barangay manual volume i (operating procedures)

DESCRIPTION

Barangay ManualTRANSCRIPT

OPERATING PROCEDURES IN THE

MANAGEMENT OF BARANGAY FUNDS AND PROPERTY

Volume I

Introduction

Objectives of the Manual.

1. To provide uniform guidelines in the administration and recording of barangay funds and property; and

2. To prescribe barangay financial reports to be submitted to the City/Municipal Accountant.

Legal Basis. Article 1X-D, Section 2 par. (2) of the 1987 Constitution of the Republic of the Philippines provides:

“The Commission on Audit shall have the exclusive authority xxx to promulgate accounting and auditing rules and regulations xxx.”

Coverage. This Manual presents:

1. The general and basic policies in monitoring barangay funds and property; and2. The detailed narrative operating procedures and the corresponding procedural

flow charts for the following major financial transactions:

a. Receipts and Deposits b. Appropriations and Commitmentsc. Disbursementsd. Inventory, Property, Plant and Equipment (PPE), Public Infrastructures (PI)

and Reforestation Projects (RP)

The different forms prescribed are provided with instructions and presented as appendices in this Manual. For a comprehensive understanding of the operations of barangays in managing their funds and property, this Manual should be read side by side with the other two volumes on recording and reporting procedures.

1

Receipts and Deposits

Policies and Procedures. The basic policies for receipts and deposits of collections are as follows:

1. Collections

a. The Barangay Treasurer (BT) shall be responsible in handling collections of income and other receipts of the barangay and their deposit with the Authorized Government Depository Bank (AGDB);

b. All collections, either in cash or in check, shall be acknowledged by the issuance of a pre-numbered Official Receipt (OR) – General Form 51 or its equivalent;

c. All accountable forms shall be secured from the City/Municipal Treasurer; d. All checks shall be in the name of the Barangay;e. Temporary or provisional receipts shall not be issued to acknowledge collections; f. Endorsed checks shall not be accepted as payment of obligations to the Barangay; g. For checks received, the OR number and date of issue shall be indicated at the back

of the check for reference purposes; h. All particulars in the OR shall be filled out. Duplicate and triplicate copies of the

OR shall be the exact carbon copy of the original; i. Overages discovered during the cash count/cash examination shall be receipted and

added to the accountability of the BT; j. Cash shortages, including the loss of cash through force majeure, theft, robbery,

fire, etc. shall be deducted from the total cash account and the BT/Accountable Officer (AO) shall be held personally accountable, pending the result of the “Request for Relief from Cash Accountability” submitted to the Commission on Audit (COA); and

k. All collections by the BT for the barangay shall be reported in the Summary of Collections and Deposits (SCD).

2. Deposit of Collections

a. The BT shall deposit collections intact with AGDB, preferably on the following banking day and in exceptional cases deposit shall be done within five (5) days after receipt;

b. In the absence of an AGDB, deposits may be made in any bank nearest the Barangay as may be authorized by the Monetary Board of the Bangko Sentral ng Pilipinas;

c. The selection of a depository bank other than the AGDB shall be covered by a Resolution of the Sanggunian Barangay (SB) and approved by the Punong Barangay (PB). The said Resolution shall indicate the name of the bank, the type of

2

deposit to be maintained, whether current, savings or time deposit and the authorized signatories to the checks/fund withdrawals;

d. Funds earmarked for future operation which are not immediately needed may be transferred to time deposits for the account of the Barangay. Placement in time deposits shall be duly authorized by the SB and approved by the PB. Certificate of time deposit/bank book shall be in the name of the Barangay. Upon maturity, the check for the proceeds shall be issued in the name of the Barangay. Pre-termination of time deposit or its renewal/rollover, shall have prior authorization of the SB and approval of the PB;

e. In case of dishonored check, a “Notice of Dishonor” shall be immediately sent to the payor upon receipt of the Debit Memo (DM) from the bank;

f. The original of the dishonored check and a copy of the bank DM shall remain with the BT; and

g. All deposits by the BT for the Barangay shall be reported in the SCD.

3. Collections by the BT as deputized by the City/Municipal Treasurer

a. Collections made by the BT on behalf of the City/Municipal Treasurer, as deputized, shall be remitted intact daily to the City/Municipal Treasurer. In exceptional circumstances, remittances of said collections must be made within five (5) days after receipt;

b. All remittances shall be supported with a Summary of Collections and Remittances (SCR); and

c. The BT shall be accountable for all the forms received from the City/Municipal Treasurer for use in the collection.

4. Collections by the Barangay Collector as deputized by PB

a. Collections of Deputized Barangay Collector (DBC) shall be remitted daily to the BT;

b. All remittances shall be supported with SCR; c. The DBC shall be accountable for all the forms received from the BT for use in the

collection.

5. Credit Memo and Bank Statement

a. Credit memo received from the bank for direct remittance made by Local Government Units (LGUs) or the Department of Budget and Management (DBM) for the barangay share in Real Property Tax (RPT) or the Internal Revenue Allotment (IRA), respectively shall be recorded direct to the Cash on Hand and in

3

Bank Register (CHBReg) and in the Cash Receipts and Deposits Register (CRDReg);

b. The LGU or the DBM making the direct remittance shall furnish the barangay, a copy of the advice, for information and counter-check with the CM received from the bank: and

c. Interest earned on bank deposits shall be recorded at gross to the CHBReg and CRDReg.

6. Accountable Officers and Transfer of Accountabilities

a. The PB/BT and all AOs shall be bonded in accordance with the Department of the Interior and Local Government (DILG) Memo Circular No. 99-186 dated October 11, 1999. The corresponding premium shall be paid out of the barangay funds;

b. All PPE with insurable risk shall be covered by the Property Insurance Fund of the Government Service Insurance System;

c. All AOs leaving the office, either thru resignation or completion of terms/ suspension/retirement, shall seek clearances from money and property accountabilities. They shall accomplish the Transfer of Property and Money Accountability (TPMA) form.

1) All cash held shall be refunded/account closed and any unused accountable forms shall be surrendered and property accountabilities returned;

2) The Property Acknowledgement Report (PAR) and Inventory Custodian Slip (ICS) held shall be cancelled upon return of the items; and

3) The AO’s shall likewise transfer/submit/surrender all documents supporting the entries in the registers submitted to the City/Municipal Accountant and any records in their possession to the incoming officers.

4) All AOs shall seek clearance from the PB5) The PB shall seek clearance from the City/Municipal Mayor6) The approved clearance shall served as one of the supporting documents to the

last claim for honoraria/salaries of the officials

7. Barangay Record Keeper

When the funds of the barangay permits a Barangay Record Keeper (BRK) shall be hired to do the following:

a. Maintain the different registers and registries;b. Examine correctness of recording and completeness of supporting documents in the

different summaries:

4

1) Act as custodian of the different summaries and supporting documents of the different AOs;

2) Prepares the Disbursement Vouchers (DVs)/payroll, Purchase Requests (PRs), Purchase Orders (POs), contracts; and

3) Prepares the transmittal letter submitting the registers, DM/Credit Memo (CM) bank statement, copies of the summaries and other documents to the City/Municipal Accountant.

Barangay Collections. Barangay collections include, but are not limited, to the following:

1. Share in national and local taxes/revenues:

a. Internal Revenue Allotment b. Utilization of national wealth, such as: lands of public domain, water, mineral, coal,

petroleum, mining, oil, gas and oil deposits, etc.c. Tobacco Excise Tax (R.A. 7171)d. Real Property Tax, including interests and penalties imposed thereone. Tax imposed on sand, gravel and other quarry products f. Community Tax Certificate (CTC)

2. Barangay fees and taxes:

a. Fees imposed on:

1) Peddlers2) Breeding of fighting cocks3) Use of barangay roads, waterways, bridges and parks4) Parking5) Use of barangay properties/facilities6) Clearance/certification 7) Other fees imposed by the barangay

b. Taxes imposed on stores/retailers within the barangay c. Penalties for violation of barangay ordinance

3. Other fees and charges from:

a. Operation of cockpits, places of recreation, etc.b. Fund raising activities

5

c. Charges on billboards, signboards and other outdoor advertisementsd. Use of barangay operated public markets, slaughterhouses and waterworkse. Operation of other barangay economic enterprises

4. Others sources:

a. Subsidies from:

1) National Government 2) Financial assistance from provinces, cities or municipalities

b. Proceeds from: 1) Loans and other indebtedness2) Sale of PPE

c. Receipt of:

1) Performance/Bidders/Bail bonds2) Refund of Payroll Fund/Advances to Officers 3) Funds intended for specific purpose4) Payment for lost properties5) Payment due to overpayment of claims6) Other receipts

d. Grants and donations receivede. Dividend/Interest from investments

6

Table 1Receipt of Collections by Barangay Treasurer

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer 1 Receives cash/checks from payor representing collections of income/other receipts as well as remittances of DBC.

2 Prepares the OR.

Note 1. The OR shall be prepared in three copies to be distributed as follows:

Original – payor 2nd copy – to support the SCD )3rd copy – BT (retained in the booklet)

3 Issues OR to the payor to acknowledge collection.

Payor 4 Receives the original OR.

Barangay Treasurer 5 Retains the duplicate OR for submission to the BRK, as supporting document to the SCD.

6 Retains the 3rd copy of the OR in the booklet for file.

7

Legend: Symbols:

OR -Official Receipt - Flow of documentsSCD -Summary of Collections and Deposits - Prepares

- FileNotes:1. The OR shall be prepared in three copies - Document

to be distributed as follows: Original – Payor - Cash/Check 2 nd copy – to support the SCD

3 rd copy – BT (retained in the booklet) - Process

OPERATING PROCEDURES RECEIPT OF COLLECTIONS BY BARANGAY TREASURER

Procedural Flow Chart (Table 1a)

Barangay Treasurer

Cash/Check

1

44

OR 1-3

2

3

6

receives

issues

prepares

receive

to BRK

files

from vault

to payor

from payor

5

retains

note 1

OR 1

OR 2

OR 2

8

Table 2Collection and Remittance by Deputized Barangay Collectors

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

A Deputization of Barangay Collectors Deputized Barangay Collector

1 Receives the Authority from PB deputizing the DBC to collect markets/parking fees, etc.

2 Receives the accountable forms to be used/issued to acknowledge collections.

3 Files the Authority.

B Collections 4 Collects fees on market operation by issuing

cash tickets to market peddlers or parking fee tickets on the use of barangay pay parking lots.

5 Records collections in the SCR daily.

Note 1. See Table 2, Volume 11 for the recording of collections in the SCR and submission to the BT by DBC.

C Remittance of Collections 6 Submits three copies of duly certified SCR to

the BT together with the remitted collections.

Barangay Treasurer 7 Receives three copies of the SCR, together with the remittance.

8 Reviews the SCR and checks the completeness of data. Checks computation of accountable forms issued/sold as against the reported collections. Informs the collector in case of discrepancy.

9 Acknowledges the remittance by completing the acknowledgement portion of the SCR.

Note 2. The “acknowledgement” portion of the SCR shall be filled out by recording thereat the amount received and date of receipt.

10 Forwards a copy of the acknowledged SCR to the DBC and keeps the original file of SCR.

Deputized Barangay Collector

11 Receives the copy of the acknowledged SCR. Checks the amount remitted against the amount as acknowledged. Files copy of the SCR.

9

Area of Responsibility/Person Responsible Seq. Activity

Note 3. In case of discrepancy, informs the BT immediately.

Barangay Treasurer 12 Forwards another copy of the duly accomplished SCR to the BRK for file and checking the Report of Accountability for Accountable Forms (RAAF).

10

Legend: Symbols:

AF - Accountable Forms - Flow of DocumentsCT - Cash Tickets - Records/Issues

PFT - Parking Fee Tickets - FileSCR - Summary of Collections & RemittanceBRK - Barangay Record Keeper - Document

Note: - Cash1 See Table 2, Volume 11 for the recording

of collections in the SCR and submission - Processto the BT by DBC.

2 The “acknowledgement” portion of the SCR shall be filled out by recording thereat the amount received and date of receipt.

