bannister - stifel nicolaus mid-2011 macro outlook

TRANSCRIPT

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 1/59

All relevant disclosures and certifications appear on pages 58 - 59 of this report.

July 11, 2011

Stifel Nicolaus Mid-2011 Macro Outlook Slide

DeckBarry B. Bannister, CFA (443) 224-1317 [email protected]

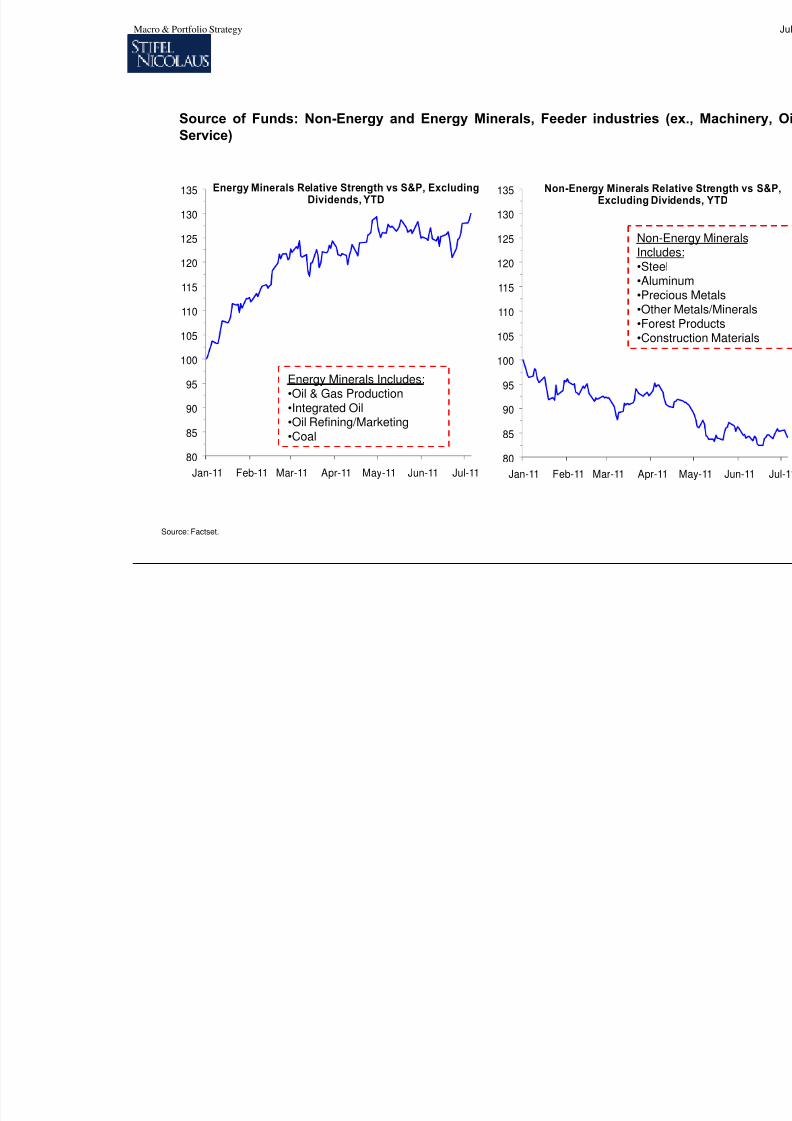

Context - Interlocking structural challenges: U.S. needs traction, the EU a unified bond market, and Chinarebalancing. Favored Sectors: Technology, Communications, Health Tech., Finance (i.e., growth stocks and depressed rate sensitive) and Source of Funds: Non-Energy Minerals, Energy Minerals, and Mineral feeder industries(ex., Machinery, Oil Service).

In our view:

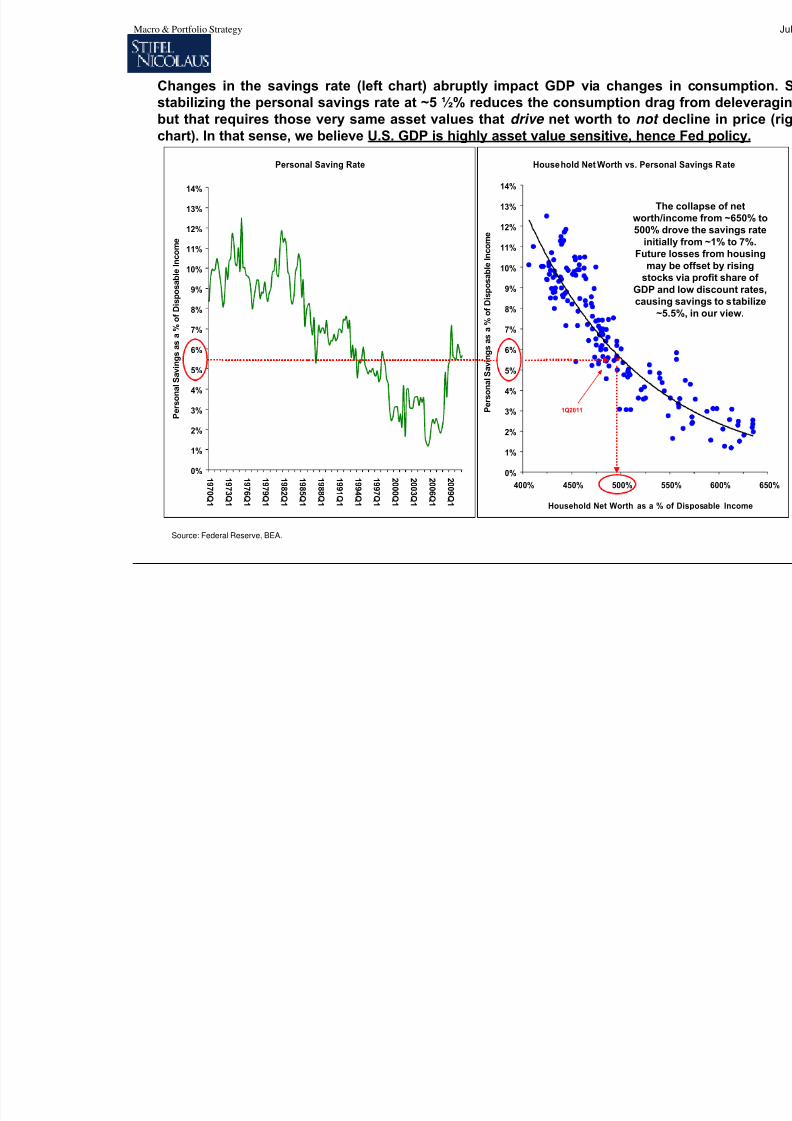

TRACTION: The U.S. structural challenge is to transfer private housing liabilities to the public sector while levitatingasset values until nominal GDP growth offsets “missing” housing investment.

Outlook: U.S. succeeds in 2H11 GDP traction, U.S. dollar stabilizes, commodities roll over April-December 2011,2H11 corporate investment improves, and the S&P 500 rises, bounded at the low end by 1,200 and high end at 1,400fair value (~5% over-shoot either side of 200dma).

UNITY: The EU structural challenge is a transfer of fiscal sovereignty to a single bond market while preservingsolvency, despite a stubbornly hawkish and increasingly vulnerable ECB.

Outlook: EUR/USD down to ~1.35 as peripheral debt situation is far from over. European central bank balance sheetsmay be the next in focus. Portuguese public and Spanish private debt require restructuring, possibly along the lines of the Greek debt swaps and maturity extensions.

REBALANCE: The Chinese structural challenge is to achieve the first “soft landing” in Emerging Market historyfollowing years of rapid credit growth, while rebalancing growth to bottom-up consumption despite such a directivecoming from top-down authority.

Outlook: Despite Chinese inflation peaking we see Chinese GDP weakening sharply in 2H11 with a traditional lag tomonetary tightness, thereby significantly weakening construction-dependent commodities. Top-down authority canorder fixed investment, but not consumption.

Sections

• Since 4/4/11 we have said the Hard Asset vs. Paper Asset trade, a defining trade for leadership since 2002,is over (page 5-13)

• Favored Sectors: Technology, Communications, Health Tech., Finance (i.e., growth stocks and depressedrate sensitive) (page 14)

• Source of Funds: Non-Energy Minerals, Energy Minerals, Mineral feeder industries (ex., Machinery, Oil

Service) (page 15-16)

• We see S&P 500 bouncing off the 200 day average in 2011, especially weak in summer, then 1,400 by theend of year (page 17-26)

• We see WTI Oil ~$75/bbl.in a year (more supply, less demand), but not without Asia slowing and Libyareturning (page 27-34)

Macro & Portfolio Strategy

Stifel Nicolaus does and seeks to do business with companies covered in its research reports. As a result,investors should be aware that the firm may have a conflict of interest that could affect the objectivity of thisreport. Investors should consider this report as only a single factor in making their investment decision.

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 2/59

• Since commodities have become a financial asset, they should be subject to/pressured by a monetaryrelationship (page 35-38)

• The frightening scenario – is the commodity market signaling a 20% S&P 500 bear market betweenApril-August 2011? (page 39-45)

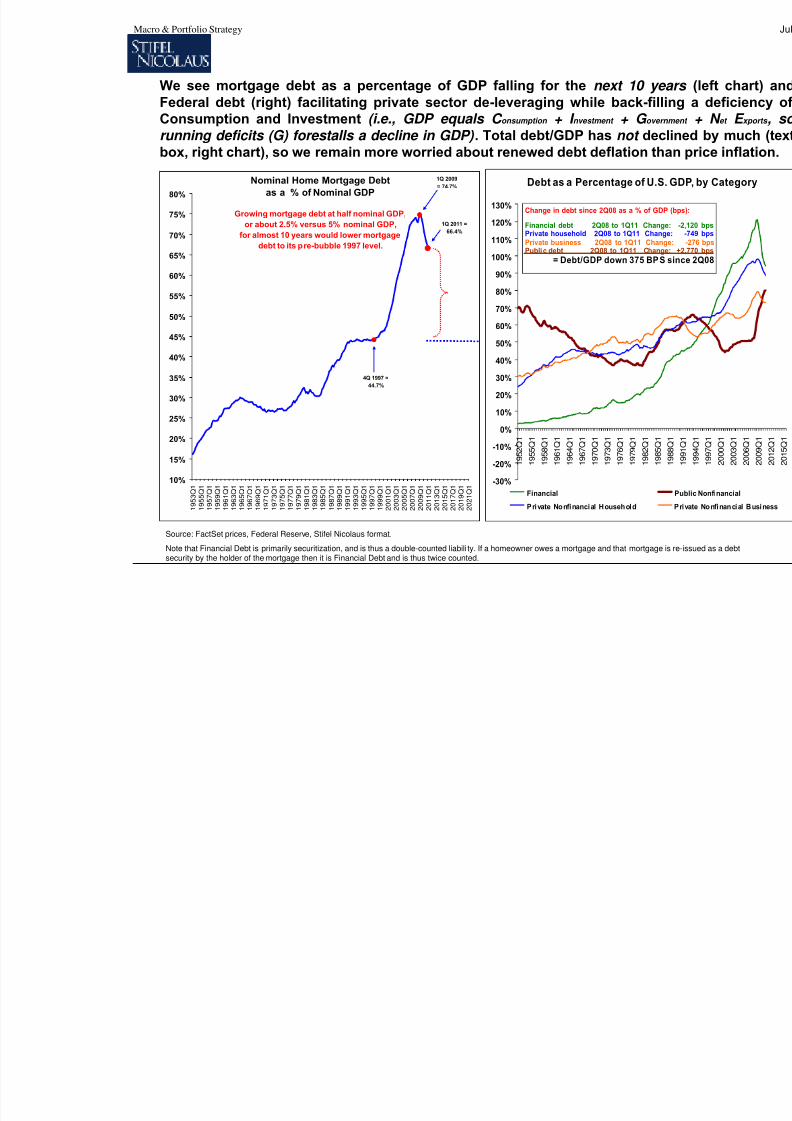

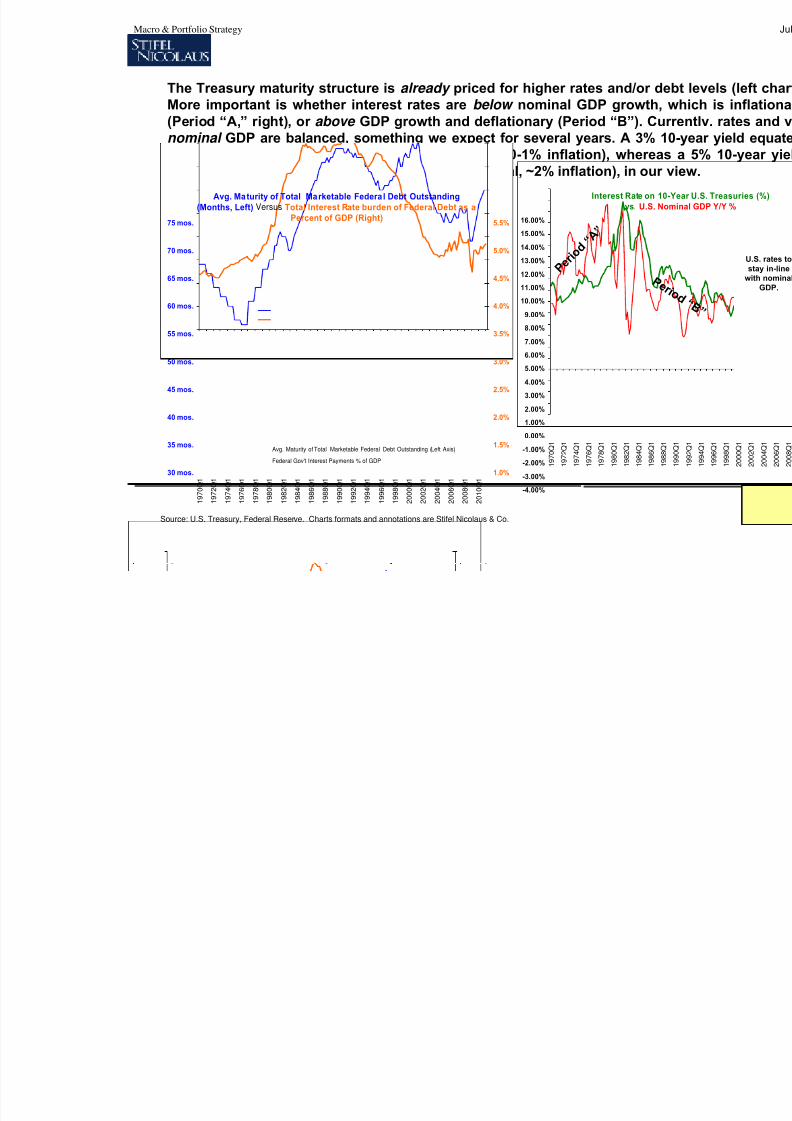

• Fed & Treasury are brilliantly converting a “Depression” into debt a work-out; we see the 10-year near 4%within a year (page 46-53)

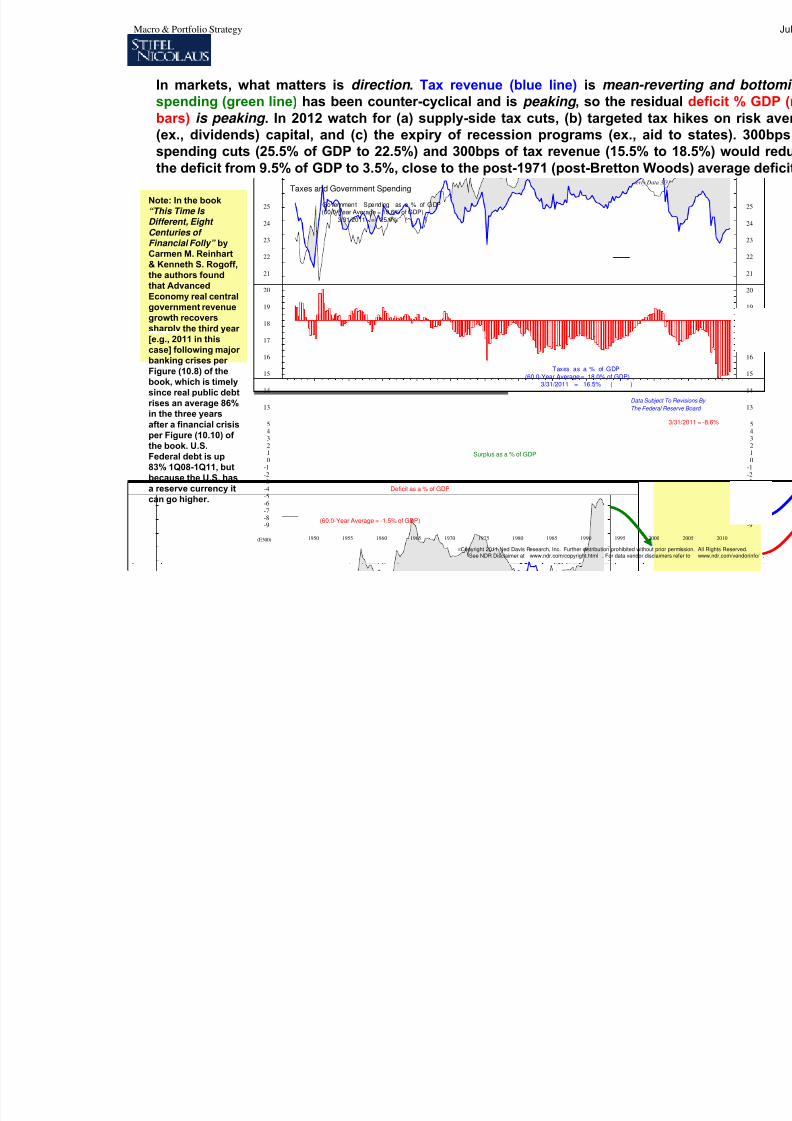

• U.S. fiscal deficits are desirable, inflation should average about 3% to 2015, and debt deflation is a far greater risk (page 54-57)

Page 2

Macro & Portfolio Strategy July 11, 2011

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 3/59

Stifel Nicolaus Mid-2011 Macro Outlook Slide

Interlocking Structural Challenges: Traction, Unity anAs of July 2011 S&P 500 1,353 (7/7/11) 10-Yr. 3.14% / 10/2yr. 267bps WTI Oil $99/bbl. / CRB-CCI 642

In our view:

(1) Context - Interlocking structural challenges: U.S. needs traction, the EU a single bond market, a

(2) Since 4/4/11 we have said the Hard Asset vs. Paper Asset trade, a defining trade for leadership s

(3) Favored Sectors: Technology, Communications, Health Tech., Finance (i.e., growth stocks, depr

(4) Source of Funds: Non-Energy Minerals, Energy Minerals, Mineral feeder industries (ex., Machine

(5) We see S&P 500 bouncing off the 200 day average in 2011, especially weak in summer, then 1,40(6) We see WTI Oil ~$75/bbl. in a year (more supply, less demand), but not without Asia slowing and

(7) Since commodities have become a financial asset, they should be subject to/pressured by a mo

(8) The frightening scenario – is the commodity market signaling a 20% S&P 500 bear market betwe

(9) Fed & Treasury are brilliantly converting a “Depression” into debt a work-out; we see the 10-yea

(10) U.S. fiscal deficits are desirable, inflation should average about 3% to 2015, and debt deflation i

Barry B. Bannister, CFAManaging Director, Equity Research - Macro & Sector Strategy

Stifel Nicolaus & Co. [email protected] 443-224-1317

Stifel Nicolaus does and seeks to do business with companies covered in its research reports. As a result, the firm may have a conflict of interest that could affect the objectivity of this report. Investors should cons

factor in making their investment decision.

All relevant disclosures and certifications can be found on page 58-59 of this report and on the rese

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 4/59

Structural Challenges: Traction (U.S.), Unity (EU), Re

In Our View:

TRACTION: The U.S. structural challenge is to transfer private housing liabsector while levitating asset values until nominal GDP growth offsets “missinvestment.

Outlook: U.S. succeeds in 2H11 traction, U.S. $ stabilizes, commodities rolDecember 2011, 2H11 corporate investment improves, and S&P 500 rises, bend by 1,200 and high end at 1,400 fair value (~5% over-shoot either side o

-----------------------------------------------------------------------------------------------------------

UNITY: The EU structural challenge is a transfer of fiscal sovereignty to a s

while preserving solvency, despite a stubbornly hawkish and increasingly

Outlook: EUR/USD down to ~1.35 as peripheral debt situation is far from ocentral bank balance sheets next in focus. Portuguese public and Spanish restructuring, possibly along the lines of the Greek debt swaps and maturi

-----------------------------------------------------------------------------------------------------------

REBALANCE: The Chinese structural challenge is to achieve the first “softEmerging Market history following years of rapid credit growth, while rebal

bottom-up consumption despite such a directive coming from top-down au

Outlook: Despite Chinese inflation peaking we see Chinese GDP weakeningwith a traditional lag to monetary tightness, thereby significantly weakenindependent commodities. Top-down authority can order fixed investment, b

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 5/59

Since 4/4/11 we have said the Hard Asset vs. trade, a defining trade for leadership since 20

• Successful U.S. economic traction removes U.S. $ deba

• Deep EU debt woes reduce the downward pressure on t

• Chinese efforts to restrain lending remove commodity d

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 6/59

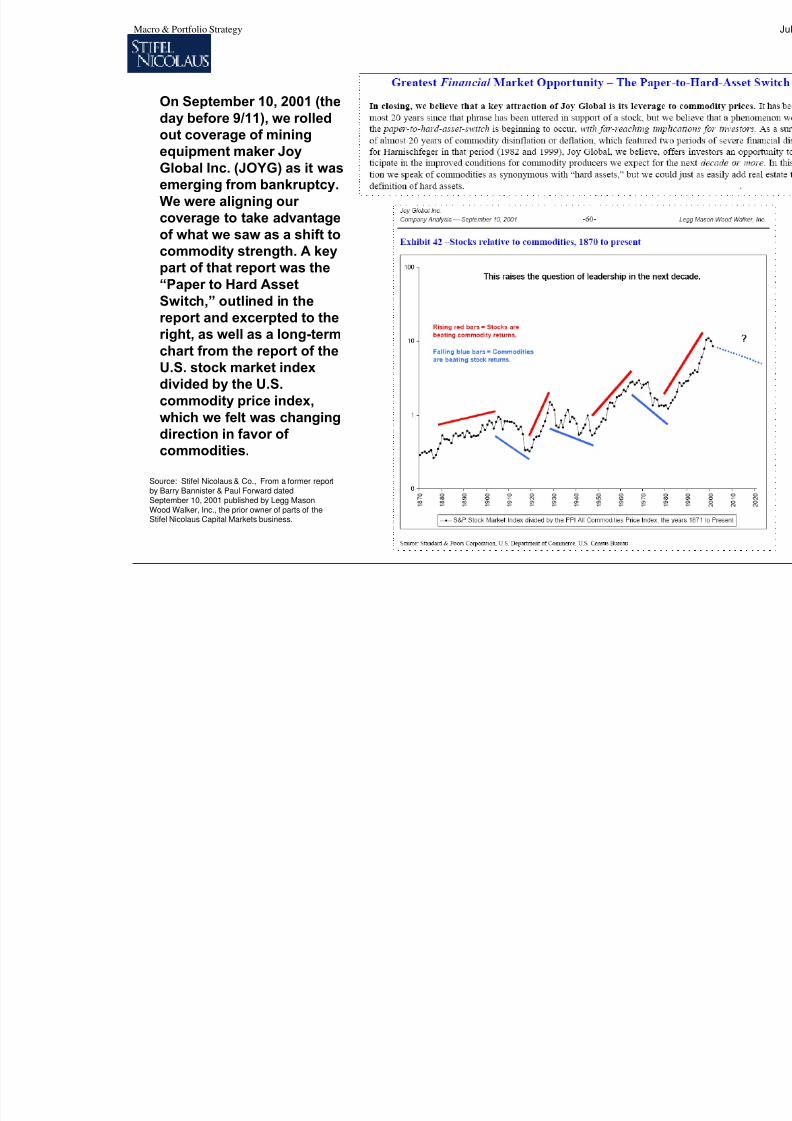

On September 10, 2001 (theday before 9/11), we rolledout coverage of mining

equipment maker JoyGlobal Inc. (JOYG) as it wasemerging from bankruptcy.We were aligning our coverage to take advantageof what we saw as a shift tocommodity strength. A keypart of that report was the“Paper to Hard Asset

Switch,” outlined in thereport and excerpted to theright, as well as a long-termchart from the report of theU.S. stock market indexdivided by the U.S.commodity price index,which we felt was changingdirection in favor of

commodities.

