australian hotel market update 2015 in review€¦ · 4 performance (year ending dec 2015) source:...

TRANSCRIPT

AUSTRALIAN HOTEL MARKET

UPDATE – 2015 IN REVIEW

Trading, Development and Investment

February 2016

2

1. Australian Hotel Markets Snapshot 1

2. Snapshot per Key Australian Market 2

3. Australian Hotel Development Pipeline 12

4. New Zealand Update 13

5. Australian Hotel Sales 14

6. Australian Hotel Yields 15

7. A Year of Consolidation 17

8. Are We Talking About the Same ADR? 18

9. Australian Outlook for 2016 19

10. CBRE Hotels Services 20

TABLE OF CONTENTS

3

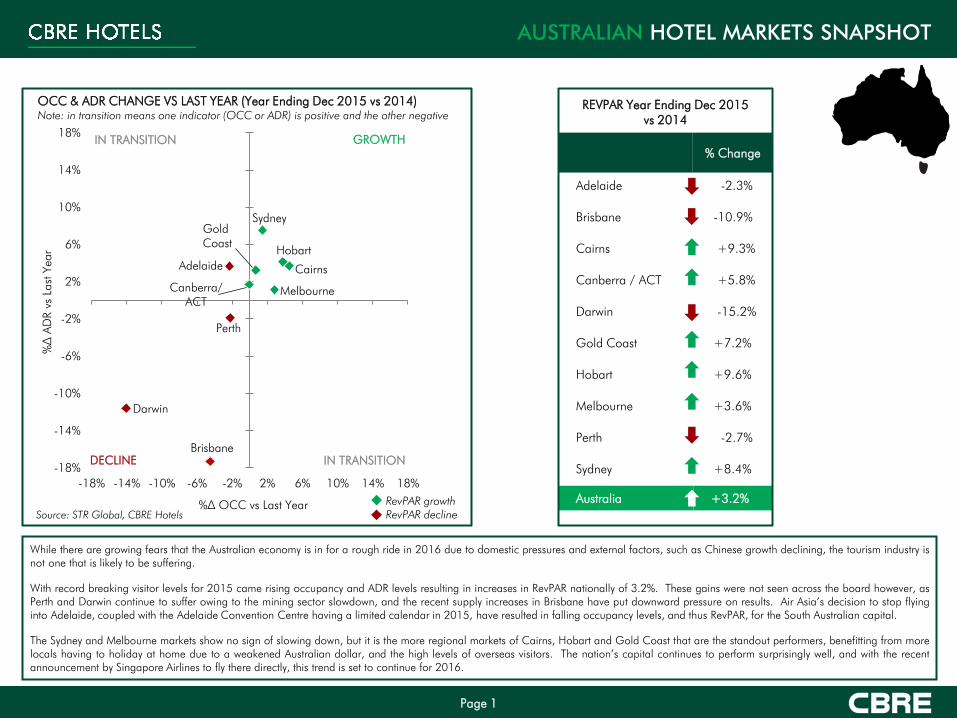

% Change

Adelaide -2.3%

Brisbane -10.9%

Cairns +9.3%

Canberra / ACT +5.8%

Darwin -15.2%

Gold Coast +7.2%

Hobart +9.6%

Melbourne +3.6%

Perth -2.7%

Sydney +8.4%

AUSTRALIAN HOTEL MARKETS SNAPSHOT

Australia +3.2%

Source: STR Global, CBRE Hotels

Page 1

OCC & ADR CHANGE VS LAST YEAR (Year Ending Dec 2015 vs 2014)

Note: in transition means one indicator (OCC or ADR) is positive and the other negative

REVPAR Year Ending Dec 2015

vs 2014

While there are growing fears that the Australian economy is in for a rough ride in 2016 due to domestic pressures and external factors, such as Chinese growth declining, the tourism industry is

not one that is likely to be suffering.

With record breaking visitor levels for 2015 came rising occupancy and ADR levels resulting in increases in RevPAR nationally of 3.2%. These gains were not seen across the board however, as

Perth and Darwin continue to suffer owing to the mining sector slowdown, and the recent supply increases in Brisbane have put downward pressure on results. Air Asia’s decision to stop flying

into Adelaide, coupled with the Adelaide Convention Centre having a limited calendar in 2015, have resulted in falling occupancy levels, and thus RevPAR, for the South Australian capital.

The Sydney and Melbourne markets show no sign of slowing down, but it is the more regional markets of Cairns, Hobart and Gold Coast that are the standout performers, benefitting from more

locals having to holiday at home due to a weakened Australian dollar, and the high levels of overseas visitors. The nation’s capital continues to perform surprisingly well, and with the recent

announcement by Singapore Airlines to fly there directly, this trend is set to continue for 2016.

