baader bank german corporate day - k+s aktiengesellschaft

TRANSCRIPT

Baader Bank GermanCorporate Day

K+S Group

Lutz Grüten, Head of Investor Relations

Toronto, 17 January 2019

1

K+S Group

K+S Group

Disclaimer

No reliance may be placed for any purpose whatsoever on the information or opinions contained in the Presentation or on its completeness, accuracy of fairness. No

representation or warranty, express or implied, is made or given by or on behalf of the Company or any of its respective directors, officers, employees, agents or

advisers as to the accuracy, completeness or fairness of the information or opinions contained in the Presentation and no responsibility or liability is accepted by any of

them for any such information or opinions. In particular, no representation or warranty, express or implied, is given as to the achievement or reasonableness of, and no

reliance should be placed on any projections, targets, ambitions, estimates or forecasts contained in this Presentation and nothing in this Presentation is or should be

relied on as a promise or representation as to the future.

This Presentation contains facts and forecasts that relate to the future development of the K+S Group and its companies. The forecasts are estimates that we have made

on the basis of all the information available to us at this moment in time. Should the assumptions underlying these forecasts prove not to be correct or should certain

risks – such as those referred to in the Annual Report – materialise, actual developments and events may deviate from current expectations. Given these risks,

uncertainties and other factors, recipients of this document are cautioned not to place undue reliance on these forecasts.

This Presentation is subject to change. In particular, certain financial results presented herein are unaudited, and may still be undergoing review by the Company’s

accountants. The Company may not notify you of changes and disclaims any obligation to update or revise any statements, in particular forward-looking statements, to

reflect future events or developments, save for the making of such disclosures as are required by the provisions of statue. Thus statements contained in this

Presentation should not be unduly relied upon and past events or performance should not be taken as a guarantee or indication of future events or performance.

This Presentation has been prepared for information purposes only. It does not constitute an offer, an invitation or a recommendation to purchase or sell securities

issued by K+S Aktiengesellschaft or any company of the K+S Group in any jurisdiction.

Current Trading

3

K+S Group

K+S Group

Potash Market update

Strong demand holds across all regions

Many producers are sold out

Recovery of MOP prices continued

Global demand 2018 again slightly up to ~72m tons KCl

But:

European MOP and Specialty prices are lagging behind

Pricing (Source: FMB)

80%

90%

100%

110%

120%

130%

140%

Q1/17 Q2/17 Q3/17 Q4/17 Q1/18 Q2/18 Q3/18 Q4/18

SOP Europe

MOP Brazil

MOP Europe

4

K+S Group

K+S Group

Salt Market update

De-icing

Mixed picture in our winter regions

Promising pre-stocking in US Mid-West

Highly competitive US East Coast

Dec below average in terms of snow events

Non de-icing

Solid demand

Logistics costs inflation to continue in 2019

Pricing trends in de-icing

5

K+S Group

K+S Group

Extreme weather situation in Germany - implications

0

50

100

Ma

y

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

In l/m2

Rainfall comparison (Werra)

2018

5yr Average

Source: Wetterkontor.de

Impact on K+S

Long-lasting severe drought in 2018 led to temporary

shutdowns in Q3 and Q4

EBITDA impact for each site is up to € 1.5 million per day

-> € ~ 110 million in 2018

Basin capacities have been increased by

> 10% to 600,000 cubic meters

Water levels were low!

High logistics costs for remote disposal (old mines)

Inland shipping was also impacted

2018: 64 days of weather related plant shut downs !

In 2019, significantly higher storage capacity available

Q1 2019 now secured due to heavy rainfalls in Dec

-> basin levels significantly lowered

Shaping 2030 Strategy

K+S Group 7

K+S Group

Tapping the full potential of our existing assets... and establish the most value-creating portfolio combination

Exploring new adjacent growth areas... pursuing growth by venturing into new markets where we can use our existing capabilities

Increasing the share of our specialties business... to ensure an overall stabilized performance and reduce our dependency on standard products and weather

'One Company' ... thinking and acting as 'One Company' and realizing synergies between our businesses

We will be the most customer-focused, independent minerals company and grow our EBITDA to €3bn in 2030 by ...

