autoforecast solutions engine, transmission, & drivetrain trends and outlook september 16, 2015...

TRANSCRIPT

AutoForecast Solutions

Engine, Transmission, & Drivetrain Trends and OutlookSeptember 16, 2015

Global Powertrain Analysis

Brian MaximVice President, Global Powertrain Forecasting

AutoForecast Solutions

Global Engine & Transmission Analysis

2

AutoForecast Solutions

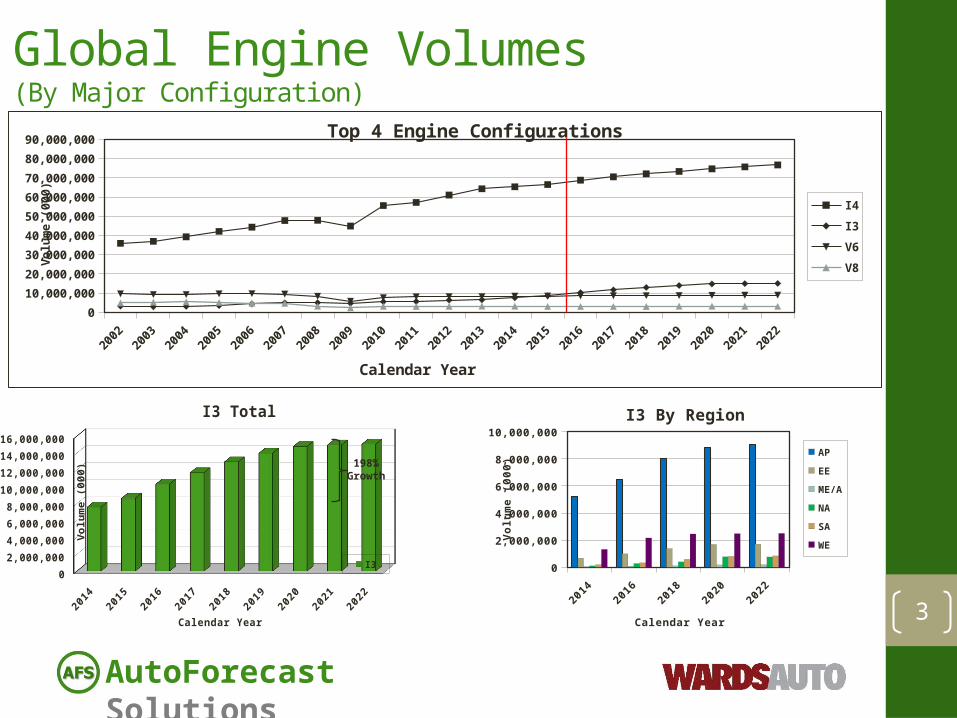

Global Engine Volumes(By Major Configuration)

3

20022003

20042005

20062007

20082009

20102011

20122013

20142015

20162017

20182019

20202021

2022

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000Top 4 Engine Configurations

I4

I3

V6

V8

Calendar Year

Vol

ume

(000

)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

I3 Total

I3

Calendar Year

Vol

um

e (0

00

)

20142016

20182020

2022

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

10,000,000

I3 By Region

AP

EE

ME/A

NA

SA

WE

Calendar Year

Vol

um

e (0

00

)198%Growth

AutoForecast Solutions

Global Engine Trends• Programs gravitating down similar paths

• Smaller engine programs looking fairly similar• 2.0L I4 GDI Turbo

• Still replacing smaller V6s• Offered as upgrade to non-turbo 2.0L

• 1.5L GDI Turbo• Some are 1.4L or 1.6L• Replacing larger I4s

• 1.0L GDI Turbo• Replacing medium and small I3/I4s

• 3.0L 6-cylinder with GDI• 3.0L is a global approach

• Fiat Chrysler (FCA), GM and Ford differ slightly• V8s diverge

• Reserved more for sports cars and truck based vehicles• Non-NA assemblers choosing GDI • NA assemblers going different paths, embracing different technologies

