bank audi syria sa † annual report · pdf filetowards end 2006, the bank ensured a ......

TRANSCRIPT

Bank Audi Syria sa • Annual Repor t 2006

3

INDEX

BOARD OF DIRECTORS’ REPORT FOR 2006 ACTIVITIES 5

MAJOR SHAREHOLDING AND FOUNDING MEMBERS 7

BOARD OF DIRECTORS 8

MANAGEMENT 9

FUNCTIONAL ORGANIZATIONAL CHART OF THE HEAD OFFICE 10

BANK AUDI SYRIA sa ACTIVITIES IN 2006 13 1- EXPANSION PLAN 15 2- RETAIL STRATEGY 15 2.1. NEW RETAIL PROJECTS 16 2.2. THE BANK AUDI BRAND 16 3- HUMAN CAPITAL 16 4- INFORMATION TECHNOLOGY 17 5- FINANCIAL PERFORMANCE 18 5.1. ASSETS 18 5.2. LIABILITIES AND EQUITY 20 5.3. OFF-BALANCE SHEET COMMITMENTS 21 5.4. PROFITABILITY 21 6- NET INCOME ALLOCATION 22

INDEPENDENT AUDITORS’ REPORT 25

BANK AUDI SYRIA sa FINANCIAL STATEMENTS 27 - INCOME STATEMENT 29 - BALANCE SHEET 30 - STATEMENT OF CHANGES IN EQUITY 31 - STATEMENT OF CASH FLOWS 32

BANK AUDI SYRIA sa NOTES TO THE FINANCIAL STATEMENTS 33

HEAD OFFICE AND BRANCH NETWORK 59

5

BOARD OF DIRECTORS’ REPORT FOR 2006 ACTIVITIES

Submitted to Shareholders Regular General Assembly

Bank Audi Syria witnessed an exciting and successful first full-year where it was able to offer a wide range of products and services to achieve our vision of becoming a universal bank. The Bank invested in developing products and services in the Traditional, Retail, Trade finance, Corporate and Project Finance in order to cover the financial and economic needs of the Syrian market.

The year witnessed the opening of the Bank’s Head Office and main branch at Youssef Al-Azmeh Square, located in the center of Damascus. Concurrently, the Bank proceeded to structure a solid organization, staffed with highly educated professionals eager to further develop their skills and offer high quality service to the Bank’s customers. I personally consider this year’s performance as a benchmark for what the Bank is able to accomplish in the future. Bank Audi Syria developed and maintained its high quality of service, with our goal in mind to preserve and enhance clients’ and investors’ trust, by building solid and loyal partnerships.

In addition, the Bank’s branch network expanded to reach 5 branches, distributed as follows: 3 branches in Damascus, a regional branch in Aleppo to serve the Northern area, and one in Lattakia to cover the coastal side. The Bank plans to aggressively expand its presence into all governorates, to ensure serving its clients wherever they are located.

The year 2006 was characterized by major economic developments and a significant liberalization of the banking sector, both a response to the issuance of valiant regulations by specialized authorities. Consequently, banks were given the opportunity to play a bigger and more effective role in stimulating and enlivening economic activity. It is worth mentioning that other major advancements are underway which will enable banks to fully play their role in developing the Syrian economy.

On the other hand, Bank Audi sal - Audi Saradar Group, Bank Audi Syria’s major shareholder, moved a step ahead in its strategic regional expansion plan, adding in 2006 five new implementations, namely in Egypt, Sudan, Qatar, Saudi Arabia (through an investment company) and in the UAE, over and above its presence in Lebanon, France, Switzerland, Jordan and Syria. To support its expansion plan, the Group closed in April 2006 a US$ 600 million capital increase, raising its shareholders’ equity at end-2006 to US$ 1.7 billion, placing the Bank among the top 25 Arab banking groups in the Middle East.

As a matter of fact, I am pleased to inform you that our Bank began to generate a net positive income at the end of 2006 due to proper management, dedication and team work efforts which resulted in surpassing targeted objectives.

However, and as a result of new regulations issued by the Credit and Monetary Council during 2006 concerning setting a threshold for foreign exchange positions, Bank Audi Syria, along with the other Syrian Banks, had to liquidate a large portion of its structural position by conversion to Syrian Pounds, which resulted in significant losses. Despite that, the Bank’s operations during 2006 generated sufficient revenues to absorb the foreign exchange losses and resulted in a net after tax income amounting to SYP 452,873 and an overall positive bottom line for the second year in a row.

Finally, I would like to take this opportunity to express my gratitude to the Board of Directors, management and staff for the Bank’s achievements this year. Hoping that we will continue to add value to our community and to the Syrian economy as a whole.

Dr. Georges Achi Chairman - Bank Audi Syria sa

7

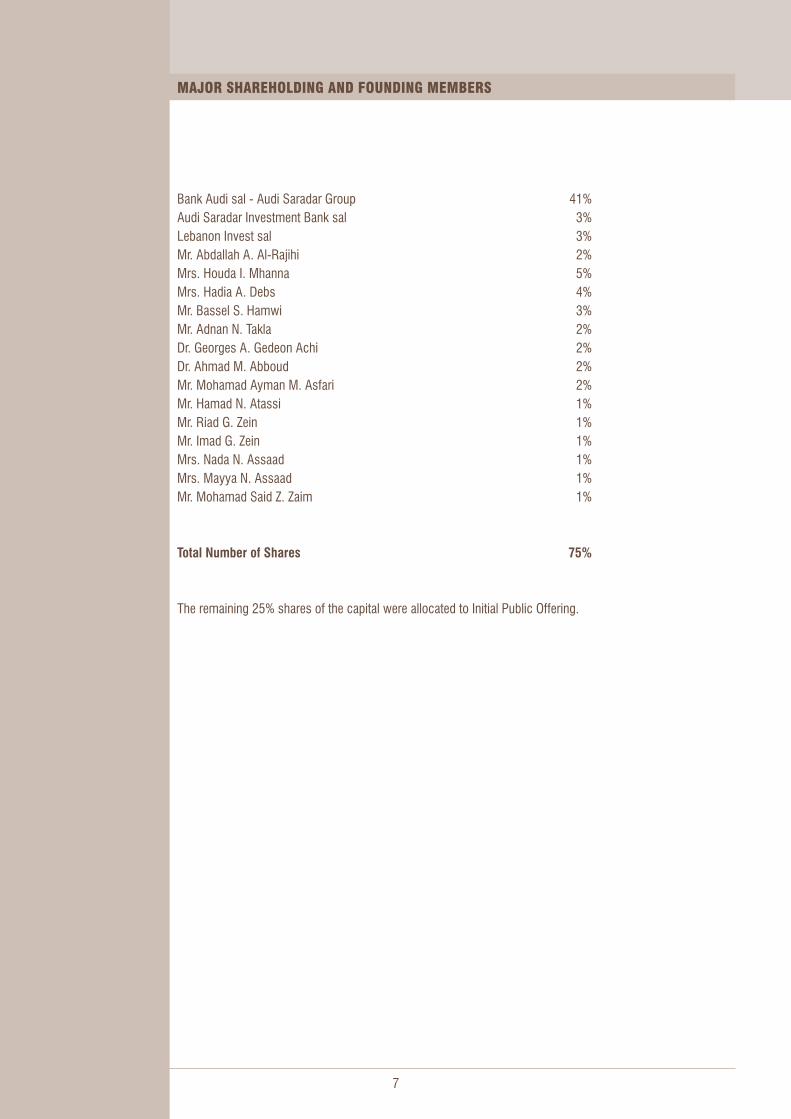

MAJOR SHAREHOLDING AND FOUNDING MEMBERS

Bank Audi sal - Audi Saradar Group 41%Audi Saradar Investment Bank sal 3%Lebanon Invest sal 3%Mr. Abdallah A. Al-Rajihi 2%Mrs. Houda I. Mhanna 5%Mrs. Hadia A. Debs 4%Mr. Bassel S. Hamwi 3%Mr. Adnan N. Takla 2%Dr. Georges A. Gedeon Achi 2%Dr. Ahmad M. Abboud 2%Mr. Mohamad Ayman M. Asfari 2%Mr. Hamad N. Atassi 1%Mr. Riad G. Zein 1%Mr. Imad G. Zein 1%Mrs. Nada N. Assaad 1%Mrs. Mayya N. Assaad 1%Mr. Mohamad Said Z. Zaim 1%

Total Number of Shares 75%

The remaining 25% shares of the capital were allocated to Initial Public Offering.

8

BOARD OF DIRECTORS

Chairman Dr. Georges A. Gedeon Achi

Deputy Chairman Mr. Bassel S. Hamwi (*)

Board Members Mr. Raymond W. Audi Mr. Samir N. Hanna Mr. Adnan N. Takla Dr. Ahmad M. Abboud Mr. Mohamad Said Z. Zaim Mrs. Rana T. Zein Dr. Freddie C. Baz

Advisors to the Board Mrs. Nada N. Assaad Mrs. Yasmina R. Azhari Mr. Abdulateef A. Al-Rajihi

Legal Advisors Sarkis Law Office

Auditors Ernst & Young

(*) General Manager

9

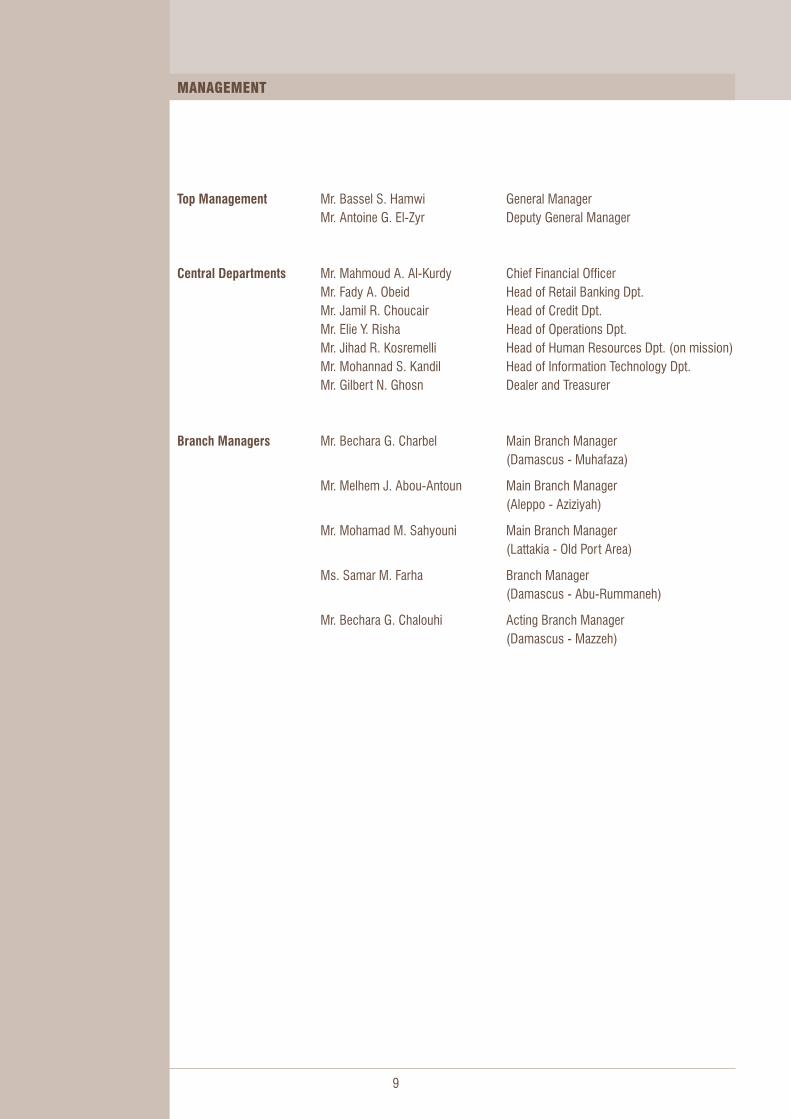

MANAGEMENT

Top Management Mr. Bassel S. Hamwi General Manager Mr. Antoine G. El-Zyr Deputy General Manager

