baltic tigers facing the middle-income trap? · ernests bordāns, madis teinemaa 1 bachelor thesis...

TRANSCRIPT

Ernests Bordāns, Madis Teinemaa

1

Bachelor Thesis

Baltic Tigers Facing the Middle-Income Trap?

Authors:

Ernests Bordāns

Madis Teinemaa

Supervisor:

Oļegs Krasnopjorovs

May 2016

Riga

Ernests Bordāns, Madis Teinemaa

2

Table of Contents

Abstract ................................................................................................................................................... 4

1. Introduction .................................................................................................................................... 5

Research Questions ........................................................................................................................ 6

2. Literature Review ............................................................................................................................ 7

2.1. Theory of MIT ........................................................................................................................... 7

2.2. Middle income level definition in the literature ...................................................................... 8

2.3. Middle income trap definition in the literature ..................................................................... 10

2.4. Literature on MIT determinants ............................................................................................ 13

3. Methodology ................................................................................................................................. 14

3.1 Our MIT Definition ...................................................................................................................... 14

3.1.1. Setting the middle income level ......................................................................................... 15

3.1.2 Choosing the “trap” criteria ................................................................................................. 15

3.1.3 Other characteristics of our definition ................................................................................. 17

3.2 Estimating the MIT determinants and probability of MIT .......................................................... 18

3.2.1. Multivariate logistic panel data regressions ....................................................................... 18

3.2.2. Choosing the control variables ..................................................................................... 18

3.2.3. Fitting the model(s) ....................................................................................................... 19

3.2.4. Individual exogenous factors analysis ........................................................................... 21

3.3. Data description ......................................................................................................................... 21

4. Empirical results ................................................................................................................................ 23

4.1. Findings of the MIT .................................................................................................................... 23

4.2. Results of regression models with exogenous MIT probability determinants .......................... 28

4.2.1. Macroeconomic environment ............................................................................................ 28

4.2.2. Development ....................................................................................................................... 30

4.2.3. Governance ......................................................................................................................... 32

4.3. MIT predictions for Baltics ......................................................................................................... 35

5. Discussion of Results ......................................................................................................................... 38

5.1 Predicted probability for the Baltic States .................................................................................. 38

5.2. Performance of the Baltics in the context of previous literature MIT definitions ..................... 39

5.3. Discussion of key determinants of MIT: relevance for the Baltics ............................................. 41

5.3.1. Income level ........................................................................................................................ 41

5.3.2. Macro stability .................................................................................................................... 41

5.3.3. Competitiveness.................................................................................................................. 42

5.3.4. Economic structure ............................................................................................................. 43

5.3.5. Human capital ..................................................................................................................... 43

Ernests Bordāns, Madis Teinemaa

3

5.3.6. Income inequality ............................................................................................................... 44

5.3.7. Public sector performance .................................................................................................. 44

5.3.8. Corruption ........................................................................................................................... 45

6. Conclusions ....................................................................................................................................... 46

7. Reference list .................................................................................................................................... 48

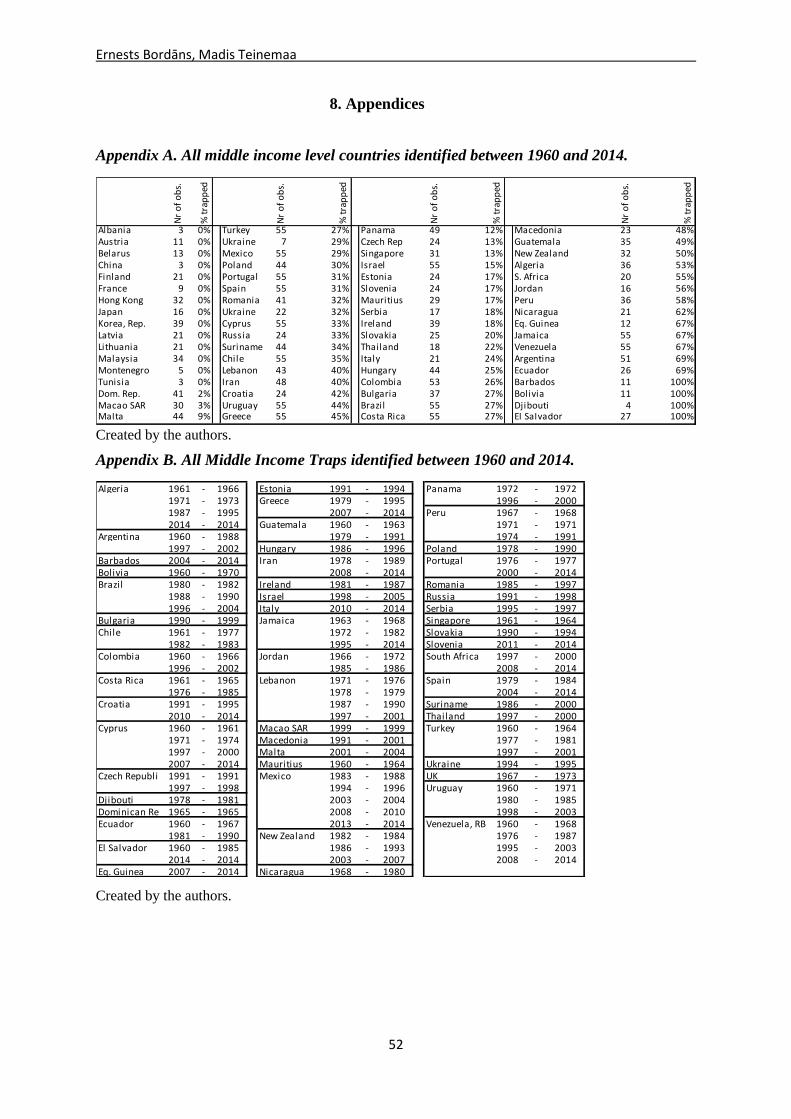

8. Appendices ........................................................................................................................................ 52

Appendix A. All middle income level countries identified between 1960 and 2014. ........................ 52

Appendix B. All Middle Income Traps identified between 1960 and 2014. ...................................... 52

Appendix C. Prediction models ......................................................................................................... 53

Appendix D. Cross-correlation table of the main prediction model. ................................................. 54

Appendix E. Example of individual regressions. ................................................................................ 54

Appendix F. Estimated MIT probabilities using the main prediction model for all countries in

specific year. ..................................................................................................................................... 55

Appendix H. MIT predictions for Baltics with “HIC” and “MIC” scenario adjustments .................... 56

Appendix I. Predicted MIT probabilities for all countries in 2014. ................................................... 56

Appendix J. Data sources. ................................................................................................................. 57

Ernests Bordāns, Madis Teinemaa

4

Abstract

This paper studies the characteristics of middle income trap (MIT) and estimates the

probability of the Baltic Tigers facing it. We complement the existing literature in three ways.

First, we propose an original MIT definition considering major drawbacks of previous

researches and compiling unique country-specific benchmarks based on weighted average

income growth of trading partners. Second, we construct several multivariate panel data logit

models to study which economic, social and political factors could be associated with MIT.

Third, we are first to quantitatively assess the probability of the Baltic countries facing

MIT. Our results suggest the Baltic countries currently are not trapped since their GDP per

capita growth rate exceeds that of comparable middle-income countries, weighted average of

trading partners and the EU region; additionally, none of the existing literature’s MIT

definition suggests that any Baltic economy is trapped. Furthermore, the probability of them

facing a MIT is low (somewhat higher in Latvia and Lithuania than in Estonia), compared to

other European countries. However, MIT probability of the Baltic countries is likely to rise if

further income convergence with advanced countries will not be accompanied with structural

reforms. We find that quality of public institutions (especially government effectiveness and

control of corruption), business-friendly regulations, income equality, stable macroeconomic

environment, prudent fiscal policy as well as developments in higher education, innovation

and product sophistication are crucial to avoid MIT in the future.

Ernests Bordāns, Madis Teinemaa

5

1. Introduction

Even despite the deep economic recession in 2008-2009 the Baltic States have shown

impressive economic performance since the beginning of 21st century. Beating the odds of

many, Latvia, Estonia and Lithuania have managed to increase their GDP per capita levels (at

PPS) from 36%, 43% and 39% of the European Union average respectively in 2000, to 63%

in Latvia and 74% in Estonia and Lithuania respectively in 2014 (Eurostat, 2015). In truth,

this rapid catching up was experienced largely because the income gap between the Baltics

and the EU was so large (thus, the Baltics had relatively competitive labour market (lower

wages), higher marginal returns to capital, opportunity to import technologies etc.) and due

some short term economic growth boosts (e.g. credit boom). However, the post-crisis period

has experienced a considerable slowdown in the economic growth compared to pre-crisis

period, and many suggest that Baltic States might be facing the mysterious middle income

trap (MIT) (IMF, 2015; OECD, 2015).

