automatic balance mechanisms for notional defined ... fileautomatic balance mechanisms for notional...

TRANSCRIPT

IntroductionThe Model

Numerical illustrationConclusion

Automatic Balance Mechanisms for Notional DefinedContribution Accounts in the presence of uncertainty

Jennifer Alonso Garcıa(joint work with Carmen Boado-Penas and Pierre Devolder)

Universite Catholique de Louvain (UCL), Belgium

27/01/2015

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Overview

1 IntroductionWhy?OverviewNDC

2 The ModelAimOLG SetupLiquidity & Solvency RatioABM

3 Numerical illustrationMethodologyNo Baby BoomBaby Boom

4 Conclusion

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Why?OverviewNDC

Why should we consider a pension reform?

In Belgium the following demographic changes are observed:

Rising longevity: people are living longer and longer but retire at the sameage as 50 years ago.

Life expectancy in 1960: 70 yearsLife expectancy in 2011: 80 years

Drop in fertilityFertility rate in 1960: 2.58 births per woman.Fertility rate in 2011: 1.84 births per woman.

Shortcomings of Defined Benefit (DB):

Shifting from defined benefits to defined contributions seems better interms of steady-state income per capita (Artige, Cavenaile & Pestieau,2014)

Lack of actuarial fairness: No direct link between the contributions madeand amount of pension received at retirement.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Why?OverviewNDC

Change in gross public pension expenditure over 2010-2060 (in % of GDP)

Table : Change in gross public pension expenditure over 2010-2060 (in % of GDP)

Country 2010 2020 2040 2060 Change 2010-2060

BE 11,0 13,1 16,5 16,6 5,6DE 10,8 10,9 12,7 13,4 2,6IT 15,3 14,5 15,6 14,4 -0,9

SW 9,6 9,6 10,2 10,2 0,6PL 11,8 10,9 10,3 9,6 -2,2UK 7,7 7,0 8,2 9,2 1,5

UE27 11,3 11,3 12,6 12,9 1,5

Source: European Commission - The 2012 Ageing Report

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Why?OverviewNDC

Overview of pension systems

Basic financing techniquesPay as you go (PAYG): current contributors pay current pensioners(Unfunded schemes)Funding: contributions are accumulated in a fund which earns a marketinterest rate (Funded schemes)

Benefit formulaeDefined Benefit: Pension is calculated according to a fixed formula whichusually depends on the members salary and the number of contributionyears.Defined Contribution: Pension is dependent on the amount of moneycontributed and their return.

⇒ Notional Accounts: Mix of PAYG and Defined Contribution !

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Why?OverviewNDC

Notional Defined Contribution

The non-financial defined contribution or notional model combines:Pay-as-you-go (PAYG) financingA pension formula that depends on the amount contributed and the returnon it which is determined by the notional rate.

The account is called notional because no pot of pension fund moneyexists as the system is PAYG financed.

At retirement age: Accumulated capital ⇒ Annuity

The annuity takes into account:Life expectancy of the individualThe indexation of pensionsThe technical interest rate

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

Aim of the Article

The aim of this article is twofold:

Show at what extent the liquidity and solvency indicators are affected byfluctuations in the financial and demographic conditions,

Explore the issue of choosing the most suitable automatic balancingmechanism into the notional model to re-establish financial equilibrium.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

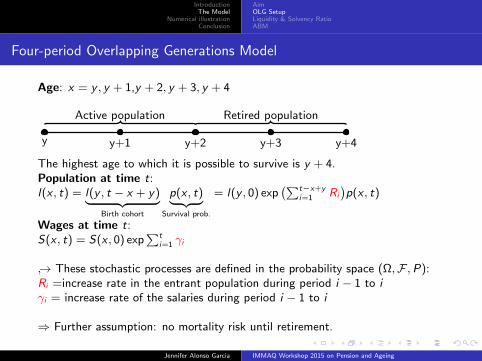

Four-period Overlapping Generations Model

Age: x = y , y + 1,y + 2, y + 3, y + 4

y y+1 y+2 y+3 y+4

Active population Retired population

The highest age to which it is possible to survive is y + 4.Population at time t:l(x , t) = l(y , t − x + y)︸ ︷︷ ︸

Birth cohort

p(x , t)︸ ︷︷ ︸Survival prob.

