audits of state compensatory education thomas d. canby, jr. director of research and technology...

TRANSCRIPT

1

Audits of State Compensatory Education

Thomas D. Canby, Jr.Director of Research and Technology

TASBO

2

Objectives

• Timeline for audit• Factors trigger an audit• TEA requirements for an audit• Best practices

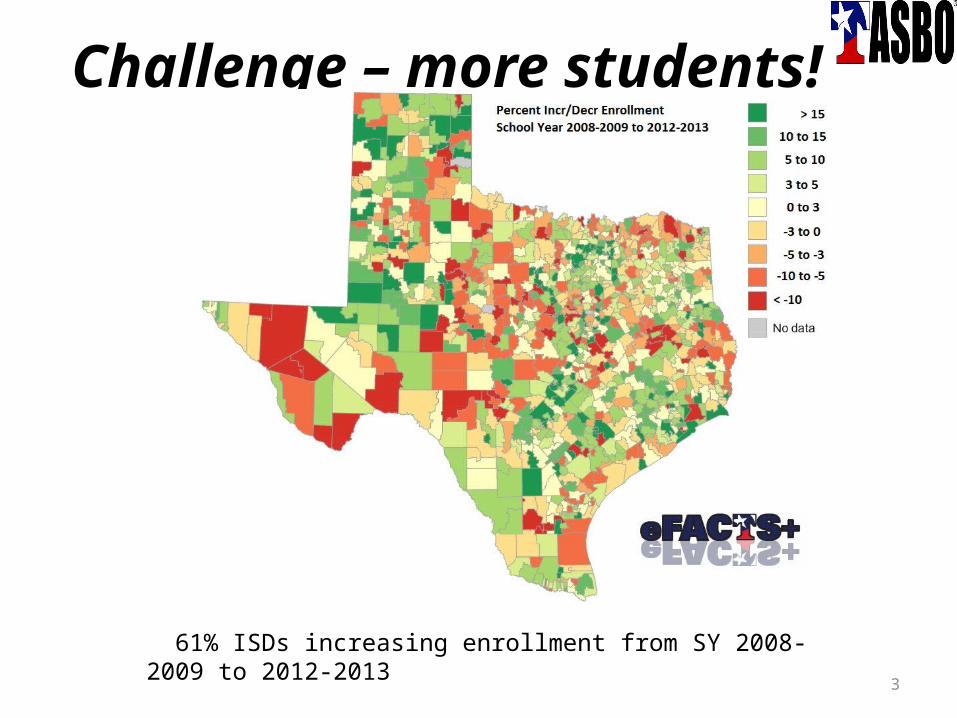

Challenge – more students!