4

AutoForecast Solutions

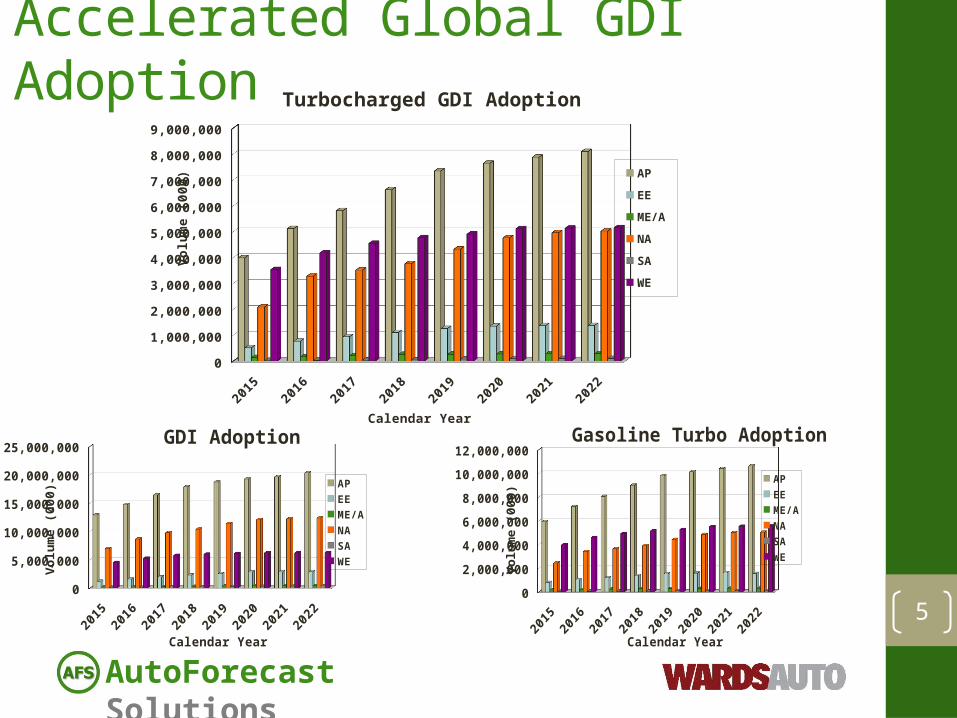

Accelerated Global GDI Adoption

50

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000GDI Adoption

APEEME/ANASAWE

Calendar Year

Vol

um

e (0

00

)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000Gasoline Turbo Adoption

APEEME/ANASAWE

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

Turbocharged GDI Adoption

AP

EE

ME/A

NA

SA

WE

Calendar Year

Vol

um

e (0

00

)

AutoForecast Solutions

Light Vehicle Diesel Volume Analysis

6

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000Global Diesel

WE

SA

NA

ME/A

EE

AP

Calendar Year

Vo

lum

e (0

00

)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

North America

Calendar Year

Vol

um

e (0

00

)

Most growth from Asia• India and China lead the way• West Europe stabilizing• Mild growth in North America

North America adding applications• Small diesels on full-sized pickups• Some car offerings increasing slightlyFuel and purchase price cost pressures still a factor

AutoForecast Solutions

Light Vehicle Hybrid Volume Analysis

7

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000Global Hybrids

WE

NA

EE

AP

Calendar Year

Vo

lum

e (0

00

)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

North America

Calendar Year

Vol

um

e (0

00

)

Global growth expected• China may finally be picking up

some steam• Many new hybrids planned• Toyota is clear leader• Ford planning significant

increasesRegional volumes are based on vehicle production• Many hybrids are exported from

OEM’s home market

North America is planning to add applications and volume• Attempting to meet future fuel economy related

mandatesRecent significant pressure from low fuel prices and fickle consumers

AutoForecast Solutions

Light Vehicle EV Volume Analysis

8

0

100,000

200,000

300,000

400,000

500,000

600,000Global EVs

WE

NA

ME/A

EE

AP

Calendar Year

Vo

lum

e (0

00

)

