banking business performance and...

TRANSCRIPT

BANKING BUSINESS PERFORMANCE AND PRIORITIES BGEO Investor Day 9 November 2017 Tbilisi, Georgia Speaker: Kaha Kiknavelidze, CEO, Bank of Georgia

1

CONTENT

Banking industry highlights

Banking business targets and priorities

Banking business performance update – 3Q17 & 9M17

Q&A

Macroeconomic overview

2

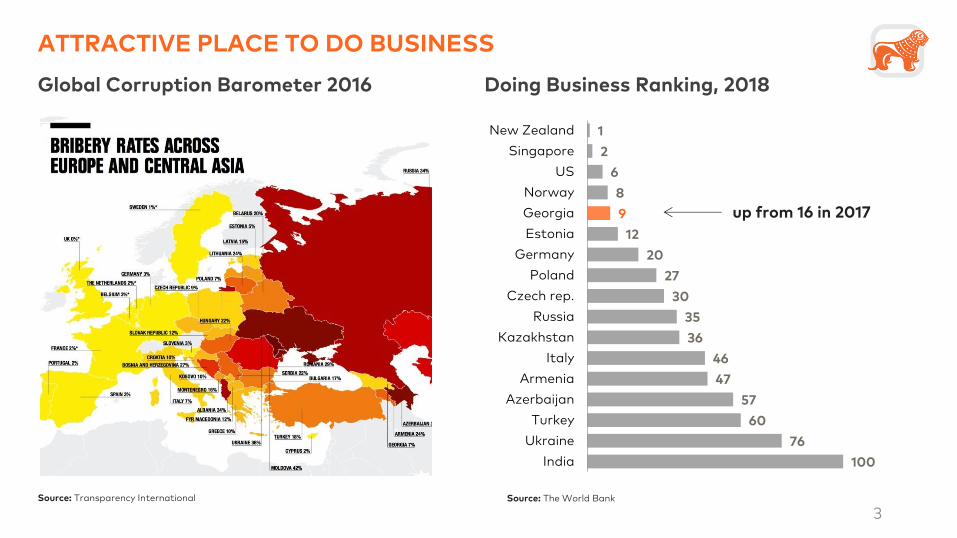

ATTRACTIVE PLACE TO DO BUSINESS

Global Corruption Barometer 2016

Source: Transparency International

Doing Business Ranking, 2018

1

2

6

8

9

12

20

27

30

35

36

46

47

57

60

76

100

New Zealand

Singapore

US

Norway

Georgia

Estonia

Germany

Poland

Czech rep.

Russia

Kazakhstan

Italy

Armenia

Azerbaijan

Turkey

Ukraine

India

up from 16 in 2017

Source: The World Bank

3

DIVERSIFIED ECONOMY BY SECTORS AND REGIONS

Diversified GDP structure, 2016 Diversified economic linkages, 2016

Industry

17.1%

Trade

16.3%

Transport &

commun.

10.1% Agriculture

9.3%

Public

administration

9.1%

Construction

8.3%

Real estate

6.6%

Healthcare

5.8%

Financial

interm.

4.0%

Hotels &

restaurants

2.8%

Other

10.7%

EU

15.4%

Russia

8.0%

Turkey

5.8%

Azerbaijan

4.0%

Armenia

2.6%

Ukraine

1.0%

Other

countries

12.7%

Exports, FDI, remittances and

Tourism by country as % of

GDP

Source: GeoStat Source: GeoStat, GNTA, NBG, G&T calculations

• Two largest sectors (trade and industry) accounting for just 33% of GDP

• EU accounts for one third of overall external earnings

• Deepening trade relations to new large markets (EU and China) are expected to broaden export base

4

HIGHER BASELINE GROWTH OF THE ECONOMY

Historical GDP Growth, Georgia vs. Region

IMF’s GDP growth projections, 2018-22 average

Source: IMF

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2010 2011 2012 2013 2014 2015 2016 2017F

Georgia CIS

Eastern Europe

4.9%

3.8% 3.7% 3.5% 3.5% 3.3% 3.3% 3.3% 3.1% 2.8%

2.6% 2.4%

1.5%

0%

1%

2%

3%

4%

5%

6%

Ge

org

ia

Mo

ldo

va

Ukra

ine

Tu

rke

y

Ka

za

kh

sta

n

La

tvia

Arm

en

ia

Lit

hu

an

ia

Est

on

ia

Bu

lga

ria

Az

erb

aija

n

Cz

ech

Re

p.

