automotive battery committee european starter...

TRANSCRIPT

Automotive Battery Committee

European Starter Battery Market 2012-2016

Johann-Friedrich Dempwolff

Johnson Controls EMEA

EUROBAT AGM - Rome

June 7, 2013

1. Automotive Battery Market Volumes 2012 - 2016

2

2. Automotive Sector : Market figures

3. Automotive Sector: Trends

Automotive Battery Committee - June 2013

Agenda

Automotive Battery Market Volumes 2012 - 2016

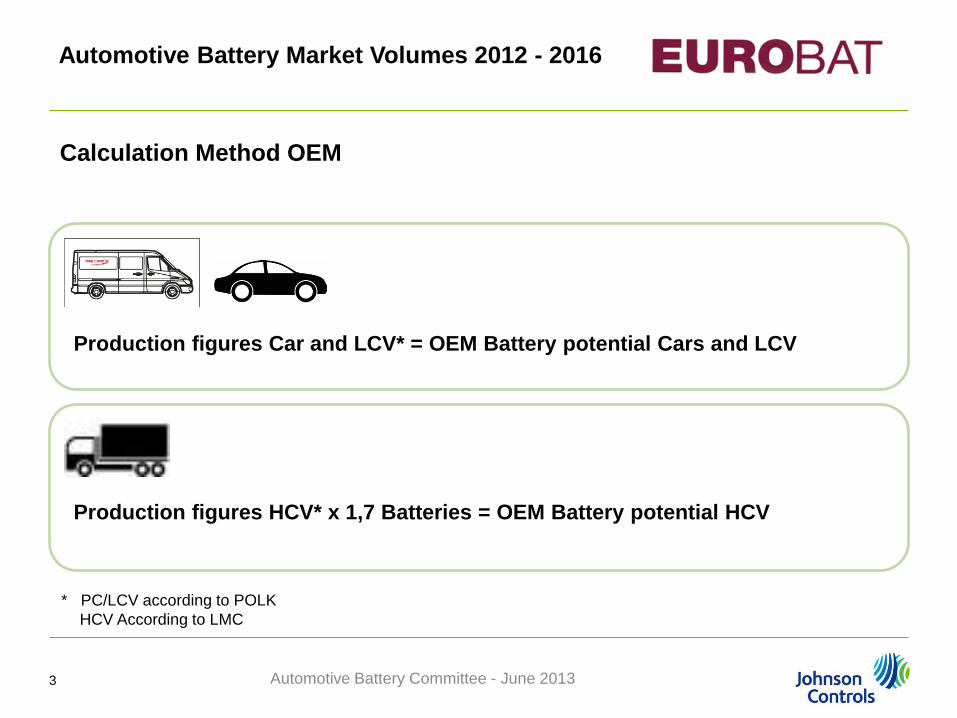

* PC/LCV according to POLK

HCV According to LMC

Calculation Method OEM

Production figures Car and LCV* = OEM Battery potential Cars and LCV

Production figures HCV* x 1,7 Batteries = OEM Battery potential HCV

Automotive Battery Committee - June 2013 3

467 489 492 553 602

17.007 16.595 17.674 19.005 19.365

17.474 17.084 18.166

19.557 19.968

2012 2013 2014 2015 2016

HCV CARS + LCV

PC/LCV according to POLK

HCV According to LMC

Vehicle Production Europe* 2012-2016 (in m units)

Automotive Battery Market Volumes 2012 - 2016

Automotive Battery Committee - June 2013 4

PC/LCV according to POLK

HCV According to LMC

5.753 5.673 5.748 5.815 5.829

1.942 2.084 2.261 2.522 2.585

1.981 1.832 2.073 2.031 1.929

1.575 1.574 1.663 1.776 1.857 769 667 799

1.087 1.109 12.019 11.830

12.545 13.232 13.308

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2012 2013 2014 2015 2016

Germany Spain France UK Italy

Vehicle Production per country 2012-2016 (in m units)