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000

North America

Calendar Year

Vol

um

e (0

00

)

Strong North American growth• Tesla and Renault/Nissan lead the way• Smaller volumes from traditional

manufacturersLow fuel prices hurt budget market vehicles

Global growth expected• China may finally be picking up

some steam• Many high-end sports car

models being added• All major OEMs adding

applications and volume

AutoForecast Solutions

North American Engine Volumes(By Major Configuration)

9

20022003

20042005

20062007

20082009

20102011

20122013

20142015

20162017

20182019

20202021

2022

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000Top 3 Engine Configurations

I4

V6

V8

Calendar Year

Vol

ume

(000

)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

I3

Calendar Year

Vol

um

e (0

00

)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

H4

Calendar Year

Vol

um

e (0

00

)

247%Growth

Roughly 1/3 of global total

742%Growth

AutoForecast Solutions

North American Engine Trends• OEMs developing similar programs

• Smaller engine programs looking fairly similar• 2.0L I4 GDI Turbo• 1.4L -1.5L GDI Turbo

• Replacing larger I4s• 3.6L V6s for FCA and GM

• Ford taking a more fractured approach• 2.7L V6 EcoBoost• 3.3L V6 non-EcoBoost• 3.5L V6 sticks around

• V8s diverge• GM keeping OHV, but utilizing add-on technologies and reducing friction• Fiat-Chrysler keeping OHV but utilizing add-on technologies• Ford using more expensive OHC technologies

10

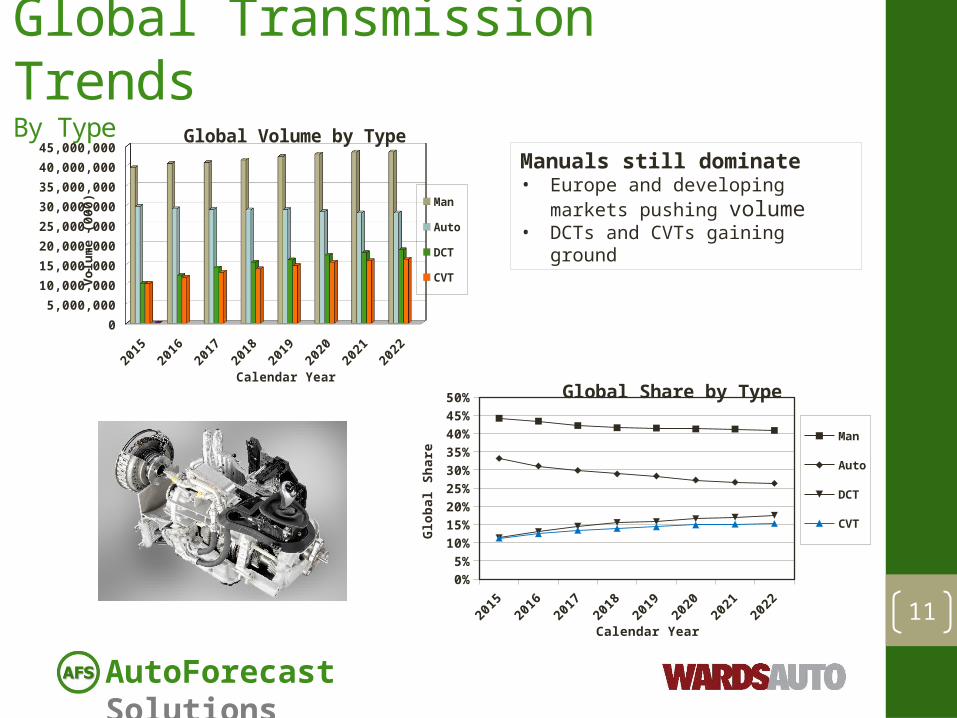

AutoForecast Solutions

Global Transmission TrendsBy Type

11

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000Global Volume by Type

Man

Auto

DCT

CVT

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%5%

10%15%20%25%30%35%40%45%50% Global Share by Type

Man

Auto

DCT

CVT

Calendar Year

Glo

bal

Sh

are

Manuals still dominate• Europe and developing markets

pushing volume• DCTs and CVTs gaining ground

AutoForecast Solutions

Global Automatic Adoption(Traditional Automatics)