Ru

ssia

5

POTENTIAL FOR CONTINUED PRODUCTIVITY IMPROVEMENT

Contribution to growth, 2006-16 Employment and GDP by sector, 2016

Capital stock

2.2%

Labor force

0.7%

TFP growth

2.0%

Source: GeoStat, G&T calculations Note: Total Factor Productivity (TFP) determines how efficiently and intensely the inputs (capital, labor) are utilized in production

Source: GeoStat

Agriculture

Agriculture

Services

Services

Manufacturing Manufacturing

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Employment GDP

6

LARI’S FLEXIBLE EXCHANGE RATE REGIME

Limited and efficient FX interventions Exchange rate remains competitive

Source: NBG

140

-120

80

160

40 27 60

45

-243

60

140

-90

-40

-300

-250

-200

-150

-100

-50

0

50

100

150

200

1Q14

2Q

14

3Q

14

4Q

14

1Q15

2Q

15

3Q

15

4Q

15

1Q16

2Q

16

3Q

16

4Q

16

1Q17

2Q

17

3Q

17

NBG purchased

US$ 130mn YTD

US$ sale

US$ purchase

80

90

100

110

120

130

140

80

90

100

110

120

130

140

Ja

n-0

3

Se

p-0

3

Ap

r-0

4

No

v-0

4

Ju

l-0

5

Fe

b-0

6

Se

p-0

6

Ma

y-0

7

De

c-0

7

Ju

l-0

8

Fe

b-0

9

Oct-

09

Ma

y-1

0

De

c-1

0

Au

g-1

1

Ma

r-12

Oct-

12

Ju

n-1

3

Ja

n-1

4

Au

g-1

4

Ma

r-15

No

v-1

5

Ju

n-1

6

Ja

n-1

7

Se

p-1

7

REER Jan03=100

7

CONTENT

Banking industry highlights

Banking business targets and priorities

Banking business performance update – 3Q17 & 9M17

Q&A

Macroeconomic overview

8

ROOM FOR FURTHER CREDIT GROWTH

Source: NBG Source: Central Banks, IMF, as of 31 Dec 2016

Banking sector loan portfolio growth Banking Penetration (Sector Loans to GDP)

84.9%

74.7%

64.6%

62.1%

57.9%

56.9%

55.7%

53.2%

48.1%

41.4%

Estonia

Serbia

Russia

Lithuania

Latvia

Turkey

Georgia

Bulgaria

Armenia

Ukraine

• Loan portfolio increased 16.0% y/y excluding FX effect in Sep-17

0%

10%

20%

30%

40%

50%

60%

0%

10%

20%

30%

40%

50%

60%

Ja

n-1

4

Ma

r-14

Ma

y-1

4

Ju

l-14

Se

p-1

4

No

v-1

4

Ja

n-1

5

Ma

r-15

Ma

y-1

5

Ju

l-15

Se

p-1

5

No

v-1

5

Ja

n-1

6

Ma

r-16

Ma

y-1

6

Ju

l-16

Se

p-1

6

No

v-1

6

Ja

n-1

7

Ma

r-17

Ma

y-1

7

Ju

l-17

Se

p-1

7

GEL-denominated loans, % change y/y

FX-denominated loans, % change y/y (exc. FX effect)

Total loan portfolio, % change y/y (exc. FX effect)

9

PRUDENTLY MANAGED BANKING SECTOR

Source: NBG Source: IMF

Gradual de-dollarization with NBG’s 10-point plan

One of the lowest levels of NPLs worldwide (latest 2017 data)

