bank borrowing.pdf

TRANSCRIPT

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 1/23

INSTITUTE OF DEVELOPING ECONOMIES

IDE Discussion Papers are preliminary materials circulated

to stimulate discussions and critical comments

IDE DISCUSSION PAPER No. 144

Bank Borrowing and Financing of

Medium-sized Firms in Indonesia

Miki HAMADA†

March 2008

†Institute of Developing Economies

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 2/23

Abstract

The improvement of financial intermediation functions is crucial for a robust banking

system. When lending, banks have to cope with such problems as information

asymmetry and adverse selection. In order to mitigate these problems, banks have to

product information and improve their techniques of lending. During the 1998

financial crisis, Indonesia’s banking system suffered severe damage and revealed that

the country’s banking intermediation functions did not work well. This paper examines

the financial intermediation functions of banks in Indonesia and analyzes the

importance of bank lending to firms. The focus is on medium-sized firms, and

“relationship lending”, one of the bank lending techniques, is used to examine financial

intermediation in Indonesia. The results of logit regressions show that the relationship

between a bank and a firm affects the probability of bank lending. The amount of

borrowing and collateral are also affected by a firm’s relationship with a bank. When

viewed from the standpoint of relationship lending to medium-sized firms, Indonesian

banks cannot be criticized for any malfunction of financial intermediation.

Keywords: relationship lending, financial intermediation function, medium-sized firms,

Indonesia,

JEL classification: G21, N25, G30

The Institute of Developing Economies (IDE) is a semigovernmental,

nonpartisan, nonprofit research institute, founded in 1958. The Institute

merged with the Japan External Trade Organization (JETRO) on July 1, 1998.

The Institute conducts basic and comprehensive studies on economic and

related affairs in all developing countries and regions, including Asia, the

Middle East, Africa, Latin America, Oceania, and Eastern Europe.

The views expressed in this publication are those of the author(s). Publication does

not imply endorsement by the Institute of Developing Economies of any of the views

expressed within.

INSTITUTE OF DEVELOPING ECONOMIES (IDE), JETRO

3-2-2, WAKABA, MIHAMA-KU, CHIBA-SHI

CHIBA 261-8545, JAPAN

©2008 by Institute of Developing Economies, JETRO

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 3/23

Bank Borrowing and Financing of Medium-sized Firms in Indonesia

Miki Hamada†

Abstract

The improvement of financial intermediation functions is crucial for a robust banking system. When

lending, banks have to cope with such problems as information asymmetry and adverse selection. In

order to mitigate these problems, banks have to product information and improve their techniques of

lending. During the 1998 financial crisis, Indonesia’s banking system suffered severe damage and

revealed that the country’s banking intermediation functions did not work well. This paper examines

the financial intermediation functions of banks in Indonesia and analyzes the importance of bank

lending to firms. The focus is on medium-sized firms, and “relationship lending”, one of the bank

lending techniques, is used to examine financial intermediation in Indonesia. The results of logit

regressions show that the relationship between a bank and a firm affects the probability of bank

lending. The amount of borrowing and collateral are also affected by a firm’s relationship with a

bank. When viewed from the standpoint of relationship lending to medium-sized firms, Indonesian

banks cannot be criticized for any malfunction of financial intermediation.

Keywords relationship lending, financial intermediation function, medium-sized firms, Indonesia

† Institute of Developing Economies

1

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 4/23

2

1. Introduction

Financial systems in development economies are often perceived as fragile. The fragility can

be attributed to the immaturity of banking financial intermediation functions such as a deficiency of

screening ability, banks’ poor risk management, and undeveloped legal and accounting systems.

Improvement of financial intermediation is one of the most crucial issues in the development of a

country’s financial system.

When providing loans, banks have to cope with problems of asymmetric information and

adverse selection, therefore collecting information on clients and the production of information are

most important for banks. A rapid increase in non-performing loans is one of the consequences of

massive lending based on the production of insufficient information. Indonesia is a case in point.

This paper examines the financial intermediation functions in the Indonesian banking sector

and analyzes the importance of bank lending to firms. It seems that the vulnerability of the banking

sector aggravated the situation in Indonesia during the financial crisis in 1998, as indicated by the

fact that the rate of nonperforming loans rose to 58.7% in 1999. In this paper the financial

intermediation functions of banks will be evaluated from the standpoint of the relationship between

firms and banks with the focus of examination being on medium-sized firms.

2. Bank Lending to Medium-sized Firms in Indonesia

2.1 Why medium-sized firms?

During and after the 1998 financial crisis, Indonesia’s banking sector suffered serious damage.

The large depreciation of the Indonesian rupiah made the net worth of most commercial banks

inadequate. Non-performing loans rose rapidly, and the average rate for such loans at foreign

exchange banks increased to 76.9%. Major commercial banks were bailed out through capital

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 5/23

injections from the government and nationalization. At that time it was reported that 70% to 90% of

bank loans had been channeled to related companies (September 29, 1998, Jakarta Post ). This fact

raises doubts about the financial intermediation functions of Indonesian banks. Before the financial

crisis and nationalization, major private banks belonged to conglomerates or business groups.

Indonesian conglomerates had many large blue-chip companies operating in various sectors.

Therefore Indonesian banks did not need to product information for channeling loans to related

parties because information asymmetry did not exist within the business group. Thus if there were no

information problems when banks allocated loans to related companies, it is difficult to affirm

whether or not Indonesian banks have financial intermediation functions. However, how about when

lending to small and medium-sized firms? Unlike large companies, small and medium-sized firms

are not related to conglomerates, and their information varies. Thus small and medium-sized firm

lending seems to be meaningful for examining and evaluating banks’ financial intermediation

functions.

Although most bank lending is allocated to large companies, these companies have various

funding sources in addition to domestic bank borrowing. Issuing stocks and bonds on capital markets

and borrowing on international markets are other alternatives. For small and medium-sized firms,

however, financing is a major difficulty, and bank borrowing, while difficult, is the most important

external financial source for them. This is another reason for focusing on lending to small and

medium-sized firms.

Another reason lies within the context of Indonesia. Lending to small firms is not so difficult

for banks because such lending is given preferential treatment. Loans to small firms are regulated by

the central bank, and commercial banks in Indonesia are obligated to allocate 20% of their total

loans to small-scale business, up to Rp500 million (= US$56,000) per client. This preferential

treatment is called KUK (Kredit Usaha Kecil [Small Business Credit]). If a bank does not conform

3

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 6/23

to this regulation, it is penalized. On the other hand, if a bank follows the regulation, it gets a bonus.

