bankruptcy outline

TRANSCRIPT

09/08/2003

I. If this is a money obligation, and there is not enough to go around. Establishes the boundary line for how hard the creditor can squeeze. Also, boundary line of how long the creditor can squeeze. When there are several creditors all vying for the same pool of assets, which one comes first.

II. Article I, Section 8 provides that Congress can establish a uniform law of bankruptcies. a. Constitution usually has no commercial provisions to it.b. Bankruptcy has a checkered history. Tell you a little bit about the fortunes of the people who signed

the declaration of independence. c. 1898: first bankruptcy law that is fixed.

i. Substantially amended in 1903 that gets more balance in itii. Also substantially amended during the depression.

1. Repayment element of bankruptcyiii. Amended in 1970’s: 1973 commission recommends lots of changes. Bankruptcy act of 1978

—goes into effect 1979.d. In 1984, more creditor provisions and other business provision. In 1986, a new provision was added

for family farmers (Chapter 12). e. In 1994, pursuant to credit industry, got what we’ll do is appoint another commission.

i. Results in commission report in 1997. As bankruptcy becomes more polarized, in October ’97, the credit industry said was dead on arrival. So congress put in credit versions to Congress.

1. Congress that adjourned in ’98, passed in house but not senate.2. Clinton vetoed in 2000.

III. Bankruptcy is a course in corporate refinance. This is where any business in financial trouble looks (11 U.S.C. ). What would happen if this business files for Chapter 11? Businesses who get into financial trouble and decide not to and go to creditors instead to work something out in corporate refinance. a. If this went into Bankruptcy, here are what my rights might be. The second way that it is important in

corporate refinance and as more companies have become more leveraged. What has begun happening is that as more deals come about, the more sophisticated players try to figure out what the bankruptcy position is. If at different points down the time line and the other party to the deal collapse, how much could you still squeeze, leverage, and get services or could you back away cleanly to find other sources for goods/services.

b. Bankruptcy has now moved transnationally. c. Bankruptcy established a framework for negotiation.

i. When Maxwell (publisher) collapsed financially a few years back with the suicide of the CEO and financial troubles, where did it file for bankruptcy. It was a UK company but had huge assets in US. They filed dual actions in UK and US and both courts negotiated what law would apply. What was the very first thing negotiated? Attorney’s fees (at US rates).

ii. There is another game going on. The US is way down on one spectrum on bankruptcy on debtor relief and creditor power. US bankruptcy law provides more protection for debtors than any law in the world.

1. But now, more countries are adopting bankruptcy laws like the US. (See Canada, Mexico).

iii. Many things that happen in transnational business is that they try to get enough assets in the US so that they can file a domestic bankruptcy. Once a filing in the United States, we claim to deal with property across the world.

1. There is a shift of how world deals with financial problems since US is asserting jurisdiction across the world.

IV. Macro-economicsa. Organized system for dealing with failure in free-market economy.b. Not having a bankruptcy system may mean that the fastest guy, or biggest guy, or guy that gets the

sheriff moving first.

1

c. When soviet fell apart, big problem was that people were working in state-owned businesses. They didn’t want to close the businesses so what they did was enact strong bankruptcy law and use it as a way to transfer from state to private owned.

i. Also important is contract law, judicial system that you can rely on. d. When something fails, how do we get the people and services back to productive use?

i. It makes no sense to tear building down and lay people off.ii. The horror of acknowledging what went wrong (acknowledging losses) is what is dragging

down the Asian economies. e. Sovereign Insolvency

i. Countries going bankrupt (those who took out large loans from the IMF)ii. The real question when you understand bankruptcy is that should we do this with countries as

well. Perhaps we should start thinking about these in the international economy. 1. Should we take losses with respect to countries.

V. Social Policya. About job, families, healthcare.

i. Bankruptcy law has become the insurer of last resort.ii. Half of families that file for bankruptcy do so after a serious medical problems (800,000

families / year)iii. 2/3 of all families that file for bankruptcy do so after they have had a job loss (1.2 million /

year)b. So if we don’t liquidate factories, perhaps we may save 50K jobs for those already there.c. Middle-class social safety net (along with social security and unemployment)

i. Public safety net is there largely for the poor (welfare, subsidized medical care)d. When you use a measurement of the middle-class (education, whether you have a home, prestige job),

well over 90% have 1 criteria of the 3 and over half have 2 of the 3 characteristics.e. A family with minor children is 3x more likely to file for bankruptcy.

i. This year, more children will live though parent’s bankruptcies than divorces, cancer, graduate from college.

I. General Topicsa. Leverageb. Distinction between secured and unsecured creditc. Garnishmentd. Fraudulent conveyances ***e. Bankruptcy

i. Consumer in Chapter 7 (liquidation)ii. Chapter 13

iii. Chapter 11 (reorganization)

II. P. 14 (Problem Set 1)a. Problem 1.1

i. Consumer1. Debtors

a. Where they owe money?i. Mortgage on their home

ii. Student loansiii. Car loansiv. Credit Cardsv. Tax liability (sold something where no one collected money)

vi. Business liability (not incorporated and personally liable)1. the might have become personally liable on a note

(personal guarantee –secondarily liable)a. Order of liability

i. Go to business firstvii. Are you a debtor in this action before there has been a

lawsuit? (running stop sign and hitting someone) yes

2

1. Liability is not yet fixed. A jury might find that you are not liable (contingent liability).

2. Unliquidated liability (don’t know the judgment amount)

viii. Alimony or child supportix. Anything you’ve gotten something and haven’t paid for it yet.x. Gambling debts

xi. Falling behind on payments of rentxii. Property taxes (many jurisdictions for past services)

xiii. Home equity loans1. Contract says that we’ll lend you money, and if you

don’t pay, then we will come get your house. 2. Compare to credit cards: balance on credit cards can

go up and down (revolving loans compared to fixed loans of fixed term (home equity))

xiv. Payday loans1. Short term cash loans. Distinct from credit cards. 2. Payday loans have fixed term (i.e. 14 days). 3. Payday loans have fixed amount. 4. Tricks:

a. Effective interest rate: $50 interest on $150 loan (i.e. 1,000% APR)

b. Rollover to next period for a fee2. Creditors

a. Money is owed to you (whenever you prepay)b. Where you prepay rent. Why do landlords want you to prepay? (it’s a

leverage point)c. Prepaid insurance (1 month, 6 months into future)

i. Why do most insurance companies insist on being the debtor? If you paid the premium for past periods, then you know if you’ve been in a wreck.

d. Bank accounts (i.e. you lent money to Fleet when you put your money into checking account)

e. Bondsf. College Tuitiong. Creditor to your employerh. Warranty on appliances (you are a creditor for the period of the

warranty)i. Pension planj. Vacation Plan / Sick Day (you are putting in work now for something

promised in the future)k. Airline Miles / Rebatesl. Down payments (i.e. layaways)m. Utility depositsn. Tort Victimo. If you lent someone money (personal loan)p. Uncashed lottery ticketq. (Contingent creditor) unscratched lottery ticketr. Postage stamps. Cash value in your life insurance (riskier that someone dies as time

goes up so cost goes up). i. Whole life insurance is stable fixed amount every year. That

amount exceeds the insurance amount, so they invest the rest of the amount so in effect what you are buying is a mutual fund and life insurance together.

b. Business Context

3

i. Creditor1. Account Receivable

ii. Debtor1. Account Payable

09/09/2003

I. Contingent, liquidated, unliquidated debtsII. Contracts usually happen over time.

a. When an individual goes bust, there may be several mid-steps (pre-contract, post-contract actions) III. Problem 1.2 (Leverage) p. 15

a. Pathologist brings 10K a month. Owes 1,200 / month. Before exploring any legal action is to look at leverage each of the other creditors have.

i. Central Bank—home mortgage: they can take her home away so very high leverage. If you lose your home, what may happen to you financially? Your living expenses may actually increase. Tax advantages. For middle class, it is your largest asset. Can’t get job without address. If you can’t keep a home in that zip code, kids can’t stay in the same school or cub scouts (social ramifications).

1. Why would people be willing to go 1 or 2 months without paying mortgage?a. It’s not so easy to toss people out of their homes. The ramification of

paying 1 month late is the $150 penalty and interest. The peculiar point is that it is hard to exercise the leverage.

ii. Watkins Savings, car loan—they can take your car. Seems like less leverage because attachment is less. But in reality, you need it for work/food, but the real leverage is that they can repossess the car. You fall behind on the car payment, and they can take away the car really fast.

iii. Veterinarian—unsecured obligation. The special leverage is that the vet can always refuse future services. How often does the dog get sick? The leverage comes from “denial of future services.”

iv. Reich, the coworker: He can ruin your reputation at work. Why don’t you like owing money to coworkers? because you have to see them everyday. (personalized pressure)

v. Farmington Country Club: clearly something about “social embarrassment.” Country club posts delinquent lists.

vi. Shell Oil: can deny future services but not much leverage because there is “big supply,” so no leverage.

1. Only leverage is that the credit rating can be hurt. a. This is painful because they are finding another way to get future denial of

services. b. They are also trying to accomplish “scarcity”c. They are also trying to make it cost you a lot more money because they will

keep you from buying at the “cheap rate.” They will also increase the default rate of interest.

vii. MASTERCARD, bank card: Mastercard’s success has turned out to be its downfall. If the margin (difference b/w what credit card has to get the money and what they can charge you) is small, they must ensure that you pay it back. If the margin is great (borrow at 3% and lend it on CC’s at 15.5%), then the decision to lend from the CC’s point of view is that it is a marketing game rather than careful screening. The game is loaded that even if you can’t pay forever, but maybe 7 months, they will be in the black on your loan.