55%

60%

65%

70%

75%

80%

55%

60%

65%

70%

75%

80%

Ja

n-1

1

Ma

y-1

1

Se

p-1

1

Ja

n-1

2

Ma

y-1

2

Se

p-1

2

Ja

n-1

3

Ma

y-1

3

Se

p-1

3

Ja

n-1

4

Ma

y-1

4

Se

p-1

4

Ja

n-1

5

Ma

y-1

5

Se

p-1

5

Ja

n-1

6

Ma

y-1

6

Se

p-1

6

Ja

n-1

7

Ma

y-1

7

Se

p-1

7Loan Dollarization Deposit Dollarization

16.4% 16.2%

13.7% 13.7%

12.4% 11.8%

11.5% 10.7%

9.7% 8.3%

6.8% 6.2% 6.1%

5.6% 5.4%

4.9% 4.1% 4.0% 3.9%

3.5% 3.5%

3.1%

PortugalMoldovaCroatiaBelarus

BulgariaIreland

Bosnia & Herz.Kazakhstan

RussiaRomaniaArmenia

KosovoMacedonia

SpainHungary

LithuaniaPoland

Czech Rep.France

GeorgiaLatviaTurkey

10

REGULATORY CHANGES (1/2)

Liquidity Coverage Ratio (LCR)

Basel III Macroprudential Tools

Deposit Insurance Scheme

- Effective from 1 September 2017

- Total LCR >=100%, LC >=75%, FC >=100%

- Effective from 10 August 2017

- Caps on PTI and LTV ratios introduced

- Effective from 1 January 2018

- Insured deposits - up to GEL 5,000

- No material impact expected

- RWA increase in 2018: ~GEL 77mln

- Tier I capital: ~7bps increase

- Additional insurance expense in 2018: ~GEL 4mln

- Cost of funds increase: ~4bps

DESCRIPTION

Larisation Initiatives

- Local currency denominated loans up to 39% in

Sep-17 from 30% a year ago

- Effective 15 January 2017

- Ban on FC lending - loans up to GEL100,000

IMPACT

1

2

3

4

11

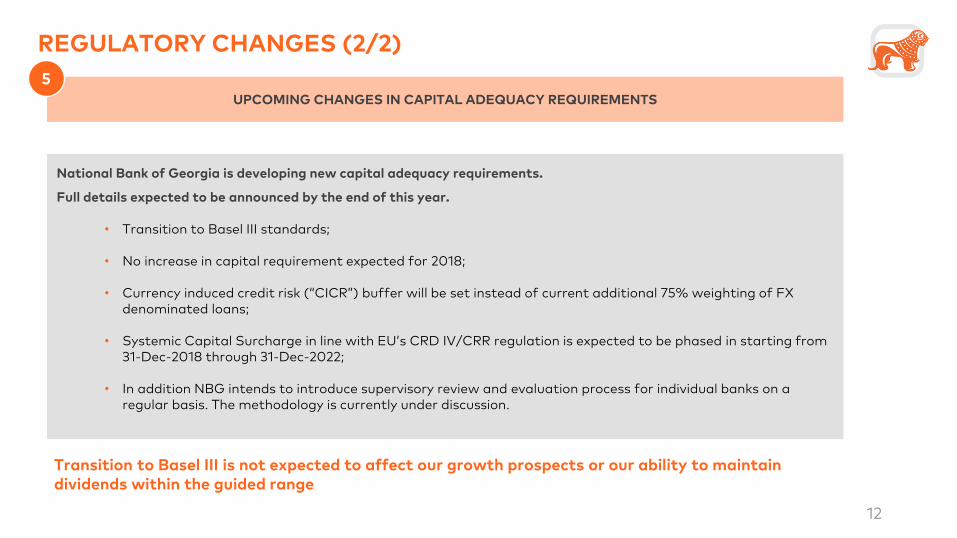

REGULATORY CHANGES (2/2)

UPCOMING CHANGES IN CAPITAL ADEQUACY REQUIREMENTS

5

National Bank of Georgia is developing new capital adequacy requirements.

Full details expected to be announced by the end of this year.

• Transition to Basel III standards;

• No increase in capital requirement expected for 2018;

• Currency induced credit risk (“CICR”) buffer will be set instead of current additional 75% weighting of FX denominated loans;

• Systemic Capital Surcharge in line with EU’s CRD IV/CRR regulation is expected to be phased in starting from 31-Dec-2018 through 31-Dec-2022;

• In addition NBG intends to introduce supervisory review and evaluation process for individual banks on a regular basis. The methodology is currently under discussion.

