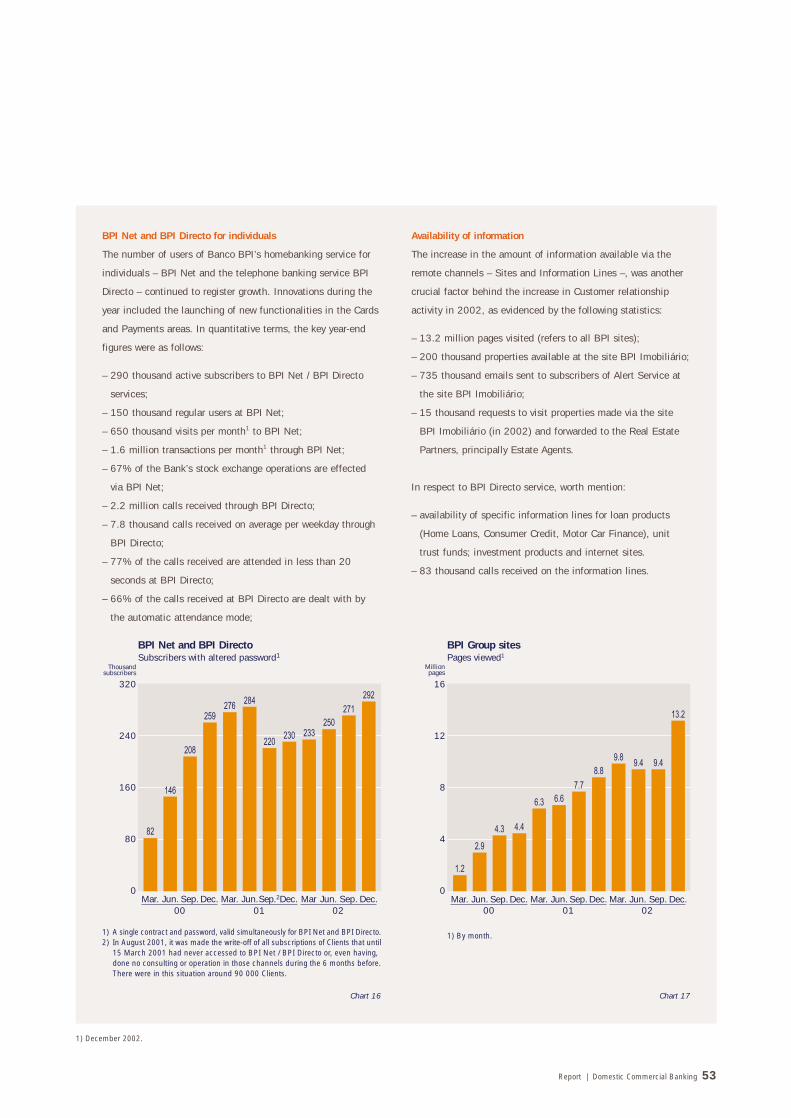

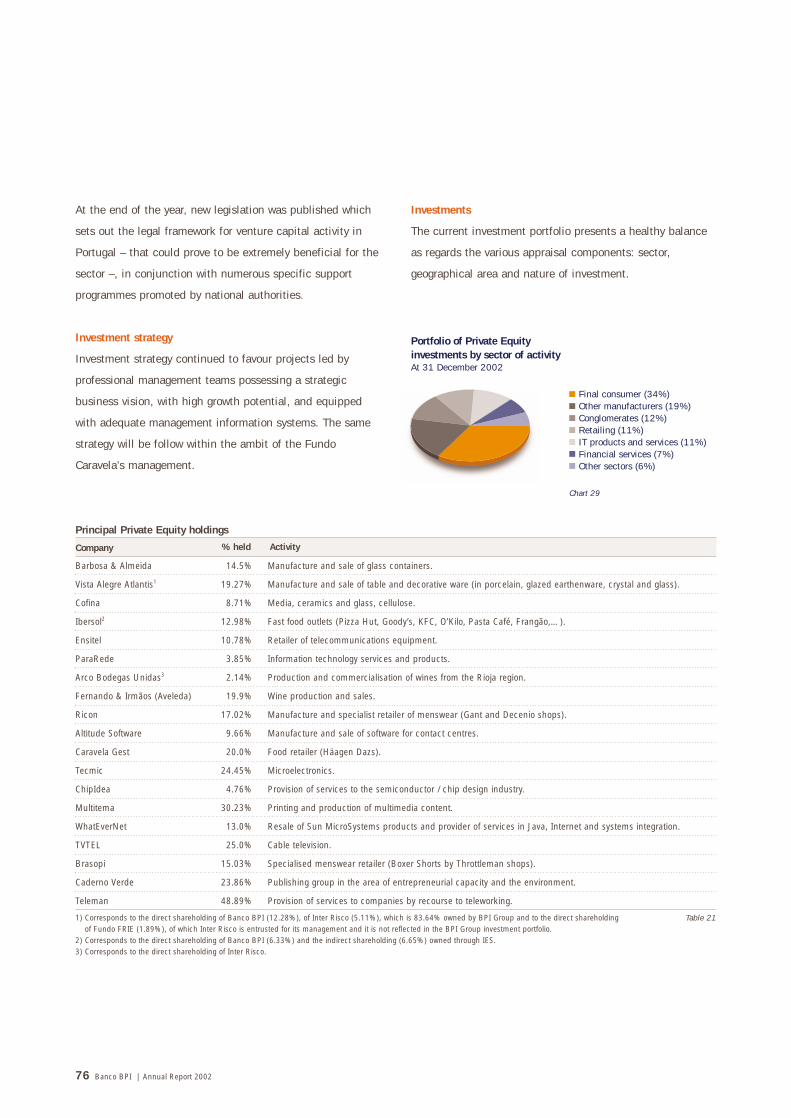

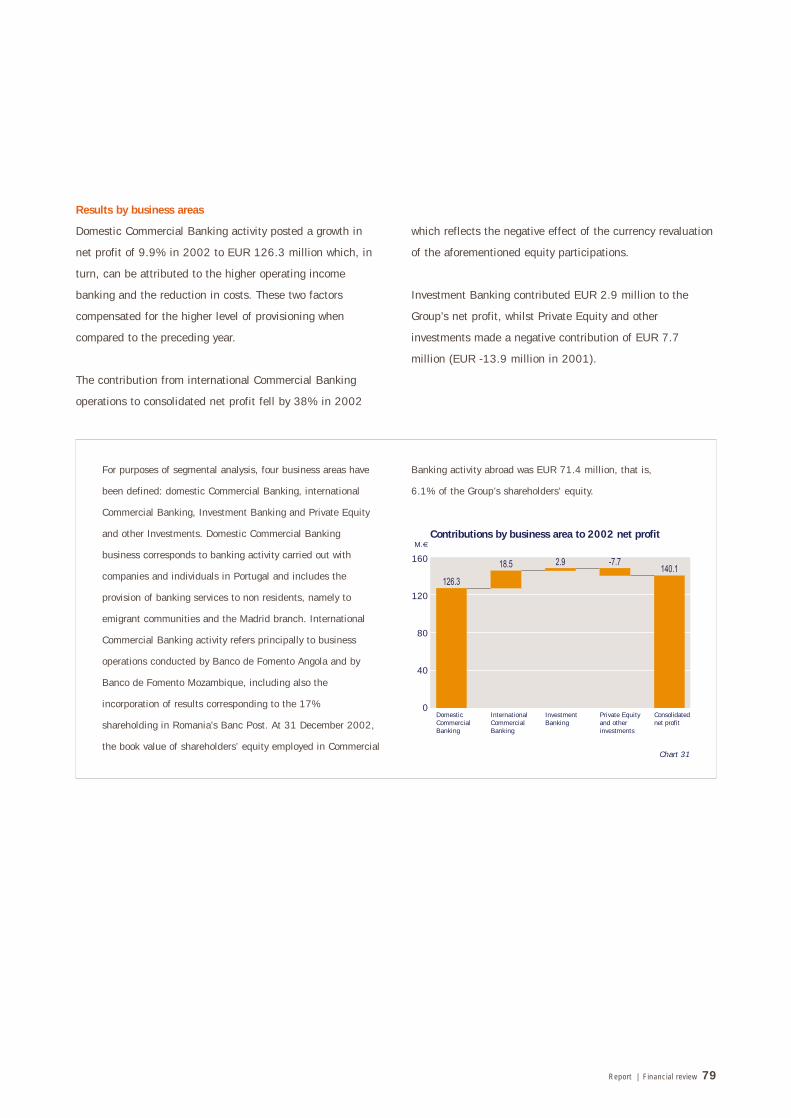

banco bpi 2002 · 2005-01-17 · leading business indicators (consolidated figures in millions of...

