autonomous group learning (agl) agl no. 1 - agl no. 1 - finance for finance for non - financial...

TRANSCRIPT

AUTONOMOUS GROUP LEARNING (AGL)AUTONOMOUS GROUP LEARNING (AGL)

AGL NO. 1 - AGL NO. 1 -

FINANCE FOR FINANCE FOR

NON - FINANCIAL MANAGERSNON - FINANCIAL MANAGERS

DAILY WORK PACK - PART IDAILY WORK PACK - PART I Copyright: RGAB/IR 2010/2Copyright: RGAB/IR 2010/2

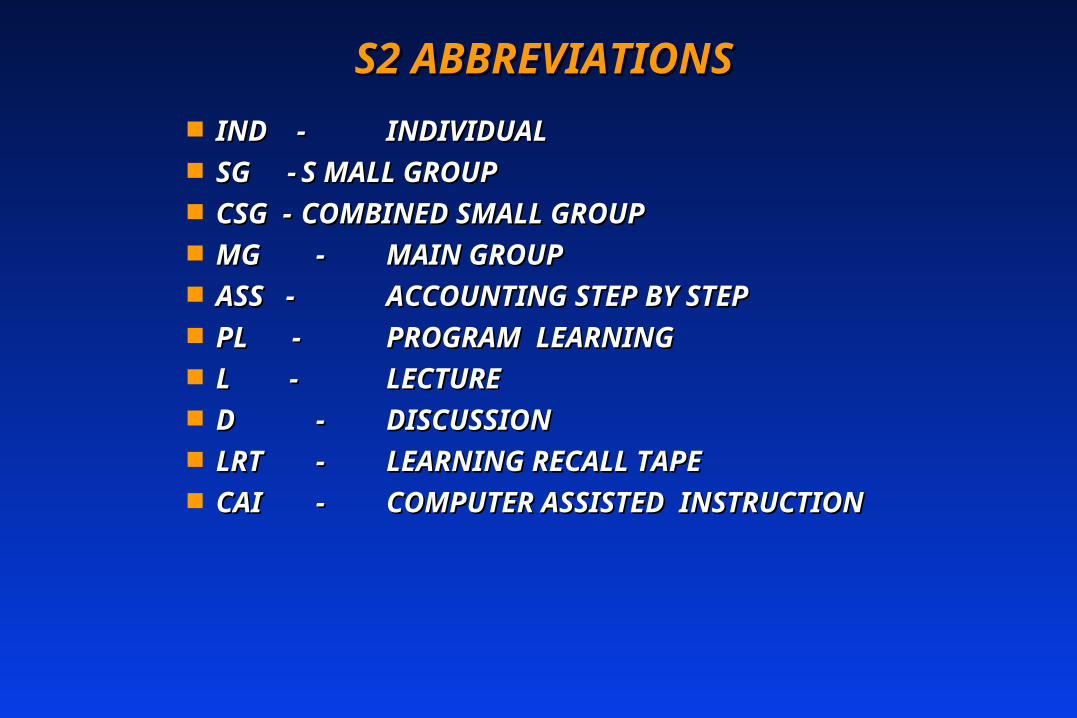

S2 ABBREVIATIONSS2 ABBREVIATIONS IND - IND - INDIVIDUALINDIVIDUAL SG -SG - S MALL GROUPS MALL GROUP CSG - CSG - COMBINED SMALL GROUPCOMBINED SMALL GROUP MG MG - - MAIN GROUPMAIN GROUP ASS - ASS - ACCOUNTING STEP BY STEP ACCOUNTING STEP BY STEP PL - PL - PROGRAM LEARNINGPROGRAM LEARNING L - L - LECTURELECTURE D D - - DISCUSSIONDISCUSSION LRTLRT - - LEARNING RECALL TAPELEARNING RECALL TAPE CAICAI - - COMPUTER ASSISTED COMPUTER ASSISTED

INSTRUCTION INSTRUCTION

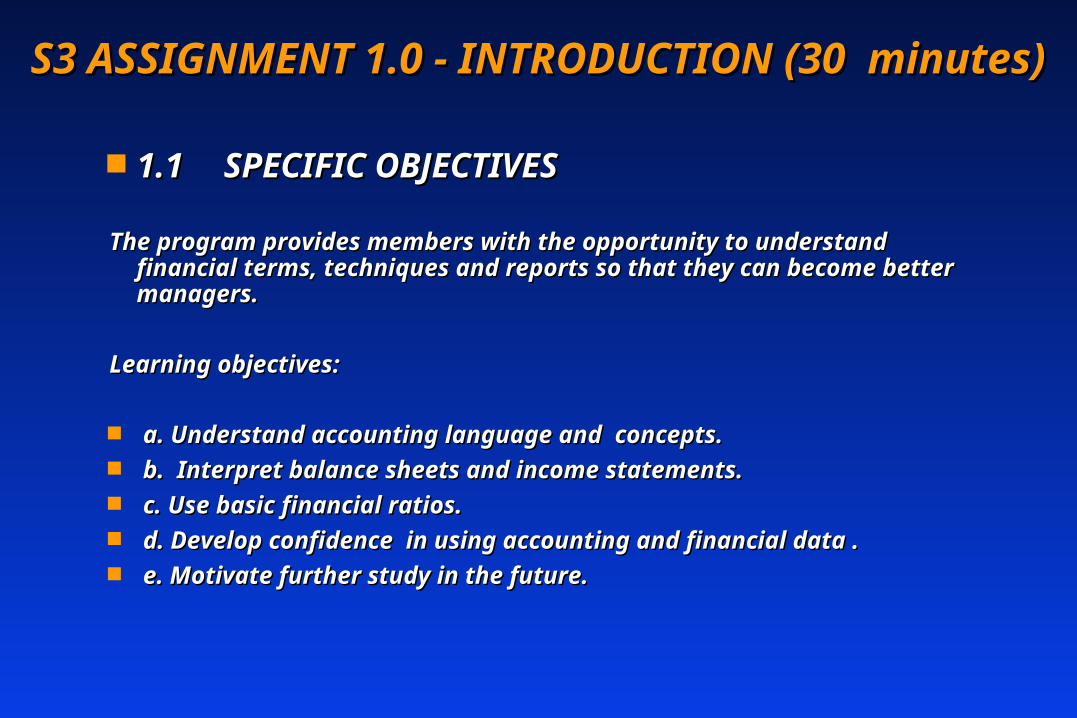

S3 ASSIGNMENT 1.0 - INTRODUCTION (30 S3 ASSIGNMENT 1.0 - INTRODUCTION (30 minutes) minutes)

1.11.1 SPECIFIC OBJECTIVESSPECIFIC OBJECTIVES

The program provides members with the opportunity to The program provides members with the opportunity to understand financial terms, techniques and reports so that understand financial terms, techniques and reports so that they can become better managers.they can become better managers.

Learning objectives:Learning objectives:

a. Understand accounting language and concepts.a. Understand accounting language and concepts. b. Interpret balance sheets and income statements.b. Interpret balance sheets and income statements. c. Use basic financial ratios.c. Use basic financial ratios. d. Develop confidence in using accounting and financial d. Develop confidence in using accounting and financial

data .data . e. Motivate further study in the future.e. Motivate further study in the future.

S4 1.1 SPECIFIC OBJECTIVES (continued)S4 1.1 SPECIFIC OBJECTIVES (continued)

The syllabus of the program includes: The syllabus of the program includes:

accounting terminology, concepts, and reports accounting terminology, concepts, and reports liquidity & profitabilityliquidity & profitability evaluating business potential of new ventures and evaluating business potential of new ventures and

projectsprojects activity analysis & operating statementsactivity analysis & operating statements reserves and equityreserves and equity financial forecasting & budgeting financial forecasting & budgeting LAPP system of financial analysis.LAPP system of financial analysis.

S5 1.2 AUTOMATED GROUP LEARNING S5 1.2 AUTOMATED GROUP LEARNING (AGL)(AGL)

The AGL method is designed to achieve rapid The AGL method is designed to achieve rapid individual learning using special materials and the individual learning using special materials and the stimulus of group activity without a formal stimulus of group activity without a formal instructor. instructor.

The groups use the materials to find the answers to The groups use the materials to find the answers to

all problems and questions.all problems and questions.

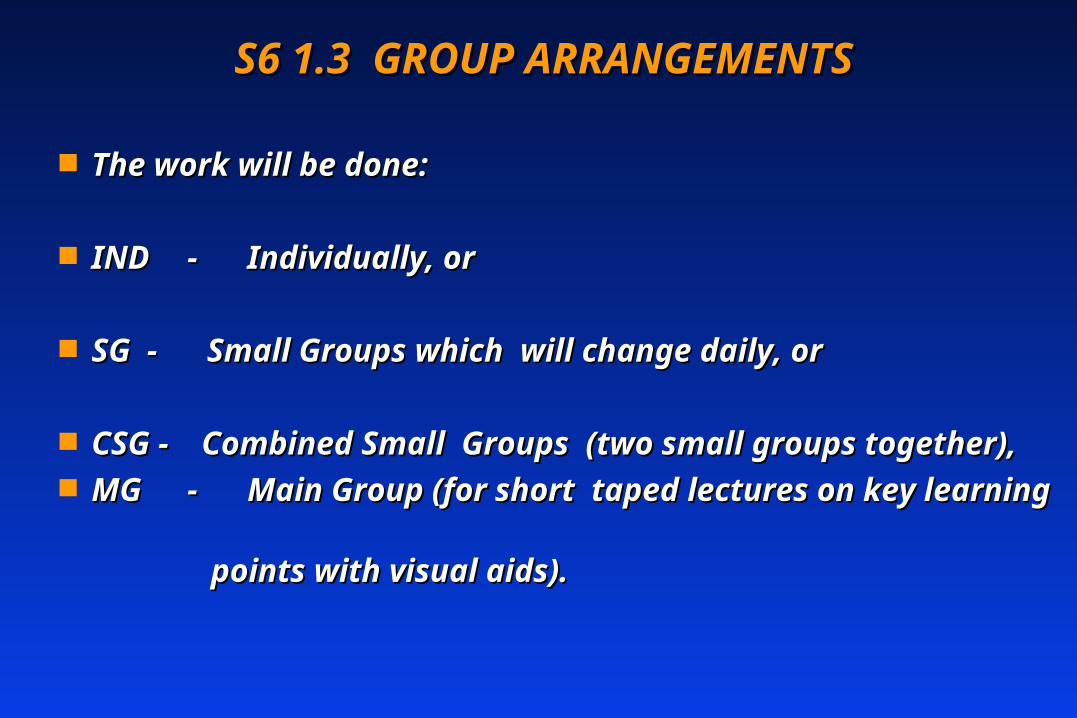

S6 1.3 GROUP ARRANGEMENTSS6 1.3 GROUP ARRANGEMENTS

The work will be done:The work will be done:

INDIND - Individually, or- Individually, or

SG - Small Groups which will change daily, orSG - Small Groups which will change daily, or

CSG - Combined Small Groups (two small groups CSG - Combined Small Groups (two small groups together), together),

MGMG - Main Group (for short taped lectures on key - Main Group (for short taped lectures on key learning learning

points with visual aids).points with visual aids).

S7 1.4 SG - SMALL GROUPSS7 1.4 SG - SMALL GROUPS

Group names provided on the flip charts. Group names provided on the flip charts.

Please note the name of your SG and names Please note the name of your SG and names of the other members.of the other members.

S8 1.5 LEARNING MATERIALSS8 1.5 LEARNING MATERIALS

(a)(a) Retained by membersRetained by members

Textbook (ASS)Textbook (ASS)

Notebook - for recording every key pointNotebook - for recording every key point

Daily Course DiaryDaily Course Diary

Learning Recall TapeLearning Recall Tape

Articles (2)Articles (2)

(b) Used by not retained by members:(b) Used by not retained by members:

Daily work packs including: introduction, lectures, Daily work packs including: introduction, lectures,

cases, exercises and key learning points cases, exercises and key learning points

S9 1.5 LEARNING MATERIALS (continued)S9 1.5 LEARNING MATERIALS (continued)

Use your notebook. Do not mark the Daily Use your notebook. Do not mark the Daily Workpack which must be handed back at the Workpack which must be handed back at the end of each day.end of each day.

You receive all the materials in your SG. You receive all the materials in your SG.

Don't look ahead in the workpack until you are Don't look ahead in the workpack until you are specifically asked to do so!specifically asked to do so!

S10S10 1.61.6 METHODMETHOD

Try to complete every task in the time allowed. Try to complete every task in the time allowed.

A pattern of learning methods will be used including:A pattern of learning methods will be used including:

• Programmed learningProgrammed learning• Case analysisCase analysis• LecturesLectures• QuizzesQuizzes• Learning patternsLearning patterns• Homework readingHomework reading• Learning Recall Tape (LRT)Learning Recall Tape (LRT)• CAICAI

S11S11 1.71.7 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW 1. Objectives

Language

Ratios Concepts

Forecasting Balance Sheets

Income Statements Financial Health

CONFIDENCE

S12S12 1.71.7 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW2. Learning

continuous activity ....

• IND SG CSG MG

Program Learning Small Groups

Lectures Combined Small Group

Cases & Exercixes Main Group

LRT CAI

LEARNING FOR YOU

S13 1.7 LEARNING PATTERNS - REVIEWS13 1.7 LEARNING PATTERNS - REVIEW 3 3. Methods

S14S14 1.81.8 INSTRUCTIONS (15 minutes)INSTRUCTIONS (15 minutes)

Assemble in SG's to introduce yourself, indicate Assemble in SG's to introduce yourself, indicate your past experience in finance and what you your past experience in finance and what you hope to contribute to and gain from the course.hope to contribute to and gain from the course.

Complete the registration sheet in the Daily Complete the registration sheet in the Daily Course Diary.Course Diary.

NOTE: Please check that you have a full set of NOTE: Please check that you have a full set of learning materials now.learning materials now.

S15 ASSIGNMENT 2.0 - QUIZ (45 S15 ASSIGNMENT 2.0 - QUIZ (45 minutes)minutes)

2.1 INSTRUCTIONS SMALL GROUP WORK2.1 INSTRUCTIONS SMALL GROUP WORK

Assemble in SGAssemble in SG

Answer the quiz of 100 questions; mark your Answer the quiz of 100 questions; mark your answers a, b, c, or d with a clear "x" on the special answers a, b, c, or d with a clear "x" on the special form provided in the course diaryform provided in the course diary

Work as quickly as possible but don't guess - leave Work as quickly as possible but don't guess - leave blanks. Hand in your answer sheet to the Organizerblanks. Hand in your answer sheet to the Organizer

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

S 16 ASSIGNMENT 3.0 - PROGRAMME S 16 ASSIGNMENT 3.0 - PROGRAMME LEARNING (60 minutes) LEARNING (60 minutes)

Assemble in SGAssemble in SG

Read ASS pages 9 and 10 "How to use the programme"Read ASS pages 9 and 10 "How to use the programme"

Read ASS Ch. 1. Do ASS Ch. 2 in writing and aloudRead ASS Ch. 1. Do ASS Ch. 2 in writing and aloud

Record significant points in your notebookRecord significant points in your notebook

Reassemble in MG when the bell rings AReassemble in MG when the bell rings A

S17 3. 1 INSTRUCTIONS - INDIVIDUAL S17 3. 1 INSTRUCTIONS - INDIVIDUAL WORK (continued)WORK (continued)

Work very quickly. Work very quickly.

Write the answers in the ASS book; check out one Write the answers in the ASS book; check out one question at a time.question at a time.

Don't hesitate to "cheat" when you don't know the Don't hesitate to "cheat" when you don't know the answer answer

In finance a little "cheating" can be very educational In finance a little "cheating" can be very educational ......

S18 ASSIGNMENT 4.0 - LECTURE ON S18 ASSIGNMENT 4.0 - LECTURE ON ACCOUNTING REPORTS ACCOUNTING REPORTS

4.1 METHOD4.1 METHOD

Read aloud, listen and respond Read aloud, listen and respond verbally to any questions. verbally to any questions.

S19 4.2 ACCOUNTING REPORTSS19 4.2 ACCOUNTING REPORTS

(a) Income Statement (IS)(a) Income Statement (IS)

Profit and Loss Account or Operating StatementProfit and Loss Account or Operating Statement Accounting period is one yearAccounting period is one year

Sales less cost of goods actually sold = gross profitSales less cost of goods actually sold = gross profit Gross profit less expenses = net profit Gross profit less expenses = net profit

Ratios are thermometersRatios are thermometers Gross profit over sales = gross profit percentageGross profit over sales = gross profit percentage Net profit over sales = net profit percentageNet profit over sales = net profit percentage

S20 4.2 ACCOUNTING REPORTS S20 4.2 ACCOUNTING REPORTS (continued)(continued)

(b) Balance Sheet (BS)(b) Balance Sheet (BS)

Situation at the beginning of accounting period Situation at the beginning of accounting period

Situation at end of accounting periodSituation at end of accounting period

Assets of a business are financed by liabilities and Assets of a business are financed by liabilities and owners' equityowners' equity

S21 ASSETS AND LIABILITIESS21 ASSETS AND LIABILITIES

4.3 ASSETS (A)4.3 ASSETS (A)

Things owned by a business which have measurable Things owned by a business which have measurable cost: cash, accounts receivable (debtors), inventories cost: cash, accounts receivable (debtors), inventories (stock), prepayments, equipment, buildings, land, etc.(stock), prepayments, equipment, buildings, land, etc.

4.4 LIABILITIES (L)4.4 LIABILITIES (L)

Amounts due to be paid (cash must be paid to "them"): Amounts due to be paid (cash must be paid to "them"): accounts payable, trade creditors, other liabilities, accounts payable, trade creditors, other liabilities, taxation payable, long term liabilitiestaxation payable, long term liabilities

S22 4.5 OWNERS' EQUITYS22 4.5 OWNERS' EQUITY

Rights of the owners of a businessRights of the owners of a business

Initial capital plus profitsInitial capital plus profits

Assets less liabilities = owners' equityAssets less liabilities = owners' equity

Assets less liabilities = owners' equityAssets less liabilities = owners' equity

Profits increase owners' equityProfits increase owners' equity

Losses reduce owners' equityLosses reduce owners' equity

S23 4.6 EQUITY:DEBT (LIABILITIES) (E:D)S23 4.6 EQUITY:DEBT (LIABILITIES) (E:D)

This means equity as distinct from liabilitiesThis means equity as distinct from liabilities

Ratio of assets financed from owners equity and Ratio of assets financed from owners equity and liabilitiesliabilities

This is the “gearing” of the company which is This is the “gearing” of the company which is critical to financial health..critical to financial health..

S24 4.7 TRANSACTIONSS24 4.7 TRANSACTIONS

Each transaction has a dual effectEach transaction has a dual effect

Assets increase and cash decreases, orAssets increase and cash decreases, or

Assets increase and liabilities increase, orAssets increase and liabilities increase, or

Cash decreases and liabilities decreaseCash decreases and liabilities decrease

S25 4.8S25 4.8 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW

1. Key Issues•

CASH• INVENTORY

• ORDERS

S26 4.8S26 4.8 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW

2. Income Statements

• C + E + P = S

• C + E + P = S

• C + E + P = S

S27 4.8S27 4.8 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW

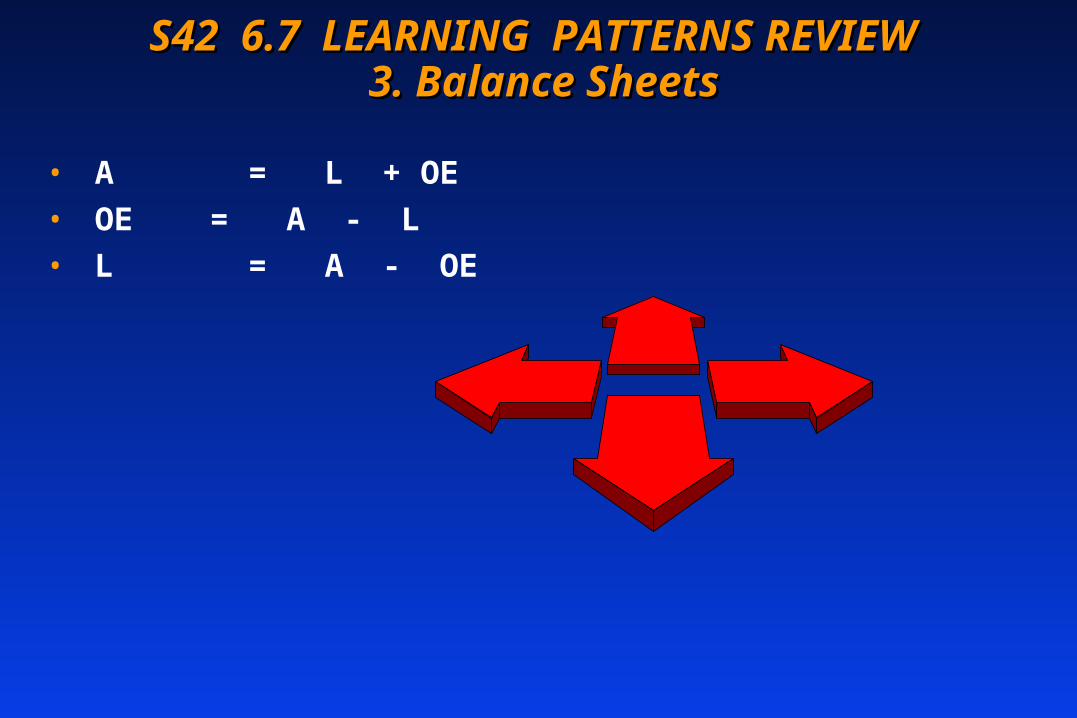

3. Balance Sheets• A = L + OE

• OE = A - L

• L = A - OE

S28 4.8S28 4.8 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW

4. Transactions CASH 0 A + L +

CASH - A 0 L -

S29 4.9S29 4.9 INSTRUCTIONS (10 minutes)9INSTRUCTIONS (10 minutes)9

Reassemble in SGReassemble in SG

Study the lecture very carefully and record key Study the lecture very carefully and record key points in your notebookpoints in your notebook

Discuss any outstanding questions in SGDiscuss any outstanding questions in SG

When the bell rings carry on with the case study When the bell rings carry on with the case study which followswhich follows

S30 ASSIGNMENT 6.0 LECTURE - JOHN S30 ASSIGNMENT 6.0 LECTURE - JOHN MARAIS MARAIS

6.16.1 STORY OF THE CASESTORY OF THE CASE

John Marais has been in business for 6 months John Marais has been in business for 6 months producing a toy. producing a toy.