Source: Stifel Nicolaus & Co., From a former reportby Barry Bannister & Paul Forward datedSeptember 10, 2001 published by Legg MasonWood Walker, Inc., the prior owner of parts of theStifel Nicolaus Capital Markets business.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 7/59

0.1

1.0

10.0

100.0

1 8 7 0

1 8 7 5

1 8 8 0

1 8 8 5

1 8 9 0

1 8 9 5

1 9 0 0

1 9 0 5

1 9 1 0

1 9 1 5

1 9 2 0

1 9 2 5

1 9 3 0

1 9 3 5

1 9 4 0

1 9 4 5

1 9 5 0

1 9 5 5

1 9 6 0

R e l a t i v e p r i c e s t r e n g t h , s

t o c k s v s . c o m m o d i t i e s , l o g s c a l e

U.S. stock market composite relative to the U.S. comm

Key: When the line is rising, the S&P stock market index b

index and when the line is falling the oppos

U.S. Stock Market relative to the Commodity Mar

Post-Civil War

Reconstruction ends

in 1877, gold

standard begins

1879, deflationary

boom, stocks ra lly.

WW2

1939-45

'29

Crash,

Gold

siezed

U.S.$

devalued

in 1933.

Post-WW 1

commodity

bubble bursts,

bull market

begins.

WW1

1914 to

1918

Post-W.W. 2/Kore

commodity inflatio

bubble bursts,

disinflation ensue

1950s bull marke

begins.

Populism in

U.S. politics.

Panic of 1907,

a banking

crisis & stock

market crash.

Source: Standard & Poor’s (Cowles Composite joined to S&P 500), U.S. PPI All Co(rebased).

Note: While this is the time for cyclical (over) investment in commodity capacity thaproducers for a generation, the underlying equities respond to commodity prices, wh

Note: Excludes dividends for simplicity of

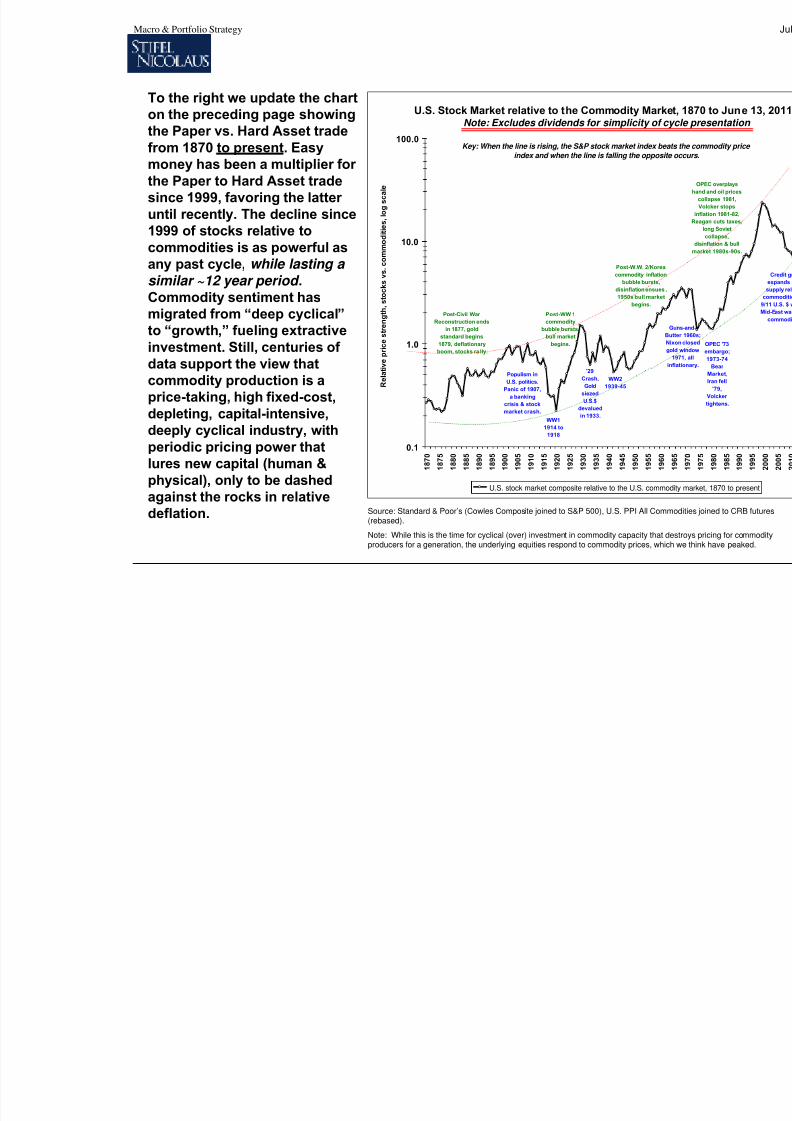

To the right we update the charton the preceding page showingthe Paper vs. Hard Asset trade

from 1870 to present. Easymoney has been a multiplier for the Paper to Hard Asset tradesince 1999, favoring the latter until recently. The decline since1999 of stocks relative tocommodities is as powerful asany past cycle, while lasting a similar ~12 year period .

Commodity sentiment hasmigrated from “deep cyclical”to “growth,” fueling extractiveinvestment. Still, centuries of data support the view thatcommodity production is aprice-taking, high fixed-cost,depleting, capital-intensive,deeply cyclical industry, with

periodic pricing power thatlures new capital (human &physical), only to be dashedagainst the rocks in relativedeflation.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 8/59

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

O c t - 9 8

A p r - 9 9

O c t - 9 9

A p r - 0 0

O c t - 0 0

A p r - 0 1

O c t - 0 1

A p r - 0 2

O c t - 0 2

A p r - 0 3

O c t - 0 3

A p r - 0 4

O c t - 0 4

A p r - 0 5

O c t - 0 5

A p r - 0 6

O c t - 0 6

A p r - 0 7

O c t - 0 7

A p r - 0 8

O c t - 0 8

A p r - 0 9

O c t - 0 9

A p r - 1 0

O c t - 1 0

A p r - 1 1

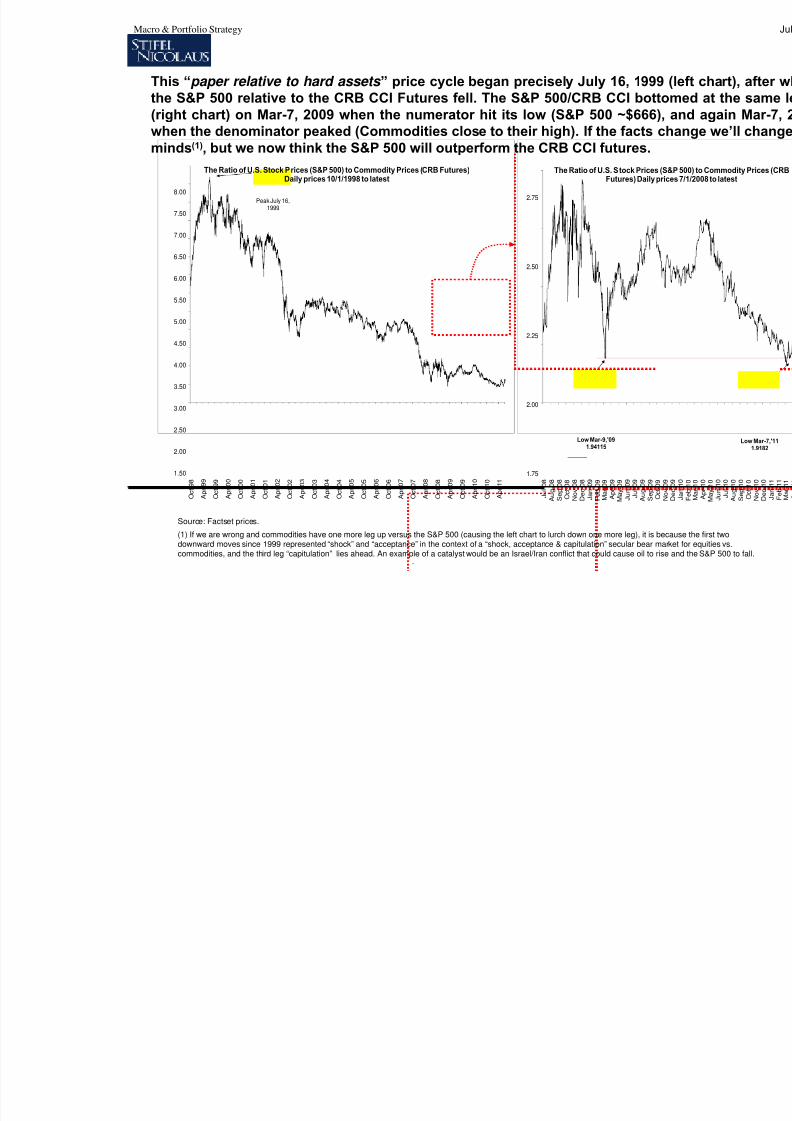

The Ratio of U.S. Stock Prices (S&P 500) to Commodity Prices (CRB Futures)Daily prices 10/1/1998 to latest

Peak July 16,1999

1.75

2.00

2.25

2.50

2.75

J u l - 0 8

A u g - 0

8

S e p - 0

8

O c t - 0 8

N o v - 0

8

D e c - 0

8

J a n - 0

9

F e b - 0

9

M a r - 0 9

A p r - 0 9

M a y - 0

9

J u n - 0

9

J u l - 0 9

A u g - 0

9

S e p - 0

9

O c t - 0 9

The Ratio of U.S. Stock Prices (Futures) Daily pr

Low Mar-9,'091.94115

Source: Factset prices.

(1) If we are wrong and commodities have one more leg up versus the S&P 500 (causing the left chart to lurch down one more leg), it is bdownward moves since 1999 represented “shock” and “acceptance” in the context of a “shock, acceptance & capitulation” secular bear mcommodities, and the third leg “capitulation” lies ahead. An example of a catalyst would be an Israel/Iran conflict that could cause oil to ri

This “paper relative to hard assets ” price cycle began precisely July 16, 1999the S&P 500 relative to the CRB CCI Futures fell. The S&P 500/CRB CCI bott(right chart) on Mar-7, 2009 when the numerator hit its low (S&P 500 ~$666)when the denominator peaked (Commodities close to their high). If the facts c

minds(1)

, but we now think the S&P 500 will outperform the CRB CCI futures.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 9/59

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

1 8 3 5

1 8 4 5

1 8 5 5

1 8 6 5

1 8 7 5

1 8 8 5

1 8 9 5

1 9 0 5

1 9 1 5

1 9 2 5

S&P Stock Market Composite 10-YeReturn (Incl. Reinvest

Data from 1825 to

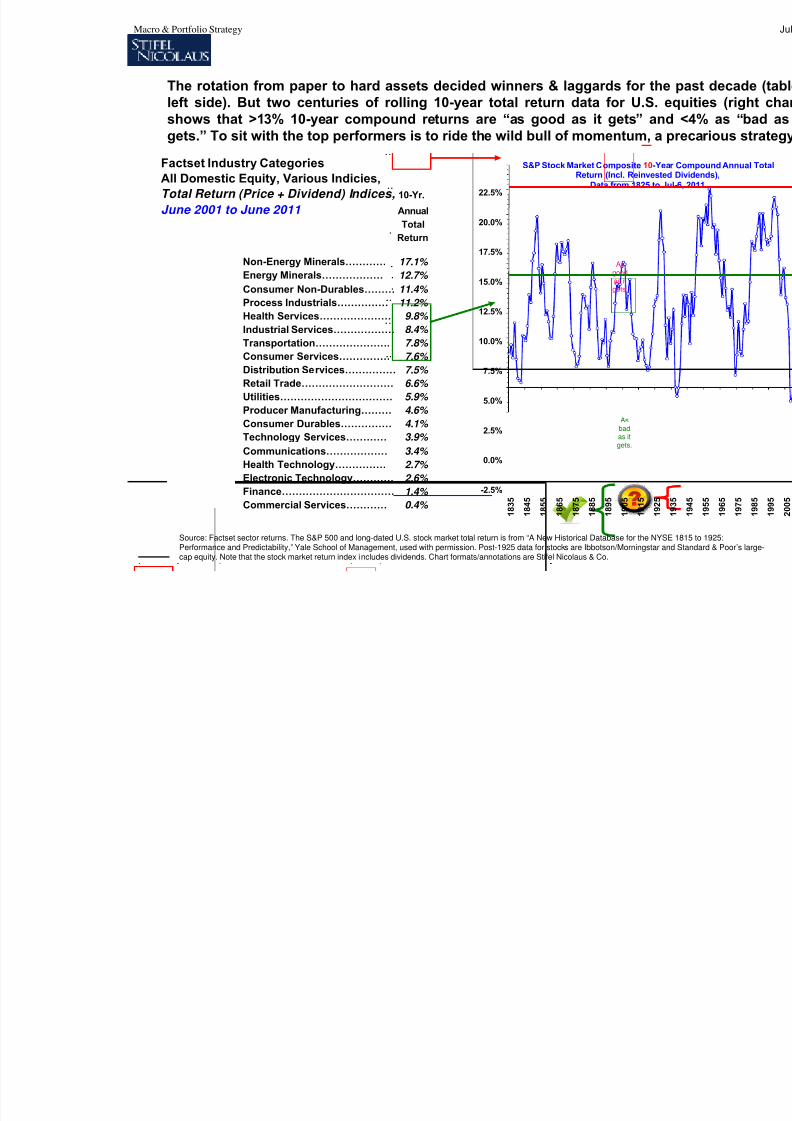

Factset Industry Categories

All Domestic Equity, Various Indicies,

Total Return (Price + Dividend) Indices, 10-Yr.

June 2001 to June 2011 Annual

Total

Return

Non-Energy Minerals………… 17.1%

Energy Minerals……………… 12.7%

Consumer Non-Durables……… 11.4%

Process Industrials…………… 11.2% Health Services………………… 9.8%

Industrial Services……………… 8.4%

Transportation…………………. 7.8%

Consumer Services…………… 7.6%

Distribution Services…………… 7.5%

Retail Trade……………………… 6.6%

Utilities…………………………… 5.9%

Producer Manufacturing……… 4.6%

Consumer Durables…………… 4.1%

Technology Services………… 3.9%

Communications……………… 3.4% Health Technology…………… 2.7%

Electronic Technology………… 2.6%

Finance…………………………… 1.4%

Commercial Services………… 0.4%

Source: Factset sector returns. The S&P 500 and long-dated U.S. stock market total return is from “A New Historical Database for the NYPerformance and Predictability,” Yale School of Management, used with permission. Post-1925 data for stocks are Ibbotson/Morningstar cap equity. Note that the stock market return index includes dividends. Chart formats/annotations are Stifel Nicolaus & Co.

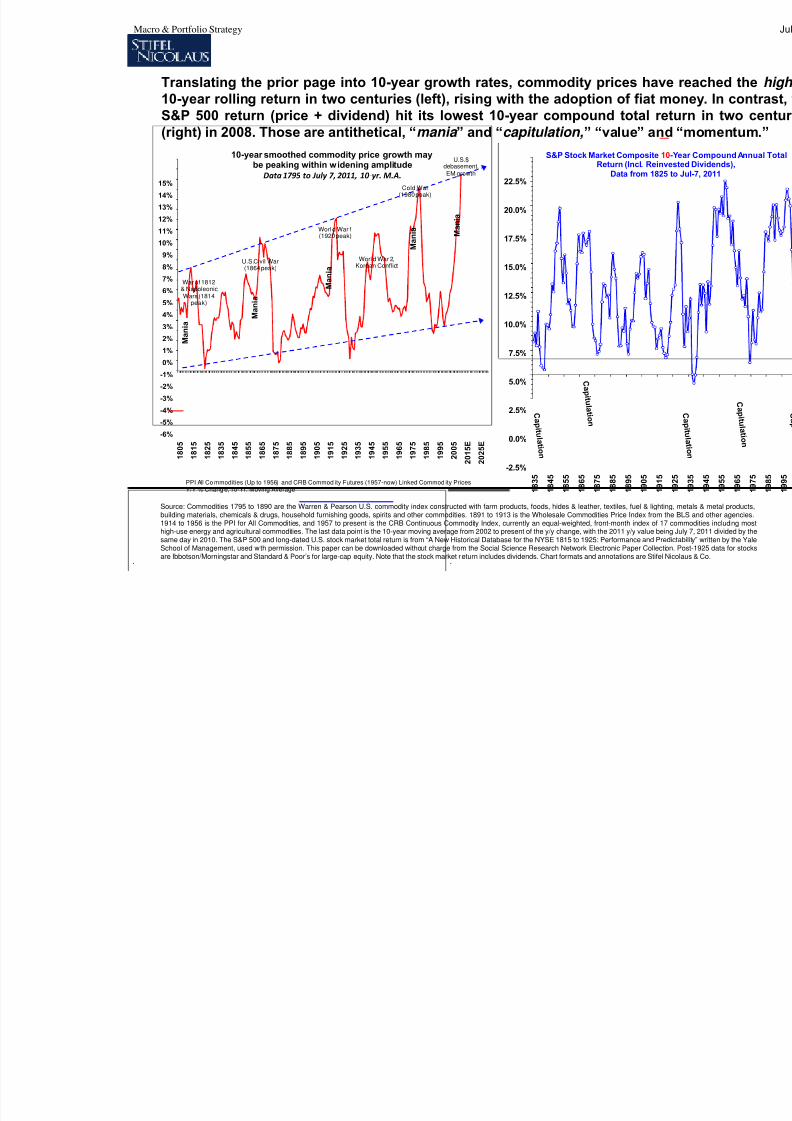

The rotation from paper to hard assets decided winners & laggards for thleft side). But two centuries of rolling 10-year total return data for U.S. shows that >13% 10-year compound returns are “as good as it gets” angets.” To sit with the top performers is to ride the wild bull of momentum, a

Asgoodas itgets.

Asbadas itgets.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 10/59

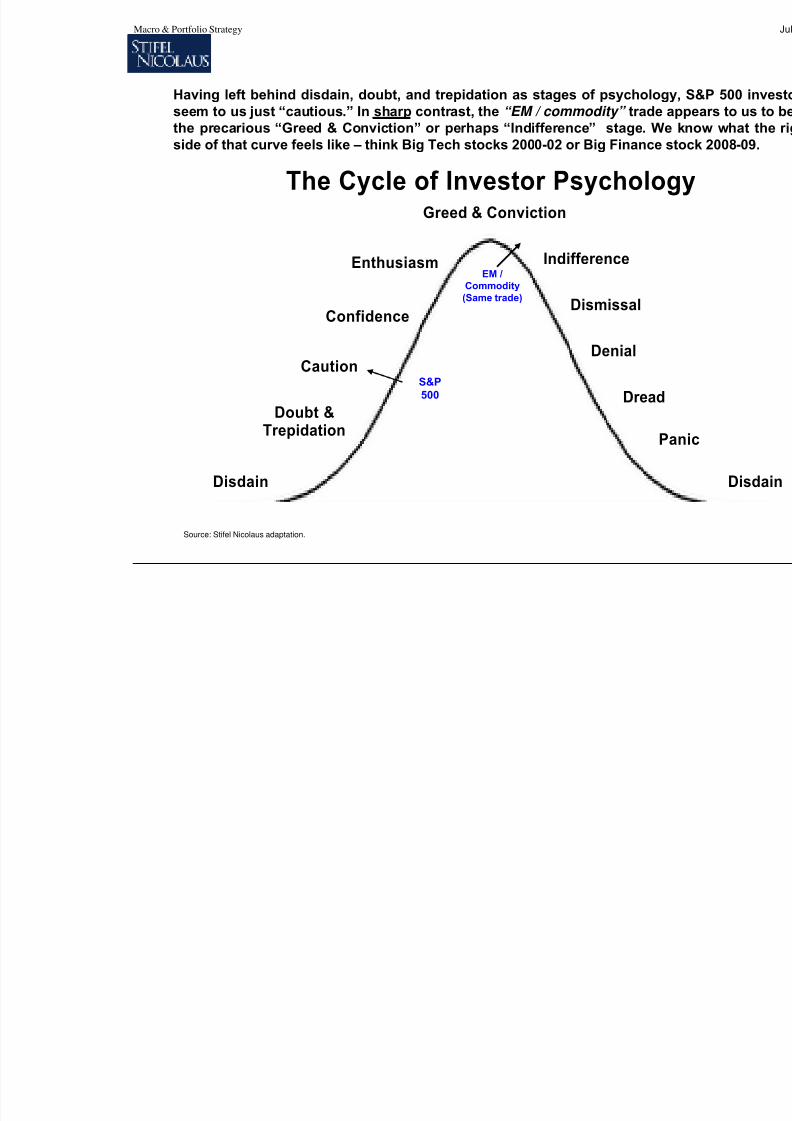

The Cycle of Investor Psycholo

Disdain

Doubt &Trepidation

Greed & Conviction

Enthusiasm

Confidence

Caution

P

Dread

Denial

Dismissal

Indifference

Source: Stifel Nicolaus adaptation.

