aught hort - rmit universitymams.rmit.edu.au/pvvp5ou0qcic1.pdf · aught hort. 2 marcus banks ... do...

TRANSCRIPT

Exploring the role of small, short-term loansin the lives of Australians

Australian Research Council Linkage Project 0990992

Interim ReportSeptember2011

Marcus Banks

aughthort

2

Marcus Banks

Caught Short:Exploring the role of small, short-term loans in the

lives of Australians, Interim Report

September 2011

RMIT University, Melbourne

3

Contents

Executive summary 4

1 Introduction 62 Methodology 73 The sample 84 Borrowing patterns 115 Borrower attitudes to lenders and loans 196 Borrowers’ ideas and hopes for the future 227 Discussion 22

Tables

1 Some major characteristics of the sample 82 Types of debt mentioned by respondents 133 Why did you take out your first loan? 144 Respondent reasons for taking out a small, short-term loan 155 Patterns of borrowing practices 18

Figures

1 Borrower age 82 Centrelink income support payments or pensions by gender 93 Size of loan 114 Borrowing frequency 115 Borrowing frequency by size of loan 126 Borrowing frequency by receipt of Centrelink payment 127 What is your credit rating, do you have a credit card or a credit card debt? 138 Loan amount by reasons for borrowing 169 Loan frequency by reasons for borrowing 16

10 Borrowing practices by gender 1711 Borrowing practices by receipt of Centrelink payment 1712 Should short-term lenders exist by amounts borrowed 20

4

Executive summaryThis interim report summarises key initial findings of a research project, undertaken byRMIT, Queensland University, National Australia Bank and Good Shepherd Youth & Family Service, investigating the lived experiences of people borrowing small, short-term loans from non-bank companies in Australia. In-depth interviews of 160 borrowers, lenders, regulators, consumer advocates and financial counsellors were mainly conducted in late 2010. A number of the more significant borrowing patterns of 112 individuals are highlighted in the paper, with more brief mention of the attitudes borrowers expressed about their relationships with lenders and their hopes for the future.

Findings

Being ‘caught short’ has structural and personal dimensions. Poverty pervades the lives of most borrowers interviewed: 78 per cent of research participants were receiving a Centrelink payment when interviewed.

The current debate about the impact of payday lending on the lives of many borrowers needs to be reframed from a market to an income security issue. Most people accessing small loans live in such impoverished circumstances that notions of customer choice lose meaning. One of the study’s strongest findings was that many people talked about the lack of choice they had in struggling to manage their finances.

More women (59 per cent) than men (41 per cent) take out payday loans.

People in their 30s (32 per cent) and 40s (24 per cent) were more likely to borrow small, short-term loans than individuals in the 20s (19 per cent), 50s (13 per cent) or those over 60 years of age (12 per cent).

Two fifths of people interviewed had dependent children in their care.

Most people talked about borrowing amounts less than $300 (54 per cent), followed by $301 to $500 loans (21 per cent).

Over half the respondents had taken out more than 10 loans since they had started borrowing from this sector, with many saying they had taken out more than 50 loans.

Few people (7 per cent) had a credit card and over 60 per cent mentioned they had a poor credit rating.

When asked why they first took out a loan, the most commonly cited reasons (food, ‘had no money’, bills and rent) were to meet regular, weekly-type needs and expenses.

People who took out loans below $500 were more likely to spend this money on weekly rather than irregular expenses, as were individuals who had borrowed more than ten loans.

Four themes provide a more complex understanding of a participant’s borrowing practices: one-off, cycling, spiralling or parallel loans:

Less than half (42 per cent) of the respondents reported taking out one or more one-off loans separated by periods of time.

Forty four per cent of people discussed a practice of cycling – how they had immediately taken out a new loan once the previous loan had been paid out.

Twenty three per cent of borrowers became involved in a spiralling process of refinancing the balance of a partially paid-out loan to start a new loan.

A quarter of respondents described how they took out two or more parallel loans from the same or different lenders simultaneously.

5

The comments by many borrowers that they felt ‘caught in a vicious cycle’, of being ‘trapped’ or ‘stuck’ reflect these lending patterns since the majority of respondents were continuously indebted to one or more short-term, small-loan companies for considerable periods of time.

Borrowers’ attitudes about their relationships with short-term lenders and their personal experiences of loans are not readily captured through a binary of positive and negative views. Only a small minority of participants (less than 16 per cent) clearly thought the short-term lending industry should be shut down. Most people had ambiguous and conflicting opinions. There were 71 respondents who expressed positive views about the friendliness of lending staff, but many also perceived that this was also a problem of continually reinforcing their circumstances of being ‘caught short’.

Borrowers who are caught up in highly restrictive financial circumstances are far more likely to support or have ambiguous views about the continued existence of the payday lending industry than individuals who have slightly greater financial resources or options.

Borrowers had many ideas of what would create change in their lives. Gaining employment was overwhelmingly the most commonly cited view, followed by suggestions to increase government support for them to pursue education or on-the-job training, or the personal goal of consolidating their debts.

Ninety nine respondents had often strongly-held opinions about what needs to happen to help people on low incomes. The most common views were:

Increase Centrelink payments and pensions (43 per cent of respondents)

Increased government support for education, training or finding a job (27 per cent)

Centrelink payments be made weekly rather than fortnightly

Centrelink advances be more flexible to reflect respondents’ borrowing practices with small-loan, short-term lenders (23 per cent). Many proposed that smaller amounts (down to $50) be available through Centrelink with short repayment schedules of two to four fortnights.

