ayb219 taxation law and practice notes - amazon...

TRANSCRIPT

AYB219 – Taxation Law and Practice Notes

Page 1 of 98

Lecture 1 – Introduction

Two general types of tax: o Direct taxes – taxes are levied on the person who is liable to pay the tax, e.g. income tax o Indirect taxes – tax is passed onto consumers by incorporating the taxes into the price of

goods & services, e.g. GST

Historical background of tax o 1902-1915: Queensland levied personal income tax o 1915-1942: Both state and commonwealth governments levied income tax o 1942: Commonwealth Government gained sole control of income tax under the Income Tax

Assessment Act (1936)

Constitutional Basis of Taxation o s51 of constitution

“The Parliament shall, subject to this Constitution, have power to make laws for the peace, order, and good government of the Commonwealth with respect to: (i) Trade and commerce with other countries, and among the States: (ii) Taxation; but so as not to discriminate between States or parts of States”.

o s55 of constitution “Laws imposing taxation shall deal only with the imposition of taxation, and any

provision therein dealing with any other matter shall be of no effect. Laws imposing taxation shall deal with one subject of taxation only”.

Taxation Acts o Income Tax Assessment Act (ITAA)

Deals with incidence, assessment & collection of tax Determines taxable income on which income tax is levied Does not “impose taxation” Two ITAAs, 1936 and 1997

1963 is difficult to understand

The ITAA 1997 overrules the ITAA 1936 o Income Tax Rates Act

Imposes and fixes the rate of taxation

Administration of Income Tax o ATO enforces compliance, parliament sets tax rates o Taxpayers charter sets out a taxpayers rights, but it is

statement of intention with no legal force

Sources of taxation law and rules o Statute law

ITAA (1936 / 1997) FBT Assessment Act (1986) Taxation Administration Act (1953)

o Case law Administrative appeals tribunal -> federal court ->

full federal court -> high court o ATO Tax Determinations & Tax Rulings

Not law Commissioner’s opinion on how a particular aspect of tax law should be interpreted Two types of rulings: public (for everyone) and private (for a particular person’s case)

AYB219 – Taxation Law and Practice Notes

Page 2 of 98

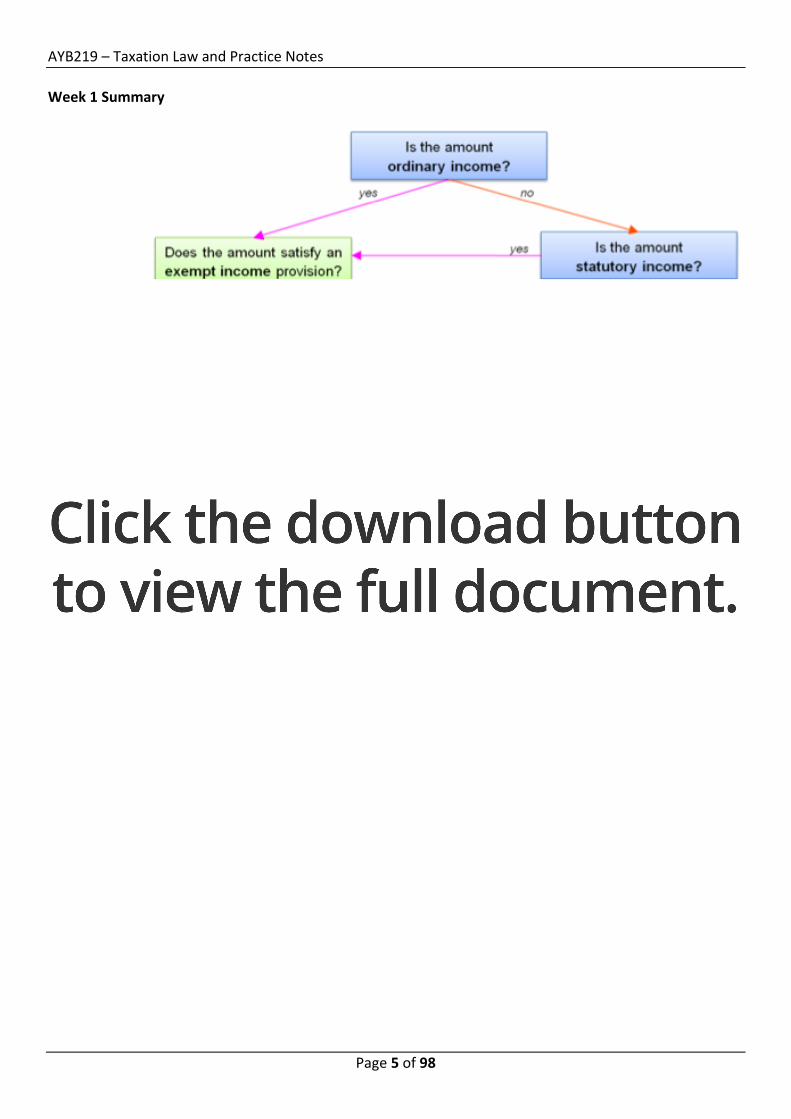

Assessing Income Tax

Ordinary Income

Income is not defined in ITAA 1936 or 1997

Determined by the courts (case law) o Developed “income according to ordinary concepts” o Leading case: Scott v C of T (1935) SR (NSW) 215 o 9 characteristics

What comes into the pocket

Tennant v Smith (1892) AC 150 o Amount must come home to the taxpayer o Unrealized gains and saving from not incurring expenditure (fixing the

toilet yourself) is not income o Money doesn’t have to be physically received (i.e. may be in the form

of receiving shares) Money or money’s worth

Income received must be: o Money o Capable of being converted into money

E.g. barter arrangements (someone washes the dishes for you instead of paying for their meal)

o FCT v Cooke & Sherden 80 ATC 4140 Resulted in the addition of s21A ITAA (1936) that business

related gains are income Income in the hands of the person that has derived it

Tax is paid by the person who derives the income Often exhibit periodicity, recurrence and regularity

More regular receipts are more likely to be income

Not essential to be considered income

AYB219 – Taxation Law and Practice Notes

Page 3 of 98

Normal proceeds of personal exertion, property or business are income

Personal exertion – income

Return on investment – income

Carrying on a business – income

Unless a pastime of hobby Compensation receipts may be income if it replaces a revenue loss

Compensation receipts: same character as the item/amount it replaces o e.g. compensation for loss of wages = ordinary income o e.g. compensation for loss, surrender or substantial impairment of a

capital asset = capital Higgs v Oliver (1951), TC 899

Even if the receipt is illegal, immoral etc. it may be income

Same test for legal & illegal activities (i.e. 9 characteristics)

Proceeds of illegal activities are assessable as income o e.g. drug dealing, burglary, illegal bookmaker etc

“Mutual” receipts are not income

Principle of mutuality: a person cannot derive income by dealing with themselves

o i.e. only income if derived from external sources o e.g. income derived by members of a club/association = generally not

assessable o income from non-members (visitors) = generally assessable

Capital gains are not income

Sale of a capital asset = capital gain o Not income according to ordinary concepts

I.e. fruit generates income but sale of the tree does not

Reportable under capital gains tax since 1985 Exempt Income

s6-20 ITAA 1997

Income that is ordinary or statutory income

But specifically made exempt from income tax by: ITAA or other commonwealth law

How is income exempt? o Entity is exempt (Div 50)

Charities Educational institutions Scientific & religious institutions etc

o Type of income is specifically exempt (Div’s 51 & 52) d51 Certain types of income are exempt from income tax

e.g. income derived whilst being a part-time member of the Army or Navy Reserve Forces (s 51-5)

d52 Social security payments (e.g. some Centrelink payments)

Majority exempt: (see para 10-195 Master Tax Guide)

e.g. carer allowance, mobility allowance, seniors supplement etc

AYB219 – Taxation Law and Practice Notes

Page 4 of 98

Examples Constitution

a) Can a Commonwealth bill that imposes a tax on plastic bags be enacted (as law) if the same bill also seeks to introduce a $1,000 note as a new denomination of currency? Briefly explain why/why not. No

b) Can a Commonwealth bill that only imposes a tax on plastic bags be enacted (as law) if the tax is only to be imposed on those bags sold in Queensland? No

Assessable Income Determine whether the following amounts constitute income according to ordinary concepts:

1) A lump sum of $25,000 awarded as damages to Simon by Guardian Insurance. The money was paid to him under an income protection policy as he was unable to work for 10 weeks due to breaking his leg. Yes, as it replaces a revenue loss

2) Paul receives a payment of $4 per pizza from his employer, Beagle Boys Pizza when he delivers a pizza. He also occasionally receives tips from customers when the pizzas are delivered Yes, as it is a proceed of personal exertion (both the tip and payment)

MCQ Which of the following statements is correct?

a) Exempt income is included in assessable income b) Only ordinary income can be exempt income c) Ordinary income includes income from personal exertion, income from property & income from

business d) A capital gain derived under the capital gains tax provisions is an example of ordinary income

Exempt Income Which of the following is NOT considered exempt income?

a) A double orphan pension received from Centrelink b) An apprenticeship wage top-up payment received c) A mobility allowance paid under the Social Security Act 1991 d) An allowance paid to a member of the Defence Force e) All of the above amounts would be considered exempt income

AYB219 – Taxation Law and Practice Notes

Page 5 of 98

Week 1 Summary

AYB219 – Taxation Law and Practice Notes

Page 6 of 98

Lecture 2 – Income 1 Compensation and Gifts

Income from personal exertion o Reward to taxpayer as a result of their exertion/services o All personal exertion income = ordinary income (s6-5)

May also be statutory income:

“Your assessable income includes the value to you of all allowances, gratuities (tips), compensations, benefits, bonuses and premiums provided to you in respect of, or for or in relation directly or indirectly, to any employment of or services rendered by you”. s 15-2 ITAA 1997

o Allowances vs. reimbursements Allowance: Upfront payment for a predetermined amount

Cover an estimated expense o e.g. travel or uniform allowance o Assessable: s 15-2

Reimbursement: Employee compensated exactly for all / part of an expense already incurred

Not assessable or deductible

Exception: reimbursed for car expenses using cents per kilometer method (s 15-70)

o Compensation (insurance) Loss of wages

e.g. income protection policies

Assessable: ordinary income o FCT v Inkster 89 ATC 5142

Personal injury

e.g. loss of limb, eye etc

Not assessable

Gifts vs. Income o A gift is not assessable o The most important question to ask is: why was the payment made

If it was connected to services provided then it’s assessable If it was because of personal qualities then it’s not assessable

o Important cases Midland Railway Co v Sharpe (1904) AC 349 at 351:

“As long as the receipt accrues by virtue of the taxpayers office, it constitutes income.”

Hayes v FCT (1956) 96 CLR 47

1939 - 1950, Mr Hayes acted as Mr Richardson’s full-time accountant & financial advisor. He was adequately remunerated for this work

Mr Richardson’s business prospered & in 1950 became a public company

Later that year, Mr Richardson made several large cash gifts to various public bodies & gifts of shares in his public company to his two sons & certain other persons, including Mr Hayes, who was given 12,000 shares in the company

Over the years, Hayes had become close friends of Richardson & his wife often exchanging social visits

AYB219 – Taxation Law and Practice Notes

Page 7 of 98

High Court held: transfer of shares = gift; stated: "In this case, it was not sufficient that the gift of shares had been motivated to some extent by the taxpayer's past services. Richardson had also been motivated by a general feeling of goodwill arising from a close relationship, which had both a business aspect and a personal aspect.

What is decisive is the fact that it is impossible to relate the receipt of shares by Hayes to any income producing activity on his part. Hence, the shares were no more than a gift from a grateful friend."

o Considerations when making the distinction Relationship between the parties

e.g. personal friends? known each other long? Motive of donor

Thank you for services rendered or thank you for being a close/good friend? Something given in return? Person receiving the gift owed money for outstanding fees? Expected or unexpected? Customary in this industry? Re-occurring & regular? Time of the year gift was given?

