auckland, november 5 th, 2009 private label cpg export opportunities

TRANSCRIPT

Auckland, November 5th, 2009

Private Label CPG Export Opportunities

1.

Private Label CPG Export Opportunities

North America and EuropeAuckland, November 5th, 2009

1.

2.

3.

Private Label Export Opportunities

Key Retailer Trends

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

1. Key Retailer Trends

1. Key Retailer Trends....Europe

1. Key Retailer Trends....North America

Key Challenges & Opportunities1. Key Retailer Trends...common ground in Europe and North America

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Private Label is a tool to improve and develop

Customer Loyalty

Profitability

What’s the basic issue here?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Many Retailers believe that National Brands are tools to improve and develop

• Customer Loyalty

• Profitability

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

They are so wrong……………

•Everyone sells the National Brands i.e. No Loyalty

•Their Profitability is way lower than Store Brand Profitability

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

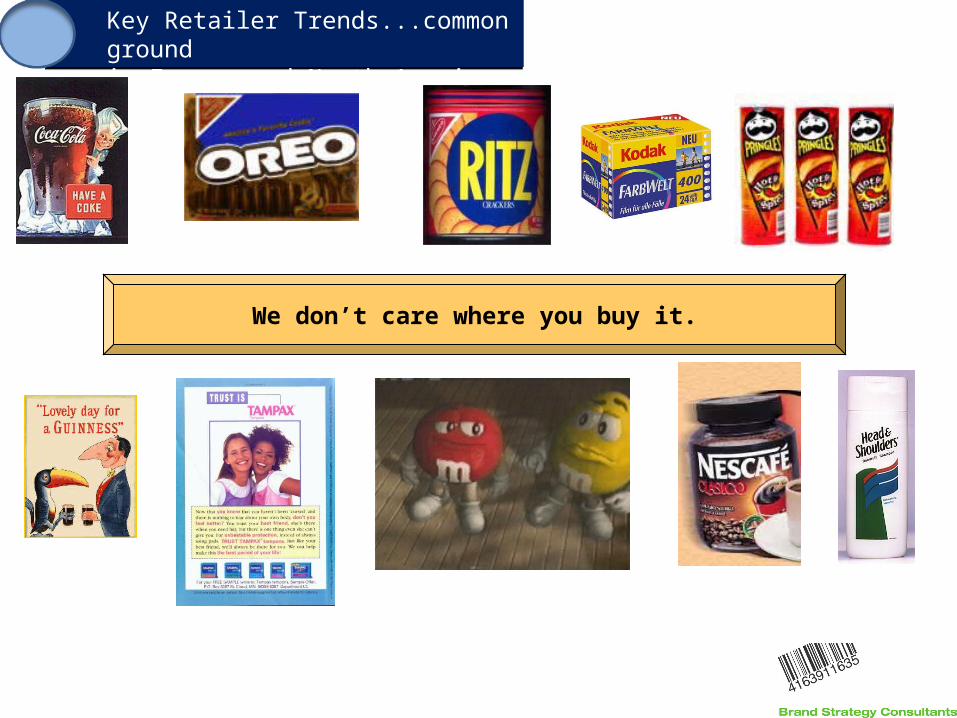

No matter what the product, the manufacturer’s message is the same…….

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

We don’t care where you buy it.

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

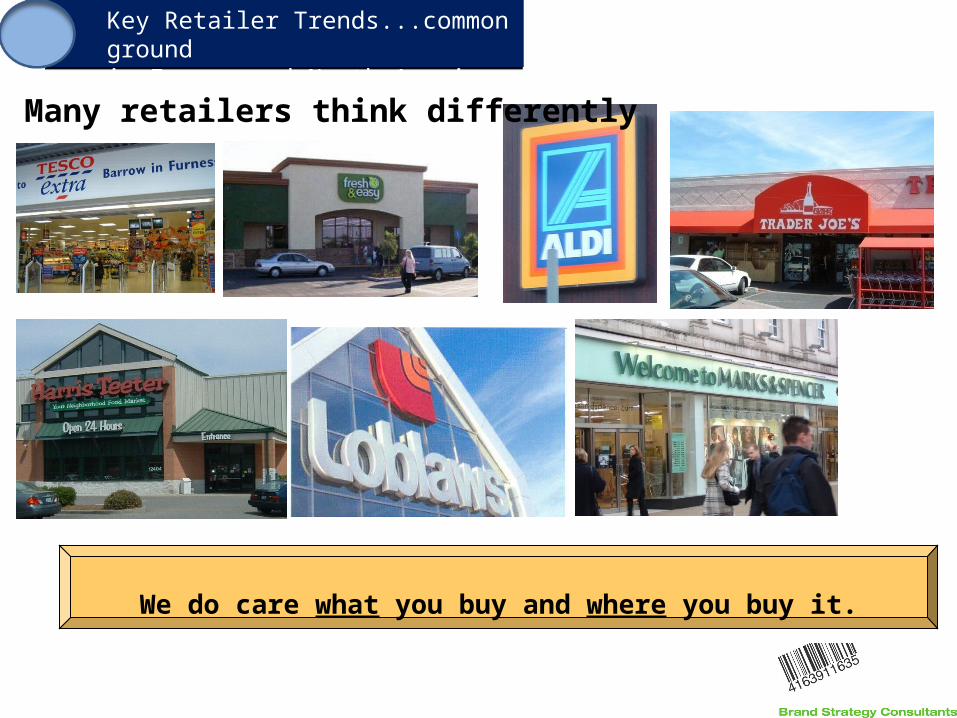

We do care what you buy and where you buy it.

