bajaj auto ltd. absolute: reduce ), pt ( margins unlikely...

TRANSCRIPT

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112 +91 79-40504017) Page 1 of 12

Before reading this report, you must refer to the disclaimer on the last page.

Bajaj Auto Ltd. Absolute: REDUCE

Relative: BENCHMARK

1QFY18 Result: Estimate (), PT (), Rating () Regular Coverage 2% ATR in 14 months

Margins unlikely to scale historical highs, domestic volumes to stay weak; maintain REDUCE Auto

© 2017 Equirus All rights reserved

Rating Information

Price (Rs) 2,815

Target Price (Rs) 2,811

Target Date 30th Sep' 18

Target Set On 21st Jul'17

Implied yrs of growth (DCF) 12

Fair Value (DCF) 2,461

Fair Value (DDM) 1,167

Ind Benchmark BSEAUTO

Model Portfolio Position NA

Stock Information

Market Cap (Rs Mn) 814,568

Free Float (%) 50.70 %

52 Wk H/L (Rs) 3122/2510

Avg Daily Volume (1yr) 288,668

Avg Daily Value (Rs Mn) 795

Equity Cap (Rs Mn) 2,894

Face Value (Rs) 10

Bloomberg Code BJAUT IN

Ownership Recent 3M 12M

Promoters 49.3% 0.0% 0.0%

DII 7.7% -0.7% -0.2%

FII 17.4% -0.2% -0.7%

Public 25.6% 0.9% 0.8%

Price % 1M 3M 12M

Absolute 0.2 % -0.1 % 1.9 %

Vs Industry -0.9 % -10.8 % -16.6 %

Hero Motocorp -1.4 % 16.0 % 13.8 %

TVS Motors 3.9 % 17.6 % 88.8 %

Standalone Quarterly EPS forecast

Rs/Share 1Q 2Q 3Q 4Q

EPS (17A) 33.8 38.8 32.0 27.7

EPS (18E) 33.0 35.1 34.9 31.0

BJAUT’s EBITDA margin at 17.2% (-322bps yoy/-126bps qoq, 196bps below EE)

disappointed due to heavy discounts in the entry segment and increased RM costs.

Entry-segment discounts during the peak wedding season suggest weakness in CT and

Platina variants. As highlighted in our earlier notes, even the V family and Avenger

volumes have tapered off from their last year’s monthly averages and are unlikely to

rebound to those levels. We remain negative on BJAUT’s domestic sales but expect

good growth in exports off a lower base yoy. We pare our FY18/FY19 EBITDAM

estimates by 103bps/87bps, leading to a 6.3%/5.5% cut in our EPS estimates. Maintain

REDUCE with a Sep’18 TP of Rs 2,811 (vs. Rs 2,984 earlier).

Entry segment, V and Avenger to pressurize domestic volumes: During the peak

wedding season, BJAUT offered discounts on its entry-segment bikes CT100 and

Platina; this suggests weakness in these brands as other OEMs reported stock-outs for

their large-selling models in this period. Monthly average volumes for V family (V15,

V12) fell to 14k in 1QFY18 vs. 27k in 1QFY17 despite the addition of V12. Similarly, for

Avenger, volumes declined from 19k to 8k in 1QFY17. While management guided for V

family monthly volume of 20-25k during the festive season and 12-15k for Avenger,

this would happen only during peak demand months. Therefore, we expect domestic

volumes to remain weak in 1H and recover in 2H only due to a lower base.

Margins unlikely to touch historical highs as <150cc bikes will remain competitively

priced: If BJAUT has to gain share in the domestic motorcycle market, it has to do

well in executive and entry segments, where its bikes (including V, CT100 and Platina)

are competitively priced and hence lower in mrgin. We already saw the impact of this

on 1Q EBITDAM. As such, management accepted that in percentage terms, margins

would be lower than historical levels.

EBITDA down 20% yoy as raw material costs rise 279bps yoy: RM cost as a percentage

of sales increased 279bps yoy & 220bps qoq due to (1) an increase in RM prices, which

was partially passed on from April-end only, (2) higher discounts on CT100 and Platina,

and (3) passing on of only cost increases related to RM and shift from BS-III to BS-IV

norms; therefore, in percentage terms, margins will tend lower. A&P expenses are

also likely to increase going ahead as the company will intensify promotions to revive

V, Avenger and Dominor volumes. Management guided for

19.5-20% margins for FY18E, including ‘others’ component of other income.

Estimate Revision:

Current Change from previous

(%)

RsMn FY18E FY19E FY18E FY19E

Sales 241,977 273,770 -3.2% -2.1%

EBITDA 44,948 51,302 -8.3% -6.5%

PAT 40,127 45,505 -6.3% -5.5%

EPS 138.7 157.3 -6.3% -5.5%

Consolidated Financials

Rs. Mn YE Mar FY17A FY18E FY19E FY20E

Sales 217,667 241,977 273,770 306,228

EBITDA 44,194 44,948 51,302 57,386

Depreciation 3,073 3,125 3,325 3,588

Interest Expense 14 2 0 0

Other Income 12,222 11,747 12,877 14,562

Reported PAT 40,795 39,803 45,505 50,963

Recurring PAT 40,795 40,127 45,505 50,963

Total Equity 178,566 197,471 220,337 246,920

Gross Debt 1,692 1,692 1,692 1,692

Cash 123,757 138,781 157,439 178,680

Rs. Mn Per Share FY17A FY18E FY19E FY20E

Earnings 141.0 138.7 157.3 176.1

Book Value 617 682 761 853

Dividends 55.0 60.0 65.0 70.0

FCFF 63.5 114.7 132.6 146.9

P/E (x) 20.0 20.3 17.9 16.0

P/B (x) 4.6 4.1 3.7 3.3

EV/EBITDA (x) 15.8 15.2 12.9 11.2

ROE (%) 26 % 21 % 22 % 22 %

Core ROIC (%) 49 % 43 % 47 % 50 %

EBITDA Margin (%) 20 % 19 % 19 % 19 %

Net Margin (%) 19 % 17 % 17 % 17 %

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 2 of 12

Exhibit 01: Domestic quarterly 2W volume mix (in ‘000 units)