RevPAR growth

RevPAR decline

Adelaide

Brisbane

Cairns

Canberra/

ACT

Melbourne

Perth

Sydney

Gold

Coast

Darwin

Hobart

-18%

-14%

-10%

-6%

-2%

2%

6%

10%

14%

18%

-18% -14% -10% -6% -2% 2% 6% 10% 14% 18%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

4

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Peppers Adelaide Hotel1 5 202 keys Sep-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 109 (8,191 rooms)

Dominant Source Markets1

1. Victoria

2. New South Wales

3. Queensland

ADELAIDE

ADR

AU$150.14

OCC

76.8%

VS. 2014

-2.3% Length of Stay

2.7 days

Visitors (‘000): 1,178

Visitor Nights (‘000): 3,208

Page 2

The decision by Air Asia to stop flights into Adelaide at the end of 2014 and reduced

conference activity at the Adelaide Convention Centre contributed to decreased room demand

during 2015. The completion of the Adelaide Oval and new footbridge linking the CBD with

that facility were significant in terms of attendances to this venue and will increase substantially

during 2016. The new Adelaide Hospital and adjacent SA University developments will be

completed later in 2016 whilst the new 3,500 seat Plenary Theatre and additional function

space at the Adelaide Convention Centre will be completed in 2017. No new room supply is

expected in 2016; this will provide the market an opportunity to consolidate. The relativity of

the Australian dollar should see increased domestic travel and low oil prices should contribute

to air fare discounting; both are considered beneficial attributes to the Adelaide market.

CBRE Hotels anticipates that 2016 will see growth in both ADR and occupancy reflecting a

RevPAR increase of 2.5% to 3.0%.

REVPAR

AU$115.26

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Source: STR Global, CBRE Hotels 1

Rebrand / Refurbishment

Selected Projects Likely to Proceed

Holiday Inn Express Adelaide 4 245 keys Apr-2017

Aloft Adelaide (New Mayfield) 4.5 200 keys Jan-2018

Lester Hotel 4.5 244 keys 2018

Selected Mooted Projects

Sheraton Adelaide 4.5 160 keys May-2019

Sofitel Adelaide 5 252 keys Jun-2019

Adelaide Airport Hotel 4 260 keys Dec-2025

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

RevPAR growth

RevPAR decline

75%

25%

Visitor Nights

Domestic International

87%

13%

Visitor Arrivals

42%

34%

14%

10%

Purpose of Visit1

Holiday

Business

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-7%

-5%

-3%

-1%

1%

3%

5%

7%

-7% -5% -3% -1% 1% 3% 5% 7%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

5

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Capri by Fraser 4.5 239 keys Mar-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 210 (15,835 rooms)

Dominant Source Markets2

1. Queensland

2. New South Wales

3. Victoria

BRISBANE

ADR

AU$173.57

OCC

74.4%

VS. 2014

-10.9% Length of Stay

2.6 days

Page 3

An increase in room supply over and above demand has seen the Brisbane market occupancy

levels fall and room rates decline as hotels compete for market share. STR Global results for

the 12 months to December 2015 indicate rooms available increased by 6.7% over the same

period in 2014, whilst rooms sold increased by 2.4%, resulting in a decline of 4.0% in

occupancy. Over the same period, room rates declined by 7.2% with RevPAR reflecting a fall

of 10.9%. The RevPAR decline was magnified somewhat as results were measured off 2014

results which was boosted by the G20 held in November 2014. With a number of new

developments under way and significant supply mooted, it is anticipated that ongoing supply

will exceed demand for the medium term, resulting in lower occupancy levels and further

declines in RevPAR. Over the longer term, however, Brisbane’s outlook is considered positive

with increased demand being generated by infrastructure development, new supply and world

class facilities.

REVPAR

AU$129.06

Source: STR Global, CBRE Hotels

Selected Properties Under Construction

Rydges RNA Hotel 4 208 keys Feb-2016

Holiday Inn Express 4 226 keys Jun-2016

Ibis Styles Brisbane 3.5 368 keys 2016

Emporium Southpoint 5 142 keys Dec-2017

W Brisbane 5 305 keys Jan-2018

Selected Projects Likely to Proceed

Westin Brisbane 5 286 keys Jan-2018

42 James Street 5 178 keys Sep-2018

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 2,337

Visitor Nights (‘000): 6,042

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

RevPAR growth

RevPAR decline

71%

29%

Visitor Nights

Domestic International

81%

19%

Visitor Arrivals

41%

38%

11%

10%

Purpose of Visit1

Business

Holiday

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

-13%-11%-9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%13%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