Thus banks have incentives to lend to small firms: they avoid penalties and get bonuses

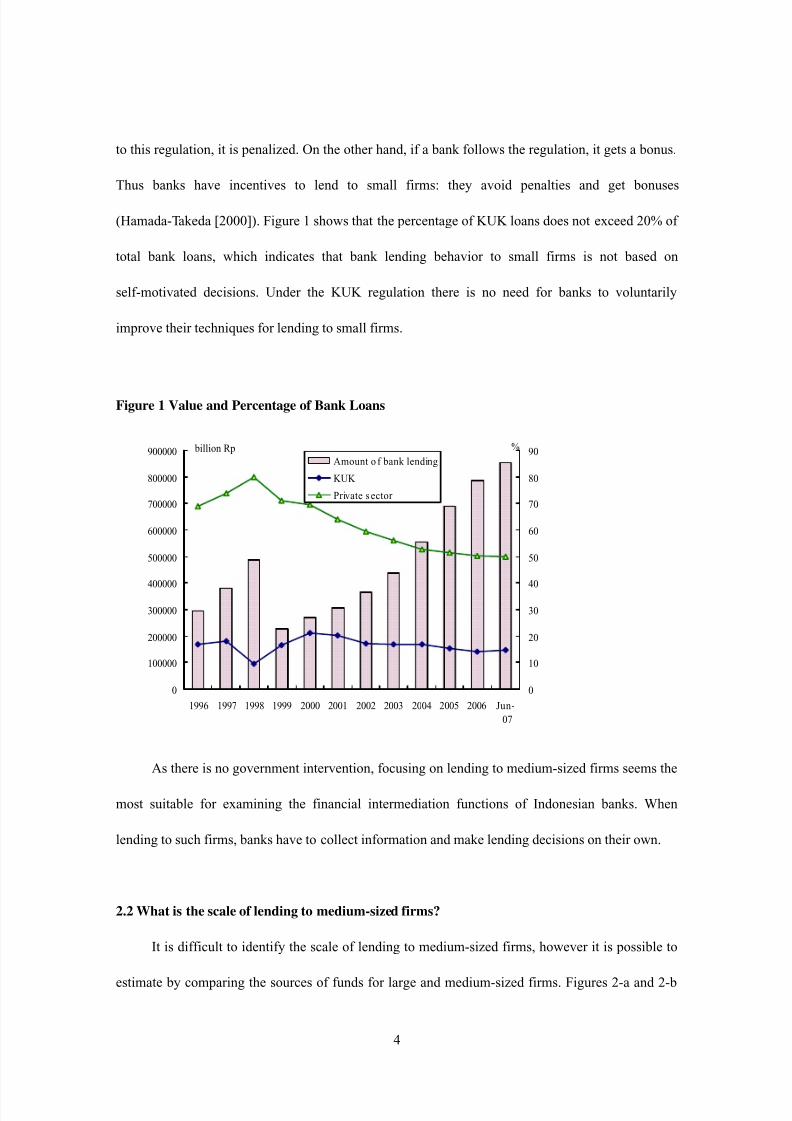

(Hamada-Takeda [2000]). Figure 1 shows that the percentage of KUK loans does not exceed 20% of

total bank loans, which indicates that bank lending behavior to small firms is not based on

self-motivated decisions. Under the KUK regulation there is no need for banks to voluntarily

improve their techniques for lending to small firms.

Figure 1 Value and Percentage of Bank Loans

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Jun-

07

billion Rp

0

10

20

30

40

50

60

70

80

90%

Amount o f bank lending

KUK

Private s ector

As there is no government intervention, focusing on lending to medium-sized firms seems the

most suitable for examining the financial intermediation functions of Indonesian banks. When

lending to such firms, banks have to collect information and make lending decisions on their own.

2.2 What is the scale of lending to medium-sized firms?

It is difficult to identify the scale of lending to medium-sized firms, however it is possible to

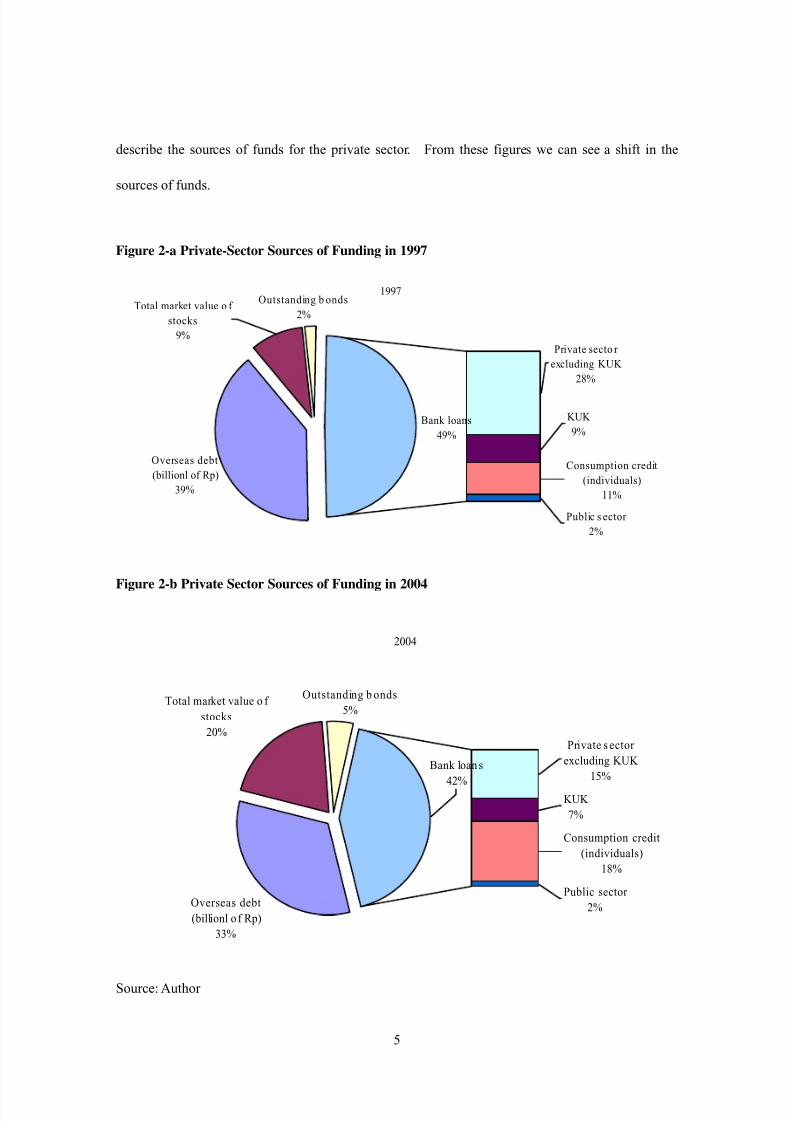

estimate by comparing the sources of funds for large and medium-sized firms. Figures 2-a and 2-b

4

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 7/23

describe the sources of funds for the private sector. From these figures we can see a shift in the

sources of funds.

Figure 2-a Private-Sector Sources of Funding in 1997

1997

Public s ector

2%

Consumption credit

(individuals)

11%

Overseas debt

(billionl of Rp)

39%

Outstanding b onds

2%

KUK

9%

Private secto r

excluding KUK

28%

Total market value o f

stocks

9%

Bank loans

49%

Figure 2-b Private Sector Sources of Funding in 2004

2004

KUK

7%

Public sector

2%

Consumption credit

(individuals)

18%

Private s ector

excluding KUK

15%

Overseas debt

(billionl o f Rp)

33%

Total market value o f

stocks

20%

Outstanding b onds

5%

Bank loans

42%

Source: Author

5

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 8/23

Before the financial crisis in 1997, massive amounts of foreign capital flowed in: 39% of

private sector capital was overseas debt; 49% was lending from domestic banks, and capital markets

accounted for 11%. After the crisis overseas debt decreased to 33%: domestic bank loans fell to 42%,

while capital markets increased to 25%.

In the two figures, “private sector excluding KUK” is regarded as bank lending to large and

medium-sized firms. The “private sector excluding KUK” decreased between 1997 and 2004 from

28% to 15% as a percentage of total sources of funds, while utilization of capital markets increased

from 11% to 25%. Conjecturing that large firms for the most part shifted from domestic bank loans

to capital markets, the current domestic bank-loan market would then be composed by and large of

medium-sized firms and some large firms unable to shift to capital markets. Thus it can be argued

that the 15% “private sector excluding KUK” lending in 2004 was mostly to medium-sized firms.

3. Relationship Lending Versus Transaction Lending

In the previous section we estimated the present scale of bank lending to medium-sized firms.

In this section we will look at bank lending techniques to these firms. Boot defined the provision of

financial services by a financial intermediary as the: 1) investment in obtaining customer-specific

information, often proprietary in nature; and 2) evaluation of the profitability of these investments

though multiple interactions with the same customer over time and/or across products (Boot[1999]).

