barbados: summary bond termsvmwealth.vmbs.com/documents/barbadosbondsanalysisfeb2013.pdf ·...

TRANSCRIPT

Prepared by: VMWM Research Department; February 19, 2013

Page 1 of 11

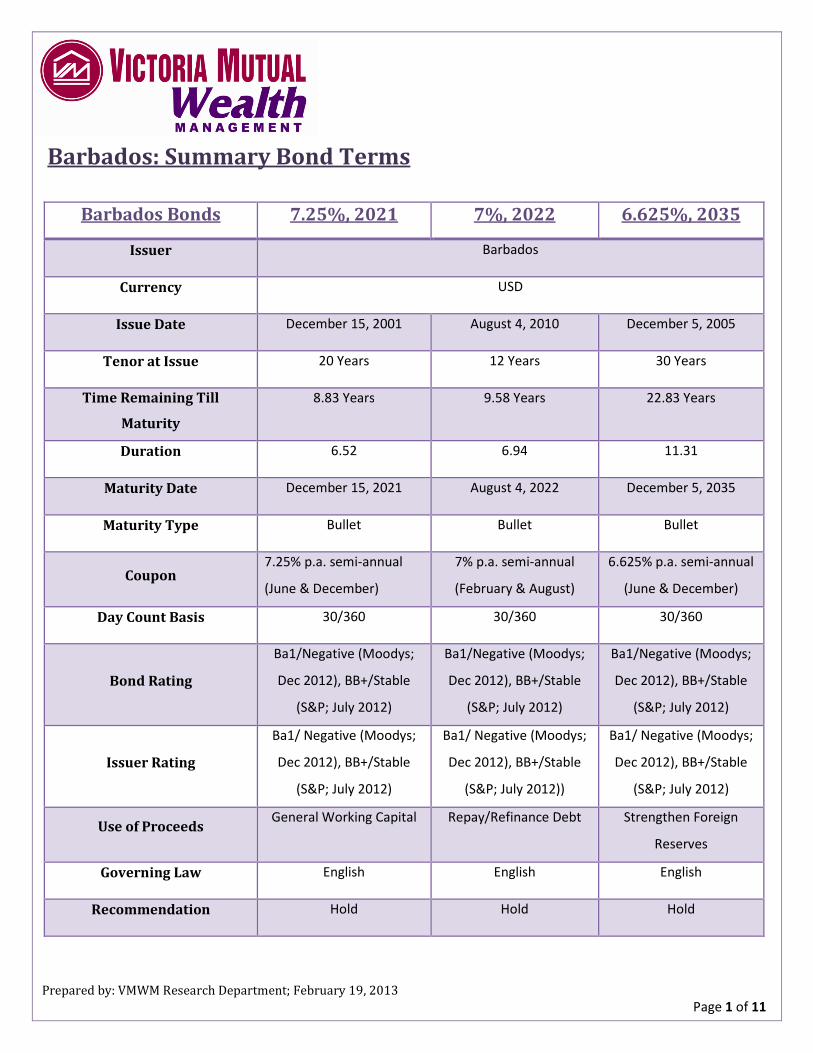

Barbados: Summary Bond Terms

Barbados Bonds 7.25%, 2021 7%, 2022 6.625%, 2035

Issuer Barbados

Currency USD

Issue Date December 15, 2001 August 4, 2010 December 5, 2005

Tenor at Issue 20 Years 12 Years 30 Years

Time Remaining Till

Maturity

8.83 Years 9.58 Years 22.83 Years

Duration 6.52 6.94 11.31

Maturity Date December 15, 2021 August 4, 2022 December 5, 2035

Maturity Type Bullet Bullet Bullet

Coupon 7.25% p.a. semi-annual

(June & December)

7% p.a. semi-annual

(February & August)

6.625% p.a. semi-annual

(June & December)

Day Count Basis 30/360 30/360 30/360

Bond Rating

Ba1/Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012)

Ba1/Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012)

Ba1/Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012)

Issuer Rating

Ba1/ Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012)

Ba1/ Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012))

Ba1/ Negative (Moodys;

Dec 2012), BB+/Stable

(S&P; July 2012)