12

Transition to Basel III is not expected to affect our growth prospects or our ability to maintain dividends within the guided range

CONTENT

Banking industry highlights

Banking business targets and priorities

Banking business performance update – 3Q17 & 9M17

Q&A

Macroeconomic overview

13

STRONG LOAN BOOK GROWTH

GROWING SHARE OF RB LOANS

RB LOAN BOOK’S SHARE TARGET OF 65% ACHIEVED

*Other mainly includes BNB, GLC and Banking Business eliminations

1,613 2,067 2,796

3,902 3,287

4,541 1,833 2,179

2,211

2,395

2,083

1,994

3,567

4,442

5,367

6,682

5,716

6,951

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2013 2014 2015 2016 Sep-16 Sep-17

RB CIB Other*

CAGR 19.5%

68.4% 60.2 % 60.9% 55.0% 48.2% 46.0%

-4.3%

+38.2%

GE

L m

illio

ns

14

21.6%

…AND DEPOSIT GENERATION

GROWING SHARE OF RB DEPOSITS

1,528 1,539 2,393

2,838 2,312

3,284

1,612 1,950

2,618

2,918

2,588

3,266

3,141 3,489

5,011

5,756

4,900

6,550

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015 2016 Sep-16 Sep-17

Current accounts & demand deposits Time deposits

+26.2%

+42.0%

GE

L m

illio

ns

47.1% 45.3% 44.8% 39.6% 40.4% 36.4%

33.7%

CAGR 21.6%

15

YEAR OF DE-DOLLARISATION

LOANS & LOAN YIELDS

4,016 4,157 4,261

1,700 2,423 2,690

5,716

6,580 6,951

14.1% 14.3% 14.3%

3Q16 2Q17 3Q17

Loans to customers, GELLoans to customers, FCCurrency blended loan yield

3,728 4,187 4,508

1,172 1,468

2,042 4,900 5,655

6,550

4.7%

4.8% 4.8%

3Q16 2Q17 3Q17

Client deposits and notes, GEL

Client deposits and notes, FC

Cost of Funds, currency blended

CLIENT DEPOSITS & COST OF FUNDS

GE

L m

illio

ns

GE

L m

illio

ns 30%

70%

37%

63%

39%

61%

24%

76%

26%

74%

31%

69%

16 Share in total loan book Share in total deposits

STRONG COMPETITIVE POSITION

CLIENT DEPOSITS

LOANS TO INDIVIDUALS DEPOSITS TO INDIVIDUALS

* Excluding Credo Bank, which registered as a bank in 1Q 2017 Source: NBG

31.7%

38.2%

4.6% 4.4% 4.7%

16.3%

0%

10%

20%

30%

40%

50%

BOG TBC ProCredit Liberty VTB Others

GROSS LOANS

1.4 1.8 2.5

3.3 2.8

3.8

29.3% 29.0%

32.4% 34.9% 34.3% 36.4%*

0%

10%

20%

30%

40%

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2013 2014 2015 2016 Sep-16 Sep-17

BOG loans to individuals BOG market share

33.5%

38.6%

3.4% 7.0% 5.2%

12.3%

0%

10%

20%

30%

40%

50%

BOG TBC ProCredit Liberty VTB Others

1.4 1.8

2.4 3.0 2.6

3.4

29.9% 30.3%

33.2% 33.0% 33.2% 34.2%*

-5%

5%

15%

25%

35%

45%

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2013 2014 2015 2016 Sep-16 Sep-17

BOG deposits to individuals BOG market share

GE

L b

illio

ns

GE

L b

illio

ns

17

129 129 138 158 161 160 168

396

489

49 48 56 66 53 52 55

154

160

178 177 194

224 214 212 223

550

649

0

100

200

300

400

500

600

700

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 9M16 9M17

Net interest income Net non-interest income

SOLID BANKING REVENUE GROWTH

+14.9%

+5.3%

+18.1%

GE

L m

illio

ns

REVENUE

18

STABLE MARGINS

Resilient spread

7.4% 7.5% 7.3% 7.6% 7.4% 7.3% 7.3%

5.0% 4.8% 4.7% 4.6% 4.6% 4.8% 4.8%

14.4% 14.1% 14.1% 14.4% 14.0% 14.3% 14.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