Pundits suggest that we cannot expect Baltics to simply keep converging with the EU with

the same pace as before given a considerable change in their relative income and overall

macroeconomic environment, and remind that that the only European country that has

substantially changed its position in GDP per capita ranking in Europe is Ireland. Moreover,

there is no consensus about the existence of absolute convergence between countries globally

(Sala-i-Martin, 1996).

International Monetary Fund (IMF, 2015) and Bank of Latvia economists (Kasjanovs, 2015)

that have discussed the MIT as a threat to the Baltic economies, agree that the current

slowdown might not yet mean that we are trapped; however, it indicates a necessity for more

profound structural reforms. In a recent study, Staehr (2015) points specifically at the Baltic

States facing the risk of MIT; and Swedbank has identified necessity for more growth-

friendly government spending in Latvia to avoid the MIT (Strašuna, 2015).

Continued steady growth is a matter of policies and MIT literature suggests that countries at

similar development stage as the Baltic States need to revise their economic policy in order to

avoid economic slowdown (Ohno, 2009). We want to find out whether based on social and

economic indicators, that roughly represent the economic policies pursued, the Baltic States,

are ready to avoid the MIT and continue convergence with the European average income.

Ernests Bordāns, Madis Teinemaa

6

Even though pundits have conceptually agreed on what is and what might be causing the

middle income trap, there is no official definition for MIT. Apparently, it is something that

combines being at middle-income level and experiencing low economic growth. Different

researchers offer different numeric definitions for such situation; literature has agreed neither

on thresholds for middle income level, nor characteristics of trap. Thus, the first objective of

this paper is to review the literature on each of the component of MIT definition and propose

original definition that addresses the drawbacks in previous literature by offering country-

specific benchmarks. By applying our definition, we find which middle income countries

have historically been or currently are caught in MIT.

The second objective is to study the impact of different economic, social and political factors

on the probability of countries being caught in MIT. We construct several multivariate panel

data logit models to find factors that are consistently associated with MIT occurrence.

The third objective is to quantitatively assess the probability of each Baltic country facing the

MIT. This is achieved by fitting a highly significant multivariate panel data logit model that

takes into account all factors that are found to be the most significant during the research.

Research Questions

Hence, we aim at sequentially answering the following research questions:

1) Which countries have historically been or currently are caught in the

MIT?

2) What is the current probability of Baltic countries facing the MIT and

which Baltic country is most likely to get trapped?

3) Which factors are associated with MIT and what policies particularly

Baltic States should implement to avoid MIT?

To our best knowledge, no study taking into account so many explanatory factors and

quantitatively assessing the probability of countries facing the MIT has been carried out. By

answering our research questions we aim at being able to provide policy recommendations

for the Baltic States.

The remainder of the paper is structured as follows: section 2 offers a review of existing

literature by paying particular attention to the definition of MIT; section 3 describes the

methods used and process of quantitative data analysis; section 4 presents the findings of

Ernests Bordāns, Madis Teinemaa

7

MIT occurrence, results of estimated predicted probabilities for the Baltic States and impact

of exogenous factors; and section 5 offers discussion of results.

2. Literature Review

2.1. Theory of MIT

In their original paper Gill, Kharas and Bhattasali (2007) were the first to name and discuss

MIT as a potential threat to a continued East Asian countries’ growth to high income level.

They claimed that in order to continue to grow, the East Asian countries must develop

economies of scale by continuing to increase the share of high-technology products in their

immense international trade, improving the knowledge absorption capacities (via education,

property rights, competitiveness), building strong financial system, including peripheric

regions in trade networks and eliminating inequality. Since then, researchers have mostly

studied the MIT in the context of sustainability of East Asian “miracle”, and the slowdown of

Latin American and Middle East countries.

When defining the MIT, most papers refer to how Gill et.al. (2007) characterized it initially.

To their mind, country is caught in MIT at the point when it is not capable of outcompeting

lower-income countries with their factor prices and also not able to compete with the

technology and productivity of high-income countries. In other words, the strategy for

economic growth at low-income level is not so efficient at middle-income level anymore

(Kharas and Kohli, 2011).

The loss of competitiveness among middle-income countries can be explained by W. Arthur

Lewis (dual-sector) development model which states that low wages and imitated technology

may boost growth at the low-income economies by moving labor from labor-intensive

agricultural sector to more productive (and better paid) manufacturing; however, eventually,

with rising income, labor-intensive sectors become less competitive and marginal returns

from imitated technology decrease. Thus, further growth can only occur with technological

advancements based on innovation not imitation (Agenor, Canuto and Jelenic, 2012).

Similarly, Ohno (2009) proposes to view the economic development as a four-stage process

where slowdown can occur at any transition between the stages. In his view, the MIT occurs

when an economy is moving from light manufacturing, that is mostly established by FDI, to a

stage where local human capital is developed and share of high-quality production is

increasing.

Ernests Bordāns, Madis Teinemaa

8

It is important to note that because MIT has not been defined unambiguously and its

identification in most researches depends on the definition chosen by authors, we cannot be

fully sure that MIT is really a trap; i.e. Im and Rosenblatt (2013) conclude that even though it

can be observed that middle income countries rarely advance to high income levels and it is a

troubling issue, the growth and convergence patterns of middle income countries do not differ

that much from the usual path of convergence where human capital, infrastructure,

institutions, TFP and investments are crucial for absolute convergence. Similarly, skeptical

authors have shown middle income countries do not present signs of consistently lower

growth than low-income countries (Bulman, Eden and Nguyen, 2014).

Given that thus far no unified MIT definition exists, but acknowledging the determinative

impact that MIT definition has on any further research, in order to define the MIT we must

firstly, agree on “middle income level”, and secondly - on characteristics of trap. Further, we

review on what assumptions has previous literature been based; and what are the findings.

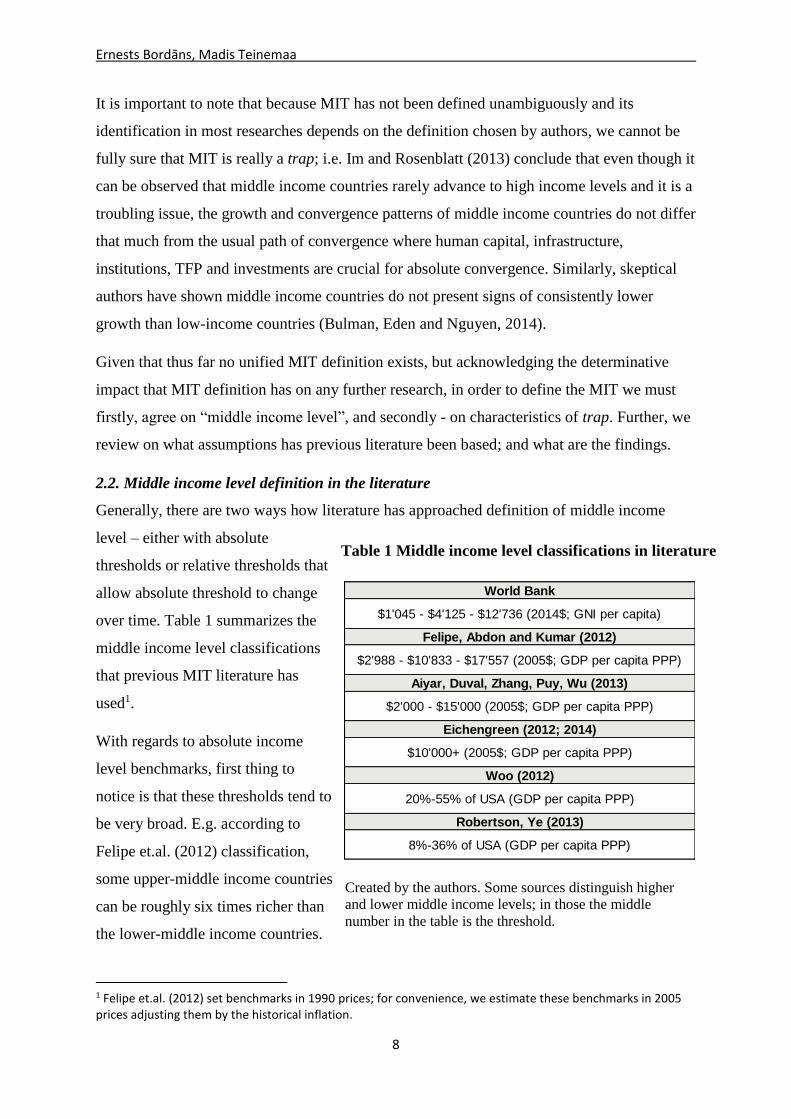

2.2. Middle income level definition in the literature

Generally, there are two ways how literature has approached definition of middle income

level – either with absolute

thresholds or relative thresholds that

allow absolute threshold to change

over time. Table 1 summarizes the

middle income level classifications

that previous MIT literature has

used1.

With regards to absolute income

level benchmarks, first thing to

notice is that these thresholds tend to

be very broad. E.g. according to

Felipe et.al. (2012) classification,

some upper-middle income countries

can be roughly six times richer than

the lower-middle income countries.