Many retailers think differently

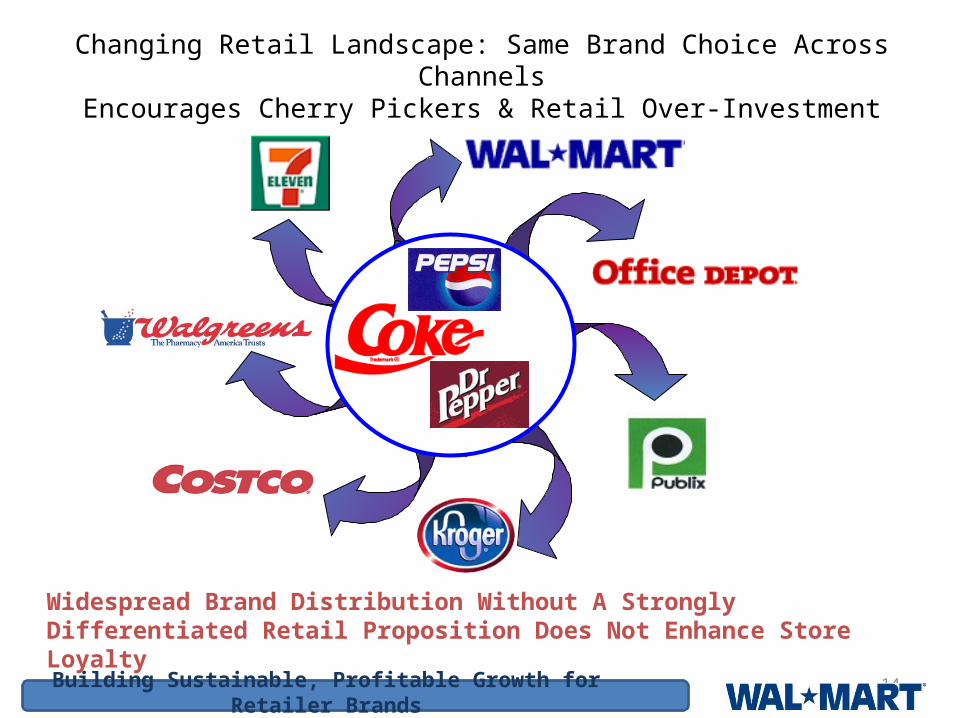

Building Sustainable, Profitable Growth for Retailer Brands 14

Changing Retail Landscape: Same Brand Choice Across ChannelsEncourages Cherry Pickers & Retail Over-Investment

Widespread Brand Distribution Without A Strongly Differentiated Retail Proposition Does Not Enhance Store Loyalty

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Where’s the loyalty and to what?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Where’s the Profit$?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

private label nat. brand competitive

Retail Price 2.99 3.99 2.99

Cost 0.85 3.41 3.41

GM 71.6% GM 14.5%

Store Profit 2.14 0.58 -0.42

how does it actually work?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

private label nat. brand competitive

Retail Price 2.29 3.99 2.99

Cost 0.85 3.41 3.41 2.72

GM 62.8% GM 14.5%

Store Profit 1.44 0.58 -0.42 0.27

how does it actually work?

Shielding price reductions

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

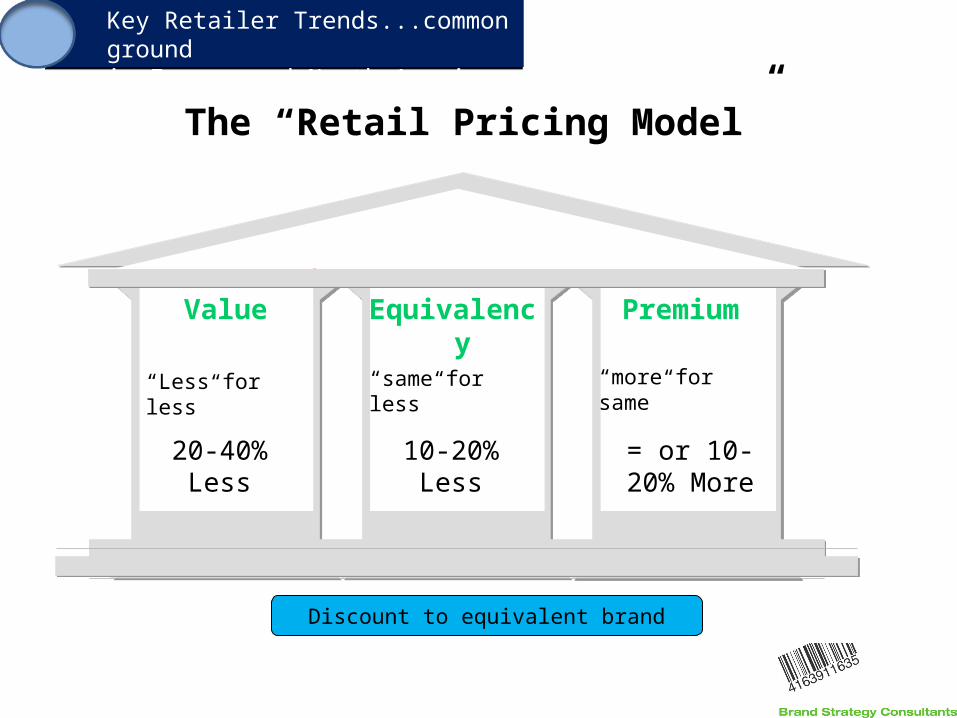

Value Equivalency Premium

“Less for less” “same for less” “more for same”

The “Retail Pricing Model”