6

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Mooted Projects

Aquis Great Barrier Reef Resort

(8 luxury resorts)

5 7,500 keys 2020

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 92 (7,352 rooms)

Dominant Source Markets1

1. Queensland

2. New South Wales

3. China

CAIRNS

ADR

AU$129.92

OCC

80.6%

VS. 2014

+9.3% Length of Stay

3.5 days

Page 4

Cairns continues to be one of the best performers in the market, exceeding market

expectations and recording a strong recovery from a low base. Based on STR Global results

for the 12 months to December 2015, RevPAR increased by 9.3% with market occupancy of

80.6%; however, ADR and RevPAR remain well below other destinations. Cairns is currently

witnessing a strong rebound in international and domestic tourist arrival numbers as a result of

increased air capacity into the region, especially from Asia. There are a lack of developments

in the pipeline but recent transactions including the Pullman Cairns International and Pacific

Hotel Cairns reflect renewed interest in existing properties and an increase in value levels.

REVPAR

AU$104.77

Source: STR Global, CBRE Hotels

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 1,008

Visitor Nights (‘000): 3,482

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

56% 44%

Visitor Nights

Domestic International

55% 45%

Visitor Arrivals

76%

12%

6%

6%

Purpose of Visit1

Holiday

Business

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

7

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Little National Hotel 4 120 keys Sep-2015

Adobe Narrabundah 4 86 keys Sep-2015

Vibe Hotel Canberra Airport 4.5 191 keys Nov-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 73 (7,032 rooms)

Dominant Source Markets2

1. New South Wales

2. Victoria

3. Queensland

CANBERRA / ACT

ADR

AU$164.19

OCC

73.6%

VS. 2014

+5.8% Length of Stay

2.3 days

Page 5

The nation’s capital posted increases across the major measures of hotel performance,

including occupancy rates at 76.6%, and RevPAR up 5.8% on the same period last year.

These increases are driven mainly by domestic visitors, however with the announcement of

Singapore Airlines flying direct to Canberra from both Singapore and Wellington, expect to

see increases in the number of international visitors in 2016.

New stock is continuing to come into the market, with three new hotels coming online in the

last few months which coincides nicely with the opening of the new Singapore Airline route, so

there should be no supply issues for any potential increases in international visitors.

REVPAR

AU$120.77

Source: STR Global, CBRE Hotels

Selected Properties Under Construction

Mantra Canberra Hotel 4 176 keys Feb-2017

Selected Mooted Projects

Canberra Bowling Club Hotel TBA 80 keys TBA

Campbell 5 TBA 150 keys TBA

Malmo Bruce Hotel TBA 60 keys TBA

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 1,090

Visitor Nights (‘000): 2,533

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

90%

10%

Visitor Nights

Domestic International

94%

6%

Visitor Arrivals

46%

33%

14%

7%

Purpose of Visit1

Business

Holiday

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14 Q4 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

8

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Argus Apartments Darwin

4.5 101 keys Jun-2015

Top End 105 Mitchell Street

4.5 180 keys Aug-2015

Oaks Elan Darwin1

4.5 218 keys Sep-2015

Rydges Palmerston 4 200 keys Sep-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 44 (5,120 rooms)

Dominant Source Markets2

1. Victoria

2. New South Wales

3. Queensland

DARWIN

ADR

AU$170.70

OCC

67.4%

VS. 2014

-15.2% Length of Stay

5.0 days

Page 6

The Darwin market continues its struggles, with both occupancy rates and ADR falling 7.8%

and 7.9% respectively. This in turn has resulted in a further fall of 15.2% in RevPAR compared

to 2014. The contraction in the mining industry has played a big part in this decline, but so

has the increased levels of new supply entering the market.

This decline may well be the market normalizing after better than average results during the

off-peak seasons in recent years and could be a sign of things to come.

REVPAR

AU$114.97

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

2Extension

Selected Properties Under Construction

Club Tropical Resort Darwin2 4 104 TBA

Selected Projects Likely to Proceed

85 Mitchell Street TBA 200 keys Jan-2017

Casuarina Shell Site TBA 175 keys 2018

Gateway Shopping Centre TBA 195 keys 2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 362

Visitor Nights (‘000): 1,799

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

75%

25%

Visitor Nights

Domestic International

87%

13%

Visitor Arrivals

38%

37%

13%

12%

Purpose of Visit1

Holiday

Business

Employment

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-15%

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

15%

-15%-12% -9% -6% -3% 0% 3% 6% 9% 12% 15%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

9

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 170 (17,004 rooms)