3 In case of discrepancy, informs the BT immediately

OPERATING PROCEDURES COLLECTION AND REMITTANCE BY DEPUTIZED BARANGAY COLLECTORS

Procedural Flow Chart (Table 2a)Deputized Barangay Collector Barangay Treasurer

PFT

AF 1Authority

12

1

CashCT

4

SCR1-33

3 2

SCR

1

7

6

8

10

3

SCR

2

11

Cash

3

5

Cash

9

12

Note 2Note 1

receives

receivesfrom Punong

Barangay

files

From Payor

collects &issues

records

submits

receives

reviews

acknowledges

receives

forwards

forwards

to BRK

11

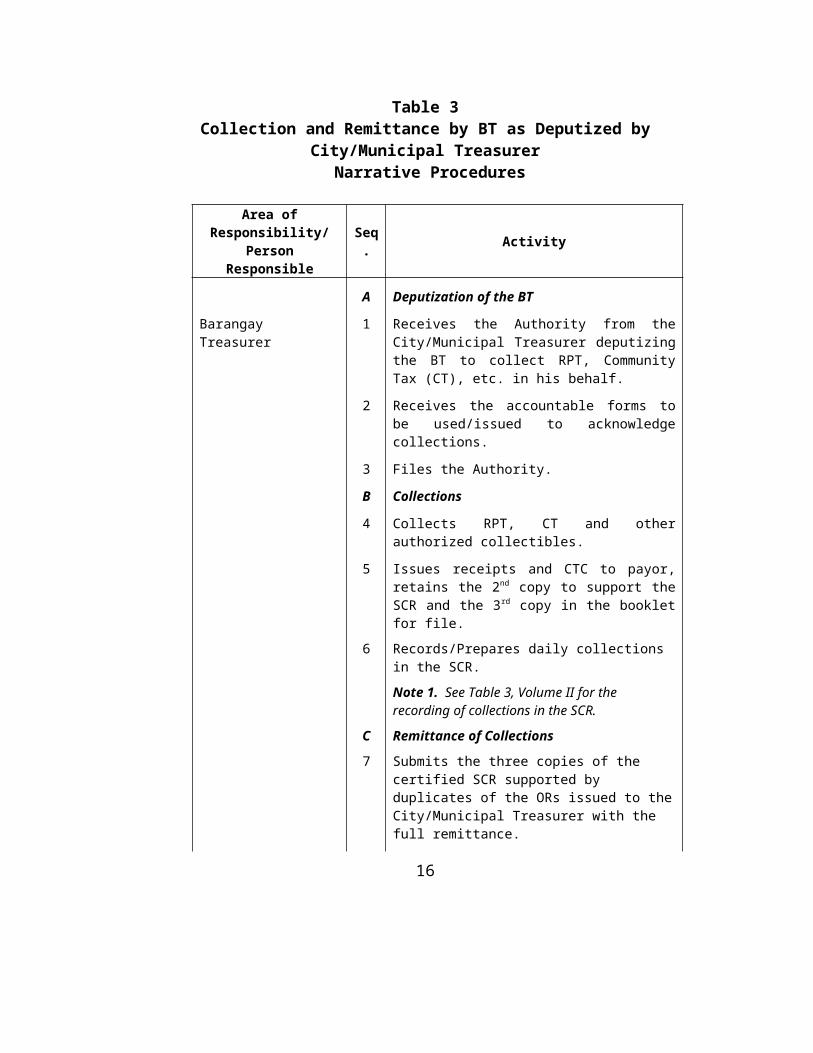

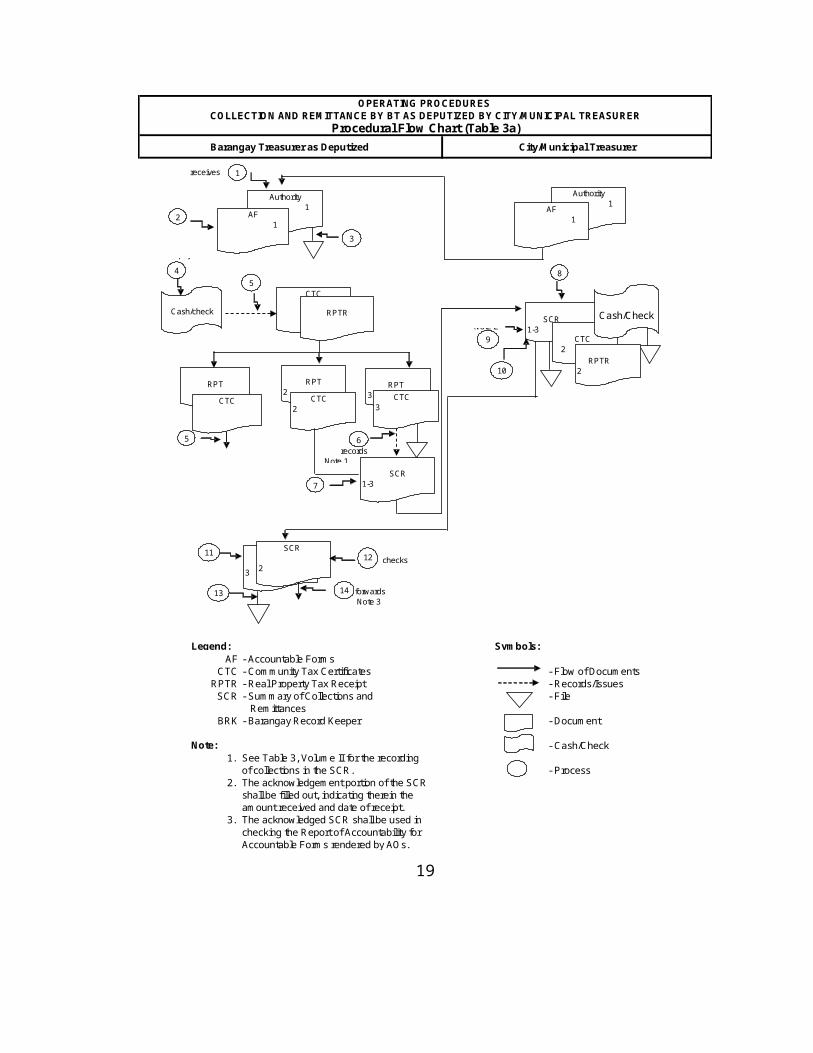

Table 3Collection and Remittance by BT as Deputized by

City/Municipal Treasurer Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

A Deputization of the BT Barangay Treasurer 1 Receives the Authority from the City/Municipal

Treasurer deputizing the BT to collect RPT, Community Tax (CT), etc. in his behalf.

2 Receives the accountable forms to be used/issued to acknowledge collections.

3 Files the Authority.

B Collections 4 Collects RPT, CT and other authorized

collectibles.

5 Issues receipts and CTC to payor, retains the 2nd copy to support the SCR and the 3rd copy in the booklet for file.

6 Records/Prepares daily collections in the SCR.

Note 1. See Table 3, Volume II for the recording of collections in the SCR.

C Remittance of Collections7 Submits the three copies of the certified SCR

supported by duplicates of the ORs issued to the City/Municipal Treasurer with the full remittance.

City/Municipal Treasurer

8 Examines the SCR as to completeness of supporting documents and correctness of recording of the OR issued.

9 Acknowledges receipt of the SCR and the remittance. Signs the acknowledgement portion of the SCR.

Note 2. The acknowledgement portion of the SCR shall be filled out, indicating therein the amount received and date of receipt.

10 Forwards two copies of the acknowledged SCR to the BT and retains the original copy for file.

Barangay Treasurer 11 Receives the two acknowledged copies of the SCR.

12

Area of Responsibility/Person Responsible Seq. Activity

12 Checks correctness of amount received and acknowledged against the actual remittance.

13 Files the acknowledged copy of the SCR.

14 Forwards a copy of the acknowledged SCR to the BRK.

Note 3. The acknowledged SCR shall be used in checking the RAAF rendered by AOs.

13

Legend: Symbols:AF - Accountable Forms

CTC - Community Tax Certificates - Flow of DocumentsRPTR - Real Property Tax Receipt - Records/Issues

SCR - Summary of Collections and - File Remittances

BRK - Barangay Record Keeper - Document

Note: - Cash/Check1. See Table 3, Volume II for the recording

of collections in the SCR. - Process2. The acknowledgement portion of the SCR

shall be filled out, indicating therein the amount received and date of receipt.

3. The acknowledged SCR shall be used in checking the Report of Accountability for Accountable Forms rendered by AOs.

OPERATING PROCEDURES COLLECTION AND REMITTANCE BY BT AS DEPUTIZED BY CITY/MUNICIPAL TREASURER

Procedural Flow Chart (Table 3a)Barangay Treasurer as Deputized City/Municipal Treasurer

Authority 1

AF 1

Authority 1

AF 1

2

Cash/check

4

SCR1-3

CTC

SCR1-33 CTC

2

8

7

6

3

SCR

2

13

1

Cash/Check

12

3

1-3 RPTR

1-39

5

RPT

CTC1

1

142

receives

receives

files

issues

collectsfrom payor

5

RPTR2

RPT2

CTC2

RPT3 CTC

3

issues records Note 1

submits

examines

acknowledges Note 2

10

forwards

checks11

receives

to BRk

forwards Note 3

files

14

Table 4Deposit of Collections with the Bank

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer 1 Counts collections (cash and checks).

2 Compares actual cash counted with the total collections indicated in the ORs issued and recorded in the SCD.

3 Prepares deposit slip.

Note 1. The Deposit Slip shall be prepared in three copies for bank validation, to be distributed as follows:

Original – bank 2nd copy – to support the recording in the

SCD 3rd copy – BT

4 Deposits collections intact with the depository bank, the following banking day.

Note 2. See Table I, Volume II for the recording of deposits in the SCD.

5 Receives two (2) copies of the VDS from the bank.

6 Retains a copy for file and attaches the original copy of the VDS to the SCD for submission to the BRK.

15

Legend: Symbols:

DS - Deposit Slip - Flow of DocumentsVDS - Validated Deposit Slip - PreparesOR - Official Receipts - File

SCD - Summary of Collections and Deposits

BRK - Barangay Record Keeper - DocumentsNotes:

1. The Deposit Slip (DS) shall be prepared in three copies for bank validation, to be - Cash and Checksdistributed as follows: Original – bank - Process 2nd copy – to support the recording in the SCD 3rd copy – BT

2. See Table I, Volume II for the recording of deposits in the SCD.

OPERATING PROCEDURES DEPOSIT OF COLLECTIONS WITH THE BANK

Procedural Flow Chart (Table 4a)Barangay Treasurer

Cash

VDS

1-2

1

VDS 2 6

DS

1-3

Cash

1

4

5

Checks

2

3

Checks

DS

1-3

from vault compares

prepares Note 1

OR 2

SCD

1

from file

counts

to bank

Note 2 deposits

from bank

receives

retains

attaches to SCD for submission to the BRK

16

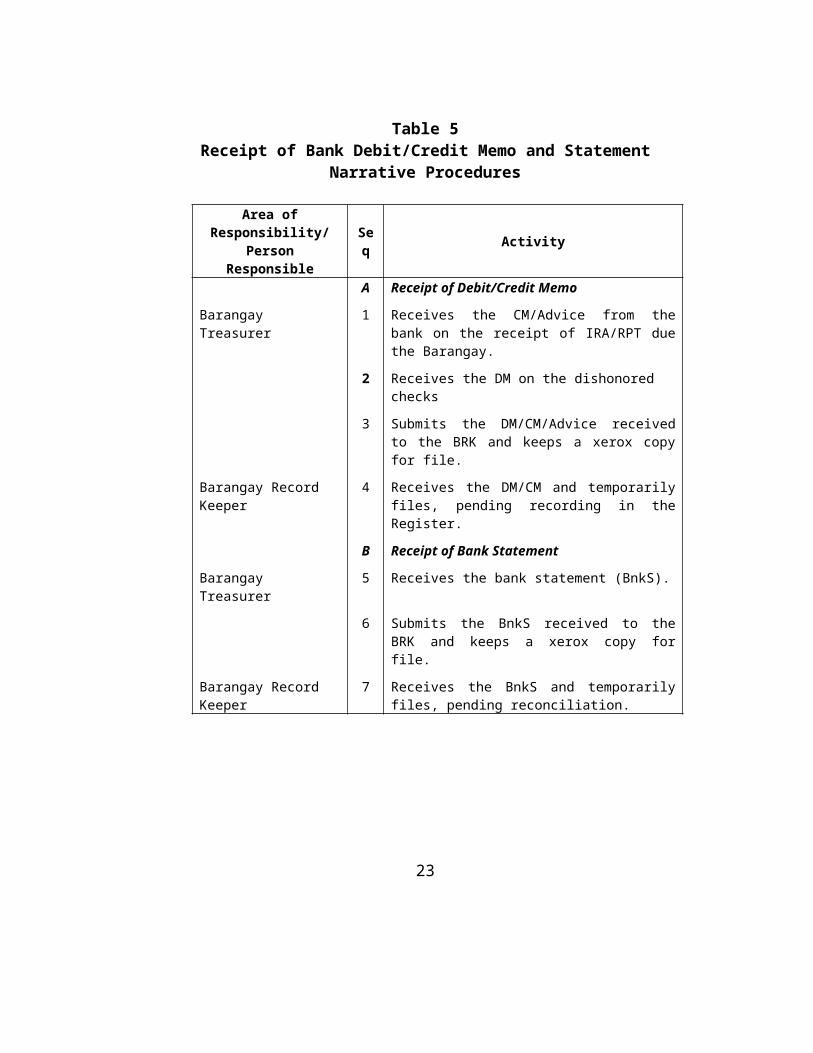

Table 5Receipt of Bank Debit/Credit Memo and Statement

Narrative Procedures

Area of Responsibility/Person Responsible Seq Activity

A Receipt of Debit/Credit MemoBarangay Treasurer 1 Receives the CM/Advice from the bank on the

receipt of IRA/RPT due the Barangay.

