audit focuses under the new mfrs - msra

TRANSCRIPT

Audit focuses under the new MFRS

Speaker: Charles Fung [email protected]

18 September 2019

18 Sept 2019 1 Audit focuses under the new MFRS

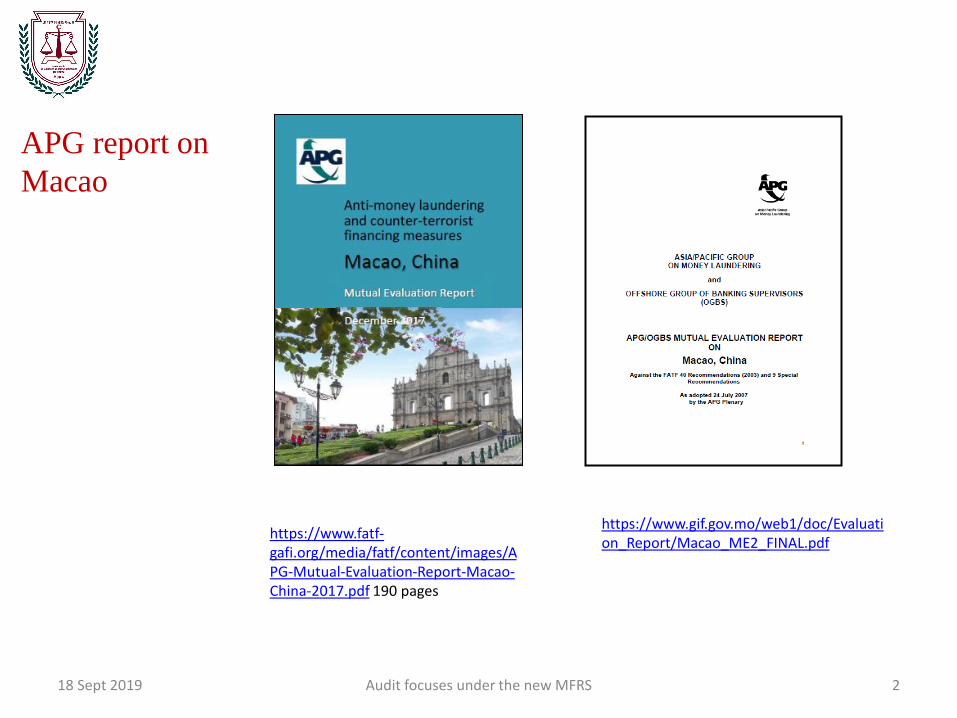

APG report on

Macao

18 Sept 2019 Audit focuses under the new MFRS 2

https://www.fatf-gafi.org/media/fatf/content/images/APG-Mutual-Evaluation-Report-Macao-China-2017.pdf 190 pages

https://www.gif.gov.mo/web1/doc/Evaluation_Report/Macao_ME2_FINAL.pdf

To highlight the key audit considerations when the new MFRS becomes effective

Objective of

today's

presentation

18 Sept 2019 Audit focuses under the new MFRS 3

• An overview of the new MFRS

• Characteristics of Macau accountancy environment

• Key impacts of the New MFRS on financial reporting of a majority of Macau companies

• Auditing a group

• Auditing Accounting Estimates

• Auditing Related Party Transactions

• Commercial Code considerations

• A personal perspective of possible audit implications arising from the new MFRS

Today’s agenda

18 Sept 2019 Audit focuses under the new MFRS 4

An overview of the new MFRS

18 Sept 2019 5 Audit focuses under the new MFRS

新的MFRS採納IFRS (紅皮書) 2015年版內的

• 概念框架 (Conceptual Framework for Financial Reporting 2010) Note: The Framework has been further updated in 2018.

• 15 項國際財務報告準則(IFRS)

• 26 項國際會計準則(IAS)

• 21 項解釋公告(Interpretations)(IFRIC)

MFRS 新發展

18 Sept 2019 Audit focuses under the new MFRS 6

High level comparison between the existing and the new MFRS

現行的 MFRS 新的 MFRS

概念框架 (Conceptual Framework for Financial Reporting)

1997年版

2010年版

國際財務報告準則 (IFRS) 1 項 15 項

國際會計準則 (IAS) 15 項 26 項

解釋公告 (Interpretations)(IFRIC) 0 項 21 項

18 Sept 2019 Audit focuses under the new MFRS 7

2015 年版國際財務報告準則(IFRS)

IFRS 1: 首次採用國際財務報告準則* IFRS 9: 金融工具

IFRS 2: 以股份為基礎的支付 IFRS 10: 合併財務報表

IFRS 3: 企業合併 IFRS 11: 合營安排

IFRS 4: 保險合同 IFRS 12: 在其他主體中權益的披露

IFRS 5: 持有待售的非流動資產和終止經營 IFRS 13: 公允價值計量

IFRS 6: 礦產資源的勘探和評價 IFRS 14: 遞延管制帳戶

IFRS 7: 金融工具:披露 IFRS 15: 客戶合同收入

IFRS 8: 經營分部

Note: * Only IFRS 1 is included in the existing MFRS.