3

61% ISDs increasing enrollment from SY 2008-2009 to 2012-2013

4

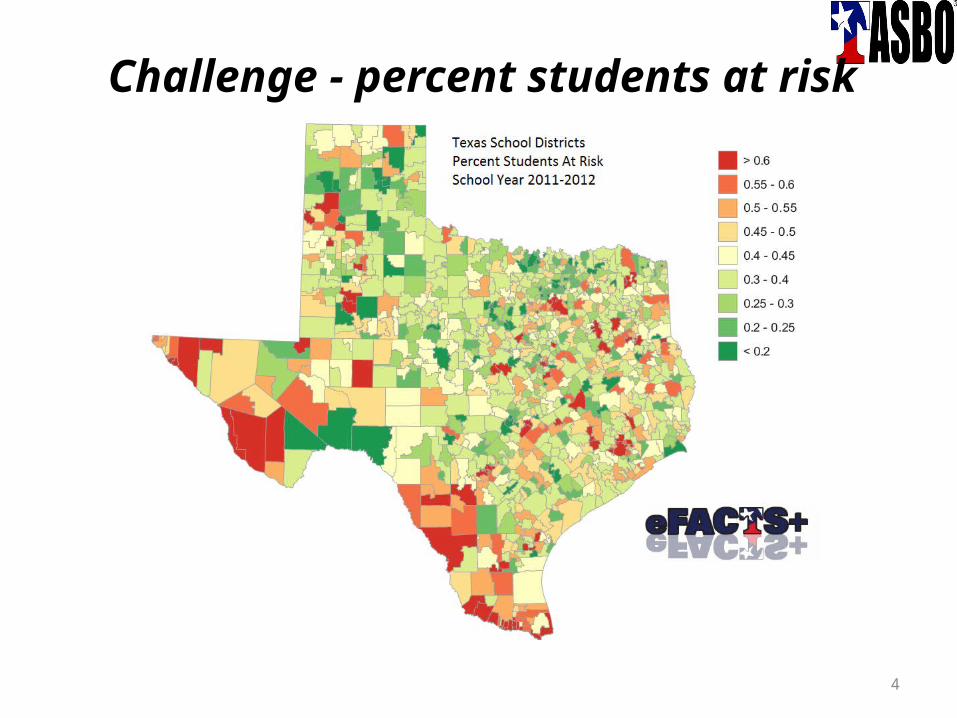

Challenge - percent students at risk

Challenge – changing demographics!

5

TEA AEIS for membership 2001-2001 to 2010-2012

2001-2002 2002-2003 2003-2004 2004-2005 2005-2006 2006-2007 2007-2008 2008-2009 2009-2010 2010-2011 2011-2012 2012-20130

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2,093,511 2,201,534 2,277,9012,394,001 2,503,755 2,540,888 2,572,093 2,681,474

2,848,067 2,909,554 3,008,464 3,058,894

600,922 630,148 660,308 684,007 711,237 731,304 774,719 799,801 815,998 830,795 837,536 864,682

4,146,653 4,239,911 4,311,502 4,383,8714,505,572 4,576,933 4,651,516 4,728,204 4,824,778 4,912,385 4,994,813 5,075,840

Trends for Total Students, Econ Disadv, and LEP

Econ Disadv

LEP

Students

929,187 Students

965,383 Econ Disadv

263,760 LEP

6

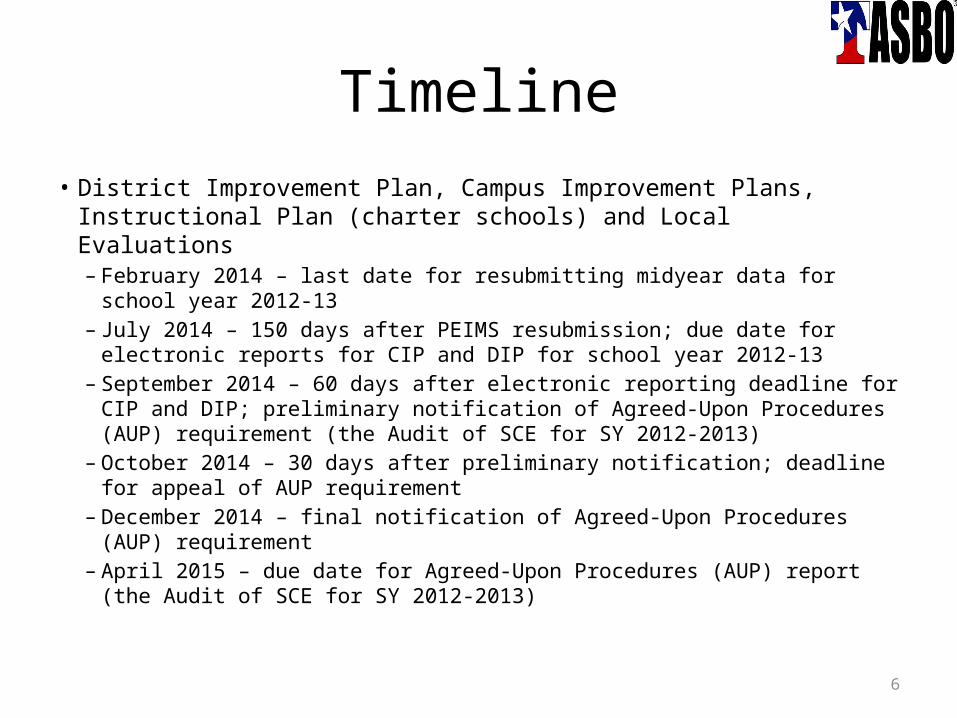

Timeline• District Improvement Plan, Campus Improvement Plans, Instructional

Plan (charter schools) and Local Evaluations– February 2014 – last date for resubmitting midyear data for school year 2012-