Our vision for 2030

IndustryAgriculture

ConsumersCommunities

K+S Group 8

K+S Group

Phase 2: Growth

203020202017

Phase 1: Transformation

Realize synergies

Advance corporate culture

Net debt/ halvedEBITDA vs. H1/2017

Synergies > €150m

EBITDA-Ambition €3bn

ROCE > 15%

Revenue growthbeyond 2030

> 4%

Increased share of specialties

Tapping the full potential of our existing assets

Exploring new adjacent growth areas

Shaping the organizationand focusing towards our clients

Reduce indebtedness

Investment grade ratingachieved in 2023

We will implement our strategy in two phases

Phase I

10

K+S Group

K+S Group

Phase I: Building a basis for our growth options

Matrix

Operating Unit Function

Agriculture

Industries

Consumers

Communities

Customer Segments

Operations

IndustryAgriculture

ConsumersCommunities

Board of Executive Directors

COO Group CFO GroupCEO Group

CEO Americas

Head of Human Resources

Head of Corporate Communications

Head of Corporate Development

Head of Corporate Controlling

Matrix

Executive Committee

Head of Marketing,Sales & Supply Chain

Excellence

Marketing & SalesCommittee

Operations Excellence Committee

Head of Operations Excellence

CEO Europe & Agriculture

Board of Executive Directors

Divisional Silos

11

K+S Group

K+S Group

SHAPING 2030

Lift synergies

Operations

Procurement

Supply Chain and Logistics

Commercial Excellence

SG&A Optimization

> €50m

Net synergies YE 2020 (vs. 2017)

> €30m

> €20m

> €20m

~ €30m

COO

Sponsor

CFO

COO

COO

CEO

∑ > €150m

Synergies: Breakdown by program

12

K+S Group

K+S Group

Shaping 2030 EBITDA impact

Costs Synergies > €150m

Total costs for synergy program: ~ €150m (2020 year end)

2018e 2019e 2020e

K+S Group 13

K+S GroupA

ssu

mp

tio

ns

Current purchase conditions for gas reflected

Modified ramp-up curve taken into consideration

WACC (before taxes) = 8.5%

USD/EUR = 1.15

EUR/CAD = 1.55

View on the 2019 - 2070 period

MOP gran. Brazil: 2019 - 23 = 330-370 USD/t

We have updated our valuation for Bethune

Net Present Value (NPV) Bethune (1)

K+S Group 14

K+S Group

This NPV equals an EV per share of 25 EUR

Variation NPV change

MOP gran. Brazil +/- 10 USD/t +/- €200 million

“We create value for our stakeholders!”

Net Present Value (NPV) Bethune (2)

Sen

siti

viti

es

NPV for Bethune EUR 4.8 bn

15

K+S Group

K+S Group

Site costs (FOB) in comparison (2020)

* column width = production capability in million tonsSource: CRU Report 2016, K+S

-30%

BU Potashw/o Bethune

(incl. Specialties)

Best-in-class

USD/t

K+S Bethune(in 2023)

K+S Zielitz(Purely MOP)

K+S Bethune*

The Bethune ramp-up to 2.86 million tons in 2023 (production capability) significantly improves K+S's competitive position.