18 Sept 2019 Audit focuses under the new MFRS 8

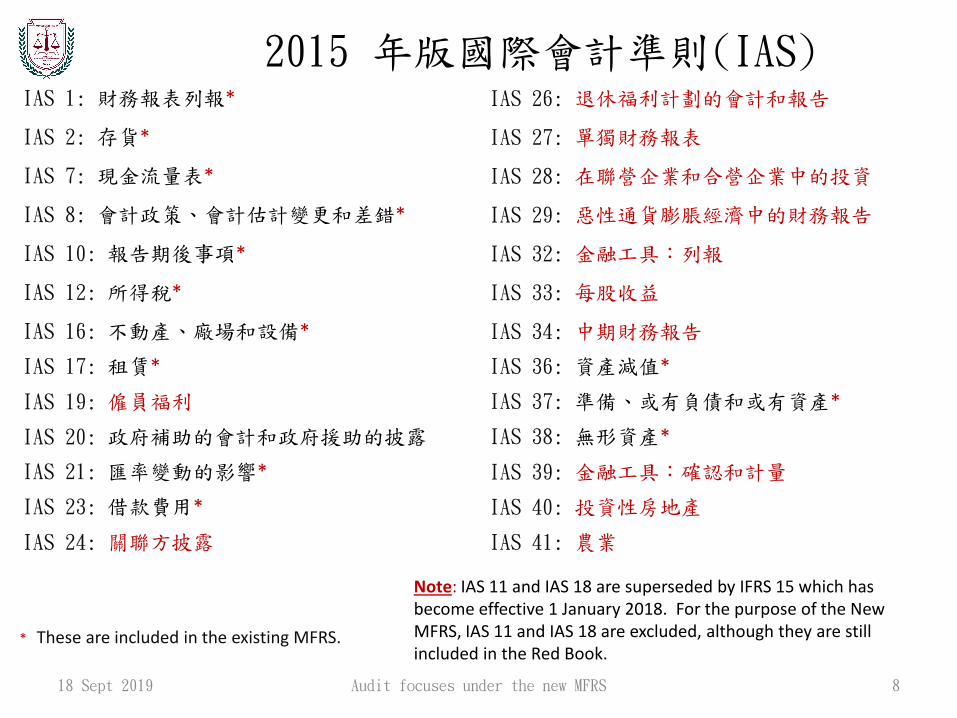

2015 年版國際會計準則(IAS) IAS 1: 財務報表列報* IAS 26: 退休福利計劃的會計和報告

IAS 2: 存貨* IAS 27: 單獨財務報表

IAS 7: 現金流量表* IAS 28: 在聯營企業和合營企業中的投資

IAS 8: 會計政策、會計估計變更和差錯* IAS 29: 惡性通貨膨脹經濟中的財務報告

IAS 10: 報告期後事項* IAS 32: 金融工具:列報

IAS 12: 所得稅* IAS 33: 每股收益

IAS 16: 不動產、廠場和設備* IAS 34: 中期財務報告

IAS 17: 租賃* IAS 36: 資產減值*

IAS 19: 僱員福利 IAS 37: 準備、或有負債和或有資產*

IAS 20: 政府補助的會計和政府援助的披露 IAS 38: 無形資產*

IAS 21: 匯率變動的影響* IAS 39: 金融工具:確認和計量

IAS 23: 借款費用* IAS 40: 投資性房地產

IAS 24: 關聯方披露 IAS 41: 農業

* These are included in the existing MFRS.

Note: IAS 11 and IAS 18 are superseded by IFRS 15 which has become effective 1 January 2018. For the purpose of the New MFRS, IAS 11 and IAS 18 are excluded, although they are still included in the Red Book.

18 Sept 2019 Audit focuses under the new MFRS 9

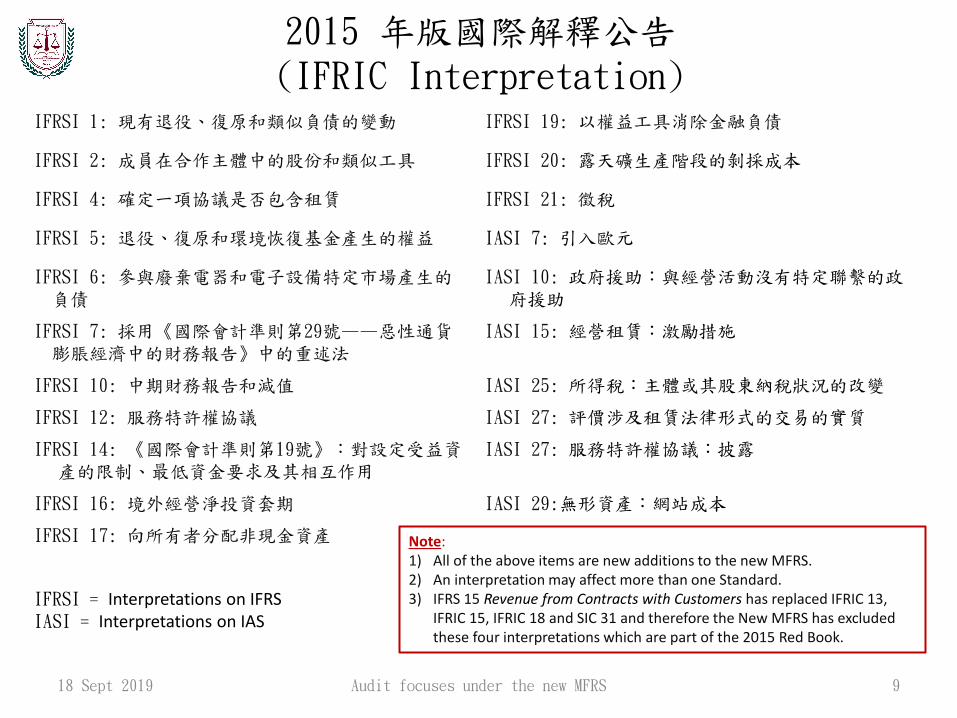

2015 年版國際解釋公告 (IFRIC Interpretation)

IFRSI 1: 現有退役、復原和類似負債的變動 IFRSI 19: 以權益工具消除金融負債

IFRSI 2: 成員在合作主體中的股份和類似工具 IFRSI 20: 露天礦生產階段的剝採成本

IFRSI 4: 確定一項協議是否包含租賃 IFRSI 21: 徵稅

IFRSI 5: 退役、復原和環境恢復基金產生的權益 IASI 7: 引入歐元

IFRSI 6: 參與廢棄電器和電子設備特定市場產生的負債

IASI 10: 政府援助:與經營活動沒有特定聯繫的政府援助

IFRSI 7: 採用《國際會計準則第29號——惡性通貨膨脹經濟中的財務報告》中的重述法

IASI 15: 經營租賃:激勵措施

IFRSI 10: 中期財務報告和減值 IASI 25: 所得稅:主體或其股東納稅狀況的改變

IFRSI 12: 服務特許權協議 IASI 27: 評價涉及租賃法律形式的交易的實質

IFRSI 14: 《國際會計準則第19號》:對設定受益資產的限制、最低資金要求及其相互作用

IASI 27: 服務特許權協議:披露

IFRSI 16: 境外經營淨投資套期 IASI 29:無形資產:網站成本

IFRSI 17: 向所有者分配非現金資產

IFRSI = Interpretations on IFRS IASI = Interpretations on IAS

Note: 1) All of the above items are new additions to the new MFRS. 2) An interpretation may affect more than one Standard. 3) IFRS 15 Revenue from Contracts with Customers has replaced IFRIC 13,

IFRIC 15, IFRIC 18 and SIC 31 and therefore the New MFRS has excluded these four interpretations which are part of the 2015 Red Book.

