australian wheat exports in the global · pdf fileaustralian wheat exports in the global...

TRANSCRIPT

AUSTRALIAN WHEAT

EXPORTS IN THE GLOBAL

CONTEXT:LOCAL & INTERNATIONAL

PRESSURES ON PRICE FORMATIONAustralian Grains Industry ConferenceGTA Advisory & Compliance Workshop25-27 Jul 2016

Julien Hall

WHEAT EXPORT PRICE

UPDATE

FORCES AT WORK IN PRICE

FORMATION

WHAT IS A ROBUST PRICE

INDEX

3

PLATTS 100+ YEAR HISTORY

FOUNDED IN

1909S&P Global Platts is the leading

independent provider of information and benchmark prices for the

commodities and energy markets.

4

AREAS OF COVERAGE

BIOFUELS SUGAR GRAINS

Global Ethanol and Biodiesel coverageUS & Europe ethanol benchmarks

Started in 2003 Started in 2014Kingsman acquisition in 2012

Global Analysis and pricing Global Wheat and Corn coverage

WHEAT EXPORT PRICE

UPDATE

6

LONG-TERM TRENDUSD/mt

200

250

300

350

400

450

Au

g-1

0

Oct-

10

Dec-1

0

Fe

b-1

1

Ap

r-11

Jun

-11

Au

g-1

1

Oct-

11

Dec-1

1

Fe

b-1

2

Ap

r-12

Jun

-12

Au

g-1

2

Oct-

12

Dec-1

2

Fe

b-1

3

Ap

r-13

Jun

-13

Au

g-1

3

Oct-

13

Dec-1

3

Fe

b-1

4

Ap

r-14

Jun

-14

Au

g-1

4

Oct-

14

Dec-1

4

Fe

b-1

5

Ap

r-15

Jun

-15

Au

g-1

5

Oct-

15

Dec-1

5

Fe

b-1

6

Ap

r-16

Jun

-16

(US

D/M

T)

APW FOB Kwinana Nominal Replacement

7

Overall trend - slow erosion

interrupted by sharper volatility

• Pressure from Black Sea,

Canada & US milling wheat, W.

Europe & Argentina feed wheat

• Low global freight rates

reducing Australian freight

advantage to Asian buyers

• Mar-Jul volatility caused by

CBOT and forex

LAST NINE MONTHS

200

205

210

215

220

225

230

235

Platts APW FOB Kwinana

FORCES AT WORK IN

PRICE FORMATION

9

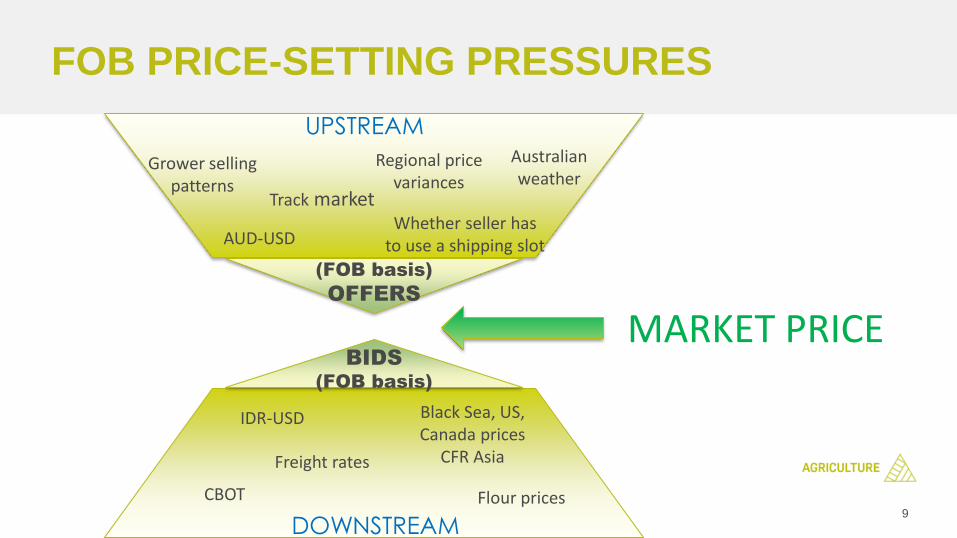

FOB PRICE-SETTING PRESSURES

Grower selling patterns

Regional price variances

Australian weather

AUD-USDWhether seller has

to use a shipping slot

Track market

(FOB basis)