Income of sportspersons o Does the sportspersons earn income from their sport?

Payments & prizes assessable

Commercial exploitation of their skills

Unless pastime or hobby o Taxation Ruling TR 1999/17

o Income includes: prize money, sponsorship & appearance fees FCT v Stone (2005) 222 CLR 289

Windfall gains and prizes o e.g. lottery winnings, betting / gambling wins

Generally not assessable Unless carrying on a business of betting/gambling

o Doesn’t display usual characteristics of ordinary income Unexpected, isolated, lump sum payment etc

o Lacks connection with income producing activity o Taxation Ruling IT 167: TV or radio

Prizes won for the first time: not assessable Regular appearances or invited back

Income: assessable o Exploiting skill or expertise o = Ordinary income

AYB219 – Taxation Law and Practice Notes

Page 8 of 98

Business Income

Determining the existence of a business o Important because:

Business income is assessable (s6-5), Hobby income is not assessable Deduction for expenses necessarily incurred in carrying on a business (s8-1) Taxpayers carrying on a business must adjust for trading stock (division 70)

What constitutes carrying on a business? o No “black & white” determinations (e.g. $ or period of time) o Courts have established the characteristics of a business

Repetition of acts & transactions

Frequency and duration of taxpayers activities o Repetitive and sustained conduct indicated business

Ferguson v FCT 79 ACT 4261

Single transaction can constitute a business o Provided a commercial character exists

Evans v FCT 89 ATC 4540 FCT v St Hubert’s Island Pty Ltd (1978) 138 CLR 210

Commercial nature of the activities

Systematically & Regularly (Hyde v Sullivan (1956) 73 NSW 25)

Trade on the open market on normal terms and conditions o Not just use products themselves or sell to friends/family

Rutledge v IRC (1929) 14 TC 490 Size and scale of the activities

Smaller scale less likely to be a business & visa versa o FCT v Whitfords Beach Pty Ltd (1982) 150 CLR 355

While volume & size relevant → not determinative o May be a small business but still a business

FCT v Walker 85 ATC 179 Existence of a profit motive

Courts: existence of a profit motive very important o Intention to make a profit

Does not actually have to make a profit

Businesses: undertaken with a view to making profit

Activities with little prospect of commercial success more likely = hobby Whether the activity is conducted in a continuous & systematic manner

Emphasis on commerciality / business-like nature of activities o Businesses: conducted in organised & systematic manner

Do you keep accounts? o Hobbies: usually little/no commercial characteristics

o The ATO has determined some questions that would identify a business Do you have a business plan?, Specialised knowledge or skills, which you use?, Have

you had prior experience in this area?, How much capital have you invested?, Have you done market research?, How much time do you spend on the activity?, Activity part-time or side-line or your main income earning activity?, Do you give quotes and supply invoices or tax invoices?, Have you obtained an ABN or registered for GST?, Have you registered a business name & opened a bank account?, Do you have printed letterhead, business cards & a web page?, Do you advertise?

AYB219 – Taxation Law and Practice Notes

Page 9 of 98

Realisation of Capital Assets o Not every receipt received by a business is “income according to ordinary concepts” o Sale of assets incidental to business activities may be treated as capital

e.g. Scottish Australian Mining Co Ltd v FCT (1950) 81 CLR 188 o Principles

Profit derived from sale of capital asset is not income according to ordinary concepts if:

Sale is outside business’ ordinary operations

Minimal efforts made to dispose of property But will be if:

Realisation of income becomes so significant it amounts to a carrying on a business in its own right

Investment Income

Interest Income o Interest income is ordinary income (s6-5 ITAA 1997) o Interest derived by a resident from all sources must be declared to the ATO

When received or credited (cash basis) o ATO: data matches information

Dividend income o “Dividend” defined:

Any profit distribution made by a company to its shareholders Whether in money or other property (e.g. shares)

s 6(1) ITAA 1936 o Resident taxpayers: declare all dividends paid from any source o Non-resident taxpayers: Aus source

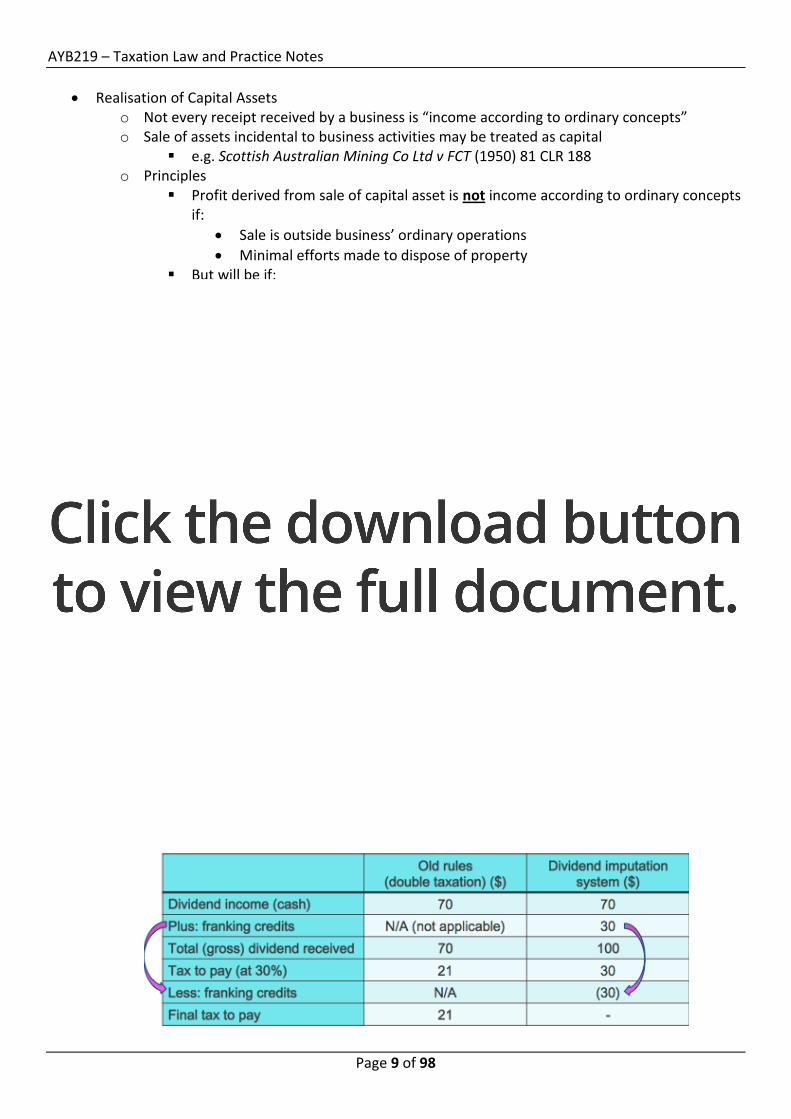

s 44(1) ITAA 1936 o Previously, double taxation on dividends

Dividend imputation system introduced 1 July 1987

Credit for income tax paid by company to the shareholders o “franking credit” or “imputation credit” o Removed double taxation on dividends

o Example

In November 2011, Simone, an Australian resident receives a $70 cash dividend plus franking credits of $30 attached from Silver Ltd. Assume Simone has a marginal tax rate of 30%. Calculate Simone’s income tax to pay for the 2012 income year

AYB219 – Taxation Law and Practice Notes

Page 10 of 98

o Types of dividends Unfranked dividend

Company chosen not to attach franking credits

Shareholders: declare amount of unfranked dividend (cash) received in ITR

Effectively double taxed o No franking credit available to offset dividend income

Franked dividend

Company chosen to attach franking credits to dividend o Franking percentage: 1% - 100%

Shareholders: o Receive a credit for company tax paid o Declare amount of dividend received (cash) plus amount of franking

credit in ITR (s 207-20)

Company paying dividends must provide shareholders with a distribution statement

o Calculating amount of franking credit Distribution statement may only provide franking %

Shareholder:

Entitled to credit for amount of franking credit (s207-20)

Franking credit exceeds net tax payable? o Excess is refundable

Rental Income o Ordinary income: s 6-5 ITAA 1997 o Rental income earned by co-owners of a property

Shared according to their legal interests E.g. 40/60 legal split = 40/60 income/expenses split

Trading Stock

Why is it important? o Sales of trading stock = ordinary income

s6-5 ITAA 1997 o Deduction allowed for cost of purchasing trading stock

s8-1 ITAA 1997 o Taxpayers carrying on a business must adjust for trading stock

Movement between opening & closing stock (statutory)

Defined in s70-10 ITAA 1997 as including: o Anything produced, manufactured or acquired that is held for purposes of manufacture,

sale or exchange in the ordinary course of a business & o Livestock o Inventory = goods held with the intention of sale o Goods acquired for the purpose of hire to customers

AYB219 – Taxation Law and Practice Notes

Page 11 of 98

Meaning of stock on hand o Inventory “on hand” if you have legal power to dispose of it

Depends on terms of shipping not physical possession

FOB shipping & FOB destination

“free on board” or “freight on board” o FOB shipping point: legal title to goods passes to the buyer at the point of shipping o FOB destination: legal title to goods remains with seller until goods are received by buyer at

destination

Valuation of trading stock: taxation o s70-45(1): each item of trading stock on hand at end of IY can be valued at either:

Cost Market selling value Replacement

o Different basis may be adopted for each class of stock & each individual item of stock

Obsolescence o Value of trading stock falls due to obsolesce / other circumstances

E.g. discontinued product line May elect to value trading stock at its obsolete value

s 70-50 ITAA 1997

Taxation ruling TR 93/23 provides guidelines in these circumstances

Disposal of stock o Stock given to others

E.g. donations, gifts to friends/family members etc Taxpayer must include in the AI market value of stock on date of disposal (s70-90)

o Stock taken by owner for personal use Taxpayer must include in their AI cost price of stock on date of disposal (s70-90)

Small business entities & trading stock o Special trading stock rules apply to small business entities (SBE) o A business is classified as a SBE if:

It carried on business in that year; and Its aggregated turnover for the year is < than $2 million

s328-110 ITAA 1997 o Where difference between the value of opening & closing stock is less than $5,000

Determined by a reasonable estimate SBE does not have to:

Value each item of trading stock on hand at year end

Account for any change in value of trading stock

Closing value same as opening value for the year

AYB219 – Taxation Law and Practice Notes

Page 12 of 98

Lecture 3 – Income 2

Assessable income is divided into ordinary income (income under ordinary concepts) and statutory income (statute classifies it as income)

Assessable income is affected by: o Residency – where earned o Source – where from o Derivation – when

Residency

Taxation of residents o s 6-5(2) & 6-5(3): main assessing provisions dealing with ordinary income o s 6-5(2) states:

“if you are an Australian resident, your assessable income includes the ordinary income you derived directly or indirectly from all sources whether in or out of Australia during the income year

Taxation of non-residents o s 6-5(3) states:

If you are a foreign resident, your assessable income includes:

The ordinary income you derived directly or indirectly from all Australian sources during the income year;

Other ordinary income that a provision includes in your assessable income for the income year on some basis other than having an Australian source