Dominant Source Markets2

1. New South Wales

2. Queensland

3. Victoria

GOLD COAST

ADR

AU$174.01

OCC

72.5%

VS. 2014

+7.2% Length of Stay

3.5 days

Page 7

With increased international visitor numbers, the Gold Coast market has recorded an increase

in both occupancy and ADR. STR Global results for the year ending December 2015 reflected

an increase in RevPAR of 7.2%. This recovery has buoyed investor confidence, with a number

of recent transactions reflecting strong growth in value levels. The upcoming 2018

Commonwealth Games will see an expansion of infrastructure including major upgrades to

the airport and will spotlight the destination. The Gold Coast hotel market has enjoyed

relatively stable supply over the last five years and going forward, the supply outlook looks

relatively benign. Increased demand from both domestic and international visitors is expected

to result in continual growth in both occupancy and ADR over the short and medium term.

REVPAR

AU$126.21

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 2,079

Visitor Nights (‘000): 7,263

Selected Properties Under Construction

Jupiter's Casino Hotel2 5 80 Nov-2017

Jewel Luxury Resort 5 153 Dec-2018

Selected Mooted Projects

Orchid Avenue Short Term

Accommodation Building

TBA 178 2018

Source: STR Global, CBRE Hotels 2Extension

74%

26%

Visitor Nights

Domestic International

76%

24%

Visitor Arrivals

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

79%

13%

6% 2%

Purpose of Visit1

Holiday

Business

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-7%

-5%

-3%

-1%

1%

3%

5%

7%

-7% -5% -3% -1% 1% 3% 5% 7%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

10

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Properties Under Construction

Macquarie Wharf Shed Hotel 4.5 114 keys Dec-2016

Crowne Plaza Hobart 4.5 187 keys Oct-2017

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 53 (2,806 rooms)

Dominant Source Markets1

1. Victoria

2. New South Wales

3. Tasmania

HOBART

ADR

AU$163.63

OCC

81.7%

VS. 2014

+9.6% Length of Stay

3.1 days

Page 8

The Hobart market enjoyed a bumper 2015 with average occupancy just below 82% and ADR

growing by 3.8% to $164. The average occupancy level is suggestive of a market which operates

regularly to capacity. It is these peak trading periods which will provide the platform for demand

growth to cater for the new room supply during 2017, 2018 and 2019 which will swell supply by

over 36%. The accolade from Lonely Planet which nominated Tasmania as one of the world’s

‘must-see’ regions in its ‘Best in Travel 2015’ and the visit in November 2014 by China’s

President are two important foundations for inbound growth. Increased domestic airline capacity

and the introduction of direct international flights into Hobart are considered essential to this

market, both are demand sensitive which means that management of Tasmania’s tourism

becomes the most important ingredient to medium term outcomes. CBRE Hotels’ pragmatic view

is that occupancy levels will decline variously by 5% to 8% over the three year supply period

mentioned; the resultant impact on average market RevPAR forecast to fall by 2% to 4% per

annum.

REVPAR

AU$133.65

Source: STR Global, CBRE Hotels

Selected Mooted Projects

HOMO at MONA 4 90 keys May-2017

Former Roberts Building 4 80 keys Aug-2017

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 690

Visitor Nights (‘000): 2,123

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

83%

17%

Visitor Nights

Domestic International

87%

13%

Visitor Arrivals

73%

16%

10%

1%

Purpose of Visit1

Holiday

Business

VFR

Other

Selected Projects Likely to Proceed

Argyle Street

4 120 keys May-2018

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14 Q4 2015

vs '14

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

-11% -9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

11

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

BreakFree on Collins1

4 193 keys Jun-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 365 (32,032 rooms)

Dominant Source Markets1

1. New South Wales

2. Queensland

3. Victoria

MELBOURNE

ADR

AU$186.99

OCC

82.8%

VS. 2014

+3.6% Length of Stay

2.9 days

Page 9

Demand growth is currently constrained by lack of room supply. All facets of room demand

sources are considered strong, with a particular emphasis on inbound tourism. There remains

some price sensitivity in the market however with ADR growth in 2015 reflecting an increase

over 2014 of only 1.3%. During the period 2017 to 2019 it is likely that an additional 3,500

new rooms will be added to supply; this will test market resilience but provide operators with

their first real opportunity to promote Melbourne as a destination with the confidence of

sufficient supply to cater for the demand. Nevertheless, we expect occupancy levels to fall

from the current (2015) level of 83% to the upper mid 70% levels, given the quantity of new

room supply. ADR should register annual growth in the 2% to 3% range. Melbourne’s

calendar remains the envy of other Australian capital cities with a broad base of international

and domestic sporting, cultural and convention based events which has and will continue to

drive high yielding opportunities and provide fertile ground for room demand growth.