2 Receives the DM on the dishonored checks

3 Submits the DM/CM/Advice received to the BRK and keeps a xerox copy for file.

Barangay Record Keeper

4 Receives the DM/CM and temporarily files, pending recording in the Register.

B Receipt of Bank StatementBarangay Treasurer 5 Receives the bank statement (BnkS).

6 Submits the BnkS received to the BRK and keeps a xerox copy for file.

Barangay Record Keeper

7 Receives the BnkS and temporarily files, pending reconciliation.

17

Legend: Symbols:

x - xerox copy - Flow of DocumentsDM - Debit Memo

- File

- Document

- Process

OPERATING PROCEDURES RECEIPT OF BANK DEBIT/CREDIT MEMO AND STATEMENT

Procedural Flow Chart (Table 5a)Barangay Treasurer Barangay Record Keeper

CM/Advice1DM

2

5

1

DMx 1

3

xerox

Bank Statement x 1

7

from bank

receives

submits & xerox

receives

from bank

receives

Bank Statement 1

6 submits

receives & files

Credit Memo/Advice 1

DM

Credit Memo/Advice x

receives4

18

Appropriations and Commitments

Policies and Procedures. Laws, rules and regulations of the government provide that all disbursements of public funds, except those received for specific purposes, shall be covered by an approved General Appropriations Ordinance (GAO) authorizing appropriation for the annual budget. Unless authorized by the DBM, and covered by subsequent SB Resolution approving the appropriation, in no case shall commitments exceed the approved appropriations. The policies and procedures in monitoring the approved appropriations and its utilization are as follows:

1. Appropriations

a. The Kagawad, designated as Chairman, Committee on Appropriations (CCA) shall be responsible in monitoring the approved appropriations and the charges against the following funds:

1) General Fund ) 2) 20% Development Fund 3) Calamity Fund 4) Sanggunian Kabataan Fund 5) Gender and Development Fund

b. The CCA shall monitor the use of appropriated funds thru the Registry of Appropriations and Commitments (RAC) which shall be maintained by Fund and object of expenditures. In case the BRK maintains the registries, the CCA shall be provided a copy of the RAC monthly for his file. The CCA may inspect/examine/check anytime, the availability of funds and the recording in the registries.

2. Commitments

a. Charges (deductions) against the appropriated funds shall be based on the commitment made by the Barangay as shown in its Disbursement Vouchers (Appendix 1)/Payrolls (Appendix 2), Contract or Purchase Order (Appendix 3) and Requisition and Issue Slip (Appendix 4);

b. For infrastructure projects or purchase of equipment, the CCA shall certify availability of Funds by stamping “Funds Available” on the face of the PR and affixes his signature indicating the estimated required amount on the available appropriation on the Purchase Request (Appendix 5) based on the SB Resolution authorizing the construction/procurement;

19

c. In addition to the certification in the DVs/payrolls, the existence of available appropriation as reflected in the SB Resolution shall also be shown on the face of the contracts and PO; and

d. Expenses for Personal Services (PS), Maintenance and Other Operating Expenses (MOOE) and Financial Expenses (FE) shall be charged against Current Operating Expenses (COE) while investments, purchase of PPE and construction of infrastructures and reforestation projects shall be charged against appropriations for Capital Outlay (CO).

3. Certification of the CCA on the PO/Contract, etc.

The certification of the CCA that “funds available” is construed to mean the “availability of appropriations” to cover the commitment made on the PO, contract, etc.

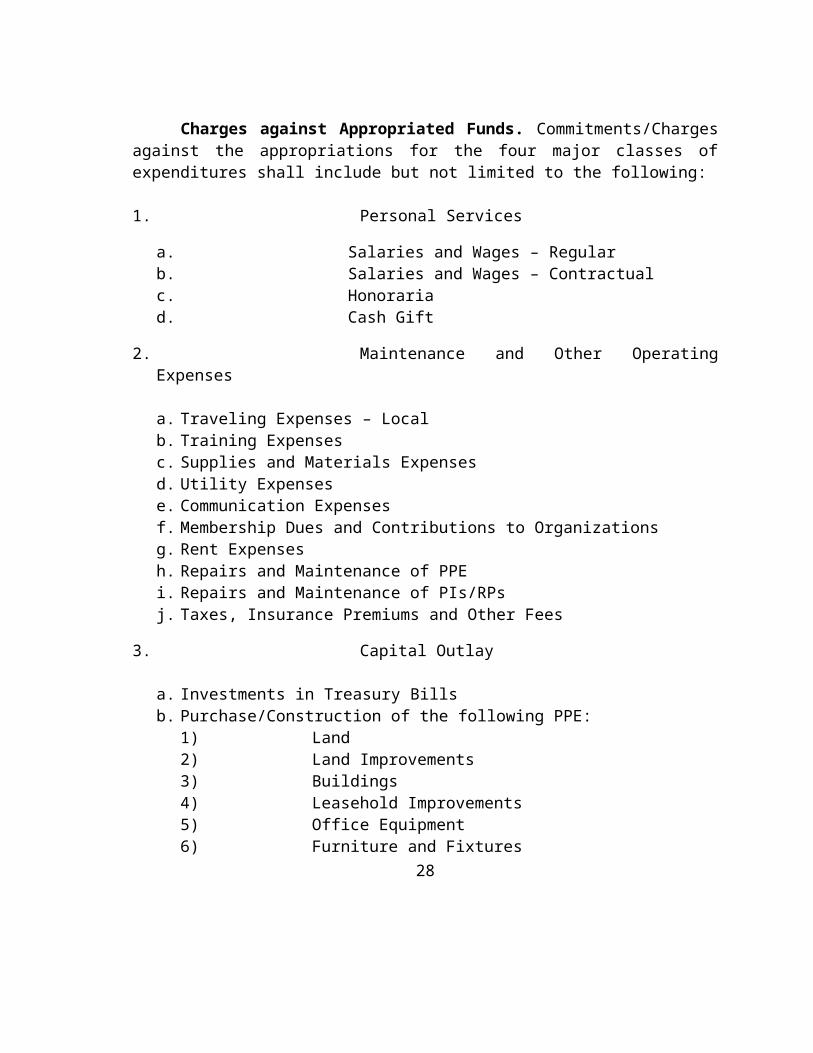

Charges against Appropriated Funds. Commitments/Charges against the appropriations for the four major classes of expenditures shall include but not limited to the following:

1. Personal Services

a. Salaries and Wages – Regularb. Salaries and Wages – Contractualc. Honorariad. Cash Gift

2. Maintenance and Other Operating Expenses

a. Traveling Expenses – Localb. Training Expensesc. Supplies and Materials Expensesd. Utility Expensese. Communication Expensesf. Membership Dues and Contributions to Organizationsg. Rent Expensesh. Repairs and Maintenance of PPE i. Repairs and Maintenance of PIs/RPsj. Taxes, Insurance Premiums and Other Fees

3. Capital Outlay

a. Investments in Treasury Billsb. Purchase/Construction of the following PPE:

20

1) Land2) Land Improvements 3) Buildings4) Leasehold Improvements5) Office Equipment6) Furniture and Fixtures7) Books8) Motor Vehicles9) Other Equipment

10) Public Infrastructures11) Reforestation Projects

4. Financial Expenses

a. Bank Charges (cost of checkbooks)b. Interest Expensesc. Other Financial Charges

21

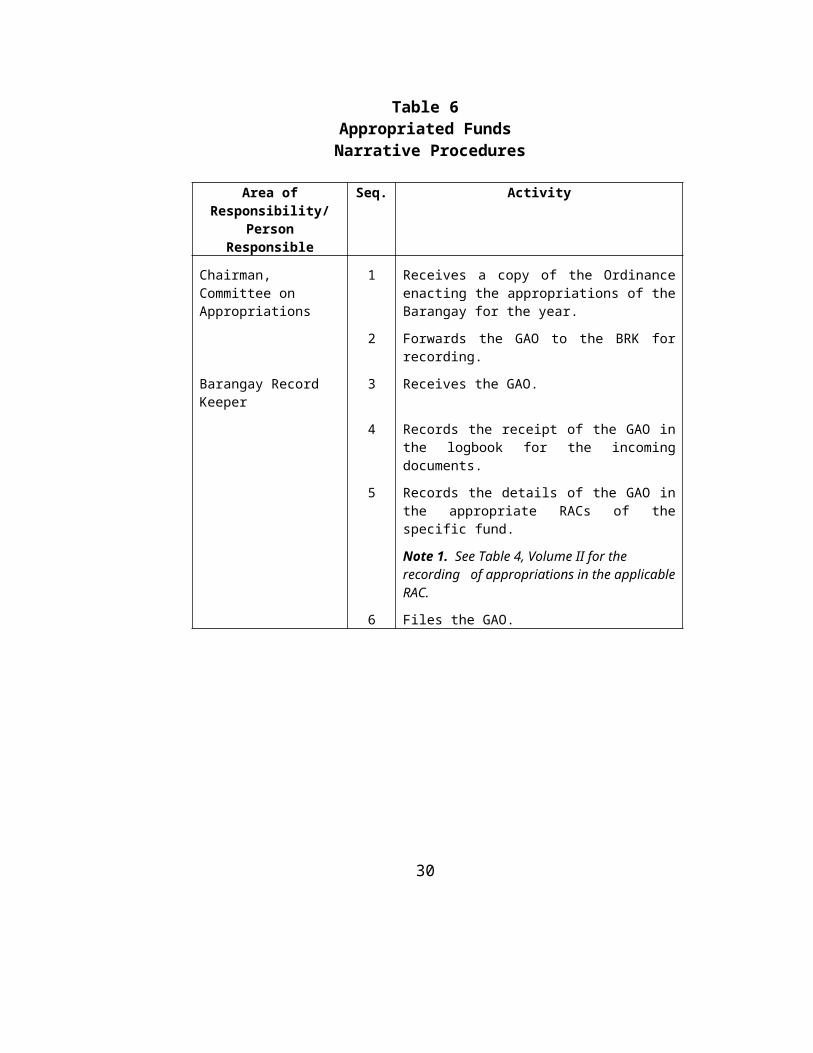

Table 6Appropriated Funds

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

Chairman, Committee on Appropriations

1 Receives a copy of the Ordinance enacting the appropriations of the Barangay for the year.

2 Forwards the GAO to the BRK for recording.

Barangay Record Keeper

3 Receives the GAO.

4 Records the receipt of the GAO in the logbook for the incoming documents.

5 Records the details of the GAO in the appropriate RACs of the specific fund.

Note 1. See Table 4, Volume II for the recording of appropriations in the applicable RAC.

6 Files the GAO.

22

Legend: Symbols: - Flow of Documents

RAC - Registry of Appropriations and - Records Commitments - File

LB - Log Book GAO - General Appropriations Ordinance - Document

Note:1 See Table 4, Volume II for the recording - Book /Registryof appropriations in the applicable RAC.

