barclays ceo energy/power conference - encana.com · barclays ceo energy/power conference eric...

TRANSCRIPT

Encana Corporation

Barclays CEO Energy/Power Conference

Eric Marsh | Executive Vice-President, Encana Corp. & Sr. Vice-President, USA Division

September 6, 2012 | New York, NY

take a closer look

1

2

Greater Sierra (inc. Horn River)

Duvernay

Cutbank Ridge (inc. Montney)

Bighorn

Coalbed Methane

Jonah

DJ NiobraraNiobrara/Mancos

Piceance

TexasHaynesville

Tuscaloosa

*Excludes confidential land.

Collingwood/Utica

Deep Panuke

Encana CorporationLeading North American Resource Play Company

Kitimat LNG Export Project

Existing Key Resource Play

New Liquids Play

Mississippian LimeSan Juan

Eaglebine

Production Volumes

• 2011 Actual:

•

Natural Gas (MMcf/d)Liquids (Mbbls/d)

2012 Forecast:Natural Gas (MMcf/d)Liquids (Mbbls/d)

3,33324

3,00030

Clearwater Oil

3

Accelerate pace of investment in oil and liquids rich natural gas plays

Minimize dry natural gas investments Enhance financial strength and flexibility through

multiple joint ventures and divestitures Continue to achieve industry leading cost structures

Maintaining Financial Strength While Transitioning to a More Diversified Portfolio

2

4

Building Momentum65% Two Year Liquids CAGR*

2011 2012F 2013F

Capital Investment ($B) 4.6 3.5 4.0 – 5.0

Net Divestitures ($B) 1.6 3.0 1.0 – 1.5

Net Capital Investment ($B) 3.0 0.5 3.0 – 3.5

Natural Gas (Bcf/d) 3.3 3.0 2.9 – 3.1

Oil (Mbbls/d) 14.6 15.6 25 – 30

NGLs (Mbbls/d) 9.4 14.4 35 – 40

Total Liquids (Mbbls/d) 24 30 60 – 70

Cash Flow ($B) 4.2 3.5 2.5 – 3.5

Total Debt ($B) 8.2 7.7 7.2

Cash ($B) 0.8 2.5 1.0

Net Debt ($B) 7.4 5.2 6.2

Based on mid point of 2013F liquids production.

5

Balancing Our Operating Cash FlowGrowing Contribution from Oil and NGLs

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

2011 2012F 2013F

Oil NGLs Natural Gas

$ Billions

2012F operating cash flow based on guidance as at June 20, 20112. 2013F operating cash flow based on mid-point of $4.0 - $5.0 capital investment.

9% 6%

85%

81%

12%7%

57%

21%22%

Operating Cash Flow by Commodity

3

6

Base capital program funded by cash flow Expect to achieve net divestitures of $1.0B - $1.5B High degree of confidence in our ability to execute joint ventures and

divestitures Will only spend beyond cash flow once additional proceeds are secured

through divestitures or JVs

2013 Capital Program Funding SourcesMaintaining Financial Strength & Flexibility a Top Priority

4

Capital ($B)

2

0

1

3

5Expected proceeds

Preliminary Projections of 2013 Capital

Base program

Additional proceeds

Minimum expected proceeds

2013F cash flow generation $2.5B - $3.5B

Assumptions: 2013F NYMEX $3.50, WTI $90, NGLs 40% of WTI; hedge price is $5.24 on 500 MMcf/d. Field condensate booked as oil.

7

Transitioning to a More Balanced PortfolioAccelerating Pace of Development in Oil & Liquids Rich Natural Gas Plays

Liquids PlayOriginal 2012FWells

Current 2012F Wells

Duvernay 5 - 10 10

Tuscaloosa 5 12

DJ Basin Niobrara 10+ 12

Eaglebine 6 12

Piceance Niobrara/Mancos

5+ 5+

San Juan 5 12

Collingwood/Utica - 5

Mississippian Lime - 15

Clearwater Oil - 30

Other 2 – 5 2 - 5

Total 40 - 45 115 - 120

Increased oil and liquids rich natural gas land position to ~3 million net acres over past 3 years

Accelerated pace of exploration and delineation

Achieved technical success across most plays

Expect to drill up to 350 wells in 2013

Expect multiple plays to reach commerciality in 2012

Expect meaningful contribution to 2013F production and cash flow

4

8

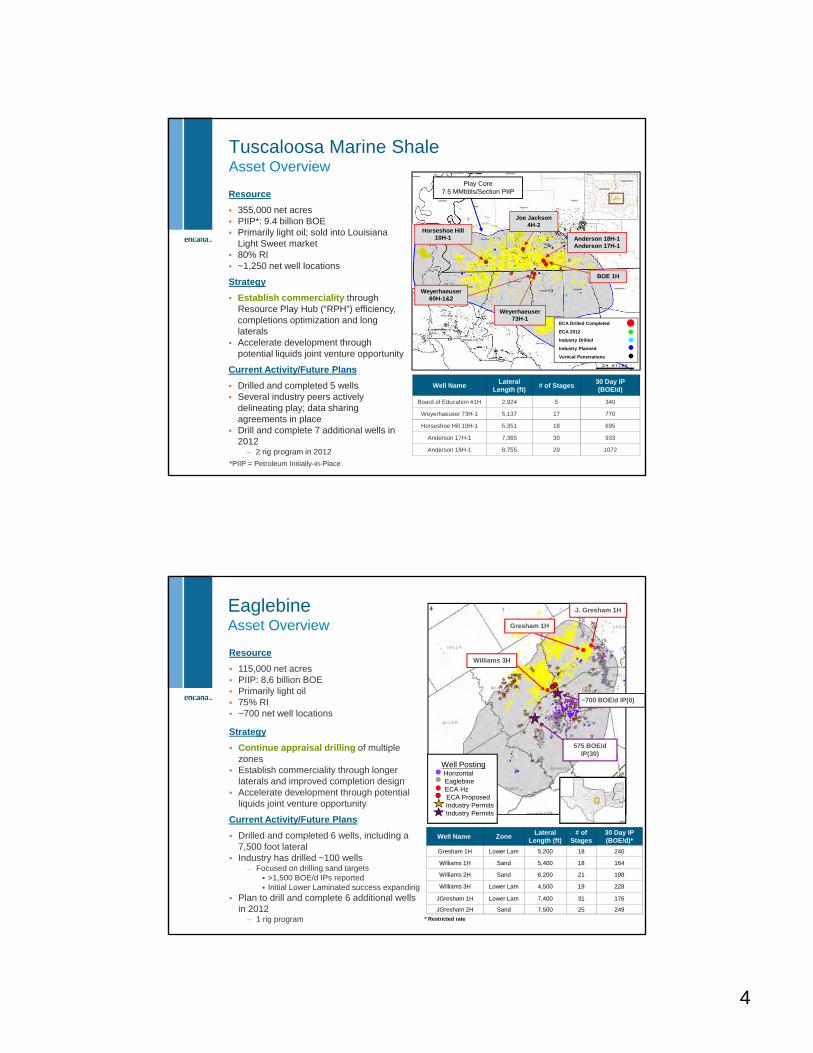

Tuscaloosa Marine Shale Asset Overview

Weyerhaeuser 73H-1

BOE 1H

Anderson 18H-1 Anderson 17H-1

Joe Jackson 4H-2

Play Core 7.5 MMbbls/Section PIIP

ECA Drilled Completed

ECA 2012

Industry Drilled

Industry Planned

Vertical Penetrations

Well NameLateral

Length (ft)# of Stages

30 Day IP (BOE/d)

Board of Education #1H 2,924 5 340

Weyerhaeuser 73H-1 5,137 17 770

Horseshoe Hill 10H-1 5,351 18 695

Anderson 17H-1 7,365 30 933

Anderson 18H-1 8,755 29 1072

Weyerhaeuser 60H-1&2

Horseshoe Hill 10H-1

Resource

355,000 net acres PIIP*: 9.4 billion BOE Primarily light oil; sold into Louisiana

Light Sweet market 80% RI ~1,250 net well locations

Strategy

Establish commerciality through Resource Play Hub (“RPH”) efficiency, completions optimization and long laterals

Accelerate development through potential liquids joint venture opportunity

Current Activity/Future Plans

Drilled and completed 5 wells Several industry peers actively

delineating play; data sharing agreements in place

Drill and complete 7 additional wells in 2012

– 2 rig program in 2012

*PIIP = Petroleum Initially-in-Place

9

EaglebineAsset Overview

Well Name ZoneLateral

Length (ft)# of

Stages30 Day IP (BOE/d)*

Gresham 1H Lower Lam 5,200 18 240

Williams 1H Sand 5,400 18 164

Williams 2H Sand 6,200 21 198

Williams 3H Lower Lam 4,500 19 228

JGresham 1H Lower Lam 7,400 31 176

JGresham 2H Sand 7,500 25 249

* Restricted rate

Resource

115,000 net acres PIIP: 8.6 billion BOE Primarily light oil 75% RI ~700 net well locations

Strategy

Continue appraisal drilling of multiple zones

Establish commerciality through longer laterals and improved completion design

Accelerate development through potential liquids joint venture opportunity

Current Activity/Future Plans

Drilled and completed 6 wells, including a 7,500 foot lateral

Industry has drilled ~100 wells– Focused on drilling sand targets

>1,500 BOE/d IPs reported Initial Lower Laminated success expanding

Plan to drill and complete 6 additional wells in 2012

– 1 rig program

Gresham 1H

J. Gresham 1H

Williams 3H

~700 BOE/d IP(0)

575 BOE/d IP(30)

Well PostingHorizontal EaglebineECA HzECA ProposedIndustry PermitsIndustry Permits

5

10

Mississippian LimeAsset Overview

Kansas

Oklahoma

EncanaPlay Outline

Industry HZ Drilling

Industry VT Drilling

Industry HZ Permits

Industry HZ Producers

Industry VT Producers

ECA 2012 Locations

Mississippian production: ~44,000 vertical wells ; ~900 horizontal wells

Resource

360,000 net acres PIIP: 16 billion BOE Primarily light oil with associated NGLs 82.5% RI ~1,900 net well locations

Strategy

Establish commerciality on acreage

Current Activity/Future Plans

No wells drilled to date Industry has drilled >700 horizontal wells 210 horizontal wells permitted Plan to drill and complete 15 wells in 2012

– 2 rig program

RPH Target Well Parameters

Well cost: $2.8 million EUR: 425 MBOE Lateral length: 4,600 feet TVD: 4,800 feet

11

San Juan BasinAsset Overview

Well Name Lateral Length (ft) # of Stages30 day IP (BOE/d)

Lybrook H36 4,087 16 445

Good Times P32 4,189 17 210

Escrito P16 3,977 17 287

Meadows IO8 3,886 16 -

Bisti I32 H09 3,917 17 -

Good Times I32 3,817 17 -

Good Times A06 - - -

First 7 Wells Encana acreage

NM

20-Miles

Lybrook H36

Escrito P16

Meadows I08

Bisti H09

Good Times P32

Oil Window

Resource

174,000 net acres in oil window PIIP: 7.5 billion BOE Primarily light oil with associated NGLs 80% RI ~905 net locations

Strategy

Appraise oil window of the Gallup formation

Establish RPH efficiencies Ramp-up to commercial development

pace

Current Activity/Future Plans

Encana has 4 gross wells producing, 1 well waiting on facilities, 1 well completing, 1 well drilling

– 1 rig program in 2012 Industry has drilled 3 horizontal wells in

gas window

RPH Target Well Parameters

Well cost: $4.3 million EUR per well: 550 MBOE Lateral length: 5,000 feet TVD: 5,500 feet

Good Times I32Good Times A06

6

12

DuvernayAsset Overview

Resource

400,000 net acres

97% average working interest

PIIP*: ~8.7 billion BOE

50 – 60 API oil gravity

1,020 – 1,170 Btu/scf average heat content

1,000 – 1,600 net well locations

160 – 330 acre expected well spacing

Strategy

Appraisal and early Resource Play Hub (RPH) development evaluation

Current Activity/Future Plans

10 wells planned for 2012– 2 rig program

Continue reservoir characterization

Design liquids handling facilities

Upgrade roads and infrastructure

13

Duvernay The Encana Advantage Encana has captured over half of

the high-graded liquids rich gas condensate fairway

Encana free condensate yield results are top quartile

Estimate 30 Tcf and 4 Bbbls PIIP on Encana lands

Cutting edge reservoir characterization techniques

Well developed infrastructure and access to markets enables early production growth

WellLateral

Length (ft)# of

StagesGas

(MMcf/d)Field Liquid Yields

(bbls/MMcf)

11-8-62-24W5 Vertical 1 0.2 300

16-5-62-24W5 3,940 10 2.7 200

13-17-43-4W5* 4,100 10 0.5 190

13-5-43-6W5 1,700 8 1.6 120

* The 13-17 well was highly restricted

RPH Target Well Parameters

Well cost: $15 million

EUR per well: – 3 – 6 Bcf

– 350 – 600 Mbbls

Lateral length: 3,500 – 6,500 feet

TVD: 8,300 – 13,000 feet

7

14

Increasing Liquids Extraction with Deep CutLow-Risk, Low-Cost Barrels

Planned Deep Cut expansions:

– 5,000 bbls/d at Musreau – Q3 2012

– 3,000 bbls/d at Gordondale –Q4 2012

– 12,000 bbls/d at Resthaven –Phase 1 Q2 2014

– 11,800 bbls/d at Dawson Creek – Q3 2015

– Plus additional expansions

15

$1.39 $1.38

$1.01

$0.70$0.88

$1.39

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Dewpoint Shallow Cut Deep Cut

Natural Gas NGLs

Increasing Exposure to Oil and NGLsLiquids Value Uplift

C$/Mcfe*

* Based on 1,100 Btu/Mcf wellhead gas yielding approximately 90 bbls of NGLs per 1 MMcf. Before transportation costs. Canadian Deep Basin illustrative example.