Central Departments Mr. Mahmoud A. Al-Kurdy Chief Financial Officer Mr. Fady A. Obeid Head of Retail Banking Dpt. Mr. Jamil R. Choucair Head of Credit Dpt. Mr. Elie Y. Risha Head of Operations Dpt. Mr. Jihad R. Kosremelli Head of Human Resources Dpt. (on mission) Mr. Mohannad S. Kandil Head of Information Technology Dpt. Mr. Gilbert N. Ghosn Dealer and Treasurer

Branch Managers Mr. Bechara G. Charbel Main Branch Manager (Damascus - Muhafaza)

Mr. Melhem J. Abou-Antoun Main Branch Manager (Aleppo - Aziziyah)

Mr. Mohamad M. Sahyouni Main Branch Manager (Lattakia - Old Port Area)

Ms. Samar M. Farha Branch Manager (Damascus - Abu-Rummaneh)

Mr. Bechara G. Chalouhi Acting Branch Manager (Damascus - Mazzeh)

10

11

BANK AUDI SYRIA sa

ACT IV IT IES IN 2006

15

BANK AUDI SYRIA sa ACTIVITIES IN 2006

1. Expansion Plan

Starting with the ribbon cutting of its main branch and Head Office in January 2006, Bank Audi Syria achieved an aggressive expansion strategy throughout 2006 and shall extend its expansion plans into 2007. The Bank’s third branch in Damascus was opened soon after, early May 2006, in one of Damascus’ prime areas in terms of commercial and residential concentration: Abu-Rummaneh.

In line with the spread-out in Damascus, the Bank started up a branch in Aleppo in April 2006, celebrated by a major event held at the Blue Lagoon. The event was organized to reflect the importance of Aleppo as Syria’s major industrial city, gathering over 500 attendees representing the city’s traders, businesspersons and officials. Towards end 2006, the Bank ensured a presence, though minor, in Lattakia where the plan for the opening of the main branch in the governorate and the associated gala event are to be held during the first quarter of 2007 (*).

Bank Audi Syria will continue its geographic spread, implementing its vertical and horizontal expansion plans to cover all major Syrian cities and prime locations, as new branches will be established in Harasta and Kafarsouseh (Damascus) and will reach new destinations such as Homs and Tartous.

2. Retail Strategy

The Bank’s strategy is based on serving the market with added value products and services, and building a long-term relationship with customers from all age groups. In a highly competitive and rapidly growing market, the Bank aims at differentiating itself by providing its customers with easy access to high quality, modern and highly innovative technological banking solutions.

As a building stone, a partnership was made in April 2006 with the first internet service provider in Syria, Aloola, to jointly provide Bank Audi Syria’s Net Account. The product, designed to be accessible to all customers falling under different age groups in an emerging market thirsty for technology, greatly contributed to the franchise building of the Bank’s customer base, as its holders represented a significant percentage of the Bank’s clients by end 2006.In line with the introduction of the Net Account, the Bank launched its first consumer lending product, the PC Loan, in alliance with Toshiba, enabling cutomers to own one of the highest technology portable computers at monthly installments as low as SYP 3,000.By mid 2006, the Bank had launched Visa Electron local and international debit cards, in association with VISA International. In a highly cash dependent market, Bank Audi Syria was the first to introduce the International Visa Electron debit card which granted the Bank’s clients access to their accounts at Bank Audi Syria from all over the world. By end 2006, the Bank successfully facilitated customers’ accessibility to ATMs by establishing a link with one of Syria’s largest ATM networks. The Bank’s cards thus became functional in over 200 ATMs in Syria and its ATMs were the exclusive dispensers of US Dollars.

In order to increase its retail franchise and to set the basis of its consumer lending portfolio, the Bank realized massive payroll acquisitions by presenting the Payroll Account, the most sophisticated payroll product to corporations of all sizes. The Payroll Account aims at encouraging the replacement of cash with a convenient e-transfer salary payment. It offers clients:

• A revolving credit line of one month salary;• Free personal accident coverage reaching up to 10 times their monthly salaries, but not to exceed SYP 500,000;• Preferential access to personal loans for amounts reaching up to 10 times their monthly salaries.

(*) Lattakia main branch was officially inaugurated on February 11, 2007.

16

BANK AUDI SYRIA sa ACTIVITIES IN 2006

At the same time, the impact of payroll acquisition on the customer base growth became noticeable as the Bank witnessed a significant increase in new account openings on a monthly basis.

By the end of 2006, the Bank inaugurated its e-Banking interface, Audi On-line, which enables clients to access their accounts on the internet from anywhere in the world.

The perception of Bank Audi Syria as a secure and reliable institution induced the introduction of a number of safe deposit boxes in all its branches, offering clients a highly secure solution and enabling them to keep their valuable belongings available whenever needed.

2.1. New Retail Projects

Retail activities in 2006 also included preparations for new products which would enrich the Bank’s consumer lending services.

An early entrant by quarter I of 2007 will be the Special Car Deal offer, whereby the Bank, along with Syria’s top car dealers, jointly provide extra value to customers on specific car models.

With liberalization in the insurance sector, the Bank entered as a founding shareholder in the Syrian Arab Insurance, along with Audi Saradar Group. Once regulations will allow it, the Bank will develop the first range of Bancassurance products, in partnership with its sister company. This initiative is meant to stir up the market by serving and informing Syrian consumers on the benefits and advantages of insurance made easy.

2.2. The Bank Audi Brand

The highlight of all events organized by Bank Audi Syria in 2006 was the large-scale gala dinner held at the Four Seasons Hotel on the occasion of the opening of the Bank’s Headquarters, early 2006, as well as the massive outdoor campaign which accompanied it. The campaign introduced the slogan of Bank Audi sal – Audi Saradar Group, “Grow Beyond your Potential”, represented by its famous wheat feature. This campaign was by far the largest any financial institution had launched till date on the Syrian market.

This was followed by a highly visible Net Account campaign consolidating the technology edge of the Bank. Launched concurrently in Damascus and Aleppo, this campaign led to more awareness and positioned Bank Audi Syria as the first private-owned bank to introduce retail products.

Furthermore, Bank Audi Syria marked a noticeable presence in all exhibitions held in 2006 within varying areas of focus. These include “Shaam Expo” for Technology and Communications, “Buildex” for building tools and materials, and the “Schools and Exhibitions” exhibition.

Finally, Bank Audi Syria will conduct corporate image campaigns to capitalize on its goodwill and further promote its brand image, so as to become a reference for excellence in banking.

3. Human Capital

Investing in Human Capital is one of the essential components of success for Bank Audi Syria. Accordingly, the Bank aims at attracting highly qualified Syrian staff, from inside and outside the country. Once on board, these employees undergo extensive specialized trainings on modern banking practices, in addition to on-the-job trainings in all corresponding departments and branches.

BANK AUDI SYRIA sa ACTIVITIES IN 2006

17

In 2006, the number of employees reached 149, distributed among the Bank’s 5 branches and Headquarters. Bank policies and procedures were further upgraded and an Employee Performance Appraisal system was developed to ensure proper career planning and recognize employees’ performance.

Evolution of staff number

Jan-06 Feb-06 Mar-06 Apr-06 May-06 Jun-06 Jul-06 Aug-06 Sep-06 Oct-06 Nov-06 Dec-06

Percentage of trainees in Lebanon and Syria for 2006

■ Percentage of trainees in Bank Audi sal

■ Percentage of trainees in Bank Audi Syria

4. Information Technology

Bank Audi Syria heavily invested in its IT infrastructure, in line with the best international practices for modern banks. The Bank is continuously working on enhancing its IT capacity through building a solid IT infrastructure, while keeping up with international standards and developments in order to secure system reliability and flexibility.

The Bank has invested in state-of-the-art technology enabling real-time online connection between branches and Headquarters, and using thin client units instead of a PC network at the end user level. It has also opened a gateway to its banking system through the internet whereby the client uses a secured connection to access his accounts from anywhere in the world. In addition, the Bank has invested in IP Telephony technology where a single network (Data Network) is used to exchange voice and fax data among branches and Headquarters while maintaining secrecy and encryption provided by the VPN technology which enables a safe data transfer environment.

Num

ber o

f em

ploy

ees

18

BANK AUDI SYRIA sa ACTIVITIES IN 2006

5. Financial Performance

Bank Audi Syria achieved substantial growth in its activity by the end of its first complete financial year. Indeed, the Bank’s balance sheet shows an increase of 257% in total assets, exceeding SYP 17.8 billion, while total deposits with margin accounts reached SYP 15 billion, marking an increase of 582% compared to 2005 figures. As for the loan portfolio, it revealed the promising potential of the Syrian market by reaching SYP 5 billion, in addition to SYP 2.2 billion of off-balance sheet commitments by end 2006.

Net income before tax and unrealized losses reached SYP 144.3 million as at December 31st, 2006. Net income reached SYP 452,873, after deducting the income tax of SYP 36.8 million, as well as unrealized losses due to the revaluation of structural position which amounted to SYP 107.5 million (not subject to tax).