Use of Proceeds General Working Capital Repay/Refinance Debt Strengthen Foreign

Reserves

Governing Law English English English

Recommendation Hold Hold Hold

Prepared by: VMWM Research Department; February 19, 2013

Page 2 of 11

Barbados Bonds - Analysis

Country Overview

Barbados is a sovereign island located in the Lesser Antilles with an approximate population of 284,000

people. The country holds the privilege of being one of the most developed Caribbean islands and one of

the leading tourist destinations in the region. Being a highly service dominated economy (75% of GDP

and 80% of exports); tourism is well-known to be its flagship income generator with diversification

towards light industrial activities in recent years. From 2009, at the onset of the global economic

downturn, the tourism sector faced declining revenues. This trend continued through 2012 as issues

involving the UK’s Air Passenger Duty increase, closure of the popular Almond Resorts and a reduced

number of flights to the island have significantly contributed to the contraction of the tourism sector.

Regardless of this fall-off in revenue over the years, the country still enjoys one of the highest per capita

incomes in the region. To supplement tourism, offshore finance and information services are also

important foreign exchange earners for the Barbadian economy which boasts a highly educated

workforce and 99.7% literate population. Despite strong economic fundamentals, Barbados suffers a

high public debt-to-GDP ratio which increased from 88% in 2008 to over 100% in June 2009 as a result

of the sharp decline in revenues from tourism and financial services.

In 2012, ratings agencies S&P and Moody’s lowered their ratings and outlook on the sovereign to

BB+/speculative and Ba1/negative, making Barbados sovereign bonds below investment grade (junk

bonds). This is representative of the country’s weak growth prospects and flat economic performance

along with a gradual deterioration in the debt position. Barbados has also been experiencing a decline in

global competitiveness and reduced productivity due in part to the economy’s heavy dependence on

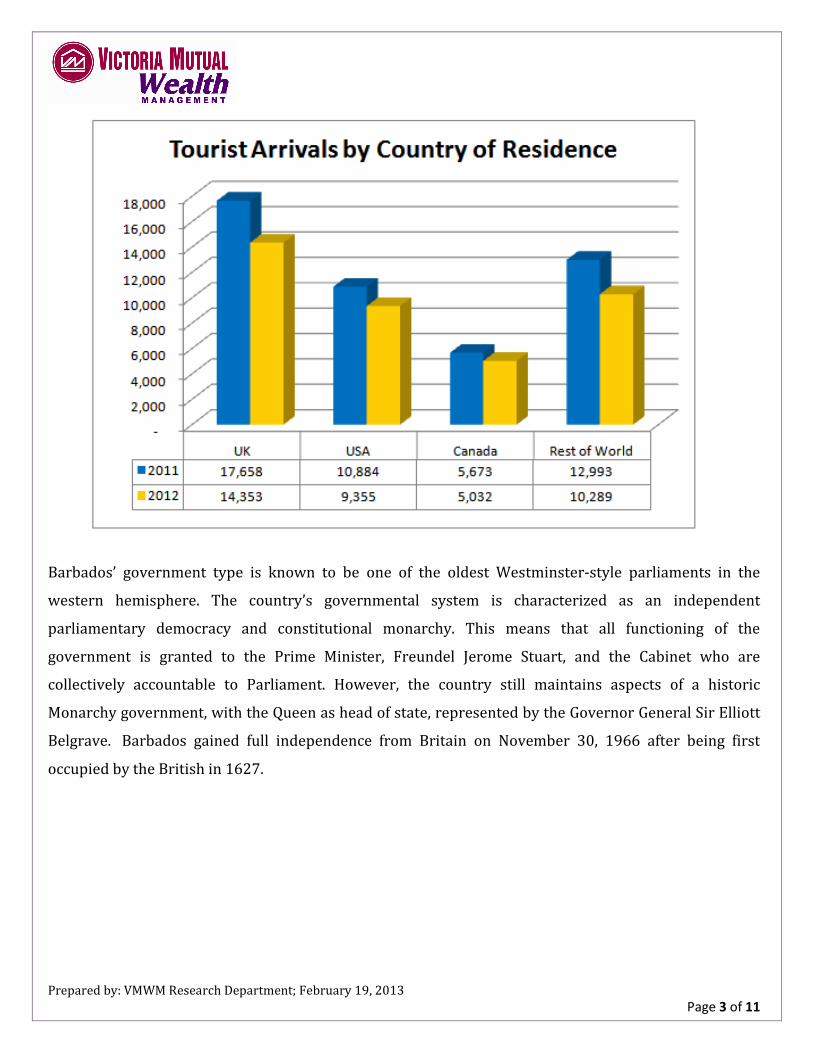

tourism, which has been on the decline for a number of years. For the period January – November 2012,

the country recorded a decrease when compared with the same period in 2011 of 6.4% with 480,183

stay-over arrivals. This may be as a result of the depressed global economy, upon which Barbados

depends for business, especially from the North American region (USA & Canada) and the United