REVPAR

AU$154.91

Source: STR Global, CBRE Hotels 1Rebrand / Refurbishment

Selected Properties Under Construction

QT Hotel Melbourne 4 188 keys May-2016

Peppers Docklands 4.5 87 keys Dec-2016

Punt Hill Apartments 4

130 keys Aug-2017

Selected Projects Likely to Proceed

Parkroyal Docklands 5 281 keys Jul-2017

Four Points Docklands 4 320 keys Jan-2017

Aloft Melbourne 4.5 312 keys Aug-2017

80 Collins Street 5 250 keys Sep-2018

Crown Resorts Hotel 4.5 408 keys Jun-2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 5,230

Visitor Nights (‘000): 15,055

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

67%

33%

Visitor Nights

Domestic International

79%

21%

Visitor Arrivals

49%

34%

10%

7%

Purpose of Visit1

Holiday

Business

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14 Q3 2015

vs '14

Q4 2015

vs '14

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

-9% -7% -5% -3% -1% 1% 3% 5% 7% 9%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

12

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

1Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

Alex Hotel 4 74 keys May-2015

Hougoumont Hotel 4 92 keys Jun-2015

Como The Treasury 5 48 keys Sep-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 102 (10,345 rooms)

Dominant Source Markets1

1. Western Australia

2. Queensland

3. New South Wales

PERTH

ADR

AU$196.86

OCC

81.6%

VS. 2014

-2.7% Length of Stay

3.2 days

Page 10

STR Global data indicates that the Perth market continues its slow downward correction

process (post GFC) albeit that the $161 RevPAR achieved in 2015 is second only to Sydney.

The Perth market commands strong demand from the corporate, domestic leisure and

inbound segments. However, it is likely that some 3,000 new rooms will enter the Perth

market over the next five years. CBRE Hotels’ analysis identifies 2017 as a crunch year with

approximately 1,000 rooms to be completed. In CBRE Hotels’ view, the market’s capacity to

absorb such supply will be constrained by airline passenger capacities in the short term;

occupancy levels will decrease to the mid 70% range over the medium term as a consequence

of the new supply, however ADR is anticipated to increase at or around CPI largely because of

the pricing of these new venues and a strengthening inbound market in particular.

REVPAR

AU$160.64

Source: STR Global, CBRE Hotels

Selected Properties Under Construction

Quest West Perth 4 72 keys Jan-2016

Quest East Perth 4 130 keys May-2016

Westin Hotel 5 362 keys 2017

Selected Projects Likely to Proceed

DoubleTree Perth Waterfront 4 247 keys Jun-2016

Ritz Carlton Perth 5 204 keys Jan-2018

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 1,401

Visitor Nights (‘000): 4,554

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

64%

36%

Visitor Nights

Domestic International

80%

20%

Visitor Arrivals

42%

37%

9%

12%

Purpose of Visit1

Business

Holiday

VFR

OtherQ1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-6%

-4%

-2%

0%

2%

4%

6%

-6% -4% -2% 0% 2% 4% 6%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

13

PERFORMANCE (Year Ending Dec 2015)

Source: STR Global, CBRE Hotels

2Based on visitor nights

Source: TRA, CBRE Hotels VFR: Visiting friends and relatives

Selected Recent Openings (in Last 12 Months)

The Tank Stream St Giles 4 282 keys Sep-2015

Greenland Primus Hotel 5 173 keys Sep-2015

SUPPLY (YE Dec 2015)

Existing Hotels, Motels and Serviced Apartments: 358 (39,096 rooms)

Dominant Source Markets2

1. New South Wales

2. Queensland

3. Victoria

SYDNEY

ADR

AU$211.95

OCC

85.3%

VS. 2014

+8.4% Length of Stay

3.0 days

Page 11

Another strong year for the Sydney market sees ADR at record levels and occupancy rates

continuing their climb. With limited new supply coming into the market, these levels are

expected to remain above long term averages. The low Australian dollar relative to major

currencies across the globe, will see increased numbers of international visitors to Sydney

which will further push up daily rates and occupancy levels.

CBRE Hotels understands that a number of existing hotels are planning refurbishment

programs over the next few years, which will have a direct impact on the market during

constrained periods. The refurbished products will re-enter the market with expectations of

achieving high ADR levels, which should also flow through the market.