S&P500

EM /Commodity

(Same trade)

Having left behind disdain, doubt, and trepidation as stages of psycholoseem to us just “cautious.” In sharp contrast, the “EM / commodity” tradethe precarious “Greed & Conviction” or perhaps “Indifference” stage. W

side of that curve feels like – think Big Tech stocks 2000-02 or Big Finance

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 11/59

$0.01

$1.00

$100.00

$10,000.00

$1,000,000.00

1 8 2 5

1 8 3 5

1 8 4 5

1 8 5 5

1 8 6 5

1 8 7 5

1 8 8 5

1 8 9 5

U.S. S&P Stock Market(Includes Rei

Data from 18

With exponenta

1.00

10.00

100.00

1 8 0 5

1 8 1 5

1 8 2 5

1 8 3 5

1 8 4 5

1 8 5 5

1 8 6 5

1 8 7 5

1 8 8 5

1 8 9 5

1 9 0 5

1 9 1 5

1 9 2 5

1 9 3 5

1 9 4 5

1 9 5 5

1 9 6 5

1 9 7 5

1 9 8 5

1 9 9 5

2 0 0 5

2 0 1 5 E

2 0 2 5 E

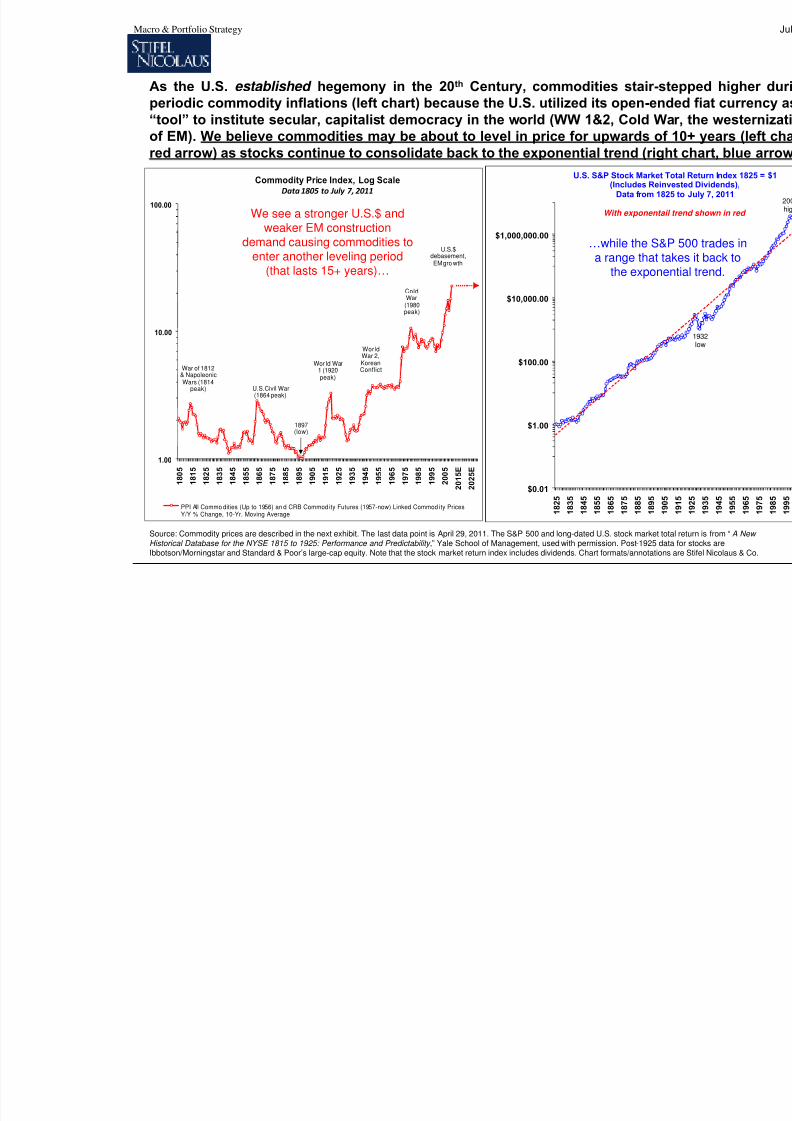

PPI All Commo dities (Up to 1956) an d CRB Commod ity Futures (1957-now) Linked Commod ity PricesY/Y % Change, 10-Yr. Moving Average

War of 1812& NapoleonicWars (1814

peak) U.S.Civil War(1864 peak)

Wor ld War1 (1920peak)

ColdWar(1980peak)

U.S.$debasement,EM gro wth

Commodity Price Index, Log ScaleData 1805 to July 7, 2011

WorldWar 2,KoreanConflict

1897(low)

Source: Commodity prices are described in the next exhibit. The last data point is April 29, 2011. The S&P 500 and long-dated U.S. stock market Historical Database for the NYSE 1815 to 1925: Performance and Predictability,” Yale School of Management, used with permission. Post-1925 dIbbotson/Morningstar and Standard & Poor’s large-cap equity. Note that the stock market return index includes dividends. Chart formats/annotatio

We see a stronger U.S.$ andweaker EM construction

demand causing commodities toenter another leveling period

(that lasts 15+ years)…

…while the S&a range that t

the expon

As the U.S. established hegemony in the 20th Century, commodities stair-speriodic commodity inflations (left chart) because the U.S. utilized its open-en“tool” to institute secular, capitalist democracy in the world (WW 1&2, Cold Wof EM). We believe commodities may be about to level in price for upwards o

red arrow) as stocks continue to consolidate back to the exponential trend (rig

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 12/59

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

1 8

0 5

1 8

1 5

1 8

2 5

1 8

3 5

1 8

4 5

1 8

5 5

1 8

6 5

1 8

7 5

1 8

8 5

1 8

9 5

1 9

0 5

1 9

1 5

1 9

2 5

1 9

3 5

1 9

4 5

1 9

5 5

1 9

6 5

1 9

7 5

1 9

8 5

1 9

9 5

2 0

0 5

2 0 1

5 E

2 0 2

5 E

PPI All Co mmodities (Up to 1956) and CRB Commod ity Futures (1957-now) Linked Commod ity PricesY/Y % Chang e, 10-Yr. Moving Average

War of 1812& NapoleonicWars (1814

peak)

U.S.Civil War(1864 peak)

Worl d War 1(1920 peak)

Cold War(1980 peak)

U.S.$debasement,EM growth

10-year smoothed commodity price growth maybe peaking within widening amplitude

Data 1795 to July 7, 2011, 10 ‐yr. M.A.

Worl d War 2,Korean Conflict

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

1 8 3 5

1 8 4 5

1 8 5 5

1 8 6 5

1 8 7 5

1 8 8 5

1 8 9 5

1 9 0 5

1 9 1 5

S&P Stock Market CompositeReturn (Incl. Rein

Data from 182

Translating the prior page into 10-year growth rates, commodity prices hav10-year rolling return in two centuries (left), rising with the adoption of fiat mS&P 500 return (price + dividend) hit its lowest 10-year compound total r(right) in 2008. Those are antithetical, “mania ” and “capitulation,” “value” an

M a n i a

M a n i a

M a n i a

M a n i a M

a n i a

Source: Commodities 1795 to 1890 are the Warren & Pearson U.S. commodity index constructed with farm products, foods, hides & leather, textiles, fuel & lighbuilding materials, chemicals & drugs, household furnishing goods, spirits and other commodities. 1891 to 1913 is the Wholesale Commodities Price Index from1914 to 1956 is the PPI for All Commodities, and 1957 to present is the CRB Continuous Commodity Index, currently an equal-weighted, front-month index of 1high-use energy and agricultural commodities. The last data point is the 10-year moving average from 2002 to present of the y/y change, with the 2011 y/y value besame day in 2010. The S&P 500 and long-dated U.S. stock market total return is from “A New Historical Database for the NYSE 1815 to 1925: Performance and PrSchool of Management, used with permission. This paper can be downloaded without charge from the Social Science Research Network Electronic Paper Collecare Ibbotson/Morningstar and Standard & Poor’s for large-cap equity. Note that the stock market return includes dividends. Chart formats and annotations are Stife

C a

p i t u

l a t i

o n

C a

p i t u

l a t i o

n

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 13/59

0%1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

Fed Funds Rate

Markets adjust to level, so momentum matters.

Each decade has featured a ~400bps

Fed Funds rate hike...

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%120%

140%

160%

180%

200%

220%

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

Fed Funds Rate y/y%

…but each 400bps rate cycle w

percentage change in rates fr

base, causing ever larger finan

A

B

A = Mar-89 peak, Drexel Burn. fails Feb-90

B = Dec-94 peak, Mexico Dec-94, EM 1997

C = May-05 peak, housing peaks the next

Source: U.S. Fed and government data, Stifel Nicolaus format.

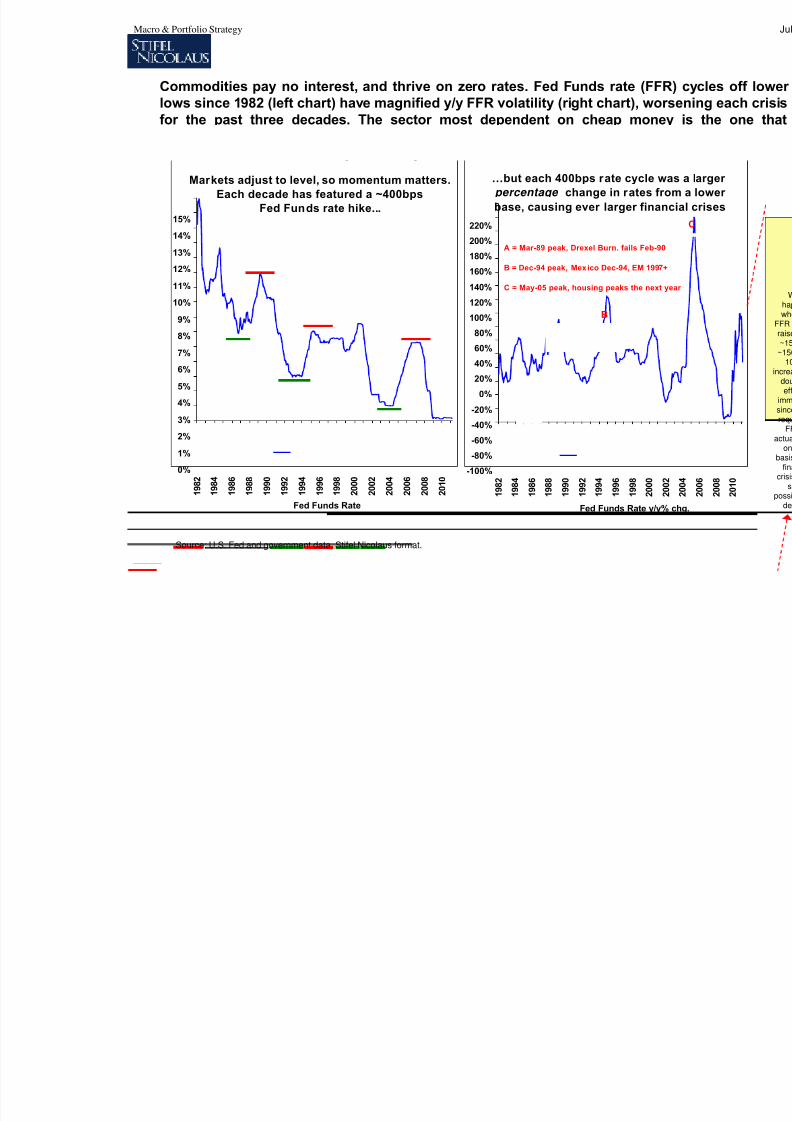

Commodities pay no interest, and thrive on zero rates. Fed Funds rate (FFlows since 1982 (left chart) have magnified y/y FFR volatility (right chart), wofor the past three decades. The sector most dependent on cheap monecollapses shortly after the y/y change in the FFR peaks. We t

EM/Commodities/Commodity FX this cycle.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 14/59

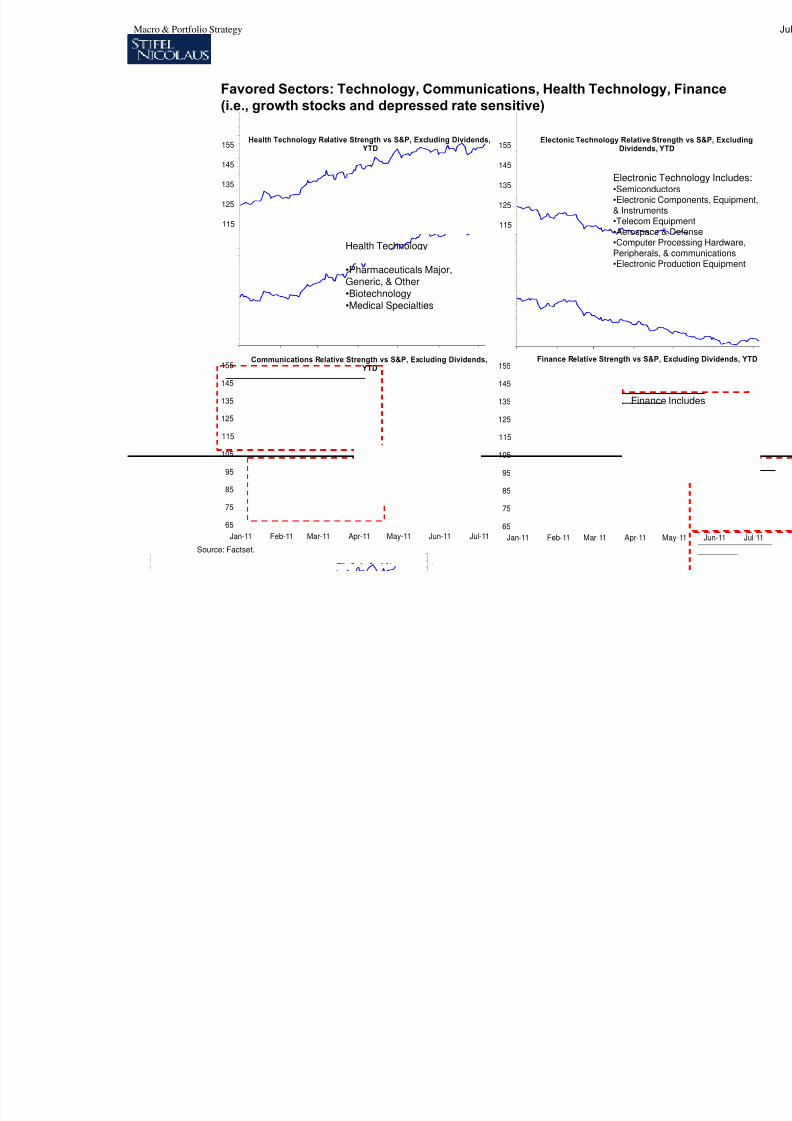

Favored Sectors: Technology, Communications, Health Technology(i.e., growth stocks and depressed rate sensitive)

Source: Factset.

65

75

85

95

105

115

125

135

145

155Health Technology Relative Strength vs S&P, Excluding Dividends,

YTD

65

75

85

95

105

115

125

135

145

155Electonic Technology Relative Str

Dividends, Y

65

75

85

95

105

115

125

135

145

155

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11

Communications Relative Strength vs S&P, Excluding Dividends, YTD

65

75

85

95

105

115

125

135

145

155

Jan-11 Feb-11 Mar-11 Apr-11

Finance Relative Strength vs S&P,

Health TechnologyIncludes:•Pharmaceuticals Major,Generic, & Other•Biotechnology

•Medical Specialties

Electronic T•Semiconduc•Electronic C& Instrument•Telecom Eq•Aerospace •Computer PPeripherals, •Electronic P

Finance•Banks•Invest•Insura•Real Eas well Communications

Includes:•Major, Specialty, &Wireless Telecom

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 15/59

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 16/59

Source: Stifel Nicolaus & Co.

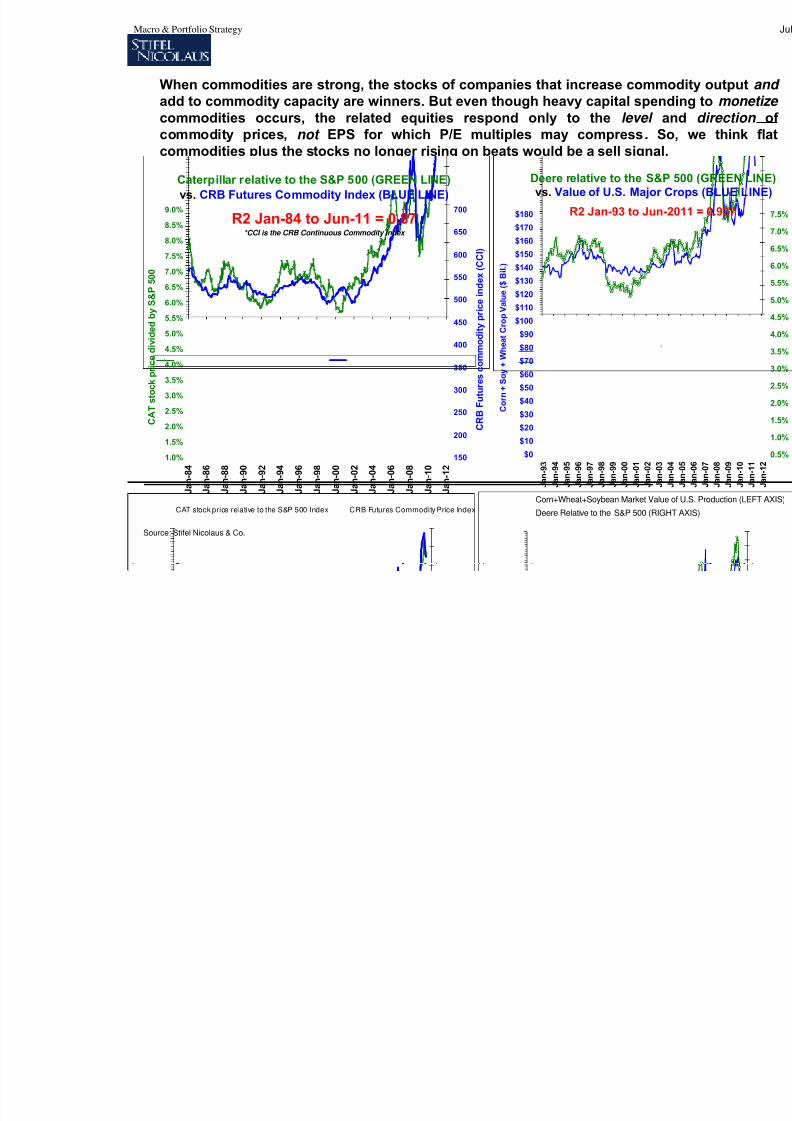

When commodities are strong, the stocks of companies that increase commadd to commodity capacity are winners. But even though heavy capital spencommodities occurs, the related equities respond only to the level commodity prices, not EPS for which P/E multiples may compress. S

commodities plus the stocks no longer rising on beats would be a sell signa

Caterpillar relative to the S&P 500 (GREEN LINE)

vs. CRB Futures Commodity Index (BLUE LINE)

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

J a n - 8 4

J a n - 8 6

J a n - 8 8

J a n - 9 0

J a n - 9 2

J a n - 9 4

J a n - 9 6

J a n - 9 8

J a n - 0 0

J a n - 0 2

J a n - 0 4

J a n - 0 6

J a n - 0 8

J a n - 1 0

J a n - 1 2

C A T s t o c k p r i c e d i v i d e d b y S

& P 5 0 0

150

200

250

300

350

400

450

500

550

600

650

700

C R B F u t u r e s c o m m o d i t y p r i c e

i n d e x ( C C I )

CAT stock price relative to the S&P 500 Index CRB Futures Commodity Price Index

R2 Jan-84 to Jun-11 = 0.87*CCI is the CRB Continuous Commodity Index

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

$170

$180

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

J a n - 0 1

J a n - 0 2

J a n - 0 3

C o r n + S o y + W h e a t C r o p V a l u e ( $ B i l . )

Deere relative to the S&vs. Value of U.S. Major

R2 Jan-93 to Jun

Corn+Wheat+Soybean Market Valu

Deere Relative to the S&P 500 (RIG

`

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 17/59

We see the S&P 500 bouncing off 200 dma iespecially weak through summer, then 1,4

the end of year

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 18/59

600

700

800

900

1000

1100

1200

1300

1400

1500

1600

1 / 3 / 0 0

5 / 1 1 / 0 0

9 / 1 9 / 0 0

1 / 2 9 / 0 1

6 / 7 / 0 1

1 0 / 1 9 / 0 1

3 / 1 / 0 2

7 / 1 0 / 0 2

1 1 / 1 4 / 0 2

3 / 2 7 / 0 3

8 / 0 5 / 0 3

1 2 / 1 1 / 0 3

4 / 2 2 / 0 4

8 / 3 1 / 0 4

1 / 0 7 / 0 5

5 / 1 8 / 0 5

9 / 2 6 / 0 5

2 / 0 3 / 0 6

6 / 1 4 / 0 6

1 0 / 2 0 / 0 6

3 / 0 5 / 0 7

7 / 1 2 / 0 7

1 1 / 1 6 / 0 7

3 / 3 1 / 0 8

8 / 0 6 / 0 8

1 2 / 1 2 / 0 8

4 / 2 4 / 0 9

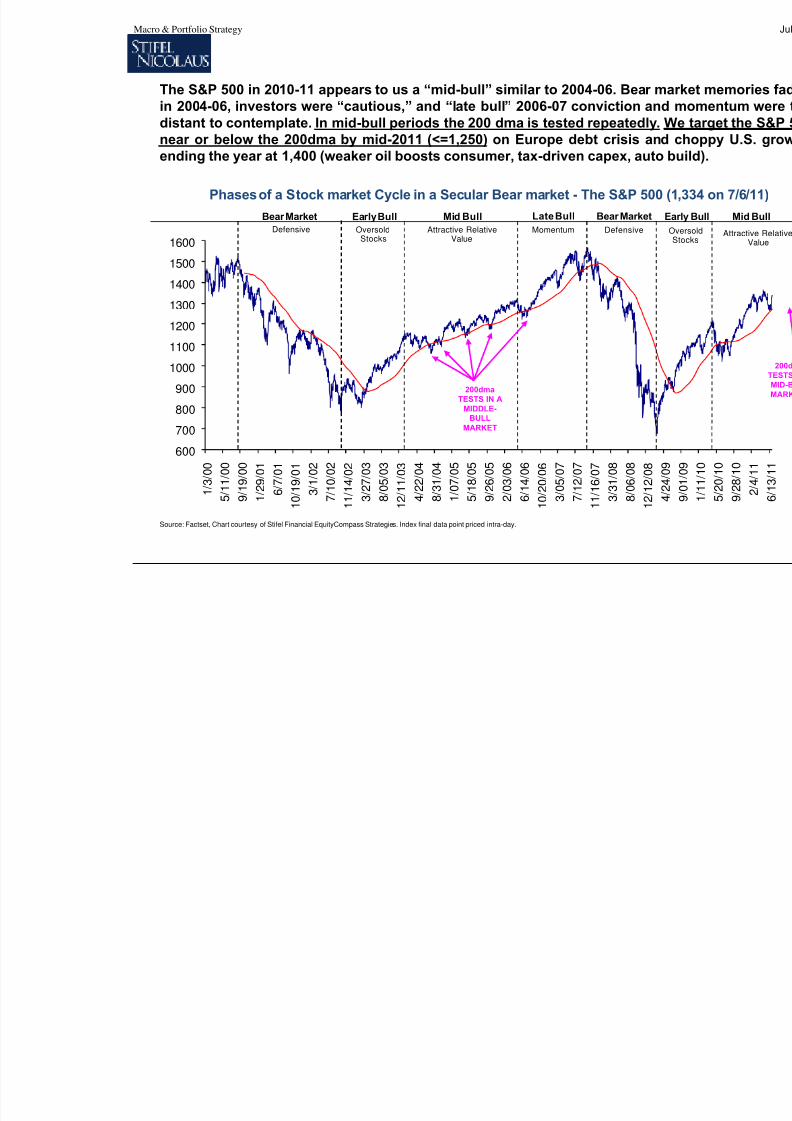

Phases of a Stock market Cycle in a Secular Bear market - The S&P 500

Bear Market Mid BullEarlyBull LateBull Bear Market

Defensive OversoldStocks

Attractive RelativeValue

Momentum Defensive

The S&P 500 in 2010-11 appears to us a “mid-bull” similar to 2004-06. Bear min 2004-06, investors were “cautious,” and “late bull” 2006-07 conviction andistant to contemplate. In mid-bull periods the 200 dma is tested repeatedly.near or below the 200dma by mid-2011 (<=1,250) on Europe debt crisis an

ending the year at 1,400 (weaker oil boosts consumer, tax-driven capex, auto

200dmaTESTS IN A

MIDDLE-BULL

MARKET

Source: Factset, Chart courtesy of Stifel Financial EquityCompass Strategies. Index final data point priced intra-day.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 19/59