6

Caught shortExploring the role of small, short-term loans in the lives of Australians________________________________________________________________________

1 Introduction

This interim report highlights a number of key initial findings of a project exploring the experiences of Australians borrowing small, short-term loans from non-bank companies. Funded by a three-year Australian Research Council Linkage grant in 2009, with financial support from Good Shepherd Youth & Family Service and the National Australia Bank, the study investigates the relationships between lenders and borrowers in this sector, their motivations, and the economic circumstances which underlie these interactions. Chief Investigators of this project are Professors Catherine McDonald, Roslyn Russell (RMIT), Howard Karger (University of Queensland) and Greg Marston (QUT). Research support has been provided by Dr Lynda Shevellar (University of Queensland) and Marcus Banks (RMIT). The chief investigators and research partners will present a final report in late 2011, which will incorporate analysis of interviews with lenders, an analysis of the international context of short-term loans and information on the changing policy context in Australia.

The project primarily focuses on the experiences and views of borrowers. What are the current borrowing practices of people taking out small, short-term loans? How do individuals manage their loans and view their relationships with lenders? Why are people borrowing these financial products? What general attitudes do borrowers have towards the industry? Do borrowers think the sector should exist? Have they alternatives?

This report focuses on three themes:

Respondents’ borrowing patterns

Borrower attitudes to lenders and loans

Borrowers’ ideas and hopes of the future

Centrally informing the study are the in-depth interviews researchers have conducted with borrowers, lenders and other industry stakeholders (regulators, consumer advocates and financial counsellors). Of the 160 people interviewed, 112 were individuals who had borrowed between $50 and $1500 from non-bank lenders for short periods of time in three states – Queensland, Victoria and NSW.

The research occurs in the context of a remarkable growth of the payday lendingindustry in the last decade and a current national debate about whether regulatory change is needed in the sector. This study seeks to clarify this discussion by providing academic, evidence-based analysis and evaluation. Until recently, research into borrowers’ experiences with short-term micro-lenders has relied upon initiatives taken by a Victorian advocacy agency, the Consumer Action Law Centre (CALC). Dean Wilson’s 2002 report for CALC was based on three to five minute, street-level surveys of 78

7

people leaving various Victorian payday lending outlets1. Zac Gillam’s updating of this research in 2010 primarily drew on the responses of 448 individuals who had completed a national online survey. Gillam’s main conclusion that small, short-term loans were a form of ‘usury’ having a ‘broad negative impact’ on many borrowers’ livesled CALC to forcefully recommend to the Federal Government it impose an immediate and comprehensive interest rate cap of 48 per cent per annum on micro loans.2 The peak body representing Australian micro lenders has led a vigorous campaign against CALC’s recommendation, claiming the methodology used to capture the data in the 2010 report was unrepresentative of the national borrowing population, ‘misleading’ and ‘biased’.3 The final report of this project will discuss and evaluate these claims and counter claims.

2 Methodology

To initiate and support a more robust methodological and evidentiary inquiry into the sector, a 12-month pilot study was conducted by the University of Queensland during 2009. The methodology piloted by this study, its literature review, and 28 of the face-to-face interviews with borrowers gathered at this time have been critically adapted and employed by the larger ARC project.

The project design applies a mixed-method approach comprising a demographic survey and semi-structured questions to elicit what Sarbin terms ‘storied data’ from the people interviewed4. Borrowers were asked about their previous experiences with money, their present financial and social circumstances, and their thoughts and hopes about the future. Interviews were conducted between July and November 2010 in Queensland, northern NSW and Victoria. A range of methods were used to source borrowers willing to be involved in the project. Approximately 4,000 cards were distributed, supplemented by emailing electronic versions of the card to payday lending outlets, financial counselling agencies, Neighbourhood Houses and other community organisations. A $50 honorarium was offered to prospective interviewees in Victoria. NSW and Queensland borrowers received $40.

1 Wilson, Dean (2002), Payday Lending in Victoria – A Research Report, Consumer Law Centre Victoria Ltd, July 2002, Melbourne, page 15.2 Gillam & the Consumer Action Law Centre (2010), Payday loans: Helping hand or quicksand?, Consumer Action Law Centre, September 2010, Melbourne, pages 30, 218.3 National Financial Services Federation (2010), Failings Flaws and Biased Findings: Review of the Victorian Consumer Action Law Centre Report:, September 2010, Nerang, Queensland.4 Sarbin, TR (1986), ‘The Narrative as a Root Metaphor for Psychology’, in TR Sarbin (ed.), Narrative Psychology: The Storied Nature of Human Conduct, Praeger, New York, pages 3-21.

8

3 The sample

Being ‘caught short’ has structural and personal dimensions. The fact of poverty pervades the lives of most borrowers interviewed. A large majority (78 per cent) of participants were receiving a Centrelink payment or pension. Only nine people owned their homes, with most (75 per cent) renting their accommodation either privately (36 per cent) or publicly (39 per cent). Eight people were homeless. Less than a quarter (24 per cent) had some form of paid employment. Half (48 per cent) the income-supported interviewees had left school by the end of Year 11, compared to only a quarter (28 per cent) of borrowers not in receipt of a Centrelink payment. Table 1 outlines where borrowers were interviewed, their gender and how they found out about the study. Figure 1 details the age groups of participants. About half (47 per cent) of intervieweesreliant on an income security payment were under 40 years of age, compared to two thirds (64 per cent) of borrowers not receiving a Centrelink allowance, payment or pension.

