august 19, 2009 the emerald hotel, bangkok - listed...

TRANSCRIPT

PTT Aromatics and Refining

Public Company Limited

August 19, 2009

The Emerald Hotel, Bangkok

2

Presentation Outline

1. Operational Results

2. Market Outlook

3. PTTAR Strategic Position

3

Operational Results

4

PTTAR – 7th Largest Aromatics Producer in Asia

1.New Aromatics complex –(AR3) started up since Jan. 09, doubling capacity from 1,189 KTA to 2,259 KTA

2.Condensate residue splitter and MEROX complex completed since Mar. 09, will increase Jet and Diesel production capacity from 86 KBD to 138 KBD

3.Plant operation is supported by newly developed global linear programming model, SGS technical advisors and PTTAR dedicated and experienced personnel

5

PTTAR Intake

Plant Operation benefited for full integration

Condensate96 KBD

Crude155 KBD

251 KBD

Condensate95 KBD

Crude146 KBD

241 KBD

Petroleum Products

FO 11% FO 12%

Jet, Diesel, CR 51%

Jet, Diesel, CR 53%

Light Naphtha 25%Light Naphtha

19%

Reformate 10%Reformate 2%

LPG 8% LPG 8%Others 1%

Shut down the HCU to fix the leakage at re-boiler from Apr. 26 to May. 2, 2009

Heavy aromatics is used to blend into fuel oil pool in place of diesel which is more expensive.

With weak gasoline market, Reformate from AR1 is used to top up aromatics units at AR2, maximizing aromatics production while lower condensate intake.