5.1. Assets

The Bank’s total footings reached SYP 17,788 million in total assets as at December 31st, 2006, distributed as such:- Cash in safe and Central Bank current accounts of SYP 2,154 million;- Placements with correspondents of SYP 9,706 millions;- Loan portfolio extended to customers of SYP 4,858 million;- Fixed assets of SYP 547 million;- Other assets of SYP 523 million, of which SYP 240 million blocked deposit at Central Bank, representing

10% of paid-up capital.

Growth indicators

■ 2005

■ 2006

Total assets Deposits & margins Lending

Assets breakdown

■ Bank placements■ Loan portfolio■ Cash & Central Bank■ Fixed assets■ Other assets

BANK AUDI SYRIA sa ACTIVITIES IN 2006

19

5.1.1. Assets GrowthThe comparison of asset figures of Quarter IV 2005 with those at end 2006 shows that the Bank’s placement portfolio increased by 216%, while its loan volume improved significantly, as the loan portfolio at end 2005 was minor. Tangible fixed assets grew by 104%, which goes in parallel with the Bank’s expansion plan in Damascus and other major cities.

5.1.2. Placements with Correspondent BanksThe placements portfolio was managed in a way to optimize the return on investments while maintaining the total liquidity ratio above 50%, in compliance with circulars issued by the Central Bank of Syria requiring a minimum liquidity ratio of 20% in all currencies. The placement portfolio reached SYP 9.7 billion by end 2006, broken down as such: - SYP 6.8 billion in term deposits maturing in less than one year; - SYP 1.9 billion in certificates of deposit in local and foreign currencies; - SYP 1 billion in bank current accounts.

5.1.3. Loan PortfolioThe loan portfolio witnessed a remarkable growth during 2006, compared to 2005, since the Bank’s management was keen on allocating these loans to various productive and performing economic sectors. As a result, both commercial and industrial sectors seized the largest share, which reached SYP 4,250 million of total facilities granted to customers, while the real estate sector share reached SYP 419 million and SYP 234 million constituted the amounts granted to the remaining sectors.

Assets growthIn millions of SYP

■ 2005

■ 2006

Bankplacements

Loanportfolio

Cash &Central Bank

Fixedassets

Otherassets

Placements portfolio

■ Certificates of deposit■ Term deposits■ Current accounts

20

BANK AUDI SYRIA sa ACTIVITIES IN 2006

5.2. Liabilities and Equity

5.2.1. Customer DepositsThe year 2006 witnessed an evident increase in customers’ deposits which grew from SYP 2,184 million in 2005 to SYP 13,451 million by end 2006, registering an increase of 516% without accounting for margin accounts. This is primarily due to customers’ confidence in the Bank. Further growth in the sources of funds is expected through an increase in the customer deposit base, as a result of the geographical expansion Bank Audi Syria plans to achieve in 2007, with a view to reaching all Syrian cities.

• Deposits at sight reached 38% of total deposits, compared to 46% in 2005;• Term deposits accounted for 62% of total deposits, compared to 54% in 2005; and• Syrian Pounds deposits reached 49% of total deposits, compared to 68% in 2005.

Loan portfolio breakdown by economic sector

■ Trade & Industry■ Real-estate■ Other

Deposits by currency

■ SYP deposits■ Foreign currency deposits

BANK AUDI SYRIA sa ACTIVITIES IN 2006

21

5.2.2. EquityBank Audi Syria’s capital is SYP 2.5 billion, allocated to 2,500,000 shares with a nominal value of SYP 1000 per share. The Bank’s net equity increased from SYP 2,548,074,359 in 2005 to reach SYP 2,548,527,232 by end 2006, thus growing by SYP 452,873 representing the net profit for 2006.

5.3. Off-Balance Sheet Commitments

Bank Audi Syria has actively participated in financing Syrian foreign trade, which is made evident in the total volume of indirect facilities that the Bank offered its customers, in the form of letters of credit and letters of guarantees, which reached 45% of total direct facilities extended to customers. The total indirect facilities reached SYP 2,169 million, broken down as such:

• Letters of guarantees and letters of credits issued at the request of customers reached SYP 1,482 million;

• Letters of guarantees and letters of credits issued at the request of banks reached SYP 687 million.

5.4. Profitability

Bank Audi Syria registered a realized net income of SYP 107,992,873 for the year 2006, after deducting the income tax of SYP 36,350,459. The realized net income is decreased by the value of SYP 107,540,000, representing unrealized losses not subject to tax and not available for distribution, to reach a net income of SYP 452,873 as shown in the Bank’s income statement. As a result, the earnings per share reach SYP 0.1811 for the year ending December 31st, 2006.

5.4.1. Interest MarginThe net interest margin for 2006 reached over SYP 266 million, coming from customers and banks, compared to SYP 19 million in 2005, knowing that the interest spread on the Syrian Pound and foreign currencies is subject to market conditions which were kept relatively stagnant since 2005. Growth in interest margin, compared to 2005 figures, is mainly due to growth in the Bank’s total assets, which is considered as a good and healthy growth indicator.

Deposits by type

■ Sight deposits■ Term deposits■ Saving deposits

22

BANK AUDI SYRIA sa ACTIVITIES IN 2006

5.4.2. Commissions and Other RevenuesTotal non-interest income reached SYP 60.5 million, resulting from commissions on loans and commissions on trade finance operations. The profits arising from trading activity reached SYP 122.5 million, while other revenues reached SYP 3.8 million.

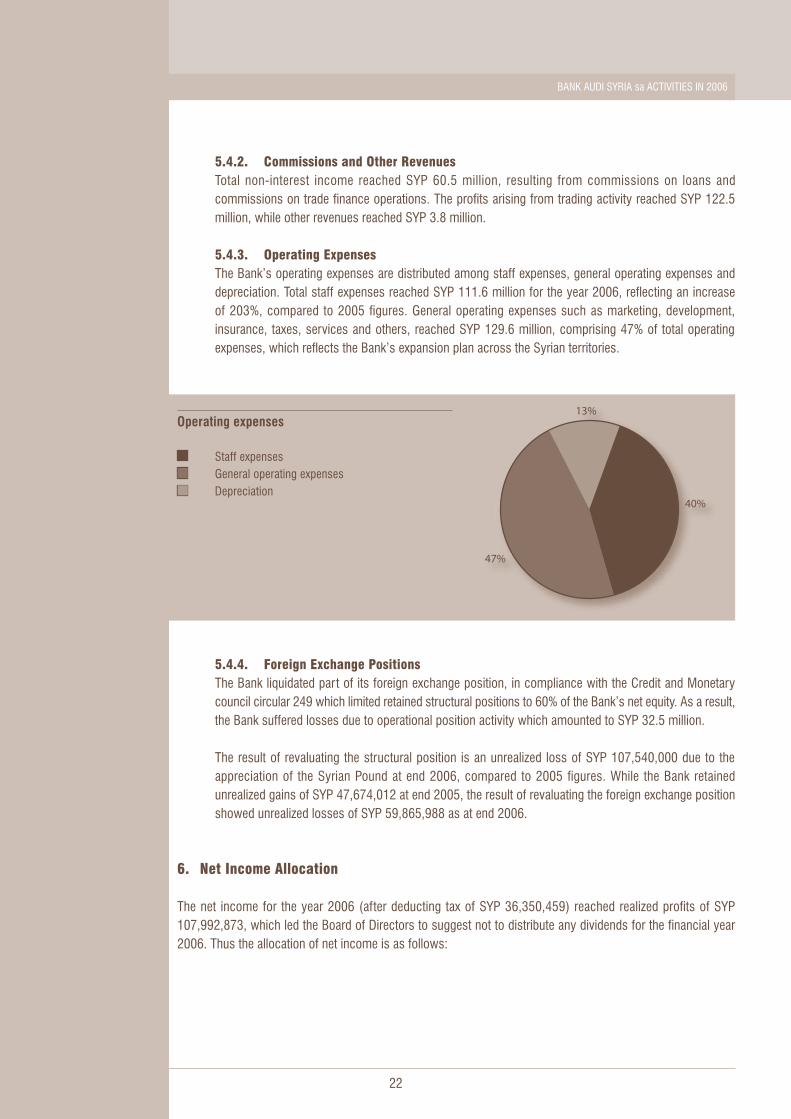

5.4.3. Operating ExpensesThe Bank’s operating expenses are distributed among staff expenses, general operating expenses and depreciation. Total staff expenses reached SYP 111.6 million for the year 2006, reflecting an increase of 203%, compared to 2005 figures. General operating expenses such as marketing, development, insurance, taxes, services and others, reached SYP 129.6 million, comprising 47% of total operating expenses, which reflects the Bank’s expansion plan across the Syrian territories.

5.4.4. Foreign Exchange PositionsThe Bank liquidated part of its foreign exchange position, in compliance with the Credit and Monetary council circular 249 which limited retained structural positions to 60% of the Bank’s net equity. As a result, the Bank suffered losses due to operational position activity which amounted to SYP 32.5 million.

The result of revaluating the structural position is an unrealized loss of SYP 107,540,000 due to the appreciation of the Syrian Pound at end 2006, compared to 2005 figures. While the Bank retained unrealized gains of SYP 47,674,012 at end 2005, the result of revaluating the foreign exchange position showed unrealized losses of SYP 59,865,988 as at end 2006.

