bank and · the world bank for official use only report no. 33538-co international bank for...

TRANSCRIPT

Document o f The World Bank

FOR OFFICIAL USE ONLY

Report No. 33538-CO

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED FIRST PROGRAMMATIC BUSINESS PRODUCTIVITY AND EFFICIENCY LOAN

IN THE AMOUNT OF US$250 MILLION

TO THE

REPUBLIC OF COLOMBIA

September 27,2005

Colombia-Mexico Country Management Unit Finance, Private Sector and Infrastructure Department Latin America and Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance of their off icial duties. I t s contents may not otherwise be disclosed without W o r l d Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

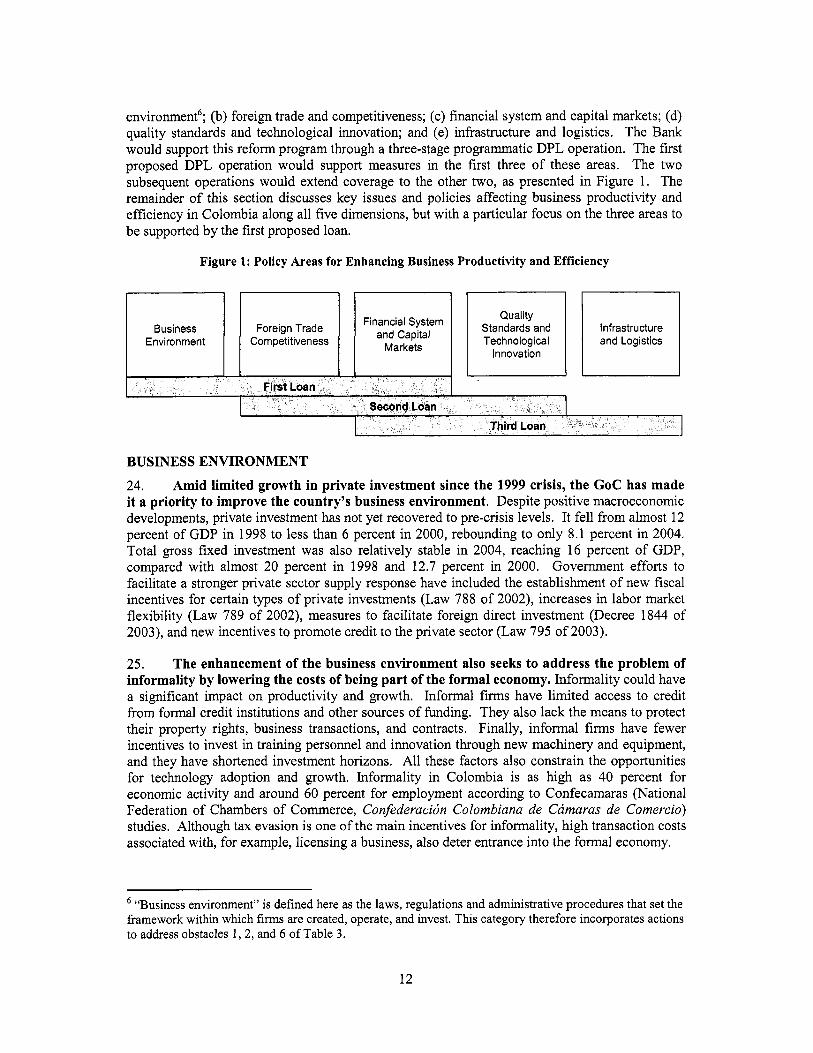

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

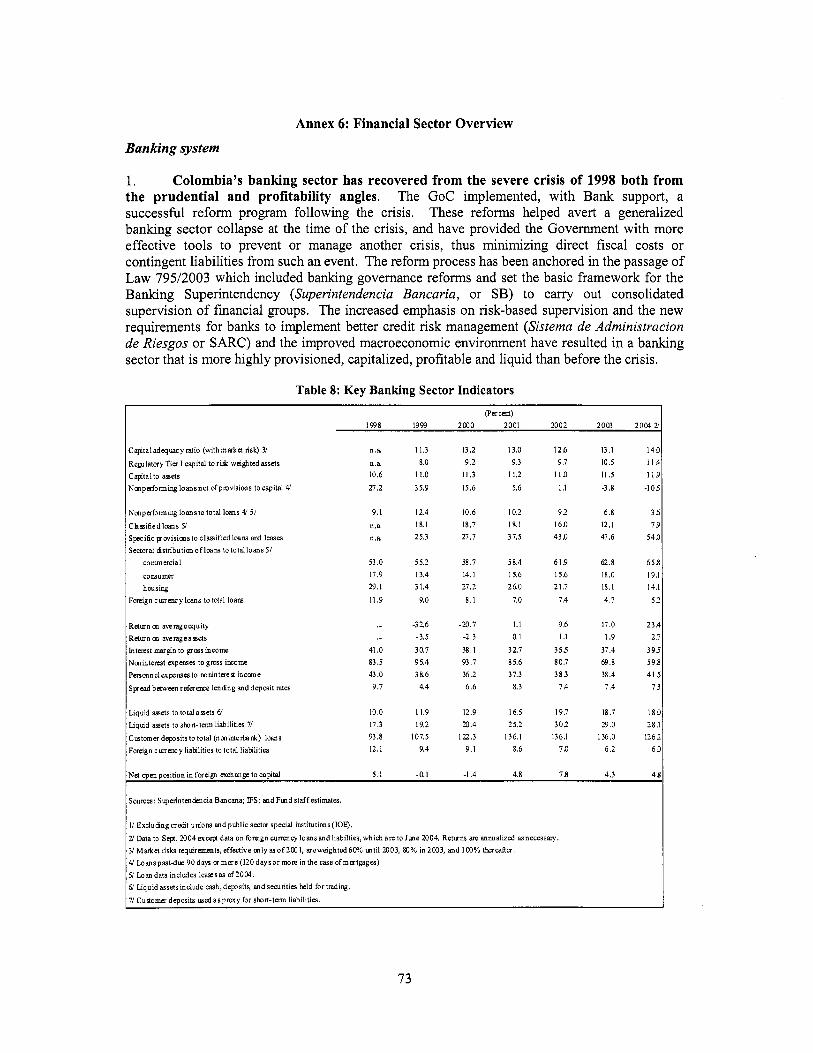

Pub

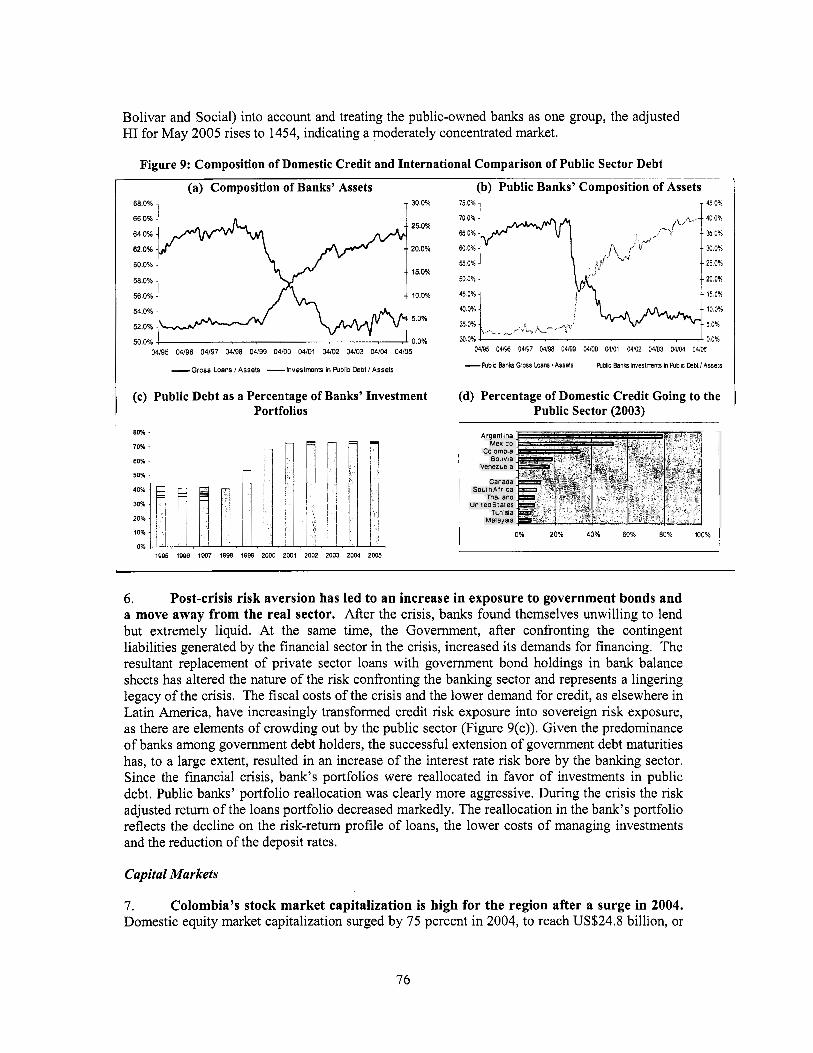

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

COLOMBIA - GOVERNMENT FISCAL YEAR

AAA A I

AMUCFT

BdR CAE

CAF

CAS CFAA

CHMC Confecamams

CONFIS

CONPES

DIAN

DNP

DPL FDI FIAL

FSAL FSAP FRL FTA GDP GNI GoC

January 1-December 3 1

CURRENCY EOUIVALENTS (as o f 20 September 2005) Currency Unit = Peso

2,295 Pesos = US$1

WEIGHTS AND MEASURES Metric System

SELECTED ABBREVIATIONS AND ACRONYMS

Analytical Advisory Activities Agenda Intema para la Productividad y Competitividad de Colombia. (hemal Agenda for the Productivity and Competitiveness of Colombia) Anti Money LaunderingiCombating the Financing of Terrorism Banco de la Republica (Central Bank) Centro de Atencidn Empresarial (Centers for Enterprise Assistance) Corporacidn Andina de Foment0 (Andean Development Corporation) Country Assistance Strategy Country Financial Accountability Assessment Colombia Home Mortgage Corporation Confederacidn Colombiana de Camaras de Comercio (Colombian Confederation of Chambers of Commerce) Consejo Superior de Politica Fiscal (Senior Council on Fiscal Policy) Consejo Nacional de Politica Econbmica y Social (National Council on Economic and Social Policy) Direccion de Impuestos y Aduanas Nacionales (Tax and Customs Directorate) Departamento Nacional de Planeacidn (National Planning Department) Development Policy LoadLending Foreign Direct Investment Programmatic Fiscal and Institutional Adjustment Loan Financial Sector Adjustment Loan Financial Sector Assessment Program Fiscal Responsibility Law Free Trade Agreement (US-Andean) Gross Domestic Product Gross National Income Government of Colombia