He reckons he made a profit of 10,000 and has He reckons he made a profit of 10,000 and has drawn 50,000 from the business. drawn 50,000 from the business.

He thinks he has done rather well, so let's now He thinks he has done rather well, so let's now

review the accounts. review the accounts.

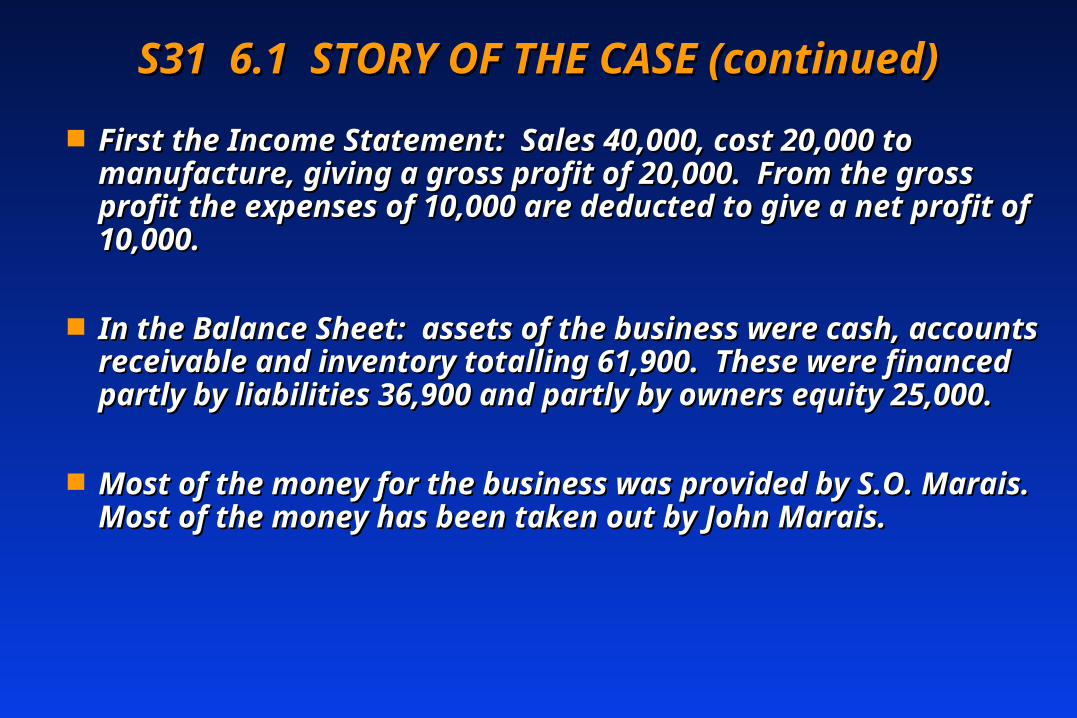

S31 6.1 STORY OF THE CASE (continued)S31 6.1 STORY OF THE CASE (continued)

First the Income Statement: Sales 40,000, cost 20,000 to First the Income Statement: Sales 40,000, cost 20,000 to manufacture, giving a gross profit of 20,000. From the manufacture, giving a gross profit of 20,000. From the gross profit the expenses of 10,000 are deducted to give a gross profit the expenses of 10,000 are deducted to give a net profit of 10,000.net profit of 10,000.

In the Balance Sheet: assets of the business were cash, In the Balance Sheet: assets of the business were cash, accounts receivable and inventory totalling 61,900. These accounts receivable and inventory totalling 61,900. These were financed partly by liabilities 36,900 and partly by were financed partly by liabilities 36,900 and partly by owners equity 25,000. owners equity 25,000.

Most of the money for the business was provided by S.O. Most of the money for the business was provided by S.O.

Marais. Most of the money has been taken out by John Marais. Most of the money has been taken out by John Marais.Marais.

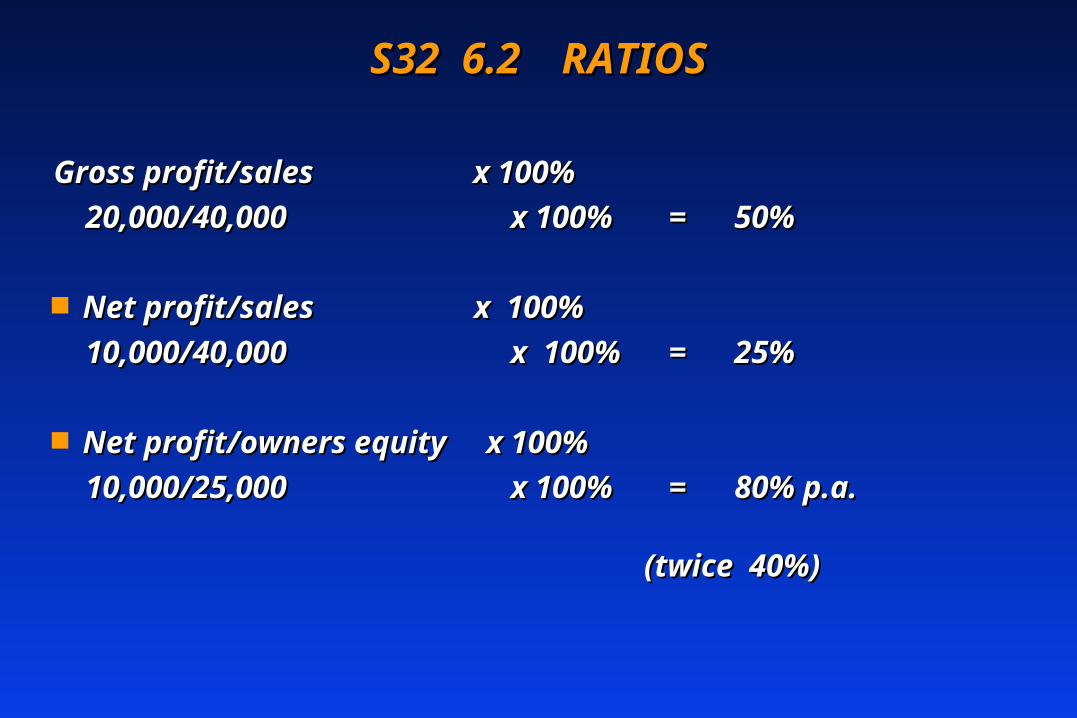

S32 6.2S32 6.2 RATIOSRATIOS

Gross profit/sales x 100%Gross profit/sales x 100%

20,000/40,000 x 100% = 50%20,000/40,000 x 100% = 50%

Net profit/sales x 100%Net profit/sales x 100%

10,000/40,000 x 100% = 25%10,000/40,000 x 100% = 25%

Net profit/owners equity x 100%Net profit/owners equity x 100%

10,000/25,000 x 100% = 80% 10,000/25,000 x 100% = 80% p.a. p.a.

(twice 40%)(twice 40%)

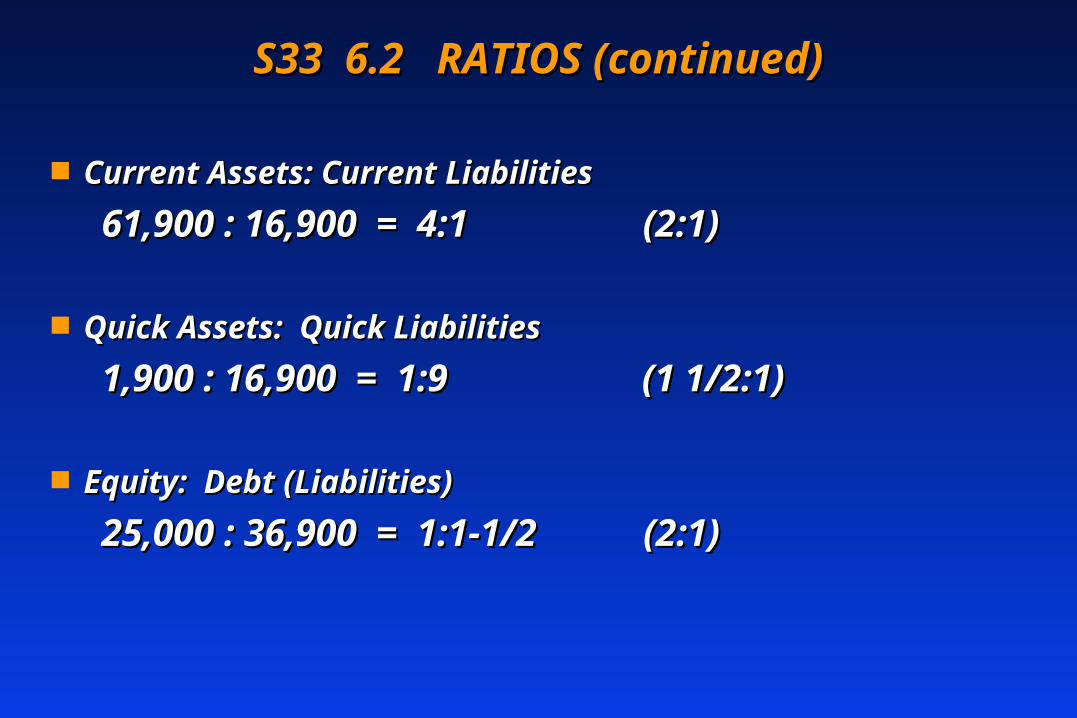

S33 6.2 RATIOS (continued)S33 6.2 RATIOS (continued)

Current Assets: Current LiabilitiesCurrent Assets: Current Liabilities

61,900 : 16,900 = 4:1 (2:1)61,900 : 16,900 = 4:1 (2:1)

Quick Assets: Quick LiabilitiesQuick Assets: Quick Liabilities

1,900 : 16,900 = 1:9 (1 1/2:1) 1,900 : 16,900 = 1:9 (1 1/2:1)

Equity: Debt (Liabilities)Equity: Debt (Liabilities)

25,000 : 36,900 = 1:1-1/2 (2:1)25,000 : 36,900 = 1:1-1/2 (2:1)

S34 6.3 FINANCIAL HEALTHS34 6.3 FINANCIAL HEALTH

((a) Liquidity - current assets to current liabilities a) Liquidity - current assets to current liabilities are strong but quick assets to quick liabilities are are strong but quick assets to quick liabilities are weak, indicating a cash shortage = Critical Point.weak, indicating a cash shortage = Critical Point.

Equity : Debt - less than 1:1 means that there is not Equity : Debt - less than 1:1 means that there is not enough equity in the business = Critical Point.enough equity in the business = Critical Point.

Drawings of 50,000 in this early stage of the Drawings of 50,000 in this early stage of the business have led to a cash shortage = Critical business have led to a cash shortage = Critical Point. Point.

S35 6.3 FINANCIAL HEALTH (continued)S35 6.3 FINANCIAL HEALTH (continued)

(b)(b) Activity - sales of 40,000 cost only 20,000 Activity - sales of 40,000 cost only 20,000 against a remaining inventory of 60,000.against a remaining inventory of 60,000.

Thus for one toy sold we have three unsold in Thus for one toy sold we have three unsold in inventory. inventory.

Production and marketing must be balanced = Production and marketing must be balanced = Critical Point.Critical Point.

S36 6.3 FINANCIAL HEALTH (continued)S36 6.3 FINANCIAL HEALTH (continued)

(c)(c) Profitability - good, but profit depends upon the value of Profitability - good, but profit depends upon the value of the inventory which includes 50,000 of wages. If the inventory the inventory which includes 50,000 of wages. If the inventory valued at market price is lower than cost (Christmas market valued at market price is lower than cost (Christmas market has disappeared) then the inventory value must come down. has disappeared) then the inventory value must come down.

Reduction in inventory value reduces the profit. Thus a Reduction in inventory value reduces the profit. Thus a reduction from 60,000 to 50,000 in inventory would mean no reduction from 60,000 to 50,000 in inventory would mean no profit this year at all! = Critical Point.profit this year at all! = Critical Point.

(d) (d) Potential - Christmas is over; there is only one product; Potential - Christmas is over; there is only one product; the garage is full of unsold toys; the cash is short; payments the garage is full of unsold toys; the cash is short; payments to creditors are overdue; management is doubtful = Critical to creditors are overdue; management is doubtful = Critical Point.Point.

S37 6.4 ACHIEVEMENTS AND PROBLEMSS37 6.4 ACHIEVEMENTS AND PROBLEMS

John Marais has started the business and if the inventory John Marais has started the business and if the inventory can be sold at least for cost, he has made a small profit.can be sold at least for cost, he has made a small profit.

He has drawn a large salary which is only earned if the He has drawn a large salary which is only earned if the inventory can be sold.inventory can be sold.

The Christmas trade is over and he may make no sales for The Christmas trade is over and he may make no sales for the next few months. He needs cash to pay his creditors. the next few months. He needs cash to pay his creditors. His inventory is too high and he may never sell it.His inventory is too high and he may never sell it.

He is not managing his finances well and may be bankrupt He is not managing his finances well and may be bankrupt if the creditors press for payment.if the creditors press for payment.

S38 6.5 PLAN OF ACTION S38 6.5 PLAN OF ACTION

Get cash to pay the creditorsGet cash to pay the creditors

Stop production and sell off the inventory.Stop production and sell off the inventory.

Consider whether the business is viable or product range Consider whether the business is viable or product range too narrow to be worthwhiletoo narrow to be worthwhile

Cut the salary to nothing. Look for partner with some Cut the salary to nothing. Look for partner with some moneymoney

Go out and sell (or go to work for someone else).Go out and sell (or go to work for someone else).

S39 6.6 LEARNING POINTS (continued) S39 6.6 LEARNING POINTS (continued)

(a) Cash is more important than profit in running a business, (a) Cash is more important than profit in running a business,

because without cash the manager can do nothing.because without cash the manager can do nothing.

(b) Ratios are useful in assessing the health of a business as (b) Ratios are useful in assessing the health of a business as

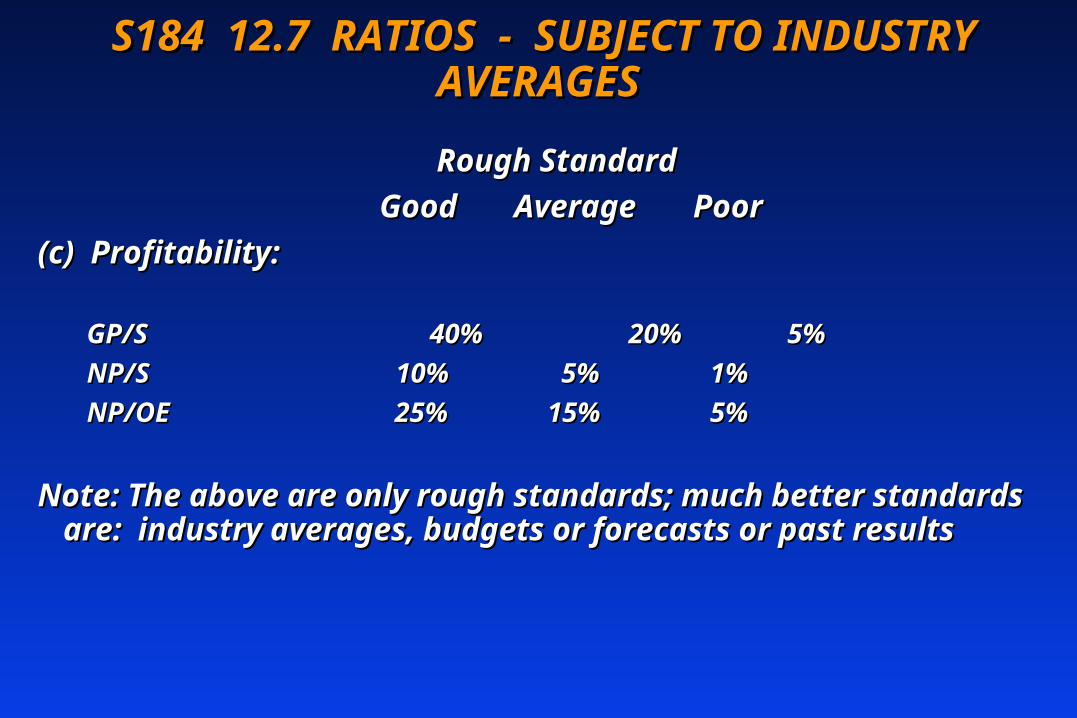

follows: Liquidity & Gearing, Activity, Profitability and Potential.follows: Liquidity & Gearing, Activity, Profitability and Potential.

(c) It is not correct to charge all the wages to manufacturing (c) It is not correct to charge all the wages to manufacturing

cost, because this increases the cost of the inventory .cost, because this increases the cost of the inventory .

S39 6.6 LEARNING POINTS (continued) S39 6.6 LEARNING POINTS (continued)

(d)(d) The inventory is valued at the lower cost or market valueThe inventory is valued at the lower cost or market value

(e)(e) Inventory valuation is the key to profitInventory valuation is the key to profit

(f)(f) High drawings by the owner are bad for an expanding High drawings by the owner are bad for an expanding business.business.

(g)(g) Look for the story behind the figures. Learn the Look for the story behind the figures. Learn the language of accounting quickly.language of accounting quickly.

(h)(h) All financial statements are estimates based upon All financial statements are estimates based upon assumptions. They are not scientific facts.assumptions. They are not scientific facts.

S40 6.7 LEARNING PATTERNS - REVIEWS40 6.7 LEARNING PATTERNS - REVIEW 1. Key Issues 1. Key Issues

• CASH

• INVENTORY

• ORDERS

S41 6.7 LEARNING PATTERNS REVIEW S41 6.7 LEARNING PATTERNS REVIEW 2. Income Statements2. Income Statements

• C E P = S

• C E P = S

• C E P = S

S42 6.7 LEARNING PATTERNS REVIEW S42 6.7 LEARNING PATTERNS REVIEW 3. Balance Sheets 3. Balance Sheets

• A = L + OE

• OE = A - L

• L = A - OE

S43 6.8 INSTRUCTIONS (10 minutes)S43 6.8 INSTRUCTIONS (10 minutes)

Re-assemble in CSGRe-assemble in CSG

Study carefully the lecture on the caseStudy carefully the lecture on the case

Record key learning points in your notebookRecord key learning points in your notebook

Discuss outstanding questionsDiscuss outstanding questions

When the bell rings it is time for lunchWhen the bell rings it is time for lunch

S44 ASSIGNMENT 7.0 - PROGRAM S44 ASSIGNMENT 7.0 - PROGRAM LEARNING LEARNING

(75 minutes) (75 minutes) 7.1 INSTRUCTIONS7.1 INSTRUCTIONS

Reassemble in new SG. Do ASS Ch. 3 in writingReassemble in new SG. Do ASS Ch. 3 in writing

Review the glossary for any difficulties with new Review the glossary for any difficulties with new wordswords

Record significant points in your notebookRecord significant points in your notebook

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

S45 ASSIGNMENT 8.0 - LECTURE ON S45 ASSIGNMENT 8.0 - LECTURE ON BALANCE SHEETSBALANCE SHEETS

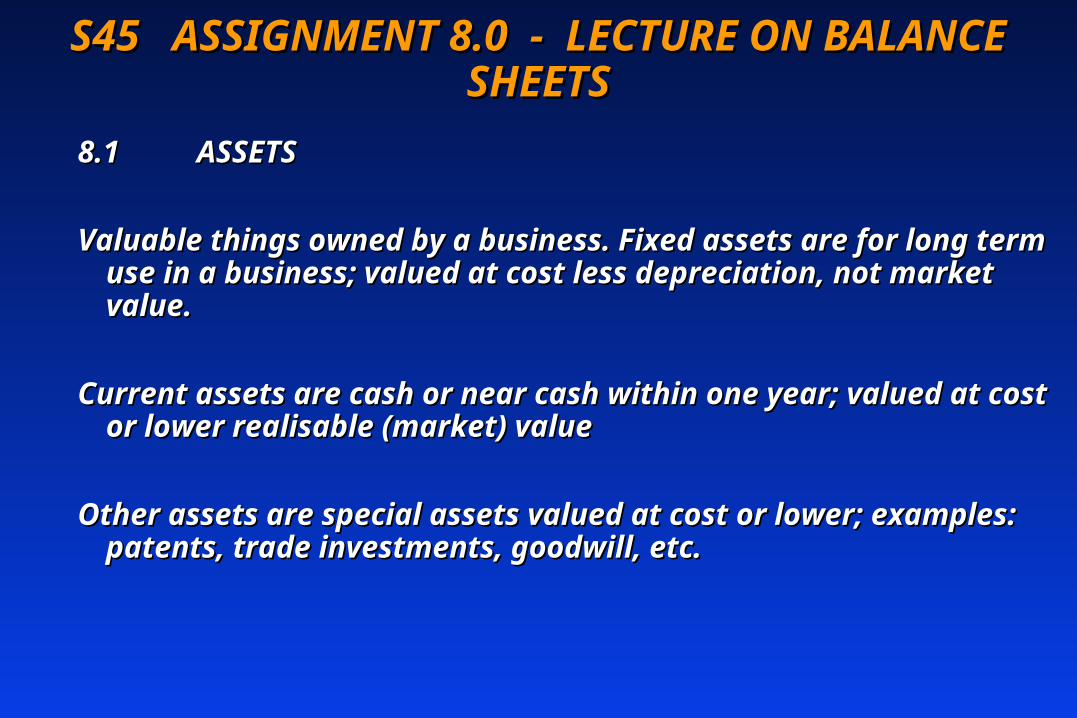

8.18.1 ASSETSASSETS

Valuable things owned by a business. Fixed assets are Valuable things owned by a business. Fixed assets are for long term use in a business; valued at cost less for long term use in a business; valued at cost less depreciation, not market value. depreciation, not market value.