Exhibit 02: Quarterly 2W export volume mix (In ‘000 units)

Source: SIAM, Equirus Securities

Exhibit 03: 3W domestic & export sales volumes (In ‘000 units)

Exhibit 04: Export & domestic sales (Rs bn); exports as % of sales vs. EBITDA margins

Source: SIAM, Equirus Securities

319 278 258200 195 181

290230 217 184

231 251204

149 186

5461

57

26 18 13

1345 54

3529 25

3145

36

102109 124

172 164127

126119 128

169

223 218

165

137134

527494 491

462439

379

486 469 475 469

549580

459414 427

0

100

200

300

400

500

600

7003Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

1Q

FY18

>75cc & <=110cc >110cc <=125cc >125cc but <=150cc >150 <= 200 cc >=200cc

235 219 241 248 251

137

244 258214

137172 155 158 158 168

3025

3880

45

39

2426

20

22

2726 22 24

35

5547

56

6062

74

7297

70

79

90 99 75 7385

3435

36

3838

34

38

46

42

35

26 2928 22

41

360331

384

438406

294

389

434

352

284

324 318290 287

349

0

50

100

150

200

250

300

350

400

450

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

1Q

FY18

>75cc & <=110cc >110cc <=125cc >125cc but <=150cc >150 <= 200 cc >=200cc

44 4456

7555 49 51

67 66 71 75 7454 50 52

62 6658

82

84

61

87

86

58 49 4760

4937

60

106 110 114

156

139

110

138

153

124 120 122135

103

87

113

-10

10

30

50

70

90

110

130

150

170

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

1Q

FY18

Domestic Export

41% 42% 43%46%

47%44%

47% 47%

41%38%

36% 35%38%

36%

46%

22.1%18.9%17.6%18.9%

21.7%

17.7%20.4%21.7%21.1%21.5%20.5%21.4%20.6%

18.5%17.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

3Q

FY14

4Q

FY14

1Q

FY15

2Q

FY15

3Q

FY15

4Q

FY15

1Q

FY16

2Q

FY16

3Q

FY16

4Q

FY16

1Q

FY17

2Q

FY17

3Q

FY17

4Q

FY17

1Q

FY18

Domestic Exports

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 3 of 12

Key concall takeaways:

Raw material cost increase, price hikes, EBITDA margins & dealer compensation:

Raw material cost as a percentage of sales increased by 220bps qoq and 279bps

yoy on account of:

1. Metal cost increases from 1 Apr, when quarterly price increases of vendors

came into effect, which contributed ~1.1% of sales.

2. Discounts on CT100 and Platina during the wedding season.

3. A shift from excise free to excise duty zone in Pantnagar, which

contributed around 0.5% of sales.

The company hiked domestic 2W prices by Rs 500-1,000/unit and 3W prices by

Rs 1500-2000/unit from 24 May’17.

From 1 July, BJAUT will effect price increases for 2W/3W in exports markets.

For FY18, we expect EBITDA margin to remain around 19.5-20%.

The Rs 320mn compensation to dealers include three elements: (1) 3W

compensation, (2) price drop over 14-30 June to post GST pricing, (3) payment

of CST and entry tax which included 2% entry tax for Madhya Pradesh and West

Bengal, 1% entry tax for Orissa, and 2% CST provided to dealers on inventory.

CBS should increase cost by Rs 1,000-1,500/bike.

EBITDA margin in the month of May and June was close to 20%.

Margins for exports, 3Ws and spares are over 25%.

BJAUT expects US$-INR realizations of 66.7-66.8 on exports in the remaining

quarters of FY18.

Spare part sales for 1QFY18 stood at Rs 6.51bn (1QFY17: Rs 6.37bn), of which

domestic market contributed Rs 4.6bn and exports the remaining.

Domestic 2W volumes:

BJAUT expects volumes for V to go up to 20-25k/month during the festive season

(September-October).

Avenger volumes should stabilise around 12-15k per month; the company intends

to undertake extensive field activity to revive Avenger volumes.

Advertising for Dominor has increased from June to revive volumes.

The domestic 2W domestic industry is expected to grow by ~7% in FY18.

BJAUT expects 10% volume growth from July.

June-end inventory stood at around 150k, and stocks corrected by 45,000 during

the month.

Pulsar lost volumes in West Bengal, Orissa, Bihar and Uttar Pradesh (UP).

The average inventory with dealers is generally maintained at 4-4.5 weeks,

however currently its lower due to destocking.

The first 10 days of July saw soft retail sales due to pre-GST buying spurred by

discounts in June.

In the V family, focus will be on V15.

No new brand is likely to be launched in FY18.

BJAUT has around 650 2W primary dealers in the domestic market.

Domestic 3W volumes:

BJAUT’s 3W monthly run-rate going ahead should be ~20-22k driven by:

1. Mandatory conversion of 2-stroke 3Ws to 4-stroke 3Ws in Karnataka.

2. A ban on diesel vehicles in Bengaluru, which should benefit BJAUT’s CNG

portfolio.

3. More permits in Delhi and a shift from quota permits in Maharashtra

BJAUT expects 5% growth in domestic 3Ws next year, mainly driven by goods

vehicles.

The company doesn’t see any market share losses with the opening of

Maharashtra permits.

Electric 3Ws are likely to be launched in one year.

3Ws would be first to move to electric vehicle platform; therefore, BJAUT is

moving swiftly to launch the product.

Exports:

BJAUT expects exports for H1 at ~0.8mn and to close FY18 at 1.6mn.

The company’s export mix has changed with improved proportion of high-value

bikes.

Export margins have gone up despite a decline in exports to Nigeria.

The company is doing well in the export markets of Turkey, Iran and South East

Asia.

3W exports to Bangladesh, Egypt and Peru have picked up, while exports to Sri

Lanka have declined.