NIM Cost of Funds Loan yield, annualised

NIM, LOAN YIELD & COST OF FUNDING

19

27.9 29.5 30.7 36.8 30.2 31.4 33.1

88.1 94.7

17.4 16.5 21.6

27.7 19.7 19.3 19.6

55.5 58.6

48.5 48.7 56.5

66.6

52.9 51.7 55.4

153.7 160.0

0

20

40

60

80

100

120

140

160

180

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 9M16 9M17

Net fee and commission income Net banking foreign currency gain Net other banking income

SOLID BANKING REVENUE GROWTH G

EL

mill

ion

s

NET NON-INTEREST INCOME

20

-1.9%

+7.1%

+4.1%

23.0 26.2 26.8

33.1

27.0 28.6 29.4

76.0

85.0

0

10

20

30

40

50

60

70

80

90

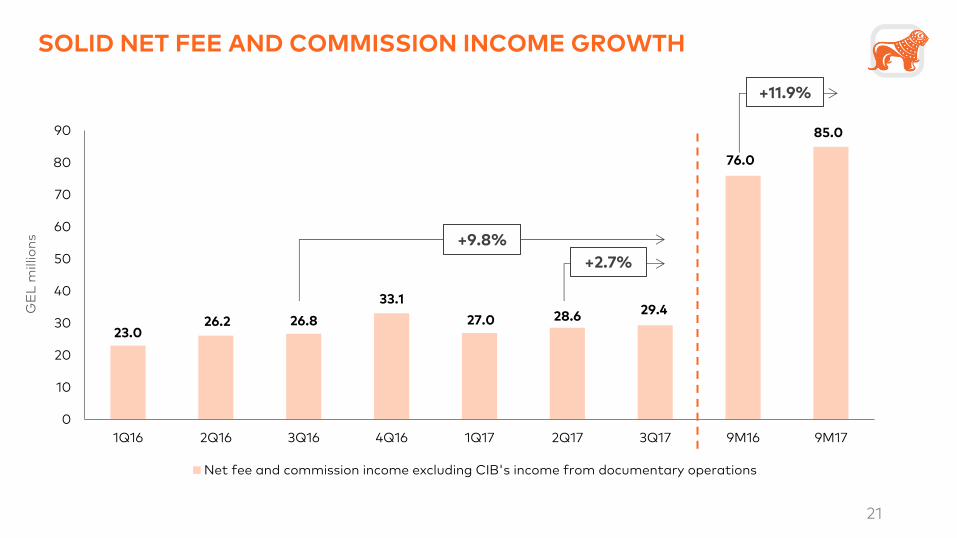

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 9M16 9M17

Net fee and commission income excluding CIB's income from documentary operations

SOLID NET FEE AND COMMISSION INCOME GROWTH G

EL

mill

ion

s

21

+9.8%

+2.7%

+11.9%

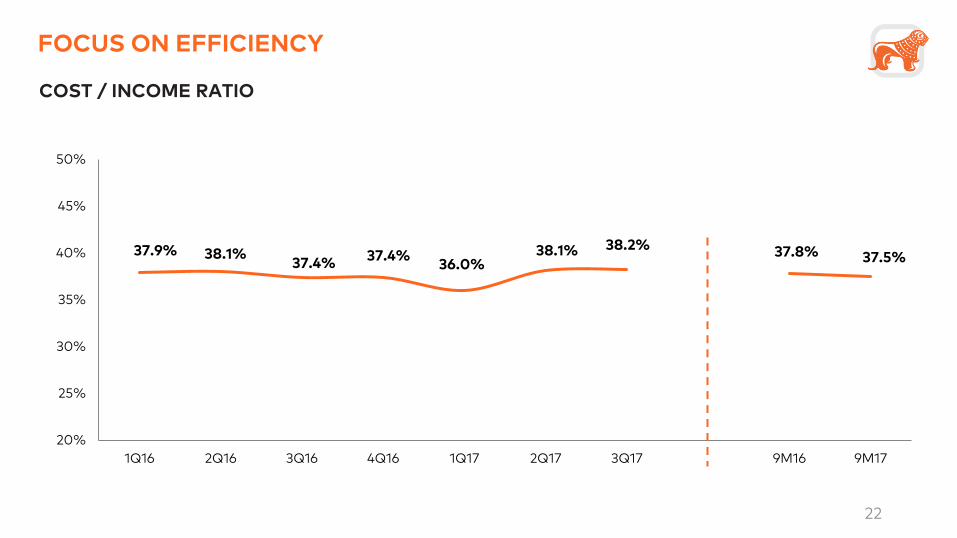

37.9% 38.1% 37.4%

37.4% 36.0%

38.1% 38.2% 37.8% 37.5%

20%

25%

30%

35%

40%

45%

50%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 9M16 9M17

FOCUS ON EFFICIENCY

COST / INCOME RATIO

22

IMPROVED LOAN PORTFOLIO QUALITY (1/2)

COST OF RISK RATIO, QUARTERLY

COST OF RISK RATIO, YEAR TO DATE

1.3% 1.2%

2.7% 2.7%

2.2% 2.2%

0%

1%

2%

3%

4%

5%

2013 2014 2015 2016 9M16 9M17

2.3% 2.0%

2.3%

4.2%

2.4% 2.2% 2.0%

0%

1%

2%

3%

4%

5%

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

23

86.0% 85.8% 86.5% 86.7% 87.1% 90.2%

93.6%

60%

70%

80%

90%

100%

110%

120%

130%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

IMPROVED LOAN PORTFOLIO QUALITY (2/2)

NPL COVERAGE RATIO

24

RETAIL BANKING DRIVING GROWTH AND PROFITABILITY

33.4% 24.3% 13.0% 24.5%

Quarterly

ROAE:

+21.2% -31.2% +7.1%