Residents: taxed on all income / Non-residents: only taxed on Australian income

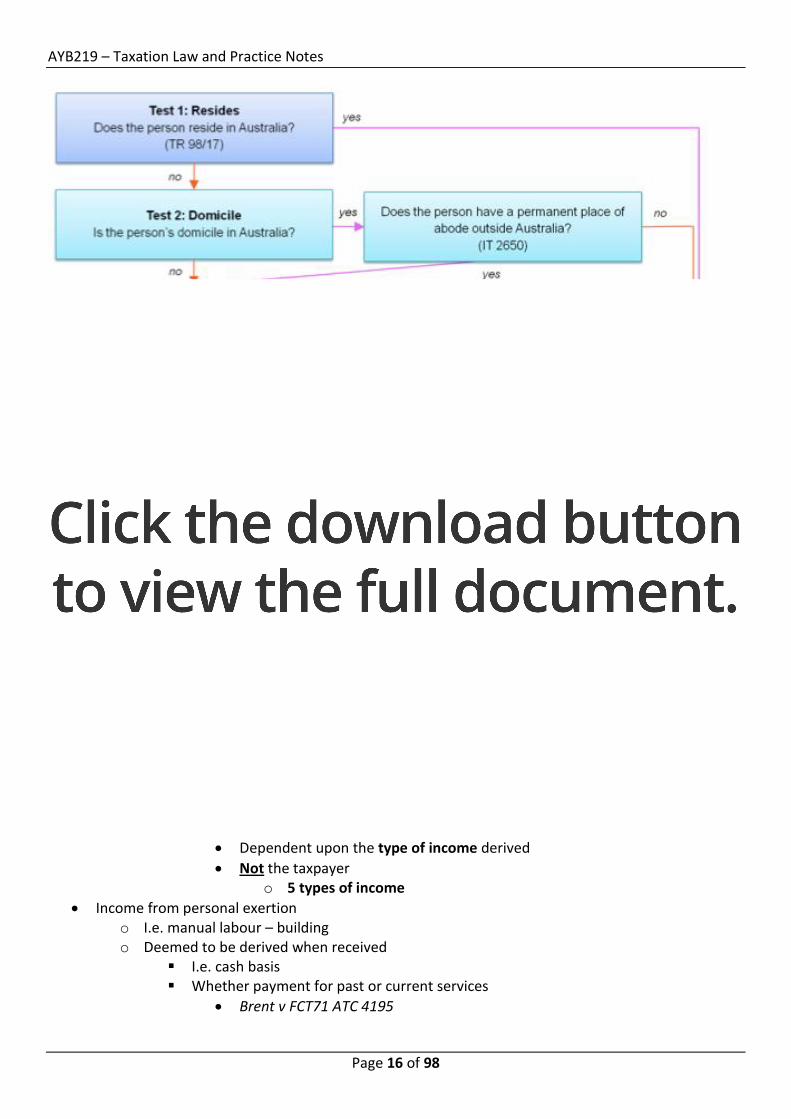

Who is a resident for taxation purposes? o Resides test

Reside means to dwell permanently or for a considerable time, to have one’s settled or usual abode, to live, in or at, a particular place (dictionary)

There is not much difficulty in defining the residence of an individual, it is where he sleeps, lives and eats (Cesena Sulphur Co Ltd v Nicholson (1876) LR 1 Ex D 428)

Court’s interpretation of “resides” in Australia depends on:

Length of their physical presence

Family, employment or business ties

Maintenance of a home or place of abode

Frequency, regularity & duration of visits

Habits & mode of life (ie. day-to-day behaviour whilst in Aus)

Business & social relations Resides test: commissioner’s 4 factors

TR 98/17 o Applies to individuals entering Aus o Length of time spent in Aus not decisive

Critical question: o Whether individual’s day-to-day behaviour in Aus is consistent with

someone residing in Aus Similar continuity, routine or habit Emphasis on 4 factors

AYB219 – Taxation Law and Practice Notes

Page 13 of 98

(a) Intention or purpose of presence o “Why is the individual here?” o Settled purpose may support an intention to reside in Aus

E.g. long-term employment, enrolling in Bachelor/ Masters degree

Traveller/visitor doing casual work to supplement income?

(b) Family & business / employment ties o Individual bring their family to Aus with them?

More likely to be considered Aus resident (Peel v The Commissioners of Inland Revenue (1927) 13 TC 443)

(c) Maintenance & location of assets o Occupation of a dwelling in Aus? o Owns, rents or leases accommodation for a significant period of time? o Other assets here? (e.g. cars, furniture, bank accounts?)

More likely to be Aus resident o What about assets located overseas?

Doesn’t affect Aus tax – i.e. doesn’t matter if you have a home overseas

(d) Social and living arrangements o May also indicate Aus resident e.g.

Joining sporting or community organisations Enrolling children in school Redirecting mail to Aus Committing to a residential lease

Resides test summary

Does an individual reside in Aus? o Intention o Family & business / employment ties o Assets o Social & living o Length of time

Commissioner: individual an Aus resident if: o Physically present in Aus for at least 6 months and

6 months test is only applicable if all other tests are inconclusive – based on intentions not actuals

o Behaviour consistent with an Aus resident

AYB219 – Taxation Law and Practice Notes

Page 14 of 98

o Domicile test Domicile = legal concept, defined as:

“The intention that a person has to make his home indefinitely in that country.”

s 10, Domicile Act (1982) An Aus domiciled person = deemed Aus resident:

Unless individual has a permanent place of abode (PPOA) outside Aus A person will retain Aus domicile if they:

Travel overseas temporarily

Do not intend to permanently set up home in another country

Intend returning to Aus within a definite period To be regarded as a non-resident:

Must prove they changed domicile to another country

i.e. have a “PPOA outside Aus” o A person establishing a residence or home outside Aus o “Permanent” ≠ everlasting but more than temporary o Practically = having a fixed address outside Aus

FCT v Applegate 79 ATC 4307

Background o Taxpayer was an Aus solicitor o Transferred to Vila in Vanuatu to set up a branch of his firm o Taxpayer’s wife & children accompanied him o Transferred for indefinite time o Intended to return to Australia eventually o Taxpayer left no assets in Aus & gave up lease on his house o In Vila, taxpayer leased premises, obtained resident status & was

admitted to practice o Taxpayer returned to Aus after 21 months due to ill health

Commissioner treated taxpayer as Aus resident o i.e. taxpayer had retained his Aus domicile on basis he intended to

return to Aus o Had not established a PPOA outside Aus

Court disagreed, held: taxpayer was not an Aus resident o Had established a PPOA in Vila o Abandoned home in Aus o Intention of saying in Vila an indefinite & substantial period

August 1991, Commissioner issued IT 2650

Applies to domicile test

In particular for residents departing Australia

6 factors Commissioner will consider if taxpayer has a PPOA outside Australia o Intended & actual length of taxpayer's stay o Whether taxpayer intended to return at some definite point in time o Whether taxpayer has established a home outside Aus (fixed address) o Whether place of abode exists in Aus or has been abandoned

because of the overseas absence o Duration & continuity taxpayer's presence in the overseas country o Durability of association that they have with Aus

AYB219 – Taxation Law and Practice Notes

Page 15 of 98

Iyengar & FCT (2011) AATA 856

Taxpayer spent 2 years 7 months working in Qatar

Lived in a serviced apartment

Did not buy/lease any assets

Paid in Aus $; mostly sent back to Aus

Wife & children remained in Aus

Tribunal: still Aus resident: retained Aus domicile o Didn’t establish PPOA outside of Australia o “Temporary”

Domicile test guidelines

Taxpayer leaves Aus for 2+ years (or intends to) and

Establishes a home in another country or

Only a vague possibility of returning to Australia o Taxpayer has a PPOA outside Australia o i.e. domicile test not met

Taxpayer leaves Aus with definite intention of returning within 2 years o Normally remain an Aus resident o Unless established a PPOA outside Aus

o 183 days test

Deemed Aus resident if physically present in Aus for > 183 days in an income year However, only applies where taxpayer:

Does not have a usual place of abode outside Aus and

Has the intention to take up residence in Aus IT 2681:

Presence in Aus does not need to be continuous

Time starts when person arrives in Aus

Based on income year

o Superannuation fund test Active contributing member (or immediate family member is) of a Commonwealth

superannuation scheme

Deemed to be an Aus resident Relevant to Commonwealth Government employees located in an overseas country

e.g. Australian embassy employees in a foreign country

AYB219 – Taxation Law and Practice Notes

Page 16 of 98

(Residency Test Summary) Derivation of Income: timing

“When has the income been derived? o Determines income year amount will be assessed in

2 methods: o Cash basis (receipts)

When does the taxpayer received cash? o Accrual basis (accruals)

Treated as income when taxpayer accrues the right to receive income

e.g. when goods are delivered / services performed Which basis to use?

Dependent upon the type of income derived

Not the taxpayer o 5 types of income

Income from personal exertion o I.e. manual labour – building o Deemed to be derived when received

I.e. cash basis Whether payment for past or current services

Brent v FCT71 ATC 4195

AYB219 – Taxation Law and Practice Notes

Page 17 of 98

Trading (business income) o Income from carrying on a business must be on accruals basis

i.e. income recognised when earned not when cash is received

Henderson v FCT (1970) 119 CLR 612 o Exception: income from lay-by-sales

Derived when buyer pays final instalment & goods delivered

Revenue received in advance o Payment received upfront for goods / services yet to be provided

Consider accounting & tax implications o e.g. Arthur Murray (NSW) Pty Ltd v FCT (1965) 114 CLR 314 o Tax implications

High Court: payments received up-front were not income

Receipts assessable in income year when dance lessons provided Accruals basis was appropriate

On basis refunds were given If deposit refunds are not given = cash basis (TR 95/7)

Income from professional practices o Accounting basis depends on several factors

Most important: size of professional practice o Smaller professional practices:

Income earning more like personal services income? Cash basis appropriate

FCT v Firstenberg 76 ATC 4141 o Larger professional practices

Accruals basis appropriate if:

Income earning constitutes carrying on a business

More like trading income

Large scale of operations o e.g. Henderson v FCT (1970) 119 CLR 612

Commissioner: borderline cases = accruals basis generally appropriate

Income from property o Interest, dividends & rent

Cash basis o Exceptions: taxpayer carrying on a business of money lending (e.g. banks) or landlord

Accruals basis appropriate

Summary of derivation rules

Type of income Derivation rule

Income from personal exertion Cash

Trading (business) income Accruals

Revenue received in advance Accruals (where refunds given), Cash (no refunds)

Income from professional practices Cash (small)

Accruals (large)

Income from property Cash (individual)

Accruals (main business)

AYB219 – Taxation Law and Practice Notes

Page 18 of 98

Source: where

Source is a question of “where?” o “Where has the income been derived?”

Geographical location at which the act, transaction or event that produces the income occurs

Link between source & residency o Issue is only relevant for non-residents

Course: type of income

o Source of income depends upon the type of income derived, not the taxpayer o Income can be classified as:

Income from personal services Trading (business) income Interest Dividends Rent Royalties

Income from personal services o Source of salary, wages, professional services income etc. may be:

(i) Place where the contract was entered into (ii) Place where the work is performed (iii) Location of payment

o Courts held: source is determined based on the most important factor in each case o French v FCT (1957) 98 CLR 398

Taxpayer (Aus resident); employed as an engineer in Aus Taxpayer spent 2 to 3 weeks a year in NZ acting as an inspecting engineer for his

employer His salary was paid into his Sydney bank account as usual Taxpayer argued income earned whilst in NZ was sourced outside Aus & therefore

should be exempt (old section) Court found the source was the place where the work was performed (NZ)

As the services which gave rise to the remuneration were carried out in NZ o FCT v Mitchum (1965) 113 CLR 401

Taxpayer, an actor, was a USA resident He contracted with a Swiss company to be paid $50,000 to act in 2 films Entitled to payment even if his services were not utilised Film was produced largely in Aus Taxpayer was sent to Aus for 11 weeks to act & provide consultancy services Payment was made in the USA Court: most important factor: where contract was signed

AYB219 – Taxation Law and Practice Notes

Page 19 of 98

o Personal services general rule Normal contract of employment/for services?