TRANSCRIPT

Banco BPI 2002

Report

Index

REPORTLeading business indicators 4

Introduction 6

Governing bodies 11

Historical milestones 12

The identity of BPI 14

The BPI brand 15

Corporate governance at the BPI Group 16

Social investment 18

Financial and business structure 20

Distribution channels 21

Human resources 22

Technology 25

Operations 35

Highlights of 2002 38

Background to operations 40

Domestic Commercial Banking 48

International Commercial Banking 62

Insurance 65

Asset Management 66

Investment Banking 72

Private Equity 75

Financial review 77

Risk management 108

Rating 120

BPI shares 122

Shareholders 125

Shareholders value creation 126

Final acknowledgements 127

Proposed appropriation of net profit 128

CONSOLIDATED FINANCIAL STATEMENTS AND NOTESConsolidated financial statements 129

Notes to the consolidated financial statements 137

Legal certification of accounts and audit report 195

Auditor's report 197

Report and opinion of the Audit Board 198

ANNEXESThe BPI Group's Corporate Governance Report 201

Trading information 223

Appendices

Definitions, acronyms and abbreviations 226

Glossary 228

Formulary 230

Methodological notes 231

Index of figures, tables, charts and "boxes" 232

General index 234

Miscellaneous information 237

Leading business indicators

(Consolidated figures in millions of euro, except where indicated otherwise)

4 Banco BPI | Annual Report 2002

1) Administrative overheads (personnel costs and outside supplies and services) as % of operating income from banking.2) Administrative overheads and depreciation as % of operating income from banking, excluding profits from financial operations.3) Calculated in accordance with the Portuguese Central Bank's rules governing minimum own funds requirements (Notice 7 / 96).4) Pension liabilities recognised in the balance sheet.5) Adjusted for capital increase, re-denomination and re-nominalisation.6) Includes traditional branches (508 in 2001 and 483 in 2002), housing shops, in-store branches, investment centres and automatic shops.7) Distribution network specialising in serving medium-sized companies (44 Corporate Centres), large companies (7 Corporate Centres), 4 Wholesale Centres,

1 Project Finance Centre and Institutionals (5 Centres).8) Group staff complement in the domestic and international activities. Includes term Employees and temporary workers.

20022001 ∆% 01 / 02200019991998

Total assets 15 579.9 16 550.5 21 907.4 24 792.9 25 669.1 3.5%

Total assets plus disintermediation 19 885.2 20 758.0 26 335.8 29 127.7 29 605.6 1.6%

Shareholders’ equity 566.4 650.7 930.0 908.7 1 168.9 28.6%

Loans to Customers (gross) and guarantees 9 903.6 12 023.4 16 542.8 18 768.9 19 738.0 5.2%

Customer deposits 9 053.6 9 458.5 10 463.7 11 494.3 12 224.6 6.4%

Total Customer resources 13 909.8 14 806.0 16 507.8 17 402.9 17 647.5 1.4%

Assets under management 7 009 7 249 7 639 7 545 7 513 (0.4%)

Operating cash flow 227.2 207.2 278.6 327.0 310.4 (5.1%)

Net operating income 159.2 139.6 152.5 190.6 192.1 0.7%

Net profit 137.0 124.8 152.4 133.3 140.1 5.1%

Cash flow after taxation 205.0 192.3 278.5 269.6 258.4 (4.2%)

Return on average total assets (ROA) 0.8% 0.8% 0.8% 0.6% 0.6%

Return on Shareholders’ equity (ROE) 25.6% 22.4% 21.6% 14.7% 13.5%

Cost-to-income1 61.7% 65.0% 60.7% 58.1% 58.7%

Efficiency ratio2 74.5% 79.6% 71.9% 68.3% 67.1%

Ratio of own funds requirements3 11.1% 11.6% 9.8% 9.2% 10.2%

Tier I3 6.0% 6.8% 6.7% 5.9% 7.3%

Loans in arrears for more than 90 days as % of Customer loans 1.8% 1.4% 1.0% 0.9% 1.3%

Provisioning cover for arrear loans 141.0% 157.3% 194.2% 210.0% 153.0%

Cover of pension obligations4 101.7% 102.4% 101.6% 100.0% 100.1%

Data per share adjusted (euro)5

Cash flow after taxation 0.35 0.32 0.45 0.40 0.36 (10.7%)

Net profit 0.24 0.21 0.24 0.20 0.19 (2.0%)

Dividend 0.07 0.09 0.09 0.08 0.08 (2.4%)

Book value 0.97 1.05 1.37 1.34 1.54 14.9%

Weighted average no. of shares (in millions)5 584.0 603.8 626.3 679.0 728.3 7.3%

Closing price (euro)5 3.86 3.86 3.18 2.15 2.18 1.5%

Total Shareholder return 31.2% 2.5% (16.0%) (30.4%) 3.0%

Stock market capitalisation at year end 2 252.7 2 390.0 2 156.4 1 459.1 1 656.8 13.5%

Dividend yield 2.5% 2.4% 2.4% 2.7% 3.9%

Individuals and small businesses distribution network (retail branches)6 487 592 592 584 564 (3.4%)

Corporate and institutionals centres network7 53 54 63 63 61 (3.2%)

BPI Group staff complement (number)8 7 695 8 239 8 359 8 106 7 576 (6.5%)

Table 1

Net total assets1

Disintermediation2

Net total assets plusdisintermediation

1) Corrected for duplication ofbalances.

2) Off-balance sheet Customerresources.

32

24

16

8

00199

Bi.€

98 00 02

Loans and Customerresources

0199

Bi.€

98 00 02

Total Customer resources1

Loans to Customers

20

15

10

5

0

Net profit per share€

0.28

0.21

0.14

0.07

0.00

Net profitM.€

160

120

80

40

0

6

4

2

0

-2

Quality of loan portfolio%

Ratio of loans in arrears1

Loans in arrears1 net ofprovisions, as % of loans

to Customers

1) Loans in arrears for more than90 days.

2.0

1.5

1.0

0.5

0

Own funds and own fundsrequirements

Bi.€

Own fundsOwn funds requirements

BPI RatingsIssuer

Stock market capitalisationBi.€2.8

2.1

1.4

0.7

0

Fitch Ratings13 Jan. 03*

Moody’s7 Jan. 03*

Standard & Poor’s20 Dec. 02*

A+Stable

A2Stable

A-Stable Long-term rating notations

* last revision

1) Corrected for duplication ofbalances.

019998 00 02 019998 00 02

019998 00 02 019998 00 02

019998 00 02

Report | Leading business indicators 5

GROWTH, PROFITABILITY, STRENGTH AND VALUE

Figure 1

The BPI Group’s performance in 2002, marked by an important reorganisation of its system of

governance, confirms the satisfactory execution of the strategy mapped out for the three-year

period 2002-2004. This approach is based on a programme of selective and more efficient

growth, not only from the viewpoint of operating costs, but also in terms of capital allocation.

In 2002, BPI managed to surpass the targets set for cost containment, while simultaneously

achieving robust growth in its domestic activity. It continued to present risk and financial base

indicators within the best in the Portuguese banking system. Net profit posted a rise of 5%, in

spite of the pressure exerted on net interest income by the decline in interest rates.

The objectives for 2003 and 2004 have been revised in the light of the predictable impact of

the negative economic environment on the growth in demand and GDP. The new goals

envisage nil growth in both years in administrative overheads, defined as the sum of personnel

costs, other administrative costs and depreciation and amortisation. Considering that these

items had already registered a decline in 2002 of 2.8%, the revised objectives constitute an

even more demanding challenge. On the other side, the target set for gross operating income

from banking (excluding profits from financial operations) remains unaltered, that is, this item

is still projected to rise at a rate of 5% in 2003 and 2004, after having fallen slightly (1%) in

the year under review. As a consequence of this trend in costs and revenues, the new goal laid

down for the ratio administrative overheads / operating income from banking (excluding profits

from financial operations) is 61% in 2004, against 67% in 2002; in turn, the cost-to-income

ratio, which is calculated by expressing personnel costs and other administrative costs as a

percentage of operating income from banking, should decline from 58.7% in 2002 to 53% in

2004, thus confirming the Bank’s commitment to improve the efficiency and profitability of its

business operations.

Selective growth

Net profit from domestic operations (including the Madrid branch and banking services to

emigrant communities), climbed 17% in 2002 and accounted for 87% of the Group’s

consolidated profit. This in turn is explained by around 103% by commercial banking (with an

ROE of 15%) and helped to compensate for the negative contribution from participating

interests. Investment banking’s share was situated at 6%, corresponding to a return on capital

of 33%.

Net interest income in narrow sense generated by domestic activity rose by 3%, while

commissions from commercial banking grew by 7%, with very significant increases in net

income from insurance brokerage (+80%), transfers and payment orders (+11%), operations

relating to loans and guarantees (+9%) and cards (+7.5%).