1. MASTERCARD’s problem is that this is a market share game, in fact, it is astonishing to watch the competition—whether there is leverage, it’s a question of (1) credit reporting (2) costs and (3) whether you will be cut off from other types of CC’s

viii. Talbot’s Clothing Store: Leverage is that if you really like to shop there, you may not be able to. But today, is that you can use general credit cards. So retailers have lost capacity for you to come into store.

4

ix. John South, alimony payment: can get remedy from judge. If you don’t have alimony, you can have (1) wages garnished, (2) humiliation (3) state has an interest

1. The law got tweaked up because state had an interest because they have no good leverage otherwise. Further, politicians sought women votes by making stronger alimony laws.

2. The best leverage is that you can actually send them to jail. 3. Gov’t agencies are now spending 10X more on enforcement of child support than

they were a generation ago. b. Our client doesn’t have much leverage except for reporting to credit card agencies.

i. Perhaps you could sue for $53,666. Downside is that she might be judgment proof and the litigation costs are not recoverable. Chance is that you might lose (sympathetic jury, some defect, some clause that turns out is not lawful, some defense available that you didn’t know about)

1. This is not like a default judgment (where they don’t come in at all)a. People who usually don’t come in are usually in defaultb. These are poor people (not sophisticated, not stable addresses)c. Our debtor here is sophisticated so she will not default, and is a high risk.

ii. You could report her to the IRS for cancellation of debt (but then she is unlikely to repay)1. The leverage is the “threat to tell the IRS.” Once you tell, you have little leverage

left.iii. What other advice do you have?

1. Get all three loans consolidated into one and get house for leverage—the legal problem is her permission is to take that loan and link it to the house and car.

2. Perhaps, Security Bank can renegotiate the loan and offer lower payments. (looking for credit rating reporting, threaten to sue her). Make it cheaper for her to pay and more expensive not to pay.

a. A safe bank is a count of number of non-performing loans to performing loans.

i. What kind of cheating problems do you have?1. I can turn any non-performing loans into performing loans

(i.e. turn it into $1 / month and a balloon payment at the end).

b. You could also offer to renegotiate the payment terms3. I’d rather have 2/3 of the amount of the loan, but what I want is a second security

interest on your house, and your car. IV. P.30 (Problem 2.1)

a. Payday lending problem (“Your failure to respond to this notice …will result in apply for a warrant for your arrest.”)

i. Violation of state usury laws? No violation of usury laws. You become a national bank, and make your home state a jurisdiction with no usury rate or a very high one (MD, DEL).

1. Interest rate in the home jurisdiction controls. ii. Fair Debt Collections Act?

1. Is Payday loan a debt collector?a. § 803(6): A debt collector is one who is in the business of collecting debts.

i. Offers no protection from the bank. ii. Includes any creditor who “in the process of collecting his own

debts, not in their own name”1. If under Payday-lending then they don’t care if they

violate that. 2. It says that the action is not wrong but only wrong if done by others.

a. (Policy) Why? Political pressure from banks and other lenders. i. Debtors testified that they were being harassed. So credit industry

said that: 1. let me tell you who the bad guys are, the debt collectors,

and let the debt collectors in the cold. a. The debt collectors are the guys on the bikes.

5

b. These debt collectors are not the same guys. c. Department stores bolstered their argument by:

i. Common law is not an effective against Sears and two-guys. When you get the giant judgment against two-guys, you can’t get any money.

ii. Not many lawyers would sue two-guys. Sears argument is that they have larger assets and lawyers will sue us. If you cut out the debt collection agencies, you will get the worst folks out of the game.

d. Reputational Argument: they can’t afford to hire people who will piss off their (that’s why you can’t do debt collection under a different name and still claim the exemption).

b. What are the options for a dentist (who really pays for the FDCA)?i. Prices are raised. So if two-guys have to double their prices (because they might get hit), who

pays it? Sears is big enough so that it can form it’s own collection agency and not subject to FDCA. However, a dentist, a small creditor, MUST to outsource it.

1. Interesting competitive effects (big stores v. small stores)

c. Why is it that Payday lenders use post-dated checks? i. Having a check in hand is that they can deposit it. In a sense, it’s like an assignment.

ii. What are Payday lenders looking for?1. It is a felony in many states when you write a post-dated check. They can go to

sheriff and get you thrown in jail or sheriff will say that they will throw you in jail if you don’t pay.

d. What could be the violations here?i. 808(3) Intent to threaten with criminal sanctions

ii. 808(4) depositing check earlyiii. 808(2) Taking more than 5 days and not giving notice within 10 daysiv. 808(?) Threatening action that you don’t intend to take.

e. This seems like a good investment

V. Problem 2.2a. Lawyers as debt collectors. L represents Ms. Chalmers and a tenant who left with $2000 on damage.

Debtor charges Fair Debt Collections action. i. Does FDCA apply to you? Are you a debt collector?

1. Lawyer is collecting for someone else? Argue no, FDCA does apply to you. a. Argue not a principal business of collecting debts for others. “I represent

people who are trying to get paid.” ii. Is this a debt collection action?

1. Trying to enforce a legal right, and this is not a debt. iii. Did L violate any action of FDCA?

1. How many times did you haul youself down and litigate for $2,000? If I can show you never litigated anything below $2,000, if § 807(5): huffing and puffing is not OK if you are a debt collector.

2. Threaten to sue in small claims court (lends credibility, but not for a lawyer bringing it).

3. Are you absolutely sure that $2000 is the actual damage. If it turns out that it is only $1000 worth of damage, then perhaps § 808(1) violated (falsely represent the amount of the debt).

VI. Problem 2.3a. K-market hires a debt collector. Debt collector, Fiddle, returns 85%. Debt collector tacks on own

collection fees to the debt. Violation of FDCA?i. Fiddle’s first defense is that he is not a debt collector:

6

1. He’s paying 85% of what he collects that makes him a squarely a debt collector2. When customer handed check, they never went into a credit-debtor relationship

because K-Market doesn’t take debt.a. It turns out to be a debt. They ran the risk that you would run into a debt.

ii. Consequence of adding fee on in violation of FDCA?1. FDCA prohibits tacking on the fee unless provided by contract. § 808(1)

a. By posting a terms of the contract, does the person agree when using a check?

VII. Usurya. Usury laws were removed when inflation was really high, and these usury laws seemed not so bad.

09/15/03

I. Problem 3.1 (p. 42)a. Flora-Ship has asked to have a line of credit above the current $6 million. DiSilvia believes Flora-Ship

is a failing business.i. How closely is this debtor tied to the bank economically?

1. Very closely tied. What are the things that tie Flora-Ship to DiSilvia? a. They have 1 creditor. Look at their cash flow: They are making all of their

payments out of borrowed money. They pay down weekly. b. The put all of the money they get all day and deposit it into a blocked

account. The next day, they get their money by their revolving account. A blocked account is an account that you can’t access. Economically, it is always a payment on a loan. All of their receipts go to the bank and pay down the loan, and the next day they borrow again.

c. You have a blocked account because i. (1) to keep the debt lower and

ii. (2) so that continued existence is at the bank’s mercy (this is a leverage point to make sure that they get paid…if you don’t pay them, they have a lot of leverage

iii. (3) very seasonal debtors like this because they aren’t borrowing a lot of money when they don’t need it (they are just paying down when they have it)

iv. (4) You are standing in front of someone’s books everyday. d. Remember there are no other accounts. Also, bank has security interest in

the flowers, van, and equipment. The first bank has taken a security interest in almost everything, and this ties the debtor to the creditor tightly. They can’t put their receipts anywhere. Can they raise cash anywhere else? No, there is no collateral left.

2. This loan is not ever supposed to pay off. They make money off the interest. ii. How secure is the loan?

1. Book Value of equipment is the $3.5 million. It may not actually be $3.5 million (either high or low) depending on the amount of depreciation. Book value comes from the purchase price according to either a tax/accounting formula.

2. You also have accounts receivable of $2.1 million. There is no way they are worth $2.1 million. What would you want to know if you wanted to value?

a. Do they tend to collect 90%, 94% of what they have outstanding?b. The number of people whose bills will fall to lower priority (because if they

are going out of business, customers will not be able to return). c. If you have lots of small ones, they may be expensive to collect.d. Also want to know how many of the accounts are past due.

i. Accounts have discount rates (i.e. 5%, 10%, 40%) for those 30/60/90 days past due.

3. Inventory has value of $0.5 million.

7

a. You have no time before this one falls apart. You must have contacts to sell it to someone else.

b. What should the bank do to back out of the deal?i. Do NOT unblock the account receivables (because then you increase the amount of losses by

the amount of the account receivables). ii. Current debt is $5.7 million. If the equipment is worth $5.8 million, you would want to

liquidate.iii. If the equipment is actually worth $2.5 million, then what are you inclined to do?

1. The worst shape the debtor is, the impulse is to hang in there for longer. If you cancel the deal, then you take a guaranteed hit.

a. But if you hang on, a year from now, the value of the equipment may depreciate further.

iv. When you decide that you want out of this business decision, what is the debtor’s first move? 1. Uncooperative debtor can destroy much of the accounts receivable (or destroy

anything of value that you have). a. What would you have to show on a lender liability suit?

i. If you live in the 2nd circuit, then no lender liability suit possible. ii. KMC (p. 34): Flora-Ship has to show for a lender-liability suit:

1. Notice Issue: That bank sprung this on the debtor and didn’t give debtor chance. So you would make it seem that it was a blocked account (tightly tied), and if you pull the line of credit, you knew that my company would not survive under those circumstances. You knew that my company would fail.