Discount to equivalent brand

20-40% Less 10-20% Less = or 10-20% More

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

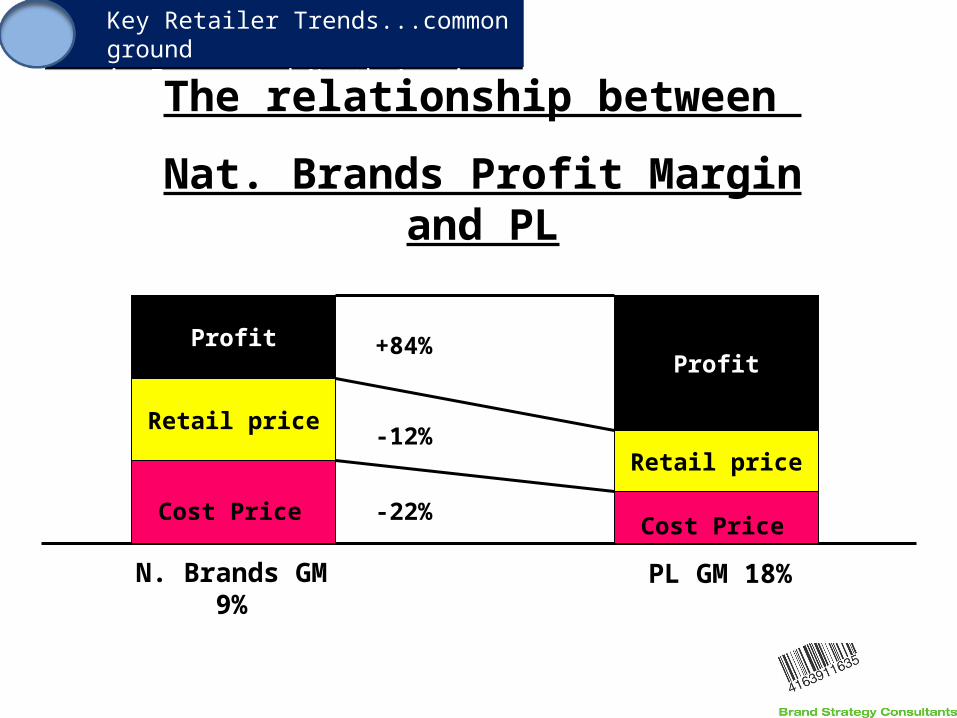

Retail price

Profit

Cost Price

Retail price

Profit

Cost Price

-12%

-22%

+84%

PL GM 18%

The relationship between

Nat. Brands Profit Margin and PL

N. Brands GM 9%

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

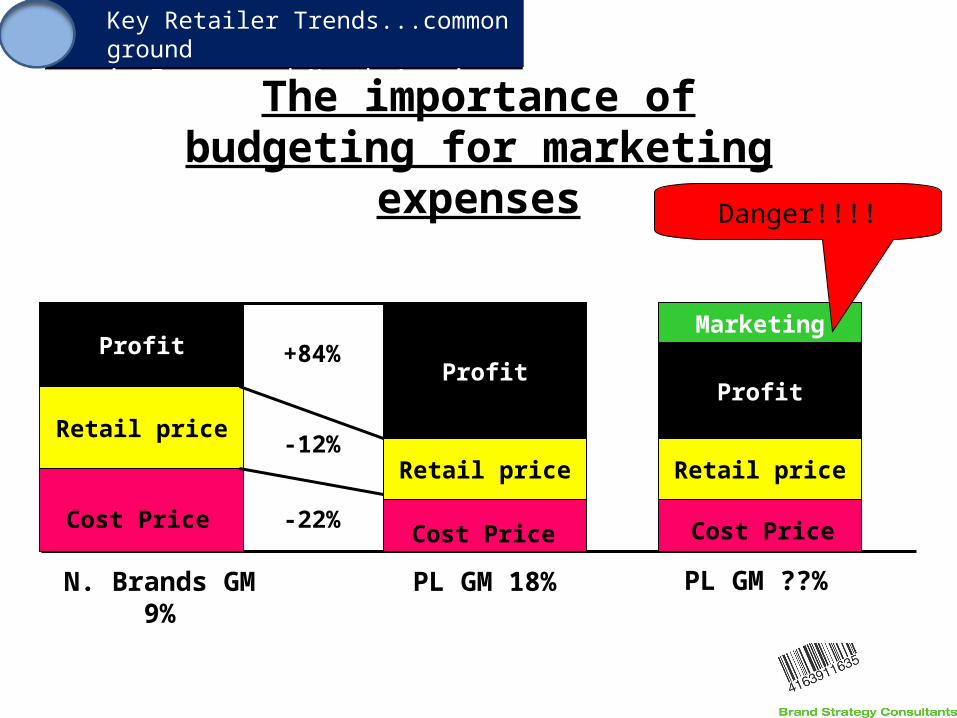

Retail price

Profit

Cost Price

Retail price

Profit

Cost Price

-12%

-22%

+84%

PL GM 18%

Retail price

Cost Price

Profit

Marketing

PL GM ??%

The importance of budgeting for marketing expenses

N. Brands GM 9%

Danger!!!!