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 4 of 12

Quarterly Results Table (Standalone)

Rs Mn 1QFY18 1QFY18E 4QFY17 1QFY17 % Change

Comments 1QFY18E 4QFY17 1QFY17

Net Sales 54,424 54,320 48,973 57,480 0% 11% -5%

Raw Material 38,093 37,101 33,203 38,628 3% 15% -1%

Employee Cost 2,725 2,390 2,273 2,683 14% 20% 2%

Other Expenses 4,222 4,400 4,438 4,405 -4% -5% -4%

Total Expenditures 45,040 43,891 39,913 45,716 3% 13% -1%

EBITDA 9,384 10,429 9,060 11,763 -10% 4% -20%

EBITDA before MTM 9,384 10,429 9,060 11,763 -10% 4% -20%

Depreciation 753 769 757 775 -2% -1% -3%

EBIT 8,631 9,661 8,303 10,989 -11% 4% -21%

Interest 2 0 2 2 0% 9%

Other Income 4,573 2,816 2,936 2,671 62% 56% 71%

PBT 13,201 12,477 11,236 13,657 6% 17% -3%

Tax 3,642 3,743 3,218 3,873 -3% 13% -6%

Recurring PAT 9,559 8,734 8,018 9,784 9% 19% -2%

Extraordinaries 324 0 -1,259 190

Reported PAT 9,235 8,734 9,277 9,594 6% 0% -4%

EPS (Rs) 33.0 30.2 27.7 33.8 9% 19% -2%

Gross Margin 30.0% 31.7% 32.2% 32.8% -169 bps -220 bps -279 bps

EBITDA Margin 17.2% 19.2% 18.5% 20.5% -196 bps -126 bps -322 bps

Adj EBITDA Margin 17.2% 19.2% 18.5% 20.5% -196 bps -126 bps -322 bps

EBIT Margin 15.9% 17.8% 17.0% 19.1% -193 bps -110 bps -326 bps

PBT Margin 24.3% 23.0% 22.9% 23.8% 129 bps 131 bps 50 bps

PAT Margin 17.0% 16.1% 18.9% 16.7% 89 bps -197 bps 28 bps

Tax Rate 27.6% 30.0% 28.6% 28.4% -241 bps -105 bps -77 bps

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 5 of 12

1QFY18 1QFY18E 4QFY17 1QFY17 % Change

Comments 1QFY18E 4QFY17 1QFY17

2W Volumes 775,714 775,714 701,017 872,540 0.0% 10.7% -11.1%

Domestic 2W 426,562 426,562 413,539 548,880 0.0% 3.1% -22.3%

Export 2W 349,152 349,152 287,478 323,660 0.0% 21.5% 7.9%

3W Volumes 112,720 112,720 86,610 122,193 0.0% 30.1% -7.8%

Domestic 3W 52,347 52,347 50,037 75,204 0.0% 4.6% -30.4%

Export 3W 60,373 60,373 36,573 46,989 0.0% 65.1% 28.5%

Domestic Volumes 478,909 478,909 463,576 624,084 0.0% 3.3% -23.3%

Export Volumes 409,525 409,525 324,051 370,649 0.0% 26.4% 10.5%

Domestic Sales (Rs mn) 29,634 29,419 31,183 36,910 0.7% -5.0% -19.7%

Export Sales (Rs mn) 24,790 25,005 17,790 20,570 -0.9% 39.3% 20.5%

ASP (Rs/unit) 61,258 61,141 62,178 57,784 0.2% -1.5% 6.0%

Domestic ASP (Rs/unit) 61,878 61,213 67,267 59,142 1.1% -8.0% 4.6%

Export ASP (Rs/unit) 60,534 61,058 54,899 55,497 -0.9% 10.3% 9.1%

EBITDA/Vehicle (Rs/unit) 10,562 11,739 11,503 11,826 -10.0% -8.2% -10.7%

Cost items as % of Sales

RM 70.0% 68.3% 67.8% 67.2% 169 bps 220 bps 279 bps

Employee Cost 5.0% 4.4% 4.6% 4.7% 61 bps 37 bps 34 bps

Other Expenses 7.8% 8.1% 9.1% 7.7% -34 bps -130 bps 9 bps

Adj Other Expenses 0.0% 0.0% 7.8% 8.8% 0 bps -782 bps -883 bps

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 6 of 12

Company Snapshot

How we differ from Consensus

- Equirus Consensus % Diff Comment

EPS FY18E 138.7 150.0 -8 % Below consensus due to lower margin

assumptions FY19E 157.3 166.3 -5 %

Sales FY18E 241,977 247,459 -2 %

FY19E 273,770 276,849 -1 %

PAT FY18E 39,803 43,155 -8 %

FY19E 45,505 48,060 -5 %

Key Assumptions:

FY17A FY18E FY19E FY20E

2W Domestic Sales 2,001,391 2,024,972 2,205,702 2,382,158

yoy change 5.4% 1.2% 8.9% 8.0%

2W Export Sales 1,218,541 1,393,963 1,548,042 1,702,846

yoy change -16.5% 14.4% 11.1% 10.0%

Total 2W Sales 3,219,932 3,418,936 3,753,744 4,085,004

yoy change -4.1% 6.2% 9.8% 8.8%

3W Domestic Sales 253,226 267,300 314,994 340,194

yoy change -0.7% 5.6% 17.8% 8.0%

3W Export Sales 192,792 225,102 237,270 256,251

yoy change -31.1% 16.8% 5.4% 8.0%

Total 3W Sales 446,018 492,403 552,264 596,445

yoy change -16.6% 10.4% 12.2% 8.0%

ASP 59,375 61,865 63,578 65,413

yoy change 2.3% 4.2% 2.8% 2.9%

EBITDA Margin 20.3% 18.6% 18.8% 18.7%

Tax Rate 28.3% 29.4% 30.0% 30.0%

NCW Days -2 0 1 2 Risk to our view: A sharp recovery in domestic volumes would be an upside risk to our

volume estimates.