Thus information is key to a financial intermediary.

When providing financial services, information asymmetry is a serious problem for banks

especially in the case of small and medium-sized firms because information on large firms is

relatively available. Large firms usually prepare financial statements and provide public information.

According to Udell lending techniques are based on: 1) financial statements, 2) relationship between

bank and firm, 3) credit-scored lending, 4) asset, 5) factoring, and 6) trading credit (Udell: 2004).

6

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 9/23

Among these techniques, transactions-based lending is the most major one, under which the lending

decisions are based on “hard” information that is relatively easily available like financial statement,

credit score and asset at the time of loan origination, and does not rely on the “soft” data gathered

over the course of a relationship with the borrower (Berger and Udell [2002]). While the most

important in lending to small firms is relationship lending which emphasizes the length of time in a

relationship between a bank and a firm.

The relationship between a bank and a firm has several advantages for the firm that go beyond

just borrowing. The fact of obtaining a loan from a bank improves the firm’s reputation and a longer

bank-firm relationship brings more merits to the borrower. For example, at the beginning of a

relationship, the interest rate on a loan is higher and much more collateral is required; however after

several years, the interest rate decreases and the required collateral also decreases because of the

bank’s accumulation of information on the firm. The interest rate especially is greatly affected by the

length of a firm’s relationship with a bank (Berger and Udell[1995]).

It is understandable that banks product and accumulate information through their relationships

with firms, and this mitigates the problem of information asymmetry. As required collateral

decreases proportionally with the length of a relationship, the function of collateral comes to be

regarded not as a prerequisite but a compliment of lending.

As well as being a useful technique for banks, relationship lending is also useful for small

firms. The next section examines the actual conditions of financing for medium-sized firms in

Indonesia, and the funding sources these firms prefer.

4. Financing of Medium-sized Firms

The BPS (Badan Pusat Satistik [Statistics of the Republic of Indonesia]) provides data on

large (more than 100 employees) and medium-sized (from 20 to 99 employees) manufacturing firms

7

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 10/23

covering basic information about firms, their output, value added, expenditures on inputs, sales,

investment and financing. The data are obtained through annual surveys of more than 20,000 firms.

This paper uses data for 1993, 1996, 1999 and 2001 in order to examine financing for investment.

The reasons of choosing the years 1993, 1996, 1999 and 2001 are the following. In 1993 the

largest number of firms responded to the annual survey, and the year 1993 is regarded as reflecting

very well Indonesia’s strong economy before the financial crisis. The year 1996 is expected to reflect

the bubble economy just before the crisis; the year 1999 reflects the worst economic situation just

after the crisis, and the year 2001 is expected to show the slight recovery from the damage of the

crisis.

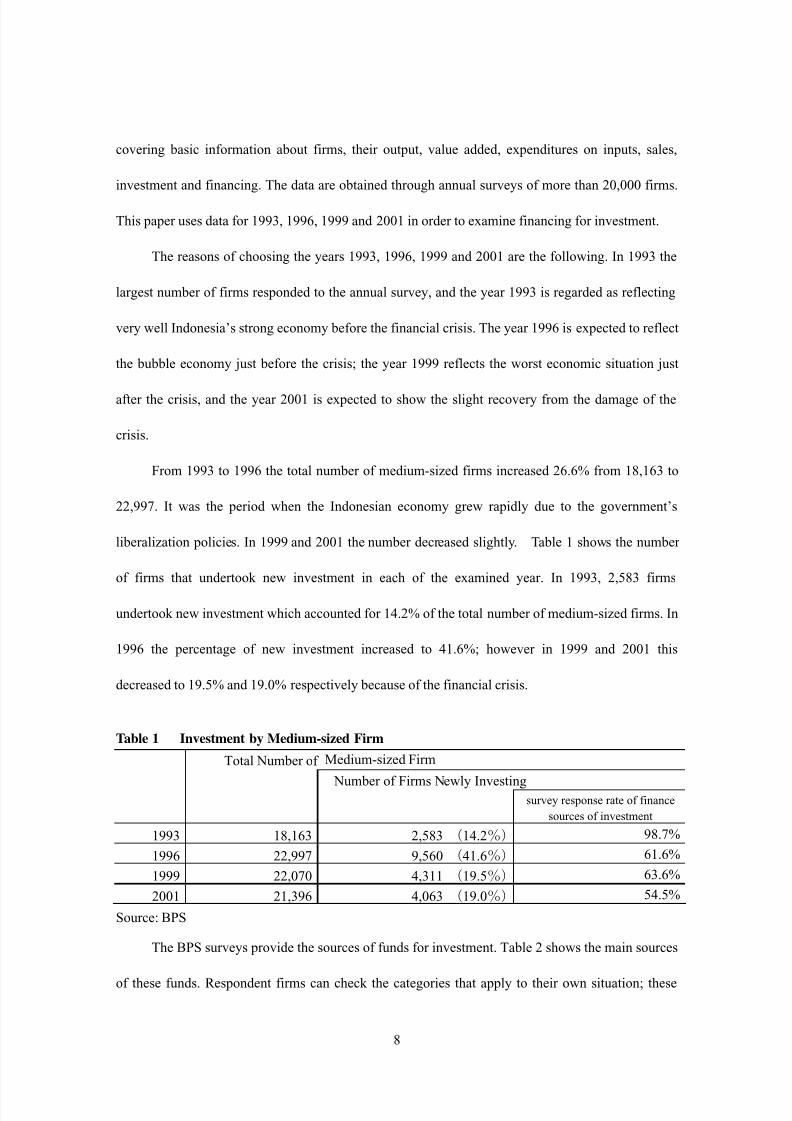

From 1993 to 1996 the total number of medium-sized firms increased 26.6% from 18,163 to

22,997. It was the period when the Indonesian economy grew rapidly due to the government’s

liberalization policies. In 1999 and 2001 the number decreased slightly. Table 1 shows the number

of firms that undertook new investment in each of the examined year. In 1993, 2,583 firms

undertook new investment which accounted for 14.2% of the total number of medium-sized firms. In

1996 the percentage of new investment increased to 41.6%; however in 1999 and 2001 this

decreased to 19.5% and 19.0% respectively because of the financial crisis.