BIG-5 countries W. EU

Automotive Battery Market Volumes 2012 - 2016

Automotive Battery Committee - June 2013 5

PC/LCV according to POLK

HCV According to LMC

1.051 1.065 1.207 1.248 1.367

646 521 479 756

1028 1107 1012 1074

1237 1221

795 827 844

882 850

228 289 395

417 422

341 387 392

402 392

4.167 4.100 4.391 4.943

5.281

0

1.000

2.000

3.000

4.000

5.000

6.000

2012 2013 2014 2015 2016

TR PL CZ SK HU RO

Vehicle Production per country 2012-2016 (in m units)

BIG-6 countries E. EU

Automotive Battery Market Volumes 2012 - 2016

Automotive Battery Committee - June 2013 6

* Source: POLK

** Source: GIPA

Car park figures Car and LCV*

Battery replacement rate

per country (in %) **

= AM Battery potential Cars and LCV

Calculation Method Aftermarket Battery Potential

X

Automotive Battery Market Volumes 2012 - 2016

Automotive Battery Committee - June 2013 7

Replacement calculation

Replacement rate historical (up to 2012):

Evaluation of the replacement rate is provided by end consumer market

research (GIPA)

Main European countries (D,UK,ES,FR,IT,PL,CZ,H,RO,SLO,SK) are covered

by individual market studies. For the other countries a weighted average is

taken.

Replacement rate development (2013-2016):

Three different scenarios are build up , based on following presumptions:

Declining

Stable

Average

Automotive Battery Market Volumes 2012 - 2016

Automotive Battery Committee - June 2013 8

* Source: POLK

** Assumptions: Battery Lifespan = 3 years; average number ob Batteries per vehicle = 1,7

Calculation Method Aftermarket Battery Potential

Car park figures HCV*

Battery Lifespan (3 years)**

X 1,7** = AM Battery potential HCV

Automotive Battery Committee - June 2013 9

Automotive Battery Market Volumes 2012 - 2016

4.147 4.190 4.243 4.306 4.370

40.736 40.780 41.065 41.476 42.094

44.883 44.970 45.309 45.782 46.464

2012 2013 2014 2015 2016

HCV CARS + LCV

After market battery volume* 2012-2016 (in m Units)