1 Felipe et.al. (2012) set benchmarks in 1990 prices; for convenience, we estimate these benchmarks in 2005 prices adjusting them by the historical inflation.

World Bank

$1'045 - $4'125 - $12'736 (2014$; GNI per capita)

Felipe, Abdon and Kumar (2012)

$2'988 - $10'833 - $17'557 (2005$; GDP per capita PPP)

Aiyar, Duval, Zhang, Puy, Wu (2013)

$2'000 - $15'000 (2005$; GDP per capita PPP)

Eichengreen (2012; 2014)

$10'000+ (2005$; GDP per capita PPP)

Woo (2012)

20%-55% of USA (GDP per capita PPP)

Robertson, Ye (2013)

8%-36% of USA (GDP per capita PPP)

Table 1 Middle income level classifications in literature

Created by the authors. Some sources distinguish higher

and lower middle income levels; in those the middle

number in the table is the threshold.

Ernests Bordāns, Madis Teinemaa

9

However, can we actually compare the situation in two so different countries, and can we

have the same policy recommendations for them? Moreover, the absolute thresholds hold

stable over time. Thus, theoretically we could e.g. identify that Honduras (GDP per capita in

1950s was above $2000) was in a MIT back in 1950s and 1960s. However, can we directly

compare the economic situation of Honduras during 1960s with that of Spain in 2010, which

is also believed to be trapped?

At the same time, this absolute threshold would mean that back in 1950s there were

practically no high-income economies. However, back in 1960s when the richest countries

were advancing to high-income levels (by absolute values) they lived in much poorer world

overall, with less developed trading partners, less foreign technologies to imitate and, thus,

determinants of their growth might have been different. So, can we apply their lessons to

nowadays world? Similarly, Rosenblatt et.al. (2013) points out that if we assume an absolute

threshold for middle income, then the majority of high income countries were trapped in MIT

in the 20th century because it took very long for them to advance to high-income. This raises

a question of whether a middle income trap is fully endogenous problem of countries and

being trapped or escaping is a question of their policies regardless of the time and income-

level of other countries, or is it dependent on how the country looks relatively to others?

Moreover, setting a precise absolute benchmark is even more ambiguous task.

MIT is assumed to be a point where a country is stuck because it has not transformed its

economy into a productivity-driven one and, thus, it can compete with neither low, nor high

income countries (Gill et.al., 2007). This definition inherently assumes that there are

wealthier and more productive countries in this world. Furthermore, wealth and

productiveness have grown substantially over the last 60 years e.g. one of the richest country

in the world, USA’s per-capita income grew more than three times between 1950 and 2010,

and consequently changed the assumption of what are “wealthier and more productive

countries” “with which the middle-income countries must compete”. In other words, the

income level that can be achieved by imitation of foreign technologies increases over time.

Following these logics, it seems obvious that for studying middle-income trap, we need a

definition of middle income that includes some dynamic, time-varying trend. However, using

a relative benchmark or a catch-up index as a threshold also raises serious ambiguity issues.

Firstly, relative benchmarks have been widely criticized because of their underlying

assumption of existence of absolute convergence, which does not have a robust empirical

Ernests Bordāns, Madis Teinemaa

10

proof (Sala-i-Martin 1996). World Bank (2012) and other researchers point out that – there

were 101 countries that had advanced to relative (to USA) middle income benchmark level

by 1960; however, only 13 of them had reached high income level by 2008; and five of those

are East Asian “miracles“ (Felipe et.al., 2012) (Rosenblatt et.al., 2013) (Woo, 2012). But can

we really say that all the rest are trapped, if they have experienced growth in absolute terms?

Woo (2012) acknowledges that as the income levels globally have been rising consistently

over the last centuries, some dynamic trend must be included in the definition of middle

income. He proposes a catch-up index benchmarked to the USA per capita GDP, defining

middle income countries as those with income level between 20 and 55% of USA’s. The

author analyzes data of 1960-2008 and finds that middle income countries tend to converge

among themselves (e.g. Latin America) but not catch up with the USA. This methodology

does not estimate a precise time period of trap and because of the wide range, we cannot

know whether the country was growing at the same pace throughout the whole time periods,

or maybe it did not grow during the first years and at one point - rocketed up. Moreover,

relative catch-up benchmarks imply that middle-income countries should grow faster than the

high-income countries. Some empirical findings support these claims; however, it is arguable

whether it is it right to assume that middle income country growing at the same pace as high

income is trapped forever.

2.3. Middle income trap definition in the literature

Once the benchmarks for middle income level are set (if at all), existing literature on MITs

offer us several ways how to identify traps. Generally, two approaches can be taken for

identifying traps – statistical methods or intuitive rules (of thumb).

With regards to intuitive methods, Felipe et.al. (2012) offer identifying countries in the MIT

as those that have spent more years as middle income countries than on average countries

historically have. They find that the median number of years it took on average for countries

to get through the middle income was 42 years. And thus, they estimate that 35 of 52 middle

income countries were trapped in 2010.

Advantages of this definition are that authors can estimate the average growth rate necessary

for countries to avoid MIT and also specific periods in history when different countries have

been trapped. However, this definition also has major flaws. Firstly, authors admit that the

number of years spent in middle income largely depend on the historical time period we look

at, i.e. the later country entered the lower-middle income level, the shorter time it spent there

Ernests Bordāns, Madis Teinemaa

11

on average, and nowadays countries tend to cross the absolute thresholds quicker. Secondly,

no consistent data is available for countries before 1950s, thus, we cannot know how long

before 1950 some countries had already been in the middle income level. Thirdly, authors’

methodology implies that there always must be countries in the MIT (those that are below

average growth) i.e. country can be considered to be trapped simply if it is growing slower

than others have been historically. And lastly, given that countries’ growth rates could

actually differ quite substantially over time such definition makes it almost impossible to

analyze the influence of specific exogenous factors on the probability of being trapped.

Eichengreen et.al. (2014) offer another intuitive method for identifying the MIT. They do not

define middle income, and simply look at all countries above 10000$ GDP per capita PPP

(2005-prices). By employing GDP per capita data starting from 1957 they look for points in

time (years) where a country after 7-year (t-7) average annual income growth of at least 3.5%

experiences a drop in the average growth for the next 7 years (t+7) by at least 2 percentage

points. The time “t” is identified as a slowdown. In case several years in a row are identified

as slowdowns, Chow test for these years is employed to find the most significant break point

in the growth rate. Eichengreen et.al. (2014) identify that most often slowdowns occur at 10

000 – 11 000$, 15 000 – 16 000$, and around 17 000$ GDP per capita PPP.

Advantage of this methodology is that it identifies years when the slowdown (trap) is the

most pronounced and, thus, should work well for studying which factors caused a slowdown.

However, the assumptions of this model raise many questions. Firstly, according to Penn

World Tables there were only 11 countries with income level above 10 000$ in 1956, thus,

this methodology rules out many possible subjects for study. Secondly, the benchmark of

3.5% for growth before the slowdown rules out all countries that have been in a trap for the

whole period and never achieved 3.5% growth (e.g. South Africa), and the value of this

benchmark seems arbitrary; third, the 2 percentage point growth slowdown is not well

justified. For instance, countries that have experienced GDP per capita growth of 10% and

now have slowed down to 8% would also be identified as being in a trap.

Using a statistical approach, Aiyar et.al. (2013) assumes middle income level to be 2000 –

15000$ GDP per capita PPP (2005-prices). He gathers consistent data for 138 countries

between 1955 and 2009. First, expected GDP per capita growth is predicted for each year by

regressing GDP per capita growth on physical capital stock, human capital index and lagged

per capita income. Then they identify MIT by looking at the distribution of differences

Ernests Bordāns, Madis Teinemaa

12

between the expected growth of economy and the actual; country is identified to be in a trap

if the residuals for certain years are in the 20th percentile of all residuals calculated (i.e. the

expected growth was substantially larger than the actual). Authors divided the sample into

eleven 5-year periods and looked for those 5-year periods that met their definition; 11% of

them were found to be in a MIT. They also found that middle income countries experience

the slowdowns more frequently than other countries.

The obvious flaw of this methodology is that its accuracy depends on the assumptions of their

theoretical growth model (that GDP growth can be predicted by those three factors). Thus, we

face the joint-hypothesis problem (when we cannot tell whether their theoretical growth

model is wrong or whether MIT do not exist). Moreover, this model would not identify a

MIT in countries where MIT is caused or is reflected in low investment in physical and

human capital. Hence, it is more of a simple test for the model.

Robertson and Ye (2013) offers another statistical model for defining the MIT by looking

particularly at the long-run growth of economies. They assume middle income level to be

between 8 – 36% of USA’s (assuming it to be the world’s technology frontier), and for a

country to “qualify” as MIT country, its long-run per capita income forecast should lie in the

middle income range and the distribution of the differences between the country’s log income

level and USA’s log income level should be stationary (i.e. countries’ income levels are not

converging). They find that out of 46 middle income countries, 19 are trapped. To our mind,

the main flaw of this definition of MIT is that it does not allow any convergence; thus, it

might not identify countries that are growing very slowly but have some convergence; or

countries that are diverging from the USA.