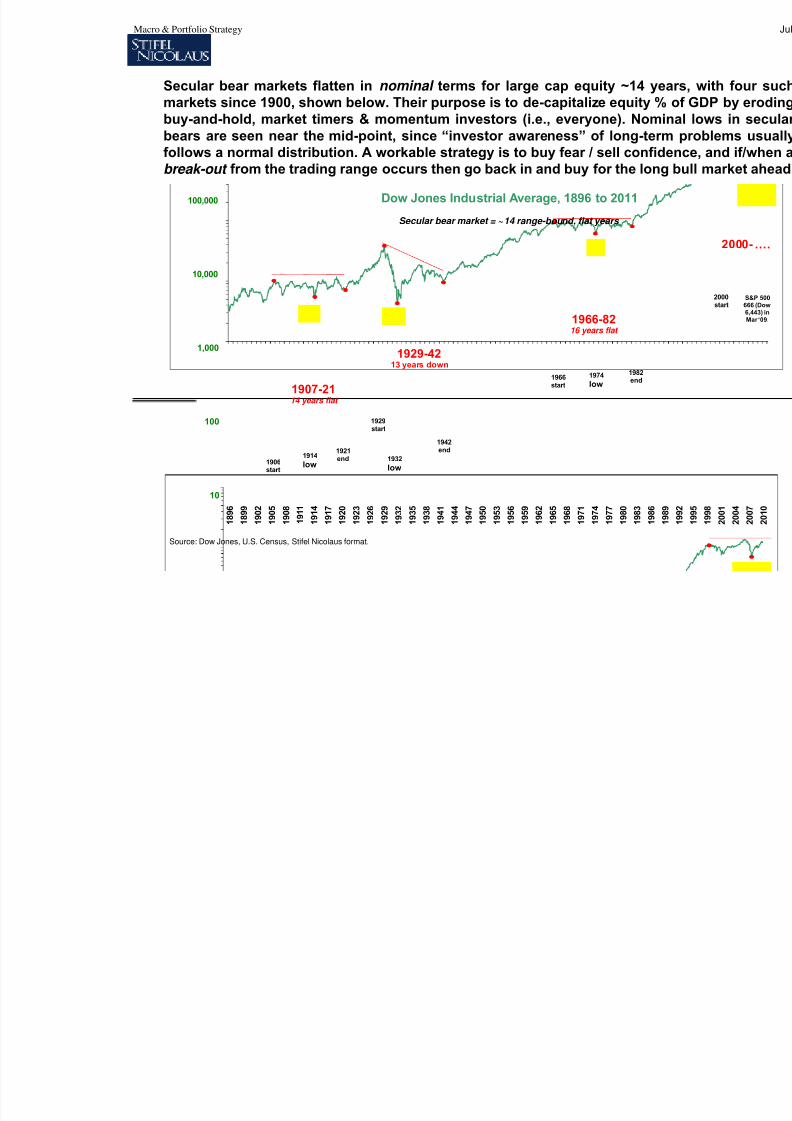

Secular bear markets flatten in nominal terms for large cap equity ~14 yemarkets since 1900, shown below. Their purpose is to de-capitalize equity %buy-and-hold, market timers & momentum investors (i.e., everyone). Nombears are seen near the mid-point, since “investor awareness” of long-ter

follows a normal distribution. A workable strategy is to buy fear / sell confidbreak-out from the trading range occurs then go back in and buy for the long

Source: Dow Jones, U.S. Census, Stifel Nicolaus format.

10

100

1,000

10,000

100,000

1 8 9 6

1 8 9 9

1 9 0 2

1 9 0 5

1 9 0 8

1 9 1 1

1 9 1 4

1 9 1 7

1 9 2 0

1 9 2 3

1 9 2 6

1 9 2 9

1 9 3 2

1 9 3 5

1 9 3 8

1 9 4 1

1 9 4 4

1 9 4 7

1 9 5 0

1 9 5 3

1 9 5 6

1 9 5 9

1 9 6 2

1 9 6 5

1 9 6 8

1 9 7 1

1 9 7 4

1 9 7 7

1 9 8 0

1 9 8 3

1 9 8 6

Dow Jones Industrial Average, 1896 to 2011

Secular bear market = ~14 range-bound, flat years

1907-2114 years flat

1929-4213 years down

1966-8216 years flat

1914low

1921end 1932

low

1942end

1974

low

1982end

1906start

1929start

1966start

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 20/59

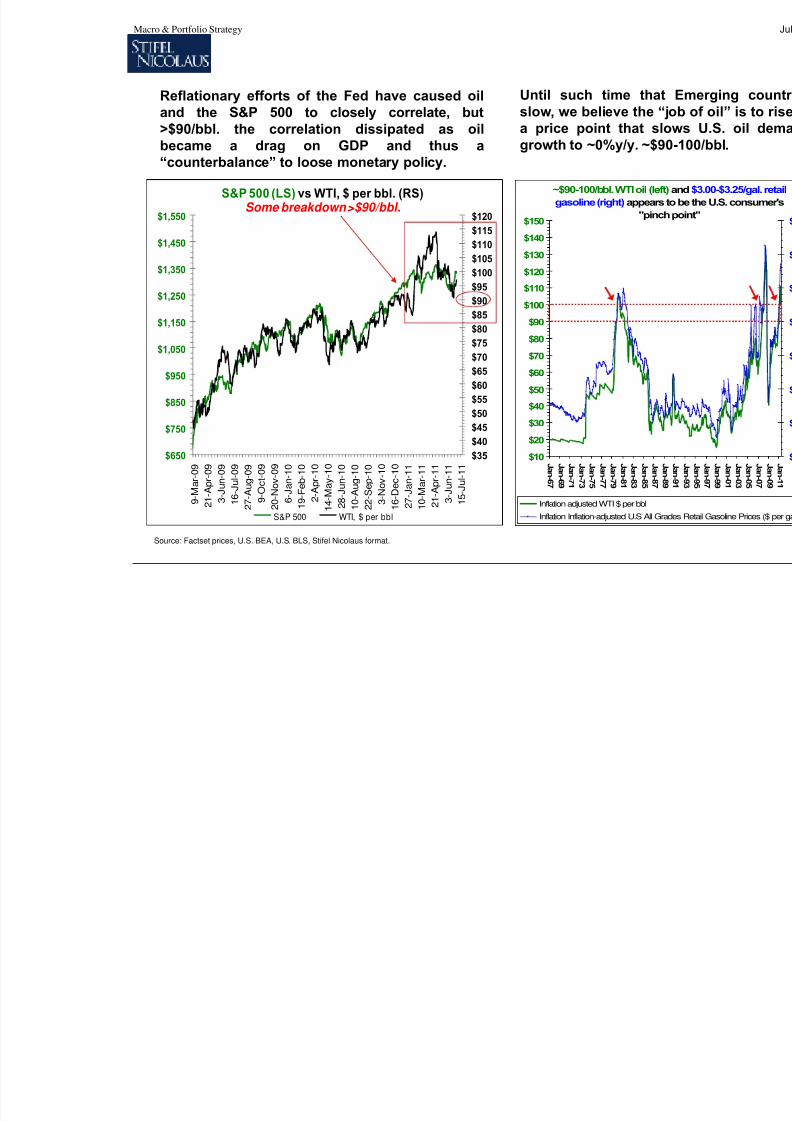

Reflationary efforts of the Fed have caused oiland the S&P 500 to closely correlate, but>$90/bbl. the correlation dissipated as oil

became a drag on GDP and thus a“counterbalance” to loose monetary policy.

Source: Factset prices, U.S. BEA, U.S. BLS, Stifel Nicolaus format.

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85$90

$95

$100

$105

$110

$115

$120

$650

$750

$850

$950

$1,050

$1,150

$1,250

$1,350

$1,450

$1,550

9 - M

a r - 0 9

2 1 - A

p r - 0 9

3 - J

u n - 0

9

1 6 - J

u l - 0 9

2 7 - A

u g - 0

9

9 - O

c t - 0 9

2 0 - N

o v - 0

9

6 - J

a n - 1

0

1 9 - F

e b - 1

0

2 - A

p r - 1 0

1 4 - M

a y - 1

0

2 8 - J

u n - 1

0

1 0 - A

u g - 1

0

2 2 - S

e p - 1

0

3 - N

o v - 1

0

1 6 - D

e c - 1

0

2 7 - J

a n - 1

1

1 0 - M

a r - 1 1

2 1 - A

p r - 1 1

3 - J

u n - 1

1

1 5 - J

u l - 1 1

S&P 500 (LS) vs WTI, $ per bbl. (RS)Some breakdown >$90/bbl.

S&P 500 WTI, $ per bbl

Until such time thatslow, we believe the “a price point that sl

growth to ~0%y/y. ~$9

~$90-100/bbl. WTI oil (lef

gasoline (right)appears

"pinc

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

J an- 6 7

J an- 6 9

J an-7 1

J an-7 3

J an-7 5

J an-7 7

J an-7 9

J an- 8 1

J an- 8 3

J an- 8 5

J an- 8 7

Inflation adjusted WTI $ per bbl

Inflation Inflation-adjusted U.S All G

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 21/59

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

J u l - 9 8

J a n - 9 9

J u l - 9 9

J a n - 0 0

J u l - 0 0

J a n - 0 1

J u l - 0 1

J a n - 0 2

J u l - 0 2

J a n - 0 3

J u l - 0 3

J a n - 0 4

J u l - 0 4

J a n - 0 5

J u l - 0 5

J a n - 0 6

J u l - 0 6

J a n - 0 7

J u l - 0 7

J a n - 0 8

J u l - 0 8

J a n - 0 9

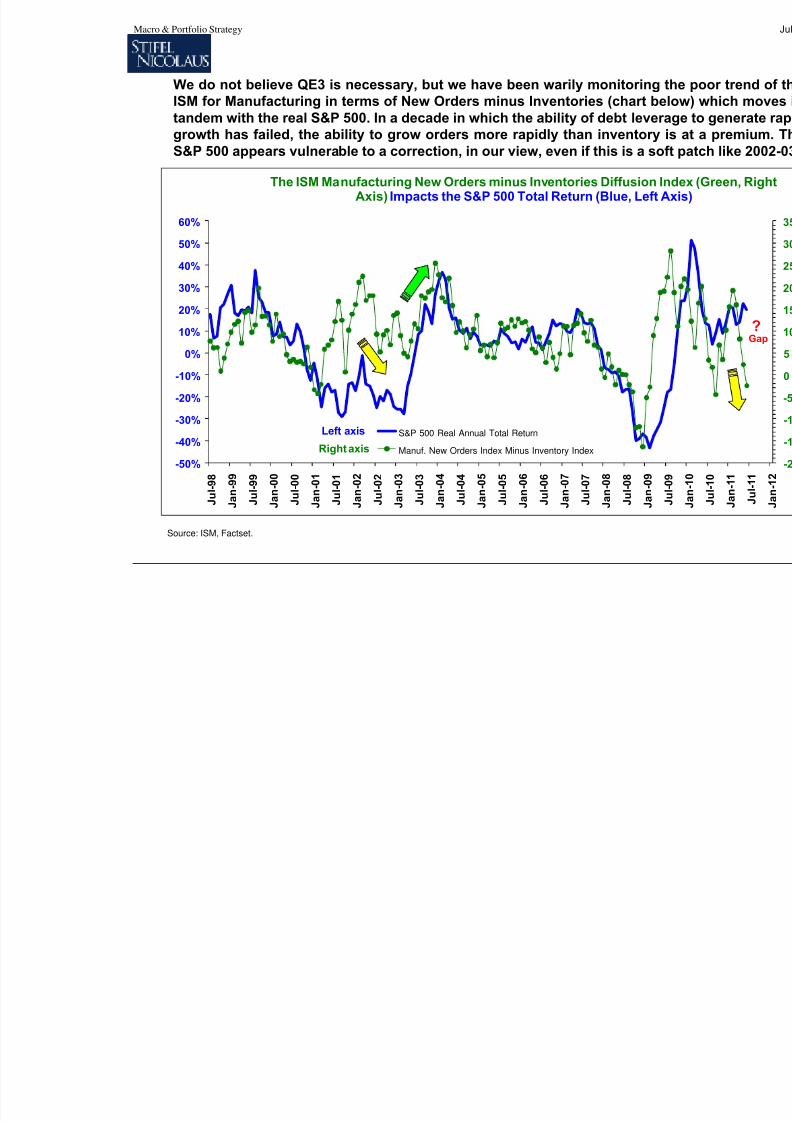

The ISM Manufacturing New Orders minus Inventories Diffusion IAxis) Impacts the S&P 500 Total Return (Blue, Left

S&P 500 Real Annual Total Return

Manuf. New Orders Index Minus Inventory Index

Left axis

Right axis

Source: ISM, Factset.

We do not believe QE3 is necessary, but we have been warily monitoring ISM for Manufacturing in terms of New Orders minus Inventories (chart betandem with the real S&P 500. In a decade in which the ability of debt levergrowth has failed, the ability to grow orders more rapidly than inventory

S&P 500 appears vulnerable to a correction, in our view, even if this is a so

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 22/59

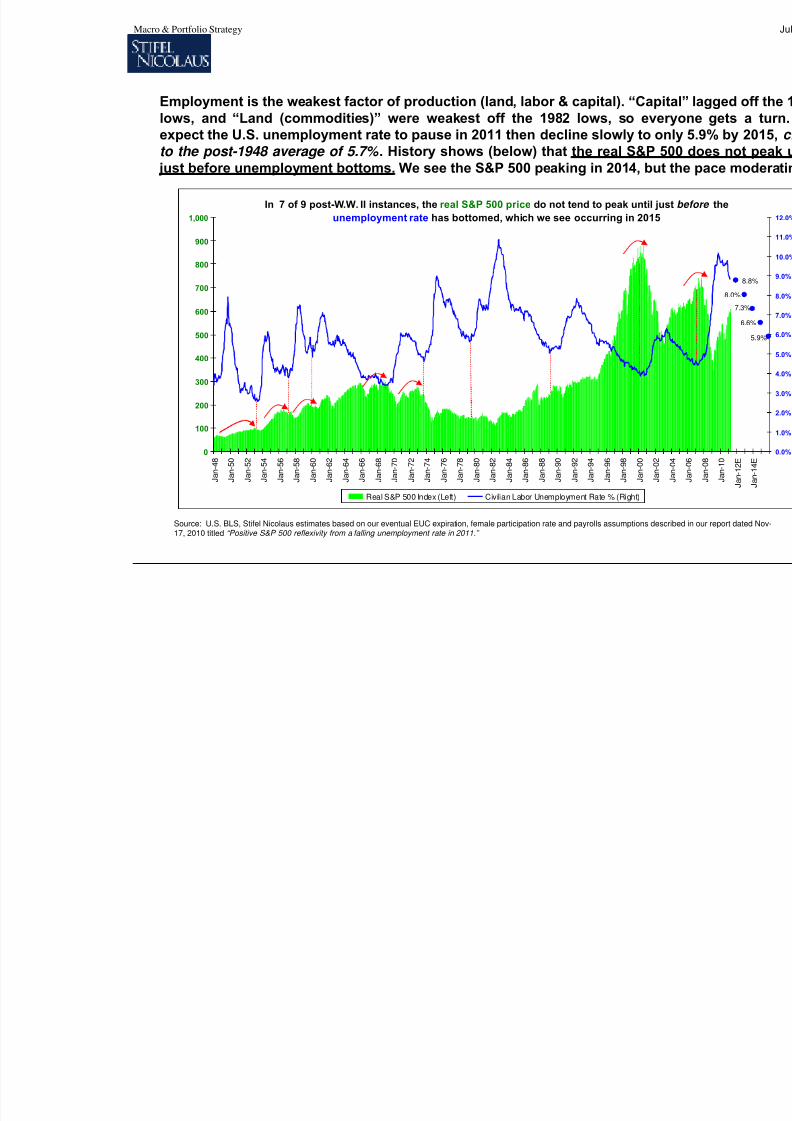

In 7 of 9 post-W.W. II instances, the real S&P 500 price do not tend to peak until ju

unemployment rate has bottomed, which we see occurring in 2015

0

100

200

300

400

500

600

700

800

900

1,000

J a n - 4

8

J a n - 5

0

J a n - 5

2

J a n - 5

4

J a n - 5

6

J a n - 5

8

J a n - 6

0

J a n - 6

2

J a n - 6

4

J a n - 6

6

J a n - 6

8

J a n - 7

0

J a n - 7

2

J a n - 7

4

J a n - 7

6

J a n - 7

8

J a n - 8

0

J a n - 8

2

J a n - 8

4

J a n - 8

6

J a n - 8

8

J a n - 9

0

J a n - 9

2

J a n - 9

4

J a n - 9

6

J a n - 9

8

J a n - 0

0

J a n - 0

2

Real S&P 500 Index (Left) Civilian Labor Unemployment Rate % (Right)

Employment is the weakest factor of production (land, labor & capital). “Caplows, and “Land (commodities)” were weakest off the 1982 lows, so eveexpect the U.S. unemployment rate to pause in 2011 then decline slowly to o

to the post-1948 average of 5.7% . History shows (below) that the real S&P 5 just before unemployment bottoms. We see the S&P 500 peaking in 2014, bu

Source: U.S. BLS, Stifel Nicolaus estimates based on our eventual EUC expiration, female participation rate and payrolls assumptions des17, 2010 titled “Positive S&P 500 reflexivity from a falling unemployment rate in 2011.”

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 23/59

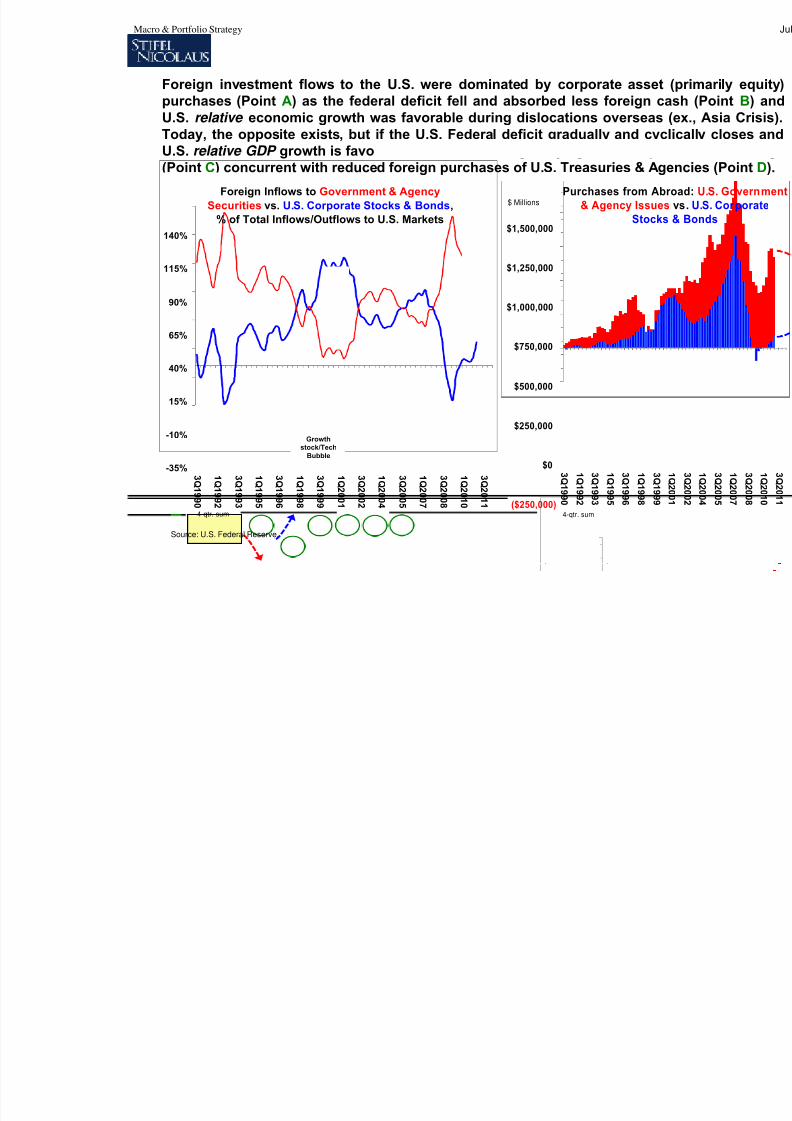

Foreign Inflows to Government & Agency

Securities vs. U.S. Corporate Stocks & Bonds,

% of Total Inflows/Outflows to U.S. Markets

-35%

-10%

15%

40%

65%

90%

115%

140%

3 Q1 9 9 0

1 Q1 9 9 2

3 Q1 9 9 3

1 Q1 9 9 5

3 Q1 9 9 6

1 Q1 9 9 8

3 Q1 9 9 9

1 Q2 0 0 1

3 Q2 0 0 2

1 Q2 0 0 4

3 Q2 0 0 5

1 Q2 0 0 7

3 Q2 0 0 8

1 Q2 0 1 0

3 Q2 0 1 1

4-qtr. sum

Source: U.S. Federal Reserve.