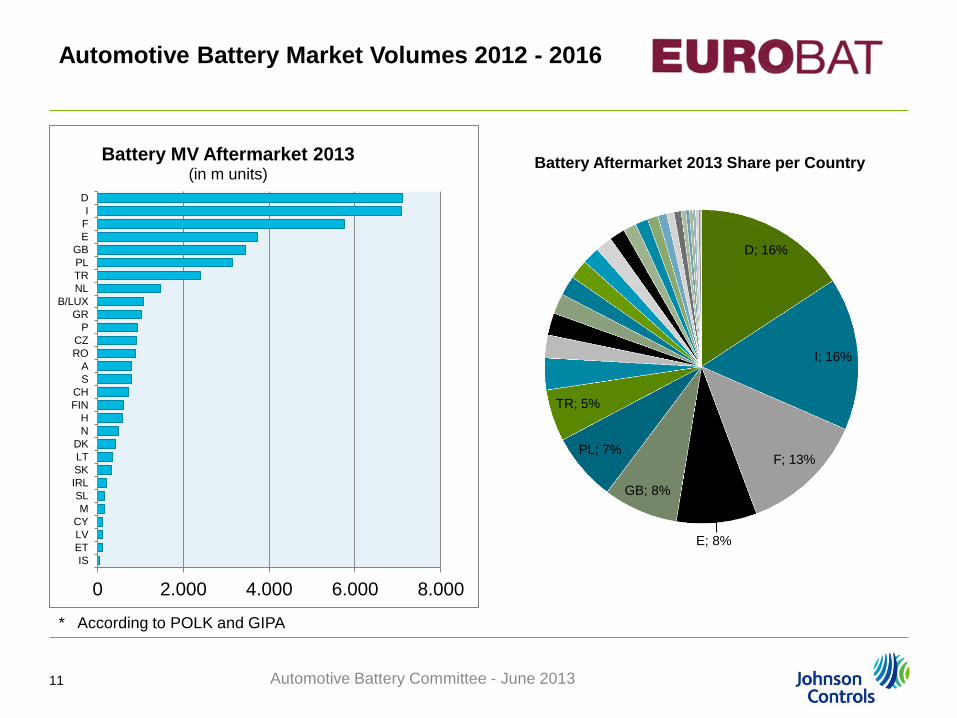

* According to POLK and GIPA

Automotive Battery Committee - June 2013 10

Automotive Battery Market Volumes 2012 - 2016

* According to POLK and GIPA

0 2.000 4.000 6.000 8.000

IS

ET

LV

CY

M

SL

IRL

SK

LT

DK

N

H

FIN

CH

S

A

RO

CZ

P

GR

B/LUX

NL

TR

PL

GB

E

F

I

D

Battery MV Aftermarket 2013 (in m units)

D; 16%

I; 16%

F; 13%

E; 8%

GB; 8%

PL; 7%

TR; 5%

Battery Aftermarket 2013 Share per Country

Automotive Battery Committee - June 2013 11

Automotive Battery Market Volumes 2012 - 2016

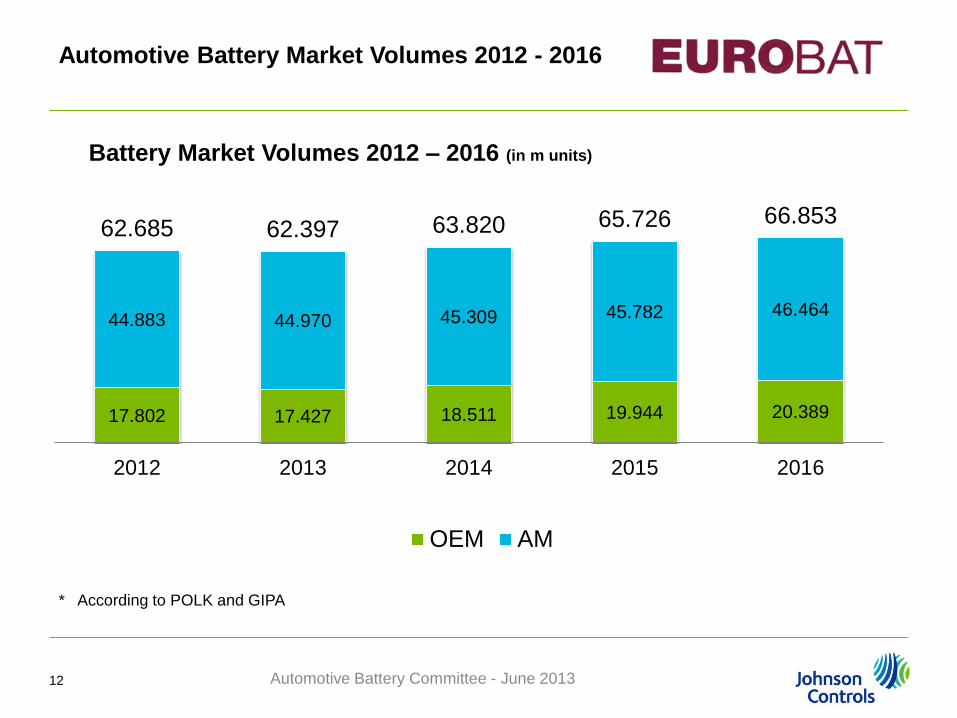

17.802 17.427 18.511 19.944 20.389

44.883 44.970 45.309 45.782 46.464

62.685 62.397 63.820 65.726 66.853

2012 2013 2014 2015 2016

OEM AM

Battery Market Volumes 2012 – 2016 (in m units)

* According to POLK and GIPA

Automotive Battery Committee - June 2013 12

Automotive Battery Market Volumes 2012 - 2016

1. Automotive Battery Market Volumes 2012 - 2016

13

2. Automotive Sector : Market figures

3. Automotive Sector: Trends

Automotive Battery Committee - June 2013

Agenda

Global New Passenger Vehicle Registrations continue to increase

2012 - Overall growth of 7.2% 2011 registrations to reach 66.6 million units

Automotive Sector : Market figures

Automotive Battery Committee - June 2013 14

Global Passenger Vehicle Registrations per region 2011-2012

2012 was an excellent year for the automotive industry.......