Price Differential Example on 1 Mcf at the Wellhead

8

16

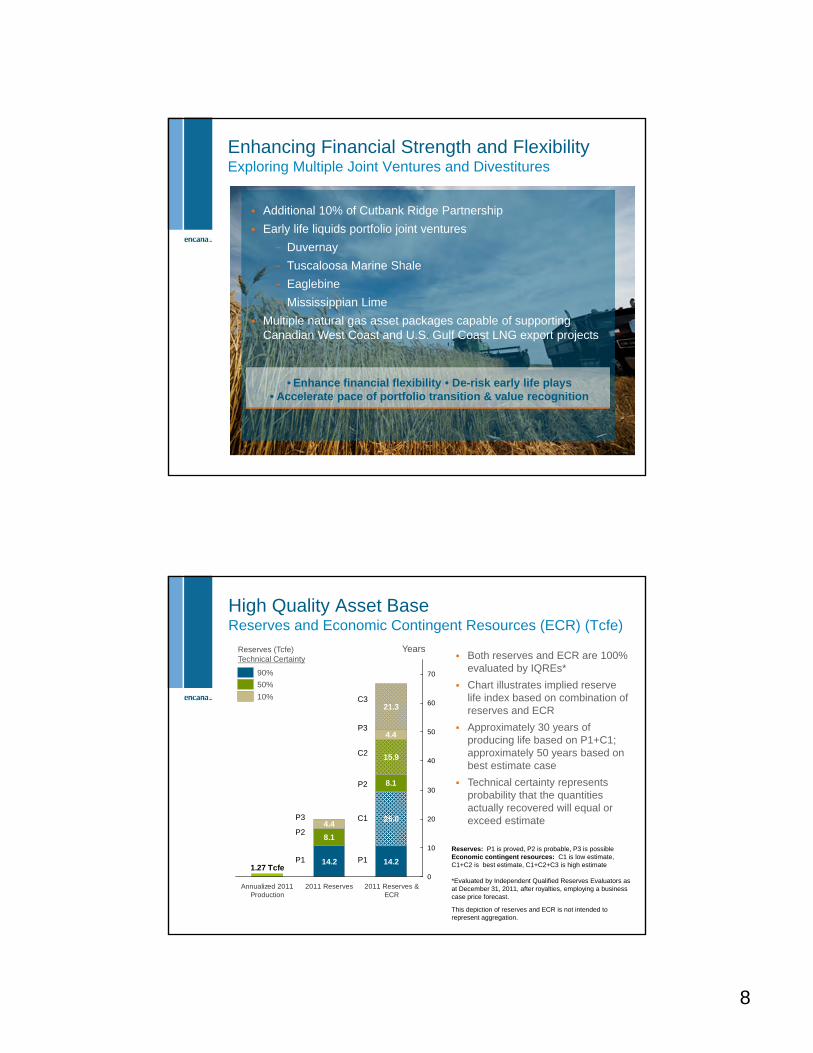

Enhancing Financial Strength and FlexibilityExploring Multiple Joint Ventures and Divestitures

Additional 10% of Cutbank Ridge Partnership

Early life liquids portfolio joint ventures

− Duvernay

− Tuscaloosa Marine Shale

− Eaglebine

− Mississippian Lime

Multiple natural gas asset packages capable of supporting Canadian West Coast and U.S. Gulf Coast LNG export projects

• Enhance financial flexibility • De-risk early life plays • Accelerate pace of portfolio transition & value recognition

17

High Quality Asset BaseReserves and Economic Contingent Resources (ECR) (Tcfe)

Reserves: P1 is proved, P2 is probable, P3 is possibleEconomic contingent resources: C1 is low estimate, C1+C2 is best estimate, C1+C2+C3 is high estimate

*Evaluated by Independent Qualified Reserves Evaluators as at December 31, 2011, after royalties, employing a business case price forecast.

This depiction of reserves and ECR is not intended to represent aggregation.

Both reserves and ECR are 100% evaluated by IQREs*

Chart illustrates implied reserve life index based on combination of reserves and ECR

Approximately 30 years of producing life based on P1+C1; approximately 50 years based on best estimate case

Technical certainty represents probability that the quantities actually recovered will equal or exceed estimate

Years

14.2 14.2

8.1

25.04.4

8.1

1.27 Tcfe

15.9

4.4

21.3

0

10

20

30

40

50

60

70

80

90

100

Annualized 2011Production

2011 Reserves 2011 Reserves &ECR

0

10

20

30

40

50

60

70

P1

P2

P3

P1

P2

P3

C1

C2

C3

90%

50%

10%

Reserves (Tcfe)Technical Certainty

9

18

$1.5 billion of long term debt maturing in the next five years

$1.8 billion of cash and short term investments at June 30, 2012; expect ~$2.5 billion by year end

~$5 billion of undrawn bank lines committed until 2015

Joint venture partners are expected to partially fund development of select plays

Maintain investment grade credit rating as it provides cost effective financing options

− Moody’s – Baa2 (Stable)

− Standard & Poor’s – BBB (Stable)

− DBRS – BBB+ (Negative)

Encana CorporationLiquidity Supports Execution of Strategy

19

Continue to Achieve Industry Leading Cost StructuresEncana - North America’s Resource Play Specialist

Established history of developing resource plays from the

ground up:

From early stage identification

– Supported by dedicated new venture teams

To large scale commercialization

– “Resource Play Hub” development model

Ingrained culture of innovation and defineddevelopment model with a successful track record

10

20

North American Fundamentals Attractive Fundamentals Emerging for Gas, Oil & NGLs

Natural gas prices are bottoming and will start trending to levels that are more sustainable long-term

Natural gas demand growth from power generation, industry, transportation and LNG exports has the potential for the North American gas market to reach 100 Bcf/d by 2020

Significant opportunities exist to grow North American oil production and displace imports

The NGL market is responding with demand and infrastructure expansions sufficient to accommodate supply growth

21

Maintaining financial strength while transitioning to a more diversified portfolio

Why Invest in Encana?Take A Closer Look See the Upside

Leading North American resource play company

− Exposure to natural gas

− Growing exposure to oil and natural gas liquids

Track record for value creation

− Proud of meeting our commitments

Innovative, value-driven culture

11

Supplemental

23

0 1 2 3 4 5 6 7 8

Other

Jonah

Texas

Piceance

Haynesville

Bighorn

CBM

Horn River

Greater Sierra

Peace River Arch

Cutbank Ridge1

2

3

1P (Proved)

Reserves

Evaluated by Independent Qualified Reserves Evaluators as of December 31, 2011.*Increase relative to year-end 20101. Includes Montney, Cadomin and Doig in B.C.; includes Partnership and Non-Partnership reserves and resources.2. Includes Gordondale, Pipestone and Sexsmith.3. Greater Sierra is Jean Marie only (excluding Horn River).

Proved Reserves and 1C Economic Contingent Resources (Tcfe)

1C (Low Estimate)

Economic Contingent Resources

Tremendous Resource PotentialIncreased 1C Economic Contingent Resources by 25%*

High quality, low risk inventory – 90%

probability.

12

24

Comprehensive Disclosure of Reserves & ResourcesLargest Reserves and Resource Life in Encana’s History

Encana Reserves and Resources (Tcfe) 1

Estimated reserves Estimated economic contingent resources

KRPP1

Proved

P2

Probable

P3

PossibleC1 C2 C3

Cutbank Ridge 2 1.7 0.7 0.5 6.0 2.1 3.6

Peace River Arch 3 0.5 0.1 0.1 1.3 0.3 0.3

Greater Sierra 4 1.3 0.9 0.5 2.2 2.6 5.2

CBM 1.9 0.4 0.4 1.4 0.1 0.2

Bighorn 1.2 0.6 0.3 1.1 1.4 1.6

Haynesville 2.4 2.6 0.8 4.2 4.1 3.6

Piceance 1.5 1.0 0.7 3.2 3.0 3.2

Texas 0.7 0.6 0.1 3.5 1.2 2.1

Jonah 1.8 0.5 0.5 0.3 0.7 0.7

Other 5 1.2 0.7 0.5 1.8 0.4 0.8

Total 14.2 8.1 4.4 25.0 15.9 21.3

1. As of December 31, 2011 using forecast prices and costs. 2. Includes Montney, Cadomin and Doig in B.C.; includes Partnership and Non-Partnership reserves and resources. 3. Includes Gordondale, Pipestone and Sexsmith.4. Includes Horn River.5. Includes Panuke, DJ, Wind/Green River Basins, Canadian non-KRP.

25

Reserves and Contingent Resources Definitions

Characterization of Petroleum Initially in Place (PIIP)Reserve – Resource DescriptionPetroleum Resource Management System

SPE – PRMS

Deve lopme ntnot viable

Onproduc tion

P lay

Prospect

Lead

Deve lopme ntunc larifiedor on hold

Deve lopme ntpe nding

Justified fordevelopme nt

App roved fordevelopment

Project MaturitySub-Classes

Inc

rea

sing

Ch

an

ce o

f C

om

me

rcia

lity

Increasing Uncertainty of Recovery

PROSPECTIVE RESOURCES

-------------Commercially or Physically Unrecoverable---------------

CONTINGENT R ESOURCES1C (Low ) 2C (Best)

3C (High)

P 90Es tima te

P 50Estimate

P10E stimate

UN

DIS

CO

VE

RE

DD

ISC

OV

ER

ED

SU

B-C

OM

ME

RC

IAL

CO

MM

ER

CIA

L

LowBest

High

SU

B-E

CO

NO

MIC

EC

ON

OM

IC

-------------Commercially or Physically Unrecoverable---------------

Incr

eas

ing

Ch

anc

e o

f C

om

me

rcia

lityP ossible (P3)Probab le (P2)Proved (P1)

RESERVES

1P2P

3P

Characterization of Petroleum Initially in Place (PIIP)Reserve – Resource DescriptionPetroleum Resource Management System

SPE – PRMS

Deve lopme ntnot viable

Onproduc tion

P lay

Prospect

Lead

Deve lopme ntunc larifiedor on hold

Deve lopme ntpe nding

Justified fordevelopme nt

App roved fordevelopment

Project MaturitySub-Classes

Inc

rea

sing

Ch

an

ce o

f C

om

me

rcia

lity

Increasing Uncertainty of Recovery

PROSPECTIVE RESOURCES

-------------Commercially or Physically Unrecoverable---------------

CONTINGENT R ESOURCES1C (Low ) 2C (Best)

3C (High)

P 90Es tima te

P 50Estimate

P10E stimate

UN

DIS

CO

VE

RE

DD

ISC

OV

ER

ED

SU

B-C

OM

ME

RC

IAL

CO

MM

ER

CIA

L

LowBest

High

SU

B-E

CO

NO

MIC

EC

ON

OM

IC

-------------Commercially or Physically Unrecoverable---------------

Incr

eas

ing

Ch

anc

e o

f C

om

me

rcia

lityP ossible (P3)Probab le (P2)Proved (P1)

RESERVES

1P2P

3P

13

26

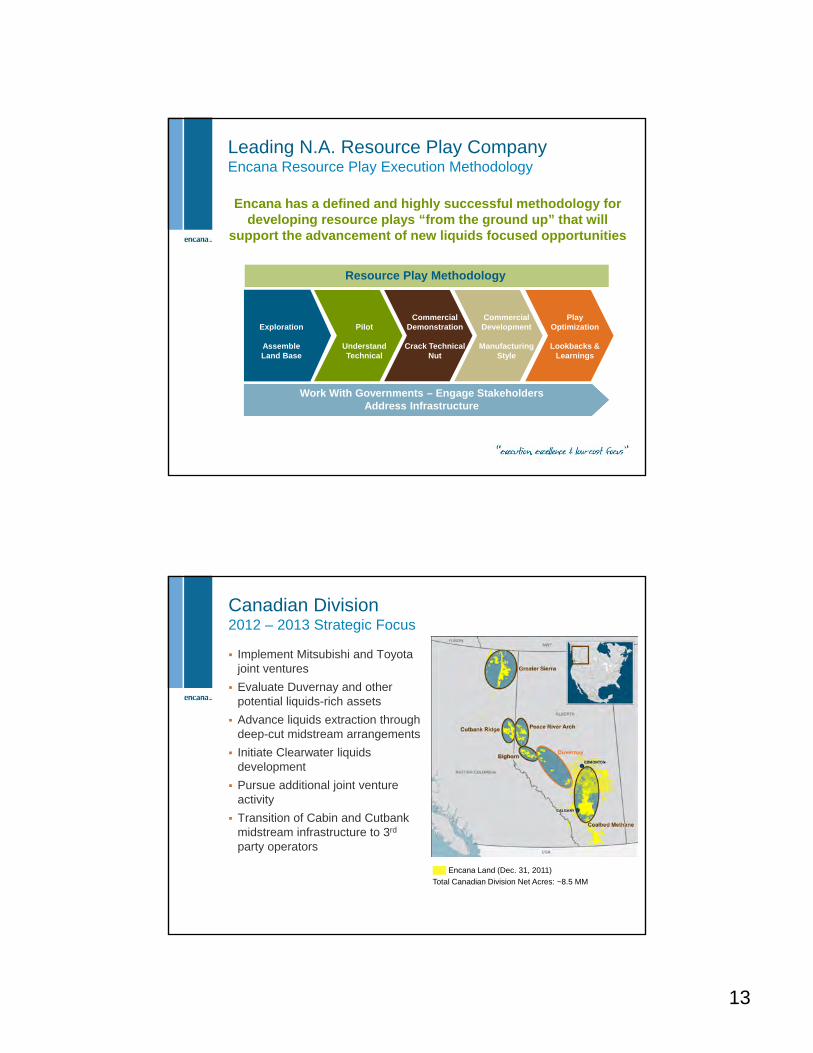

Leading N.A. Resource Play CompanyEncana Resource Play Execution Methodology

Resource Play Methodology

Work With Governments – Engage Stakeholders Address Infrastructure

Exploration

Assemble Land Base

Pilot

Understand Technical

CommercialDemonstration

Crack Technical Nut

CommercialDevelopment

Manufacturing Style

PlayOptimization

Lookbacks & Learnings

Encana has a defined and highly successful methodology for developing resource plays “from the ground up” that will

support the advancement of new liquids focused opportunities

27

Implement Mitsubishi and Toyota joint ventures

Evaluate Duvernay and other potential liquids-rich assets

Advance liquids extraction through deep-cut midstream arrangements

Initiate Clearwater liquids development

Pursue additional joint venture activity

Transition of Cabin and Cutbank midstream infrastructure to 3rd

party operators

Canadian Division2012 – 2013 Strategic Focus

Encana Land (Dec. 31, 2011)