2. Debtor may bring a lender liability suit?v. DaSilva needs to give notice to avoid lender liability suit.

1. The more notice you give your client, your client has more time to make your collateral worthless.

2. It may take weeks to get new credit. The other banks are going to want to know why they want new credit if they also have a relationship with DaSilvia (commercial bank).

3. If creditor comes and seize everything, the business is gone. c. Assume that there is a personal guarantee.

i. Creditor has more leverage to get debtor’s cooperation if business is going down by offering to remove the personal guarantee if cooperation is given (by bringing $3 million on liquidation).

ii. If no personal guarantee, then have lesser leverage.

d. Here, there is no personal guarantee. The advice for DiSilva is to take everything and run. No notice. Get assets and get them out there. Possible lender liability and you may have to pay a couple hundred thousand, but Flora-Ship will settle.

II. Problem 3.2 a. Sympathetic debtor here. This lender (Maury) is equity holder in a competing business. Whether

KMC ultimately is about technicalities, leverage for debtors, or just crazy?i. Creditor has the right, negotiated right to repossess property.

ii. We don’t really know if KMC is right. But it is part of the leverage.

III. Problem 3.3a. Two examples of people who possibly would fall into lender liability.

i. Small business guy. Received notice. Couldn’t get another loan. 1. There have been a few cases where consumers or small business people have brought

lender liability suits.

8

a. In re Boone (FL): Mortgage company put in a dragnet clause to take interest in house and furnishings. Jury said that it was overreaching (including punitive damages).

b. Mississippi jury: fell behind on car payment, and because of that increased charges on the life policy. Jury brought $38 million recovery.

ii. Another woman’s car was repossessed and they took her refrigerator.

IV. Secured and Unsecured Credit:a. Difference between secured and unsecured creditor.

i. How do you get money?1. Get a final judgment (by suing them)2. Court issues a writ (i.e. the order to pay)3. take writ to a sheriff in the locality where the person’s goods are located. Tell sheriff

to execute on writ. Sheriff goes to the house/business of person and says that he’s there to seize goods. They walk through the house. They pick stuff up, and put it back in the sheriff’s office and then the sell goods. After sale, sheriff gets paid first and then distributed to the creditor, and excess will be given back to the debtor.

a. Every state allows debtors to keep some stuff. (in DE, gets to keep up to $5000 total things…including house)

i. In TX, get to keep life insurance policy, 60K personalty, the houseii. There are state law determined things. (exemption statutes)

b. Whoever is first gets paid in full before those with subordinate claims. i. First to get judgment

ii. First to get writiii. First to get sheriff to execute.iv. Relation back:

1. If two people get writs simultaneously, then you might be able to relate back to the time of judgment.

a. A gets judgment, then B gets a judgment. B then gets a writ and execution on the writ. Now A gets a writ and then an execution. Relationback to the judgment means that A wins as long as before sale is made and cash distributed.

ii. Remember, once you are first, you get first dibs until you are fully paid. 1. In bankruptcy, you are pro-rata distribution.

b. Secured Creditorsi. Promise attached: If I don’t pay when I said I would, you can come and get the collateral

(A/R, ring, house, etc…)ii. (1) No exemptions as to secured creditors on the collateral. In TX, you can’t reach furniture

unless more than $60K. A secured creditor can reach those things directly.iii. (2) Secured creditor has easier time in court or don’t need to go to court.

1. Entitled to self-help (i.e. repo man)a. But not allowed to breach the peace.b. Really only good against the ignorant

2. If you have to go to court, you are given a shorter game in court. You get in and out of court faster.

iv. (3) You beat out unsecured creditors in priorityv. However, security interest must be filed in order to be perfected.

1. First in time to get perfected (in notice) is the first in right-- priority (because you can have 2 secured creditors on same property).

c. Securitizationi. In a regular loan, you have the debtor and the bank. The bank gives the debtor cash, and

debtor promises cash + interest (unsecured). Throw in collateral, and now it is secured.ii. Securitization is where the Seller (debtor) sells it’s A/R, inventory, Everythings to this

company (the Special Purpose Entity, SPE) for cash. Now the SPE is the owner of the A/R’s.

9

The bank or investors are the ones that lend that same amount of cash to the SPE, and the SPE promises to pay back to the bank money, interest, and any collateral that the SPE owns.

1. Ordinary sales are not dragged into bankruptcy courts. 2. This is called Asset Securitization. Sometimes SPE’s sell shares to stock to raise the

money that will be lent back to the seller. SPE will never go into bankruptcy because the Bank has its directors it on the board of the SPE. The SPE will not file for bankruptcy because it requires a vote from the board.

3. This means that all the other creditors (of the seller) can’t reach assets of the seller because its all been moved into the SPE.

--------------------------

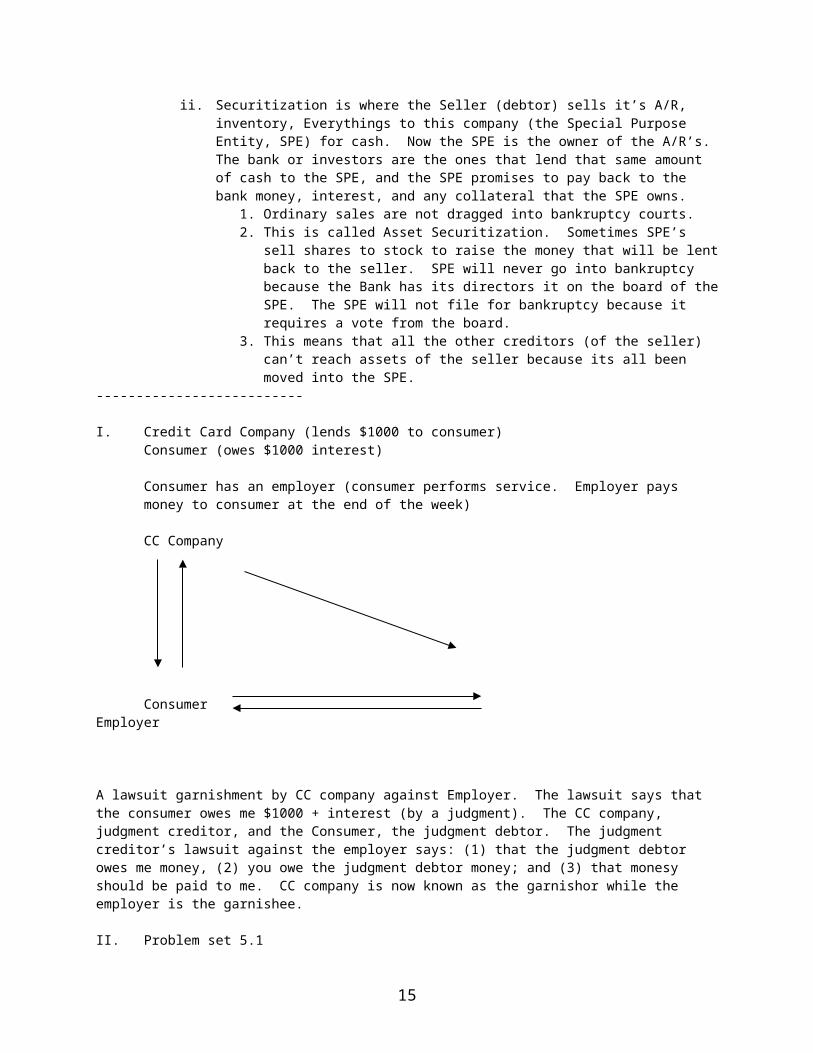

I. Credit Card Company (lends $1000 to consumer)Consumer (owes $1000 interest)

Consumer has an employer (consumer performs service. Employer pays money to consumer at the end of the week)

CC Company

Consumer Employer

A lawsuit garnishment by CC company against Employer. The lawsuit says that the consumer owes me $1000 + interest (by a judgment). The CC company, judgment creditor, and the Consumer, the judgment debtor. The judgment creditor’s lawsuit against the employer says: (1) that the judgment debtor owes me money, (2) you owe the judgment debtor money; and (3) that monesy should be paid to me. CC company is now known as the garnishor while the employer is the garnishee.

II. Problem set 5.1a. 2/1, First finance gets $2000 judgment and gets writ to sheriff ( -10)b. 2/5, Wayne deposits $5000 (4990)c. 2/7, Second finance company gets writ for $3000d. 2/9, Sheriff delivers both writse. What are the questions we ask?

i. How much money is available for the creditors? 4,990 (Bank paid itself the $10 overdrawn before the writ was delivered). Creditors get whatever is there at the time they come in when the writ arrives.

ii. Which creditor beats who?1. Backdated to date of judgment? First Bank gets entire $3000; Second creditor gets

$1990.2. If dated back to writ? Same result above3. If leaves with Sheriff? Pro-rata, or depends on which one the sheriff delivered first,

and which one was delivered second.

09/16/2003

I. 2/1: Writ to Sheriff: FF $3000 (-10)2/5: Deposit (4,990)

10

2/7: J, Writ to Sheriff, SF $3000 2/9: Sheriff delivers writs2/9: D writes the check $5002/10:Bank Pays Check $500 (4,490)2/11:D deposits $200 (4,690)2/15: Bank answers2/16: D Deposits (4,490)

You are testing two parts: (1) status of account is frozen when the writ arrives. What matters is when the sheriff delivers the writ to the bank. What does that mean? If you haven’t received anything from a sheriff, then you can continue to operate as normal. Notice to the third parties? Nothing happens until something happens in an overt way.