Kingdom. It is for this reason that the government wishes to embark on a mission to pursue a

diversification strategy which will see the capturing of new markets in Latin America, specifically

targeting mining, oil and gas as well as financial services.

Prepared by: VMWM Research Department; February 19, 2013

Page 3 of 11

Barbados’ government type is known to be one of the oldest Westminster-style parliaments in the

western hemisphere. The country’s governmental system is characterized as an independent

parliamentary democracy and constitutional monarchy. This means that all functioning of the

government is granted to the Prime Minister, Freundel Jerome Stuart, and the Cabinet who are

collectively accountable to Parliament. However, the country still maintains aspects of a historic

Monarchy government, with the Queen as head of state, represented by the Governor General Sir Elliott

Belgrave. Barbados gained full independence from Britain on November 30, 1966 after being first

occupied by the British in 1627.

Prepared by: VMWM Research Department; February 19, 2013

Page 4 of 11

Barbados: Economic Indicators

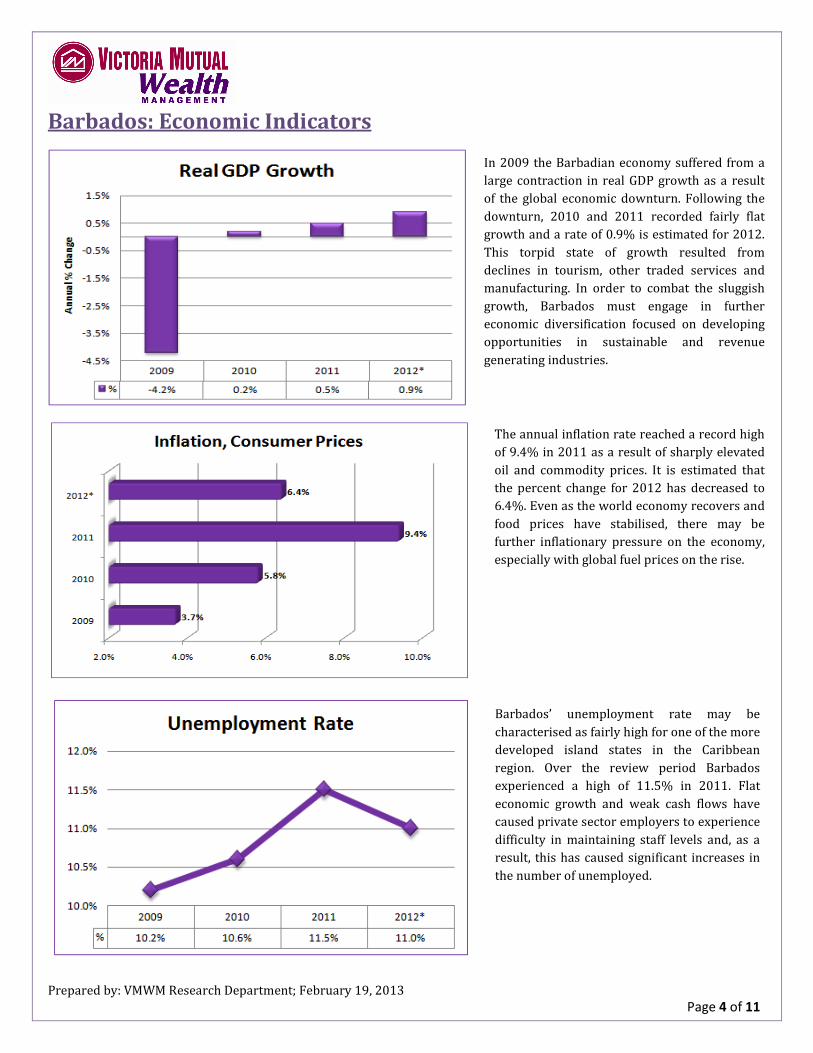

In 2009 the Barbadian economy suffered from a

large contraction in real GDP growth as a result

of the global economic downturn. Following the

downturn, 2010 and 2011 recorded fairly flat

growth and a rate of 0.9% is estimated for 2012.