Introduction

ON THE RIGHT COURSE

6 Banco BPI | Annual Report 2002

There was also a slight decrease (-4%) in asset management commissions,

a result that can be considered favourable in the light of the situation

pervading the markets and the lesser importance of investment banking

commissions (-27%). The latter were influenced significantly by the slump

in commissions from brokerage and capital market operations, which

dropped 48% as a consequence of the negative climate enveloping the

major stock markets.

The Group’s good operating performance, notably in commercial banking,

was mirrored in the trend in deposits, which expanded by 6.4% and so

outpacing the market average, and the 7.2% growth in global lending. This

index reflects highly contrasting patterns among broad Customer and

product segments: whilst the large companies’ loan portfolio registered a

year-on-year fall of 9% in line with the strategy subordinated to criteria

relating to returns on allocated capital, lending to individuals and small

businesses climbed 19%, with a strong impulse from home loans (which

expanded 26%, against an estimated market growth rate of 16%). This

translated itself into a new market share gain, replicating the trend since

1999. In just three years, BPI’s mortgage-loan portfolio market share has

increased by more than 50% to stand at 10% at the end of 2002. This

performance illustrates the competitive capacity that the Group has been

building in the principal specialised markets of commercial banking

following the 1998 merger, having captured positions well above its natural

market share in the financing of investment, housing loans, motor car

finance, credit cards and unit trust funds.

Another noteworthy development was the evolution of business activity

in the Angolan market, which constitutes the most important area of

the Group’s international involvement. Banco de Fomento de Angola

(100% owned by BPI) became a local-law bank in July 2002 and

carried out a major expansion programme during the year. It now boasts

the country’s second biggest banking network with 17 branches. This

expansion has enabled the bank to conquer second place in deposit-

-taking and third place in lending business. These activities are

complemented by an expressive participation in the Angolan economy’s

external transactions. BPI’s international presence (which includes

Banco de Fomento de Mozambique and a 17% stake in Rumania’s

Report | Introduction 7

Chairman of the Management Board

Artur Santos Silva

Banc Post) contributed 13% to consolidated earnings, absorbing approximately 6% of the

Group’s shareholders’ equity.

Efficiency and modernisation

The Group’s increasing competitiveness has been permanently accompanied by a qualitative

thrust centred on three focal points: absolute reduction in operating costs through the

elimination of unwarranted expenses, improved capacity to automate through technological

investment, and human resource upgrading induced by the rejuvenation of work teams and

vocational training.

The strict execution of the rationalisation programme in the operations’ arena announced for

the period 2002-2004, paved the way for a 3% reduction in the Group’s administrative

overheads (personnel costs, outside supplies and services, depreciation and amortisation), with

decreases of 1% in personnel costs, 6% in other administrative costs and 3.2% in

depreciation and amortisation. These savings led to an improvement from 68.3 to 67% in the

efficiency indicator, expressed by the quotient of administrative overheads over recurring

income (defined as operating income from banking excluding profits from financial

operations). A combination of factors contributed to this result, amongst which were the

intensified migration of transactions to virtual channels, the automation of operating

processes, the active management of the branch network (reflected in the net decrease of

25 points of sale), the integration of leasing and factoring into the commercial bank’s

structure, and an ambitious plan for early retirements. This plan, which involved 22% of the

Group’s senior management, made it possible to reduce the overall number of Employees by

around 9%. It should be emphasised that the impact on costs arising from this reduction in

staffing is progressive, that is, it was not fully reflected in the past year; furthermore, in spite

of being apparently inconsiderable as regards the number of early retirements, the saving in

total personnel costs more than cancels out the rise stemming from the collective employment

agreement that had a global effect of close to 4%.

In the sphere of modernisation of processes with repercussions on operations rationalisation,

automation and the ability to improve future income-generating capabilities, meriting special

reference are the structural refinements which started to be introduced into the Group’s

distribution systems and which are organised into two main camps:

– overhaul of the branch image and space, conceived to boost the sales and Customer

relationship capability at the expense of transaction flow, and increasingly directed at the

remote channels and automated zones available 24 hours a day, where it is possible to carry

out all the banking operations not requiring personal contact;

8 Banco BPI | Annual Report 2002

– service specialisation by segment and by product, flowing from the reinforcement of the

small business team, the opening of Investment Centres designed to cater for the

commercial bank’s high-income Customers, and the extension of the dedicated attendance

capability with the consolidation of the Housing Shops and the branch spaces reserved for

mortgage loans and the Internet.

By the end of 2003, at least eight Investment Centres and 18 Housing Shops should be

working, while 100 branches are expected to benefit from the new lay-out, with the

consequent extension of the methods and equipment that have made possible the intensive

migration of transactions and simple operations to automated banking under a specific project

with specific goals managed by its own section head.

A decisive factor for the success of this transformation process has been staff rejuvenation and

training, especially in the case of those working at the Individuals and Small Business Banking

networks. In 2002, this universe benefited from a behavioural training programme devoted to

boosting Customer-attendance quality and which involved more than three thousand

Employees. The average age at these networks (whose staff have mostly been trained at the

Bank) fell from 43 to 40 in the period 1999-2002.

Report | Introduction 9

Executive Members

of the Board

Manuel Ferreira da Silva

(Deputy-chairman) Fernando Ulrich

(Chairman) Artur Santos Silva

António Domingues

António Farinha Morais

Maria Celeste Hagatong

José Pena do Amaral

Strength and confidence

BPI’s rationalisation and renovation has been carried out without ever losing sight of the crucial

elements that ensure the Group’s sound financial base. In an economic environment – domestic

and external – that is indubitably depressive and with a tendency to deteriorate, the quality of

the loan portfolio depicts a slight deterioration, but nonetheless continues to present the

market’s best indicators: at 31 December 2002 the consolidated ratios of loans in arrears for

more than 90 days was situated at 1.3%, with a provisioning level of 153%. Overall, the

specific provisions for loans in arrears more than doubled in 2002. Roughly half of this increase

was earmarked to cover a specific default situation, excluding which the loans in arrears for

more than 90 days would have declined to 1.1%.

At the end of 2002, the capital adequacy ratio was situated at 11.4% using the BIS (Bank of

International Settlements) criterion, and 10.2% using Bank of Portugal rules, with Tier 1

calculated at 7.4 and 7.3%, respectively, thereby confirming the Bank’s healthy financial

situation. In similar vein was the return of 3.3% earned by the pension funds, which compares

very favourably with the market, preserving a unutilised margin of EUR 25 million in the 10%

"corridor" envisaged by the Bank of Portugal for accommodating the actuarial and income

variances without affecting net profit.

2002 will be primarily recalled in BPI’s history for the far-reaching corporate reorganisation

concluded at the end of the year, with important effects on the Group’s system of governance.

The principal and most visible alteration entailed the incorporation of Banco BPI in BPI SGPS,

which simultaneously assumed the corporate object of a commercial bank and adopted the

name of the incorporated institution – Banco BPI – assuming the mantle of the entity at the

head of the Group and is listed on the stock exchange. In the same step, companies were

extinguished which had hitherto headed important specialised activities that are now integrated

in the Group’s two banks: Leasing and Factoring at the commercial bank, Brokerage and

Development Capital at the investment bank. This restructuring brought about a definite

simplification of the Group’s organisation structure and was responsible for an important

reduction of the management structure and the attainment of considerable gains in terms of

efficiency and operating expenditure.

This potential was acknowledged by the rating agencies Moody’s, Standard & Poor’s and Fitch,

which confirmed BPI’s previous ratings and the stable outlook grading – the best classification

amongst the universe of Portuguese banks. The success attained in 2002 in terms of operating

efficiency, newly-manifested commercial ability and the principal indices of financial strength

confirmed that BPI is on the right course for securing the best conditions of competitiveness

and profitability in a future that is predicted to become increasingly demanding.

10 Banco BPI | Annual Report 2002

1) Co-opted to fill the vacancy left by António Seruca Salgado's renouncement; the registration process with the relevant authorities is currently being attended to.

2) Succeeded Corporació de Participacions Estrangeres, S.L. – which was 100% held – as a consequence of a merger.

