banking finance in india - wegweiser gmbh berlin | is one of the founding board members of npci...

TRANSCRIPT

Banking & Finance in IndiaSandeep Uppal,

Managing Director & Head of Commercial Banking, HSBC India

Agenda – Banking & Finance in India

Banking Sector & Regulatory Issues for MNCs

Payment Landscape

Foreign Exchange & Hedging Market

Financing Options

HSBC in India

3

Banking Sector & Regulatory Issues for MNCs

Banking Overview

Reserve Bank of India

Scheduled Banks (232)

Commercial Banks (163) Co‐operatives (69)

Foreign Banks (34)

Public Sector Banks (26)

Pvt Sector Banks (21)

Regional Rural Banks (82)

Source: RBI

Top 5 Banks as per Advances:

1. Stan Chart2. Citibank3. HSBC4. Deutsche5. RBS

Top 5 Banks as per Advances:

1.State Bank of India2. PNB3. Canara Bank4. IDBI Bank5. Bank of Baroda

Top 5 Banks as per Advances:

1. ICICI Bank2. HDFC Bank3. Axis Bank4. Yes Bank5. Federal Bank

Indian banks as change agents

Indian banks are seen as being more than just financial intermediaries

Providing jobs and funding infrastructure development

Agents of Social Change. Increasing financial inclusion by serving all sections of the population.

Safe repositories of public deposits, suppliers of credit to support enterprise and fuel economic development in the micro, small and medium enterprises

Supporting agriculture sector through financing

Accounts

• Branch/ Liaison Offices require prior RBI approval – typically 8-10 weeks if all documentation correct. Minimum criteria must be met (e.g. parent must be in existence for 5 years).

• Non-Resident Account is allowed – subject to specific conditions and Regulatory approval (if required)

• Currency is Regulated for Capital Account Transactions

• Capital Infustion (FDI) is generally freely permitted – Mandatory filings within timelines

• Parental Loans (In FCY termed ECBs) are Permitted subject to specified tenors, end uses and values with an interest rate caps.

Lending

• Onshore Foreign currency borrowings only allowed for trade transactions (pre/ post shipments).

• Offshore External Commercial Borrowings (foreign currency term loans - ECBs) only allowed for certain purposes (e.g. expansion, new capex).

• Financial due diligence and justification for use of facility required

• Erosion of capital by a certain amount requires reporting to the BIFR Board

Regulatory Issues for Multinationals

7

Payment Landscape in India

The Evolving Banking Landscape in India – RBI Initiatives

Year of Introduction

1995 2004 2005 20082007 2009 - 12

Electronic Clearing Service

(ECS)

Electronic Fund Transfer

(EFT)

Real Time Gross Settlement

(RTGS)

National Electronic

Fund Transfer(NEFT)

ChequeTruncation

Service (CTS)

National Electronic Clearing Service (NECS)

Speed Clearing(SCS)

Mandatory E-payment of

Govt dues / taxes

High-value cheque clearing

Phased out

Fee Standardisation

for electronic transactions

National Financial Switch

connecting all ATM’s in India- free usage across banks

Introduction of Electronic Clearing in India

Real-time Settlement for HV Transfers

Batch Settlement for Low Value High Volume

Transfers

Increased Efficiency in Outstation

Clearing

Centralised Bulk Electronic Clearing,

further efficiency in o/s clearing

DisincentivisePaper Clearing

Cheques / Drafts

Primarily Paper-based

Clearing

Upto 1994

*

The Financial Settlement Infrastructure of India is undergoing a rapid change Exponential growth in volumes of RTGS/NEFT settlements Electronic transactions now represent 90% of payments by value

Source: RBI Monthly Bulletin May 2012

HSBC is one of the founding board members of NPCI (National Payments Corp of India)

New Frontiers ‐ Emerging Banking Channels

Mobile Banking Transactions- Rapid expansion in the use of mobile phones as a mode of communication has created new opportunities for banks to use this channel for banking transactions. Active mobile connection base is 683 Million as at Mar’12 (source: TRAI & MediaNama)- Guidelines allow mobile banking transactions both for e-commerce and money transfer Purposes, subject to limits prescribed by each bank.

Pre-paid Payment Instruments- Pre-paid payment instruments facilitate purchase of goods and services against the value stored on such instruments via smart cards, magnetic strip cards, internet accounts, internet wallets, mobile accounts, etc

- To bring in transparency and facilitate orderly growth of this payment product, RBI issued guidelines in 2009 on issuance and operations of pre-paid payment instruments.

Point of Sale (PoS) terminals- The number of Point of Sale (PoS) terminals in India is now more than eight times the number of ATMs, offering added convenience to customers and merchants. Over 99,000 ATMs are deployed in India as of Jun’12 (Source: RBI)

- The Bank has permitted small value cash withdrawals at PoS terminals. Electronic/online mode of payments

- Intermediaries like aggregators and payment gateway service providers handle customer funds.