PROFIT:

GE

L m

illio

ns

86

68

92 19 5

0

10

20

30

40

50

60

70

80

90

100

3Q16 RB CIB BNB &

other

3Q17

Nine-month

29.1% 22.4% 17.1% 23.7%

+21.8% 0.0% +17.0%

GE

L m

illio

ns

224

172

262

78 12

0

50

100

150

200

250

300

9M16 RB CIB BNB &

other

9M17

Growth (y-o-y):

25

STRONG LIQUIDITY

LIQUIDITY RATIO

BOG Standalone

178

789

418

843 35.0%

46.2%

37.7%

44.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

Dec-14 Dec-15 Dec-16 Sep-17

Excess liquidity Liquid assets / liabilities ≥ 30%

26

GE

L m

illio

ns

10.1% 10.2% 11.0%

9.1% 10.1%

10.6% 11.1%

15.8% 15.5% 16.2%

14.4% 15.2% 15.6%

16.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

Tier I Capital Adequacy Ratio Total Capital Adequacy Ratio

EXCELLENT CAPITAL ADEQUACY POSITION

CAPITAL ADEQUACY RATIOS

BOG Standalone

8.5% NBG Tier I CAR

Min Requirements: 10.5% NBG Total CAR

27

CONTENT

Banking industry highlights

Banking business targets and priorities

Banking business performance update – 3Q17 & 9M17

Q&A

Macroeconomic overview

28

RESULTS IN 2017 vs. OUR TARGETS & PRIORITIES

De-concentrate corporate loan book Top-10 borrowers: 10% 11.9%

Increase Mass Retail product to client ratio 3.0 1.7

Grow retail share in loan book 65% 60.2%

ROAE 20%+

Targets

22.4%

9M16

Retail banking growth 20%+ 19.5%

NPL coverage ratio 80-120% 86.5%

10.4%

1.8

68.4%

23.7%

9M17

38.2%

93.6%

Increase number of Solo clients To 40,000 16,964 28,492

Cost of risk c.2.0% 2.2% 2.2%

Become a regional private banking hub AUM: GEL 2.5bln GEL 1.4bln GEL 1.8bln

KEY TARGETS

PRIORITIES

FINANCIAL METRICS

Cost / income c. 35% 37.8%

NIM 7.25% - 7.75% 7.4%

37.5%

7.3%

Progress

1

2

1

2

3

4

1

5

2

3

4

29

KEY MILESTONES IN 2017 (1/4)