Key triggers

Margin decline & volume pressure

Sensitivity to Key Variables % Change % Impact on EPS

EBITDA Margin 1 % 5 %

Volume 1 % 1 %

- - -

DCF Valuations & Assumptions

Rf Beta Ke Term. Growth Debt/IC in Term. Yr

6.8 % 0.9 11.9 % 2.5 % 2.2 %

- FY18E FY19E FY20-22E FY23-27E FY28-32E

Sales Growth 11 % 13 % 11 % 9 % 8 %

NOPAT Margin 12 % 12 % 12 % 12 % 12 %

IC Turnover 3.51 3.76 3.95 3.95 3.95

RoIC 43.5 % 47.4 % 50.6 % 50.7 % 50.4 %

Years of strong growth 1 2 5 10 15

Valuation as on date (Rs) 1,536 1,651 1,853 2,083 2,247

Valuation as of 30thSep'18 1,756 1,888 2,118 2,382 2,569

On P/E basis, our Sep’18 TP stands at Rs 2,811 set at 19x TTM EPS. Our DCF-based Sep’18

fair value is Rs 2,569.

Company Description:

Bajaj Auto is the flagship company of Bajaj group, one among the Top 10 business houses

in India. Company is also India’s largest 2W & 3W exporter, accounting for 2/3rd of India’s

2W export. Company came into existence as M/s Bachraj Trading Corporation Private

Limited in 1945. In 1972 company launched their 1st scooter by the name ‘Chetak’. The

Rear Engine Auto rickshaw was introduced in 1977 &Bajaj achieved production and sales

of 100,000 vehicles in a single financial year. Company entered into the motorcycle

segment in 1986 with launch of Bajaj M-80 and the Kawasaki Bajaj KB100.

Comparable valuation Mkt Cap

Rs. Mn.

Price

Target

Target

Date

EPS P/E BPS P/B RoE Div Yield

Company Reco. CMP FY17A FY18E FY19E FY17A FY18E FY19E FY17A FY18E FY17A FY18E FY19E FY17A FY18E

Bajaj Auto REDUCE 2,815 816,666 2,811 30th Sep' 18 141.0 138.7 157.3 20.0 20.3 17.9 617 4.1 26% 21% 22% 2% 2%

Hero Motocorp REDUCE 3,716 742,073 3,331 30th June'18 169.1 184.1 189.8 22.0 20.2 19.6 464 6.9 39% 37% 33% 2% 2%

TVSMOTOR NA 567 269 NA NA 16.2 15.6 20.8 35.0 36.2 27.3 18 27.4 12% 22% 23% 0% 0%

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 7 of 12

Standalone Quarterly Earnings Forecast and Key Drivers Rs in Mn 1Q17A 2Q17A 3Q17A 4Q17A 1Q18A 2Q18E 3Q18E 4Q18E 1Q19E 2Q19E 3Q19E 4Q19E FY17A FY18E FY19E FY20E

Revenue 57,480 60,545 50,669 48,973 54,424 65,057 65,066 57,429 65,591 71,170 72,757 64,252 217,667 241,976 273,769 306,227

EBITDA 11,763 12,961 10,439 9,060 9,384 12,549 12,363 10,682 11,829 13,728 13,824 11,951 44,224 44,977 51,332 57,417

Depreciation 775 770 772 757 753 780 791 802 813 824 835 853 3,073 3,125 3,325 3,588

EBIT 10,989 12,192 9,667 8,303 8,631 11,769 11,572 9,880 11,016 12,904 12,989 11,098 41,151 41,852 48,007 53,830

Interest 2 7 3 2 2 0 0 0 0 0 0 0 14 2 0 0

Other Income 2,671 3,420 3,193 2,936 4,573 2,737 2,849 2,935 3,239 3,064 3,245 3,326 12,220 13,094 12,874 14,559

PBT 13,657 15,605 12,858 11,236 13,201 14,507 14,421 12,815 14,255 15,969 16,234 14,424 53,356 54,944 60,882 68,389

Tax 3,873 4,378 3,612 3,218 3,642 4,352 4,326 3,844 4,276 4,791 4,870 4,327 15,081 16,165 18,265 20,517

Recurring PAT 9,784 11,228 9,246 8,018 9,559 10,155 10,095 8,970 9,978 11,178 11,364 10,097 38,276 38,779 42,617 47,872

Extraordinary 190 -325 254 -1,259 324 0 0 0 0 0 0 0 -1,142 324 0 0

Reported PAT 9,594 11,553 8,992 9,277 9,235 10,155 10,095 8,970 9,978 11,178 11,364 10,097 39,417 38,455 42,617 47,872

EPS (Rs) 33.81 38.80 31.95 27.71 33.03 35.09 34.89 31.00 34.48 38.63 39.27 34.89 132.27 134.01 147.28 165.44

Key Drivers

2W Domestic Volumes 548,880 579,545 459,427 413,539 426,562 556,363 537,530 504,518 490,546 589,745 580,532 544,879 2,001,391 2,024,972 2,205,702 2,382,158

2W Export Volumes 323,660 317,869 289,534 287,478 349,152 346,477 353,361 344,974 398,749 381,125 388,697 379,471 1,218,541 1,393,963 1,548,042 1,702,846

3W Domestic Volumes 75,204 74,383 53,602 50,037 52,347 76,614 79,795 58,543 82,845 82,744 86,179 63,227 253,226 267,300 314,994 340,194

3W Export Volumes 46,989 60,148 49,082 36,573 60,373 61,952 63,278 39,499 59,981 66,289 68,340 42,659 192,792 225,102 237,270 256,251

- - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - -

Sequential Growth (%)

Revenue 7 % 5 % -16 % -3 % 11 % 20 % 0 % -12 % 14 % 9 % 2 % -12 % - - - -

EBITDA 2 % 10 % -19 % -13 % 4 % 34 % -1 % -14 % 11 % 16 % 1 % -14 % - - - -

EBIT 2 % 11 % -21 % -14 % 4 % 36 % -2 % -15 % 11 % 17 % 1 % -15 % - - - -

Recurring PAT 3 % 15 % -18 % -13 % 19 % 6 % -1 % -11 % 11 % 12 % 2 % -11 % - - - -

EPS 3 % 15 % -18 % -13 % 19 % 6 % -1 % -11 % 11 % 12 % 2 % -11 % - - - -

Yearly Growth (%)

Revenue 3 % 0 % -9 % -9 % -5 % 7 % 28 % 17 % 21 % 9 % 12 % 12 % -4 % 11 % 13 % 12 %