22

A W.A.W.A word or two about

Building Sustainable, Profitable Growth for Retailer Brands23

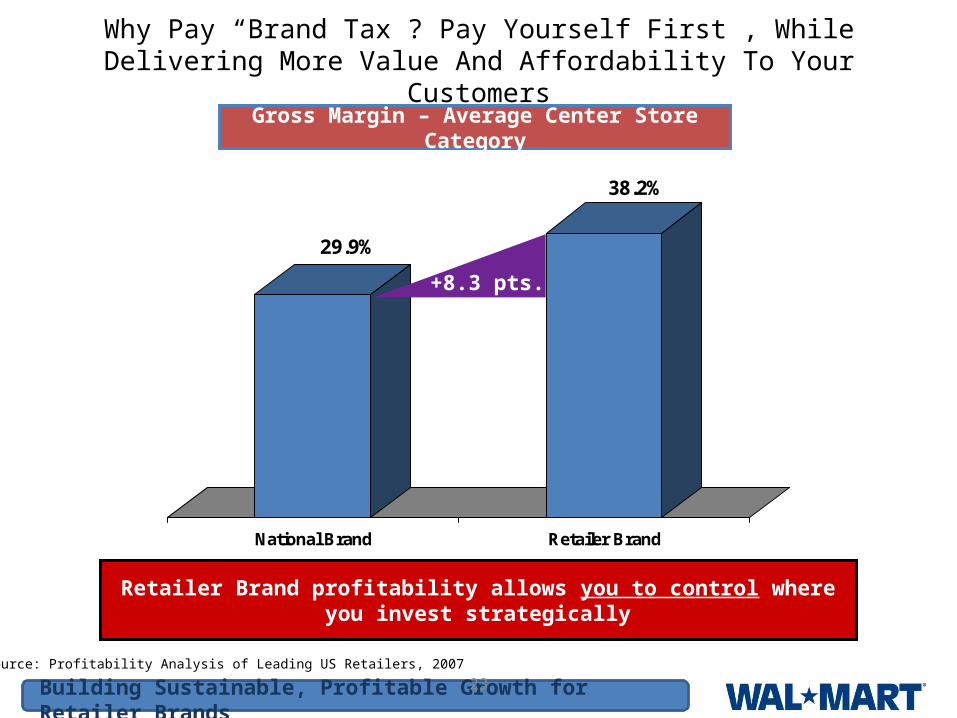

29.9%

38.2%

Retailer BrandNational Brand

Why Pay “Brand Tax”? Pay Yourself First , While Delivering More Value And Affordability To Your Customers

Gross Margin – Average Center Store Category

+8.3 pts.

Source: Profitability Analysis of Leading US Retailers, 2007

Retailer Brand profitability allows you to control where you invest strategically

Retailer Brand profitability allows you to control where you invest strategically

Building Sustainable, Profitable Growth for Retailer Brands 2424

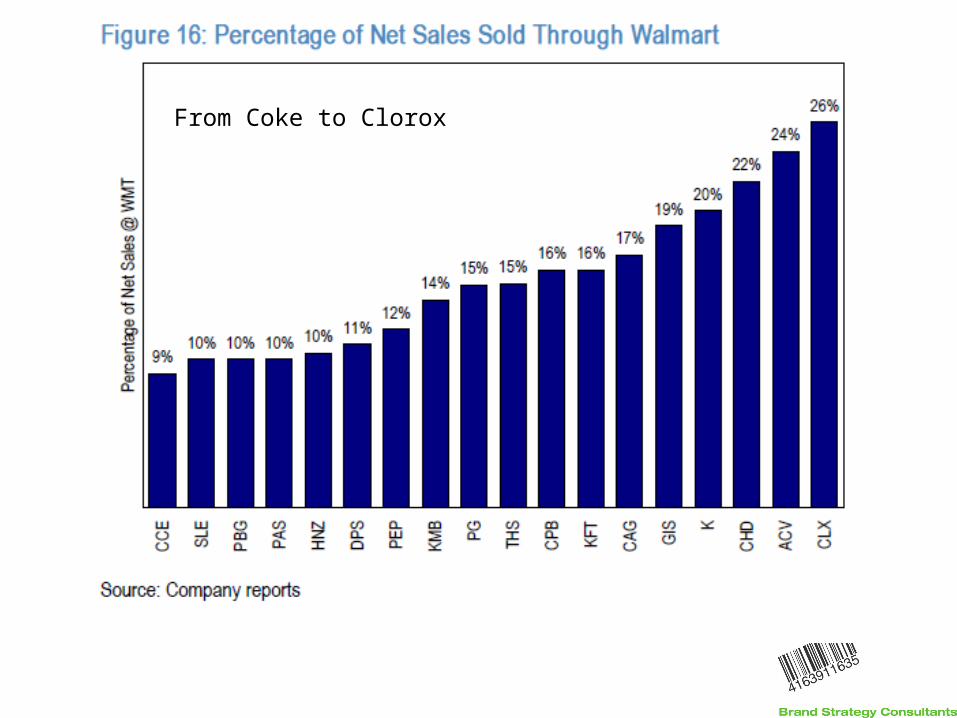

Retailer Controlled Brand Share At Wal-Mart Represents A Tremendous Growth Opportunity Relative To The Market, And It’s Potential

Source: Nielsen’s Strategic Planner, FDM (including Wal-Mart)

2004 2005 2006 2007

W*M

FDM+WM

Competitive Momentum Gaining Pace as Retailers Build Store Loyalty

25

Project Impact: Includes the re-birth of PL at Walmart

26

27

From Coke to Clorox

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Key Findings• Growing customer acceptance of private label (PL) means it is more critical for grocery retailers to

develop a successful and comprehensive PL strategy.

• Showing affordability and value remains the imperative. However, PL has matured into a strategic lever driving multiple aspects.

• A weapon against the fast-changing discount sector, PL also needs to demonstrate a mainstream retailer’s core values.

• Value (economy) ranges have been re-developed to better display their value/quality credentials with improved packaging and reformulation.

• Whilst the recession has clearly boosted volume growth at the value end of the market, premium and ethical ranges are still faring well…

• …And a number of retailers are launching new umbrella structures and ranges.

September 2009

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Key Findings (cont’d)• Private label is increasingly central to marketing strategies and is leveraged in innovative ways to

build brand equity.

• Retailers have also been promoting PL to drive penetration and to build basket size.

• Bundle deals are now more important in private label, with a special focus on chilled meals.

• Bold promotions and in-store displays are now prominent in many international markets.

• One of the next frontiers for PL will be sustainability and, specifically, carbon label footprint, which requires PL suppliers to innovate apace with branded manufacturers.