Phase II

17

K+S Group

K+S Group

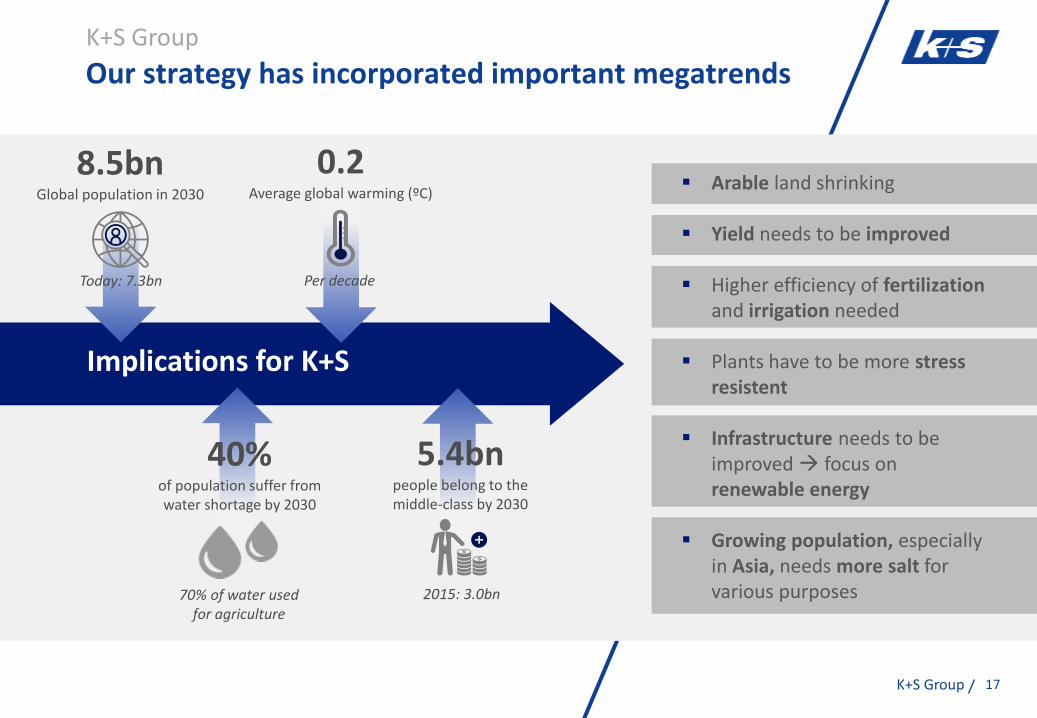

Implications for K+S

Arable land shrinking

Yield needs to be improved

Higher efficiency of fertilizationand irrigation needed

Plants have to be more stressresistent

Infrastructure needs to beimproved focus on renewable energy

Growing population, especiallyin Asia, needs more salt forvarious purposes

Today: 7.3bn

8.5bnGlobal population in 2030

Per decade

0.2Average global warming (ºC)