Current assets are cash or near cash within one year; Current assets are cash or near cash within one year; valued at cost or lower realisable (market) valuevalued at cost or lower realisable (market) value

Other assets are special assets valued at cost or lower; Other assets are special assets valued at cost or lower; examples: patents, trade investments, goodwill, etc.examples: patents, trade investments, goodwill, etc.

S46 8.2 LIABILITIESS46 8.2 LIABILITIES

Amounts due to be paid by the business to someone else.Amounts due to be paid by the business to someone else.

Accounts payable (creditors) are liabilities.Accounts payable (creditors) are liabilities.

Current liabilities are due for payment within one year.Current liabilities are due for payment within one year.

Long term liabilities are due for payment in more than one Long term liabilities are due for payment in more than one year.year.

Bank loans and overdrafts. Liabilities are normally unsecured Bank loans and overdrafts. Liabilities are normally unsecured but may have special security on particular assets.but may have special security on particular assets.

S47 8.3 OWNERS' EQUITYS47 8.3 OWNERS' EQUITY

Assets are financed by either liabilities or owners' equity.Assets are financed by either liabilities or owners' equity.

Owners' equity is the capital issued to shareholders Owners' equity is the capital issued to shareholders (stockholders), in exchange for cash, plus reserves (stockholders), in exchange for cash, plus reserves accumulated in the business.accumulated in the business.

Reserves include capital reserves (share premium) or revenue Reserves include capital reserves (share premium) or revenue reserves (retained earnings) or accumulated profits.reserves (retained earnings) or accumulated profits.

Assets less liabilities = owners' equityAssets less liabilities = owners' equity

Assets = liabilities plus owners' equityAssets = liabilities plus owners' equity

Assets less owners' equity = liabilitiesAssets less owners' equity = liabilities

S48 8.4 RATIOSS48 8.4 RATIOS

Ratios are like a thermometer which takes the actual Ratios are like a thermometer which takes the actual temperature of a business in relation to some standard scale.temperature of a business in relation to some standard scale.

Good Average PoorGood Average Poor

(a) Liquidity(a) Liquidity

CA : CLCA : CL 2:1 1:1 2:1 1:1 1:2 1:2

QA : QLQA : QL 1.5:1 1.5:1 1:1 1:1 1:2 1:2

E : DE : D 2:1 2:1 1:1 1:1 1:2 1:2

(b) Profitability(b) Profitability

GP/S UpGP/S Up Same Down Same Down

NP/S UpNP/S Up Same Down Same Down

NP/OE p.a UpNP/OE p.a Up Same Down Same Down

S49 8.5 LEARNING PATTERNS - REVIEW S49 8.5 LEARNING PATTERNS - REVIEW 1. Asset Structure1. Asset Structure

FA FA FA

CA CA CA

OA OA OA

S50 8.5 LEARNING PATTERNS - REVIEW S50 8.5 LEARNING PATTERNS - REVIEW 2. Receivables & Payables2. Receivables & Payables

R - receives the cash ,...

P - pays the cash ...

S51 8.5 LEARNING PATTERNS - REVIEW S51 8.5 LEARNING PATTERNS - REVIEW 3. Funding Structure3. Funding Structure

CL CL CL

LTL LTL LTL

TL TL TL

OE OE OE

S52 8.6 INSTRUCTIONS (10 minutes)S52 8.6 INSTRUCTIONS (10 minutes)

Reassemble in SGReassemble in SG

Study the lecture carefullyStudy the lecture carefully

Discuss outstanding questionsDiscuss outstanding questions

Record key points in your notebookRecord key points in your notebook

When the bell rings, carry on with the case study When the bell rings, carry on with the case study which followswhich follows

S53 ASSIGNMENT 10.0 - LECTURE ON CAPE S53 ASSIGNMENT 10.0 - LECTURE ON CAPE ELECTRONICS COMPANY ELECTRONICS COMPANY

10.110.1 STORY OF THE CASESTORY OF THE CASE

Two engineers had an idea for a new product and while Two engineers had an idea for a new product and while fully employed elsewhere, they produced and sold a few fully employed elsewhere, they produced and sold a few units to their employers. They advertised and sold a few units to their employers. They advertised and sold a few more units.more units.

They worked part-time in a garage and made a profit (if we They worked part-time in a garage and made a profit (if we ignore: labor, equipment, depreciation of patents, ignore: labor, equipment, depreciation of patents, overhead, etc.). overhead, etc.).

Should they now work in this new business full-time?Should they now work in this new business full-time?

S54 10.2 RATIOS - COMPARED WITH A S54 10.2 RATIOS - COMPARED WITH A GOOD STANDARDGOOD STANDARD

Actual GoodActual Good

(a) Liquidity: Ratio Standard(a) Liquidity: Ratio Standard

QA : QLQA : QL 10,380 : 9,87010,380 : 9,870 1 : 1 1 1/2 : 1 1 : 1 1 1/2 : 1

CA : CL 45,880 : 9,870 5 : 1 2 : 1CA : CL 45,880 : 9,870 5 : 1 2 : 1

E : D 64,800 : 59,870E : D 64,800 : 59,870 1 : 1 2 : 1 1 : 1 2 : 1

(b) Activity:(b) Activity:

Sales/Assets p.a.Sales/Assets p.a.

93,750 /124,670 (twice) 1+ 1+ 93,750 /124,670 (twice) 1+ 1+

Cost of G. S./InventoryCost of G. S./Inventory

48,620/ 35,490 (twice) 2+ 2+ 48,620/ 35,490 (twice) 2+ 2+

S55 10.2 RATIOS - COMPARED WITH A S55 10.2 RATIOS - COMPARED WITH A GOOD STANDARD (continued)GOOD STANDARD (continued)

(c) Profitability: Actual Standard (c) Profitability: Actual Standard

Gross Profit/Sales X 100%Gross Profit/Sales X 100%

45,120/93,75045,120/93,750 48% 30% 48% 30%

Net Profit/Sales X 100%Net Profit/Sales X 100%

24,800/93,75024,800/93,750 27% 5% 27% 5%

Net Profit /Owners Equity (p.a.)Net Profit /Owners Equity (p.a.)

24,800 /64,800 X 100% (twice) 76% 25%24,800 /64,800 X 100% (twice) 76% 25%

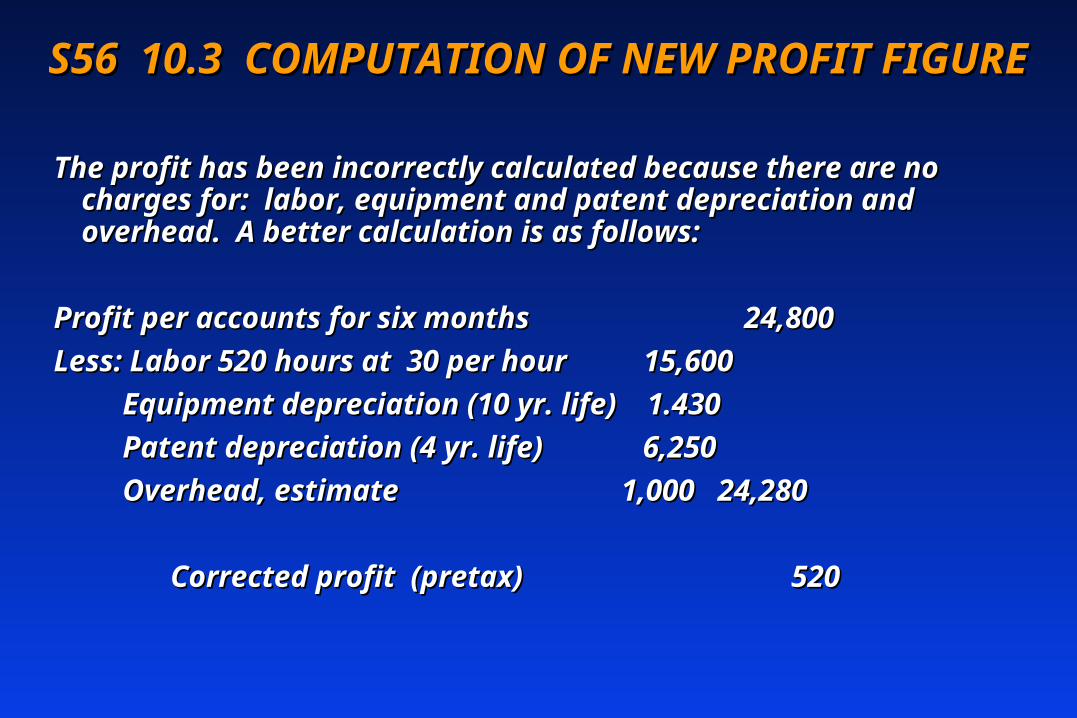

S56 10.3 COMPUTATION OF NEW PROFIT S56 10.3 COMPUTATION OF NEW PROFIT FIGUREFIGURE

The profit has been incorrectly calculated because there The profit has been incorrectly calculated because there are no charges for: labor, equipment and patent are no charges for: labor, equipment and patent depreciation and overhead. A better calculation is as depreciation and overhead. A better calculation is as follows: follows:

Profit per accounts for six months 24,800Profit per accounts for six months 24,800

Less: Labor 520 hours at 30 per hour 15,600Less: Labor 520 hours at 30 per hour 15,600

Equipment depreciation (10 yr. life) 1.430Equipment depreciation (10 yr. life) 1.430

Patent depreciation (4 yr. life) 6,250Patent depreciation (4 yr. life) 6,250

Overhead, estimate 1,000 24,280Overhead, estimate 1,000 24,280

Corrected profit (pretax) 520 Corrected profit (pretax) 520

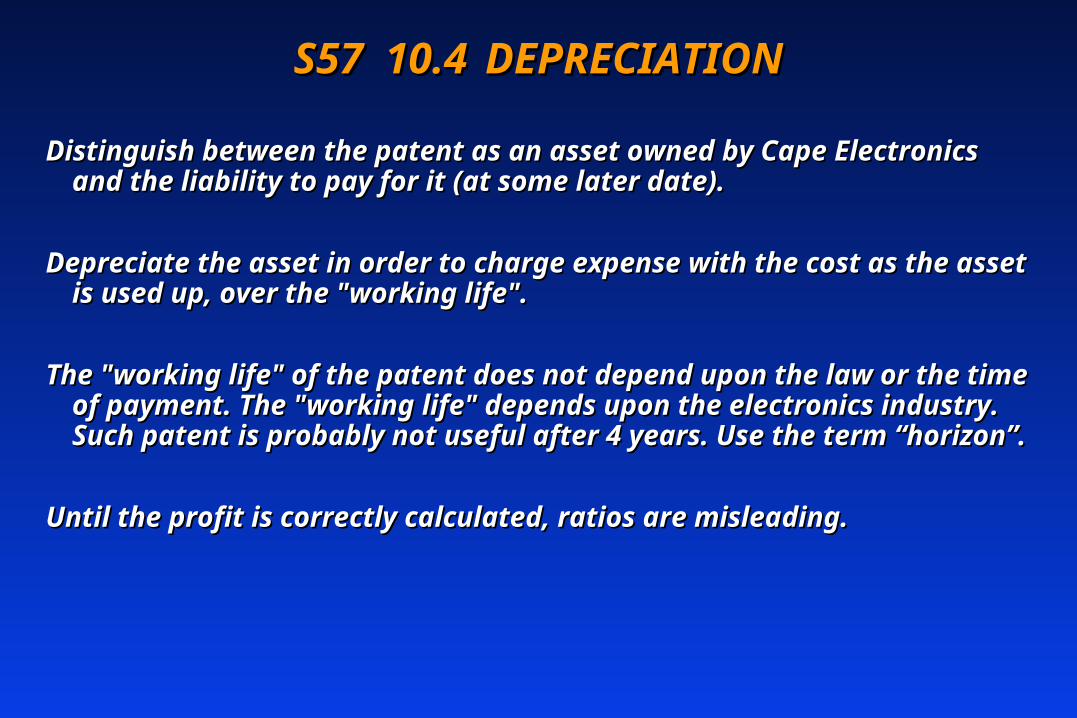

S57 10.4S57 10.4 DEPRECIATIONDEPRECIATION

Distinguish between the patent as an asset owned by Cape Distinguish between the patent as an asset owned by Cape Electronics and the liability to pay for it (at some later date). Electronics and the liability to pay for it (at some later date).

Depreciate the asset in order to charge expense with the cost Depreciate the asset in order to charge expense with the cost as the asset is used up, over the "working life".as the asset is used up, over the "working life".

The "working life" of the patent does not depend upon the law The "working life" of the patent does not depend upon the law or the time of payment. The "working life" depends upon the or the time of payment. The "working life" depends upon the electronics industry. Such patent is probably not useful electronics industry. Such patent is probably not useful after 4 years. Use the term “horizon”.after 4 years. Use the term “horizon”.

Until the profit is correctly calculated, ratios are misleading.Until the profit is correctly calculated, ratios are misleading.

S58 10.5 COMMENTS ON THE HEALTH OF S58 10.5 COMMENTS ON THE HEALTH OF THE COMPANYTHE COMPANY

Liquidity - the current ratio is reasonable, but the quick Liquidity - the current ratio is reasonable, but the quick ratio indicates a shortage of cash to pay creditors ratio indicates a shortage of cash to pay creditors

Activity - fairly active, but the advertising of 14,630 has Activity - fairly active, but the advertising of 14,630 has only produced 5 more sales.only produced 5 more sales.

Profitability - the profit is nil after adjustment, except as a Profitability - the profit is nil after adjustment, except as a part-time hobby.part-time hobby.

Potential - product limited; market limited; physical Potential - product limited; market limited; physical facilities in a garage are not adequate for full scale facilities in a garage are not adequate for full scale production; management may not be adequate.production; management may not be adequate.

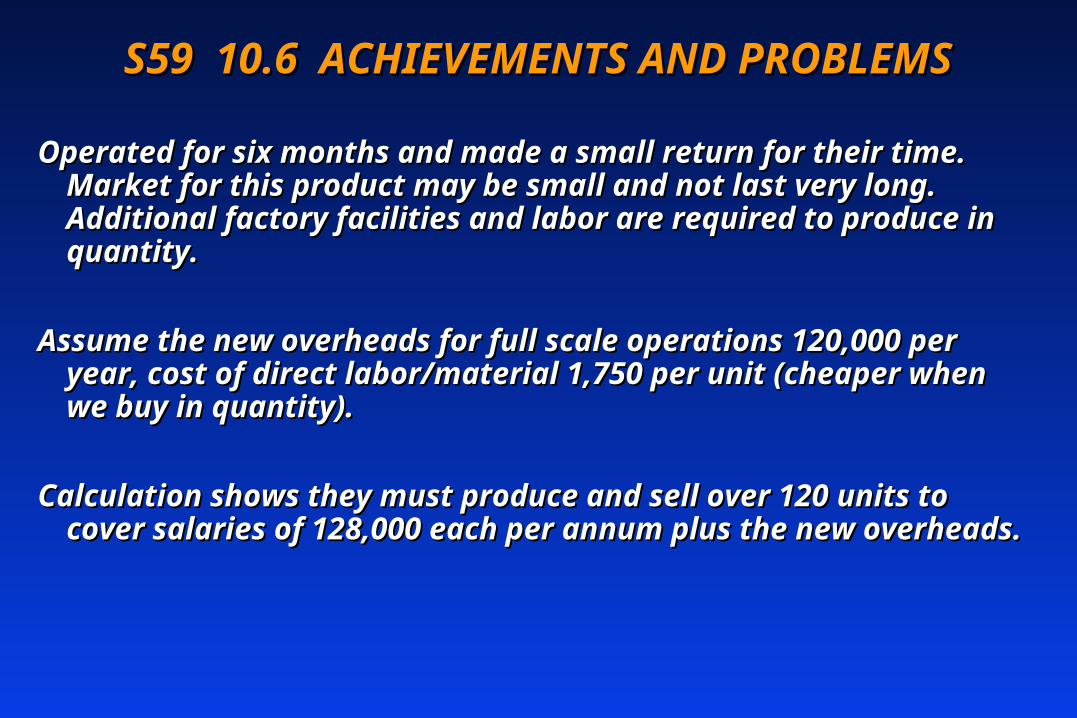

S59 10.6 ACHIEVEMENTS AND PROBLEMSS59 10.6 ACHIEVEMENTS AND PROBLEMS

Operated for six months and made a small return for Operated for six months and made a small return for their time. Market for this product may be small and their time. Market for this product may be small and not last very long. Additional factory facilities and not last very long. Additional factory facilities and labor are required to produce in quantity.labor are required to produce in quantity.

Assume the new overheads for full scale operations Assume the new overheads for full scale operations 120,000 per year, cost of direct labor/material 1,750 120,000 per year, cost of direct labor/material 1,750 per unit (cheaper when we buy in quantity).per unit (cheaper when we buy in quantity).

Calculation shows they must produce and sell over 120 Calculation shows they must produce and sell over 120 units to cover salaries of 128,000 each per annum plus units to cover salaries of 128,000 each per annum plus the new overheads.the new overheads.

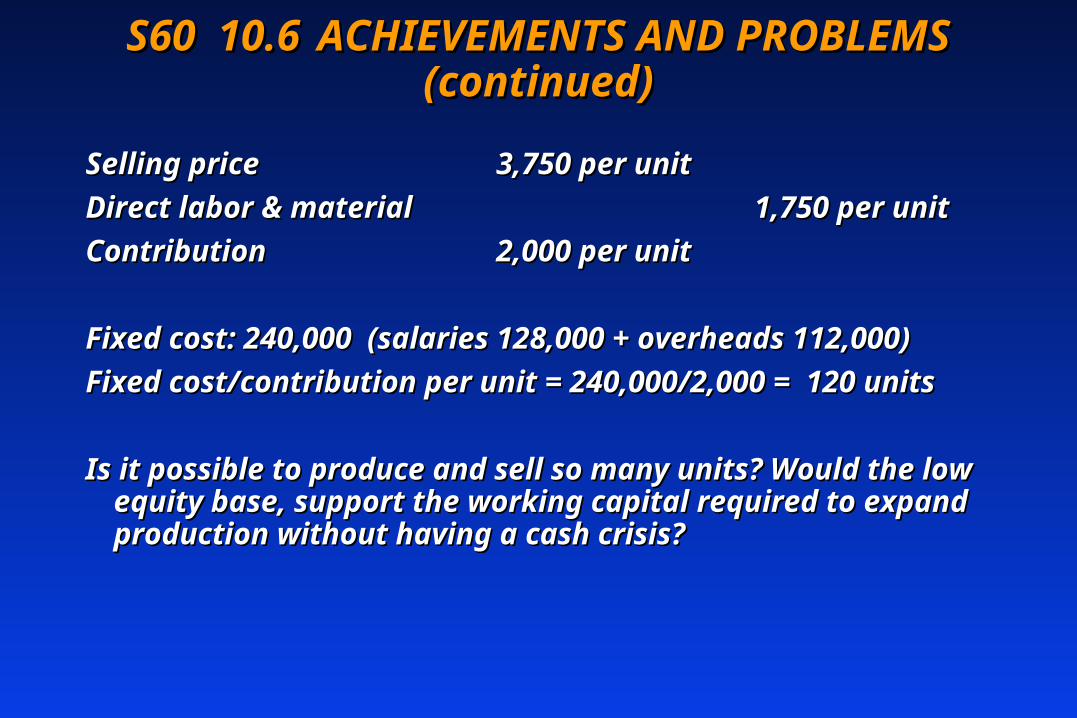

S60 10.6S60 10.6 ACHIEVEMENTS AND ACHIEVEMENTS AND PROBLEMS (continued)PROBLEMS (continued)

Selling price Selling price 3,750 per unit 3,750 per unit

Direct labor & materialDirect labor & material 1,750 per unit 1,750 per unit

Contribution Contribution 2,000 per unit 2,000 per unit

Fixed cost: 240,000 (salaries 128,000 + overheads 112,000)Fixed cost: 240,000 (salaries 128,000 + overheads 112,000)

Fixed cost/contribution per unit = 240,000/2,000 = 120 unitsFixed cost/contribution per unit = 240,000/2,000 = 120 units

Is it possible to produce and sell so many units? Would the Is it possible to produce and sell so many units? Would the low equity base, support the working capital required to low equity base, support the working capital required to expand production without having a cash crisis?expand production without having a cash crisis?