Foreign investment flows to the U.S. were dominated by corporate assetpurchases (Point A) as the federal deficit fell and absorbed less foreign cU.S. relative economic growth was favorable during dislocations overseasToday, the opposite exists, but if the U.S. Federal deficit gradually and cyc

U.S. relative GDP growth is favorable, we believe foreign buying of U.S. equ(Point C) concurrent with reduced foreign purchases of U.S. Treasuries & Ag

A

B

D

CGrowthstock/Tech

Bubble

Purchases from Ab& Agency Issue

Stock

($250,000)

$0

$250,000

$500,000

$750,000

$1,000,000

$1,250,000

$1,500,000

3 Q1 9 9 0

1 Q1 9 9 2

3 Q1 9 9 3

1 Q1 9 9 5

3 Q1 9 9 6

1 Q1 9 9 8

3 Q1 9 9 9

$ Millions

4-qtr. sum

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 24/59

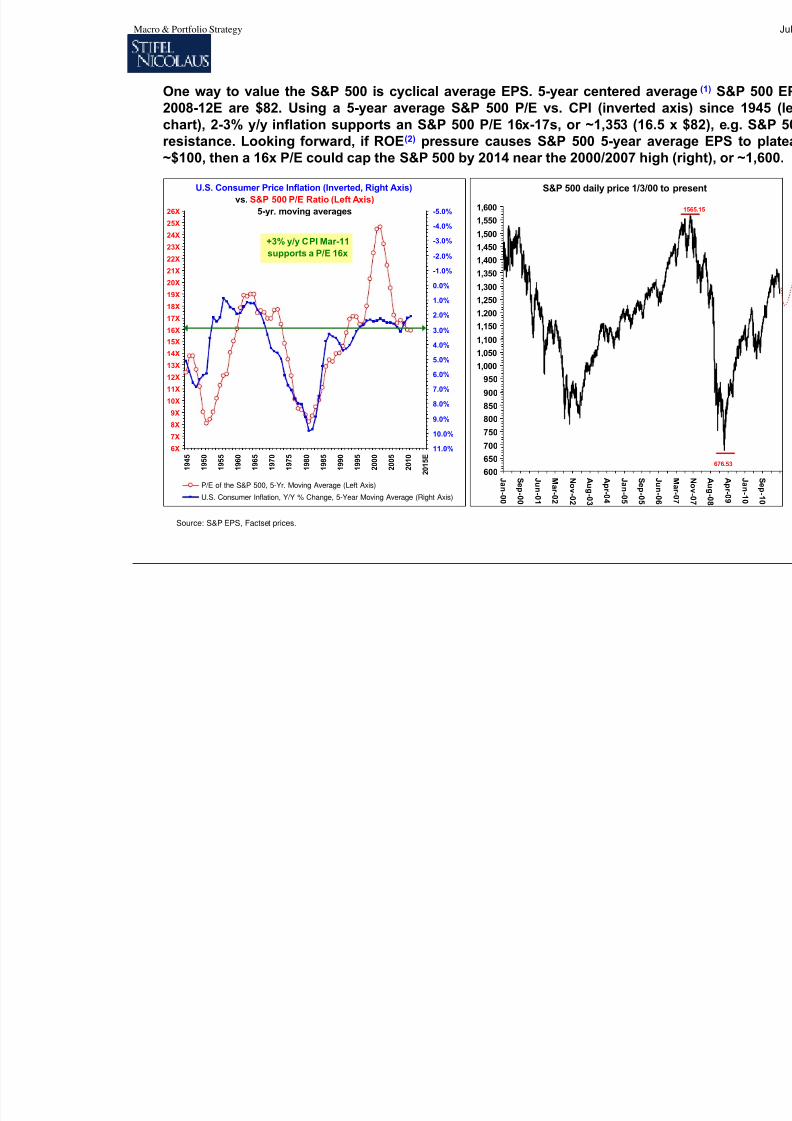

One way to value the S&P 500 is cyclical average EPS. 5-year centered av2008-12E are $82. Using a 5-year average S&P 500 P/E vs. CPI (inverted chart), 2-3% y/y inflation supports an S&P 500 P/E 16x-17s, or ~1,353 (16.5resistance. Looking forward, if ROE(2) pressure causes S&P 500 5-year av~$100, then a 16x P/E could cap the S&P 500 by 2014 near the 2000/2007 hig

6X

7X

8X

9X

10X

11X

12X

13X

14X

15X

16X

17X

18X

19X

20X

21X

22X

23X

24X

25X

26X

1 9 4 5

1 9 5 0

1 9 5 5

1 9 6 0

1 9 6 5

1 9 7 0

1 9 7 5

1 9 8 0

1 9 8 5

1 9 9 0

1 9 9 5

2 0 0 0

2 0 0 5

2 0 1 0

2 0 1 5 E

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

P/E of the S&P 500, 5-Yr. Moving Average (Left Axis)

U.S. Consumer Inflation, Y/Y % Change, 5-Year Moving Average (Right Axis)

U.S. Consumer Price Inflation (Inverted, Right Axis)

vs. S&P 500 P/E Ratio (Left Axis)

5-yr. moving averages

+3% y/y CPI Mar-11

supports a P/E 16x

S&P 500 daily price 1/3/00 t

600

650

700

750

800

850

900

950

1,000

1,050

1,100

1,150

1,2001,250

1,300

1,350

1,400

1,450

1,500

1,550

1,600

J an- 0 0

S e p- 0 0

J un- 0 1

M ar - 0 2

N ov- 0 2

A u g- 0 3

A pr - 0 4

J an- 0 5

S e p- 0 5

J un- 0 6

Source: S&P EPS, Factset prices.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 25/59

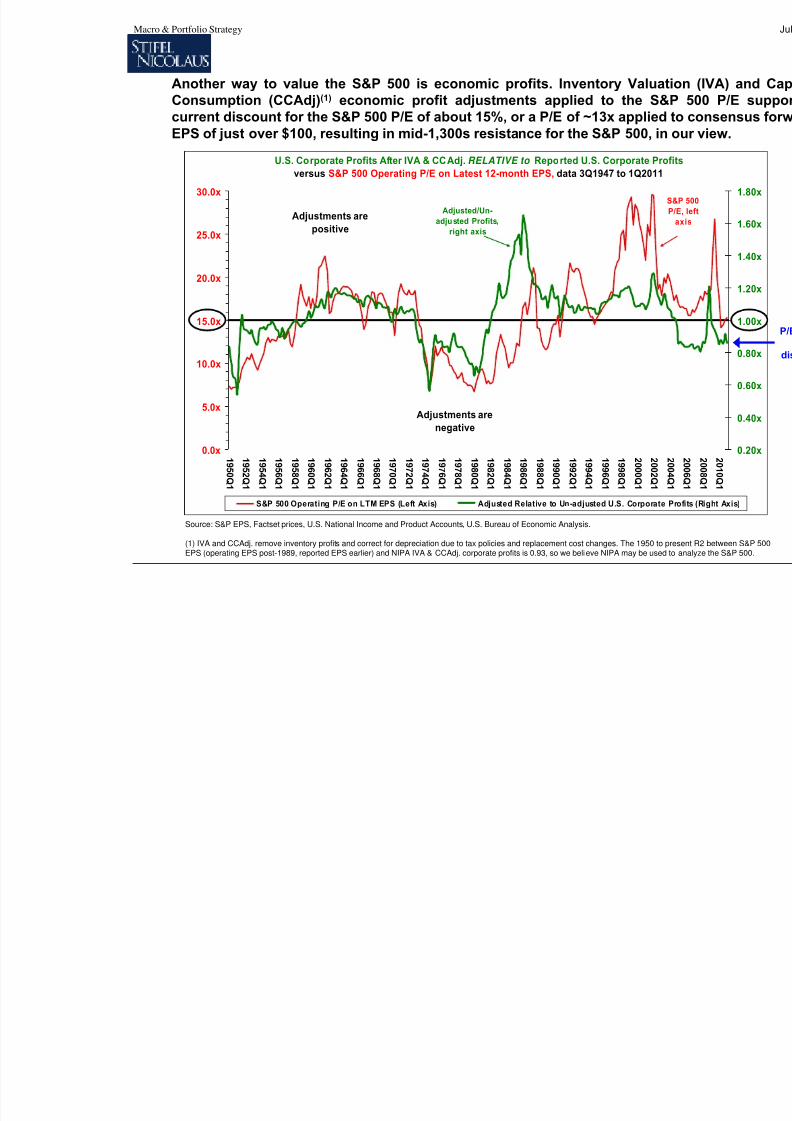

Another way to value the S&P 500 is economic profits. Inventory ValuaConsumption (CCAdj)(1) economic profit adjustments applied to the S¤t discount for the S&P 500 P/E of about 15%, or a P/E of ~13x appliedEPS of just over $100, resulting in mid-1,300s resistance for the S&P 500, i

Source: S&P EPS, Factset prices, U.S. National Income and Product Accounts, U.S. Bureau of Economic Analysis.

(1) IVA and CCAdj. remove inventory profits and correct for depreciation due to tax policies and replacement cost changes. The 1950 toEPS (operating EPS post-1989, reported EPS earlier) and NIPA IVA & CCAdj. corporate profits is 0.93, so we believe NIPA may be use

U.S. Corporate Profits After IVA & CCAdj. RELATIVE to Reported U.S. Corporate Pr

versus S&P 500 Operating P/E on Latest 12-month EPS, data 3Q1947 to 1Q2011

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

1 9 5 0 Q1

1 9 5 2 Q1

1 9 5 4 Q1

1 9 5 6 Q1

1 9 5 8 Q1

1 9 6 0 Q1

1 9 6 2 Q1

1 9 6 4 Q1

1 9 6 6 Q1

1 9 6 8 Q1

1 9 7 0 Q1

1 9 7 2 Q1

1 9 7 4 Q1

1 9 7 6 Q1

1 9 7 8 Q1

1 9 8 0 Q1

1 9 8 2 Q1

1 9 8 4 Q1

1 9 8 6 Q1

1 9 8 8 Q1

1 9 9 0 Q1

1 9 9 2 Q1

1 9 9 4 Q1

1 9 9 6 Q1

1 9 9 8 Q1

2 0 0 0 Q1

2 0 0 2 Q1

S&P 500 Operating P/E on LTM EPS (Left Axis) Adjusted Relative to Un-adjusted U.S. Corporate

Adjustments are

negative

Adjustments are

positive

Adjusted/Un-

adjusted Profits,

right axis

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 26/59

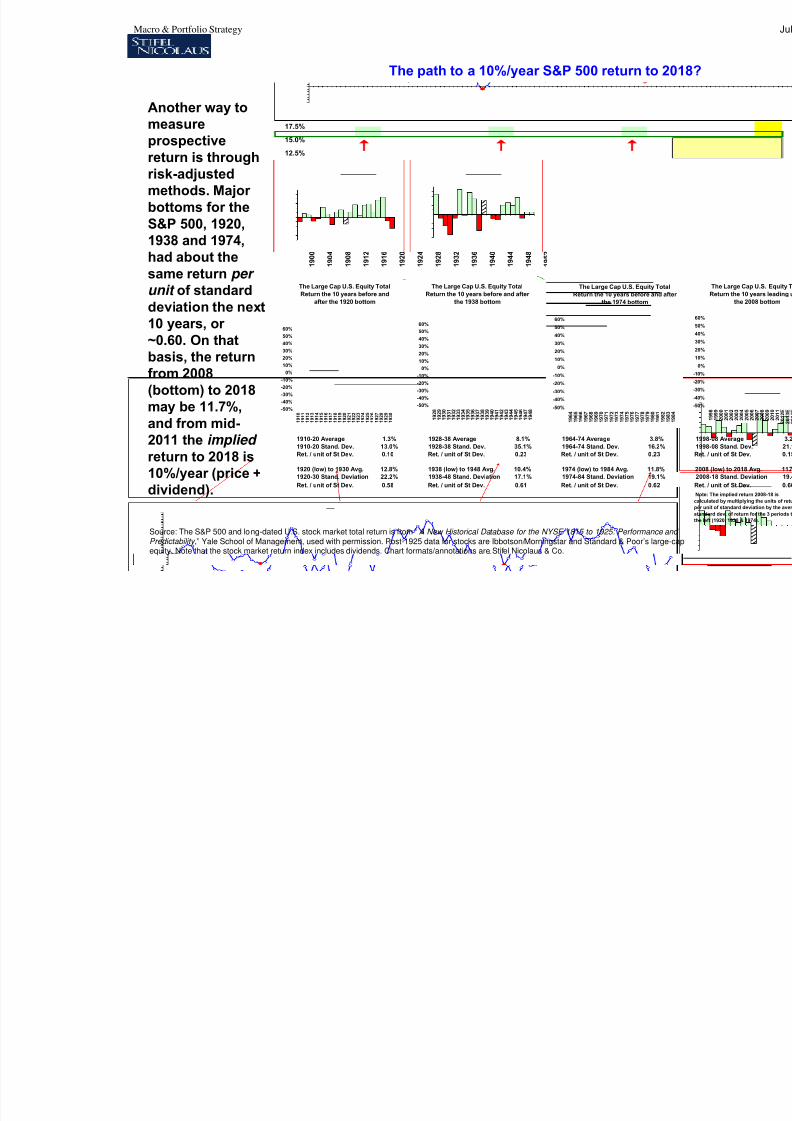

Another way tomeasureprospectivereturn is throughrisk-adjustedmethods. Major bottoms for theS&P 500, 1920,1938 and 1974,had about thesame return per unit of standard

deviation the next10 years, or ~0.60. On thatbasis, the returnfrom 2008(bottom) to 2018may be 11.7%,and from mid-2011 the implied

return to 2018 is10%/year (price +dividend).

1910-20 Average 1.3% 1928-38 Average 8.1% 1964-74 Average 3.8%

1910-20 Stand. Dev. 13.0% 1928-38 Stand. Dev. 35.1% 1964-74 Stand. Dev. 16.2%

Ret. / unit of St Dev. 0.10 Ret. / unit of St Dev. 0.23 Ret. / unit of St Dev. 0.23

1920 (low) to 1930 Avg. 12.8% 1938 (low) to 1948 Avg. 10.4% 1974 (low) to 1984 Avg. 11.8%1920-30 Stand. Deviation 22.2% 1938-48 Stand. Deviation 17.1% 1974-84 Stand. Deviation 19.1%

Ret. / unit of St Dev. 0.58 Ret. / unit of St Dev. 0.61 Ret. / unit of St Dev. 0.62

S&P Stock Market Composite 10-Year Compound Annual Total Return (Including Re

Data 1900 to Apr-28, 2011

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

12.5%

15.0%

17.5%

20.0%

22.5%

1 9 0 0

1 9 0 4

1 9 0 8

1 9 1 2

1 9 1 6

1 9 2 0

1 9 2 4

1 9 2 8

1 9 3 2

1 9 3 6

1 9 4 0

1 9 4 4

1 9 4 8

1 9 5 2

1 9 5 6

1 9 6 0

1 9 6 4

1 9 6 8

1 9 7 2

1 9 7 6

The Large Cap U.S. Equity Total

Return the 10 years before and after

the 1938 bottom

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 9 2 8

1 9 2 9

1 9 3 0

1 9 3 1

1 9 3 2

1 9 3 3

1 9 3 4

1 9 3 5

1 9 3 6

1 9 3 7

1 9 3 8

1 9 3 9

1 9 4 0

1 9 4 1

1 9 4 2

1 9 4 3

1 9 4 4

1 9 4 5

1 9 4 6

1 9 4 7

1 9 4 8

The Large Cap U.S. Equity ToReturn the 10 years before and

the 1974 bottom

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 9 6 4

1 9 6 5

1 9 6 6

1 9 6 7

1 9 6 8

1 9 6 9

1 9 7 0

1 9 7 1

1 9 7 2

1 9 7 3

1 9 7 4

1 9 7 5

1 9 7 6

1 9 7 7

1 9 7 8

1 9 7 9

1 9 8 0

1 9 8 1

1 9 8 2

The Large Cap U.S. Equity Total

Return the 10 years before and

after the 1920 bottom

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

1 9 1 0

1 9 1 1

1 9 1 2

1 9 1 3

1 9 1 4

1 9 1 5

1 9 1 6

1 9 1 7

1 9 1 8

1 9 1 9

1 9 2 0

1 9 2 1

1 9 2 2

1 9 2 3

1 9 2 4

1 9 2 5

1 9 2 6

1 9 2 7

1 9 2 8

1 9 2 9

1 9 3 0

Source: The S&P 500 and long-dated U.S. stock market total return is from “A New Historical Database for the NYSE 1815 to 1925: PerformancePredictability,” Yale School of Management, used with permission. Post-1925 data for stocks are Ibbotson/Morningstar and Standard & Poor’s larequity. Note that the stock market return index includes dividends. Chart formats/annotations are Stifel Nicolaus & Co.

The path to a 10%/year S&P 500 return to

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 27/59

We see WTI Oil ~$75/bbl. in a year (more less demand), but not without Asia slowi

Libya returning

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 28/59

G7 (U.S., U.K., Ger, Fr, It, Jap, Can)

Oil Demand, 1970-2010 (000s bbl.)

38% of world oil demand growing

at an average 0.4% y/y growth rate

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1 9 7 0

1 9 7 3

1 9 7 6

1 9 7 9

1 9 8 2

1 9 8 5

1 9 8 8

1 9 9 1

1 9 9 4

1 9 9 7

2 0 0 0

2 0 0 3

2 0 0 6

2 0 0 9

bbl. 000s/day

Non-G7 Country O

1970-2010 (000

62% of world oil dem

at an average 3.0% g

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

1 9 7 0

1 9 7 3

1 9 7 6

1 9 7 9

1 9 8 2

1 9 8 5

1 9 8 8

1 9 91

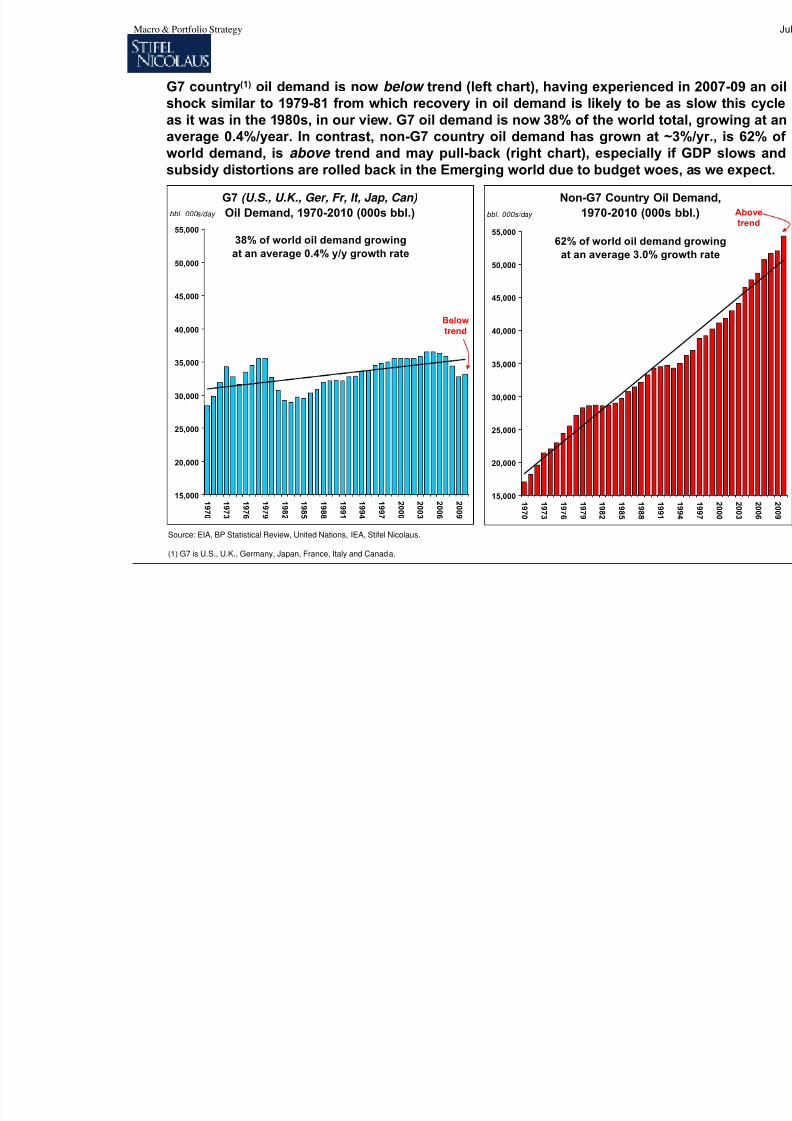

bbl. 000s/day

G7 country(1) oil demand is now below trend (left chart), having experienceshock similar to 1979-81 from which recovery in oil demand is likely to beas it was in the 1980s, in our view. G7 oil demand is now 38% of the world taverage 0.4%/year. In contrast, non-G7 country oil demand has grown at

world demand, is above trend and may pull-back (right chart), especiallysubsidy distortions are rolled back in the Emerging world due to budget wo

Source: EIA, BP Statistical Review, United Nations, IEA, Stifel Nicolaus.

(1) G7 is U.S., U.K., Germany, Japan, France, Italy and Canada.

Belowtrend

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 29/59

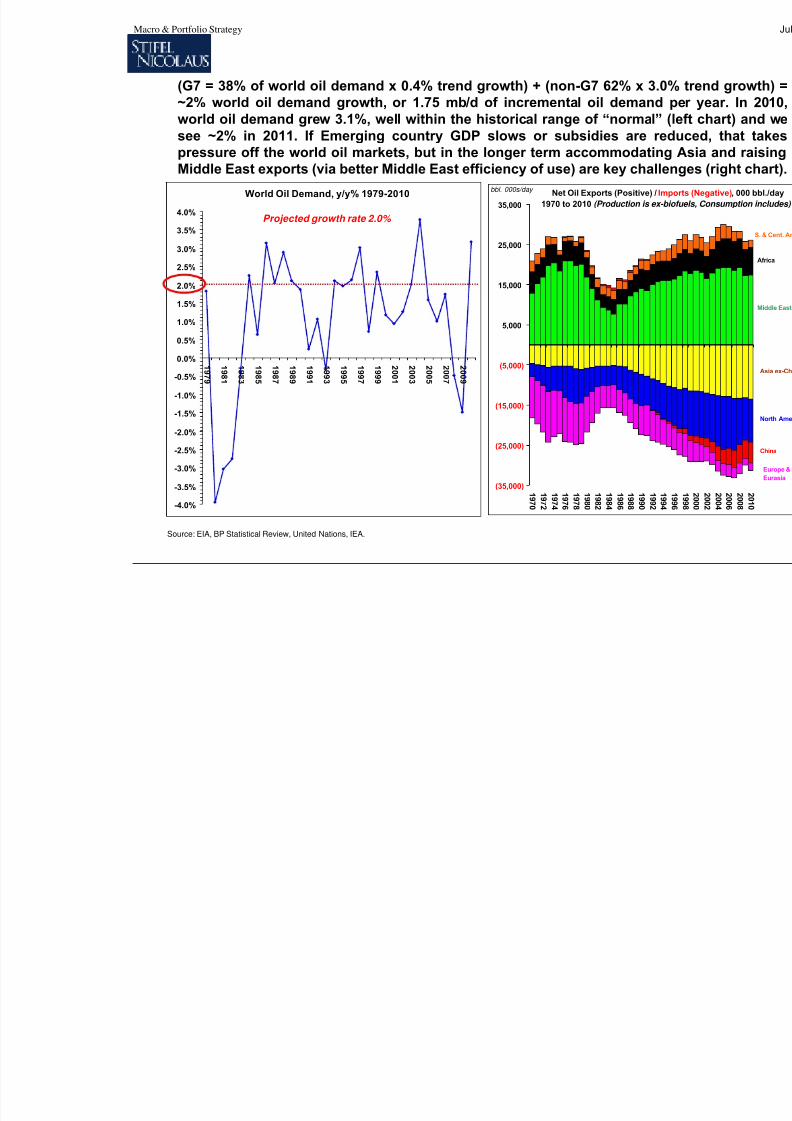

(G7 = 38% of world oil demand x 0.4% trend growth) + (non-G7 62% x 3.0~2% world oil demand growth, or 1.75 mb/d of incremental oil demandworld oil demand grew 3.1%, well within the historical range of “normal”see ~2% in 2011. If Emerging country GDP slows or subsidies are re

pressure off the world oil markets, but in the longer term accommodatinMiddle East exports (via better Middle East efficiency of use) are key chall

Source: EIA, BP Statistical Review, United Nations, IEA.