70% of water used for agriculture

40%of population suffer from water shortage by 2030

2015: 3.0bn

5.4bnpeople belong to the middle-class by 2030

Our strategy has incorporated important megatrends

18

K+S Group

K+S Group

Geo-expansion Fertilizer Industry

Africa

Asia

Increase of fertilizer specialties

Ramp of low cost commodities

Expand Pharma & Food portfolio

Chemical applications

Growth areas and ideas cover the full growth landscape

K+S Growth Landscape

Growth areas and ideas cover core and adjacent businesses

Financials

20

K+S Group

K+S Group

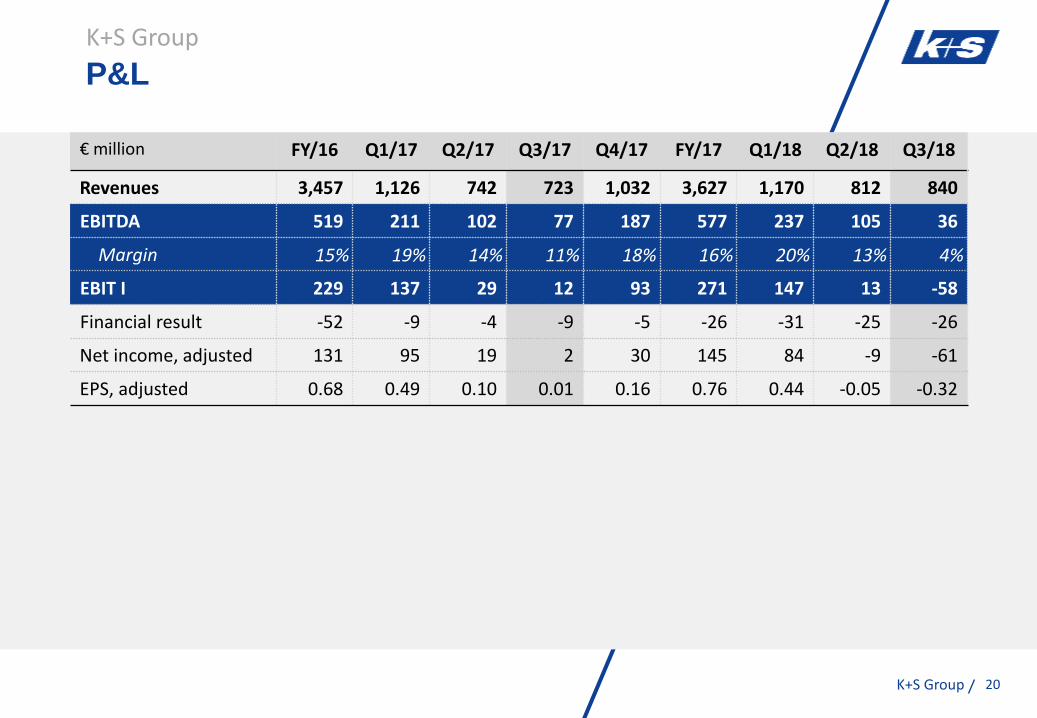

P&L

€ million FY/16 Q1/17 Q2/17 Q3/17 Q4/17 FY/17 Q1/18 Q2/18 Q3/18

Revenues 3,457 1,126 742 723 1,032 3,627 1,170 812 840

EBITDA 519 211 102 77 187 577 237 105 36

Margin 15% 19% 14% 11% 18% 16% 20% 13% 4%

EBIT I 229 137 29 12 93 271 147 13 -58

Financial result -52 -9 -4 -9 -5 -26 -31 -25 -26