12

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000Regional Consumption Volumes

AP

EE

ME/A

NA

SA

WE

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%

10%

20%

30%

40%

50%

60%

70%

80% Automatic Share In Each Region

AP

EE

ME/A

NA

SA

WE

Calendar Year

Reg

ion

al S

har

e

Influenced by North America and Europe• Asia Volumes mostly from China• North America prefers the traditional

automatic• Europe prefers manuals, keeping

volumes low

AutoForecast Solutions

Global CVT Adoption

13

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000 Regional Consumption Volumes

AP

EE

ME/A

NA

SA

WE

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%

5%

10%

15%

20%

25%

30%CVT Share In Each Region

AP

EE

ME/A

NA

SA

WE

Calendar Year

Reg

ion

al S

har

e

Strong Japanese Influence• Asia volumes mostly Japan with

some in China• NA a result of Japan• Other regions prefer DCTs and

automatics

AutoForecast Solutions

Global DCT Adoption

14

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000 Regional Consumption Volumes

AP

EE

ME/A

NA

SA

WE

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%

5%

10%

15%

20%

25%

30%

35%DCT Share In Each Region

AP

EE

ME/A

NA

SA

WE

Calendar Year

Reg

ion

al S

har

e

Strong European Influence• Asia Volumes mostly from China• Europe volumes fairly low due to

preferring manuals• North America influenced some by

Europe

AutoForecast Solutions

North America Transmission Trends

15

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000Transmission Volume by Type

Auto

CVT

DCT

Man

Calendar Year

Vol

um

e (0

00

)

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000Automatics Breakdown

A10

A9

A8

A7

A6

A5

A4

Calendar Year

Vol

um

e (0

00

)

NA Automatics - 2005

A4

A3A7

A6

A5

NA Transmissions - 2005

Auto

DCT

CVT

Man

AutoForecast Solutions

Recent Powertrain Developments• Evolving transmission programs

• GM/Ford FWD transmission agreement• Larger 9-speed to be replaced by an 8-speed• Ford to add small 8-speed to lineup

• To be built in 3 plants around the world• Will replace some medium 9-speeds, at lower end• Primarily replacing automatic 6-speeds and some DCTs

• CVT programs for Ford and GM coming back• Both are planning CVTs again, in lower volumes

• Ford applications are for non-North American vehicles• Magna acquisition of Getrag

• Will greatly expand Magna drivetrain portfolio• Will lead to closer relationship with Ford through Getrag/Ford JVs

• Ford to offer small diesel in F-150• 3.0L V6 to combat current Ram and future GM offerings

16

AutoForecast Solutions

Recent Powertrain Developments(cont.)

• Falling fuel prices – fuel economy less important • Consumers choosing larger engines again

• Choosing different vehicles with larger engines• Choosing larger engines within the vehicle category

• Hybrid and EV growth slowing• More difficult to justify added costs and/or compromises

• China is bucking the trend and growing

17Sales of fuel efficient vehicles in North America are

driven more by government incentives and mandates than by consumer preferences

Jan-0

8

Apr-08

Jul-0

8

Oct-08

Jan-0

9

Apr-09

Jul-0

9

Oct-09

Jan-1

0

Apr-10

Jul-1

0

Oct-10

Jan-1

1

Apr-11

Jul-1

1

Oct-11

Jan-1

2

Apr-12

Jul-1

2

Oct-12

Jan-1

3

Apr-13

Jul-1

3

Oct-13

Jan-1

4

Apr-14

Jul-1

4

Oct-14

Jan-1

5

Apr-15

Jul-1

5

20.0

21.0

22.0

23.0

24.0

25.0

26.0

27.0

Monthly US Fuel Economy, Weighted by New Vehicle Sales*

MPG

* From the Transportation Research Institute, University of Michigan

Small diesel programs being revived for pickups

AutoForecast Solutions

Global Drivetrain AnalysisSystems and Market Trends

18

AutoForecast Solutions

4WD/AWD Systems – Brief Overview• There are three basic 4WD/AWD systems

• Transfer Cases • An additional “gearbox” in conjunction with the transmission which

allows for the selection of neutral and at least one gear ratio, but usually two• Ford F150• Jeep Grand Cherokee