Table 1: some major characteristics of the sample

Interview location Gender

Receiving a Centrelink pension or

payment

How participants found out about the study Total

M F Yes No LendersCommunity

organisationsOther

Brisbane Metro

10 18 21 7 20 0 8 28

Queensland Regional5 8 8 14 2 9 6 1 16

NSWRegional6 3 5 8 0 3 0 5 8

MelbourneMetro

18 26 31 13 24 13 7 44

VictoriaRegional

7 9 13 3 4 10 2 16

Total Respondents

46 66 87 25 60 29 23 112

Figure 1: borrower age7

1012 12

84

0

11

24

15

7

5

40

5

10

15

20

25

30

35

40

21-30 31-40 41-50 51-60 61-70 Over 70

F

M

Number of respondents – 112

5 Including the Gold Coast6 Including one participant who was living in Sydney at the time of the interview.7 One Geelong participant aged 18 was also interviewed. He is included in the 21-30 category.

9

Sixty one per cent of the 87 participants receiving a Centrelink income support payment or pension were women. Men were more likely to be on Newstart Allowance and women on a higher, pension rate of payment. A gender balance existed among the 25 interviewees not reliant on an income security payment.

The proportions of borrowers receiving one of the eight allowances, payments and pensions in Figure 2 differ significantly from the overall Centrelink populations in three of these payment streams. Most strikingly, 37 per cent of income-supported interviewees were Disability Support Pensioners though only 18 per cent of Australians within these payment streams receive DSP. The proportion of borrowers receiving Newstart Allowance was also far higher (30 per cent of the income-supported sample) than in the overall eight-payment population (11 per cent). Conversely, Age/Veterans Affairs Pensioners were highly under-represented in the sample (nine per cent) compared to the wider, eight-payment, population (54 per cent). This disparity was far less pronounced among recipients of Parenting Payment Single (14 per cent of the sample, compared to 10 per cent of the overall population), Parenting Payment Partnered (four per cent of the sample, six per cent of the population) and Carer Payment(four per cent of the sample, three per cent of the population)..8

Figure 2: Centrelink income support payments or pensions by gender

17

11

10

6

5

3

1

15

1

16

2

0

2

4

6

8

10

12

14

16

18

Disability SupportPension

ParentingPayment Single

NewstartAllowance

Age or DVAPension

ParentingPaymentPartnered

Carer Payment Austudy

F M

Number of respondents - 87

Less than a third (31 per cent) of those receiving an income security payment were partnered, compared to about half the participants who did not receive a Centrelink payment. Forty per cent of interviewees (31 women and 14 men) had dependent children in their care. Seventy nine per cent of the participants were born in Australia, 28 per cent spoke a second language at home and 10 interviewees identified as indigenous.

The largest proportion of borrowers (36 per cent) talked about their financial experiences of growing up as average or normal. Thirty per cent of participants considered their family never had much money and 19 per cent said their upbringings

8 Source: Harmer, J (2008), Pension Review. Background Paper. FaHCSIA, Table 1, page 3.

10

were extremely hard. Half the non-income-support borrowers considered they had grown up in financially average or well-off families, compared to a third of interviewees receiving a Centrelink payment.

When asked to recall the most significant events which financially shaped their adult lives, the most common events or factors cited were:

accommodation issues; reduced employment or unemployment; caring for children or losing care of a child; nothing of significance – ‘it’s always been up and down’; getting into or out of drugs, alcohol or gambling; becoming partnered or separated; death of a family member; behaviour of partner, child or parent; and becoming ill, injured or disabled

More participants considered their current financial circumstances were worse than before (46 per cent) than those who thought they were the same (35 per cent) or better (18 per cent). Half the borrowers in receipt of a Centrelink payment had pessimistic assessments of their current financial circumstances, compared to a quarter on non-income-support respondents.

Lenders interviewed for the study thought that a distorted picture of the ‘average’ customer would emerge unless the study directly sourced most participants from payday outlets. A majority (54 per cent) of people interviewed found out about the study from cards displayed in payday outlets or from talking to a researcher situated in an outlet. The rest saw a card or heard about the project from financial counsellors (20 per cent), via word of mouth (10 per cent), newspaper advertising (8 per cent), other community organisations (6 per cent) and the source for three participants is unknown.

Participants who found out about the project at a loans outlet share many common demographic and attitudinal characteristics with interviewees originally contacted through community and financial counselling agencies. A remarkably similar proportion of borrowers in each category were receiving a Centrelink income support payment: 78 per cent of interviewees sourced from lenders compared to 83 per cent from community/financial counselling agencies. The majority of individuals in both groups had taken out more than ten loans since they first started borrowing (57 per cent of people who had found out about the study through a lender and 79 per cent of individuals sourced from community or financial counselling agencies). Among interviewees in stable rental accommodation (74 per cent of the sample) there was little difference between lender-sourced (78 per cent) or agency-sourced (72 per cent) customers.

11

4 Borrowing patterns

There were 47 interviewees who explained how they found out about the lending company they first used. Word of mouth was most commonly (23) cited, followed by seeing an advertisement in a newspaper, on television or online (16) while eight people had walked passed or already knew about a local lender. Interviewees were asked to recall the total number of small, short-term loans they had taken out from payday lenders and the amounts. There were 33 interviewees who had borrowed up to $100 from a lender. The most common loan amount was between $100 and $300 (54 interviewees). Thirty-four people had borrowed $300 to $500, 22 individuals had taken out loans of $500 to $1,000, and 17 had borrowed between one and three thousand dollars (Figure 3). Participants in receipt of a Centrelink payment were more likely to take out loans of $300 or less (59 per cent of loans cited) than over $300 (41 per cent of loans cited). Conversely, non-income-supported interviewees were more likely to mention they had had taken out larger loans of over $300 (60 per cent of all loans this group cited). Seventeen people in the sample had only borrowed one small, short-term loan. Over half the respondents had taken out more than ten loans, with many saying they had received over 50 loans (Figure 4).

