovation, 25, 1251–1262.

Forman, C. (2005). The corporate digital divide: Determinants of internet adoption. ManagementScience, 51, 641–654.

Fornell, C., & Larcker, D.F. (1981). Evaluating structural equation models with unobservablevariables and measurement error. Journal Mark Res, 18, 39–50.

Fruhling, A.L., & Digman, L.A. (2000). The impact of electronic commerce on business-levelstrategies. Journal of Electronic Commerce Research, 1, 13–23.

Fuentelsaz, L., Gomez, J., & Polo, Y. (2002). Followers’ entry timing: Evidence from the Spanishbanking sector after deregulation. Strategic Management Journal, 23, 245–264.

Grant, R.M. (1991). The resource-based theory of competitive advantage: Implications for strategyformulation. California Management Review, 33(3), 114–135.

Gruca, T.S., & Sudharshan, D. (1995). A framework for entry deterrence strategy: The competitiveenvironment, choices, and consequences. Journal of Marketing, 59(3), 44–55.

Hadaya, P., & Pellerin, R. (2008). Determinants of manufacturing firms’ intent to use web-basedsystems to share inventory information with their key suppliers. International Journal ofE-Collaboration, 4(2), 29–54.

Han, J.K., Kim, N., & Kim, H.B. (2001). Entry barriers: A dull-, one-, or two-edged sword forincumbents? Unraveling the paradox from a contingency perspective. Journal of Marketing,65(1), 1–14.

Iacovou, C.L., Benbasatand, I., & Dexter, A.S. (1995). Electronic data interchange and smallorganizations: Adoption and impact of technology. MIS Quarterly, 19, 465–485.

Johnson, J.Y., & Tellis, G.J. (2008). Drivers of success for market entry into China and India.Journal of Marketing, 72(3), 1–13.

Karakaya, F., & Kerin, R. (2007). Impact of product life cycle stages on barriers to entry. JournalStrategic Marketing, 15, 287–298.

Karakaya, F., & Stahl, M.J. (1989). Barriers to entry and market entry decisions in consumer &industrial goods markets. Journal of Marketing, 53(2), 80–91.

Karakaya, F., & Stahl, M.J. (1992). Underlying dimensions of barriers to entry in consumer goodsmarkets. Journal of the Academy of Marketing Science, 20, 275–278.

Karakaya, F., & Yannopoulos, P. (2010). Defensive strategy framework in global markets: A mentalmodels approach. Euro Journal of Marketing, 44, 1077–1100.

Kerin, R.A., Varadarajan, P.R., & Peterson, R.A. (1992). First-mover advantage: A synthesis,conceptual framework. Journal of Marketing, 56(4), 33–52.

Kor, Y.Y., &Mahoney, J.T. (2004). Edith Penrose’s (1959) contributions to the resource-based viewof strategic management. Journal of Management Studies, 41, 183–191.

Mahoney, J.T. (1995). The management of resources and the resource of management. JournalBusiness Research, 33(2), 91–101.

Markides, C. (1997). Strategic innovation. Sloan Management Review, 38(3), 9–23.Olusoga, S., Mokwa, M.P., & Noble, C.H. (1995). Strategic groups, mobility barriers, and

competitive advantage: An empirical investigation. Journal of Business Research, 33, 153–163.Patterson, P.G., & Cicic, M. (1995). A typology of service firms in international markets: An

empirical investigation. Journal of International Marketing, 3(4), 57–83.

F. Karakaya and S. Parayitam46

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4

Pehrsson, A. (2009). Barriers to entry and market strategy: A literature review and a proposed model.European Business Review, 21, 64–77.

Peteraf, M.A., & Barney, J.B. (2003). Unraveling the resource based tangle. Managerial andDecision Economics, 24, 309–323.

Podsakoff, P.M., MacKenzie, S.B., Lee, J.-Y., & Podsakoff, N.P. (2003). Common method biases inbehavioral research: A critical review of the literature & recommended remedies. Journal ofApplied Psychology, 88, 879–903.