• Torque Adjustable Couplings• Allows for sending mechanical forces to the other set of tires not

normally powered by the transmission• BMW X-Drive• Chevrolet Equinox• Subaru Outback

• Electronic AWD• Two or four wheels of the vehicles are powered by electric motors

• Toyota Highlander Hybrid• Tesla Model X

19

AutoForecast Solutions

North American AWD/4WD Volumes(By Drive Type)

20

20152016

20172018

20192020

20212022

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500AWD/4WD Volume by Type

AWD

4WD

AWD E

Calendar Year

Vo

lum

e (0

00

)

20152016

20172018

20192020

20212022

0102030405060708090

100

Electronic AWD

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%

5%

10%

15%

20%

25%

NA Light Vehicle Production

AWD

4WD

AWD E

Calendar Year

Shar

e of

Tot

al

Volvo effect

Tesla effect

AutoForecast Solutions

European AWD/4WD Volumes(By Drive Type)

21

20152016

20172018

20192020

20212022

0

500

1,000

1,500

2,000

2,500

3,000

3,500AWD/4WD Volume by Type

AWD

4WD

AWD E

Calendar Year

Vo

lum

e (0

00

)

20152016

20172018

20192020

20212022

0

10

20

30

40

50

60

70

Electronic AWD

Calendar Year

Vol

um

e (0

00

)

20152016

20172018

20192020

20212022

0%

2%

4%

6%

8%

10%

12%

14%

16%European Light Vehicle Production

AWD

4WD

AWD E

Calendar Year

Shar

e of

Veh

icle

Tot

al

Porsche Pajuneffect

AutoForecast Solutions

European Market Trends• Mild growth of AWD/4WD

• As vehicle prices rise, more new vehicle purchases have a greater amount of options, including AWD/4WD• Consumers looking to purchase less expensive products moving toward

the used car market

• Growth in “CUVs” not pushing AWD growth as much• Most European CUVs are just normal hatchbacks that have been

raised higher• Most of these vehicles do not offer AWD systems

• European consumers do not purchase vehicles with AWD/4WD systems as much as other regions• For example, UK consumers do not opt AWD/4WD systems