6. Net Income Allocation

The net income for the year 2006 (after deducting tax of SYP 36,350,459) reached realized profits of SYP 107,992,873, which led the Board of Directors to suggest not to distribute any dividends for the financial year 2006. Thus the allocation of net income is as follows:

Operating expenses

■ Staff expenses■ General operating expenses■ Depreciation

BANK AUDI SYRIA sa ACTIVITIES IN 2006

23

• Income after Tax SYP 107,992,873

• Statutory Reserve: Not available for distribution for 10% of net income as stated in Central Bank regulations and ar ticle 242 of Trade Law SYP 10,799,287

• Special Reserve: Not available for distribution for 10% of net income as stated in Central Bank regulations and ar ticle 97/A of Law 23 for 2002 SYP 10,799,287

• Retained earnings SYP 86,394,300

As described above, net equity reached SYP 2,548,527,232, broken down as such:

• Share capital SYP 2,500,000,000• Statutory Reserve SYP 10,839,322• Special Reserve SYP 10,839,322• (Accumulated losses) not available for distribution SYP 59,865,988

• Retained earnings SYP 86,714,576

25

INDEPENDENT AUDITORS’ REPORT

BANK AUDI SYRIA sa

F INANC IAL STATEMENTS

31 DECEMBER 2006

29

From 13 September 2005 till 2006 31 December 2005In Syrian Pounds Notes Interest and similar income 8 599,930,846 26,302,061Interest and similar expenses 9 (333,310,363) (7,150,380) Net interest income 266,620,483 19,151,681 Net fee and commission income 10 60,453,235 991,753Unrealised net foreign exchange difference 29 (107,540,000) 47,674,012Gains less losses arising from dealing in foreign currencies (32,523,920) (12,364)Gains arising from trading activities 32 122,520,000 -Other income 3,798,214 36,758,686 313,328,012 104,563,768 Personnel expenses 11 (111,622,527) (36,701,834)Depreciation and amor tization 19 & 20 (35,255,922) -Other operating expenses 12 (129,646,231) (19,654,127) (276,524,680) (56,355,961) PROFIT BEFORE TAX 36,803,332 48,207,807 Income tax expense 13 (36,350,459) (133,448) PROFIT FOR THE YEAR 452,873 48,074,359 Basic earnings per share 14 0.18 76.92Diluted earnings per share 14 0.18 76.92

INCOME STATEMENT

Year ended 31 December 2006

BALANCE SHEET

31 December 2006

2006 2005In Syrian Pounds Notes

ASSETS Cash and balances with the Central Bank 15 2,153,644,331 1,265,303,765Due from banks 16 9,705,730,991 3,071,377,030Loans and advances to customers 17 4,857,663,532 16,805,612Available for sale investments 18 50,000,000 -Premises, equipment and projects under construction 19 436,188,291 213,452,006Intangible assets 20 111,162,048 102,717,542Other assets 21 233,696,061 56,300,864Statutory blocked funds 22 239,523,878 255,772,557

TOTAL ASSETS 17,787,609,132 4,981,729,376 LIABILITIES AND EQUITY LIABILITIES Due to banks 23 130,149,405 18,682,756Margin Accounts 24 1,513,334,580 10,772,544Customers’ deposits 25 13,451,086,984 2,184,367,462Other liabilities 26 144,510,931 219,832,255

15,239,081,900 2,433,655,017

EQUITY Share capital 27 2,500,000,000 2,500,000,000Statutory reserve 28 10,839,322 40,035Special reserve 28 10,839,322 40,035(Accumulated losses) Retained earnings not available for distribution 29 (59,865,988) 47,674,012Retained earnings 29 86,714,576 320,277 2,548,527,232 2,548,074,359

TOTAL LIABILITIES AND EQUITY 17,787,609,132 4,981,729,376

The financial statements were authorised for issue in accordance with a resolution of the directors on 1 February 2007.

Dr. Georges Achi Mr. Bassel HamwiChairman Deputy Chairman & General Manager

The attached notes 1 to 34 form par t of these financial statements.

30

(Acc

umul

ated

loss

es)

R

etai

ned

earn

ings

not a

vaila

ble

Shar

e ca

pita

l St

atut

ory

rese

rve

Spec

ial r

eser

ve

for

dist

ribu

tion

Ret

aine

d ea

rnin

gs

Tota

lIn

Syr

ian

Poun

ds

Not

es

Bala

nce

at 1

Jan

uary

200

6

2,50

0,00

0,00

0 40

,035

40

,035

47

,674

,012

32

0,27

7 2,

548,

074,

359

Net p

rofit

for t

he y

ear

-

- -

- 45

2,87

3 45

2,87

3

Tran

sfer

to re

tain

ed e

arni

ngs

not a

vaila

ble

for d

istri

butio

n 29

-

- -

(107

,540

,000

) 10

7,54

0,00

0 -

Tran

sfer

to s

tatu

tory

rese

rve

28

- 10

,799

,287

-

- (1

0,79

9,28

7)

-

Tran

sfer

to s

peci

al re

serv

e 28

-

- 10

,799

,287

-

(10,

799,

287)

-

Bala

nce

at 3

1 D

ecem

ber

2006

2,50

0,00

0,00

0 10

,839

,322

10

,839

,322

(5

9,86

5,98

8)

86,7

14,5

76

2,54

8,52

7,23

2

Bala

nce

at 1

3 Se

ptem

ber 2

005

-

- -

- -

-

Capi

tal P

aym

ent

27

2,50

0,00

0,00

0 -

- -

- 2,

500,

000,

000

Prof

it fo

r the

per

iod

-

- -

- 48

,074

,359

48

,074

,359

Tran

sfer

to re

tain

ed e

arni

ngs

not a

vaila

ble

for d

istri

butio

n

29

- -

- 47

,674

,012

(4

7,67

4,01

2)

-

Tran

sfer

to s

tatu

tory

rese

rve

28

- 40

,035

-

- (4

0,03

5)

-

Tran

sfer

to s

peci

al re

serv

e 28

-

- 40

,035

-

(40,

035)

-

Bala

nce

at 3

1 D

ecem

ber

2005

2,50

0,00

0,00

0 40

,035

40

,035

47

,674

,012

32

0,27

7 2,

548,

074,

359

The

atta

ched

not

es 1

to 3

4 fo

rm p

art o

f the

se fi

nanc

ial s

tate

men

ts.

31

STATEMENT OF CHANGES IN EQUITY

Year ended 31 December 2006

32

STATEMENT OF CASH FLOWS

From 13 September 2005 till 2006 31 December 2005In Syrian Pounds Notes

OPERATING ACTIVITIESProfit before tax 36,803,332 48,207,807Adjustments for:

Depreciation & Amortisation 35,255,922 -Non-recurring income 30 - (36,749,500)Unrealised foreign exchange loss 16,248,679 10,051,558

Operating profit before changes in operating assets and liabilities 88,307,933 21,509,865

Due from banks (4,594,622,089) -Loans and advances to customers (4,840,857,920) (16,805,612)Other assets (177,395,197) (56,300,864)Margin accounts 1,502,562,036 10,772,544Customers’ deposits 11,266,719,522 2,184,367,462Other liabilities (111,538,335) 246,396,749

Net cash flows from operations 3,133,175,950 2,389,940,144

Income tax paid (133,448) -

Net cash flows from operating activities 3,133,042,502 2,389,940,144

INVESTING ACTIVITIESPurchase of premises, equipment and projects under construction (253,018,220) (213,452,006)Purchase of intangible assets (13,418,493) (102,717,542)Statutory blocked funds - (255,772,557)Purchase of non-trading investments (50,000,000) -

Net cash flows used in investing activities (316,436,713) (571,942,105)

FINANCING ACTIVITIESCapital payment - 2,500,000,000

Net cash flows from financing activities - 2,500,000,000

INCREASE IN CASH AND CASH EQUIVALENTS 2,816,605,789 4,317,998,039

Cash and cash equivalents at 1 January 4,317,998,039 -

CASH AND CASH EQUIVALENTS AT 31 DECEMBER 31 7,134,603,828 4,317,998,039

The attached notes 1 to 34 form par t of these financial statements.

BANK AUDI SYRIA sa

NOTES TO THE

F INANC IAL STATEMENTS

31 DECEMBER 2006

NOTES TO THE FINANCIAL STATEMENTS

35

1. Corporate Information

Bank Audi Syria sa (the “Bank”) was established as a public shareholding company on 30 August 2005 under commercial registration number (14456), and based on the decree of the government banking control commission number 703/IA dated 13 September 2005 and in accordance with the banking law number 28 for the year 2001. The Bank was registered under number (12) as a private bank, with its Headquarters in Damascus - Syria. The Bank’s paid in capital is SYP 2,500,000,000 divided into 2,500,000 shares with a par value of SYP 1,000 per share. The Bank commenced its operations on 28 September 2005.

The Bank provides several banking activities through its Headquarters and its branches in Damascus, Aleppo and Lattakia.

The Bank is 47% owned by Bank Audi sal.

The First General Assembly of the Bank’s shareholders held on 20 August 2005 resolved to enter into a technical assistance agreement with Bank Audi sal to transfer some of Bank Audi sal’s know-how and management experience in banking activities to Bank AudiSyria sa.

Under the terms of this agreement, Bank Audi sal will provide the following services:

• Assisting in defining and implementing strategy for banking operations in Syria.• Operational assistance through recruiting, training, supervising and evaluating the performance of the Bank’s employees in

addition to staff provisioning to the Bank.• Assisting in defining and implementing procedures for the operational risk management• Assisting in evaluating, developing and selecting the required information technology, management information systems and

communication infrastructure necessary to carry out the Bank’s business.• Assisting in product development, through making available to the Bank a range of Bank Audi sal products that are appropriate

for the Syrian market.• Assisting in research products, through making available Bank Audi sal research products to the Bank or conducting specific

research.

2. Significant Accounting Policies

The significant accounting policies adopted in the preparation of the financial statements are set out below:

Basis of PreparationThe financial statements are prepared under the historical cost convention as modified for the measurement at fair value of available for sale investments and trading investments.

The financial statements have been presented in Syrian Pound which is the functional and presentation currency of the Bank.

Statement of ComplianceThe financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and Central Bank of Syria’s laws and regulations.

The accounting policies are consistent with those used in the previous year.

36

NOTES TO THE FINANCIAL STATEMENTS

New and Amended Standards and Interpretations Issued but not yet Effective

Amendments to IAS 1 – Capital DisclosuresAmendments to IAS 1 Presentation of Financial Statements were issued by the IASB as Capital Disclosures in August 2005. They are required to be applied for periods beginning on or after 1 January 2007. When effective, these amendments will require disclosure of information enabling evaluation of the Bank’s objectives, policies and processes for managing capital.

IFRS 7 Financial Instruments: DisclosuresIFRS 7 Financial Instruments: Disclosures was issued by the IASB in August 2005, becoming effective for periods beginning on or after 1 January 2007. The new standard will require additional disclosure of the significance of financial instruments for the Bank’s financial position and performance and information about exposure to risks arising from financial instruments.

Due from Banks and Other Money Market PlacementsThese are stated at cost, less any amounts written off and provision for impairment.

Loans and AdvancesThese are stated at cost, net of interest suspended, provisions for impairment and any amounts written off.

Trading InvestmentsThese are initially recognised at cost and subsequently remeasured at fair value. All related realised and unrealised gains or losses are included in gains less losses arising from trading activities. Interest earned or dividends received are included in interest and similar income and dividend income respectively.

Non-Trading InvestmentsThese are classified as follows:

• Held to maturity• Available for sale• Investments carried at fair value through income statement • Loans and advances

All investments are initially recognised at fair value, being the fair value of the consideration given including directly attributable transaction costs.

Premiums and discounts on non-trading investments (excluding those carried at fair value through income statement) are amortised using the effective interest rate method and taken to interest income.

Held to Maturity

Investments classified as held to maturity have fixed or determinable payments and fixed maturity and are intended to be held to maturity. They are carried at amortised cost using the effective interest method, less provision for impairment.