Table 1 Investment by Medium-sized Firm

Total Number of Medium-sized Firm Number of Firms Newly Investing

survey response rate of finance

sources of investment

1993 18,163 2,583 (14.2%) 98.7%

1996 22,997 9,560 (41.6%) 61.6%

1999 22,070 4,311 (19.5%) 63.6%

2001 21,396 4,063 (19.0%) 54.5%

Source: BPS

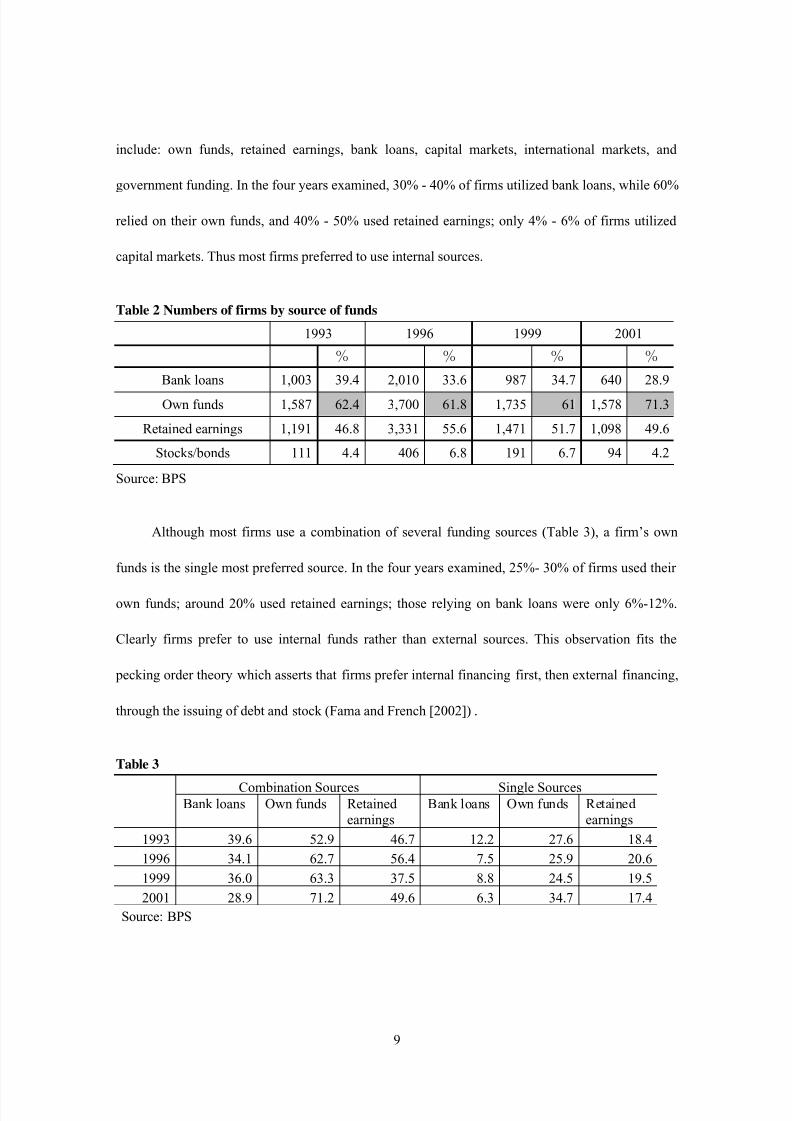

The BPS surveys provide the sources of funds for investment. Table 2 shows the main sources

of these funds. Respondent firms can check the categories that apply to their own situation; these

8

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 11/23

include: own funds, retained earnings, bank loans, capital markets, international markets, and

government funding. In the four years examined, 30% - 40% of firms utilized bank loans, while 60%

relied on their own funds, and 40% - 50% used retained earnings; only 4% - 6% of firms utilized

capital markets. Thus most firms preferred to use internal sources.

Table 2 Numbers of firms by source of funds

1993 1996 1999 2001

% % % %

Bank loans 1,003 39.4 2,010 33.6 987 34.7 640 28.9

Own funds 1,587 62.4 3,700 61.8 1,735 61 1,578 71.3

Retained earnings 1,191 46.8 3,331 55.6 1,471 51.7 1,098 49.6

Stocks/bonds 111 4.4 406 6.8 191 6.7 94 4.2

Source: BPS

Although most firms use a combination of several funding sources (Table 3), a firm’s own

funds is the single most preferred source. In the four years examined, 25%- 30% of firms used their

own funds; around 20% used retained earnings; those relying on bank loans were only 6%-12%.

Clearly firms prefer to use internal funds rather than external sources. This observation fits the

pecking order theory which asserts that firms prefer internal financing first, then external financing,

through the issuing of debt and stock (Fama and French [2002]) .

Table 3

Combination Sources Single SourcesBank loans Own funds Retained

earningsBank loans Own funds Retained

earnings

1993 39.6 52.9 46.7 12.2 27.6 18.4

1996 34.1 62.7 56.4 7.5 25.9 20.6

1999 36.0 63.3 37.5 8.8 24.5 19.5

2001 28.9 71.2 49.6 6.3 34.7 17.4

Source: BPS

9

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 12/23

5. Data and Empirical model

5.1 Data

The above discussion has showed that medium-sized firms prefer internal funding sources.

The question then is how banks determine loans. This section examines determinants of bank

lending using logit regression analysis. From the BPS data of large and medium-sized manufacturing

firms, the data for medium-sized firms in 1993, 1996 and 1999 are used. Table 4 presents the

descriptive statistics.

Table 4 Descriptive Statistics

1993 Total of 2583 firms (thousand Rp)

Average minimum maximum Std. Dev.

Employees 45 20 99 21

Output 1,167,948 3,756 60,741,006 3,958,345

Own funds 778,059 0 666,547,444 17,819,240

Bank loans 613,302 0 795,805,182 16,412,820

Retained earrings 628,952 0 640,079,853 17,809,960

Age of firms 12 0 93 13

Assets 117,003 0 50,500,000 1,464,434

1996 Total of 4448 firms (thousand Rp)

Average minimum maximum Std. Dev.

Employees 38 20 99 19

Output 737,308 3,069 101,920,749 2,754,430

Own funds 377,296 0 568,000,000 9,631633

Bank loans 58.360 0 11,080,000 450,533

Retained earrings 74,809 0 36,800,000 750.943

Age of firms 10 0 95 10

Assets n.a n.a n.a n.a

1999 Total of 1636 firms

Average minimum maximum Std. Dev.

Employees 42 20 99 21

Output 3,002,649 4,200 287,187,024 12,148,175

Own funds 954,354 0 848,250,000 21,133,012

Bank loans 430,680 0 175,000,000 5,028,543

Retained earrings 267,540 0 150,000,000 4,080,154

Age of firms 13 0 99 13

Assets 1,479,545 20 286,340,600 12,331,658

10

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 13/23

5.2 Model

Using the above data, we will examine the probability of firm borrowing . Firm i uses a

bank loan for new investment in period t .

iit iit it t i

i

i

it

uoutput year earnownloan

p

pY

++++++=

⎟⎟ ⎠

⎞⎜⎜⎝

⎛

−=

− ln

1ln

5432)1(10 β β β β β β

i p is the probability of firm i using a bank loan.

Y 1, in the case of firm i using a bank loan in t. =it

0, in the case firm i not using a bank loan in t .

1−t LOAN : dummy variable: if firm i used a bank loan in t-1, 1, not used a bank loan, 0.

=t OWN dummy variable: if firm i used own capital in t, 1, not used own capital, 0.

=t EARN dummy variable: if firm i used retained earnings in t, 1, not used retained earnings, 0.