OFFERS

BIDS

(FOB basis)

IDR-USD

Freight rates

CBOT Flour prices

Black Sea, US, Canada prices

CFR Asia

UPSTREAM

DOWNSTREAM

MARKET PRICE

MARKET PRICE BETWEEN THE BEST BID AND

OFFER

Best bid

OFFERS

BIDS

USD/mt

200

205

210

215

220

225

230

235

10

-Nov

17

-Nov

24

-Nov

1-D

ec

8-D

ec

15

-Dec

22

-Dec

29

-Dec

5-J

an

12

-Jan

19

-Jan

26

-Jan

2-F

eb

9-F

eb

16

-Fe

b

23

-Fe

b

1-M

ar

8-M

ar

15

-Mar

22

-Mar

29

-Mar

5-A

pr

12

-Apr

19

-Apr

26

-Apr

3-M

ay

10

-May

17

-May

24

-May

31

-May

7-J

un

14

-Jun

21

-Jun

28

-Jun

BIDS

OFFERS

PLATTS APW

UPSTREAM

TYPICAL SUPPLY CHAIN COSTS

Price atfarm

Cartage toBin

Storage Upcountryhandling

Transportto Port

Handlingat Port

Exportdiscount

Handymaxfreight toIndonesia

“FOB Replacement”CFR Indonesia

“True FOB”

Source: AEGIC, Platts

13

Export prices at a discount to

replacement

• Since Nov 2015, on average $6.47/mt

discount to FOB Kwinana replacement

value

• Due to more shipping capacity than

wheat demand, traders are discounting

to avoid wasting the cost slots (up to

$9/mt)

• Export discount has reduced to around

$4/mt since late May 2016

EXPORTS AT A DISCOUNT TO DOMESTIC

Source: Profarmer Australia, Platts

200

205

210

215

220

225

230

235

240

9-Nov 9-Dec 9-Jan 9-Feb 9-Mar 9-Apr 9-May 9-Jun

Platts APW FOB Australia (export price)Profarmer Kwinana FOB replacement (domestic price)Transactions

14

EXPORT DISCOUNT NARROWING

Source: Profarmer Australia, Platts

USD/mt

Since Nov 2015, on

average $6.47/mt

discount to FOB

Kwinana replacement

value

Export discount has

reduced to around

$4/mt since late May

2016 -> less supply +

traders long slots

-14

-12

-10

-8

-6

-4

-2

0

2

4

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Export elevation margin

15 per. Mov. Avg. (Export elevation margin)