World Oil Demand, y/y% 1979-2010

Projected growth rate 2.0%

-4.0%

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1 9 7 9

1 9 8 1

1 9 8 3

1 9 8 5

1 9 8 7

1 9 8 9

1 9 9 1

1 9 9 3

1 9 9 5

1 9 9 7

1 9 9 9

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

2 0 0 9

Net Oil Exports (Positive) / Im

1970 to 2010 (Production is ex-

(35,000)

(25,000)

(15,000)

(5,000)

5,000

15,000

25,000

35,000

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 94

bbl. 000s/day

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 30/59

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 31/59

Nominal Trade-Weighted U.S.$ Major Currency Index, 1936 to Jun-2011 (Left) versus U.

share of global GDP expressed in PPP U.S. $, 1950 to 2011E (Right)

30

40

50

60

70

80

90

100

110

120

1 9 3 6

1 9 4 1

1 9 4 6

1 9 5 1

1 9 5 6

1 9 6 1

1 9 6 6

1 9 7 1

1 9 7 6

1 9 8 1

1 9 8 6

1 9 9 1

1 9 9 6

2 0 0 1

2 0 0 6

N o m i n a l t r a d e - w e i g h t e d U

. S . $

Bretton Woods

Agreementbegan U.S. dollar

ascent that we're

still unwinding; U.S.

share world GDP

peaks.

Emerging markets

reserves increase,

dollar rallies.

Fed tightens 1968-69, dollar

rallies, Martin -> Burns Fed

transition 1970, then

Bretton W oods abandoned.

Fed's Volcker hikes

rates sharply.

Source: U.S. GDP with a base year 1990 links the OECD Geary-Khamis 1950 to 1979 series to the IMF World Economic Outlook 1980 to data is from the U.S. Federal Reserve 1971 to present, for 1970 and prior we use R.L. Bidwell - “Currency Conversion Tables - 100 Years London, 1970, and B.R. Mitchell - British Historical Statistics - Cambridge Press, pp. 700-703. For trade weightings pre-1971 we use “HistStates, Colonial Times to 1970,” a U.S. Census publication.

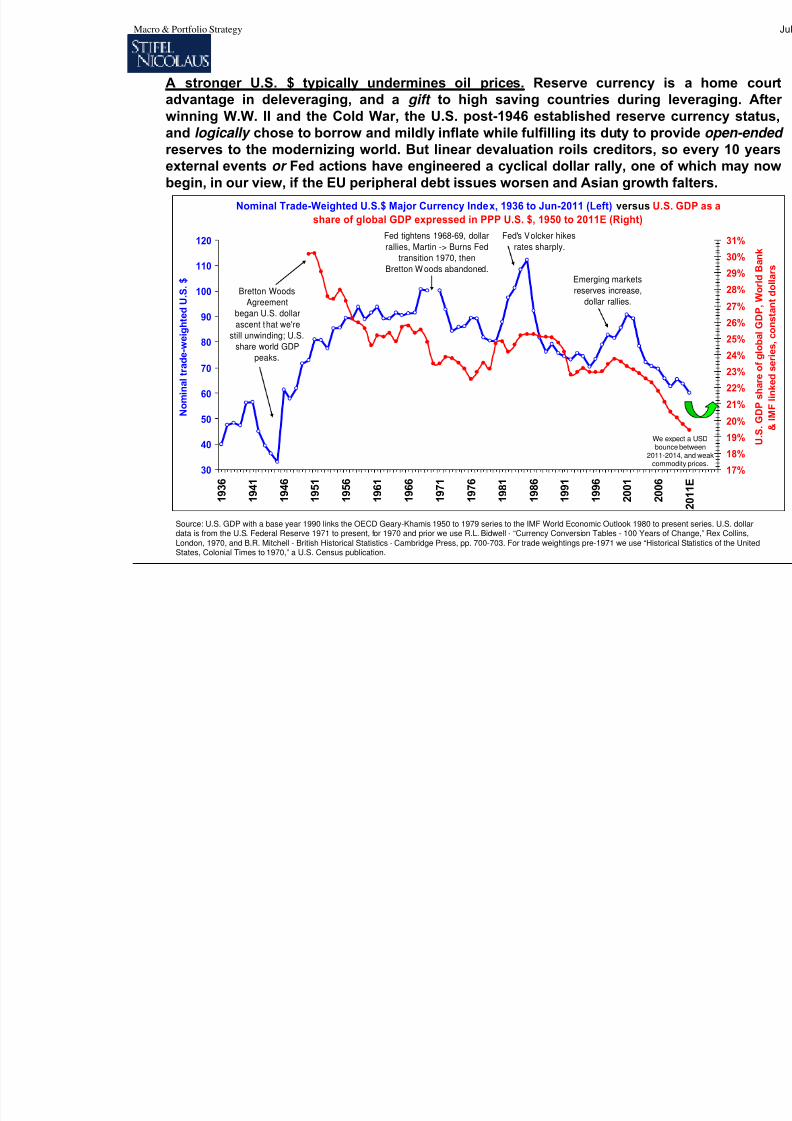

A stronger U.S. $ typically undermines oil prices. Reserve currency advantage in deleveraging, and a gift to high saving countries during winning W.W. II and the Cold War, the U.S. post-1946 established reserveand logically chose to borrow and mildly inflate while fulfilling its duty to pr

reserves to the modernizing world. But linear devaluation roils creditors, external events or Fed actions have engineered a cyclical dollar rally, one begin, in our view, if the EU peripheral debt issues worsen and Asian growt

Webo

2011com

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 32/59

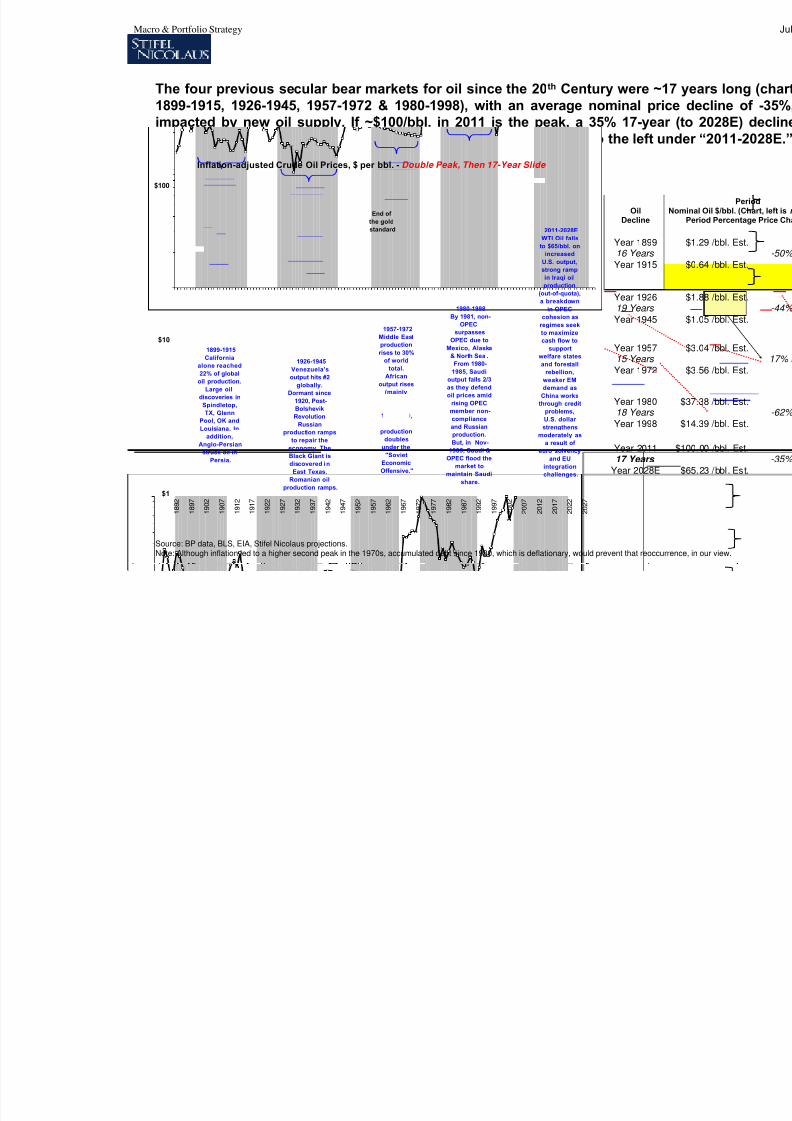

The four previous secular bear markets for oil since the 20th Century were ~1899-1915, 1926-1945, 1957-1972 & 1980-1998), with an average nominal primpacted by new oil supply. If ~$100/bbl. in 2011 is the peak, a 35% 17-yeawould take oil prices to $65/bbl for the reasons we list in the chart to the left u

Source: BP data, BLS, EIA, Stifel Nicolaus projections.Note: Although inflation led to a higher second peak in the 1970s, accumulated debt since 1980, which is deflationary, would prevent that reoccu

Inflation-adjusted Crude Oil Prices, $ per bbl. - Double Peak, Then 17-Year Slide

$1

$10

$100

1 8 9 2

1 8 9 7

1 9 0 2

1 9 0 7

1 9 1 2

1 9 1 7

1 9 2 2

1 9 2 7

1 9 3 2

1 9 3 7

1 9 4 2

1 9 4 7

1 9 5 2

1 9 5 7

1 9 6 2

1 9 6 7

1 9 7 2

1 9 7 7

1 9 8 2

1 9 8 7

1 9 9 2

1 9 9 7

2 0 0 2

2 0 0 7

2 0 1 2

2 0 1 7

2 0 2 2

2 0 2 7

1899-1915

California

alone reached

22% of global

oil production.

Large oil

discoveries in

Spindletop,

TX, Glenn

Pool, OK and

Louisiana. In

addition,

Anglo-Persian

struck oil inPersia.

1926-1945

Venezuela's

output hits #2

globally.

Dormant since

1920, Post-

Bolshevik

Revolution

Russian

production ramps

to repair the

economy. The

Black Giant isdiscovered i n

East Texas.

Romanian oil

production ramps.

1957-1972

Middle East

production

rises to 30%

of world

total.

African

output rises

(mainly

Libya).

Between

1955-1960,

Russian

production

doubles

under the

"SovietEconomic

Offensive."

1980-1998

By 1981, non-

OPEC

surpasses

OPEC due to

Mexico, Alaska

& North Sea .

From 1980-

1985, Saudi

output falls 2/3

as they defend

oil prices amid

rising OPEC

member non-

compliance

and Russian

production.

But, in Nov-

1985, Saudi &

OPEC flood the

market to

maintain Saudi

share.

End of

the gold

standard 2011-2028E

WTI Oil falls

to $65/bbl. on

increased

U.S. output,

strong ramp

in Iraqi oil

production

(out-of-quota),

a breakdownin OPEC

cohesion as

regimes seek

to maximize

cash flow to

support

welfare states

and forestall

rebellion,

weaker EM

demand as

China works

through credit

problems,

U.S. dollar

strengthens

moderately as

a result of

euro solvency

and EU

integration

challenges.

OilDecline

Year 189916 Years

Year 1915

Year 192619 Years

Year 1945

Year 195715 Years

Year 1972

Year 198018 Years

Year 1998

Year 201117 Years

Year 2028E

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 33/59

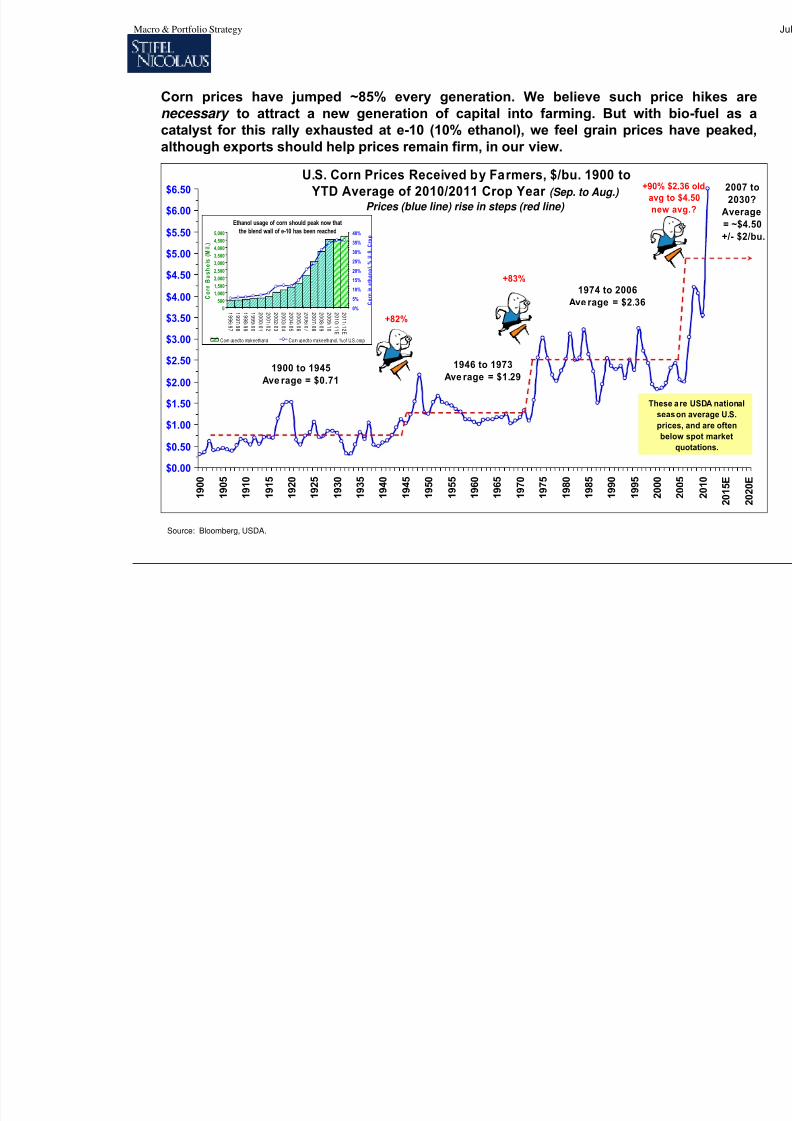

Corn prices have jumped ~85% every generation. We believe such prnecessary to attract a new generation of capital into farming. But with catalyst for this rally exhausted at e-10 (10% ethanol), we feel grain prices

although exports should help prices remain firm, in our view.

Source: Bloomberg, USDA.

U.S. Corn Prices Received by Farmers, $/bu. 1900 to YTD Average of 2010/2011 Crop Year (Sep. to Aug.)

Prices (blue line) rise in steps (red line)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50$4.00

$4.50

$5.00

$5.50

$6.00

$6.50

1 9 0 0

1 9 0 5

1 9 1 0

1 9 1 5

1 9 2 0

1 9 2 5

1 9 3 0

1 9 3 5

1 9 4 0

1 9 4 5

1 9 5 0

1 9 5 5

1 9 6 0

1 9 6 5

1 9 7 0

1 9 7 5

1 9 8 0

1 9 8 5

1 9 9 0

1 9 9 5

2 0 0 0

1900 to 1945

Ave rage = $0.71

1946 to 1973Ave rage = $1.29

1974 to 2006

Ave rage = $2.36

The

s

p

b

+82%

+83%

+90%

avg

ne

Ethanol usage of corn should peak now that

the blend wall of e-10 has been reached

0500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1 9 9 6 / 9 7

1 9 9 7 / 9 8

1 9 9 8 / 9 9

1 9 9 9 / 0 0

2 0 0 0 / 0 1

2 0 0 1 / 0 2

2 0 0 2 / 0 3

2 0 0 3 / 0 4

2 0 0 4 / 0 5

2 0 0 5 / 0 6

2 0 0 6 / 0 7

2 0 0 7 / 0 8

2 0 0 8 / 0 9

2 0 0 9 / 1 0

2 0 1 0 / 1 1 E

2 0 1 1 / 1 2 E

C o r n

B u s h e l s ( M i l . )

0%

5%

10%

15%

20%

25%

30%

35%

40%

C o r n

i n

e t h a n o l , %

U . S .

C r o p

Corn used to make ethanol Corn used to make ethanol, % of U.S. crop

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 34/59

100

1000

10000

1 9 0 4

1 9 0 7

1 9 1 0

1 9 1 3

1 9 1 6

1 9 1 9

1 9 2 2

1 9 2 5

1 9 2 8

1 9 3 1

1 9 3 4

1 9 3 7

1 9 4 0

1 9 4 3

1 9 4 6

1 9 4 9

1 9 5 2

1 9 5 5

1 9 5 8

1 9 6 1

1 9 6 4

1 9 6 7

1 9 7 0

1 9 7 3

1 9 7 6

1 9 7 9

1 9 8 2

1 9 8 5

I r o n o r e p r o d u c e d ,

m i l . m e t r i c t o n n e s

World iron ore production, left axis World per capita iron ore pr

World Annual Production of Iron Ore

Absolute and Per Capita, 1904-2010E

100

1000

1 9 4 5

1 9 4 7

1 9 4 9

1 9 5 1

1 9 5 3

1 9 5 5

1 9 5 7

1 9 5 9

1 9 6 1

1 9 6 3

1 9 6 5

1 9 6 7

1 9 6 9

1 9 7 1

1 9 7 3

1 9 7 5

I r o n o r e p r o d u c e d , m i l . m e t r i c t o n n e s

0.05

0.07

0.09

0.11

0.13

0.15

0.17

0.19

0.21

0.23

0.25

T on s p er c a pi t a pr o d u c t i on

World iron ore production, left axis

World per capita iron ore production, right axis

World Annual Production of Iron Ore

Absolute and Per Capita, 1945-1975

1000

10000

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0 E

2 0 1 2 E

2 0 1 4 E

I r o n o r e p r o d u c e d , m i l . m e t r i c t o n n e s

World iron ore p

World per ca pita

World Annual P

Absolute and P

1 9 4 6 - 5 4 C A G R

1 3 %

2 0 0 2 - 1 0

C A G R

1 0 %

1 9 5 4

- 7 5 C A G R

4 %

Post-WW2 were8 strong years

for infrastructure,followed by

cyclical growth.

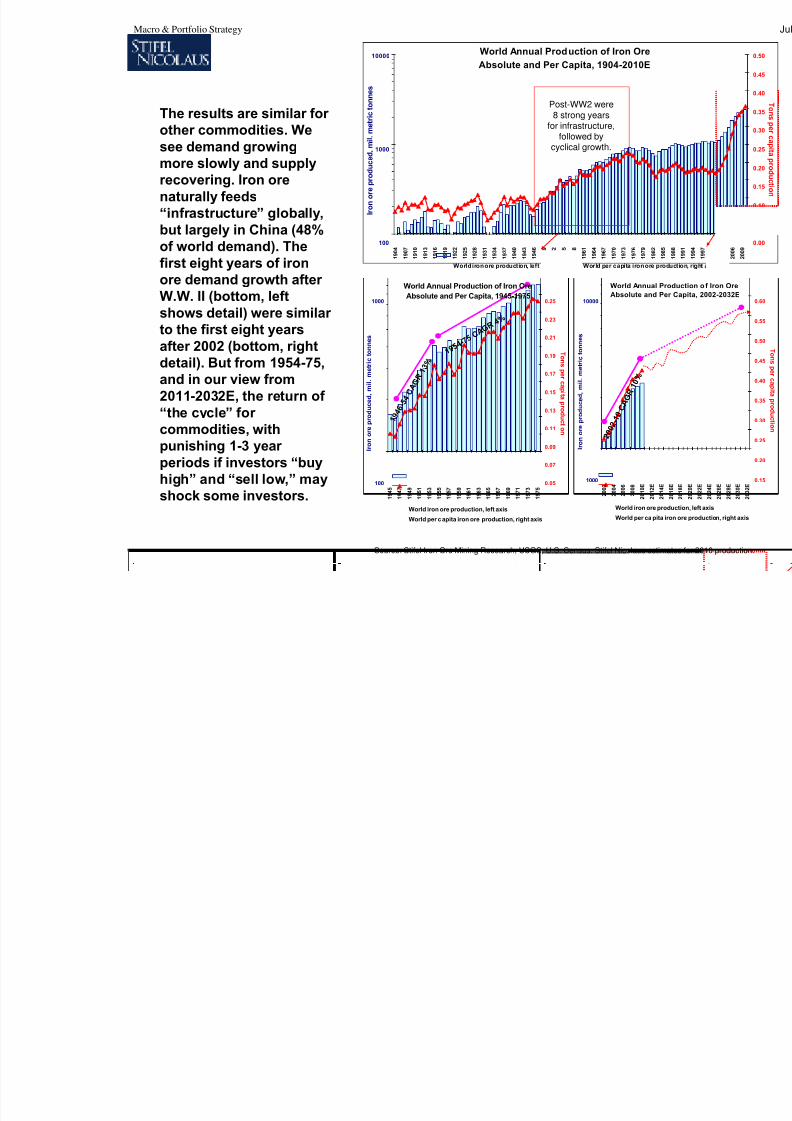

The results are similar for other commodities. We

see demand growingmore slowly and supplyrecovering. Iron orenaturally feeds“infrastructure” globally,but largely in China (48%of world demand). Thefirst eight years of ironore demand growth after

W.W. II (bottom, leftshows detail) were similar to the first eight yearsafter 2002 (bottom, rightdetail). But from 1954-75,and in our view from2011-2032E, the return of “the cycle” for commodities, withpunishing 1-3 year periods if investors “buyhigh” and “sell low,” mayshock some investors.