Net income, adjusted 131 95 19 2 30 145 84 -9 -61

EPS, adjusted 0.68 0.49 0.10 0.01 0.16 0.76 0.44 -0.05 -0.32

21

K+S Group

K+S Group

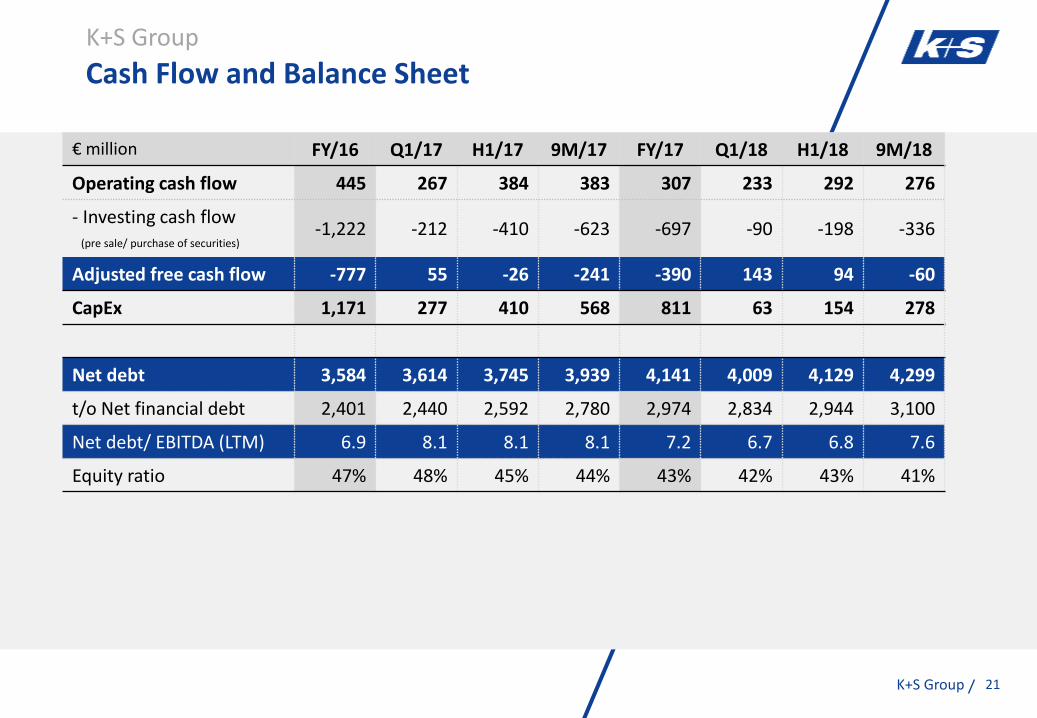

Cash Flow and Balance Sheet

€ million FY/16 Q1/17 H1/17 9M/17 FY/17 Q1/18 H1/18 9M/18

Operating cash flow 445 267 384 383 307 233 292 276

- Investing cash flow(pre sale/ purchase of securities)

-1,222 -212 -410 -623 -697 -90 -198 -336

Adjusted free cash flow -777 55 -26 -241 -390 143 94 -60

CapEx 1,171 277 410 568 811 63 154 278

Net debt 3,584 3,614 3,745 3,939 4,141 4,009 4,129 4,299

t/o Net financial debt 2,401 2,440 2,592 2,780 2,974 2,834 2,944 3,100

Net debt/ EBITDA (LTM) 6.9 8.1 8.1 8.1 7.2 6.7 6.8 7.6

Equity ratio 47% 48% 45% 44% 43% 42% 43% 41%

22

K+S Group

K+S Group

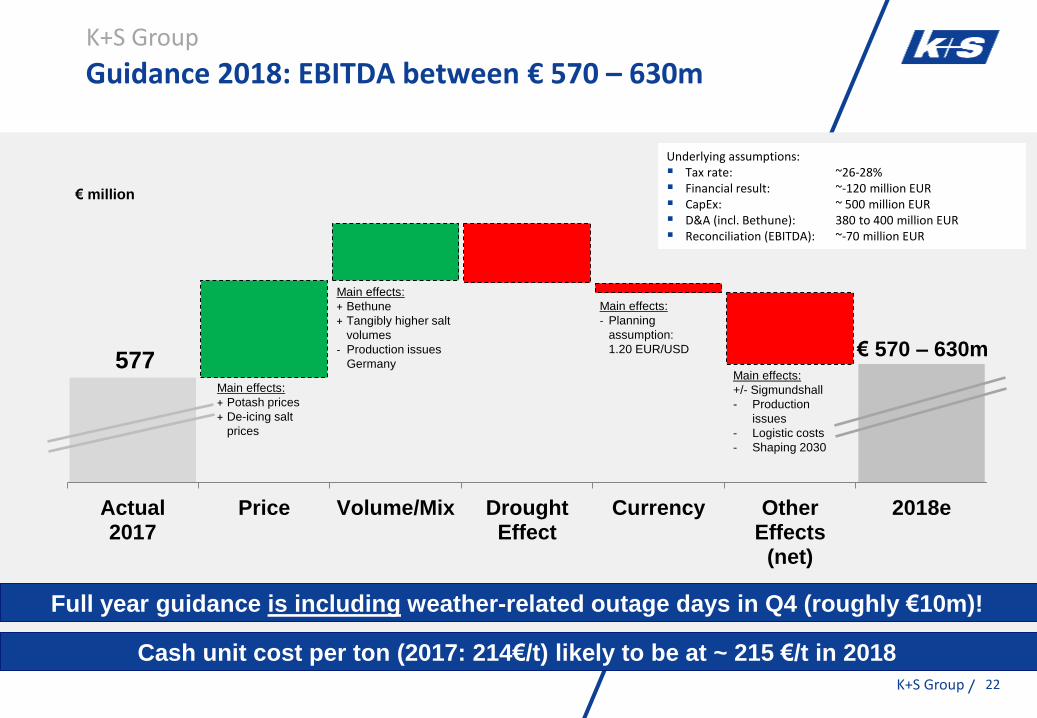

Actual2017

Price Volume/Mix DroughtEffect

Currency OtherEffects

(net)