- Process

OPERATING PROCEDURES APPROPRIATED FUNDS

Procedural Flow Chart (Table 6a)Chairman, Committee on Appropriations Barangay Record Keeper

GAO 1

GAO 1

1

2

3

LB

RAC

4

56

receives

forwards

receives

records

records Note 1

files

23

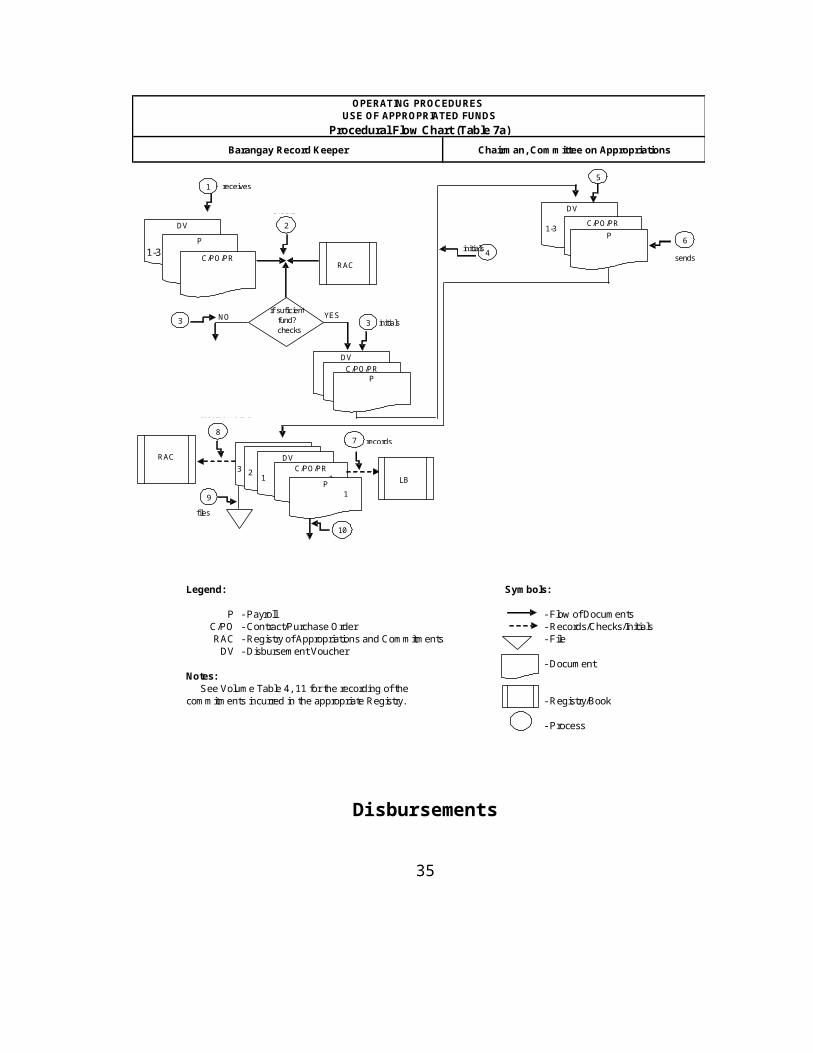

Table 7Use of Appropriated Funds

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

Barangay Record Keeper

1 Receives DV/payroll/claims/PR/contract/PO/ request together with all the supporting documents, for certification on the existence of available appropriation to cover the claims/PO/contract.

2 Checks the applicable Registry on the availability of appropriations for the specific charges/expenses.

3 If appropriations are not sufficient to cover the charges/expenses presented, returns the documents to the BT with the necessary information. In case the appropriations are sufficient, initials below the name of the CCA in Box A of the DV/payroll or in the applicable PO/contract.

4 Forwards the DV/payroll/PO/contract to the CCA for certification as to availability of appropriation.

Chairman, Committee on Appropriations

5 Examines the documents, checks the initial of the BRK and if in order, certifies on the “availability of appropriation” by signing in Box A of the DV/payroll/PO or in the case of infrastructure projects certifies availability of funds by stamping “Funds Available” on the face of the PR/contract.

6 Sends the certified documents back to the BRK for recording in the appropriate RAC.

Barangay Record Keeper

7 Acknowledges receipt of the certified document and records receipt in the logbook.

8 Records the commitments made in the appropriate RAC.

Note 1. See Volume II Table 4, 11 for the recording of the commitments incurred in the appropriate Registry.

9 Files a copy of the certified document.

10 Forwards the original documents together with supporting papers to the BT for

24

Area of Responsibility/ Person Responsible

Seq. Activity

processing/appropriate action.

Legend: Symbols:

P - Payroll - Flow of DocumentsC/PO - Contract/Purchase Order - Records/Checks/InitialsRAC - Registry of Appropriations and Commitments - File

DV - Disbursement Voucher - Document

Notes: See Volume Table 4, 11 for the recording of the commitments incurred in the appropriate Registry. - Registry/Book

- Process

OPERATING PROCEDURES USE OF APPROPRIATED FUNDS

Procedural Flow Chart (Table 7a)Barangay Record Keeper Chairman, Committee on Appropriations

DV

DV

1

RAC

5

3

P

DV

1-3

9

3 2

DV

1C/PO/PR

1P

1

2

C/PO/PR

7

1-31-3

6

10

receives

checks

if suficient fund?

checks

YES

C/PO/PR

NO

to BT

3 initials

returns

examines

P

P

sendsinitials

LB

LB

records

RAC

8

records Note 1

files

forwards

to BT

C/PO/PR

1-3

4

forwardsinitials

25

Disbursements

Policies and Procedures. Existing rules and regulations require that all disbursements of public funds be supported by documents necessary to prove their validity, propriety and legality. The basic policies on disbursement are as follows:

1. Disbursements by check

a. All disbursements shall be covered with duly processed and approved DVs/payrolls;

b. The DVs/payrolls shall be prepared by the BT/BRK;c. The BT shall be responsible for paying claims against the Barangay. All

disbursements shall be in accordance with existing rules and regulations;d. All claims shall be approved by the PB and certified as to the validity,

propriety and legality of the claim. In case of claim chargeable against Sanggunian Kabataan Fund (SKF) the Sanggunian Kabataan (SK) Chairman shall initial under the name of the PB;

e. Payments shall be drawn against the depository account maintained by the Barangay with AGDB;

f. The check shall be issued in the name of the payee as indicated in the DV/payroll;

g. The check shall be signed by the BT and countersigned by the PB;h. All disbursements by check shall be reported in the Summary of Checks

Issued (SCkI);i. In case of check which is waylaid, lost through theft or force majeure, etc.,

the BT shall be immediately notified and a “Stoppage of Payment” shall immediately be given to the bank; and

j. Stale check shall be replaced only when the original is submitted to the BT for replacement.

2. Disbursements out of cash advance for payroll

a. Cash payments shall be made out of the cash advance given to the BT/AO;

b. The cash advance shall be used solely for payment of salaries, honoraria and other allowances due the barangay officials;

c. Proceeds of the cash advance shall not be used for the encashment of checks or for liquidation of previous cash advances;

d. The cash advance shall be equal to the net amount of the payroll corresponding to the pay period;

26

e. The cash advance shall be liquidated within five (5) days after the end of the pay period. Any unclaimed honoraria/salaries/allowances shall be refunded to close the account;

f. The Summary of Cash Payments (SCP), supported by paid DVs/payroll shall be accomplished to support the liquidation of the cash advance for payroll. In case the cash advance is more than the disbursements the excess shall be refunded and an OR shall be issued. If disbursements is more than the cash advance a reimbursement shall be made;

g. All paid DVs/payrolls shall be recorded in the SCP; andh. Succeeding cash advance shall be granted only after full liquidation of the previous

one.

3. Disbursements out of cash advance for travel and special purpose

a. For local/foreign travel, liquidation shall be done within 30/60 days upon return to their respective station;

b. Cash advance for time-bound special activity shall be liquidated upon completion of the purpose for which it was granted;

c. The Liquidation Report (LR) shall be accomplished to support the liquidation of the cash advance. In case the cash advance is more than the disbursements, the excess shall be refunded and an OR shall be issued. If total disbursements is more than the cash advance, a reimbursement shall be made; and

d. In case the cash advance is equal to the total disbursements the LR supported with appropriate documents shall be submitted to the BRK who in turn shall submit it to the City/Municipal Accountant for recording in the books on the first week of the following month with transmittal letter.

4. Disbursements out of the Petty Cash Fund

a. The Petty Cash Fund (PCF) shall be maintained using the Imprest System;b. The fund shall be kept separately from the regular collections and advances granted

for a particular purpose;c. The amount of the PCF shall be determined by the SB but “not to exceed twenty

percent (20%) of the funds available and to the credit of the barangay treasury” (Sec. 334 (b) of R.A. 7160);

d. All disbursements out of PCF shall be covered by duly approved and accomplished Petty Cash Vouchers (Appendix 6) supported by cash invoices, ORs or other evidences of disbursements required under applicable accounting and auditing rules and regulations;

e. All paid Petty Cash Vouchers (PCVs) shall be reported in the Summary of Paid PCVs (SPPCVs) to be certified by the BT/Petty Cash Fund Custodian (PCFC);

27

f. The PCF shall be replenished as soon as disbursements reach seventy five percent (75%) or as needed;

g. Replenishment of the PCF shall be supported with duly certified SPPCVs, paid PCVs and supporting documents;

h. The balance of the PCF shall not be closed at the end of the year;i. In case the PCFC resigns or ceases as custodian of the Fund, full

accounting/liquidation of the Fund shall be made. Any remaining cash shall be refunded to close the account; and

j. In no case shall the remaining cash of the former PCFC be transferred to the incoming PCFC. For a complete accounting, the account of the former PCFC shall be closed and a new account shall be opened for the incoming PCFC.

Basic Supporting Documents for Disbursements. The basic supporting documents for typical barangay disbursement include but not limited to the following:

1. For payment of salaries/honoraria and other personal services:

a. Approved payroll supported by Daily Time Record (DTR)b. Minutes of Meeting of the Barangay Council duly signed by the council members

and Barangay Secretary granting honoraria to barangay personnel (for first claim)c. Approved application for leave (for leave with pay)d. Approved Appointment, Oath of Office, Certificate of Assumption of Office and

Statement of Assets and Liabilities for newly hired employees (for first claim)

2. For cash advance for payroll

a. Net payroll for the period

3. For grant of cash advance for travel

a. Travel Order (TO)b. Itinerary of Travel (IT)

4. Liquidation of cash advances

a. Payroll Fund – paid DVs/payroll and LRb. Travel - original of the TO, plane/bus tickets or its equivalent, ORs, if any, boarding

pass, Certificate of Appearance and Liquidation Report (Appendix 7) c. Training Expenses – Certificate of Appearance and Certificate of Training (for

claims after the training) and Invitation to attend the training (claim before the training)

28

5. For payment of maintenance and other operating expenses

a. Membership Dues – Statement of Accounts/bills of the organizationb. Utility and Communication expenses – Billsc. Repairs and Maintenance – Job Orders, Invoices, Certificate of

Warranty/Guarantee, Pre-repair Inspection Report and Post-repair Inspection Report, Inspection and Acceptance Report (IAR), labor payroll (for repairs undertaken by administration) or contract (for repairs undertaken by contract)

6. For purchase of equipment, supplies and other items (please refer to R.A. 9184 for the modes of procurement, necessary procedures and documents needed):

a. Purchase Orderb. Bidding Documents (If through bidding)c. Supplier’s Invoiced. Delivery Receipt or the “Receipt” portion of the supplier’s invoice duly signed e. Inspection and Acceptance Report

7. For infrastructures and reforestation projects

a. By contract (please refer to R.A. 9184 for the necessary procedures and documents needed)

1) Bidding documents2) Plan and specifications3) Notice of Bidding4) Contract5) Notice to proceed6) Billings of contractors7) Inspection and Acceptance Report 8) Duly verified Contractor’s Project

Accomplishment/Completion Report9) Program of Work

b. By administration

1) Supplies – PO, Suppliers Invoice, Bidding documents or equivalent (depending on the mode of procurement used), Delivery Receipts and IAR

2) Wages – Labor payroll, DTR and contract for labor3) Plans/Program of Work

29

8. For repair and maintenance of PPE

a. Pre-Repair Inspection Reportb. Job Order/Contractc. Supplier’s Invoiced. Inspection and Acceptance Reporte. Post-Repair Inspection Report

30

Table 8Certification and Approval of Payment

Narrative Procedures

Area of Responsibility/ Person Responsible Seq. Activity

Barangay Treasurer 1 Receives DV/payroll in three copies duly certified in Box A by the CCA as to availability of funds together with all supporting documents.