- Guidelines were issued in 2009, which prohibit the use of such funds by these intermediaries to ensure the safety of the funds.

- Banks holding these balances are to ensure timely onward settlement of funds to public utility companies/ merchants.

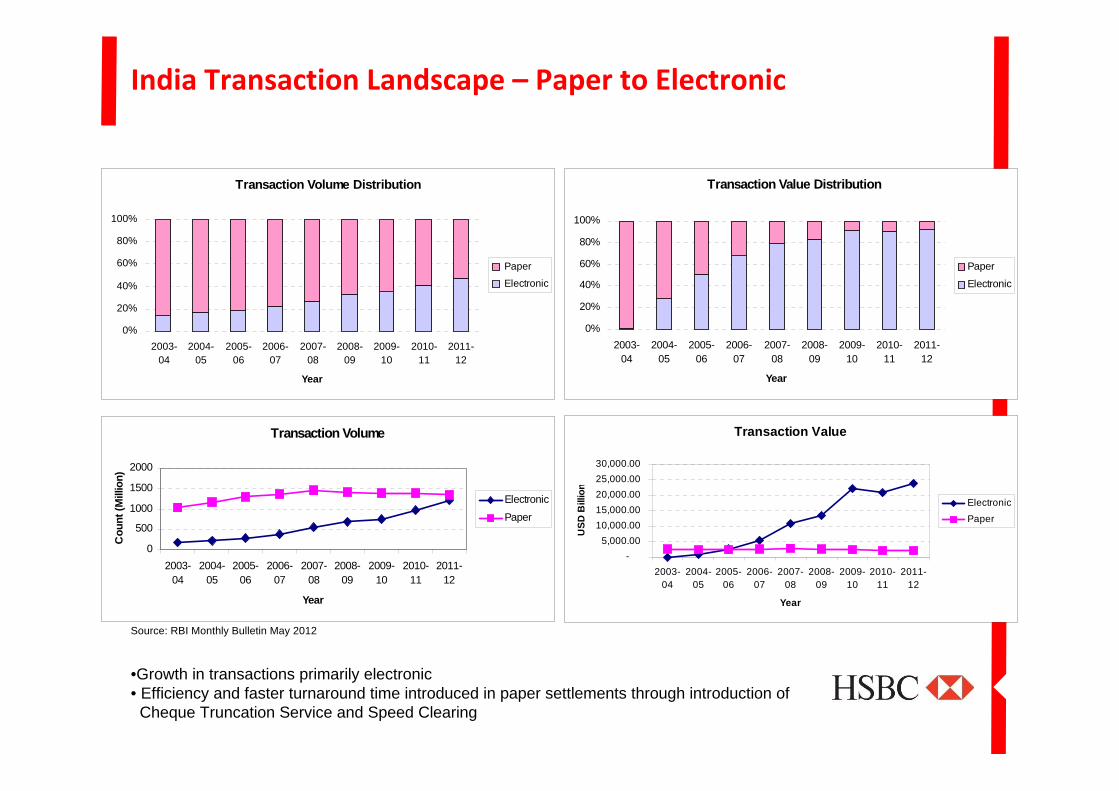

India Transaction Landscape – Paper to Electronic

Source: RBI Monthly Bulletin May 2012

•Growth in transactions primarily electronic• Efficiency and faster turnaround time introduced in paper settlements through introduction of

Cheque Truncation Service and Speed Clearing

Transaction Volume

0

500

1000

1500

2000

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

Year

Cou

nt (M

illio

n)

ElectronicPaper

Transaction Value

-5,000.00

10,000.0015,000.0020,000.0025,000.0030,000.00

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

Year

USD

Bill

ion

ElectronicPaper

Transaction Volume Distribution

0%

20%

40%

60%

80%

100%

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

Year

Paper Electronic

Transaction Value Distribution

0%

20%

40%

60%

80%

100%

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

Year

Paper Electronic

11

Foreign Exchange & Hedging Market in India

FX Market ‐ Characteristics

Spot & Forwards

Very liquid spot market – estimated daily volume of USD 4 billion

Over 15 active interbank counterparties

Very liquid forwards market up to 5 Years

Typical Interbank Lot Size is USD 1-3 Mio

Interbank Spreads for a lot size of USD 1 Mio is INR 0.0100 to 0.0200

Options

An active Options market with 6-7 main Interbank counterparties

Market is liquid up to 5 Years but quotes up to 7 Years

Market Characteristics

Market Timing from 9:00 AM to 4:30 PM IST

Active involvement of the Central Bank (Reserve Bank of India)