DOWNSTREAM

16

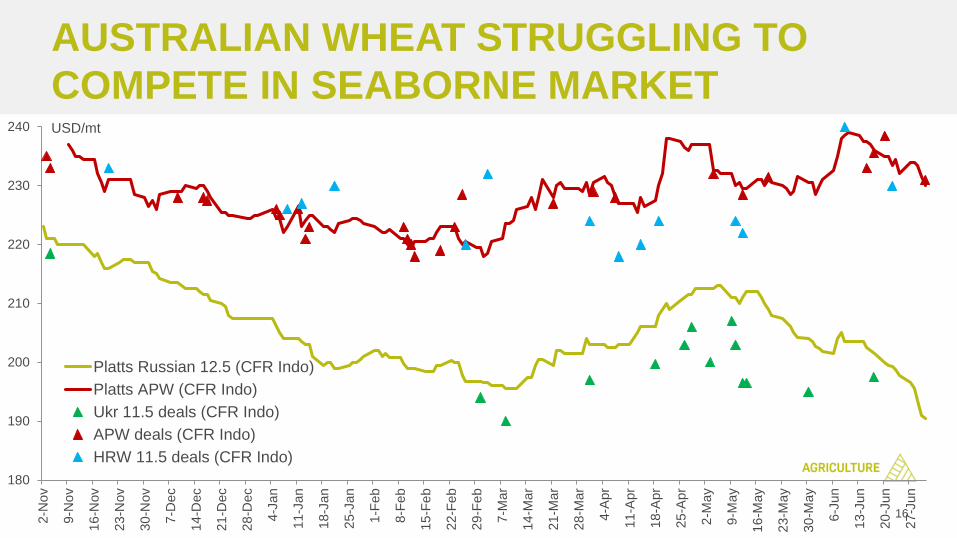

AUSTRALIAN WHEAT STRUGGLING TO

COMPETE IN SEABORNE MARKETUSD/mt

180

190

200

210

220

230

240

2-N

ov

9-N

ov

16

-Nov

23

-Nov

30

-Nov

7-D

ec

14

-Dec

21

-Dec

28

-Dec

4-J

an

11

-Jan

18

-Jan

25

-Jan

1-F

eb

8-F

eb

15

-Fe

b

22

-Fe

b

29

-Fe

b

7-M

ar

14

-Mar

21

-Mar

28

-Mar

4-A

pr

11

-Apr

18

-Apr

25

-Apr

2-M

ay

9-M

ay

16

-May

23

-May

30

-May

6-J

un

13

-Jun

20

-Jun

27

-Jun

Platts Russian 12.5 (CFR Indo)

Platts APW (CFR Indo)

Ukr 11.5 deals (CFR Indo)

APW deals (CFR Indo)

HRW 11.5 deals (CFR Indo)

17

… ADDITIONAL COMMENTS

USD/mt

180

190

200

210

220

230

240

2-N

ov

9-N

ov

16

-Nov

23

-Nov

30

-Nov

7-D

ec

14

-Dec

21

-Dec

28

-Dec

4-J

an

11

-Jan

18

-Jan

25

-Jan

1-F

eb

8-F

eb

15

-Fe

b

22

-Fe

b

29

-Fe

b

7-M

ar

14

-Mar

21

-Mar

28

-Mar

4-A

pr

11

-Apr

18

-Apr

25

-Apr

2-M

ay

9-M

ay

16

-May

23

-May

30

-May

6-J

un

13

-Jun

20

-Jun

27

-Jun

Platts Russian 12.5 (CFR Indo)

Platts APW (CFR Indo)

Ukr 11.5 deals (CFR Indo)

APW deals (CFR Indo)

HRW 11.5 deals (CFR Indo)

US pricing competitive

18

…USING APW CFR INDONESIA AS THE

BASELINE

-50

-40

-30

-20

-10

0

10

20

2-Nov 2-Dec 2-Jan 2-Feb 2-Mar 2-Apr 2-May 2-Jun

Rus 12.5 price advantage

Ukr 11.5 price advantage

HRW 11.5 price advantage

APW CFR Indonesia

19

CFR PRICING V PROTEIN

150

170

190

210

230

250

270

290

10 11 12 13 14 15 16 17 18

Price CFR SE Asia ($/mt)

Protein % (dry basis)

DNS 14

CWRS 2 13.5

HRW 11.5

RUS 12.5

APW

UKR 11.5

France 11

US SWW 10.5

ASW

ASW APW

WHAT IS A ROBUST

PRICE ASSESSMENT –

AND HOW CAN IT BE USED?

21

Main characteristics

• Accurately reflects market value

• Transparent and precise methodology

• Open to market scrutiny and feedback

• Broad industry participation

• Powered by rich, granular and verifiable price data

• Independent, impartial

WHAT IS A ROBUST PRICE ASSESSMENT?

PLATTS’ PRICES SERVE AS BENCHMARKS

Dated Brent: Price of physical, light North Sea crude. Estimated to be the reference for 60% of world’s oil.

Platts IODEX: Primary physical market pricing reference for seaborne iron ore fines delivered into China, the biggest importer of iron ore.

Henry Hub: Platts price for physical Henry Hub and related basis point are the benchmark for North American gas and underpin ICE’s exchange contracts

JAPAN

Platts Japan Korea Marker (JKM™): Price of liquefied natural gas (LNG) delivered into Japan and South Korea, the largest global importers. Considered the global reference for LNG pricing.

CHINAUK NBP: Platts price for UK NBP, gas traded within the national transmission system. Widely used as an indicator for Europe’s wholesale gas market.

UNITED KINGDOM

UNITED STATES

NORTH SEA

Platts Dubai: Physical price of Dubai crude oil loading through the month of assessment. Price reference for crude oil delivered to Asia from the Middle East.