IBRD

IADB IFC I S 0 IMF MCIT

MHCP

MSME MTEF NGO OECD

PLaRSSAL

PRAP

RED1 REIF SARC

SB

SENA

SIIF

ss sv

TAL TES UAIF

VIS WEF

lntemational Bank for Reconstruction and Development Inter- American Development Bank Intemational Finance Corporation International Organization for Standardization Intemational Monetary Fund Ministerio de Comercio, Industria y Turismo (Ministry of Trade, Industry and Tourism) Ministerio de Hacienda y Credit0 Publico (Ministry of Finance and Public Credit) Micro, Small and Medium Enterprise Medium Term Expenditure Framework Non-Govemmental Organization Organization for Economic Co-operation and Development Programmatic Labor Reform and Social Sector Adjustment Loan Programa de Renovacidn de la Administracidn Publica (Public Administration Renewal Program) Recent Economic Developments in Infrastructure Real Estate Investment Fund Sistema de Administracidn de Riesgos Crediticios (Credit Risk Management System) Superintendencia Bancaria (Banking Superintendency) Servicio Nacional de Aprendizaje (National Training Service) Sistema Integrado de Informacibn Financiera (Integrated Financial Information System) Superintendencia de Sociedades (Companies Superintendency) Superintendencia de Valores (Securities Superintendency) Technical Assistance Loan Titulos de Tesoreria (Treasury Securities) Unidad de Infomacibn y Analisis Financier0 (Financial Information and Analysis Unit) Vivienda de Interts Social (low-income housing) World Economic Forum

Vice President: Pamela Cox Country Director: Isabel M. Guerrero Director, LCSFP: Makhtar Diop

Sector Leader, LCSFP: Anna Wellenstein Sector Manager, LCSFF: Susan Goldmark

Task Team Leader: Juan Carlos Mendozmar t i n Naranjo Landerer

FOR OFFICIAL USE ONLY COLOMBIA: FIRST PROGRAMMATIC

BUSINESS PRODUCTIVITY AND EFFICIENCY LOAN TABLE OF CONTENTS

I . INTRODUCTION ..................................................................................................................................... 5

I1 . THE COUNTRY CONTEXT 6 ................................................................................................................. RECENT ECONOMIC DEVELOPMENTS .............................................................................................. 6 MACROECONOMIC OUTLOOK AND CHALLENGES ........................................................................ 8

I11 . THE OVERALL GOVERNMENT PROGRAM ................................................................................. 9 I V . KEY ISSUES AFFECTING BUSINESS PRODUCTIVITY AND EFFICIENCY ........................ -10

BUSINESS ENVIRONMENT ..................................................................................................... 12 FOREIGN TRADE AND COMPETITIVENESS .................................................................................... 16 FINANCIAL SYSTEM AND CAPITAL MARKETS ............................................................................ 17 QUALITY STANDARDS AND TECHNOLOGICAL INNOVATION ................................ INFRASTRUCTURE AND LOGISTICS ..............................................................................

V . BANK SUPPORT TO THE GOVERNMENT'S STRATEGY .......................................................... 34

LINK TO THE CAS ................................................................................................................................. 34 COLLABORATION WITH THE IMF AND OTHER DONORS AND LENDERS ................................ 34 RELATIONSHIP TO OTHER BANK OPERATIONS ........................................................................... 35 LESSONS LEARNED ......................................................................................... . 37 ANALYTICAL UNDERPINNINGS ....................................................................................................... 38

V I . THE PROPOSED PROGRAMMATIC DEVELOPMENT POLICY LOAN ................................. 39

OPERATION DESCRIPTION ................................................................................................................. 39 LOAN AMOUNT .............................................................. ............................ ................. 41 POLICY AREAS ............................................................... 41

VI1 . OPERATION IMPLEMENTATION ................................................................................................ 43

SOCIAL ASPECTS AND POVERTY IMPACT ..................................................................................... 43 SUPERVISION ........................................................................................................................................ 44 FIDUCIARY ASPECTS .................................................. ............................................................ 44 DISBURSEMENT AND AUDITING ...................................................................................................... 46 ENVIRONMENT ..................................................................................................................................... 47 R I S K S ....................................................................................................................................................... 47

ANNEXES Annex 1: Colombia At A Glance ................................................................................................................ 49 Annex 2: Le t te r Of Development Policy .................................................................................................... 51 Annex 3: Debt Sustainability Analysis ...................................................................................................... 63 Annex 4: Matrix Of Policy Actions And Expected Outcomes ................................................................. 67 Annex 5: Fund relations note ..................................................................................................................... 69 Annex 6: Financial Sector Overview ......................................................................................................... 73 Annex 7: Quality Standards And Technical Innovation .......................................................................... 78 Annex 8: Colombia's Operations Portfolio (Ibrd And Grants) ............................................................... 84 Annex 9: Statement Of IFC's Held And Disbursed Portfolio ................................................................. -85

........................................................

ACKNOWLEDGEMENTS T h e World Bank Group greatly appreciates the close collaboration o f the Government o f Colombia in the preparation of this Development Policy Loan . This loan has been prepared by a team composed of: Juan Carlos Mendoza and Martin Naranjo Landerer (Task Managers); Constantinos Stephanou (LCSFF); Pablo Fajnzylber. Leonid Kotyukin (LCSFR); Mary Morrison (LCSFP); Alessandra Campanaro (OPD); Bess Michael. Pierre-Laurent Chatain. Marilyn Goncalves (FSEFI); Mariluz Cortes (consultant) . The team benefited from the comments from other Bank staf f including peer reviewers: August0 de la Tome (LCRCE). Patrick Honohan (OPD). and Simon Bell (SASFP) as well as Todd Crawford (LCOQE) and Harold Bedoya (OPCS) . Additional assistance was provided by Helena Issa .

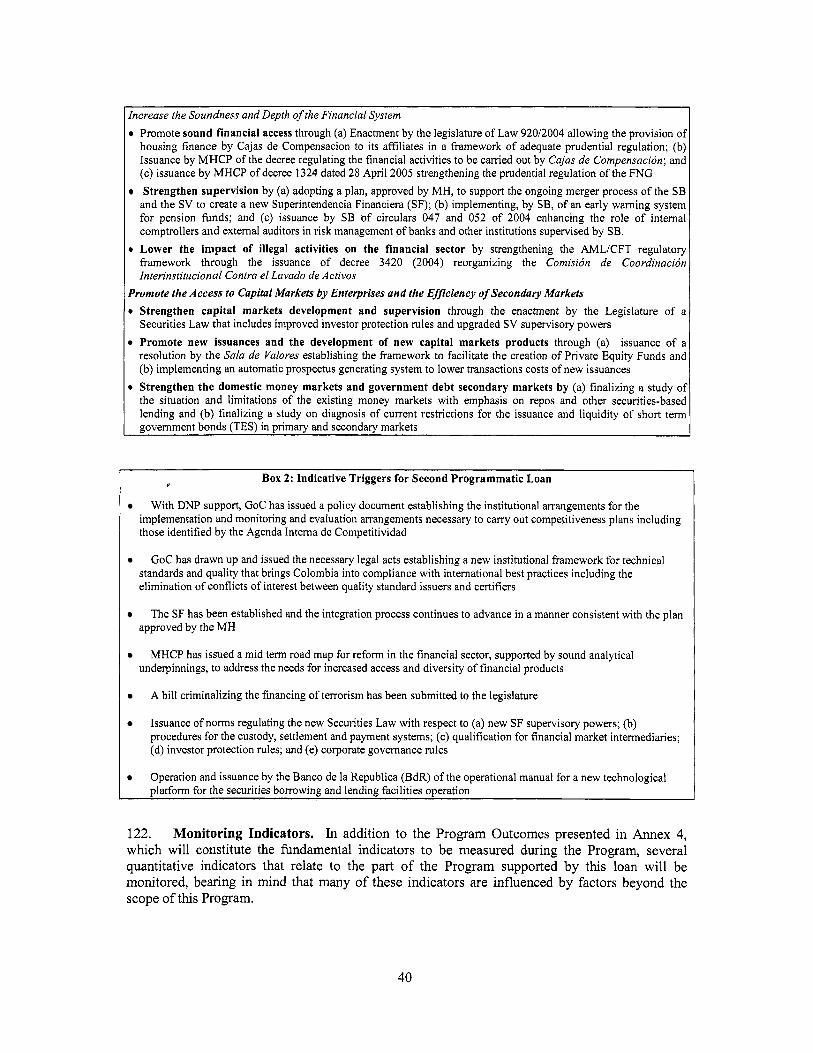

This document has a restr icted distribution and may be used by recipients only in the performance of their official duties . I t s contents may not be otherwise disclosed without World Bank authorization .

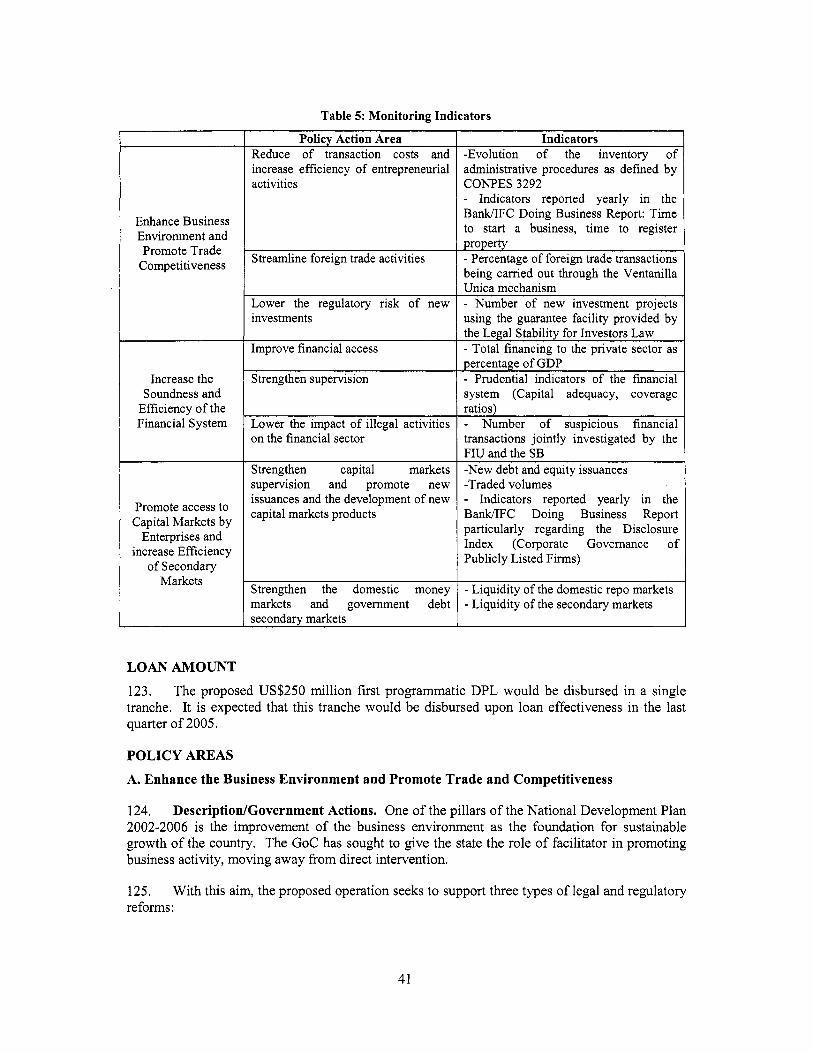

LOAN AND PROGRAM SUMMARY COLOMBIA FIRST PROGRAMMATIC BUSINESS PRODUCTIVITY AND

EFFICIENCY LOAN

Borrower

Implementing Agencies

Amount

Terms

Commitment Fee Front-End Fee Tranching

Objective

Description

Benefits

Risks

Project ID No.