Total Canadian Division Net Acres: ~8.5 MM

14

28

0

5

10

15

20

25

30

2011 2012F 2013F

Oil NGLs

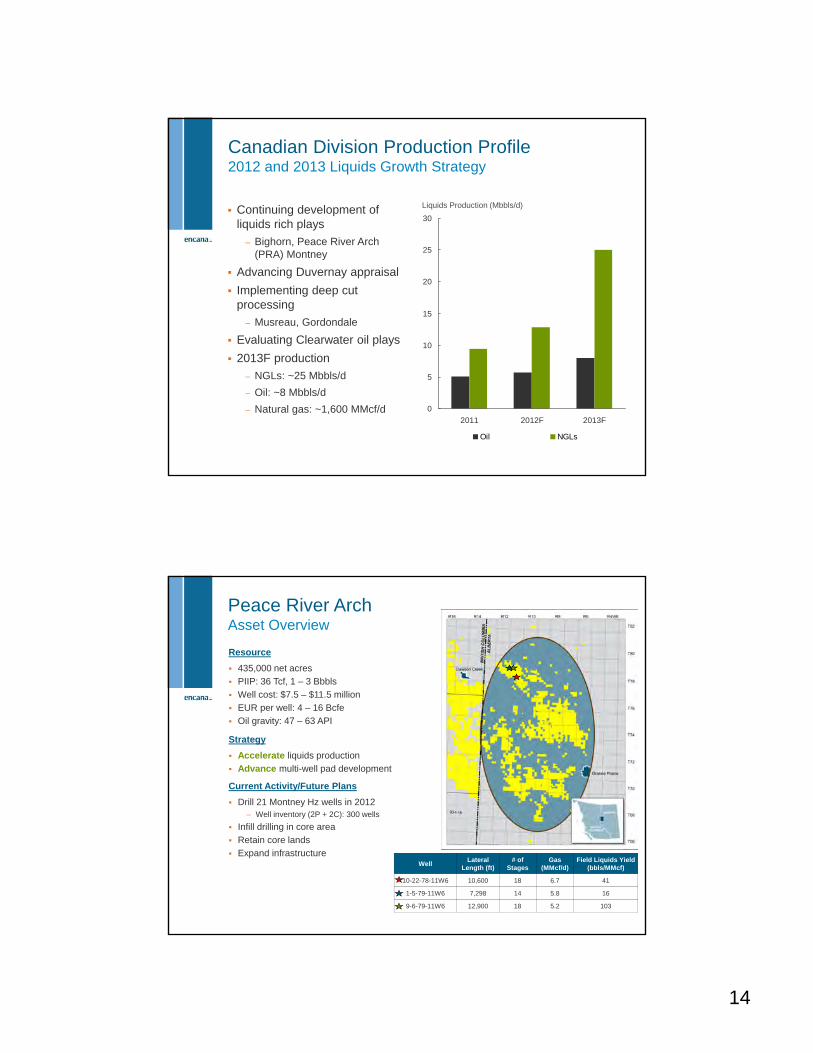

Continuing development of liquids rich plays

– Bighorn, Peace River Arch (PRA) Montney

Advancing Duvernay appraisal

Implementing deep cut processing

– Musreau, Gordondale

Evaluating Clearwater oil plays

2013F production

– NGLs: ~25 Mbbls/d

– Oil: ~8 Mbbls/d

– Natural gas: ~1,600 MMcf/d

Canadian Division Production Profile2012 and 2013 Liquids Growth Strategy

Liquids Production (Mbbls/d)

29

Peace River Arch Asset Overview

WellLateral

Length (ft)# of

StagesGas

(MMcf/d)Field Liquids Yield

(bbls/MMcf)

10-22-78-11W6 10,600 18 6.7 41

1-5-79-11W6 7,298 14 5.8 16

9-6-79-11W6 12,900 18 5.2 103

Resource

435,000 net acres

PIIP: 36 Tcf, 1 – 3 Bbbls

Well cost: $7.5 – $11.5 million

EUR per well: 4 – 16 Bcfe

Oil gravity: 47 – 63 API

Strategy

Accelerate liquids production

Advance multi-well pad development

Current Activity/Future Plans

Drill 21 Montney Hz wells in 2012– Well inventory (2P + 2C): 300 wells

Infill drilling in core area

Retain core lands

Expand infrastructure

15

30

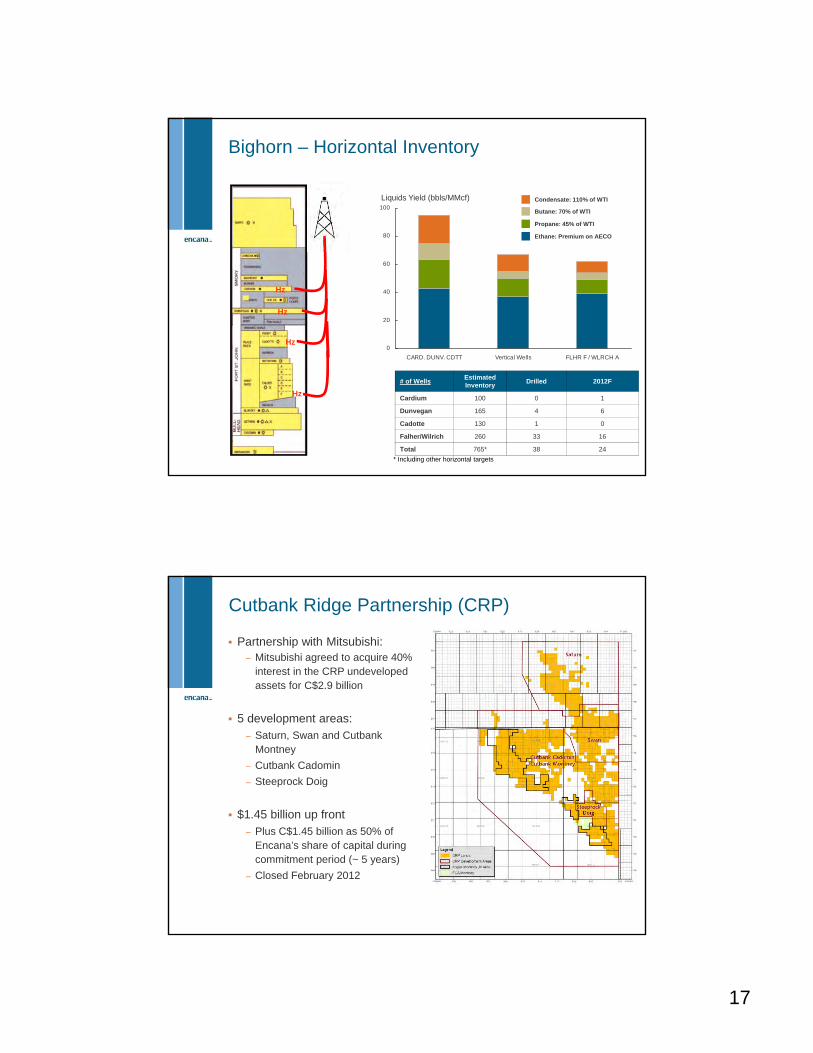

BighornAsset Overview

Well NameLateral

Length (ft)# of

StagesGas

(MMcf/d)Field Liquids Yield

(bbls/MMcf)

09-15-060-03W6 6,000 14 8.3 45

13-14-060-03W6 4,600 13 7.6 48

Resource

383,000 net acres

PIIP: 33 Tcf, 1 – 2 Bbbls

Well cost: $5 – $10 million

EUR per well: 2 – 12 Bcfe

Oil gravity: 55 – 60 API

Strategy

Pursue liquids-rich opportunities

Demonstrate cost control and repeatability in well design and execution

Secure processing and transportation for future growth

Current Activity/Future Plans

Drill 33 net wells in 2012– Well inventory (2P + 2C): ~1,400 wells

Advance RPH development

31

Cutbank RidgeAsset Overview

Well NameLateral

Length (ft)# of Stages IP (MMcf/d)

G12-31-77-15W6 8,935 12 19*

*Normalized

Resource

819,000 gross acres

PIIP: 130 Tcf, 1 – 2 Bbbls

Well cost: $5 – $10 million

EUR per well: 4 – 16 Bcfe

Oil gravity: 45 – 65 API

Strategy

Increase value through accelerated development and continuous supply cost reductions

Current Activity/Future Plans

Drill ~70 gross wells in 2012 – ~4,500 well inventory

Advance water resource hub – Sustainable water source solution

Spectra Dawson Creek Plant start-up– FEED study ongoing for 400 MMcf/d

C3+ processing

16

32

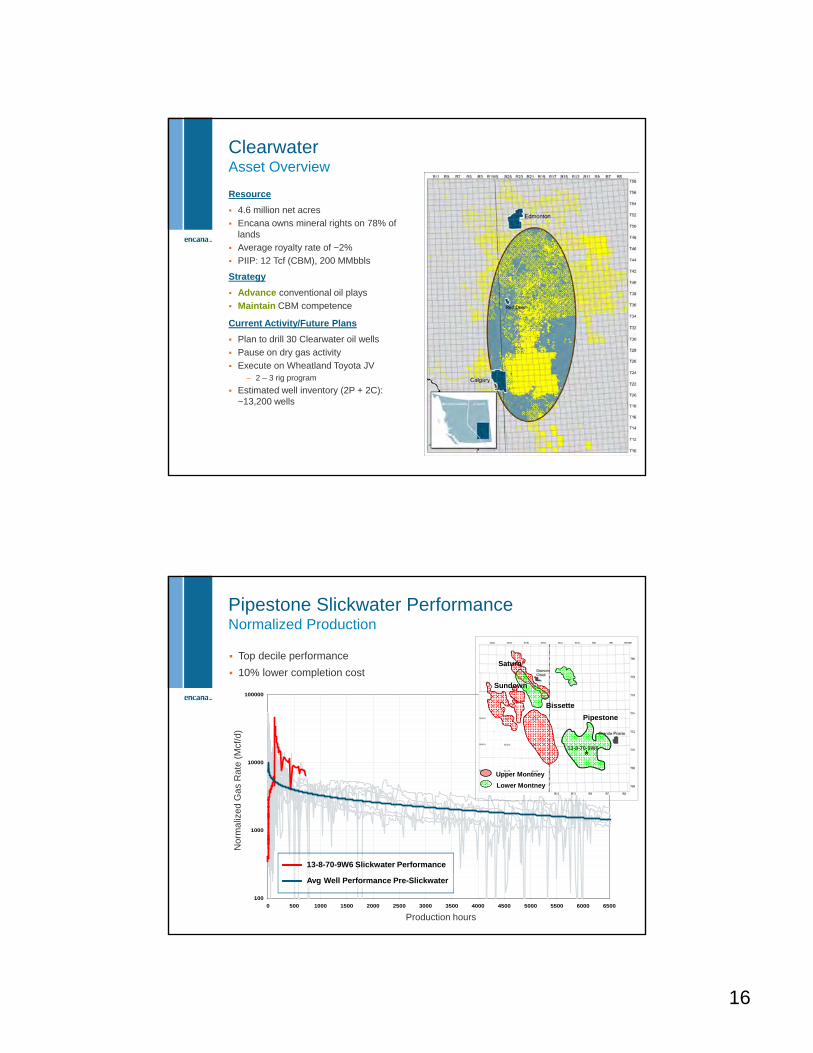

Clearwater Asset Overview

Resource

4.6 million net acres

Encana owns mineral rights on 78% of lands

Average royalty rate of ~2%

PIIP: 12 Tcf (CBM), 200 MMbbls

Strategy

Advance conventional oil plays

Maintain CBM competence

Current Activity/Future Plans

Plan to drill 30 Clearwater oil wells

Pause on dry gas activity

Execute on Wheatland Toyota JV– 2 – 3 rig program

Estimated well inventory (2P + 2C): ~13,200 wells

33

100

1000

10000

100000

0 500 1000 1500 2000 2500 3000 3500 4000 4500 5000 5500 6000 6500

Flow Time (hrs)