What’s the purpose of relation back? Intersect between the creditors that determines who gets ahead. But doesn’t make the garnishment go back.

Writ served on 2/9: What’s the legal consequence of the debtor writing a check and handing it over vis-à-vis this garnishment action? This check does not affect the garnishment. Nothing happens when you write the check. It is not an assignment of money in the account, at least not legally.

The bank then pays the check for $500. Bank is still responsible for the entire $4,990, at least to the garnishor. Now, bank becomes the creditor of $500 that was paid. The bank’s error falls on the bank. ----Debtor deposits $200 on 2/1l. The rule of garnishment is: if deposits keep coming in, they are falling into the garnishment “net.”

The bank answers on 2/15: what does this mean? You want all activity since the writ was delivered.

Can you reach the new deposit after the Bank answers? Suppose the bank does not contest. When was the answer due? The answer was due 2/20. Does the next extend to the date the answer is due or when the date. The court guarantees you the temporal net. It does not matter if the bank answers early (so after the bank answers, but before the deadline, catches all deposits in the net). What is the bank thinking about? --Bank’s incentives may be with the customers rather than the garnishor. What aligns the incentives between the bank and the customers is if “there is a loan.” What else may be at that bank? Probably a loan outstanding from the bank. The juiciest asset is “cash.” You would be asking the bank to give up the cash for another creditor. What does the bank always do? The bank has 2 incentives—(1) they’d like to take the money in the account and take it themselves (feast off carcus) (2) or alternatively, they’d like to keep the business alive so that they can get the money later.

What is the bank likely to do when they get a garnishment order? They’d like to apply the money to their own debt (set off the money in the account vis-à-vis their loans). You can do offsets before you receive the garnishment? Yes, but NOT after the garnishment writ is delivered. What’s going to happen at a bank where there is an outstanding loan? Banks remarkably “set off” moments before garnishment orders arrive.

When bank gets the garnishment order, what else might they do? Does the bank call and say stop putting money into the account? What is the best chance of keeping you alive? Depends on what is better chance of keeping you alive.

II. Problem 5.2

J. Creditor (Judgment collections)

11

J. Debtor (Baker) Garnishee (Nicholson)

Here, it is a garnishment order because what is happening here is that Nicholson owns something that belongs to the J. Debtor (it can be anything, not just cash). What is the dispute about? You, as garnishor, are only allowed (entitled) to seize what I’m holding that belong to Baker. If Baker has no right, then Baker’s judgment creditor have no right. Baker’s right is right to possession of physical property at end of the lease term. Baker may also have the right to money payments from Garnishee to Baker. If this is a straight up deal, 2 things can be garnished: (1) money payments owed to Baker and (2) property at the end of the lease term—so at the end of the lease term, you have to give property back to garnishor.

If Doyle is telling the truth, what is the legal consequences? They can garnish because the garnishment order already delivered, then Nicholson has no freedom. The consequence of the garnishment order has been served, so Nicholson is now holding the property in trust for the creditor. If they disobey the order after the garnishment order, then you set aside the lease that was made after the garnishment order was delivered. All you have to do is that you get a garnishment order that says “I want all things that you have that are owed to the judgment creditor.” If garnishee has superior right that predated the garnishment order, the garnishing creditor CAN’T defeat that.

Who are the two parties to the litigation? Judgment Collections and Garnishee (Nicholson) will litigate regarding the relationship of Nicholson to J. Debtor (Baker).

You can do anything with your property (sell, lease, etc) right until the court order arrives.

III. Problem 5.3a. Valdez wants to fire the employee after a garnishment order arrives. What do you advise?

§ 1674. Restriction on discharge from employment by reason of garnishment

(a) Termination of employment

No employer may discharge any employee by reason of the fact that his earnings have been subjected to garnishment for any one indebtedness.

If employer gets two garnishments, and you can fire them. Why? You want to give them a chance. But a second garnishment is OK, because employer’s argument for this is: (1) it is expensive to administer (2) further less incentive for someone to come to work because wages will be garnished (3) you might be pulled into litigation and be liable for the entire judgment.

Why fire them outright anyways? The teeth in the statute is $1,000 or imprisonment. There is NO private cause of action means that it is not there. Fire him, what are the chances that you will get charged? Little. What will happen to you if the worse goes wrong?

I. Problem 7.1a. Fraudulent conveyance?

i. No bad intent. She was in good faith. Is that a defense to fraudulent conveyance? No. we don’t care about the good-faith of the seller.

1. § 4(a)(1): with actual intent to hinder, delay, or defraud (set aside for past and present)2. §5(a) (applies to previous creditors at the time of transaction):

12

a. Without (1) receiving an equivalent value and (2) the debtor was insolvent or rendered insolvent by the transaction.

3. Do we care about the good-faith of the buyer? a. § 8(a): A transfer or obligation is not voidable under Section 4(a)(1) against a

person who took in good faith and for a reasonably equivalent obligation. i. Here, we are doing a 5(a), and there is no defense of good faith.

b. Fraudulent conveyances: 2 rules when a creditor set aside: i. no reasonably equivalent value AND debtor is insolvent or rendered

insolventii. §4(a)(1): actual intent to hinder, delay, or defraud.

ii. What is the buyer’s best defense? Reasonably equivalent value (because good-faith no available)

1. It was used, big scratch. 2. What’s the rule that what constitutes reasonably equivalent value?

a. Suppose you were advising the buyer? Some deals are too good a deal but there is always one other fact (i.e. insolvency).

i. It’s too good of a deal if you are insolvent. So you can give your money away unless you owe it to someone else.

1. This is the constraint of fraudulent conveyance.b. You can give your stuff away as long as you are SOLVENT. c. Look at the remedy if you engage in a not-reasonably equivalent value and insolvent?

i. I.e. you pay $750 for $15,000 piano? What happens to the buyer? 1. If it turns out down the line, you would lose your deal (benefit of the bargain or the

expectancy)—this would have been the difference between the $750 and $15,000. a. What position am I put in? status quo ante (same position if you never had the

contract)b. So you should go ahead and do it. Because the creditor has to pay the person

$750 to get the piano back. ii. What if you destroyed the piano and now need to give you back?

1. Fraudulent conveyance law does not answer it.

II. Problem 7.6a. They were insolvent and whatever spiritual value was not equivalent value. b. You can do a fraudulent conveyance claim on a donation.c. What about the chiropractor?

III. Problem 7.7a. They are not absolutely void, just voidable.b. Can you come back and say that you intended to “have a fraudulent conveyance.”

i. Will that work? Courts of equity said that only relief given for clean hands. One court has said (in peri delecto). Other court has said that the bargain should be honored.

09/23/03I. Problem 7.2

a. Can AX successfully claim a fraudulent conveyance?i. §5(a) only applies to pre-transaction creditors so doesn’t apply here

ii. § 4(a): applies to present OR future creditors 1. Here, AX is a future creditor at the time of transaction. 2. Maybe § 4(a)(1) applies:

a. Requires actual intent to hinder, delay, or defraud any creditor of the debtor. i. Part (b) lists certain factors to consider, listing from (1) . . .(7)

1. Actual intent means listed in (b) or others—actual intent is that someone is determining it and can infer from circumstances of the case.

3. § 4(a)(2): didn’t receive reasonably equivalent value AND

13

a. (i): debtor was engaged or about to engage in a business or transaction for which the remaining assets of the debtor were unreasonably small in relation to the business or transaction; or

i.b. (ii): debtor intended to incur, or believed or reasonably should have

believed that he would incur, debts beyond his ability to pay as they became due

i. difference from § 5(a) : in § 5(a), there is no intent as there is here. 1. as a practical matter, what is the difference in the

standard? Didn’t know is not a defense. 2. The real test in § 4 (a)(2)(ii) is that you need to prove that

debtor reasonably should have known that they would have been insolvent.

ii. If preexisting creditors, all you have to show is that they are insolvent (this is easier than § 4 (a)(2)(ii))

1. There is a sense that perhaps there really isn’t much difference.

c. Why are present and future creditors treated differently? i. Present creditors can tell debtor, under fraudulent conveyances, not

to make transfer with actual intent to hinder, delay, or defraud PLUS also can’t tell them transfer less than reasonably equivalent value if debtor was insolvent or under § 4a(ii) that they reasonably knew that they should have been insolvent.

4. Future creditors should check the ship to see if it is seaworthy.a. If indeed § 4(a)(ii) and §5(a), then we are diminishing the importance of

future creditors of checking out the debtor themselves before lending.II. Securitization

a. Loan to the bankruptcy vehicle and the bank lent to the bankruptcy vehicle.

D BRV Creditor

i. The attack here is that there may be actual intent to hinder, delay or defraud under § 4(a)(i). Convey assets out of hands of shareholders to defraud them (to pump up Enron’s balance sheet). To reduce the amount of debt to keep their high credit lending.