Aromatics Products

212 KBD 185 KBD

Paraxylene57%

Benzene35%

Paraxylene58%

Benzene28%

Cyclohexane 3%Cyclohexane 8%

Others 5% Others 6%

Production Yield

403 K.Ton 474 K.Ton

71% 84%Production Yield 93% 81%

6

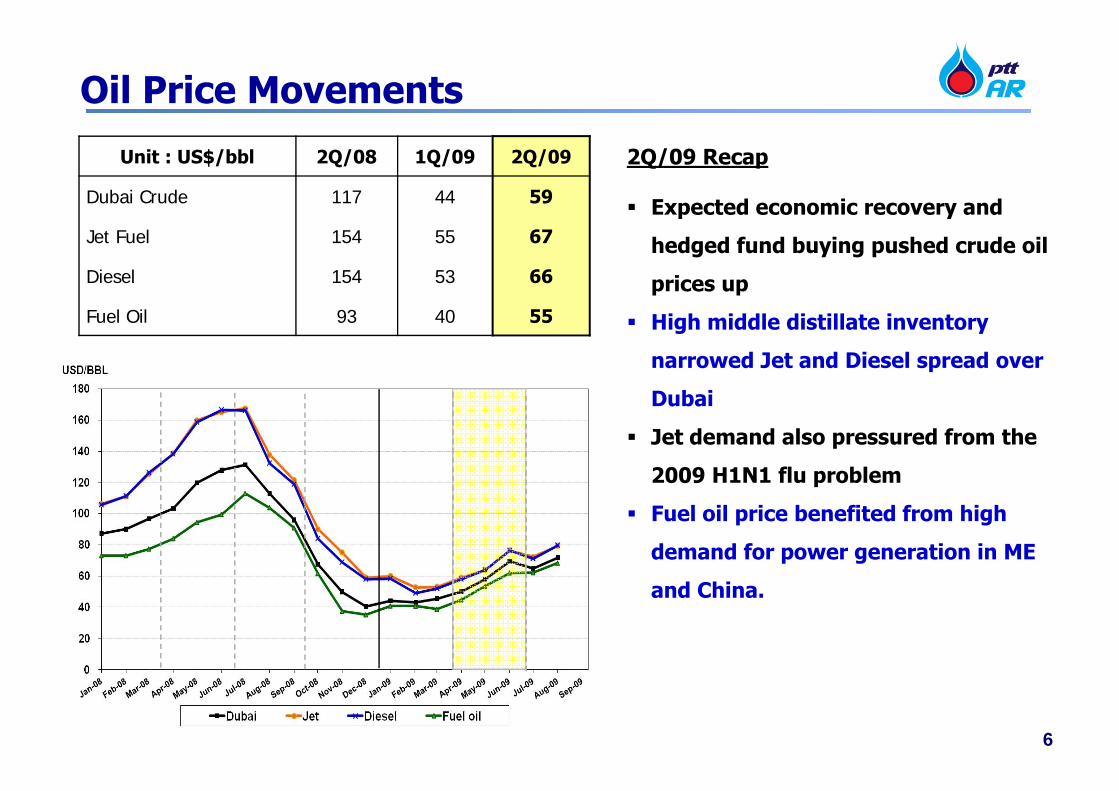

Oil Price Movements

2Q/09 Recap

Expected economic recovery and

hedged fund buying pushed crude oil

prices up

High middle distillate inventory

narrowed Jet and Diesel spread over

Dubai

Jet demand also pressured from the

2009 H1N1 flu problem

Fuel oil price benefited from high

demand for power generation in ME

and China.

Unit : US$/bbl 2Q/08 1Q/09 2Q/09

Dubai Crude 117 44 59

Jet Fuel 154 55 67

Diesel 154 53 66

Fuel Oil 93 40 55

7

Aromatics Price Movements2Q/09 Recap

PX and BZ prices were supported by

strong demand from China

China’s car sales in July grew 71%

YoY

Despite the increase in aromatics

capacities in China, the country

continued to import PX to meet

increasing demand for polyester and

PET resin

Tight supply of PX and BZ supported

strong margins throughout the

quarter

Unit : US$/Ton 2Q/08 1Q/09 2Q/09

Paraxylene 1,427 850 1,059

Benzene 1,219 386 655

Condensate 1,026 397 464

PX – Condensate 401 453 595

BZ – Condensate 193 -11 191

8

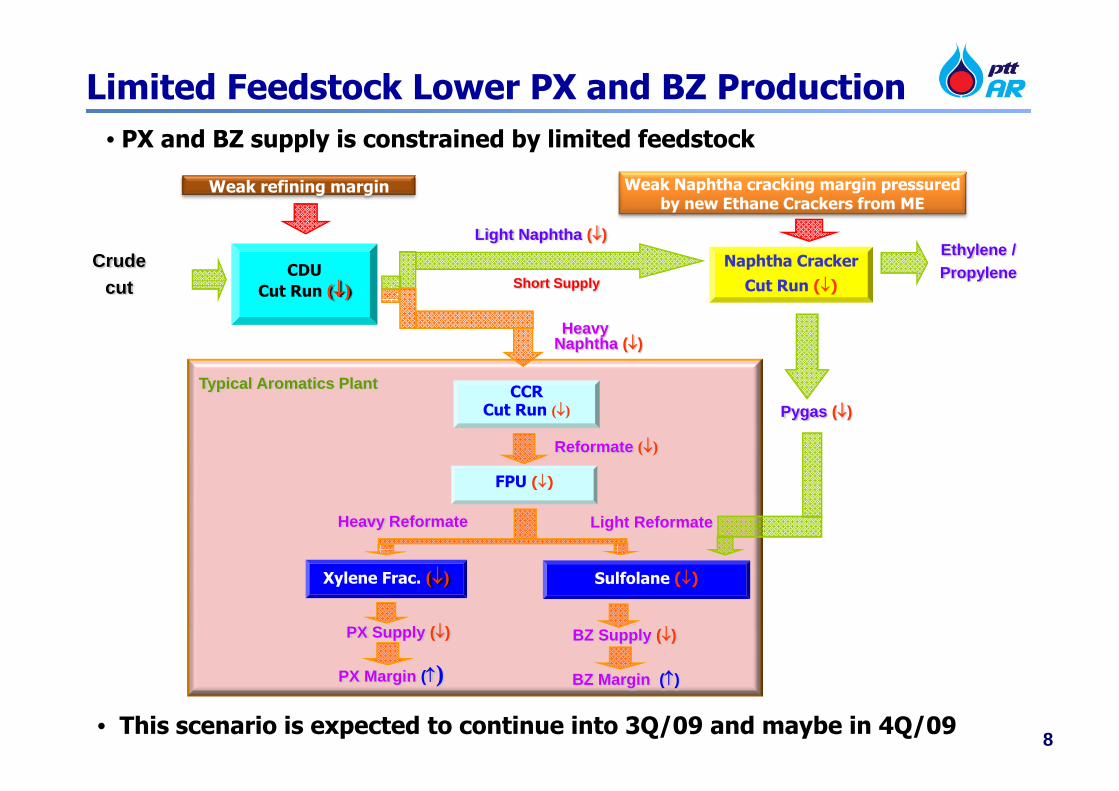

• PX and BZ supply is constrained by limited feedstock

• This scenario is expected to continue into 3Q/09 and maybe in 4Q/09

Weak Naphtha cracking margin pressured by new Ethane Crackers from ME

Weak refining margin

Limited Feedstock Lower PX and BZ Production

Naphtha Cracker Cut Run ()