Country/Region 2012 change from 2011

China 13.5 million +9.3%

United States 14.5 million +13%

EU 12 million -8.2%

Japan 4.6 million +29.5%

Brazil 2.9 million +7.7%

Russia 2.7 million +10.9%

India 2.5 million +11.1%

South Africa 443,000 +11%

Global 66.6 million +7.2%

* According to Volkswagen Annual Report

Automotive Battery Committee - June 2013 15

Automotive Sector : Market figures

16

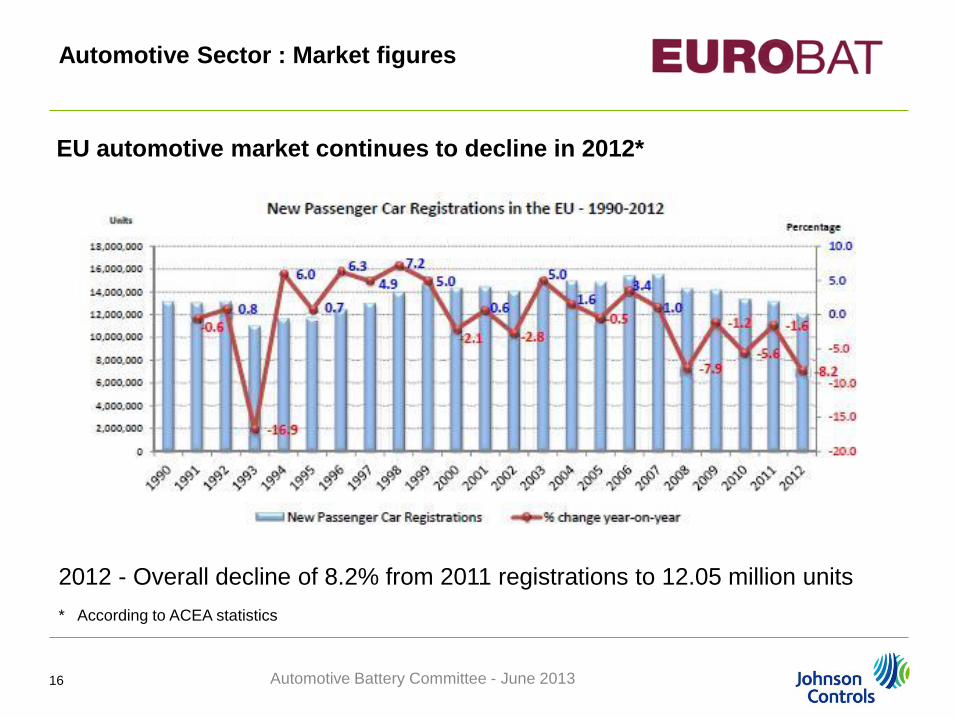

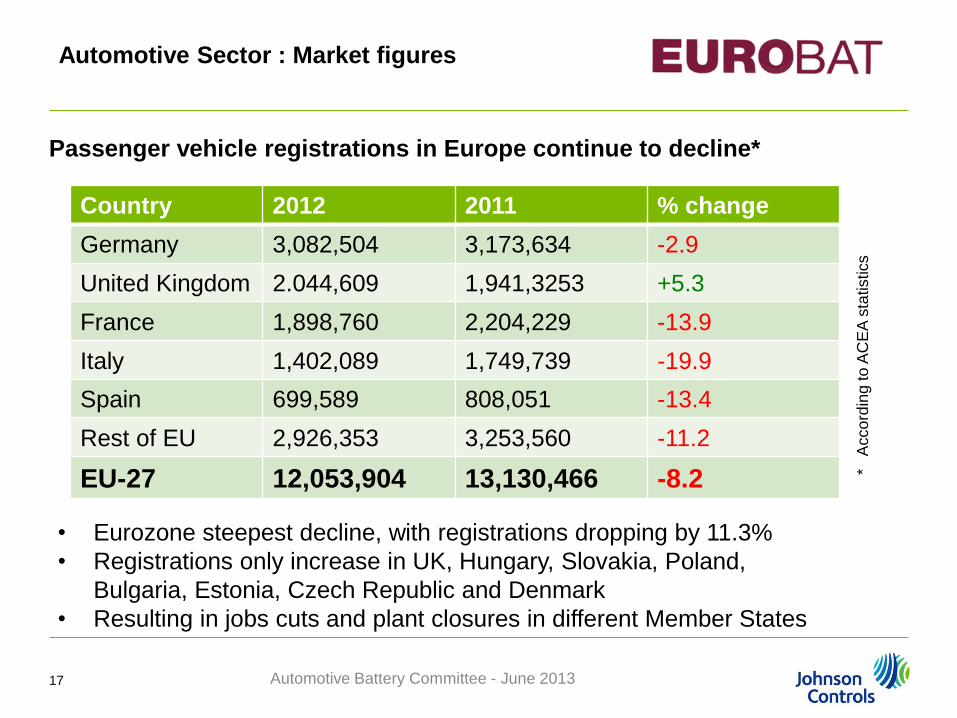

EU automotive market continues to decline in 2012*

* According to ACEA statistics

2012 - Overall decline of 8.2% from 2011 registrations to 12.05 million units

Automotive Battery Committee - June 2013

Automotive Sector : Market figures

Passenger vehicle registrations in Europe continue to decline*

Country 2012 2011 % change

Germany 3,082,504 3,173,634 -2.9

United Kingdom 2.044,609 1,941,3253 +5.3

France 1,898,760 2,204,229 -13.9

Italy 1,402,089 1,749,739 -19.9

Spain 699,589 808,051 -13.4

Rest of EU 2,926,353 3,253,560 -11.2

EU-27 12,053,904 13,130,466 -8.2

* A

cco

rdin

g to

AC

EA

sta

tistics

• Eurozone steepest decline, with registrations dropping by 11.3%

• Registrations only increase in UK, Hungary, Slovakia, Poland,

Bulgaria, Estonia, Czech Republic and Denmark

• Resulting in jobs cuts and plant closures in different Member States

Automotive Battery Committee - June 2013 17

Automotive Sector : Market figures