22

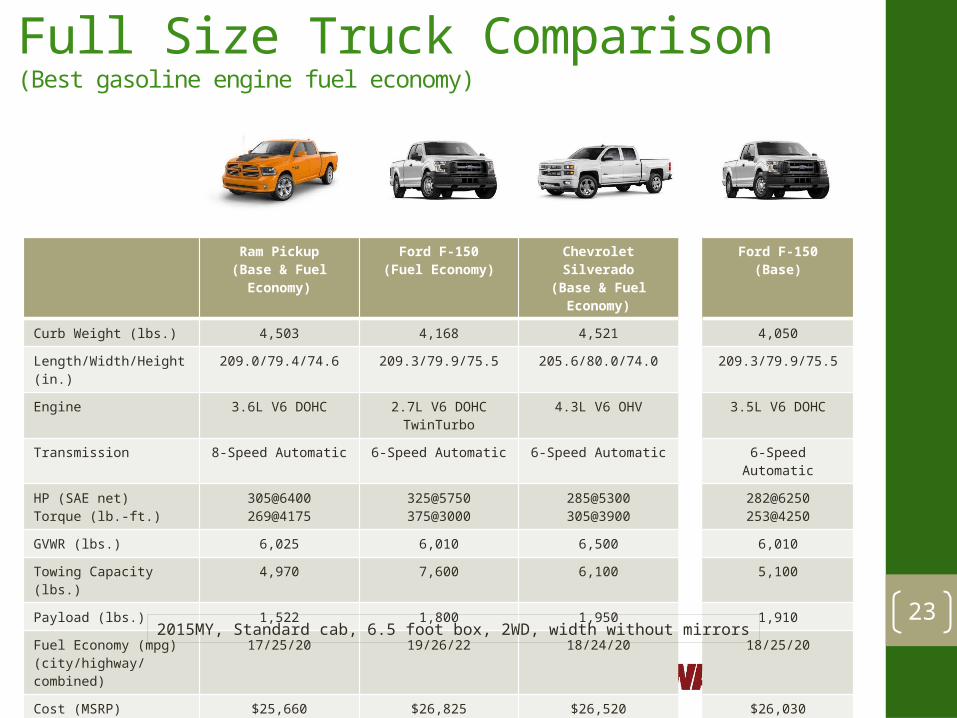

AutoForecast Solutions

Full Size Truck Comparison(Best gasoline engine fuel economy)

23

Ram Pickup(Base & Fuel Economy)

Ford F-150(Fuel Economy)

Chevrolet Silverado(Base & Fuel Economy)

Ford F-150(Base)

Curb Weight (lbs.) 4,503 4,168 4,521 4,050

Length/Width/Height (in.) 209.0/79.4/74.6 209.3/79.9/75.5 205.6/80.0/74.0 209.3/79.9/75.5

Engine 3.6L V6 DOHC 2.7L V6 DOHC TwinTurbo 4.3L V6 OHV 3.5L V6 DOHC

Transmission 8-Speed Automatic 6-Speed Automatic 6-Speed Automatic 6-Speed Automatic

HP (SAE net)Torque (lb.-ft.)

305@6400269@4175

325@5750375@3000

285@5300305@3900

282@6250253@4250

GVWR (lbs.) 6,025 6,010 6,500 6,010

Towing Capacity (lbs.) 4,970 7,600 6,100 5,100

Payload (lbs.) 1,522 1,800 1,950 1,910

Fuel Economy (mpg)(city/highway/combined)

17/25/20 19/26/22 18/24/20 18/25/20

Cost (MSRP) $25,660 $26,825 $26,520 $26,030

2015MY, Standard cab, 6.5 foot box, 2WD, width without mirrors

AutoForecast Solutions

Powertrain Relationships

24

AutoForecast Solutions

OEM Agreements and Outsourcing Continues

• Significant agreements for diesels• Ford heavily relies on PSA designs

• Buys some from PSA, but builds most themselves• GM uses several different diesel designs

• Builds and uses designs from Isuzu, VM Motori and FCA around the world• FCA sources diesels from Cummins and VM Motori for Ram Pickups

• Gasoline engine designs• GM’s L850 I4 engines

• The “L” stands for Lotus, the primary designer• GM has greatly refined the engine since

• Hyundai’s Zeta (Theta) I4 family• Used by FCA and Mitsubishi

• Aston Martin will use Mercedes engines• Currently uses Ford based engines – from previous ownership

• Nissan building and using Mercedes 2.0L Turbo I4• Built in Decherd for MB and Nissan in North America 25

AutoForecast Solutions

OEM Agreements and Outsourcing Continues(Cont.)

• Transmission agreements• Significant cooperation between Ford and GM in North America

• GM is primary designer of FWD transmissions• Ford makes adjustments to give them a Ford flavor

• Started with the current mid and large A6s• Will extend to future A8s and A9s• Ford will produce them in their own plants

• Ford is primary designer of RWD transmissions• GM will make adjustments to give them a GM flavor

• Includes 10-speed units for trucks and large SUVs• GM will produce them in their own plants

• FCA heavily relying on ZF• FCA licensed designs and is producing them in their own plants

• 8-speed RWD automatics for trucks• 9-speed FWD automatics for medium and larger FWD vehicles

• Most recently Magna’s purchase of Getrag• Highlights how transmissions are becoming a huge area of growth

• Significant experience and volume of DCTs 26

AutoForecast Solutions

Mandates

27

AutoForecast Solutions

Can OEMs meet future MPG Targets?• Misconceptions of the 54.5 mpg target for the 2025MY