Retail Transformation

Optimised branch operating model - effective client-centric service

‣ Reduced number of mass retail branches from 141 before transformation to 114 currently

Pro-active interaction with clients

‣ 141% increase in the number of products sold

‣ 5.6% increase in number of transactions per month through flagship branches

v

Plus Loyalty Programme

Status levels achieved by using multiple banking products, which translates into exclusive benefits

More than 400,000 program members since launch in July 2017

22.9% of enrolled customers have upgraded vs. the 10% initial target

30

KEY MILESTONES IN 2017 (2/4)

Public Transportation Contract

Sole provider of payment support services to the public transportation network for another ten years

+2.1 million transactions per month

Additional revenue stream from other banks’ card transactions

New Mobile Banking App

Volume of transactions: +55% q-o-q

Number of transactions: +47% q-o-q

Number of active users: +15% q-o-q

Android,

121,900

iPhone,

66,777

31

188,677 mBank downloads since June

DIGITAL PENETRATION

TRANSACTIONS THROUGH NEW mBANK

63

90 94

122

190

700

855

980

1,233

1,812

3Q16 4Q16 1Q17 2Q17 3Q17

Volume of transaction (millions)

Number of transactions (thousands)

DIGITAL VS NON-DIGITAL TRANSACTIONS

6.6

7.6 7.6 8.2 8.1

9.0 9.2

4.3 4.3 4.2 4.0

3.2 3.1 2.9

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17

Through digital channels Through tellers

32

KEY MILESTONES IN 2017 (3/4)

Solo Club

A membership group within Solo offering exclusive access to Solo’s products ahead of other Solo clients at a higher fee

Premium banking lifestyle

Launched in 2Q17 – currently 1,527 members

American Express Platinum credit card exclusive offering

Switch from traditional statistical models to machine learning

Underwriting

‣ 77% fully automated decisions ‣ <5min for 85% of applications processed ‣ 105,000 applications processed per month

Targeted campaigns though different channels

‣ 116 campaigns ‣ 205,000 sold products

33

Data Analytics

KEY MILESTONES IN 2017 (4/4)

BANK OF GEORGIA 500MLN GEL INNAUGURAL LARI EUROBOND ISSUANCE

Listing Irish Stock Exchange

GEL 500 million, 3 year, 11.00% Eurobonds payable in U.S.$

Notes

Notes rating Moody’s Ba3 / Fitch BB-

Joint Lead Managers / Bookrunners

J.P. Morgan, Renaissance Capital

Co-Manager JSC Galt & Taggart

ALLOCATION BY GEOGRAPHY

USA

46%

UK

30%

Georgia

14%

Germany

5%

Other Europe

3% Nordics

2%

ALLOCATION BY INVESTOR TYPE

Asset

Managers

71%

Multilateral

Institutions

22%

Banks /

PBs

7%

34

RETAIL BANKING CLIENT-CENTRIC, MULTI-BRAND STRATEGY

Brands & target

segments Emerging Retail Mass Retail Mass Affluent

1 2 3

Selected Operating

Data (9M17)

Strategic Focus

To

tal

No

of

Cli

en

ts

(ex

clu

din

g M

SM

E)

2

,09

6,8

43

514,183 clients

1,554,168 clients

28,492 clients

Double number of transactions

Product/client ratio growth to 3.0

Client growth to 40,000

Business Model

Product centric

cross-selling

Focused on transactional

banking

360° financial

planning

Advisory based 5-step approach

SOLO Lifestyle

1%

35

69%

23%

734 806 824 889 1,054

1,245

1,452

2,000 2,141

2,255

-

300

600

900

1,200

1,500

1,800

2,100

2,400

2,700

3,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 9M17

OVER 2 MILLION RETAIL CLIENTS

NUMBER OF RETAIL BANKING CLIENTS

Aggressive client acquisition phase is over We target growth through increasing engagement of existing clients

CAGR 13.7%

Th

ou

san

ds

36

MSME & CORPORATE BANKING STRATEGIC HIGHLIGHTS

Brands & target

segments

Selected Operating

Data (9M17)