Furthermore, apart from defining the MIT, there is fair amount of literature focusing on

simply determining economic slowdowns. One of the most straightforward ways to try to

estimate slowdowns is by using econometric tests that look for structural breaks in series e.g.

the Chow test or Quandt-Andrews test; however, these tests generally tell us less about the

direction of the break and they identify individual years, rather than a time period that could

be assumed MIT. Berg, Ostry and Zettelmeyer (2012) offer a relatively more sophisticated

method for identifying breaks in the growth. They define a period that starts with a statistical

upbreak in growth (2-3% growth) and ends with a downbreak in growth (or the end of

sample) as a “growth spell”. The breaks are identified by minimizing the sum of squared

residuals between average growth rates before and after the break using the Monte Carlo

Ernests Bordāns, Madis Teinemaa

13

simulation. Depending on the minimum years set between the breaks (5 or 8), authors

identify 174 to 280 breaks (including both upbreaks and downbreaks) starting from 1950s.

2.4. Literature on MIT determinants

In a qualitative paper, Kharas et.al. (2011) suggest that in order to avoid MIT, apart from the

prerequisites of manufacturing industry becoming more capital and skill intensive and

services as share of GDP increasing, the key strategy should be development of the domestic

demand that is necessary as a platform for domestic companies with global ambitions.

Relatedly, income inequality might be a reason for country to be stuck in a MIT, as unequal

income distribution can lead to domestic demand growing slower than the GDP, and at some

point country can face a slowdown because of underinvestment in human capital. Kharas

et.al. (2011) recommends three key policy changes – specialization, structural reforms for

improving TFP, and decentralization and privatization.

Researchers have employed different intuitive arithmetic and statistical estimation methods

like probit, logit and proportional hazard models for studying the determinants of MIT. Aiyar

et.al. (2013) employ probit regressions (with binary variable whether a country in a specific

year is in MIT or not) and Bayesian averaging as robustness tests, and estimate the impact of

42 different explanatory variables (including lagged and differenced values). They find that

better rule of law, less government involvement, lower regulations, lower dependency ratio,

higher trade openness, higher investments, services and agriculture as share of GDP, lower

capital inflows, larger public debt, smaller distance to trade, higher regional integration and

higher export diversification are associated with lower probability of MIT. By employing

similar econometric methodology, Eichengreen et.al. (2014; 2011) complements the literature

by finding that lower MIT probability is also associated with higher consumption, lower

fertility rates, lower employment share in manufacturing, higher share of population with

secondary and tertiary education and more high-technology exports.

Furthermore, Berg et.al. (2012) employ proportional hazard model to estimate the expected

length of (previously described) “growth spells” (including lagged and differenced factor

values). They find that growth is likely to persist if there is current account surplus, more

sophisticated exports, openness to FDI, income equality, democratic institutions and

macroeconomic stability. Agenor et.al. (2015) employ an overlapping generations simulation

model, and find that MIT occurs because of misallocation of talent, low productivity growth,

Ernests Bordāns, Madis Teinemaa

14

inefficient labor market, lack of property rights and weak (especially – advanced (e.g. IT))

infrastructure.

All policy recommendations in the literature require structural reforms. Felipe et.al. (2012)

emphasize the potential of a country for further structural changes. They estimate revealed

comparative advantage (RCA) and apply Hausmann and Klinger (2006) methodology to

export data. They find that number of products with RCA, share of core products in exports,

product sophistication and uniqueness of country’s exports are associated with lower risk of

MIT.

Notably, we identify considerable gaps and drawbacks in the previous literature on MIT

determinants. Firstly, all previous papers that have used logit or probit estimations have had

possible econometric estimations biases, i.e. Aiyar et.al.(2013) and Eichengreen et.al. (2014)

do not attempt fitting multivariate regression models that would include more control

variables that previous economic growth literature has identified to be relevant; their

regression specifications may feature large multicollinearity; and regression specifications

include just few significant variables (the insignificant ones are not excluded). Secondly, vast

majority of the previous literature has focused simply on identifying the significant factors;

however, none has attempted to quantify the actual probability of certain countries facing the

MIT or assessed the magnitude of the effect of certain factors on a particular country.

3. Methodology

3.1 Our MIT Definition

Credibility of any findings of this paper are dependent on a successful and appropriate

definition of the MIT in context of the Baltic States. As can be seen, the definition of middle

income trap is ambiguous and we identify all methodologies to have major flaws. The key

characteristics that the definition should inhabit in order to be used for our quantitative

analysis are (1) ability to capture a precise time period when the slowdown occurs, (2) trap

should differ from a short term economic slowdown, (3) countries identified as middle

income level must be comparable (at a similar development stage), (4) the definition must

take into account global, as well as regional macroeconomic environment (other country

income levels and growth) and (5) most importantly, the definition of middle income trap

must correspond as much as possible to how the researchers have agreed to characterize it –

country stuck between competitive low-wage and high-productivity status. Our key premise

is that country can be considered trapped if it is growing slower than it should be.

Ernests Bordāns, Madis Teinemaa

15

We offer an intuitive middle income trap definition that we believe solves most of the

problems identified previously, and that is specifically adjusted for the purpose of our

research – to study the Baltic States.

3.1.1. Setting the middle income level

Firstly, we must be sure that we have a comparable set of countries in our study sample and

that we can compare these countries over time. As showed by Felipe et.al. (2012) countries at

the same absolute income levels have performed substantially different over time, growing

much slower historically than countries at the same income level are growing nowadays.

Keeping that in mind, we choose to use relative benchmarks for determining middle income

countries, and these benchmarks are set accordingly, so that Baltic countries qualify as

middle income countries. We define relative income ranges as percentages of the USA’s

income level (assuming USA to be the World economic leader for the whole time period

observed (Robertson et.al., 2013)).

As discussed previously, researchers have chosen to use very different relative middle

income level benchmarks. In the context of MIT, Woo (2012) explains that income level of

15-60% of the USA features almost exactly the same set of countries throughout time since

1960s. Considering this and the fact that income level benchmark at 15% of the USA ensures

that all Baltic countries are identified to be middle income level for the whole period since

their data is observed (since 1990s) we set the bottom benchmark for middle income level at

15% of the USA (that is approximately 2270$ at PPP 2005 $ in 1960 and 6402$ in 2014).

Next, we choose 70% of the USA GDP per capita as the upper benchmark for middle income

level because that represents approximately the average income level of the European Union

over the time, and we assume that being above the average income level of the one of the

richest regions in the world (EU) would imply that country is above the middle income.

Baltic States started off in 1990s with the income level at PPP of around 20% of USA and

now are approximately halfway through our middle income definition. Setting the respective

middle income level benchmarks ensures us that almost half of the countries are European

and most African countries are excluded (list of all countries identified as middle income at

some point can be found in Appendix A).

3.1.2 Choosing the “trap” criteria

According to our proposed MIT definition, a country is trapped in a certain year if it fulfils

three country-specific criteria related to its GDP per capita growth rate.

Firstly, we wish to compare each country’s growth rate with other countries at similar

Ernests Bordāns, Madis Teinemaa

16

economic development stage, to see if the specific country is performing as well as other

countries that are also in the transition between labour and technology-intensive industries.

However, even within our defined middle income level range, countries at the poles of the

defined range have fairly different growth trends over time. Thus, in order to be sure that we

compare growth rates of countries across comparable sets, we divide middle-income

countries into four groups according to their income level – (1) countries at income level of

15%-20% of the USA, (2) at 20%-30%, (3) at 30%-50% and (4) at 50%-70% of the USA (list

of countries in each range may change every year). These income level intervals were chosen

(a) to ensure enough observations in each group every year; (b) to make sure that each

interval is not too wide and we can expect each set of countries to be similar; and (c) because

in recent years all Baltic countries belong to the same (30%-50% of USA) income level

interval.

Secondly, keeping in mind that growth rates differ across regions, we compare each

country’s growth rate with its respective region’s average growth rate. According to World

Bank classification we divide countries into the following regions – East Asia and Pacific,

Europe and Central Asia, European Union (partly overlaps with Europe and Central Asia),

Middle East & North Africa & South Asia, Sub-Saharan Africa, Latin America. Most middle

income trap definitions offered by previous researchers do not take into account how the

external macroeconomic environment impacts country’s performance; however, we believe

that it is important to control for external factors when studying which internal factors are

associated with MIT. And we believe that regional growth is a better proxy for external

macroeconomic environment than the World growth rate. Moreover, comparing middle

income countries growth rates with region’s average growth rate (despite the fact that the

regions also include countries at much different income levels) is justifiable because

according to the underlying MIT theory, countries that are in MIT should be growing slower

than both low and high income countries (as they can compete neither with low-wage

countries, nor more productive high-income countries).

