automotive industry - ibef · profile of indian automotive industry ... n bajaj auto n hero honda...

TRANSCRIPT

www.ibef.org

AU TO M OT I V E I N D U S T RYOctober 2007

Contents

AUTOMOTIVE INDUSTRYOctober 2007

• Profile of Indian Automotive Industry

• Growth Potential of Indian Automotive Industry

• India as a Manufacturing Hub

www.ibef.org

PROFILE OF INDIAN AUTOMOTIVE INDUSTRY

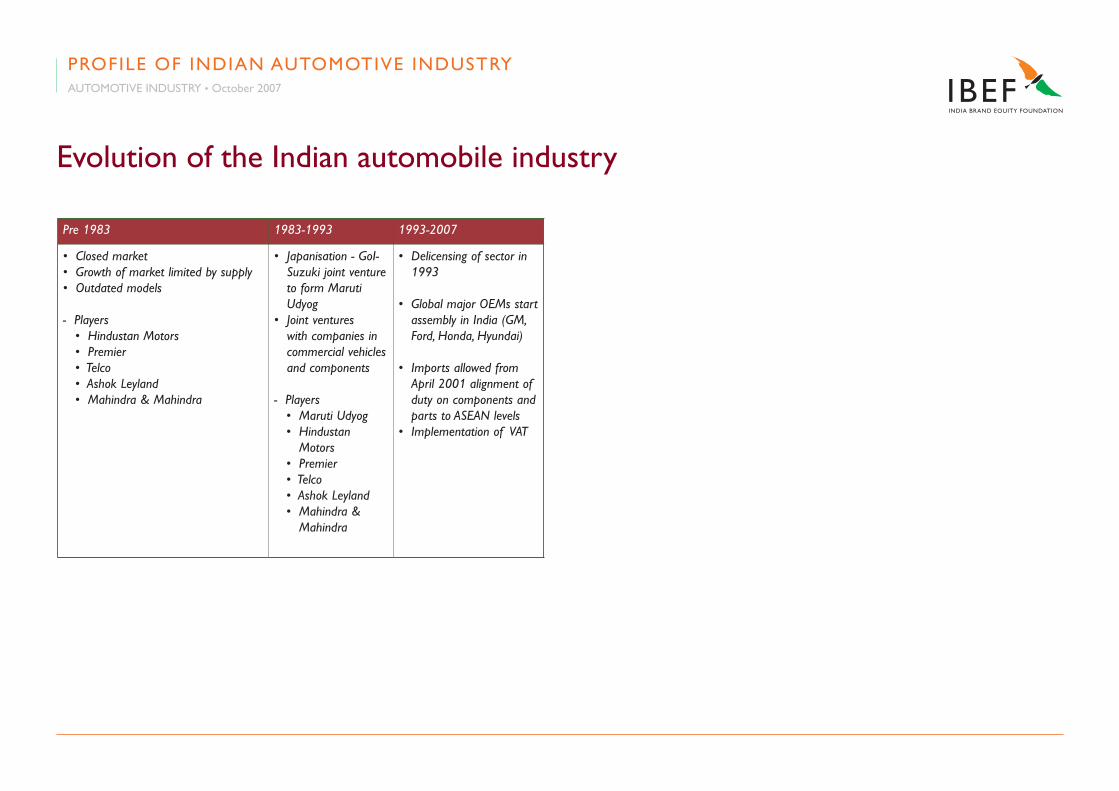

Evolution of the Indian automobile industry

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Pre 1983 1983-1993 1993-2007

• Closed market• Growth of market limited by supply• Outdated models

- Players • Hindustan Motors • Premier • Telco • Ashok Leyland • Mahindra & Mahindra

• Japanisation - GoI-Suzuki joint venture to form Maruti Udyog

• Joint ventures with companies in commercial vehicles and components

- Players • Maruti Udyog • Hindustan

Motors • Premier • Telco • Ashok Leyland • Mahindra &

Mahindra

• Delicensing of sector in 1993

• Global major OEMs start assembly in India (GM, Ford, Honda, Hyundai)

• Imports allowed from April 2001 alignment of duty on components and parts to ASEAN levels

• Implementation of VAT

�India’s�position�in�world��production

• 2nd in two wheelers

• 11th in passenger cars

• 13th in commercial vehicles

• Indian auto industry sales grew to 11.12 billion units in 2006-07, exhibiting an impressive CAGR of 15.5% during the past 5 years

• Two wheelers have the maximum share in the industry by volume, followed by passenger vehicles, three wheelers and commercial vehicles

• Maximum growth has been witnessed in the commercial vehicles segment, followed by three-wheelers

Indian automobile industry crossed a historic landmark of 10 million vehicles in 2006-07

Source: SIAM, IMaCS analysis

Automotive sales (domestic and exports )

CAGR15.5%

5.412002

11.122007

2006

8.532005

7.292004

6.252003

Segment Share in total CAGR

Two wheelers 76.2% 14.5%

Passenger vehicles 14.2% 16.7%

Three wheelers 4.9% 20.5%

Commercial vehicles 4.7% 26.7%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

million units

• Tata Motors• Mahindra & Mahindra• Bajaj Auto• TVS Motors• Hero Honda• Bajaj Tempo• Ashok Leyland

• Bharat Gorge• Sundram Fasteners• Rane Group• Shriram Pistons• RICO Auto• Sona Koyo Steering

Global OEM Indian OEM

Global Suppliers

Indian Suppliers

• GM • Toyota • Ford • Hyundai • Maruti Suzuki • Honda • Skoda• Volvo• Mercedes

• Delphi• Visteon• Bosch• Denso• Valeo• Thyssen Krupp

The OEM as well as the component industry is highly competitive

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• The Indian auto industry is highly competitive with a number of global and Indian auto companies present

• The supplier industry is equally competitive with a mix of global and Indian players

The OEM as well as the component industry is highly competitive

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Most automotive players are present in more than one segment

Manufacturer Segments

Ashok Leyland LCVs, M&HCVs, buses

Asian Motor Works M&HCVs

Atul Auto Three wheelers

Bajaj Auto Two and three wheelers

BMW India Cars and MUVs

Daimler Chrysler India Cars

Eicher Motors LCVs, M&HCVs, buses

Electrotherm India Electric two wheelers

Fiat India Cars

Force Motors Three wheelers, MUVs and LCVs

Ford India Cars and MUVs

General Motors India Cars & MUVs

Hero Honda Motors Two Wheelers

Hindustan Motors Cars, MUVs and LCVs

Honda Two wheelers, cars and MUVS

Hyundai Motors Cars and MUVs

Kinetic Motor Two wheelers

Manufacturer Segments

Mahindra & Mahindra Three wheelers, cars, MUVs, LCVs

Majestic Auto Three wheelers

Maruti Suzuki Cars, MUVs, MPVs

Piaggio Three wheelers, LCVS

Reva Electric Car Co. Electric cars

Royal Enfield Motors Two wheelers

Scooters India Three wheelers

SkodaAuto India Cars

Suzuki Motorcycles Two wheelers

Swaraj Mazda Ltd LCVs, M&HCVSs, buses

Tata Motors Cars, MUVs, LCVs,M&HCVs, buses

Tatra Vectra Motors M&HCVs

Toyota Kirloskar Cars, MUVs

TVS Motor Co Two wheelers

Volvo India M&HCVs, buses

Yamaha Motor India Two wheelers

MUVs: Multi utility vehicles; MPVs: Multi purpose vehicles; LCV: Light commercial vehicles; M&HCVs: Medium and heavy commercial vehicles