= AGE years for operation

=t LNOUT natural logarithm of output at t

6. Empirical Results

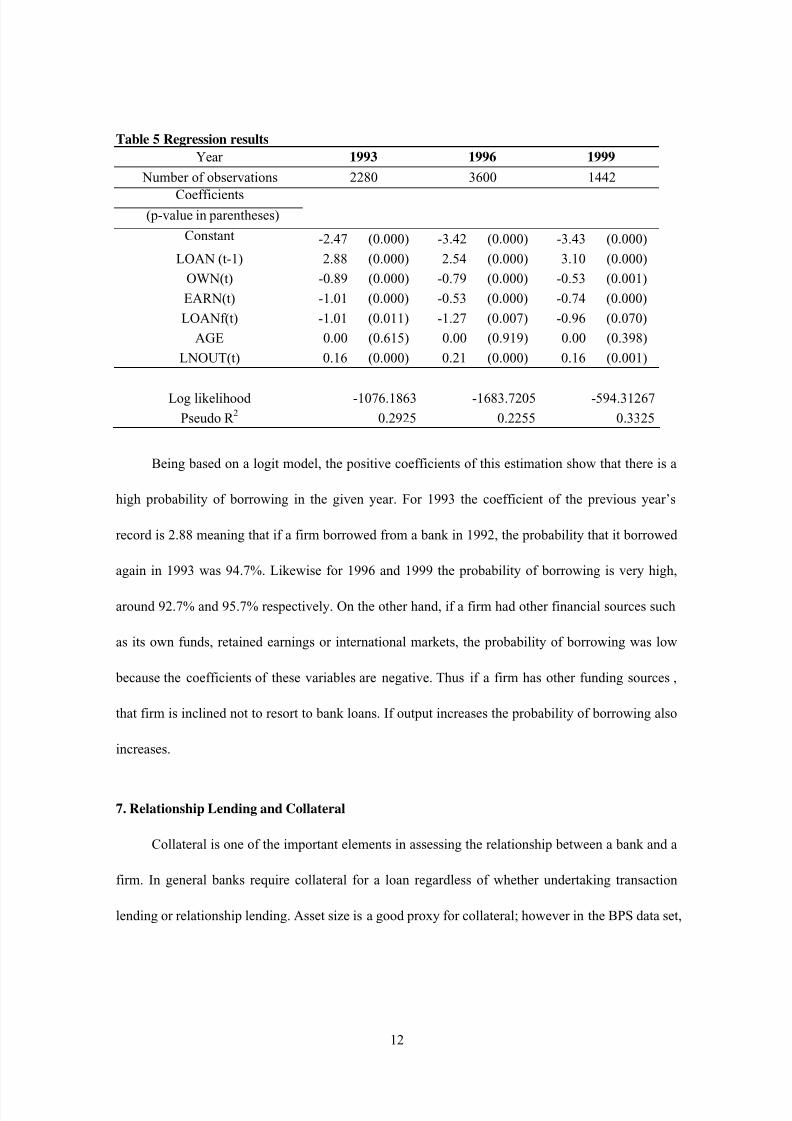

The results of the analysis show that the record of past loans has a positive effect on future

borrowing. The coefficients of all variables, except AGE, are significant in all three of the years

examined: 1993, 1996 and 1999. The coefficients of the borrowing record and the natural logarithm

of output are positive while the coefficients of own funds, retained earnings and international

borrowing are negative. AGE was expected to affect bank borrowing positively, however it turns out

not to be significant.

11

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 14/23

Table 5 Regression results

Year 1993 1996 1999

Number of observations 2280 3600 1442

Coefficients(p-value in parentheses)

Constant -2.47 (0.000) -3.42 (0.000) -3.43 (0.000)

LOAN (t-1) 2.88 (0.000) 2.54 (0.000) 3.10 (0.000)

OWN(t) -0.89 (0.000) -0.79 (0.000) -0.53 (0.001)

EARN(t) -1.01 (0.000) -0.53 (0.000) -0.74 (0.000)

LOANf(t) -1.01 (0.011) -1.27 (0.007) -0.96 (0.070)

AGE 0.00 (0.615) 0.00 (0.919) 0.00 (0.398)

LNOUT(t) 0.16 (0.000) 0.21 (0.000) 0.16 (0.001)

Log likelihood -1076.1863 -1683.7205 -594.31267

Pseudo R 2

0.2925 0.2255 0.3325

Being based on a logit model, the positive coefficients of this estimation show that there is a

high probability of borrowing in the given year. For 1993 the coefficient of the previous year’s

record is 2.88 meaning that if a firm borrowed from a bank in 1992, the probability that it borrowed

again in 1993 was 94.7%. Likewise for 1996 and 1999 the probability of borrowing is very high,

around 92.7% and 95.7% respectively. On the other hand, if a firm had other financial sources such

as its own funds, retained earnings or international markets, the probability of borrowing was low

because the coefficients of these variables are negative. Thus if a firm has other funding sources ,

that firm is inclined not to resort to bank loans. If output increases the probability of borrowing also

increases.

7. Relationship Lending and Collateral

Collateral is one of the important elements in assessing the relationship between a bank and a

firm. In general banks require collateral for a loan regardless of whether undertaking transaction

lending or relationship lending. Asset size is a good proxy for collateral; however in the BPS data set,

12

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 15/23

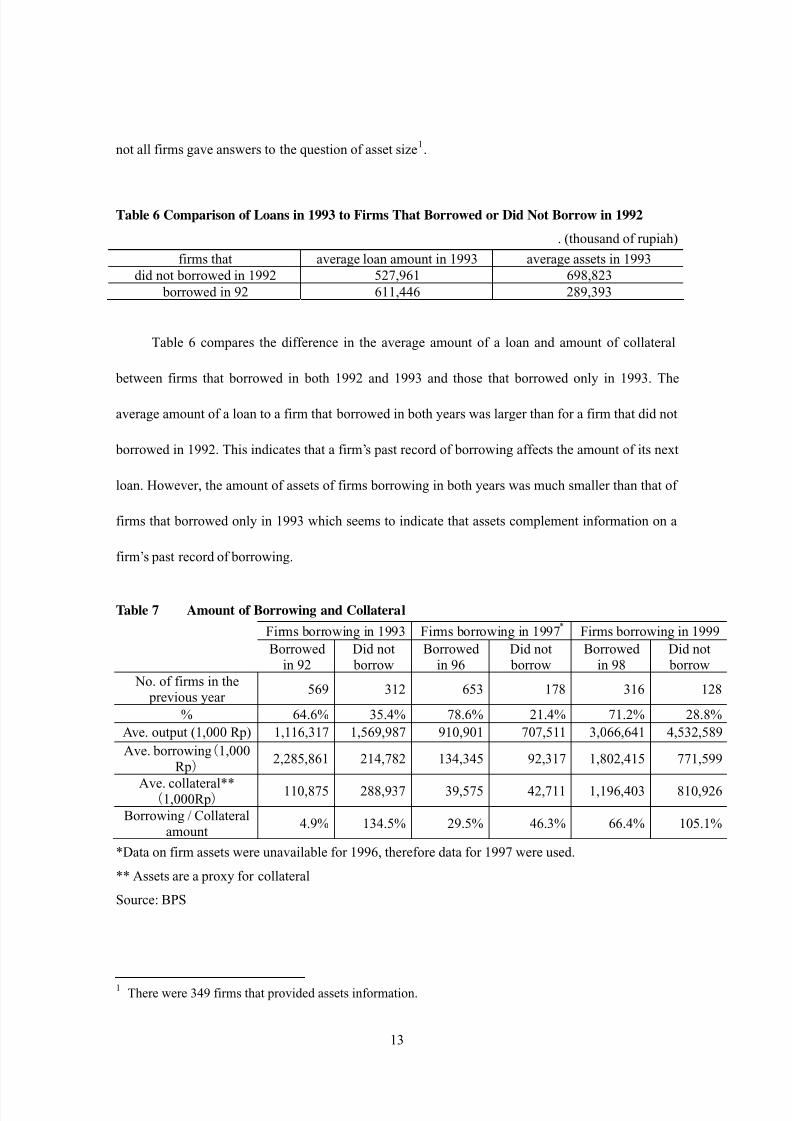

not all firms gave answers to the question of asset size1.

Table 6 Comparison of Loans in 1993 to Firms That Borrowed or Did Not Borrow in 1992

. (thousand of rupiah)

firms that average loan amount in 1993 average assets in 1993

did not borrowed in 1992 527,961 698,823

borrowed in 92 611,446 289,393

Table 6 compares the difference in the average amount of a loan and amount of collateral

between firms that borrowed in both 1992 and 1993 and those that borrowed only in 1993. The

average amount of a loan to a firm that borrowed in both years was larger than for a firm that did not

borrowed in 1992. This indicates that a firm’s past record of borrowing affects the amount of its next

loan. However, the amount of assets of firms borrowing in both years was much smaller than that of

firms that borrowed only in 1993 which seems to indicate that assets complement information on a

firm’s past record of borrowing.