This torpid state of growth resulted from

declines in tourism, other traded services and

manufacturing. In order to combat the sluggish

growth, Barbados must engage in further

economic diversification focused on developing

opportunities in sustainable and revenue

generating industries.

The annual inflation rate reached a record high

of 9.4% in 2011 as a result of sharply elevated

oil and commodity prices. It is estimated that

the percent change for 2012 has decreased to

6.4%. Even as the world economy recovers and

food prices have stabilised, there may be

further inflationary pressure on the economy,

especially with global fuel prices on the rise.

Barbados’ unemployment rate may be

characterised as fairly high for one of the more

developed island states in the Caribbean

region. Over the review period Barbados

experienced a high of 11.5% in 2011. Flat

economic growth and weak cash flows have

caused private sector employers to experience

difficulty in maintaining staff levels and, as a

result, this has caused significant increases in

the number of unemployed.

Prepared by: VMWM Research Department; February 19, 2013

Page 5 of 11

Barbados: Economic Indicators

*Estimated Figures

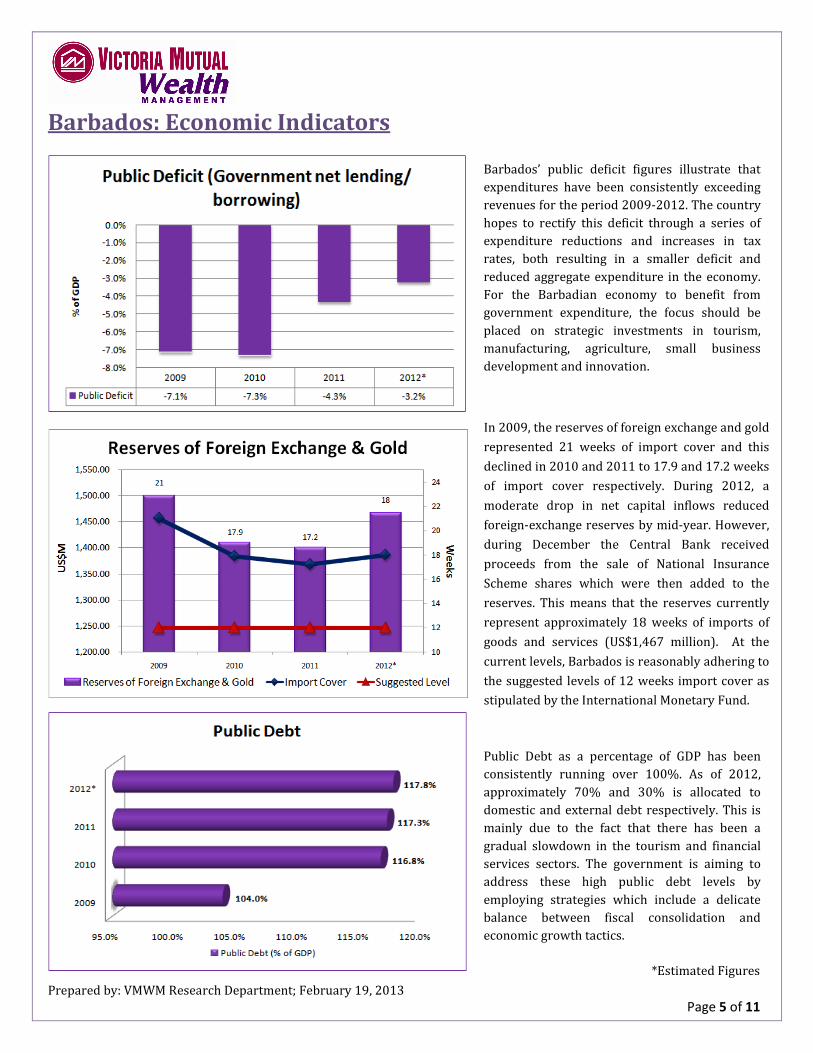

Barbados’ public deficit figures illustrate that

expenditures have been consistently exceeding

revenues for the period 2009-2012. The country

hopes to rectify this deficit through a series of

expenditure reductions and increases in tax

rates, both resulting in a smaller deficit and

reduced aggregate expenditure in the economy.