Light Naphtha ()

Pygas ()

PX Supply () BZ Supply ()

BZ Margin ()PX Margin ()

Heavy Naphtha ()

Short Supply

Ethylene /PropyleneCDU

Cut Run ()

CCR Cut Run ()

Reformate ()

FPU ()

Sulfolane ()Xylene Frac. ()

Typical Aromatics Plant

Heavy Reformate Light Reformate

Crude cut

9

GIMGIM

Unit : $/BBL

7.3

2.295.85 5.23 4.03

(3.32)

3.02

1.22

(1.78)

2.15

10.75

1.78

3.58 6.33 2.66

2Q/08 1Q/09 2Q/09 1H/08 1H/09

Mkt GRM

Hedging

Stock Gain/(Loss) incl LCM

14.73

7.09

10.65 9.78

8.84

Acc. GIM

Improved GIM also resulted from the following initiatives

2Q/09 1H/09

1. Internal Synergy 39.48 54.18

2. Synergy with SPRC and IRPC 1.25 5.28

3. Better Crude Optimization 1.14 2.11

4. PX Yield Improvement 6.73 7.80

Unit: M. US$

Ending Inventory 2Q/09

Volume Cost

Crude 4.39 M.BBL 63.60 $/BBL

Condensate 185 K.Ton 537 $/Ton

10

Risk Management Policy

• To protect downside risk from business plan

• Crack spread hedging approximate 50% of

production

• Hedge PX spread by using crude forward

market in place of condensate

• Explore market mechanism to hedge inventory

risk where possible

11

Realized in 1H/09 gain of 3,344 M.THB,

2Q/09 gain of 928 M.THB

2H/09 current position

Fuel oil Hedged ~2.1 M.bbl

Crack Spread Hedging

Jet Diesel Fuel Oil

Hedging PX – Dubai Spread

Fuel Used Hedging

Risk Management Activities

Feedstock Price Rolling

200

400

600

800

1,000

1,200

29Dec-2Jan

23-27 Feb

16-22 Apr

11-17 Jun

USD/Ton

Dubai Hedging

PX

Rolling prices of feedstock from loading month

to production month

Crude

1Q/09 : 2.2 M.bbl

2Q/09 : 3.0 M.bbl

Condensate

2Q/09: 0.7 M.bbl

Fuel Used in

Production 3%

Minimize cost via

locking Dubai crude

at ~ 50$/bbl

Hedge feedstock

where selling price

are fixed/known

Lock in Dubai price

to secure PX

margin

20

30

40

50

60

70

80 USD/BBL

J F M A M J

J F M A M J

12

Cash CostCash Cost

OPEX

Financing Cost Total Interest and Operating cost

included costs relating to the new CRS

and Merox units but intake into these

unit was not included in the calculation

of cash cost per barrel

2Q/09 average interest cost is 4.19% ,

Fixed : Floated is 43 : 57

Higher interest cost when compared with

2Q/08 was due to higher loan

outstanding related to AR3 and CRS

complex

1.851.38 1.34 1.60 1.36

0.430.89 0.96 0.38 0.93

2Q/08 1Q/09 2Q/09 1H/08 1H/09

Unit : $/BBL

Total Intake

KBD 190 251 241 208 246

2.28 2.27 2.301.98

2.29

13

EBITDA and Net Income Depreciation amounting to 1,258

M.THB , rose from AR3 and CRS

complex

Net foreign exchange gain from US

dollar loans amounting to 896 M.THB

Income tax expense amounting to

1,820 M.THB

EBITDA

7,264

4,754

7,162

10,023 11,916

2Q/08 1Q/09 2Q/09 1H/08 1H/09

Unit : M.THB

Net Income

4,103

1,742

4,214

5,591 5,956

2Q/08 1Q/09 2Q/09 1H/08 1H/09

Unit : M.THB

2Q/08 2Q/09

Gross Profit Margin 12.2% 9.4%

Net Profit Margin 5.5% 8.3%

Interest Coverage Ratio (Times) 30.0 9.5

Financial Ratio

14

Balance Sheet

30 Jun. 09

152,843137,540

Equities

Current Liabilities

Long Term Loan

Other Liabilities

Higher current assets and current

liabilities were due to the increases in

oil and aromatics price as well as

higher volume from AR3

Issued THB Bond 15,000 M.THB to

refinance LT loans 12,367 M.THB and

partially ST loans.