Source: Stifel Iron Ore Mining Research, USGS, U.S. Census. Stifel Nicolaus estim

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 35/59

Since commodities have become a financial should be subject to/pressured by a monetary

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 36/59

150

200

250

300

350

400

450

500

550

600

650

700

750

A u g - 9

8

F e b - 9

9

A u g - 9

9

F e b - 0

0

A u g - 0

0

F e b - 0

1

A u g - 0

1

F e b - 0

2

A u g - 0

2

F e b - 0

3

A u g - 0

3

F e b - 0

4

A u g - 0

4

F e b 0 5

Commodity Prices (CRB FCommodity

Daily prices 10/14/19

Cg

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

$13,000

$14,000

$15,000

J a n - 8 1

J a n - 8 2

J a n - 8 3

J a n - 8 4

J a n - 8 5

J a n - 8 6

J a n - 8 7

J a n - 8 8

J a n - 8 9

J a n - 9 0

J a n - 9 1

J a n - 9 2

J a n - 9 3

J a n - 9 4

J a n - 9 5

J a n - 9 6

J a n - 9 7

J a n - 9 8

J a n - 9 9

J a n - 0 0

J a n - 0 1

J a n - 0 2

J a n - 0 3

J a n - 0 4

J a n - 0 5

J a n - 0 6

J a n - 0 7

J a n - 0 8

J a n - 0 9

J a n - 1 0

J a n - 1 1

Growth of Components of U.S. M3 Money Supply ($ bil.)

Institutional Mone yFunds

Eurodollars

Repos

Large-Time Deposits

Retail Money Funds

Small Denom. TimeDeposits

Savings Deposits

Demand & Other

Check Deposits

Currency & TravelersChecks

M2 = Below

Sum = M3

M1 = Below

Deng currencyreforms in China,Mexican Peso &

Asian debt crises.

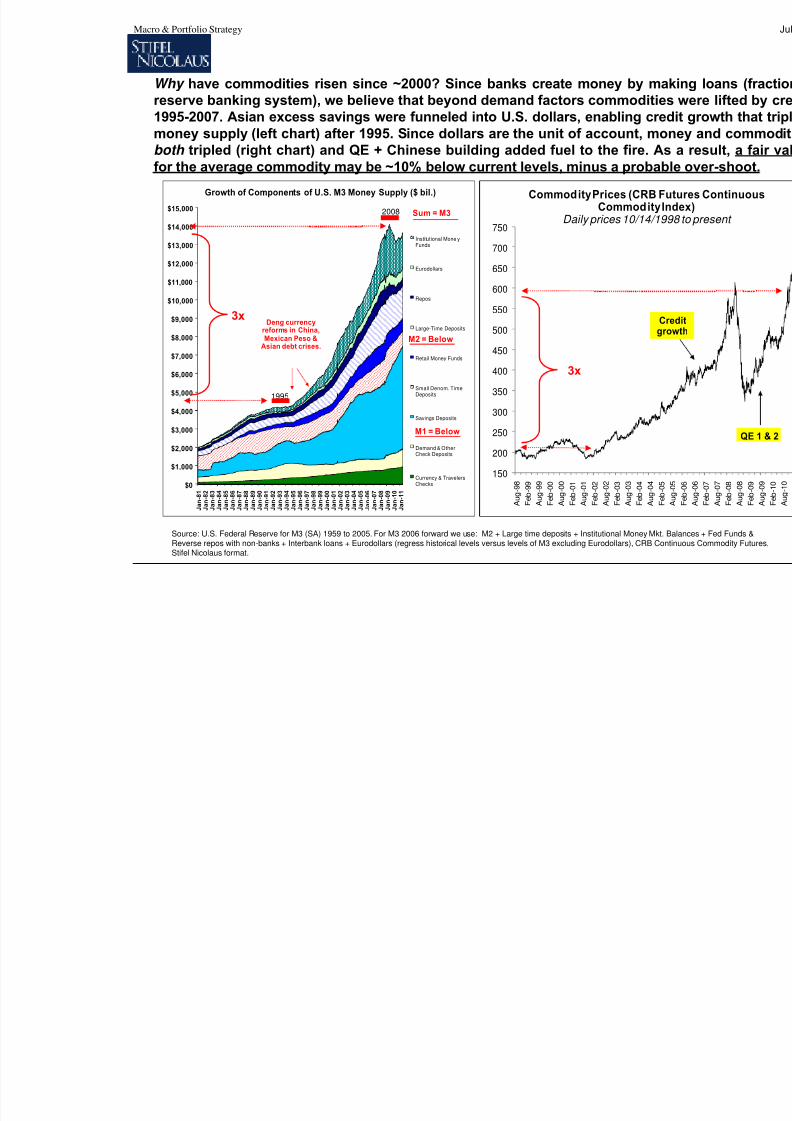

Why have commodities risen since ~2000? Since banks create money by mreserve banking system), we believe that beyond demand factors commoditie1995-2007. Asian excess savings were funneled into U.S. dollars, enabling cremoney supply (left chart) after 1995. Since dollars are the unit of account, mo

both tripled (right chart) and QE + Chinese building added fuel to the fire. Afor the average commodity may be ~10% below current levels, minus a proba

Source: U.S. Federal Reserve for M3 (SA) 1959 to 2005. For M3 2006 forward we use: M2 + Large time deposits + Institutional Money MktReverse repos with non-banks + Interbank loans + Eurodollars (regress historical levels versus levels of M3 excluding Eurodollars), CRB CoStifel Nicolaus format.

3x

1995

3x

2008

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 37/59

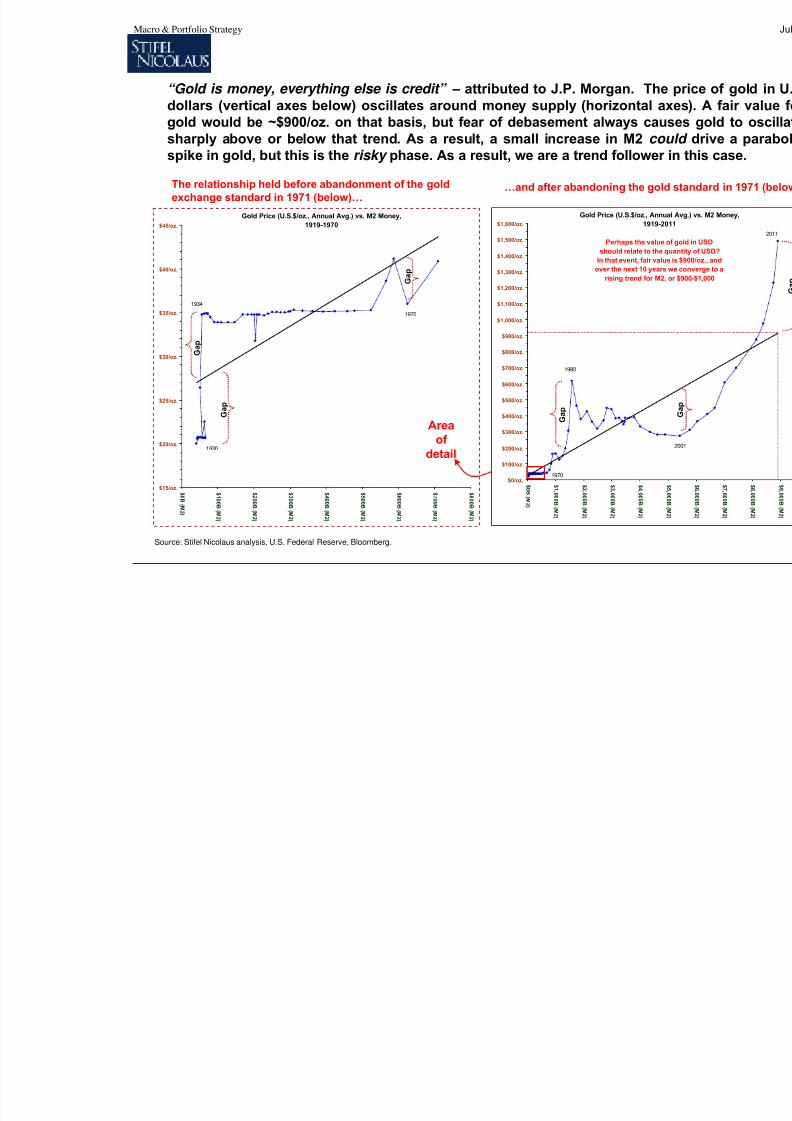

“Gold is money, everything else is credit” – attributed to J.P. Morgan. Thedollars (vertical axes below) oscillates around money supply (horizontal agold would be ~$900/oz. on that basis, but fear of debasement always causharply above or below that trend. As a result, a small increase in M2 co

spike in gold, but this is the risky phase. As a result, we are a trend follower

Source: Stifel Nicolaus analysis, U.S. Federal Reserve, Bloomberg.

Gold Price (U.S.$/oz., Ann

1919-2

Perhaps the value

should relate to the

In that event, fair val

over the next 10 year

rising trend for M2

$0/oz.

$100/oz.

$200/oz.

$300/oz.

$400/oz.

$500/oz.

$600/oz.

$700/oz.

$800/oz.

$900/oz.

$1,000/oz.

$1,100/oz.

$1,200/oz.

$1,300/oz.

$1,400/oz.

$1,500/oz.

$1,600/oz.

$ 0 B

( M2 )

$ 1 , 0 0 0 B

( M2 )

$ 2 , 0 0 0 B

( M2 )

$ 3 , 0 0 0 B

( M2 )

$ 4 , 0 0 0 B

( M2 )

1980

1970

Gold Price (U.S.$/oz., Annual Avg.) vs. M2 Money,

1919-1970

$15/oz.

$20/oz.

$25/oz.

$30/oz.

$35/oz.

$40/oz.

$45/oz.

$ 0 B

( M2 )

$ 1 0 0 B

( M2 )

$ 2 0 0 B

( M2 )

$ 3 0 0 B

( M2 )

$ 4 0 0 B

( M2 )

$ 5 0 0 B

( M2 )

$ 6 0 0 B

( M2 )

$ 7 0 0 B

( M2 )

$ 8 0 0 B

( M2 )

1934

1970

1930

Areaof

detail

G a p

G a p

G a p

G a p

The relationship held before abandonment of the goldexchange standard in 1971 (below)…

…and after abandoning the go

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 38/59

$0/bbl.

$1/bbl.

$1/bbl.

$2/bbl.

$2/bbl.

$3/bbl.

$3/bbl.

$4/bbl.

$4/bbl.

$5/bbl.

$ 0 B ( M2 )

$ 1 0 0 B ( M2 )

$ 2 0 0 B ( M2 )

$ 3 0 0 B ( M2 )

$ 4 0 0 B ( M2 )

$ 5 0 0 B ( M2 )

$ 6 0 0 B ( M2 )

$ 7 0 0 B ( M2 )

Oil Price (U.S.$/bbl., Annual Avg.) vs. M2 Money,1919-1970

1968

1949

1960

1945

1920

1931

$0/bbl.

$10/bbl.

$20/bbl.

$30/bbl.

$40/bbl.

$50/bbl.

$60/bbl.

$70/bbl.

$80/bbl.

$90/bbl.

$100/bbl.

$110/bbl.

$ 0 B ( M2 )

$ 1 , 0 0 0 B ( M2 )

$ 2 , 0 0 0 B ( M2 )

$ 3 , 0 0 0 B ( M2 )

$ 4 , 0 0 0 B ( M2 )

Oil Price (U.S.$/Bbl., Annua1919-20

1998

1980

Area of detail

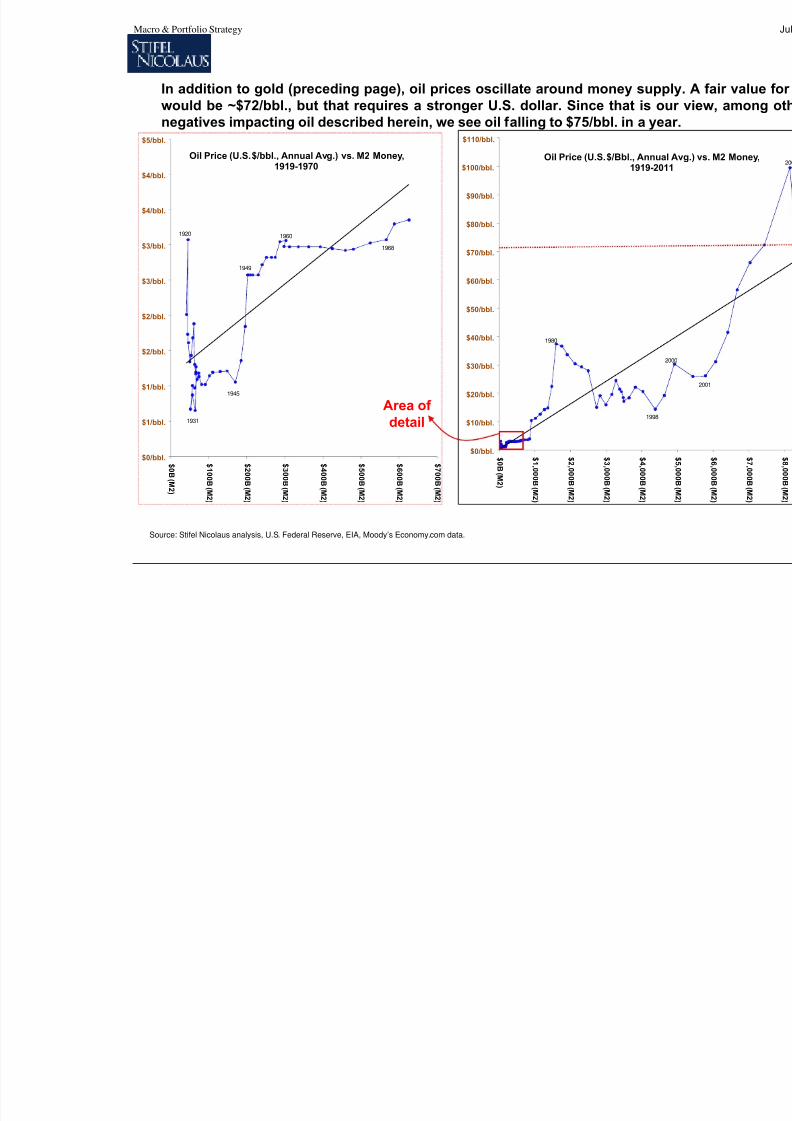

In addition to gold (preceding page), oil prices oscillate around money supwould be ~$72/bbl., but that requires a stronger U.S. dollar. Since that is onegatives impacting oil described herein, we see oil falling to $75/bbl. in a ye

Source: Stifel Nicolaus analysis, U.S. Federal Reserve, EIA, Moody’s Economy.com data.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 39/59

The frightening scenario – is the commmarket signaling a 20% S&P 500 bear m

April-August 2011?

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 40/59

$0

$50

$100

$150

$200

$250

$300

$350

$400

1 / 3 / 1 9

2 1

1 / 3 / 1 9

2 2

1 / 3 / 1 9

2 3

1 / 3 / 1 9

2 4

1 / 3 / 1 9

2 5

1 / 3 / 1 9

2 6

1 / 3 / 1 9

2 7

1 / 3 / 1 9

2 8

1 / 3 / 1 9

2 9

1 / 3 / 1 9

3 0

1 / 3 / 1 9

3 1

1 / 3 / 1 9

3 2

1 / 3 / 1 9

3 3

1 / 3 / 1 9

3 4

1 / 3 / 1 9

3 5

1 / 3 / 1 9

3 6

Dow Jones Industrial Average,1/3/1921-12/31/1936

2

1

3

Fail

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1 / 2 / 1 9

8 5

1 / 2 / 1 9

8 6

1 / 2 / 1 9

8 7

1 / 2 / 1 9

8 8

1 / 2 / 1 9

8 9

1 / 2 / 1 9

9 0

1 / 2 / 1 9

9 1

1 / 2 / 1 9

9 2

1 / 2 / 1 9

9 3

1 / 2 / 1 9

9 4

1 / 2 / 1 9

9 5

1 / 2 / 1 9

9 6

Nikkei 225,1/2/1985 - 12/30/1996

2

1

3

Fail

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1 2 / 1 / 9 4

1 2 / 1 / 9 5

1 2 / 1 / 9 6

1

$0

$20

$40

$60

$80

$100

$120

$140

$160

1 / 2 / 1 9 9 7

1 / 2 / 1 9 9 8

1 / 2 / 1 9 9 9

1 / 2 / 2 0 0 0

1 / 2 / 2 0 0 1

1 / 2 / 2 0 0 2

1 / 2 / 2 0 0 3

1 / 2 / 2 0 0 4

1 / 2 / 2 0 0 5

1 / 2 / 2 0 0 6

1 / 2 / 2 0 0 7

1 / 2 / 2 0 0 8

1 / 2 / 2 0 0 9

1 / 2 / 2 0 1 0

WTI Oil,1/2/1998 - 12/31/2010

2

1

3Fail

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1 2 / 3 0

1 2 / 3 0

1 2 / 3 0

1 2 / 3 0

$100

$200

$300

$400

$500

$600

$700

$800

$900

0 1 / 2 6 / 7 8

0 5 / 2 6 / 7 8

0 9 / 2 6 / 7 8

0 1 / 2 6 / 7 9

0 5 / 2 6 / 7 9

0 9 / 2 6 / 7 9

0 1 / 2 6 / 8 0

0 5 / 2 6 / 8 0

0 9 / 2 6 / 8 0

0 1 / 2 6 / 8 1

0 5 / 2 6 / 8 1

0 9 / 2 6 / 8 1

Gold Price $/oz. 1980 Bubble

2/1/78 - 1/31/82

2

1

3Fail

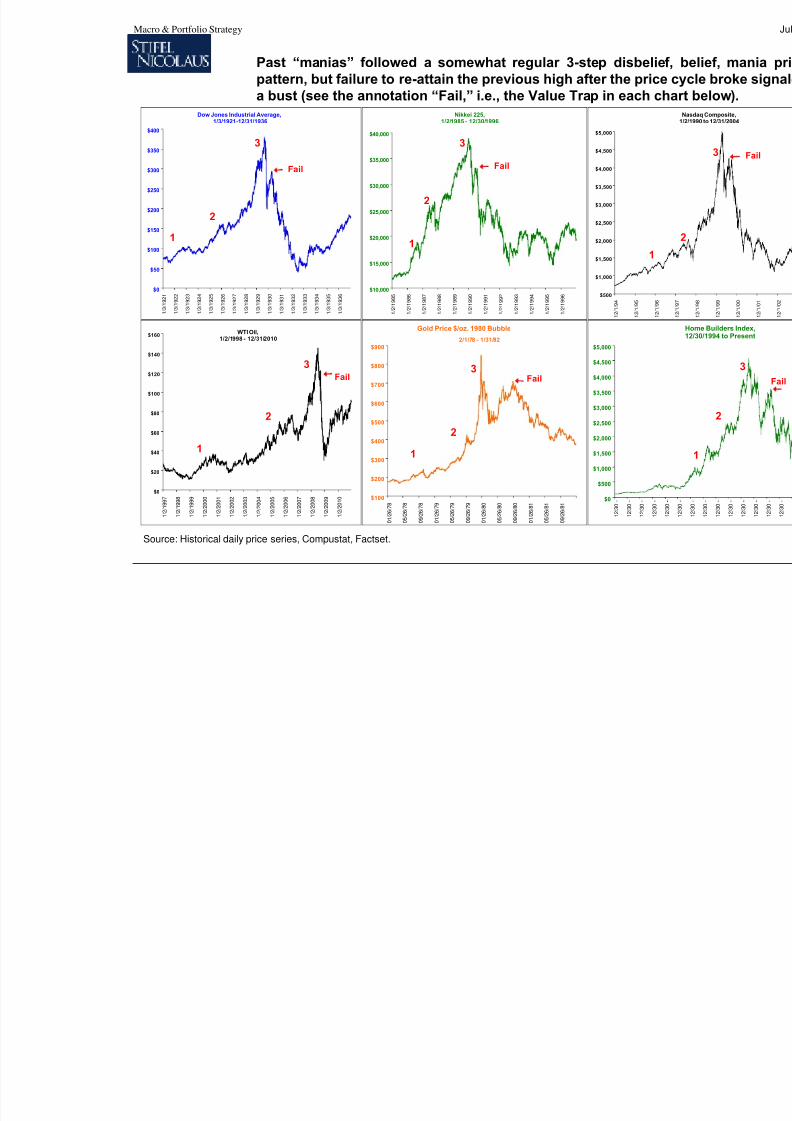

Past “manias” followed a somewhat regular 3-step disbeliepattern, but failure to re-attain the previous high after the pricea bust (see the annotation “Fail,” i.e., the Value Trap in each c

Source: Historical daily price series, Compustat, Factset.

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 41/59

100

150

200

250

300

350

400

450

500

550

600

650

700

A u g - 9 8

F e b - 9 9

A u g - 9 9

F e b - 0 0

A u g - 0 0

F e b - 0 1

A u g - 0 1

F e b - 0 2

A u g - 0 2

F e b - 0 3

A u g - 0 3

F e b - 0 4

A u g - 0 4

F e b - 0 5

Commodity Prices (CRB FuCommodity In

Daily prices 10/14/19

D I S B

E L I E F

B E L I E F

G

R E E D

I N E V I T A B L E B U S T

D I M I N I S H I N G R E T U R N S B O T T O M T O T O P

“SECULAR” BULLMARKET STAGES

Source: Stifel Nicolaus, CRB Futures from Factset.

B E A

R

T R A P

B U L L

T R A P

V A L U

E

T R A P

D I S B

E L I E F

B E L I E F

B E A

R

T R A P

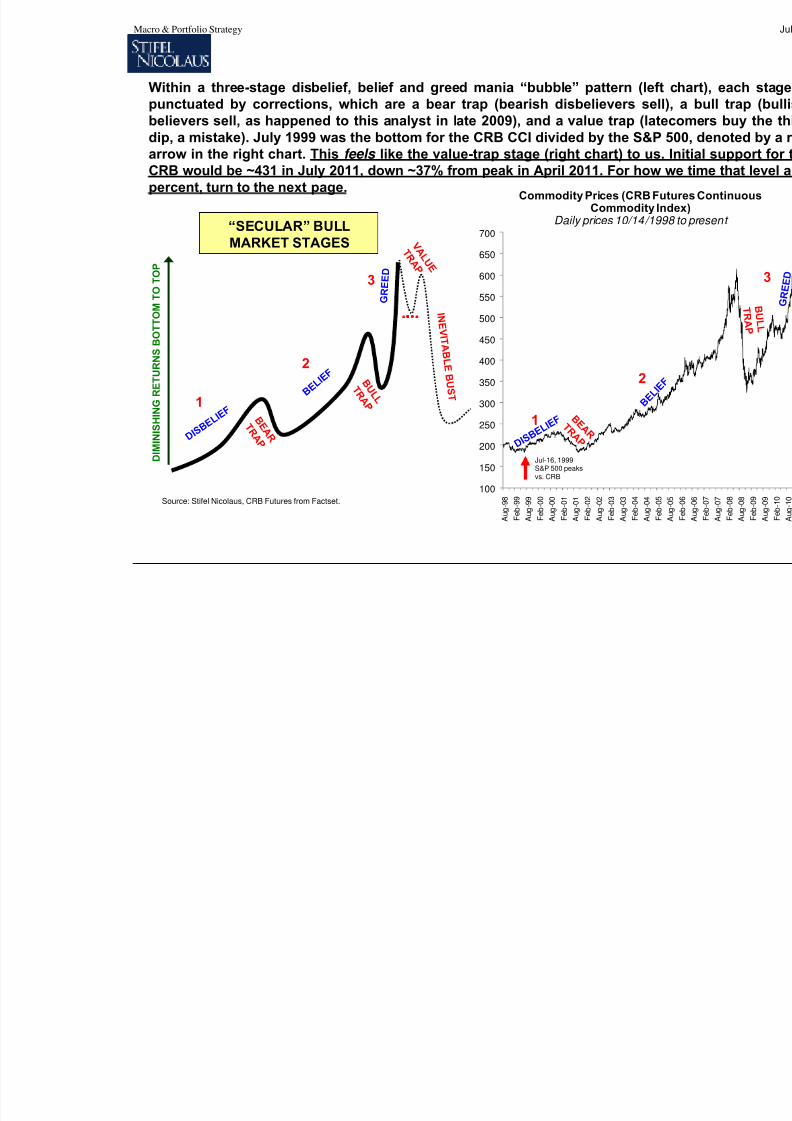

Within a three-stage disbelief, belief and greed mania “bubble” pattern (leftpunctuated by corrections, which are a bear trap (bearish disbelievers selbelievers sell, as happened to this analyst in late 2009), and a value trap (latdip, a mistake). July 1999 was the bottom for the CRB CCI divided by the S&P

arrow in the right chart. This feels like the value-trap stage (right chart) to usCRB would be ~431 in July 2011, down ~37% from peak in April 2011. For howpercent, turn to the next page.