1. Automotive Battery Market Volumes 2012 - 2016

18

2. Automotive Sector : Market figures

3. Automotive Sector: Trends

Automotive Battery Committee - June 2013

Agenda

Automotive Battery Committee - June 2013

Automotive Sector: Trends

19

Europe

– 15% by 2015

– 25% improvement over 2015

levels by 2020

United States

– 15% by 2016

– 40+% improvement in average

fuel economy by 2025

China

‒ Aligning requirements around

EU regulations

Existing and pending legislation continues to

push automakers to introduce new technologies

179 160 116

182 162 132

154 130 95

2012 2015 2020 CO2 Targets

grams CO2/km

335.611 394.802 450.872 509.396 579.509

2012 2013 2014 2015 2016

Automotive Sector: Trends

Hybrid Electric Vehicles in operation Europe (2012-2016)*

* According to POLK and GIPA, based on models on the market in 2011/2. Surveyed countries – AU, BE, HR, CZ, DE,

FI, DE, HU, IR, IT, LU, NL, NO, PO, PT, RO, RU, ES, SI, SK, SE, CH, TU, UK

18.652 31.173

50.316 72.333

95.195

2012 2013 2014 2015 2016

Full Electric Vehicles in operation Europe (2012-2016)*

Automotive Battery Committee - June 2013 20

Automotive Battery Committee - June 2013

Future Start/Stop Technologies

Start-Stop with voltage stabilization system

“eHDi” technology with lead-acid AGM battery

and Supercaps

“Hybrid Air “ system PSA/Bosch w/o specific battery Engine off while approaching a stop,

but at vehicle speed < 20 km/h

(not after complete vehicle standstill as today)