Figure 3: size of loan

22

30

22

10 10

10

23

11

127

0

10

20

30

40

50

60

Up to $100 $101 - $300 $301 - $500 $501 - $1000 $1001 - $3000

M

F

Number of responses- 157Figure 4: borrowing frequency

0 1

7

10

3

32

9

2 2

6 7

3

25

00

5

10

15

20

25

30

35

Went throughprocess but

application wasrejected by

Lender

Went throughprocess but

decided againsttaking out a loan

First loan 2-5 loans 6-10 loans More than 10loans - too many

to count

Unsure - can'trecall

F

M

Number of respondents - 107

12

Borrowing frequency did not vary markedly compared to the loan amounts (Figure 5).

Figure 5: borrowing frequency by size of loan

23

2 211

5

8

2

5

10

21

10

5 5

0

5

10

15

20

25

Up to $100 $101 - $300 $301 - $500 $501 - $1000 $1001 - $3000

First loan2-10 loansMore than 10 loans

Number of respondents - 82

Little difference was found between the total number of small, short-term loans people estimated they had ever taken out and whether a participant was receiving a Centrelink income support payment or pension (Figure 6). Similar proportions of non-income supported interviewees (57 per cent) and borrowers receiving a Centrelink payment (63 per cent) had taken out more than 10 loans.

Figure 6: borrowing frequency by receipt of Centrelink payment

9

18

45

4

5

12

0

10

20

30

40

50

60

First loan 2-10 loans More than 10 loans

Receiving a Centrelink payment or pension NoYes

Number of respondents - 93

13

Interviewees were asked to recall the types of outstanding, recurrent or occasional debts they had incurred (Table 2). Few people had a current credit card (8) and 68 respondents commented that they had a poor credit rating, compared to twelve people who thought they had a good credit rating. There were 58 individuals who had utilised a Centrelink advance payment or had a debt with Centrelink, and 44 people had used food or fuel vouchers provided by community organisations

Table 2: types of debt mentioned by respondents

Outstandingdebt

Past debt Total

Borrowing from family & friends 14 28 42NILS type loan 6 3 9House mortgage 6 11 17Rental firms (Radio Rentals, Flexirent etc) 12 1 13Car-related (purchase, maintenance, car fines) 18 6 24Communication-related – internet, phone or Foxtel (not recurrent expenditures on plans), computer

23 5 28

Utility-related – gas, water, electricity or council rates (not recurrent bills)

22 3 25

Other – dentist, optometrist, chemist, veterinarian, landlord or courts

18 18

Personal bank loans or overdrawn accounts 12 13 25Never taken out a bank loan 69

Credit card debt 21 1 22Has a current credit card 8Does not have a current credit card 95Has, or has had, a poor credit rating 68Currently has a good credit rating 12

Centrelink debt or advance 58Number of respondents 112

Male and female respondents had proportionately similar incidences of credit card debt, comparable credit ratings and equally low possession of a current credit card. The ratio of poor to good credit ratings was far higher among Centrelink income support recipients (about 7 to 1) than respondents not receiving these payments (about 3 to 1) (Figure 7).

Figure 7: do you know your credit rating, have you got a current credit card and do you have a credit card debt?

35 4 4

9

13 1210

30

37

53

14

4

8 8

4

0

10

20

30

40

50

60

M F Receiving a Centrelink payment Not receiving a Centrelinkpayment

Have a credit card

Currently have a creditcard debt

Poor credit ratinghistory

Have a good creditrating

Number of respondents - 109

14

Contrary to the Australian industry claim that a payday loan is ‘designed to help meet unexpected expenses’, the seven most commonly cited reasons borrowers gave why they took out their first loan were all to meet regular, weekly-type needs and expenses.9 Significantly, only four people could not remember the events or circumstances which led them to take out their first payday loan (Table 3).

Table 3: Why did you take out your first loan?F M Total

Food 11 7 18

Had no money - 'couldn't make ends meet' 9 7 16

Bills (unspecified) 12 2 14

Utilities and telecommunications bills 5 4 9

Rent 5 3 8

For gambling or due to gambling 4 4 8

Regular children’s expenses 3 4 7

Car registration 3 3 6

To meet Centrelink ‘off-week’ expenses 2 2 4

Relocation expenses: bond or 4 weeks advance rent 3 1 4

Health expenses 3 1 4

Car maintenance or repair 3 0 3

Car purchase or repayments 2 1 3

Relocation expenses: other 2 1 3

Sewerage pump, air conditioner 3 0 3

Furniture 2 1 3

Clothing or shoes 1 2 3

Starting work - work-related expenses 2 1 3

Shopping - Xmas shopping 2 1 3

School expenses 3 0 3

Unidentified one-off items 2 0 2

To pay back debts owed by another person 2 0 2

To pay back money owed to another person 2 0 2

Funeral expenses 2 0 2

Travel expenses 2 0 2

Drugs 1 1 2

Due to reduction in Centrelink payments or less paid work 1 1 2

Petrol 1 1 2

Cigarettes 0 2 2

Birthday 1 0 1

Extra money to meet deposit on a house purchase 0 1 1

For beer or drinking 0 1 1

Business-related expenses 0 1 1

To get a better credit rating 0 1 1

Don't remember 2 2 4

Number of responses 96 56 152

Number of respondents 61 39 100

9 What is microlending?, National Financial Services Federation, http://www.nfsf.org.au/about-microlending-pay-day-advances.htm, accessed 6/7/11.

15

Table 4 captures the reasons given by respondents for all the loans they have taken out, categorised as irregular and regular needs and expenses. Non-income-supported interviewees were somewhat more likely to borrow for irregular expenses (60 per cent of reasons given) than interviewees reliant on a Centrelink payment (50 per cent of reasons given). The final report will discuss these results and compare them with data in other Australian studies.

Table 4: respondent reasons for taking out a small, short-term loan

Irregular needs and expenses F M Total

Car repairs, maintenance, registration or fines 12 4 16Travel expenses 4 6 10Birthday or Christmas presents 6 3 9Hot water system. Whitegoods, computer or sewage pump 6 2 8School expenses 6 0 6Clothing or shoes 5 1 6Car purchase 4 1 5Give money to another person or pay another person's debt 3 2 5To pay back money owed to another person 4 0 4Bond or 4 weeks rent due to moving 3 1 4Funeral expenses 2 2 4Entertainment (eg holiday or night out or books or CDs) 0 4 4Furniture 3 1 4Relocation expenses 2 2 4Starting work - work-related expenses 2 1 3Health expenses 2 1 3'Get a few things done around the house' 1 1 2Pet expenses 0 2 2Unidentified one-off items 1 0 1For wedding 0 1 1To get a better credit rating 0 1 1extra money to meet deposit for house purchase 0 1 1Business-related expenses 0 1 1Number of responses 66 38 104Number of respondents 53 35 88

Regular weekly-type needs and expenses F M Total

Food 18 11 29'Bills' 21 8 29To pay back another loan 13 8 21Had no money or less money 12 8 20Utilities & Telecommunications bills 8 7 15Medical (drugs or regular hospital expenses) 12 3 15Things for the kids and childcare costs 11 4 15Rent 7 7 14For gambling or due to gambling 5 7 12Shopping -'personal goods' - 'day-to-day things' 7 2 9To meet Centrelink off-week gap 4 3 7For illegal drugs 4 3 7Cigarettes 2 3 5Petrol 2 3 5Due to reduced Centrelink payments or lack of maintenance payments 4 1 5Public transport fares 2 1 3For beer or drinking 1 1 2car repayments 2 0 2Heating - air con (often disability related) 1 0 1Unknown 1 0 1Number of responses 137 80 217Number of respondents 48 34 82

16

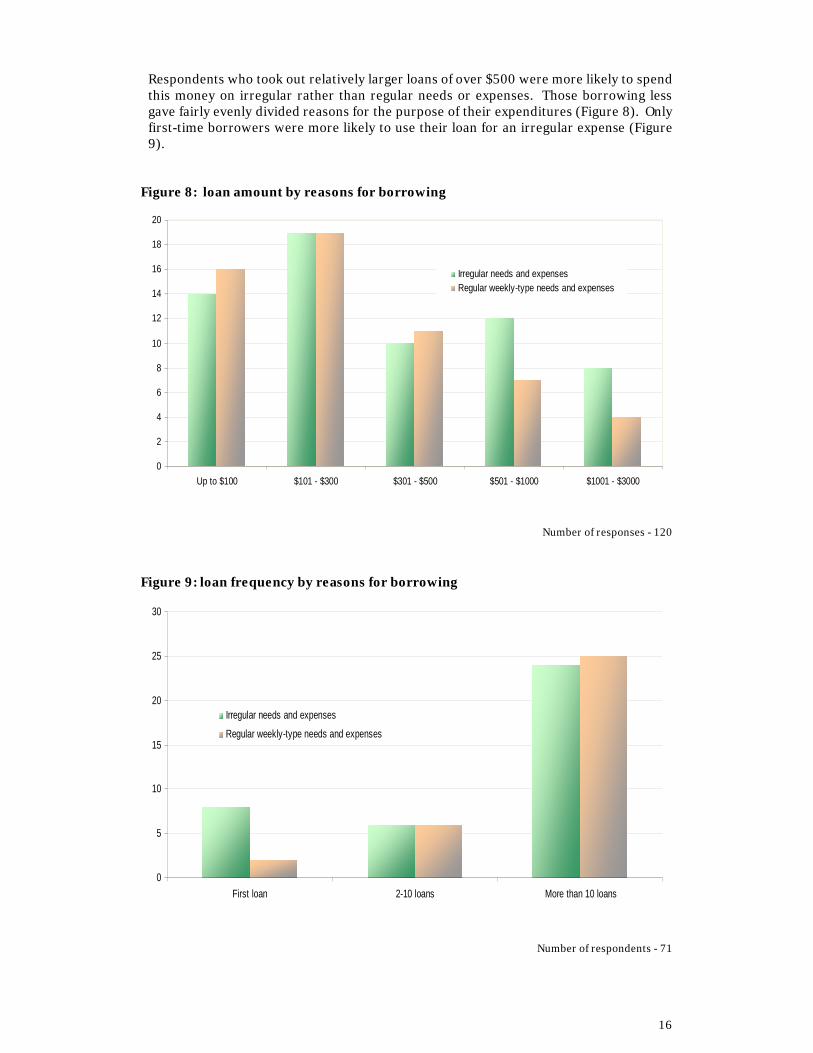

Respondents who took out relatively larger loans of over $500 were more likely to spend this money on irregular rather than regular needs or expenses. Those borrowing less gave fairly evenly divided reasons for the purpose of their expenditures (Figure 8). Only first-time borrowers were more likely to use their loan for an irregular expense (Figure9).