Strategic Focus

MSME Micro, Small and Medium

Business

4

Corporate Investment Banking Business

5

Resume loan portfolio growth

Manage concentration risk

Grow fee business

Attract new talents

Increase number of clients

Increase profitability per client

Organize SME around customers

instead of products

New products and services for SME

clients

MSME Loan book GEL 1.6 billion

CIB Loan book GEL 2.1 billion

MS

ME

& C

IB L

oa

n

Bo

ok

GE

L 3

.7 b

illi

on

43% 57%

37

BUILDING BLOCKS TO BECOME THE FINANCIAL SERVICES HUB

Wealth Management

Brokerage

Research

Corporate Advisory

Strong international presence: Israel (since 2008), UK (2010), Hungary (2012), Turkey (2013) and Cyprus (2017)

AUM of GEL 1,818 million, up 29.1% y-o-y

Diversified funding sources: • Georgia 35% • Israel 14% • UK 4% • Germany 2% • Other 45%

Wide product coverage

Exclusive partner of SAXO Bank via While Label structure, that provides highly adaptive trading platform with professional tools, insights and world-class execution

Sector, macro and fixed income coverage International distribution

Bond placements

“First in corporate bond placements in the Caucasus Region in 2016” – Cbonds

More than GEL 260mln local bonds placed in 2017

Sample Transactions

Corporate advisory platform Proven track record of more than 15 completed

transactions over the past 8 years

Wealth Management & Brokerage

38

UPDATED GUIDANCE

Become a regional private banking hub AUM: GEL 2.5bln

Increase Mass Retail product to client ratio 3.0

ROAE 20%+

Targets

Total Banking Business loan book growth 15% - 20%

NPL coverage ratio 80-120%

Increase number of Solo clients To 40,000

Cost of risk (through the cycle) 2.0%

KEY TARGETS

PRIORITIES

FINANCIAL METRICS

Cost / income ~35%

NIM 7%+

Dividend payout ratio 25-40%

1

2

1

2

3

1

2

3

4

5 39

BANKING BUSINESS SUMMARY

#1 in terms of Net Interest Income #1 in terms of Net Fee and Commission Income #1 most cost efficient with 37.5% cost/income ratio #1 in terms of Net Income

40

OUTSTANDING ROAE

19.9% 20.0%

21.3%

21.7%

22.4%

23.7%

18%

19%

20%

21%

22%

23%

24%

2013 2014 2015 2016 9M16 9M17

ROAE

41

QUESTIONS? BGEO Investor Day 9 November 2017 Tbilisi, Georgia

42

DISCLAIMER – FORWARD LOOKING STATEMENTS

This presentation contains forward-looking statements, including, but not limited to, statements concerning expectations, projections, objectives, targets, goals, strategies, future events, future revenues or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, competitive strengths and weaknesses, plans or goals relating to financial position and future operations and development. Although BGEO Group PLC believes that the expectations and opinions reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations and opinions will prove to have been correct. By their nature, these forward-looking statements are subject to a number of known and unknown risks, uncertainties and contingencies, and actual results and events could differ materially from those currently being anticipated as reflected in such statements. Important factors that could cause actual results to differ materially from those expressed or implied in forward-looking statements, certain of which are beyond our control, include, among other things: currency fluctuations, including depreciation of the Georgian Lari, and macroeconomic risk; corporate loan portfolio exposure risk; regional tensions; regulatory risk; cyber security, information systems and financial crime risk; investment business strategy risk; and other key factors that we have indicated could adversely affect our business and financial performance, which are contained elsewhere in this presentation and in our past and future filings and reports, including the 'Principal Risks and Uncertainties' included in BGEO Group PLC's Annual Report and Accounts 2016 and in its Half Year 2017 Results announcement. No part of this presentation constitutes, or shall be taken to constitute, an invitation or inducement to invest in BGEO Group PLC or any other entity, including any future entity such as BGEO Investments PLC or Bank of Georgia PLC, and must not be relied upon in any way in connection with any investment decision. BGEO Group PLC undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent legally required. Nothing in this presentation should be construed as a profit forecast.

43