REVPAR

AU$180.8

Selected Properties Under Construction

Four Points by Sheraton2 4 222 keys 2016

Sofitel Sydney – ICC 5 616 keys 2017

Selected Projects Likely to Proceed

Crown Sydney – Barangaroo 5 350 keys 2019

OCC & ADR CHANGE VS LAST YEAR Note: OCC tracks horizontally and ADR vertically

DEMAND for Hotels, Motels and Serviced Apartments (YE Sep 2015)

Visitors (‘000): 5,928

Visitor Nights (‘000): 17,511

Source: STR Global, CBRE Hotels

2Extension

Selected Properties Exiting Market

The Menzies Hotel 4 -446 keys 2016

Mercure Potts Point 4 -227 keys 2016

Source: STR Global, CBRE Hotels

Note: in transition

means one

indicator (OCC or

ADR) is positive

and the other

negative

RevPAR growth

RevPAR decline

58%

42%

Visitor Nights

Domestic International

73%

27%

Visitor Arrivals

46%

37%

10%

7%

Purpose of Visit1

Holiday

Business

VFR

Other

Q1 2015

vs '14

Q2 2015

vs '14

Q3 2015

vs '14

Q4 2015

vs '14

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

14

AUSTRALIAN HOTEL DEVELOPMENT PIPELINE

Source: STR Global, CBRE Hotels

Whilst there is little change in the net supply for Sydney, the other major cities will experience significant increases in the next few years. This will test the market’s ability

to absorb new supply whilst still maintaining the high levels of occupancy and ADR. Australia’s smaller cities will face a similar issue, in particular Adelaide and Darwin

who are already struggling with increased supply and falling demand. Hobart’s tourism fundamentals are strong and should remain so; however a net supply increase

of 19% will be tough for the market to cope with, and will likely result in falling occupancy rates and thus, RevPAR levels.

Page 12

Key Australian Markets

City Markets Greater City Regions Markets

(including City and Surrounds)

1Net percentage increase on existing supply in respective markets

Note: 'Likely to Proceed' are based on CBRE's estimates of developments more than 50% likely of occurring (not including rebrands) and opening

before Jan 2019. City was selected for Brisbane, Melbourne, Perth and Sydney due to their size.

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Brisbane

City

Melbourne

City

Perth

City

Sydney

City

Num

ber of Room

s

Under Construction Likely to Proceed To Be Removed

+22.7%1

+16.4%1

+26.1%1

+6.4%1

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Adelaide Cairns Canberra /

ACT

Darwin Gold

Coast

Hobart

Num

ber of Room

s

Under Construction Likely to Proceed To Be Removed

+8.4%1

+0.0%1

+2.5%1

+12.9%1

+1.4%1

+19.1%1

15

NEW ZEALAND UPDATE

Double-digit RevPAR growth in most key New Zealand

markets, however Christchurch is experiencing negative

growth.

Page 13

Visitor levels hitting fresh new highs, and a strong economy have helped

key performance indicators for the New Zealand hotel market reach

record highs in 2015.

National occupancy levels maintain their momentum to close 2015 at a

record 77.8%, which beats the previous best of 76% achieved in the 12

months to October 2004. Strong gains for Wellington and Queenstown

of 5.4% and 6.7% respectively are the star performers, whilst Auckland

and Christchurch post small increases.

ADR levels are also continuing their upward trend, reaching NZ$155.97

which is an increase of 9% on 2014, and the highest levels ever achieved.

The strong performances of Auckland, Queenstown and Wellington more

than offset the 4% reduction in ADR posted by Christchurch.

New Zealand’s high level of occupancy and ADR growth have resulted in

yet another record broken with RevPAR increasing 13.4%. At

NZ$121.33, this is the highest level achieved, and is further evidence that

the New Zealand hotel market is booming.

% Change

Auckland +12.9%

Christchurch -3.3%

Queenstown +17.5%

Wellington +15.3%

New Zealand +13.4%

REVPAR

Year Ending Dec 2015 vs 2014

Source: STR Global, CBRE Hotels

OCC & ADR CHANGE VS LAST YEAR (Year Ending Dec 2015 vs 2014)

Note: in transition means one indicator (OCC or ADR) is positive and the other negative

RevPAR growth

RevPAR decline

Auckland

Christchurch

Queenstown

Wellington

-13%

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

-13%-11%-9% -7% -5% -3% -1% 1% 3% 5% 7% 9% 11% 13%

%∆

A

DR vs Last Year

%∆ OCC vs Last Year

GROWTH

DECLINE

IN TRANSITION

IN TRANSITION

16

AUSTRALIAN HOTEL SALES

Total sales expenditure for hotels in Australia in 2015 reached over AU$2.6 billion, the highest level ever recorded.