EBITDA 3 % -2 % -11 % -21 % -20 % -3 % 18 % 18 % 26 % 9 % 12 % 12 % -8 % 2 % 14 % 12 %

EBIT 3 % -2 % -12 % -23 % -21 % -3 % 20 % 19 % 28 % 10 % 12 % 12 % -8 % 2 % 15 % 12 %

Recurring PAT 2 % 7 % -5 % -16 % -2 % -10 % 9 % 12 % 4 % 10 % 13 % 13 % -3 % 1 % 10 % 12 %

EPS 2 % 7 % -5 % -16 % -2 % -10 % 9 % 12 % 4 % 10 % 13 % 13 % -3 % 1 % 10 % 12 %

Margin (%)

EBITDA 20 % 21 % 21 % 18 % 17 % 19 % 19 % 19 % 18 % 19 % 19 % 19 % 20 % 19 % 19 % 19 %

EBIT 19 % 20 % 19 % 17 % 16 % 18 % 18 % 17 % 17 % 18 % 18 % 17 % 19 % 17 % 18 % 18 %

PBT 24 % 26 % 25 % 23 % 24 % 22 % 22 % 22 % 22 % 22 % 22 % 22 % 25 % 23 % 22 % 22 %

PAT 17 % 19 % 18 % 16 % 18 % 16 % 16 % 16 % 15 % 16 % 16 % 16 % 18 % 16 % 16 % 16 %

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 8 of 12

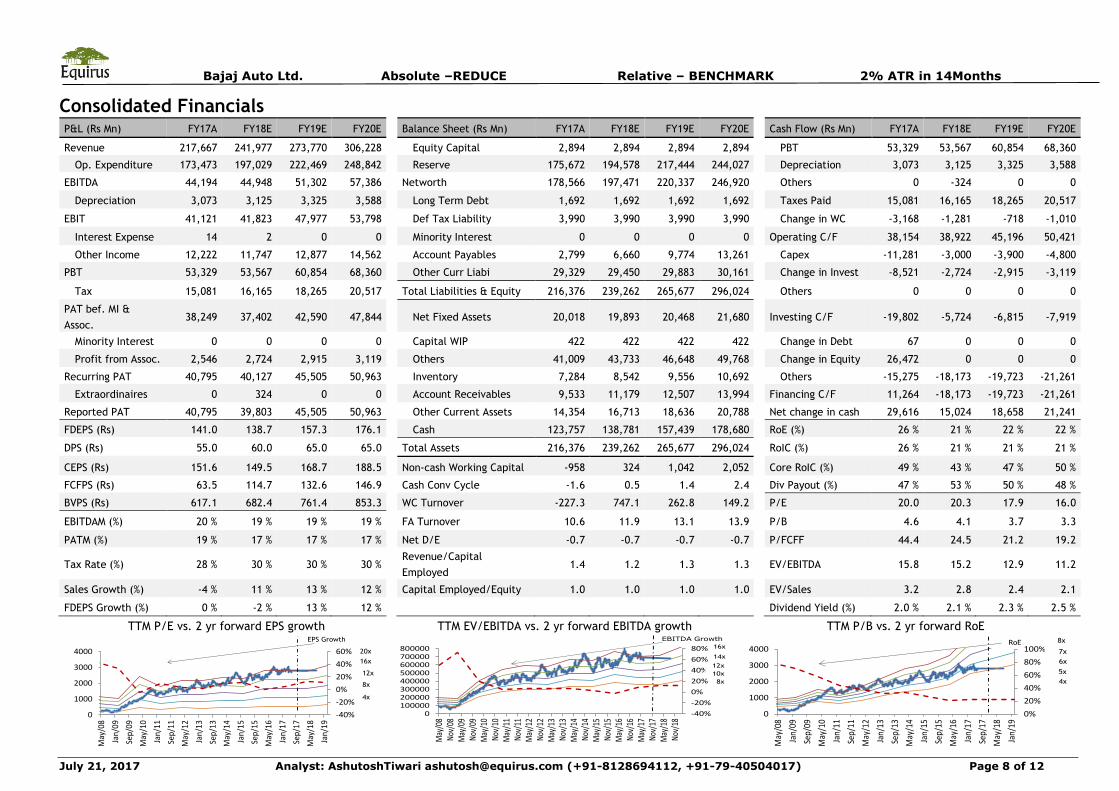

Consolidated Financials P&L (Rs Mn) FY17A FY18E FY19E FY20E Balance Sheet (Rs Mn) FY17A FY18E FY19E FY20E Cash Flow (Rs Mn) FY17A FY18E FY19E FY20E

Revenue 217,667 241,977 273,770 306,228 Equity Capital 2,894 2,894 2,894 2,894 PBT 53,329 53,567 60,854 68,360

Op. Expenditure 173,473 197,029 222,469 248,842 Reserve 175,672 194,578 217,444 244,027 Depreciation 3,073 3,125 3,325 3,588

EBITDA 44,194 44,948 51,302 57,386 Networth 178,566 197,471 220,337 246,920 Others 0 -324 0 0

Depreciation 3,073 3,125 3,325 3,588 Long Term Debt 1,692 1,692 1,692 1,692 Taxes Paid 15,081 16,165 18,265 20,517

EBIT 41,121 41,823 47,977 53,798 Def Tax Liability 3,990 3,990 3,990 3,990 Change in WC -3,168 -1,281 -718 -1,010

Interest Expense 14 2 0 0 Minority Interest 0 0 0 0 Operating C/F 38,154 38,922 45,196 50,421

Other Income 12,222 11,747 12,877 14,562 Account Payables 2,799 6,660 9,774 13,261 Capex -11,281 -3,000 -3,900 -4,800

PBT 53,329 53,567 60,854 68,360 Other Curr Liabi 29,329 29,450 29,883 30,161 Change in Invest -8,521 -2,724 -2,915 -3,119

Tax 15,081 16,165 18,265 20,517 Total Liabilities & Equity 216,376 239,262 265,677 296,024 Others 0 0 0 0

PAT bef. MI &

Assoc. 38,249 37,402 42,590 47,844 Net Fixed Assets 20,018 19,893 20,468 21,680 Investing C/F -19,802 -5,724 -6,815 -7,919