Report | Governing bodies 11

Governing bodies

General MeetingChairman Rui Manuel Chancerelle de Machete

Deputy-Chairman Vasco Manuel Airão Marques

Secretaries Galucho – Indústrias Metalomecânicas, S.A. Vitalina Justino AntunesProdutos Sarcol, Lda. Estela M. Barbot

Company secretary Rui de Faria Lélis

Management BoardChairman Artur Santos Silva

Deputy-Chairmen Carlos da Câmara PestanaFernando UlrichRuy Octávio Matos de Carvalho

Members Alfredo Rezende de AlmeidaAntónio DominguesAntónio Farinha Morais1

Armando Leite de PinhoCaixa Holding, S.A., Sociedad Unipersonal2 Fernando RamirezIsidro Fainé CasasJoão Sanguinetti TaloneJosé Pena do AmaralKlaus DührkopManuel de Oliveira ViolasManuel Ferreira da SilvaMaria Celeste HagatongRiunione Adriática di Sicurtá Diethart BreipohlRoberto Egydio SetúbalTomaz Jervell

Executive Committeeof Management Board

Chairman Artur Santos SilvaDeputy-Chairman Fernando Ulrich

Members António DominguesJosé Pena do AmaralMaria Celeste HagatongManuel Ferreira da SilvaAntónio Farinha Morais

Audit BoardChairman Jorge de Figueiredo Dias

Members José Ferreira AmorimMagalhães, Neves e Associados, SROC Augusta FranciscoAntónio Dias & Associados, SROC (alternate) António Dias

Remunerations CommitteeChairman Itaúsa Portugal – Sociedade Gestora de Participações Sociais, S.A.

Members Cotesi – Companhia de Têxteis Sintéticos, S.A.Arsopi – Indústrias Metalúrgicas Arlindo Soares de Pinho, S.A.

Internal Control CommitteeChairman Ruy Octávio Matos de Carvalho

Members Carlos da Câmara PestanaAlfredo Rezende de AlmeidaCaixa Holding, S.A., Sociedad Unipersonal2 Fernando Ramirez

Figure 2

Historical milestones

LEADERSHIP, INNOVATION AND GROWTH

Sociedade Portuguesa de Investimentos was conceived in 1981

with a well-defined project for a decade that had just started: to

finance investment projects launched by the private sector, to

participate in the creation of a dynamic capital market and to

contribute to the country’s industry modernisation. BPI counted

on a diversified shareholder base that included a strong domestic

component, represented by 100 of the most dynamic companies

in the country, and five of the most prominent international

financial institutions.

SPI was transformed into an investment bank in 1985, thereby

allowing it to attract sight and term deposits, grant short-term

loans, participate in the interbank markets and engage in

currency operations. A year later, in 1986, the bank’s future

direction was marked by the opening of its capital to the general

public and the listing of its shares on the Lisbon and Oporto

Stock Exchanges.

In 1991, a decade after its formation, BPI had already conquered

an undisputed leadership in the principal areas of Investment

Banking and assumed its ambition to consolidate its position as

one of the country’s premier financial groups. It was in this spirit

that it resolved to acquire Banco Fonsecas & Burnay marking

BPI’s entry into the Commercial Banking arena, affording it a

substantial gain in size in preparation for the corporate

concentration process in the Portuguese financial system. It was

the Group’s overriding objective to guarantee the provision of the

complete range of financial services for companies and

individuals alike. An alliance was then forged with Banco Itaú,

initially through its equity participation in BFB. In 1994, this

interest was converted into a direct shareholding in BPI, following

which Banco Itaú became one of the key shareholders.

The Institution’s composition was reorganised in 1995: the

original BPI was transformed into an SGPS (holding company),

following which it was the only Group company listed on the

stock exchange, controlling Banco Fonsecas & Burnay and Banco

Português de Investimento, in the meantime formed through the

transfer of the assets and liabilities allocated to the business

activity traditionally conducted by this type of institution and

hitherto undertaken by BPI.

This reorganisation precipitated the specialisation of the Group’s

various units and was accompanied by an important

reinforcement of its shareholder structure with the entry of two

new strategic partners of considerable size to team up with the

Itaú Group: La Caja de Ahorros y Pensiones de Barcelona ("La

Caixa"), and the German insurance group Allianz.

A year later (in 1996) the acquisition of Banco de Fomento and

Banco Borges was the beginning of a process that would

culminate, two years later, with the creation of Banco BPI,

providing it with the largest single-brand banking network in

Portugal. Banco BPI was formed, in 1998, by the merging of

Banco Fonsecas & Burnay (BFB), Banco de Fomento e Exterior

(BFE) and Banco Borges & Irmão (BBI), to be joined later that

year by Banco Universo (an in-store bank), acquired in the

meantime. After the merger, the structure was significantly

simplified: BPI SGPS now comprises just two banking

institutions: Banco Português de Investimento, named BPI

–Investimentos, and a new commercial bank called Banco BPI.

12 Banco BPI | Annual Report 2002

Report | Historical milestones 13

The next three years – 1999 to 2001 – have confirmed BPI’s

potential for growth, modernisation and structural reinforcement

engendered by the 1998 merger: the Group has boosted market

shares in all the key areas of commercial banking, it has

expanded and streamlined its distribution structure, rapidly

transforming itself into a multi-channel bank, it has thoroughly

renovated its technological capability and built up one of the

financial system’s most dynamic brand names.

In 2002, BPI concluded an important internal reorganisation

programme that substantially altered its societary structure and

the manner in which it is governed. In essence, the programme

involved the centralisation of commercial banking at Banco BPI,

while the investment bank focused on its natural business

vocation. BPI SGPS incorporated Banco BPI and, simultaneously,

assumed the core business mission of a commercial bank,

adopting the name Banco BPI and in simultaneous assuming the

role as the entity at the Group’s helm. These alterations endowed

BPI with a simplified legal configuration, more attuned to its

present business model: it will enable BPI to secure cost savings

and efficiency gains in the Group’s functioning over the next few

years.

In parallel, BPI intensified the programme – permanently being

implemented – aimed at the rationalisation, rejuvenation and

qualification of its human resources, with the overriding object of

equipping the Bank with a staff structure that is properly

dimensioned and armed with the essential skills required for it to

affirm the objectives that form the basis for the Bank’s future

programme: efficiency, quality and service.

Total assets plus disintermediation (left-hand scale)Stock market capitalisation (right-hand scale)

Growth through asset consolidation

30 000

22 500

15 000

7 500

081

Chart 1

3 000

2 250

1 500

750

0

M.€

82 83 84 0185 86 87 88 89 90 91 92 93 94 95 96 97 98 99

M.€

00 02

The identity of BPI

14 Banco BPI | Annual Report 2002

A company is just like a person: it has its own identity and personality, it stands out for its character, its

principles, its way of doing, its objectives.

Banco BPI’s identity is marked by the financial and business culture of Banco Português de Investimento. The

essential traits of this culture are management independence, organisational flexibility, team work, recognition of

merit, the ability to anticipate, strict management of risks and the secure creation of value.

Earning a just return from the Bank’s business operations through the adoption of superior management and

service practices constitutes a fundamental goal of our activity. The safeguarding of Customer interests, with

dedication, loyalty and confidentiality, is one the core principles of the business ethics and code of conduct

assumed by the Bank’s Employees.

An institution’s personality asserts itself through its own attributes, which gain consistency and credibility in its

daily interaction with Customers and the community. In particular, BPI values two of these attributes: Experience

and Harmony.

Experience is the reflection of the training undergone by our teams and the important professional capital

accumulated during the history of each one of the institutions which gave rise to the Bank. It translates itself

into the dimension of our commercial presence, the soundness of our financial indicators, the security of our

growth and in our proven ability to achieve and lead.

We wish to combine Experience with Harmony, which expresses the permanent ambition of serving our

Customers and the community with the highest standards of ethics and quality. It is a projected aspiration for

the future, always open-ended, imposed by the constant desire to refine so that we do better. It is our most

challenging mission that, in the final analysis, justifies all others.

Report | The identity of BPI and the BPI brand 15

The BPI brand

In 2002, BPI Brand maintained its third place in the ranking

of Portuguese banking brands according to the «spontaneous

awareness» indicator included in the Estudo Base sobre o

Sistema Financeiro (Basef) published by the independent

company Marktest. This result is confirmed by the Bank’s

own polls and by the Publivaga polls carried out by Marktest

which assess the impact of advertising campaigns conducted

during the course of the year.

Notoriety

The results achieved enabled BPI to realise (for the third

consecutive year) one of the principal objectives of its

brand-management policy: to be situated amongst the top

three places in the spontaneous awareness (top-of-mind

reference) category. The BPI brand strengthened slightly in

absolute terms and improved vis-à-vis the second and

fourth-ranked banks. Accordingly, this performance confirms

the consistent improvement in this domain in a year marked

once again by a significant decrease in advertising

expenditure. In comparison with the preceding financial

year, BPI reduced its advertising spend by two thirds, falling

from fifth to seventh place in the table of financial sector

advertisers.

Efficiency

According to data supplied by Publivaga, the only

multimedia campaign conducted by the Bank in 2002 –

BPI Automóvel,– attained high spontaneous and proven

recollection levels. The same source places the Bank in the

number one position in the 2002 classification for proven

recollection in Television advertising, and second in terms of

total spontaneous recollection taking into consideration all

media channels. Besides the high degree of efficacy

mirrored in these indices, BPI once again presented the

best efficiency index for advertising investment within the

financial system, as expressed by the relationship between

the amount of space bought at market prices and the

recollection level attained.