Jul-16, 1999S&P 500 peaksvs. CRB

1

2

3

1

2

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 42/59

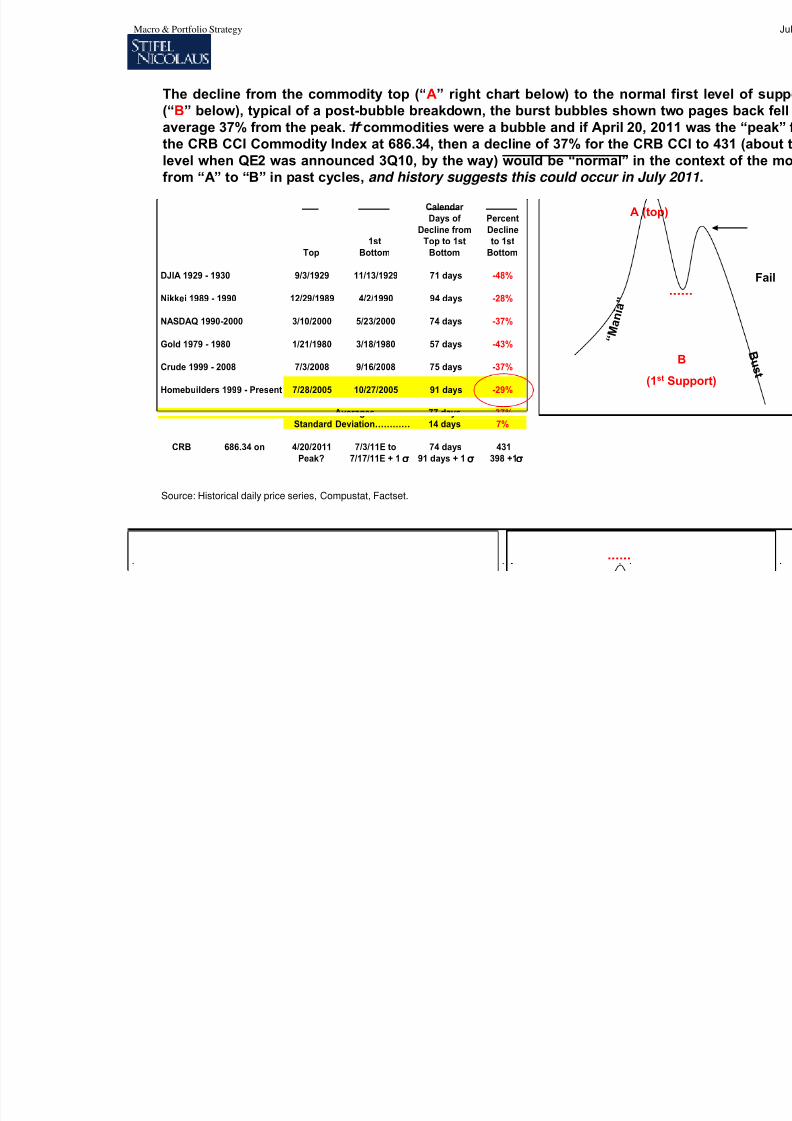

The decline from the commodity top (“A” right chart below) to the norma(“B” below), typical of a post-bubble breakdown, the burst bubbles shown taverage 37% from the peak. If commodities were a bubble and if April 20, 20the CRB CCI Commodity Index at 686.34, then a decline of 37% for the CRBlevel when QE2 was announced 3Q10, by the way) would be “normal” in thfrom “A” to “B” in past cycles, and history suggests this could occur in July

Source: Historical daily price series, Compustat, Factset.

Calendar Days of Percent

Decline from Decline1st Top to 1st to 1st

Top Bottom Bottom Bottom

DJIA 1929 - 1930 9/3/1929 11/13/1929 71 days -48%

Nikkei 1989 - 1990 12/29/1989 4/2/1990 94 days -28%

NASDAQ 1990-2000 3/10/2000 5/23/2000 74 days -37%

Gold 1979 - 1980 1/21/1980 3/18/1980 57 days -43%

Crude 1999 - 2008 7/3/2008 9/16/2008 75 days -37%

Homebuilders 1999 - Present 7/28/2005 10/27/2005 91 days -29%

77 days -37%14 days 7%

CRB 686.34 on 4/20/2011 7/3/11E to 74 days 431

Peak? 7/17/11E + 1 91 days + 1 398 +1

Averages…………Standard Deviation…………

σ σ σ

A (top

(1st

“ M

a n i a ”

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 43/59

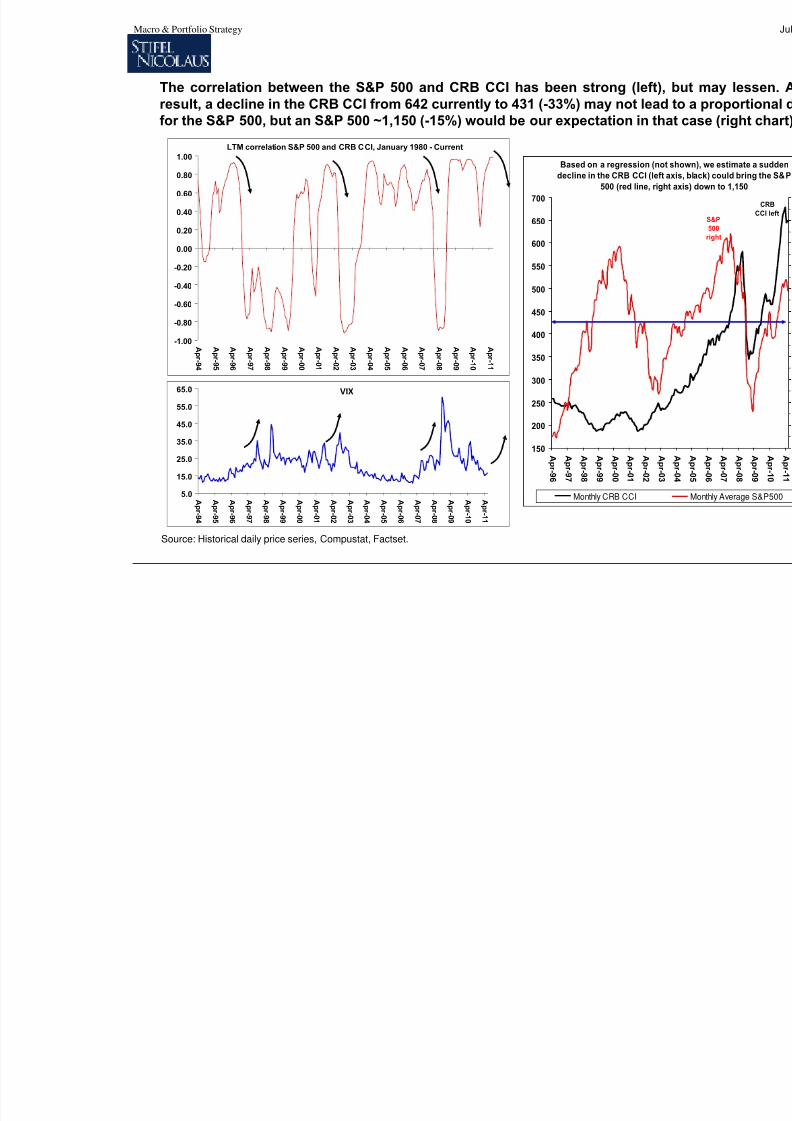

The correlation between the S&P 500 and CRB CCI has been strong (left)result, a decline in the CRB CCI from 642 currently to 431 (-33%) may not leafor the S&P 500, but an S&P 500 ~1,150 (-15%) would be our expectation in th

Source: Historical daily price series, Compustat, Factset.

LTM correlation S&P 500 and CRB CCI, January 1980 - Current

-1.00

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

A pr - 9 4

A pr - 9 5

A pr - 9 6

A pr - 9 7

A pr - 9 8

A pr - 9 9

A pr - 0 0

A pr - 0 1

A pr - 0 2

A pr - 0 3

A pr - 0 4

A pr - 0 5

A pr - 0 6

A pr - 0 7

A pr - 0 8

A pr - 0 9

A pr -1 0

A pr -1 1

VIX

5.0

15.0

25.0

35.0

45.0

55.0

65.0

A pr - 9 4

A pr - 9 5

A pr - 9 6

A pr - 9 7

A pr - 9 8

A pr - 9 9

A pr - 0 0

A pr - 0 1

A pr - 0 2

A pr - 0 3

A pr - 0 4

A pr - 0 5

A pr - 0 6

A pr - 0 7

A pr - 0 8

A pr - 0 9

A pr -1 0

A pr -1 1

Based on a regression (no

decline in the CRB CCI (lef

500 (red line, rig

150

200

250

300

350

400

450

500

550

600

650

700

A pr - 9 6

A pr - 9 7

A pr - 9 8

A pr - 9 9

A pr - 0 0

A pr - 0 1

A pr - 0 2

A pr- 0 3

Monthly CRB CCI

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 44/59

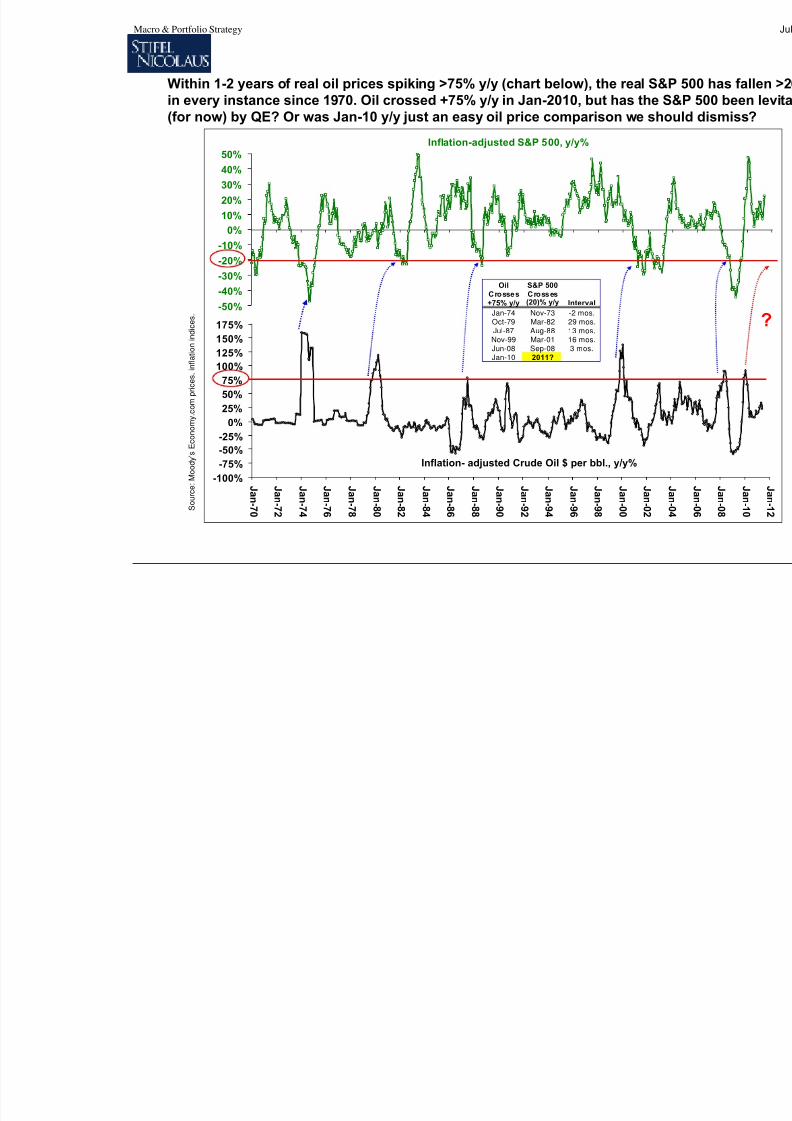

Within 1-2 years of real oil prices spiking >75% y/y (chart below), the real S&in every instance since 1970. Oil crossed +75% y/y in Jan-2010, but has the (for now) by QE? Or was Jan-10 y/y just an easy oil price comparison we sh

S o u r c e :

M o o

d y ’ s

E c o n o m y . c

o m

p r i c e s ,

i n f l a t i o n

i n d i c e s .

Inflation-adjusted S&P 500, y/y%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

Inflation- adjusted Crude Oil $ per bbl., y/y%

-100%

-75%-50%

-25%

0%

25%

50%

75%

100%

125%

150%

175%

J an-7 0

J an-7 2

J an-7 4

J an-7 6

J an-7 8

J an- 8 0

J an- 8 2

J an- 8 4

J an- 8 6

J an- 8 8

J an- 9 0

J an- 9 2

J an- 9 4

J an- 9 6

J an- 9 8

J an- 0 0

J an- 0 2

Oil S&P 500Crosses Crosses

+75% y/y (20)% y/y IntervalJan-74 Nov-73 -2 mos.Oct-79 Mar-82 29 mos.Jul-87 Aug-88 13 mos.Nov-99 Mar-01 16 mos.Jun-08 Sep-08 3 mos.Jan-10 2011?

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 45/59

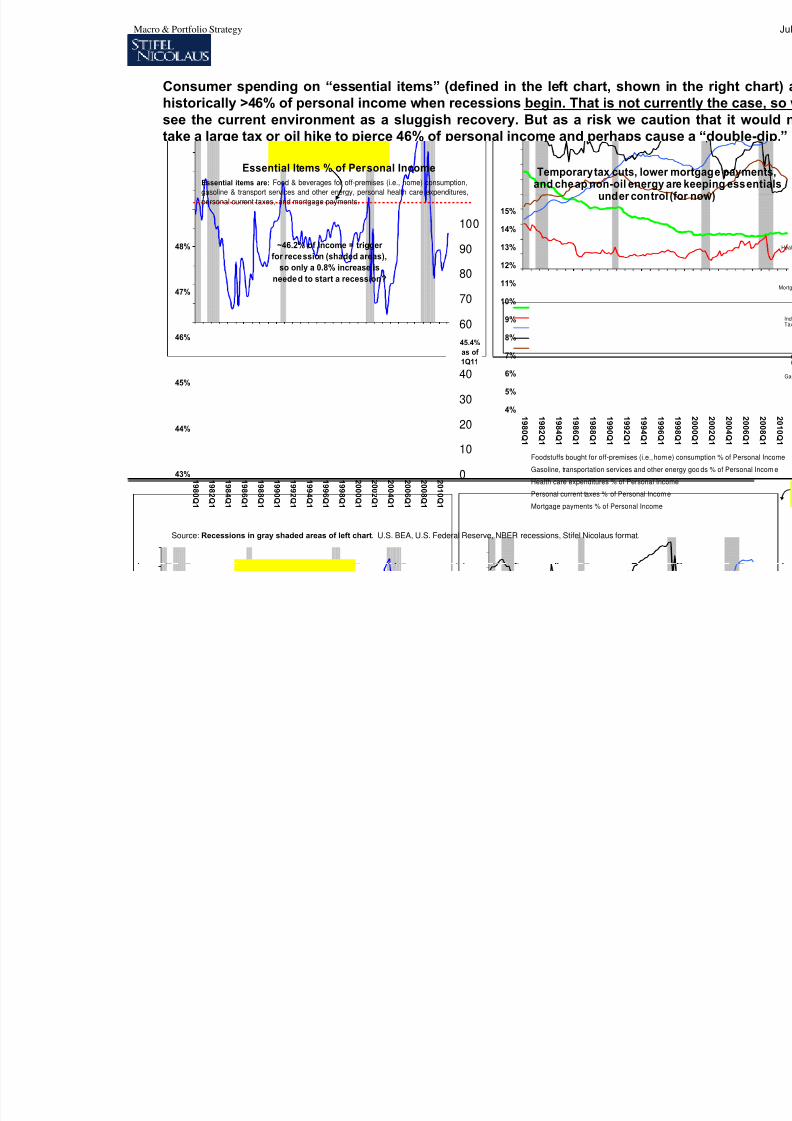

Consumer spending on “essential items” (defined in the left chart, shown historically >46% of personal income when recessions begin. That is not cusee the current environment as a sluggish recovery. But as a risk we cautake a large tax or oil hike to pierce 46% of personal income and perhaps ca

Source: Recessions in gray shaded areas of left chart. U.S. BEA, U.S. Federal Reserve, NBER recessions, Stifel Nicolaus format.

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

1 9 8 0 Q1

1 9 8 2 Q1

1 9 8 4 Q1

1 9 8 6 Q1

1 9 8 8 Q1

1 9 9 0 Q1

1 9 9 2 Q1

1 9 9 4 Q1

1 9 9 6 Q1

Temporary tax cuts, loweand cheap non-oil energy

under contro

Foodstuffs bought for off-premises (i.e., ho

Gasoline, transportation services and othe

Health care expenditures % of Personal In

Personal current taxes % of Personal Inco

Mortgage payments % of Personal Income

Essential Items % of Personal Income

43%

44%

45%

46%

47%

48%

1 9 8 0 Q1

1 9 8 2 Q1

1 9 8 4 Q1

1 9 8 6 Q1

1 9 8 8 Q1

1 9 9 0 Q1

1 9 9 2 Q1

1 9 9 4 Q1

1 9 9 6 Q1

1 9 9 8 Q1

2 0 0 0 Q1

2 0 0 2 Q1

2 0 0 4 Q1

2 0 0 6 Q1

2 0 0 8 Q1

2 0 1 0 Q1

010

20

30

40

50

60

70

80

90

100

Essential items are: Food & beverages for off-premises (i.e., home) consumption,

gasoline & transport services and other energy, personal health care expenditures,

personal current taxes, and mortgage payments.

~46.2% of Income = trigger

for recession (shaded areas),

so only a 0.8% increase is

needed to start a recession?

45.4%

as of

1Q11

Macro & Portfolio Strategy

8/6/2019 Bannister - Stifel Nicolaus Mid-2011 Macro Outlook

http://slidepdf.com/reader/full/bannister-stifel-nicolaus-mid-2011-macro-outlook 46/59

Fed & Treasury are brilliantly converting a “Depr

debt work-out; we see the 10-year near 4% wi

Faced with the same debt deflation issues as 1929-33 the in 2008-11 responded with every tool not available in 1929

(a) a fiat reserve currency,

(b) unused federal debt capacity,(c) relatively open global labor markets (d) knowledge the democratic U.S. could survive unemplo(e) …knowledge that the Communist Chinese regime coul

U.S. policymakers have chosen to let the air debt out of thborrowing GDP from the future to avoid uncontrolled liqui

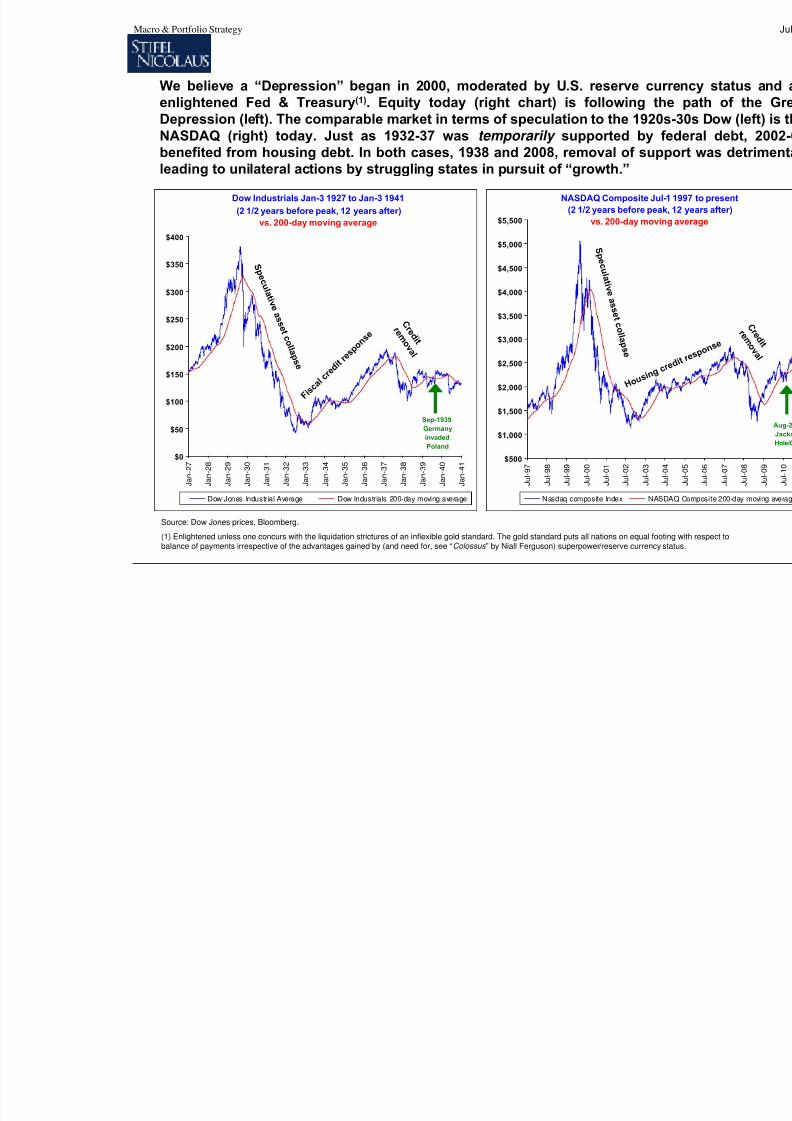

Macro & Portfolio Strategy