2 Checks the availability of fund (cash) to support the claim.

3 Signs Box B of the DV/payroll certifying in the availability of fund (cash).

4 Forwards the signed DV/payroll to the PB together with the supporting documents for certification and approval.

Punong Barangay 5 Certifies the DV/payroll as to validity, propriety and legality, and approves it by signing in Box C.

6 Forwards the approved DV/payroll to the BT for the preparation of the check.

Barangay Treasurer 7 Receives the approved DV/payroll for the preparation of the check/cash payments.

31

for the preparation of the check/payment

Legend: Symbols:

DV - Disbursement Voucher - Flow of DocumentsI - Invoices - Document

DTR - Daily Time RecordOSD - Other Supporting Documents - Process

P - Payroll

OPERATING PROCEDURES CERTIFICATION AND APPROVAL OF PAYMENT

Procedural Flow Chart (Table 8a)

Barangay Treasurer Punong Barangay

I

II

1

DTROSD

DV/P

1-3

2

3

4

5

7

DTR

OSD

DV

1-3

DTR

OSD

DV

1-3

receives

checks

signs

forwards

certifies

6

forwards

receives

Se procedural flowchart onPayment by check (Table 9a)

32

Table 9Payment by Check

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer 1 Verifies completeness of signatures on the DV/payroll.

2 Prepares the check in the name of the payee for the amount indicated in the DV/payroll

Note 1. The check shall be prepared with a carbon copy, to be distributed as follows:

Original – Payee Carbon copy – attach to the DV/Payroll

3 Signs the check.

4 Forwards the check together with the DV/payroll and supporting documents to the PB for countersignature on the check.

Punong Barangay 5 Countersigns the check and returns it to the BT together with the supporting documents for release.

Barangay Treasurer 6 Receives and releases the check and a copy of the DV to the payee. Temporarily files the carbon copy of the check to be attached to the DV/payroll paid.

Payee/Supplier 7 Acknowledges the receipt of payment by signing in Box D of the DV and retains third copy of the file.

8 Issues an OR to acknowledge the payment received.

Note 2. The OR (if applicable) shall be made as an additional supporting document for the disbursements

9 Returns back the signed DV together with the OR to the BT.

Barangay Treasurer 10 Attaches the OR issued by the payee/supplier to the DV together with the carbon copy of the check.

11 Records the paid DV/payroll in the SCkI to

33

Area of Responsibility/Person Responsible Seq. Activity

account for all checks issued.

Note 3. See Table 5, Volume II for the recording of the check issued in the SCkI.

12 Files the paid DV together with all supporting documents temporarily.

34

Notes:1. The check shall be prepared with a duplicate

copy, to be distributed as follows:Original – Payee2nd copy – attach to the DV/Payrol

2. The OR (if applicable) shall be made as an additional supporting document for the disbursements.

3. See Table 5, Volume II for the recording of the check issued in the SCkI.

Legends: Symbols: - Flow of documents - Flow of Documents

DV - Disbursement Voucher - Recorded prepare - Prepares/RecordsI - Invoices - file - File

DTR - Daily Time RecordOSD - Other Supporting Documents - Document - Documents

CC - Carbon Copy of the CheckOR - Official Receipt - Cash/Check - Check

SCkl - Summary of Checks Issued - connector - Process

OPERATING PROCEDURES Payment by Check

Procedural Flow Chart (Table 9a)

Barangay Treasurer Punong Barangay Payee/ Supplier

1

3

IDTR

OSD

DV/P

1-3

2

Check

4

5

IDTR

OSD

DV/P

1-3

Check

37

2

DV

1

OR

11

2 DV

1

6

8

CC

CC

1

OR

SCkI

12 10

verifies

prepares Note 1

signs

countersigns

DV/P

1-3

Check

cc

I

DTROSD

cc

receives/ releases

acknowledges

IssuesNote 2

9

returns back

CC

Check

attaches

records Note 3

files

forwards

35

Table 10Payment in Cash

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer 1 Receives the check for the cash advance.

2 Signs in Box D, under the “Received payment” caption of the DV to acknowledge the receipt of the check. Files his copy of the DV.

3 Encashes the check and prepares the distribution of payment based on the approved payroll.

4 Pays the officers/employees named in the payroll.

Note 1. The officers/employees shall be required to sign in the last column of the payroll to acknowledge the receipt of payment from the BT.

5 Refunds any unclaimed salaries/wages/ honoraria to fully liquidate the cash advance received for the pay period. Issues the OR for the refund.

6 Records payments in the SCP.

Note 2. See Table 6, Volume II for the preparation of the SCP.

7 Files the paid DV/payroll temporarily to support SCP.

36

Legend: Symbols: - Flow of Documents

DV - Disbursement Voucher - Records/Encashes/Refunds/PaysAP - Approved Payroll

SCP - Summary of Cash Payments - File OR - Official Receipt

Notes: - Document1. The officers/employees shall be required

to sign in the last column of the payroll to acknowledge the receipt of payment from - Cash/Check the BT.

2. See Table 6, Volume II for the preparation - Processof the SCP.

OPERATING PROCEDURES PAYMENT IN CASH

Procedural Flow Chart (Table 10a)

Barangay Treasurer

1

Check

Cash

DV 1

2

3

A P

DV

1

4

Cash SCP

56

OR

7

receives

signs

encashes

A P

Officer/employees

pays Note 1

refundsrecordsNote 2

files

37

Table 11Liquidation of Cash Advance

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer/ Accountable Officer

1 Prepares the LR based on cash payments made.

Note 1. The LR shall be prepared in three copies to be distributed as follows:

Original – to support the liquidation of the Cash Advance

2nd copy – BRK 3rd copy – BT/AO

2 Checks supporting documents against the SCP.

3 Signs Box A “Prepared by” portion of the LR.

4 Submits the duly accomplished LR to the BRK for signature in Box B under the “Certified Correct” caption of the LR, together with all paid DVs/payrolls and the certified SCP.

Barangay Record Keeper

5 Records the receipt of the LR in the log book.

6 Examines the LR as to correctness and completeness of supporting documents.

7 Signs in Box B of the LR.

8 Sends the LR together with the supporting documents to the PB for approval and signature in Box C.

38

Legend: Symbols:

DV - Disbursement Voucher - Flow of DocumentsAP - Approved Payroll - Records/ prepares

SCP - Summary of Cash Payments - FileLR - Liquidation ReportLB - Log Book - DocumentPB - Punong Barangay

Note 1: - Book The LR shall be prepared in three copies to be distributed as follows: - ProcessOriginal – to support the liquidation of the

Cash Advance2nd copy – BRK 3rd copy – AO

OPERATING PROCEDURES LIQUIDATION OF CASH ADVANCE

Procedural Flow Chart (Table 11a)

Barangay Record Keeper Barangay Treasurer

SCP 1 LR

1-3

1

AP 1

DV 1

LR

1-3DV

1AP 1SCP

1

4

56

7

LB

2

3

8

from file Note 1 prepares

checks

3

signs

forwards

recordsexamines

examines

sends

to PB

39

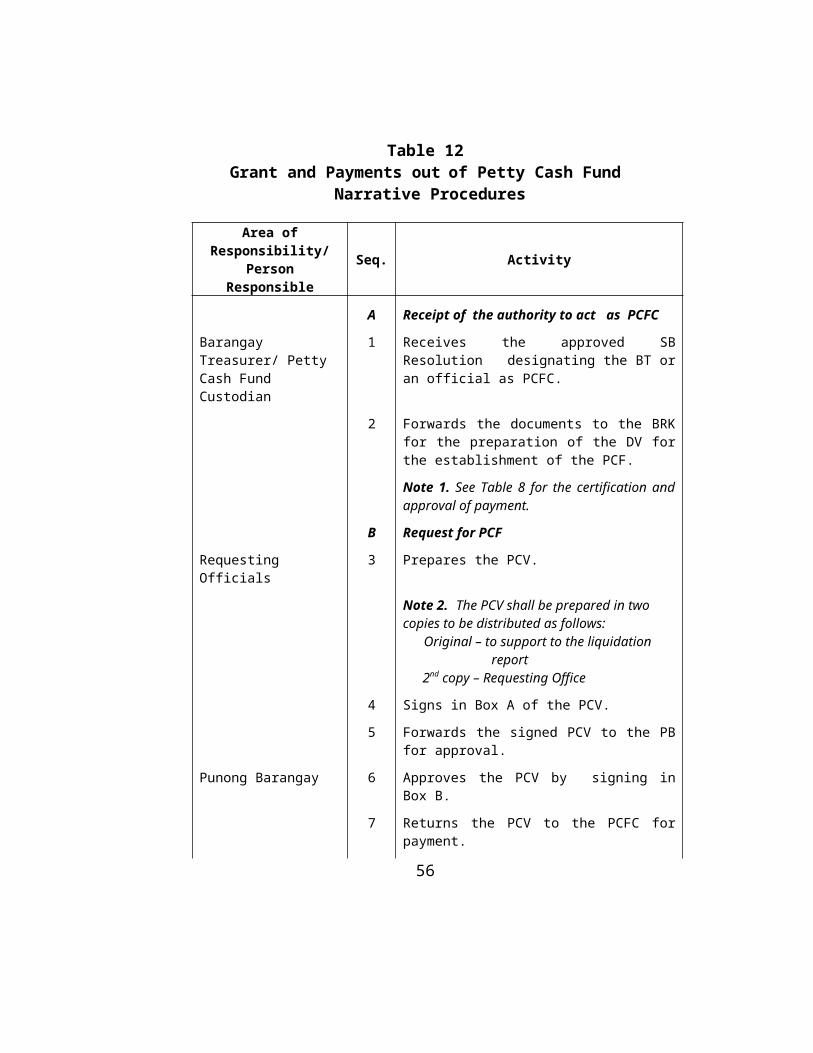

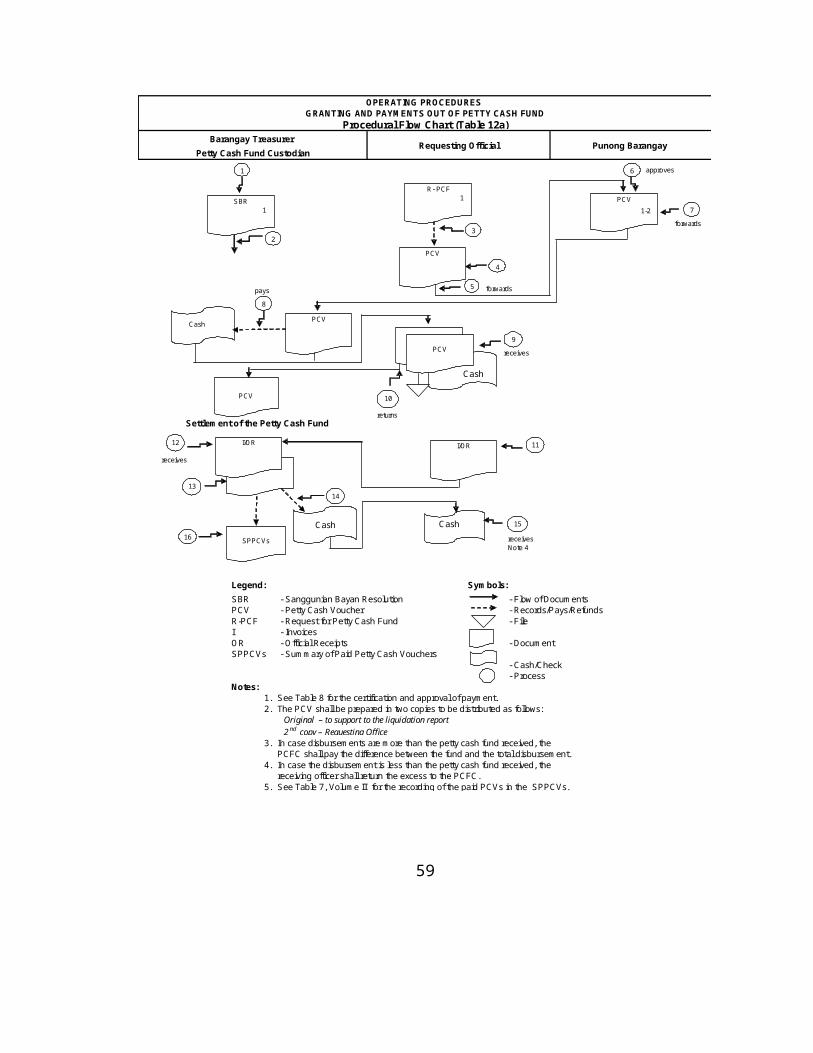

Table 12Grant and Payments out of Petty Cash Fund

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

A Receipt of the authority to act as PCFCBarangay Treasurer/ Petty Cash Fund Custodian

1 Receives the approved SB Resolution designating the BT or an official as PCFC.

2 Forwards the documents to the BRK for the preparation of the DV for the establishment of the PCF.

Note 1. See Table 8 for the certification and approval of payment.