Satisfaction

On another plane, very positive results were obtained in the

surveys carried out by the bank and by independent entities

covering the trend in service quality, a crucial benchmark in

brand positioning strategy. In this arena, BPI secured top place

amongst the largest banks in the National Index of Customer

Satisfaction, which was based on a poll conducted in the last

quarter of 2002. This annual index, which has been built up

regularly since 1999, is founded on an European wide model

and is managed by two international organisations – the

European Foundation for Quality Management and the European

Organization for Quality. In Portugal, the index is compiled by a

partnership of entities independent from the financial sector,

involving the Instituto Português da Qualidade (Portuguese

Quality Institute), the Associação Portuguesa para a Qualidade

(Portuguese Association for Quality) and Instituto Superior de

Estatística (Higher Institute for Statistics) and the Universidade

Nova de Lisboa’s Information Management Centre.

16 Banco BPI | Annual Report 2002

Corporate governance at the BPI Group

At the end of 2002, the BPI Group concluded an important

process of internal reorganisation, the principal aims of

which were simplifying the legal structure and streamlining

its governance model. BPI’s principles, policies and practices

relating to the set of issues associated with the manner in

which it is managed and supervised are described in the

section dealing with the BPI Group’s corporate governance,

which is presented as an annex1 to the Management Board’s

Report.

Corporate and management reorganisation

In December 2002, the BPI Group finalised an extensive

internal reorganisation programme that essentially involved

the following facets.

– the concentration at Banco BPI and Banco Português de

Investimento of typical commercial and investment

banking activities, respectively. With this end in mind,

certain specific business areas were incorporated into

these banks’ structures, entailing the consequent

extinction of the companies which had hitherto conducted

the aforementioned business activities.

– Banco BPI’s positioning at the head of the Group (Banco

BPI was incorporated by BPI SGPS which simultaneously

assumed the business object of a commercial bank and

adopted the name Banco BPI).

– the creation, modification and closing down of a

considerable number of divisions, with the consequent

redistribution of areas of responsibility and the change in

the directors and managers attached to these.

Report on the BPI Group’s corporate governance

The set of practices and guiding principles – whose

application ensures a diligent, efficacious and balanced

management of the interests of the company and of all its

shareholders – is described in the Report on the BPI Group’s

corporate governance. In this regard, we highlight:

– the equilibrium in the management body between the

number of directors representing key shareholders, the

number of independent non-executive directors and the

number of executive directors;

– the binding observance by members of management bodies

and Employees of the Group’s various companies of a set

of internal rules which, in certain cases, are more onerous

than those imposed by law and professional associations;

– the existence since 1999 of an Internal Control

Committee, which is composed of members with non-

-executive functions, reinforces its independence and the

effective compliance with its objectives;

– the functioning since 1993 of a structure dedicated

exclusively to relations with investors and the market.

Insofar as shareholder participation in the company’s affairs

is concerned and, more specifically, the exercise of voting

rights, BPI consistently pursues information dissemination

practices which are aimed at stimulating shareholder

participation by means of the ample disclosure (by post,

electronic mail and the Internet) of the holding of general

meetings, the matters to be dealt with and the different ways

of exercising votes.

1) See pages 201 to 222.

Report | Corporate governance at the BPI Group 17

Within the ambit of BPI’s Corporate Governance practices, it

is also worth noting:

– the provision of detailed information about the policy and

remuneration paid to the members of Banco BPI’s

Management Board, including the stock incentive and

option programmes for Executive Directors and Employees;

– the existence of an institutional website (www.bpi.pt),

where information supplied to the market by BPI is

permanently available in Portuguese and English (press

releases, report and accounts, presentations etc.), and

specific information about events of paramount importance

for shareholders, such as the preparatory documents for

general meetings, important data relating share capital

increases or dividend payments.

Public recognition

Within the ambit of the XVth edition of the awards for the

best annual reports published by companies listed on the

Portuguese stock exchange, BPI was distinguished in 2002

with the prize for the best financial sector annual report (for

the seventh time) and the prize – created for the first time –

for the best report covering Corporate Governance amongst

all the companies listed on Euronext Lisbon. These awards

constitute unequivocal public acknowledgement of the

exhaustive and all-embracing manner in which BPI transmits

information to the market addressing not only financial and

management aspects, but also the way in which it is

governed and controlled.

18 Banco BPI | Annual Report 2002

Social investment

CULTURE, RESEARCH, EDUCATION AND SOCIAL SOLIDARITY

In the 2002 financial year, patronage in the cultural,

education, research and social solidarity fields continued to

receive the BPI Group’s attention in projects and initiatives

which showed themselves to be properly structured and of

undoubted merit.

In the cultural arena, the BPI Group renewed the Protocol

signed with the Serralves Foundation and continued to lend

support to the following Foundations: António de Almeida;

Eugénio de Andrade, Júlio Resende, Luís Miguel Nava and

Maria Isabel Guerra Junqueiro.

The protocol with the Calouste Gulbenkian Foundation providing

support for the cycle of "Great World Orchestras" was also

renewed. Of particular significance was the participation involving

the concerts promoted by the Fundations Casa de Mateus and

Casas de Fronteira and Alorna, as well as those which took place

at the Associação Cultural Monte de Fralães and the Oporto

Musical Culture Circle. Also worth noting was the sponsorship

forthcoming since 1998 of the Oporto Internal Music Contest.

Still in the cultural field, the highlights included the

acquisition and placing of the work by Pedro Calapez, offered

by the BPI Group to the Jerónimos Monastery, the purchase of

a tiled panel conceived by José de Guimarães, destined for the

Deutsche Oper station in Berlin, and the support for the

exhibition of paintings by Francisco Laranjo.

Giving continuity to BPI’s sponsorship of the collection of books

on the work of Portuguese artists, a book was published entitled

"Mário Botas – o pintor e o mito", an anthology of the artist’s

works. Assistance was also given to the publication of the book

"Domingo de Manhã" with photographs by Jorge Henriques.

The Centro Nacional de Cultura (National Culture Centre) was

the recipeint of the BPI Group’s patronage for the publication

of the book "Pensar o Milénio com Edgar Morin", as well as for

the Associação Amigos de Yehudi Menuhin Portugal.

Support continued to be granted to Cultur Porto – Associação

de Produção Cultural; Associação Comercial do Porto, for the

publication of "O Tripeiro"; Associação da Casa Museu Abel

Salazar; Ateneu Comercial do Porto; Centro Social Cultural e

Recreativo Abel Varzim; CRAT-Centro Regional de Artes

Tradicionais, of the Oporto Municipal Council; Associação

Divulgadora da Vida e Obra de Teixeira de Pascoaes – Marãnus.

In the learning and research areas, the Group continued to

dispense support for institutions of acknowledged merit, with

special emphasis on the Oporto and Coimbra Universities, the

Universidade Católica Portuguesa in both Oporto and Lisbon

and the Universidade Técnica de Lisboa. BPI once again

sponsored the magazine for past students – "Uporto". Also

sponsored were the exhibition of Dr.ª Beatriz Gentil at the Fine

Arts Faculty and the publication of the book paying homage to

Professor Edgar Cardoso at the Engineering Faculty.

At the Coimbra University the Group continued to sponsor the

Teixeira Ribeiro Prize, the creation of the research institute Jus

Gentium Conimbrigae and the participation in the activities of

the Instituto de Direito Bancário, Bolsa e Seguros.

As in previous years, the BPI Group was also heavily involved

at the Catholic University, above all in the creation of the

Universidade Católica Portuguesa Foundation with a

commitment to continued backing until 2011.

Report | Social investment 19

Support was also received by AR.CO Centro de Arte &

Comunicação Visual; CITEX Centro de Formação Profissional da

Indústria Textil and Colégio Universitário de Montes Claros.

In the social solidarity area, assistance was given to the Banco

Alimentar contra a Fome (Anti-hunger food bank), to Abraço, to

ASAS, to Cerci, to Clube Stress, to Liga dos Amigos das

Crianças do Hospital Maria Pia, to Liga Portuguesa Contra o

Cancro, to Fundação Pro Dignitate and to União das

Misericórdias Portuguesas.

Through the auspices of Banco de Fomento in Angola, a

partnership accord was forged to give aid to the activities

envisaged under the "Projecto de Alfabetização para Crianças,

Jovens e Mulheres na Província de Kuanza Norte" (a project

promoting literacy amongst children, adolescents and women

in the province of Kuanza Norte).

Still in Angola, Banco de Fomento contributed on the basis of

the protocol established with the Ministério da Assistência e

Reinserção Social, for the financial effort made towards the

peace process.