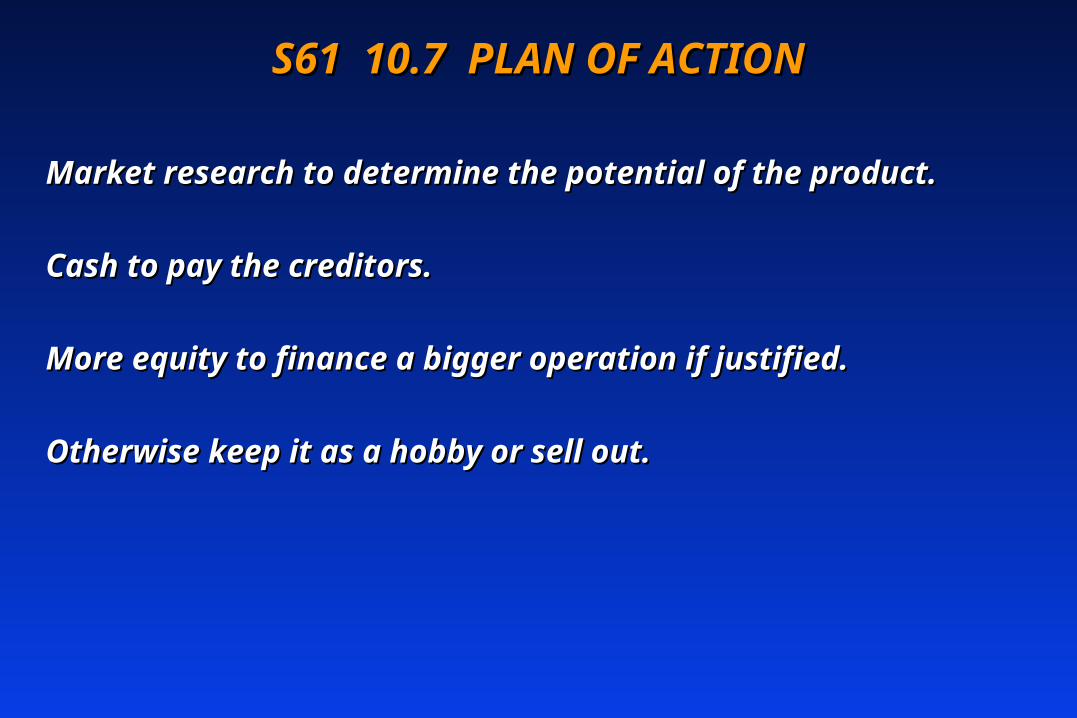

S61 10.7 PLAN OF ACTIONS61 10.7 PLAN OF ACTION

Market research to determine the potential of the Market research to determine the potential of the product.product.

Cash to pay the creditors.Cash to pay the creditors.

More equity to finance a bigger operation if justified.More equity to finance a bigger operation if justified.

Otherwise keep it as a hobby or sell out.Otherwise keep it as a hobby or sell out.

S62 10.8S62 10.8 LEARNING POINTSLEARNING POINTS

a) Accounting depends upon assumptions; figures are a) Accounting depends upon assumptions; figures are only estimates.only estimates.

b) Income Statement is not valid unless all costs have b) Income Statement is not valid unless all costs have been charged including: labor, depreciation, been charged including: labor, depreciation, overhead, etc.overhead, etc.

c) Depreciation is based on the working life (“horizon”) c) Depreciation is based on the working life (“horizon”) of a fixed asset, not the time of payment. of a fixed asset, not the time of payment. Depreciation of a patent is difficult because the Depreciation of a patent is difficult because the working life is uncertain. Four years seems working life is uncertain. Four years seems reasonable.reasonable.

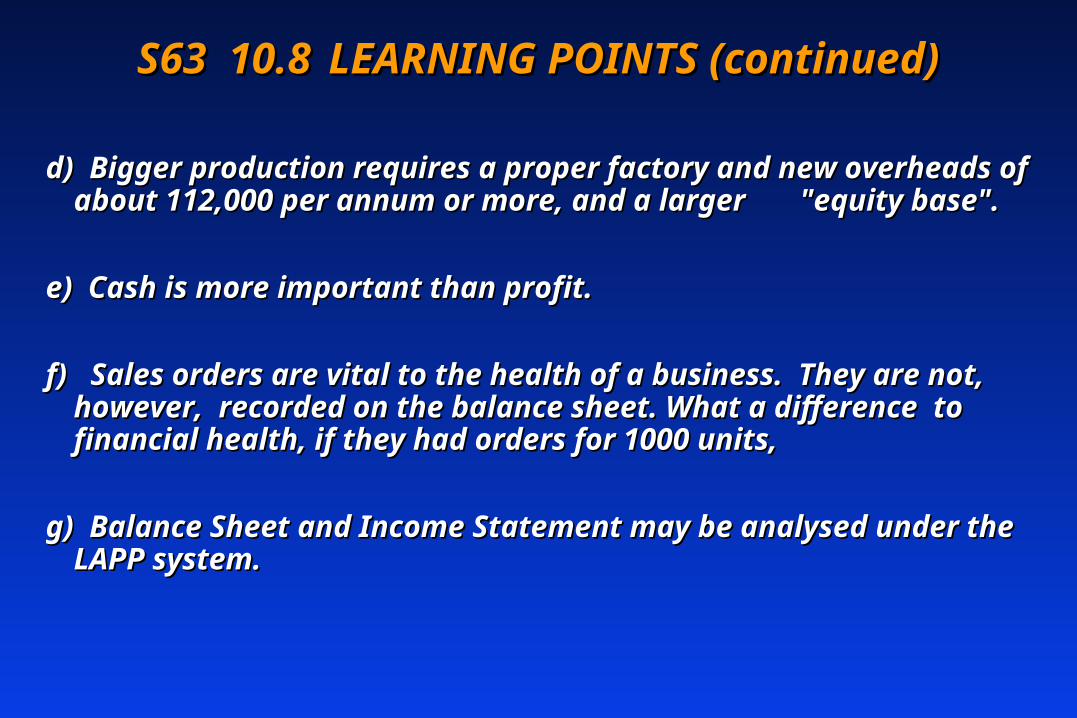

S63 10.8S63 10.8 LEARNING POINTS (continued)LEARNING POINTS (continued)

d) Bigger production requires a proper factory and new d) Bigger production requires a proper factory and new overheads of about 112,000 per annum or more, and a larger overheads of about 112,000 per annum or more, and a larger "equity base". "equity base".

e) Cash is more important than profit.e) Cash is more important than profit.

f) Sales orders are vital to the health of a business. They are f) Sales orders are vital to the health of a business. They are not, however, recorded on the balance sheet. What a not, however, recorded on the balance sheet. What a difference to financial health, if they had orders for 1000 difference to financial health, if they had orders for 1000 units,units,

g) Balance Sheet and Income Statement may be analysed g) Balance Sheet and Income Statement may be analysed under the LAPP system.under the LAPP system.

S64 10.8S64 10.8 LEARNING POINTS (continued)LEARNING POINTS (continued)

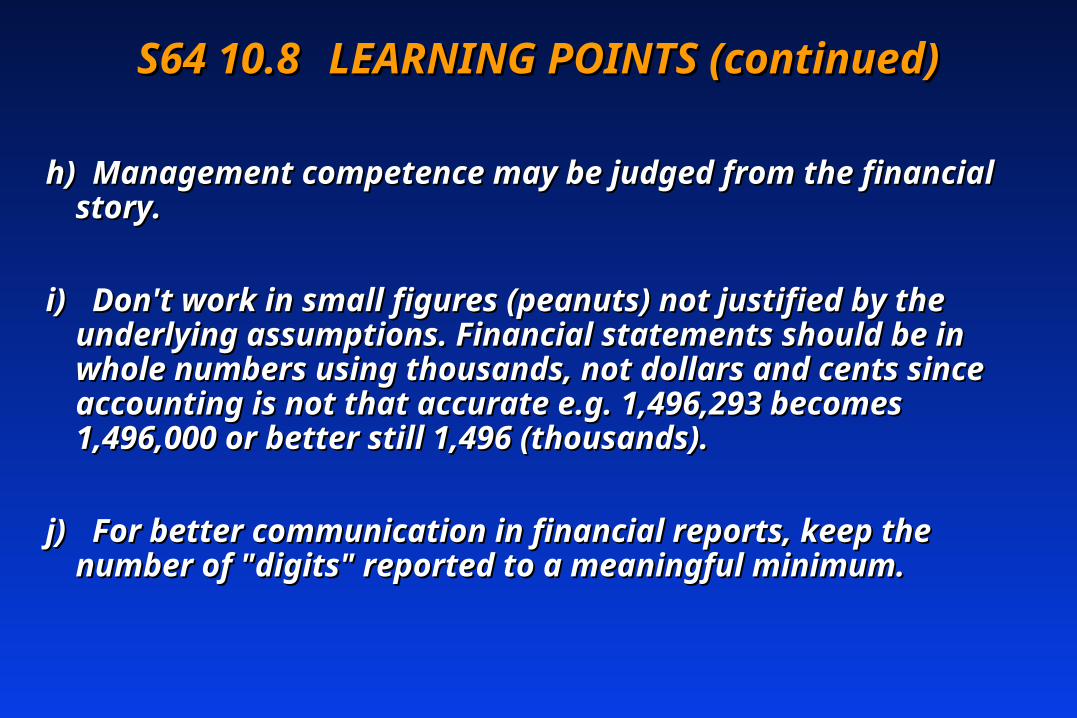

h) Management competence may be judged from the h) Management competence may be judged from the financial story.financial story.

i)i) Don't work in small figures (peanuts) not justified by Don't work in small figures (peanuts) not justified by the underlying assumptions. Financial statements the underlying assumptions. Financial statements should be in whole numbers using thousands, not should be in whole numbers using thousands, not dollars and cents since accounting is not that accurate dollars and cents since accounting is not that accurate e.g. 1,496,293 becomes 1,496,000 or better still 1,496 e.g. 1,496,293 becomes 1,496,000 or better still 1,496 (thousands).(thousands).

j)j) For better communication in financial reports, keep the For better communication in financial reports, keep the number of "digits" reported to a meaningful minimum.number of "digits" reported to a meaningful minimum.

S65 10.9S65 10.9 LEARNING PATTERNS - REVIEW LEARNING PATTERNS - REVIEW 1. Estimates1. Estimates

• Coconuts ...

• Big figures ...

S66 10.9 S66 10.9 LEARNING PATTERNS - REVIEW LEARNING PATTERNS - REVIEW 2. Horizon for Depreciation2. Horizon for Depreciation

• Legal life

• Payment life

• Technical life

• Economic life

S67 10.9 S67 10.9 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW 3. Cash is the Key 3. Cash is the Key

Cash now ...

Profit later

Profit later

Profit later ...

Profit later ...

S68 10.9 S68 10.9 LEARNING PATTERNS - REVIEWLEARNING PATTERNS - REVIEW 4. Inventory Valuation 4. Inventory Valuation

• Cost

• Realisable Market value

• Replacement Market value

• Sales orders?

S69 10.10 INSTRUCTIONS (10 minutes)S69 10.10 INSTRUCTIONS (10 minutes)

Re-assemble in CSGRe-assemble in CSG

Study carefully the lecture on the caseStudy carefully the lecture on the case

Record key learning points in your notebookRecord key learning points in your notebook

Discuss outstanding questionsDiscuss outstanding questions

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

S70 ASSIGNMENT 11.0 - SUMMARY S70 ASSIGNMENT 11.0 - SUMMARY LECTURE FOR PART 1 LECTURE FOR PART 1

11.111.1 OBJECTIVESOBJECTIVES

Understand accounting language and conceptsUnderstand accounting language and concepts

Interpret balance sheets and profit and loss accountsInterpret balance sheets and profit and loss accounts

Use basic financial ratiosUse basic financial ratios

Develop confidence in using accounting and financial dataDevelop confidence in using accounting and financial data

Motivate further study in the futureMotivate further study in the future

S71 11.2S71 11.2 ACCOUNTING LANGUAGEACCOUNTING LANGUAGE

Glossary of ASS is a continuous referenceGlossary of ASS is a continuous reference

Two hundred words (only) is the vocabularyTwo hundred words (only) is the vocabulary

USA/European accounting languages may be USA/European accounting languages may be comparedcompared

S72 11.2S72 11.2 ACCOUNTING LANGUAGE ACCOUNTING LANGUAGE (continued)(continued)

USA/European accounting languages may be compared:USA/European accounting languages may be compared:

receivablesreceivables debtors debtors

payablespayables creditors creditors

inventory stockinventory stock

capital stockcapital stock share capital share capital

capital surpluscapital surplus capital reserve capital reserve

earned surplus ) accumulated profitearned surplus ) accumulated profit

retained savings ) revenue reserveretained savings ) revenue reserve

earnings statement )earnings statement )

operating statement )operating statement ) profit and loss account profit and loss account

income statement )income statement )

Records of transactions are converted into accounting Records of transactions are converted into accounting reports by using practical accounting concepts:reports by using practical accounting concepts:

cost (assets generally at cost)cost (assets generally at cost)

consistency/conservatism/comparabilityconsistency/conservatism/comparability

accounting periodaccounting period

going concern (not break-up values)going concern (not break-up values)

entity (the business not its workers)entity (the business not its workers)

profit realisationprofit realisation

accrual (cash and credit transactions included)accrual (cash and credit transactions included)

true and fair (as possible)true and fair (as possible)

MATERIALITY (most important of all!)MATERIALITY (most important of all!)

S74 11.4S74 11.4 ACCOUNTING PERIOD ACCOUNTING PERIOD

Try to associate all sales costs, expenses and profits Try to associate all sales costs, expenses and profits with a specific accounting period.with a specific accounting period.

All accounting figures are estimates not scientific All accounting figures are estimates not scientific facts.facts.

S75 11.5S75 11.5 PROFIT AND LOSS ACCOUNTPROFIT AND LOSS ACCOUNT

Sales less cost of goods sold equals gross profit.Sales less cost of goods sold equals gross profit.

Gross profit less selling and administrative expenses Gross profit less selling and administrative expenses equals net profit for the accounting period.equals net profit for the accounting period.

Profit depends upon: charging all the proper costs Profit depends upon: charging all the proper costs and stock valuation.and stock valuation.

S76 11.6S76 11.6 BALANCE SHEETBALANCE SHEET

Assets of the business: how they are financed from liabilities Assets of the business: how they are financed from liabilities and owners equity.and owners equity.

Fixed assets valued at cost less depreciation (based on the Fixed assets valued at cost less depreciation (based on the horizon of the asset).horizon of the asset).

Fixed assets such as land and building may have to be revalued Fixed assets such as land and building may have to be revalued periodically. Accounting periods create uncertainty and doubt.periodically. Accounting periods create uncertainty and doubt.

Current assets (one year only) valued at cost or lower realisable Current assets (one year only) valued at cost or lower realisable (market) value. Inventory valued at the lower cost or market (market) value. Inventory valued at the lower cost or market value.value.

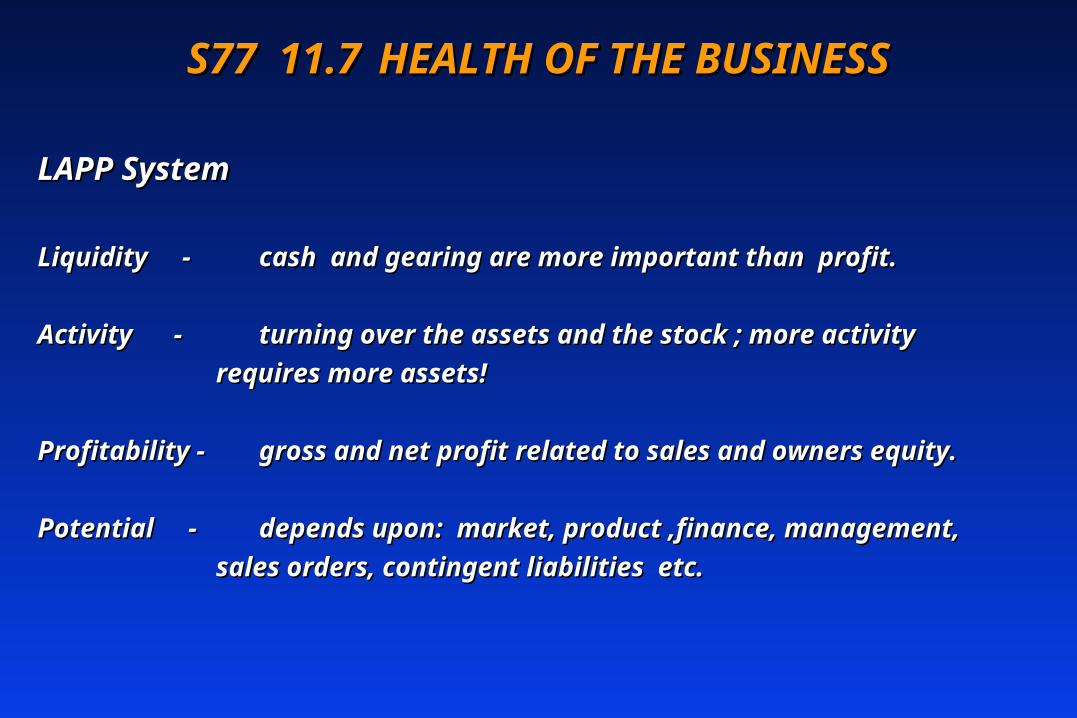

S77 11.7S77 11.7 HEALTH OF THE BUSINESSHEALTH OF THE BUSINESS

LAPP SystemLAPP System

Liquidity -Liquidity - cash and gearing are more important than profit.cash and gearing are more important than profit.

Activity -Activity - turning over the assets and the stock ; more turning over the assets and the stock ; more activity activity

requires more assets!requires more assets!

Profitability -Profitability - gross and net profit related to sales and owners gross and net profit related to sales and owners equity.equity.

Potential -Potential - depends upon: market, product ,finance, depends upon: market, product ,finance, management,management,

sales orders, contingent liabilities etc.sales orders, contingent liabilities etc.

S78 11.8S78 11.8 BASIC FINANCIAL RATIOS BASIC FINANCIAL RATIOS (continued) (continued)

Good Average PoorGood Average Poora) Liquidity:a) Liquidity:

CA : CLCA : CL 2 : 1 2 : 1 1 : 1 1 : 1 1 : 21 : 2

QA : QLQA : QL 1+: 1 1+: 1 1 : 1 1 : 1 1 : 21 : 2

E : DE : D 2 : 1 2 : 1 1 : 1 1 : 1 1 : 2 1 : 2b) Activity:b) Activity:

Sales/ AssetsSales/ Assets Up Up Same Down Same Down

CGS/Stock UpCGS/Stock Up Same Same DownDown

S79 11.8S79 11.8 BASIC FINANCIAL RATIOS BASIC FINANCIAL RATIOS (continued)(continued)

Good Average Good Average PoorPoor

c) Profitability:c) Profitability:

Gross Profit/SalesGross Profit/Sales UUpp Same DownSame Down

Net Profit/Sales UpNet Profit/Sales Up Same DownSame Down

Net Profit/Owners Equity UpNet Profit/Owners Equity Up Same DownSame Down

S80 11.9S80 11.9 MATERIALITYMATERIALITY

Look for the big figures which are significant.Look for the big figures which are significant.

Compare them with the past, the future and Compare them with the past, the future and the industry averages to determine the the industry averages to determine the significance of changes. significance of changes.

Look for "CHANGE" and ask the reasons why.Look for "CHANGE" and ask the reasons why.