Table 7 Amount of Borrowing and Collateral

Firms borrowing in 1993 Firms borrowing in 1997*

Firms borrowing in 1999 Borrowed in 92

Did not borrow

Borrowed in 96

Did not borrow

Borrowed in 98

Did not borrow

No. of firms in the previous year

569 312 653 178 316 128

% 64.6% 35.4% 78.6% 21.4% 71.2% 28.8%

Ave. output (1,000 Rp) 1,116,317 1,569,987 910,901 707,511 3,066,641 4,532,589

Ave. borrowing(1,000Rp)

2,285,861 214,782 134,345 92,317 1,802,415 771,599

Ave. collateral**(1,000Rp)

110,875 288,937 39,575 42,711 1,196,403 810,926

Borrowing / Collateralamount

4.9% 134.5% 29.5% 46.3% 66.4% 105.1%

*Data on firm assets were unavailable for 1996, therefore data for 1997 were used.

** Assets are a proxy for collateral

Source: BPS

1 There were 349 firms that provided assets information.

13

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 16/23

From the foregoing analysis it can be argued that for banks in Indonesia, financial

intermediation functions operate from the standpoint of relationship lending. Table 7 shows that if a

firm already has a relationship with a bank, the amount that can be borrowed is larger and collateral

can be smaller than for a firm without a relationship.

7. Conclusion

This paper examined the funding sources of medium-sized firms and the financial

intermediation functions of banks in Indonesia from the standpoint of relationship lending. In order

to mitigate problems of information asymmetry, banks have to product information and improve

their techniques of lending. This paper examined whether Indonesian banks product information as a

function of financial intermediation. The results of logit regression show that the relationship

between banks and firms affects the probability of borrowing. The amount of borrowing and

collateral is also affected by the existence of a firm’s relationship with a bank. Due to the lack of

information, the effect of this relationship on interest rates was not examined. However, it can be

argued that in Indonesia banks perform financial intermediation functions when examined from the

standpoint of relationship lending.

14

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 17/23

15

References

Booth, James R. [1996], Loan Collateral Decisions and Corporate Borrowing Costs, Arizona State

University Working Paper.Berger, Allen N. and Udell, Gregory F [1995], “Relationship Lending and Lines of Credit in Small

Firm Finance,” The Journal of Business, Vol.68, No.3, pp351-381

--------[2002], Small Business Credit availability and relationship lending: the importance of bank

Organizational Structure, The Economic Journal, 112, pp32-53.

Bebczuk, R. N., [2004] “What Determines the Access to Credit by SMEs in Argentina?,” Faculltad

de Clenclas Economicas Universidad Nacional de la Plata.

Boot, A. W. A., [2000] Relationship banking: What do we know?, Journal of Financial

Intermediation, 9, pp.7-25.

Badan Pusat Staristik (BPS), Statistik Industri (various years).

Eugene F. Fama; Kenneth R. French [2002] “Testing Trade-Off and Pecking Order Predictions about

Dividends and Debt,” The Review of Financial Studies, Vol.15, No1, pp.1-33.

Ramakrishnan, S., and Thakor, A.V. [1984] Information Reliability and a Theory of Financial

Intermediation. Review of Economic Studies Vol. 51, pp.415-432.

Udell, Gregory F. [2004], “SME Lending: Defining the Issues in a Global Perspective,” Kelley

School of Business, Indiana University.

In Japanese

Miki Hamada-Takeda [2000] “The Sequence of Financial Liberalization and Financial Fragility,” in

The Asian Currency Crisis: Causes and Problems in Prescription, eds K. Kunimune, Institute

of Developing Economies, Chiba.

--------------------------[2001] “Restructuring Indonesia’s Banks and Corporate”, in Financial

Restructuring and Corporate Restructuring: Asian Experience, eds K. Kunimune Institute of

Developing Economies, Chiba.

---------------------------[2002] “Formation and Structural Change of the Financial Sector”, in

Democratizing Indonesia: Politics and Economy in Historical Perspective, eds Y. Sato,

Institute of Developing Economies, Chiba.

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 18/23

No. Author(s) Title

143 Yoko IWASAKIMethodological Application of Modern Historical Science to‘Qualitative Research’

2008

142 Masahiro KODAMAMonetary Policy Effects in Developing Countries with

Minimum Wages

2008

141 Yasushi Hazama The Political Economy of Growth: A Review 2008

140 Kumiko MAKINOThe Changing Nature of Employment and the Reform of Labor and Social Security Legislation in Post-Apartheid South Africa

2008

139 Hisao YOSHINOTechnology Choice, Change of Trade Structure, and A Case of Hungarian Economy

2008

138 Shigeki HIGASHIThe Policy Making Process in FTA Negotiations: A CaseStudy of Japanese Bilateral EPAs

2008

137Arup MITRA andMayumi MURAYAMA

Rural to Urban Migration: A District Level Analysis for India 2008

136 Nicolaus Herman SHOMBE Causality relationship between Total Export and AgriculturalGDP and Manufacturing GDP case of Tanzania

2008

135 Ikuko OKAMOTOThe Shrimp Export Boom and Small-Scale Fishermen inMyanmar

2008

134 Chibwe CHISALAUnlocking the Potential of Zambian Micro, Small and MediumEnterprises "learning from the international best practices - theSoutheast Asian Experience"

2008

133 Miwa YAMADAEvolution in the Concept of Development: How has the WorldBank's Legal Assistance Extended its Reach?

2008

132 Maki AOKI-OKABELooking Toward the “New Era”:Features and Background of the Japan-Thailand Economic

Partnership Agreement

2008

131Masanaga KUMAKURA andMasato KUROKO

China’s Impact on the Exports of Other AsianCountries: A Note

2007

130 Koichiro KIMURAGrowth of the Firm and Economic Backwardness:A Case Study and Analysis of China's Mobile HandsetIndustry

2007

129 Takahiro FUKUNISHIHas Low Productivity Constrained Competitiveness of AfricanFirrms?: Comparison of Firm Performances with Asian Firms

2007

128 Akifumi KUCHIKI Industrial Policy in Asia 2007

127 Teiji SAKURAIJETRO and Japan’s Postwar Export Promotion System:Messages forLatin American Export Promotion Agencies

2007

126 Takeshi KAWANAKA Who Eats the Most? Quantitative Analysis of Pork BarrelDistributions in the Philippines

2007

125 Ken IMAI and SHIU JingmingA Divergent Path of Industrial Upgrading: Emergence andEvolution of the Mobile Handset Industry in China

2007

124 Tsutomu TAKANEDiversities and Disparities among Female-Headed Householdsin Rural Malawi

2007

123 Masami ISHIDAEvaluating the Effectiveness of GMS Economic Corridors:Why is There More Focus on the Bangkok-Hanoi Road thanthe East-West Corridor

2007

122 Toshihiro KUDOBorder Industry in Myanmar: Turning the Periphery into theCenter of Growth

2007

121 Satoru KUMAGAI A Mathematical Representation of "Excitement" in Gamesfrom the Viewpoint of a Neutral Audience

2007

120 Akifumi KUCHIKIA Flowchart Approach to Malaysia'sAutomobile Industry Cluster Policy

2007

119 Mitsuhiro KAGAMIThe Sandinista Revolution and Post-ConflictDevelopment - Key Issues

2007

~Previous IDE Discussion Papers ~

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 19/23

No. Author(s) Title

118 Toshihiro KUDO Myanmar and Japan: How Close Friends Become Estranged 2007

117 Tsutomu TAKANEGambling with Liberalization: Smallholder Livelihoods inContemporary Rural Malawi

2007

116Toshihiro KUDO and FumiharuMIENO

Trade, Foreign Investment and Myanmar's EconomicDevelopment during the Transition to an Open Economy

2007

115 Takao TSUNEISHI

Thailand's Economic Cooperation with Neighboring Countries

and Its Effects on Economic Development within Thailand 2007

114Jan OOSTERHAVEN,Dirk STELDER andSatoshi INOMATA

Evaluation of Non-Survey International IO ConstructionMethods with the Asian-Pacific Input-Output Table

2007

113 Satoru KUMAGAIComparing the Networks of Ethnic Japanese and EthnicChinese in International Trade

2007

112 Rika NAKAGAWAInstitutional Development of Capital Markets in Nine AsianEconomies

2007

111Hiroko UCHIMURA andJohannes JÜTTING

Fiscal Decentralization, Chinese Style: Good for HealthOutcomes?