Source = where work is undertaken Creative powers/special knowledge involved?

Where the work undertaken may be relatively unimportant

Source? Where contract/payment made?

e.g. an author writing a book o On a certain subject? o On a particular country?

o Income from property

(a) Interest

Location of bank account where money deposited or

Place loan contract is made

Spotless Services Ltd v FCT 95 ATC 4775 (b) Dividends

Where company paying the dividends made its profits

Esquire Nominees Ltd v FCT 72 ATC 4076 (c) Rent

Country where the property is located (d) Royalties

Right to use intellectual property (IP) o e.g. copyright, patents, trademarks, designs, licenses etc o Source: country where IP is located & registered

Source summary

Type of Income Source Rule

Income from personal services Where work performed

Trading (business) income Place of business profits

Interest Bank a/c located

Dividends Place of business profits

Rent Place of rental property

Royalties Where IP registered

AYB219 – Taxation Law and Practice Notes

Page 20 of 98

Week 3 Summary

AYB219 – Taxation Law and Practice Notes

Page 21 of 98

Examples Michelle is a doctor who comes to Australia from France to conduct medical research for five months. She actually stays for seven months to complete the Australian phase of her research project. Michelle's husband and children do not accompany her to Australia. They stay in their home in Paris. From Australia, she assists her husband in running the family business. While in Australia, Michelle stays in a hotel. She uses credit cards to meet day-to-day expenses that are reimbursed by her employer. Her concentration on her research is often interrupted because she has to constantly fax and phone her husband about their emerging business problems. In fact, she occasionally makes a quick trip home for a week to Paris to sort out business dilemma’s.

Michelle is likely a non-resident under the resides test o There was no intention for a long term stay o There is no family or permanent employment ties o Assets are located overseas o Social and living arrangements are that of a non-resident o The length of time was intended to be short

Mohammad is a student from India who comes to Australia to study a 4-year bachelor degree in civil engineering. Mohammad lives in rental accommodation near the university with fellow students and works part-time at the university social club as a barman. Soon after arriving, he receives a call from his mother informing him that his father is seriously ill. After five months, Mohammad withdraws from his studies and permanently returns home to India.

Mohammad is likely a resident under the resides test o There was an intention for a long term stay o Assets are located in Australia o Social and living arrangements are that of a resident o The length of time was intended to be long

AYB219 – Taxation Law and Practice Notes

Page 22 of 98

Lecture 4 – General Deductions

Deductions under s8-1

s8-1(1): You can deduct from your assessable income any loss or outgoing to the extent that: o (a) It is incurred in gaining or producing your assessable income, or o (b) It is necessarily incurred in carrying on a business for the purposes of gaining or

producing assessable income

Hence there are considered to be two positive ‘limbs’

s8-1(2): No deduction is allowed under s8-1(1) to the extend that: o (a) It is a loss or outgoing of capital, or of a capital nature o (b) It is a loss or outgoing of a private or domestic nature o (c) It is incurred in relation to the gaining or producing your exempt income, or o (d) A provision of this Act prevents you from deducting it

Hence there are considered to be four negative ‘limbs’ First Positive Limb s8-1(1a) “You can deduct from your assessable income any loss or outgoing to the extent that it is incurred in gaining or producing your assessable income”

AYB219 – Taxation Law and Practice Notes

Page 23 of 98

When is a loss or outgoing “incurred?” o “Incurred:” not defined in either ITAA 1936 or 1997 o Courts: expenditure is incurred if it is:

Definitively committed to (existing obligation) & Capable of reasonable estimation (quantifiable)

o Courts have held that incurred does not mean the same as paid

Does a loss or outgoing have to be exactly quantified? o CIR v Mitsubishi Motors New Zealand Limited (1995) 17 NZTC 12,351 o Taxpayer assembled motor vehicles & sold them to dealers o Based on previous experience, taxpayer estimated:

63% of all vehicles sold in 1998 contained defects covered by warranty Total cost of all repair work for those vehicles

o Taxpayer offset these costs against income from vehicles sold o Court: followed RACV Insurance v FCT 74 ATC 4169

Confirms incurred ≠ paid: para 6(a): "A loss or outgoing may be incurred within s 8-1 even though it remains unpaid (at

year-end), provided the taxpayer is 'completely subjected' to the loss or outgoing"

Expenses incurred before business starts o “Preparatory” acts

Incurred before business activity undertaken Not deductible under s 8-1: incurred “too soon”

Deductible under s 40-880? o When does a business start?

“current operations” begin o Softwood Pulp & Paper Ltd v FCT 76 ATC 4439 o Goodman Fielder Wattie Ltd v FCT 91 ATC 4438

Expenses incurred in closing down a business o E.g. payments to receivers, liquidators, ASIC in deregistering a company etc. o Generally non-deductible under s8-1

Taxpayer is no longer carrying on a business Expenditure incurred “too late”

o Peyton v FCT (1963) 109 CLR 315

Expenditure incurred after business has ceased operations o Entity may incur day-to-day business expenses after business has ceased trading

Generally non-deductible: not deriving any AI

Placer Pacific Management Pty Ltd v FCT 95 ATC 4459

FCT v Jones (2002) ATC 4135 o May be deductible provided expenditure deductible if business was still trading

AYB219 – Taxation Law and Practice Notes

Page 24 of 98

s40-880 Blackhole expenditure o Business-related capital expenditure not deductible elsewhere

Deductible under s 40-880 ITAA 1997 Section of last resort

o Expenses deductible over a 5 year period 20% deduction each year Expenditure not apportioned if incurred part way through IY

Second Positive Limb s8-1(1b) “You can deduct from your assessable income any loss or outgoing to the extent that it is necessarily incurred in carrying on a business for the purposes of gaining or producing assessable income.”

Meaning of “necessarily incurred” o Courts: outgoing appropriate to taxpayer’s business o ≠ absolutely essential or necessary o Some connection with taxpayers business/income earning process

e.g. head office expenses, entertainment etc

Magna Alloys & Research Pty Ltd v FCT 80 ATC 4542 o “For practical purposes and within the limits of reasonable human conduct, it is for the man

who is carrying on the business to be the judge of what outgoings are necessarily incurred. o It is no part of the function of the Act or those who administer it to dictate to taxpayers in

what business they shall engage or how to run the business profitably or economically.”

First Negative Limb s8-1(2a) “It is a loss or outgoing of capital, or of a capital nature”

Expenses of a capital nature

Accounting: o Expense: P&L – generally deductible for tax o Acquisition of asset: capital – balance sheet

Tax: o “Income” & “Capital” not defined o Courts: 3 tests to distinguish

Once & for all test

Vallambrosa Rubber Co Ltd v Farmer (1910) 5 TC 529:

“…capital expenditure is something that is going to be spent once and for all, and income expenditure is a thing that is going to recur every year”

General rule, not definitive in every case Enduring benefit test

British Insulated & Helsby Cables Ltd v Atherton (1926) A.C. 205

“When expenditure is made…with a view to bringing into existence an asset or an advantage for the enduring benefit, I think that there is very good reason for treating such an expenditure as properly attributable…to capital”

What does the payment represent? Or what is it for?

AYB219 – Taxation Law and Practice Notes

Page 25 of 98

Business entity text -> generally most important

Incurred to create / enhance profit-yielding structure: generally capital

Question o Incurred to restore the profit-yielding structure? Or o Protect/defend day-to-day business operations?

Generally deductible

Sun Newspapers Ltd & Associated Newspapers Ltd v FCT (1938) 61 CLR 337 o Held expenditure not deductible because: o (i) Lump sum payment incurred to remove competition o (ii) Made to enlarge taxpayer's organisation o (iii) Consequences, e.g. loss in circulation, were of a lasting character o (iv) Transaction involved purchase of a capital asset, i.e. printing

equipment

Legal fees: capital or deductible? o Use previous tests, i.e.:

Incurred to enlarge, preserve, protect or defend profit yielding structure = capital Existence of the business is threatened = capital Incurred to protect / defend day-to-day business operations = deductible under s 8-1

Second Negative Limb s8-1(2b) “It is a loss or outgoing of a private or domestic nature”

Expenditure directly related to income earning activity? o Consider: clothing, food, home-office expenses

“Essentially” private or domestic nature o No deduction allowed

FCT v Cooper 91 ATC 4396 o Food consumed not deductible

Clothing o Clothing classified into 5 categories: (a) Conventional, (b) Compulsory uniforms, (c) Non-

compulsory uniforms, (d) Occupation specific, (e) Protective o Tax deductibility: Division 34 ITAA 1997 o Day-to-day clothing = private expense

Non-deductible under s 8-1 o Employer requires taxpayer to dress in a particular way?

Suits for lawyers/accountants, sports clothes by sports teachers etc?

Still ‘conventional clothing’ as can be worn outside of work

Limited exceptions to rule: TR 97/12 o Non-conventional clothing which employee required to wear = deductible o Non-compulsory uniforms: not deductible

Unless uniform design entered on Register of Approved Occupational Clothing at time expense incurred (s 34-25 ITAA 1997)

Uniform must have a sufficiently distinctive look & an obvious identity

AYB219 – Taxation Law and Practice Notes

Page 26 of 98

o Occupation specific clothing

Deduction generally allowed

Provided not conventional clothing

E.g. nurse’s traditional uniform, chef’s hat, barrister’s wig o s 34-20(1) ITAA 1997

o Protective clothing Protective clothing & safety footwear = deductible

Provided use relates to income earning activity Clothing worn to protect taxpayer from personal injury, disease or death Protect taxpayers everyday clothing from damage

Laundry and dry cleaning o Costs of laundry and dry cleaning follow clothing treatment o Amount claimed < $150

No need to keep records Commissioner will accept estimate: TR 98/5

Hairdressing & Grooming expenses o Non-deductible: private expense o Taxpayer required to maintain high standard of appearance?

TR 69/18 o Performing artist

May be deductible if required for particular role

Home-office expenses o Carried on business or employment activities at home?

May be entitles to home-related deductions o TR 93/30: is the home a:

Place of business? Or A convenient place to work

AYB219 – Taxation Law and Practice Notes

Page 27 of 98

o Deductions may be available for: Interest on home, rent, insurance, council & water rates** Heating & lighting Depreciation, insurance, repairs & maintenance for relevant equipment & furniture

relating to business Repairs & maintenance to home** Cleaning calculated on floor space area Telephone costs ** Only available for place of business

o Deduction is apportioned between business & private use E.g. floor space Floor area of business / total floor area of house * relevant expenditure Para 16-480 2012 CCH Australian Master Tax Guide

o Claiming home office expenses Actual expenses vs. 34 cents per hour: TR 93/30 Heating/cooling & lighting

Difference between what actually paid & what would have paid if not worked from home

Depreciation: items used in income-producing activities 34 cents per hour: record amount of time working from home over 4-week period

Third Negative Limb s8-1(2c) “It is incurred in relation to the gaining or producing your exempt income”

Deduction not allowed o Not deriving any assessable income o E.g. expenditure incurred by a taxpayer doing voluntary work for a charity

TD 93/185 Fourth Negative Limb s8-1(2d) “A provision of this Act prevents you from deducting it”

E.g. deduction under s 8-1(1) specifically denied for: o Fines & penalties for breaching the law (s 26-5) o HECS & HELP payments (s 26-20) o Recreational club fees (s 26-45) o Leisure facilities (s 26-50) o Bribes paid to public officials (ss 26-52 & 26-53) o Most entertainment (subdivision 32-B) o The first $250 of self-education expenses (s 82A) o Employee’s car parking expenses (s 51AGA)

AYB219 – Taxation Law and Practice Notes

Page 28 of 98

AYB219 – Taxation Law and Practice Notes

Page 29 of 98

Summary

AYB219 – Taxation Law and Practice Notes

Page 30 of 98

Examples Rachel is a sales consultant with a telemarketing company. She uses her mobile telephone, to make work-related telephone calls. Her mobile phone bill for the month of June 2012 was $100. Based on a breakdown of these calls, Rachel reliably estimates that she used the phone 75% for business and 25% for private purposes What amount is deductible to Rachel under s 8-1?