• The 2025MY target has not been mandated• A mid-term meeting in 2017 is when the EPA and NHTSA will determine

what the target will be for 2025MY and the schedule to get there• The 54.5 mpg target is not a CAFE target

• Future fuel economy targets are not directly mandated• OEMs must meet various emissions targets, including a CO2 target which

effectively equates to fuel economy (2025 = 163 grams/mile)• All light vehicles do not have to meet the 54.5 mpg target

• Actual CO2 targets are based on footprint (shadow) of each vehicle• Larger vehicles have an easier target than smaller vehicles• Different targets exist for cars (143 g/mi) and light trucks (203 g/mi)

• Each OEM does not have to meet the 54.5 mpg target• Targets are determined by individual product lines and their footprints

• No pressure to build small cars to offset fuel economy of large cars• No pressure to build cars to offset fuel economy of pickups and SUVs

28

AutoForecast Solutions

Can OEMs meet future MPG Targets?(Cont.)

• What are the hard targets?• 2017MY – 2021MY have been mandated• 2022MY – 2025MY have not been mandated

• Uses the CO2 Model

29

• Credit Banking and Trading (same as 2012MY-2016MY rules)• Credits may be carried for 3 years to offset a deficit in a previous year• Credits may be banked for 5 years for future offsets• Credits may be traded between companies

2017MY 2018MY 2019MY 2020MY 2021MY 2022MY 2023MY 2024MY 2025MY

Cars (g/mi) 212 202 191 182 172 164 157 150 143

Light Trucks (g/mi) 295 285 277 269 249 237 225 214 203

Combined - Cars & Light Trucks (g/mi)

243 232 222 213 199 190 180 171 163

MPG Equivalent for Combined

36.6 38.3 40.0 41.7 44.7 46.8 49.4 52.0 54.5

AutoForecast Solutions

Can OEMs meet future MPG Targets?(Cont.)

• Credits for implementing new technologies• Credits can be earned to help achieve targets

• Multiplier concept adopted for alternative powered vehicles• Each vehicle is multiplied by a factor in meeting emissions targets for the

2017MY to 2021MY timeframe – 2022MY+ uses no multipliers• EVs and FCVs (2.0 in 2017MY going to 1.5 in 2021MY)• PHEVs and CNG (1.6 in 2017MY going to 1.3 in 2021MY)

• Full-Size Pickup Hybridization Credits• Mild HEV - 10g/mi credit for each vehicle, if used on at least 20% in 2017MY

full-size pickups, ramping up to 80% in 2021MY• Strong HEV – 20g/mi credit for each vehicle, if used on at least 10% of pickups

• Air Conditioning credits• Using systems that reduce tailpipe CO2 through efficiency improvements• Using refrigerants with much less hydrofluorocarbons (HFCs)

• Off-Cycle credits (efficiency gains not reflected in test cycles)• Solar panels on hybrids• Start/stop systems• Active aerodynamics• Others – If OEM can provide proof that gains exist 30

AutoForecast Solutions

Future Powertrain Technologies• Areas of significant promise

• Compression ignition direct injected gasoline engines (CIDI)• Currently considered the holy grail for gasoline internal combustion

• Mazda claims release of SkyActive generation 2 around 2020 with CIDI• Electronic Valvetrain

• Has been in development for a fairly long time• Difficulty meeting velocity of operation requirements

• Innovative concepts• New battery chemistry for EVs and hybrids

• Increasing power density and shortening recharge times• More a question of when, rather than if

• Improved catalysts for better emissions• Greatly helping with cold start emissions

• Resurgence of 2-stroke• Possible revival using new technologies not previously available

31OEMS are continually going to push on their supply base to help meet current and potential future mandates and differentiate them in the market place.

AutoForecast Solutions

Engine, Transmission, & Drivetrain Trends and OutlookSeptember 16, 2015

Global Powertrain Analysis

Brian MaximVice President, Global Powertrain Forecasting