Minority Interest 0 0 0 0 Capital WIP 422 422 422 422 Change in Debt 67 0 0 0

Profit from Assoc. 2,546 2,724 2,915 3,119 Others 41,009 43,733 46,648 49,768 Change in Equity 26,472 0 0 0

Recurring PAT 40,795 40,127 45,505 50,963 Inventory 7,284 8,542 9,556 10,692 Others -15,275 -18,173 -19,723 -21,261

Extraordinaires 0 324 0 0 Account Receivables 9,533 11,179 12,507 13,994 Financing C/F 11,264 -18,173 -19,723 -21,261

Reported PAT 40,795 39,803 45,505 50,963 Other Current Assets 14,354 16,713 18,636 20,788 Net change in cash 29,616 15,024 18,658 21,241

FDEPS (Rs) 141.0 138.7 157.3 176.1 Cash 123,757 138,781 157,439 178,680 RoE (%) 26 % 21 % 22 % 22 %

DPS (Rs) 55.0 60.0 65.0 65.0 Total Assets 216,376 239,262 265,677 296,024 RoIC (%) 26 % 21 % 21 % 21 %

CEPS (Rs) 151.6 149.5 168.7 188.5 Non-cash Working Capital -958 324 1,042 2,052 Core RoIC (%) 49 % 43 % 47 % 50 %

FCFPS (Rs) 63.5 114.7 132.6 146.9 Cash Conv Cycle -1.6 0.5 1.4 2.4 Div Payout (%) 47 % 53 % 50 % 48 %

BVPS (Rs) 617.1 682.4 761.4 853.3 WC Turnover -227.3 747.1 262.8 149.2 P/E 20.0 20.3 17.9 16.0

EBITDAM (%) 20 % 19 % 19 % 19 % FA Turnover 10.6 11.9 13.1 13.9 P/B 4.6 4.1 3.7 3.3

PATM (%) 19 % 17 % 17 % 17 % Net D/E -0.7 -0.7 -0.7 -0.7 P/FCFF 44.4 24.5 21.2 19.2

Tax Rate (%) 28 % 30 % 30 % 30 % Revenue/Capital

Employed 1.4 1.2 1.3 1.3 EV/EBITDA 15.8 15.2 12.9 11.2

Sales Growth (%) -4 % 11 % 13 % 12 % Capital Employed/Equity 1.0 1.0 1.0 1.0 EV/Sales 3.2 2.8 2.4 2.1

FDEPS Growth (%) 0 % -2 % 13 % 12 % Dividend Yield (%) 2.0 % 2.1 % 2.3 % 2.5 %

TTM P/E vs. 2 yr forward EPS growth

TTM EV/EBITDA vs. 2 yr forward EBITDA growth

TTM P/B vs. 2 yr forward RoE

4x

8x

12x

16x

20x

-40%

-20%

0%

20%

40%

60%

0

1000

2000

3000

4000

May/08

Jan/09

Sep/09

May/10

Jan/11

Sep/11

May/12

Jan/13

Sep/13

May/14

Jan/15

Sep/15

May/16

Jan/17

Sep/17

May/18

Jan/19

EPS Growth

-40%

-20%

0%

20%

40%

60%

80%

0100000200000300000400000500000600000700000800000

May/08

Nov/08

May/09

Nov/09

May/10

Nov/10

May/11

Nov/11

May/12

Nov/12

May/13

Nov/13

May/14

Nov/14

May/15

Nov/15

May/16

Nov/16

May/17

Nov/17

May/18

Nov/18

8x

10x

12x

14x

16x

EBITDA Growth

0%

20%

40%

60%

80%

100%

0

1000

2000

3000

4000

May/08

Jan/09

Sep/09

May/10

Jan/11

Sep/11

May/12

Jan/13

Sep/13

May/14

Jan/15

Sep/15

May/16

Jan/17

Sep/17

May/18

Jan/19

RoE

4x

5x

6x

7x

8x

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 9 of 12

Historical Consolidated Financials P&L (Rs Mn) FY14A FY15A FY16A FY17A Balance Sheet (Rs Mn) FY14A FY15A FY16A FY17A Cash Flow (Rs Mn) FY14A FY15A FY16A FY17A

Revenue 201,583 216,143 225,865 217,667 Equity Capital 2,894 2,894 2,894 2,894 PBT 46,549 44,232 54,575 53,329

Op. Expenditure 160,031 175,010 178,054 173,473 Reserve 98,779 108,060 127,561 175,672 Depreciation 1,813 2,675 3,072 3,073

EBITDA 41,552 41,132 47,811 44,194 Networth 101,673 110,953 130,454 178,566 Others -2,454 -6,460 0 0

Depreciation 1,813 2,675 3,072 3,073 Long Term Debt 577 1,118 1,625 1,692 Taxes Paid 13,152 12,853 16,177 15,081

EBIT 39,739 38,458 44,739 41,121 Def Tax Liability 3,518 2,816 2,656 3,990 Change in WC 3,716 -6,457 -8,908 -3,168

Interest Expense 8 65 11 14 Minority Interest 1 0 0 0 Operating C/F 36,472 21,138 32,562 38,154

Other Income 6,818 5,840 9,846 12,222 Account Payables 21,118 17,998 20,271 2,799 Capex -2,540 -2,949 -4,489 -11,281

PBT 46,549 44,232 54,575 53,329 Other Curr Liabi 26,191 26,770 9,260 29,329 Change in Invest -24,403 -4,185 20,685 -8,521

Tax 13,887 13,492 16,177 15,081 Total Liabilities & Equity 153,078 159,656 164,266 216,376 Others 2,156 2,994 0 0

PAT bef. MI & Assoc. 32,662 30,740 38,398 38,249 Net Fixed Assets 20,064 19,172 20,257 20,018 Investing C/F -24,788 -4,140 16,197 -19,802

Minority Interest -4 0 0 0 Capital WIP 1,441 2,549 522 422 Change in Debt -271 0 507 67

Profit from Assoc. 1,455 2,137 2,214 2,546 Others 75,328 42,266 23,941 41,009 Change in Equity 940 467 -1,956 26,472