September 2009

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

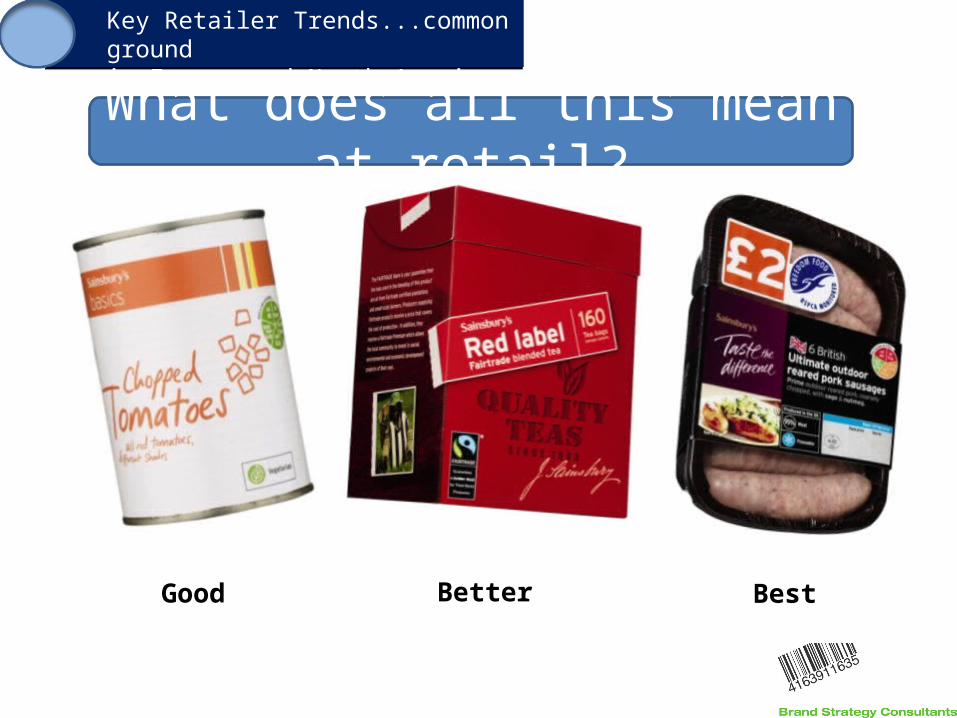

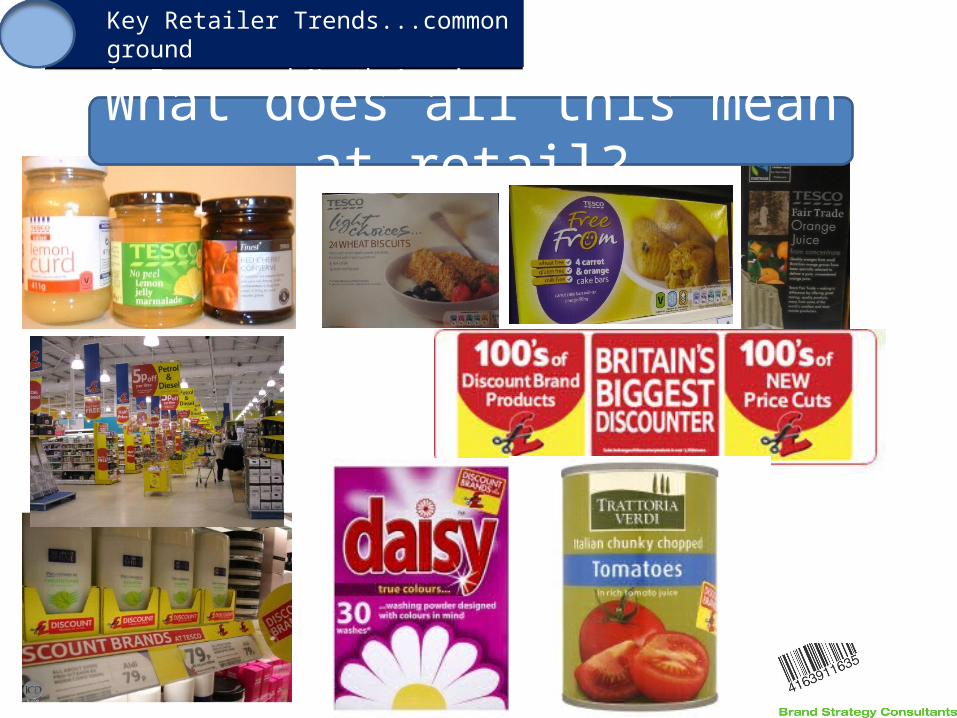

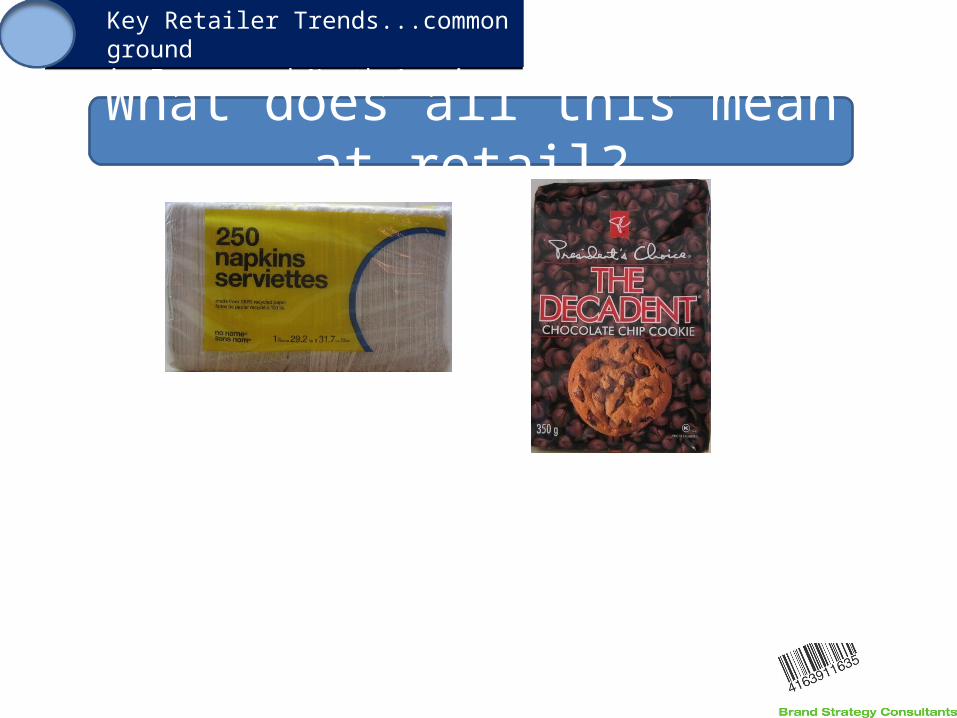

What does all this mean at retail?

BestBetterGood

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

What does all this mean at retail?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

What does all this mean at retail?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

What does all this mean at retail?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

What does all this mean at retail?

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

Price Promotions getting Crazier

1.