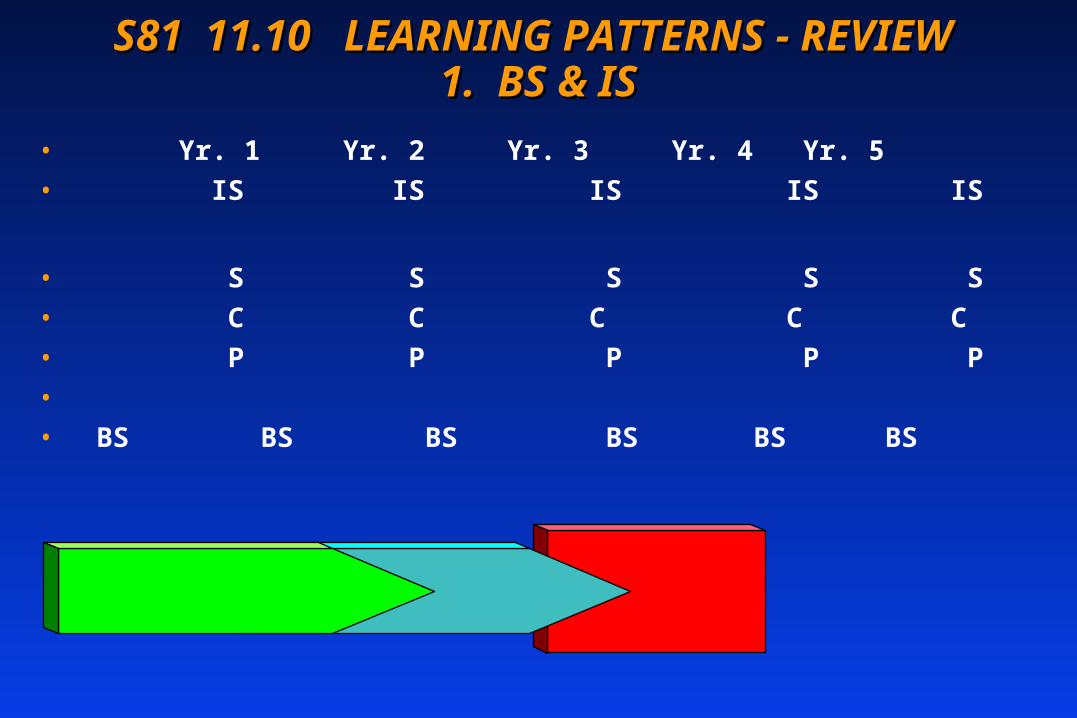

S81 11.10 LEARNING PATTERNS - REVIEW S81 11.10 LEARNING PATTERNS - REVIEW

1. BS & IS1. BS & IS• Yr. 1 Yr. 2 Yr. 3 Yr. 4 Yr. 5

• IS IS IS IS IS

• S S S S S

• C C C C C

• P P P P P

•

• BS BS BS BS BS BS

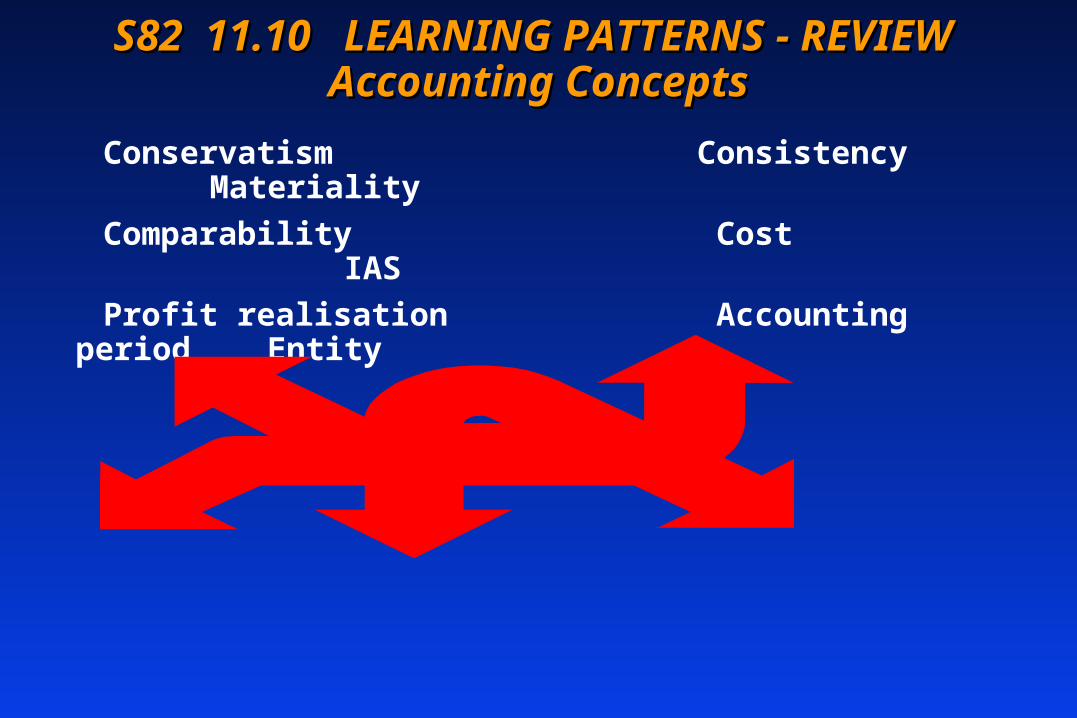

S82 11.10 LEARNING PATTERNS - REVIEW S82 11.10 LEARNING PATTERNS - REVIEW Accounting Concepts Accounting Concepts

Conservatism Consistency Materiality

Comparability Cost IAS

Profit realisation Accounting period Entity

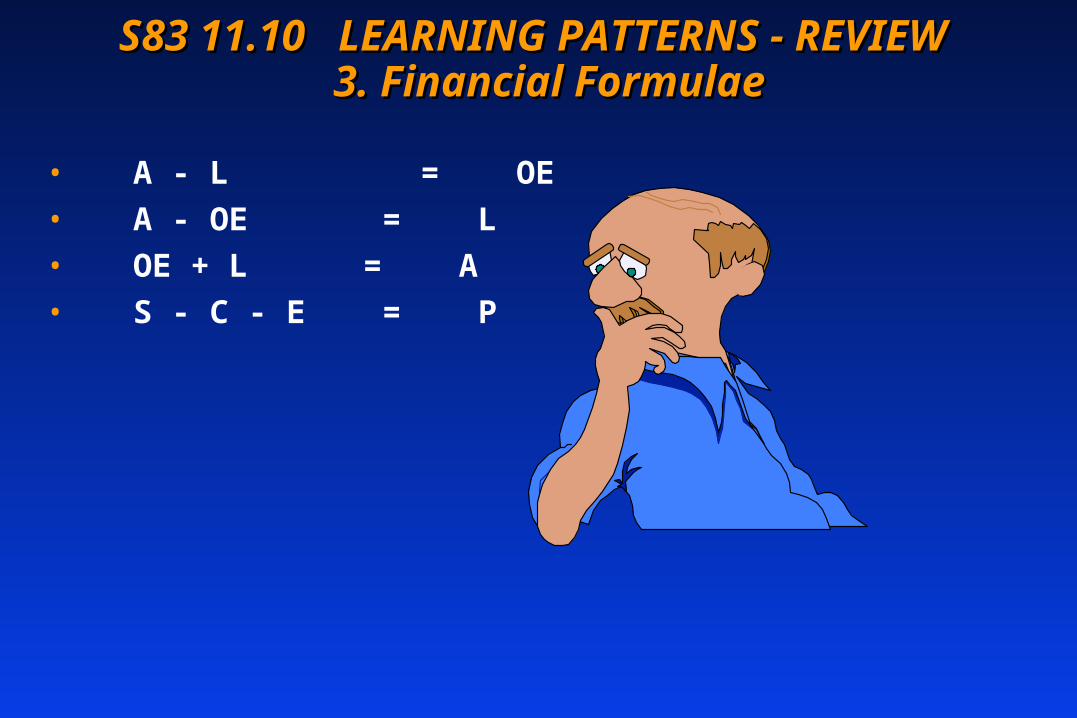

S83 11.10 LEARNING PATTERNS - REVIEW S83 11.10 LEARNING PATTERNS - REVIEW 3. Financial Formulae 3. Financial Formulae

• A - L = OE

• A - OE = L

• OE + L = A

• S - C - E = P

S84 11.10 LEARNING PATTERNS - REVIEW S84 11.10 LEARNING PATTERNS - REVIEW

4. More Financial Formulae 4. More Financial Formulae• CA:CL

• QA: QL

• E: D

• S/A

• CGS/I

• GP/S

• NP/S

• NP/OE

S85 11.10 LEARNING PATTERNS - REVIEW S85 11.10 LEARNING PATTERNS - REVIEW 4. Materiality 4. Materiality

• Peanuts ...................................................... and coconuts ...

S86 11.11 INSTRUCTIONS (20 minutes)S86 11.11 INSTRUCTIONS (20 minutes)

Reassemble in SGReassemble in SG

Review the Summary Lecture for Part I in the Review the Summary Lecture for Part I in the course diary and discuss questions arisingcourse diary and discuss questions arising

To get the best out of Part II of the program, To get the best out of Part II of the program, try to complete ALL of the following ... try to complete ALL of the following ... homework tonight ...homework tonight ...

S87 11.11 INSTRUCTIONS (continued) ... S87 11.11 INSTRUCTIONS (continued) ... very useful ... homework ... tonight ...very useful ... homework ... tonight ...

Read the articles on the accounting Read the articles on the accounting

In the ASS text, review the chapter summaries and the In the ASS text, review the chapter summaries and the glossaryglossary

Do the optional exercises in the course diary and check the Do the optional exercises in the course diary and check the answersanswers

Review the summary lecture for Part I in the course diaryReview the summary lecture for Part I in the course diary

Review your notes for Part I of the course and list Review your notes for Part I of the course and list outstanding questions to be resolved in Part IIoutstanding questions to be resolved in Part II

S88 11.11 INSTRUCTIONS (continued) S88 11.11 INSTRUCTIONS (continued) Final Note for Part I ... Final Note for Part I ...

Thank you for working so hard today ....

Tomorrow .... it’s downhill all the way ....

S101 AUTOMATED GROUP LEARNING S101 AUTOMATED GROUP LEARNING (AGL)(AGL)

AGL NO. 1 - AGL NO. 1 -

FINANCE FOR NON-FINANCIAL MANAGERSFINANCE FOR NON-FINANCIAL MANAGERS

DAILY WORK PACK - PART IIDAILY WORK PACK - PART II

Copyright: RGAB/IR 2010/2Copyright: RGAB/IR 2010/2

S102S102 ABBREVIATIONS ABBREVIATIONS

IND - IND - INDIVIDUALINDIVIDUAL

SG -SG - S MALL GROUPS MALL GROUP

CSG - CSG - COMBINED SMALL GROUPCOMBINED SMALL GROUP

MG MG - - MAIN GROUPMAIN GROUP

ASS - ASS - ACCOUNTING STEP BY STEP ACCOUNTING STEP BY STEP

PL - PL - PROGRAM LEARNINGPROGRAM LEARNING

L - L - LECTURELECTURE

D D - - DISCUSSIONDISCUSSION

LRTLRT - - LEARNING RECALL TAPELEARNING RECALL TAPE

CAICAI - - COMPUTER ASSISTED INSTRUCTIONCOMPUTER ASSISTED INSTRUCTION

S103S103 ASSIGNMENT 1.0 REVIEW AND ASSIGNMENT 1.0 REVIEW AND SHORT QUIZ (45 minutes)SHORT QUIZ (45 minutes)

1.11.1 INSTRUCTIONSINSTRUCTIONS

Assemble in new SG. Discuss outstanding questions from Part Assemble in new SG. Discuss outstanding questions from Part II

Do the short quiz which follows. Work on each question Do the short quiz which follows. Work on each question individually and then compare answers in SGindividually and then compare answers in SG

When all answers have been completed, check with the When all answers have been completed, check with the correct solution and discuss points arisingcorrect solution and discuss points arising

Reassemble in MG when the bell rings Reassemble in MG when the bell rings

S104S104 ASSIGNMENT 2.0 PROGRAM ASSIGNMENT 2.0 PROGRAM LEARNING LEARNING

(75 minutes)(75 minutes)2.12.1 INSTRUCTIONSINSTRUCTIONS

Reassemble in SG. Review the summaries of Reassemble in SG. Review the summaries of ASS Ch. 1, 2, and 3ASS Ch. 1, 2, and 3

Do Ch. 4 in writingDo Ch. 4 in writing

Record key points in your notebookRecord key points in your notebook

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

S105 ASSIGNMENT 3.0 - LECTURE - S105 ASSIGNMENT 3.0 - LECTURE - INCOME STATEMENTS (30 minutesINCOME STATEMENTS (30 minutes

3.1 ACCOUNTING PERIOD CONCEPT3.1 ACCOUNTING PERIOD CONCEPT

Income statement (profit and loss account, earnings Income statement (profit and loss account, earnings statement for the accounting period.statement for the accounting period.

Balance sheet at the start and end of the accounting Balance sheet at the start and end of the accounting period. Normally one year.period. Normally one year.

3.2 ACCRUAL CONCEPT3.2 ACCRUAL CONCEPT

Sales, cost and expenses may be for cash or credit. Sales, cost and expenses may be for cash or credit. Income statement includes both cash and credit Income statement includes both cash and credit transactions. transactions.

S106 3.3 INCOME STATEMENTS AND S106 3.3 INCOME STATEMENTS AND BALANCE SHEETSBALANCE SHEETS

Income statement shows Income statement shows howhow the profit was made.the profit was made.

Balance sheet shows assets and Balance sheet shows assets and howhow they are financed. they are financed.

S107 3.4 SALES AND GROSS PROFITS107 3.4 SALES AND GROSS PROFIT

A measure of activity is: Sales/assetsA measure of activity is: Sales/assets

Cost of goods sold means cost of sales.Cost of goods sold means cost of sales.

"Trading Account" is part of income statement which "Trading Account" is part of income statement which indicates: sales less cost of sales = gross profit.indicates: sales less cost of sales = gross profit.

Cost of sales for a trading company (buying and Cost of sales for a trading company (buying and selling finished goods) is: opening inventory plus selling finished goods) is: opening inventory plus purchases of finished goods less closing inventory.purchases of finished goods less closing inventory.

S108 3.4 SALES AND GROSS PROFIT S108 3.4 SALES AND GROSS PROFIT (continued)(continued)

Cost of sales for a manufacturing company is Cost of sales for a manufacturing company is different because it does not purchase different because it does not purchase finished goods. finished goods.

Finished goods are manufactured from factory Finished goods are manufactured from factory labor, raw materials and manufacturing labor, raw materials and manufacturing overhead.overhead.

Manufacturing cost of finished goods must be Manufacturing cost of finished goods must be adjusted for work in process changes.adjusted for work in process changes.

S109 3.4 SALES AND GROSS PROFIT S109 3.4 SALES AND GROSS PROFIT (continued)(continued)

For a manufacturer, therefore: factory labor + factory For a manufacturer, therefore: factory labor + factory materials used + factory overhead ... plus or minus ... materials used + factory overhead ... plus or minus ... work in process changes = ... cost of finished goods work in process changes = ... cost of finished goods manufactured for the period.manufactured for the period.

This is the same as the "purchase of finished goods" by a This is the same as the "purchase of finished goods" by a trading company.trading company.

Work in process is inventory unfinished. As the amount at Work in process is inventory unfinished. As the amount at the beginning and end of the accounting period changes, the beginning and end of the accounting period changes, this difference must be added or deducted to this difference must be added or deducted to manufacturing cost incurred, in order to compute cost of manufacturing cost incurred, in order to compute cost of finished goods manufactured.finished goods manufactured.

S110 3.5 NET PROFITS110 3.5 NET PROFIT

Net income, net earnings, net profit.Net income, net earnings, net profit.

Expenses divided into:Expenses divided into:

(a) normal operating expenses, and(a) normal operating expenses, and

(b) special non-operating expenses(b) special non-operating expenses

Operating expenses (including selling, general and Operating expenses (including selling, general and administrative) are normal costs not connected administrative) are normal costs not connected with manufacturing.with manufacturing.

S111 3.5 NET PROFIT (continued)S111 3.5 NET PROFIT (continued)

Non-operating expenses are abnormal costs not connected Non-operating expenses are abnormal costs not connected with normal operations (e.g., loss of sales of assets, with normal operations (e.g., loss of sales of assets, interest paid).interest paid).

There may be non-operating income too! (e.g., profit on There may be non-operating income too! (e.g., profit on sales of assets, dividends received, etc.)sales of assets, dividends received, etc.)

Gross profit less operating expneses = operating profit.Gross profit less operating expneses = operating profit.

Operating profit less non-operating expenses = profit Operating profit less non-operating expenses = profit before taxes. before taxes.

Profit before taxes less income tax = net profit.Profit before taxes less income tax = net profit.

S112 3.6 RATIOSS112 3.6 RATIOS

Profitability:Profitability:

Gross Profit/Sales Gross Profit/Sales x 100% x 100%

Net Profit/SalesNet Profit/Sales x 100% x 100%

Net Profit/Owners Equity x 100% (p.a.)Net Profit/Owners Equity x 100% (p.a.)

S113 3.6 RATIOS (continued)S113 3.6 RATIOS (continued)

Activity:Activity:

Sales /Assets = measure of "turnover" of Sales /Assets = measure of "turnover" of assets (p.a.)assets (p.a.)

Cost of Goods Sold/Inventory = measure of Cost of Goods Sold/Inventory = measure of "turnover" of inventory (p.a.)"turnover" of inventory (p.a.)

S114 3.7 ACCUMULATED PROFITS114 3.7 ACCUMULATED PROFIT

Retained earnings, revenue reserves.Retained earnings, revenue reserves.

Part of the Reserves in the Owners Equity part of the Part of the Reserves in the Owners Equity part of the Balance Sheet. Appropriation Account or Statement of Balance Sheet. Appropriation Account or Statement of Retained Earnings.Retained Earnings.

Balance brought forward + net profit less dividends = Balance brought forward + net profit less dividends = balance carried forward. Profit increases owners equity.balance carried forward. Profit increases owners equity.

Reserves increase the equity of the business but not Reserves increase the equity of the business but not necessarily the cash; cash may have been used to buy necessarily the cash; cash may have been used to buy more assets or pay creditors.more assets or pay creditors.

S115 3.8 LEARNING PATTERNS - REVIEWS115 3.8 LEARNING PATTERNS - REVIEW 1. Credit Transactions 1. Credit Transactions

• Buy now A + L+

• Pay later A - L -

S116 3.8 LEARNING PATTERNS - REVIEW S116 3.8 LEARNING PATTERNS - REVIEW 2. Cost of Goods Sold - Trading2. Cost of Goods Sold - Trading

• Inventory + Purchases - Closing Inventory =

• Cost of goods sold

S117 3.8 LEARNING PATTERNS - REVIEWS117 3.8 LEARNING PATTERNS - REVIEW 3. Cost of Goods Sold - Manufacturing 3. Cost of Goods Sold - Manufacturing

• RM + Labour + Manufacturing Overhead

• - Work in Process Changes =

• Cost of Finished Goods "purchased" from the factory

S118 3.8 LEARNING PATTERNS - REVIEW S118 3.8 LEARNING PATTERNS - REVIEW 4. Charges 4. Charges

Type - material, labour, overhead

Function - production, sales, administration

S119 3.9 INSTRUCTIONS (10 minutes)S119 3.9 INSTRUCTIONS (10 minutes)

Reassemble in SGReassemble in SG

Study the lecture carefully and record key Study the lecture carefully and record key points in your note bookpoints in your note book

Discuss outstanding questionsDiscuss outstanding questions

When the bell rings continue with the case When the bell rings continue with the case study which followsstudy which follows

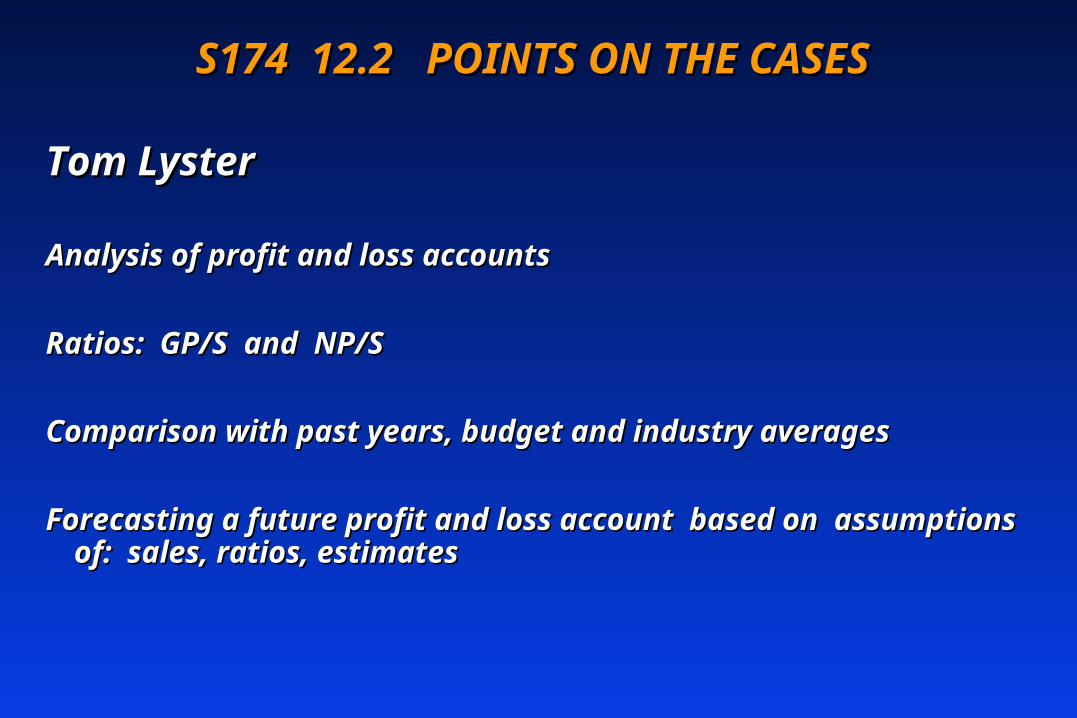

S120 ASSIGNMENT 5.0 - LECTURE ON TOM S120 ASSIGNMENT 5.0 - LECTURE ON TOM LYSTER (30 minutes)LYSTER (30 minutes)

5.15.1 STORY OF THE CASESTORY OF THE CASE

Tom Lyster compares this year's performance Tom Lyster compares this year's performance with that of last year, before preparing a with that of last year, before preparing a budget for next year, using specific budget for next year, using specific assumptions. assumptions.

All figures in 000 (thousands) - “coconuts” ....All figures in 000 (thousands) - “coconuts” ....