B Request for PCFRequesting Officials 3 Prepares the PCV.

Note 2. The PCV shall be prepared in two copies to be distributed as follows:

Original – to support to the liquidation report

2nd copy – Requesting Office

4 Signs in Box A of the PCV.

5 Forwards the signed PCV to the PB for approval.

Punong Barangay 6 Approves the PCV by signing in Box B.

7 Returns the PCV to the PCFC for payment.

Barangay Treasurer/ Petty Cash Fund Custodian

8 Pays the amount requested and signs Box C of the PCV.

Requesting Official 9 Receives the amount requested and signs Box D of the PCV.

10 Returns the signed PCV to PCFC and retains file copy for file.

C Liquidation of the PCV11 Submits the documents supporting the

disbursement to liquidate the amount received, upon completion of the purpose for which the fund is requested.

40

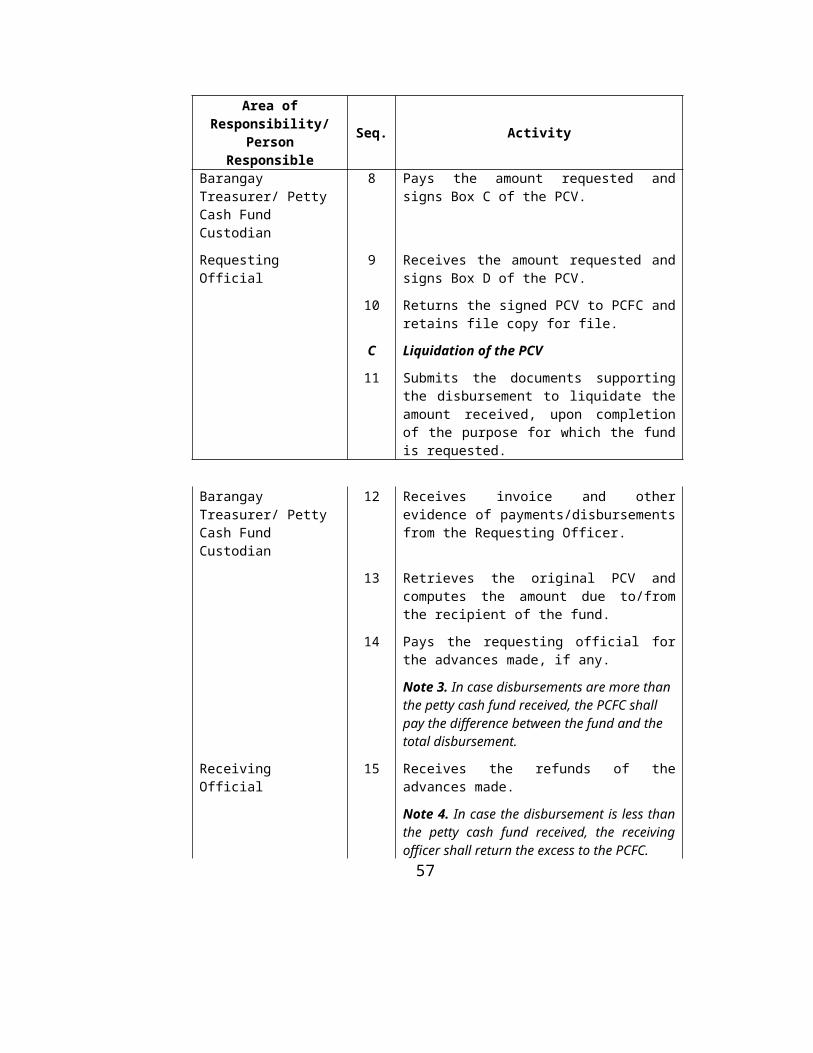

Area of Responsibility/Person Responsible Seq. Activity

Barangay Treasurer/ Petty Cash Fund Custodian

12 Receives invoice and other evidence of payments/disbursements from the Requesting Officer.

13 Retrieves the original PCV and computes the amount due to/from the recipient of the fund.

14 Pays the requesting official for the advances made, if any.

Note 3. In case disbursements are more than the petty cash fund received, the PCFC shall pay the difference between the fund and the total disbursement.

Receiving Official 15 Receives the refunds of the advances made.

Note 4. In case the disbursement is less than the petty cash fund received, the receiving officer shall return the excess to the PCFC.

16 Records the PCV in the Summary of Paid PCVs.

Note 5. See Table 7, Volume II for the recording of the paid PCVs in the SPPCVs.

41

Settlement of the Petty Cash Fund

Legend: Symbols:SBR - Sanggunian Bayan Resolution - Flow of DocumentsPCV - Petty Cash Voucher - Records/Pays/Refunds R-PCF - Request for Petty Cash Fund - FileI - InvoicesOR - Official Receipts - DocumentSPPCVs - Summary of Paid Petty Cash Vouchers

- Cash/Check - Process

Notes:1. See Table 8 for the certification and approval of payment. 2. The PCV shall be prepared in two copies to be distributed as follows:

Original – to support to the liquidation report 2 nd copy – Requesting Office

3. In case disbursements are more than the petty cash fund received, the PCFC shall pay the difference between the fund and the total disbursement.

4. In case the disbursement is less than the petty cash fund received, the receiving officer shall return the excess to the PCFC.

5. See Table 7, Volume II for the recording of the paid PCVs in the SPPCVs.

Petty Cash Fund CustodianRequesting Official Punong Barangay

OPERATING PROCEDURES GRANTING AND PAYMENTS OUT OF PETTY CASH FUND

Procedural Flow Chart (Table 12a)Barangay Treasurer

SBR 1

1

21

R- PCF 1

31

PCV

PCVCash

Cash

Cash 151

9

12

Cash

61

71

81

112=

13

SPPCVs161

4

51

1-2

1-2

1-2

1

PCV 10

141

receives

forwards Note 1

To BRKPCV

preparesNote 2

signs

approves

1-2

forwards

forwards

pays

receivesPCV 2

returns

1

I/OR

submits

I/OR

receives

PCV 1

retreives

Note 3pays

receivesNote 4records

Note 5

42

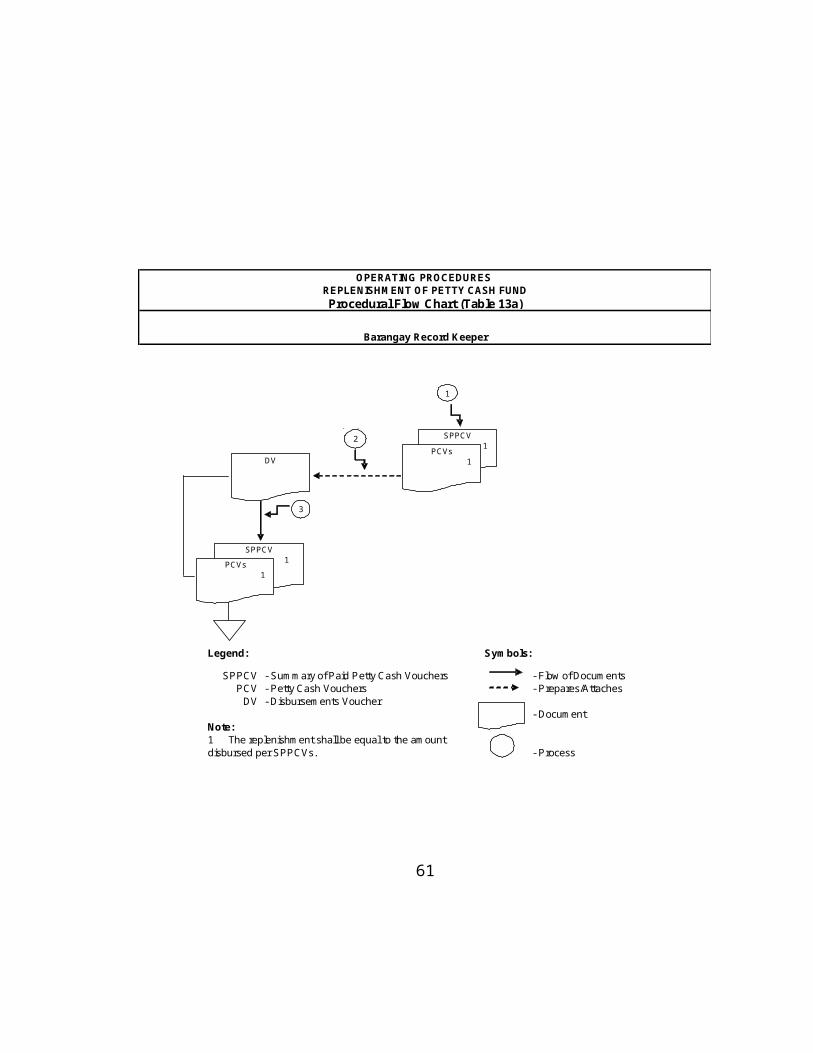

Table 13Replenishment of Petty Cash Fund

Narrative Procedures

Area of Responsibility/Person Responsible Seq. Activity

Barangay Record Keeper

1 Retrieves paid PCVs and SPPCVs on file.

2 Prepares the DV for the replenishment of the PCFC.

Note 1. The replenishment shall be equal to the amount disbursed per SPPCVs.

3 Attaches the original of the SPPCVs and the paid PCVs to the DV for the replenishment of the PCF.

43

Legend: Symbols:

SPPCV - Summary of Paid Petty Cash Vouchers - Flow of DocumentsPCV - Petty Cash Vouchers - Prepares/Attaches

DV - Disbursements Voucher - Document

Note:1 The replenishment shall be equal to the amount disbursed per SPPCVs. - Process

Barangay Record Keeper

OPERATING PROCEDURES REPLENISHMENT OF PETTY CASH FUNDProcedural Flow Chart (Table 13a)

DV

SPPCV 1PCVs

1

2

1

SPPCV 1PCVs

1

1-3

3

retrieves

Note 1prepares

attaches

44

Inventory, Property, Plant and Equipment, Public Infrastructures and Reforestation Projects

Polices and Procedures. Requisitions, procurement, issuance, physical inventory and loss of inventories and PPE are governed by existing government rules and regulations. The basic policies are:

1. Requisition and procurement

a. The BT shall act as the Property Officer of the Barangay and shall be responsible for the receipt, upkeep, issuance and physical inventory of Barangay properties;

b. All procurement shall be in accordance with the requirements of RA 9184 or the Procurement Law;

c. Purchases shall be covered by a PO;d. Receipts shall be covered by IAR;e. Receipts shall be recorded in a logbook (Appendix 8 )maintained for the purpose; f. Procurement of supplies shall be charged to appropriation for MOOE while

procurement of PPE and construction of public infrastructures and reforestation projects shall be charged against appropriation for CO;

g. Purchase of supplies shall be directly charged to expense while purchase of PPE shall be capitalized and recorded in the Property, Plant and Equipment Register (PPEReg) for control and monitoring purposes; and

h. All deliveries shall be inspected by the designated Kagawad and accepted by the BT.

2. Issuance of Inventory and PPE

a. Inventory

1) Issuances of inventories shall be recorded in the logbook;2) For accountability purposes, the end-user or the recipient of small tangible

items shall be issued an Inventory Custodian Slip (Appendix 9); 3) The recipient shall be responsible for the upkeep of the issued small tangible

items and shall be accountable thereto during the estimated useful life of the item as determined by COA; and

4) Unserviceable small tangible items shall be returned to the BT for cancellation of accountability and the ICS for replacement.