Norm

alize

d G

as R

ate

(m

cf/d)

Nor

mal

ized

Gas

Rat

e (M

cf/d

)

Production hours

13-8-70-9W6 Slickwater Performance

Avg Well Performance Pre-Slickwater

Pipestone Slickwater PerformanceNormalized Production

Top decile performance

10% lower completion cost

Pipestone

Saturn

Sundown

Bissette

Upper Montney

Lower Montney

13-8-70-9W6

17

34

0

20

40

60

80

100

CARD. DUNV. CDTT Vertical Wells FLHR F / WLRCH A

Bighorn – Horizontal Inventory

# of WellsEstimatedInventory

Drilled 2012F

Cardium 100 0 1

Dunvegan 165 4 6

Cadotte 130 1 0

Falher/Wilrich 260 33 16

Total 765* 38 24

* Including other horizontal targets

Hz

Hz

Hz

Hz

Condensate: 110% of WTI

Butane: 70% of WTI

Propane: 45% of WTI

Ethane: Premium on AECO

Liquids Yield (bbls/MMcf)

35

Cutbank Ridge Partnership (CRP)

Partnership with Mitsubishi:– Mitsubishi agreed to acquire 40%

interest in the CRP undeveloped assets for C$2.9 billion

5 development areas:– Saturn, Swan and Cutbank

Montney

– Cutbank Cadomin

– Steeprock Doig

$1.45 billion up front– Plus C$1.45 billion as 50% of

Encana’s share of capital during commitment period (~ 5 years)

– Closed February 2012

18

36

Montney Supply Cost EvolutionAdvancing Resource Play Hub Design and Development

*Supply Cost is defined as the flat NYMEX price that yields a risked IRR of 9% and does not include land or G&A costs.

$0.50$0.55

$3.20

$0.63 $0.51

$1.50

$0.94 $0.81

$3.17 $3.15$2.76

$4.10

$6.45

$4.55

$3.40

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2006Vertical

2006 2007 2008 2009 2010 2011 2012F0

1

2

3

4

5

6

7

Cost/Interval Supply Cost*

$/MMBtu$MMCDN

Montney Performance HistoryD

CT

cos

ts /

inte

rval

NY

ME

X

4 6 8 9 13Completion Stages14 15

37

Aerial extent ~150km x 600km

Montney fairway contains over 1,800 Tcf of NGIP

ECA Montney acreage well positioned in the highest NGIP/section area.

MONTNEY FAIRWAY

High

Montney Tight Gas Play Total Resource

GR_1GAPI0 200

2500

2550

2600

2650

2700

2750

2451.5

2754.0

MD

2451.5

2754.0

NPSS_1V/V0.45 -0.15

RHOB_2

K/M31950 2950

EVAL_MONTNEY.PHIT_1V/V0.15 0

EVAL_MONTNEY.PHIT_1V/V0.15 0

EVAL_MONTNEY.VOL_UWAT_V/V0.15 0

GR Porosity

Upper Montney

Neutron/Porosity

Lower Montney

Por. & BVW

ECA Portfolio of Montney Assets

Cutbank Area

OGIP Map

Low

Upper Montney

Lower Montney

19

38

5 well pilot: Improved initial rates compared to offsetting wells

Cost reduction expected with continued optimization

More sustainable approach to completions

Gas Rate/100m (Mcf/d)

Production Days

Pilot Wells

Offsets

60% Increase

Improved Completions ResultsSlickwater/Cluster Perforation Application

39

Clearwater Business Unit Liquids Potential

Currently evaluating more than 9

prospective oil zones

300 high graded oil locations identified

to date

Well cost: $1 – $3 million

EUR per well: 60 – 150 Mbbls

Oil gravity: 30 – 40 API

Current ECA Key Oil Zones

20

40

Toyota Tsusho

*Encana Joint Venture Lands with Toyota Tsusho

Wheatland

Toyota Tsusho Corporation:

– Upfront cash component of $100 million

Provides capital funding of $502 million over 7 years:

– 1,488 drilling locations

– 1,606 recompletion locations

– Acquired uniform 32.5% GORR on PDP and Future Development

41

KOGAS Joint VentureKiwigana

Two Separate Deals

Deal 1− Signed February 26, 2010− 38 sections− $324 million earning capital

Earned 50% WI in April 2012

Deal 2− Signed July 28, 2011− 33 sections− $185 million earning capital − Spend by YE 2013 to earn

50% WI

21

42

Kitimat LNG Project – Encana 30% InterestDiversifying Markets – Building Demand

Co-owners− Apache (40%, operator)

− Encana (30%)

− EOG (30%)

1,400 MMcf/d (10 MMTPA) export capacity

Final investment decision pending− Completion of FEED study

− Marketing efforts

Project offered equity interest to strategic market partners

Expect natural gas price uplift through linkage to global oil pricing

Bish Cove, British Columbia (650 km north of Vancouver)Artist’s rendition of proposed facility.

*MMTPA = million metric tonnes per annum.

43

Deep Panuke ProjectFirst Natural Gas Production Forecast: Q3 2012

Operating cost ($/Mcfe) $0.95-$0.65 at 200 – 300 MMcf/d

Transportation cost ($/Mcfe) $1.68

Royalties 2%

Delivery point Dracut

22

44

Advance oil and liquids-rich plays to commercial viability

Transfer knowledge and technology from natural gas development to liquids plays

Optimize processing contracts to capture liquids value

Accelerate third party funding

Manage supply chain

Preserve natural gas resource base

USA DivisionKey Strategies

Encana Land (Dec. 31, 2011)

Total USA Division Net Acres: 2.4 MM

Resource Play

Potential Liquids Play

Jonah

Piceance

Niobrara/Mancos

DJ Niobrara

TexasHaynesville

Collingwood/Utica

Tuscaloosa

Mississippian Lime

San Juan

Eaglebine

45

USA DivisionEmerging Liquids Portfolio

Develop a low cost portfolio of high impact liquids plays

Continue appraisal drilling program to assess prospectivity within existing

liquids plays

Capture additional acreage in existing and new liquids plays

2012 Program

Encana Existing Liquids Plays

Industry Producing Oil Wells

We have assembled a portfolio of liquids plays

totalling over 1.7 million net acres

DJ Niobrara

San JuanMississippian Lime

Tuscaloosa Marine Shale

Collingwood/Utica

Eaglebine

PiceanceNiobrara/Mancos

23

46

0

2

4

6

8

10

12

14

16

18

20

2011 2012F 2013F

Oil NGLs

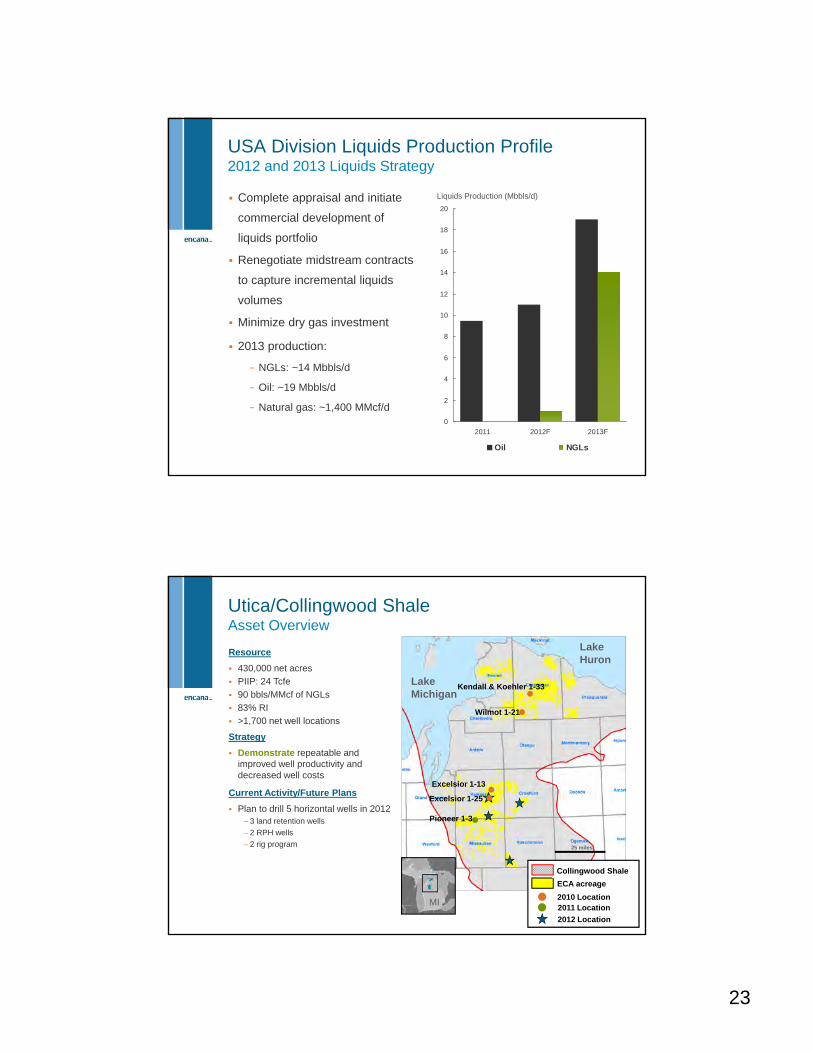

USA Division Liquids Production Profile2012 and 2013 Liquids Strategy

Complete appraisal and initiate

commercial development of

liquids portfolio

Renegotiate midstream contracts

to capture incremental liquids

volumes

Minimize dry gas investment

2013 production:

− NGLs: ~14 Mbbls/d

− Oil: ~19 Mbbls/d

− Natural gas: ~1,400 MMcf/d

Liquids Production (Mbbls/d)

47

Utica/Collingwood ShaleAsset Overview

Lake Michigan

Lake Huron

ECA acreage

Collingwood Shale

2010 LocationMI

25 miles

2011 Location

2012 Location

Pioneer 1-3

Excelsior 1-25

Excelsior 1-13

Wilmot 1-21

Kendall & Koehler 1-33

Resource

430,000 net acres

PIIP: 24 Tcfe

90 bbls/MMcf of NGLs

83% RI

>1,700 net well locations

Strategy

Demonstrate repeatable and improved well productivity and decreased well costs

Current Activity/Future Plans

Plan to drill 5 horizontal wells in 2012– 3 land retention wells

– 2 RPH wells

– 2 rig program

24

48

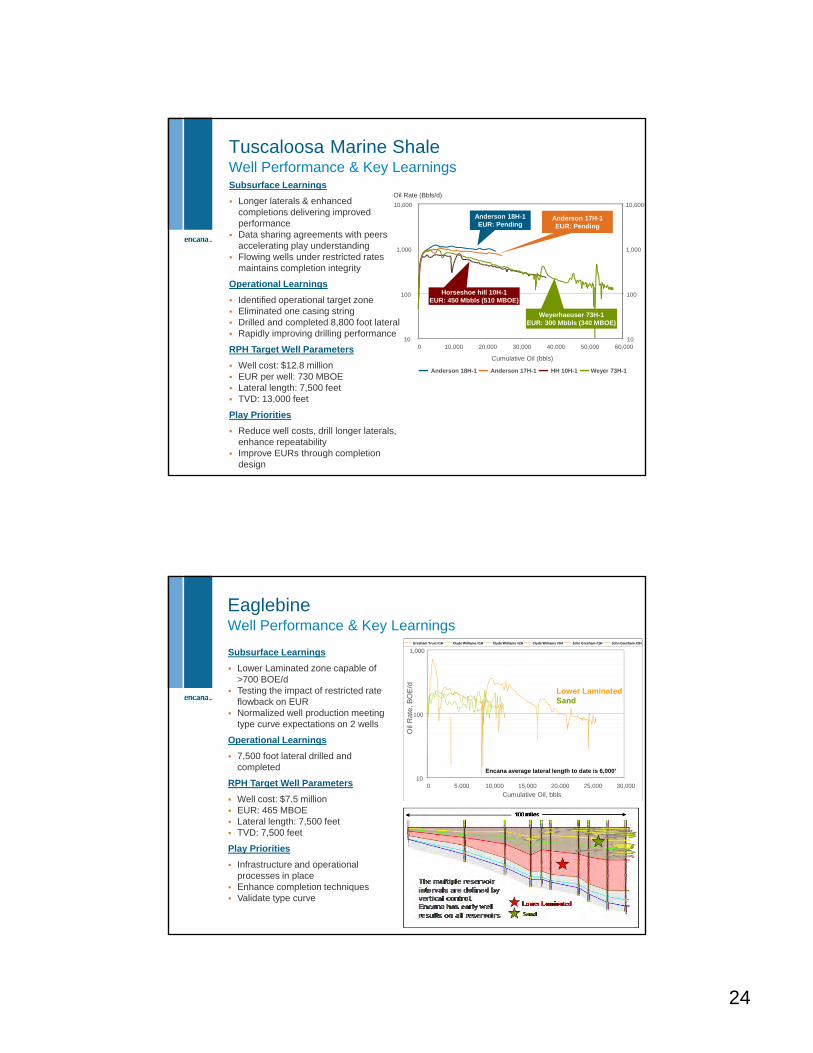

Oil Rate (Bbls/d)