$75 is deductible is it fits 8-1(1a), but the remaining $25 is excluded under 8-1(2b)

Ned, an Australian resident individual taxpayer, receives his Telstra telephone bill (for $290) for the month of June on 16 June 2012. Ned pays his telephone bill on 2 July 2012. Ned used the telephone 100% for work-related purposes When has Ned incurred the telephone expense? 2012 income year or 2013 income year?

The 2012 income year as it is a quantifiable, existing obligation for the 2012 income year Jim operates a renovation business. Jim is contracted to renovate Suzie’s kitchen for $5,000. Jim finishes this work on 12 August 2011 & is fully paid for this work on that date. At Christmas, Jim gives Suzie a bottle of champagne as a gift. Jim expects the gift will either generate future business from Suzie or motivate her to refer Jim’s services to others Is Jim able to deduct the cost of the champagne under s 8-1?

Yes, it is an entertainment expense that has some connection to the taxpayer’s business An engineering consulting firm “Eng Co” employed James. One of the terms of his employment agreement was that if James left Eng Co & took clients with him, he would reimburse Eng Co. James resigned from Eng Co & some clients followed James into his new business. Eng Co sued for breach of contract. James incurred $8,500 in legal expenses regarding the legal action, which eventually resulted in an out of court settlement. The out of court payment settled in full any claims made by Eng Co in relation to the clients, so that James was able to continue his new business. Is James able to deduct his legal costs under s 8-1?

No – as it is capital expenditure

It brought into existence an asset or an advantage for enduring benefit

AYB219 – Taxation Law and Practice Notes

Page 31 of 98

Jessica builds & markets houses in Brisbane. Following allegations of improper business tactics, a Royal Commission was established to investigate her activities. The Royal Commission proceedings are unlikely to threaten the existence of the business itself. However, the proceedings are likely to cause embarrassment to Jessica and a decline in her future business. Jessica incurred $50,000 of legal expenses & another $20,000 in public advertising to counter the allegations made Can Jessica deduct these costs under s 8-1?

No, as it wasn’t to protect day-to-day operations Galvin owns a successful cocktail bar & restaurant. Sam applies for a liquor license to open a cocktail bar near Galvin’s business. Galvin opposes the license & incurs legal fees of $3,500 Is the cost of the legal fees deductible to Galvin under s 8-1?

No, as it is incurred to protect/defend Greg, a pharmacist, is sued due to reckless dispensing of certain drugs. The maximum penalty that can be imposed is a fine of $5,000. Greg cannot be suspended or deregistered if found guilty. Greg incurs legal fees of $2,000 in defending these charges Is the cost of the legal fees deductible to Greg under s 8-1?

Yes, as it is to defend day-to-day business operations Kirstin works as bank teller from 9-5pm, 5 days a week. 2 days a week she also work at a liquor store from 6-9pm. Before starting work at the liquor store, Kirstin buys an evening meal for $15 Is the cost of the meal deductible to Kirstin under s 8-1?

No, as it is essentially of domestic nature Mel is a marriage celebrant who purchases dress suits, accessories, shoes & stockings for her work. She does not wear these items when she is not working. The items are far more extensive than she would ordinarily acquire. During the 2012 income year Mel spends $2,820 on clothing to wear when acting as a marriage celebrant Would Mel be able to claim a deduction for the clothing costing $2,820 under s 8-1?

No, as it is still conventional clothing that can be worn outside of work

AYB219 – Taxation Law and Practice Notes

Page 32 of 98

Evelyn is a lawyer. Evelyn works from home in her study approx. 20 hours per week (out of approx. 80 hours per week), 45 weeks of the year. The study is principally used for her work, though is occasionally used for personal reasons. Based on the house’s floor plans, the study consists of 16% of the house’s floor area. Evelyn asks you whether she can claim a deduction for a portion (16%) of interest on her mortgage, rates & insurance premiums (totaling $10,000), and if so, how much?

No, as it is not the only place available for business (as required for interest repayments)

AYB219 – Taxation Law and Practice Notes

Page 33 of 98

Lecture 5 – Allowable Specific Provisions

General and Specific Deductions

s 8-5(1) ITAA 1997 states: o “You can also deduct from your assessable income an amount that a provision of the Act

allows you to deduct.”

s 12-5 ITAA 1997 contains a summary of all the specific deductions available to taxpayers

Importance of deduction o The size of your tax deductions is directly related to your ability to know and tack all your

expenses o To balance out inequalities o ATO’s focus for 2012-13

Defence Force IT managers Plumbers Medical practitioners Tax avoidance schemes Data matching (dividends, interest, capital gains, foreign income) “How can this expense be legitimately related to my income?”

Repairs s25-10

s25-10 ITAA 1997: repairs deductible? Must: (i) Incur repair in income year (ii) Not be capital (iii) Be to premises, plant etc used for producing AI (iv) Not be an initial repair

AYB219 – Taxation Law and Practice Notes

Page 34 of 98

Borrowing Expenses s25-25

Expenses incurred in borrowing money: o Not interest o Transaction costs etc.

If money is used to produce AI; expenses are deductible over: o 5 Years or o Loan Term (or period of loan if repaid early)

Whatever is shorter

Calculation is done on a daily basis Car Expenses: Div 28 ITAA 1997

What is a car? o S995-1 ITAA 1997

Car expenses deductible under s8-1 ITAA 1997 if: o Own or lease car o Incurred in deriving AI or carrying on a business

Cost of travelling between home & work/business is not deductible o Lunney v FCT (1958) 100 CLR 478

4 Methods to claim car expenses: s28-15 o Cents per kilometer o 12% of original value o One-third of actual expenses o Logbook method

Choose any method for each car o Can change methods at end of IY (s28-20) o ATO: work related car expenses calculator can be helpful

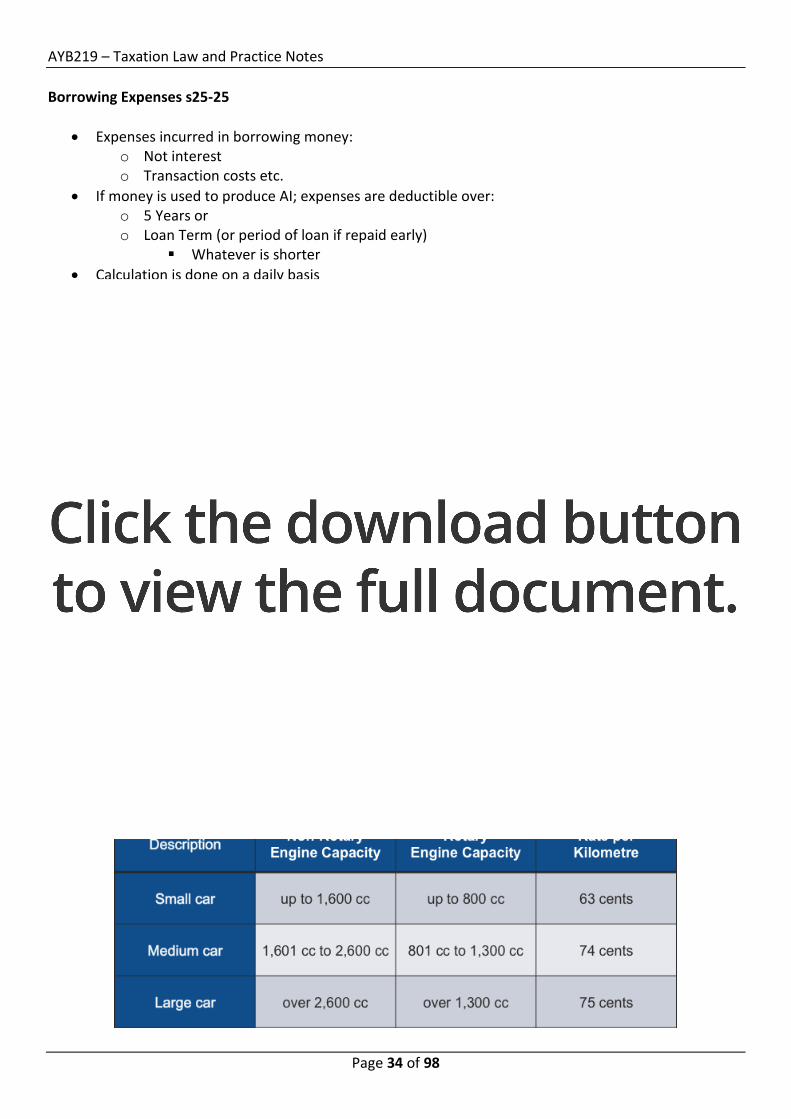

1. Cents per km method

o s28-25: claim maximum of 5,000 business kms Number of business kms travelled during income year * rate per kms (cents)

o Records: not required to maintain logbook / keep receipts Justify how business kms estimated

o Rate per km (cents) depends on car’s engine capacity

AYB219 – Taxation Law and Practice Notes

Page 35 of 98

2. 12% of original value: s28-45 o Only use this method if:

Travelled > 5,000 business kms during IY Or would have if car owned for full year

o 12% of original cost of car * number of days owned in income year

o Original cost = acquisition price / MV of car when leased

Limited to luxury car limit $57,466 for 2012 IY

3. One-third actual expenses: s28-70

o Only use this method if: Travelled > 5,000 business kms during IY Or would have if car owned for full year

o Calculation

One-third of actual expenses

o Records: not required to maintain logbook / keep receipts

4. Logbook Method: s28-90 ITAA 1997 o Use this method regardless of number of kms travelled

o Records: logbook detailing odometer readings for each trip undertaken for 12 consecutive

weeks Valid for 5 years if no change in pattern of use Separate logbook for each car Receipts of all car expenses must be kept

o Business % * total car expenses incurred during IY

AYB219 – Taxation Law and Practice Notes

Page 36 of 98

Depreciating Assets: Div 40 ITAA 1997

s8-1(2): denied immediate deduction for any outgoing of a “capital nature”

Deduction for: decline in value o “Depreciating asset” o Holder (generally owner) o Used in the course of gaining or producing AI

Two methods to calculating the depreciation deduction

What is a depreciating asset? o Asset with limited effective life o Expected to decline in value

E.g. plant & machinery, computer equipment etc o Expenditure on capital works (e.g. buildings):

May qualify for capital works write-off: Division 43 o Cost: purchase price & incidental costs o Holder?