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Two wheelers industry is dominated by motorcycles

2003

2002

Domestic two wheeler industry

Source: SIAM, IMaCS Analysis

4.81

4.2 5%

Break up of the industry by segment

n Motorcycles n Scooters n Mopeds

83%

12%

• Scooter/Scooterette : Wheel size less than or equal to 12 inches

• Motorcycle: Wheel size more than 12 inches

• Mopeds: Engine capacity less than 75 cc with fixed transmission, wheel size more than 12 inches

• Electric Two Wheelers: Electrically Driven

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Million units

2004

2007

2006

2005

CAGR13%

5.36

7.86

7.05

6.21

0 1 2 3 4 5 6 7 8

• Domestic two wheeler industry has steadily grown at a CAGR of 13% to reach 7.85 million units in 2006-07

• Motorcycle segment has attained highest growth and dominates the market

• Entry level bikes (engine power below 125 cc and price US$ 850-1,100) account for around 80% sales

• Cost of ownership and economics of operation are key purchase criteria

• Premium bike segment (engine power above 125 cc and price US$ 1,200-2,000) growing at a faster pace as compared to the entry level vehicles, an indication of increasing affluence of users

Two wheelers industry is dominated by motorcycles

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• Scooter segment as a whole has been shrinking, except for the A2 segment

• Bikes having engine capacity 75-125 cc corner the major share of the two wheeler market

• Cost of ownership and economics of operation are most important criteria determining purchase

While the motorcycles segment is growing, the scooter segment is shrinking

Segment Description Share in 2001-02

Share in 2006-07

CAGR

A1 Scooter with engine capacity less than 75 cc

5% 0% -33.9%

A2 Scooter with engine capacity between 75-125 cc

5% 10% 32.9%

A3 Scooter with engine capacity between 125-250 cc

12% 1% -27.7%

B2 Motorcycle�with�engine�capacity�between�75-125�cc

62% 66% 14.9%

B3 Motorcycle�with�engine�capacity�between�125-250�cc

5% 17% 44.8%

B4 Motorcycle with engine capacity above 250 cc

1% 1% 5.7%

C1 Mopeds 10% 5% -2.7%

Segment-wise analysis of two wheeler market

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

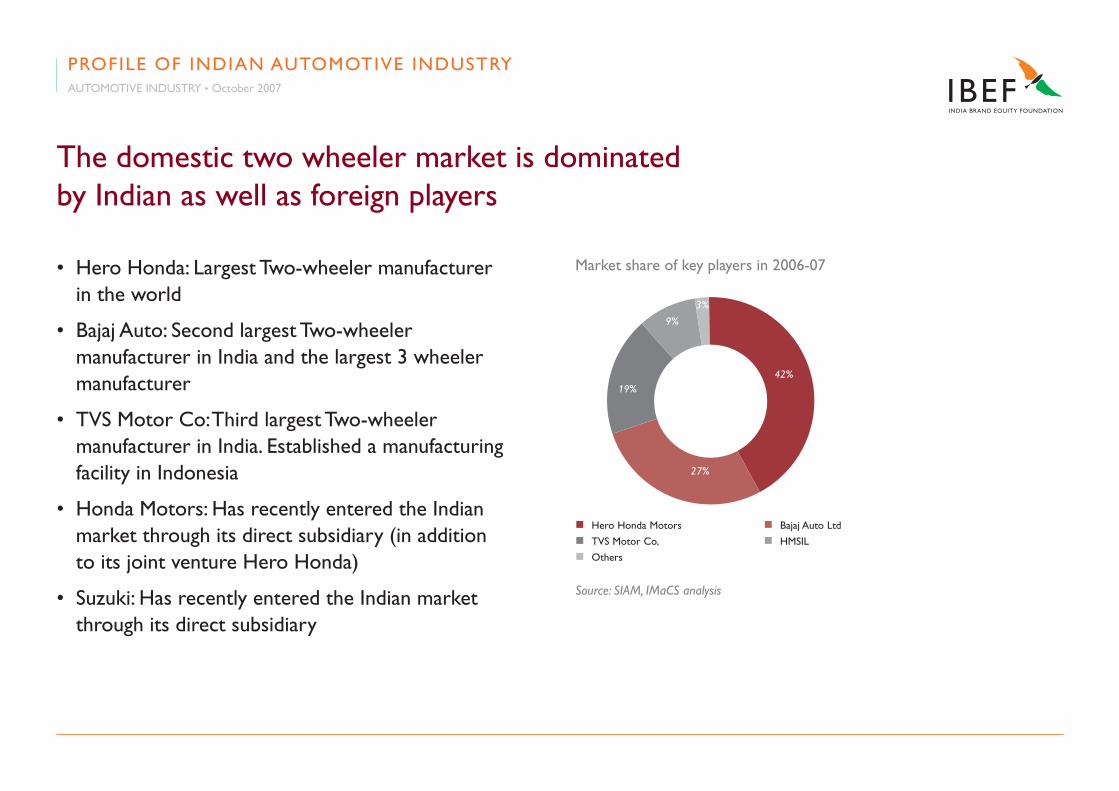

• Hero Honda: Largest Two-wheeler manufacturer in the world

• Bajaj Auto: Second largest Two-wheeler manufacturer in India and the largest 3 wheeler manufacturer

• TVS Motor Co: Third largest Two-wheeler manufacturer in India. Established a manufacturing facility in Indonesia

• Honda Motors: Has recently entered the Indian market through its direct subsidiary (in addition to its joint venture Hero Honda)

• Suzuki: Has recently entered the Indian market through its direct subsidiary

The domestic two wheeler market is dominated by Indian as well as foreign players

Market share of key players in 2006-07

Source: SIAM, IMaCS analysis

n Hero Honda Motors n Bajaj Auto Ltd n TVS Motor Co, n HMSIL

n Others

42%

27%

19%

9%

3%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• In the Two-wheeler market in India, competition is intense with around 10 players competing for the share of the industry

• The players include global giants like Honda, Suzuki, Yamaha as well as Indian players like Bajaj and TVS

• The market leader is Hero Honda Motors, closely followed by Bajaj Auto

• Industry is characterised by frequent new product launches, with over 20 models launched in 2006-07

The domestic two wheeler market is dominated by Indian as well as foreign players

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Two wheelers exports have grown at an impressive CAGR of 42%

Source :SIAM, IMaCS Analysis

Two wheeler exports from IndiaThousand units

16%

10%

Market share of key players in exports 2006-07

Source: SIAM, IMaCS Analysis

n Bajaj Auto n Hero Honda Motors Ltd n TVS Motor Company n Yamaha India

n Others

46%

15%

13%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

CAGR42.8%

104.22002

179.72003

265.12004

366.42005

513.22006

619.22007

0 700100 200 300 400 500 600

(in ‘000 units)