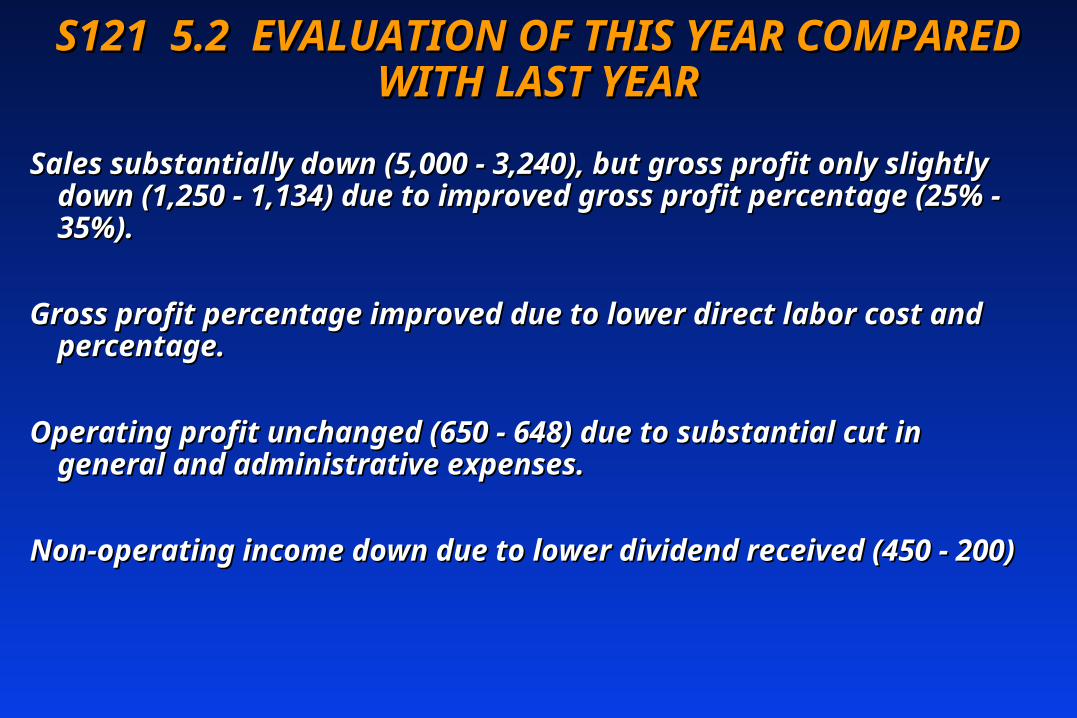

S121 5.2 EVALUATION OF THIS YEAR S121 5.2 EVALUATION OF THIS YEAR COMPARED WITH LAST YEARCOMPARED WITH LAST YEAR

Sales substantially down (5,000 - 3,240), but gross profit Sales substantially down (5,000 - 3,240), but gross profit only slightly down (1,250 - 1,134) due to improved gross only slightly down (1,250 - 1,134) due to improved gross profit percentage (25% - 35%).profit percentage (25% - 35%).

Gross profit percentage improved due to lower direct labor Gross profit percentage improved due to lower direct labor cost and percentage.cost and percentage.

Operating profit unchanged (650 - 648) due to substantial Operating profit unchanged (650 - 648) due to substantial cut in general and administrative expenses.cut in general and administrative expenses.

Non-operating income down due to lower dividend received Non-operating income down due to lower dividend received (450 - 200)(450 - 200)

S122 5.2 EVALUATION OF THIS YEAR S122 5.2 EVALUATION OF THIS YEAR COMPARED WITH LAST YEAR (continued)COMPARED WITH LAST YEAR (continued)

Net profit lower than prior year (450 - 324) due to: Net profit lower than prior year (450 - 324) due to: lower sales, lower dividend received, despite lower sales, lower dividend received, despite improved gross profit percentage, and cuts in improved gross profit percentage, and cuts in general and administrative expenses.general and administrative expenses.

Causes of all these significant differences should be Causes of all these significant differences should be investigated.investigated.

Company failed to make adequate sales but did well Company failed to make adequate sales but did well to improve efficiency; however, falling dividends to improve efficiency; however, falling dividends received reduced the overall profitability.received reduced the overall profitability.

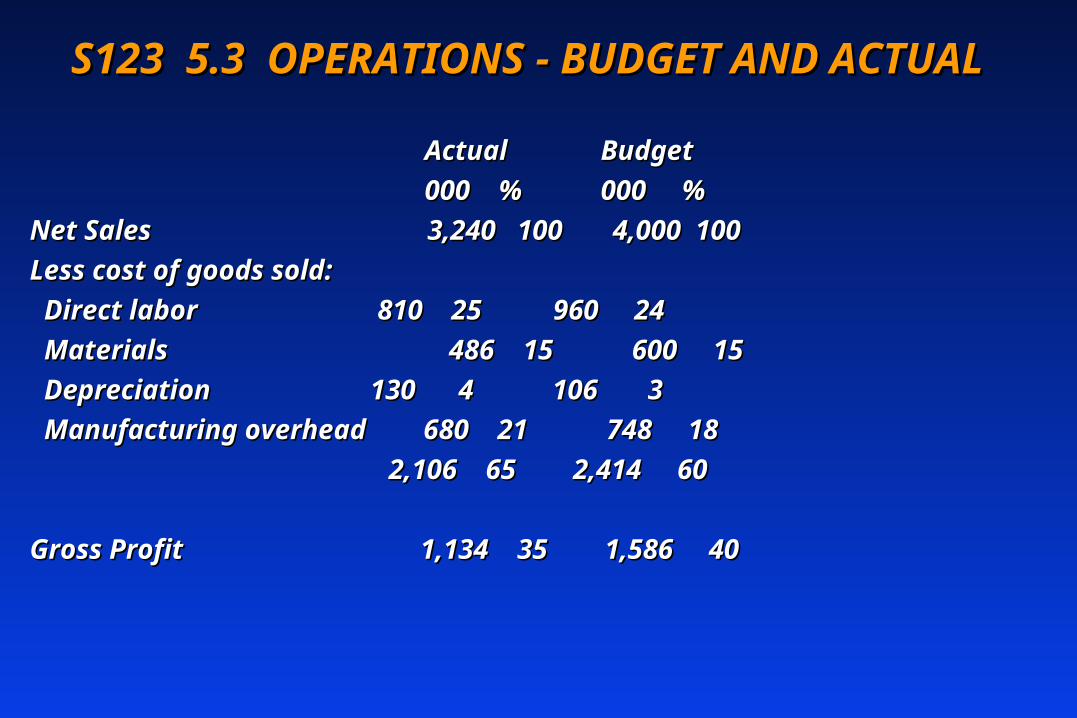

S123 5.3 OPERATIONS - BUDGET AND S123 5.3 OPERATIONS - BUDGET AND ACTUAL ACTUAL

Actual Budget Actual Budget

000 % 000 % 000 % 000 %

Net Sales Net Sales 3,240 100 4,000 100 3,240 100 4,000 100

Less cost of goods sold:Less cost of goods sold:

Direct laborDirect labor 810 25 960 24 810 25 960 24

MaterialsMaterials 486 15 600 15 486 15 600 15

DepreciationDepreciation 130 4 106 3 130 4 106 3

Manufacturing overhead 680 21 748 18Manufacturing overhead 680 21 748 18

2,106 65 2,414 602,106 65 2,414 60

Gross ProfitGross Profit 1,134 35 1,586 40 1,134 35 1,586 40

S124 5.3 OPERATIONS (continued)S124 5.3 OPERATIONS (continued)

Actual % Budget %Actual % Budget %

Gross ProfitGross Profit 1,134 35 1,134 35 1,586 40 1,586 40

Operating expense:Operating expense:

SellingSelling 292 9 292 9 392 10 392 10

General & administrative 194 6General & administrative 194 6 240 6 240 6

486 15486 15 632 16 632 16

Operating ProfitOperating Profit 648 20 648 20 954 24 954 24

Non-operating income & expense:Non-operating income & expense:

Dividends receivedDividends received 200 7 200 7 400 10 400 10

Interest paidInterest paid (200) (7) (100) (200) (7) (100) (3)(3)

Profit before taxes 648 20Profit before taxes 648 20 1,254 31 1,254 31

Income TaxIncome Tax 324 10 324 10 627 16 627 16

Net Profit 000Net Profit 000 324 10% 627 324 10% 627 15% 15%

S125 5.4 COMMENTARY - BUDGET S125 5.4 COMMENTARY - BUDGET COMPARED TO ACTUALCOMPARED TO ACTUAL

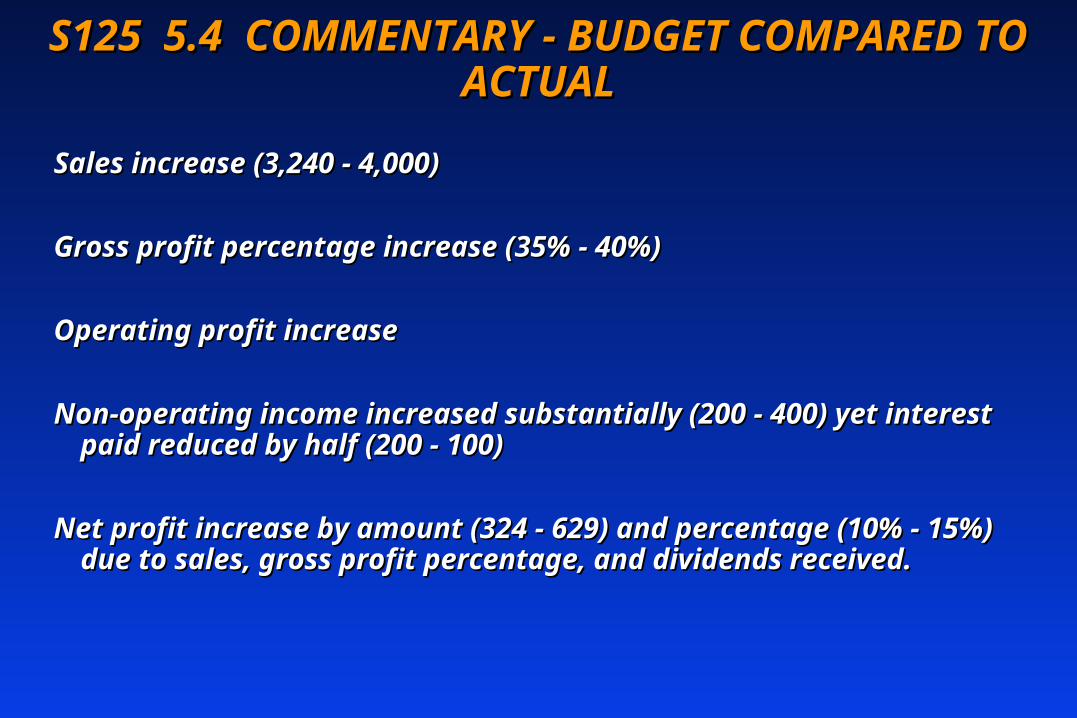

Sales increase (3,240 - 4,000)Sales increase (3,240 - 4,000)

Gross profit percentage increase (35% - 40%)Gross profit percentage increase (35% - 40%)

Operating profit increaseOperating profit increase

Non-operating income increased substantially (200 - 400) yet Non-operating income increased substantially (200 - 400) yet interest paid reduced by half (200 - 100)interest paid reduced by half (200 - 100)

Net profit increase by amount (324 - 629) and percentage Net profit increase by amount (324 - 629) and percentage (10% - 15%) due to sales, gross profit percentage, and (10% - 15%) due to sales, gross profit percentage, and dividends received.dividends received.

S126 5.4 COMMENTARY - BUDGET S126 5.4 COMMENTARY - BUDGET COMPARED TO ACTUAL COMPARED TO ACTUAL

Ratios:Ratios:

ACTUAL BUDGETACTUAL BUDGET

Gross Profit/Sales 1,134/3240 1,586/4000Gross Profit/Sales 1,134/3240 1,586/4000

= 35%= 35% = 40% = 40%

Net Profit/Sales 324/3240 629/4000 Net Profit/Sales 324/3240 629/4000

= 10%= 10% = 15% = 15%

S127 5.5 LEARNING POINTSS127 5.5 LEARNING POINTS

(a) Sales less cost of goods sold = gross profit less operating (a) Sales less cost of goods sold = gross profit less operating expense = operating profit.expense = operating profit.

(b) Operating expense = selling, general and administrative(b) Operating expense = selling, general and administrative

(c) Operating profit less non-operating income and expense = (c) Operating profit less non-operating income and expense = profit before tax.profit before tax.

(d) Non-operating income may be: dividends received or (d) Non-operating income may be: dividends received or interest received or profit on sale of assets; non-operating interest received or profit on sale of assets; non-operating expense is: interest paid, special losses, loss on sale of assets.expense is: interest paid, special losses, loss on sale of assets.

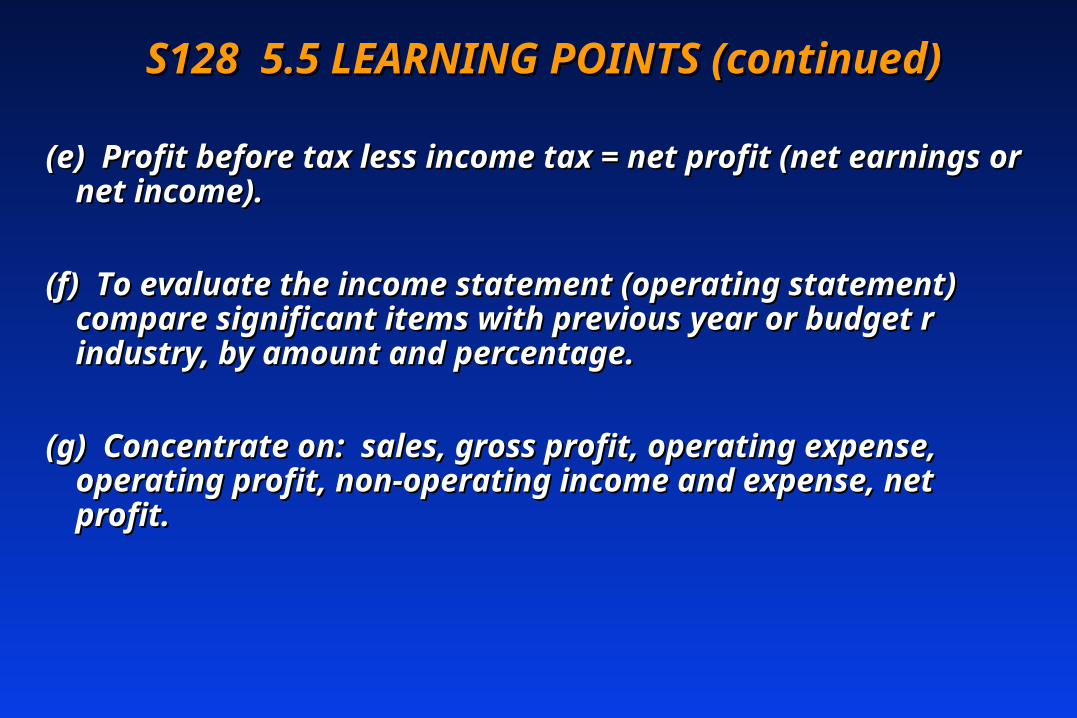

S128 5.5 LEARNING POINTS (continued)S128 5.5 LEARNING POINTS (continued)

(e) Profit before tax less income tax = net profit (net (e) Profit before tax less income tax = net profit (net earnings or net income).earnings or net income).

(f) To evaluate the income statement (operating (f) To evaluate the income statement (operating statement) compare significant items with previous statement) compare significant items with previous year or budget r industry, by amount and year or budget r industry, by amount and percentage.percentage.

(g) Concentrate on: sales, gross profit, operating (g) Concentrate on: sales, gross profit, operating expense, operating profit, non-operating income expense, operating profit, non-operating income and expense, net profit.and expense, net profit.

S129 5.5 LEARNING POINTS (continued)S129 5.5 LEARNING POINTS (continued)

(h) Distinguish operating profit (OP) from net profit (h) Distinguish operating profit (OP) from net profit (NP). Net profit should be the total profit from all (NP). Net profit should be the total profit from all sources for the year after income tax.sources for the year after income tax.

(i) Non-operating income may materially affect the (i) Non-operating income may materially affect the net profit of the period.net profit of the period.

S130 5.5 LEARNING POINTS (continued)S130 5.5 LEARNING POINTS (continued)

(j) Forecast a future income statement when given: (j) Forecast a future income statement when given: sales, ratios, estimates. sales, ratios, estimates.

(k) Distinguish trading from a manufacturing (k) Distinguish trading from a manufacturing company; "purchases of finished goods" are company; "purchases of finished goods" are "manufactured" in the factory. "manufactured" in the factory.

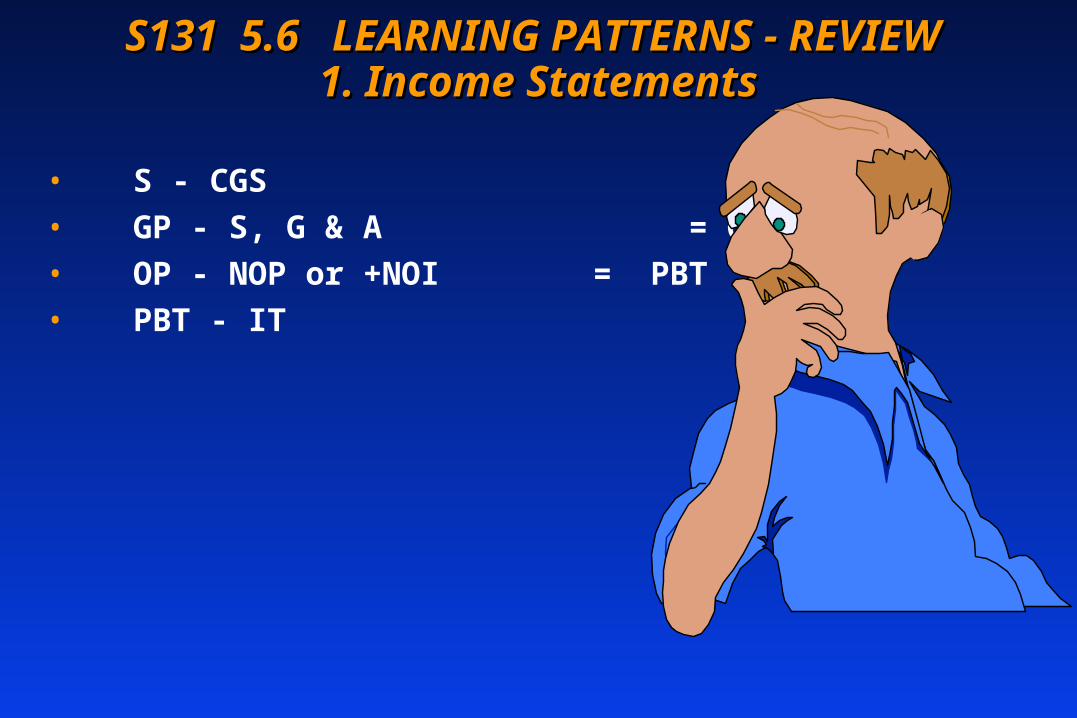

S131 5.6 LEARNING PATTERNS - REVIEW S131 5.6 LEARNING PATTERNS - REVIEW 1. Income Statements1. Income Statements

• S - CGS = GP

• GP - S, G & A = OP

• OP - NOP or +NOI = PBT

• PBT - IT = NP

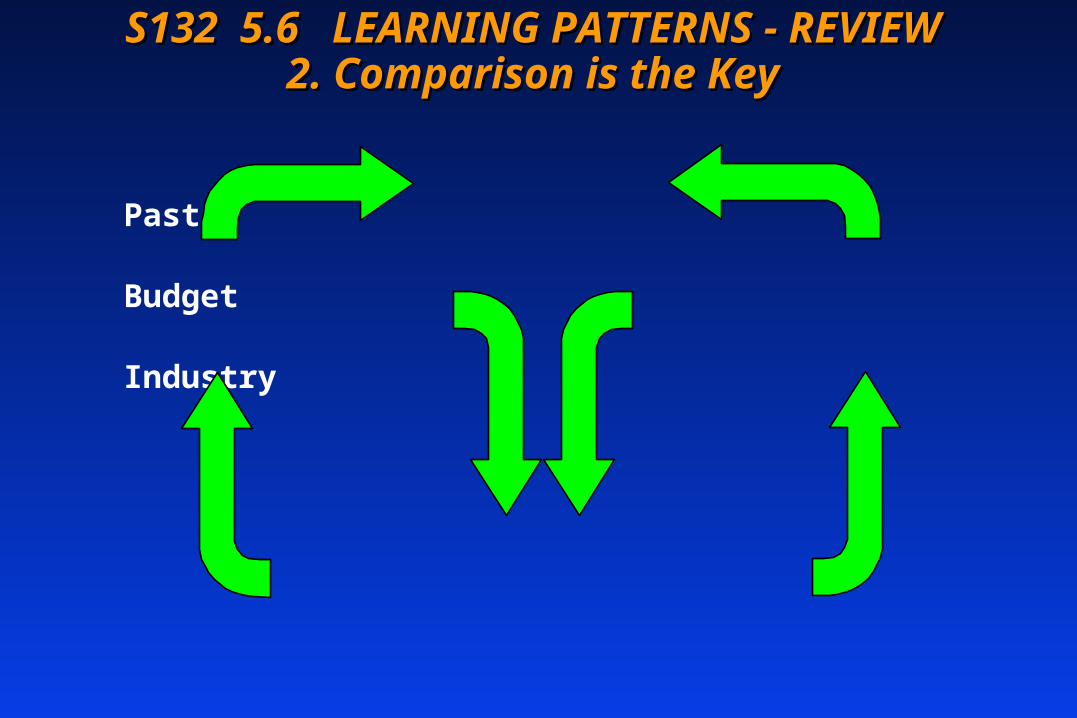

S132 5.6 LEARNING PATTERNS - REVIEW S132 5.6 LEARNING PATTERNS - REVIEW 2. Comparison is the Key 2. Comparison is the Key

Past

Budget

Industry

S133 5.6 LEARNING PATTERNS - REVIEWS133 5.6 LEARNING PATTERNS - REVIEW 3. Forecasting 3. Forecasting

• Sales

• Ratios

• Income Statements

• Balance Sheets

S134 5.7 INSTRUCTIONS (10 minutes)S134 5.7 INSTRUCTIONS (10 minutes)

Reassemble in CSGReassemble in CSG

Study the lecture on the case and resolve outstanding Study the lecture on the case and resolve outstanding questionsquestions

Record key points in your notebookRecord key points in your notebook

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

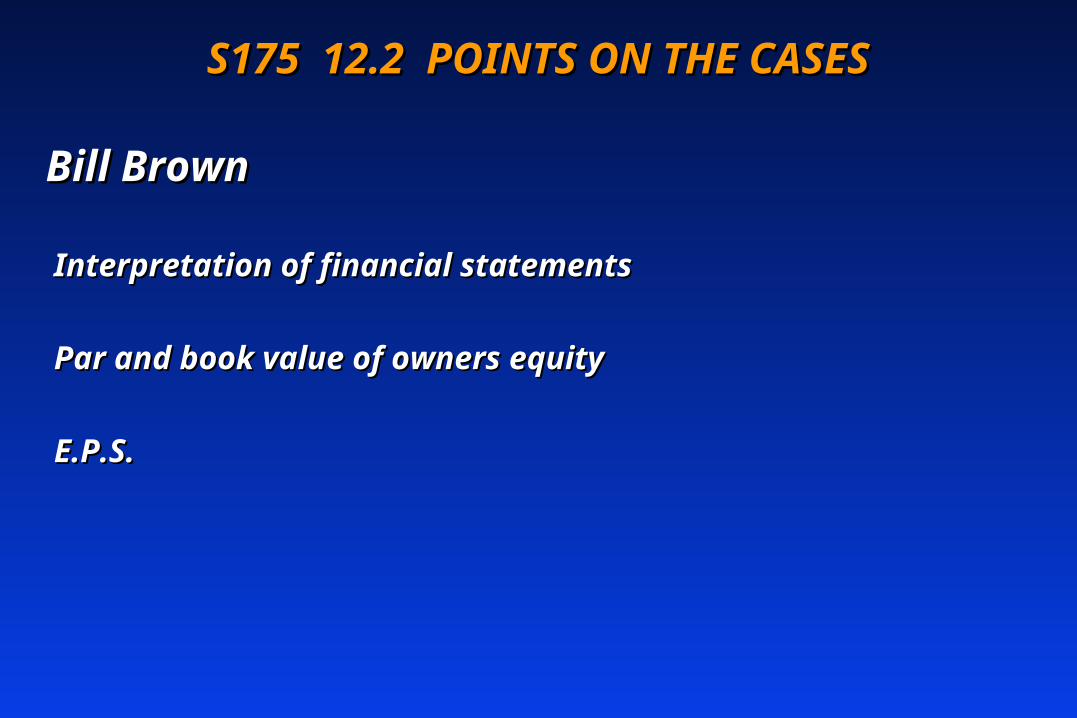

S135 ASSIGNMENT 6.0 - BILL BROWN (30 S135 ASSIGNMENT 6.0 - BILL BROWN (30 minutes)minutes)

6.16.1 INSTRUCTIONSINSTRUCTIONS

Reassemble in SGReassemble in SG

Study the case and individually answer all the questions Study the case and individually answer all the questions (on the worksheet in the diary)(on the worksheet in the diary)

Compare your answers in SGCompare your answers in SG

When the bell rings, stop for lunch! After lunch, check with When the bell rings, stop for lunch! After lunch, check with the correct solutions and discuss outstanding questionsthe correct solutions and discuss outstanding questions

S136 ASSIGNMENT 7.0 PROGRAM S136 ASSIGNMENT 7.0 PROGRAM LEARNING LEARNING

(30 minutes)(30 minutes)

7.17.1 INSTRUCTIONS INSTRUCTIONS

Reassemble in new S. Do Assignment Ch. 5 in writingReassemble in new S. Do Assignment Ch. 5 in writing

Review the summary and glossaryReview the summary and glossary

Record outstanding questions in your notebookRecord outstanding questions in your notebook

Reassemble in MG when the bell ringsReassemble in MG when the bell rings

S137 ASS. 8.0 - LECTURE - The Package S137 ASS. 8.0 - LECTURE - The Package of Accounting Reports of Accounting Reports

8.1 OBJECTIVES8.1 OBJECTIVES

True and fair view (old idea)True and fair view (old idea)

Fair in accordance with IAS (International Accounting Fair in accordance with IAS (International Accounting Standards) - the new view!Standards) - the new view!

MaterialityMateriality

JudgementJudgement

Estimates not scientific factsEstimates not scientific facts

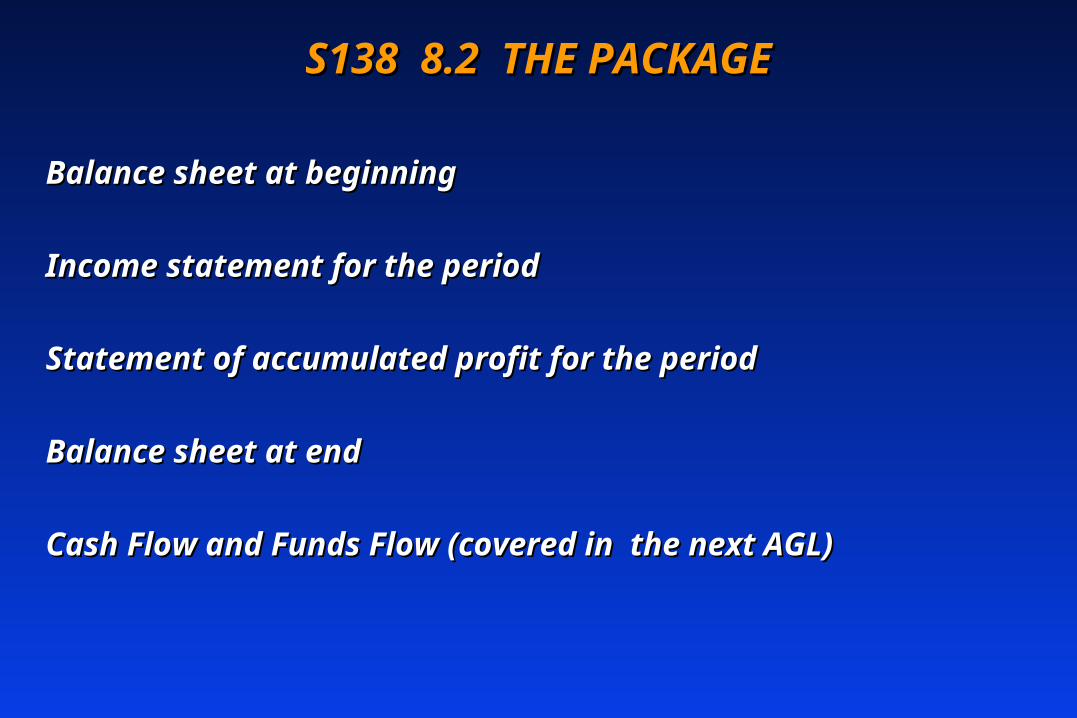

S138 8.2 THE PACKAGES138 8.2 THE PACKAGE

Balance sheet at beginningBalance sheet at beginning

Income statement for the periodIncome statement for the period

Statement of accumulated profit for the periodStatement of accumulated profit for the period

Balance sheet at endBalance sheet at end

Cash Flow and Funds Flow (covered in the next AGL)Cash Flow and Funds Flow (covered in the next AGL)

S139 8.3 STATEMENT OF ACCUMULATED S139 8.3 STATEMENT OF ACCUMULATED PROFITPROFIT

Retained earnings statement. Appropriation accountRetained earnings statement. Appropriation account

Connects one balance sheet with anotherConnects one balance sheet with another

Balance brought forward plus net profit less Balance brought forward plus net profit less dividends equals balance carried forwarddividends equals balance carried forward

Special charges to accumulated profit (i.e. not Special charges to accumulated profit (i.e. not charged via the income statement) need special charged via the income statement) need special investigation!investigation!

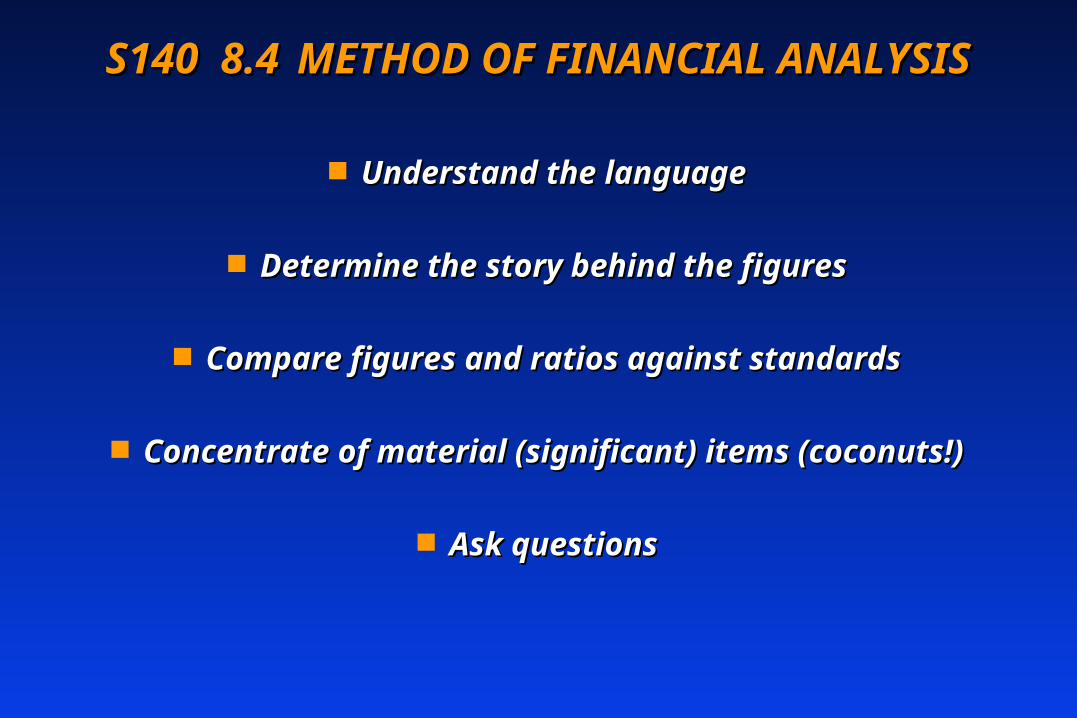

S140 8.4S140 8.4 METHOD OF FINANCIAL METHOD OF FINANCIAL ANALYSISANALYSIS

Understand the languageUnderstand the language

Determine the story behind the figuresDetermine the story behind the figures

Compare figures and ratios against standardsCompare figures and ratios against standards

Concentrate of material (significant) items Concentrate of material (significant) items (coconuts!)(coconuts!)

Ask questionsAsk questions

S141 8.5S141 8.5 LAPP SYSTEM OF FINANCIAL LAPP SYSTEM OF FINANCIAL ANALYSISANALYSIS

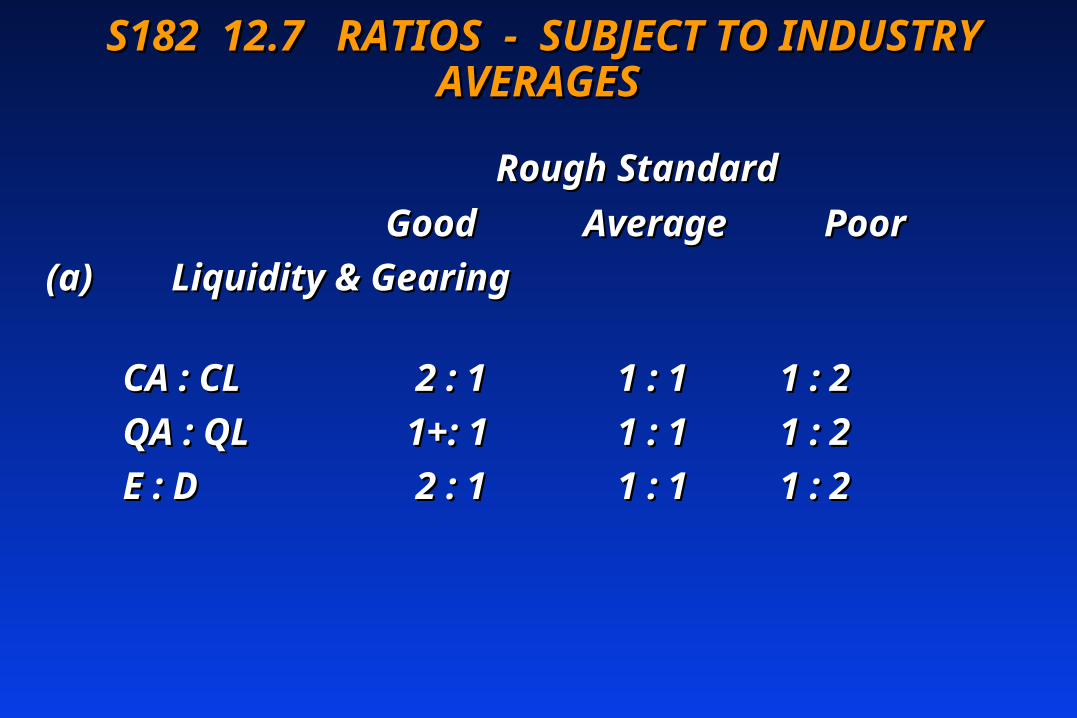

(a) Liquidity(a) Liquidity Rough Rough StandardStandard

Current Assets: Current LiabilitiesCurrent Assets: Current Liabilities 2 : 2 : 11

Quick Assets: Quick LiabilitiesQuick Assets: Quick Liabilities 1 1/2 : 11 1/2 : 1

Equity : Debt Equity : Debt 2 : 1 2 : 1

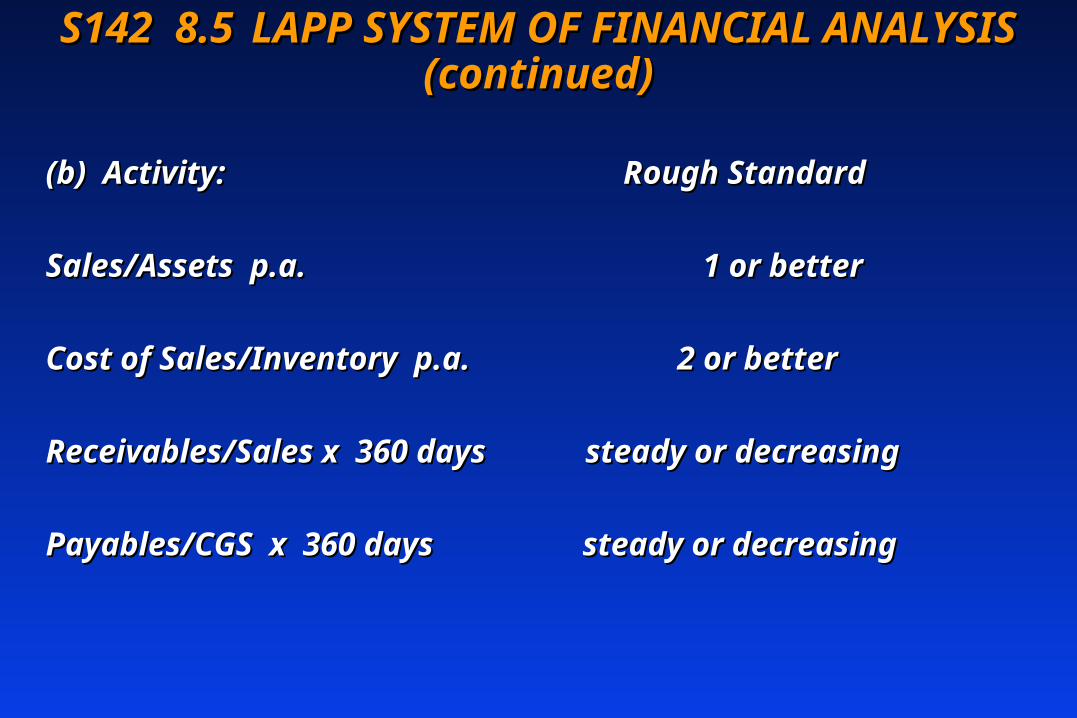

S142 8.5S142 8.5 LAPP SYSTEM OF FINANCIAL LAPP SYSTEM OF FINANCIAL ANALYSIS (continued)ANALYSIS (continued)

(b) Activity: Rough Standard(b) Activity: Rough Standard

Sales/Assets p.a.Sales/Assets p.a. 1 or better 1 or better

Cost of Sales/Inventory p.a. 2 or betterCost of Sales/Inventory p.a. 2 or better

Receivables/Sales x 360 days steady or decreasingReceivables/Sales x 360 days steady or decreasing

Payables/CGS x 360 days steady or decreasingPayables/CGS x 360 days steady or decreasing

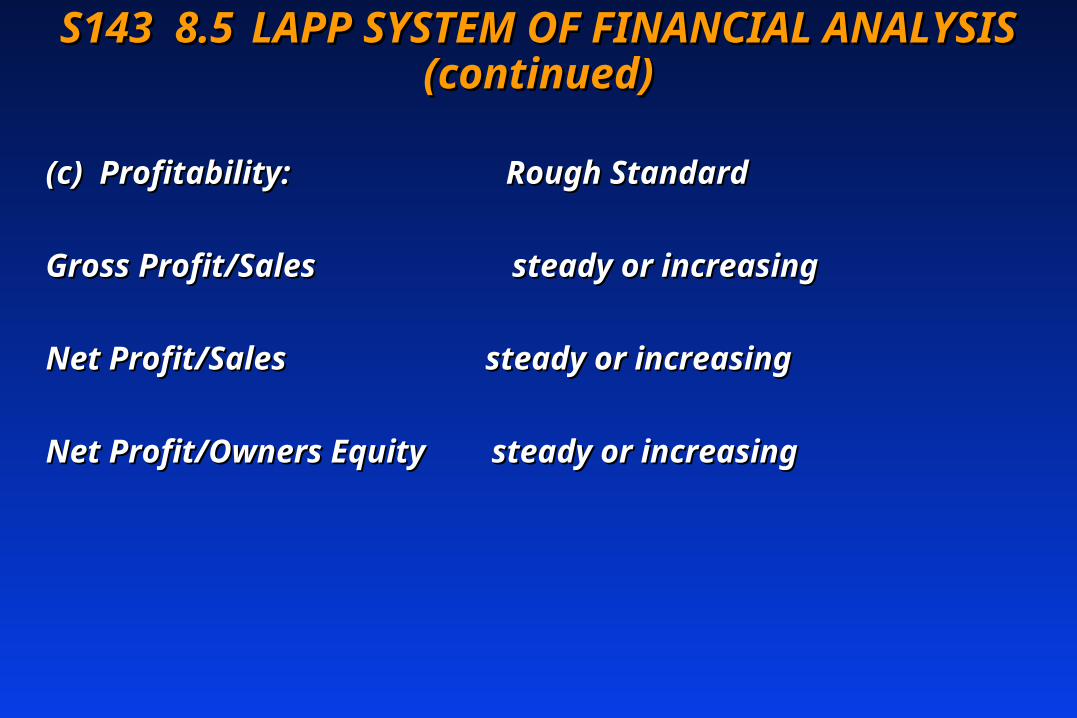

S143 8.5S143 8.5 LAPP SYSTEM OF FINANCIAL LAPP SYSTEM OF FINANCIAL ANALYSIS (continued)ANALYSIS (continued)

(c) Profitability: Rough Standard(c) Profitability: Rough Standard

Gross Profit/SalesGross Profit/Sales steady or increasing steady or increasing

Net Profit/Sales steady or increasingNet Profit/Sales steady or increasing

Net Profit/Owners Equity steady or increasing Net Profit/Owners Equity steady or increasing

S144 8.5 S144 8.5 LAPP SYSTEM OF FINANCIAL LAPP SYSTEM OF FINANCIAL ANALYSIS (continued)ANALYSIS (continued)

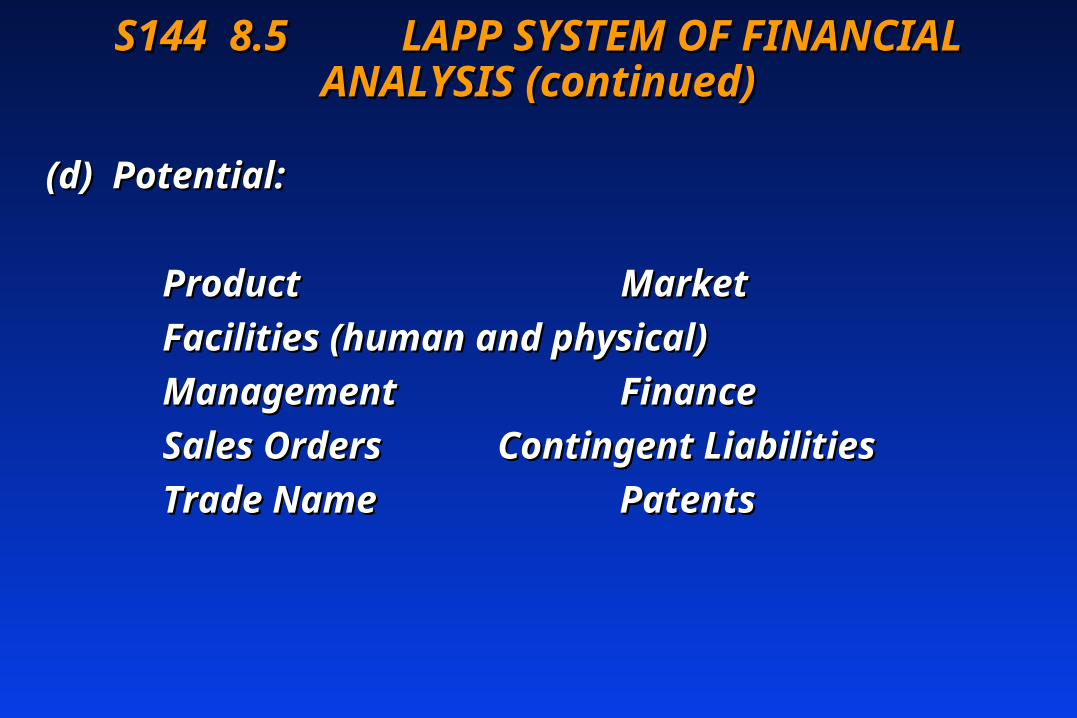

(d) Potential:(d) Potential:

Product MarketProduct Market

Facilities (human and physical)Facilities (human and physical)

Management FinanceManagement Finance

Sales Orders Sales Orders Contingent Contingent LiabilitiesLiabilities

Trade Name PatentsTrade Name Patents

S145 8.6 COMPARISON - KEY TO S145 8.6 COMPARISON - KEY TO FINANCIAL ANALYSISFINANCIAL ANALYSIS

Compare the amounts and ratios against a Compare the amounts and ratios against a standard:standard:

Ask: What is important? Did it change? Why Ask: What is important? Did it change? Why did it change?did it change?