Recurring PAT 34,121 32,877 40,613 40,795 Inventory 6,412 8,142 7,191 7,284 Others -13,015 -16,909 -17,101 -15,275

Extraordinaires 0 0 0 0 Account Receivables 7,962 7,170 7,179 9,533 Financing C/F -12,347 -16,442 -18,550 11,264

Reported PAT 34,121 32,877 40,613 40,795 Other Current Assets 13,964 16,424 11,036 14,354 Net change in cash -662 556 30,208 29,616

EPS (Rs) 117.9 113.6 140.3 141.0 Cash 27,906 63,933 94,141 123,757 RoE (%) 37 % 31 % 34 % 26 %

DPS (Rs) 50.0 50.0 55.0 55.0 Total Assets 153,078 159,656 164,266 216,376 RoIC (%) 36 % 30 % 33 % 26 %

CEPS (Rs) 124.2 122.9 151.0 151.6 Non-cash Working Capital -18,970 -13,033 -4,125 -958 Core RoIC (%) 89 % 67 % 66 % 49 %

FCFPS (Rs) 40.4 58.9 168.5 63.5 Cash Conv Cycle -34.3 -22.0 -6.7 -1.6 Div Payout (%) 50 % 52 % 47 % 47 %

BVPS (Rs) 351.4 383.4 450.8 617.1 WC Turnover -10.6 -16.6 -54.8 -227.3 P/E 23.9 24.8 20.1 0.0

EBITDAM (%) 21 % 19 % 21 % 20 % FA Turnover 9.4 10.0 10.9 10.6 P/B 8.0 7.3 6.2 0.0

PATM (%) 17 % 15 % 18 % 19 % Net D/E -0.3 -0.6 -0.7 -0.7 P/FCFF 69.7 47.8 16.7 44.4

Tax Rate (%) 30 % 31 % 30 % 28 % Revenue/Capital

Employed 2.1 2.0 1.8 1.4 EV/EBITDA 19.1 18.4 15.2 15.8

Sales growth (%) 1 % 7 % 4 % -4 % Capital Employed/Equity 1.0 1.0 1.0 1.0 EV/Sales 3.9 3.5 3.2 3.2

FDEPS growth (%) 9 % -4 % 24 % 0 % Dividend Yield (%) 1.8 % 1.8 % 2.0 % 2.0 %

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112 +91 79-40504017) Page 10 of 12

Before reading this report, you must refer to the disclaimer on the last page.

Equirus Securities

Research Analysts Sector/Industry Email Equity Sales E-mail

Abhishek Shindadkar IT Services [email protected] 91-22-43320643 Vishad Turakhia [email protected] 91-22-43320633

Ashutosh Tiwari Auto, Metals & Mining [email protected] 91-79-61909517 Subham Sinha [email protected] 91-22-43320631

Depesh Kashyap Mid-Caps [email protected] 91-79-61909528 Sweta Sheth [email protected] 91-22-43320634

Devam Modi Power & Infrastructure [email protected] 91-79-61909516 Viral Desai [email protected] 91-22-43320635

Dhaval Dama FMCG, Mid-Caps [email protected] 91-79-61909518 Binoy Dharia [email protected] 91-22-43320632

Manoj Gori Consumer Durables [email protected] 91-79-61909523 Dealing Room E-mail

Maulik Patel Oil and Gas [email protected] 91-79-61909519 Ashish Shah [email protected] 91-22-43320662

Praful Bohra Pharmaceuticals [email protected] 91-79-61909532 Ilesh Savla [email protected] 91-22-43320666

Rohan Mandora Banking & Financial Services [email protected] 91-79-61909529 Manoj Kejriwal [email protected] 91-22-43320663

Associates E-mail Dharmesh Mehta [email protected] 91-22-43320661

Ankit Choudhary [email protected] 91-79-61909533 Sandip Amrutiya [email protected] 91-22-43320660

Ashdeep Kaur [email protected] 91-79-61909527 Compliance Officer E-mail

Bharat Celly [email protected] 91-79-61909524 Jay Soni [email protected] 91-79-61909561

Harshit Patel [email protected] 91-79-61909522

Meet Chande [email protected] 91-79-61909513

Parva Soni [email protected] 91-79-61909521

Pranav Mehta [email protected] 91-79-61909514

Ronak Soni [email protected] 91-79-61909525

Samkit Shah [email protected] 91-79-61909520

Shreepal Doshi [email protected] 91-79-61909541

Vikas Jain [email protected] 91-79-61909531

Rating & Coverage Definitions: Absolute Rating • LONG : Over the investment horizon, ATR >= Ke for companies with Free Float market cap > Rs 5 billion and ATR >= 20% for rest of the companies • ADD: ATR >= 5% but less than Ke over investment horizon • REDUCE: ATR >= negative 10% but <5% over investment horizon • SHORT: ATR < negative 10% over investment horizon Relative Rating • OVERWEIGHT: Likely to outperform the benchmark by at least 5% over investment horizon • BENCHMARK: likely to perform in line with the benchmark • UNDERWEIGHT: likely to under-perform the benchmark by at least 5% over investment horizon Investment Horizon Investment Horizon is set at a minimum 3 months to maximum 18 months with target date falling on last day of a calendar quarter. Lite vs. Regular Coverage vs. Spot Coverage We aim to keep our rating and estimates updated at least once a quarter for Regular Coverage stocks. Generally, we would have access to the company and we would maintain detailed financial model for Regular coverage companies. We intend to publish updates on Lite coverage stocks only an opportunistic basis and subject to our ability to contact the management. Our rating and estimates for Lite coverage stocks may not be current. Spot coverage is meant for one-off coverage of a specific company and in such cases, earnings forecast and target price are optional. Spot coverage is meant to stimulate discussion rather than provide a research opinion.

Registered Office:

Equirus Securities Private Limited

Unit No. 1201, 12th Floor, C Wing, Marathon Futurex,

N M Joshi Marg, Lower Parel,

Mumbai-400013.