• Exports of two wheelers have grown at over 42% CAGR in last 5 years

• Majority of exports are to Bangladesh, Sri Lanka, Bhutan and Nepal

• Highest growth (CAGR of 57.2%) witnessed in motorcycles segment, which constituted 88% of Two-wheeler market

• Most of the bikes exported were those with engine capacity below 125 cc, indicating preference for Indian made economy bikes

• Bajaj Auto is the market leader in exports with 46% share

Two wheelers exports have grown at an impressive CAGR of 42%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

200 1400800600 1200400 1000

Passenger vehicles segment in India is dominated by cars

Domestic passenger vehicles industry

78%

Source: SIAM, IMaCS Analysis

n Passenger cars n SUVs/MVs

22%

Domestic passenger vehicles industrythousand units

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Source: SIAM, IMaCS Analysis

2002

2003

2004

2005

2006

2007

CAGR15.4%

675.1

707.2

902.1

1061.6

1143.1

1379.7

• The domestic Indian passenger vehicles market has grown at a CAGR of 15.4% over the last 5 years to reach 1.38 million units in 2006-07

• Passenger cars, contributing to 78% of volumes, grew at a CAGR of 16%

• The remaining share is with utility vehicles and sports vehicles

Passenger vehicles segment in India is dominated by cars

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• Maruti Udyog: Largest passenger car manufacturer in the country, India considered as strategic market by Suzuki

• Tata Motors: Largest automotive player in the Indian industry; launching the Rs. 1 lakh (US$ 2,500) car

• Hyundai Motors: Third largest passenger car manufacturer in India, has established India as one of its manufacturing bases in the world

All major global players in passenger vehicles segment have a presence in India

Market shares of key players in 2006-07

Source: SIAM, IMaCS Analysis

n Maruti Udyog Ltd. n Tata Motors Ltd . n Hyundai Motor India Ltd. n Mahindra & Mahindra n Toyota n Others

14%

16%

46%

7%

4%

13%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• Mahindra & Mahindra: Amongst the largest players in the multi utility vehicles segment, has tied up with Renault for manufacturing and marketing of Logan brand of cars in India

• Toyota: Has vision of capturing 10% share of the Indian passenger car market by 2010

• Honda Motors: One of the leading players in the Indian premium cars segment

• Ford: Leading player in the premium cars segment

• General Motors: Leading player in the premium segment; entered the compact car segment recently

All major global players in passenger vehicles segment have a presence in India

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

• There are more than a dozen manufacturers in the industry

• Most of the leading global players have a presence in India in the form of joint ventures or subsidiaries

• The industry leader is Maruti Udyog with 46% market share, closely followed by Tata Motors and Hyundai Motors at 16% and 14% respectively

All major global players in passenger vehicles segment have a presence in India

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

India is increasingly becoming a manufacturing hub for passenger cars

Cars Exports from IndiaThousand units

Market share of key players in Exports 2006-07

Source: SIAM, IMaCS Analysis

n Hyundai Motor India Ltd. n Maruti Udyog n Ford India Pvt Ltd. n Tata Motors

n Others

20%

58%

12%

9%

1%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Source: SIAM, IMaCS Analysis

CAGR30%

53.172002

72.012003

129.292004

166.402005

175.572006

198.482007

0 25 50 75 100 125 150 175 200

• Exports of cars from India have grown at a CAGR of 30% CAGR in the last 5 years to reach 198 thousand units in 2006-07

• Hyundai Motors is the market leader in exports of cars with 68% share; the company uses India as a manufacturing base for compact cars across the globe

• Exports are made to South America, Africa, Europe, Latin America and the Middle East

India is increasingly becoming a manufacturing hub for passenger cars

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Commercial vehicles segment has witnessed the highest growth rate in the automotive industry

Breakup of the Industry by segment

n M & HCV Goods n LCV Goods n M & HCV Passenger n LCV Passenger

53%36%

6%5%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Domestic CV Industry

CAGR26%

146.672002

190.682003

260.112004

318.432005

351.042006

467.882007

0 100 200 300 400 500

Commercial vehicles segment has witnessed the highest growth rate in the automotive industry

• Domestic CV industry sales reached 467.88 thousand vehicles in 2006-07, registering a CAGR of 26% over last 5 yrs

• Share of LCVs is gradually increasing, indicating the emergence of hub and spoke model of transportation

• While the passenger bus industry has seen only a moderate growth, goods industry grew 37% in FY 2006-07

• Goods industry is dominated by multi axle vehicles, which account for nearly 50% of the market

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

CV industry is dominated by Indian players

• Tata Motors Ltd: Largest commercial vehicle manufacturer in the country, has acquired the Korean manufacturer Daewoo Gap Motors

• Ashok Leyland Ltd: Second largest player with considerable market share in M&HCV segment; has formed a JV to manufacture LCVs with Nissan

• Mahindra & Mahindra Ltd: Relatively new player in the segment; has formed JV with International Trucks to manufacture M&HCV trucks in India

• Eicher Motors Ltd: Leading player in the LCV trucks segment; has entered the M&HCV trucks segment recently

• Swaraj Mazda Ltd: One of the leading players in the LCV segment

• Volvo India: One of the leading players in luxury passenger buses and heavy duty tippers

Market Shares of Key Players in 2006-07

Source: SIAM, IMaCS Analysis

n Tata Motors Ltd n Ashok Leyland Ltd n M&M Ltd n Eicher Motors Ltd

n Others

64%

10%

16%

6%4%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

CV industry is dominated by Indian players

• Tata Motors is the market leader in both goods and passenger segments, closely followed by Ashok Leyland

• LCV market is dominated by Tata Motors, followed by Mahindra & Mahindra

• Introduction of Tata Ace has contributed significant growth in the sub 1 tonne segment

• All the players in the segment are in the process of enhancing the capacities and launching new products

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Indian CV exports have witnessed a more impressive growth

CV Exports from IndiaThousand units

Source: SIAM, IMaCS Analysis

Market Share of Key Players in Exports

n Tata Motors n Ashok Leyland n M&M Ltd n Others

6%

11%

71%12%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Source: SIAM, IMaCS Analysis

CAGR33.2%

11.872002

12.262003

17.432004

29.942005

40.602006

49.772007

0 10 20 30 40 50

Indian CV exports have witnessed a more impressive growth

• Exports have grown at a fast pace of over 33% over the last 5 years

• Tata Motors accounts for more than 70% of the CV exports, with Ashok Leyland and Mahindra & Mahindra making up for a large portion of the balance

• LCV goods carriers accounted for 52% of the overall exports

• Major portion of the exports are to Sri Lanka, Gulf countries and Africa

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Growth in three wheelers has been driven by the need for low cost last mile transportation system

Break-up of Industry by segment

Source: SIAM, IMaCS Analysis

n Passenger n Goods

41% 59%

Domestic three wheeler Industry (units)

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Source: SIAM, IMaCS Analysis