For the Barbadian economy to benefit from

government expenditure, the focus should be

placed on strategic investments in tourism,

manufacturing, agriculture, small business

development and innovation.

Public Debt as a percentage of GDP has been

consistently running over 100%. As of 2012,

approximately 70% and 30% is allocated to

domestic and external debt respectively. This is

mainly due to the fact that there has been a

gradual slowdown in the tourism and financial

services sectors. The government is aiming to

address these high public debt levels by

employing strategies which include a delicate

balance between fiscal consolidation and

economic growth tactics.

In 2009, the reserves of foreign exchange and gold

represented 21 weeks of import cover and this

declined in 2010 and 2011 to 17.9 and 17.2 weeks

of import cover respectively. During 2012, a

moderate drop in net capital inflows reduced

foreign-exchange reserves by mid-year. However,

during December the Central Bank received

proceeds from the sale of National Insurance

Scheme shares which were then added to the

reserves. This means that the reserves currently

represent approximately 18 weeks of imports of

goods and services (US$1,467 million). At the

current levels, Barbados is reasonably adhering to

the suggested levels of 12 weeks import cover as

stipulated by the International Monetary Fund.

Prepared by: VMWM Research Department; February 19, 2013

Page 6 of 11

Barbados Bonds – Historical Data*

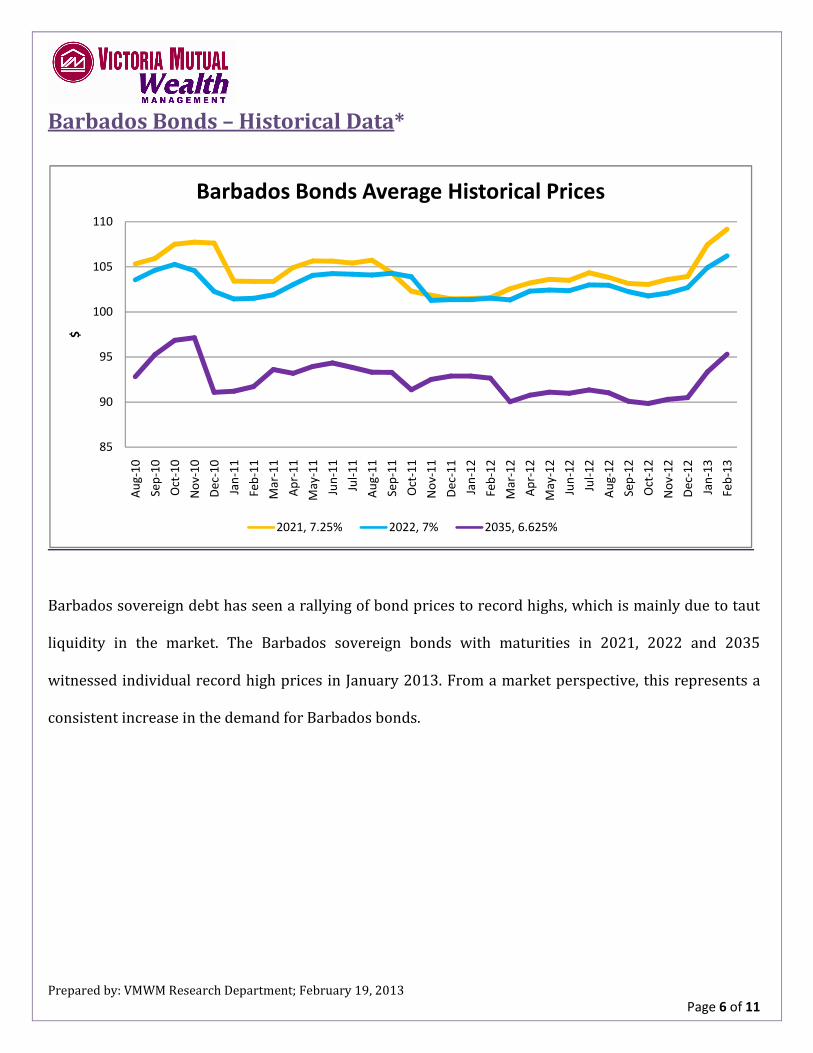

Barbados sovereign debt has seen a rallying of bond prices to record highs, which is mainly due to taut

liquidity in the market. The Barbados sovereign bonds with maturities in 2021, 2022 and 2035

witnessed individual record high prices in January 2013. From a market perspective, this represents a

consistent increase in the demand for Barbados bonds.