“Stop-in-motion”: Engine off at higher

whenever acceleration is not needed

Future Market

Start-Stop functionality in 70% of new European vehicles

Research tells that 90% of all owners are very satisfied

Global Start/Stop market for new vehicles to reach 35 million by 2017

21

Automotive Sector: Trends

Automotive Battery Committee - June 2013

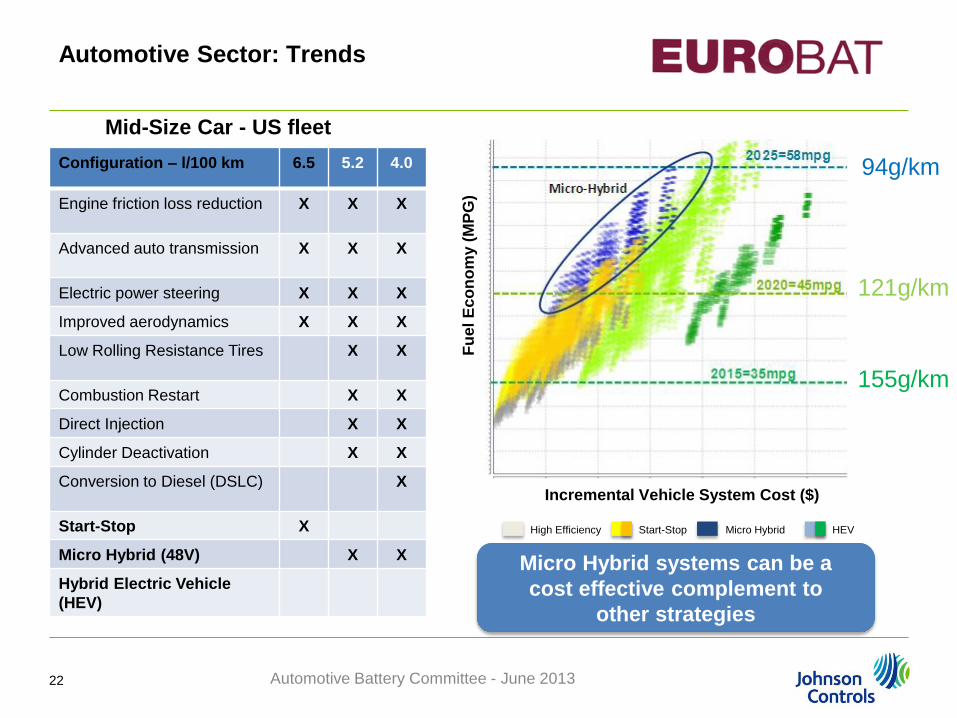

Mid-Size Car - US fleet

Configuration – l/100 km 6.5 5.2 4.0

Engine friction loss reduction X X X

Advanced auto transmission X X X

Electric power steering X X X

Improved aerodynamics X X X

Low Rolling Resistance Tires X X

Combustion Restart X X

Direct Injection X X

Cylinder Deactivation X X

Conversion to Diesel (DSLC) X

Start-Stop X

Micro Hybrid (48V) X X

Hybrid Electric Vehicle

(HEV)

Incremental Vehicle System Cost ($)

X

X

Fu

el

Ec

on

om

y (

MP

G)

X

High Efficiency Start-Stop Micro Hybrid HEV

Micro Hybrid systems can be a

cost effective complement to

other strategies

22

Automotive Sector: Trends

94g/km

121g/km

155g/km

23 Automotive Battery Committee - June 2013

€1,21 US, €1,62 EU, €1,41 China Global Gas Average € / l:

2020 Forecast (2012 look)

Updated 2020

Outlook

< 50 V +

+

+ +

Automotive Sector: Trends

Automotive Battery Committee - June 2013 24

Cost and driving range remains

the challenge for consumers

Lack of charging infrastructure also a limitation –

but EU Clean Fuels Strategy sets binding 2020

targets for charging points in Member States

Pike Research estimates 1.8 million EVs

+ 1.2 million PHEVs on EU roads by 2020

Automotive Sector: Trends

Automotive Battery Committee - June 2013 25

Thank you for

your attention !

Automotive Battery Committee