Thirdly, we compare each country’s growth rate with the weighted average growth rate of its

trading partners’ in the specific year (weighted by the share of total exports). We believe that

having a country-specific benchmark is particularly important, because firstly, the trading

partners’ growth accounts for external shocks even better than regional growth rate (countries

located in periphery areas of their regions might not be affected from regional developments

as significantly as from its trading partners); secondly, trading partners’ growth rate is an

Ernests Bordāns, Madis Teinemaa

17

approximate benchmark of external demand and if country is not able to keep up with the

growth in trading partners, it might indicate that there is an issue with country’s

competitiveness.

To our best knowledge we are the first to create unique country-specific benchmarks for

researching middle income traps.

To summarize, our proposed MIT definition is as follows: we consider a country be trapped

in middle income during a specific year if its GDP per capita lies in the range of 15-70% of

the USA’s income level, and its GDP per capita growth rate is lower than a) the average

growth rate of other countries globally in its respective income level range (15-20%, 20-30%,

30-50% and 50-70% of the USA), 2) its respective region’s average growth, and 3) weighted

average growth of each country’s trading partners.

3.1.3 Other characteristics of our definition

The key advantage of using all three growth benchmarks lies in the fact that we use all of

them together and, thus, account for many limitations that each of the three benchmarks

would have if they were used individually and exclusively. If a country is growing slower

than each of the benchmark, we can be more certain that the growth of this country is lower

than it should be.

Similarly, we need several growth benchmarks to avoid a situation when half of the countries

would be trapped “by definition”. By comparing countries growth rates not only to other

middle income countries, we avoid situations when fast-growing middle income countries

would be considered trapped just because other middle income countries are growing even

faster (a flaw of Felipe et.al., (2012) methodology). Moreover, our definition does not assume

that there must definitely be an absolute convergence with the USA.

By using Hodrick-Prescott filter for GDP per capita values (described further in

methodology), we remove impact from economic cycles and record slowdown as a middle

income trap only when it is related to a long term growth trend. Moreover, we can identify a

country to be in MIT even if we do not have long historical GDP per capita data (as is the

case for the Baltics).

Nevertheless, we acknowledge that using the USA as a benchmark may be challenged, as this

approach assumes that countries at e.g. 50% of the USA’s income level in 1960s had the

same priorities as countries at 50% income level nowadays; however, it can be the case that

countries at the same relative income level in 1960s were still less developed and required

Ernests Bordāns, Madis Teinemaa

18

different strategy.

Moreover, we identify few cases when a country was caught in MIT for just one year. Such

finding may seem unintuitive as MIT is usually associated with more persistent long term

economic trends; however, we still include such observations because given that our GDP per

capita data is smoothed, it is unlikely that a country was identified to be in MIT due to one-

off event; it rather indicates that this country was on the edge of MIT.

3.2 Estimating the MIT determinants and probability of MIT

In order to estimate the probability of the Baltics facing the MIT and quantitatively assess the

impact of different explanatory factors on the probability of MIT we (1) choose control

variables for initial assessment of significance of different factors, (2) construct several

multivariate panel data logit models, (3) predict the probability of MIT using these models,

and (4) study the impact of individual factors by estimating their significance and consistency

of the impact across different model specifications.

3.2.1. Multivariate logistic panel data regressions

We employ multivariate panel data logit regressions in order to quantitatively assess the

impact of different factors on the probability of MIT and also predict the probability given

values of factors for each country. A binary variable indicating whether country in the

specific year was trapped or not is always used as the dependent variable.

We choose to perform random effect regressions. Firstly, Hausman specification test implies

that performing random effect estimations is appropriate for our data (Hausman and

McFadden, 1984); and secondly, fixed effect estimations automatically omit many countries

with zero variance in the dependent variable (e.g. countries that have never been trapped).

Furthermore, because all of our factors are continuous (not categorical) variables, estimated

marginal effects of our logit regressions can be misleading and not precise (Williams, 2015).

Hence, instead of estimating the marginal effects we manually adjust the factors of interest

and look at what is the change of predicted probability given different values for explanatory

variables. Further in our paper we test our prediction models in the described manner, by

altering some of the explanatory factors for the Baltic States.

3.2.2. Choosing the control variables

We cannot fully rely on previous literature when proposing our control variables because,

firstly, middle income trap literature is currently still very limited and inconclusive with

Ernests Bordāns, Madis Teinemaa

19

regards to its findings; secondly, even economic growth literature is largely indecisive about

which factors have consistently significant influence on economic growth (Levine and

Renelt, 1992) and, thirdly, our middle income trap definition is original and it is worth testing

as many variables as possible.

Findings of cross-country economic growth research are extremely sensitive to the

specification of regression model; thus, researchers often find contradicting coefficient signs

for the same factors and no clear consensus on the right model specification exists (Durlauf

and Quah, 1999) (Levine, 1992).

Nevertheless, most economists agree that univariate regressions can be misleading and

individual factors should always be studied by using a set of relevant control variables,

moreover, there should be some robustness checks (Hosmer, Lemeshow and Sturdivant,

2000) (Sala-i-Matin, 1997). After surveying the literature we find that the most often used

control variables in economic growth research are level of GDP per capita, investment share

in GDP, population growth, some human capital measure, proxy for trade openness, fertility,

world growth, government size and dummies for time periods (but rarely all of them are used

together) (Levine and Renelt, 1991).

We choose our control variables based on the following criteria: 1) they must have been used

as control variables in previous literature and found to be consistently significant, 2) all

chosen control variables must be significant when regressed together and they must maintain

their significance in majority of regressions with other factors added to the model, 3) they

must have low cross-correlation, 4) they must have sufficient amount of observations in our

dataset (starting from 1960s), and 5) their influence on MIT risk must have a clear causality.

After testing different factors, we find that GDP per capita, investment level, tertiary

education enrolment rate, trade openness and government spending as a share of GDP meets

all of our five criteria. Population growth, fertility and dummies for time periods often were

not significant when regressed together with other control variables. We do not consider

world growth rate as a control variable because it is indirectly included in our MIT definition.

3.2.3. Fitting the model(s)

Firstly, we want to restrict the number of factors for further consideration for inclusion in the

prediction models. After choosing five control variables we perform a preliminary assessment

of all the rest factors in our dataset. We perform logistic regressions using the five control

variables and adding all other variables one by one as the sixth explanatory variable to the

Ernests Bordāns, Madis Teinemaa

20

model (we do not perform univariate regressions at all). We consider a variable for further

inclusion in the main regression model if its p-value in the regression with control variables is

below 0.25 (similar approach for choosing candidates for group regressions is proposed by

Bursac, Gauss, Williams and Hosmer (2008).

Secondly, we fit the regression model using a stepwise selection procedure (adding variables

to the control variables in the model one by one and eliminating any variable that was added

previously if it turns insignificant (there are too many variables for using a backwards

selection in our case)). However, when using stepwise selection, the model that we end up

with is very dependent on what are the first variables that we add to the model and on which

we build it2. Hence, we repeat the stepwise selection procedure numerous times, each time

starting by different variables as the first ones to be considered in the model. Following the

recommendations in literature (Peng, Lee and Ingersoll, 2002) (Hoetker, 2007) we base

selection of the best model on the following criteria: 1) all variables included in the model

must be significant at p=0.053, 2) we consider the Wald Chi-Square goodness of fit test when

comparing similar models, 3) we validate how precise are the predicted probabilities of the

models for those observations that are actually trapped or not trapped, 4) we consider cross-

correlation between the variables in order to avoid multicollinearity (Appendix D), 5) we

include those variables that have sufficient amount of historic observations, and 6) we want

to have variables representing different categories (e.g. institutions, economic structure,

human capital etc.) in order to be sure that the model does not miss any crucial factors.

For robustness check we fit eight additional multivariate prediction models by largely

following the same described conditions of a good model; however, we compromise for one of

the conditions – for instance, including variables with less observations. The alternative

models’ predicted probabilities are less precise than for the main prediction model, they have

fewer explanatory variables and different number of observations; however, all variables are

still significant. Variables that are included in the all prediction models can be seen in Appendix

C, with our main prediction model marked as Model 1.

2 This appears because, firstly, there is still some cross-correlation between the variables, thus, the coefficients

interact between themselves and, secondly, because we are analysing such a long time period, different variables

observations might not overlap and once we add a variable to the model which has less observations than other

variables in the model it influences the sample. 3 Our main prediction model includes two variables significant at 90% level, to compromise for other good

characteristics of the model.

Ernests Bordāns, Madis Teinemaa

21

3.2.4. Individual exogenous factors analysis

The fitted models allow us to make some conclusions about those variables that are included

in the model; however, we would still like to analyse also variables that did not fit in the

models (they may still be relevant factors and may not be included in the models e.g. because

of too low number of observations). Thus, we follow Sala-i-Martin (1997) and Levine (1992)

and employ each variable in many different model specifications by using different sets of

control variables. The robustness of the impact can be assessed by judging in how many of

the regression specifications each variable was found significant.

Each variable in our dataset is regressed in 15 different regression specifications. In our

results, we present in how many of the 15 regressions (as percentage) each variable was

significant and with what sign.