Determining an asset’s effective life o Decline in value based on asset’s effective life

Expressed in years o 2 choices:

Commissioner’s determination: TR 2011/2 Self-assess

o Choice made when: asset first used or Installed & ready for use (s 40-60)

AYB219 – Taxation Law and Practice Notes

Page 37 of 98

Diminishing Value Method o Base value = cost – accumulated depreciation o Pro-rated on day count (max 366 days) o “Diminishing value rate”

200% if asset acquired on/after 10 May 2006 Otherwise 150%

Special rules for individual tax payers

Low Value Pool (LVP) o Once allocated to a LVP, asset must remain in LVP o No need for day count test if asset bought/sold

AYB219 – Taxation Law and Practice Notes

Page 38 of 98

Depreciation rules for small business entities

Large business taxpayers

Computer software o Computer hardware (e.g. computers, screens etc.) depreciated using ordinary rules o Computer software: special deprecation rules

2 types:

Internally developed software o Optional: “software development pool”

Intended use: solely for producing assessable income o Depreciable using prime cost method:

0% in 1st year, 40% in 2nd year, 40% in 3rd year, 20% in 4th year

AYB219 – Taxation Law and Practice Notes

Page 39 of 98

Purchased software (“in-house” software) o Software purchases “off the shelf” o Developed/commissioned software not allocated to software

development pool o Depreciated over 4 years using prime cost method

I.e. 25%

Disposals of depreciated assets o “Balancing adjustment event” o Accounting term = gain / loss on sale

Comparison of accounting and tax terminology

AYB219 – Taxation Law and Practice Notes

Page 40 of 98

Deduction for Capital Works Expenditure

Available when capital works used to produce AI

Calculated on daily basis

Based on original construction cost o ATO will accept estimates TR 97/25

Rate depends on: o Year construction commenced and use of capital works

Division 43: “capital works”

What does construction expenditure include? o Construction costs o Preliminary expenses o Integral structural features o Does not include costs associated with:

Acquiring land Clearing land Demolishing existing structures Pre-construction site clearance Landscaping

AYB219 – Taxation Law and Practice Notes

Page 41 of 98

Substantiation of Work-Related Expenses

Required to substantiate: o Work, car & business travel expenses

Written evidence Retained for minimum of 5 years

Not required for: o Employment related expenses if total claim < $300 o Laundry expenses < $150 o Travel & overtime meal claims if < allowance received o Car expenses using cents per km method

AYB219 – Taxation Law and Practice Notes

Page 42 of 98

Examples William purchases a house that appeared to be in good repair. To make it more attractive to prospective tenants, minor repairs & renovations are undertaken costing $3,200. During the course of these repairs & renovations, William discovers that the ravages of white ants seriously affect the woodwork. William incurs $27,000 to remedy the problems caused by the white ant infestation & to restore the property to a state in which it is suitable for occupation by tenants What deductions (if any) can William claim under s 25-10 ITAA 1997?

No as it is an initial repair

Ken runs a manufacturing business in a building in which the wooden floor needs repairing. Ken’s options are either to repair the old floor or to replace it with an entirely new one of steel & concrete. Ken decides to adopt the second option because it will save future repairs & because it has distinct advantages over the old wooden floor Can Ken claim a deduction under s 25-10 ITAA 1997 for the replacement of the wooden floor?

No as it is a capital replacement cost On 17 January 2012, Mark incurred borrowing expenses totaling $8,240 with the Commonwealth Bank in arranging a $350,000 loan to finance the purchase of a rental property. Mark also incurred interest of $9,050 from 17 Jan - 30 June 2012. Property will be used exclusively for renting to tenants. Loan is for a term of 20 years What amount can Mark claim under s 25-25 ITAA 1997 in respect of the 2012 income year? Hint: from 17 Jan 2012 - 30 Jun 2012: 165 days

8240/(5*365)*165 = $745 On 22 February 2012, Debbie purchased a rental property for $450,000 & immediately rented it out. Debbie obtained a report from a quantity surveyor stating that the property was built in 2002 for an estimated construction cost of $300,000 What can Debbie claim as a capital works allowance for the 2012 income year? Hint: there are 129 day from 22 Feb 2012 to 30 Jun 2012

$300,000 * 2.5% * 129/365 = $2,651

AYB219 – Taxation Law and Practice Notes

Page 43 of 98

Lecture 6 – Capital Gains Tax

s102-5 ITAA 1997 says specifically that a net capital gain is included in your assessable income

CGT introduced on 20 Sept 1985 o Parts 3-1 & 3-3 ITAA 1997

CGT is not a separate tax

CGT applies: o Disposal of capital asset acquired on or after 20 Sept 1985 (examples?) o Disposal not undertaken in ordinary course of business

Assessable: s 6-5 (examples?)

Examples of where CGT applies: o Property (but not the house you live in – it is exempt) o Shares

CGT only applies if you are not taxed under your normal taxable income conditions

AYB219 – Taxation Law and Practice Notes

Page 44 of 98

Process of CGT determination

AYB219 – Taxation Law and Practice Notes

Page 45 of 98

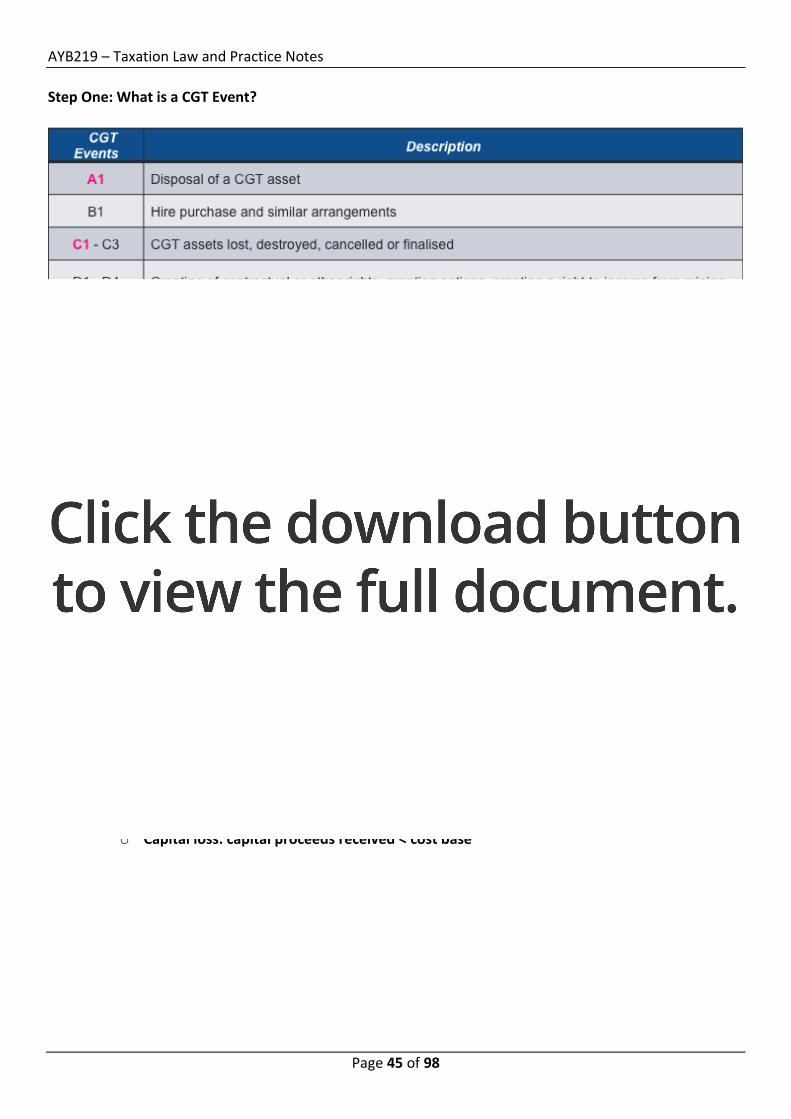

Step One: What is a CGT Event?

CGT Event A1: Disposal of a CGT asset o Disposal = change in legal & beneficial ownership o Event A1 occurs when:

(a) Contract signed (not settlement) (b) If no contract: physical change of ownership

CGT Event C1: Loss or destruction of a CGT asset o CGT event C1 occurs when:

Taxpayer insured: first received compensation Taxpayer not insured: destruction occurred

Can’t determine: loss is first discovered o Capital gain: capital proceeds received > cost base o Capital loss: capital proceeds received < cost base

AYB219 – Taxation Law and Practice Notes

Page 46 of 98

Step Two: What is a CGT Asset?

Post-CGT asset

S108-5(1) ITAA 1997: any kind of property o Examples? o How does CGT affect depreciating assets?

Classification: o Collectables

s 08-10(2):

(a) Paintings, sculptures, drawings, engravings, photographs, jewellery, an antique, coin or medallion;

(b) A rare portfolio, manuscript or book; or

(c) A postage stamp or a first day cover

that is used or kept mainly for the taxpayers personal use or enjoyment Calculation of CG & CL from collectibles

Rule 1: collectable acquired for > $500: CGT applies

Rule 2: collectable acquired for <= $500: exempt from CGT

Rule 3: Capital losses from collectables can only be used to offset capital gains from collectables

o Personal-use assets s108-20(2): CGT asset kept mainly for the taxpayer’s personal use or enjoyment

Excludes: o Collectibles o Land & buildings

E.g.: boats, furniture, electrical goods, household items (including pets) Calculation of CG & CL from personal use assets

Rule 1: personal use asset acquired for > $10,000: CGT applies

Rule 2: personal use asset acquired for ≤ 10,000: exempt from CGT

Rule 3: capital losses from personal use assets: disregarded o Other assets

Land and buildings

s108-55(1): land & buildings = separate assets for CGT purposes

Important for pre-CGT land & post-CGT buildings o Pre CGT land: exempt from CGT o Post CGT buildings: CGT applies

What is a post CGT building? o Contract?

Capital improvements

Capital improvements to post CGT asset o Included in cost base (4th element: s 110-25(4))

Capital improvements to pre-CGT asset? o Separate CGT asset if (s 108-70(2)): o Cost base when CGT event occurs is greater than:

CGT improvement threshold (2012: $130,418) and 5% of capital proceeds from sale of asset

Otherwise exempt from CGT

AYB219 – Taxation Law and Practice Notes

Page 47 of 98

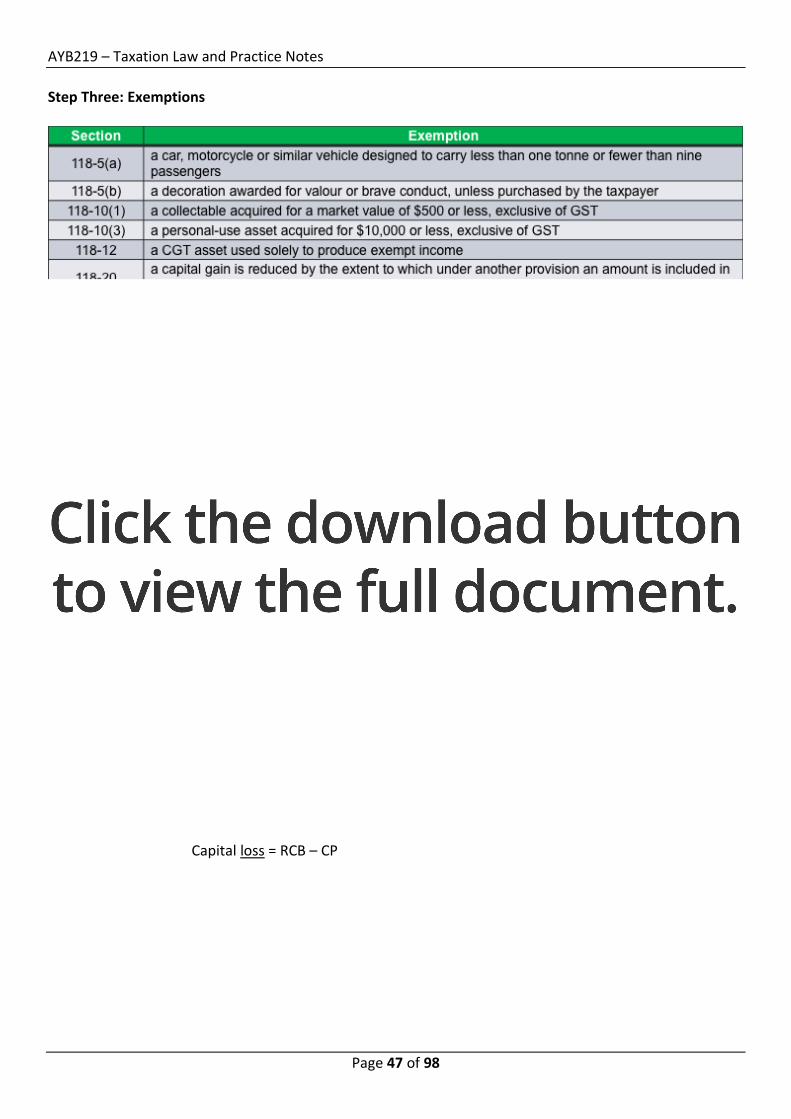

Step Three: Exemptions

Step Four: Rollover Relief

CGT rollover = CGT deferred

4 situations quality for rollover relief e.g.: o Disposal of CGT asset by an individual to wholly-owned company