Many price assessments have become “benchmarks” that market participants use to write contracts, monitor their commodity market and achieve full transparency around transactions. For example:

23

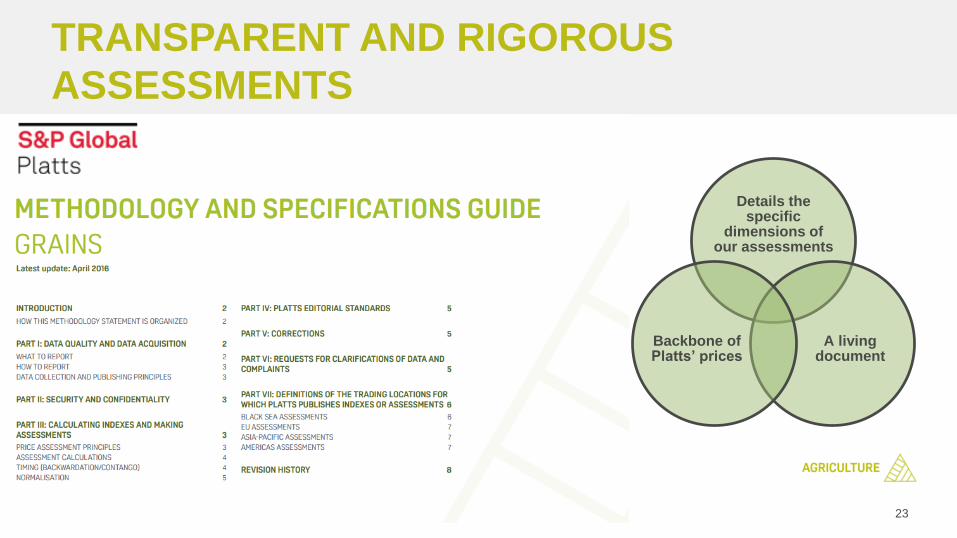

TRANSPARENT AND RIGOROUS

ASSESSMENTS

Details the specific

dimensions of our assessments

A living document

Backbone of Platts’ prices

24

Main applications of an index in the physical cargo market

• Frame agreements (long-term contracts) at “market price” which mitigate price volatility

• Lower-risk, index-linked spot transactions, which help to manage cash flow

• Fixed margins for millers selling flour as a “wheat plus” formula

• Improved “mark-to-market” for risk and accounting functions

• New trading strategies (sell fixed / buy floating priced cargoes in a falling market, for example)

• A reference for current market price (for analysts, investors, traders just returned from

holidays…)

HOW CAN A ROBUST PRICE ASSESSMENT

BE USED?

Other applications of a credible index

• Used in supply contracts as a ‘fall-back’ pricing solution in case of non-agreement

• Used in arbitration for commercial dispute resolution

• Used by governments for royalty calculations & domestic pricing formulas

25

Applications of an index for derivative markets

• The index functions as the underlying price for settlement basis of derivatives

• Used for both OTC (over the counter) paper swaps and exchange-cleared futures & options

• Settlement mechanism tends to use average of the month of index prices

HOW CAN A ROBUST PRICE ASSESSMENT

BE USED FOR HEDGING?

Other points

• Liquidity tends to concentrate in the first few months where spot cargo hedging takes place

• Speculative position-taking in paper markets is an important liquidity provider for market players

seeking true risk management (hedging)

• A forward curve tends to be priced (by brokers & market makers) 1-2 years into the future

• Month, Quarter and Annual contracts help producers/end-users and buyers/sellers to lock in their