2018e

577

€ million

€ 570 – 630m

Main effects:

+ Potash prices

+ De-icing salt

prices

Main effects:

+ Bethune

+ Tangibly higher salt

volumes

- Production issues

Germany

Main effects:

- Planning

assumption:

1.20 EUR/USD

Main effects:

+/- Sigmundshall

- Production

issues

- Logistic costs

- Shaping 2030

Cash unit cost per ton (2017: 214€/t) likely to be at ~ 215 €/t in 2018

Full year guidance is including weather-related outage days in Q4 (roughly €10m)!

Guidance 2018: EBITDA between € 570 – 630m

Underlying assumptions: Tax rate: ~26-28% Financial result: ~-120 million EUR CapEx: ~ 500 million EUR D&A (incl. Bethune): 380 to 400 million EUR Reconciliation (EBITDA): ~-70 million EUR

23

K+S Group

K+S Group

Expected Development of our Potash Production

Change in Production

>500ktWerra: no lack of staff and 50% broken machinery backWerra: no outage days Neuhof: roof stability improved

+100ktKCF

-600ktSigmundshall

+300 to 500kt

Bethune

-100ktLower K2O content in

Germany

High-cost production to be replaced by low-cost volumes from Bethune

~ 6.2mt Germany (incl. outage days)

~ 1.4mt Bethune

0.1mt Huludao

Total: ~ 7.7mt

Sales Volume: ~7.5mt

2018

6.1 – 6.2mt Germany

1.7 – 1.9mt Bethune

0.1mt Huludao

Total: 7.9 – 8.2mt

Cash Unit Cost: > € 200

due to overall cost inflation

2019

24

K+S Group

K+S Group

CapEx development 2015-2020

0

200

400

600

800

1.000

1.200

2015 2016 2017 2018e 2019e 2020e

BU Potash (ex Bethune)