Podsakoff, P.M., & Organ, D.W. (1986). Self-reports in organizational research: Problems &prospects. Journal of Management, 12, 531–544.

Porter, M.E. (1985). Competitive advantage: Creating and sustaining superior performance. NewYork: The Free Press.

Priem, R.L., & Butler, J.E. (2001). Is the resource-based ‘view’ a useful perspective for strategicmanagement research? Academy of Management Review, 26, 22–40.

Razi, M.A., Tarn, M.J., & Siddiqui, F.A. (2004). Exploring the failure and success of dotcoms.Information Management & Computer Security, 12, 228–244.

Rennhoff, A. (2008). Paying for shelf space: An investigation of merchandising allowances in thegrocery industry. Journal of Agricultural and Food Industrial Organization, 6, 1542–1585.

Robinson, W.T., & Fornell, C. (1985). Sources of market pioneering advantages in consumer goodsmarkets. Journal of Marketing, 7(4), 219–242.

Ruiz-Ortega, M., & Garcıa-Villaverde, P. (2008). Capabilities & competitive tactics influences onperformance: Implications of the moment of entry. Journal of Business Research, 61, 332–345.

Santhanam, R., & Hartono, E. (2003). Issues in linking IT capability to firm performance. MISQuarterly, 27, 125–153.

Sashi, C.M., & Stern, L.W. (1995). Product differentiation and market performance in producergoods industries. Journal of Business Research, 33, 115–127.

Shoham, A., & Albaum, G.S. (1995). Reducing the impact of barriers to exporting: A managerialperspective. Journal of International Marketing, 3(4), 85–106.

Simon, D. (2005). Incumbent pricing responses to entry. Strategic Management Journal, 26,1229–1244.

Simon, H. (1996). Hidden champions. Boston, MA: Harvard Business School Press.Stockdale, R., & Standing, C. (2004). Benefits and barriers of electronic marketplace participation:

An SME perspective. Journal of Enterprise Information Management, 17, 301–311.Stockdale, R., & Standing, C. (2006). A classification model to support SME ecommerce adoption

initiatives. Journal of Small Business and Enterprise Development, 13, 381–394.Thornton, J., & Marche, S. (2003). Sorting through the dot bomb rubble: How did the high-profile

e-tailers fail? Info Man., 23, 121–138.Tippins, M., & Sohi, R. (2003). IT competency and firm performance: Is organizational learning a

missing link? Strategic Management Journal, 24, 745–761.To, M.L., & Ngai, E.W.T. (2006). Predicting the organizational adoption of B2C ecommerce: An

empirical study. Industrial Management and Data Systems, 106, 1133–1147.Tsui, A.S., Ashford, S.J., St Clair, L., & Xin, K.R. (1995). Dealing with discrepant expectations:

Response strategies and managerial effectiveness. Academy of Management Journal, 38,1515–1543.

Usero, B., & Fernandez, Z. (2009). First come, first served: How market and non-market actionsinfluence pioneer market share. Journal of Business Research, 62, 1139–1145.

Wade, M., & Holland, J. (2004). The RBV and IS research: Review, extension and suggestions forfuture research. MIS Quarterly, 28, 107–142.

Wen, J.H., & Tarn, M.J. (2001). The impact of the next generation internet protocol on ecommercesecurity. Information Strategy: The Executive Journal, 17(2), 22–28.

Wernerfelt, B. (1984). A resource based view of the firm. Strategic Management Journal, 5,171–180.

Zhu, K., Kraemer, K.L., & Xu, S. (2003). E-business adoption by European firms: A cross-countryassessment of the facilitators and inhibitors. European Journal of Information Systems, 12,251–268.

Journal of Strategic Marketing 47

Dow

nloa

ded

by [

Uni

vers

ity o

f C

onne

ctic

ut]

at 2

0:53

05

Oct

ober

201

4