III. Problem 7.3a. It’s only fraudulent if you transfer an asset, but an asset does not mean things that are exempt under

non-bankruptcy law. i. Preserves exemptions under State Law. What makes property valuable that you can convey

it. ii. Additional notion are creditor expectations:

1. You can transfer exempt property, because creditor does not have any expectations to the property.

IV. Problem 7.5a. Pat’s letter explained that the business is struggling with bills piling up. b. Structured transaction:

Magic Clean ---------------if liquidated,Up to $100,000 Goes to Kim.(if sells for $120K,

14

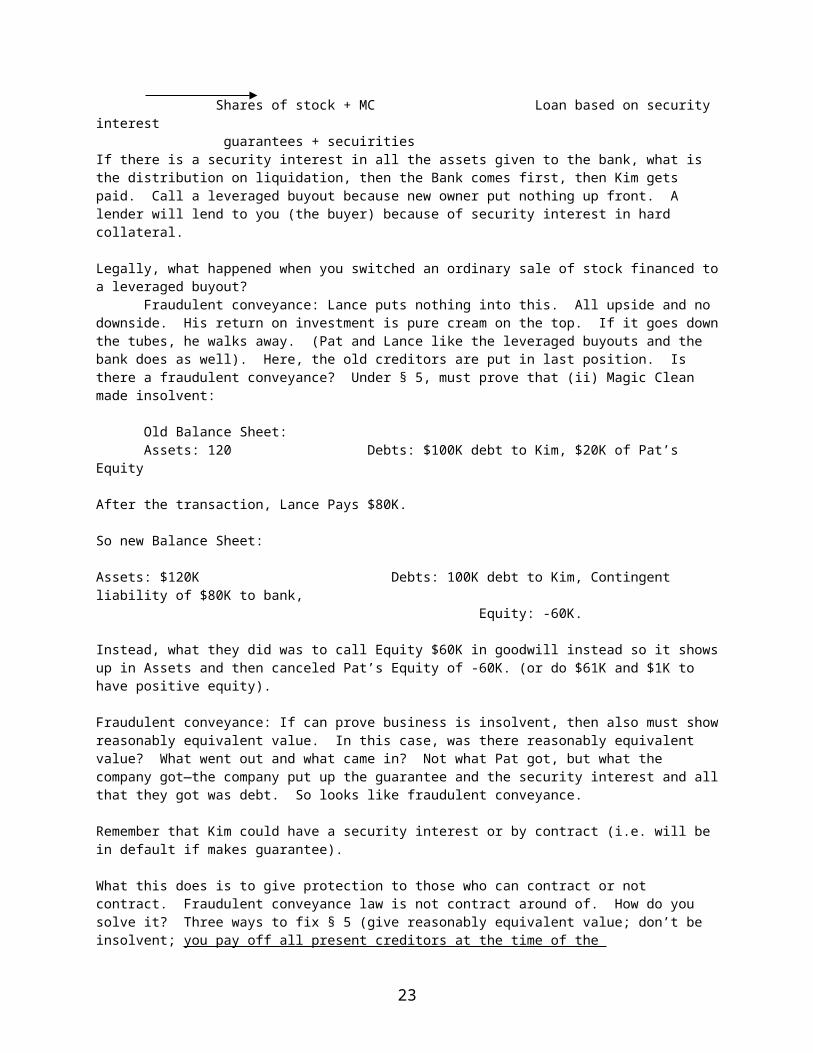

$100 to Kim, $20Kto Pat) shares of the stockKim $100KPat $20 K Lance $XIf Pat wants to sell ownership of the business to Lance, then contract b/w Pat and Lance. Pat will transfer stocks of business and Lance would pay Pat money. Suppose Lance doesn’t have the money? Lance will get a loan from bank, probably offering security interest in the thing he is about to buy (the stock). How much will you lend against the shares? (remember Kim is secured on assets to $100K). Bank will probably lend less than 50% of the face value of the value of the stock.

What would happen if this is a leveraged buy-out? Security interest Paid cash rcv’d from bnk Pat Lance Bank Shares of stock + MC Loan based on security interest guarantees + secuiritiesIf there is a security interest in all the assets given to the bank, what is the distribution on liquidation, then the Bank comes first, then Kim gets paid. Call a leveraged buyout because new owner put nothing up front. A lender will lend to you (the buyer) because of security interest in hard collateral.

Legally, what happened when you switched an ordinary sale of stock financed to a leveraged buyout? Fraudulent conveyance: Lance puts nothing into this. All upside and no downside. His return on

investment is pure cream on the top. If it goes down the tubes, he walks away. (Pat and Lance like the leveraged buyouts and the bank does as well). Here, the old creditors are put in last position. Is there a fraudulent conveyance? Under § 5, must prove that (ii) Magic Clean made insolvent:

Old Balance Sheet:Assets: 120 Debts: $100K debt to Kim, $20K of Pat’s Equity

After the transaction, Lance Pays $80K.

So new Balance Sheet:

Assets: $120K Debts: 100K debt to Kim, Contingent liability of $80K to bank, Equity: -60K.

Instead, what they did was to call Equity $60K in goodwill instead so it shows up in Assets and then canceled Pat’s Equity of -60K. (or do $61K and $1K to have positive equity).

Fraudulent conveyance: If can prove business is insolvent, then also must show reasonably equivalent value. In this case, was there reasonably equivalent value? What went out and what came in? Not what Pat got, but what the company got—the company put up the guarantee and the security interest and all that they got was debt. So looks like fraudulent conveyance.

Remember that Kim could have a security interest or by contract (i.e. will be in default if makes guarantee).

What this does is to give protection to those who can contract or not contract. Fraudulent conveyance law is not contract around of. How do you solve it? Three ways to fix § 5 (give reasonably equivalent value; don’t be insolvent; you pay off all present creditors at the time of the transaction(but then you lose your leveraged buyout trick)—also you could cancel 1 st loan with a second loan with a higher interest rate ) To the extent that § 4(a)(ii) overlaps with § 5, you are stuck with present and future creditors.

------------------V. Problem 8.1

15

a. Toto and furniture (exempt property): Yes, part of the estate even if exempt.i. § 541(a): Such estate is comprised of all the following property . . .

1. General rule is that everything that they have is in the estate, including their exempt property.

b. Pinto, that has no value (because subject to excess security interest):i. Pinto is in the estate because they have legal title to it.

1. The person can use the car.c. The photos:

i. Yes, no requirement of value to be part of estate.d. Michael Jackson Tickets:

i. Still part of estate whether you can transfer it or not (no requirement of value, just need legal title or equitable interest)

e. Catcher’s Mitt?i. Yes, “wherever located and by whomever held”

f. Bank Account held by Donald in trust for Sherry?i. Legal title to bank account, but equitable ownership by Sherry. What comes into the estate

then? 1. Legal ownership comes into estate, but corpus (equitable interest) stays out of estate.

g. Baby Parakeets?i. In estate because of § 541(a)(6).

h. Retirement Account? i. Under state or federal law, must be spendthrift trust.

1. What is a spendthrift trust? You can’t get in there to play around the money. Also, the creditors couldn’t touch it outside of bankruptcy. Spendthrift trust says that creditors can’t touch the corpus.

ii. If you have a retirement account, and if that retirement account is a spendthrift trust, creditors can’t reach it. That’s the key feature.

1. State law or ERISA-qualified plan (spendthrift provisions)iii. Look at what happened to property of the estate—it is a big definition with a carved out for

spend-thrift trust. Why?1. Because creditors had no expectation to it.2. You also don’t have to litigate what comes in. 3. You protect it from other creditors 4. Trustees have control over all the property

16

09/29/03

I. Problem 8.2 a. Ticket is property of the estate. The fact that it is more valuable later is great the estate (estate takes

good/bad news)b. Why is an engagement to a rich person not part of the estate (compared to the lottery ticket)?

i. There is a continuum of expectancies. 1. Suppose I expect you to sell me wheat on contract, and it turns out to become more

valuable. Yes, this is property of the estate.

II. Problem 8.3a. The estate gets it: § 541(a)(1)—legal or equitable interest for the wheat

i. contracts can be property of the estate (property exempted is still part of the estate and just determines what debtors will get back )

b. § 541(a)(6): proceeds, products, offspring, rents, or profits of or from property of the estate, EXCEPT such as are earnings from services performed by an individual debtor after the commencement of the case

i. Whatever value he added post-bankruptcy does not belong to the estate. Thus, the value of his post-bankruptcy services should be excepted.

ii. Negotiation for this with trustee should have happened after bankruptcy. 1. Ask trustee what they are you going to do with the wheat?2. Remember trustee can hire someone else to harvest wheat.3. Trustee can give %’ge repayment scheme, a percentage on sale.

a. Farmer is not obligation to contribute services post-petition. (like watering, fertilizing, threshing the estate’s wheat)

b. Debt must realize that this is not their wheat anymore.i. But his human capital is still his.

III. Problem 8.4a. Cratchet gets to keep $1,000 because “his continued performance was necessary for him to receive his

payment.” Therefore, it reflects labor done post-petition. (but-for test). b. What’s the trustee’s argument?

i. This was at least ¾ earned prepetition, and thus would be a ¾ & 1/4 split.ii. Further, more aggressively, the notion is that by teaching for ¾ of the year fabulously, he

actually won the award by the petition. He only had to do a trivial amount of post-bankruptcy work. All the hard work was done early, and this tiny amount of work post-petition.