45

b. Property, Plant and Equipment

1) Issuance of property to end-user shall be covered by a Property Acknowledgement Receipt (PAR) (Appendix 10) which shall be renewed at least every three years or whenever there is a change in custodianship;

2) Any unserviceable PPE shall be returned to the BT for the cancellation of the PAR and its eventual disposal;

3) All unserviceable items for disposal shall be summarized in the Inventory and Inspection Report of Unserviceable Properties (IIRUP);

4) Properties which are no longer needed by the Barangay and reported in the IIRUP shall be disposed of in accordance with regulations set by COA; and

5) Elected Officials/Employees of the Barangay shall be cleared of property accountability by accomplishing the Transfer of Money and Property Accountability (Appendix 11).

3. Physical Count of PPE

a. A physical inventory of all Barangay property shall be conducted at least once a year;

b. A committee headed by the PB shall conduct the physical count of PPE owned by the Barangay;

c. The result on the physical inventory shall be reported in the Report on the Physical Count of PPE (RPCPPE);

d. The report, approved by the PB, shall be submitted to the BRK and the City/Municipal Accountant for reconciliation with the recorded PPE;

e. Any unrecorded inventory shall be booked up at appraised cost; and f. Any shortages shall be looked into and the AO shall be held accountable for the

loss.

4. Disposal of PPE and Inventory

a. All obsolete and unserviceable small items covered by ICS which could no longer be used, shall be turned over to the BT for disposal. For small items covered by ICS,the corresponding ICS shall be cancelled to erase the accountability of the user.

b. All unserviceable PPE shall also be turned over to the BT for disposal. The corresponding PAR previously issued shall be cancelled

c. Items for disposal shall be summarized in the Inventory and Inspection Report of Properties ( IIRUP)

d. The PPE disposed of, shall be dropped from the books m, only upon receipt of the report on its disposal.

46

5. Loss of PPE

a. For property lost through force majeure, theft, robbery or negligence, a “Notice of Loss” shall immediately be rendered by the AO to the PB;

b. Immediately upon receipt of the report of loss, the PB shall notify the Property Insurance Fund of the GSIS for the recovery of the insurable value of the lost asset.

c. Simultaneously, a request for “Relief from Property Accountability” shall be submitted through the PB to the COA for decision;

d. The property lost shall be dropped from the books and the AO shall be held accountable for the lost property pending the receipt of the COA decision on the request for Relief from Property Accountability;

e. Accountability over lost property shall be computed at “sound value” of the property lost;

f. Sound value is computed at replacement cost less accumulated depreciation based on replacement cost; and

g. In case the request for relief is denied, the AO shall pay for the item lost.

6. Public Infrastructure/Reforestation Project

a. Infrastructure project, such as roads, parks, etc, which are constructed for public use, shall be classified as Public Infrastructures. Project such as marshland or swampland, shall be classified as Reforestation Projects;

b. The cost incurred for the projects shall be monitored, with the use of the appropriate Registries, ie,

1) Registry of Public Infrastructure- Road2) Registry of Public Infrastructure – Parks3) Registry of Reforestation Projects – Marshland

c. The registry shall include information such as the cost and the cumulative repair and maintenance cost of the project;

d. The projects are not subject to depreciation; ande. Total project cost shall be included in the Notes to Financial Statements, when the

FS are submitted to COA.

Costing of Inventory. The cost of inventory acquired through purchase shall cover only the invoice cost. Due to difficulty in apportioning incidental expenses incurred in bringing the supplies to the Barangay shall be charged to account “Delivery Expenses”.

47

Property, Plant and Equipment. The PPE of the Barangay include but not limited to the following:

1. Land and Land Improvements2. Building purchased/constructed3. Leasehold Improvements4. Equipment5. Furniture and Fixtures6. Books 7. Motor Vehicles

Costing of Property. The cost of property acquired through purchase shall include the purchase cost and all expenses incurred in bringing the asset to its intended location and make it operational. Such expenses include transportation cost, insurance, arrastre, freight charges, installation cost, etc. These shall be recorded as part of the total cost of the purchased asset.

Normally, the costs chargeable against the PPE include but are not limited to the following:

1. Land

a. Purchase priceb. Cost of clearing and demolishing unnecessary structuresc. Payment to squatters/illegal tenants for vacating the place (if any) d. Cost of surveye. Fees for registration and transfer of titlef. Taxes paid (transfer and capital gain tax depending on the agreement)

2. Building - through purchase

a. Purchase priceb. Payment to tenants for vacating the place (if part of the agreement) c. Payment of any liability or encumbrance on the property (if assumed

by the buyer per agreement) d. Cost incurred in renovating the building to put it to suitable condition

such as lighting installation, partitions and repairs made prior to occupancy

3. Building – by contract

a. Contract cost

48

b. Cost of advertising the bidding c. Consultancy fee as supervision costd. Any expenses related to the construction

4. Building – by administration

b. Materials used, labor and overhead expenses incurred during construction c. Supervision fee (consultant) d. Excavation coste. Cost of bunk house (used as temporary construction office, materials and tools

storeroom)f. Rental of service equipmentg. Cost of building permits and other permitse. Architectural fees

5. Machinery, equipment, furniture and fixtures

a. Purchase priceb. Insurance while in transitc. Freight in d. Storage, handling and any cost related to the purchasee. Installation cost, including site preparation and assemblyf. Testing, trial run and other expenses necessary for the machinery and other

equipment to functiong. Taxes and customs duties

49

Table 14Requisition of Inventory and PPE

Narrative Procedures

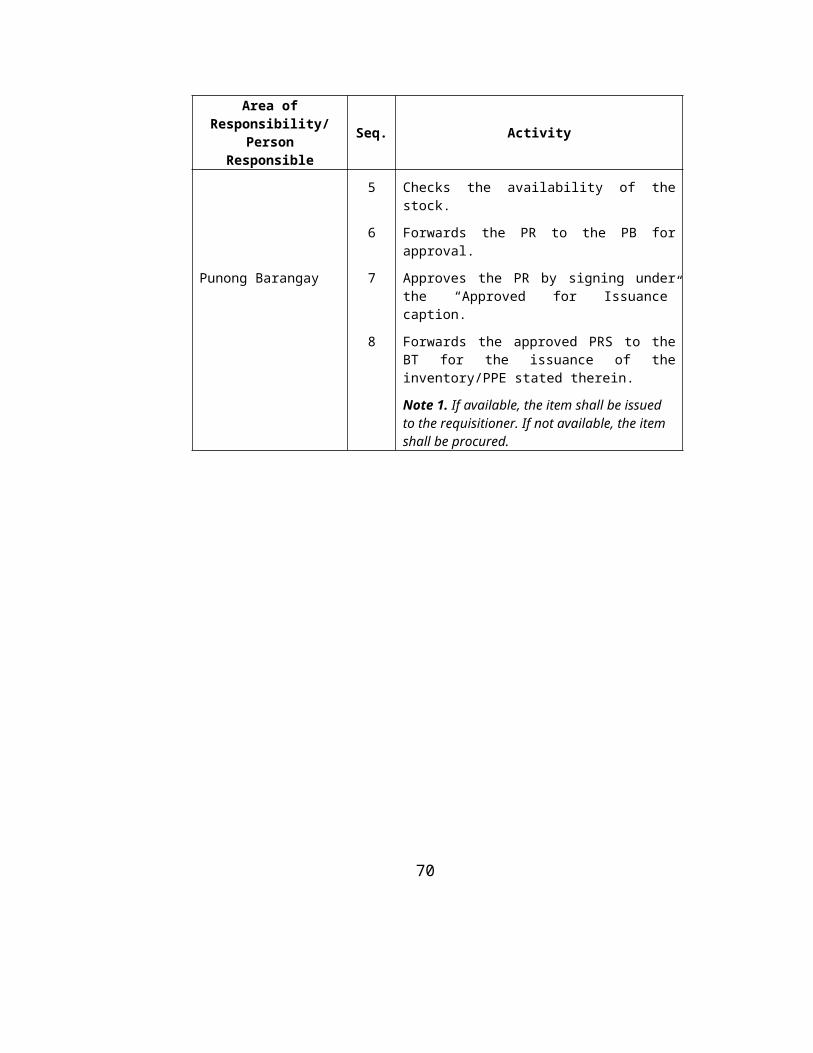

Area of Responsibility/ Person Responsible Seq. Activity

Requisitioner 1 Prepares the PR, by filling out information in the “Requisition” portion.

2 Signs under the “Requested by” caption.

3 Forwards the signed PR to the BT.

Barangay Treasurer 4 Receives the PR.

5 Checks the availability of the stock.

6 Forwards the PR to the PB for approval.

Punong Barangay 7 Approves the PR by signing under the “Approved for Issuance” caption.

8 Forwards the approved PRS to the BT for the issuance of the inventory/PPE stated therein.

Note 1. If available, the item shall be issued to the requisitioner. If not available, the item shall be procured.

50

Legend: Symbols: - Flow of Documents

PR - Purchase Request - Document

Note:1 If available, the item shall be issued to the - Decisionrequisitioner. If not available, the item shall be procured. - Process

Punong Barangay Requisitioner Barangay Treasurer

OPERATING PROCEDURES REQUISITION OF INVENTORY AND PPEProcedural Flow Chart (Table 14a)

PR

PR

2

1

PR

Stocks Available?

3

4

5

6

7

81-3

1-31-3

PR

1-3

prepares

signs

forwards

receives

checks

YESNO

Note 1 forwards

approves

forwards

PR

1-3for issuance of inventory

51

Table 15Procurement of Inventory and PPE

Narrative Procedures

Area of Responsibility/ Person Responsible Seq. Activity

Bids and Awards Committee

1 Based on the PR, makes an estimate of the cost of the items to come up with the Approved Budget for the Contract (ABC).

2 Forwards, the PR and the estimate or ABC to the CCA for earmarking of appropriation.

Chairman, Committee on Appropriation

3 Receives the request for earmarking.

4 Forwards the PR to the BRK for earmarking of the funds needed.

Barangay Record Keeper

5 Checks the RAC and verify the availability of the fund.

6 Earmarks the needed account.

7 Sends back the PR to the CCA for certification in the availability of appropriation.

Chairman, Committee on Appropriation

8 Receives and returns the PR to the BAC with the amount needed duly earmarked.

Bids and Awards Committee

9 Conducts biding or adopts alternative mode of procurement under RA 9184.

10. Forward the result recommendation for award of contract/PO to the PB for approval

Punong Barangay 11 Approves the result of the bidding

12 Sends the approved result of the BAC to BRK for the preparation of PO

Barangay Record Keeper

13 Receives and prepares the contract/PO

14 Initials below the name of the CCA under the “Fund available” caption of the contract/PO.

15 Forwards the contract/PO to the CCA for release to the supplier/Contractor

Chairman, Committee on Appropriation

16 Signs the certification of “funds available”

17 Forward the contract/PO to the PB for Approval

52

Area of Responsibility/ Person Responsible Seq. Activity

Punong Barangay 18 Approves or signs the contract/PO

19 Forward the contract/PO to the BT for release

Barangay Treasurer 20 Receives the signed contract/[PO and release it to contractor/Supplier

53

BAC Bnarangay Book Keeper Punong Bayan

Legend: Symbols: - Flow of Documents

PR - Purchase Requesr - Pays/Issues ABC - Approved Budget Contract - FileR - Result of the BiddingRAC - Registry of Appropriation - Document and CommitmentPO - Purchase Order - Cash/CheckC - Contract

- Process

Committee on Appropriation

OPERATING PROCEDURES Procurement of Inventory and PPE

Procedural Flow Chart (Table 15a)Chairman

1

84

PR

2

5

makes forwards

returns

checks receives

9

ABC

PR

ABC

forwards

3

4

PR ABC

RAC

6 earmarks

PR ABC

7

PR ABC

sends & certifies

conducts

R

104

forwards

PR ABC

R

11 approves

PR ABC

R

12 sends

PO/C

13 prepares14

initials

PR ABC R

15

signsPO/C

forwards

16

PR ABC

R PO/C

17forwards

18 approves

to BT

19forwards

20receives & releases

54

Table 16Delivery of Inventory and PPE

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

Barangay Treasurer 1 Receives deliveries.

Requisitioner/BT 2 Inspects deliveries and checks in conformity with the specifications stated in the PO.