Subsurface Learnings

Longer laterals & enhanced completions delivering improved performance

Data sharing agreements with peers accelerating play understanding

Flowing wells under restricted rates maintains completion integrity

Operational Learnings

Identified operational target zone Eliminated one casing string Drilled and completed 8,800 foot lateral Rapidly improving drilling performance

RPH Target Well Parameters

Well cost: $12.8 million EUR per well: 730 MBOE Lateral length: 7,500 feet TVD: 13,000 feet

Play Priorities

Reduce well costs, drill longer laterals, enhance repeatability

Improve EURs through completion design

Tuscaloosa Marine Shale Well Performance & Key Learnings

10

100

1,000

10,000

0 10,000 20,000 30,000 40,000 50,000 60,000

Cumulative Oil (bbls)

10

100

1,000

10,000

Anderson 18H-1 Anderson 17H-1 HH 10H-1 Weyer 73H-1

-

Anderson 18H-1EUR: Pending

Anderson 17H-1EUR: Pending

Weyerhaeuser 73H-1EUR: 300 Mbbls (340 MBOE)

Horseshoe hill 10H-1EUR: 450 Mbbls (510 MBOE)

49

EaglebineWell Performance & Key Learnings

Encana average lateral length to date is 6,000’

Lower LaminatedSand

Subsurface Learnings

Lower Laminated zone capable of >700 BOE/d

Testing the impact of restricted rate flowback on EUR

Normalized well production meeting type curve expectations on 2 wells

Operational Learnings

7,500 foot lateral drilled and completed

RPH Target Well Parameters

Well cost: $7.5 million EUR: 465 MBOE Lateral length: 7,500 feet TVD: 7,500 feet

Play Priorities

Infrastructure and operational processes in place

Enhance completion techniques Validate type curve

10

100

1,000

0 5,000 10,000 15,000 20,000 25,000 30,000

Cumulative Oil, bbls

Oil

Rat

e, B

OE

/d

Gresham Trust #1H Clyde Williams #1H Clyde Williams #2H Clyde Williams #3H John Gresham #1H John Gresham #2H

25

50

Utica/Collingwood ShaleWell Performance

Well NameLateral

Length (ft)# of

Stages30 Day IP (MMcfe/d)

Excelsior 1-25 7,500 30 5.9

Excelsior 1-13 5,300 20 2.5

Pioneer 1-3 5,000 15 2.6

Subsurface Learnings

Reservoir responds well to “soak time” before production start up

RPH Target Well Parameters

Well cost: $7.3 million

EUR per well: 5.3 Bcfe

Lateral length: 7,500 feet

TVD: 9,500 feet

Play Priorities

Ongoing completions optimization

Extend horizontal laterals up to 10,000 feet

Demonstrate RPH development

0.1

1.0

10.0

0 100 200 300 400Cumulative (MMcf)

MMcf/d

Excelsior 1-25 Excelsior 1-13 Pioneer 1-3

51

10

100

1,000

0 5 10 15 20 25 30 35 40 45 50 55 60

Cumulative (Mbbls)

Herren 1A-33H (Longitudinal) McConahay 1A-34H (Oblique) Frederiksen 1A-28H (Longitudinal)

William Peltier 1A-20H (Oblique) Williams 3A-18H (Longitudinal) Grattan 4A-30H (Transverse)

Grattan 4B-30H (Transverse) 2011 Average

DJ Basin- Horizontal NiobraraAsset Overview

Well NameLateral

Length (ft)# of

Stages30 Day IP (BOE/d)

Herren 1A-33H 4205 17 595

McConahay 1A-34H 4142 16 907

Frederiksen 1A-28H 4145 17 732

William Peltier 1A-20H 4450 17 834

Williams 3A-18H 4323 19 539

DenverResource

49,000 net acres PIIP: 735 million BOE 105 bbls/MMcf of NGLs Primarily light oil with associated

gas/NGLs 80% RI ~150 net well locations

Strategy

Accelerate commercial development

Test lateral orientation and length

Current Activity/Future Plans

Plan to drill and complete 24 gross wells in 2012

– 2 rig program

RPH Target Well Parameters

Well cost: $5.4 million EUR per well: 525 MBOE Lateral length: 4,200 feet TVD: 7,300 feet

bbls/d

26

52

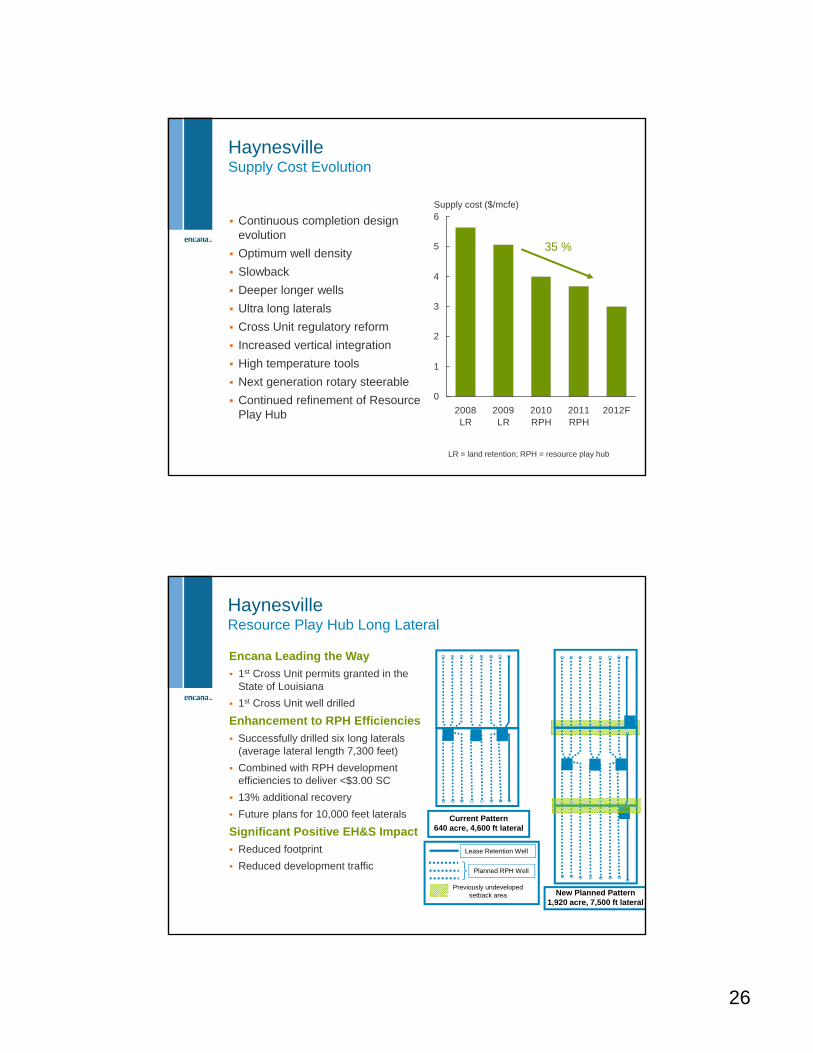

HaynesvilleSupply Cost Evolution

0

1

2

3

4

5

6

2008LR

2009LR

2010RPH

2011RPH

2012F

Continuous completion design evolution

Optimum well density

Slowback

Deeper longer wells

Ultra long laterals

Cross Unit regulatory reform

Increased vertical integration

High temperature tools

Next generation rotary steerable

Continued refinement of Resource Play Hub

35 %

Supply cost ($/mcfe)

LR = land retention; RPH = resource play hub

53

HaynesvilleResource Play Hub Long Lateral

Current Pattern640 acre, 4,600 ft lateral

Previously undeveloped setback area

Planned RPH Well

Lease Retention Well

New Planned Pattern1,920 acre, 7,500 ft lateral

Encana Leading the Way

1st Cross Unit permits granted in the State of Louisiana

1st Cross Unit well drilled

Enhancement to RPH Efficiencies

Successfully drilled six long laterals (average lateral length 7,300 feet)

Combined with RPH development efficiencies to deliver <$3.00 SC

13% additional recovery

Future plans for 10,000 feet laterals

Significant Positive EH&S Impact

Reduced footprint

Reduced development traffic

27

54

$0

$5

$10

$15

$20

$25

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Gas

Price per MMBtu

Oil

Source: NYMEX oil, coal, and gas spot prices. Forward prices as of August 1, 2012.

Coal

Abundance of Natural Gas expected to sustain price difference……making it an attractive economic choice

Nymex Strip Prices

Historic Energy Commodity Price SpreadsSituation Enables Expanded Markets for Natural Gas

55

0%

10%

20%

30%

40%

50%

60%

Jan-10

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

Jan-12

Mar-12

% of TotalGeneration

Coal

Natural Gas

58

60

62

64

66

68

1997 1999 2001 2003 2005 2007 2009 2011

Share of Power Generation

0

5

10

15

20

25

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Plant/Pipeline

Electric

Industrial

Commercial

Transportation

Residential

Source: Energy Information Administration (EIA); *3 year growth.

U.S Natural Gas Demand StoryStrong Growth Continues

Natural Gas Consumption Sectors (Bcf/d)

Natural Gas Consumption (Bcf/d)

28

56

Short-term: Coal to Gas DisplacementHistorical and Implied by Gas Forward Curve

0

2

4

6

8

10

12

Jan2010

May2010

Sep2010

Jan2011

May2011

Sep2011

Jan2012

May2012

Sep2012

Jan2013

May2013

Sep2013

Forecast Displacement Measured Displacement Henry Hub, May 21 NYMEX, June 1

Source: Encana fundamentals, Ventyx; *Note: Displacement is measured relative to 2008.

The forward curve implies about 4.1 Bcf/d of displacement year over year from July to December

Bcf/d

57

Source: Encana fundamentals, company announcements.

39 GWs of coal-fired capacity retirements have been announced equaling 4 Bcf/d of potential NG demand by 2025

Over 50 GWs of coal-fired capacity are expected to ultimately retire by 2025 representing over 5 Bcf/d of potential NG demand

Long-term: Coal Unit Retirements5 Bcf/d Demand Opportunity

29

58

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

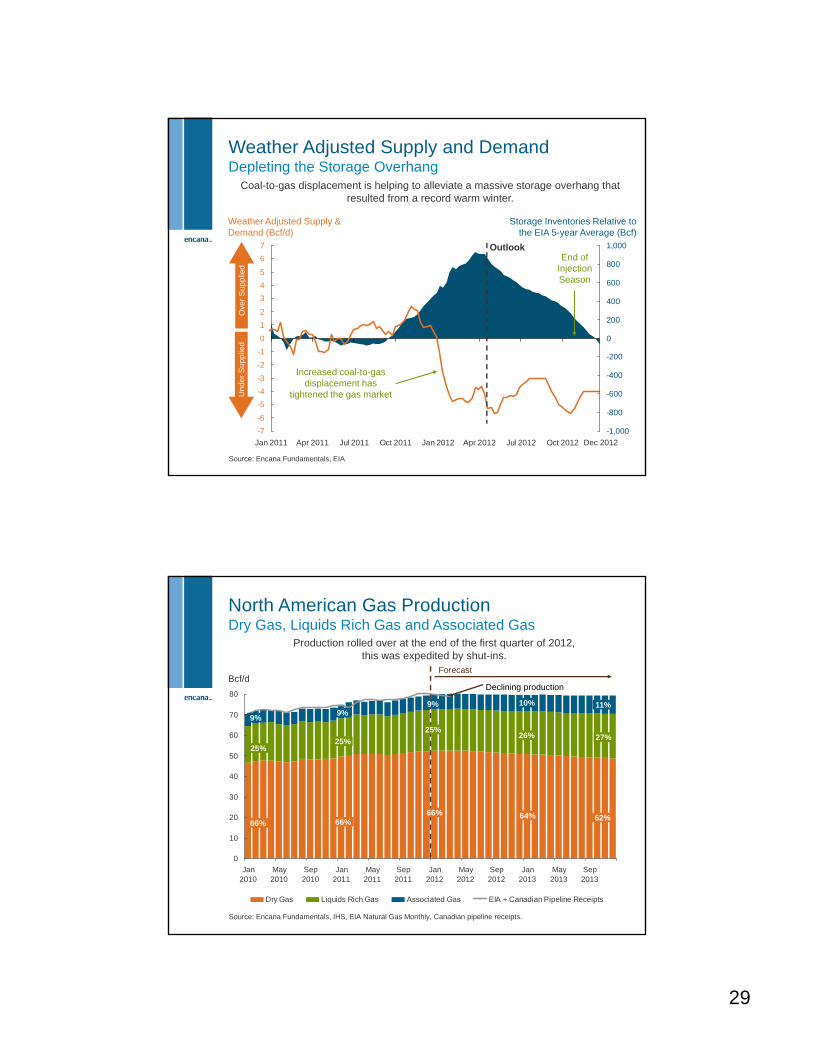

Jan 2011 Apr 2011 Jul 2011 Oct 2011 Jan 2012 Apr 2012 Jul 2012 Oct 2012

-1,000

-800

-600

-400

-200

0

200

400

600

800

1,000

Source: Encana Fundamentals, EIA

Coal-to-gas displacement is helping to alleviate a massive storage overhang that resulted from a record warm winter.