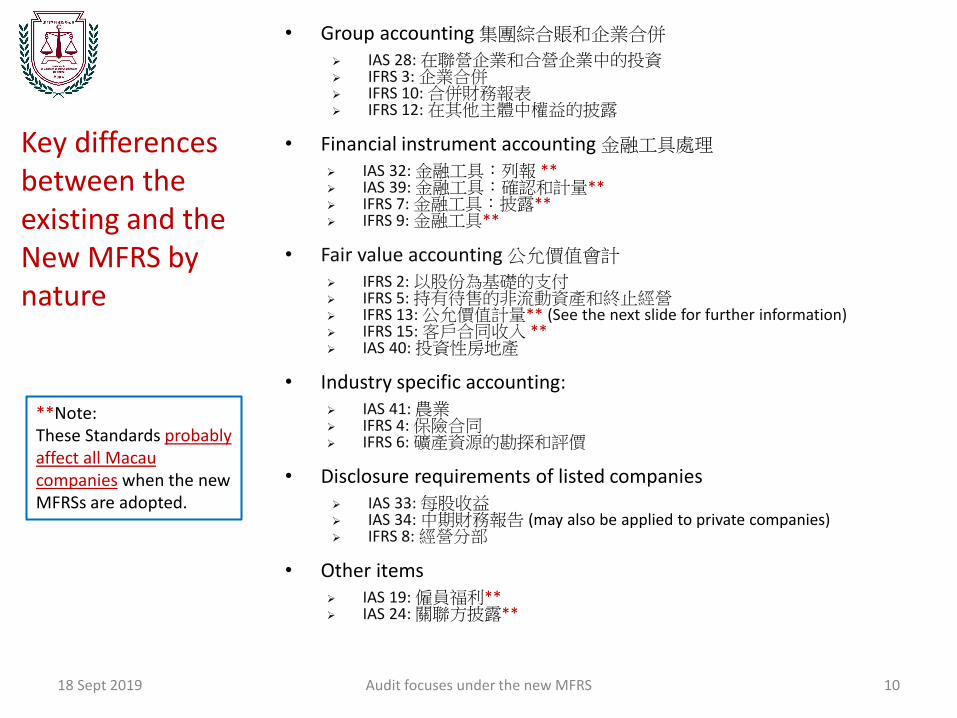

• Group accounting 集團綜合賬和企業合併

IAS 28: 在聯營企業和合營企業中的投資 IFRS 3: 企業合併 IFRS 10: 合併財務報表 IFRS 12: 在其他主體中權益的披露

• Financial instrument accounting 金融工具處理

IAS 32: 金融工具:列報 ** IAS 39: 金融工具:確認和計量** IFRS 7: 金融工具:披露** IFRS 9: 金融工具**

• Fair value accounting 公允價值會計

IFRS 2: 以股份為基礎的支付 IFRS 5: 持有待售的非流動資產和終止經營 IFRS 13: 公允價值計量** (See the next slide for further information) IFRS 15: 客戶合同收入 ** IAS 40: 投資性房地產

• Industry specific accounting: IAS 41: 農業 IFRS 4: 保險合同 IFRS 6: 礦產資源的勘探和評價

• Disclosure requirements of listed companies IAS 33: 每股收益 IAS 34: 中期財務報告 (may also be applied to private companies) IFRS 8: 經營分部

• Other items IAS 19: 僱員福利** IAS 24: 關聯方披露**

Key differences between the existing and the New MFRS by nature

18 Sept 2019 Audit focuses under the new MFRS 10

**Note: These Standards probably affect all Macau companies when the new MFRSs are adopted.

18 Sept 2019 Audit focuses under the new MFRS 11

Significant items that call for the use of fair value in accordance with IFRS 13

Source: https://www.pwc.com/us/en/cfodirect/assets/pdf/accounting-guides/fair-value-measurements-global-guide.pdf

IAS 18 has been

superseded by

IFRS 15

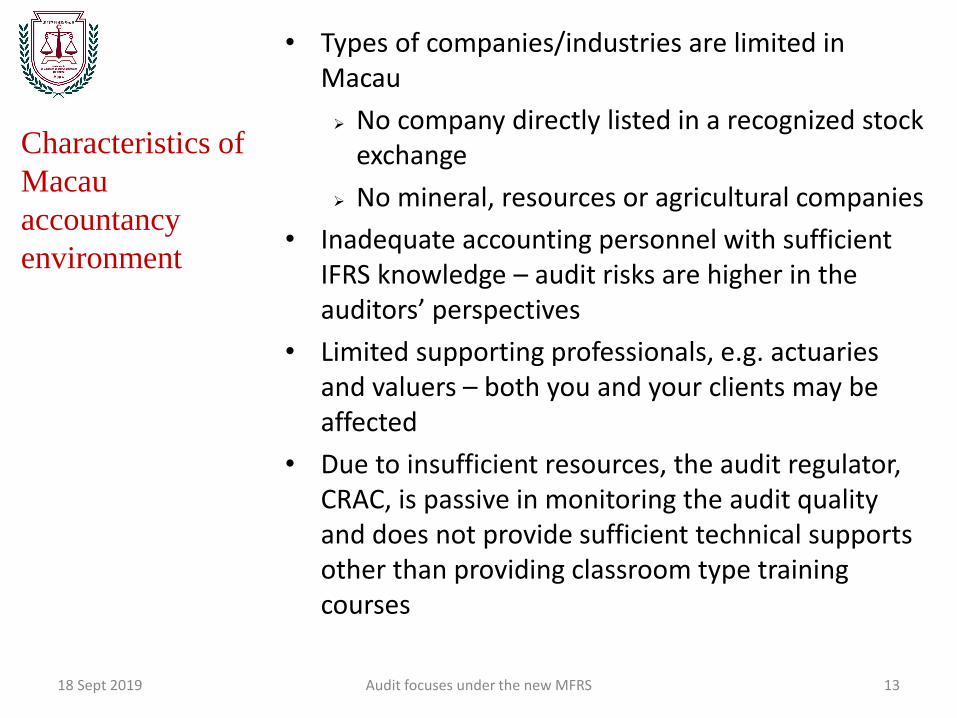

Characteristics of Macau accountancy environment

18 Sept 2019 Audit focuses under the new MFRS 12

• Types of companies/industries are limited in Macau

No company directly listed in a recognized stock exchange

No mineral, resources or agricultural companies

• Inadequate accounting personnel with sufficient IFRS knowledge – audit risks are higher in the auditors’ perspectives

• Limited supporting professionals, e.g. actuaries and valuers – both you and your clients may be affected

• Due to insufficient resources, the audit regulator, CRAC, is passive in monitoring the audit quality and does not provide sufficient technical supports other than providing classroom type training courses

Characteristics of

Macau

accountancy

environment

18 Sept 2019 Audit focuses under the new MFRS 13

Key impacts of the New MFRS on financial reporting of a majority of Macau companies

18 Sept 2019 Audit focuses under the new MFRS 14

1) Consolidated financial statements • 2020 and 2021 consolidated data will be required for 2022 • Consistent accounting policies throughout the group • Goodwill accounting, i.e. NAV of investees at dates of acquisition

and goodwill impairment calculation (IAS 36) • Components not audited by the principal auditor in Macau • Potential qualified opinion, hence a potential ethical issue

2) Investment property accounting • Hotel owners’ PPE versus investment properties • Property owners for rental income • Valuation for 2022 as well as 2021

3) Financial instrument accounting • Categorization and measurements of financial instruments • Use of accounting estimates

4) Fair value accounting • Fair value measurements of non-controlling equity interests, e.g.

fair value of unlisted investments • Disclosure requirements

5) Revenue recognition • IAS 11 and IAS 18 were replaced by a single standard – IFRS 15 • The COPAR 5-Step approach • 2020 and 2021 data for long term contracts (such as engineering

and construction companies) may be required for preparing the 2022 financial statements

Key impacts of

the New MFRS

on financial

reporting of a

majority of Macau

companies

18 Sept 2019 Audit focuses under the new MFRS 15

Auditing a group

18 Sept 2019 Audit focuses under the new MFRS 16

• The definition of subsidiary company in company law can be different from the one adopted in the MFRS

• The group auditor takes sole responsibility for the audit of the group financial statements (Note: Duties can be delegated, but not responsibilities)

• Consolidation is an accounting process and the auditor should be independent of the process

• The group auditor must ensure that all components use consistent accounting policies, including accounting estimates

• The group auditor needs to perform risk assessment and determine on risk response on the company level as well as on the group level, and ensure the component auditors will perform appropriate risk assessments

Key concepts of

auditing a group (1/2)

18 Sept 2019 Audit focuses under the new MFRS 17

• The group auditor must demonstrate his/her involvement in the component auditors’ audits

• The group auditor must ensure that the component auditors will perform the audits in accordance with similar standards and quality as the group audit team

• The group auditor must perform additional work he/she considers necessary if the component auditors fail to do, or refuse to do.