Available for Sale

After initial recognition, investments which are classified “available for sale” are normally remeasured at fair value, unless fair value cannot be reliably determined in which case they are measured at cost less impairment. Fair value changes which are not part of an effective hedging relationship are reported as a separate component of equity until the investment is derecognised or the investment is determined to be impaired. On derecognition or impairment the cumulative gain or loss previously reported as “cumulative changes in fair value” within equity, is included in the income statement for the period.

NOTES TO THE FINANCIAL STATEMENTS

37

Dividends earned on investments are recognised in the income statement as “Dividends received” when the right of payment has been established.

That portion of any fair value changes relating to an effective hedging relationship is recognised directly in the income statement.

Investments Carried at Fair Value through Profit and LossInvestments are classified as fair value through profit and loss account if the fair value of the investment can be reliably measured and the classification as fair value through profit and loss account is as per the documented strategy of the Bank. Investments classified as “Investments at fair value through profit and loss” upon initial recognition are remeasured at fair value with all changes in fair value being recorded in the income statement.

Fair ValuesFor investments and derivatives quoted in an active market, fair value is determined by reference to quoted market prices. Bid prices are used for assets and offer prices are used for liabilities.

For financial instruments where there is no active market fair value is normally based on one of the following:• recent transactions• brokers’ quotes• the expected cash flows discounted at current rates applicable for items with similar terms and risk characteristics • option pricing models.

The estimated fair value of deposits with no stated maturity, which includes non-interest bearing deposits, is the amount payable on demand.

Premises and EquipmentAll items of premises and equipment are initially recorded at cost. Depreciation is provided on a straight-line basis over the estimated useful lives of all premises and equipment. Whenever the recoverable amount of an asset is impaired, the carrying value is reduced to the recoverable amount and the impairment loss is recorded in the statement of income.

Projects under construction are not depreciated until such time as the relevant assets are completed and put into operational use.

DepositsAll money market and customer deposits are carried at cost less amounts repaid.

TaxationThe Bank provides for income tax in accordance with the Banks Law no. (28) for the year 2001, and in accordance with IAS 12.

Deferred income taxation is provided using the liability method on all temporary differences at the balance sheet date. Deferred income tax liabilities are measured at the tax rates that are expected to apply to the period when the liability is settled, based on laws that have been enacted at the balance sheet date. The Bank does not recognise deferred income tax asset since it is not probable that deferred income tax asset will be utilised against taxable profits.

ProvisionsProvisions are recognised when the Bank has a present obligation (legal or constructive) arising from a past event and the costs to settle the obligation are both probable and able to be reliably measured.

38

NOTES TO THE FINANCIAL STATEMENTS

OffsettingFinancial assets and financial liabilities are only offset and the net amount reported in the balance sheet when there is a legally enforceable right to set off the recognised amounts and the Bank intends to either settle on a net basis, or to realise the asset and settle the liability simultaneously.

Revenue RecognitionInterest income as well as fees which are considered an integral part of the effective yield of a financial asset, are recognised using the effective yield method, unless collectibility is in doubt. The recognition of interest income is suspended when loans become impaired, such as when overdue by more than 90 days.

Notional interest is recognised on impaired loans and other financial assets based on the rate used to discount future cash flows to their net present value. Other fees receivable are recognised as the services are provided. Dividend income is recognised when the right to receive payment is established.

Foreign Currencies

Translation of Foreign Currency Transactions

Transactions in foreign currencies are initially recorded in the functional currency rate of exchange (published by the Central Bank of Syria) at the date of the transaction. Monetary assets and liabilities in foreign currencies are translated into SYP at rates of exchange prevailing at the balance sheet date (published by the Central Bank of Syria). Any gains or losses are taken to the income statement.

Cash and Cash EquivalentsCash and cash equivalents comprise cash and balances with Central Bank and deposits with banks and other financial institutions with original maturities of less than 90 days, less due to banks and other financial institutions with original maturities of less than 90 days.

Impairment of Financial AssetsAn assessment is made at each balance sheet date to determine whether there is objective evidence that a specific financial asset may be impaired. If such evidence exists, any impairment loss is recognised in the income statement.

Impairment is determined as follows:

(a) for assets carried at amortised cost, impairment is based on estimated cash flows, which are discounted at the original effective interest rate;

(b) for assets carried at fair value, impairment is the difference between cost and fair value;(c) for assets carried at cost, impairment is present value of future cash flows discounted at the current market rate of return for

a similar financial asset.

For available for sale equity investments reversal of impairment losses are recorded as increases in cumulative changes in fair value through equity.

Intangible AssetsIntangible assets include the value of computer software and key money. Intangible assets acquired separately are measured on initial recognition at cost. Following initial recognition, intangible assets are carried at cost less any accumulated amortisation and any accumulated impairment losses. The useful lives of intangible assets are assessed to be either finite or indefinite. Intangible assets with finite lives are amortised over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortisation period and the amortisation method for an intangible asset with a finite useful life is reviewed at least at each financial year-end. Changes in the expected useful life or the expected pattern of consumption of future economic

NOTES TO THE FINANCIAL STATEMENTS

39

benefits embodied in the asset is accounted for by changing the amortisation period or method, as appropriate, and treated as changes in accounting estimates. The amortisation expense on intangible assets with finite lives is recognised in the income statement in the expense category consistent.

Use of EstimatesThe preparation of the financial statements requires management to make estimates and assumptions that affect the reported amount of financial assets and liabilities and disclosure of contingent liabilities. These estimates and assumptions also affect the revenues and expenses and the resultant provisions as well as fair value changes reported in equity. The key assumptions concerning the future and other key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the financial year are discussed below:

Impairment Losses on Loans and Advances

The Bank reviews its problem loans and advances on a quarterly basis to assess whether a provision for impairment should be recorded in the income statement. In particular, considerable judgement by management is required in the estimation of the amount and timing of future cash flows when determining the level of provisions required. Such estimates are necessarily based on assumptions about several factors involving varying degrees of judgment and uncertainty, and actual results may differ resulting in future changes to such provisions.

Fiduciary AssetsAssets held in a fiduciary capacity are not reported in the financial statements, as they are not the assets of the Bank.

Dividends on Ordinary SharesDividends on ordinary shares are recognized as liability and deducted from equity when they are approved by the Bank’s shareholders. Interim dividends are deducted from equity when paid.

3. Credit Risk and Concentration of Assets, Liabilities and Off-Balance Sheet Items

Credit risk is the risk that one party to a financial instrument will fail to discharge an obligation and cause the other party to incur a financial loss. The Bank manages credit risk by setting limits for individual borrowers and groups of borrowers and for geographical and industry segments. The Bank also monitors credit exposures, and continually assesses the creditworthiness of counterparties. In addition, the Bank obtains security where appropriate, enters into master netting agreements and collateral arrangements with counterparties, and limits the duration of exposures.

The maximum credit risk, without taking into account the fair value of any collateral and netting agreements, is limited to the amounts on the balance sheet plus commitments to customers disclosed in note 33.

Concentrations arise when a number of counterparties are engaged in similar business activities, or activities in the same geographic region, or have similar economic features that would cause their ability to meet contractual obligations to be similarly affected by changes in economic, political or other conditions. Concentrations indicate the relative sensitivity of the Bank’s performance to developments affecting a particular industry or geographic location.

40

NOTES TO THE FINANCIAL STATEMENTS

The distribution of assets, liabilities, and off-balance sheet items by geographic region and industry sector was as follows:

2006 2005 Credit Credit Assets Liabilities Commitments Assets Liabilities Commitments In thousands of Syrian Pounds

Geographic region:Domestic (Syria) 9,853,353 15,237,890 1,210,990 2,324,317 2,243,058 61,543Other Middle East 2,719,013 1,192 853,458 2,070,478 190,597 2,700Europe 5,215,243 - 104,500 586,934 - 47,919

17,787,609 15,239,082 2,168,948 4,981,729 2,433,655 112,162

Industry sector:Trading and manufacturing 3,907,298 1,553,415 1,101,817 - 2,183,221 63,478Banks and financial institutions 12,148,900 130,149 687,108 4,438,965 190,597 -Construction and real estate 950,365 5,647 378,523 16,802 - -Other 781,046 13,549,871 1,500 525,962 59,837 48,684