Reserve Bank prohibits any international speculative access to the Rupee

RBI declares a daily USD/INR RBIB benchmark spot rate which is polled from randomly

chosen banks in a random 5 minute period between 11.45 AM to 12.15 PM

Market Participants

FX Market

Corporates

Interbank

Central Bank

Institutional

FII

Retail

Rates Market

Corporates Interbank

InstitutionalFII

Offshore Participants – FX

As an Investor:

Permissible Trades:

1. Capital infusion 2. Hedging of Dividends 3. Hedging of translation risk from investment in India

Products:

1. Spot2. Forwards - Fixed date or Settlement anytime during a window period3. Plain Vanilla FCY Put(Call) INR Call(Put) Options (*HSBC India is also positioned to arrange for Escrow services on your capital inflows and

outflows) Regulations:

1. For equity inflow:1. Firm underlying and any necessary approvals a must2. Equity Inflow hedge can be executed for a tenor of upto six months3. If cancelled, hedge cant be rebooked for same underlying and exchange gains if any

will have to be foregone2. Dividends can be hedged once declared3. For translation risk hedging:

a. Market value of investment can be hedgedb. If cancelled, hedge cannot be rebooked for the

same underlying

Onshore Participants – FX

As an Operating Company:

Permissible Trades:

1. To hedge FX risk against transaction Specific Documentation:a. To hedge FX risk on account of current account exposuresb. To hedge foreign currency interest/principal repaymentsc. To hedge translation risk from investments made overseas

2. To hedge FX risk against Past Performance – for trade in goods and services

Products:

1. Spot2. Forwards - Fixed date or Settlement anytime during a window period3. Plain Vanilla Options4. Cost reduction structures viz. Collars, Call/Put Spreads etc. (Additional eligibility criteria)

Regulations:

1. Tenor and Amount of hedge should not exceed the valid underlying and quarterly statutory auditor certificates on the same

2. Signed hard copy of specific underlying to be submitted to the bank within 15 calendar days of executing the Fx trade

3. Contracts can be rolled over, but not cancelled and rebooked4. Corporates are prohibited from selling naked options

Key Regulations – FX ForwardsRBI regulations require proof of underlying currency risk in order to book a forward contract. This can be in the form of a specific underlying or past performance

Specific Underlying Currency Risk - The underlying documents need to be submitted with the bank within 15 days. The documents need to equal or exceed

the forward booked in the amount and tenor of the hedge.

- Contracts once cancelled cannot be rebooked under the same underlying document except under certain specified conditions stipulated by RBI.

- In case of failure to comply, penalties include : i) cancellation of contract with the loss passed on to the client but not the gain if any, or ii) requirement of production of underlying documents prior to dealing in future

Past Performance - Past Performance route allows booking of forwards based on exports/imports by the company in previous years.

- The past performance limit for exporters is defined by the average of the previous three financial years actual export turnover or the previous year’s actual export turnover, whichever is higher. For imports, the limit is 25% of this number

- Contracts booked under PP must be delivered and cannot be cancelled

- There is no restriction on the tenor of the hedge under the past performance route.

- Quarterly statutory auditor certificates stating that the contracts outstanding at any point in time with all banks during the quarter did not exceed the value of the underlying exposures/past performance limit are required to be submitted.

Interest Rate Products

A person resident in India who has borrowed foreign exchange may enter into the following for hedging / transforming

their loan exposure :

An Interest Rate Swap or

A Currency Swap or

A Coupon Swap or

An Interest Rate Cap or Collar (purchases) or

A Forward Rate Agreement (FRA) contract

Regulations:

Booking and Cancellation:

Contract does not involve the Rupee – Freely cancelled and rebooked

Contract involves Rupee – If cancelled once shall not be rebooked

Final approval has been accorded or loan identification/registration number issued by the RBI for borrowing in foreign

currency

Notional principal amount of the hedge does not exceed the outstanding amount of the foreign currency loan

Maturity of the hedge does not exceed the unexpired maturity of the underlying loan

Relevant Master Circulars for Regulations

Master Circular on Risk Management and Interbank Dealings

Master Circular on External Commercial Borrowings and Trade Credit

Master Circular on Foreign Investments into India

Master Circular on Direct Investment by Residents in Joint Venture (JV)/Wholly Owned Subsidiary (WOS) Abroad

All available on the RBI website under Notifications Section

19

Financing Options in India

Short Term Financing OptionsTenor Pricing Security Documentation

Working Capital Demand Loan

As per trade cycle assessment

Floating rate linked to base rate of the bank.

Charge on current assets including stock and book debts

Loan Agreement and Demand Promissory Note

Receivables Factoring

As per trade cycle assessment

Floating rate linked to base rate of the bank.