85

90

95

100

105

110

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Jun

-12

Jul-

12

Au

g-1

2

Se

p-1

2

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Fe

b-1

3

$

Barbados Bonds Average Historical Prices

2021, 7.25% 2022, 7% 2035, 6.625%

Prepared by: VMWM Research Department; February 19, 2013

Page 7 of 11

Barbados Bonds – Historical Data*

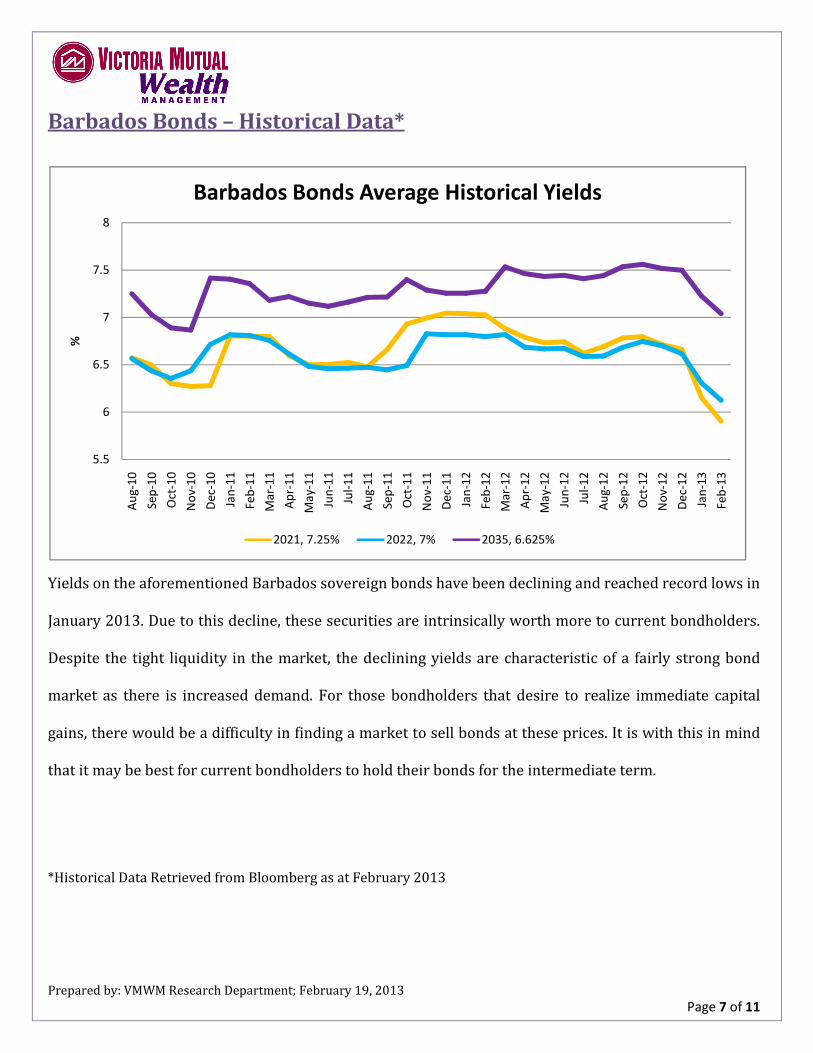

Yields on the aforementioned Barbados sovereign bonds have been declining and reached record lows in

January 2013. Due to this decline, these securities are intrinsically worth more to current bondholders.

Despite the tight liquidity in the market, the declining yields are characteristic of a fairly strong bond

market as there is increased demand. For those bondholders that desire to realize immediate capital

gains, there would be a difficulty in finding a market to sell bonds at these prices. It is with this in mind

that it may be best for current bondholders to hold their bonds for the intermediate term.