In the same manner, another important initiative was the

participation in the campaign "Vencer a Fome, Consolidar a

Paz – Angola 2002" (Conquering Hunger, Peace Consolidation

– Angola 2002) which the Fundação Pro Dignitate conducted

in that country.

Substantial assistance was once again given to Mozambique

through the Presidência da República (the Republic’s Presidency)

and the Comissão Especial de Ajuda Humanitária a Moçambique

(Special Commission for Humanitarian Aid to Mozambique).

Banco BPI continued to support the activities of the Fundação

Portugal África (Portugal-Africa Foundation), of which it is the

principal founder. 2002 will be remembered as the year in

which the foundation’s new headquarters were inaugurated.

This event inspired BPI to donate the works of art and

furnishings which adorn the workplace and exhibition areas, as

well as an important collection of documents dealing with the

theme Economic Development. Moreover, the Bank offered the

services of four of its Employees, which is equivalent to an

annual contribution of around EUR 250 000.

The programme of the Fundação Portugal África’s activities for

2002 included initiatives such as reactivating the teaching of

arts and crafts in Mozambique, the Programa de

Desenvolvimento Agrário Integrado da Região do Chóckwè (an

integrated agrarian development programme for the Chóchuè

region), the projects Observatório de África and Diáspora

Africana, the database project Memória de África, the

dissemination of an AIDS prevention programme and the

scheme supporting small investment projects in Cape Verde.

An important contribution was also made to the project aimed

at teaching Portuguese in the Diocese de Baucau (Timor).

Also in the domain of social solidarity, support was given to the

Diplomatic Corps Bazaar with the high patronage of the

Republic’s Presidency.

20 Banco BPI | Annual Report 2002

Financial structure and business

The BPI Group – headed by Banco BPI – is a universal

financial and mutli-specialist group, focusing predominantly

on commercial banking business and on domestic activity, to

which are allocated 94% of its capital.

Banco BPI serves more than 1.3 million Customers –

individuals, companies and institutions – by means of a

multichannel distribution network comprising approximately

500 retail branches, a homebanking service (BPI Net),

telephone banking (BPI Directo), specialist branches and

structures dedicated to the corporate and institutional

segment.

Banco Português de Investimento, the BPI Group’s original

matrix, is engaged in investment banking business –

Equities, Corporate Finance and Private Banking – in which

BPI occupies a leading position. Private Equity business is

conducted through a subsidiary company (84% controlled).

In asset management activity, BPI is a prime player in the

management of unit trust (mutual) funds, pension funds and

life-capitalisation insurance.

International commercial banking business (which accounts

for 6% of allotted capital) is essentially carried out by Banco

de Fomento Angola and Banco de Fomento Mozambique.

In the insurance sector, BPI operates in partnership with

Allianz through a 35% stake in Allianz Portugal, as well as

via an insurance distribution agreement covering the Bank’s

commercial network. BPI also owns a 50% interest in a

credit insurance company.

Asset Management Private EquityInvestment Banking

Banco BPI

InternationalCommercial banking

Insurance

Banco BPICayman 100%

Banco Portuguêsde Investimento 100%

Domestic Commercial Bankingand financial investments

Banco de FomentoAngola 100%

Banco de FomentoMozambique 100%

Banc Post17%

BPI Fundos100%

BPI Pensões100%

BPI Vida100%

Inter-Risco84%

Allianz Portugal35%

Cosec50%

Main units of the BPI Group1

1) Effective direct / indirect participations. Figure 3

Report | Financial structure and business and distribution channels 21

Distribution channels

Physical network

Remote channels

Clients

Corporate Banking, Institutional Banking and Project FinanceIndividuals Banking and Small Businesses

BPI distribution channels in mailand Portugal

Turnover betweenEUR 1.25 million andEUR 25 million

Turnover aboveEUR 25 million

Wholesale

Traditional branches 483

Housing areas 64

BPI Net areas 228

In-store 13

70 biggest businessgroups

Large companies Medium-sizedcompanies

Investment centres 3

Housing shops 18

Automatic branches 47

Automatic Bank (ATM) 1 007

1) Local authorities, autonomous regions, social security system, universities, public utility associations and other non-profit entities.

Banco Electrónico BPI

BPI Net empresaswww.bpinetempresas.pt

Project Finance Institutional1

Wholesalecentres

Medium-sizedcompanies centres

Largecompanies centres

4 7 44

ProjectFinance centres

Institutionalcentres

1 5

Turnover belowEUR 2.5 million

Individuals Small Businesses

BPI Directo (telephone banking)808 200 500

350 thousand subscribers

BPI Net (homebanking)www.bpinet.pt

350 thousand subscribers

BPI Imobiliáriowww.bpiimobiliario.pt

200 th. real estate properties announced

BPI Online (brokerage)www.bpionline.pt

12 largest world-wide markets

Banks

Representativeoffices

Overseas branches

Overseas distribution network

Investment BankingCommercial Banking

Santiago de Compostela

Madrid

BPI Suisse (Private Banking)

Paris (9 branches)

Madrid

S.ta Maria – Azores (offshore branch)

Funchal – Madeira (offshore branch)

Paris

Geneva

Hambourg

Newark

Caracas

Johannesbourg

Banco de Fomento, SARL (17 branches)Angola

Banco de Fomento, SARL (7 branches)Mozambique

Banco BPI Cayman

Banc Post1

1) 17% shareholding.2) Distribution agreements with banks or post offices (marked with a *) and agent networks.

Distribution agreements2

Canada (Montreal banc)*

Luxembourg*

Belgium*

Sweden*

United Kingdom*

Australia

Brazil

The Netherlands

Figure 4

22 Banco BPI | Annual Report 2002

Human resources

RATIONALISATION, REJUVENATION AND QUALIFICATION

The BPI Group’s human resources policy remained

concentrated on the execution of the strategic programme

directed at cost reduction and efficiency enhancement for

the three-year period 2002-2004. The implementation of

rationalisation, rejuvenation and qualification measures

contributed decisively to the continued and gradual

qualitative improvement in human resources.

The internal reorganisation carried out by BPI during 2002

with the aim of simplifying and boosting the flexibility of its

organisation whilst at the same time reducing its operating

costs, involved the redistribution of the areas of

responsibility and changes in the directors and managers

associated therewith that resulted in a net reduction of 30

Employees (22%) with top management functions.

At the end of 2002, the BPI Group’s workforce numbered

7 007 in Portugal and a total of 7 576, of whom 6 583

were employed at BPI, 200 at the investment bank and 224

at various subsidiary companies, while 569 were deployed in

overseas operations.

1) Includes limited-term contracts and temporary employment of people having no binding work contracts. Note: at 31 December 2000, 2001 and 2002 the number of Employees with limited-term contracts in Portugal stood at 570, 569 and 359, respectively, while in the same years the corresponding numbers relating to overseas activity were 23, 22 and 15. On the other hand, there were 166 people working on a temporary basis in December 2000, 111 in December 2001and 46 in December 2002.

2) Activity with non residents, namely, emigrant communities; includes branches in France and Spain and representative offices. 3) Banco de Fomento Angola and Banco de Fomento Mozambique.

BPI Group Employees1

Period average figures

2002 ∆% 01 / 0220012000

End-of-period figures

Dec 2002 ∆% 01 / 02Dec 2001Dec 2000

Banco BPI 7 035 6 699 6 583 (1.7%) 7 187 6 958 6 494 (6.6%)

Banco Português de Investimento 427 453 200 (55.8%) 398 444 433 (2.5%)

Other subsidiary companies 459 450 224 (50.2%) 474 436 414 (5.0%)

Activity in Portugal 7 921 7 602 7 007 (7.8%) 8 059 7 838 7 345 (6.3%)

Overseas branches and representative offices2 160 163 162 (0.6%) 161 150 164 9.6%

Overseas banks3 278 341 407 19.4% 257 314 370 17.8%

Overseas activity 438 504 569 12.9% 417 464 534 15.2%

Total1 8 359 8 106 7 576 (6.5%) 8 476 8 302 7 879 5.1%

Table 2

BPI Group staff complementsNo.

10 000

9 000

8 000

7 000

6 000Chart 296 98 00 01 02

Activity abroadActivity inPortugal

97 99

8 995

8 123

7 695

8 2398 359

8 106

7 576

Report | Human resources 23

BANCO BPI

The human resources policy adopted – bearing in mind that

the banking sector is associated with more demanding

quality standards and where competitiveness is ever

increasing – had as its chief goal securing productivity gains.

Following the organisational restructuring concluded in

2002, of the 6 583 Employees working at Banco BPI �

at the end of 2002, 4 605 were integrated in commercial

activity and 1 978 in central services.

Of the 385 integrated into Banco BPI by reason of merger or

demerger, at the close of 2002 379 were attached to areas

included in "central services".