Key Retailer Trends...common ground in Europe and North America

Key Retailer Trends...common ground in Europe and North America

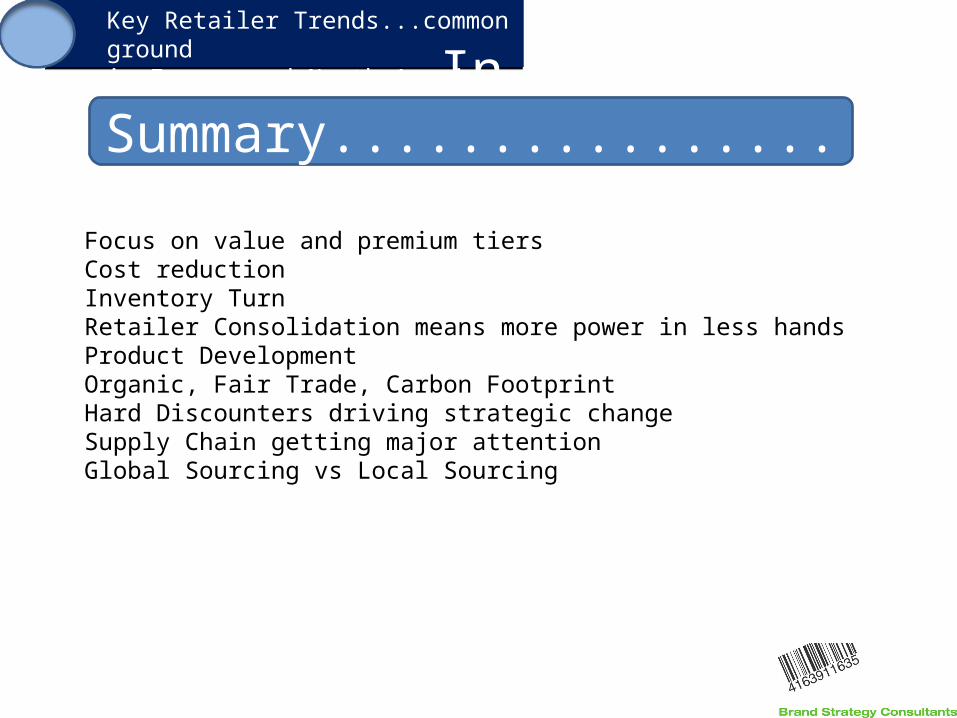

In Summary..................

Focus on value and premium tiersCost reductionInventory TurnRetailer Consolidation means more power in less handsProduct Development Organic, Fair Trade, Carbon FootprintHard Discounters driving strategic changeSupply Chain getting major attentionGlobal Sourcing vs Local Sourcing

2. Key Challenges & Opportunities for NZ Manufacturers

2. Key Challenges & Opportunities for NZ Manufacturers

Why Private Label and not Branded?CPG focus

2. Key Challenges & Opportunities for NZ Manufacturers

Why Private Label and not Branded?