For choosing the 15 regression specifications we follow Levine (1991) approach (who is

analysing robustness of FDI impact on economic growth). This implies having a set of fixed

control variables and adding additional relevant variables one by one (and thus having

additional regression model when each variable is added). The variables that are added

additionally to the five control variables are those variables that are included in the main

prediction model. Additionally, we regress each variable of interest by adding it to our main

model and four of the alternative models. Appendix E presents an example of our approach to

analysing each variable of interest (in this case - population growth)4.

3.3. Data description

Our data covers 152 countries for the period of 1960-2014. However, among these only 68

countries have been at middle income level at some point during our study time period, see

Appendix A for countries and periods under investigation. We follow Aiyar et.al.(2013) and

Eichengreen et.al.(2014) and exclude resource-exporter countries whose resource extraction

between 1960 and 2013 exceeds 20% of GNI on average5 based on data of Natural resources

depletion (as % of GNI) (WDI, 2015). Similarly as Felipe et.al. (2012), we also exclude

microstates (that we define as those with average population of less than 250 000 between

4 Detailed results (similar to Appendix E) on all other individual regressions are available upon request. We do

not attach all regression outputs here because of the large number of such estimation tables. 5 Countries that we exclude due to their resource richness are Angola, Azerbaijan, Bahrain, Brunei, Darussalam,

Bhutan, Congo, Rep., Gabon, Iraq, Kazakhstan, Kuwait, Libya, Nigeria, Oman, Qatar, Saudi Arabia,

Turkmenistan, Trinidad and Tobago, Uzbekistan

Ernests Bordāns, Madis Teinemaa

22

1960 and 2014) from further analysis6. We base all calculations of GDP per capita and

growth rates on data from a single database (Penn World Tables 7.1)7. The data sample that is

finally used for our analysis includes 2154 annual observations.

Following Eichengreen et.al.(2014) we intended to use seven-year average growth rates (t+/-

3 years) for cross-country growth rate comparisons, assuming that 7 years is period of

economic cycle, so that the smoothed growth would represent income growth based in

fundamentals. However, as in that case we would lose the growth rates of last three years, we

smooth our GDP per capita data using Hodrick-Prescott (HP) filter8. Moreover, we calculate

regional growth rates by weighing them by total GDP of countries in each region.

We create a dataset with annual data on the relative wealth and growth of each country’s

export partners (weighted by the amount of trade), in order to create country specific

benchmarks for our MIT definition and use trading partners’ relative wealth as one of our

factor in quantitative analysis, (IMF Direction of Trade Statistics database, 2016). To our

knowledge we are the first to study middle income traps using such specific dataset. The

weighted average trading partners’ data is compiled by assembling the annual export values

between all countries in our dataset from 1960 till 2014, computing weights for each country/

counterparty/year treble (e.g. Estonia’s proportional weight as Latvia’s export partner in

2014), and calculating the weighted average GDP per capita of trading partners and weighted

average trading partners’ growth in each year between 1960-2014.

Additionally to absolute values of our factors, we estimate the average value of each factor

based on all middle income countries in specific year, and then – estimate what is the value of

each country’s factor relatively to all middle income country average in that year (e.g. how

large was Latvia’s tertiary education enrolment rates in 1997 compared to average enrolment

6 Countries that we exclude are Aruba, Andorra, American Samoa, Antigua and Barbuda, Belize, Bermuda,

Brunei Darussalam, Curacao, Cayman Islands, Dominica, Faeroe Islands, Micronesia, Fed. Sts., Grenada,

Greenland, Guam, Isle of Man, Kiribati, St. Kitts and Nevis, St. Lucia, Liechtenstein, St. Martin (French part),

Monaco, Maldives, Marshall Islands, New Caledonia, Palau, French Polynesia, San Marino, Sao Tome and

Principe, Sint Maarten (Dutch part), Seychelles, Tonga, Tuvalu, St. Vincent and the Grenadines, Virgin Islands

(U.S.), Vanuatu Samoa

7 This database (PWT 7.1) features GDP per capita in constant 2005 prices for time period 1950-2010 and is

used by most middle income trap researchers (Eichengreen et.al., 2014) (Aiyar et.al., 2013). In order to be able

to also study the years of 2010 – 2014 (which are not covered) for the missing years we apply the growth rates

of GDP per capita PPP at constant prices data from the World Bank WDI database, and thus, get uninterrupted

GDP per capita data until 2014 8 We set the smoothing parameter 𝜆 at 21, in order to maximize the correlation between the estimated 7-year

average growth rate and HP-filtered GDP per capita growth rate.

Ernests Bordāns, Madis Teinemaa

23

rates among all middle income countries in 1997). Given that our study covers such a long

time period, considerable political, social and economic developments that have taken place

globally over time can have an influence on the findings of important factors (Levine and

Zervos, 1993). A bias in results can be caused e.g. by the fact that countries that had

relatively high human capital back in 1960s (and arguably – back then it caused a positive

effect on economic growth) at the same time had relatively low level of human capital if

compared to nowadays standards (as education enrolment rates have increased globally);

hence, some factors are less comparable over time. The estimated relative factor values do

not completely substitute the absolute values of each factor in our quantitative estimations;

they are used as robustness checks and we report results from all regressions - with relative

and absolute values of each factor.

Some factors (e.g. GINI index, Economic Freedom Index before 2000, BTI index and other)

are not observed in every year; hence, in order not to lose observations, we estimate the

missing observations by taking the average value of the closest existing observations.

Additionally, for the purpose of consistency, when studying exogenous factors impact, we

use a dataset where the values of all independent factors are included as averages of the

actual values of current and previous three years. Similar approach by lagging explanatory

variables is used by Aiyar et.al. (2013). We believe that such approach is more appropriate in

our research because, firstly, we are using smoothed GDP per capita data, and, secondly, we

are interested in finding the impact of sustained, structural problems in some of the factors

(not short term fluctuations) and these problems should be pronounced enough to also be

observed when averaged over several years.

The list of explanatory factors whose impact on the MIT we test can be found in Appendix J.

4. Empirical results

4.1. Findings of the MIT

Out of 2154 total middle income level countries observations for time period of 1960 – 2014,

689 (32%) are trapped. Our observed frequency is lower than e.g. for Felipe et.al. (2012) who

assumed that country is trapped if it grows through middle income level in more years than

other countries on average (which should yield approximately 50% frequency); however, our

frequency is substantially higher than was found by Aiyar et.al. (2013) who estimated it to be

around 11%. Note, however, that MIT probability cannot be compared directly to other

papers as the MIT definitions are different.

Ernests Bordāns, Madis Teinemaa

24

We find that the Baltic countries currently are not caught in the MIT; and among European

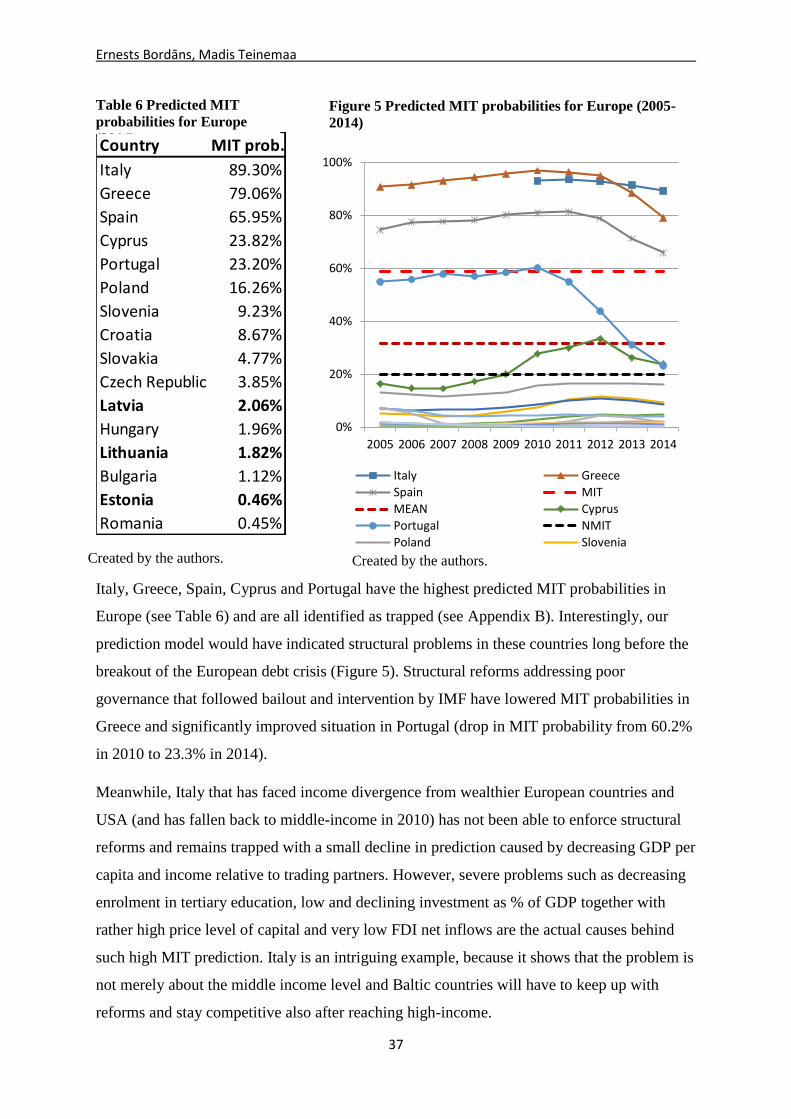

countries, Spain, Croatia, Cyprus, Portugal, Greece, Italy and Slovenia are currently trapped

(Italy slipped back into middle income level from high income level in 2010, see Appendix

A). Figures 2 below shows that the Baltic States have been avoiding the MIT since 1994 with

a great confidence beating all three middle income trap growth thresholds (regional, trading

partners and other middle income countries growth rates). Nevertheless, the economic

recession has had a significant influence on all three Baltic States growth rates, and Latvia’s

growth rate during 2009-2012 dropped somewhat below that of trading partners.