Weather Adjusted Supply & Demand (Bcf/d)

Storage Inventories Relative to the EIA 5-year Average (Bcf)

Un

de

r S

up

plie

d

End of Injection Season

Outlook

Increased coal-to-gas displacement has

tightened the gas market

Ove

r S

up

plie

d

Weather Adjusted Supply and DemandDepleting the Storage Overhang

Dec 2012

59

0

10

20

30

40

50

60

70

80

Jan2010

May2010

Sep2010

Jan2011

May2011

Sep2011

Jan2012

May2012

Sep2012

Jan2013

May2013

Sep2013

Dry Gas Liquids Rich Gas Associated Gas EIA + Canadian Pipeline Receipts

Bcf/d

Source: Encana Fundamentals, IHS, EIA Natural Gas Monthly, Canadian pipeline receipts.

North American Gas Production Dry Gas, Liquids Rich Gas and Associated Gas

Production rolled over at the end of the first quarter of 2012, this was expedited by shut-ins.

Forecast

66%

9%

25%

66%

9%

25%

66%

9%

25%

64%

10%

26%

62%

11%

27%

Declining production

30

60

New Natural Gas Demand CreationExcellent Opportunities Diversified Across Many Sectors

Bcf/dShort Term

< 3 yrsMedium Term

3 to 10 yrs Long Term10 years +

Announced Retirements 1 to 2* 2 to 4 4 +

Incremental Power 0 to 1 7 to 9 10 to 14 +

Industrial 0 to 1 2 to 3 3 +

LNG Export – USA 0 2 to 4 4 to 6

LNG Export – Canada 0 2 to 3 2 to 5

Transportation < 0.1 1 to 2 2 +

Gas to Liquids 0 < 1 1 +

Total 1 to 4 16 to 26 26 to 35

*A portion of this demand is currently being realized by natural gas.

61

Supply Factors Supply growth from liquids rich plays and oil plays alone will be

insufficient to balance market requirements

Full-cycle returns for natural gas development will need to be competitive with liquids rich and oil investment alternatives to attract capital

Demand Factors Power generation demand is expected to grow as the existing natural

gas fleet is increasingly utilized and natural gas becomes the preferred fuel for new capacity

Industrial demand is expected to grow as affordable North American feedstock promotes a renaissance in U.S. manufacturing

The transportation sector is expected to grow as natural gas captures market share from traditional liquid fuels

LNG exports will enable access to global markets

Future North American Natural Gas Prices Long-term Sustainability

Natural gas prices will need to range between $4.00 and $6.00/MMBtu to provide acceptable returns for producers and enable demand growth.

31

62

North American Oil Growth, Displacement and Infrastructure Investment

Significant opportunities to grow North American oil production and

displace imports

We expect continued robust growth− Significant investment capital is being

redirected to N.A. oil plays− Emerging plays could experience a rapid

growth profile due to the transfer of technology

New production will continue displacing crude imports− In 2011, the U.S. and Canada imported

over 7 MMbbls/d− Nearly 5 MMbbls/d were light and

medium crudes

Infrastructure investments will be required to access premium markets− Over 7 MMbbls/d of pipeline capacity is

slated to be online by June 2017− Refineries are retooling to handle the

lighter crude slate

63

Demand Factors

North America is one of the lowest cost ethylene producers in the world and we expect ethane demand to thrive as a result

Overall propane demand is expected to grow steadily as exports increase

The heavier NGLs (C4+) are expected to be absorbed into local markets

Infrastructure Factors

Numerous new NGL pipelines are currently under development across North America

Several new pipelines are being developed to relieve constraints between the Mid-Continent and Gulf Coast

Substantial LPG export capacity is being added on the Gulf Coast

North American Natural Gas Liquids Optimism Centered on Long-term Demand Growth

Demand and infrastructure is expected to keep pace with

supply growth

32

64

What Makes LNG for Transportation Viable?Illustrative Full Cycle Cost Components – LNG vs. Diesel

Sales andExcise Tax

Retailing

Distribution

LNG offers 20% to 40% savings depending on region* LNG feed stock price is one third of diesel* LNG per unit margin can provide at least a $4.00/mcf uplift in value to

feedstock*

*$4.00/MMBtu gas and $100/bbl oil, blended Canada/U.S. analysis; Encana estimates; DGE: Diesel Gallon Equivalent.

LNG$2.50 to $2.90/DGE

Diesel$3.70 to $5.00/DGE

65

Transforming North American Transportation Strategic with Economic Return on Infrastructure Investment

0

2.5

5

7.5

2012 2015 2018 2021 2024 2027

0

2.5

5

7.5

2012 2015 2018 2021 2024 2027

*Assumes $4.00/mcf NYMEX gas and $100/bbl WTI oil; Encana estimates.

~5% of Fuel Market Share ~10% of Fuel Market Share

Industry Wide Investment

Total capital: $30 to $70 billion

Annual EBITDA: $10 to $25 billion

100s of LNG plants

5,000 to 20,000 LNG and CNG stations

Industry Wide Results

Natural gas consumption: 3 to 7 Bcf/d

Annual fuel savings: $8 to $15 billion

NGV sales build to 3% to 8% of annual market

Home fueling will be game changer

Example of 15 Year Plan to Success

Bcf/dBcf/d

CNG LNG

Low Adoption High Adoption

33

66

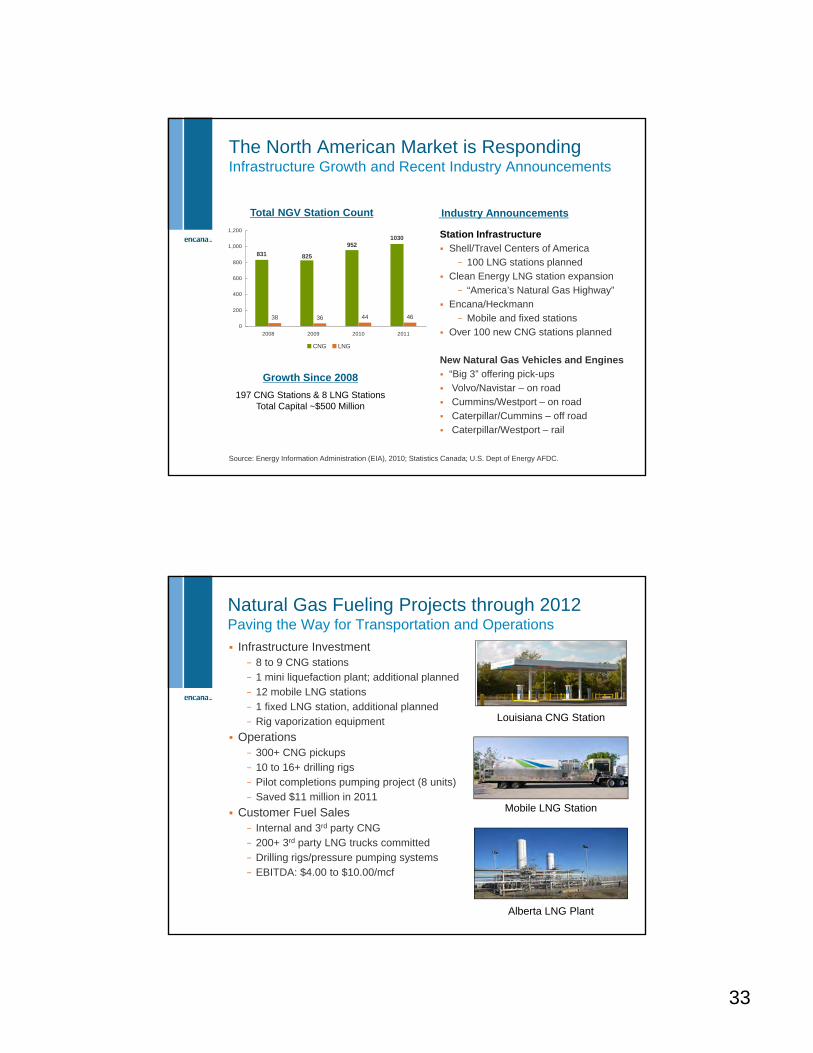

The North American Market is RespondingInfrastructure Growth and Recent Industry Announcements

38 36 44 46

1030

831 825

952

0

200

400

600

800

1,000

1,200

2008 2009 2010 2011

CNG LNG

Total NGV Station Count

Growth Since 2008

197 CNG Stations & 8 LNG Stations Total Capital ~$500 Million

96

Source: Energy Information Administration (EIA), 2010; Statistics Canada; U.S. Dept of Energy AFDC.

Station Infrastructure

Shell/Travel Centers of America

− 100 LNG stations planned

Clean Energy LNG station expansion

− “America’s Natural Gas Highway”

Encana/Heckmann

− Mobile and fixed stations

Over 100 new CNG stations planned

New Natural Gas Vehicles and Engines

“Big 3” offering pick-ups

Volvo/Navistar – on road

Cummins/Westport – on road

Caterpillar/Cummins – off road

Caterpillar/Westport – rail

Industry Announcements

67

Natural Gas Fueling Projects through 2012Paving the Way for Transportation and Operations

Infrastructure Investment− 8 to 9 CNG stations− 1 mini liquefaction plant; additional planned− 12 mobile LNG stations− 1 fixed LNG station, additional planned− Rig vaporization equipment

Operations− 300+ CNG pickups − 10 to 16+ drilling rigs− Pilot completions pumping project (8 units)− Saved $11 million in 2011

Customer Fuel Sales− Internal and 3rd party CNG− 200+ 3rd party LNG trucks committed− Drilling rigs/pressure pumping systems− EBITDA: $4.00 to $10.00/mcf

Louisiana CNG Station

Mobile LNG Station

Alberta LNG Plant

34

68

0

10

20

30

40

50

60

70

2009 2011 2013 2015 2017 2019

Bcf/d

China Korea Taiwan Singapore Thailand India Japan

Forecast

Source: Encana, IEA, IMF, Japan Statistics Bureau, KEEI, National Bureau of Statistics of China, Taiwan Bureau of Energy.

North American LNG Export OpportunityAsian Market Forecast to grow 25 Bcf/d by 2020

United States and Canada Poised to Capture a Material Portion

69

North American Proposed LNG Export Projects

Kitimat T1/T21.4 Bcf/d

2016Greenfield

Received Regulatory Approval

Approval Pending/ Not Filed

Shell/Asian Consortium

1.6 Bcf/d2020

Greenfield

Progress/ PETRONAS

2 Bcf/dUnknownGreenfield

Jordan Cove1.2 Bcf/dUnknownGreenfield

Gulf Coast LNG2.8 Bcf/dUnknownGreenfield

Freeport1.4 Bcf/dQ2 2017

Regas to Export

Cameron1.7 Bcf/dQ4 2016

Regas to Export

Lake Charles2 Bcf/d

UnknownRegas to Export

Cove Point1 Bcf/d

UnknownRegas to Export

Bcf/d of LNG Capacity

Regulatory Approved

Proposed Total

Canada 1.4 3.6 5.0

USA 2.2 10.1 12.3

Total North America

3.6 12.9 17.3

Source: Encana, Company Reports/Filings, J.P. Morgan

Sabine Pass2.2 Bcf/d

Q4 2015 – PH 1Q1 2017 – PH 2Regas to Export

35

70

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

(200) (100) 0 100 200 300 400 500 600 700 800

August 2011 - March 2012 April 2012 - Present

NYMEX

Weekly L48 Storage Inventory Compared to Five-Year Moving Average

Source: Encana Fundamentals, EIA, and CME Group; *Note: the five-year average used in this analysis is not the same as EIA reported five-year average.

Prices fell as inventory relative to the five-year average grew substantially. Starting in April, the relative inventory started to decrease as storage injections

have remained well below the five-year average.

Growing surplus relative to five-year average sends prices lower

Shrinking surplus relative to five-year average sends prices higher

Natural Gas Yield CurveRelative Storage and Price Relationship

71

2.8

0.4

3.3

0.9

-2.1

-0.4

1.0

1.1

0.8

0.6

0.7

0.9

-0.1 -0.3

0.10.2

-0.1

-3

-2

-1

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013

Dry Gas Liquids Rich Gas Associated Gas

Bcf/d

Dry natural gas production is expected to continue to decline and will only partially be offset by increases in liquids rich gas and associated gas production.

North American Production Change by Year Dry, Liquids Rich, and Associated Gas Breakout

Source: Encana Fundamentals, IHS; *Note: Forecast does not contemplate shut-in volumes.