*Historical Data Retrieved from Bloomberg as at February 2013

5.5

6

6.5

7

7.5

8

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Jun

-12

Jul-

12

Au

g-1

2

Se

p-1

2

Oct

-12

No

v-1

2

De

c-1

2

Jan

-13

Fe

b-1

3

%

Barbados Bonds Average Historical Yields

2021, 7.25% 2022, 7% 2035, 6.625%

Prepared by: VMWM Research Department; February 19, 2013

Barbados Bonds – Spread An

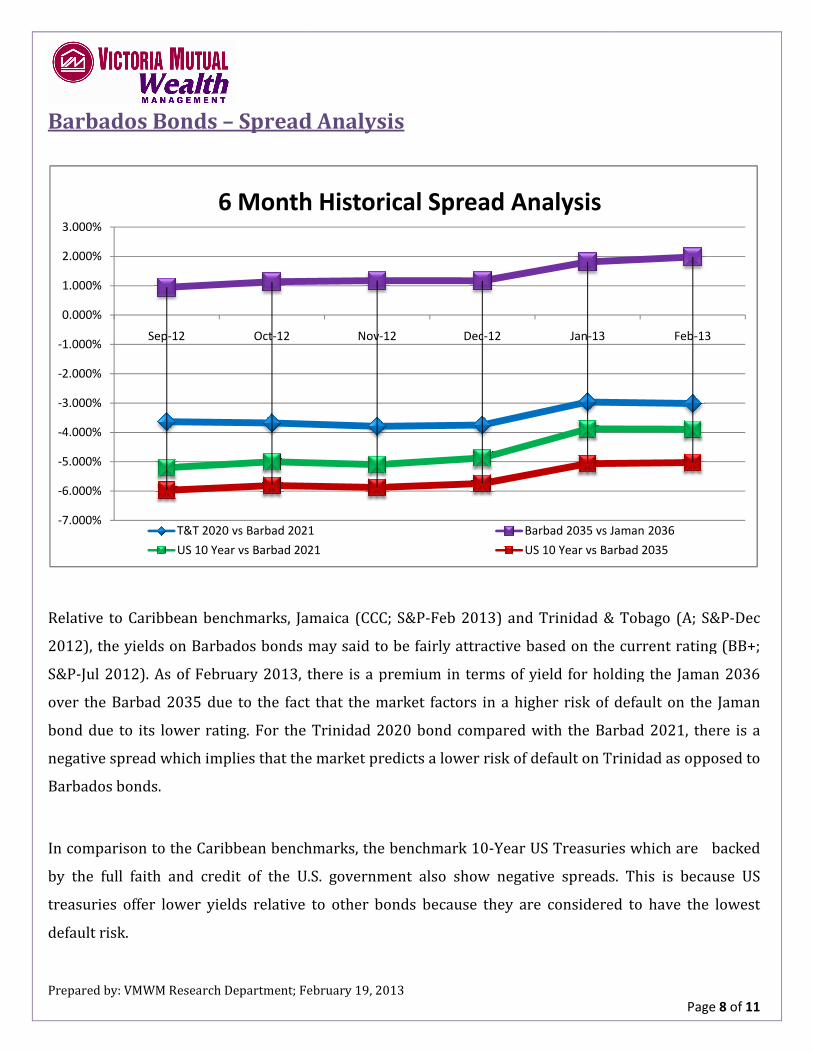

Relative to Caribbean benchmarks, Jamaica (CCC; S&P

2012), the yields on Barbados bonds may said to be

S&P-Jul 2012). As of February 2013, there is a premium in terms of yield for holding the Jaman 2036

over the Barbad 2035 due to the fact that the

bond due to its lower rating. For the Trinidad 2020 bond compared wi

negative spread which implies that the market predicts a low

Barbados bonds.

In comparison to the Caribbean benchmarks, the benchmark 10

by the full faith and credit of the U.S. government also show negative spreads. This is because US

treasuries offer lower yields relative to other bonds because they are considered to have the lowest

default risk.