Figure 8: loan amount by reasons for borrowing

0

2

4

6

8

10

12

14

16

18

20

Up to $100 $101 - $300 $301 - $500 $501 - $1000 $1001 - $3000

Irregular needs and expensesRegular weekly-type needs and expenses

Number of responses - 120

Figure 9: loan frequency by reasons for borrowing

0

5

10

15

20

25

30

First loan 2-10 loans More than 10 loans

Irregular needs and expenses

Regular weekly-type needs and expenses

Number of respondents - 71

17

Four themes provide a more complex understanding of a participant’s borrowing practices: one-off, cycling, spiralling or parallel loans. Forty two per cent of borrowers reported taking out one or more one-off loans separated by periods of time. Forty four per cent of people discussed a practice of cycling – how they had immediately taken out a new loan once the previous loan had been paid out. Twenty three per cent became involved in the spiralling process of refinancing the balance of a partially paid-out loan to start a new loan, and a quarter of respondents described how they took out two or more parallel loans from the same or different lenders simultaneously. Men and women in the sample had proportionately similar patterns of borrowing practices (Figure 10) as did participants in receipt of Centrelink payments compared to non-Centrelink borrowers (Figure 11).

Figure 10: borrowing practices by gender

1918

8

11

25

28

1615

0

5

10

15

20

25

30

One-off loans Cycling Spiralling Paralleling

M

F

Number of respondents - 104

Figure 11: borrowing practices by receipt of Centrelink payment

34 34

1920

1012

56

0

5

10

15

20

25

30

35

40

One-off loans Cycling Spiralling Paralleling

Yes

No

Number of respondents - 104

18

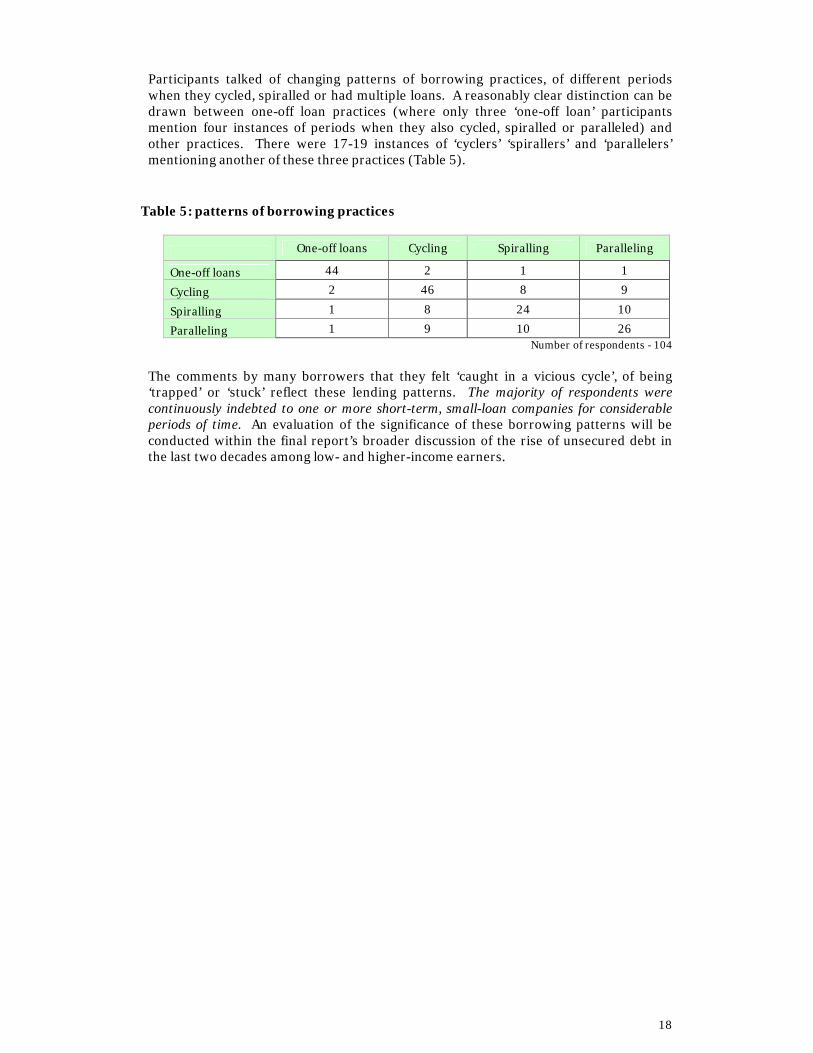

Participants talked of changing patterns of borrowing practices, of different periods when they cycled, spiralled or had multiple loans. A reasonably clear distinction can be drawn between one-off loan practices (where only three ‘one-off loan’ participants mention four instances of periods when they also cycled, spiralled or paralleled) and other practices. There were 17-19 instances of ‘cyclers’ ‘spirallers’ and ‘parallelers’ mentioning another of these three practices (Table 5).

Table 5: patterns of borrowing practices

One-off loans Cycling Spiralling Paralleling

One-off loans 44 2 1 1

Cycling 2 46 8 9

Spiralling 1 8 24 10

Paralleling 1 9 10 26Number of respondents - 104

The comments by many borrowers that they felt ‘caught in a vicious cycle’, of being ‘trapped’ or ‘stuck’ reflect these lending patterns. The majority of respondents were continuously indebted to one or more short-term, small-loan companies for considerable periods of time. An evaluation of the significance of these borrowing patterns will be conducted within the final report’s broader discussion of the rise of unsecured debt in the last two decades among low- and higher-income earners.