= l(y , 0) exp(∑t−x+y

i=1 Ri

)p(x , t)

Wages at time t:S(x , t) = S(x , 0) exp

∑ti=1 γi

→ These stochastic processes are defined in the probability space (Ω,F ,P):Ri =increase rate in the entrant population during period i − 1 to iγi = increase rate of the salaries during period i − 1 to i

⇒ Further assumption: no mortality risk until retirement.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

Contributions and notional rate

Active members contribute a rate π of their salaries to the pension system.C(t) denotes the total contribution:

C(t) = πS(y , t)l(y , t) + πS(y + 1, t)l(y + 1, t)

= πl(y , 0) exp (t∑

i=1

γi +t−1∑i=1

Ri )KC (t)

where : KC (t) = S(y , 0)eRt + S(y + 1, 0)

The notional factor I (t) is chosen as the rate of increase of totalcontribution base and is affected by both salary and demographic risks:

I (t) =C(t)

C(t − 1)= eγt+Rt−1

KC (t)

KC (t − 1)= 1 + nrt (1)

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

Pension calculation and expenditure

Individual contributions are indexed by the notional factor.

Its accumulated value at retirement age corresponds to the notionalcapital NDCCO(y + 2, t).

The initial pension is based on this notional capital and the annuity at attime of retirement t:

P(y + 2, t) =NDCCO(y + 2, t)

at · l(y + 2, t)

The pension expenditures, denoted by O(t) depend on past notionalcapitals and life expectancy:

O(t) = P(y + 2, t)l(y + 2, t) + P(y + 2, t − 1)Λ∗(t)l(y + 3, t) = C(t)KO(t)

Indexation design Λ∗(t) ensures actuarial fairness per cohort.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

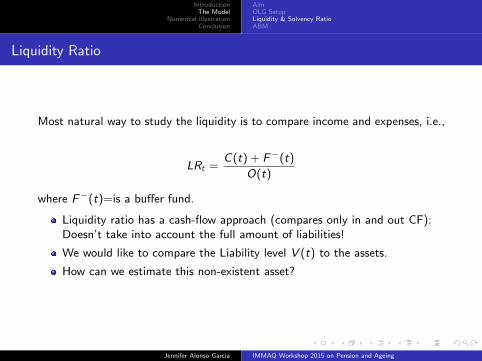

Liquidity Ratio

Most natural way to study the liquidity is to compare income and expenses, i.e.,

LRt =C(t) + F−(t)

O(t)

where F−(t)=is a buffer fund.

Liquidity ratio has a cash-flow approach (compares only in and out CF):Doesn’t take into account the full amount of liabilities!

We would like to compare the Liability level V (t) to the assets.

How can we estimate this non-existent asset?

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

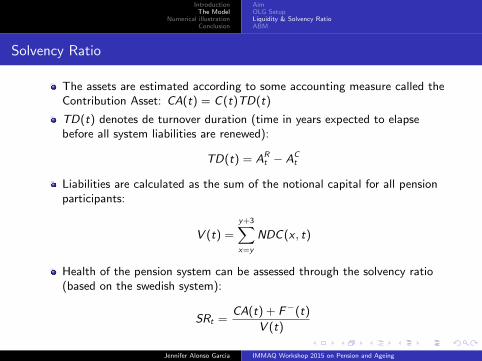

Solvency Ratio

The assets are estimated according to some accounting measure called theContribution Asset: CA(t) = C(t)TD(t)

TD(t) denotes de turnover duration (time in years expected to elapsebefore all system liabilities are renewed):

TD(t) = ARt − AC

t

Liabilities are calculated as the sum of the notional capital for all pensionparticipants:

V (t) =

y+3∑x=y

NDC(x , t)

Health of the pension system can be assessed through the solvency ratio(based on the swedish system):

SRt =CA(t) + F−(t)

V (t)

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

AimOLG SetupLiquidity & Solvency RatioABM

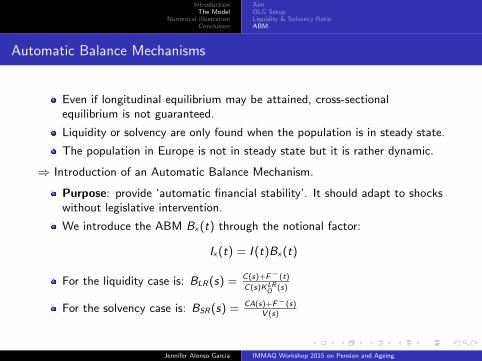

Automatic Balance Mechanisms

Even if longitudinal equilibrium may be attained, cross-sectionalequilibrium is not guaranteed.