-7.000%

-6.000%

-5.000%

-4.000%

-3.000%

-2.000%

-1.000%

0.000%

1.000%

2.000%

3.000%

Sep-12 Oct-12

6 Month Historical Spread Analysis

T&T 2020 vs Barbad 2021

US 10 Year vs Barbad 2021

February 19, 2013

Spread Analysis

Relative to Caribbean benchmarks, Jamaica (CCC; S&P-Feb 2013) and Trinidad &

on Barbados bonds may said to be fairly attractive based on the current rating

As of February 2013, there is a premium in terms of yield for holding the Jaman 2036

d 2035 due to the fact that the market factors in a higher risk of

For the Trinidad 2020 bond compared with the Barbad 2021, there is a

negative spread which implies that the market predicts a lower risk of default on Trinidad as opposed to

In comparison to the Caribbean benchmarks, the benchmark 10-Year US Treasuries which are backed

credit of the U.S. government also show negative spreads. This is because US

treasuries offer lower yields relative to other bonds because they are considered to have the lowest

Nov-12 Dec-12 Jan-13

6 Month Historical Spread Analysis

T&T 2020 vs Barbad 2021 Barbad 2035 vs Jaman 2036

US 10 Year vs Barbad 2021 US 10 Year vs Barbad 2035

Page 8 of 11

Feb 2013) and Trinidad & Tobago (A; S&P-Dec

fairly attractive based on the current rating (BB+;

As of February 2013, there is a premium in terms of yield for holding the Jaman 2036

factors in a higher risk of default on the Jaman

th the Barbad 2021, there is a

er risk of default on Trinidad as opposed to

Year US Treasuries which are backed

credit of the U.S. government also show negative spreads. This is because US

treasuries offer lower yields relative to other bonds because they are considered to have the lowest

Feb-13

Barbad 2035 vs Jaman 2036

US 10 Year vs Barbad 2035

Prepared by: VMWM Research Department; February 19, 2013

Page 9 of 11

Risk Factors

1. The economic growth of the Barbadian economy is significantly dependent on revenue from its

tourism and international business and financial services sectors, both of which have been

negatively affected by the global economic downturn.

2. The Government’s liquidity has been previously negatively affected by the global economic crisis.

If any similar exogenous factors further affect the potential economic prosperity of Barbados, this

could put extreme pressure on the net international reserves (NIR) in the future.

3. The Government may have to increase borrowing if it continues to run fiscal deficits.

4. There is an inherent liquidity risk for bondholders that may want to sell their securities quickly.

Currently, these bonds are not widely traded in the markets and as such there may not be a

medium through which to sell and realize immediate capital gains.

5. Policies imposed by the central government in the future such as the adjusting of any interest

rates will have an impact on bond prices. Duration analysis is used to measure this interest rate

risk and demonstrates the sensitivity of bond prices to a change in interest rates. Based on the

duration calculations, for every 100 basis-point (1%) decrease in interest rates for the 2021,

2022 and 2035 bonds it is expected that bond prices will increase by 6.54%, 6.96% and 11.33%

respectively. These Barbados sovereign bonds are fixed-rate in nature and consequently, if there

is any change in interest rates, investors will see bond price changes reflective of the increasing

volatility associated with a longer time until maturity.

Prepared by: VMWM Research Department; February 19, 2013

Page 10 of 11

Outlook & Recommendation

The Barbadian economy is expected to experience modest growth due to the expected increase in

economic growth of the country’s main trading partners (US, UK and Canada). With this in mind, the

government’s goal to diversify the economy to take advantage of opportunities in the oil and gas and

financial services sectors will further solidify its trade and industry position in the region. With this

diversification strategy, the government will tackle concerns of competitiveness and growth, while

prudently managing the debt. This will cause Barbados to be well on its way to restoring investor

confidence and promoting economic stability over the long term.

With regards to Barbados sovereign debt, the current yields are fairly attractive for bonds with a non-

investment grade rating. It is known however that there is some illiquidity in the market for Barbados

bonds and we suggest that current investors may want to HOLD these bonds for the long term, if they

are willing to handle the exposure at current yields.

Sources: Bloomberg, Economic Commission for Latin America & the Caribbean (ECLAC), The Central Bank of Barbados, Central Intelligence Agency (CIA) World Factbook 2012, International Monetary Fund (IMF)

Disclaimer: This Research Paper is for information purposes only. The information stated herein may reflect the opinion and views of VM Wealth Management in relation to market conditions and does not constitute any representation or warranties in relation to investment returns and the credibility of the sources of information relied upon in the preparation of this

Prepared by: VMWM Research Department; February 19, 2013

Page 11 of 11

report, without further research and verification. Before making any investment decision, please consult a VM Wealth Management Advisor.