IV. Discrimination Claim: a. She should have mentioned that lawsuit against TWA because it was part of the estate

V. Problem 8.6

a. Yes, it’s property of the estate. Bankruptcy Code in § 541(C)(1) on transferability— (restriction on transfer doesn’t keep it out of the estate): nothwithstanding any provision in an agreement, transfer, instrument, or applicable nonbankruptcy law—(A) that restrict or conditions transfer of such interest by the debtor.

b. How can debtor keep license out of the estate?i. Debtor argues that it’s not property— that it’s only a privilege and not property.

ii. When you file for bankruptcy, is it valuable to have a driver’s license? Yes. 1. Is the driver’s license property of the estate?2. How about a license to practice medicine valuable? Yes, and it’s something you had

prepetition. But not a property right.c. Branoff Airlines was a victim of growth. Branoff decided that it was going to buy up landing

slots/planes and expanded nationally. Branoff has a meeting with its creditors and could not meet interest payments—it did not have any secured debt at all.

i. So Branoff divided up all the creditors, and gave them security interests to stave off payments.

17

ii. 1 year to the date Branoff filed for bankruptcy. But, what did Branoff have? All the landing slots on earth. East Coast, West Coast, Europe.

1. There was big arguments in 5th circuit: 1 group says property of the estate and other says that it was not.

a. The other airlines said was not property of the estate because the Federal Aviation owns the strips. (1) if not part of estate, then Branoff will definitely fold because can’t be sold

i. If Branoff folds and landing slots not part of the estate, then (2) FAA will distribute the landing slots (but not through money)

1. But small airlines wanted it to be property of the estate because they wanted to buy it (since FAA doesn’t sell it). They wanted Branoff to pare itself down, and sell of the rest.

b. Creditors of Branoff would want it to be property because more money to pay off debts.

c. Trustee wants big estate because big money for trustee.d. Branoff management’s view is that they want to be property of the estate

because only chance they have of a “going-concern but bankrupt” airline.e. The district court says that it is part of the estate. (Branoff would live).

Fifth circuit said no property (Branoff died from this ruling)

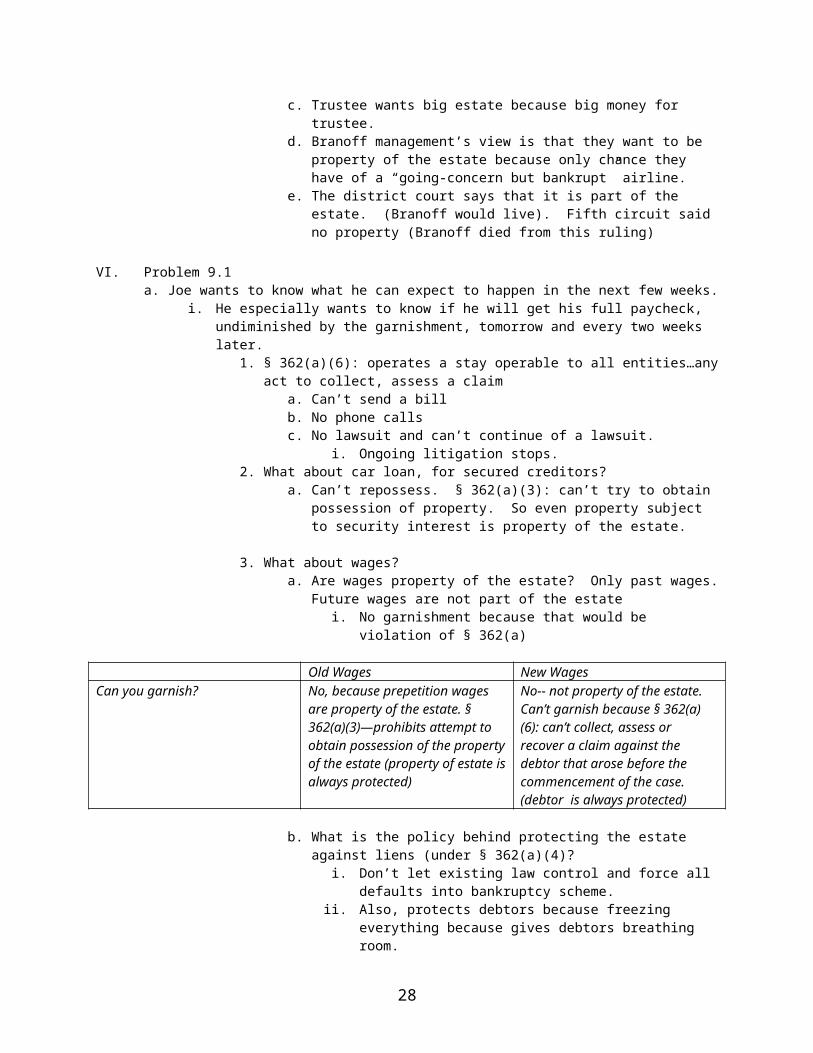

VI. Problem 9.1a. Joe wants to know what he can expect to happen in the next few weeks.

i. He especially wants to know if he will get his full paycheck, undiminished by the garnishment, tomorrow and every two weeks later.

1. § 362(a)(6): operates a stay operable to all entities…any act to collect, assess a claima. Can’t send a billb. No phone callsc. No lawsuit and can’t continue of a lawsuit.

i. Ongoing litigation stops. 2. What about car loan, for secured creditors?

a. Can’t repossess. § 362(a)(3): can’t try to obtain possession of property. So even property subject to security interest is property of the estate.

3. What about wages?a. Are wages property of the estate? Only past wages. Future wages are not

part of the estatei. No garnishment because that would be violation of § 362(a)

Old Wages New WagesCan you garnish? No, because prepetition wages are

property of the estate. § 362(a)(3)—prohibits attempt to obtain possession of the property of the estate (property of estate is always protected)

No-- not property of the estate. Can’t garnish because § 362(a)(6): can’t collect, assess or recover a claim against the debtor that arose before the commencement of the case. (debtor is always protected)

b. What is the policy behind protecting the estate against liens (under § 362(a)(4)?

i. Don’t let existing law control and force all defaults into bankruptcy scheme.

ii. Also, protects debtors because freezing everything because gives debtors breathing room.

b. What if it turned out alimony or child support?i. § 362(b): You can go forward and establish liability for alimony or paternity.

18

1. Why? to Give special place for support of children. 2. But, what can you collect against? You can collect against property not part of the

estate (§ 362(b)(2)(B)).a. So if you were garnishing wages, you don’t get anything for this paycheck,

but something from future paychecks.

c. Action for “hot” check. (See exception in § 362(b)(1))i. You question of the D.A. is: if he pays off on the check, will you drop the action?

1. Now your pitch is that this is a creditor trying to collect on a pre-petition debt not state enforcement of its own laws.

2. Sometimes, bankruptcy courts prevent creditors for showing up on the hot-check charges so that the DA loses.

d. Utility Payments:i. § 366(a): they can’t discontinue service unless you pay once you file for bankruptcy (because

would be action to collect)1. However, the protection is under § 362(b), it means that they can ask court for a

deposit. They can’t say pay or we’ll cut you off, but we don’t have to provide future services unless we have a deposit (must be reasonable according to the court). If no deposit, can shut them off.

VII. Problem 9.2a. The association has asked you to prepare a general outline of what creditor behavior is appropriate

once a debtor files for bankruptcy. i. There is nothing you can do.

VIII. Problem 11.1a. What is part of the claim?

Principal loan: $180,000 Pre-petition int. $14,000Post-Petition Atty $1,000

§ 502(a): money is presumed owed as soon as debtor lists it; (b) has objections Is there anything to litigate under § 502(b)? Yes, the post-petition attorneys’ fees. Remember, post-petition interest is not in under § 502(b)(2) under unmatured interest. So should you get post-petition attorneys’ fees? Nope, just like unmatured interest.

Here, assume general unsecured is $194,000 (don’t follow second circuit): 10% of $194,00 = $19,400 is actually what the client gets. The remainder of the claim ($194,000 - $19,400 = $174,600) is discharged.

09/30/03

I. Problem 11.2a. What do you explain to Buckeye about it’s financial position in bankruptcy?

i. Under § 506(b): There is $225,000 in collateral. What can client get?$180,000 loan$14,000 interest$1,000 attorneys’ fees if provided for by contract (§ 506(b): allows reasonable fees, cost, or charges provided for under the agreement under which such claim arose)----------------$195,000

If the secured creditor pays broker fees, then their claim would then be $197,750 (+ $2750). However, if trustee sells it, the secured creditor can’t include the $2750.

ii. Who pays the broker fees? 1. Oversecured: Collateral worth $225,000. Broker fees decrease amount of estate if

they were paid by the secured creditor. Their claim is for $195,000.

19

a. Now assume secured party pays the fees: i. They would net $195,000 still because estate recovery is reduced

by $2750. 2. Undersecured: Collateral worth $165,000. Because you don’t have room for the rest,

you don’t get attorneys’ fees, and the remaining unsecured claim is $29,000. The amount the creditor walks away with is $165,000 + 0.10 ($29,000) = $167,900.

a. Now if secured party pays the fees:i. They lay out $2750. What’s going to change is that their

unsecured claim increases from $29,000 to ($29,000 + 2,750 = $31,750).

1. so then 10% of the $31,750= $3,175b. Total recovery is $165,000 + $3,175 = $168, 175, but remember he paid

the $2750 so his recovery really is $165,425: i. (secured creditor shouldered 90% of the cost of selling).

1. So residual claimant paid. II. Problem 11.4

a. Explain what happens to CF: Collateral: $23,800i. Claim under § 502 (unsecured claim): $24,600

1. Is there anything else besides the $24,600? Can only get post-petition interest if oversecured (only up to value of the collateral).

ii. His § 506 secured claim is for $23,800 and there is a § 502 unsecured for $800. Assuming 10% on the dollar, then recovers $80.