Tel. No: +91 – (0)22 – 4332 0600

Fax No: +91- (0)22 – 4332 0601

Corporate Office:

3rd floor, House No. 9,

Magnet Corporate Park, Near Zydus Hospital, B/H Intas Sola Bridge,

S.G. Highway Ahmedabad-380054

Gujarat

Tel. No: +91 (0)79 - 6190 9550

Fax No: +91 (0)79 – 6190 9560

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 11 of 12

© 2017 Equirus Securities Private Limited. All rights reserved. For Private Circulation only. This report or any portion hereof may not

be reprinted, sold or redistributed without the written consent of Equirus Securities Private Limited

Analyst Certification

I, Ashutosh Tiwari, author to this report, hereby certify that all of the views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also

certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Disclosures

Equirus Securities Private Limited (ESPL) having Corporate Identification Number U65993MH2007PTC176044 is registered in India with Securities and Exchange Board of India (SEBI) as a trading member on the

Capital Market (Reg. No. INB231301731), Futures & Options Segment (Reg. No.INF231301731) of the National Stock Exchange of India Ltd. (NSE) and on Cash Segment (Reg. No.INB011301737) of Bombay Stock

Exchange Limited (BSE).ESPL is also registered with SEBI as Research Analyst under SEBI (Research Analyst) Regulations, 2014 (Reg. No. INH000001154), as a Portfolio Manager under SEBI (Portfolio Managers

Regulations, 1993 (Reg. No. INP000005216) and as a Depository Participant of the Central Depository Services (India) Limited (Reg. No. IN-DP-324-2017). There are no disciplinary actions taken by any regulatory

authority against ESPL. ESPL is a subsidiary of Equirus Capital Pvt. Ltd. (ECPL) which is registered with SEBI as Category I Merchant Banker and provides investment banking services including but not limited to

merchant banking services, private equity, mergers & acquisitions and structured finance.

As ESPL and its associates are engaged in various financial services business, it might have: - (a) received compensation (except in connection with the preparation of this report) from the subject company for

investment banking or merchant banking or brokerage services in the past twelve months;(b) managed or co-managed public offering of securities for the subject company in the past twelve months; or (c) have

received a mandate from the subject company; or (d) might have other financial, business or other interests in entities including the subject company (ies) mentioned in this Report. ESPL & its associates, their

directors and employees may from time to time have positions or options in the company and buy or sell the securities of the company (ies) mentioned herein. ESPL and its associates collectively do not own (in

their proprietary position) 1% or more of the equity securities of the subject company mentioned in the report as the last day of the month preceding the publication of the research report. ESPL or its Analyst or

Associates did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ESPL nor

Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or

brokerage service transactions. ESPL has not been engaged in market making activity for the subject company.

The Research Analyst engaged in preparation of this Report:-

(a) has not received any compensation from the subject company in the past twelve months; (b) has not managed or co-managed public offering of securities for the subject company in the past twelve months;

(c) has not received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (d) has not received any compensation for products

or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months; (e) has not received any compensation or other benefits from the subject

company or third party in connection with the research report; (f) might have served as an officer, director or employee of the subject company; (g) is not engaged in market making activity for the subject

company.

This document is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ESPL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein

may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession of this document are required to inform themselves of, and to observe, such applicable

restrictions. Please delete this document if you are not authorized to view the same. By reading this document you represent and warrant that you have full authority and all rights necessary to view and read this

document without subjecting ESPL and affiliates to any registration or licensing requirement within such jurisdiction.

This document has been prepared solely for information purpose and does not constitute a solicitation to any person to buy, sell or subscribe any security. ESPL or its affiliates are not soliciting any action based on

this report. The information and opinions contained herein is from publicly available data or based on information obtained in good faith from sources believed to be reliable but ESPL provides no guarantee as to

its accuracy or completeness. The information contained herein is as on date of this report, and is subject to change or modification and any such changes could impact our interpretation of relevant information

contained herein. While we would endeavour to update the information herein on reasonable basis, ESPL and its affiliates, their directors and employees are under no obligation to update or keep the information

current. Also there may be regulatory, compliance, or other reasons that may prevent ESPL and its group companies from doing so. This document is prepared for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the

securities of companies referred to in this document including the merits and risks involved. This document is intended for general circulation and does not take into account the specific investment objectives,

financial situation or particular needs of any particular person. ESPL and its group companies, employees, directors and agents accept no liability, and disclaim all responsibility, for the consequences of you or

anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. ESPL/its affiliates do and seek to do business with companies covered in its

research report. Thus, investors should be aware that the firm may have conflict of interest.

Bajaj Auto Ltd. Absolute –REDUCE Relative – BENCHMARK 2% ATR in 14Months

July 21, 2017 Analyst: AshutoshTiwari [email protected] (+91-8128694112, +91-79-40504017) Page 12 of 12

A graph of daily closing prices of securities is available at http://www.nseindia.com/ChartApp/install/charts/mainpage.jsp and www.bseindia.com (Choose a company from the list on the browser and select the

“three years” period in the price chart).

Disclosure of Interest statement for the subject Company Yes/No If Yes, nature of such interest

Research Analyst’ or Relatives’ financial interest No

Research Analyst’ or Relatives’ actual/beneficial ownership of 1% or more No

Research Analyst’ or Relatives’ material conflict of interest No

Disclaimer for U.S. Persons

ESPL/its affiliates are not a registered broker–dealer under the U.S. Securities Exchange Act of 1934, as amended (the“1934 act”) and under applicable state laws in the United States. In addition Equirus is not a

registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the “Acts”), and under applicable state laws in the United States.

Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by Equirus, including the products and services described herein are not available to or intended

for U.S. persons. The information contained in this Report is not intended for any person who is a resident of the United States of America or a resident of any jurisdiction, the laws of which imposes prohibition on

soliciting the securities business in that jurisdiction without going through the registration requirements and/ or prohibit the use of any information contained in this report. This Report and its respective contents

do not constitute an offer or invitation to purchase or subscribe for any securities or solicitation of any investments or investment services and/or shall not be considered as an advertisement tool. "U.S. Persons"

are generally defined as a natural person, residing in the United States or any entity organized or incorporated under the laws of the United States. US Citizens living abroad may also be deemed "US Persons" under

certain rules.