Forecast

2.3

0.10.2

4.9

2.8

(0.4)

36

72

0 2 4 6 8 10 12 14 16 18 20 22

$0.00 - 0.50

$0.50 - 1.00

$1.00 - 1.50

$1.50 - 2.00

$2.00 - 2.50

$2.50 - 3.00

$3.00 - 3.50

$3.50 - 4.00

$4.00 - 4.50

$4.50 - 5.00

$5.00 - 5.50

$5.50 - 6.00

>$6.00

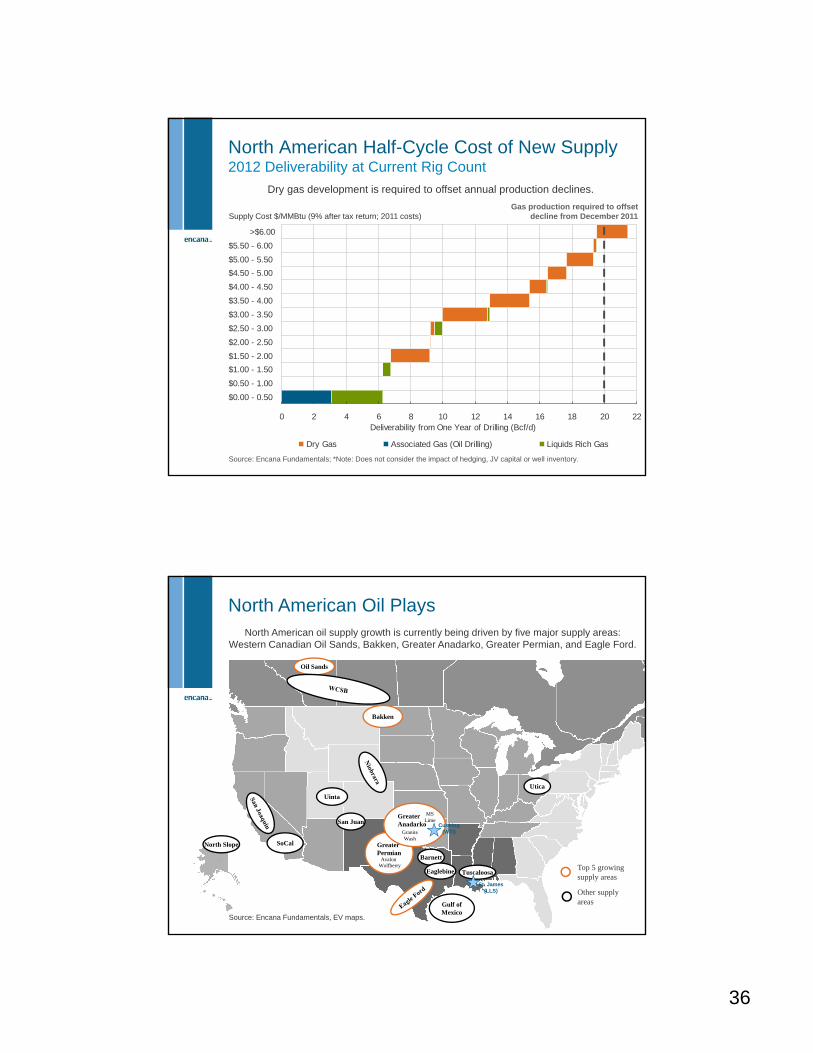

Deliverability from One Year of Drilling (Bcf/d)

Dry Gas Associated Gas (Oil Drilling) Liquids Rich Gas

Supply Cost $/MMBtu (9% after tax return; 2011 costs)

Dry gas development is required to offset annual production declines.

North American Half-Cycle Cost of New Supply 2012 Deliverability at Current Rig Count

Source: Encana Fundamentals; *Note: Does not consider the impact of hedging, JV capital or well inventory.

Gas production required to offset decline from December 2011

73

Tuscaloosa

St. James(LLS)

Source: Encana Fundamentals, EV maps.

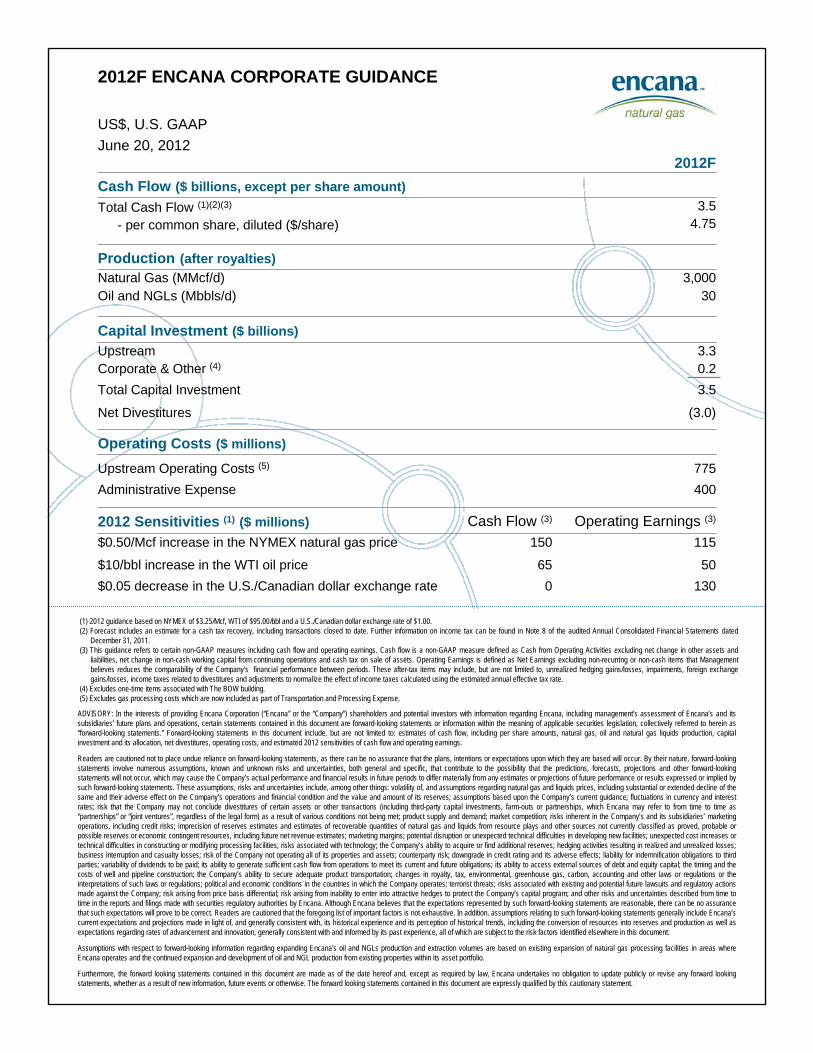

North American Oil Plays

Oil Sands

Bakken

Utica

SoCal

Uinta

San Juan

Gulf ofMexico

Greater Permian

WolfberryAvalon Barnett

Eaglebine

Greater Anadarko Cushing

(WTI)

MS Lime

Granite Wash

North Slope

North American oil supply growth is currently being driven by five major supply areas: Western Canadian Oil Sands, Bakken, Greater Anadarko, Greater Permian, and Eagle Ford.

Top 5 growing supply areas

Other supply areas

37

74

Cushing(WTI)

St. James (LLS)

Keystone XLNorth(700)

Flanagan South (585)

Keystone XLMarketLink

(830)

Seaway Projects**

(850)

Trans Mountain

Expansions(450)

NorthernGateway

(850)

10 Projects(>1,500)

2 Projects(275)

Basin(50)

2 Projects(250)

7 Projects (825)

Primary Hub

XX

XX

XX

XX

XX

XX

XX

Oilsands/Bakken: 585 Mbbls/d by Jun-14

Bakken: 825 Mbbls/d by Jan-15

Rockies: 250 Mbbls/d by Mar-14

Permian: 325 Mbbls/d by Mar-13

Eagle Ford: 1,500 Mbbls/d by Jan-13

Midcon to Gulf: 1,680 Mbbls/d by Jan-15

Oilsands: 2,000 Mbbls/d by Jun-17

N.A. Oil Pipeline Projects under Development7 MMbbls/d of Capacity Slated to be Online by Mid-2017*

Source: Encana Fundamentals, Bentek, Deutsche Bank, various pipeline companies.

*Includes only major projects (new projects and expansions of existing pipelines).

**Includes a reversal in direction for the existing pipeline (400) and the construction of a new “twin” project (450).

75

Proposed N.A. NGL Pipeline Expansion 2 MMbbls/d Slated to be Online by Mid-2014

MontBelvieu

Conway

Sarnia

Marcellus

WesternCanada

Hobbs

South LA

East Rockies

SkellyMedford

Midwest

Bakken

West Rockies

+60

+65

+400

+50

+50

+267

+60

+45

+480+470

+150

+125

+343

Primary Hub

Secondary Hub

Mixed NGLs

Ethane Only

LPG Export

+XX Expansion Mbbls/d

Source: Encana Fundamentals, EV Maps, company announcements.

Numerous new NGL pipelines are currently under development across North America.

38

76

500

700

900

1,100

1,300

1,500

1,700

2005 2007 2009 2011 2013 2015 2017

New Builds

Exports

Restart

Conversions,Debottlenecking andExpansions

Base Demand

Supply

Mbbls/d

Source: Encana Fundamentals (outlook), EIA (historical).

U.S. Ethane Supply vs. DemandIncluding Exports

In the near-term, we expect the market to be tightly balanced. Going forward, the viability of the North American ethane market depends on how many new

greenfield steam crackers are built.

Forecast

77

0

50

100

150

200

250

300

350

2005 2007 2009 2011 2013 2015 2017

DemandExpansions

Demand*

Supply

The ethane market in Western Canada has the ability to expand to meet growing supply.

Western Canadian Ethane Supply vs. Demand Including Imports

Source: Encana, BCMEMR, ERCB, Linde Engineering, NEB, Nova Chemical; *Calculated as 96% of ethylene capacity.

Mbbls/dForecast

39

78

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2005 2007 2009 2011 2013 2015 2017

Spare ExportCapacity

Exports

Demand

Supply (IncludingImports fromCanada)

Propane demand is expected to grow steadily as exports increase.

Mbbls/d

Source: Encana Fundamentals (outlook), EIA (historical).

U.S. Propane Supply vs. Demand

Forecast

79

0

50

100

150

200

250

2005 2007 2009 2011 2013 2015 2017

Spare ExportCapacity

Exports

Demand

Supply

Western Canadian Propane Supply vs. Demand

Post 2016 export capacity expansions will likely be required to meet expected propane supply growth.

Mbbls/d

Source: Encana, BCMEMR, ERCB, NEB, USITC.

Cochin Pipeline Reversal

Forecast

40

80

0

1

2

3

4

5

6

7

8

9

10

Jan2005

Jul2005

Jan2006

Jul2006

Jan2007

Jul2007

Jan2008

Jul2008

Jan2009

Jul2009

Jan2010

Jul2010

Jan2011

Jul2011

Jan2012

Jul2012

Jan2013

Jul2013

Gulf of Mexico Other Anadarko Granite Wash

Williston Eagle Ford Wolfberry Avalon/Bone Springs

Permian Emerging

Bcf/d

Source: Encana Fundamentals, IHS, EIA.

Gas production from oil-directed drilling is currently 7.1 Bcf/d and is expected to increase to 8.8 Bcf/d by the end of 2013.

Forecast

Associated Gas Production Contribution from Oil Directed Drilling

81

The Evolving NGL Barrel

Ethane (C2) 37%

Propane (C3) 29%

Butanes (C4) 18%

Pentanes (C5+) 16%

Ethane (C2) 42%

Propane (C3) 28%

Butanes (C4) 17%

Pentanes (C5+) 13%

2001

NGL Barrel NGL Barrel

2011

NGL Barrel

2015F*

Ethane (C2) 45%

Propane (C3) 29%

Butanes (C4) 14%

Pentanes (C5+) 12%

The NGL barrel is becoming lighter over time for two reasons:(1) Gas stream’s composition is changing(2) Additional Cryogenic Capacity (Deep Cut facilities) are adding more ethane to the market

Source: Encana, U.S. EIA; *Encana estimate.

Ethane will continue to become a larger portion of the NGL barrel.

41

82

2012 U.S. GAAP Conversion

Encana has adopted U.S. GAAP for 2012 financial reporting

– Previously followed Canadian GAAP/IFRS, with annual U.S. GAAP reconciliations

Why convert?

– Improves comparability of financial results with peers

– Uncertainty on the future role of IFRS in the U.S.

– Provides quarterly U.S. GAAP financial results and analysis

Conversion completed in early 2012

– 2012 first quarter financial statements and MD&A issued under U.S. GAAP

83

APA EOG DVN ECA TLM NXY APC SWN CHK

Credit Rating Comparison As of May 31, 2012

- Indicates ratings below investment grade

S&P Moody’s

AAA Aaa

AA+ Aa1

AA Aa2AA- Aa3

A+ A1

A A2

A- A3

BBB+ Baa1

BBB Baa2

BBB- Baa3

BB+ Ba1

BB Ba2

BB- Ba3

B+ B1B B2

42

84

2012 U.S. GAAP ConversionCash Flow & Operating Earnings

($ millions)

$0

$200

$400

$600

$800

$1,000

$1,200

Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 11 Q1 12

U.S. GAAP - Cash Flow U.S. GAAP - Operating Earnings

IFRS - Cash Flow IFRS - Operating Earnings

85

Refocusing Capital AllocationRapid Transition to Liquids Focused Investments

0

0.5

1

1.5

2

2.5

3

2011 2012F 2013F

Oil Liquids Rich Natural Gas Natural Gas

Represents upstream capital only. 2013 based on mid-point or $4.0 - $5.0 capital investment.