The overall number of transactions may be down on 2014, primarily due to a lack of available assets rather than a lack of buyers, but the quality of the hotels

transacted has resulted in a record breaking year.

The sales of The Westin Sydney and the Hilton Sydney were the biggest deals of the year, combining for a 30% piece of total transaction expenditure. The lack of

available stock will lead to further decline in the overall number of transactions in 2016, but in turn could see investors having to pay even more of a premium to

secure their piece of the Australian hotel market.

The Ascendas Hospitality Trust and M&L Hospitality portfolios are currently on the market, and are rumoured to be receiving interest from a number of different

parties. Given the size of the holdings in Australia, if they do sell, they will go a long way to helping beat 2015’s sales record.

Page 14

0

10

20

30

40

50

60

0

500

1,000

1,500

2,000

2,500

3,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Nu

mber o

f H

ote

l Sale

s

Tota

l H

ote

l Sa

les (

AU

$ m

illi

on

)

Total Hotel Sales vs Number of Hotels Sold

Total Hotel Sales Total Number of Hotels Sold

Source: CBRE Hotels

17

AUSTRALIAN HOTEL YIELDS

There has been significant tightening of yields in 2015 as a result of some major assets transacting below levels traditionally associated with well performing assets,

most notably The Westin Sydney which traded at less than 4.5%.

Over the last four years there has been a considerable increase in the number of hotels being bought by overseas investors, mainly from Asia, as Australia is seen as a

safe haven, and hotels a sound investment. The widening gap between initial and stabilised yields indicates that investors believe there to be further growth in the

market in the medium to long term.

In previous years yield compression has mostly occurred in the major markets of Sydney and Melbourne, but it is worth noting that regional markets are starting to see

compression and this trend is set to continue as more investors look to regional markets for deals.

Page 15

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Initial Yield to Stabilised Yield Gap

Initial Yield Stabilised Yield

Source: CBRE Hotels

18

Initial Yields 2015 (Notable Sales)

Surfers Paradise Marriott

Resort & Spa

Yield: ~6.0%

Hilton Sydney

Yield: 6.3%

Westend Hotel Sydney

Yield: 6.8%

Quest Dubbo

Yield: 8.7%

Hilton Surfers Paradise

Hotel

Yield: ~6.0%

The Westin Sydney

Yield: 4.2%

Crowne Plaza Surfers

Paradise

Yield: 5.5%

AUSTRALIAN HOTEL YIELDS

The yield profile highlights investors’ willingness to pay a premium for quality assets located in major destinations that have strong market fundamentals. This is not only

true for the more corporate locations of Sydney and Melbourne, but also for the leisure destinations in Queensland as investors look to more regional locations for

investment. The record levels of visitor arrivals coupled with the low supply in Cairns and the Gold Coast should see this trend continue throughout 2016.

Page 16

Source: CBRE Hotels

4% 5% 6% 7% 8% 9%

Pullman Sydney Airport

Yield: 5.6%

Intercontinental Rialto

Yield: 5.8%

Crowne Plaza Melbourne

Yield: 6.6%%

19

The hospitality industry is

awash with talk of whether

home-sharing businesses

such as Airbnb, Stayz and

HomeAway, to name but a

few, are cannibalising the

hotel business. Whilst the

scale of the problem of

home-sharing sites is

constantly debated, there is

no doubt that they have a

disruptive influence on the

industry. Many believe that

home-sharing is only

impacting cheaper brands

targeting leisure travellers,

and not corporate travel.

This may well be the case

but given that many of the

larger brands have low-cost

budget hotels, they are

still facing increasing

competition.

A YEAR OF CONSOLIDATION

Page 17

2015 has been a year of consolidation for the industry. Mergers and acquisitions (M&A) were

sparked in late 2014 when Shanghai Jin Jiang International Hotels Group announced that it

would acquire Louvre Hotels Group and IHG agreed to acquire Kimpton Hotels & Restaurants.

The largest deal announced is that of Marriott International acquiring Starwood Hotels &

Resorts Worldwide – together, it makes them the biggest hotel company worldwide, with more

than one million rooms. This type of consolidation seems to be a growing trend with more

M&As set to be announced in 2016 therefore;

is consolidation the way to combat online travel agencies and home-

sharing sites?

The hotel industry has long been

fragmented, and the merging of brands is

a way to consolidate and increase the

scale of operations without having to buy

land and build. Picking up an existing,

well-established brand allows a company

to circumvent traditional barriers to entry,

and enter new markets where they

previously have not had a presence, with

minimal fuss. This not only increases the

size of their existing pipeline in one fell

swoop, but is a way to improve

economies of scale. And by consolidating

their management and removing

inefficiencies, brands are not only able to

make cost savings across the board, they

are able to redeploy their efforts in

combating the ever increasing problem of

OTAs and home-sharing sites. Size

matters, particularly in the hotel market.