17,787,609 15,239,082 2,168,948 4,981,729 2,433,655 112,162

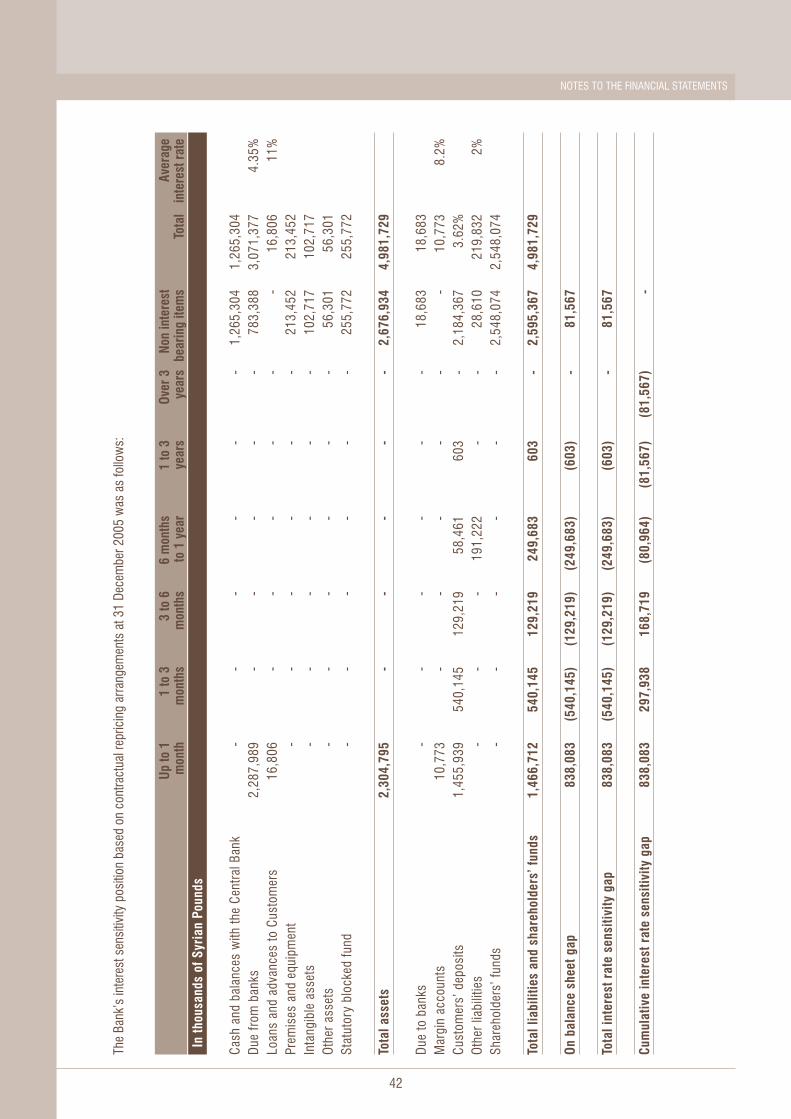

4. Interest Rate Risk

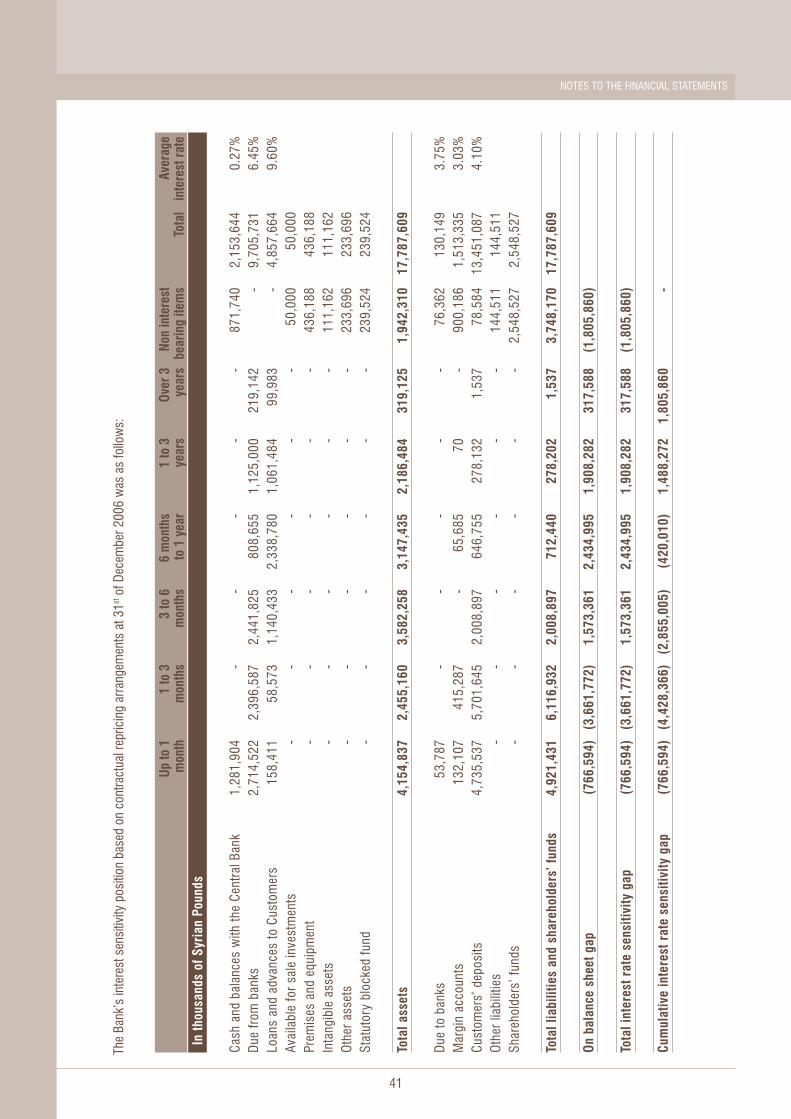

Interest rate risk arises from the possibility that changes in interest rates will affect future profitability or the fair values of financial instruments. The Bank is exposed to interest rate risk as a result of mismatches of interest rate repricing of assets and liabilities.The Bank’s interest sensitivity position based on contractual repricing arrangements or maturity at 31 December 2006 has been shown in the table below. The expected repricing and maturity dates may differ significantly from the contractual dates particularly with regard to the maturity of customer demand deposits amounting to SYP 8,601,776,453 (2005: SYP 1,138,040,704).

NOTES TO THE FINANCIAL STATEMENTS

41

The

Bank

’s in

tere

st s

ensi

tivity

pos

ition

bas

ed o

n co

ntra

ctua

l rep

ricin

g ar

rang

emen

ts a

t 31st

of D

ecem

ber 2

006

was

as

follo

ws:

Up

to 1

1

to 3

3

to 6

6

mon

ths

1

to 3

Ov

er 3

No

n in

tere

st

Av

erag

e

mon

th

mon

ths

mon

ths

to 1

yea

r ye

ars

year

s be

arin

g ite

ms

Tota

l in

tere

st ra

teIn

thou

sand

s of

Syr

ian

Poun

ds

Cash

and

bal

ance

s w

ith th

e Ce

ntra

l Ban

k

1,28

1,90

4 -

- -

- -

871,

740

2,15

3,64

4 0.

27%

Due

from

ban

ks

2,71

4,52

2 2,

396,

587

2,44

1,82

5 80

8,65

5 1,

125,

000

219,

142

- 9,

705,

731

6.45

%Lo

ans

and

adva

nces

to C

usto

mer

s 15

8,41

1 58

,573

1,

140,

433

2,33

8,78

0 1,

061,

484

99,9

83

- 4,

857,

664

9.60

%Av

aila

ble

for s

ale

inve

stm

ents

-

- -

- -

- 50

,000

50

,000

Prem

ises

and

equ

ipm

ent

- -

- -

- -

436,

188

436,

188

Inta

ngib

le a

sset

s -

- -

- -

- 11

1,16

2 11

1,16

2O

ther

ass

ets

- -

- -

- -

233,

696

233,

696

Stat

utor

y bl

ocke

d fu

nd

- -

- -

- -

239,

524

239,

524

Tota

l ass

ets

4,15

4,83

7 2,

455,

160

3,58

2,25

8 3,

147,

435

2,18

6,48

4 31

9,12

5 1,

942,

310

17,7

87,6

09

Due

to b

anks

53

,787

-

- -

- -

76,3

62

130,

149

3.75

%M

argi

n ac

coun

ts

132,

107

415,

287

- 65

,685

70

-

900,

186

1,51

3,33

5 3.

03%

Cust

omer

s’ d

epos

its

4,73

5,53

7 5,

701,

645

2,00

8,89

7 64

6,75

5 27

8,13

2 1,

537

78,5

84

13,4

51,0

87

4.10

%O

ther

liab

ilitie

s -

- -

- -

- 14

4,51

1 14

4,51

1Sh

areh

olde

rs’ f

unds

-

- -

- -

- 2,

548,

527

2,54

8,52

7

Tota

l lia

bilit

ies

and

shar

ehol

ders

’ fun

ds

4,92

1,43

1 6,

116,

932

2,00

8,89

7 71

2,44

0 27

8,20

2 1,

537

3,74

8,17

0 17

,787

,609

On

bala

nce

shee

t gap

(7

66,5

94)

(3,6

61,7

72)

1,57

3,36

1 2,

434,

995

1,90

8,28

2 31

7,58

8 (1

,805

,860

)

Tota

l int

eres

t rat

e se

nsiti

vity

gap

(7

66,5

94)

(3,6

61,7

72)

1,57

3,36

1 2,

434,

995

1,90

8,28

2 31

7,58

8 (1

,805

,860

)

Cum

ulat

ive

inte

rest

rat

e se

nsiti

vity

gap

(7

66,5

94)

(4,4

28,3

66)

(2,8

55,0

05)

(420

,010

) 1,

488,

272

1,80

5,86

0 -

42

NOTES TO THE FINANCIAL STATEMENTS

The

Bank

’s in

tere

st s

ensi

tivity

pos

ition

bas

ed o

n co

ntra

ctua

l rep

ricin

g ar

rang

emen

ts a

t 31

Dece

mbe

r 200

5 w

as a

s fo

llow

s:

Up

to 1

1

to 3

3

to 6

6

mon

ths

1

to 3

Ov

er 3

No

n in

tere

st

Av

erag

e

mon

th

mon

ths

mon

ths

to 1

yea

r ye

ars

year

s be

arin

g ite

ms

Tota

l in

tere

st ra

teIn

thou

sand

s of

Syr

ian

Poun

ds

Cash

and

bal

ance

s w

ith th

e Ce

ntra

l Ban

k

- -

- -

- -

1,26

5,30

4 1,

265,

304

Due

from

ban

ks

2,28

7,98

9 -

- -

- -

783,

388

3,07

1,37

7 4.

35%

Loan

s an

d ad

vanc

es to

Cus

tom

ers

16,8

06

- -

- -

- -

16,8

06

11%

Prem

ises

and

equ

ipm

ent

- -

- -

- -

213,

452

213,

452

Inta

ngib

le a

sset

s -

- -

- -

- 10

2,71

7 10

2,71

7O

ther

ass

ets

- -

- -

- -

56,

301

56,3

01St

atut

ory

bloc

ked

fund

-

- -

- -

- 25

5,77

2 25

5,77

2

Tota

l ass

ets

2,30

4,79

5 -

- -

- -

2,67

6,93

4 4,

981,

729

Due

to b

anks

-

- -

- -

-

18,6

83

1

8,68

3M

argi

n ac

coun

ts

1

0,77

3 -

- -

- -

-

10,

773

8.2%

Cust

omer

s’ d

epos

its

1,45

5,93

9 54

0,14

5 12

9,21

9 58

,461

60

3 -

2,18

4,36

7 3.

62%

Oth

er li

abili

ties

- -

- 19

1,22

2 -

- 28

,610

219,

832

2%Sh

areh

olde

rs’ f

unds

-

- -

- -

- 2,

548,

074

2,54

8,07

4

Tota

l lia

bilit

ies

and

shar

ehol

ders

’ fun

ds

1,46

6,71

2 54

0,14

5 12

9,21

9 24

9,68

3 60

3 -

2,59

5,36

7 4,

981,

729

On

bala

nce

shee

t gap

8

38,0

83

(540

,145

) (1

29,2

19)

(249

,683

) (6

03)

- 81

,567

Tota

l int

eres

t rat

e se

nsiti

vity

gap

8

38,0

83

(540

,145

) (1

29,2

19)

(249

,683

) (6

03)

- 81

,567

Cum

ulat

ive

inte

rest

rat

e se

nsiti

vity

gap

8

38,0

83

297,

938

16

8,71

9

(80,

964)

(8

1,56

7)

(81,

567)

-

NOTES TO THE FINANCIAL STATEMENTS

43

5. Currency Risk

Currency risk is the risk that the value of a financial instrument will fluctuate due to changes in foreign exchange rates. The Bank views the Syrian Pound as its functional currency.

Breakdown of Assets and Liabilities by Currency

31 December 2006 31 December 2005 SYP USD Other SYP USD OtherIn thousands of Syrian Pounds

ASSETSCash and balances with the Central Bank 1,732,345 362,337 58,962 1,153,823 98,732 12,749Due from banks 2,272,627 6,802,542 630,563 337,815 2,664,352 69,210Loans and advances to customers 3,927,184 802,031 128,448 16,806 - -Available for sale investments 50,000 - - - - -Premises and equipment 436,188 - - 213,452 - -Intangible assets 111,162 - - 102,717 - -Other assets 134,720 94,236 4,740 56,301 - -Statutory blocked funds 21,236 218,288 - 21,236 234,536 -

Total assets 8,685,462 8,279,434 822,713 1,902,150 2,997,620 81,959

LIABILITIESDue to banks and other financial Institutions 42,758 85,037 2,354 15,658 3,025 -Margin accounts 834,052 676,080 3,203 7,762 2,029 982Customers’ deposits 6,649,153 6,322,790 479,143 1,493,986 612,126 78,255Other liabilities 110,830 16,770 16,912 27,468 192,364 -Shareholders’ funds 2,548,527 - - 2,548,074 - -

Total liabilities and shareholders’ Equity 10,185,320 7,100,677 501,612 4,092,948 809,544 79,237

Net exposure (1,499,858) 1,178,757 321,101 (2,190,798) 2,188,076 2,722

6. Liquidity Risk

Liquidity risk is the risk that the Bank will be unable to meet its liabilities when they fall due. To limit this risk, management has arranged diversified funding sources, manages assets with liquidity in mind, and monitors liquidity on a daily basis. In addition, the Bank maintains a statutory deposit with the Central Bank of Syria equals to 5% of customer deposits and 10% of the Bank’s capital.

44

NOTES TO THE FINANCIAL STATEMENTS

U

p to

1

Up

to 3

3

to 6

6

mon

ths

1 to

3

Over

3

No

spec

ific

m

onth

m

onth

s m

onth

s to

1 y

ear

year

s ye

ars

mat

urity

To

tal

In th

ousa

nds

of S

yria

n Po

unds

Cash

and

bal

ance

s w

ith th

e Ce

ntra

l Ban

k 1,

281,

903

- -

- -

- 87

1,74

1 2,

153,

644

Due

from

ban

ks

2,71

4,52

2 2,

396,

587

2,44

1,82

5 80

8,65

5 1,

125,

000

219,

142

- 9,

705,

731

Loan

s an

d ad

vanc

es to

Cust

omer

s 15

8,41

1 58

,573

1,

140,

433

2,33

8,78

0 1,

061,

484

99,9

83

- 4,

857,

664

Avai

labl

e fo

r sal

e in

vest

men

ts

- -

- -

- -

50,0

00

50,0

00Pr

emis

es a

nd e

quip

men

t -

- -

- -

- 43

6,18

8

436,

188

Inta

ngib

le a

sset

s -

- -

- -

- 11

1,16

2

111,

162

Oth

er a

sset

s 5,

706

1,61

9 6,

000

15,4

74

4,00

0 6,

445

194,

452

233,

696

Stat

utor

y bl

ocke

d fu

nds

- -

- -

- -

239,

524

239,

524

Tota

l ass

ets

4,16

0,54

2 2,

456,

779

3,58

8,25

8 3,

162,

909

2,19

0,48

4 32

5,57

0 1,

903,

067

17,7

87,6

09

Due

to b

anks

13

0,14

9 -

- -

- -

- 13

0,14

9M

argi

n ac

coun

ts

132,

107

415,

287

- 65

,685

70

-

900,

186

1,51

3,33

5Cu

stom

ers’

dep

osits

4,

814,

121

5,70

1,64

5 2,

008,

897

646,

755

278,

132

1,53

7 -

13,4

51,0

87O

ther

liab

ilitie

s 37

,969

39

,066

50

,046

7,

813

1,63

0 -

7,98

7 14

4,51

1To

tal l

iabi

litie

s 5,

114,

346

6,15

5,99

8 2,

058,

943

720,

253

279,

832

1,53

7 90

8,17

3 15

,239

,082

N

et li

quid

ity g

ap

(953

,804

) (3

,699

,219

) 1,

529,

315

2,44

2,65

6 1,

910,

652

324,

033

994,

894

2,54

8,52

7

The

tabl

e be

low

sum

mar

ises

the

mat

urity

pro

file

of th

e Ba

nk’s

ass

ets

and

liabi

litie

s ba

sed

on c

ontra

ctua

l rep

aym

ent a

rran

gem

ents

and

doe

s no

t tak

e ac

coun

t of t

he e

ffect

ive

mat

uriti

es

as in

dica

ted

by th

e Ba

nk’s

dep

osit

rete

ntio

n hi

stor

y. T

he m

atur

ity p

rofil

e of

the

asse

ts a

nd li

abilit

ies

at 3

1 De

cem

ber 2

006

was

as

follo

ws:

NOTES TO THE FINANCIAL STATEMENTS

45

The

mat

urity

pro

file

of th

e as

sets

and

liab

ilitie

s at

31

Dece

mbe

r 200

5 w

as a

s fo

llow

s:

U

p to

1

Up

to 3

3

to 6

6

mon

ths

1 to

3

Over

3

No

spec

ific

m

onth

m

onth

s m

onth

s to

1 y

ear

year

s ye

ars

mat

urity

To

tal

In th

ousa

nds

of S

yria

n Po

unds

Cash

and

bal

ance

s w

ith th

e Ce

ntra

l Ban

k 1,

265,

304

-

- -

- -

- 1,

265,

304

Due

from

ban

ks

783,

388

2,

287,

990

-

- -

- -

3,07

1,37

8

Loan

s an

d ad

vanc

es to

Cust

omer

s 16

,805

-

- -

- -

- 16

,805

Pr

emis

es a

nd e

quip

men

t -

- -

- -

- 21

3,45

2 21

3,45

2In

tang

ible

ass

ets

- -

- -

- -

102,

717

10

2,71

7 O

ther

ass

ets

- -

- -

- -

56,3

01

56,3

01

Stat

utor

y bl

ocke

d fu

nds

- -

- -

- -

255,

772

255,

772

Tota

l ass

ets

2,06

5,49

7

2,28

7,99

0

- -

- -

628,

242

4,98

1,72

9

Due

to b

anks

18

,683

-

- -

- -

- 18

,683

M

argi

n ac

coun

ts

10,7

73

- -

- -

- -

10,7

73

Cust

omer

s’ d

epos

its

1,45

5,93

9

540,

145

12

9,21

9

58,4

61

603

- -

2,18

4,36

7 O

ther

liab

ilitie

s -

- -

191,

222

-

- 28

,610

21

9,83

2To

tal l

iabi

litie

s 1,

485,

395

54

0,14

5

129,

219

24

9,68

3

603

- 28

,610

2,

433,

655

Net

liqu

idity

gap

58

0,10

2

1,74

7,84

5

(129

,219

) (2

49,6

83)

(603

) -

599,

632

2,54

8,07

4

46

NOTES TO THE FINANCIAL STATEMENTS

7. Fair Value of Financial Instruments

There are no material differences between carrying values and fair value of on and off-balance sheet financial instruments.

As explained in note 18, included under available for sale investments are unquoted equity investments with a value of SYP 50,000,000 for which fair value cannot be reliably determined due to non existence of an active securities market. There is no indication of impairment in the value of these investments as at the balance sheet date.

8. Interest and Similar Income

2006 2005In Syrian Pounds

Overdrafts 124,930,394 135,669Loans and advances to customers 64,362,867 -Discounted bills 18,872,685 -Due from banks 391,764,900 26,166,392

599,930,846 26,302,061

9. Interest and Similar Expenses

2006 2005In Syrian Pounds

Due to banks 11,060,488 1,583Customer deposits 306,909,457 7,142,270Margin accounts 15,340,418 6,527

333,310,363 7,150,380

10. Net Fee and Commission Income

2006 2005In Syrian Pounds

Fee and commission income 65,107,033 1,175,076Fee and commission expense (4,653,798) (183,323)

60,453,235 991,753

NOTES TO THE FINANCIAL STATEMENTS

47

11. Personnel Expenses

2006 2005In Syrian Pounds

Salaries and benefits 96,027,654 35,594,394Social securities 5,123,112 1,107,440Training and other expenses 10,471,761 - 111,622,527 36,701,834

12. Other Operating Expenses

2006 2005In Syrian Pounds

Rental expenses 16,074,289 3,286,284Adver tising and marketing 31,581,890 2,792,546Stationary and printing expenses 7,291,118 2,539,021Post, telephone, telex and internet 8,593,539 2,216,619Credit card expenses 1,615,955 2,200,000Governmental fees 1,103,736 2,147,615Consultation and legal fees 3,868,250 1,642,700Swift expenses 1,297,093 12,096Development expenses (note 32) 31,960,879 -Maintenance 4,208,212 -Travel and transpor tation 3,258,212 851,571Utilities 3,211,890 -Insurance 4,841,510 -Interest expense on balance due to related par ties (note 32) 1,246,316 624,945Other 9,493,342 1,340,730

129,646,231 19,654,127

48

NOTES TO THE FINANCIAL STATEMENTS

13. Income Tax

The relationship between the tax expense and the accounting profit can be explained as follows:

2006 2005In Syrian Pounds

Accounting profit before tax 36,803,332 48,207,807Add (subtract) unrealised loss (gain) on difference of exchange (note 29) 107,540,000 (47,674,012)Add key money amor tisation 1,058,502 -

145,401,834 533,795

Effective rate of income tax 25% 25%

Current income tax expense 36,350,459 133,448

14. Earnings Per Share

Basic earnings per share are calculated by dividing the net profit for the year by the weighted average number of shares outstanding during the year as follows:

2006 2005In Syrian Pounds

Profit for the year 452,873 48,074,359

Weighted average number of shares outstanding during the year 2,500,000 625,000Basic earnings per share 0.18 76.92

Diluted earnings per share have the same figure as the basic earnings per share since the Bank has not issued any instruments which would have an impact on earnings per share when exercised.

NOTES TO THE FINANCIAL STATEMENTS

49

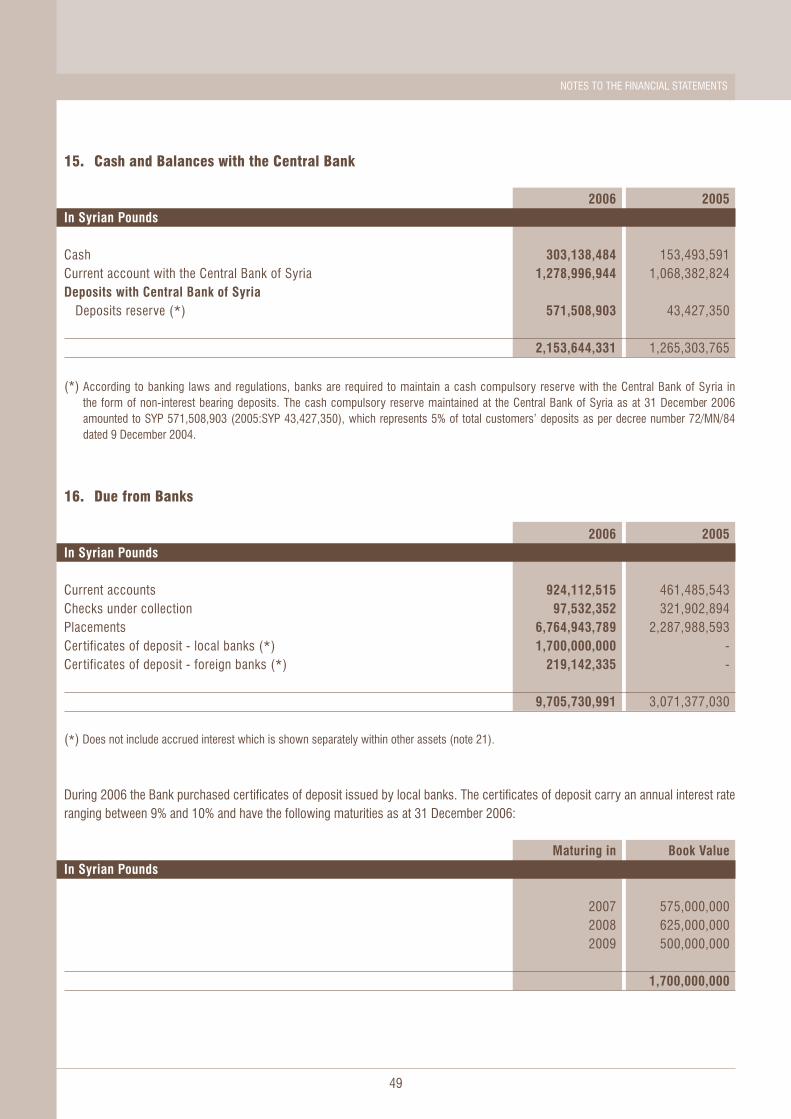

15. Cash and Balances with the Central Bank

2006 2005In Syrian Pounds

Cash 303,138,484 153,493,591Current account with the Central Bank of Syria 1,278,996,944 1,068,382,824Deposits with Central Bank of Syria

Deposits reserve (*) 571,508,903 43,427,350

2,153,644,331 1,265,303,765

(*) According to banking laws and regulations, banks are required to maintain a cash compulsory reserve with the Central Bank of Syria in the form of non-interest bearing deposits. The cash compulsory reserve maintained at the Central Bank of Syria as at 31 December 2006 amounted to SYP 571,508,903 (2005:SYP 43,427,350), which represents 5% of total customers’ deposits as per decree number 72/MN/84 dated 9 December 2004.

16. Due from Banks

2006 2005In Syrian Pounds

Current accounts 924,112,515 461,485,543Checks under collection 97,532,352 321,902,894Placements 6,764,943,789 2,287,988,593Cer tificates of deposit - local banks (*) 1,700,000,000 -Cer tificates of deposit - foreign banks (*) 219,142,335 -

9,705,730,991 3,071,377,030

(*) Does not include accrued interest which is shown separately within other assets (note 21).

During 2006 the Bank purchased certificates of deposit issued by local banks. The certificates of deposit carry an annual interest rate ranging between 9% and 10% and have the following maturities as at 31 December 2006:

Maturing in Book ValueIn Syrian Pounds

2007 575,000,000 2008 625,000,000 2009 500,000,000 1,700,000,000

50

NOTES TO THE FINANCIAL STATEMENTS

Moreover, the Bank purchased through Bank Audi sal certificates of deposit (Euro CDs) issued by foreign banks. The certificates of deposit carry an annual interest rate 7.625% and have the following maturities as at 31 December 2006:

Maturing in Book ValueIn Syrian Pounds

2010 101,334,250 2012 117,808,085 219,142,335

17. Loans and Advances to Customers

2006 2005In Syrian Pounds

Overdrafts 2,288,284,423 16,805,612Loans 1,973,767,814 -Discounted bills 697,098,150 -Unearned revenue (101,486,855) -

4,857,663,532 16,805,612 The composition of the loans and advances portfolio is as follows:

2006 2005In Syrian Pounds

Trading and manufacturing 4,205,370,240 -Private individuals 53,599,930 -Construction and real estate 418,641,238 16,805,612 Other 180,052,124 -

Total 4,857,663,532 16,805,612

All loans were granted to customers in the Syrian Arab Republic and secured by real estates and personal guarantees.

18. Available for Sale Investments

Available for sale investments represent 5% equity shares in the Syrian Arab Insurance Company sa purchased by the Bank during the year. The investment is stated at cost due to non-existence of an active securities market, unpredictable nature of cash flows and lacks of suitable other methods for arriving to a reliable fair value.

NOTES TO THE FINANCIAL STATEMENTS

51

19. Premises, Equipment and Projects under Construction

The estimated useful lives of the assets for the calculation of depreciation are as follows:

Premises and leasehold improvements 20 to 25 yearsFurniture and equipment 5 to 10 years

Projects under construction are not depreciated until the relevant assets are completed and put into operational use.

Premises & leasehold Furniture Projects under improvements equipment construction TotalIn Syrian Pounds

CostAt 1 January 2006 55,519,140 64,487,094 93,445,772 213,452,006Additions 45,383,459 112,875,994 94,758,767 253,018,220Transfers 146,309,325 - (146,309,325) -

At 31 December 2006 247,211,924 177,363,088 41,895,214 466,470,226

Depreciation: At 1 January 2006 - - - -Provided during the year 8,857,432 21,424,503 - 30,281,935Disposals - - - -

At 31 December 2006 8,857,432 21,424,503 - 30,281,935

Net book value: At 31 December 2006 238,354,492 155,938,585 41,895,214 436,188,291

At 31 December 2005 55,519,140 64,487,094 93,445,772 213,452,006

52

NOTES TO THE FINANCIAL STATEMENTS

20. Intangible Assets

The estimated useful lives of the intangible assets for the calculation of amortisation are as follows:

Computer softwares 5 yearsKey money 70 years

Computer software Key money TotalIn Syrian Pounds

Cost At 1 January 2006 13,803,356 88,914,186 102,717,542Additions 13,418,493 - 13,418,493Disposals - - -

At 31 December 2006 27,221,849 88,914,186 116,136,035

Amortisation: At 1 January 2006 - - -Provided during the year 3,915,485 1,058,502 4,973,987Disposals - - -

At 31 December 2006 3,915,485 1,058,502 4,973,987

Net book value: At 31 December 2006 23,306,364 87,855,684 111,162,048

At 31 December 2005 13,803,356 88,914,186 102,717,542

21. Other Assets

2006 2005In Syrian Pounds

Sundry debtors and prepayments 40,544,160 50,999,954Interest receivable 192,071,630 4,965,130Other 1,080,271 335,780

233,696,061 56,300,864

22. Statutory Blocked Funds

As per section B of article 12 of law number 28 for the year 2001, private sector banks should keep 10% of their capital as a legal blocked fund at the Central Bank of Syria. The fund is interest free rate.

As at 31 December 2006 blocked funds at the Central Bank of Syria were as follows:

NOTES TO THE FINANCIAL STATEMENTS

53

2006 2005In Syrian Pounds

Funds in Syrian Pounds 21,235,700 21,235,700Funds in United States Dollars 218,288,178 234,536,857 239,523,878 255,772,557

23. Due to Banks

2006 2005In Syrian Pounds

Current account (*)Local banks 83,231,391 18,682,756Foreign banks 46,918,014 -

130,149,405 18,682,756

(*) Does not include interest payable which is shown separately within other liabilities (note 26).

24. Margin Accounts

2006 2005In Syrian Pounds

Direct credit facilities 11,836,327 -Indirect credit facilities 1,501,498,253 10,772,544

1,513,334,580 10,772,544

25. Customers’ Deposits

2006 2005In Syrian Pounds

Current accounts 4,387,322,006 999,185,193Time and demand deposits 8,601,776,453 1,138,040,704Saving deposits 461,988,525 47,141,565 13,451,086,984 2,184,367,462

Amounts do not include interest payable which is included in note 26.

54

NOTES TO THE FINANCIAL STATEMENTS

26. Other Liabilities

2006 2005In Syrian Pounds

Unearned revenue 4,022,221 -Interest payable 70,840,329 5,905,308Staff related provisions 8,199,521 3,243,525Accrued expenses 7,777, 11,937,136Income tax withheld 10,562,413 533,037Due to related par ties (note 32) - 190,597,168Current income tax payable (note 13) 36,350,459 133,448Accounts payable and sundry creditors 6,758,362 7,482,633

144,510,931 219,832,255

27. Share Capital

The authorised, issued and fully paid share capital as at 31 December 2006 comprised 2,500,000 shares of SYP 1,000 par value each.

The authorised, issued and fully paid share capital is divided into two categories:

1- Category A: These are the stocks that shall be owned by Syrian individuals or Syrian companies and are paid in Syrian Pounds, except for non-resident Syrian individuals who shall pay the value of shares in foreign currency at neighbouring countries free rate of exchange. These shares amount to 51% of the Bank’s share capital.

2- Category B: These are the stocks that can be owned by foreign individuals or companies based on the parliament decision, the value of these shares shall be paid in foreign currencies. These shares amount to 49% of the Bank’s share capital.

Bank Audi sal shares are from category B and represent 47% of the Bank’s share capital.

28. Reserves

- Statutory Reserve The statutory reserve was computed as 10% of the profit for the year after unrealised gain or loss on difference of exchange. The

Bank may resolve to discontinue such annual transfer when the statutory reserve becomes equal to 50% of the Bank’s capital. This reserve is not available for distribution to the shareholders.

- Special Reserve Special reserve was computed as 10% of profit for the year after unrealised gain or loss on difference of exchange. The Bank may

resolve to discontinue such annual transfer when the special reserve becomes equal to 100% of the Bank’s capital. This reserve is not available for distribution to the shareholders.

NOTES TO THE FINANCIAL STATEMENTS

55

Statutory and special reserves for the year were computed as follows:

2006 2005In Syrian Pounds

Profit before tax 36,803,332 48,207,807Add (subtract) unrealised foreign exchange loss (gain) 107,540,000 (47,674,012)Less current income tax expense (36,350,459) (133,448) 107,992,873 400,347 Statutory reserve 10% 10,799,287 40,035 Special reserve 10% 10,799,287 40,035