$ billions

23%

49%

36% 27%

50%

34%

65%

15%

1%

Capital Allocation by Commodity

43

In the interests of providing Encana shareholders and potential investors with information regarding Encana, including management’s assessment of Encana’s and its subsidiaries’ future plans and operations, certain statements contained in this presentation are forward-looking statements or information within the meaning of applicable securities legislation, collectively referred to herein as “forward-looking statements.” Forward-looking statements in this presentation include, but are not limited to: projections contained in the 2012 Corporate Guidance (including but not limited to estimates of cash flow, including per share amounts, natural gas, oil and natural gas liquids (“NGLs”) production, capital investment and its allocation, net divestitures, operating costs, and estimated 2012 sensitivities of cash flow and operating earnings); projections for 2013 (including but not limited to capital investment, net divestitures, net capital investment, natural gas, oil and NGLs and total liquids production, cash flow, net debt, and cash balance as of year-end); 2012 projected net debt and cash balance as of year-end; projection for long-term natural gas prices to reflect marginal supply cost; achieving a more balanced portfolio of production and cashflow; projected number of wells to be drilled in 2012 and their distribution among the Company’s plays; projected percentage shift of capital investments to liquids rich plays from 2012 to 2013 and expected cash flow contribution from liquids production by 2013; projected increase in liquids extraction capacities; the flexibility of capital spending plans and the sources of funding therefore; the ability to maintain investment grade credit rating; ability to attract new joint venture capital and implement existing joint ventures; projection to maintain current level of dividends; the effect of the Company's risk management program, including the impact of commodity price hedges in 2012 and 2013; projections, estimates and future plans and strategies for the Canadian and USA Divisions, various properties, plays basins and other assets, including liquids content and production growth for 2012-2013, PIIP, COIP, NGIP and EUR, target well cost, drilling, completion and tie-in (“DCT”) costs, operating cost, transportation cost, drilling plans and well inventories, reductions in supply costs and estimates of reserves and economic contingent resources; forecast date of first natural gas production for Deep Panuke; projected coal to gas displacement for 2012 to 2013; expected coal unit retirements by 2025 and expected increase in potential natural gas demand; expected increase in natural gas demand from transportation; projected North American LNG export opportunity up to 2020, including from Kitimat LNG Project; short-, medium- and long-term projected increase in natural gas demand from various sectors; projected North American natural gas production from 2012 to 2013, including by product types; projected future North American natural gas prices; projected U.S. and Western Canadian ethane and propane supply and demand up to 2017; and expectations for NGLs' prices, supply and demand in the future.

Readers are cautioned not to place undue reliance on forward-looking statements, as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur, which may cause the Company’s actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. These assumptions, risks and uncertainties include, among other things: volatility of, and assumptions regarding natural gas and liquids prices, including substantial or extended decline of the same and their adverse effect on the Company’s operations and financial condition and the value and amount of its reserves; assumptions based upon the Company’s current guidance; fluctuations in currency and interest rates; risk that the Company may not conclude divestitures of certain assets or other transactions (including third-party capital investments, farm-outs or partnerships, which Encana may refer to from time to time as “partnerships” or “joint ventures”, regardless of the legal form) as a result of various conditions not being met; product supply and demand; market competition; risks inherent in the Company’s and its subsidiaries’ marketing operations, including credit risks; imprecision of reserves estimates and estimates of recoverable quantities of natural gas and liquids from resource plays and other sources not currently classified as proved, probable or possible reserves or economic contingent resources, including future net revenue estimates; marketing margins; potential disruption or unexpected technical difficulties in developing new facilities; unexpected cost increases or technical difficulties in constructing or modifying processing facilities; risks associated with technology; the Company’s ability to acquire or find additional reserves; hedging activities resulting in realized and unrealized losses; business interruption and casualty losses; risk of the Company not operating all of its properties and assets; counterparty risk; downgrade in credit rating and its adverse effects; liability for indemnification obligations to third parties; variability of dividends to be paid; its ability to generate sufficient cash flow from operations to meet its current and future obligations; its ability to access external sources of debt and equity capital; the timing and the costs of well and pipeline construction; the Company’s ability to secure adequate product transportation; changes in royalty, tax, environmental, greenhouse gas, carbon, accounting and other laws or regulations or the interpretations of such laws or regulations; political and economic conditions in the countries in which the Company operates; terrorist threats; risks associated with existing and potential future lawsuits and regulatory actions made against the Company; risk arising from price basis differential; risk arising from inability to enter into attractive hedges to protect the Company’s capital program; and other risks and uncertainties described from time to time in the reports and filings made with securities regulatory authorities by Encana. Although Encana believes that the expectations represented by such forward-looking statements are reasonable, there can be no assurance that such expectations will prove to be correct. Readers are cautioned that the foregoing list of important factors is not exhaustive. In addition, assumptions relating to such forward-looking statements generally include Encana’s current expectations and projections made in light of, and generally consistent with, its historical experience and its perception of historical trends, including the conversion of resources into reserves and production as well as expectations regarding rates of advancement and innovation, generally consistent with and informed by its past experience, all of which are subject to the risk factors identified elsewhere in this presentation.

Assumptions with respect to forward-looking information regarding expanding Encana's oil and NGLs production and extraction volumes are based on existing expansion of natural gas processing facilities in areas where Encana operates and the continued expansion and development of oil and NGL production from existing properties within its asset portfolio.

Forward-looking information respecting anticipated 2012 cash flow for Encana is based upon, among other things, achieving average production for 2012 of 3.0 Bcf/d of natural gas and 30,000 bbls/d of liquids, commodity prices for natural gas and liquids based on NYMEX $3.25 per Mcf and WTI of $95 per bbl, an estimated U.S./Canadian dollar foreign exchange rate of $1.00 and a weighted average number of outstanding shares for Encana of approximately 736 million. Forward-looking information respecting anticipated 2013 cash flow for Encana is based upon achieving average production for 2013 of between 2.9 Bcf/d and 3.1 Bcf/d of natural gas and 60,000 bbls/d to 70,000 bbls/d of liquids, commodity prices for natural gas and liquids based on NYMEX $3.50 per Mcf and WTI of $90 per bbl, an estimated U.S./Canadian dollar foreign exchange rate of $1.00 and a weighted average number of outstanding shares for Encana of approximately 736 million.

Furthermore, the forward-looking statements contained in this presentation are made as of the date hereof and, except as required by law, Encana undertakes no obligation to update publicly or revise any forward-looking statements, whether as a result of new information, future events or otherwise. The forward-looking statements contained in this presentation are expressly qualified by this cautionary statement.

Future Oriented Information

National Instrument (“NI”) 51-101 of the Canadian Securities Administrators imposes oil and gas disclosure standards for Canadian public companies such as Encana engaged in oil and gas activities. Encana complies with the NI 51-101 annual disclosure requirements in its annual information form, most recently dated February 23, 2012 (“AIF”). The Canadian protocol disclosure is contained in Appendix A and under “Narrative Description of the Business” in the AIF. Encana has obtained an exemption dated January 4, 2011 from certain requirements of NI 51-101 to permit it to provide certain disclosure prepared in accordance with U.S. disclosure requirements, in addition to the Canadian protocol disclosure. That disclosure is primarily set forth in Appendix D of the AIF.

Reserves are the estimated remaining quantities of oil and natural gas and related substances anticipated to be recoverable from known accumulations, from a given date forward, based on: analysis of drilling, geological, geophysical and engineering data, the use of established technology, and specified economic conditions, which are generally accepted as being reasonable. Proved reserves are those reserves which can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves. Probable reserves are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves. Possible reserves are those additional reserves that are less certain to be recovered than probable reserves. It is unlikely that the actual remaining quantities recovered will exceed the sum of the estimated proved plus probable plus possible reserves.

The estimates of economic contingent resources contained in this presentation are based on definitions contained in the Canadian Oil and Gas Evaluation Handbook. Contingent resources do not constitute, and should not be confused with, reserves. Contingent resources are defined as those quantities of petroleum estimated, on a given date, to be potentially recoverable from known accumulations using established technology or technology under development, but which are not currently considered to be commercially recoverable due to one or more contingencies. Economic contingent resources are those contingent resources that are currently economically recoverable. In examining economic viability, the same fiscal conditions have been applied as in the estimation of reserves. There is a range of uncertainty of estimated recoverable volumes. A low estimate is considered to be a conservative estimate of the quantity that will actually be recovered. It is likely that the actual remaining quantities recovered will exceed the low estimate, which under probabilistic methodology reflects a 90 percent confidence level. A best estimate is considered to be a realistic estimate of the quantity that will actually be recovered. It is equally likely that the actual remaining quantities recovered will be greater or less than the best estimate, which under probabilistic methodology reflects a 50 percent confidence level. A high estimate is considered to be an optimistic estimate. It is unlikely that the actual remaining quantities recovered will exceed the high estimate, which under probabilistic methodology reflects a 10 percent confidence level.

There is no certainty that it will be commercially viable to produce any portion of the volumes currently classified as economic contingent resources. The primary contingencies which currently prevent the classification of Encana's disclosed economic contingent resources as reserves include the lack of a reasonable expectation that all internal and external approvals will be forthcoming and the lack of a documented intent to develop the resources within a reasonable time frame. Other commercial considerations that may preclude the classification of contingent resources as reserves include factors such as legal, environmental, political and regulatory matters or a lack of markets.

The estimates of various classes of reserves (proved, probable, possible) and of contingent resources (low, best, high) in this presentation represent arithmetic sums of multiple estimates of such classes for different properties, which statistical principles indicate may be misleading as to volumes that may actually be recovered. Readers should give attention to the estimates of individual classes of reserves and contingent resources and appreciate the differing probabilities of recovery associated with each class.

Encana uses the terms resource play, total petroleum initially-in-place, natural gas-in-place, and crude oil-in-place. Resource play is a term used by Encana to describe an accumulation of hydrocarbons known to exist over a large areal expanse and/or thick vertical section, which when compared to a conventional play, typically has a lower geological and/or commercial development risk and lower average decline rate. Total petroleum initially-in-place (“PIIP”) is defined by the Society of Petroleum Engineers - Petroleum Resources Management System (“SPE-PRMS”) as that quantity of petroleum that is estimated to exist originally in naturally occurring accumulations. It includes that quantity of petroleum that is estimated, as of a given date, to be contained in known accumulations prior to production plus those estimated quantities in accumulations yet to be discovered (equivalent to “total resources”). Natural gas-in-place (“NGIP”) and crude oil-in-place (“COIP”) are defined in the same manner, with the substitution of “natural gas” and “crude oil” where appropriate for the word “petroleum”. As used by Encana, estimated ultimate recovery (“EUR”) has the meaning set out jointly by the Society of Petroleum Engineers and World Petroleum Congress in the year 2000, being those quantities of petroleum which are estimated, on a given date, to be potentially recoverable from an accumulation, plus those quantities already produced therefrom.

In this presentation, Encana has provided information with respect to certain of its plays and emerging opportunities which is “analogous information” as defined in NI 51-101. This analogous information includes estimates of PIIP, NGIP, COIP or EUR, all as defined in the Canadian Oil & Gas Evaluation Handbook (“COGEH”) or by the SPE-PRMS, and/or production type curves. This analogous information is presented on a basin, sub-basin or area basis utilizing data derived from Encana's internal sources, as well as from a variety of publicly available information sources which are predominantly independent in nature. Some of this data may not have been prepared by qualified reserves evaluators or auditors and the preparation of any estimates may not be in strict accordance with COGEH. Regardless, estimates by engineering and geo-technical practitioners may vary and the differences may be significant. Encana believes that the provision of this analogous information is relevant to Encana's oil and gas activities, given its acreage position and operations (either ongoing or planned) in the areas in question.

There is no certainty that it will be commercially viable to produce any portion of the estimated PIIP, NGIP, COIP or EUR. 30-day IP and short-term rates are not necessarily indicative of long-term performance or of ultimate recovery.

In this presentation, certain oil and NGLs volumes have been converted to cubic feet equivalent (cfe) on the basis of one barrel (bbl) to six thousand cubic feet (Mcf). Cfe may be misleading, particularly if used in isolation. A conversion ratio of one bbl to six Mcf is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent value equivalency at the well head. Given that the value ratio based on the current price of oil as compared to natural gas is significantly different from the energy equivalency of 6:1, utilizing a conversion on a 6:1 basis may be misleading as an indication of value.

For convenience, references in this presentation to “Encana”, the “Company”, “we”, “us” and “our” may, where applicable, refer only to or include any relevant direct and indirect subsidiary corporations and partnerships (“Subsidiaries”) of Encana Corporation, and the assets, activities and initiatives of such Subsidiaries.

Advisory Regarding Reserves Data & Other Oil & Gas Information Disclosure Protocols

(1) 2012 guidance based on NYMEX of $3.25/Mcf, WTI of $95.00/bbl and a U.S./Canadian dollar exchange rate of $1.00.(2) Forecast includes an estimate for a cash tax recovery, including transactions closed to date. Further information on income tax can be found in Note 8 of the audited Annual Consolidated Financial Statements dated

December 31, 2011. (3) This guidance refers to certain non-GAAP measures including cash flow and operating earnings. Cash flow is a non-GAAP measure defined as Cash from Operating Activities excluding net change in other assets and

liabilities, net change in non-cash working capital from continuing operations and cash tax on sale of assets. Operating Earnings is defined as Net Earnings excluding non-recurring or non-cash items that Management believes reduces the comparability of the Company's financial performance between periods. These after-tax items may include, but are not limited to, unrealized hedging gains/losses, impairments, foreign exchange gains/losses, income taxes related to divestitures and adjustments to normalize the effect of income taxes calculated using the estimated annual effective tax rate.

(4) Excludes one-time items associated with The BOW building.(5) Excludes gas processing costs which are now included as part of Transportation and Processing Expense.