The bigger the brand, the more power it

has to fight the rising tide of OTAs and

home-sharers.

20

The Agency Model is when

a booking agent is paid a

commission by the hotel.

The agent sends the client to

a hotel and the client pays

in full directly to the hotel.

The agent then invoices the

hotel commissions after the

clients departure, and this

commission is expensed as

a room cost.

The Merchant Model is

where the agent receives full

payment from its clients and

proceeds with a booking

order for the hotel at an

after commission (net)

amount.

ARE WE TALKING ABOUT THE SAME ADR?

Page 18

Average Daily Rate (ADR) is a key indicator used to benchmark a hotel’s top line performance

against its competitive set. However, with constantly evolving hotel distribution channels, and

the way each channel transacts its bookings, will the classic ADR formula still work?

Using the ADR formula of gross revenue divided by the total room nights sold, it is evident that

the Merchant Model bookings have a lower ADR compared to the ones that operate under the

Agency Model, assuming every channel charges the same compensation.

The different models have created a grey

zone in recording true ADR value for

hotels as theoretically there should not be

any discrepancies between the two. Third

party online travel agencies (OTAs) are

pertinent to the hotel business, indeed

some small hotels fully rely on attracting

business through OTAs. In Australia

especially, there are various OTAs that

bring different sources of business to

hotels and within them, the operating

models vary from each other.

We have seen markets starting to

benchmark their ADR performance

through the net ADR analysis, which

excludes the commissions from these

channels. This analysis takes into

consideration channel costs and thus

presents a hotel’s true performance and

value that flows to its bottom line.

$100 $100

$25

$75 $75

$0

$20

$40

$60

$80

$100

$120

Room Price Channel

Commission

Net hotel

revenue

ADR Merchant

Model

ADR Agency

Model

AU

D

Merchant vs Agency

21

The Australian hotel market

has maintained its strong

performance in the second

half of 2015 thanks in part

to record international

visitors. The falling

Australian dollar, coupled

with historically low oil

prices making air travel

cheaper, has resulted in

Australia being one of the

places to visit in 2015 with

this trend set to continue

into 2016. The weakened

Australian dollar means

domestic visitors are being

forced to cut back on

international travel, and

holiday locally which in turn

has further boosted

occupancy rates across the

market.

AUSTRALIAN OUTLOOK FOR 2016

Page 19

Recent volatility in global equity markets, particularly in China, and the onset of low-yielding

bond markets serve to increase the appeal of property as an investment class. Australia’s close

trade links to Asia’s developing economies enable it to benefit from Asian growth, whilst at the

same time providing investors with transparent property markets and familiar tax / legal

systems similar to other developed economies. These features have made Australia somewhat

a safe haven for capital allocation to APAC markets – a trend that will continue in 2016 and

beyond.

2015 has been a record year for Australian hotels on many levels as

investors remain optimistic about the potential for further growth

The high number of assets traded in the

last four years means that there is limited

stock available for purchase, and

investors will have to pay above the odds

in order to secure high quality assets in

well located areas. The Westin Sydney

and The Hilton Sydney both went for

above AU$440 million to overseas

investors, and accounted for over 30% of

total sales revenue. Over 75% of all hotel

sales were located in CBDs, whilst just

25% were located in regional areas.

The is no shortage of investment capital

available so we should continue to see

overseas investors looking at further

investment, but investors may well have to

start looking outside the traditional New

South Wales and Victoria CBD markets,

which accounted for 65% of sales last

year, and into the more regional areas of

Cairns and the Gold Coast.

22

CBRE HOTELS SERVICES

Page 20

For more information,

please contact:

CBRE HOTELS

AUSTRALIA

WESLEY MILSOM

National Director, Pacific

O: +61 2 9333 3423

M: +61 408 161 563

CBRE HOTELS

AUSTRALIA

JAEL FISCHER

Senior Analyst

O: +61 2 9333 9095

M: +61 411 798 913

CBRE RESEARCH

AUSTRALIA

BENJAMIN MARTIN-HENRY

Research Manager

O: +61 2 9333 3205

M: +61 415 949 742

Please click on any of the above icons for more information on CBRE Hotels services.

THROUGHOUT THIS PUBLICATION SOURCE: STR GLOBAL, LTD. REPUBLICATION OR OTHER RE-USE OF

THIS DATA WITHOUT THE EXPRESS WRITTEN PERMISSION OF STR GLOBAL IS STRICTLY PROHIBITED.