CAGR15%

200.282002

231.532003

284.082004

307.862005

359.922006

403.912007

0 500100 200 300 400

Growth in three wheelers has been driven by the need for low cost last mile transportation system

• Three Wheeler sales in India touched a new record of 0.4 Million registering a growth of 15% CAGR over the last 5 years

• The proportion of Goods carriers in the proportion of overall sales has doubled indicating towards the increased need for low cost last mile transportation systems

• Sub 1 tonne segment in Goods accounted for 73% of the sales and Sub Four seater segment in passenger versions accounted for 97% of the sales

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

The three wheeler market is dominated by Bajaj Auto

• Bajaj�Auto�Ltd. : Market leader in the Three wheeler segment, in the process of revamping its product portfolio

• Piaggio�Vehicles : The Italian manufacturer is one of the leading players with fast growing market share, in the process of making India as their global hub

• M&M�Ltd: One of the leading players in the segment

• �Atul�Auto�Ltd: Have introduced new products in the rear engine segment, and also is a manufacturer of ‘Chakda’’ a Three wheeler reengineered from Two wheeler, popular in the western parts of the country

• �Force�Motors�Ltd: A JV between Bajaj Tempo and MAN AG of Germany; leading player in the goods segment

Market Share of Key players 2006-07

Source: SIAM, IMaCS Analysis

n Bajaj Auto n Piaggio Vehicles n M&M n Others

11%

8%

45%

36%

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

The Three wheeler market is dominated by Bajaj Auto

• Bajaj Auto emerged the leader in Three Wheeler industry with 45% share, closely followed by Piaggio with 36% share

• Bajaj Auto lead the passenger carrier segment with 58% share, while Piaggio lead the goods segment with 40% market share

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

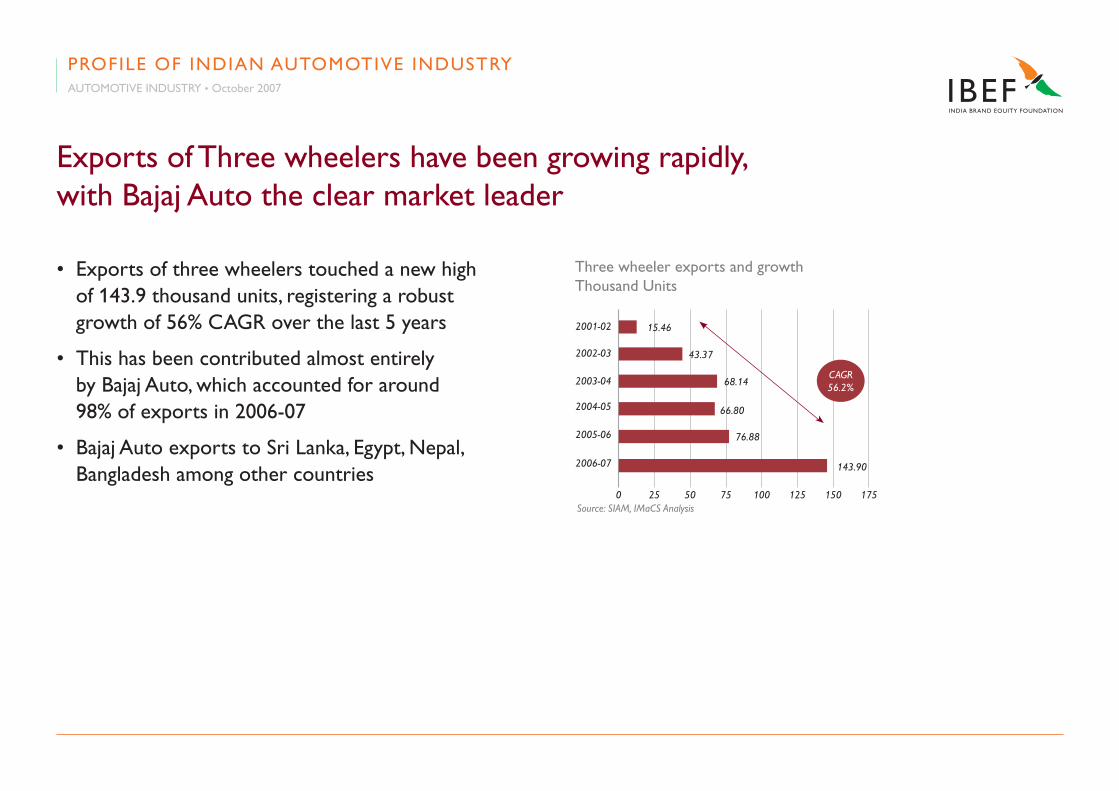

Exports of Three wheelers have been growing rapidly, with Bajaj Auto the clear market leader

• Exports of three wheelers touched a new high of 143.9 thousand units, registering a robust growth of 56% CAGR over the last 5 years

• This has been contributed almost entirely by Bajaj Auto, which accounted for around 98% of exports in 2006-07

• Bajaj Auto exports to Sri Lanka, Egypt, Nepal, Bangladesh among other countries

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Three wheeler exports and growthThousand Units

175Source: SIAM, IMaCS Analysis

CAGR56.2%

15.462001-02

43.372002-03

68.142003-04

66.802004-05

76.882005-06

143.902006-07

0 150125100755025

Indian OEM Foreign Partner Type of Partnership

Maruti Suzuki Suzuki Motor Corporation- Japan Equity partner

Mahindra Logan Renault Joint Venture

Tata motors Fiat Tie-up for manufacturing and marketing in India

KINETIC Group Sanyang Industry Co Ltd (SYM- Taiwan

Technology

Italjet -Italy Tie-up for manufacturing and distribution

Hero Honda- Japan Technology

Hero Cycles Ultra Motor Company, U.K Technology

Bajaj Auto Kawasaki Heavy Industries Ltd, Japan

Engine Technology

Engine Technology Technology

Kubota Corp, Japan Technology

L&T Ltd Scania-Spain Tie-up for marketing in India

Ashok Leyland Hino-Japan Engine Technology

Irizar-Spain Bus body Technology

ZF-Germany Gearbox Technology

Tata Motors Marco Polo-Brazil Bus/Coach Technology

Cummins-USA Engine Technology

Indian firms are increasingly partnering with foreign firms

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Three major automotive clusters exist in India

• Major automotive clusters - Mumbai-Pune-Nasik-Aurangabad (West), Chennai-Bangalore-Hosur (South) and Delhi-Gurgaon-Faridabad (North)

• Export oriented companies have formed base in the West/South regions, due to proximity to ports

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Three major automotive clusters exist in India

North�/�Central

• Ashok Leyland • Eicher

• Force Motors • Hero Honda

• Hindustan Motors • Honda

• Honda SIEL • ICML

• Kinetic • LML

• Majestic • Maruti Suzuki

• Piaggio • Yamaha

• Swaraj Mazda • Tata Motors

East

• Hindustan Motors

• Tata Motors

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Delhi-Gurgaon-Noida-Ghaziabad

Kolkata

Jamshedpur

Chennai Bangalore Hosur

Ludhiana

Haridwar

Pitampur

Three major automotive clusters exist in India

West

• Ashok Leyland • Atul Auto

• Bajaj Auto • Daimler Chrysler

• FIAT • Force Motors

• GM • Greaves

• Kinetic • M & M

• Piaggio • Premier

• Skoda • Tata Motors

Delhi-Gurgaon-Noida-Ghaziabad

Kolkata

Jamshedpur

Chennai Bangalore Hosur

Ludhiana

Haridwar

Pitampur

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Three major automotive clusters exist in India

South

• Ashok Leyland • Enfield

• Ford • Greaves

• Hindustan Motors • Hyundai

• Mahindra & Mahindra

• Tatra • Volvo

• Toyota Kirloskar • TVS Motors

Delhi-Gurgaon-Noida-Ghaziabad

Kolkata

Jamshedpur

Chennai Bangalore Hosur

Ludhiana

Haridwar

Pitampur

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Indian Auto Policy is designed for supporting the growth of the industry

• Government’s intention on harmonizing the regulatory standards with the rest of world

• Investment Incentives by the Local State Governments: Most States Customise incentives for Large Investments

• Automatic Approval for Foreign equity investment up to 100%

• No Minimum Investment Criteria

• Weighted Tax Deduction up to 150% for in-house research and R&D activities

Indian Auto Policy 2002 CONCERN FOR EMISSIONS

INVESTMENT INCENTIVES

LOWENTRYBARRIER

EMPHASIS ON R&D

Source: ARAI, IMaCS Analysis

In 2002, the Indian Government formulated an Auto Policy aimed at promoting an integrated, phased enduring and self-sustained growth of the industry

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Indian automotive regulations are in the process of being aligned with European regulations

• Indian automotive regulations are closely aligned to the ECE regulations. The diagram below depicts the level of alignment of the Indian regulations with the ECE regulations

• The key regulations that are likely to impact the auto industry and create the need for world class products in the future are crash related regulations and introduction of Bharat Stage IV norms

Source: ARAI, IMaCS Analysis

0

2007

50 100 122

81 21 20

n Fully/ Partially Allign n In Process of Being Alignedn Items/ Regulations to be covered

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Safety and emission related regulations in India - Achievements and Plans

NCR and 10 Major Cities

NCR and 10 Major Cities

Entire Country

NCR and 3 Major Metros

NCR and 10 Major Cities

Entire Country

Entire Country

Achievements Till Date Plan

Emission Regulations

2000 2001 2003 2005 2010

EURO - IV

EURO - III

EURO - II

EURO - I

Safety Regulations

• Brakes•Steering effort•Gradeability•Installation of mirror, Horn & Lighting devices•Rear Under run Protective Devices (RUPD) Lateral Protective Devices (LPD)•Safety belt•Electro Magnetic Interference (EMI)•Wiping system•Rear View Mirror etc

• Anti Brake Skid –2007 • Truck cab occupant protection -Crash

• Super structure of bus.•Airbags • Electro Magnetic Compa-

tibility (EMC) • Front Under run protecti-

ve Devices (FUPD)

Source: ARAI, IMaCS Analysis

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

The Government of India has taken a strong initiative to strengthen automotive related R&D infrastructure

Rae Bareilly Centre

Complete homologation services to Agri Tractors, Off road Vehicles , Gensets as per Indian or Global standards & Driver Training centre

Center of Excellence For Accident Data Analysis

Commissioning Schedule Phase-I : July 2010; Phase-II :Aug 2010

Ahmednagar-VRDE Up-Gradation

Research, Design, Development and Testing of Vehicles

Centre of Excellence For Photometry, EMC, EMI,Test Tracks

Commissioning Schedule Phase-I : July 2010; Phase-II :Aug 2010

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

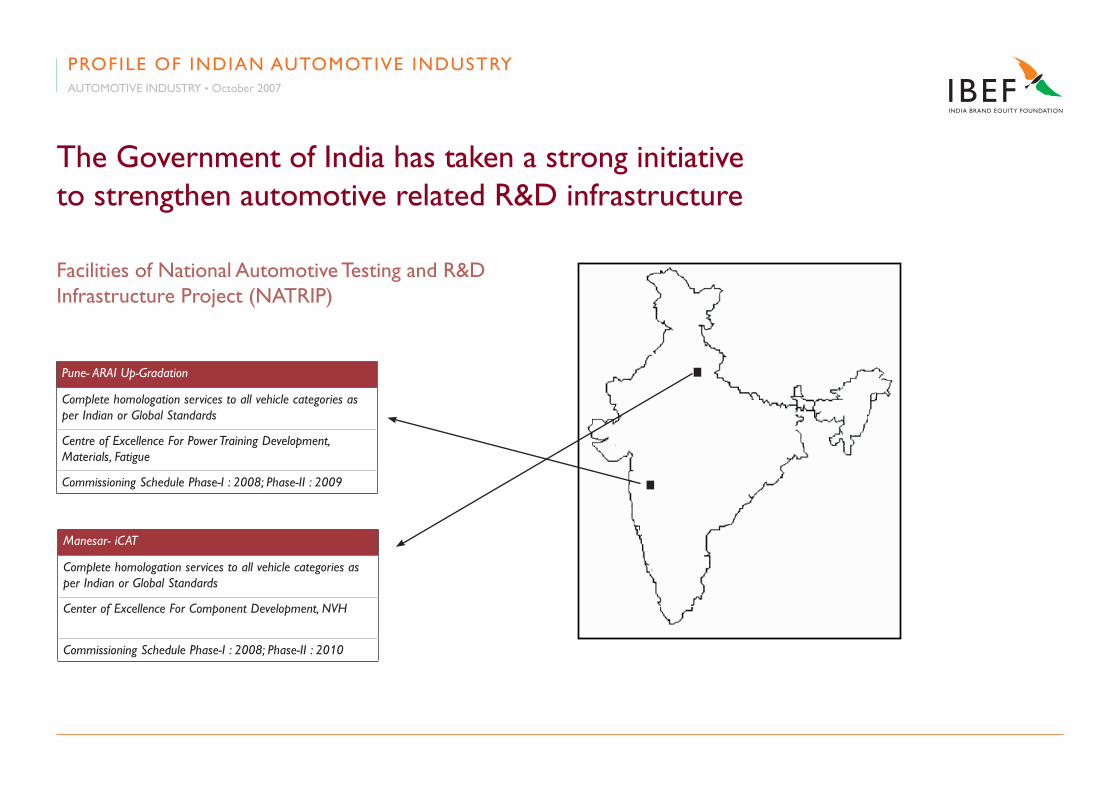

Facilities of National Automotive Testing and R&D Infrastructure Project (NATRIP)

The Government of India has taken a strong initiative to strengthen automotive related R&D infrastructure

Pune- ARAI Up-Gradation

Complete homologation services to all vehicle categories as per Indian or Global Standards

Centre of Excellence For Power Training Development, Materials, Fatigue

Commissioning Schedule Phase-I : 2008; Phase-II : 2009

Manesar- iCAT

Complete homologation services to all vehicle categories as per Indian or Global Standards

Center of Excellence For Component Development, NVH

Commissioning Schedule Phase-I : 2008; Phase-II : 2010

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

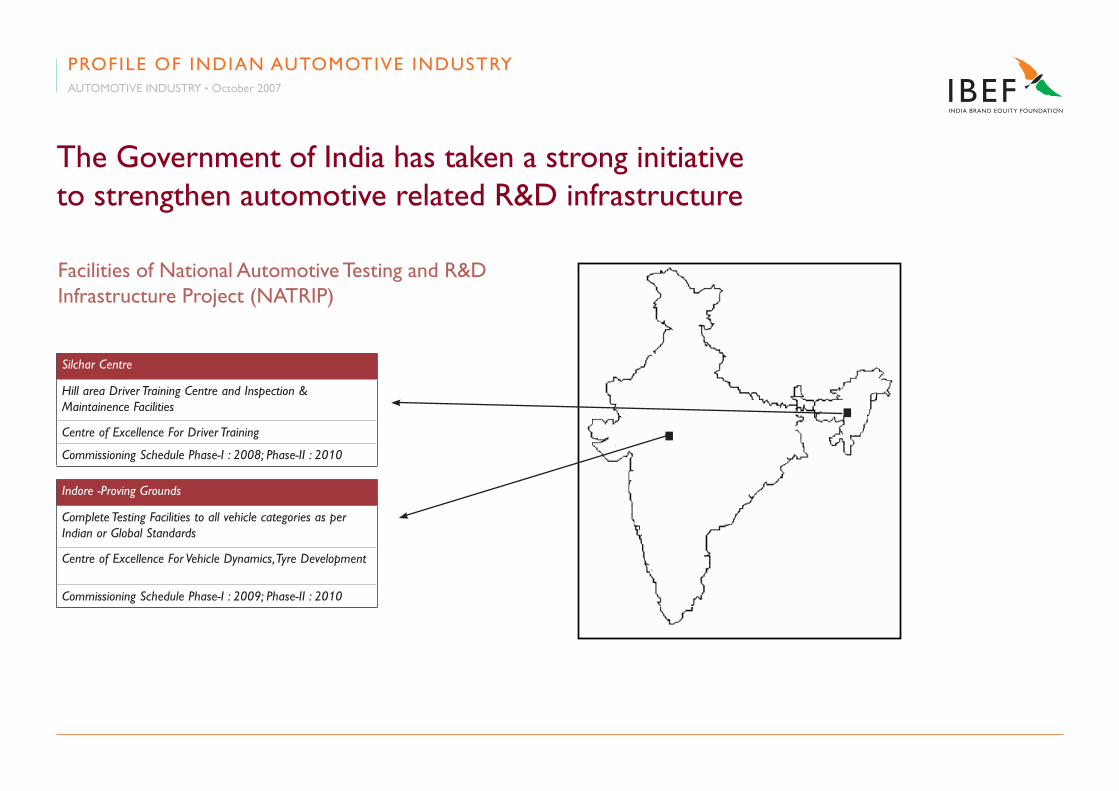

Facilities of National Automotive Testing and R&D Infrastructure Project (NATRIP)

The Government of India has taken a strong initiative to strengthen automotive related R&D infrastructure

Silchar Centre

Hill area Driver Training Centre and Inspection & Maintainence Facilities

Centre of Excellence For Driver Training

Commissioning Schedule Phase-I : 2008; Phase-II : 2010

Indore -Proving Grounds

Complete Testing Facilities to all vehicle categories as per Indian or Global Standards

Centre of Excellence For Vehicle Dynamics, Tyre Development

Commissioning Schedule Phase-I : 2009; Phase-II : 2010

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Facilities of National Automotive Testing and R&D Infrastructure Project (NATRIP)

The Government of India has taken a strong initiative to strengthen automotive related R&D infrastructure

Chennai Centre

Complete homologation services to all vehicle categories as per Indian or Global Standards

Center of Excellence For Infotronics,EMC,Passive Safety

Commissioning Schedule Phase-I : 2008; Phase-II : 2011

PROFILE OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Facilities of National Automotive Testing and R&D Infrastructure Project (NATRIP)

www.ibef.org

GROWTH POTENTIAL OF INDIAN AUTOMOTIVE INDUSTRY

Growth drivers for the Indian automotive industry

GROWTH POTENTIAL OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

Increasing consumer demand

New productslaunches

Indian Automotive Industry

Government Policies

- Contemporary products- Shorter life cycle

- Export competitiveness- Reduced cost to consumer - India emerging as a manufacturing hub

- Overall economic growth - Lower duties and taxes

- Growth in income levels- Easier financing

Cost Competiveness

Indian Automotive Mission Plan – Vehicle sales expected to grow to 32 million by 2015-16

• The size of the Indian automotive industry is expected to grow at 13% p.a over the next decade to reach around US$ 120-159 billion by 2016

• The total investments required to support the growth are estimated at around US$ 35-40 billion

• The Two wheelers industry is expected to lead the growth, with an estimated sales of 27.8 million units by 2016

• Total export in the automotive sector would be around US$ 30-5 billion, of which component exports would account for US$ 20-25 billion and vehicle exports for the rest

Potential vehicle sales in India (2015-16)million units

0.64

Total

Three

Wheelers

Two

wheelers

CVs

Cars

Source: SIAM, ACMA, AMP Vision & IMaCS Analysis

GROWTH POTENTIAL OF INDIAN AUTOMOTIVE INDUSTRYAUTOMOTIVE INDUSTRY • October 2007

www.ibef.org

INDIA AS A MANUFACTURING HUB

Automotive exports have grown at an impressive CAGR of 40% in the last 5 years

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

• Indian automotive exports have grown at a high CAGR of 40.5% over the last 5 years, with fastest growth in Three wheeler segment, followed by Two wheelers

• India is increasingly becoming a manufacturing hub of small cars for global majors

Automotive Exports (thousand units)

Source: SIAM, IMaCS Analysis

CAGR40.5%

184.682002

307.312003

479.922004

629.542005

806.222006

1011.282007

0 200 400 600 800 1000 1200

Global auto companies are taking advantage of India’s manufacturing base

• Hyundai Motors - 36% of its production is exported to 67 countries. Hyundai has shifted its entire production of the Atos Prime, its compact model, to its Chennai Plant. Similar plan is on the cards for Getz. Hyundai is planning to double the production capacity to 0.6 million cars, primarily to meet export demand

• Suzuki Motor Corp: It is investing US$ 2 billion in India, and plans to export 200,000 cars from India by 2010

• Ford Motor Co: It exports 58% of the total production from India

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Global auto companies are taking advantage of India’s manufacturing base

• Tata Motors: The company plans to make its US$ 2,500 car available in other markets. It is setting up showrooms across Africa and has tied up with Italy’s Fiat to use its South American sales network

• Nissan Motor: Has recently announced plans to make cars in India and export them to Europe

• Honda Motor: Has begun building a new plant for premium hatchbacks in western India

• Toyota: Has set us a transmission plant in India to meet its regional demand

Source: Industry News

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Proven product developmental capabilities- More than 125 Fortune 500 (including

large auto companies) have R&D cen-tres in India

- Companies can leverage India’s acknow-ledged leadership in the IT industry

Proximity to Markets- Proximity to other Asian economies - Proximity to the emerging markets like

Africa- Shipments to Europe are cheaper than

those from Brazil and Thailand

High quality standards- 9 Indian component manufacturers have

won the Deming Award for quality- Most leading component manufacturers

are QS and ISO certified

Competitive manufacturing cost- Skilled labour costs amongst the lowest

in India

Export Potential- Total value of exports by 2015 expected

to reach US$ 8–10 billion for vehicles and US$ 20–25 billion for components

Availability of Manpower- 0.4 million Engineering graduates pass

out every year- 7 million enter workforce every year

Large and growing domestic demand- Demand growth of 14% CAGR makes

India one of the fastest growing markets

Stable economic policies- Continuity in economic reforms

and policies related to investments

India as an Auto

Hub

Several factors make India a favourite investment destination

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Competitiveness of Indian automotive manufacturing

In order to emerge as a manufacturing hub, India would face competition from other low cost countries such as

• China

• Thailand

• Brazil

IMaCS has compared the cost competitiveness of automotive (car and CV compared separately) manufacturing in India with respect to these countries in terms of factors like

• Taxes and duties

• Cost of manufacturing (for example, power and fuel costs, labour costs, including productivity interest rates)

• Economies of scale

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Competitiveness of Indian automotive manufacturing

Competitiveness of manufacturing in India can be improved by reducing the level of taxes and the cascading impact of taxes and by improving the business infrastructure

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

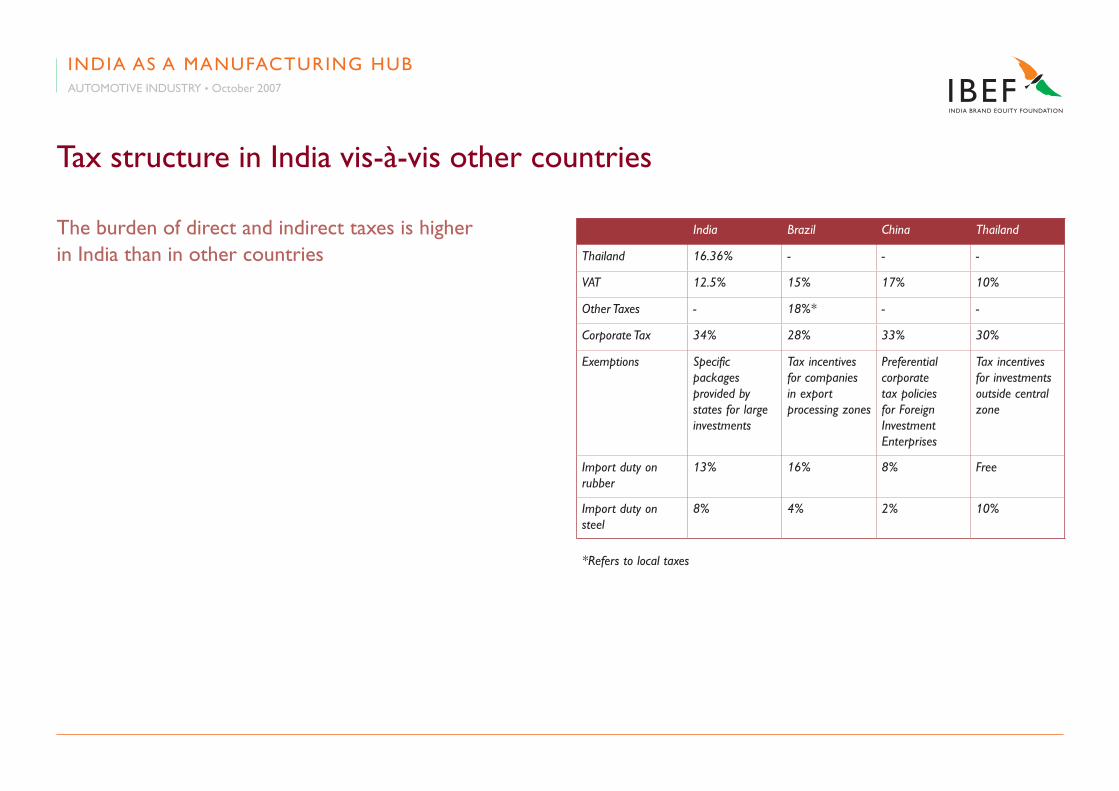

Tax structure in India vis-à-vis other countries

The burden of direct and indirect taxes is higher in India than in other countries

India Brazil China Thailand

Thailand 16.36% - - -

VAT 12.5% 15% 17% 10%

Other Taxes - 18%* - -

Corporate Tax 34% 28% 33% 30%

Exemptions Specific packages provided by states for large investments

Tax incentives for companies in export processing zones

Preferential corporate tax policies for Foreign Investment Enterprises

Tax incentives for investments outside central zone

Import duty on rubber

13% 16% 8% Free

Import duty on steel

8% 4% 2% 10%

*Refers to local taxes

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Labour & Labour Productivity in India vis-a-vis other countries

• India compares favourably with other low cost countries in productivity adjusted labour cost

• Indian labour productivity in the manufacturing sector is on an increase with the application of production management techniques and many companies have doubled their productivity in last 5 years

India Brazil China Thailand

Labour cost (US$/hour) 0.7 4.1 0.7 0.72

Labour cost (US$/day)* 5.6 32.8 5.6 5.76

Productivity index** 1.0 2.0 1.0 1.2

Productivity adjusted labour cost (US$/day)

5.6 16.4 5.6 4.8

*Assuming 8 hour shift per day** Gross value added per person employed when compared to India

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Power Cost in India vis-à-vis other countries

• Power cost in India is the highest amongst the competing countries

• However, power cost accounts for around 3% of the overall cost structure, hence not a significant disadvantage

• Power costs in India varies by state and is as low as US$ 0.1 in states like Maharashtra

• With privatisation and competition in the emerging Indian power sector, cost of power is expected to come under control

• Interest rates in India are high as compared to competing countries, but expected to soften in the future

Country Cost per kwh (US$)

India 0.14

Brazil 0.05

China 0.03

Thailand 0.11

Power costs

Country Annual lending interest rate

India 10-11%

Brazil 14-16%

China 5-6%

Thailand 7-8%

Interest costs

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

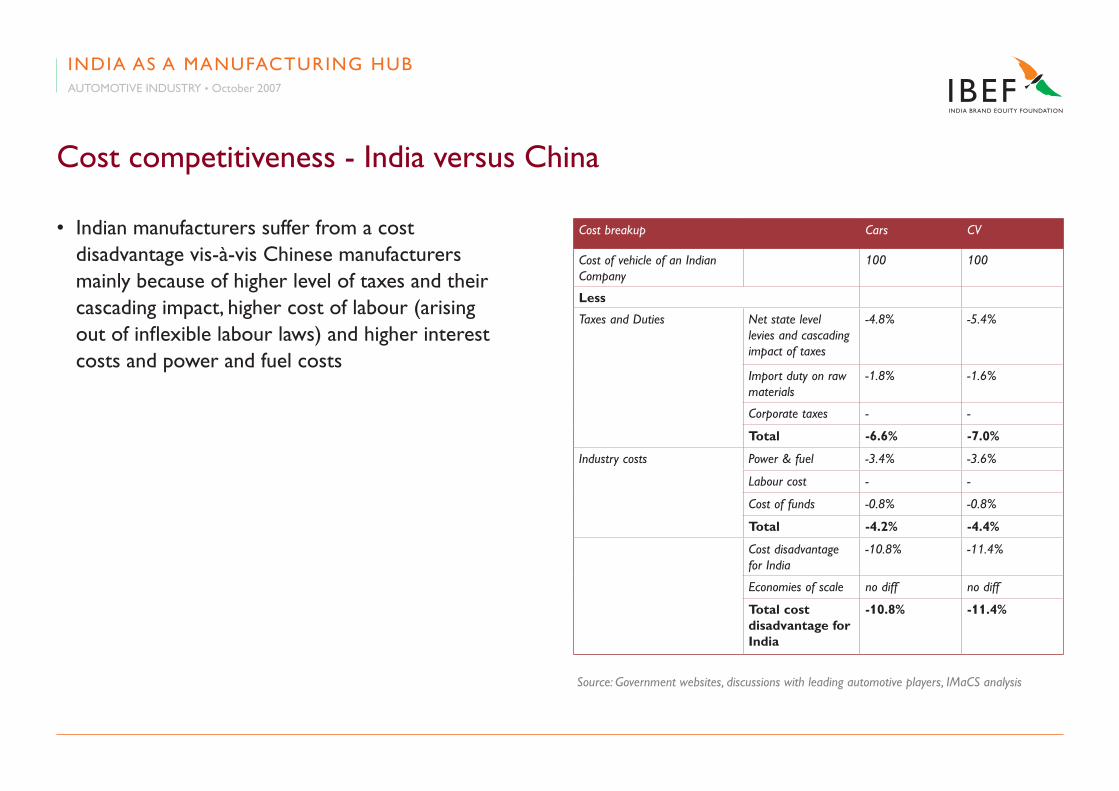

Cost competitiveness - India versus China

• Indian manufacturers suffer from a cost disadvantage vis-à-vis Chinese manufacturers mainly because of higher level of taxes and their cascading impact, higher cost of labour (arising out of inflexible labour laws) and higher interest costs and power and fuel costs

Cost breakup Cars CV

Cost of vehicle of an Indian Company

100 100

Less

Taxes and Duties Net state level levies and cascading impact of taxes

-4.8% -5.4%

Import duty on raw materials

-1.8% -1.6%

Corporate taxes - -

Total -6.6% -7.0%

Industry costs Power & fuel -3.4% -3.6%

Labour cost - -

Cost of funds -0.8% -0.8%

Total -4.2% -4.4%

Cost disadvantage for India

-10.8% -11.4%

Economies of scale no diff no diff

Total�cost�disadvantage�for�India

-10.8% -11.4%

Source: Government websites, discussions with leading automotive players, IMaCS analysis

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Cost competitiveness - India versus Thailand

• Indian vehicle manufacturers have a cost disadvantage vis-à-vis Thai vehicle manufacturers, primarily due to higher level of taxes in India

• However, the large market potential of the Indian market more than makes up for this disadvantage

Cost Break-up Cars CV

Cost of vehicle of an Indian Company

100 100

Less

Taxes and Duties Net state level levies and cascading impact of taxes

-5.61% -5.86%

Import duty on raw materials

-0.60% -0.20%

Corporate taxes -0.20% -0.20%

Total -6.41% -6.26%

Industry costs Power & fuel -1.03% -1.11%

Labour cost -1.28% -1.56%

Cost of funds -0.36% -0.36%

Total -2.67% -3.03%

Cost disadvantage for India

-9.08% -9.29%

Economies of scale no diff no diff

Total�cost�disadvantage�for�India

-9.08% -9.29%

Source: Government websites, discussions with leading automotive players, IMaCS Analysis

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Cost Competitiveness - India versus Brazil

• India is competitively positioned vis-à-vis Brazil in cars as well as CV

• India enjoys greater scale advantage as compared to Brazil in the case of cars as capacity utilisation in India is better, despite Brazil having larger installed capacities

Cost Break-up Cars CV

Cost of vehicle of an Indian Company

100 100

Less

Taxes and Duties Net state level levies and cascading impact of taxes

-3.1% -3.9%

Import duty on raw materials

- -

Corporate taxes - 0.1% - 0.1%

Total -3.2% �-4.0%

Industry costs Power & Fuel - 2.0% - 2.8%

Labour cost 7.6% 16.2%

Cost of funds 0.9% 1.6%

Total 6.5% 15.0%

Cost advantage for India

3.3% 11.0%

Economies of scale 8.3% no diff

Total�cost�advantage�for�India

11.6% 11.0%

Source: Government websites, discussions with leading automotive players, IMaCS Analysis

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Conclusions

• India has a cost advantage when compared to Brazil

• However, India suffers from a cost disadvantage vis-à-vis China and Thailand, primarily due to high level of taxes and their cascading impact

• India, in the near future is expected to go ahead with the abolition of interstate Central Sales Tax (CST), which will reduce the cascading impact of taxes to some extent

INDIA AS A MANUFACTURING HUBAUTOMOTIVE INDUSTRY • October 2007

Conclusions

• Implementation of Goods & Services tax (along the lines of VAT) and abolition of all other taxes by 2010 is under consideration, which will reduce the taxation loading on the automotive sector considerably. This step is expected to strengthen India’s future position as a leading automobile manufacturing hub

• Various steps being taken by the Indian government in improving infrastructure would reduce the disadvantage that India suffers from because of poor infrastructure that causes project delays, delays in deliveries and so on. This would increase the demand for road transportation in the country

AUTOMOTIVE INDUSTRYOctober 2007

This presentation has been prepared jointly by the India Brand Equity Foundation (“IBEF”) and ICRA Management Consulting Services Limited, IMaCS (“Authors”).

All rights reserved. All copyright in this presentation and related works is owned by IBEF and the Authors. The same may not be reproduced, wholly or in part in any material form (including photocopying or storing it in any medium by electronic means and whether or not transiently or incidentally to some other use of this presentation), modified or in any manner communicated to any third party except with the written approval of IBEF.

This presentation is for information purposes only. While due care has been taken during the compilation of this presentation to ensure that the information is accurate to the best of the

Author’s and IBEF’s knowledge and belief, the content is not to be construed in any manner whatsoever as a substitute for professional advice.

The Author and IBEF neither recommend or endorse any specific products or services that may have been mentioned in this presentation and nor do they assume any liability or responsibility for the outcome of decisions taken as a result of any reliance placed in this presentation.

Neither the Author nor IBEF shall be liable for any direct or indirect damages that may arise due to any act or omission on the part of the user due to any reliance placed or guidance taken from any portion of this presentation.

DISCLAIMER

www.ibef.org

AUTOMOTIVE INDUSTRYOctober 2007