LT loans used for financing fixed

asset amounted to 39,530 M.THB and

the rest used for financing inventory

and Taxes receivable.

Committed line available for draw

down as of 30 Jun.09 is 18,739

M.THB

Fixed Assets

OtherAssets

CurrentAssets

Unit: M.THB

Balance Sheet

31 Dec. 08

Improved Financial Ratio

31Dec.08 30Jun.09

CA/CL ≥ 1 1.1 1.3

Long Term Liability to Equity ≤ 2 1.1 1.0

15

Capex during 2009 – 2013

Long term Loan repayments scheduled for 2010, 2011 and 2012 are 67 M.US$, 79 M.US$, and 402

M.US$ respectively.

Bond 300 M.US$ which will be due in 2012, will be refinanced or rearranged to extend maturity

prior to due date.

Future Capex is expected to be financed primarily by cash flow from operation.

DHDS (Euro IV) EPC contract was signed in July 31, 2009

Unit: M.US$

2008 2010F 2011F 2012F 2013F 2009

Remaining

to 2013F

1 Reformer and Aromatics II and Unwinding 208 16 - 16 - - - - 0

2 Synergy Project (CRS, PSA) 122 14 11 25 - - - - 11

3 Reliability Improvement - - 8 8 7 - - - 15

4 MRU&Hight TAN Project 6 5 1 6 - - - - 1

5 Efficiency Improvement 7 - 5 5 - - - - 5

6 VRU, GT Nox, Biodiesel 11 4 41 45 17 - - - 58

7 DHDS (Euro IV) 3 16 4 20 45 50 75 36 210

8 Investment in PTT Phenol 22 6 10 16 - - - - 10

9 Annual Maintenance Capex and Others - 13 1 14 9 13 14 7 44

Total 379 74 80 155 78 63 89 43 353

2009

Paid Remaining 2009F

16

Market Outlook

17

-10

-5

0

5

10

Q1/0

8

Q2/0

8

Q3/0

8

Q4/0

8

Q1/0

9

Q2/0

9

Q3/0

9

Q4/0

9

Q1/1

0

Q2/1

0

Q3/1

0

Q4/1

0

% G

DP G

rowt

h (%

QoQ)

The “worst” is over?Economics Growth

US• Unemployment rate : First fall in 15 months• Consumer spending : Second consecutive month rise• Home Price Index : First rise since 2006

Europe• Euro zone : Economic sentiment 8 month high.• Germany : June industrial orders rose 7%, biggest gain in 3 years• UK : Monthly industrial production rise

Asia• China : China manufacturing expanded for 5 consecutive

months• Japan : Export increased 14.6% MoM• Thailand : Unemployment rate down 1.4% in June

Emerging & Developing

Advanced Economies

World

Housing Price

USA Unemployment RateSource: US Housing Financing Agency, Nationwide, BoT, RBS

Source: Bureau of Labor Statistics, RBSJuly 2009 Data

18

Really “Green”?