2007

110

Hiroshi KUWAMORI and

Nobuhiro OKAMOTO

Industrial Networks between China and the Countries of the

Asia-Pacific Region 2007

109 Yasushi UEKIIndustrial Development and the Innovation System of theEthanol Sector in Brazil

2007

108 Shinichi SHIGETOMIPublicness and Taken-for-granted Knowledge:A Case Study of Communal Land Formation in Rural Thailand

2007

107 Yasushi HAZAMAPublic Support for Enlargement: Economic, Cultural, or

Normative?2007

106 Seiro ITO Bounding ATE with ITT 2007

105 Tatsufumi YAMAGATASecuring Medical Personnel: Case Studies of Two SourceCountries and Two Destination Countries

2007

104 Tsutomu TAKANE

Customary Land Tenure, Inheritance Rules, and Smallholder

Farmers in Malawi 2007

103Aya OKADA and N. S.SIDDHARTHAN

Industrial Clusters in India: Evidence from AutomobileClusters in Chennai and the National Capital Region

2007

102 Bo MENG and Chao QUApplication of the Input-Output Decomposition Technique toChina's Regional Economies

2007

101 Tatsufumi YAMAGATAProspects for Development of the Garment Industry inDeveloping Countries: What Has Happened since the MFAPhase-Out?

2007

100 Akifumi KUCHIKIThe Flowchart Model of Cluster Policy:The Automobile Industry Cluster in China

2007

99

Seiro ITOH, Mariko

WATANABE, and NoriyukiYANAGAWA

Financial Aspects of Transactions with FDI: Trade CreditProvision by SMEs in China 2007

98 Norio KONDO Election Studies in India 2007

97 Mai FUJITALocal Firms in Latecomer Developing Countries amidstChina's Rise - The case of Vietnam's motorcycle industry

2007

96Kazushi TAKAHASHI andKeijiro OTSUKA

Human Capital Investment and Poverty Reduction over Generations: A Case from the Rural Philippines, 1979-2003

2007

95 Kazushi TAKAHASHISources of Regional Disparity in Rural Vietnam: Oaxaca-Blinder Decomposition

2007

94 Hideki HIRAIZUMIChanges in the Foreign Trade Structure of the Russian Far East

under the Process of Transition toward a Market Economy

2007

93 Junko MIZUNODifferences in Technology Transfers to China amongEuropean and Japanese Elevator Companies

2007

92 Kazuhiko OYAMADAIs It Worthwhile for Indonesia to Rush into a Free Trade Dealwith Japan?

2007

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 20/23

No. Author(s) Title

91 Haruka I. MATSUMOTOThe Evolution of the "One China" Concept in the Process of Taiwan's Democratization

2007

90 Koji KUBO Natural Gas and Seeming Dutch Disease 2007

89 Akifumi KUCHIKIClusters and Innovation: Beijing's Hi-technology IndustryCluster and Guangzhou's Automobile Industry Cluster

2007

88 DING Ke

Domestic Market-based Industrial Cluster Development in

Modern China 2007

87 Koji KUBODo Foreign Currency Deposits Promote or Deter Financial Development in Low-income Countries?:An Empirical Analysis of Cross-section Data

2007

86 G. BALATCHANDIRANE IT Offshoring and India: Some Implications 200785 G. BALATCHANDIRANE IT Clusters in India 2007

84 Tomohiro MACHIKITAAre Job Networks Localized in a Developing Economy?Search Methods for Displaced Workers in Thailand

2006

83 Tomohiro MACHIKITACareer Crisis? Impacts of Financial Shock on the Entry-LevelLabor Market: Evidence from Thailand

2006

82 Tomohiro MACHIKITA

Is Learning by Migrating to a Megalopolis Really Important?

Evidence from Thailand 2006

81 Asao ANDO and Bo MENGTransport Sector and Regional Price Differentials:A SCGE Model for Chinese Provinces

2006

80 Yuka KODAMAPoverty Analysis of Ethiopian Females in the Amhara Region:Utilizing BMI as an Indicator of Poverty

2006

79 So UMEZAKIMonetary and Exchange Rate Policy in Malaysia before theAsian Crisis

2006

78 Ikuo KUROIWA Rules of Origin and Local Content in East Asia 2006

77 Daisuke HIRATSUKAOutward FDI from and Intraregional FDI in ASEAN:Trends and Drivers

2006

76 Masahisa FUJITA

Economic Development Capitalizing on Brand Agriculture:

Turning Development Strategy on Its Head 2006

75 DING KeDistribution System of China’s Industrial Clusters:Case Study of Yiwu China Commodity City

2006

74Emad M. A. ABDULLATIFAlani

Crowding-Out and Crowding-In Effects of Government BondsMarket on Private Sector Investment (Japanese Case Study)

2006

73 Tatsuya SHIMIZU Expansion of Asparagus Production and Exports in Peru 2006

72 Hitoshi SUZUKIThe Nature of the State in Afghanistan and Its Relations with

Neighboring Countries2006

71 Akifumi KUCHIKI An Asian Triangle of Growth and Cluster-to-Cluster Linkages 2006

70 Takayuki TAKEUCHIIntegration under ‘One Country, Two Systems’ - The Case of Mainland China and Hong Kong-

2006

69 Shinichi SHIGETOMI Bringing Non-governmental Actors into the PolicymakingProcess: The Case of Local Development Policy in Thailand

2006

68 Kozo KUNIMUNE Financial Cooperation in East Asia 2006

67 Yasushi UEKIExport-Led Growth and Geographic Distribution of the PoultryMeat Industry in Brazil

2006

66 Toshihiro KUDOMyanmar's Economic Relations with China: Can ChinaSupport the Myanmar Economy?

2006

65 Akifumi KUCHIKI Negative Bubbles and Unpredictability of Financial Markets:The Asian Currency Crisis in 1997

2006

64 Ken IMAI Explaining the Persistence of State-Ownership in China 2006

63

Koichi FUJITA and Ikuko

OKAMOTO

Agricultural Policies and Development of Myanmar

Agriculture: An Overview 2006

62 Tatsufumi YAMAGATAThe Garment Industry in Cambodia: Its Role in PovertyReduction through Export-Oriented Development

2006

61 Hisaki KONOIs Group Lending A Good Enforcement Scheme for AchievingHigh Repayment Rates?Evidence from Field Experiments inVietnam

2006

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 21/23

No. Author(s) Title

60 Hiroshi KUWAMORIThe Role of Distance in Determining International TransportCosts: Evidence from Philippine Import Data

2006

59 Tatsuya SHIMIZU Executive Managers in Peru's Family Businesses 2006

58 Noriyuki YANAGAWA, SeiroITO, and Mariko WATANABE

Trade Credits under Imperfect Enforcement: A Theory with aTest on Chinese Experience