There is no Step Five: Does a capital gain or loss eventuate?

s 100-45 : 3 steps to calculate capital gain or loss: o 1. Determine capital proceeds (CP) o 2. Determine cost base (CB) or reduced cost base (RCB) o 3. Capital gain = CP – CB

Capital loss = RCB – CP

AYB219 – Taxation Law and Practice Notes

Page 48 of 98

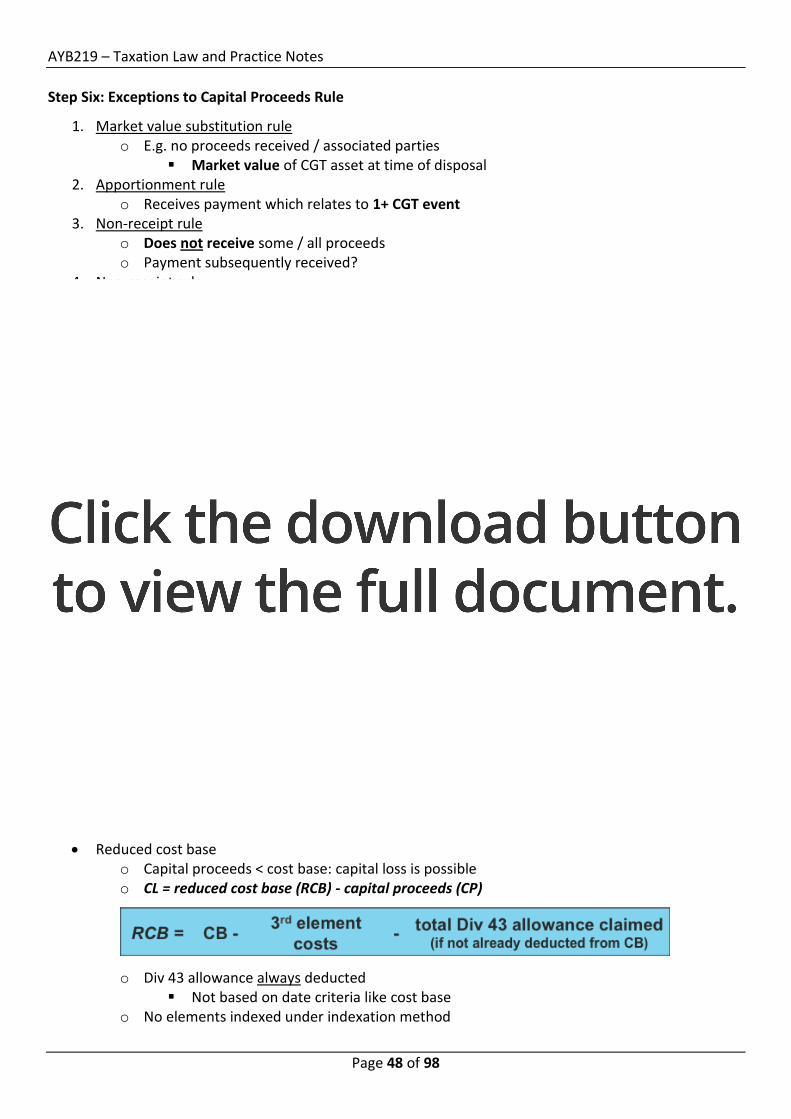

Step Six: Exceptions to Capital Proceeds Rule

1. Market value substitution rule o E.g. no proceeds received / associated parties

Market value of CGT asset at time of disposal 2. Apportionment rule

o Receives payment which relates to 1+ CGT event 3. Non-receipt rule

o Does not receive some / all proceeds o Payment subsequently received?

4. Non-receipt rule o Taxpayer repays part of proceeds to purchaser

5. Assumption of liability rule o Does purchaser assume any unpaid liability over asset?

6. Misappropriation rule o Agent or employee misappropriates capital proceeds

CP’s decreased Determining Cost Base

Reduced cost base o Capital proceeds < cost base: capital loss is possible o CL = reduced cost base (RCB) - capital proceeds (CP)

o Div 43 allowance always deducted Not based on date criteria like cost base

o No elements indexed under indexation method

AYB219 – Taxation Law and Practice Notes

Page 49 of 98

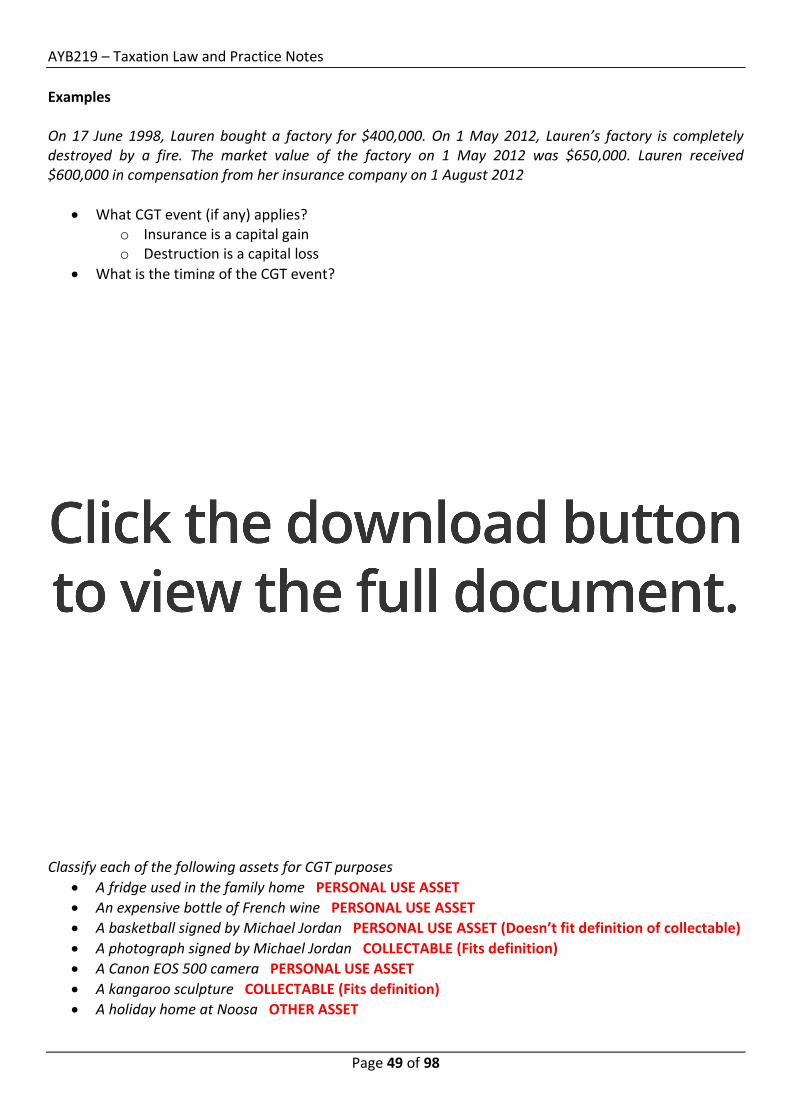

Examples On 17 June 1998, Lauren bought a factory for $400,000. On 1 May 2012, Lauren’s factory is completely destroyed by a fire. The market value of the factory on 1 May 2012 was $650,000. Lauren received $600,000 in compensation from her insurance company on 1 August 2012

What CGT event (if any) applies? o Insurance is a capital gain o Destruction is a capital loss

What is the timing of the CGT event? o 1st May

What if Lauren did not have insurance? o Always a capital loss

What is Lauren’s capital gain/loss o CL = 0 – 400,000 = $400,000 o CG = 600,000 – 400,000 = $200,000 o CL of $200,000 overall

During the 2012 income year, Adrian sells 2 collectables: a painting & a book. He derives a capital gain of $6,000 from the sale of a painting and a capital loss of $7,000 from the sale of a book. He also derives a capital gain of $10,000 from the sale of 2,000 Woolworth’s shares. What is Adrian’s assessable income for the 2012 income year?

CG = 6,000

CL = (7,000) – however it can only actually be 6000 as only collectables can offset collectables

CG = 10,000 – an other asset

Total assessable income is $10,000 On 15 December 2005, Geoff buys a boat for $12,000, which he used for his own personal use and enjoyment.

If Geoff sells the boat for $15,000 in August 2011 what are the CGT consequences (if any)?

If Geoff sells the boat for $11,000 in August 2011 what are the CGT consequences (if any)?

Sells boat for $15,000 - $3,000 CGT

Sells boat for $11,000 - $0 CGT Loss is offset (loss can never use used to offset for personal-use items)

Classify each of the following assets for CGT purposes

A fridge used in the family home PERSONAL USE ASSET

An expensive bottle of French wine PERSONAL USE ASSET

A basketball signed by Michael Jordan PERSONAL USE ASSET (Doesn’t fit definition of collectable)

A photograph signed by Michael Jordan COLLECTABLE (Fits definition)

A Canon EOS 500 camera PERSONAL USE ASSET

A kangaroo sculpture COLLECTABLE (Fits definition)

A holiday home at Noosa OTHER ASSET

AYB219 – Taxation Law and Practice Notes

Page 50 of 98

11 March 1982 Melanie purchased a block of land for $60,000. 1 May 1994 Melanie started construction of a building on this block of land, which ultimately cost $175,000. 6 March 2012 Melanie sold both the land & building for $350,000. At the time of sale, the land was valued at $140,000 Calculate Melanie’s capital gain for the year ended 30 June 2012

Value of building: 350,000 – 140,000 = 210,000

(140,000 of Land was sold tax free as it is pre CGT)

Gain on building = 210,000 – 175,000 = $35,000 CGT liability On 20 May 1993 Sharon purchases a rental property in Samford for $155,000. On 16 May 2005 she adds a veranda to the property at a cost of $35,000. On 9 February 2012 Sharon sells the rental property for $620,000 Is the veranda regarded as a separate asset for CGT purposes?

As the property is a post CGT asset then all improvements are included into the cost

CG = 620,000 – 35,000 – 155,000 = $430,000 Ruby sells a parcel of land under a contract of sale for $600,000, which was signed on 1 June 2012. Settlement (change of ownership) occurs on 1 July 2012. Ruby requires payment to be made in 3 instalments of $200,000 on 10 June 2012, 10 Sept 2012 & 10 Dec 2012.

What CGT event applies to Ruby? o Event A1 occurs

When does the CGT occur? o Event A1 is deemed to have occurred when the contract is signed, 1st June

What is Ruby’s capital proceeds? o Ruby’s capital proceeds are $600,000

When does she return this as assessable income? o CGT event A1 occurs 1st June 2012, cash she is entitled to receive happens at that time so it

is all in the 2012 income year.

On 14 April 2012, Mark transfers a vacant block of land to his wife, Tina, for no consideration. Mark acquired the land in March 1996 for $75,000. Market value of land on 14 April 2012 is $125,000

What CGT event (if any) applies to Mark? o CGT event A1 – change of ownership

What is Mark’s capital proceeds? o Are deemed to be $125,000 (the market value on sale) – even though he got no money. o He must include a capital gain of $50,000 in his tax return

Are any exemptions/concessions/rollovers available? o A vacant block of land gets none of this (could be a rollover if Family court ordered Mark to

give his wife the property)

What impact does that have on Tina? o Tina has dammed to have bought the property for $125,000. So if she later sells, this is cost

base

AYB219 – Taxation Law and Practice Notes

Page 51 of 98

On 16 May 2012, Joe signs a contract to sell a block of land to Maryanne for $275,000. Joe acquired the block of land in April 1996. Joe initially took out a loan with ANZ Bank to finance the acquisition of the block of land. On 16 May 2012, Joe still owes ANZ Bank a total of $200,000. As part of the sale agreement, Maryanne gives Joe $75,000 cash & agrees to assume liability for the outstanding amount of the loan (i.e. $200,000).