Frequency of middle income trap is different among regions; during the years of 1960-2014

Latin American countries were caught in trap in around 45% of all observations. Moreover,

most Latin American countries were trapped during the years of 1960-1988 (see Figure 3).

Such finding is consistent with previous literature. Without naming it “middle income trap”

Cimoli and Correa (2002) describe Latin America being caught in a “low growth trap” due to

their transition period. East Asia and Pacific region (middle income) countries have been

performing exceptionally well throughout our study period (MIT frequency has been just

11%), and apart from featuring some of the largest success stories of middle income countries

historically (e.g. South Korea and Singapore), also other countries have avoided prolonged

economic slowdowns, except for New Zealand in 1980s – 1990s. The average frequency of

MITs observed in the EU between 1960 and 2014 is 25%.

Our identified middle income traps usually occur for several consecutive years, and that is

consistent with the theoretical assumption that middle income trap is more than a short term

economic slowdown, and country can be caught in a bad equilibrium for a prolonged time

period. Hence, having identified long term periods of unreasonably low growth, we should be

able find the right causes of MIT.

MIT frequency has not been constant over time (see Figure 1a). Particularly, during the years

of mid-1960s to 1980 the frequency of slowdowns dropped on average well below 30%.

However, between 1980 and 2000 middle income traps occurred relatively more often (one of

the reason can be the collapse of USSR and “new” trapped middle income countries entered

the dataset); and then, together with the global economic boom the MIT frequency dropped

again in early 2000s.

Ernests Bordāns, Madis Teinemaa

25

Notably, countries at income level of 32.5-40% of the USA has had a considerably higher

frequency of MITs than at other income levels (see Figure 1b) This is a relevant finding given

that Latvia and Lithuania are currently at around 33% and 37% of USA income level

respectively.

Countries at income level of around 65-85% relatively to their trading partners on average

have experienced traps less often than countries at lower or higher income levels relatively to

their trading partners; that suggests that decreased wealth gap between home country and

trading partners might not be causing MIT per se. Estonia’s and Lithuania’s wealth relatively

to their trading partners is almost 70%; whereas, for Latvia - around 62%.

Figure 1 Frequency of MIT by years, absolute and relative income levels.

Created by the authors.

Ernests Bordāns, Madis Teinemaa

26

Figure 2 Baltic countries GDP PPP per capita growth rates compared to MIT definition

thresholds (income growth of trading partners, region and average of middle income countries

in specific income range where the country belongs to).

Created by the authors.

Ernests Bordāns, Madis Teinemaa

27

Country/Year

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

GreeceCyprusPortugalSpainTurkeyPolandRomaniaHungaryMacedoniaBulgariaCroatiaRussiaIrelandUKItalySlovakIAEstoniaSloveniaCzech Rep.SerbiaUkraineAlbaniaAustriaBelarusFinlandFranceLatviaLithuaniaMontenegroJamaicaVenezuelaArgentinaEl SalvadorUruguayPeruChileEcuadorGuatemalaMexicoBrazilCosta RicaSurinameColombiaNicaraguaBarbadosBoliviaPanamaDominican R.New ZealandSingaporeThailandMacaoChinaHong Kong JapanKorea, Rep.MalaysiaAlgeriaIranLebanonJordanIsraelDjiboutiMaltaTunisiaSouth AfricaEq. GuineaMauritius

ME

, N

A,

S.

Asia

Ea

st A

sia

an

d P

acif

icL

atin

Am

eric

aE

uro

pe

an

d C

en

tra

l A

sia

Afr

ica

Figure 3 Middle Income Traps from 1960 – 2014.

Created by the authors. Grey colour represents either missing GDP per capita data or the country being outside the middle

income level. Green colour represents a middle income country that is not trapped, red colour – a trapped middle income

country.

Ernests Bordāns, Madis Teinemaa

28

4.2. Results of regression models with exogenous MIT probability determinants

Appendix C presents the significance and signs of factors that are included in our prediction

models; in addition, Tables 2, 3, 4 present the findings on factors that were excluded from the

prediction models but which we analysed individually by employing in different regression

specifications (we also analyse individually all variables that were included in the prediction

models and report these results in Tables 2, 3, 4). In the Tables we indicate in how many of

the 15 regression specifications (as percentage) each variable of interest was significant; if

significant, what was the estimated impact on probability of MIT; and whether the variable

was significant when included in the main regression model. Moreover, we also show

whether the performance of the Baltic States (in 2014) in each factor differs significantly (at

5% significance) from the average values of other countries in the middle and high income

level in 2014 and show the results in the same tables9.

4.2.1. Macroeconomic environment

Income level

We witness that countries with lower GDP per capita levels are less likely to fall into trap

even when controlling for other factors. Impact is significant in almost all of our group

regressions including our main MIT prediction model. These findings for GDP per capita

impact on MIT likelihood are in line with vast evidence that has been found for conditional β-

convergence throughout different research approaches (Islam, 2003) (Quah, 1995) (Sala-i-

Martin, 1996).

Moreover, we find that higher income level relative to country’s trading partners has a

positive and significant impact on the probability of MIT when it is included in main

regression specification. Similar conclusion was reached by Arora and Vamvakidis (2005).

Hence, even though literature on convergence indicates that globally there could be absolute

divergence (Sala-i-Martin, 1996), trading intensively with wealthy economies can help

economy to avoid the MIT.

Macroeconomic stability

We find that favourable macroeconomic environment characterized by low inflation, low

standard deviation of inflation (our proxy for standard deviation of inflation is an Economic

Freedom index which is high if the standard deviation of inflation is low), higher budget

9 For some factors our dataset does not cover year of 2014; in that cases the latest available data is taken.

Ernests Bordāns, Madis Teinemaa

29

balance, monetary stability and lower price of capital has a significant and robust impact on

decreasing the probability of being caught in MIT (Table 2). This finding is consistent with

literature (Barro, 1996).

Economic structure

Higher investment rate has is significantly associated with lower probability of MIT and this

factor is significant in 93% of our regression specifications (including the main regression

model). We also find that higher government expenditure (% of GDP) increases the

probability of getting trapped in all 100% regression specifications. These findings are

consistent with that of Aiyar et.al. (2013). Regarding GDP structure on production side, we

find that only share of agriculture has a significant and negative impact on the probability of

MIT in most regression specifications. We find that industry as share of GDP is not

significantly related to middle income trap probability in most of the regression

specifications; however, the average share of industry as % of GDP in high and middle

income countries is also not statistically significantly different (see Table 2).

Competitiveness

We find that higher compensation as a share of total costs and pay-and-productivity relation

has a robust and significant impact on lowering the probability of MIT. Moreover, higher real

effective exchange rate proves to have a significant impact on increasing the probability of

MIT in about half of the regression specifications.