2006

57

Reiko AOKI, Kensuke KUBO,

and Hiroko YAMANE

Indian Patent Policy and Public Health: Implications from the

Japanese Experience 2006

56 Koji KUBOThe Degree of Competition in the Thai Banking Industry

before and after the East Asian Crisis2006

55 Jiro OKAMOTOAustralia's Foreign Economic Policy: A 'State-SocietyCoalition' Approach and a Historical Overview

2006

54 Yusuke OKAMOTOIntegration versus Outsourcing in Stable Industry Equilibriumwith Communication Networks

2006

53Hikari ISHIDO andYusuke OKAMOTO

Winner-Take-All Contention of Innovation under Globalization: A Simulation Analysis and East Asia’s Empirics

2006

52 Masahiro KODAMA Business Cycles of Non-mono-cultural Developing Economies 2006

51

Arup MITRA and Yuko

TSUJITA

Migration and Wellbeing at the Lower Echelons of the

Economy: A Study of Delhi Slums 2006

50

Bo MENG, Hajime SATO, Jun NAKAMURA, NobuhiroOKAMOTO, HiroshiKUWAMORI, and SatoshiINOMATA

Interindustrial Structure in the Asia-Pacific Region: Growthand Integration, by Using 2000 AIO Table

2006

49Maki AOKI-OKABE, YokoKAWAMURA, and ToichiMAKITA

International Cultural Relations of Postwar Japan 2006

48 Arup MITRA and Hajime SATOAgglomeration Economies in Japan: Technical Efficiency,Growth and Unemployment

2006

47 Shinichi SHIGETOMIOrganization Capability of Local Societies in RuralDevelopment: A Comparative Study of MicrofinanceOrganizations in Thailand and the Philippines

2006

46 Yasushi HAZAMA Retrospective Voting in Turkey: Macro and Micro Perspectives 2006

45Kentaro YOHIDA and Machiko

NAKANISHIFactors Underlying the Formation of Industrial Clusters inJapan and Industrial Cluster Policy: A Quantitative Survey

2005

44 Masanaga KUMAKURA Trade and Business Cycle Correlations in Asia-Pacific 2005

43 Ikuko OKAMOTOTransformation of the Rice Marketing System and Myanmar'sTransition to a Market Economy

2005

42 Toshihiro KUDO

The Impact of United States Sanctions on the Myanmar

Garment Industry 2005

41 Yukihito SATOPresident Chain Store Corporation's Hsu Chong-Jen: A CaseStudy of a Salaried Manager in Taiwan

2005

40 Taeko HOSHINO Executive Managers in Large Mexican Family Businesses 2005

39 Chang Soo CHOEKey Factors to Successful Community Development: TheKorean Experience

2005

38 Toshihiro KUDO Stunted and Distorted Industrialization in Myanmar 2005

37Etsuyo MICHIDA and Koji

NISHIKIMI North-South Trade and Industly-Specific Pollutants 2005

36 Akifumi KUCHIKI Theory of a Flowchart Approach to Industrial Cluster Policy 2005

35 Masami ISHIDA

Effectiveness and Challenges of Three Economic Corridors of

the Greater Mekong Sub-region 2005

34 Masanaga KUMAKURATrade, Exchange Rates, and Macroeconomic Dynamics in EastAsia: Why the Electronics Cycle Matters

2005

33 Akifumi KUCHIKITheoretical Models Based on a Flowchart Approach toIndustrial Cluster Policy

2005

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 22/23

No. Author(s) Title

32 Takao TSUNEISHIThe Regional Development Policy of Thailand and ItsEconomic Cooperation with Neighboring Countries

2005

31 Yuko TSUJITAEconomic Reform and Social Setor Expenditures: A Study of Fifteen Indian States 1980/81-1999/2000

2005

30 Satoshi INOMATATowards the Compilation of the Consistent Asian InternationalI-O Table: The Report of the General Survey on National I-O

Tables

2005

29 Bo MENG and Asao ANDOAn Economic Derivation of Trade Coefficients under theFramework of Multi-regional I-O Analysis

2005

28 Nobuhiro OKAMOTO, TakaoSANO, and Satoshi INOMATA

Estimation Technique of International Input-Output Model by Non-survey Method

2005

27Masahisa FUJITA and TomoyaMORI

Frontiers of the New Economic Geography 2005

26 Hiroko UCHIMURA Influence of Social Institutions on Inequality in China 2005

25Shinichiro OKUSHIMA andHiroko UCHIMURA

Economic Reforms and Income Inequality in Urban China 2005

24 Banri ITO and TatsufumiYAMAGATA

Who Develops Innovations in Medicine for the Poor? Trends

in Patent Applications Related to Medicines for HIV/AIDS,Tuberculosis, Malaria and Neglected Diseases

2005

23 Etsuyo MICHIDAManagement for a Variety of Environmental Pollution and

North-South Trade2005

22 Daisuke HIRATSUKA The "Catching Up" Process of Manufacturing in East Asia 2005

21Masahisa FUJITA and TomoyaMORI

Transport Development and the Evolution of EconomicGeography

2005

20 Graciana B. FEMENTIRACase Study of Applied LIP Approach/Activities in thePhilippines: The Training Services Enhancement Project for Rural Life Improvement (TSEP-RLI) Experience

2005

19 Hitoshi SUZUKI

Structural Changes and Formation of Rū st ā-shahr in Post-

revolutionary Rural Society in Iran 2004

18Tomokazu ARITA, MasahisaFUJITA, and YoshihiroKAMEYAMA

Regional Cooperation of Small & Medium Firms in JapaneseIndustrial Clusters

2004

17 Karma URA Peasantry and Bureaucracy in Decentralization in Bhutan 2004

16Masahisa FUJITA and ToshitakaGOKAN

On the Evolution of the Spatial Economy with Multi-unit・Multi-plant Firms: The Impact of IT Development

2004

15 Koji KUBOImperfect Competition and Costly Screening in the CreditMarket under Conditions of Asymmetric Information

2004

14Marcus BERLIANT andMasahisa FUJITA

Knowledge Creation as a Square Dance on the Hilbert Cube 2004

13 Gamini KEERAWELLA Formless as Water, Flaming as a Fire – Some observations onthe Theory and Practice of Self-Determination

2004

12 Taeko HOSHINOFamily Business in Mexico: Responses to Human ResourceLimitations and Management Succession

2004

11 Hikari ISHIDO East Asia’s Economic Development cum Trade “Divergence” 2004

10 Akifumi KUCHIKIPrioritization of Policies: A Prototype Model of a FlowchartMethod

2004

9 Sanae SUZUKI Chairmanship in ASEAN+3: A Shared Rule of Behaviors 2004

8Masahisa FUJITA and ShlomoWEBER

On Labor Complementarity, Cultural Frictions and StrategicImmigration Policies

2004

7 Tatsuya SHIMIZU

Family Business in Peru: Survival and Expansion under the

Liberalization 2004

6 Katsumi HIRANOMass Unemployment in South Africa: A Comparative Studywith East Asia

2004

5Masahisa FUJITA and Jacques-Francois THISSE

Globalization and the Evolution of the Supply Chain: WhoGains and Who Loses?

2004

7/28/2019 bank borrowing.pdf

http://slidepdf.com/reader/full/bank-borrowingpdf 23/23

No. Author(s) Title

4 Karma URAThe First Universal Suffrage Election, at County (Gewog)Level, in Bhutan

2004

3 Gamini KEERAWELLAThe LTTE Proposals for an Interim Self-Governing Authorityand Future of the Peace Process in Sri Lanka

2004

2 Takahiro FUKUNISHIInternational Competitiveness of Manufacturing Firms in Sub-Saharan Africa

2004

1 Pk. Md. Motiur RAHMAN andTatsufumi YAMAGATA

Business Cycles and Seasonal Cycles in Bangladesh 2004