What CGT event (if any) applies to Joe? o Sale of land

What is Joe’s capital proceeds? o $75,000 + $200,000

15 November 1995, Paul acquired a rental property for $240,000 that was used exclusively for income-producing purposes. He paid legal fees of $4,000 & stamp duty of $5,200 on the same date. On 14 August 1999, Paul added a swimming pool to the house at a cost of $17,500. On 10 May 2012, Paul sold his rental property for $300,000. Sales commission totalled $9,000 Determine the cost base of the rental property with references to the various elements contained in s 110-25

240,000 is a capital cost

Legal fees of $4,000 & stamp duty of $5,200 are not tax deductible but you do count them in your cost base (as they are once off costs associated with acquisition)

17,500 pool is a capital cost

Sales commission is counted in the capital cost (as it is an expense of sale)

Cost base: $275,700 Peter acquired a rental property under a contract on 10 May 1996 for $200,000. Incidental costs of acquisition were $8,000. Peter has claimed 2.5% capital works allowance as a deduction under Div 43 of a total of $40,000 (based on a total construction cost of $100,000). On 10 May 2012 Peter sold the rental property for $200,000 Calculate Peter’s capital gain/(loss) on sale (if any) Capital gain: 200,000 – 208,000 = (8,000) Reduced cost base: 208,000 – 40,000 = 168,000 Capital loss = 168,000 – 200,000 = (32,000) As both the gain and loss formulas are negative, there is neither a gain or a loss. Hence the client has to pay no tax, yay!

AYB219 – Taxation Law and Practice Notes

Page 52 of 98

Lecture 8 – Capital Gains Tax Advanced Reducing a capital gain: 2 methods

Can use different methods for each CGT asset o Choose method with lowest capital gain o Note: conditions to use each method

Indexation method o Division 114: allows for effects of inflation o 1. CGT asset held for <12 months before disposal

No indexation available o 2. CGT asset held for > 12 months before disposal

Capital gain = capital proceeds – indexed cost base o Indexed cost base

Each element of cost base

Multiplied by relevant indexation factor

Rounded to 3 decimal places

Except 3rd element (ownership costs) Formula to obtain indexed cost base: quarter in which asset is disposed of / quarter

in which cost was incurred o SEE EXAMPLES ONE AND TWO FOR WORKING

AYB219 – Taxation Law and Practice Notes

Page 53 of 98

CGT discount method o Was brought in to make things easier! o CGT asset held < 12 months before disposal

Discount method not available o CGT asset held > 12 months before disposal

Capital gain = (capital proceeds – cost base) x (100% - discount percentage)

o Discount percentages: Individual – 50% Trust – 50% Super Fund – 33.33% Company – 0% Partnerships – doesn’t apply because profit goes back to an individual and

depending on their circumstances, it falls under one of the other four entity types o Rules surrounding use

Date the CGT Asset was acquired and

disposed of

Methods available to be used by eligible taxpayers

Indexation method CGT discount method

Asset acquired and disposed of before 21 September 1999

Asset acquired before 21 September 1999 and disposed of

after 21 September 1999

Asset acquired and disposed of

after 21 September 1999

AYB219 – Taxation Law and Practice Notes

Page 54 of 98

What method should you use?

Applying Capital Losses

Capital losses only offset against capital gains derived o Oldest losses used first o Capital losses fully utilised?

Indexation: against indexed capital gain

CGT discount method: against gross capital gain o Before CGT discount applied

No capital gains? Capital losses carried forward

Applying Capital Losses: Example

AYB219 – Taxation Law and Practice Notes

Page 55 of 98

Main Residence Exemption: Basic Concepts

s118-110: any CG or CL from a taxpayer’s dwelling & adjacent land is disregarded if: o Taxpayer is an individual and o Dwelling was taxpayer’s MR throughout entire ownership period

CGT will apply if: o MR used for purpose of producing assessable income o MR for only part of ownership period

What is a dwelling? o s118-115: any unit of accommodation that is used mainly for residential purposes &

includes: House or cottage Apartment, flat or unit Unit in a retirement village Caravan, houseboat or other mobile home

o How long do you need to live in dwelling? o Adjacent land (s118-120)

MR exemption extends to “adjacent land” Applies provided adjacent land is:

Close to or near dwelling

Used primarily for private or domestic purposes in association with the dwelling

Total area of the land does not exceed 2 hectares (or 4.94 acres)

Land & dwelling must be sold under same contract of sale

Changing MR o Taxpayer only entitled to 1 MR at any one time o Taxpayer acquires a dwelling that will become their MR but still owns an existing residence?

Both dwellings treated as MR for up to 6 months if:

Old dwelling was taxpayer’s MR for continuous period of at least 3 months in previous 12 months before sale

Old dwelling was not used for producing assessable income in any part of that 12 month period &

New dwelling becomes the taxpayer’s MR

Only 1 MR o Takes longer than 6 months to sell old MR?

Taxpayer still entitled to 6-month exemption Time period > 6 months subject to CGT

o CG/ CL pro-rated: Number of days in excess of six-month period Total number of days taxpayer owned the dwelling

Choice of MR o Taxpayer can only claim MR exemption:

For 1 MR at a time (subject to 6-month overlap rule) Even if owns 2 places & lives in both concurrently

E.g. city home & coast home

Elect 1 as MR exemption Choice made when tax return is prepared for year when first property is sold

AYB219 – Taxation Law and Practice Notes

Page 56 of 98

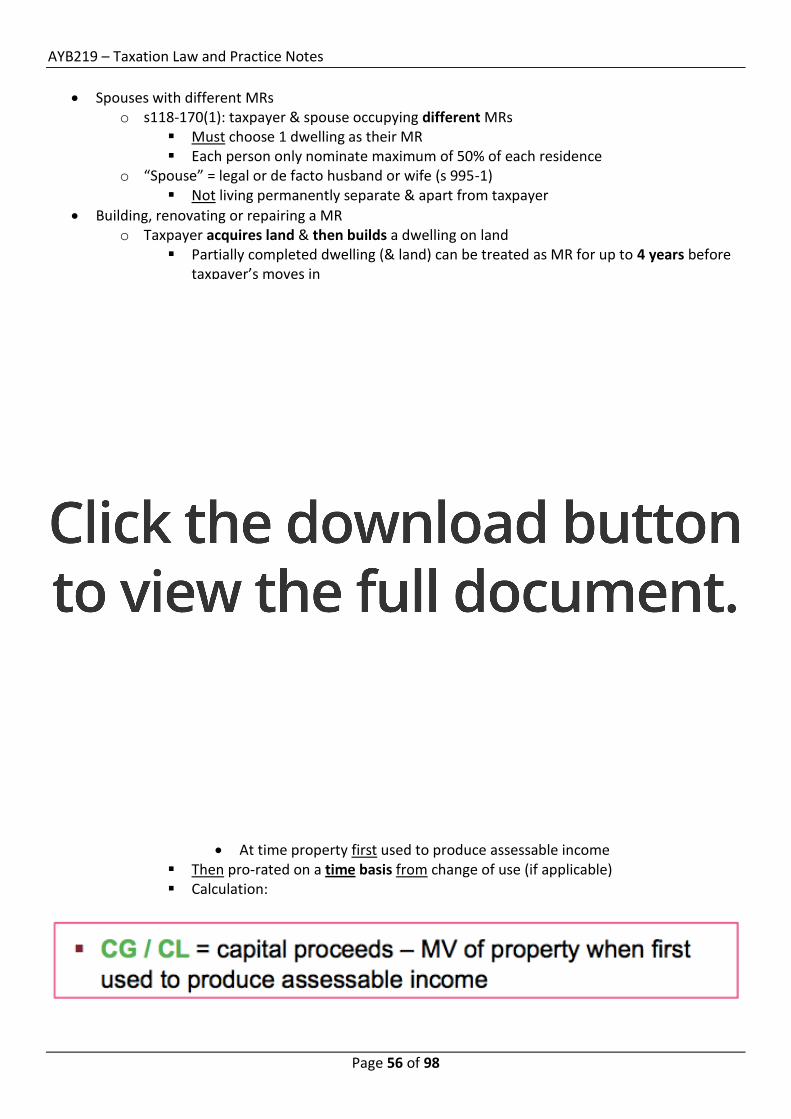

Spouses with different MRs o s118-170(1): taxpayer & spouse occupying different MRs

Must choose 1 dwelling as their MR Each person only nominate maximum of 50% of each residence

o “Spouse” = legal or de facto husband or wife (s 995-1) Not living permanently separate & apart from taxpayer

Building, renovating or repairing a MR o Taxpayer acquires land & then builds a dwelling on land

Partially completed dwelling (& land) can be treated as MR for up to 4 years before taxpayer’s moves in

o Completed dwelling must become taxpayer’s MR as soon as practicable & o Taxpayer resides in MR for at least 3 months before sale o No other dwelling can be taxpayer’s MR during same period

Except 6-month double up exemption

Absence from MR o Taxpayer who initially occupies a dwelling as a MR & then ceases to occupy it

Still treat dwelling as their MR for: o Max 6 years if dwelling used to produce assessable income while taxpayer is absent o Indefinitely if dwelling is not used to produce assessable income (s 118-145(3))

Change of purpose of MR o Taxpayer may change the use of their entire property e.g. from a MR to a rental property

CGT impact depends on when change of use occurred

I.e. before/after 20 August 1996 o Before 20 Aug 1996: apportioned on time basis o After 20 Aug 1996: based on market value when change occurred

Apportioned on time basis from that point

o Property first used to produce assessable income before 20 August 1996 s118-185: MR exemption is pro-rated on a time basis Calculation:

o Property first used to produce assessable income on or after 20 August 1996 s118-192: taxpayer deemed to have acquired dwelling at its market value

At time property first used to produce assessable income Then pro-rated on a time basis from change of use (if applicable) Calculation:

AYB219 – Taxation Law and Practice Notes

Page 57 of 98

Use of MR for producing AI o Taxpayer uses part of their MR to conduct a business?

Apportioned on both a time & area basis o Time basis: rules previously discussed still apply

I.e. when did change of use occur? Before/after 20 August 1996? o Area basis:

Lecture 4: deductions pro-rated based on floor space CG / CL also apportioned based on floor space

CGT Administration

If taxpayer inherits a CGT asset: important to keep appropriate records: o MV of pre-CGT assets on date of death o Cost base details for post-CGT assets o Capital expenditure incurred by legal representative during administration of the estate

Option of maintaining records or an asset register

CGT Records o s121-20(1): required to keep records of:

Every act, transaction, event or circumstance Reasonably expected to be relevant in calculating a CG/CL from a CGT event

o Not required if CG/CL is disregarded E.g. pre-CGT assets or CGT exempt assets

o s121-25: records maintained for 5 years from date of CGT event

Asset register o s121-35: information required:

Date of asset’s acquisition Cost of the asset A description, amount & date of each cost associated with asset’s purchase (e.g.

stamp duty & legal fees) Other relevant information (e.g. capital improvements) Date of the CGT event (e.g. date of disposal) Capital proceeds in respect of the CGT event

o Entries certified by a tax agent & in English o Source documents retained for 5 years from entry into register

AYB219 – Taxation Law and Practice Notes

Page 58 of 98