The thrust to attain the goal of enhancing productivity and

competitiveness levels led to the recruitment of 153

Employees – the vast majority with higher academic

qualifications –, at the same time providing a strong

incentive for internal mobility amongst personnel.

On the other hand, 500 Employees with an average age of

56.0 years left the company’s employment owing to early

retirement, pre-retirement or the attainment of retirement

age. These Employees had worked in the banking sector for

an average of 33 years, while their academic background

was largely primary or secondary schooling.

1) Telephone Banking, Internet, Protocol Banking and Automated Banking.

2) Cards, mortgage loan finance (which includes 18 housing shops), personalloans and motor car finance.

Note i: the criterion used for classifying Employees by operational areas wasaltered. In terms of the new classification system, in addition to personnelattached to the branch network and the corporate centres (previousconcept of the commercial network), Employees allocated to the non--traditional channels, product factories and marketing are now consideredto be deployed in commercial activity. According to the previous criterion,the number of commercial network Employees dropped from 3 848 to 3 697, while the number of central services Employees rose from 2 851 to2 886.

Note ii: does not include overseas activity.Note iii: includes temporary workers: 149 in 2000, 92 in 2001 and 43 in 2002.

Retail branches and corporate centres network 3 697 57Non-traditional channels1 296 4Products factories2 519 8Marketing 93 1Central services 1 978 30

Banco BPI Staff ComplementDistribution by area of activity

Chart 3

Commercial activity (70%)4 605

Central services (30%)1 978

Areas 2002 %

Banco BPI staffcomplementUniversity degree andaverage age1

%

50

40

30

20

10Chart 498 99 00 01 02

50

45

40

35

30

1) Figures adjusted by thenumber of years elapsedbetween each year and2002.

Staff with universitydegree as a % of total(left-hand scale)Average age1

(right-hand scale)

47.045.3

43.742.5

40.5

22%25%

28%

32%35%

24 Banco BPI | Annual Report 2002

Training

In 2002, BPI continued to pay special attention to training

as a tool promoting the development of skills and the

consolidation of attitudes and behaviour.

In this context, the main initiatives involved training

programmes focusing on attendance, sales and sales teams

with the object of enhancing operating efficiency and raising

service standards. These courses were attended by all the

personnel attached to the individuals and small businesses

network, including branch managers (departmental heads).

A total of 3 036 people attended 258 training sessions which

extended over 72 400 hours. This programme is scheduled to

continue this year to cover newly-admitted staff and others

whose careers fall within this ambit.

Behavioural training was extended to other areas of the Bank,

with special emphasis placed on themes such as team

management, team work and telephone attendance, all of

which entailed an additional 2 200 training hours.

As part of the process to strengthen staffing at the individuals

network, three training bursaries were initiated. The 25-week

programme covers theoretical-practical classroom instruction,

complemented by on-the-job training. This programme, which

is expected to finish in the first quarter of 2003, embraces

74 university graduates and occupies 64 200 training hours.

In summary, 3 857 Employees (60% of the total workforce)

participated in training courses during 2002 in a total of

105 thousand training hours.

In order to foster the personal and professional advancement of

its Employees, Banco BPI pursued a policy of giving support to

staff taking courses that confer university degrees. In this

regard, BPI gave its support to 140 graduates and 40 post-

-graduate and masters degree candidates, principally in the

academic fields of business management and information

systems.

Banco BPI’s Employees – selected indicators

20022001

Employees 6 699 6 583

Higher education 31.8% 34.5%

Average age 41.5 40.5

Average period of service 16.1 15.4

Men 53.6% 52.8%

Women 46.4% 47.2%

Employees / Branch 6.0 6.2

Note 1: does not include automated branches and includes 3 investment centres.

Note 2: in 2002 includes 385 Employees integrated into Banco BPI by force of merger or demerger of the Group companies.

Table 3

This trend was responsible for the number of Employees with

higher educational training rising to 34.5% (28.4% in 2000

and 31.8% in 2001). It also had an important impact on the

individuals’ network, where personnel with academic training

rose to 26.5% and, despite the passage of yet another year,

the average age fell to 40.1.

Technology

BPI’s information systems are based on a multi-channel

architecture, robust and scalable, and on the full integration

of Web technology and corporate transaction platforms. The

Bank has its own information and transaction intranet,

universally available, which constitutes a common interface

for an increasingly significant number of internal and

business processes. The support for business management,

marketing and sales, and for the control and management of

processes, as well as the front-end, Customer relationship

management and financial management solutions, are

available in a technologically innovative form that is

integrated with the traditional applications. High levels of

performance and robustness are central objectives in the

design and maintenance of the information systems,

translating themselves in this fashion into significant

efficiency and availability indices.

Report | Technology 25

Principal indicators of efficiency, availability and performance

Processing capacity (mainframe) 610 MIPS

Storage capacity (in Terabytes) 15.4 Tb

PCs per Employee 1.2

Employees with access to Intranet and e-mail 100%

Number of processes "intranetised" 62%

Page views in the Intranet 330 000 / day

Availability of transaction sites 99.8%

Employees with access to the Internet 20%

Page views in the Internet (all BPI sites) 33 500 / day

Branches: opening before 8h30 99.2%

Real-time Cards: from 7h00 till 4h00 100%

Response time to transactions at the branches 99.85% less than 3 seconds

Transactions on the multi-channel platform 200 000 / day

Technological help desk: resolution of problems 98% less than 2 hours

Table 4

26 Banco BPI | Annual Report 2002

Activity in the information systems’ areas during 2002

revolved around five main aspects:

Support for business and sales

The core objective of BPI’s information systems is to provide

a response to business needs. Amongst the priorities of

2002, the most noteworthy were the ongoing development of

sales-support solutions, namely, making available more

integrated information about Customers and products; the

upgrading and optimisation of management-decision

systems, the response to the needs stemming from Corporate

Banking’s new organisation and the evolution noted in the

operating applications solutions designed to handle and

control national and international payments.

Availability of structural solutions

Of the work embarked on in 2001 which extended into

2002, mention is made of the entry into service of a new

multi-channel platform at Telephone Banking (BPI Directo)

and at Online Banking (BPI Net, Individuals and

Companies), the development of the Group’s SIP project –

Sistema de Informação de Pessoas (People Information

System) – and the new global interface and operations

storage model, Operational Data Store, which involves all the

Group’s operational applications (in other words, information

factories).

Security

Special attention was paid during the year to the further

evolvement and consolidation of the disaster recovery project

and business continuity, as well as the revision and

implementation of internal control mechanisms for the use of

computer-based resources and the launch of the GAS project

– Gestão de Acessos e Segurança (Access and Security

Management).

Enhanced internal efficiency

Work continued on the projects aimed at the implementation

and consolidation of the IT rationalisation programmes and

the reorganisation of the in-house teams.

The BPI Group’s restructuring

The operating reorganisation that involved several business

areas, but in special the merger of companies into the

Group’s banks entailed a considerable adjustment of

informative systems supporting those business.

BUSINESS AND SALES SUPPORT

Opportunities Server

The Opportunities Server, one of the chief pillars supporting

the Bank’s commercial activities and functioning since

2000, was the object of major improvements in 2002 as

regards the information about Customers and products, as

well as the functionalities available, in particular, with

respect to the integration and updating of opportunities.

Report | Technology 27

Opportunities Server

Centred on the Customer, the Opportunities Server is a system

designed to support and manage the Bank’s commercial

activity, from the standpoint of both the networks and the

direct channels. More than 1 million contacts originated by the

Opportunities Server were made in 2002.

The Opportunities Server is built on a database organised

according to the products and services which are considered to

constitute Customer sales opportunities. The system also

functions as a tool for managing contacts, controlling

commercial activity and providing general backing in dealings

with Customers. The principal focus is on Customer retention,

service quality and fostering existing Customer relations,

although it also acts as an instrument for managing contacts

with potential Customers.

The Opportunities Server essentially provides information

stored in the data warehouse about products, services,

transactions and Customer profiles. Data mining of this

information is effected and automatic business rules defined

that result in the identification of opportunities.

This information is accessed via the intranet, enabling the

selection of Customers for the execution of commercial action,

recording the results and controlling the effect of sales

campaigns and activities.

On the other side, the Opportunities Server is a source and

means of controlling the results of all direct marketing and

telemarketing activity.

Data warehouseData Mining(Marketing)

Opportunities detectedby the network

Products (Cards,Loans, Funds,...)

Channels (Net,Directo, Branches,...)

Business ProcessManagers

SimulatorsCustomer requests

Automatic rulesUser defined rules

Opportunities Base

Selection of opportunities by the userOpportunity

Operations transaction(Intranet, Internet, Call-center, ATM)

Sales force management

Search instigated bySalesperson

(via any network)

Search instigated byCustomer

(via any channel)

Search instigated byMarketing

(for any product / service)

Campaign managementOpportunities

Contacts management

Figure 5

The integrated attendance solutions for special Customer

segments – Private Banking and Institutional Clients –

benefited from developments in the field of analysis and

negotiation. These areas can now count upon platforms that

integrate all the information flowing from the relationship

with the Bank: ranging from operations to contacts,

including the respective dealings. The operating and support

systems for discretionary portfolio management and

monitoring, were also subjected to a series of improvements.