Source: Bloomberg, RBS

19

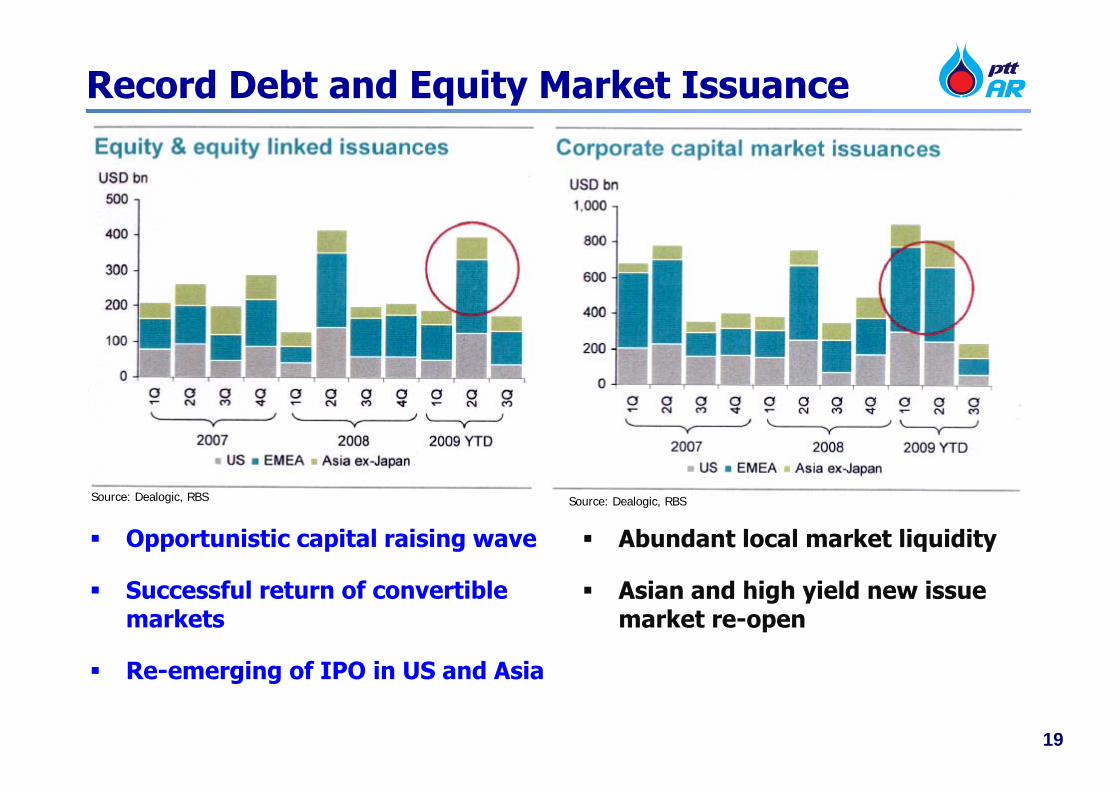

Record Debt and Equity Market Issuance

Source: Dealogic, RBS

Opportunistic capital raising wave

Successful return of convertible markets

Re-emerging of IPO in US and Asia

Abundant local market liquidity

Asian and high yield new issue market re-open

Source: Dealogic, RBS

20

2Q/09 China reported its GDP growth at 7.9%

Policy-driven monetary and credit expansion, has

enabled significant pick-up in domestic investment.

Urban fixed Asset investment growth in June rose

35.3% YoY due to massive government spending

Rmb 1.53 trillion new loans made in June sent money

and loan growth to new record highs of 28.5% YoY

and 34.4% YoY respectively.

Pick-up in domestic demand and restocking have led

value-added industrial output to grow 10.7% YoY in

June. Electricity generation in June, up 3.6% YoY.

China’s car sale in July growth of 71% YoY

• Diesel demand rose by 1.4% in May YoY, while

gasoline demand surge by over 20% YoY.

21

World Oil Forecast for 2010

The Middle Eastern economy will show double growth

compared to 2009, boosting incremental oil demand

to second place behind China.

Most of the growth in oil usage will be in the

transport fuel and petrochemical sectors.

Industrial oil consumption will show only moderate

growth as a result of delayed and slow economic

growth.

The world economic recovery will strengthen in the

second half of the year.

22

World Oil Forecast

Analysts(Reuters Poll)

WTIQ3'09 Q4'09 2009 2010 2011

Barclays 71.0 76.0 63.0 85.0 87.0BNP Paribas 58.0 60.0 55.0 75.0 -Citigroup 60.0 60.0 55.6 65.0 -Credit Suisse 60.0 60.0 55.7 60.0 70.0Deutsche Bank 75.0 75.0 63.3 55.0 80.0EIA 69.0 70.0 60.4 72.4 -Goldman Sachs 70.3 82.5 - 90.2 -JP Morgan 60.0 65.0 55.6 67.5 -MF Global 63.0 65.0 63.0 71.0 -Morgan Stanley 95.0 - 55.0 85.0 95.0RBS 62.0 64.0 57.1 56.0 61.5Soc Gen 65.0 72.5 59.9 82.5 101.0Stan Chart 68.0 75.0 61.0 82.0 85.0UBS 65.0 65.0 58.3 70.0 71.0

Mean 64.8 67.1 58.2 72.7 81.0Previous Mean (June) 42.8 47.4 49.7 66.2 79.4

• Deutsche Bank has the most pessimistic view on economic recovery which will continues to pressure the global oil demand.

• Goldman Sachs focuses their concerns towards the declining in Non-OPEC production and the fast depleting oil fields globally will tighten the future supply.

Unit: US$/bbl

23

Near term CDU additions in Asia Pacific (2009-2010)

2009 :1,576 KBD

2010 :1,007 KBD

(1,300 KBD completed up to now)

24

Complex Margin should rebound

New refining capacities from China

and India are likely to serve their

domestic market

More run cut by simple refineries

are expected as their margin

squeezed

Economic recovery will boost

diesel demand in 2010Source : Nomura International (HK)

Plant Delay and Cancellation

Date Type Refinery Company Capacity Original New

Ann. (KBD) Date Date

Apr-09 Delay Ras Tanura Aramco,Saudi 400 2012 N/A

Apr-09 Delay Al-Shaheen QP,Qatar 250 2010 2011

Mar-09 CancellationAl-Zour KNPC,Kuwait 615 2013 N/A

Mar-09 Delay Port Arthur Motiva,US 325 3Q/10 1Q/12

Mar-09 Delay Pearl GTL Shell,Qatar 140 2010 2011

Feb-09 Delay Detroit Marathon,US 15 2010 2012

Jan-09 Closure Toyama Nippon Oil,Japan 60 Mar-09 Jan-09

Jan-09 Prop. Closure Okayama Nippon Oil,Japan 150 N/A N/A

Refinery Utilization RateGlobal Refining Throughput

25

More impress PX situationIncreasing of imported PX to China

- The new PX will remain in tight supply even after new unit startup because of 3.2 M.Ton of 2009 PX will be offset partly by 3.3 M.Ton from 2009 PTA .

- Reduced output from Naphtha crackers- China’s stimulus package boost polyester demand, resulting in more import volume.

PX Plant Expansion in 2008-20132008 2009 2010 2011 2012 2013

China 104 1,791 1,820 1,100 1,050 760 NE Asia (excluded China) 636 103 - - 600 300 India & Pakistan - - - 417 833 - ME 625 479 1,161 - 100 1,060 SE Asia 115 651 - 40 150 800 Others 42 163 305 347 258 -

Total 1,522 3,187 3,286 1,904 2,991 2,920

PTA Plant Expansion in 2008-20132008 2009 2010 2011 2012 2013

China 1,260 2,017 1,800 213 2,050 3,300 NE Asia (excluded China) 517 200 India & Pakistan 20 625 325 - 1,000 ME 100 100 - - 400 400 Others 129 354 225 2,463 657

Total 2,026 3,296 2,350 2,676 4,107 3,700

PX will remain tight supply by offset PTA

Source : PCI, PTTAR update as of July 2009

Unit : K.Ton

26

China will continue to be the Major PX Consumer

Despite new PX plants built, China still needs to import PX about 2 – 4 million ton per year for the next 5 years

Including PX derivatives, China will consume roughly 55% of global PX production

By 2013, China will be the biggest player in PX market, representing 46% of global PX trade

China PX Pull Through

Dom.PX

Imp.PX

Imp.PTA

Source : CMAI’s 2009 world petrochemical conference, 25 – 26 March 2009

China

RoW

Global PXConsumption

Global PXProduction

(Right Axis)

China compare to rest of the world (RoW)

27

BZ vs Toluene Economic

Source : Dewitt APIC -09

Secondary Source of Benzene

Benzene from coal reduced as steel production declined from the recession

Benzene from Toluene Hydrodealkylation (HDA) Process is not efficient due to high production cost

Primary Source of Benzene

Pygas from Naphtha Cracking is limited by weak Olefins business

Reformate is limited from Refinery low utilization rate

Note: Pygas = Pyrolysis gasolineHDA = Toluene HydrodealkylationTDP = Toluene Disproportionation

MSTDP = Mobil Selective Toluene Disproportionation

Secondary process will be first to shutdown when P2F squeezed. Eventually, ~ 27% of BZ supply potentially disappear.

When GRM soften and refineries cut runs, it will lead to Reformate shortage and therefore limit the Aromatics feedstock supplies and eventually widening PX and BZ spreads.

Secondary Process

28

BZ potential is improving

Source : CMAI , PTTAR update Jun 2-09

BZ demand is expected to improve along with global economics recovery

Low output from Naphtha cracker could support BZ margin

PTT Phenol started up early of March 09 and used 176 KMT BZ from PTTAR (27% of PTTAR BZ production) as feedstock

PTTAR has the flexibility to adjust BZ yield to reflex economics

Under studies to develop BZ downstream derivative cooperation within PTT group

%ORKTA

Incremental Demand & Supply of world BZ

29

PTTAR Strategic Position

30

Unit: KBD

Asian AromaticsDistillation Capacity of Asian RefineriesUnit: KTA

Source : Oil & Gas Journal, Asian Ranking 2009

No.1 in ThailandNo.16 in Asia

No.1 in SE AsiaNo.7 in Asia

Leading in South-East Asia with Cost Competitiveness and High Complexity

Laggards

TH Ref 1

PTTAR

Participants

Aspirers

Leaders

US$/bbl

Source : Wood Mackenzie, 2Q/2008

Net Cash Margin

TH Ref 2 TH Ref 3

Asia Refinery Nelson Complexity Index

Source : Phatra Securities, PTTAR estimates

9.214

Remarks : Nelson Complexity Index measures of the secondary conversion capacity relative to the primary distillation capacity

0 5 10 15

S'pore PetroPetron

FormosaNZ Refining

Esso THS-Oil

SinopecCaltex

Thai OilPTTAR

Reliance

Will be 9.9with DHDS

31

Strategically located with highly advantageous infrastructure

Fully Equipped with Loading and Distribution Facilities

Crude Discharging via Single Point Mooring (SPM)

Products Dispatchingby Rail

Products Dispatching

3 Jetty Facilities

Remark: 1 Acre = 2.53 Rai or 4,048 m2

By Trucks By Pipeline

32

Synergy Projects/OperationCompletion

Date

Benefit

(M.US$/Yr)

1. Oil reserve reduction and Reformate quality control Jan.09 3.4 – 4.2

2. Use Heavy Aromatics in place of Diesel as fuel oil cutter stock Feb.09 13 - 40

3. Adjust process to reduce BZ production from AR2 about 7-15% Feb.09 2.5 - 5

4. Increased Diesel and Jet production approximately 52 KBD via Condensate Residue Upgrading project Mar.09 20-60

5. New condensate tank/Jetty modification project Mar.09 9

6. Mercury Removal project Jul.09 18

7. Chemical Injection for High TAN Crude project Jul.09 0 - 18

8. Hydrogen transfer from AR3 to AR1 & AR2 project Dec.09 18 - 53

Total 83.9 – 207.2

Synergy Benefits

33

Synergy cooperation with PTT group

BZ derivative

Light Naphtha• Swap PTTAR’s Light Naphtha and IRPC’s

Heavy Naphtha to achieve increased yield

for both side ~5 M.US$ per annum

• Co-Load of crude to safe freight

~ 2 – 3 M.US$ per annum

• Jointly review other potential for

intermediate stream exchange including

BZ derivative

• Single Point Mooring (SPM)

• Co-Load of crude

• Intermediate product exchangeSP

Heavy Naphtha

Hydrowax

HVGO

34

Market Summary

1. Dubai is expected to range 65-70 $/bbl in 2H/09.

2. Gasoline will soften in 2H/09 as driving season end while middle distillates

prices will be supported by seasonality and expected economic recovery.

3. Increase in refining capacity will be partly offset by refinery run cuts while

margin remain low.

4. Stimulus package in China is expected to continue to result in strong PX and

BZ demand in 2H/09.

5. Supply of PX & BZ will continue to be limited by lack of feedstock from

refinery and Naphtha Cracker run cuts.

6. PX capacity addition in China will not be sufficient to meet China PX demand

growth

7. Expected economic recovery will further improve overall situation in 2010

onward.

35

PTTAR is well prepared to capture the industry cycle

Strong domestic base customers, connected by pipelines- Strategic Location

Cost Competitiveness

Fully Integrated Refinery/Aromatics Plants- Advantageous size and complexity - Operation Flexibilities - Synergy Benefits

High growth opportunity - Petrochemical downstream derivatives- Further synergy with other company

Strong Management Team with full competence on both Refinery and Aromatics Business