19

5 Borrower attitudes to lenders and loans

Respondents were asked to recall and evaluate their experiences of short-term lending processes and loan products. Mixed, contradictory and frequently animated views were held by individuals about their relationships with lending organisations and workers, loan repayments and product information. Clearly negative or positive comments tended to be about specific, concrete aspects of their experiences such as problems with bank or lender dishonour fees or understanding the terms and conditions of a loan. Of the 48 people who specifically discussed the terms and conditions of their loan about half (22) had not adequately understood them.

Borrowers attitudes about their relationships with short-term lenders and their personal experiences of loans are not readily captured through a binary of positive and negative views. Of the 44 people who expressed an opinion about whether payday lenders should exist only a small minority (less than 16 per cent) clearly thought the industry should be shut down. Some interviewees held a reasonably straightforward view supporting the sector, considering lenders ‘essentially smooth out the peaks and troughs in the financial situation of disadvantaged people’ and ‘I think they’re quite good if you really need money, like quickly, then it’s pretty easy to get it through them’. However, most people (about 80 per cent) had ambiguous and conflicting opinions when asked if payday lenders should exist.

I think, like in a perfect world it would be great if they didn’t exist because then people would have enough money – there wouldn’t be that desperation. I mean as long as there’s that desperation and people aren’t earning enough to support themselves, there’s always going to be those people that are going to prey on that need. So, it’s like a necessary evil…I think that they’re filling a gap that the welfare state isn’t providing for(Partnered student in her 20s receiving Austudy).

The data provides some indicative support (though based on small numbers) for the contention that borrowers who are caught up in highly restrictive circumstances are more likely to support the continued existence of the payday lending industry than individuals who have slightly greater financial resources or options:

About 10 per cent of people who described their current financial situation as worse than before (n = 19) thought lenders should be abolished, compared to about a quarter of borrowers whose financial circumstances were either better or the same as before (n = 31);

Similarly, only 7 per cent of ‘cyclers’ said the sector should not exist (n = 15) compared to about 20 per cent of people who took out ‘one-off’ loans (n = 16);

Of people who had borrowed more than ten loans all except one individual said lenders should exist or held ambiguous views (n = 24). In contrast, a quarter of those who had taken out fewer than 10 loans said the lending industry should be abolished (n = 16);

Support for the continuation of the sector was far higher among participants who borrowed up to $300 (where 81 per cent of borrowers were receiving a Centrelink payment) compared to those who took out larger loans (where the proportion of borrowers receiving a Centrelink payment dropped to 66 per cent). Among those who borrowed up to $300 (n = 40), 93 per cent of people supported the continuation of the sector or held ambiguous views, compared to only 62 per cent of those who borrowed more than this amount (n = 29) (Figure 12).

20

Figure 12: should short-term lenders exist by amounts borrowed

37

18

3

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$50 - $300 $301 - $3000

No

Yes or ambiguous

Number of respondents = 69

Five groups of borrower comments (made by 47 respondents) were aggregated into a theme termed ‘specific mention of negative relationship with payday lenders’:

borrower tried to exclude from the process; borrower felt judged by lenders; terms and conditions of the loan not explained properly; borrower felt ashamed about using a payday lender; borrower relationship with lender mainly negative.

The research finds further support for the contention that people who have relatively greater financial resources are more likely to be openly critical of payday lenders than poorer respondents. Over half of non-income-supported interviewees (56 per cent) made at least one negative comment about their relationship with payday lenders under this construct – far higher than the 38 per cent of borrowers receiving a Centrelink payment.

It is within this context that a large number of respondents (71) considered that there were positive aspects of their relationship with their local lender. Many of the same respondents also experienced levels of hassle about the loan product – dishonour fees, unsolicited calls from lenders and other repayment problems but borrowers often tended to separate these issues when evaluating their particular relationship with staff at a local office. Only a dozen borrowers said they had a primarily negative or pragmatic relationship with their lender.

A Melbourne woman in her 50s who was receiving Newstart Allowance talked of her relationship with a Money3 staff member as one of support:

She actually ended up giving me a lot of support where I sit there and talk to her, and when I start getting anxious and everything, and with everyone, you have to produce your bank statements. So they know where your money is going to. And I make no secret that I do actually go out at the pokies, and [name of staff member] says to me, if I want to end up taking out more money or anything, she’ll say to me, no, be careful, don’t start going back to where you were. You’re doing so well with yourself now; don’t go back to where you were. Where I was getting roughly the same support from the girl at Preston,

21

at Cash Converters, but with her giving me the support, she was also giving me the extra money, where it was actually a vicious circle that I kept on going into. As for with Money 3, she was saying, no, you’re doing so well, don’t go getting yourself to go backwards now.

However, many borrowers considered this positive relationship they had with their lender to be part of the larger financial problems they faced.

Well, they were fine, they would bend over backwards to help you. And then when you showed that you could do, you could pay it back and that, they would offer you more (laughs). It was like a vicious circle (Single parent in her 30s receiving Newstart Allowance).

Thirteen people said they felt judged by the lender when they applied for a loan and twenty people commented about how they felt ashamed when going into a short-term lending outlet. However, a more common view was that lending staff were non-judgemental.

Nearly all borrowers who expressed an opinion thought the lending process was fast (23), easy (45) and flexible (28). Like borrowers’ general attitudes whether short-term lenders should exist, these respondents’ comments about the speed, ease or flexibility of the loan process were often highly ambiguous, saying the process was too easy, too flexible or too fast: ‘Yeah, I needs dope. Fuck I've got no money, I'll go visit Village Finance, give me $200…no worries, bang, bang, bang, bang’.

The contradictory relationship most borrowers had with their lenders was less pronounced when respondents talked of their experiences with the loan as a product. While still riddled with ambiguities, their comments were more clearly captured by the research as either positive or negative. Of the 48 respondents who specifically commented on the terms and conditions of their loan less than half (22) had not adequately understood them. Many people (41) talked of the repayment problems they had. This was often due to direct credit transfer issues with the bank, the lender or Centrelink which resulted in dishonour fees or extra charges. About a quarter of respondents specifically talked about how the loans they had taken out had made their lives worse.

22

6 Borrowers’ ideas and hopes of the future

Borrowers had many ideas of what would create change in their lives. Gaining employment was overwhelmingly the most commonly cited view (55 per cent of respondents), followed by suggestions to increase government support for them to pursue education or on-the-job training (19 per cent), and personal goals of consolidating their debts (12 per cent).

Ninety nine respondents had often strongly-held opinions about what needs to happen to help people on low incomes. The most common views were:

Increase Centrelink payments and pensions (43 per cent of respondents)

Increased government support for education, training or finding a job (27 per cent)

Centrelink payments be made weekly rather than fortnightly, and that Centrelink advances be more flexible to reflect their borrowing practices with small-loan, short-term lenders (23 per cent). Many proposed that smaller amounts (down to $50) be available through Centrelink with short repayment schedules of two to four fortnights.

More jobs or more steady jobs (13 per cent)

Ten per cent of people said enough was being done or that no more could be done

Ten per cent called for more affordable housing

Eight per cent of respondents, nearly all women, talked about the need for greater recognition and respect for the circumstances they faced

Seven per cent commented that the minimum wage was too low.

23

7 Discussion

The final report will incorporate policy recommendations, a review of the national/international literature and current legislation, and an analysis of lender interviews. The full report will also explore:

How financial capabilities among borrowers may be strengthened (through more comprehensive social policy programs);

How to enhance borrower access to financial assistance (increasing the amount of income support payments, and access to emergency aid services and microfinance products);

What borrowing impacts problematic gambling, drinking and illegal drug taking practices have among a minority of interviewees; and

Whether policy responses (such as regulation or registration) may curtail cycling, spiralling and paralleling loan practices.

In this interim report we seek to highlight three issues already strongly emerging from the borrower data.

1. The current debate about the impact of payday lending on the lives of many borrowers needs to be reframed from a market to an income security issue. Most people accessing small loans live in such impoverished circumstances that notions of customer choice lose meaning. One of the study’s clearest findings was that many people talked about the lack of options they had in struggling to manage their finances. The language of banking is highly problematic if straightforwardly applied to the small, short-term lending sector. In one sense, the current debate which often equates personal bank loans to payday lenders providing small amounts of money for short periods is analogous to a discussion on housing provision which assumes rents and mortgages are equivalent concepts and practices. One lender interviewed for this research gave a different analogy, saying the loans he provided were more akin to the relatively high cost of hiring a sander from Bunnings for the weekend rather than leasing it for a year or buying it. What is missing from this lender’s account is that no person continually hires a sander every weekend, as is the case with many people borrowing payday loans. Interviewees (frequently receiving Newstart Allowance) commonly pay between $15 and $17.50 to borrow $50 for a fortnight. Should this transaction be compared to a personal loan taken out through a bank? Seen through this lens, a $15 charge for a fortnight’s borrowing of $50 attracts an annual rate of 780 per cent interest. However, interviewees for this research, especially the majority who are in receipt of an income support payment from Centrelink, do not view their loans through such a long-term, abstract lens. Borrowers concretely talked of the amounts they had to repay, the dishonour fees and charges from banks and lenders, and compared these amounts to what they received from Centrelink. That is, they talked about how expensive the loan was as a proportion of what they had to live on. Nevertheless, for the large numbers of borrowers who are regularly in debt to lenders, massively high interest rates increasingly become a reality.

If a comprehensive 48 per cent annualised cap were to be applied and be the only potential source of profit for a lender, then the cost to a person borrowing $50 over two weeks (leaving to one side the struggle to stop bank and lender dishonour fees and charges) would be 92 cents. A 48 per cent cap, of course, would be unprofitable for a sector which deals with high-risk lending practices and would, according to the CEO of a major payday company interviewed for the research, abolish loans below $500. Therefore what is actually at stake in this

24

debate is the existence of payday loans below $500. Those campaigning for a 48 per cent comprehensive cap consider they are supporting borrowers by taking away their access to these lenders. Most borrowers interviewed for this research –particularly those with the least financial means – do not agree with such a unilateral position. Instead, many interviewees have proposed alternatives to help them meet their regular and irregular expenses and needs prior to any movement in this direction.

2. Borrowers requiring a loan to meet one-off household expenses would benefit if the No Interest Loan Scheme were to be expanded, marketed more widely, and provided funds within 24 hours. However, microfinance should not be seen as a replacement to payday lending. Interviewees were twice as likely to take out a loan to help meet their day-to-day, rather than irregular, expenses.

3. Many interviewees clearly indicated that having access to more frequent and flexible Centrelink payments and services would benefit them enormously. Receiving a fortnightly Centrelink payment puts undue financial pressure on many borrowers, particularly in their ‘off-week’. To ease the stress of organising their budgets, respondents clearly support the option of receiving their payments weekly and increasing the scope and flexibility of Centrepay deductions to allow calendar-monthly payments. Access to smaller Centrelink advance payments, repayable over shorter periods of time, was considered a cost-effective, flexible and realistic alternative to market-based sources of finance.

These proposals arising from the borrower data will be more concretely specified as part of the final report’s recommendations. They are raised now as initial, and urgent, contributions to the political and policy debate that is currently unfolding in Australia.