Management of business processes

The support systems for management decisions benefited in

2002 from important developments: the efficiency and

quality of the processes were improved and control boosted,

while operations have become more standardised and

simplified. In parallel, new applications models were

launched.

GPC Home loans

BPI’s pioneer module in the area of process managers (GPC)

was the target of numerous interventions with the object of

simplifying and optimising the relevant circuits, tasks and

procedures. The application was also adapted from a legal

and commercial perspective, and the interfaces with the

operational systems optimised. The alterations introduced

paved the way for costs to be reduced, internal productivity

raised and the quality of service offered to Customers

enhanced.

In 2002, the three modules described below were made

available.

GPC Personal loans

This module is designed to handle all the non-mortgage

credit on offer to individuals, whether Customers or non-

-Customers. It integrates a specific internal scoring module

and interacts directly with central applications, thereby

permitting the management of the whole process, starting

from simulation right through to the release of funds.

GPC Motor car finance

This application was developed with the aim of handling all

motor-car financing processes, both in partnerships (via

extranet) and at all the internal networks. The simulation /

/ decision component for ALD (long-term rental), Leasing and

Credit entered into service. This is a system integrated with

the Bank’s various business partners, incorporating the

unique characteristics of the respective brands and products,

as well as the existing bilateral agreements. The next stages

being developed seek to implement the handling of

proposals right through to contracting, the integration into

the operational systems and the extension to the other

channels.

GPC Cards

Designed to handle the capture of the entire range of BPI

credit cards (personal and corporate), it is characterised by

the large volume of processes handled. This constitutes an

additional challenge in the implementation of the IT

solution, since it entails the incorporation of automatic

decision criteria and specially-prepared channelling filters.

28 Banco BPI | Annual Report 2002

Report | Technology 29

Loans process management

GPC is a system that administers the entire lending process,

from the first contact by the Customer right through to the

signing of the respective operation, including the simulation,

sale, decision, operating tasks contracting, registrations and

overall control.

This is a completely Web-based, multi-channel system,

integrated with the other operational systems, available on the

Bank’s intranet, accessible by Customers on the Internet and

on the extranet for the entities with whom the Bank possesses

credit agreements, at the point of sale.

The infrastructure created is global. The aim is that all the

loan products are handled by this system so as to create a

common repository for operations, rules for decisions, business

and credit control. In the case of standard products

(consumption, cards, housing, motor car), the objective is that

loan decisions be taken in real time, at the moment when the

operation is initiated.

The computerised implementation of these concepts

presupposes a comprehensive review of the business processes

and the ex-ante conceptualisation of all the decision rules,

elements and flows. This represents an even more complex

challenge than the actual implementation of the technological

solution itself.

At the present time, the modules in service are those relating

to Housing (since 2000 and the object of permanent upgrades

and new functionalities), Consumption, Cards and Motor Car

(these launched during 2002). The strategy followed since the

conception of the GPC has been confirmed to the extent that

superior efficiency and quality, added control, cost reduction,

operating standardisation and simplification are assured.

The widespread application of this concept to Companies and

Small Businesses was the object of analysis, taking into

account the specific nature of these segments. 2002 also saw

the implementation of the first system that will permit this

model’s start-up: the Limits Management application.

People informationSystem

Data warehouse

Simulation /Application

Decision(+Scoring)

Proposal Final decision Contracting Post contracting

Simulations Loan Process Management Link to Operations

Opportunities Server

Information for Management

CustomersAccounts

LoansInsurance

Security / guaranteesReal estate

House loans

Personal loans

Motor carfinance

Credit cards

Intranet

Internet

Extranet

Other

Figure 6

Business support solutions for companies

Several IT projects were developed with the aim of making

available an application architecture integrating risk analysis

and the management of information, thereby making the

loan-decision process more flexible and improving control,

the monitoring of operations and the interaction with

Customers.

Groups of companies

This module allows defining and managing groups of

companies, since it is capable of representing various types

of associations and relationships with the attributes and

specific features of each situation.

Credit limits

This system permits the recording of approved limits

according to the class of risk relating to groups and entities,

the use and control at the various levels for complying with

the internal rules of the general credit regulations, the

gathering of utilisation proposals and the implementation of

the decision workflow, operational control and routing. It

stores the commercial information of the Groups and

Companies, and is interconnected to the document

management and Customer information system.

Information management

Information aggregated by groups of entities has now become

available, namely, that relating to the status of integrated

involvement with the Bank, rating information and various

grades.

BPI Net Empresas

This is a new service provided via the Internet and directed

at Companies. It is currently in the final phase of quality

testing. The goal is to provide an access platform to the

Bank with a view to the execution of operations and

consultation. It integrates existing IT solutions at both

technological and applications levels.

Other business support solutions

The speed of execution and the capacity to control national

payment orders, namely, those received through the remote

channels, benefited from major IT application developments.

On the other side, the handling of international payment

orders has now become fully automated. This will permit

greater speed of execution, more rigour and security. These

objectives were similarly behind the optimisation of the

applications for processing documentary operations.

AVAILABILITY OF STRUCTURAL SOLUTIONS

Multi-channel platform

This is a new transaction-access platform for the Bank’s

systems through the various remote channels, which are now

more robust and scalable, and offering better performance.

The objective is, besides guaranteeing the technological

evolution of the infrastructural solutions, to ensure the

adaptation to the increased interactivity with Customers, not

only through the remote channels, but also in the future via

the traditional channels.

30 Banco BPI | Annual Report 2002

Report | Technology 31

Multi-channel platform

Objectives

Banco BPI has had a single platform for the remote access,

call centre and BPI NET channels since February 2000. The

choice of this platform resulted, amongst other factors, from

the need to respond in a short period of time to the need to

boost the bank’s traditional business through the medium of

non-conventional channels.

According to the strategy for the evolution of the technological

infrastructures, it was decided to design and implement a

solution based on a new architecture that is more robust,

scalable and with a better performance capability. At the same

time, it had to ensure adaptation to the growth in Customers’

contacts with the Bank via all the remote channels and branch

network. The first phase of the integration of the remote

channels was concluded with success. The prototype that will

lead to the complete integration of the branch solution into the

multi-channel platform is presently being implemented.

Features

It is a platform which aggregates the operations flowing from

the various distribution channels. It functions as a go-between

the front ends and the operational applications. This new

solution’s main characteristics are the recording of the

operations originating from the various channels, the validation

of business rules, security in accessing information, extensive

availability, greater scalability and the modular architecture.

The new platform permits:

– responding more rapidly to business needs;

– obtaining an integrated vision of operations carried out with

Customers through the various channels;

– making available new functionalities without interrupting

service in the various channels.

Implementation plan

For security reasons and in order to minimise the impact on

existing solutions, a phased migration plan was formulated.

BPI Directo was the first channel to be integrated since it

constitutes the environment with the most control and can only

be accessed internally. Then followed the integration of BPI

Net (Individuals and Small Businesses) and the new channel

dedicated to companies: BPI Net Empresas.

Results

The new multi-channel platform has been providing superior

levels of efficiency, scalability and service, while preserving the

high standards of quality: in 2002, the number of transactions

per second achieved was 100% more than the previous year’s

figure, with a total daily volume in the order of 200 thousand

transactions being recorded.

Partners

Microsoft was the key partner in the platform’s design and

implementation, as was the case in other projects involving

Banco BPI’s technological infrastructure.

Call-center

12 August2002

BPI NetIndividualsand SmallBusinesses

30 November2002

BPI NetCompanies

February2003

Prototypeof the NewBranchPlatform

April2003

Figure 7

32 Banco BPI | Annual Report 2002

Data warehouse

BPI’s data warehouse is founded on a number of structured,

coherent and integrated databases, updated daily, and which

brings together the information relating to the characteristics

and flows of all the products and all the data relating to

Customers.

All this information is then made available on the various

channels. In this fashion, it is possible to analyse the

information from both a static and time span perspective when

the approach is made according to Customer, channels,

products or transactions.

This information can be accessed in three ways:

– the web pages on the Intranet permit permanent consultation

of reports, which are thus available to all Employees,

although different access levels have naturally been

established;

– the tools for exploring information, data mining or the

production of reports, are available to specialised users,

namely, from the marketing and planning areas;

– contribution of information for the other application solutions

with special functions, amongst which we highlight the

applications for analysing profitability and risk, and the

applications for producing official reports.

Amongst the Intranet pages that are permanently available, the

following are worth noting: