automotive luxury/premium portfolio expansion in · pdf filesuv expansion as growth driver,...

TRANSCRIPT

© 2017 IHS Markit © 2017 IHS Markit. All Rights Reserved.

Luxury/Premium Portfolio Expansion in light of Regulation

AUTOMOTIVE

Thomas Meininger, Senior Manager, IHS Advisory Services [email protected]

26 January 2017 | Frankfurt, Germany

© 2017 IHS Markit

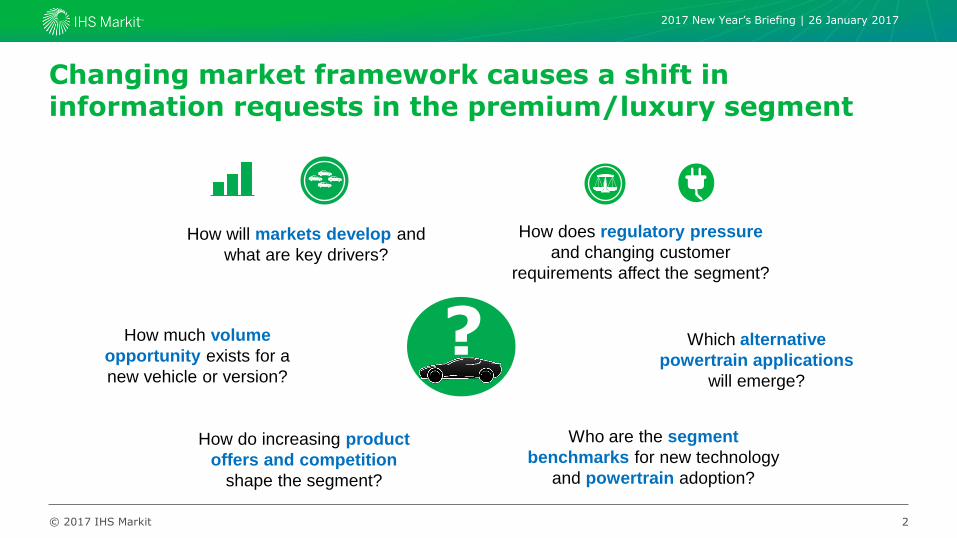

Changing market framework causes a shift in information requests in the premium/luxury segment

2

2017 New Year’s Briefing | 26 January 2017

?

How do increasing product

offers and competition

shape the segment?

How does regulatory pressure

and changing customer

requirements affect the segment?

Which alternative

powertrain applications

will emerge?

How much volume

opportunity exists for a

new vehicle or version?

How will markets develop and

what are key drivers?

Who are the segment

benchmarks for new technology

and powertrain adoption?

© 2017 IHS Markit

Presentation Agenda

3

2017 New Year’s Briefing | 26 January 2017

Luxury Segment

• Market insights and trends

• Segment development in light of regulation

Premium High Performance Segment

• Market insight and trends

• Segment development in light of regulation

Summary and Key Takeaways

1

2

3

© 2017 IHS Markit

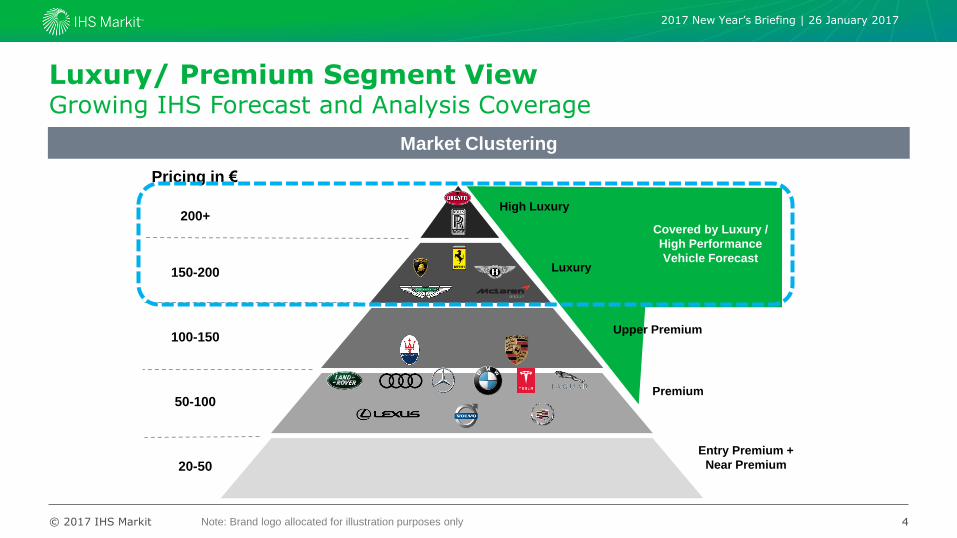

Luxury/ Premium Segment View Growing IHS Forecast and Analysis Coverage

2017 New Year’s Briefing | 26 January 2017

200+

150-200

100-150

50-100

20-50

Pricing in €

High Luxury

Luxury

Upper Premium

Premium

Entry Premium +

Near Premium

Covered by Luxury /

High Performance

Vehicle Forecast

Market Clustering

4 Note: Brand logo allocated for illustration purposes only

© 2017 IHS Markit 5

2017 New Year’s Briefing | 26 January 2017

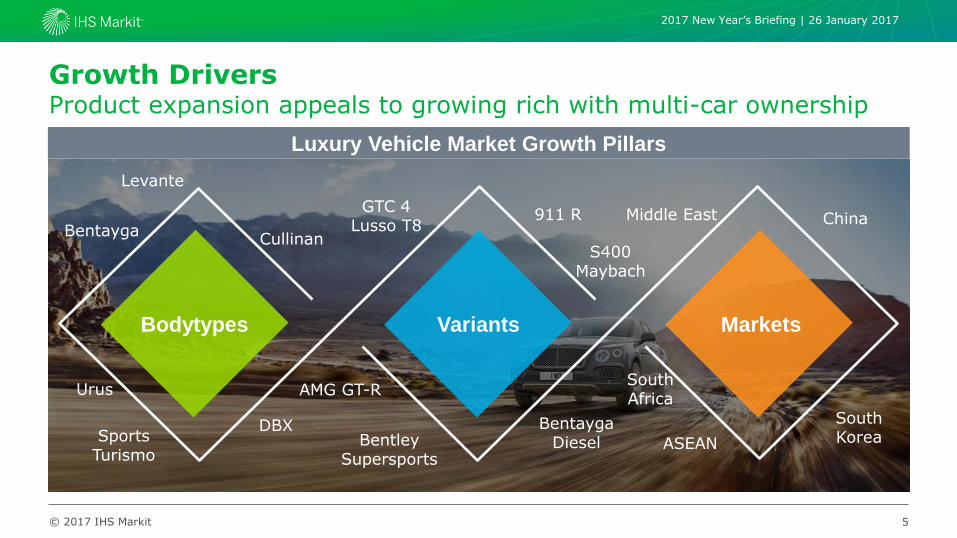

Growth Drivers Product expansion appeals to growing rich with multi-car ownership

Luxury Vehicle Market Growth Pillars

Bodytypes Variants Markets

Bentayga Cullinan

Urus

DBX Sports Turismo

Levante

AMG GT-R

GTC 4 Lusso T8

Bentayga Diesel

911 R

S400 Maybach

China

South Korea

South Africa

ASEAN Bentley Supersports

Middle East

© 2017 IHS Markit 6

2017 New Year’s Briefing | 26 January 2017

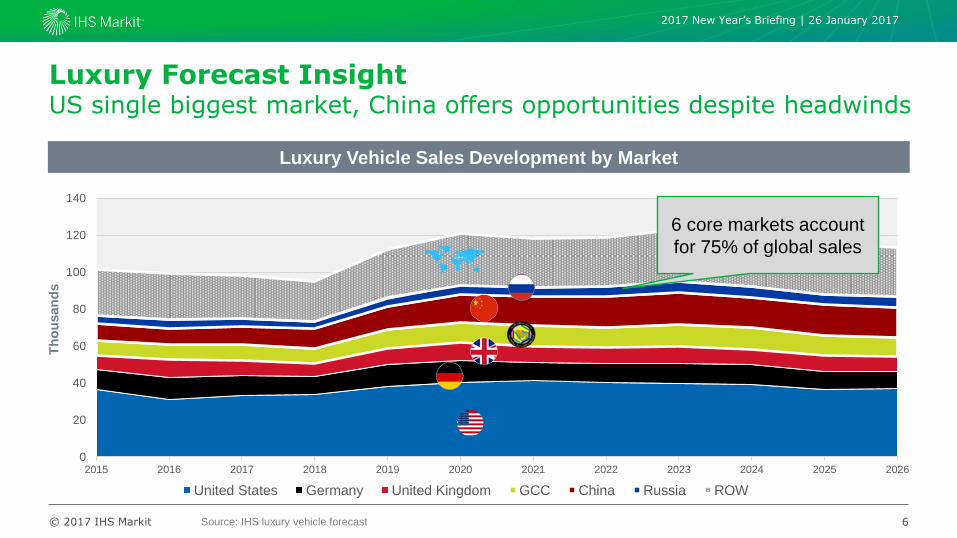

Luxury Forecast Insight US single biggest market, China offers opportunities despite headwinds

0

20

40

60

80

100

120

140

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

United States Germany United Kingdom GCC China Russia ROW

Luxury Vehicle Sales Development by Market

Th

ou

san

ds

6 core markets account

for 75% of global sales

Source: IHS luxury vehicle forecast

© 2017 IHS Markit 7

2017 New Year’s Briefing | 26 January 2017

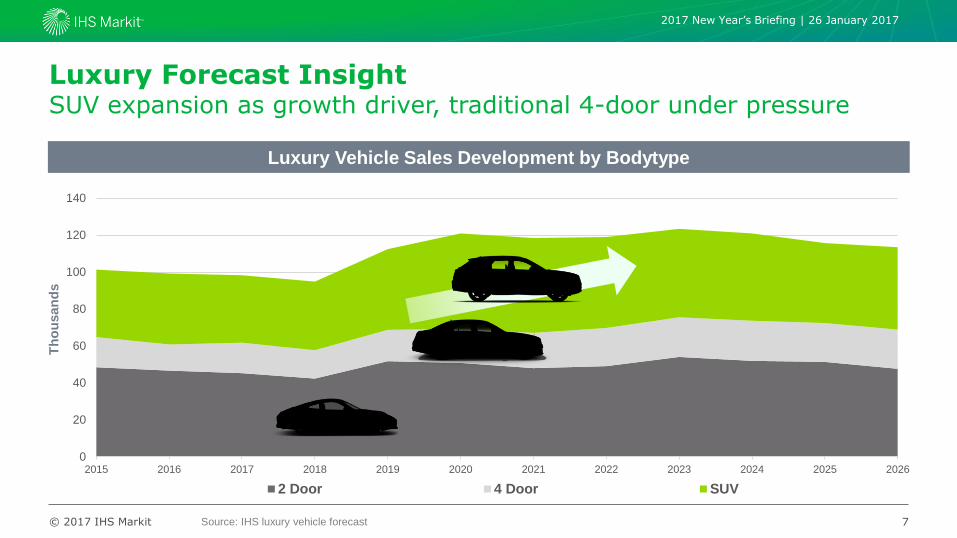

Luxury Forecast Insight SUV expansion as growth driver, traditional 4-door under pressure

0

20

40

60

80

100

120

140

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

2 Door 4 Door SUV

Luxury Vehicle Sales Development by Bodytype

Th

ou

san

ds

Source: IHS luxury vehicle forecast

© 2017 IHS Markit

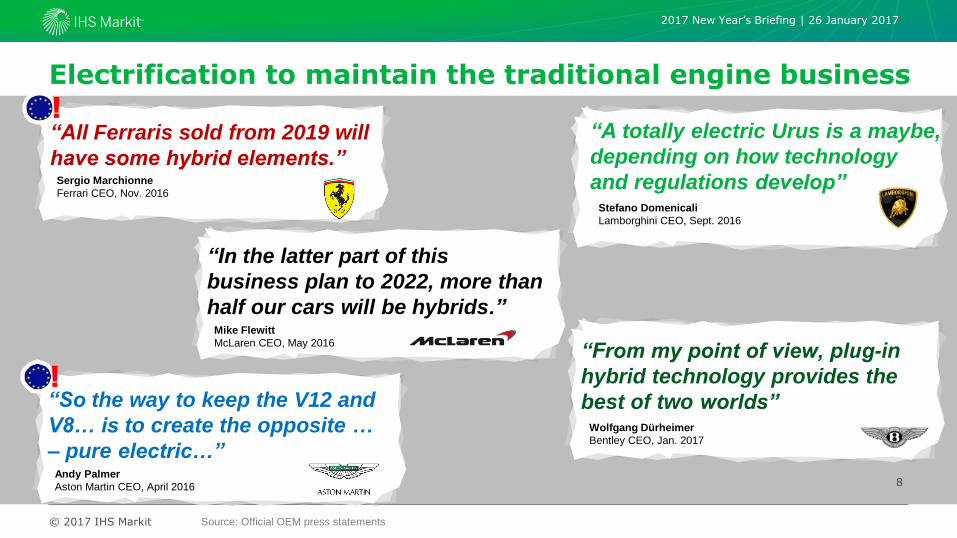

Electrification to maintain the traditional engine business

8

2017 New Year’s Briefing | 26 January 2017

Stefano Domenicali

Lamborghini CEO, Sept. 2016

“A totally electric Urus is a maybe,

depending on how technology

and regulations develop”

Mike Flewitt

McLaren CEO, May 2016

“In the latter part of this

business plan to 2022, more than

half our cars will be hybrids.”

Wolfgang Dürheimer

Bentley CEO, Jan. 2017

“From my point of view, plug-in

hybrid technology provides the

best of two worlds”

Andy Palmer

Aston Martin CEO, April 2016

“So the way to keep the V12 and

V8… is to create the opposite …

– pure electric…”

Sergio Marchionne

Ferrari CEO, Nov. 2016

“All Ferraris sold from 2019 will

have some hybrid elements.”

!

!

Source: Official OEM press statements

© 2017 IHS Markit

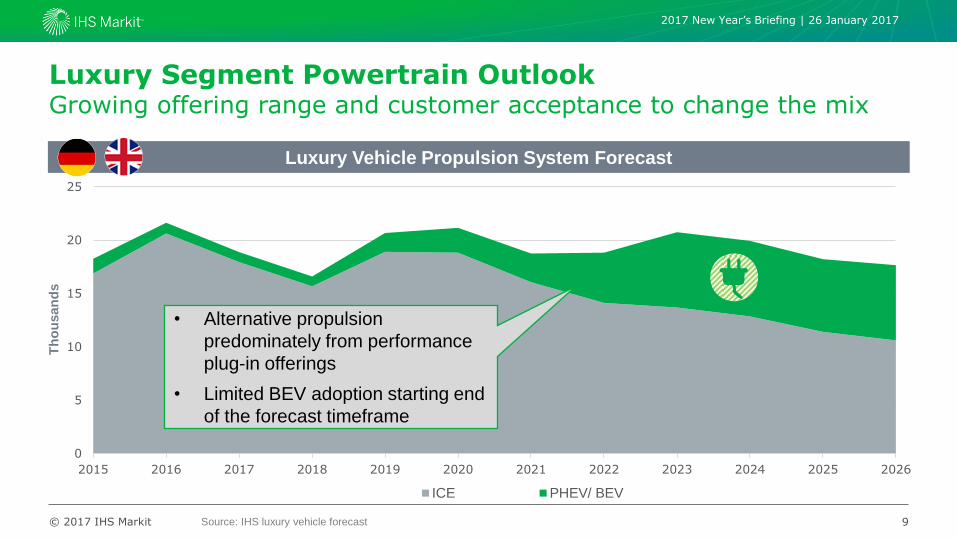

Luxury Segment Powertrain Outlook Growing offering range and customer acceptance to change the mix

9

2017 New Year’s Briefing | 26 January 2017

Luxury Vehicle Propulsion System Forecast

0

5

10

15

20

25

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

ICE PHEV/ BEV

Th

ou

san

ds

• Alternative propulsion

predominately from performance

plug-in offerings

• Limited BEV adoption starting end

of the forecast timeframe

Source: IHS luxury vehicle forecast

© 2017 IHS Markit

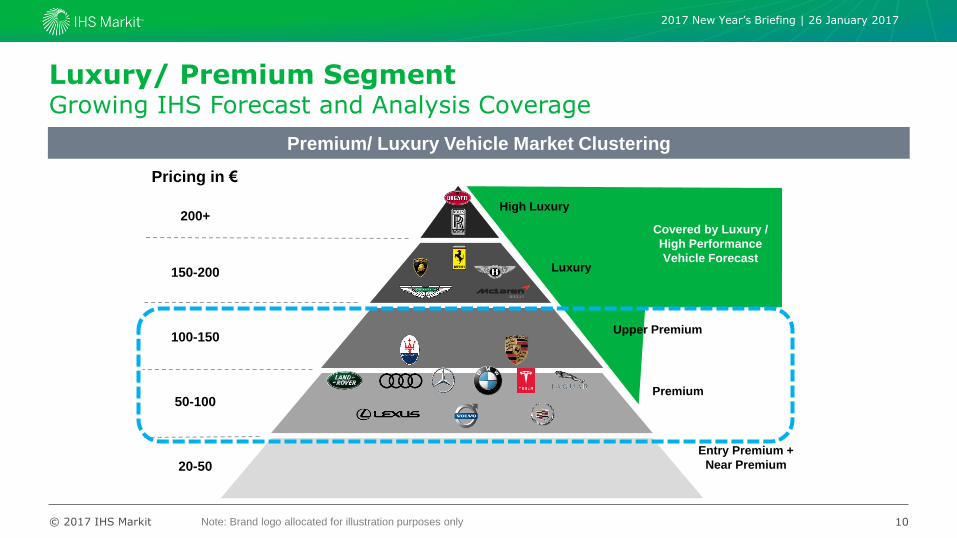

Luxury/ Premium Segment Growing IHS Forecast and Analysis Coverage

2017 New Year’s Briefing | 26 January 2017

200+

150-200

100-150

50-100

20-50

Pricing in €

High Luxury

Luxury

Upper Premium

Premium

Entry Premium +

Near Premium

Covered by Luxury /

High Performance

Vehicle Forecast

Premium/ Luxury Vehicle Market Clustering

10 Note: Brand logo allocated for illustration purposes only

© 2017 IHS Markit

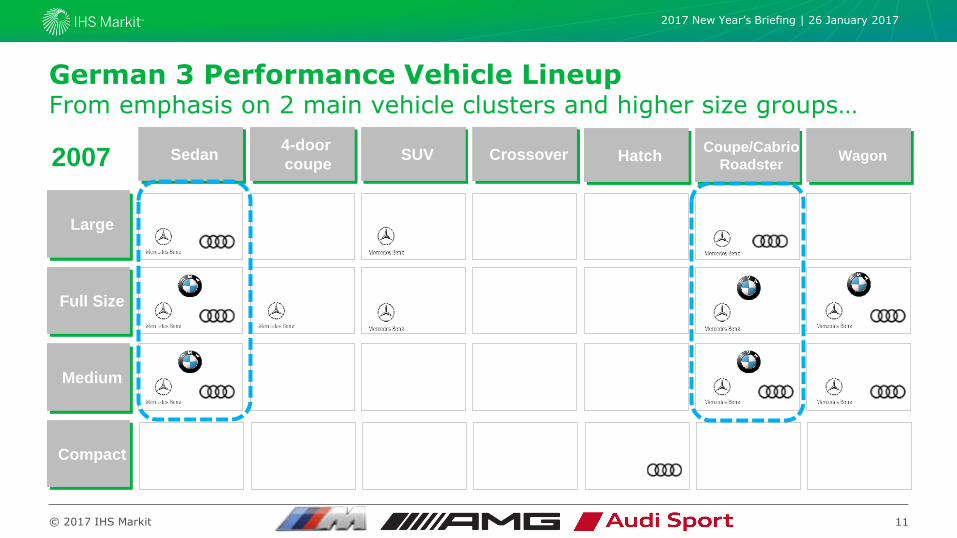

German 3 Performance Vehicle Lineup From emphasis on 2 main vehicle clusters and higher size groups…

11

2017 New Year’s Briefing | 26 January 2017

Sedan 4-door

coupe SUV Crossover

Large

Full Size

Medium

Compact

2007 Hatch Coupe/Cabrio

Roadster Wagon

© 2017 IHS Markit

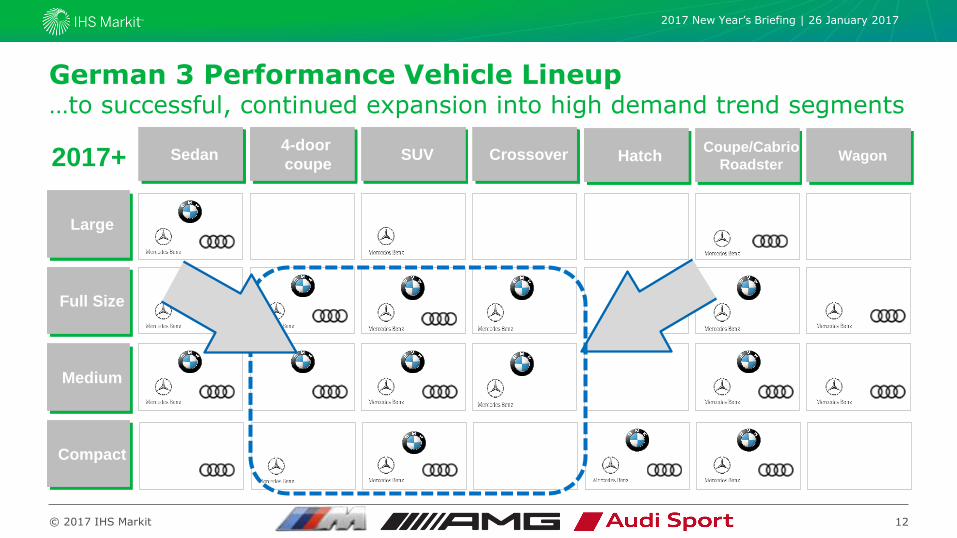

German 3 Performance Vehicle Lineup …to successful, continued expansion into high demand trend segments

12

2017 New Year’s Briefing | 26 January 2017

Sedan 4-door

coupe SUV Crossover

Large

Full Size

Medium

Compact

2017+ Hatch Coupe/Cabrio

Roadster Wagon

© 2017 IHS Markit

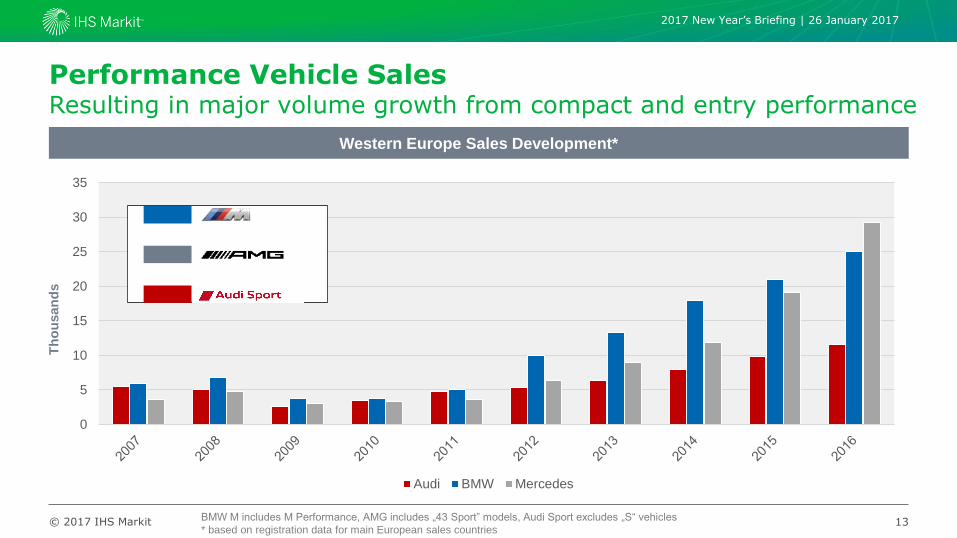

0

5

10

15

20

25

30

35

Audi BMW Mercedes

Performance Vehicle Sales Resulting in major volume growth from compact and entry performance

13

2017 New Year’s Briefing | 26 January 2017

Western Europe Sales Development*

BMW M includes M Performance, AMG includes „43 Sport” models, Audi Sport excludes „S“ vehicles

* based on registration data for main European sales countries

Th

ou

san

ds

© 2017 IHS Markit 14

2017 New Year’s Briefing | 26 January 2017

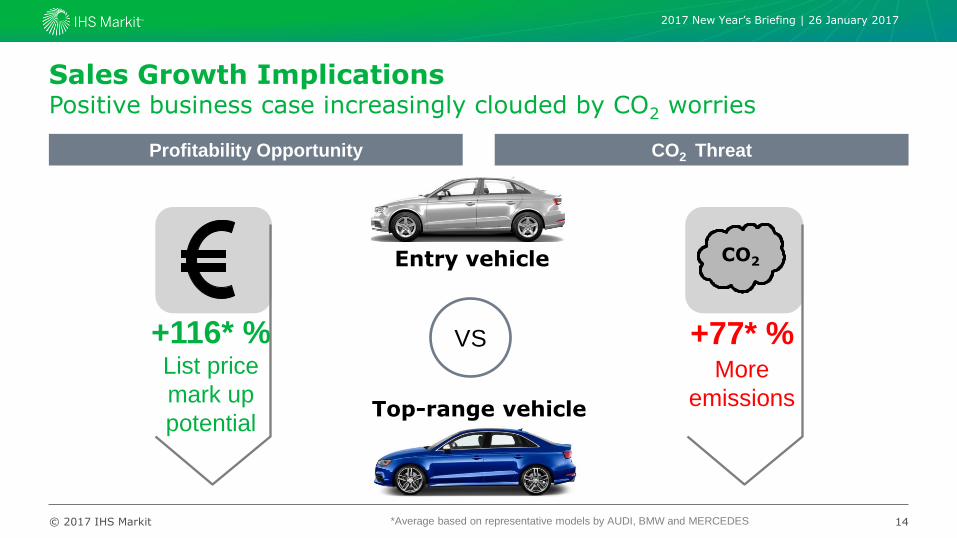

Sales Growth Implications Positive business case increasingly clouded by CO2 worries

Profitability Opportunity CO2 Threat

VS

Entry vehicle

*Average based on representative models by AUDI, BMW and MERCEDES

+116* % List price

mark up

potential

+77* % More

emissions

CO2

Top-range vehicle

© 2017 IHS Markit

154g

CO2/km

130g

CO2/km

2008

2015

2021 95g CO2/km

According to NEDC Standard

2008

2016

27,5 mpg

34,1 mpg

According to CAFE Standard

5,0l/100km

2015

2020

According to NEDC Standard

6,9l/100km

2027* 2027* 2027* 4,1l/100km 75g CO2/km? 56 mpg

2017 New Year’s Briefing | 26 January 2017

Vehicle Emission Target Regulation

15

© 2017 IHS Markit 16

2017 New Year’s Briefing | 26 January 2017

0

25

50

75

100

125

150

175

200

225

250

275

300

3251 Series 3 Series X4 5 Series X5 7 Series

x 330e

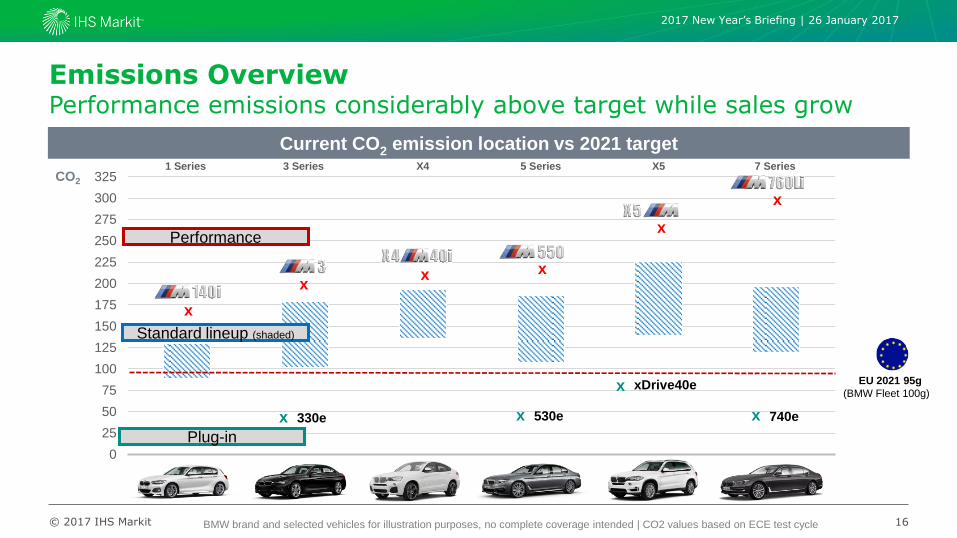

Emissions Overview Performance emissions considerably above target while sales grow

x xDrive40e

x 740e

Current CO2 emission location vs 2021 target

EU 2021 95g

(BMW Fleet 100g)

x

x

x x

x

x

x 530e

CO2

Performance

Standard lineup (shaded)

Plug-in

BMW brand and selected vehicles for illustration purposes, no complete coverage intended | CO2 values based on ECE test cycle

© 2017 IHS Markit

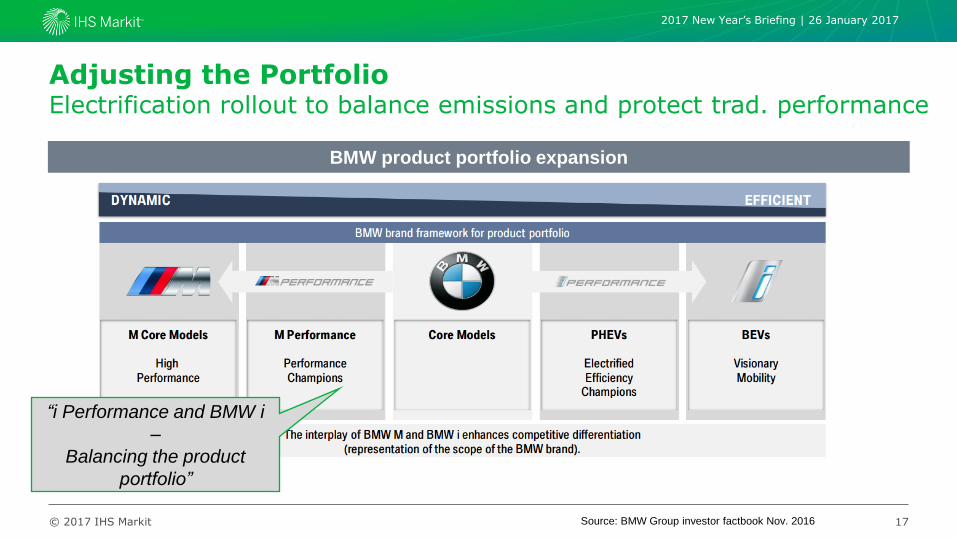

Adjusting the Portfolio Electrification rollout to balance emissions and protect trad. performance

17

2017 New Year’s Briefing | 26 January 2017

Source: BMW Group investor factbook Nov. 2016

BMW product portfolio expansion

“i Performance and BMW i

–

Balancing the product

portfolio”

© 2017 IHS Markit

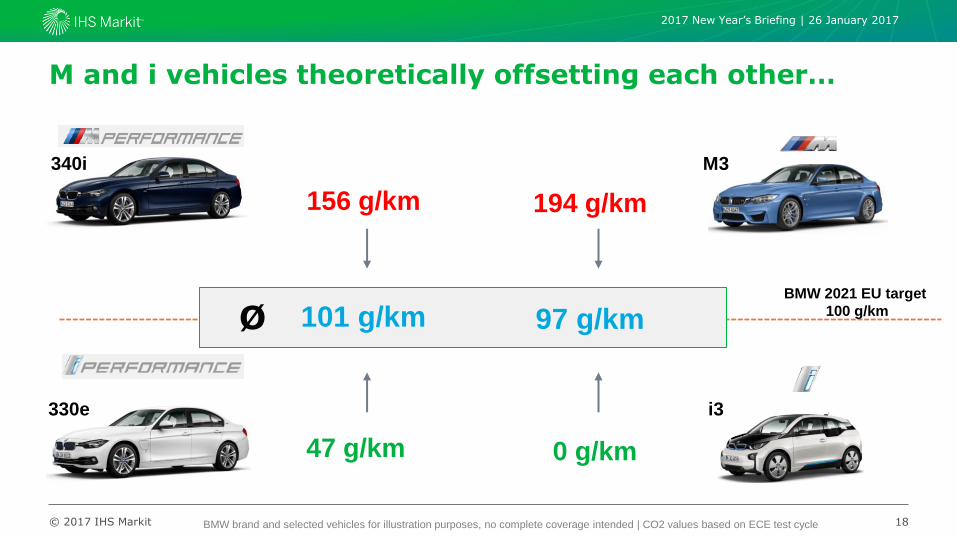

BMW 2021 EU target

100 g/km

M and i vehicles theoretically offsetting each other…

18

2017 New Year’s Briefing | 26 January 2017

340i

330e i3

M3

47 g/km

156 g/km

0 g/km

194 g/km

Ø 101 g/km 97 g/km

BMW brand and selected vehicles for illustration purposes, no complete coverage intended | CO2 values based on ECE test cycle

© 2017 IHS Markit

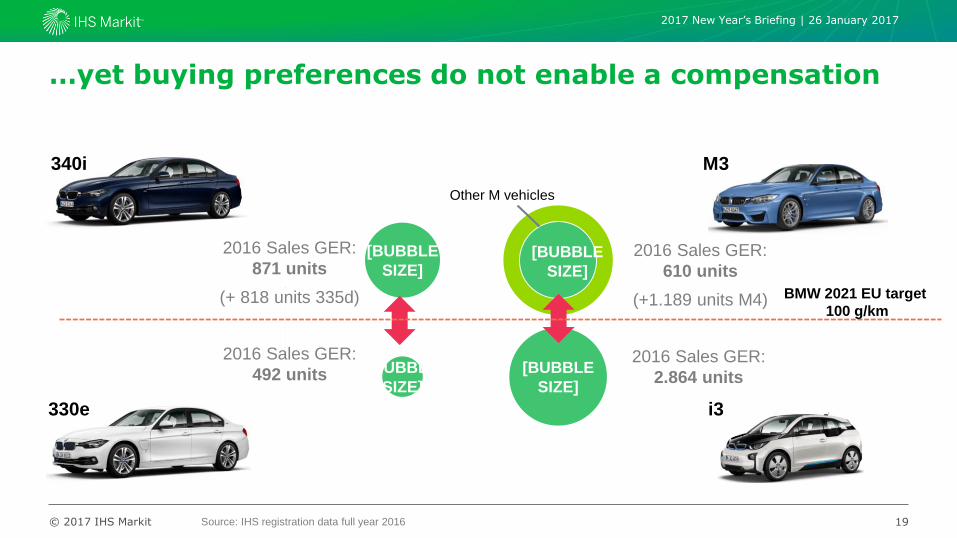

…yet buying preferences do not enable a compensation

19

2017 New Year’s Briefing | 26 January 2017

47 g/km

156 g/km

0 g/km

194 g/km

Ø 101 g/km 97 g/km BMW 2021 EU target

100 g/km

2016 Sales GER:

871 units

(+ 818 units 335d)

2016 Sales GER:

492 units

2016 Sales GER:

610 units

(+1.189 units M4)

2016 Sales GER:

2.864 units [BUBBLE

SIZE]

[BUBBLE

SIZE]

[BUBBLE

SIZE]

[BUBBLE

SIZE]

Other M vehicles

i3

M3 340i

330e

Source: IHS registration data full year 2016

BMW 2021 EU target

100 g/km

© 2017 IHS Markit

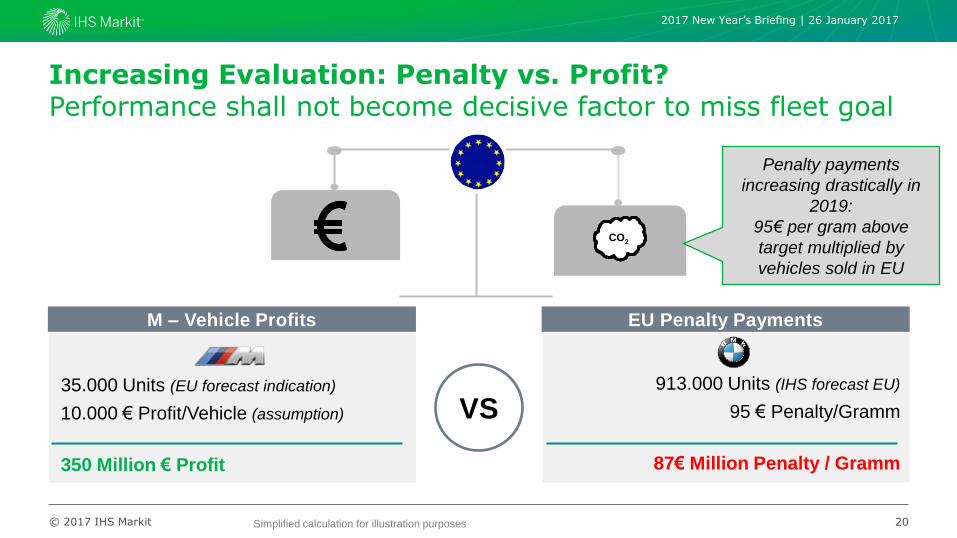

Increasing Evaluation: Penalty vs. Profit? Performance shall not become decisive factor to miss fleet goal

20

2017 New Year’s Briefing | 26 January 2017

CO2

VS 35.000 Units (EU forecast indication)

10.000 € Profit/Vehicle (assumption)

350 Million € Profit

M – Vehicle Profits

Penalty payments

increasing drastically in

2019:

95€ per gram above

target multiplied by

vehicles sold in EU

Simplified calculation for illustration purposes

913.000 Units (IHS forecast EU)

95 € Penalty/Gramm

87€ Million Penalty / Gramm

EU Penalty Payments

© 2017 IHS Markit

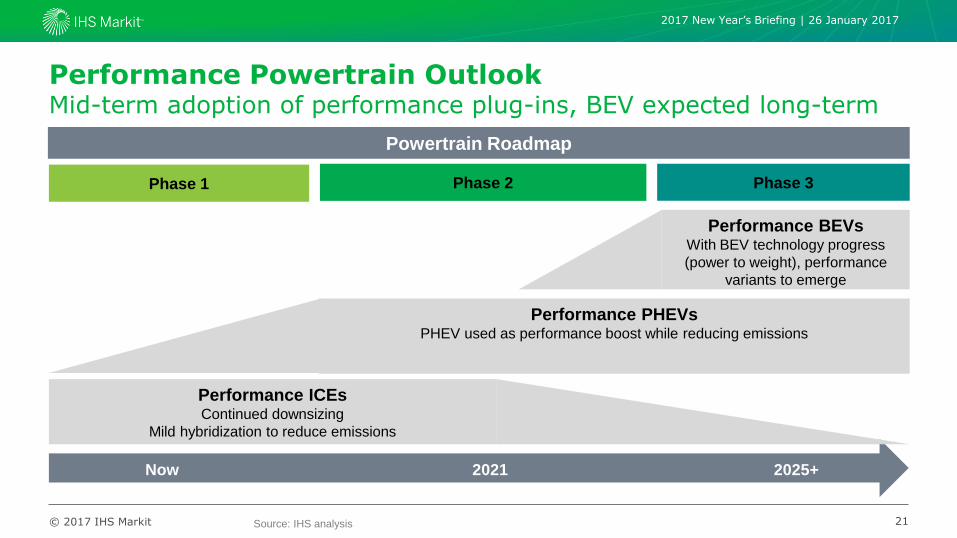

Performance Powertrain Outlook Mid-term adoption of performance plug-ins, BEV expected long-term

21

2017 New Year’s Briefing | 26 January 2017

Phase 1 Phase 2 Phase 3

Now 2021 2025+

Performance ICEs Continued downsizing

Mild hybridization to reduce emissions

Performance PHEVs PHEV used as performance boost while reducing emissions

Performance BEVs With BEV technology progress

(power to weight), performance

variants to emerge

Powertrain Roadmap

Source: IHS analysis

© 2017 IHS Markit

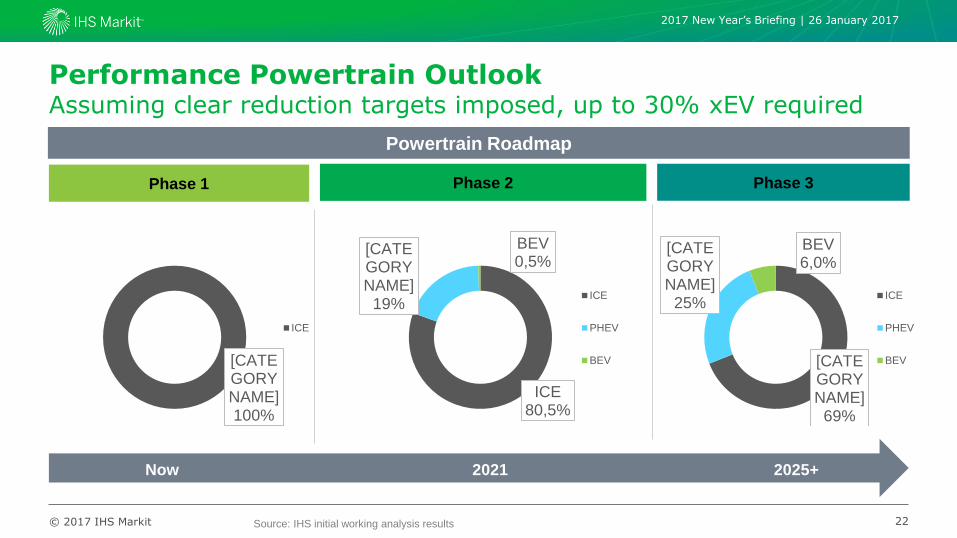

Performance Powertrain Outlook Assuming clear reduction targets imposed, up to 30% xEV required

22

2017 New Year’s Briefing | 26 January 2017

Phase 1 Phase 2 Phase 3

Now 2021 2025+

Performance ICEs

Continued downsizing

Mild hybridization to reduce emissions

Performance PHEVs

PHEV used as performance booster while reducing emissions

Performance BEVs

With BEV technology progress,

performance variants to emerge

Powertrain Roadmap

ICE 80,5%

[CATEGORY NAME]

19%

BEV 0,5%

ICE

PHEV

BEV [CATEGORY NAME]

69%

[CATEGORY NAME]

25%

BEV 6,0%

ICE

PHEV

BEV[CATEGORY NAME] 100%

ICE

Source: IHS initial working analysis results

© 2017 IHS Markit

Summary and Key Takeaways

23

• Expansion of luxury/ premium performance offerings leading to a sizable volume growth forecast.

• US and West Europe remain the key sales markets, China is growing with roomier concepts and lower engine size versions.

• The business is highly profitable, but tightening emission regulation will make the combination of high volume / high emissions an issue.

• Mid-term outlook: Securing traditional high-cylinder ICEs by means of latest fuel saving technology, downsizing and eventually plug-in applications. Understanding competitive measures and conquest vs. cannibalization effects becomes key.

• Long-term outlook: Power oriented plug-ins gaining solid volume share and are a necessity (e.g. China cities). BEV performance variants arriving mid-2020s after required technology progress.

2017 New Year’s Briefing | 26 January 2017

IHS MarkitTM COPYRIGHT NOTICE AND DISCLAIMER © 2017 IHS Markit.

No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS Markit. Content reproduced or redistributed with IHS Markit permission must display IHS Markit legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions and analyses that are based upon it, and to the extent permitted by law, IHS Markit shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially from forecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at your own risk. IHS Markit and the IHS Markit logo are trademarks of IHS Markit.

IHS Markit Customer Care:

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600