Republic o f Colombia

Ministerio de Hacienda y Crkdito Phblico, Departamento Nacional de Planeaci6n

US$250 mil l ion

Commitment-linked Fixed-Spread Loan (FSL), U S dollar denominated, payable in 17.5 years, including a 5.5-year grace period. Level repayments o f principal at the standard variable interest rate for U S dollar FSLs 0.85 percent on undisbursed loan balances for first four years and 0.75 percent on undisbursed loan balances thereafter 1 percent o f the loan amount paid by the Borrower upfront Single tranche for the full amount o f the loan

This operation will support the Colombian Government’s efforts to promote sustainable growth through the enhancement o f the business environment and the consolidation o f the financial sector and capital markets as pillars o f economic growth. The proposed loan i s the first phase o f a programmatic development policy operation in three phases, which would be executed over a period o f three years. The first proposed operation would support policy and institutional reforms in three areas: 0 enhancement o f the business environment to promote investment and trade and

improve competitiveness o f the productive sectors o f the economy increase the soundness and depth o f the financial system expansion o f access to capital markets by businesses and improvement o f efficiency o f financial secondary markets

The proposed loan would support sustainable growth and alleviation o f poverty by: facilitating the creation and operation o f businesses, leading to increased productivity and employment levels; and

0 fostering the sustainable growth o f a financial system and capital markets that address ;he needs o f inditiduals and the produciive sector.

The proposed operation supports an institutional development effort widely perceived as n e c e k y by most politicai gctors, and that the Goverken t i s already actkely implementing. Therefore, there i s little risk that the actions already taken could be reversed and that the indicative triggers for the preparation o f the next operation are not reached within the twelve months following the effectiveness o f this first loan. However, there are some risks associated with the effective implementation o f the institutional and regulatory reforms supported by the proposed Development Policy Loan (DPL). The most relevant risks are the following: 0 mechanisms for inter-institutional collaboration and coordination in support o f

entrepreneurial activities may be hampered by inter-agency rivalries 0 measures to increase access to financial services may take a long time to produce

results 0 political uncertainty and any deterioration in the internal security situation related

to the 2006 elections may delay the implementation o f important institutional and regulatory reforms current levels o f public debt may pose a threat to overall macroeconomic stability

PO94301

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT PROGRAM DOCUMENT ON A PROPOSED FIRST PROGRAMMATIC BUSINESS

PRODUCTIVITY AND EFFICIENCY LOAN TO THE REPUBLIC OF COLOMBIA

I. INTRODUCTION

1. The Government o f Colombia (GoC) has taken great strides in consolidating the economic recovery since 2002 and has made improving the business environment and strengthening the financial sector central to the country’s pursuit o f faster economic growth. The 2005 “Doing Business’’ report by the World Bank and the International Finance Corporation (IFC) ranked Colombia as the number two reformer in the area o f business environment in a sample o f 145 countries. Similarly, the Financial Sector Assessment Program (FSAP) Update, carried out in late 2004, highlighted the recovery o f the financial sector since the crisis o f the late 1990s due to a broad range o f financial sector legal and regulatory reforms. The GoC has more recently embarked on a series o f policy and institutional reforms to promote greater productivity and efficiency among enterprises. A t the core o f these reforms i s a concerted effort to further improve the business environment and continue strengthening the financial sector, to enable it to fund the investment needed for productivity and efficiency gains at the firm level.

2. The Bank’s support for the GoC’s program to promote greater business productivity and efficiency would consist o f a three-phased programmatic development policy lending (DPL) operation. The entire program would be carried out over a period o f three years and would be complemented by recently completed, as well as concurrent, Analytical and Advisory Activities (AAA) carried out at the request o f the GoC. The f i rs t operation-the US$250 mil l ion proposed here-would support greater business productivity and efficiency through reforms in three areas: (a) enhancing the business environment through improvements in the regulatory framework and a reduction in the administrative burden on enterprises; (b) increasing the soundness and depth o f the financial system; and (c) promoting access to capital markets by f i r m s and improving the efficiency o f secondary markets. The second and third phases o f the programmatic operation would continue to support the process o f reforms initiated under this f irst operation and would consider i t s extension to other areas. Key triggers for the preparation o f the second operation include: (a) pursuit o f greater international competitiveness for Colombian businesses through the establishment o f institutional arrangements for implementing, monitoring and evaluating competitiveness plans, as well as the implementation o f a new legal framework for quality standards and technology; (b) consolidation and extension o f the financial sector reform process, to diversify the range o f financial products and foster greater access to financial services; and (c) completion o f the regulatory framework to improve access to the capital markets by the real sector.

3. Agreement on the reforms supported by the proposed operation has been reached through a broad process o f consultation that the GoC has carried out, partly under the umbrella o f negotiations for the Andean-U.S. Free Trade Agreement (FTA). The reforms thus have the backing o f key stakeholders, which reduces the r isks inherent in a program that w i l l span two presidential administrations.

5

11. THE COUNTRY CONTEXT

4. Wi th 45 mil l ion inhabitants, Colombia i s the third most populous country in Latin America, after Brazil and Mexico. The country’s economy expanded steadily for decades until 1999, when a combination o f domestic and international conditions triggered a severe financial and economic crisis. A difficult security situation over the last four decades has also held back economic growth and living standards. In 2004, around 52 percent o f the population was below the national poverty line. Annual Gross National Income (GNI) per capita, at US$1,920, was only 53 percent o f the average for Latin American and the Caribbean, classifying Colombia as a lower middle-income country.

5. Despite recent diversification, Colombia’s economy s t i l l depends on primary exports, and i s vulnerable to swings in the prices o f these. The country’s traditional exports-crude oil, coal, coffee and ferronickel-generated 46 percent o f total export revenues in 2004, while other agricultural produce and minerals (particularly cut flowers, bananas and gold) contributed a hrther 15 percent. O i l alone accounted for 25 percent o f total export revenues, and a significant part o f government revenues’. However, total crude output i s dropping as discovered reserves are depleted. Production i s now roughly 525,000 barrels a day, down from a peak o f 830,000 in 1999. Security improvements and enhanced contractual terms for investors have attracted significant private sector exploration investment in the last five years, but this has so far failed to produce the major discoveries needed to sustain o i l exports. For industrial exports, key sectors include textiles, food production, chemicals, plastics and vehicle assembly.

RECENT ECONOMIC DEVELOPMENTS

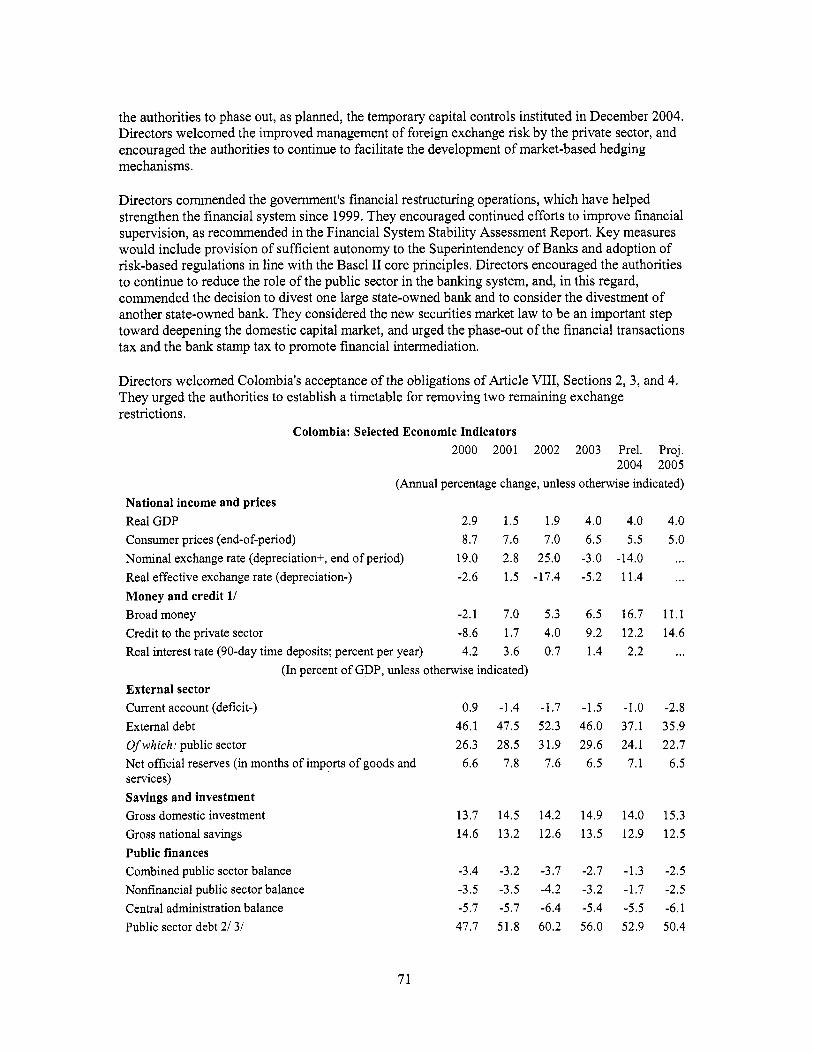

6. Colombia’s economy has recovered since the start o f the current Country Assistance Strategy (CAS) period (2002-2006)*. The near stagnation o f the economy during the four years prior to the CAS has since given way to a sustained economic recovery and a strengthening o f consumer confidence. The turnaround i s partly due to the much improved global economic environment: world growth has accelerated, the cost o f international credit has fallen, and the prices o f Colombia’s primary exports have risen. Domestic factors, particularly the improved security situation and stable macroeconomic polices, have also driven the country’s recovery. Improving conditions are reflected by an almost 1 percentage point increase in private investment as a share o f Gross Domestic Product (GDP) since 2002, and real economic growth that accelerated from 1.6 percent in 2002 to nearly 4 percent in 2003 and 2004. Colombia’s unemployment rate dropped from over 17 percent in 2002 to less than 12 percent in November 2004 (the lowest rate in the last four years), and has remained at roughly that level since. Inflation has stayed under control, falling from 7.0 percent in 2002 to 5.5 percent in 2004. The annualized inflation rate during the first semester o f 2005 was 4.0 percent. Table 1 compares Colombia’s recent economic performance with that o f the other five largest countries in the region and Table 2 summarizes key economic indicators for the country itself. Annex 1 provides further economic and social data.

State o i l company Empresa Colombiana de Petroleos transferred 6.4 tril l ion pesos to the national

‘The CAS Update, Report 32999-C0, scheduled for Board discussion on Sept. 29,2005, would extend this period through the end of2007.

overnment in 2004.

6

Table 1: Comparative Macroeconomic Indicators

Source: World Bank A t a Glance indicators

Table 2: K e y Economic Indicators for Colombia

1 Private sector 7.0 I 8.1 I 9.3 9.6 Source: Ministerio de Hacienda, CONFIS, BdR.

7. The rapid expansion o f public spending over the past decade, (from 25 percent o f GDP in 1990 to over a third today), combined with growing pension and other liabilities, has led to significant and persistent structural deficits. The combination o f domestic economic growth, improved international conditions, peso appreciation (which reduces the cost o f servicing foreign currency- denominated debt), and revenue-enhancing policy reforms has improved the fiscal accounts. The deficit decreased from 3.7 percent o f GDP in 2002 to 2.7 percent in 2003 and to 1.2 percent in 2004, well inside the 2.5 percent target o f the country’s current International Monetary Fund (IMF) stand-by agreement. Policy reforms have concentrated on the revenue side. In 2002, Congress approved Law 788, supported by the Bank’s Fiscal and Institutional Adjustment Loan (FIAL) Program. This law sought to increase revenues and reduce tax distortions through the elimination o f several targeted exemptions. Overall, the reform brought additional revenues o f 0.7 percent o f GDP in 2003 and about 1.1 percent in 2004.

The public sector deficit has improved, but fiscal concerns persist.

8. Budget and legal rigidities that resist spending cuts have slowed the progress of policy reforms on the expenditure side. These rigidities affect two main areas, in which expenditures have continued to grow: transfers to sub-national govemments and the pensions system. In 2002, the enactment of Law 715 limited the growth rate o f transfers to sub-national govemments, mandated under the Constitution, but this measure i s set to expire in 20073, and further reform i s needed if the system i s to become sustainable. Transfers to the main state-run pension system w i l l continue to expand over the next decade, as payouts greatly exceed new contributions. Fundamental reforms, including a rebalancing o f contribution and payment levels, are needed to make the system viable, to reduce government support required and enable the GoC

From 2008, the growth rate o f transfers w i l l be calculated based on the weighted average o f the previous four years’ GDP.

7

to fulfill i t s aim o f providing a safety net to the poorest elderly citizens. A constitutional reform, enacted in June 2005, has made considerable progress in this area, by eliminating a series o f special regimes for certain state employees and imposing ceilings on benefits in the public-sector pension system. The reform reduced the net present value o f pension liabilities by 19 percentage points o f GDP (from 162 percent o f GDP to about 143 percent). The original bill aimed for almost twice this, but the reform was watered down in Congress.

MACROECONOMIC OUTLOOK AND CHALLENGES

9. I n the absence of major external shocks, the economy i s expected to continue growing at least at current rates in the medium term. Since prospects for significantly improving the factors supporting domestic demand (employment, internal peace, investment and credit) are modest, it i s likely that GDP growth w i l l remain at around 4.0 percent through 2007. Imports are expected to grow by 5.4 percent in 2005, and, combined with lower exports, are expected to moderately increase the current account deficit to 2.7 percent o f GDP in 2005. Wh i le the same trend i s expected to continue in 2006, with a moderate appreciation o f the currency contributing to a current account deficit o f 2.9 percent o f GDP, this figure i s expected to fall slightly, to 2.6 percent o f GDP by 2007. Foreign direct investment (FDI) flows are expected to increase wi th the likely signing o f the FTA as well as with the enactment o f some o f the business environment reforms supported by this DPL series.

10. The level of public debt remains high but sustainable under most scenarios. Colombia’s present level o f public debt, at about 46.6 percent o f GDP remains relatively high, But i t appears manageable in the near term even when considering possible adverse economic shocks. The GoC’s target i s to reduce the level o f debt to 38 percent o f GDP by 2015. Annex 3 analyzes the impact that several economic shocks could have on the overall debt level and the primary surplus (i-e., the fiscal surplus net o f debt servicing) that would be necessary in each scenario to meet the 2015 target. This analysis concludes that even facing several combined shocks, if the primary surplus were to remain at the historical level o f 2.1 percent o f GDP, total debt levels could be kept at manageable levels.

11. Elections and export markets will generate uncertainty in the coming months. Congressional elections in March 2006 and presidential ones in May wil l l ikely slow the progress o f some structural reforms and create uncertainty among investors and consumers, particularly if illegal groups attempt to undermine the process through violence. Congress in December approved a measure that would allow President Uribe to run for a second consecutive term, but i t i s not clear if the country’s Constitutional Court w i l l approve the measure. Abroad, o i l prices w i l l continue to have major effects on the economy, through their impact on export and fiscal revenues and as a key determinant o f growth in Venezuela, the country’s main market after the U S for non-traditional exports. And the implementation o f the FTA, which could boost trade between the Andean countries and the US, s t i l l depends on both a successful outcome for negotiations and approval by the US Congress.

12. The Colombian peso has appreciated strongly in the last two years, and further strengthening could reduce the international competitiveness of local products. Driven partly by strong export revenues from higher prices for commodity exports, especially oil, Colombia’s real exchange rate has strengthened by nearly 30 percent since early 2003. However, manufactured and other non-traditional exports have continued to perform strongly so far, with the value o f 2005 first-quarter exports up 29 percent on year, and the current account deficit has remained stable. This suggests that a combination o f productivity gains and sustained

8

international demand has allowed the export sector to cushion the negative impact o f such appreciation.

111. THE OVERALL GOVERNMENT PROGRAM

13. The overall Government program i s based on the National Development Plan 2002- 2006 (Huciu un Bstudo Comuniturio). This plan was formally adopted through Law 812 o f 2003. I t has four overarching objectives:

Address the security needs of the population. The difficult domestic security situation exacerbated the deterioration o f social indicators triggered by the economic recession o f 1999, which reversed decades o f progress particularly in poverty reduction. Actions to reduce violence are essential for promoting economic growth and poverty alleviation.

Support sustainable growth and employment-generating activities in a context of macroeconomic stability, debt sustainability and good access to international markets. Efforts here concentrate on improving overall competitiveness through reducing obstacles to entrepreneurial activity, promoting bilateral and regional free trade agreements, fostering technological innovation, and improving infrastructure.

Alleviate income inequalities through the promotion of economic growth, efJicient social expenditures and better safety nets. This aspect o f the plan seeks to support improvements in human capital, increase the coverage o f welfare mechanisms, upgrade urban areas and promote growth in production through an integrated strategy to support Micro, Small and Medium Enterprises (MSME) development.

Increase the transparency and efJiciency of the state through profound cross- sectoral reforms and greater, more effective decentralization. This component wil l continue the process o f modernization o f the state, rationalizing its size and increasing the efficiency o f processes and procedures including those associated with the public (i.e., bureaucratic procedures or “red tape”).

14. The GoC has requested the preparation of this operation, to support a program that will advance toward the second and third objectives of the National Development Plan. The proposed Business Productivity and Efficiency Programmatic DPL would support the GoC in the implementation o f elements o f this Plan by fostering productivity, investment and growth in the private sector, enabling it to maximize the benefits o f increased international integration. More specifically, the reforms supported by th is DPL seek to improve the business environment, enhance international competitiveness and increase the soundness and depth o f the financial sector.

15. This program i s part o f a broader set o f policies seeking to enhance the country’s competitiveness. As the recent Colombia Country Economic Memorandum4 (CEM) highlights, competitiveness i s a broad term used to refer to the overall economic performance o f the country,

Colombia Economic Memorandum: The Foundations for Competitiveness, Report 32035C0, June 17 2005

9

particularly i t s level o f productivity, its ability to export its goods and services, and the extent to which i t can provide a good standard o f living for i t s citizens. Competitiveness therefore encompasses: a stable macroeconomic environment; the educational level and flexibility o f the labor force; the ease o f transport from ports and on roads; the efficiency o f the legal and judicial system in enforcing contracts and facilitating business activity; the quality and transparency o f corporate governance; the stability o f political institutions; the structure o f the tax system; and the conduciveness of the regulatory environment to market competition and management o f systemic risks.

16. Strong and sustainable economic growth requires an enabling environment of stability as well as targeted microeconomic policy reforms to increase private investment, reduce transaction costs and enhance competitiveness. Since 2002, Colombia’s strengthening macroeconomic and security situation has improved the business environment, with revived aggregate demand and greater confidence among consumers and producers. The GoC i s also pursuing a broad program o f microeconomic reforms to facilitate and promote business activity, in particular to h l l y exploit the export opportunities offered by the prospective FTA. This program i s supported by the policy actions to be covered by this DPL series, as discussed below.

IV. KEY ISSUES AFFECTING BUSINESS PRODUCTIVITY AND EFFICIENCY

17. This section considers the main problems and challenges for doing businesses in Colombia, and government initiatives to address these. Within this policy context, the DPL program puts emphasis on actions and outcomes that are most important for the achievement o f the Government’s objectives o f stimulating broad-based economic growth and maximizing the benefits o f increased international integration. The focus o f this loan i s also determined by the GoC’s specific priorities and achievements within i t s reform agenda, as well as the coverage o f complementary programs from the Bank and other international institutions.

Introduction.

18. Multiple surveys and analytical works have identified key constraints to business productivity and efficiency in Colombia, most of which the GoC i s addressing with direct or indirect Bank support. Table 3 lists the main obstacles to doing business identified by survey respondents for the World Economic Forum (WEF). These results are consistent with those o f other surveys and analytical studies conducted in Colombia, including the recently completed Colombia Country Economic Memorandum (CEM) and monthly surveys by Colombia’s National Association o f Entrepreneurs (Asociacibn Nacional de Empresarios, ANDI).

Table 3: Obstacles 1

so2

Doing Business in Colombia, in Order of

1. Corruption 2. Policy instability 3. High tax rates 4. Insufficient access to financing 5. Inadequate infrastructure 6. Inefficient bureaucracy 7. Tax regulation instability 8. Crime and theft 9. Restrictive labor regulations 10. Inadequately educated workforce

:e: WEF Global Competitiveness Report (2

Perceived Magnitude

104)

10

19. The presidential program to fight corruption i s moving in the right direction: focusing on the local level. Corruption, identified as the greatest obstacle in Table 3, increases costs and reduces efficiency for individuals and f i rms. A presidential program aims to tackle corruption through increasing the transparency o f government activities. The voluntary signing o f “transparency pacts” between municipal and regional authorities and citizens, has created a mechanism for local communities to gain information on the decisions and actions o f government bodies, and to call them to account. Furthermore, the reduction o f bureaucratic procedures (red tape) supported by this loan l i m i t s the scope for corruption by simplifying and accelerating such processes, allowing more o f them to be completed electronically and without personal contact with officials, and prohibiting some o f the charges associated with such procedures.

20. Policy instability i s particularly a n issue with respect to the tax regime. In the last three decades, there have been 14 reforms to the tax regime in Colombia. Overall, the reforms have contributed to increasing tax revenues from 11 percent o f GDP in 1970 to about 21 percent in 2003, and have improved fiscal accounts. But such frequent tax changes create instability, uncertainty and extra costs for businesses. Uncertainty over the outcome o f other reforms, such as to pension systems and budget processes, may also cause businesses to delay investment plans. The current system disproportionately burdens businesses, with a basic corporate income tax rate o f 35 percent. The Bank has supported, through the FIAL program, reforms that aim to broaden the tax base and reduce distortions in the current tax code.

21, The persistence of labor market rigidities hinders business efficiency and productivity. The approval of Law 789 in December 2002 reduced payroll taxes, firing costs, overtime pay and the cost o f hiring apprentice workers, as well as extending the working day. I t also increased the flexibility o f the training system by allowing for greater use o f private providers o f training services. However, in the 2005 Doing Business report, Colombia’s overall index o f labor market rigidity i s at 51, compared to 44 for the average Latin American country and 34 for the Organization for Economic Co-operation and Development (OECD). Indeed, while firing restrictions are now less stringent on average than in the rest o f the region, hiring new workers remains more difficult and costly in Colombia, and continuing l i m i t s on overtime employment make i t difficult to increase output using current staff. Altogether, these factors raise labor costs for f i r m s and hinder efficiency by curbing their ability to adjust production levels to changes in consumer demand. The Bank recently completed analytical work in this area’ which provides the GoC with a basic framework upon which to build further labor reforms.

22. Given the time constraints and political economy challenges associated with fiscal and labor issues, additional reforms in fiscal and labor areas wi l l probably have to be addressed by the next administration. The analytical work prepared by the Bank as part o f the FIAL Program, the CEM and the labor study have contributed to create the consensus among most political stakeholders for the need for additional reforms in these areas. However, implementation o f additional structural reforms i s more l ikely to be successful if carried out by the government starting in August 2006 during the period o f increased political momentum that accompanies a new administration. The Bank, in the policy notes it w i l l prepare for the incoming administration, w i l l highlight the need for such reforms.

23. The GoC has designed a Program that addresses five key policy areas to stimulate business productivity and efficiency. The GoC has designed a Program to foster business productivity and efficiency based primarily on policy reforms in five

Labor Market Adjustment, Reform, and Productivity in Colombia: What Report 32068-C0, June 2005

areas: (a) overall business

are the Factors that Matter?

11

environment6; (b) foreign trade and competitiveness; (c) financial system and capital markets; (d) quality standards and technological innovation; and (e) infrastructure and logistics. The Bank would support this reform program through a three-stage programmatic D P L operation. The f irst proposed DPL operation would support measures in the first three o f these areas. The two subsequent operations would extend coverage to the other two, as presented in Figure 1. The remainder o f this section discusses key issues and policies affecting business productivity and efficiency in Colombia along al l five dimensions, but with a particular focus on the three areas to be supported by the f i rs t proposed loan.

Figure 1: Policy Areas for Enhancing Business Productivity and Efficiency

BUSINESS ENVIRONMENT

24. Amid limited growth in private investment since the 1999 crisis, the GoC has made it a priority to improve the country’s business environment. Despite positive macroeconomic developments, private investment has not yet recovered to pre-crisis levels. I t f e l l from almost 12 percent o f GDP in 1998 to less than 6 percent in 2000, rebounding to only 8.1 percent in 2004. Total gross fixed investment was also relatively stable in 2004, reaching 16 percent o f GDP, compared with almost 20 percent in 1998 and 12.7 percent in 2000. Government efforts to facilitate a stronger private sector supply response have included the establishment o f new fiscal incentives for certain types o f private investments (Law 788 o f 2002), increases in labor market flexibility (Law 789 o f 2002), measures to facilitate foreign direct investment (Decree 1844 o f 2003), and new incentives to promote credit to the private sector (Law 795 o f 2003).

25. The enhancement of the business environment also seeks to address the problem of informality by lowering the costs of being part of the formal economy. Informality could have a significant impact on productivity and growth. Informal f i r m s have limited access to credit from formal credit institutions and other sources o f funding. They also lack the means to protect their property rights, business transactions, and contracts. Finally, informal f i r m s have fewer incentives to invest in training personnel and innovation through new machinery and equipment, and they have shortened investment horizons. All these factors also constrain the opportunities for technology adoption and growth. Informality in Colombia i s as high as 40 percent for economic activity and around 60 percent for employment according to Confecamaras (National Federation o f Chambers o f Commerce, Confederacidn Colombiana de Camaras de Comercio) studies. Although tax evasion i s one o f the main incentives for informality, high transaction costs associated with, for example, licensing a business, also deter entrance into the formal economy.

“Business environment” is defined here as the laws, regulations and administrative procedures that set the framework within which f i rms are created, operate, and invest. This category therefore incorporates actions to address obstacles 1,2, and 6 o f Table 3.

12

26. M a j o r improvements in Colombia’s business environment have been highlighted in the Doing Business report. The 2005 edition rated Colombia the second-fastest reformer in the world, after Slovakia. This high ranking was due to the country’s significant reforms in the fields of administrative simplification, contract enforcement, and property registration. In addition, Colombia has taken important steps to increase labor market flexibility and stimulate foreign direct investment.

27. The National Development Plan establishes the reduction of bureaucratic administrative procedures or “red tape” as a central element of the GoC’s drive to improve the business environment. Through the Directorate o f Public Administration (Departamento Administrativo de la Funcidn Phblica, DAFP), the Government has compiled an inventory o f bureaucratic procedures (trcimites), and identified those that have a direct effect on business activities: about 1,000 out o f a total o f 2,676 procedures. In policy document No. 3292, o f June 2004, the National Council for Economic and Social Policy (Consejo Nacional de Politica Econdmica y Social, CONPES) formulated a strategy to reduce red tape by means o f inter- institutional coordination, an update o f the legal framework, the rationalization o f existing procedures, and the technological strengthening o f government agencies. By December 2004, about 150 bureaucratic procedures had been simplified and 1 8 eliminated.

28. The July 2005 approval of L a w 962 i s a significant achievement in this area. The law, drafted by the Ministry o f Interior and Justice, created a new framework for the simplification o f government procedures that extended beyond those that could be eliminated through administrative decrees. The so-called Ley Anti-Trcimites eliminated around 80 bureaucratic processes and prevented government agencies both from creating more o f them and from raising funds through charges for such processes. I t also permitted much more documentation to be submitted electronically or by mail, limiting the need for personal appearances, and rescinded the requirement for signatures to be notarized in most bureaucratic procedures.

29. Further progress came with the creation, in collaboration with the private sector, of “one-stop shops” to streamline the process of starting a new business. The GoC’s National Planning Department (Departamento Nacional de Planeacidn, DNP) has supported Confecamaras and local governments in establishing Centers for Enterprise Assistance (Centros de Atencidn Empresarial, CAEs) in six major cities. The design and initial implementation o f the CAE program has been supported through a grant from the Inter-American Development Bank (IADB).7 CAEs collect, process and transfer all the information to the 11 agencies, on average, that are involved in the registration and licensing process for new businesses. (These 11 include national, regional and municipal tax authorities as well as labor, health, and environmental agencies). The Government has enabled registration to be carried out on the presumption o f compliance with these agencies’ requirements, with ex post verification conducted by the respective organizations at their discretion. The CAE expansion program for 2004-2007 seeks to add 5 1 more cities to the six already covered, to further simplify the business registration process, and to expand the array o f entrepreneurial support services offered by CAEs. Table 4 summarizes the program’s results.

~

’ IADB Multilateral Investment Fund Facility TC-99-05-04-7

13

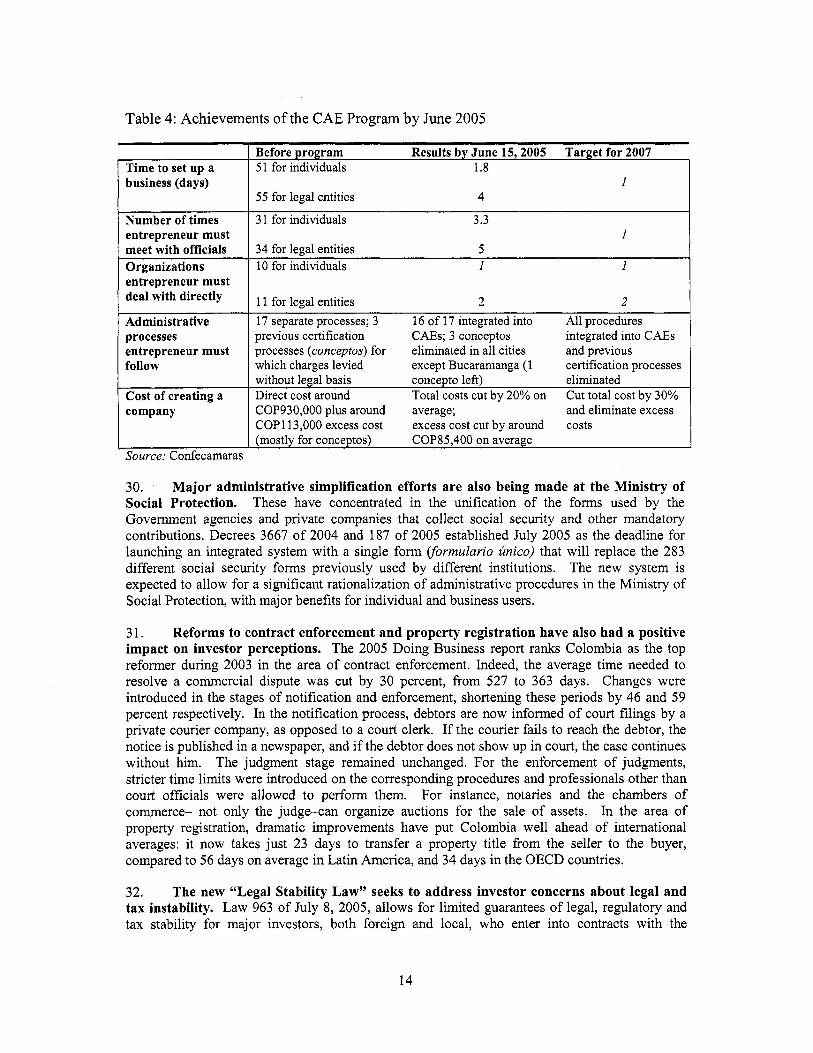

Table 4: Achievements o f the CAE Program by June 2005

Cost of creating a company

1 Before program Results by June 15,2005 Target for 2007

without legal basis concipto left) eliminated Direct cost around COP930,OOO plus around average; and eliminate excess COP1 13,000 excess cost excess cost cut by around costs (mostly for conceptos)

Total costs cut by 20% on Cut total cost by 30%

COP85,400 on average

Time to set up a I 51 for individuals 1.8 business (days)

Number of times entrepreneur must meet with officials Organizations entrepreneur must deal with directly

Administrative processes entrepreneur must follow

1 55 for legal entities 4

3 1 for individuals 3.3

34 for legal entities 5 1

10 for individuals I 1

11 for legal entities 2 2 17 separate processes; 3 previous certification C a s ; 3 conceptos integrated into CAEs processes (conceptos) for eliminated in al l cities and previous which charges levied except Bucaramanga (1 certification processes

16 o f 17 integrated into A l l procedures

30. M a j o r administrative simplification efforts are also being made at the Ministry of Social Protection. These have concentrated in the unification o f the forms used by the Government agencies and private companies that collect social security and other mandatory contributions. Decrees 3667 o f 2004 and 187 o f 2005 established July 2005 as the deadline for launching an integrated system with a single form Cformulario zinico) that wil l replace the 283 different social security forms previously used by different institutions. The new system i s expected to allow for a significant rationalization o f administrative procedures in the Ministry o f Social Protection, with major benefits for individual and business users.

3 1, Reforms to contract enforcement and property registration have also had a positive impact on investor perceptions. The 2005 Doing Business report ranks Colombia as the top reformer during 2003 in the area o f contract enforcement. Indeed, the average time needed to resolve a commercial dispute was cut by 30 percent, from 527 to 363 days. Changes were introduced in the stages o f notification and enforcement, shortening these periods by 46 and 59 percent respectively. In the notification process, debtors are now informed o f court filings by a private courier company, as opposed to a court clerk. If the courier fails to reach the debtor, the notice i s published in a newspaper, and if the debtor does not show up in court, the case continues without him. The judgment stage remained unchanged. For the enforcement o f judgments, stricter time limits were introduced on the corresponding procedures and professionals other than court officials were allowed to perform them. For instance, notaries and the chambers o f commerce- not only the judge-can organize auctions for the sale o f assets. In the area o f property registration, dramatic improvements have put Colombia well ahead o f international averages: i t now takes just 23 days to transfer a property title from the seller to the buyer, compared to 56 days on average in Latin America, and 34 days in the OECD countries.

32. The new “Legal Stability Law” seeks to address investor concerns about legal and tax instability. Law 963 o f July 8, 2005, allows for limited guarantees o f legal, regulatory and tax stability for major investors, both foreign and local, who enter into contracts wi th the

14

government for an annual fee o f one percent o f the value o f the investment. In return, the government guarantees that the project covered w i l l be exempt from any changes to applicable laws and regulations specified in the contract. Exceptions include labor and social security laws, taxes and charges introduced in a state o f emergency, indirect taxes and Central Bank (Banco de la Republica, BdR) rules. The contracts only cover new investments with a value greater than US$1 million, and can last for terms o f 3 to 20 years.

33. The GoC has made considerable progress in combating money laundering but this illegal activity still creates difficulties for legitimate businesses. In recent years, authorities have tightened the regulatory framework to limit money laundering through the financial sector and capital markets, supported by the Bank’s program o f Financial Sector Adjustment Loans (FSALs), through Anti Money LaunderingKombating the Financing o f Terrorism (AMLKFT) initiatives. These reforms are discussed in the financial sector section below. In the real sector, joint efforts by the National Tax and Customs Directorate (Direccidn de Impuestos y Aduanas Nacionales, DIAN), the Ministry o f Finance and Public Credit (Ministerio de Hacienda y Crddito Pliblico, MHCP) and the National Police have resulted in the capture and confiscation o f large quantities o f contraband imports, a principal form o f asset-laundering through the non-financial sector. But the sale within Colombia o f cheap, illegally imported goods, particularly domestic appliances, continues to represent unfair competition on a major scale for local producers, importers and retailers, as well as fuelling the drug trade. The operation o f “front” companies and other illegal businesses in construction and other sectors also undercuts legal competitors. Furthermore, the entry o f extra foreign currency through money laundering contributes to peso appreciation, which diminishes the competitiveness o f exports priced in pesos (i.e. not commodities).

34. Despite important recent reforms, the Colombia business environment still presents major challenges, such as the need to facilitate bankruptcy procedures and strengthen investor rights. The country’s collateral and bankruptcy laws are less conducive to lending than those in the OECD. The average duration o f bankruptcy procedures i s three years, which i s less than the Latin American country average o f 3.7 years, but i s s t i l l high compared with the OECD’s 1.7 years. The Companies Superintendency (Superintendencia de Sociedades, SS) i s working on a draft bankruptcy law that, among other things, w i l l reduce the time required for restructuring and liquidation procedures. However, due to the recent extension o f Law 550, which covers bankruptcy processes, consideration o f the new proposed legislation in Congress i s likely to be delayed. The Bank has provided analytical support in the context o f the Financial Sector Assessment Program (FSAP) update completed in 2005 regarding the required bankruptcy framework and given the importance that this has with respect to the supply o f credit, th is i s discussed further below in the Access to Finance section. Wi th respect to investor rights, Colombia has a score o f 2 on a scale o f 0 to 7 in the Doing Business index that measures the degree o f investor protection through the disclosure o f ownership and financial information. The regional average i s 2.3 and the average for OECD i s 5.6.

35. In the area of business environment, the first DPL would support three of the measures described here. These would be: (a) the enactment o f the Ley Anti-Trhmites; (b) the issuance o f CONPES policy document 3292, establishing the strategy on inter-institutional collaboration to rationalize bureaucratic procedures particularly regarding business activities; and (c) the enactment o f the Legal Stability for Investors Law.

15

FOREIGN TRADE AND COMPETITIVENESS

36. The G o C i s using a broad consultative process to develop a n inter-ministerial strategy for enhancing international competitiveness. The process aims to establish a “Internal Agenda for the Productivity and Competitiveness o f Colombia” (Agenda Interna para la Productividad y Competitividad de Colombia, AI). The motivation for this initiative i s the GoC’s view that the potential benefits o f the various trade agreements currently being negotiated by Co1ombia-e.g. with MERCOSUR and the U.S. and other Andean countries-depend on the adoption o f a set o f complementary domestic policies in the areas o f innovation, human resources, infrastructure, environment, institutional development and MSME support. CONPES policy document No. 3297 established a methodology for drawing up the A I by defining, prioritizing and building consensus around the set o f policies needed, through sectoral and regional. consultations coordinated by DNP. The strategy aims to enhance productivity and competitiveness in all regions and sectors, which should cushion those producers that could be negatively affected by these free trade agreements. The consultations took place in early 2005 and the final report i s scheduled for completion later in the year.

37. The A I builds upon several ongoing initiatives to eliminate obstacles to competitiveness and coordinate policies for competitiveness enhancing purposes. One o f the main initiatives i s the “Colombia Competes Network” (Red Colombia Compite), coordinated by M C I T and wi th private sector participation. This initiative i s aimed at identifying policies to deal wi th obstacles to competitiveness in ten thematic areas. Another similar initiative i s the creation o f “Competitiveness Agreements” (Acuerdos de Competitividad), also led by MCIT. These agreements have been established in 17 productive chains and clusters. In addition, there are various regional initiatives with a focus on coordinating support for SMEs, export promotion and science and technology policies at the regional level.

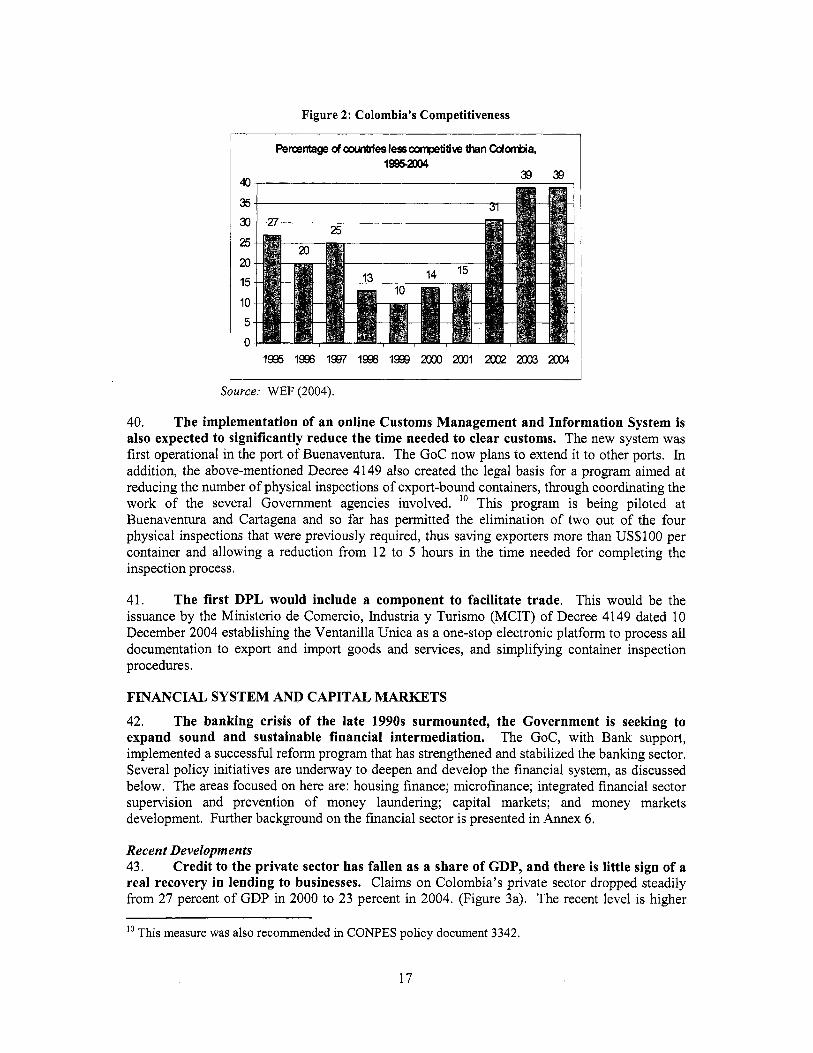

38. WEF data suggests that Colombia’s competitiveness has improved considerably this decade. While Colombia’s ranking in the WEF competitiveness index i s still relatively low (64‘h out o f 104 countries in 2004), th is has improved dramatically in recent years. Indeed, after dropping from the 27th to the 10* percentile worldwide between 1995 and 1999, Colombia recovered to the 3gth percentile in 2003 and 2004 (Figure 2). In 2004, Colombia was ahead o f 11 countries in Latin America and the Caribbean, including Peru, Argentina and Venezuela. It i s worth noting, however, that i t trailed Chile, Mexico and Brazil-ranked respectively 22nd, 48‘h and 57‘h-as well as five smaller countries.

39. The GoC has been working for more than two years with the 17 different government agencies involved to simplify import and export procedures. Through Decree 4149 o f December 2004 the Government established a six-month timeframe for the implementation o f a single web-based system*-the Ventanilla Unica-through which businesses can obtain all authorizations necessary for importing or e~por t i ng .~ The M C I T aims for the system to reduce the administrative burden on exporters from around 35 forms to just one, with the average time needed for export-related bureaucratic procedures dropping from 20 to three days. The new service was launched on July 1,2005.

* The web page i s www.vuce.gov.co

set out in CONPES policy document 3292. The ventanilla unica i s included within the GoC’s broader strategy to reduce bureaucratic procedures, as

16

Figure 2: Colombia's Competitiveness

1995 1996 1937 1998 1999 m 2001 2002 2003 2004

1 Percentage of mntries lessconpetitim than Colombia,

1

19952XM I M . .., 36 30 25

20 15

10 5 0

40. The implementation of an online Customs Management and Information System i s also expected to significantly reduce the time needed to clear customs. The new system was first operational in the port o f Buenaventura. The GoC now plans to extend it to other ports. In addition, the above-mentioned Decree 4149 also created the legal basis for a program aimed at reducing the number o f physical inspections o f export-bound containers, through coordinating the work o f the several Government agencies involved. This program i s being piloted at Buenaventura and Cartagena and so far has permitted the elimination o f two out o f the four physical inspections that were previously required, thus saving exporters more than US$lOO per container and allowing a reduction from 12 to 5 hours in the time needed for completing the inspection process.

10

41. The first DPL would include a component to facilitate trade. This would be the issuance by the Ministerio de Comercio, Industria y Turismo (MCIT) o f Decree 4149 dated 10 December 2004 establishing the Ventanilla Unica as a one-stop electronic platform to process all documentation to export and import goods and services, and simplifying container inspection procedures.

FINANCIAL S Y S T E M AND CAPITAL M A R K E T S

42. The banking crisis of the late 1990s surmounted, the Government i s seeking to expand sound and sustainable financial intermediation. The GoC, with Bank support, implemented a successful reform program that has strengthened and stabilized the banking sector, Several policy initiatives are underway to deepen and develop the financial system, as discussed below. The areas focused on here are: housing finance; microfinance; integrated financial sector supervision and prevention o f money laundering; capital markets; and money markets development. Further background on the financial sector i s presented in Annex 6.

Recent Developments 43. Credit to the private sector has fallen as a share of GDP, and there i s little sign of a real recovery in lending to businesses. Claims on Colombia's private sector dropped steadily from 27 percent o f GDP in 2000 to 23 percent in 2004. (Figure 3a). The recent level i s higher

lo This measure was also recommended in CONPES policy document 3342.

17

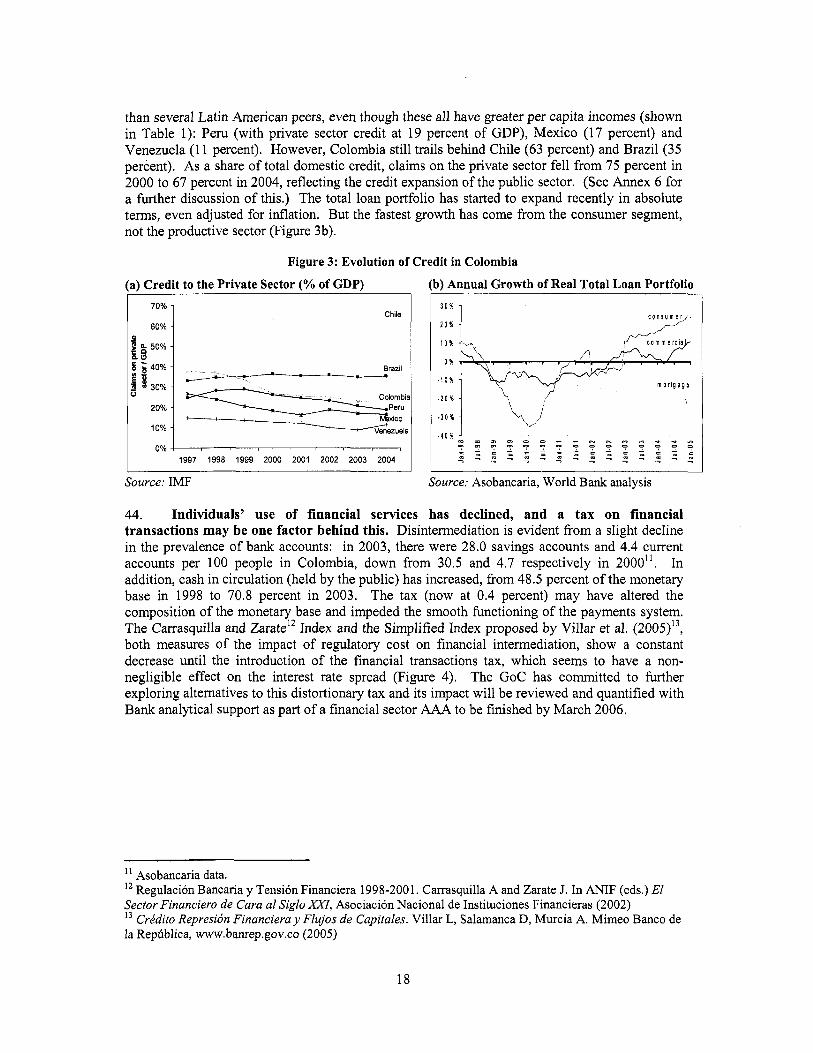

than several Latin American peers, even though these all have greater per capita incomes (shown in Table 1): Peru (with private sector credit at 19 percent o f GDP), Mexico (17 percent) and Venezuela (1 1 percent). However, Colombia s t i l l trails behind Chile (63 percent) and Brazil (35 percent). As a share o f total domestic credit, claims on the private sector fe l l from 75 percent in 2000 to 67 percent in 2004, reflecting the credit expansion o f the public sector. (See Annex 6 for a fiuther discussion o f this.) The total loan portfolio has started to expand recently in absolute terms, even adjusted for inflation. But the fastest growth has come from the consumer segment, not the productive sector (Figure 3b).

Figure 3: Evolution of Credit in Colombia

(a) Credit to the Private Sector (% of GDP)

Chile

g g 50% b o 6 $ 40%

I 30% 0

O H

20%

10%

1997 1998 1999 2000 2001 2002 2003 2004 I I I I

Source: IMF Source: Asobancaria, World Bank analysis

44. Individuals' use of financial services has declined, and a tax on financial transactions may be one factor behind this. Disintermediation i s evident f iom a slight decline in the prevalence o f bank accounts: in 2003, there were 28.0 savings accounts and 4.4 current accounts per 100 people in Colombia, down from 30.5 and 4.7 respectively in 2000'1. In addition, cash in circulation (held by the public) has increased, from 48.5 percent o f the monetary base in 1998 to 70.8 percent in 2003. The tax (now at 0.4 percent) may have altered the composition o f the monetary base and impeded the smooth functioning o f the payments system. The Carrasquilla and Zarate12 Index and the Simplified Index proposed by Vil lar et al. (2005)13, both measures of the impact o f regulatory cost on financial intermediation, show a constant decrease unti l the introduction o f the financial transactions tax, which seems to have a non- negligible effect on the interest rate spread (Figure 4). The GoC has committed to further exploring alternatives to th i s distortionary tax and its impact w i l l be reviewed and quantified with Bank analytical support as part o f a financial sector AAA to be finished by March 2006.

Asobancaria data. l2 Regulaci6n Bancaria y Tensi6n Financiera 1998-2001. Carrasquilla A and Zarate J. In ANIF (eds.) El Sector Financier0 de Cara a1 Siglo XI, Asociaci6n Nacional de Instituciones Financieras (2002) l3 Crtdito Represi6n Financiera y Flujos de Capitales. Vil lar L, Salamanca D, Murcia A. Mimeo Banco de la Rephblica, www.banrep.gov.co (2005)

18

Figure 4: The Impact of Regulatory Cost and Burden on Financial Intermediation

Source; Villar, Salamanca and Murcia (2005)’ “CrCdito, Represi6n Financiera y Flujos de Capitales en Colombia: 1974 - 2003”

45. Intermediation margins have not narrowed in recent years, and are still wider than in 2000. Despite a gradual fall in the benchmark Fixed-Term Deposit interest rate (Depdsito a Tbrmino Fijo, DTF) and lower inflation, the banking sector’s average lending rates and overall net interest margin have remained fairly stable for three years (Figure 5). This causes concem because higher lending rates deter borrowing and investment in the real sector, and may signal rising costs o f intermediation among banks. Possible explanations for higher costs include the overhang o f a large stock o f bad loans (particularly for mortgage lenders), ‘financial repression’ (Le. a term used to refer to the burden o f financial taxes, reserve requirements and directed lending programs that affect a country’s financial sector), and operational inefficiencies (overhead ratio of 5-6 percent o f assets mostly due to banks’ relatively small size). Alternative hypotheses for why lending rates have fallen less than deposit rates include: insufficient competition (despite relatively low sector concentration); and the ‘crowding out’ o f private sector borrowing by banks holding more government securities.

Figure 5: Evolution of Colombia’s Key Rates and Yields

0.“ O0 * .p‘ 9 cp‘Jhe$‘ *.p% ,*$ ,.“‘,.p’*.p’ ,*?’ J’,.p’ *.* ,*e@ J,.s” *.p*

+Average Yield on Net Loan PorHolio (annualized) -C Net Interest Margin +Interest on 8 M a y Deposit Csrtlflcates (DTF) +Inflation Rate (mlllng 12-month average)

Source; SB, DANE. Note: N e t Interest Margin i s net interest income o f the banking sector / average assets

19

Housing Finance 46. T h e mortgage sector i s recovering slowly f rom the crisis. The housing portfolio i s relatively large by regional standards, accounting for 12 percent o f GDP, against 4 percent in Brazil, 6 percent in Mexico, and 16 percent in Chile - all well below the US rate o f 70 percent. Despite a recent boom in the construction sector, Colombia still faces a large housing deficit. On the supply side, the establishment o f the Colombian Home Mortgage Corporation (CHMC, Titulizadora Colombiana) has expanded market opportunities by creating a new source o f long te rm funds for mortgage banks, through the securitization o f a large portion o f banks’ portfolios. Currently, 30 percent o f the mortgage loan portfolio i s securitized, while an additional 5 percent i s funded through bonds. On the demand side, Colombians are s t i l l reluctant to seek mortgages, after the experience o f the 1998 system collapse, when soaring interest rates caused widespread foreclosures. In the high-income segment, now recovering strongly, the mortgage industry faces increased competition from savings and remittances. Obstacles to the recovery o f the mortgage portfolio include: a) Cost of resources. Interest rates have fallen but remain high. Requirements for banks to make mandatory investments in certain instruments also exert pressure on interest rates; and b) Cap on interest rates. Colombia’s Constitutional Court in 2000 imposed a ceiling o f inflation + 11 percentage points on loan rates for low-income housing (Vivienda de Inter& Social, VIS). As long as this cap applies, this segment o f the market w i l l not really recover without additional support, as banks are unable to adequately price their risks. The GoC has attempted to eliminate th is ceiling, but its room for maneuver i s limited given the court decisions.

47. T h e GoC i s promoting the use of new investment vehicles for housing. To stimulate the use o f alternative sources o f financing, particularly for VIS, the Government issued Decree 1877 o f 2004. This provided the regulatory framework for real estate investment funds (REFS). REFS invest primarily (at least 60 percent o f assets) in real estate and the income stream i s derived from the rental payments that this real estate generates. To promote investments in the construction o f new VIS, the income stream from new VIS rental payments i s tax free for 10 years. REIFs are also allowed, subject to caps, to invest in non-VIS housing, commercial real estate and mortgage-backed securities.

48. Further regulation of other non-bank institutions wi l l permit greater participation by them in the housing finance sector. In particular, Colombia’s cajas de compensacidn familiar, non-profit associations for employee benefits and social services, are poised to expand mortgage lending, particularly to low-income members. The cajas have been allowed by law to fund the construction and acquisition o f housing since 1973, and since 1990 have been required to offer housing purchase subsides to workers earning less than four times the minimum wage. But grants o f subsidies have consistently fallen short o f projections (with 31,661 awarded in 2004 against a target o f 36,000) as many potential recipients failed to qualify for mortgages from banks. The cajas themselves have only provided home loans on a limited scale to date, as they have not had capital backing for more. Law 789 o f 2002 remedied this by permitting the sector to start taking deposits from members. Enactment o f Law 920/2004 allows for the provision o f housing finance by cajas to i t s affiliates in a framework o f adequate prudential regulation and MHCP has already regulated the financial activities to be carried out by the cajas.

49. The first DPL would promote the development of housing finance through support for such regulatory measures. Specifically, the program would include: the enactment o f Law 920/2004 and the issuance by MHCP o f a decree regulating the financial activities to be carried out by the Cajas, as described in the previous paragraph.

20

Microfin an ce

50. T h e G o C i s seeking to promote an active microfinance sector in the country. While formal lenders have been reluctant to lend to the 60 percent o f the households that earn informal incomes, unregulated micro-finance lenders are eager to do so. There are two types o f micro- finance institutions in the country: Non-Governmental Organizations (NGOs), accounting for 40 percent o f the market and the regulated banking system, which accounts for 60 percent. The development o f the microfinance sector i s hampered by NGOs’ lack o f capital and the cap on interest rates for microcredits for VIS, discussed above. Microfinance lenders, as in other countries, tailor loan products and collection methods to the earnings and living situations o f low- income, informal households, and have managed to keep default rates low. The GoC i s seeking ways to ensure that microfinance lenders are run in a prudent financial way and gain access to long-term funds, to scale up their programs without losing the advantages o f their business model.

51. Through the National Guarantee Fund (Fondo Nacional de Garantias, FNG) the G o C i s seeking to support the development of microcredit in Colombia. Established in 1982, the FNG i s a government-owned company supervised by the SB. One o f FNG’s objectives i s to facilitate access to credit for MSMEs through the provision o f partial risk guaranteed4. About 93 percent o f the guarantees provided by FNG are automatic, meaning that they are granted by banks or other financial institutions without direct consultation with FNG by either the lender or borrower, under “global automatic guarantee agreements”. These accords, which are a type o f proportional risk reinsurance agreement, are signed by institutions and the FNG after a risk study to establish the Fund’s maximum exposure to a particular intermediary. To date, FNG has signed such agreements with 15 banks and 26 non-bank financial intermediaries. Under a 2004 agreement, Bancoldex may now offer automatic guarantee products to most o f i t s MSME clients. In 2005, FNG moved to create special guarantees for microfinance institutions (MFIs) to encourage private banks to extend credit lines to MFIs. The GoC i s aware that these guarantee facilities should be seen as temporary measures to foster the beginning o f relationships between banks and MFIs. The prudential regulation o f FNG was strengthened by the issuance o f decree 1324 o f 28 April 2005 by MHCP.

52. The first DPL would promote the development of microcredit through bolstering the FNG. Thus the program would include the issuance by MHCP o f decree 1324 o f 28 April 2005, to improve the FNG’s prudential regulation.

Prudential Regulation and Prevention of Money Laundering and Terrorism Financing 53. Prudential regulations continue to be strengthened in key areas. Significant revisions o f the legal framework have been made since the crisis. Modifications to the Banking Law have raised minimum bank capital requirements for credit and market risk and provided the legal background for early warning systems, prompt corrective actions, and consolidated supervision. The Banking Law also sought to protect consumers and to diversify the range o f banking products. In addition, the SB issued regulations to define a new system o f risk-based loan classification and provisions, encompassing specific and general provisioning requirements. Risk-based regulation and consolidated supervision remain key issues going forward. The SBC, as recommended in the 2004 FSAP Update, issued norms concerning the role, duties, and responsibilities o f external auditors and internal comptrollers (revisores Jiscales), setting audit

14The guarantee applicable - o f at least ten different types-depends on the nature o f the borrower and the purpose for seeking funds (e.g. working capital, f ixed investment, starting a business.) Depending o n the type, the coverage o f FNG’s guarantee i s capped at between 50 percent and 70 percent o f the loan amount, for which commissions o f 1.50-3.05 percent are payable.

21

standards and greatly increasing its objectivity. The Pensions Department o f the SB i s in the final stages o f the development o f an Early Warning System for the analysis, control and valuation of pension managers’ portfolios. This new system wi l l allow for daily monitoring o f the structure and regulatory compliance o f managers, rather than monthly and quarterly, as now.

54. With the stated objectives of consolidating supervision and avoiding regulatory arbitrage and overlapping of supervisory efforts, the authorities plan to merge the Banking and Securities Superintendencies. The Banking Superintendency (Superintendencia Bancaria, SB) and the Securities Superintendency (Superintendencia de Valores, SV) wil l be replaced by a new institution, provisionally named the Financial Superintendency (Superintendencia Financiera, SF). Most supervisory responsibilities over banks, insurance and pension funds are already concentrated in the SB. Consolidation o f supervisory responsibilities i s supported as a means to reduce interagency coordination costs. Given the dominance o f financial conglomerates in the banking system, the ground rules for cooperation should be clearly defined within the new SF. These should include specific requirements for the exchange o f information, consultation and assistance on policy, monitoring o f markets and entities, and conflict resolution processes. The new agency should define a lead supervisor within i t s organization with clear consolidation scope, responsibility and accountability conceming market, credit and liquidity risks, and stress tests, at the consolidated financial conglomerate level.

55. I t i s desirable that the merger be conducted in a way that not only limits disruption, but also promotes progress in governance and technical capabilities. The successful implementation o f the merger w i l l require that the new body receive additional resources to develop infrastructure, organizational arrangements, procedures and professional sk i l l s consistent with the new strategy. The current scheme guarantees funding for the new entity to cover normal operating costs, through contributions from supervised entities. MHCP has prepared a Merger Plan that seeks to minimize any operational disruption during the process. The technical and organizational challenges for the final implementation o f the plan remain significant. Going forward, the Bank w i l l be closely involved with issues associated wi th both the merger and strengthening governance and technical capabilities o f the regulator, both for the banking sector and capital markets. In particular, the forthcoming AAA financial sector program includes work on consolidated supervision that w i l l be used as input in defining the new superintendency’s responsibilities.

56. Combating money laundering and the financing of terrorism i s a key element in promoting a strong and sound financial system. Money laundering and terrorist financing can weaken individual financial institutions, as well as representing a threat to overall financial sector stability. The adverse consequences for institutions are generally described as: i) reputational; as high quality clients, that provide a stable deposit base and make reliable borrowers, lose confidence in an institution connected with money laundering and take their business elsewhere; ii) operational, where impaired intemal processes or relations with other financial institutions impede the institution’s functions or raise i t s operating and funding costs; and iii) legal, due to the risk o f law suits, adverse judgments, unenforceable contracts, fines and penalties.

57. Colombia’s government attaches a high priority to AML/CFT actions, to combat drug trafficking and organized crime, and promote financial sector stability and a healthy climate for business. The govemment policy for preventing and combating the offense i s described in the President’s Democratic Security and Defense Policy and the National Development Plan (Law No. 812 o f 2003). This policy stresses the significance o f the threat of money laundering and terrorist financing and enunciated GoC concems that the laundering of the proceeds o f cocaine and heroin marketing contributes to terrorism. Moreover, the Colombian

22

government emphasizes that money laundering distorts the proper functioning o f the economy as i t disrupts the foreign exchange market and other financial markets, and promotes the under- invoicing o f imports and exports and the making o f fictitious or simulated exports as a suitable mechanism for bringing il l icit money into the country with the appearance o f legality.

58. Colombian authorities have moved to tighten the regulatory framework, to limit money laundering through the financial sector and capital markets. The SB has adopted several regulations (Circulares Externas, CEs) that have introduced new client due diligence mechanisms and reporting requirements for financial institutions and foreign exchange intermediaries, particularly concerning unusual transactions. These include: CE 25 o f 2003 and CE 34 o f 2004, on the contents and implementation o f the Comprehensive Money Laundering Prevention System (SIPLA), and CE 40 o f 2004 on the content o f suspicious transactions reports. The SV, has also modified its “Know Your Client” (KYC) ru les (obligation to identify clients and their economic activities).with CE 003 o f 2005, regarding the application o f simplified customer due diligence measures for non-resident clients. The BdR’s resolution No. 6 o f 2004 requires cross-border currency transactions above US$l 0,000 to be performed only through authorized businesses. In addition, DIAN adopted in 2002 a regulation on the prevention o f money laundering, requiring participants in international trade and currency exchanges to implement K Y C mechanisms.

59. The Financial Information and Analysis Unit (Unidad de Informacidn y Andisis Financiero, UIAF) plays an effective central role in the AML apparatus but needs improvements. The UIAF, established within MHCP in 1999, has broad authority to access information from the public and private sectors to combat money laundering. I t analyzes suspicious transaction reports and other information filed by reporting entities, including banks, exchange houses, and wire remitters, and refers cases to law enforcement for investigation and prosecution. I t also provides training on AML within Colombia and the region. The UIAF reports that Colombia has investigated more than 250 money laundering cases to date. However, independent analyses in 200415 identified key challenges for the UIAF. These include: (a) improving the volume, timeliness and quality o f cases that the UIAF refers to law enforcement; (b) adopting operational/organizational changes to enhance the flow o f work within the unit and utilize more sophisticated IT tools, including data mining software; (c) increasing levels o f financial expertise and analytical training among unit personnel; and (d) upgrading security, both for personnel and facilities, to better protect sensitive financial information.

60. The GoC i s working to improve inter-agency co-operation, the enforcement of AML regulations and the operational capacities of other supervising agencies. In 2004 the GoC’s issued Decree 3420 to reorganize and streamline the Inter-institutional Coordination Commission for AML (CCICLA), the consultative body o f the national government and coordinator o f the measures taken by the Colombian state to combat money laundering. The GoC i s also working to improve information-sharing, through the development o f a secure centralized database system that w i l l facilitate the flow o f information related to AML among the UIAF, law enforcement, regulators and supervisors and other government agencies involved. In addition, the SB, the SV and the Superintendency o f Cooperatives and Mutual Societies (Superintendencia de la Economi’a Solidaria, SES) have, with the assistance o f the Bank, formulated strategies and action plans to address operational shortcomings in AML supervision. To strengthen its preventive and supervisory AML apparatus, the SB’s priorities are to develop a risk-based approach to AML, including the establishment o f an AML early warning system; and collect more AML data from financial institutions, using questionnaires. The SES aims to further train on-site and off-site

~~ ~

l5 Prepared by the Canadian government, a Colombian firm, GAFISUD, the IMF, and the U.S