1. $23,880 total. III. THE ESTATE

IV. Estate size is 50,000V. Problem Set 12

a. § 507 controls priorityi. (1) John Harry, a private duty nurse whom Harold hired while his father was quite ill: $5,000

1. He is third here in priority. He gets $4650 first (cap and must be earned within 90 days before the date of filing the petition). And then general unsecured claim of $350. Why do they get a special break?

a. This is really for the employee benefit sections. Why do you want to give employees a better deal?

i. They want to stop the echo effect of bankruptcy. If these employees can’t get their paychecks, they may have their entire lot with this company (no risk spreading). We want employees to continue working.

b. But why do we have these limits $4,650 and within 90 days?

20

506

506

502

Exemptions

i. Who would have unclaimed wages for more than 90 days old and over $4,650? These would be CEO’s. We care less about CEO’s and if we gave them priority for unpaid wages over the past two years. What might really be going on here? If you didn’t take your paycheck for more than 90 days or more than $4,650, those people have a different relationship (an interest in the company compared with $9/hr workers)

ii. (2) Social Security Administration, social security and withholding from Harry’s earlier paychecks: $534

1. Eighth priority 2. § 507(a)(8)(C) is a trust fund tax3. § 507(a)(8)(D) is just a wage tax; taxes owed because they were your obligation that

are required by the employer to collect4. Policy:

a. They want to protect the public fisce. One dollar less means one dollar more that someone else has to pay. (the externalities argument)

b. You also can’t discharge tax debts. Why don’t give up the priority then? i. Who gets protected as a result of the priority? The debtor.

Because it means that taxes are being paid first from the estate. So the general unsecured debts will be discharged, and they will emerge with less taxes owed, which are non-dischargeable anyways (this is debtor protection as well as protection for the gov’t).

iii. (3) City of Eden, property taxes: $3,000 per year for the last 3 years, plus $500 per year penalties for each of the 3 years.

1. § 507(a)(8)(B): a property tax assessed before the commencement of the case and last

1/92 1/93 1/94 1/95 3/1 Bkrpty

(assessed)

(so the tax must have first been assessed at least 1 year before and without penalty) So really only the ’94 tax payable.s

Assume assessment is made in March of the year. ’94 is last payable one year before after the date of the filing. (really it is within 1 year so long as you understand it to not be after the date of bankruptcy—it really is a one year statute of limitations on property taxes)

We want to protect localities for their tax. Also, as a matter of policy, we are telling localities that if someone is not paying their priority taxes (if they are behind a year, we’ll give you priority; otherwise, you are at your risk). We want them (localities) to keep up on their records so that other creditors will know how they are doing financially (UCC filings, check real estate records and liens). This is a little kick at municipalities to keep their records up.

Can they also collect the penalty with a priority? § 726(a)(4) places them very far back in line (behind the § 507 priorities, the unsecured creditors . . .). But § 507(a)(8)(G) (has to be actual pecuniary loss-- which is something akin to interest)

Why do penalties have to happen like this (subordinating penalties under § 726(a)(4)? The penalty would actually be paid by the unsecured creditors.

iv. (4) George Nartowski, down payment against a tractor lawnmower Harold had agreed to sell to George: $300

1. § 507(a)(6): Sixth priority. Unsecured claims arising from deposits. Limited to $2,100 priority.

21

a. Why does this one get priority? i. Might refer to rent deposits.

ii. People of modest means, before credit cards, used to do lawaway. This part of the statute is for these consumers at Woolsworth on layaway, and Woolsworth files for bankruptcy. We don’t want their $40 to be $0.04 in discharge.

v. (5) State Department of Revenue and IRS, income taxes: state $4,000, federal $14,000.1. Falls under §507(a)(8)

91 92 93 94 95 B

3/1‘94 taxes are included. ‘93 taxes are included, ‘92 are included, and ‘91 are included (4 year reachback because filed before 4/15). You are permitted under 26 USC to bifurcate the taxes. Thus, you can get a 1/6, ¼ for your priority. Why priority for IRS: harder for IRS to place a lien on property. But, IRS collects 99.99% of all money deemed owed (reasons for 4 year reachback).

Anything over three years is actually dischargeable. You can reach back some distance but not forever.

vi. (6) Telephone, utility, and other regular bills following bankruptcy: $5,0001. Post -bankruptcy bills get no priority.

vii. (7) TIB as trustee and as trustee’s counsel: $4,0001. § 507(a)(1): administrative expenses under § 503(b).

viii. (8) Insurance premiums for insurance on the non-exempt personal property for $7501. Also § 507(a)(1). Policy for it: to preserve the property. Estate pays not only

administrative fees but also to protect itself. If utility bills are necessary to preserve the estate, then may also be an administrative expense.

ix. (9) Costs of sale of Harold’s non-exempt real estate and personal property, including advertising: $2,800

1. § 507(a)(1) x. (10) Sara Fleet, Harold’s attorney: $1,250 in fees ($500 for a will; $750 for preparing this

bankruptcy filing)1. “Preparing Will” would be classified as independent contractor. No priority on the

will. (no § 507 priority) 2. Preparing bankruptcy filing: this is § 507(a)(1)-- most courts say that this is no!

because created before estate was created.a. Would you take someone on credit even if you are in a § 507(a)(1)?

i. No. you will ask up front. Lots of consumer cases can’t even get a § 507(a)(1).

ii. Instead of paying all your other creditors, give me your paycheck first.

iii. The second way to do it is to skip the house payment. P.S. check and see where it says that IRS taxes older than 3 years are discharged.

09/29/03 (makeup class)

I. What you can protect under state law is what you can protect under Bankruptcy (ratifies state exemption clauses)a. This also permits strongly held differences to come together and still do a bankruptcy law.b. W: Bankruptcy offers discharge of debt. In order to get discharge, this is what you should give up.

Argues for uniform exemption to trump state law exemptions.

II. States can opt out of federal exemptions (so there is no floor for exemptions) a. W: recommends flooring and ceiling for these exemption amounts.

22

III. First Legal Issue: Classification Problemsa. Is a bus a car?b. Is a diamond ring wearing apparel?c. What is an annuity?d. Is the thing you have within the specified categories?

IV. Second legal issue: What do you do when things transform? a. You sold your house, then went to escrow, then into a check, then into a new house. Is it continuously

a homestead trxn? What if you are in the middle of the transaction? (i.e. holding the money as cash). When are the proceeds of something that is clearly exempt also exempt?

V. Third issue: Many of the exemption statutes are dollar capped. But 7 have unlimited home exemption. Some have unlimited health aids. Or unlimited tools of the trade. Whenever they are capped, you have to ask what is the value of the property.a. What makes valuation so hard is because you really aren’t really selling anything.

i. Is this fair market value (listed with a real estate agent)?ii. Liquidation value (seized by creditor and sold)

iii. Before Expenses of sale?iv. After expenses of sale?

b. Assume you are in a state with $50,000 homestead agent. Say you could get $300,000 if sold by a real estate agent (this is maximum). Assume $200,000 mortgage. The expenses of sale would be 9% or $27,000. If liquidated at Sheriff’s sale, would bring $200,000 (remember no one gets to see inside of it. And if you buy it, you have to get the debtor out of there.)

i. If you have a $50,000 exemption, do you force sale of the house? 1. You either allow the person to keep too much property or too little property.

c. You have backwards incentives here. i. For example, state might have $5K exemption for cars. Let’s suppose the value on this car

ranges from $18K-$22K. It has a $10,000 security interest on it. 1. If the car has been scratched, in a fender bender, what is the value? Perhaps $14K -

$18K. a. If it is in debtor’s exemption, then keeps it.

d. In most states, businesses have zero exemption. e. Partial exemption

i. Suppose you end up with a $300,000 valuation on the house. $50K exemption, $27K cost of sale, $200K mortgage.

1. Cost of sale first2. Mortgage next3. Left over $23K paid back to debtor. (b/c still within the exemption)

VI. What happens if you go into bankruptcy?a. Exemptions look like they did before. Same issues as state courts. Sometimes federal courts certify

questions to state courts. VII. Problem 10.1

a. If they go into Chap 7, what exemption options will they have and what would you advise them to do? i. § 522(b): both spouses have to take the same exemption for jointly filed cases—either federal

or state.1. What Chris filed first? And then Lisa buys stuff and then make it look hard to join

estates together and then file for bankruptcy? 2. It is also possible that they each left half of the house unprotected.

ii. Start with their biggest asset, worth $100,000 with $23,000 in equity.1. The homestead is $17, 245 (§ 522(d)(1)). If you don’t use the homestead exemption,

it is a spillover that you can use on anything up to $8,725. a. Lisa could save $17, 245 of the home plus $925 in (d)(5).

i. Chris would claim the remainder in value of the house ($5,575), plus he would get a spillover over of $8725 + his $925. (see § 522(d)(5)).

23

2. People who don’t have a home at all get $8725 dollars plus the $925 (§ 522(d)(5))3. Under § 522(d)(6), they can bring both exemptions together (includes debtor and

dependent) and combine the spillovers in (d)(5).

VIII. Problem 10.4-10.5a. Estate planning has been inconsistent—same advice, different results. b. Exemptions: pick possible categories (like in houses), but then you can sink all your money intoc. Why don’t we just go to money caps?

i. But people have different trades and money distributions.

24

10/06/03

I. Problem 12 cont’d: $750 pre-petition attorneys’ fees? a. One is a question of § 507 priority for unsecured creditors (even if allowed as administrative expense),

but another is a requirement of reasonableness.i. What does it take for the attorney of the debtor to get an allowable claim?