Bethune

BU Salt

Complementary Activities

in m€

25

K+S Group

K+S Group

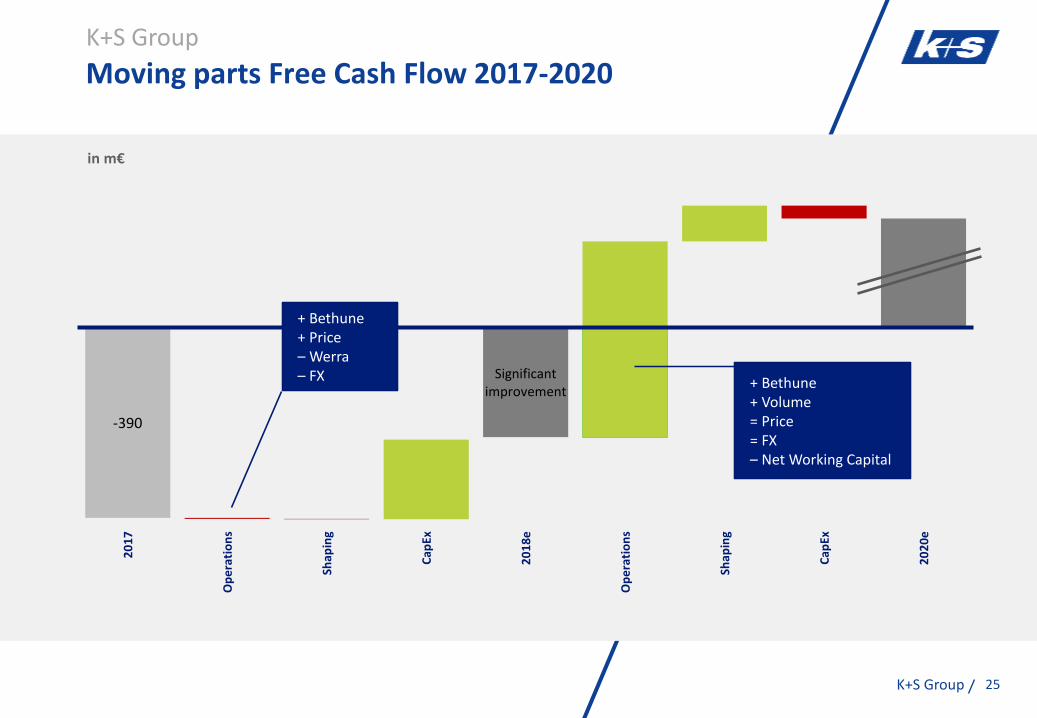

Moving parts Free Cash Flow 2017-2020

-390

Significant improvement

20

17

Op

era

tio

ns

Shap

ing

Cap

Ex

20

18

e

Op

era

tio

ns

Shap

ing

Cap

Ex

20

20

e

+ Bethune+ Price– Werra – FX + Bethune

+ Volume= Price= FX– Net Working Capital

K+S sustainability KPIs and targets 2030

K+S Group 27

K+S Group

Goal KPITarget until 2030 at

the latest

PEO

PLE

Health & Safety Lost time incident rate (LTIR)0

Vision 2030

Diversity & Inclusion

Employees’ favorable perception of inclusive work environment (percent)

>90

Human RightsSites covered by a human rights due diligence process(percent)

100

K+S sustainability KPIs and targets 2030 - People

K+S Group 28

K+S Group

Goal KPI Target until 2030 at the latest

ENV

IRO

NM

ENT

Water

Deep well injection of saline waste water in Germany (m³ p.a.)

0 Starting January 2022

Additional reduction of saline process water from potash production in Germany (m³ p.a.)

-500,000 Excluding

reduction by KCF facility and end of production SI

Waste

Amount of residue used for other purposes than tailings or increased amount of raw material yield (milliontonnes p.a.)

3

Additional area of tailings piles covered (ha) 155

Energy & Climate

Carbon footprint for power consumed (kg CO2/MWh) (percent)

-20

Specific greenhouse gas emissions (CO2) in logistics (percent)

-10

K+S sustainability KPIs and targets 2030 - Environment

K+S Group 29

K+S Group

Goal KPITarget until 2030 at

the latest

BU

SIN

ESS

ETH

ICS Sustainable Supply

Chains

Critical suppliers aligned with the K+S Group Supplier Code of Conduct (SCOC) (percent)

100

by end of 2025

Spend coverage of the K+S Group SCoC (percent)> 90

by end of 2025

Compliance & Anti-Corruption

All employees reached by communication measures and trained appropriately in compliance matters (percent)

100

by end of 2019

K+S sustainability KPIs and targets 2030 - Business ethics

30

K+S Group

K+S Group

IR Contact Details

E-mail: [email protected]: www.k-plus-s.comIR-website: www.k-plus-s.com/ir

K+S AktiengesellschaftBertha-von-Suttner-Str. 734131 Kassel (Germany)

Laura SchumberaJunior Investor Relations Manager

Phone: +49 561 / 9301-1607Fax: +49 561 / [email protected]

Lutz GrütenHead of Investor Relations

Phone: +49 561 / 9301-1460Fax: +49 561 / [email protected]

Christiane MartelRoadshow Management

Phone: +49 561 / 9301-1100Fax: +49 561 / [email protected]

Martin HeistermannSenior Investor Relations Manager

Phone: +49 561 / 9301-1403Fax: +49 561 / [email protected]

Alexander EngeInvestor Relations Manager

Phone: +49 561 / 9301-1885Fax: +49 561 / [email protected]

Julia Bock, CFASenior Investor Relations Manager

Phone: +49 561 / 9301-1009Fax: +49 561 / [email protected]