International trade and investments

Higher trade openness, lower trade barriers and tariffs have a robust and significant impact on

decreasing the probability of MIT. Moreover, we find that large current account deficits are

associated with higher MIT probability. Although, higher foreign direct investments have a

significant effect on decreasing the probability of MIT in 87% of regression specifications

(including the main model) (when used as an absolute value), when FDI is included in the

main regression model as a relative value it proves to be significant with increasing the

probability of MIT. Notably, many trade openness proxies (freedom to trade internationally

Ernests Bordāns, Madis Teinemaa

30

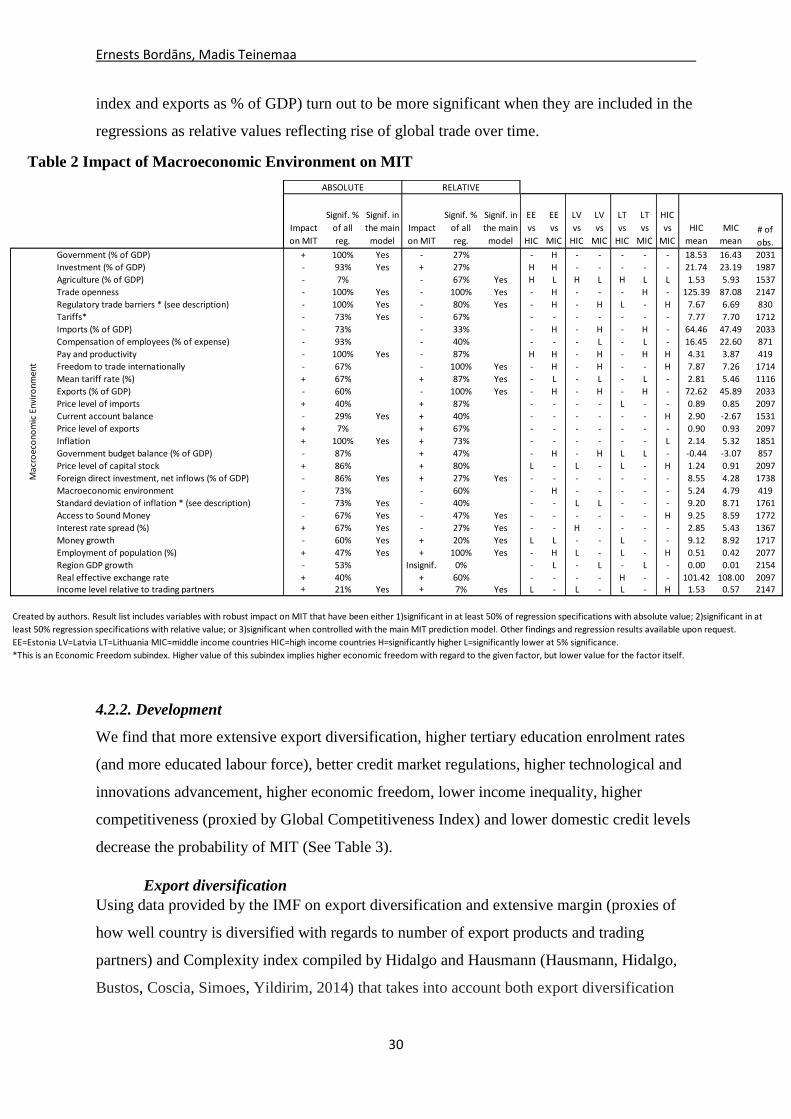

index and exports as % of GDP) turn out to be more significant when they are included in the

regressions as relative values reflecting rise of global trade over time.

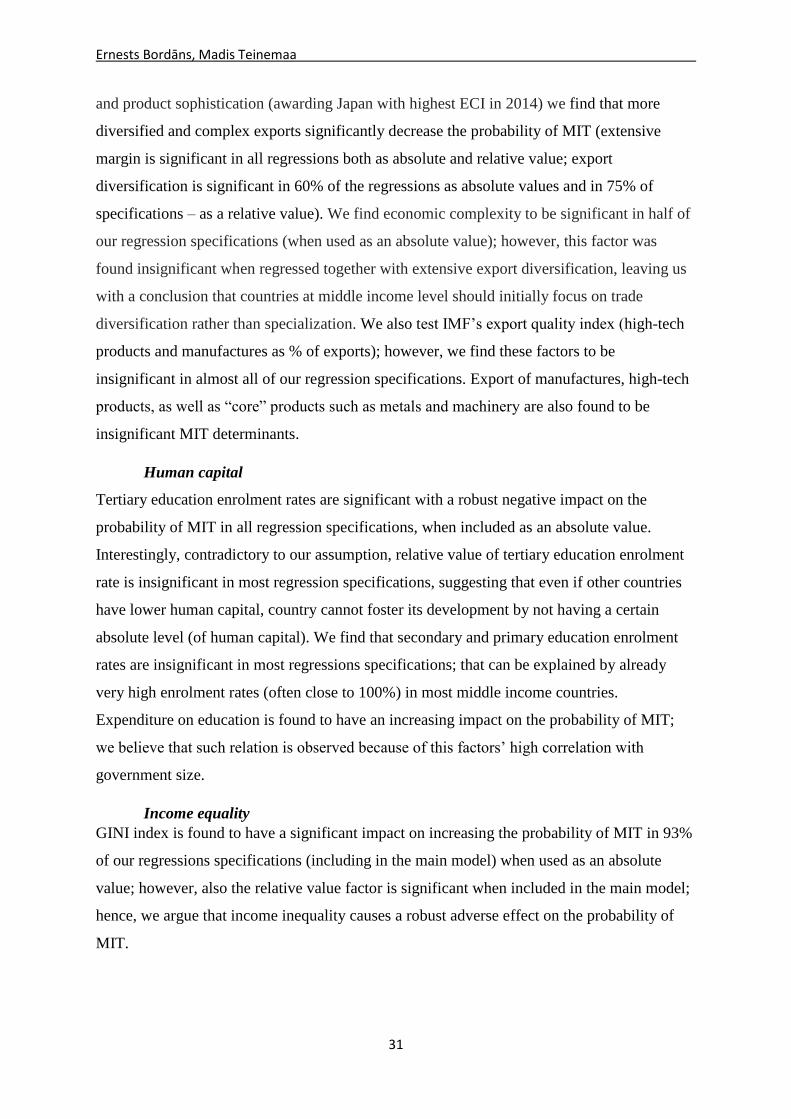

4.2.2. Development

We find that more extensive export diversification, higher tertiary education enrolment rates

(and more educated labour force), better credit market regulations, higher technological and

innovations advancement, higher economic freedom, lower income inequality, higher

competitiveness (proxied by Global Competitiveness Index) and lower domestic credit levels

decrease the probability of MIT (See Table 3).

Export diversification

Using data provided by the IMF on export diversification and extensive margin (proxies of

how well country is diversified with regards to number of export products and trading

partners) and Complexity index compiled by Hidalgo and Hausmann (Hausmann, Hidalgo,

Bustos, Coscia, Simoes, Yildirim, 2014) that takes into account both export diversification

Table 2 Impact of Macroeconomic Environment on MIT

Government (% of GDP) + 100% Yes - 27% - H - - - - - 18.53 16.43 2031

Investment (% of GDP) - 93% Yes + 27% H H - - - - - 21.74 23.19 1987

Agriculture (% of GDP) - 7% - 67% Yes H L H L H L L 1.53 5.93 1537

Trade openness - 100% Yes - 100% Yes - H - - - H - 125.39 87.08 2147

Regulatory trade barriers * (see description) - 100% Yes - 80% Yes - H - H L - H 7.67 6.69 830

Tariffs* - 73% Yes - 67% - - - - - - - 7.77 7.70 1712

Imports (% of GDP) - 73% - 33% - H - H - H - 64.46 47.49 2033

Compensation of employees (% of expense) - 93% - 40% - - - L - L - 16.45 22.60 871

Pay and productivity - 100% Yes - 87% H H - H - H H 4.31 3.87 419

Freedom to trade internationally - 67% - 100% Yes - H - H - - H 7.87 7.26 1714

Mean tariff rate (%) + 67% + 87% Yes - L - L - L - 2.81 5.46 1116

Exports (% of GDP) - 60% - 100% Yes - H - H - H - 72.62 45.89 2033

Price level of imports + 40% + 87% - - - - L - - 0.89 0.85 2097

Current account balance - 29% Yes + 40% - - - - - - H 2.90 -2.67 1531

Price level of exports + 7% + 67% - - - - - - - 0.90 0.93 2097

Inflation + 100% Yes + 73% - - - - - - L 2.14 5.32 1851

Government budget balance (% of GDP) - 87% + 47% - H - H L L - -0.44 -3.07 857

Price level of capital stock + 86% + 80% L - L - L - H 1.24 0.91 2097

Foreign direct investment, net inflows (% of GDP) - 86% Yes + 27% Yes - - - - - - - 8.55 4.28 1738

Macroeconomic environment - 73% - 60% - H - - - - - 5.24 4.79 419

Standard deviation of inflation * (see description) - 73% Yes - 40% - - L L - - - 9.20 8.71 1761

Access to Sound Money - 67% Yes - 47% Yes - - - - - - H 9.25 8.59 1772

Interest rate spread (%) + 67% Yes - 27% Yes - - H - - - - 2.85 5.43 1367

Money growth - 60% Yes + 20% Yes L L - - L - - 9.12 8.92 1717

Employment of population (%) + 47% Yes + 100% Yes - H L - L - H 0.51 0.42 2077

Region GDP growth - 53% Insignif. 0% - L - L - L - 0.00 0.01 2154

Real effective exchange rate + 40% + 60% - - - - H - - 101.42 108.00 2097Income level relative to trading partners + 21% Yes + 7% Yes L - L - L - H 1.53 0.57 2147

EE=Estonia LV=Latvia LT=Lithuania MIC=middle income countries HIC=high income countries H=significantly higher L=significantly lower at 5% significance.

*This is an Economic Freedom subindex. Higher value of this subindex implies higher economic freedom with regard to the given factor, but lower value for the factor itself.