Liquidity or solvency are only found when the population is in steady state.

The population in Europe is not in steady state but it is rather dynamic.

⇒ Introduction of an Automatic Balance Mechanism.

Purpose: provide ‘automatic financial stability’. It should adapt to shockswithout legislative intervention.

We introduce the ABM Bx(t) through the notional factor:

Ix(t) = I (t)Bx(t)

For the liquidity case is: BLR(s) = C(s)+F−(t)

C(s)KLRO

(s)

For the solvency case is: BSR(s) = CA(s)+F−(s)V (s)

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

MethodologyNo Baby BoomBaby Boom

Methodology

ABM preference stated in terms of expected value and variance.

Random variables are supposed to be stationary.⇒ However, exogenous shocks mimicking the baby-boom have beenadded.

Three mortality scenarios (base, up & down).

ABM may be symmetric or assymetric (surpluses are cumulated and notshared).

Two annuity cases taken into account: prospective (C. 1) and current(C.2).

Monte Carlo simulations on 1 million scenarios.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

MethodologyNo Baby BoomBaby Boom

Numerical illustration: No Baby Boom - N. Factor

Figure : Ex Value N. Factor: no ABM (dotted black line), LR ABM (dark gray squares) and SR

ABM (light gray rhombuses)

(a) C.1-Sym (b) C.1-Non-sym (c) C.2-Sym (d) C.2-Non-sym

Note: 1st row: base, 2nd: up and 3rd: down

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

MethodologyNo Baby BoomBaby Boom

Numerical illustration: No Baby Boom - Fund/Contributions

Figure : Expected Value Fund/Contributions: no ABM (dotted black line), LR ABM (dark gray

squares) and SR ABM (light gray rhombuses)

(a) C. 1-Sym (b) C. 1-No-sym (c) C.2-Sym (d) C.2-No-sym

Note: 1st row: base, 2nd: up and 3rd: down

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

MethodologyNo Baby BoomBaby Boom

Numerical illustration: Baby Boom

Figure : Expected Value: no ABM (dotted black line), LR ABM (dark gray squares) and SR

ABM (light gray rhombuses)

(a) N. Factor-C. 1 (b) N. Factor-C. 2 (c) Fund-C. 1 (d) Fund-C. 1

Note: 1st row: base, 2nd: up and 3rd: down

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Conclusion

Introduction of an ABM reduces the volatility of the fund.

The Solvency Ratio ABM yields the lowest value of the notional factor’svariance with lowest expected value.

Symmetric ABMs seem better by means of expected value.

Assymetric ABMs produce an over-accumulation of assets (in line w/Auerbach & Lee).

System almost auto-regulates itself after an exogenous fertility shock oncethat the shocked generation exits.

However, the NDC system can’t cope with longevity improvements inabsence of ABM.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

References

Alonso Garcia, J. , Boado-Penas, M. del C. and P. Devolder (2014). Automatic balancing

mechanisms for Notional Defined Contribution Accounts in the presence of uncertainty. ISBADiscussion Paper, 2014/38. http://hdl.handle.net/2078.1/151874

Artige, L. , Cavenaile, L. and P. Pestieau (2014). The macroeconomics of PAYG pension

schemes in an aging society. CORE Discussion Paper, 2014/33http://hdl.handle.net/2078.1/147241

Auerbach, A.J. and R. Lee (2007). Notional Defined Contribution Pension Systems in a

Stochastic Context: Design and Stability. Berkeley Program in Law and Economics, WorkingPaper Series, UC Berkeley.

Boado-Penas, C. , Valdes-Prieto, S. and C. Vidal-Melia (2008). An Actuarial Balance Sheet

for Pay-As-You-go Finance: Solvency Indicators for Spain and Sweden. Fiscal Studies, 29(1), 89–134.

Settergren and Mikula, B. D. (2005). The rate of return of pay-as-you-go pension systems:

a more exact consumption-loan model of interest. Journal of Pensions Economics andFinance, vol. 4, pp. 115–138.

Valdes-Prieto, S. (2000). The financial stability of Notional Accounts Pension. Scandinavian

Journal of Economics, 102(3), 395–417.

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing

IntroductionThe Model

Numerical illustrationConclusion

Thank you!

Jennifer Alonso Garcia IMMAQ Workshop 2015 on Pension and Ageing