Charge on current assets including stock and book debts

Factoring Agreement, Demand Promissory Note and Notice of Assignment

Vendor Finance As per trade cycle assessment

Floating rate linked to base rate of the bank.

Charge on current assets including stock and book debts

Demand Promissory Note

Buyer's Credit (availed outside India)

Max tenor - 360 days from shipment

Pricing is linked to 3/6 months LIBOR. Pricing restricted to max of L+200bps for import of raw materials

Charge on current assets including stock and book debts

TFGA, Demand Promissory Note and Counter Indemnity

Pre/Post Shipment Credit

Pre-shipment – Max tenor 180 days. Can be rolled over for further 180days with prior approval from RBI.

Pricing is linked to 3/6 months LIBOR. Pricing restricted to max of L+210bps

Charge on current assets including stock and book debts

Demand Promissory Note

Long Term Financing Options

Amount Tenor Pricing Security Documentation

INR Term Loan

No restriction Bullet repayment at the end of [ ] years. Amortizing structure is also possible

Floating rate linked to base rate of the bank.

Charge on fixed assets of the company with cover of 1.25x

Loan Agreement and Demand Promissory Note

FCY Loan No restriction, subject to availability of FCY funds

Bullet repayment. Amortizing structure is also possible –subject to availability of FCY funds for the said tenor

Pricing is linked to 3/6 months LIBOR. The borrower has full flexibility to hedge the currency and/or interest rate risk

Charge on fixed assets of the company with cover of 1.25x

Loan Agreement and Demand Promissory Note

Capex Buyer's Credit (availed outside India)

No restriction Max tenor of 3 years from date of shipment

Pricing is linked to 3/6 months LIBOR. The borrower has full flexibility to hedge

Charge on fixed assets of the company with cover of 1.25x

TFGA, Demand Promissory Note and Counter Indemnity

ECB (availed outside India)

Maximum of USD 20M for an avgmaturity of 3 years.

Average maturity in excess of 5 years if the amount is more than USD 20 M

For average maturity period of 3 to 5 yrs: Max 300 bps over 6 months LIBOR

For average maturity period more than 5 years : Max 500 bps over 6 months LIBOR

Charge on fixed assets of the company with cover of 1.25x

ECB Agreement

22

HSBC in India

HSBC in IndiaHSBC in India

Over 150 years of presence in India

A network of 50 branches across 29 commercial cities

A full service bank offering term and working capital finance, trade, cash management, treasury services, investment banking, asset management, insurance, private banking and personal banking

Total Assets of USD 20 Bn in India which includes USD 6 Bn of Advances (source: RBI – FY 2011)

Total Deposits of USD 12 Bn in India (source: RBI – FY 2011)

Kolkata

Mumbai

Chennai

Coimbatore

New Delhi

AhmedabadVadodara

Pune

Nagpur

Visakhapatnam

Trivandrum Kochi

Noida

Gurgaon

BangaloreMysore

Hyderabad

Indore

Patna

Raipur

Nashik

Surat Guwahati

Chandigarh

Jaipur

Ludhiana

24

Thank You

Disclaimer

This document is prepared, issued and presented by The Hongkong and Shanghai Banking Corporation Limited ("HSBC") based on information obtained from sources it believes to be reliable but which it has not independently verified. Whilst care has been taken in preparing such information, HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

The presentation is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Except as specifically indicated, the expressions of opinion are those of HSBC only and are subject to change without notice. The information is provided for general information purposes of its customers only and is neither intended to provide professional advice nor as an offer or solicitation and should not be relied upon in that regard. If it is received by a customer of an affiliate of HSBC, its provision to the recipient is subject to the terms of business in place between the recipient and such affiliate. Appropriate professional advice should be sought where necessary before taking any action based on the information. Information in this document is confidential. Distribution of this document or information in this document (whether by reproduction, storage in a retrieval system, or transmission, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise), without the prior written permission of HSBC, to any person other than an original recipient (or to such recipient’s advisors) is prohibited. This document remains the property of HSBC and on request this document, and all other materials provided by HSBC relating to proposals contained herein, must be returned and any copies destroyed. The issue and presentation of this document shall not be regarded as creating any form of contractual relationship between HSBC and the recipient(s).Neither HSBC nor any of its directors, officers or employees make any representation or warranty expressed or implied as to the reliability, accuracy or completeness of any of the information contained herein. While this presentation has been prepared in good faith neither HSBC nor any of its directors, officers or employees shall have any responsibility or liability whatsoever in respect of any statements or omissions here from. Any liability is accordingly expressly disclaimed by HSBC, its directors, officers and employees.

© Copyright The Hongkong and Shanghai Banking Corporation Limited 2012. ALL RIGHTS RESERVED

No part of this presentation may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, without the prior written permission of HSBC.