13– July 2014 – 150 days after PEIMS resubmission; due date for electronic reports

for CIP and DIP for school year 2012-13– September 2014 – 60 days after electronic reporting deadline for CIP and DIP;

preliminary notification of Agreed-Upon Procedures (AUP) requirement (the Audit of SCE for SY 2012-2013)

– October 2014 – 30 days after preliminary notification; deadline for appeal of AUP requirement

– December 2014 – final notification of Agreed-Upon Procedures (AUP) requirement

– April 2015 – due date for Agreed-Upon Procedures (AUP) report (the Audit of SCE for SY 2012-2013)

7

Risk Factors

• Critical Factors - 6 items• Other Factors – 5 items

• 9.4 SCE Module Exhibit 7

8

Critical Risk Factors

1 Was School FIRST rating above substandard achievement? (This indicator shall apply to charter schools beginning with the 2010-2011 school year)

9

Critical Risk Factors

2 Were actual expenditures reported in PEIMS in the General Fund for state compensatory education-related costs equal to or greater than 52% of the state compensatory education allotment, based upon a three-year average of the LEA’s allotments and actual expenditures? For the 2012-2013 and previous school years, this analysis is based on direct costs equal to or greater than 52% (or applicable percentage for year) of the state compensatory education allotment.

10

Critical Risk Factors

3 Did the school district’s or charter school’s academic rating exceed Academically Unacceptable for the most recent school year that an academic rating was assigned?

11

Critical Risk Factors

4 Was the Annual Financial and Compliance Report (and the Agreed-Upon Procedures Report for State Compensatory Education, if applicable) filed within 30 days after the due date?

12

Critical Risk Factors

5 Did more than 5 at risk students drop out annually over a three-year period OR did 1% or more of the at risk population drop out annually over a three-year period AND did the three-year trend in the dropout rate of at risk students evidence an overall increase in the dropout rate?

13

Critical Risk Factors

6 Did the three-year trend for the at risk population not evidence an overall decrease in TAKS performance?

14

An Audit is Required….

• If one or more critical indicators in Exhibit 7 (indicators one through six) are answered “no”

15

Other Risk Indicators

7 Was the percent of students at risk of dropping out of school less than the threshold value (count of at risk students in the school district or charter school /total students in the school district or charter school)? 59%

16

Other Risk Indicators

8 Was the percent of low income students less than the threshold value? 80%

17

Other Risk Indicators

9 Was the overall student teacher ratio lower than the threshold value? 16.3:1

18

Other Risk Indicators

10 Was the percent of attendance greater than the threshold value? 94.5%

19

Other Risk Indicators

11 Was the percent of limited English proficient students less than the threshold value? 33%

20

An Audit is Required….

• If indicator seven is answered yes and district passed on critical indicators - no audit required

• If indicator seven is answered “no” and one or none of the indicators eight through 11 are answered “yes” - audit is required

21

An Audit is Required….

• If the TEA identifies significant data quality issues relating to staff, students or financial data submitted through the Public Education Information Management System

• If the TEA identifies noncompliance during the course of audit, investigative or monitoring activities of other state and/or federal programs (e.g. Title I, Part A)

• If the most recent agreed-upon procedures engagement submitted to the TEA disclosed significant deficiencies or noncompliance (or if school district or charter school did not submit an agreed-upon procedures report for any subsequent school year in accordance with TEA requirements to obtain a local audit or submitted the report late)

22

An Audit is Required….