Having some control labels in your offering is often a good idea

2. Key Challenges & Opportunities for NZ Manufacturers

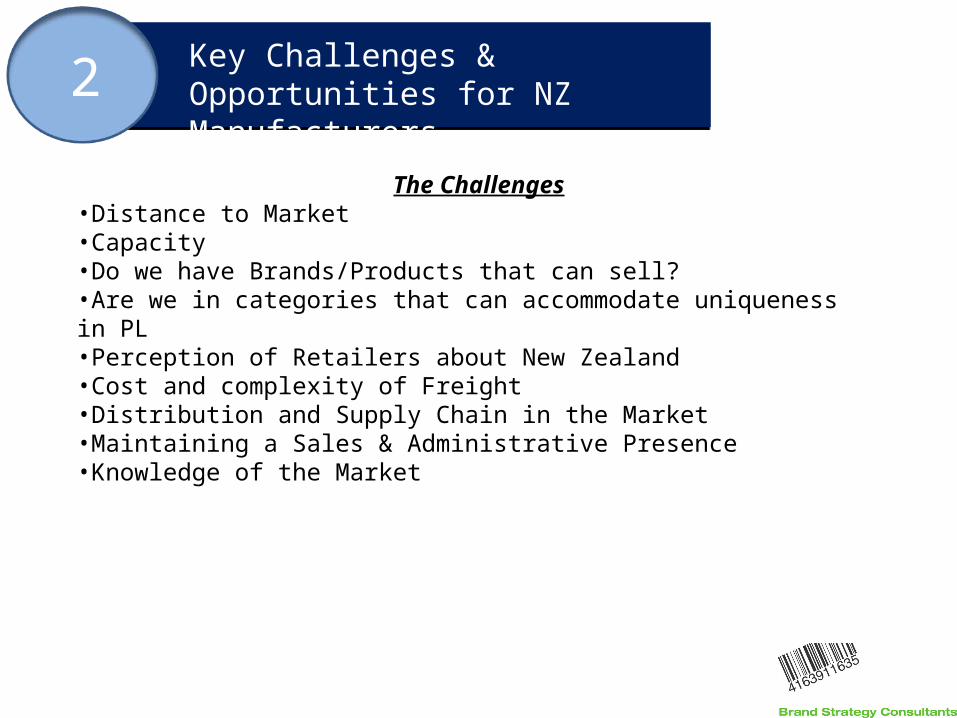

The Challenges•Distance to Market•Capacity•Do we have Brands/Products that can sell?•Are we in categories that can accommodate uniqueness in PL•Perception of Retailers about New Zealand•Cost and complexity of Freight•Distribution and Supply Chain in the Market•Maintaining a Sales & Administrative Presence•Knowledge of the Market

Key Challenges & Opportunities for NZ Manufacturers Key Challenges & Opportunities for NZ Manufacturers

1.

Key Retailer Trends...common ground in Europe and North America

2.

Focus on Knowledge of the Market as related to Private Label

1.Retail Players and their market share2.What is their PL strategy and how do your products fit into their tiers?3.Do we understand the category we are trying to enter?4.What are their quality audit practices?5.Do they self distribute or use distributors?6.Are there brokers involved either in-house or out and if so, what is their role and cost?7.What role does PLMA and the Trade Shows play?8.What help is available to you?

2. Key Challenges & Opportunities for NZ Manufacturers

The Challenges•Distance to Market•Capacity•Knowledge of the Market•Do we have Brands/Products that can sell?•Are we in categories that can accommodate uniqueness in PL•Perception of Retailers about New Zealand•Cost and complexity of Freight•Distribution and Supply Chain in the Market•Maintaining a Sales & Administrative Presence

The Opportunities•Unique Source of Product•Different Style of Products•New Zealand’s overall Consumer and Retailer Perception•PLMA locally and Internationally: Education, Seminars and Trade Shows•Other NZ Trailblazer Manufacturers•Supply Chain experience from other NZ Manufacturers•Canada and the UK may be “Commonwealth Friends”•NZTE support through Beachheads™

Key Challenges & Opportunities for NZ Manufacturers Key Challenges & Opportunities for NZ Manufacturers

1.

Key Retailer Trends...common ground in Europe and North America

2.

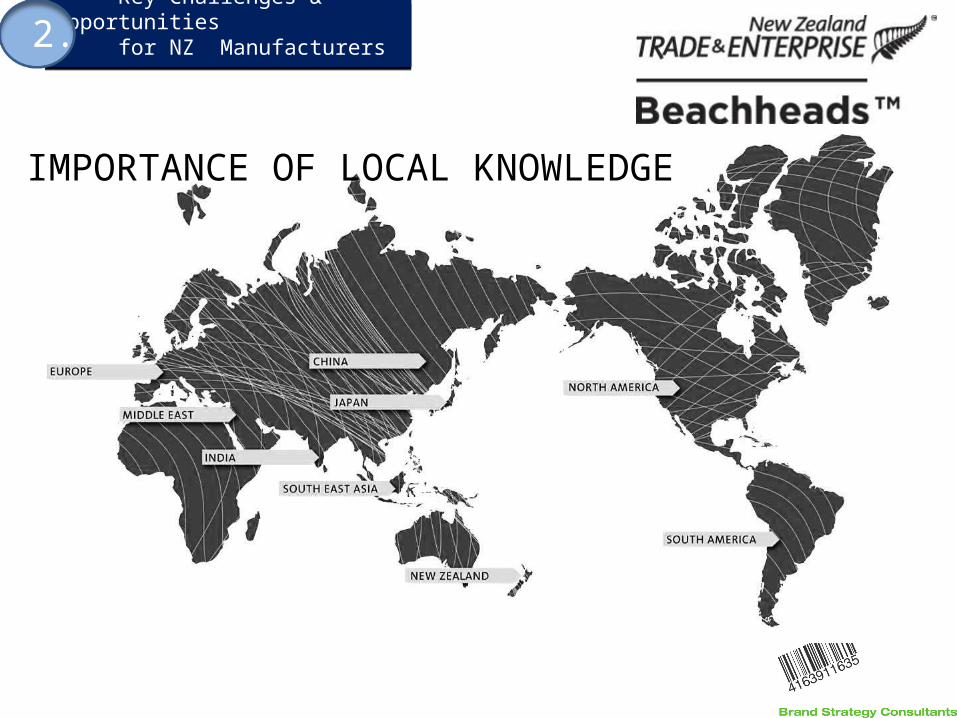

IMPORTANCE OF LOCAL KNOWLEDGE

Key Challenges & Opportunities for NZ Manufacturers Key Challenges & Opportunities for NZ Manufacturers

1.

Key Retailer Trends...common ground in Europe and North America

2.

• “The Beachheads Programme is the single most valuable government related programme for exporters…you get access to people you’d never get access to…with deep local knowledge, a real commercial focus, and, most importantly a real commitment to help”

Mark Templeton CEO - Actronic

• It’s who you know…• what they know and…• How we can help you.

Key Challenges & Opportunities for NZ Manufacturers Key Challenges & Opportunities for NZ Manufacturers

1.

Key Retailer Trends...common ground in Europe and North America

2.