3 Signs the “Received by” portion of the suppliers invoice/delivery receipt.

Barangay Treasurer 4 Prepares the IAR.

Note 1. The IAR shall be prepared in three copies to be distributed as follows:

Original – to support the DV for the payment

2nd copy – BT 3rd copy – BRK

Note 2. In case of partial delivery, only the quantity actually delivered and accepted shall be indicated in the IAR

5 Forwards two copies of the duly accomplished IAR to the BRK for recording of deliveries and of the amount due the supplier. Retains the 2nd copy for file.

Barangay Record Keeper

6 Acknowledges the receipt of the IAR. Retains the 3rd copy for file (the original shall be attached to the DV for payment).

Note 3. See Table 8, Volume II for the recording of the delivered items in the PPEReg and amount due the supplier in the Creditor’s Card (CC)

55

Legend: Symbols:

IAR - Inspection and Acceptance Report - Flow of DocumentsPO - Purchase Order - Prepares

I - Invoice - FileDR - Delivery Receipt

- DocumentNotes:

1. The IAR shall be prepared in three copies to be distributed as follows: - StocksOriginal – to support the DV for the payment2nd copy – BT - Process3rd copy – BRK

2. In case of partial delivery, only the quantity actually delivered and accepted shall be indicated in the IAR.

3. See Table 8 , Volume II for the recording of the delivered items in the PPEReg and amount due the supplier in the Creditor’s Card.

OPERATING PROCEDURES DELIVERY OF INVENTORY AND PPE

Procedural Flow Chart (Table 16a)

Barangay Treasurer Requisitioner/BT Barangay Record Keeper

1

3

3

IAR 1

Items Items

4

6

2

3

PO 1

I/DR 1

from supplier

receives

inspects

signs

preparesNote 1

1

IAR

25

forwards

acknowledges

to support the DV

56

Table 17Issuance of Supplies and Small Items Inventory

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

A Issuance of Supplies Barangay Treasurer 1 Receives the request from the requisitioner.

2 Fills out the “Issuance” section of the logbook, noting the quantity issued and giving “Remarks”, if needed.

3 Issues the items requested.

Requisitioner 4 Acknowledges the receipt by signing under the “Received by” caption of the logbook.

B Issuance of Small Tangible Items Barangay Treasurer 5 Prepares the ICS for the issuance of small

tangible items.

Note 1. The ICS shall be prepared in three (3) copies to be distributed as follows:

Original – BT2nd copy – BRK

3rd copy –Requisitioner

6 Forwards the ICS to the requisitioner for signature and issue the items requisitioned.

Requisitioner 7 Signs under the “Received by” caption of the ICS.

8 Returns the signed ICS to the BT.

Barangay Treasurer 9 Signs under the “Received from” caption of the ICS and files the original. Forwards the 2nd

and 3rd copies to the BRK and the requisitioner, respectively for their file.

57

58

Table 18Issuance of Property, Plant and Equipment

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

Barangay Treasurer 1 Prepares the PAR.

Note 1: The PAR shall be prepared in three copies distributed as follows: Original – BT 2nd Copy – BRK 3rd Copy – Requisitioner

2 Issues the item to the requisitioner together with the PAR for signature.

Requisitioner 3 Signs under the “Received by” caption of the PAR and receives the items requisitioned. Returns the PAR to the BT.

Barangay Treasurer 4 Receives the PAR and signs under the “Issued by” caption of the PAR and retains a copy for file.

5 Furnishes the requisitioner a copy of duly signed PAR for his file.

6 Forwards the duly accomplished PAR to the BRK for recording in the Register and for file.

Barangay Record Keeper

7 Acknowledges receipt of the duly accomplished PAR and files the PAR.

Note 1. See Table 8, Volume II for the recording of the PAR in the PPEReg.

59

signs

Legend: Symbols:

PAR - Property Acknowledgement Receipt - Flow of DocumentsRIS - Requisition Issues Slip - Prepares/Issues

- FileNote:

See Table 8, Volume II for the recording - Documentof the PAR in the PPE Register.

- Stocks

- Process

OPERATING PROCEDURES ISSUANCE OF PROPERTY, PLANT AND EQUIPMENT

Procedural Flow Chart (Table 18a)

Barangay Treasurer Requisitioner Barangay Record Keeper

PAR

Items

PAR

2-3

4

PAR 2

PAR 3

Items

2

5

6

3

1

1-3

PAR

1-3

7

1

prepares

issues

signs

receives & signs

furnishes

forwards

acknowledges

60

Table 19Loss of PPE

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

Accountable Officer 1 Notifies the PB through the BT on the loss of the property immediately upon discovery of the loss.

Punong Barangay 2 Receives the notification and conducts immediate investigation on the cause of the loss.

3 Prepares transmittal letter and submits the notification of the accountable officer, the investigation report and all the required documents to GSIS for indemnification of the lost property.

4 Forwards copies of all the documents on the loss of the PPE to the City/Municipal Accountant and to the BRK.

61

to GSIS to the City/Municipal

to BRK

Legend: Symbols:

PR - Police Report - Flow of DocumentsN - Notification of Loss - PreparesA - Affidavit - File

IR - Investigation ReportGSIS - Government Service Insurance System - DocumentBRK - Barangay Record Keeper

TL - Transmittal Letter - Process

OPERATING PROCEDURES LOSS OF PPE

Procedural Flow Chart (Table 19a)

Accountable Officer Punong Barangay

N

1-3PR

1-3

A

1-3

1

N 1-3

2

PR 1-3

A 1-3

PR 1

A 1

N 1

PR 2

A 2

N 2

3

4

IR 1

IR 2

TL 1-3

TL 1

TL

2

notifies

receives

prepares

forwards

PR 3

A 3

N 3

IR 3

TL

3

62

Table 20Request for Relief from Property Accountability

Narrative Procedures

Area of Responsibility/ Person Responsible

Seq. Activity

A Request for Relief from Property Accountability

Accountable Officer 1 Submits “Request for Relief from Property Accountability” to the PB thru the BT for his favorable endorsement to COA.

Barangay Treasurer 2 Endorses the request of the AO to the PB for approval.

Punong Barangay 3 Signs the endorsement and forwards to COA, through the field auditor, the “Request for Relief from Property Accountability” with all the necessary documents.

B Request for Relief from Property Accountability granted by COA

4 Receives COA resolution granting relief to the AO on the loss of the property.

5 Forwards the COA decision to the BT.

Barangay Treasurer 6 Receives the COA decision granting relief from accountability on the loss of the property.

7 Provides the AO, BRK and the City/Municipal Accountant with the copies of COA decision.

C Request for Relief Denied by COA Accountable Officer 8 Pays for the “sound value” of the lost item.

Barangay Treasurer 9 Issues OR to acknowledge receipt of payment.

63

to GSIS to the City/Municipal

to BRK

Legend: Symbols:

PR - Police Report - Flow of DocumentsN - Notification of Loss - PreparesA - Affidavit - File

IR - Investigation ReportGSIS - Government Service Insurance System - DocumentBRK - Barangay Record Keeper

TL - Transmittal Letter - Process

OPERATING PROCEDURES LOSS OF PPE

Procedural Flow Chart (Table 20a)

Accountable Officer Punong Barangay

N

1-3PR

1-3

A

1-3

1

N 1-3

2

PR 1-3 1-3

A 1-3

PR 1

A 1

N 1

PR 2

A 2

N 2

3

4

IR 1

IR 2

TL 1-3

TL 1

TL

2

notifies

receives

prepares

forwards

PR 3

A 3

N 3

IR 3

TL

3

IR 1-3

64

Fiscal Responsibilities of Barangay Officials

Fiscal Responsibilities of Barangay Officials. The responsibilities of barangay officials in the management of the funds and properties of the barangay are as follows:

1. Punong Barangay

a. General Administration

1) Implements functions, projects, activities to provide basic services and facilities as appropriated;

2) Negotiate, enter into, and sign contracts for and in behalf of the barangay, upon authorization of the Sanggunian Barangay.

3) Certifies vouchers and payrolls as to validity, propriety and legality of the claim involved ( Sec. 344 of 7160 )

4) Approves the claims (Sec. 344 of RA 7150) relating to the disbursement of barangay funds

5) Countersigns the checks in payment of the claims6) Transmit the registers and other documents to the city/municipal accountant

which will serve as basis in recording the barangay transactions in the book, preparation of the bank reconciliation statement and the checking the Report on Accountability for Accountable Forms ( RAAF) submitted by the BRK.

7) Signs the Management Responsibility over the Financial Statement (MRFS), on or before February 14 of the ensuing year, when the city/municipal accountant transmits the FS to COA.

2. Chairman, Committee on Appropriations

a. Use of appropriated Funds

1) Certifies the DV/payroll/contract/PO on the existence of available appropriation to cover the claims/commitments;

2) Monitors the use of appropriated fund with the use of the appropriate RAC;

3) Maintains the RACs, with the assistance of the BRK, for the following five funds:

a) General Fundb) 20 % Development Fundc) Calamity Fundd) Sanggunian Kabataan Fund

65

e) Gender and Development Fund

4) Ensures that commitments do not exceed the available appropriations.

b. Reporting

1) Certifies and submits the Status of Appropriation, Commitment and Balances (SACB) to the city/municipal budget officer one month after the close of the calendar year; and

2) Certifies the RAC.

3. Barangay Treasurer

a. Collection

1) Keep custody of barangay funds and properties;2) Collects all taxes, fees and other charges due and contributions

accruing to the barangay;3) Deposits collections with the AGDB;4) Collects for the city/municipal treasurer, when deputized and

remits all collection intact; and5) Renders report on collections and deposits made.

b. Disbursements

1) Certifies to the availability of cash for the claim presented;2) Issues and signs the check in payment of obligations;3) Maintains the CHBReg and the PCFReg, if designated as the PCC; and4) Renders the report on checks, cash and PCF disbursement.

c. Properties

1) Keeps the logbook for the receipt and issuance of supplies and materials;2) Issues ICS to end-user of the issuance of materials with serviceable life of more

than one year.3) Prepares the PAR for the issuance of property; and4) Assist the PB in the conduct of physical count of properties.

d. Reporting

66

1) Renders a written accounting reports of all barangay funds and properties under his custody; and

2) Certifies the CHBReg and the PCFReg and submits a copy to the BRK at month end.

4. Barangay Record Keeper

a. Prepares the DV/payroll, contract, Purchase order or RIS; b. Maintains all the registers, except the CHBReg and the PCFReg which are

maintained by the BT; c. Checks correctness of entries in the CHBReg and the PCFReg;d. Keeps and files all documents submitted by the accountable officers supporting the

Summaries intact and free from loss;e. Make all financial documents available to COA representative anytime for

audit/examination;f. Prepares the Transmittal Letter (Appendix 12), forwarding the certified registries and

documents to the City/Municipal Accountant/Treasurer/Budget Officer, as the case maybe; and

g. Assist the CCA in the maintenance of the different RAC.

5. Sanggunian Kabataan Chairman

a. Implements the SK project in accordance with the approved appropriation; and

b. Initials below the name of the PB on claims against the SK Fund.

6. Accountable Officers a. All AOs shall be bonded in accordance with the Department of the Interior and

Local Government (DILG) Memo Circular No. 99-186 dated October 11, 1999; andb. Upon resignation or completion of terms/suspension/retirement, all AOs shall seek

Clearance from Money and Property Accountability (Appendix 13).

67

MATRIX OF FORMS

Appen-dix No.

Title Frequency of

PreparationPrepared by

Number of

copies

BarangayTreasurer

BarangayRecord Keeper

Others

1 Disbursement Voucher

As needed BT/BRK 3 1 1 SCkI/SCP/Payee

2 Payroll As needed BT/BRK 2 1 1 SCP

3 Purchase Order As needed BT/BRK

3 1 1 Supplier

4 Requisition and Issue Slip

As needed Requestor 3 1 1 PO

5 Purchase Request As needed Requestor 3 1 PORequestor

6 Petty Cash Voucher

As needed PCFC 2 1 SPPCV

7 Liquidation Report As needed BT/BRK

3 1 AO DV

8 Logbook As needed BT/PC 1 Property Custodian

9 Inventory Custodian Slip

As needed BT 3 1 1 User

10 Property Acknowledgement Receipt

As needed BT 3 1 1 User

11 Transfer from Money and Property Accountability

As needed Elected Officials/BT/Employee

4 1 1 AO/User/COA