• If the school district did not submit district and campus improvement plans or the charter school did not submit instructional plans for the previous school year, in accordance with this section; or

• If the school district or charter school did not submit a local evaluation of state compensatory education strategies, activities and programs for the previous school year, in accordance with this section.

23

Electronic Reporting Requirements

• district improvement plans from school districts,

• campus improvement plans from school districts,

• instructional plans from charter schools, and • local evaluations by school districts and

charter schools of state compensatory education strategies, activities and programs

24

File Local Evaluation

• local evaluation of state compensatory education strategies, activities and programs is required for a school district or a charter school that:– had any low performing campuses or – reported more than 59% at risk students for the

previous school year

25

What About Small Enrollment Entities?

• Exempt from risk assessment and audit if– SCE allotment for prior fiscal year less than

$500,000

• Exemption from audit for small enrollment entities applies unless TEA indicates otherwise

26

Areas Covered in Audit

• Budget• SCE allotment• Expenditures• District and Campus Improvement Plans• Eligible Students• Reporting

27

Areas Covered in Audit

• Budget– Budget managers have SCE allocations for PICs 24,

26, 28, 29 and/or 30– SCE allocations align with supplemental resources

in CIP– SCE allocations align with effective strategies

28

Areas Covered in Audit

• SCE allotment– Allotment agrees with free/reduced priced meal

applications on file for best six month average

29

Areas Covered in Audit

• Expenditures– Year over year change in expenditures for SCE – Expenditures exceeded 52% of SCE allotment in

Foundation School Program Summary of Finances– Expenditures align with supplemental resources in

CIP

30

Areas Covered in Audit

• District and Campus Improvement Plans– Required components in Sections 11.251 – 11.253

Texas Education Code• Comprehensive needs assessment• Identified strategies• Supplemental financial resources• Supplemental staff resources

31

Areas Covered in Audit

• Eligible Students– Identification of students under Section 29.081

TEC– Identification of students at risk to classroom

teachers assigned to SCE strategies

32

Areas Covered in Audit

• Reporting of Expenditures and Student Records– Correct use of program intent codes for expenditures

• Expenditures• Teacher salaries• PIC 30• DAEP• AEP

– Correct use of at-risk indicators for students • (Element ID E0919) and Title I, Part A code (Element ID

E0894) in student data reported in the “Student Data – Enrollment” record (Record Type 110)

33

After Audit

• File audit with TEA– Texas Education Agency Secure Environment

(TEASE) AUDIT account

• Access electronic library of DIPS, CIPs, Evaluations and Audits– http://tuna.tea.state.tx.us/audit/PDFviewer.asp– Select fiscal year– Select 6 digit county-district number

34

After TEA Review

• TEA will determine – No action necessary– Action necessary • Informal monitoring • Recommended training• Recommended assistance from outside consultants• Financial penalties• Accreditation actions

35

• Distribute and collect signed job descriptions for staff for current position – keep current with changes in funding and/or assignments (HR)

• Track and document expenditures related to instructional settings for students at risk by locally defined fields

• Evaluate effectiveness and cost of various instructional settings

• Benchmark and compare characteristics and performance to comparable districts and campuses

Best Practices

36

Resources• TEA State Compensatory Education Module of Financial

Accountability System Resource Guide• Questions regarding the SCE Program, student identification - Consult

with your ESC State Comp. Ed. contact

• Questions regarding DIPs/CIPs – contact your ESC State Comp. Ed. contact

• Questions regarding SCE audits or D/CIPs submission - contact the Division of Financial Compliance at 512-463-9095

• Questions regarding Title I - Consult with your ESC Title I contact or the NCLB Division at 512-463-9414

• TEA Best Practices Clearinghouse• Check the Financial Compliance web site at:• http://www.tea.state.tx.us/index4.aspx?id=3819

37

Questions ?

38

Presenter Contact Information

Tom CanbyDirector of Research and TechTASBO2538 S. Congress Ave.Austin, Texas 78704

(512) 462 1711