price in forward positions, to safeguard margins and smooth their cash flow

EXPLORING THE

POTENTIAL FOR

REGIONAL, CASH-

SETTLED WHEAT FUTURES

27

CASH-SETTLED COMMODITY FUTURES SUIT

MARKETS WITH NON-STANDARD DELIVERY

Sugar, Coffee, Cocoa, Cotton

Wheat, Corn,Soybean, RBOB

Gasoline

Gold, Silver, Copper

Cash-settled futures Physically-delivered futures

Iron ore

Lean HogsEthanol

28

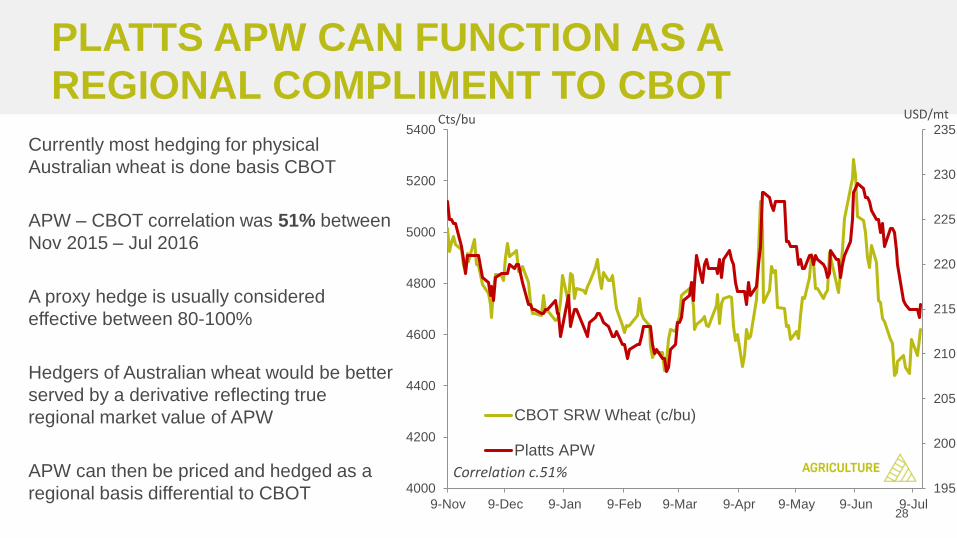

Currently most hedging for physical

Australian wheat is done basis CBOT

APW – CBOT correlation was 51% between

Nov 2015 – Jul 2016

A proxy hedge is usually considered

effective between 80-100%

Hedgers of Australian wheat would be better

served by a derivative reflecting true

regional market value of APW

APW can then be priced and hedged as a

regional basis differential to CBOT

PLATTS APW CAN FUNCTION AS A

REGIONAL COMPLIMENT TO CBOT

Correlation c.51%

Cts/bu USD/mt

195

200

205

210

215

220

225

230

235

4000

4200

4400

4600

4800

5000

5200

5400

9-Nov 9-Dec 9-Jan 9-Feb 9-Mar 9-Apr 9-May 9-Jun 9-Jul

CBOT SRW Wheat (c/bu)

Platts APW

29

Some hedging for physical Russian milling

wheat is done basis MATIF

Platts Rus 12.5 – MATIF correlation was

72% between July 2015 – June 2016

Platts Rus 12.5 – CBOT correlation was

62% between July 2015 – June 2016

A proxy hedge is usually considered

effective between 80-100%

Hedgers of Black Sea wheat would be

better served by a derivative reflecting true

regional market value of Russian milling

wheat

150

160

170

180

190

200

210

220

230

Jul-15 Oct-15 Jan-16 Apr-16

FOB-RMW

$ MATIF

CBOTSRW2 $/mt

$/mt

THE SAME APPLIES IN THE BLACK SEA

PLATTS APW:

SOME METRICS

Daily APW export value is known to core market

traders within 98% accuracy: Platts’ observed

bid-offer range of $4.96/mt on average reflects

competitive pricing at the margin

Observed wheat transactions* occur on average

within $1.01/mt of Platts APW – a consistent

market price is now being discovered

*Includes flat-price ASW and APW cargoes loading out of WA

and SA. Appropriate adjustments were made to account for

quality, loading port, and carry

THE TRUE AUSTRALIAN EXPORT PRICE IS

REASONABLY TRANSPARENT

Best Offer Platts APW

200

205

210

215

220

225

230

235

10-Nov 10-Dec 10-Jan 10-Feb 10-Mar 10-Apr 10-May 10-Jun

32

AUSTRALIAN TRADES**PLATTS-OBSERVED

Australian Trades Volume observed (kt) Number observed

Nov 2015 384 11

Dec 2015 515 15

Jan 2016 690 25

Feb 2016 743 29

Mar 2016 392 15

Apr 2016 380 18

May 2016 613 18

Jun 2016 465 17

TOTAL 4.43 mil mt 159 deals

33

PLATTS APW AT A GLANCE

Quality: Milling wheat, normalized to APW1

Volume: Typical export cargo sizes, normalized to 30,000 mt

Timing: Typical spot cargoes, normalized to a loading 60-90 days ahead of publication date

Location: WA and SA ports, normalized to Kwinana. EC loading monitored for pricing consistency

34

WHERE TO FIND OUR INFORMATION

PDF Wire

35

THANK YOU!

Best Offer APW

Asia-Pacific

Alexis Gan+65 6530 6489

Samar Niazi+65 6216 1192

EMEA

Andrei Agapi+44 207 176 3533

Thomas Houghton+44 207 176 7832

USA

Erik Papke+1 713 658 3228

Sergio Alvarado+1 832 918 3370