• “The Beachheads Programme is the single most valuable government related programme for exporters…you get access to people you’d never get access to…with deep local knowledge, a real commercial focus, and, most importantly a real commitment to help”

Mark Templeton CEO - Actronic• It’s who you know…• what they know and…• How we can help you.

Ms. Kelly DuffyTrade Commissioner for NZTE in Los Angeles

Key Challenges & Opportunities for NZ Manufacturers Key Challenges & Opportunities for NZ Manufacturers

1.

Key Retailer Trends...common ground in Europe and North America

2.

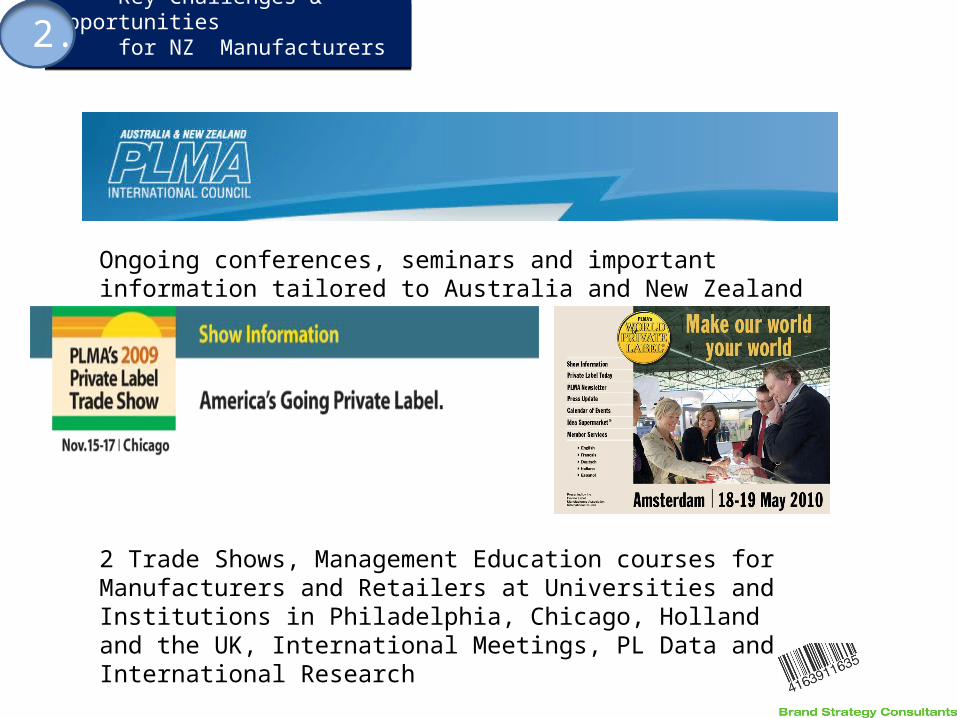

Ongoing conferences, seminars and important information tailored to Australia and New Zealand

2 Trade Shows, Management Education courses for Manufacturers and Retailers at Universities and Institutions in Philadelphia, Chicago, Holland and the UK, International Meetings, PL Data and International Research

3. Retailer Manufacturer Partnership Expectations

Yes, it’s a

myth!!!

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted•Dead net refers to fish at the bottom of the catch

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted•Dead net refers to fish at the bottom of the catch•Promotional “opportunities” are always lurking

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted•Dead net refers to fish at the bottom of the catch•Promotional “opportunities” are always lurking•Off Invoice “Discrepancy” Deductions are standard

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted•Dead net refers to fish at the bottom of the catch•Promotional “opportunities” are always lurking•Off Invoice “Discrepancy” Deductions are standard•Extended Payment Terms are always “just around the corner”

3. Retailer Manufacturer Partnership Expectations

Is it really a Myth?•Some retailers seek partners just like most people seek partners•But divorce rates are pretty high•At the end of the day, retailers are looking for people who will pay to do business with them•A cost price is never the lowest price you have quoted•Dead net refers to fish at the bottom of the catch•Promotional “opportunities” are always lurking•Off Invoice “Discrepancy” Deductions are standard•Extended Payment Terms are always “just around the corner” •If they can get “sale or return from your competitor, why not from you?”

3. Retailer Manufacturer Partnership Expectations

Bottom Line

The longevity of your partnership is in direct relation to your uniqueness in

product

value quality standards

service level and the depth of your pockets

1.

2.

3.

Private Label Export Opportunities

Key Retailer Trends

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

An enormous amount of info available

1.

2.

3.

Private Label Export Opportunities

Key Retailer Trends

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

An enormous amount of info available

1.

2.

3.

Private Label Export Opportunities

Key Retailer Trends

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

An enormous amount of info available

Reality Check but...significant help available

1.

2.

3.

Private Label Export Opportunities

Key Retailer Trends

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

An enormous amount of info available

Reality Check but...significant help available

Go in with eyes wide open!!!

4.

2.

Private Label Export Opportunities

Summary

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

Major Challenge to understand the marketplace fund, procure and place resourceslong distance to ship and control supply chainlocal representationunderstanding the buyer mentality and reading between the linesit takes a long time

4.

2.

Private Label Export Opportunities

Summary

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

Major Challenge to understand the marketplace fund, procure and place resourceslong distance to ship and control supply chainlocal representationunderstanding the buyer mentality and reading between the linesit takes a long time

Major Opportunityvolume marketsstrong trailblazing Kiwi manufacturers succeeding alreadyin market plant developmentkey PL retailers already sourcing from NZsignificant advice and assistance available in market

4.

2.

Private Label Export Opportunities

Summary

Key Challenges & Opportunities for NZ Manufacturers

Retailer Manufacturer Partnership Expectations

However, very few people will dispute that once you get there, it was worth the journey.

www.brandstrategyconsultants.ca

Thank You!

www.brandstrategyconsultants.ca

?Question Time?