1. The nurse only had to show the real contract price. IRS only has to show that is what they assessed.

ii. They review attorneys especially-- § 503(b)(2)—for a reasonable amount under § 330(a)(1). 1. § 330(a)(1): reasonable compensation for services on attorneys

iii. Why is there the reason of reasonableness? (contracts signed as part of bankruptcy process)1. Whose money is being spent here?

a. Whoever are the residual claimants of the game (so it really comes out of the creditor’s pocket). So creditors get claims at face value (assuming debtor was negotiating in best interest) but when negotiating for bankruptcy, the game changes—in effect the debtor is spending the residual creditors’ money.

i. Nobody argues with someone who has the last lifeline (debtors will spend the general unsecured money to get the lifeline)

1. Like decedent’s estate: attorneys’ fees must always be disclosed and approved by court: there really is not someone negotiating on behalf of the decedent

iv. Suzan Smith negotiable note could be a § 507(a)(7) priority for alimony, support; otherwise ordinary business loan (no priority); or part of property settlement, which gets no priority loan.

1. Why special priority?a. Making sure that children get taken care of, ex-spouses get taken care of

(stop the echo effect)b. Also, the children are terrible risk spreaders (they only have 1 parent)c. Congress, as part of proposed Bank’cy reform, proposes moving them from

§ 507(a)(7) to a § 507(a)(1)….should all women’s groups love them?i. If they move ahead of administrative fees, you are really moving

ahead of the trustees. That is very bad for you because they don’t have incentive to work for you…the trustees will say that all the money goes to you and his expenses will not be paid.

2. What else would you want to know to evaluate this plan?a. How much is actually left for the unsecured creditors. § 507(a)(1) priorities

actually don’t get that much anyhow.b. Trustee gets $4,000 (a)(1), insurance $750 (a)(1), nurse $4650, George-- $300(a)(6)—all the rest may

go to Susan if alimony/child support and then. Taxes would get about 60% on the dollar and general unsecured gets nothing (a)(8)’s get pro-rata. If susan is not priority creditor, then the general unsecured bumps up, the taxes will get paid in full ($21,534)….$16,000 left for general unsecured.

i. Who objects to Susan’s priority claim? (trustee b/c acts on behalf of general unsecured creditors)

ii. Who objects to calculation of taxes? (Trustee and also debtor because the tax is not dischargeable).

II. Dischargeabilitya. Property of the estate and automatic stayb. Then secured creditors who continue to take liensc. Exempt property for debtord. Money left over for distribution (§ 507 first), and then § 502e. 3 kinds of claims in terms of dischargeability:

i. § 523:1. If alimony, not dischargeable (§ 523(a)(5))2. If business debt, dischargeable

25

3. If property settlement, under § 523(a)(15), then dischargeabilty depends on:a. Who is more miserable (there really is no standard is)

i. How bad off is he if he has to pay? How bad off is she if she doesn’t get the money?

b. Why this standard of fairness?i. It tells the judge to do whatever is fair.

ii. Do something that kind of looks right under the circumstances. f. What else is nondischargeabile?

i. § 523(a)(1): Taxes (those under § 507(a)(2), (a)(8))ii. § 523(a)(2): if you lie about your financial condition in writing, then that debt is not

dischargeable. 1. Why not dischargeable?

a. If a debt is non-dischargeable, then out of bankruptcy, then still have to pay it. In other words, is bankruptcy a way to get off the hook for fraud? NO

2. § 523(a)(2)(C): luxury goods on consumer debt is not dischargeableiii. § 523(a)(3): If you don’t list creditors, you don’t discharge those debtsiv. § 523(a)(4): fiduciaries involved in embezzlement not dischargedv. § 523(a)(5): alimony/support

vi. § 523(a)(6): for intentional torts OR selling collateral (for malicious and willful injury by the debtor to another entity)

vii. § 523(a)(7): fines are not dischargeable (automatic stay, § 362, does not apply to criminal proceedings)

1. Once you get dinged, you don’t get out in bankruptcyviii. § 523(a)(8): student loans are not dischargeable

1. afraid that people are feeding on the public trough of student loans2. students don’t have any collateral; lenders are not lending based on collateral. 3. So very difficult to discharge student loans

ix. § 523(a)(9): drunk drivers who hit others 1. MADD got their interests taken care of it.

x. § 523(a)(10): If you don’t get a discharge the first time, stays not dischargeable forever.xi. § 523(a)(15): separation agreements

xii. § 523(a)(16): condo feesxiii. § 523(a)(17): court filing feesxiv. § 523(a)(18): when they give out welfare checks, they make them sign over support rights

from the father as a condition for getting support from the state. That one will be non-discharageable. It’s the dad who wasn’t paying. The state can collect the same way that the mother could.

1. What’s the downside to putting this provision in?a. It could impair the ability to pay the child support (he would now have 2

nondischargeable claims—1 to the state and 1 to the mother)III. § 727

a. § 727(a)(1): The court shall grant the debtor a discharge unless the debtor is not an individuali. Not as harsh on business as individual

ii. This is Chapter 7, you don’t discharge any debt because the corporation doesn’t exist anymore.

1. It is a liquidated entity.b. § 727(a)(2): If you have a 727(a)(2), you don’t get ANY discharge at all including any non-

fraudulently obtained debt. i. What’s happening in (a)(2): you get someone under fraudulent conveyances, you can keep

someone from any discharge in bankruptcyc. § 727(a)(3): the debtor has concealed, destroyed, mutilated, falsified, or failed to keep or preserve any

recorded information, including books, documents, records, and papers d. § 727(a)(4): Self-discipling, if you lie in bankruptcy, then can’t get discharge. e. § 727(a)(5): fail to explain satisfactorily any loss of assets or deficienciesf. § 727(a)(6): self-actuating (refused to obey any lawful order of the court; or taking the immunity)g. § 727(a)(7): try to catch serial filers

26

h. § 727(a)(8): Keeping you from refiling until 6 years have lapsed (so only once in seven years)i. What’s the new market in the credit industry? (who is the best customer Bank 1 is looking for

today?) People who just got out of bankruptcy (because can’t file for bankruptcy for 6 years). i. § 727(a)(9): someone who got a discharge in Chap 12/13, and if you pay off your creditors, you don’t

have to wait 6 years (or 70% and in good faith).j. § 727(a)(10): voluntary waiver of discharge (as part of the settlement of litigation, you can agree to

waive instead of being found guilty under another provision)

IV. Problem 14.1a. Can MM refuse to give Peter Service?

i. Yes. But there is protection against discriminating against bankrupts? § 525 scope is narrow 1. But MM can’t say we’ll let you now if you paid. They have violated § 524(a)—post

discharge injunction to collect.ii. What is MM doing here?

1. We really don’t know.iii. What can you do about it?

1. You chew up what would have been 2 months of payments in attorneys’ fees. iv. MM can’t say that “we’ll let you in unless you pay.” You can still get to point B with a wink

and an elbow.b. Why do we draw a line between reaffirmation and post-bankruptcy attempt to collect?

i. Reaffirmations can only occur between the date of filing petition and discharge.1. Reaffirmations don’t work before filing of the petition. (otherwise you would have

them contracting around bankruptcy—no contract waivers not to enter into bankruptcy).

2. Can do it during bankruptcy, but can’t do it after bankruptcya. Want to give them a fresh start. b. It devalues the value of discharge under bankruptcy.

i. Otherwise, the creditors, 2 or 3 months after bankruptcy, would hound you to pay your debts.

c. Part of the cleanup in 1978 was to make the reaffirmation during this time period, because at least you are still within the system (and have lawyer to approve it).

i. We don’t want debtors to make an improvident promise.V. Problem 14.3

a. under § 722 doesn’t require that an attorney must sign it.b. Why do you get attorney protection for a § 524 (reaffirmation) but not a §722 (redemption)

i. You are paying off your secured debt (total amount of loan here is $18,000 and you have to pay $15,000 to redeem).

1. The policy that is being articulated in § 722 is you get to redeem for less than face value of the note (value of the collateral) BECAUSE secured creditor could repossess and sell it off for value of the collateral…so creditor loses ability to pull it out but would get what he would have gotten anyways but what creditor really lost is the $3,000 by either getting you to reaffirm or continue to paying it off until the lien is removed.

a. You can use this provision to break this leverage off. b. The trick is that debtors really don’t have the cash to do it.

10/07/03

I. Problem Set 15.1a. § 362(d)(1): once stay is lifted, the secured creditor could then go seize the car under state law

(repossess, get a judicial judgment)….can claim lack of adequate protectioni. § 361 defines alternative ways of providing adequate protection:

1. (1) cash payment2. (2) a replacement lien

27

ii. Is Comp-u-Store adequately protected?1. Adequate protection means protection against loss in value (that value will not

decline)2. Comp-u-store needs under § 362(d)(1),

a. A lift of the stay orb. Alternatively,

i. A lien on other property for the value of the expected loss (§ 361(1))—this keeps value of collateral up

ii. Cash payments 1. For example, things depreciate over time so add cash

payments to keep time. iii. Suppose court doesn’t buy loss in value to lift the stay on Comp-u-store’s behalf.

1. then can argue for loss of the collateral itself (i.e. power surge). b. Could you argue § 362(d)(2)?

i. Must show: No equity in the property and not necessary to reorganization1. So can’t use it, because debtor has equity, § 362(d)(2) is inapplicable.

ii. Why do we have this provision?1. Here, estate doesn’t have interest in the property. So if estate has no equity in the