• A qualified audit report cannot relieve the group auditor to do less work

• The group auditor must ensure that internal controls to detect and prevent misstatements in components’ financial statements and in the group financial statements are implemented and operating effective

• The group auditor is responsible for determining materiality levels for each of the group companies

Key concepts of

auditing a group (2/2)

18 18 Sept 2019 Audit focuses under the new MFRS

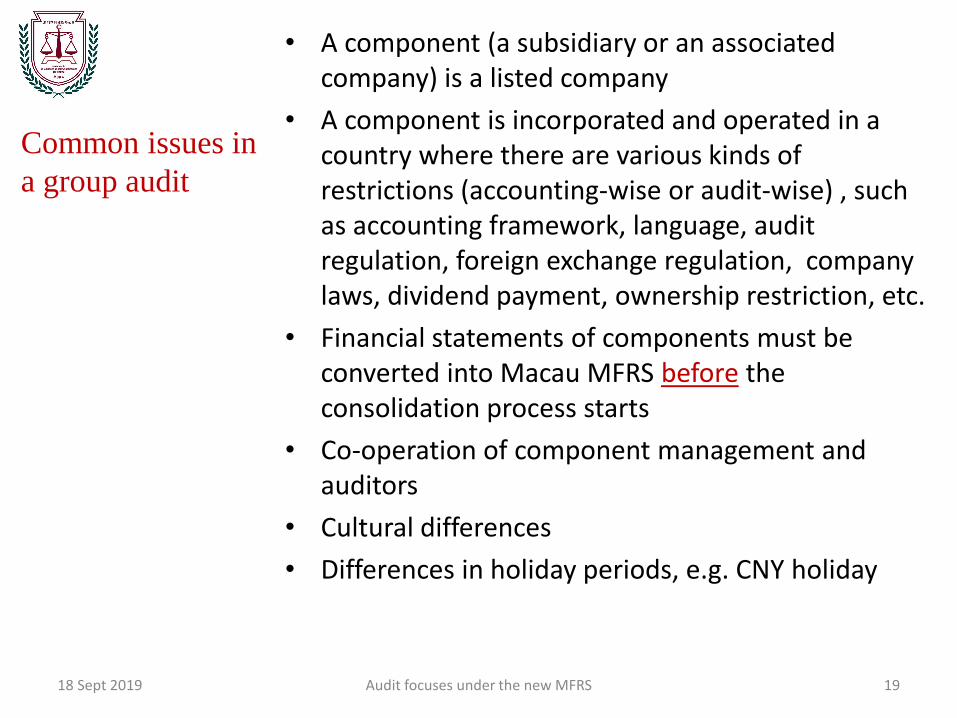

• A component (a subsidiary or an associated company) is a listed company

• A component is incorporated and operated in a country where there are various kinds of restrictions (accounting-wise or audit-wise) , such as accounting framework, language, audit regulation, foreign exchange regulation, company laws, dividend payment, ownership restriction, etc.

• Financial statements of components must be converted into Macau MFRS before the consolidation process starts

• Co-operation of component management and auditors

• Cultural differences

• Differences in holiday periods, e.g. CNY holiday

Common issues in

a group audit

19 18 Sept 2019 Audit focuses under the new MFRS

1) Acceptance and continuance of a group audit engagement

2) Overall audit strategy and audit plan of a group audit

3) Understanding the group, its components, and their environments

4) Understanding the component auditor

5) Determination of materiality at component and group levels

6) Responding to assessed risks at component level

7) Consolidation process

8) Subsequent events affecting the group financial statements

9) Communication with the component auditor

10) Evaluating the sufficiency and appropriateness of audit evidence obtained at component level

11) Communication with group management and those charged with governance of the group

12) Documentation of group audits

ISA 600 -

Considerations of

auditing a group

20 18 Sept 2019 Audit focuses under the new MFRS

Self Reading

18 Sept 2019 Audit focuses under the new MFRS 21

1. Audit planning meeting between the group auditor and the group management

8. Group consolidation in progress

2. The group management issues consolidation package to components

9. The component auditors complete the audits and meet with component management

3. The group auditor issues audit instructions and consolidation questionnaire

10. The component auditors submit audit clearance and the engagement completion memo

4. The component auditors acknowledge the audit instructions

11. The group auditor performs the final examination of the consolidation

5. Group audit conference/ telephone communications

12. The group auditor meets with the group management and TCWG

6. The component auditor submits APM to the group auditor

13. The component auditors submit the subsequent event review report

7. The component auditors identify the consolidation package being audited

14. The group auditor signs off the auditor’s report on the group financial statements

An overview of the process flow of a group audit

Initiated by management

• Consolidation package prepared by the group management for the component management

• Group consolidation policy manual

Initiated by the group auditor

• Group audit instructions prepared by the group auditor for the component auditors (further information given later)

• Audit planning and engagement completion memoranda to be submitted to the group audit team

• Consolidation questionnaire

• Audit clearances (or hard closing) to be submitted by the component auditors to the group audit team

Common “tools”

in a group audit

22 18 Sept 2019 Audit focuses under the new MFRS

• An audit documentation to substantiate the communication between the group auditor and the component auditors

• Normally enclose a copy of consolidation package or request the component auditor to obtain a copy from component management

• Use of a standardised auditing framework

• Audit risk profile from the group auditor’s perspectives

• Compliance with the Ethical Code

• Matters identified through reviews of group internal auditors’ working papers and discussions with group in-house lawyers and other specialists

• Key focus of changes in the selected accounting framework during the year since last reporting

• Work required and reporting requirements on the consolidation package, and audit time table

Group audit

instructions issued

by the group

auditor

1/2

23 18 Sept 2019 Audit focuses under the new MFRS

• Contact details of the group audit team

• Communication strategies throughout the audit of the component

• “Hard-closing”, if any, reporting requirements

• Unadjusted audit differences

• Identified internal control weaknesses

• Audit planning and engagement completion memoranda

• Audit clearance report

• Arrangements for review of the component auditors’ audit working papers

• Statutory audited financial statements and reconciliation to the group reporting package

• Subsequent event reporting

• Audit fee arrangement

Group audit

instructions issued

by the group

auditor

2/2

24 18 Sept 2019 Audit focuses under the new MFRS

1) Close involvement of parent company top management

2) Consolidation policy manual

3) Defined reporting structure and responsibilities

4) Maintaining an updated and detailed group structure, and list of related parties, and changes in group composition and related parties will be communicated to all parties on a timely basis

5) Employing a group reporting team who should be knowledgeable about the accounting frameworks adopted by the group and the components, and the businesses undertaken by the group, including the components

Illustrative

internal controls

over the

preparation of

consolidated

financial

statements

1/3

25

Remember: No one-size-fits-all internal control system.

18 Sept 2019 Audit focuses under the new MFRS

6) Independent and thorough review of components’ financial statements to ensure that the financial information is suitable to be used in the preparation of the group financial statements

7) Centralised authority at group level for investments and establishment of SPV (special purpose vehicles)

8) Permanent consolidation adjustments required at the group level are properly identified, e.g. group tax relief, liabilities secured by assets of a group member and inter company sales of assets

9) Documenting and evaluating of inter company transactions, including transfers of assets, and RPT

10) Safe custodian of audited financial information of a group member at the date of acquisition

Illustrative

internal controls

over the

preparation of

consolidated

financial

statements

2/3

26 18 Sept 2019 Audit focuses under the new MFRS

Remember: No one-size-fits-all internal control system.

11) Checking perpetual records of investees’ post-acquisition equity information

12) Reconciling opening balance of the group’s net equity

13) Independent review and monitoring of the group’s business risks

14) Assessing RMM on group level, e.g. missing out a component, and use of incorrect exchange rates in translation of foreign component

15) Maintaining a risk register on a group basis

16) Maintaining proper segregation of duties for the consolidation processes, e.g. approving consolidation journal adjustments

17) Independent oversight of consolidation status and progress reporting, e.g. issue of consolidation package, receipt of components’ confirmation

Illustrative

internal controls

over the

preparation of

consolidated

financial

statements

3/3

27

Remember: No one-size-fits-all internal control system.

18 Sept 2019 Audit focuses under the new MFRS

The firm (PwC UK) should:

• Further improve the assessment of, and level of challenge regarding, management’s estimates and provisions.

• Enhance the involvement of the group audit partner and team members in the direction and supervision of component audits in more unusual circumstances.

• Provide guidance to group audit teams in relation to the approach taken and evidence of work performed on reserves in the extractive industries.

• Require more informative reporting from the firm’s internal actuarial experts on the key assumptions underpinning the estimation of company pension scheme liabilities.

Source:

Page 5, PwC LLP Audit Quality Inspection June 2018, issued by Financial Reporting Council (UK)

Group audit

discussion

example 1

28

Group audit considerations

• The group audit team’s involvement in component auditors’ risk assessments and planned audit responses was insufficient.

• The group audit team’s evaluation of the sufficiency and appropriateness of the audit evidence obtained by the component auditors for group audit purposes required improvement.

Comment: The lead engagement team, especially the engagement partner, takes the overall responsibility for the audit opinion on the consolidated financial statements, including ethical compliance and use of internal and external specialists.

Source:

UK FRC AIU Public Report on the 2011/2012, Inspection on Ernest & Young UK, 15 June 2012

Group audit

discussion

example 2

29

Auditing Accounting Estimates

18 Sept 2019 Audit focuses under the new MFRS 30

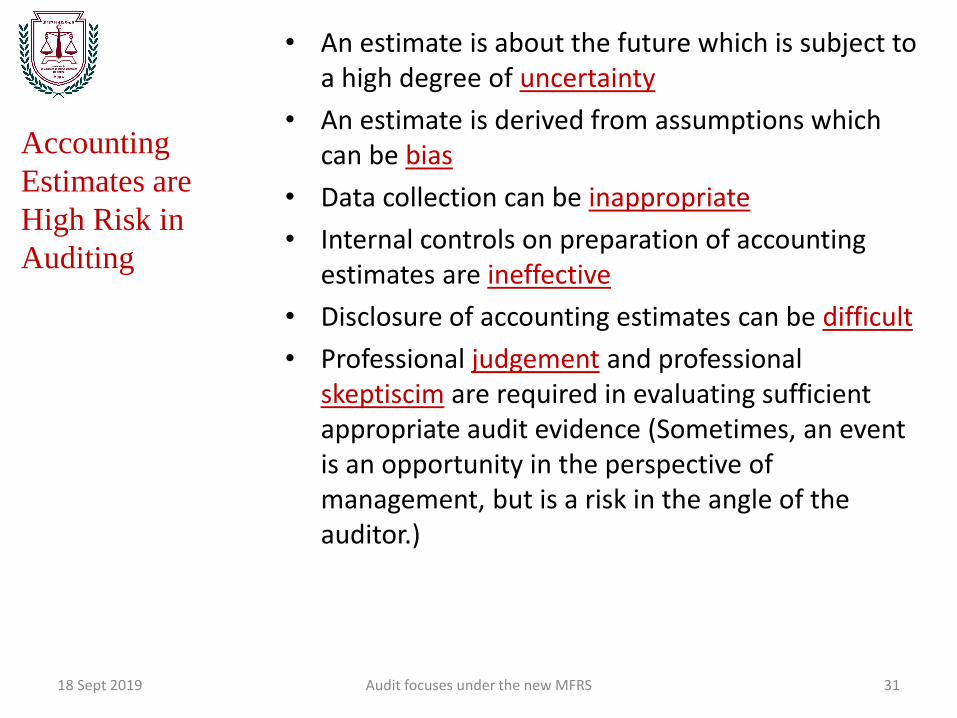

• An estimate is about the future which is subject to a high degree of uncertainty

• An estimate is derived from assumptions which can be bias

• Data collection can be inappropriate

• Internal controls on preparation of accounting estimates are ineffective

• Disclosure of accounting estimates can be difficult

• Professional judgement and professional skeptiscim are required in evaluating sufficient appropriate audit evidence (Sometimes, an event is an opportunity in the perspective of management, but is a risk in the angle of the auditor.)

Accounting

Estimates are

High Risk in

Auditing

18 Sept 2019 Audit focuses under the new MFRS 31

• The auditors shall develop their own estimate, or range of estimates, and shall assess and document their own independent assessment of estimation uncertainty for each material financial statement line item

• Assessment of internal controls over how estimates are determined

• Review of accounting policies to ensure that the policies comply with the appropriate rules of MRFS

• Investigation of outcomes of the uncertainties after the year-end but before the audit opinion is issued

• Compare historical accuracy of management estimates compared with actual outcomes

Audit of

Accounting

Estimates (1/2)

18 Sept 2019 Audit focuses under the new MFRS 32

• Verification of any underlying data used by management (e.g. obsolescence of inventories by aging) to external evidence

• For significant risks, assess if management considered alternative means for determining estimates (e.g. potential loss on litigations)

• Alert to and assess for signs of management bias

• Consider if specialist advice is required

• Obtain written management representations to confirm management’s intentions

Audit of

Accounting

Estimates (2/2)

18 Sept 2019 Audit focuses under the new MFRS 33

• Risk Assessment Procedures and Related Activities

• Identifying and Assessing the Risks of Material Misstatement

• Responses to the Assessed Risks of Material Misstatement

• Further Substantive Procedures to Respond to Significant Risks

ISA 540 -

Auditing

Accounting

Estimates,

Including Fair

Value Accounting

Estimates, and

Related

Disclosures

18 Sept 2019 Audit focuses under the new MFRS 34

See further information in the following 4 slides. Self Reading

• Obtain an understanding of the entity and its environment, including the entity's internal control

• Identify the requirements of the applicable financial reporting framework relevant to accounting estimates, including related disclosures

• Make inquiries of management about changes in circumstances that may give rise to new, or the need to revise existing, accounting estimates

• Understand how management makes the accounting estimates

• Review the outcome of accounting estimates included in the prior period financial statements, or, where applicable, their subsequent re-estimation for the purpose of the current period

ISA 540 –

Risk Assessment

Procedures and

Related Activities

18 Sept 2019 Audit focuses under the new MFRS 35

Self Reading

• Identify and assess the risks of material misstatement

• Evaluate the degree of estimation uncertainty associated with an accounting estimate

• Determine whether, in the auditor's judgment, any of those accounting estimates that have been identified as having high estimation uncertainty give rise to significant risks

ISA 540 –

Identifying and

Assessing the

Risks of Material

Misstatement

18 Sept 2019 Audit focuses under the new MFRS 36

Self Reading

• Determine whether management has appropriately applied the requirements of the applicable financial reporting framework relevant to the accounting estimate

• Determine whether the methods for making the accounting estimates are appropriate and have been applied consistently

• Determine whether any subsequent events provide audit evidence regarding the accounting estimate

• Test how management made the accounting estimate

• Test the operating effectiveness of the controls over how management made the accounting estimate

• Develop a point estimate or a range to evaluate management's point estimate

• Consider whether specialized skills or knowledge in relation to one or more aspects of the accounting estimates are required in order to obtain sufficient appropriate audit evidence

ISA 540 –

Responses to the

Assessed Risks of

Material

Misstatement

18 Sept 2019 Audit focuses under the new MFRS 37

Self Reading

• Consider how management has considered alternative assumptions or outcomes

• Determine whether the significant assumptions used by management are reasonable

• Evaluate management's intent to carry out specific courses of action and its ability to do so

• If management has not adequately addressed the effects of estimation uncertainty on the accounting estimates, develop a range with which to evaluate the reasonableness of the accounting estimate

• Document management's decision to recognize, or to not recognize, the accounting estimates

• Document the selected measurement basis for the accounting estimates

• Evaluate, based on the audit evidence, whether the accounting estimates in the financial statements are either reasonable in the context of the applicable financial reporting framework, or are misstated

ISA 540 –

Further

Substantive

Procedures to

Respond to

Significant Risks (1/2)

18 Sept 2019 Audit focuses under the new MFRS 38

Self Reading

• Ascertain that the disclosures in the financial statements related to accounting estimates are in accordance with the requirements of the applicable financial reporting framework

• Identify whether there are indicators of possible management bias

• Obtain written representations from management and those charged with governance (including the board of supervisors) whether they believe significant assumptions used in making accounting estimates are reasonable

• Record in audit working papers the basis for the auditor's conclusions about the reasonableness of accounting estimates and their disclosure that give rise to significant risks, and indicators of possible management bias

ISA 540 –

Further

Substantive

Procedures to

Respond to

Significant Risks (2/2)

18 Sept 2019 Audit focuses under the new MFRS 39

Self Reading

• How management determines the completeness, relevance and accuracy of the data used to develop accounting estimates.

• The review and approval of accounting estimates, including the assumptions or inputs used in their development, by appropriate levels of management and, where appropriate, those charged with governance.

• The segregation of duties between those committing the entity to the underlying transactions and those responsible for making the accounting estimates, including whether the assignment of responsibilities appropriately takes account of the nature of the entity and its products or services

Illustrative

internal controls

over development

of accounting

estimates

highlighted in :

ISA 540.A27

18 Sept 2019 Audit focuses under the new MFRS 40

a) Management communication of the need for proper accounting estimates

b) Accumulation of relevant, sufficient, and reliable data on which to base an accounting estimate

c) Preparation of the accounting estimate by qualified personnel

d) Adequate review and approval of the accounting estimates by appropriate levels of authority, including— • Review of sources of relevant factors • Review of development of assumptions • Review of reasonableness of assumptions and

resulting estimates • Consideration of the need to use the work of

specialists • Consideration of changes in previously established

methods to arrive at accounting estimates e) Comparison of prior accounting estimates with

subsequent results to assess the reliability of the process used to develop estimates

f) Consideration by management of whether the resulting accounting estimate is consistent with the operational plans of the entity.

Illustrative

internal controls

over development

of accounting

estimates

highlighted in

PCAOB AS

2501.06

18 Sept 2019 Audit focuses under the new MFRS 41

• Failure to sufficiently test controls over or sufficiently test the accuracy and completeness of issuer-produced data or reports

• Failure to sufficiently test significant assumptions or data that the issuer used in developing an estimate

• Failure to sufficiently test the design and/or operating effectiveness of controls that the Firm selected for testing

• Failure to identify and test any controls that addressed the risks related to a particular account or assertion

Accounting

estimate

discussion

example 1

Source:

PCAOB Release No. 104-

2015-095, Inspection of

Deloitte & Touche LLP (USA),

May 12, 2015

18 Sept 2019 Audit focuses under the new MFRS 42

Comments: • Client-produced data or reports cannot be used unless controls over preparation

and accuracy and completeness are tested with satisfactory results • Each of the controls over management assertions (Completeness, Valuation,

Existence, Right and obligations, and Presentation and disclosures) must be tested.

Valuations and estimates

We reviewed one or more areas involving audit judgments relating to valuations or accounting estimates on all 20 audits. In the following cases, which had been identified as significant risks by the relevant audit teams, there were weaknesses relating to the quality of audit evidence and/or the evidence of challenge of management.

Commentary:

• Audit methodology problem?

• Work is deemed not having been done if there is no documentation?

• Over reliance on management’s representation?

Accounting

estimate

discussion

example 2

Source:

UK FRC AIU Public Report on

the 2014/2015, Inspection on

Deloitte UK, May 2015

18 Sept 2019 Audit focuses under the new MFRS 43

Auditing Related Party Transactions

18 Sept 2019 Audit focuses under the new MFRS 44

• RPTs may be non-routine transactions and may not subject to established routine internal controls

• Management may over-ride the internal controls on RPTs, particularly on pricing and credit terms

• Non-routine RPTs can be, or mostly likely are, significant transactions

• Identification of RPTs depends, to a large degree, on management’s attitude and knowledge about RPT accounting

Related Party

Transactions

(RPTs) are high

risk in an audit

18 Sept 2019 Audit focuses under the new MFRS 45

Reminder Higher fraud risk areas identified in ISA 240, The Auditor's Responsibilities Relating to Fraud in an Audit of Financial Statements, are: • Revenue recognition • Journal adjustments • Accounting estimates • Significant contracts • Related party transactions

• Identify and evaluate internal controls over

Identification of related parties and

Recording of the RPTs

Reporting and disclosures of the RPTs

Risk assessment (see ISA 550)

• Audit considerations

Professional judgement and professional skepticism

Directors’ conflicts of interests

Arm’s length transaction in pricing (fair value accounting)

Extended credit terms

Matters of Emphasis, Modified/qualified opinion on RPTs

Audit of Related

Party Transactions

18 Sept 2019 Audit focuses under the new MFRS 46

• Definition of Related Parties (Note: There may be differences between accounting standards, statutory laws, and listing rules)

• Risk Assessment Procedures and Related Activities

• Identification and Assessment of the Risks of Material Misstatement Associated with Related Party Relationships and Transactions

• Responses to the Risks of Material Misstatement Associated with Related Party Relationships and Transactions

• Evaluation of the Accounting for and Disclosure of Identified Related Party Relationships and Transactions

• Written Representations

• Communication with Those Charged with Governance

• Documentation

ISA 550 –

Related Parties

18 Sept 2019 Audit focuses under the new MFRS 47

Self Reading

Internal controls to:

(a) Identify, account for, and disclose related party relationships and transactions in accordance with the applicable financial reporting framework;

(b) Authorize and approve significant transactions and arrangements with related parties; and

(c) Authorize and approve significant transactions and arrangements outside the normal course of business.

Illustrative

internal controls

over related party

transactions

highlighted in ISA

550.14

18 Sept 2019 Audit focuses under the new MFRS 48

See the next slide for further information.

• Internal ethical codes, appropriately communicated to the entity's personnel and enforced, governing the circumstances in which the entity may enter into specific types of related party transactions.

• Policies and procedures for open and timely disclosure of the interests that management and those charged with governance have in related party transactions.

• The assignment of responsibilities within the entity for identifying, recording, summarizing, and disclosing related party transactions.

• Timely disclosure and discussion between management and those charged with governance of significant related party transactions outside the entity's normal course of business, including whether those charged with governance have appropriately challenged the business rationale of such transactions (for example, by seeking advice from external professional advisors).

• Clear guidelines for the approval of related party transactions involving actual or perceived conflicts of interest, such as approval by a subcommittee of those charged with governance comprising individuals independent of management.

• Periodic reviews by the internal audit function, where applicable.

• Proactive action taken by management to resolve related party disclosure issues, such as by seeking advice from the auditor or external legal counsel.

• The existence of whistle-blowing policies and procedures, where applicable.

Illustrative

internal controls

over related party

transactions

highlighted in ISA

550.A17

18 Sept 2019 Audit focuses under the new MFRS 49

Background

• Company A was able to obtain a bank loan at a 10% interest.

• Mr X, a director and shareholder of Company A, agreed to provide personal guarantee to the bank and the interest rate was reduced to 3%.

• Some years later, Mr X sold his interest in Company A to Mr Y, and some more years later, Company A was insolvent. The bank called the loan and was able to get a full repayment through Mr A.

• The auditor of Company A sent a confirmation to the bank which confirmed the loan balance was nil.

• Mr Y decided to write off the loan.

Discussion

• What are the accounting implications?

• What are the auditing implications?

RPT discussion

example 1

18 Sept 2019 Audit focuses under the new MFRS 50

Background

• Company X, a listed company, is a construction company.

• The board of Company X resolved to buy a portfolio of properties from Mr H, the non-Executive Chairman and a shareholder of Company X, at market price.

• Some months later, Company X has become insolvent.

Discussion

• What are the accounting implications?

• What are the auditing implications?

RPT discussion

example 2

18 Sept 2019 Audit focuses under the new MFRS 51

Commercial Code considerations

18 Sept 2019 Audit focuses under the new MFRS 52

18 Sept 2019 Audit focuses under the new MFRS 53

Matters of interest Commentary

1 商法典 58.1.c 條: 對年度帳目內各項目之組成要素之估價,應

根據公認之會計原則為之,尤其須遵守遵循謹慎估價原則。

a) MFRS is a fair-value-based “true and fair” accounting framework whereas the Commercial Code (“CC”) contains a historical cost based “compliance” accounting framework.

b) Entities incorporated under the CC should keep their accounting books and records in accordance with the CC.

c) Entities adopting the MFRS (to present their accounts) will recognize unrealized profits in their accounts and will be required to disclose supplementary information in their MFRS financial statements about the implications on the asset valuation and the ‘retained earnings’ in accordance with the compliance framework contained in the CC.

d) Recognition of unrealized profits will affect the entities’ distributable profits.

e) No guidance on distributable profits and related disclosures is provided by CRAC.

2 商法典 58.2 條: 上款c項所指原則與其他原則有衝突時,以該

原則為準;按照該原則,列入資產負債表內之利潤,僅限於在該表

結帳日已實現之利潤,並考慮來自該營業年度或上一營業年度之可

預見之風險及可能之損失,在損失中須將已實現或不可逆轉之損失

與潛在或可逆轉之損失分開,該等風險與損失包括於資產負債表結

帳日至資產負債表制定日期間內知悉者;在此情況下,須在附件內

註明補充資料;另外,不論營業年度結餘為正數或負數,尚須注意

折舊。

商法典 公司所採用之計價標準能否正確評估財產及結餘

Note: Macau auditors should write to the clients to remind them of the above implication and suggest them to consult their lawyers for legal advice.

18 Sept 2019 Audit focuses under the new MFRS 54

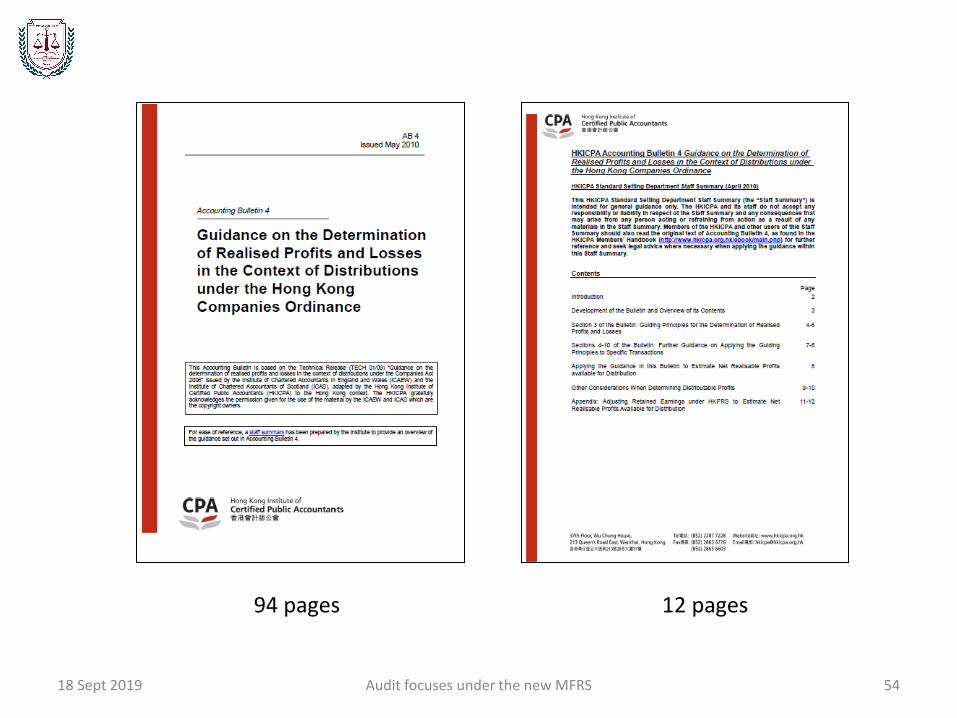

94 pages 12 pages

Macau Society of Registered Auditors 澳門註冊核數師公會

Conceptual Framework for Financial Reporting - Definition of equity

Para 4.63 Equity is the residual interest in the assets of the entity after deducting all its liabilities.

If the preference shares are not entitled to the residual interest in the assets of an entity, they should be classified as Long Term Liabilities.

Lawyers may or will dispute the accounting treatment. Laws overrule accounting standards or vice versa (?)

Presentation of

Preference shares

18 Sept 2019 Audit focuses under the new MFRS 55

A personal perspective of possible audit implications arising from the new MFRS

18 Sept 2019 Audit focuses under the new MFRS 56

• Macau SMEs do not employ sufficient and appropriate accounting personnel to prepare MFRS financial statements.

• Auditors cannot prepare MFRS financial statements for clients due to ethical requirements, i.e. the auditor cannot audit his own work.

• The new MFRS and the new Auditing Standards will cause audit work quantity to increase substantially and SMPs need to employ more audit staff. Supply of audit staff is limited in the market and salary costs will increase. Clients will be reluctant to bear significant additional fees.

• The New MFRS involves concepts which are new to SME and SMP, such as the fair value accounting and the preparation of consolidated financial statements. The 1 January 2022 effective date is not far away. It is absolutely necessary to start working side by side with your clients ASAP to help them implement the New MFRS, and to plan for the audit of the related financial statements.

A personal

perspective of

possible audit

implications

arising from the

new MFRS (1/2)

18 Sept 2019 Audit focuses under the new MFRS 57

• The New MFRS requires supports from other professionals, such as valuers. These valuers may receive more fees than the auditors whereas the auditors will be held responsible for the fairness of the valuations which are used in the financial statements.

• Your clients will have difficulties in obtaining comparatives for 2012, e.g. consolidated financial statements for 2011 and 2010 are required, and you will find many audit issues to resolve too.

• Cannot use a “Qualified opinion” to avoid performing appropriate sufficient audit procedures.

• Provide more training courses to junior level auditors are necessary!

A personal

perspective of

possible audit

implications

arising from the

new MFRS (2/2)

18 Sept 2019 Audit focuses under the new MFRS 58

• Establish specialising teams to focus on specific areas (e.g. financial instrument, investment properties, revenue recognition, group accounting, pension fund accounting, insurance companies, etc.) on accounting and auditing issues identified in Macau

• The Union or MSRA, or CRAC, should establish a Technical Panel and appoint a full time Technical Manager who may be seconded from members and member firms on a rotation of 1-2 years basis to provide technical support to auditors and accountants

• Gather external technical information on the corresponding IFRS, i.e. illustrative financial statements, disclosure checklists (the years ended 31 Dec 2015, 2016, 2017 and 2018) and tailor one set for the use of Macau MSRA preparers and auditors

• Establish technical consultation services to members and member firms

• Establish the peer review practice with the view to improving the industry, not penalizing members

• Conduct workshop type audit training courses

Suggestions to the

audit profession

in Macau

18 Sept 2019 Audit focuses under the new MFRS 59

Take away points

18 Sept 2019 60 Audit focuses under the new MFRS

• Focus on internal controls which are the fundamentals of a risk-based audit

• Focus on management’s judgement - Estimates are applied extensively in the new MFRS, i.e. the “fair value” accounting convention, and estimates are developed based on management’s judgement

• In a group audit, apart from the parent company audit, focus on the component audits which are performed by other (component) auditors, as if the audits are performed by yourself

• Focus on audits of disclosures - the New MFRSs require much more disclosures which should be audited thoroughly, i.e. the internal controls over the collecting and recording of the data, the estimates used, and the related risk disclosure

Audit focuses

under the new

MFRS

18 Sept 2019 Audit focuses under the new MFRS 61

1) Auditors must be knowledgeable in the new MFRS

2) You and your clients must take actions immediately to prepare for the new MFRS.

Take away point

18 Sept 2019 Audit focuses under the new MFRS 62

Reference materials

18 Sept 2019 63 Audit focuses under the new MFRS

• Journal of Accountancy Article: Clarifying the standard for group audits (https://www.journalofaccountancy.com/issues/2013/mar/20126525.html) 9 pages

• CPA Journal Article: Auditing Accounting Estimates (https://www.cpajournal.com/2019/03/07/auditing-accounting-estimates/ ) 5 pages

• Audit Procedures For Related-Party Transactions (article): (http://accounting-financial-tax.com/2010/02/audit-

procedures-for-related-party-transactions/ ) 15 pages

• IFAC discussion paper: Audit of Less Complex Entities (https://www.ifac.org/publications-resources/discussion-

paper-audits-less-complex-entities) 24 pages

Reference

materials

18 Sept 2019 Audit focuses under the new MFRS 64

International Accounting Standards, now IFRS

• Started in 1975

• Changed the format several times

• Have been widely adopted since 2005

• IFRS for SME was first issued in 2009

International Standards on Auditing

• Started in 1978

• Completed the Clarity Project in 2009

• Emphasized that there would not be a separate set of auditing standards for SME

• Issued a discussion paper on Audit of Less Complex Entities in 2019

International

Standards on

Auditing - Audit

of Less Complex

Entities?

18 Sept 2019 Audit focuses under the new MFRS 65

18 Sept 2019 Audit focuses under the new MFRS 66

What is a less complex entity? “An entity which typically possesses qualitative characteristics such as:

A. Concentration of ownership and management in a small number of individuals (often a single individual – either a natural person or another enterprise that owns the entity provided the owner exhibits the relevant qualitative characteristics); and

B. One or more of the following: 1) Straightforward or uncomplicated transactions; 2) Simple record-keeping; 3) Few lines of business and few products within business lines; 4) Few internal controls; 5) Few levels of management with responsibility for a broad range of

controls; or 6) Few personnel, many having a wide range of duties.

These qualitative characteristics are not exhaustive, they are not exclusive to smaller entities, and smaller entities do not necessarily display all of these characteristics.”

Source: IFAC discussion paper: Audit of Less Complex Entities (https://www.ifac.org/publications-resources/discussion-paper-audits-less-complex-entities) Page 6

Q & A

18 Sept 2019 67 Audit focuses under the new MFRS

Thank you! See you next time.

18 Sept 2019 68 Audit focuses under the new MFRS