Standard may be: past, budget, industry Standard may be: past, budget, industry averageaverage

S146 8.7 POTENTIAL FOR THE FUTURES146 8.7 POTENTIAL FOR THE FUTURE

Forecast forward to show what will happen Forecast forward to show what will happen under a range of specific assumptions.under a range of specific assumptions.

Then do a PFD ... to avoid EI ... Coconuts ...Then do a PFD ... to avoid EI ... Coconuts ...

S147 8 .8 LEARNING PATTERNS - REVIEW S147 8 .8 LEARNING PATTERNS - REVIEW 1. Reports 1. Reports

• UK/USA/Germany/Russia .... IAS

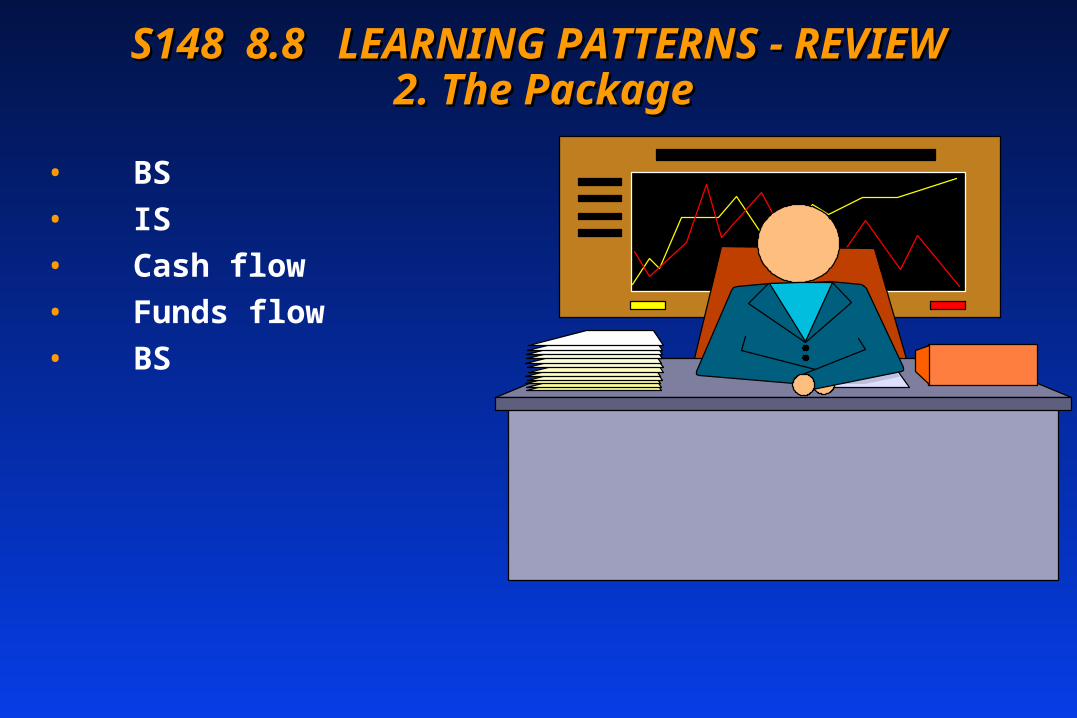

S148 8.8 LEARNING PATTERNS - REVIEWS148 8.8 LEARNING PATTERNS - REVIEW 2. The Package 2. The Package

• BS

• IS

• Cash flow

• Funds flow

• BS

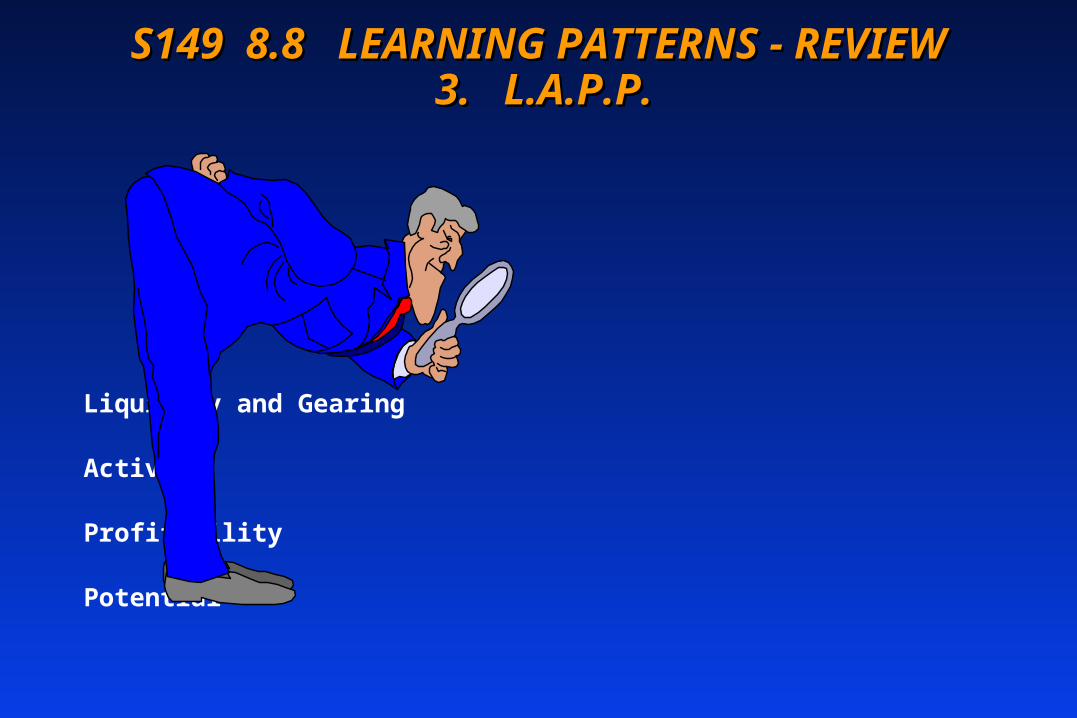

S149 8.8 LEARNING PATTERNS - REVIEWS149 8.8 LEARNING PATTERNS - REVIEW 3. L.A.P.P. 3. L.A.P.P.

Liquidity and Gearing

Activity

Profitability

Potential

S150 8.8 LEARNING PATTERNS - REVIEWS150 8.8 LEARNING PATTERNS - REVIEW 4. Effect of Expansion 4. Effect of Expansion

• Sales

• Inventory & Receivables

S151 8.9 INSTRUCTIONS (10 minutes)S151 8.9 INSTRUCTIONS (10 minutes)

Reassemble in SGReassemble in SG

Study the lecture carefully and record key Study the lecture carefully and record key points in your notebookpoints in your notebook

Discuss outstanding questionsDiscuss outstanding questions

When the bell rings, carry on with the case When the bell rings, carry on with the case study which followsstudy which follows

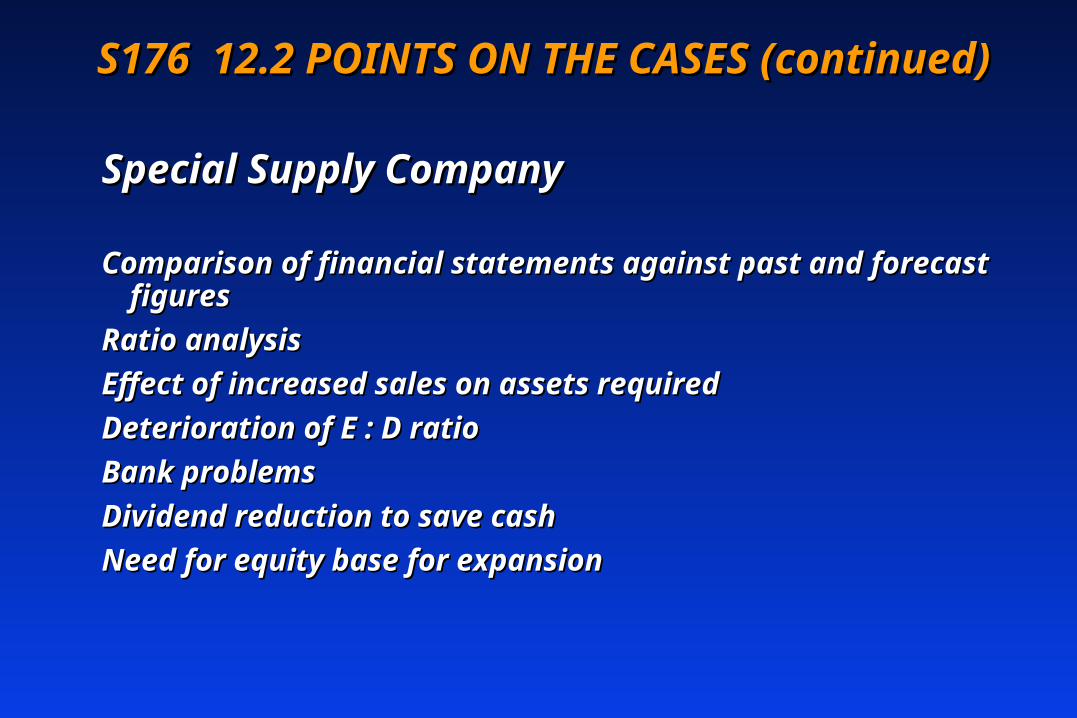

S152 ASSIGNMENT 10.0 - LECTURE - S152 ASSIGNMENT 10.0 - LECTURE - SPECIAL SUPPLY COMPANY (30 minutes)SPECIAL SUPPLY COMPANY (30 minutes)

10.110.1 STORY OF THE CASESTORY OF THE CASE

A businessman expands his business and seeks a loan from A businessman expands his business and seeks a loan from the bank. He forecasts a need of 30,000 but the bank lends the bank. He forecasts a need of 30,000 but the bank lends him 75,000. Why?him 75,000. Why?

His results show increased sales over forecast and slightly His results show increased sales over forecast and slightly increased profits. increased profits.

However, dividends use up necessary cash; inventory is high; However, dividends use up necessary cash; inventory is high; creditors (payables) are stretched. The equity:debt creditors (payables) are stretched. The equity:debt relationship is weaker. Was the expansion really worthwhile?relationship is weaker. Was the expansion really worthwhile?

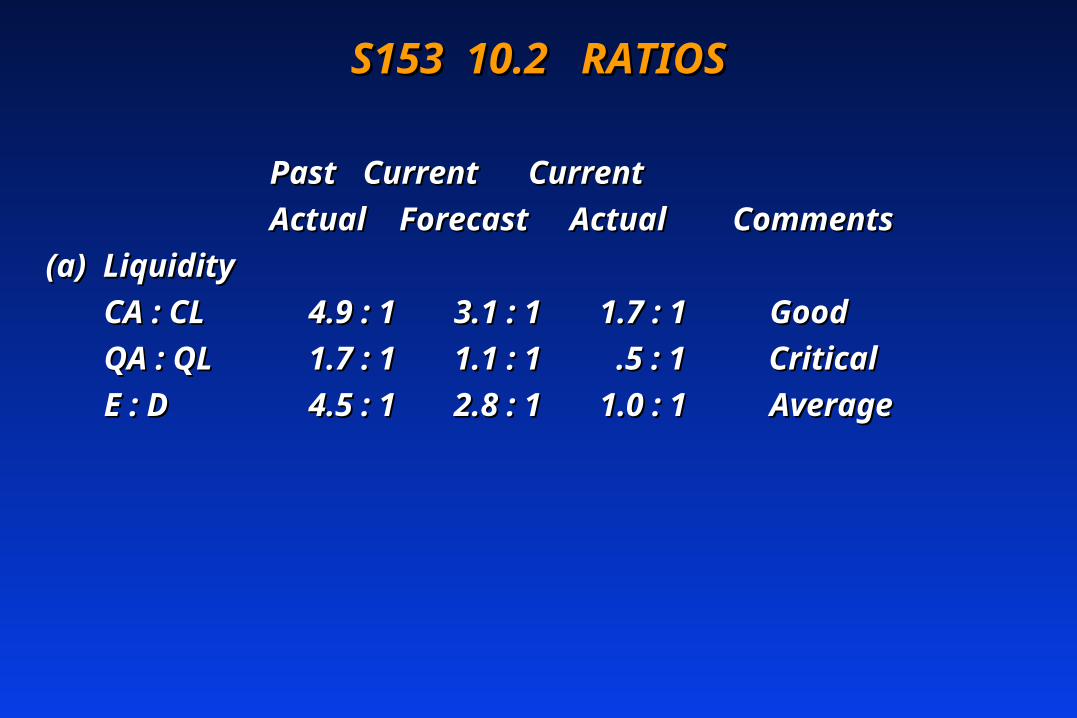

S153 10.2 RATIOSS153 10.2 RATIOS

Past Past Current Current Current Current

Actual Forecast Actual Actual Forecast Actual CommentsComments

(a) Liquidity(a) Liquidity

CA : CLCA : CL 4.9 : 1 3.1 : 1 1.7 : 1 Good 4.9 : 1 3.1 : 1 1.7 : 1 Good

QA : QLQA : QL 1.7 : 1 1.1 : 1 .5 : 1 1.7 : 1 1.1 : 1 .5 : 1 CriticalCritical

E : D E : D 4.5 : 1 2.8 : 1 1.0 : 1 4.5 : 1 2.8 : 1 1.0 : 1 AverageAverage

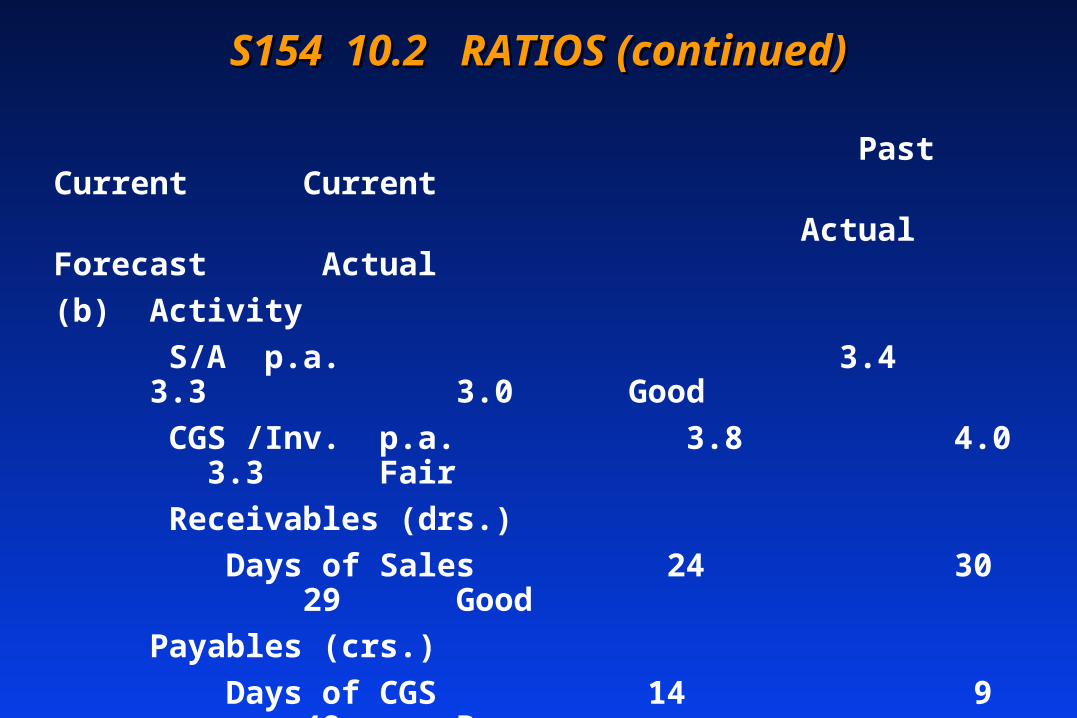

S154 10.2 RATIOS (continued)S154 10.2 RATIOS (continued)

Past Current Current

Actual Forecast Actual

(b) Activity

S/A p.a. 3.4 3.3 3.0 Good

CGS /Inv. p.a. 3.8 4.0 3.3 Fair

Receivables (drs.)

Days of Sales 24 30 29 Good

Payables (crs.)

Days of CGS 14 9 48 Poor

(losing cash discounts?)

S155 10.2 RATIOS (continued)S155 10.2 RATIOS (continued)

Past Current CurrentPast Current Current

Actual Forecast Actual Actual Forecast Actual

(c) Profitability(c) Profitability

GP/S 35.0 37.0GP/S 35.0 37.0 33.5 Poor 33.5 Poor

NP/SNP/S 4.3 4.3 5.6 5.6 4.4 Poor 4.4 Poor

NP/OE p.a. 18NP/OE p.a. 18 25 25 26 Good 26 Good

S156 10.3 HEALTH OF THE COMPANYS156 10.3 HEALTH OF THE COMPANY

Liquidity - not too good because dividends Liquidity - not too good because dividends and inventory have used up existing cash; and inventory have used up existing cash; cannot conveniently pay back the 25,000 due cannot conveniently pay back the 25,000 due in two weeks to the bank.in two weeks to the bank.

Activity - very active; sales increase has led Activity - very active; sales increase has led to increased inventory.to increased inventory.

S157 10.3 HEALTH OF THE COMPANY S157 10.3 HEALTH OF THE COMPANY (continued)(continued)

Profitability - slightly above forecast in Profitability - slightly above forecast in amount; margin percentage has fallen with amount; margin percentage has fallen with the increase in sales; however, return on the increase in sales; however, return on equity good because leverage (GEARING - E : equity good because leverage (GEARING - E : D) high.D) high.

Potential - sales potential good; could lead to Potential - sales potential good; could lead to increased working capital requirements; increased working capital requirements; cash problems and a weaker equity : debt cash problems and a weaker equity : debt ratio.ratio.

S158 10.4 STANDARDS OF PERFORMANCES158 10.4 STANDARDS OF PERFORMANCE

Compare actual last year, with forecast last Compare actual last year, with forecast last year to measure management effectiveness. year to measure management effectiveness.

Compare actual last year, with actual of the Compare actual last year, with actual of the previous year to measure the trend of previous year to measure the trend of operations.operations.

S159 10.5 EQUITY : DEBT POSITIONS159 10.5 EQUITY : DEBT POSITION

Change from 4.5 : 1 to l : 1 indicates a debt Change from 4.5 : 1 to l : 1 indicates a debt capacity used up. capacity used up.

If sales increase even further, the need for cash If sales increase even further, the need for cash will rise and this ratio will become unhealthy, will rise and this ratio will become unhealthy, i.e., 1 : 2.i.e., 1 : 2.

Cash and E : D ratio are serious problems Cash and E : D ratio are serious problems although the profit is better than the previous although the profit is better than the previous year.year.

S160 10.5 EQUITY : DEBT POSITION S160 10.5 EQUITY : DEBT POSITION (continued)(continued)

IIncrease in sales requires more assets - ncrease in sales requires more assets - ALWAYS!!ALWAYS!!

If sales increase even further, even more If sales increase even further, even more assets will be required;assets will be required;

Can only be financed from liabilities since Can only be financed from liabilities since profit is not retained sufficiently to increase profit is not retained sufficiently to increase the equity.the equity.

S161 10.6 PLAN OF ACTIONS161 10.6 PLAN OF ACTION

(a) Company (always seven alternatives!)(a) Company (always seven alternatives!)

Postpone repayment of 25,000 or stretch payables Postpone repayment of 25,000 or stretch payables

Hold back sales or get more equity capitalHold back sales or get more equity capital

Hold back dividends during rapid expansion , when Hold back dividends during rapid expansion , when cash flow from profits is needed to increase the cash flow from profits is needed to increase the equity baseequity base

S162 10.6 PLAN OF ACTION (continued)S162 10.6 PLAN OF ACTION (continued)

(b) Bank(b) Bank

Decide if company is a worthwhile client or notDecide if company is a worthwhile client or not

Decide if long term bank loan could be safeDecide if long term bank loan could be safe

Decide if another bank would give the loan Decide if another bank would give the loan

Then (a) aboveThen (a) above

S163 10.6 PLAN OF ACTION (continued)S163 10.6 PLAN OF ACTION (continued)

KEY NOTES: KEY NOTES: